Crypto World

What are liquid staking tokens? stETH and the depeg risk, explained

Staking locks your crypto and earns yield. Liquid staking hands you a tradeable receipt for that locked position, so the same capital can earn twice. It is one of DeFi’s largest markets, and it comes with a specific danger most guides skip: the receipt can trade below what it represents. Here is how liquid staking tokens work, and where the risk actually lives.

Summary

- Liquid staking tokens let users keep earning staking rewards while using a tradeable token across DeFi without unlocking the original assets.

- The biggest risk comes when liquid staking tokens trade below the value of the assets backing them, especially during periods of market stress and heavy withdrawals.

- Higher yields from liquid staking strategies often involve leverage, increasing the risk of liquidations if the token temporarily loses its peg.

Staking a proof-of-stake asset like Ether involves a trade-off that used to be absolute: lock your tokens to help secure the network and earn rewards, and accept that the locked tokens are frozen and useless for anything else. Liquid staking removes the second half of that bargain. You deposit your tokens with a protocol, the protocol stakes them for you, and in return you receive a new token, a liquid staking token, that represents your staked position and can be freely traded, sold, or put to work elsewhere in decentralized finance. The original capital keeps earning staking rewards; the receipt token lets that same capital do a second job.

That double-duty is why liquid staking became one of the largest categories in all of DeFi, with tens of billions of dollars flowing into it. It is also why it carries a risk that plain staking does not. The receipt token is only useful if the market treats it as equal in value to the asset it represents, and there are moments, usually the worst possible moments, when the market does not. A liquid staking token can trade below the value of the staked asset behind it, an event called a depeg, and understanding when and why that happens is the difference between using this tool safely and being surprised by it.

This guide explains what liquid staking tokens are, the two designs they come in, how the peg is supposed to hold and how it breaks, the concentration risk hiding behind the biggest provider, the way these tokens get stacked into leverage across DeFi, and the practical questions to ask before holding one. The star example throughout is stETH, the largest liquid staking token, but the mechanics apply across the category, from Rocket Pool’s rETH on Ethereum to the staked-asset tokens on other proof-of-stake networks. The goal is to leave you able to hold one of these tokens understanding exactly what it is, what backs it, and under what conditions its price can part ways with the asset it represents.

The problem liquid staking solves

To see why liquid staking exists, start with the friction of ordinary staking. On Ethereum, running your own validator requires locking thirty-two ether, operating node software with constant uptime, and accepting that your stake is subject to exit queues when you want out. For most holders this is impractical: they lack thirty-two ether, do not want to run infrastructure, and dislike freezing capital they might need, especially as Ethereum reworks its staking and consensus layers in ways that will reshape validator economics for years.

Staking pools solved the first problems by letting many users combine smaller amounts under professional validators, but the funds were still locked. Liquid staking solves the last problem, the lock itself. When you deposit into a liquid staking protocol, it pools your tokens with everyone else’s, stakes them across a set of validators, and mints you a token representing your share of the staked pool plus its accruing rewards. You no longer need thirty-two ether, you never touch validator software, and, crucially, your position is now liquid: the receipt token sits in your wallet and can move freely while the underlying stake keeps earning.

A coat-check analogy captures it. You hand over your coat and receive a claim ticket. The coat stays safely in the cloakroom earning nothing, but the ticket is now in your hands, and while you cannot wear the ticket, you can hold it, hand it to a friend, or even sell it. Liquid staking works the same way: the staked asset stays locked and productive, while the token proving your claim to it circulates freely. Whoever holds the ticket holds the claim, so selling the token means selling the staked position along with it.

The result is capital efficiency that plain staking cannot match. A holder can stake, receive the token, and then lend it, use it as collateral, or provide it as liquidity, earning a second layer of return on top of the base staking reward, all without unstaking. That stacking is the appeal and, as later sections show, the source of the systemic worry.

Two designs: rebasing and value-accruing

Liquid staking tokens come in two flavors, and the difference matters for how rewards show up in your wallet and how the token behaves in DeFi.

A rebasing token keeps its price pegged to the underlying asset one to one and delivers rewards by increasing the number of tokens you hold. Lido’s stETH is the classic example: hold it, and your stETH balance grows a little each day, with each stETH meant to remain worth roughly one ether. The appeal is transparency, since your balance visibly climbs, but the growing balance complicates integrations, because many DeFi protocols were not built to handle a token quantity that changes on its own.

A value-accruing token keeps the token count fixed and delivers rewards by rising in value against the underlying asset. Rocket Pool’s rETH works this way, as does the wrapped version of stETH, wstETH. You hold the same number of tokens over time, but each one is redeemable for progressively more ether as rewards accumulate; stake when one token equals one ether and, a year later, that token might redeem for meaningfully more. This design integrates more smoothly across DeFi because the balance is stable, which is why wrapped, value-accruing versions dominate in lending and liquidity protocols and increasingly appear in the institutional DeFi rails being built on other ledgers too.

The distinction is easy to miss and important in practice. A rebasing token used as collateral can behave strangely because its balance shifts; a value-accruing token trades at a price that is intentionally above one-to-one and rising, so seeing rETH or wstETH quoted above the price of ether is normal and correct, not a premium to fear. Knowing which design you hold prevents misreading its price and misusing it in a protocol.

How the peg holds, and how it breaks

The entire usefulness of a liquid staking token rests on the market valuing it close to the staked asset it represents. That relationship is a soft peg, maintained by arbitrage and redemption instead of any hard guarantee, and understanding the mechanism explains exactly when it can slip.

In normal conditions the peg holds tightly because of a redemption path. A stETH is a claim on staked ether, and once the protocol’s withdrawal queue is functioning, that claim can be redeemed for actual ether. If stETH ever trades meaningfully below one ether on the open market, arbitrageurs buy the discounted stETH, redeem it for a full ether through the queue, and pocket the difference, and that buying pressure pushes the price back toward parity. Deep secondary-market liquidity reinforces this: research on stETH has found that most deviations beyond a small threshold correct within hours, because the arbitrage is reliable and the market is deep.

The peg breaks when the redemption path is slow and the market panics faster than arbitrage can act. Redeeming a liquid staking token for the underlying asset is not instant; it runs through the network’s validator exit queue, which can take days when many people withdraw at once. In a stressed market, holders who want out immediately cannot wait for the queue, so they sell on the open market instead, and a wave of forced selling can push the token below the value of the asset behind it. This is a depeg: not a loss of the underlying stake, but a temporary discount on the receipt.

The defining real-world case came in 2022, when stETH traded as low as roughly a nickel under parity during a broad market crisis. Large holders facing liquidation needed liquidity immediately, the withdrawal path at the time did not allow direct redemption, and the resulting sell pressure drove stETH to a visible discount to ether. Critically, the underlying staked ether was never lost or impaired; the discount reflected the mismatch between an instant desire to exit and a redemption process that could not move instantly. Once redemption became possible and panic subsided, the peg restored. The episode is the template: a liquid staking token depeg is almost always a liquidity-and-timing event, not a solvency event, but that distinction is cold comfort to someone forced to sell at the discount.

How the yield actually stacks

A concrete walk-through of the returns shows both why liquid staking is popular and where the layers of risk enter, because each layer of yield is also a layer of exposure.

Start with the base. Staking ether on Ethereum earns a network reward, a modest annual percentage that comes from new issuance and transaction fees paid to validators for securing the chain. A holder who simply stakes and holds a liquid staking token captures this base reward with almost none of the friction of solo staking: no thirty-two-ether minimum, no node to run, no direct exit-queue management. For many holders, that is the entire appeal, and it is a reasonable, relatively conservative use of the tool.

The second layer comes from putting the token to work. Because the liquid staking token is freely tradeable, a holder can deposit it into a lending protocol to earn interest, supply it to a liquidity pool to earn trading fees, or use it as collateral, each adding a return on top of the base staking reward. This is the capital efficiency that plain staking cannot match: the same underlying ether earns its staking reward and a second yield simultaneously. It is also where smart-contract risk begins to compound, because the token now passes through a second protocol’s code in addition to the staking protocol’s own.

The third layer, and the dangerous one, is leverage, described earlier: borrowing against the token to acquire more of it and repeating the loop. Each turn of the loop multiplies the base yield, which is why advertised returns on some liquid staking strategies look far higher than the underlying staking reward could ever justify. The arithmetic that produces those headline numbers is leverage, and leverage is precisely what converts a survivable depeg into a forced liquidation.

The practical takeaway is to read any liquid staking yield as a signal of how many layers are involved. A return close to the base staking reward is a plain, relatively safe position. A return well above it means the token is deployed into other protocols, adding smart-contract exposure. A return far above the base almost always means leverage, and therefore liquidation risk in a depeg. The yield number is not just a reward; it is a readout of the risk stack beneath it, and matching the layer you accept to the risk you understand is the whole discipline of using these tokens well. The same logic governs every layered yield strategy in DeFi: more yield is always more of something else at risk.

The concentration problem

Beyond the depeg risk sits a subtler, more structural concern: one protocol dominates Ethereum liquid staking to a degree that worries people who think about the network’s health.

Lido, the issuer of stETH, has for long stretches controlled roughly a third of all staked ether, a share large enough that Ethereum researchers openly discuss it as a risk to the network itself. The reasoning is about consensus: if a single staking entity controls too large a fraction of validators, it gains outsized influence over block production and could, in extreme scenarios, threaten the neutrality or censorship-resistance the network depends on. This is not an accusation that Lido would misbehave; it is a structural observation that concentration itself is a vulnerability, regardless of the operator’s intentions, and it is why parts of the community actively encourage stakers to choose smaller providers.

Concentration also compounds the token-level risks. When one liquid staking token is embedded as collateral across nearly every major lending protocol, a serious problem with that token, a smart-contract bug, a governance failure, or a severe depeg, is not one protocol’s problem but a shock that ripples through all of DeFi at once. The dominant token’s ubiquity, which is a convenience in calm markets, becomes a transmission channel in stressed ones. The same dynamic appears wherever a single asset becomes foundational infrastructure, from stablecoins to the restaking protocols that layer additional yield on top of staked positions: dominance buys efficiency and sells fragility.

For an individual holder, concentration risk is mostly about awareness. Using the largest, most liquid token gives the tightest peg and the deepest DeFi integration, which is a real benefit; it also means holding the asset most entangled with everything else, so a systemic event touches it first. Diversifying across providers reduces personal exposure and, in aggregate, improves the network’s health, at the cost of slightly thinner liquidity in the smaller tokens.

The leverage stack, and why it magnifies everything

The feature that makes liquid staking tokens powerful, their usability across DeFi, also enables a leverage loop that turns a modest depeg into a cascade. Understanding this loop is essential to understanding why depegs matter beyond the inconvenience of a discount.

The loop works like this. A user stakes ether and receives a liquid staking token. They deposit that token as collateral in a lending protocol and borrow ether against it. They stake the borrowed ether, receive more of the liquid staking token, deposit that as collateral, and borrow again. Repeated, this stacks several layers of leverage on a single underlying position, each layer amplifying the yield in calm markets. It is a popular strategy precisely because the base staking reward, multiplied by leverage, produces attractive returns.

The danger is what happens when the token depegs. Each borrowing position has a liquidation threshold tied to the value of the collateral, and a depeg lowers that value. As the token slips below parity, leveraged positions approach liquidation; liquidations force the collateral token to be sold; that selling deepens the depeg; the deeper depeg triggers more liquidations. In stressed markets this becomes a self-reinforcing spiral, a domino run dressed in yield-farm packaging. The 2022 depeg was made sharper by exactly this dynamic, as leveraged holders were forced to unwind into a falling market.

The lesson for holders is that a liquid staking token held plainly is a fairly conservative instrument: it earns staking yield and, absent a solvency failure in the protocol, its worst realistic outcome is a temporary discount that arbitrage eventually closes. The same token levered several times over is a very different risk, one where a discount that a plain holder could simply wait out becomes a forced liquidation. The token did not change; the leverage around it did. Anyone evaluating liquid staking yields that look unusually high should assume leverage is involved and price the liquidation risk accordingly.

What to check before holding one

Liquid staking is a genuinely useful tool, and using it well comes down to a handful of concrete checks, not blanket caution.

Confirm the token design. Know whether you hold a rebasing token, whose balance grows, or a value-accruing one, whose price rises, because the two behave differently in your wallet and in any protocol you deposit them into. Value-accruing wrapped versions are generally the smoother choice for DeFi use.

Assess the redemption path. The peg’s strength depends on being able to redeem the token for the underlying asset, so check that direct withdrawals are live and how long the exit queue runs. A token with a fast, functioning redemption path has a stronger peg than one where exit depends entirely on selling into secondary-market liquidity.

Gauge the liquidity and the provider. Deep secondary-market liquidity is what lets arbitrage defend the peg between redemptions, so a token with thin liquidity is more prone to slipping and slower to recover, the same slippage dynamics that govern any thinly-traded swap. Weigh the largest provider’s tight peg and deep integration against its concentration risk, and consider whether spreading across providers suits your risk tolerance and, incidentally, helps the network.

Respect the layered smart-contract risk. Your capital passes through the staking protocol’s contracts, and if you deploy the token into lending or liquidity protocols, through those as well. Each layer is code that can contain bugs, and stacking layers stacks the places something can break, the same concentration-of-risk lesson that runs through every major bridge exploit. Favor audited, long-lived protocols, and treat any strategy promising outsized yield as a signal that leverage, and its liquidation risk, is present.

Held with these checks in mind, a liquid staking token does what it promises: it unlocks the value of a staked position so the same capital can work twice, earning a base reward while remaining liquid and productive. The depeg risk that defines the category is real but specific, a timing-and-liquidity event instead of a loss of the underlying stake, and it is most dangerous not to plain holders but to those who lever the token into a stack that turns a temporary discount into a forced sale. Understand which of those two users you are, and the risk becomes something you can size instead of something that surprises you.

The broader significance is worth a closing thought. Liquid staking tokens have become foundational plumbing for proof-of-stake economies: tens of billions of dollars of staked value now circulate as these receipts, and they underpin lending, trading, and collateral across DeFi. That ubiquity is a genuine achievement, turning otherwise idle staked capital into productive infrastructure. It also means the health of a few dominant tokens matters to the whole system, which is why the concentration and depeg risks discussed here are not merely individual concerns but systemic ones.

Using these tokens knowledgeably, favoring strong redemption paths, deep liquidity, and audited protocols, and staying alert to the leverage hiding behind unusually high yields, is how an individual participates in that system without being surprised by its failure modes.

Frequently asked questions

What is a liquid staking token?

A liquid staking token is a tradeable token you receive when you stake a proof-of-stake asset through a liquid staking protocol. It represents your staked position plus its accruing rewards, and it can be freely sold or used in DeFi while the underlying asset stays staked and earning. stETH from Lido and rETH from Rocket Pool are the best-known examples on Ethereum.

How is liquid staking different from regular staking?

Regular staking locks your tokens, making them unavailable for anything else until you unstake through an exit queue. Liquid staking gives you a receipt token that keeps your capital liquid, so you can trade it or use it elsewhere in DeFi while the underlying stake continues to earn rewards. The trade-off is added smart-contract risk and the possibility that the receipt token depegs.

What does it mean when stETH depegs?

A depeg means the liquid staking token trades below the value of the staked asset it represents, such as stETH trading below one ether. It usually happens when many holders want to exit faster than the redemption queue allows, so they sell on the open market and push the price to a discount. Importantly, a depeg is generally a liquidity and timing event, not a loss of the underlying staked asset.

Is my staked asset lost if the token depegs?

No. A depeg reflects a temporary market discount on the receipt token, not destruction of the underlying stake. The staked asset remains intact and continues earning, and once the redemption path clears and panic subsides, arbitrage typically restores the peg. The real risk is being forced to sell at the discount, which mainly affects leveraged holders facing liquidation.

Are rebasing and value-accruing tokens different?

Yes. A rebasing token like stETH stays pegged one-to-one and pays rewards by increasing your token balance over time. A value-accruing token like rETH or wrapped stETH keeps the balance fixed and pays rewards by rising in value against the underlying asset. Value-accruing versions integrate more smoothly into DeFi because their balance does not change unexpectedly.

Why is Lido’s dominance considered a risk?

Lido has often controlled roughly a third of all staked ether, and Ethereum researchers worry that any single staking entity holding too large a share of validators could gain outsized influence over the network’s consensus. It also means the dominant token is embedded across most of DeFi, so a serious problem with it would ripple widely. The concern is structural rather than an accusation of misconduct.

Can I lose money with liquid staking tokens?

Yes, through several channels: a smart-contract bug in the staking or DeFi protocols you use, a severe depeg that forces you to sell at a discount, or liquidation if you lever the token in a borrowing loop. Held plainly in an audited, liquid protocol, the risk is relatively modest, but stacking leverage on top substantially raises the chance of a forced loss.

What is the leverage loop with liquid staking tokens?

The loop involves staking to get the token, using it as collateral to borrow the underlying asset, staking that to get more of the token, and repeating to stack leverage and amplify yield. It works in calm markets but is dangerous in a depeg, because falling collateral value triggers liquidations that force selling, which deepens the depeg and triggers more liquidations in a self-reinforcing cascade.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 7, 2026.

Crypto World

BTC inflation quagmire gets sticker as renewed Iran conflict sends oil price soaring: Crypto Daily

Will the Fed focus on the breakevens, which are already at or below 2% at the short end, or on rising consumer concerns?

The Fed itself tends to trust breakevens because they reflect institutional capital allocation, while consumer surveys frequently lag behind and can be heavily influenced by volatile everyday costs like energy and food. Hence, the argument that falling breakevens are bullish for bitcoin still holds.

But the central bank may not entirely ignore Main Street sentiment, which can become self-reinforcing, especially if catalysts like energy prices remain volatile.

And guess what? The U.S.-Iran ceasefire has collapsed. The two sides exchanged airstrikes early today, triggering a roughly 5% jump in oil benchmarks. Bitcoin has fallen back to $62,000 and may drop further if the panic spreads to Wall Street later today.

Analysts are also watching the minutes from the Fed’s June meeting, due later today.

“Wednesday’s Fed minutes are the pin. With longs this crowded and funding this rich, a hawkish read is exactly the spark that flushes leverage, and the Strategy authorization hangs over every rally. We respect the bounce, we do not trust it, and we keep size honest into the minutes,” analysts at Marex said in an email.

Berachain is set to undergo a major protocol change this Wednesday that will reshape how the network pays incentives to participants. The upgrade, scheduled for 4:00 p.m. UTC, will retire the current Bera Governance Token (BGT) emissions and switch Berachain’s reward design to focus on its main BERA token via Wrapped BERA (WBERA).

In an announcement shared on Tuesday via the Berachain Foundation’s X account, the foundation said the hard fork will replace the network’s previous dual-token incentive structure. That model split incentives between transferable BERA and BGT, a governance asset that cannot be transferred. After the change, block rewards will be distributed as fixed WBERA amounts rather than BGT.

Key takeaways

- Berachain’s hard fork on Wednesday (4:00 p.m. UTC) will stop BGT emissions and end the dual-token incentive setup.

- Reward payouts will shift to WBERA block rewards, with the foundation describing the new design as simpler and more sustainable.

- WBERA emissions began on Tuesday, while BGT emissions are scheduled to be halted during the hard fork.

- Berachain’s foundation says APR may rise materially after the upgrade, but warned early yields could be volatile.

- Data tracking from CoinMarketCap and DefiLlama shows BERA and network TVL have recently been under pressure, suggesting activity remains subdued ahead of the change.

A shift from BGT to WBERA—and the mechanics behind it

The upgrade is designed to consolidate Berachain’s incentive system around WBERA, the wrapped form of its BERA token. According to the Berachain Foundation, the network will move away from BGT-based rewards and instead center incentives on staked WBERA (sWBERA), which it described as a more straightforward approach.

Before the upgrade, participants chasing higher yields reportedly had to work through several different reward pathways, including liquid staking mechanisms that were tied to BGT. The new plan reduces that complexity by changing what the network issues and how rewards flow.

Mechanically, the foundation outlined a two-stage transition. First, WBERA emissions started Tuesday. Then, at the scheduled time Wednesday, the hard fork will halt BGT emissions. In the days following the upgrade, the network will also phase out reward vaults and liquid staking incentives that are tied to BGT.

What it means for staking returns

Berachain’s foundation said the change could significantly improve yields, stating that annual percentage rates (APR) may triple after the upgrade. However, the foundation also cautioned that returns may swing during the first few days as the system settles into its new reward configuration.

For users, the practical implication is that the upgrade may initially produce short-term uncertainty even if the long-run incentive structure is intended to be more attractive. Traders and liquidity providers watching post-fork APR should expect the first window after Wednesday’s block transition to differ from the steady-state the foundation is aiming for.

Token performance and on-chain activity ahead of the fork

While Berachain prepares for the incentive overhaul, the market signal coming into Wednesday is not particularly strong. CoinMarketCap data cited in the coverage shows BERA was down about 7% over the 24 hours to 8:34 a.m. UTC. That move extends a broader slump in the token over the past year, bringing the decline to roughly 88%.

On the network side, DefiLlama data indicates Berachain’s total value locked (TVL) fell by $1.79 million, or about 3%, over the same 24-hour period. DefiLlama places the network around rank 37 by TVL, with approximately $56 million locked.

Activity metrics also point to a comparatively muted moment for the chain. Over the past 24 hours, the network generated $41 in chain fees and $3,359 in application revenue, while distributing $14,816 in token incentives. Together, these figures suggest that while incentives are currently being paid out under the existing model, overall utilization has not accelerated sharply ahead of the scheduled hard fork.

Why the “simpler” token economy matters

The foundation’s stated rationale is that the upgrade improves sustainability and reduces friction for users. In a dual-token system, participants often need to understand more than one asset’s role—especially when governance-related tokens like BGT are not freely transferable. By aligning incentives more directly with WBERA and emphasizing staked WBERA (sWBERA), the foundation is effectively trying to streamline how users participate and how rewards are structured.

That matters for investors and builders because incentive design can influence where liquidity concentrates. When reward logic is complex—especially when it involves multiple vaults and liquid staking pathways—capital can fragment across products and strategies. Streamlining rewards into a single centered asset may make it easier for users to evaluate positions and for liquidity to move as the network’s incentive targets shift.

At the same time, the transition introduces a period of adjustment. Since WBERA emissions started Tuesday and BGT emissions will stop only when the hard fork executes Wednesday, participants will be navigating a changing reward landscape on both days. This is especially relevant given the foundation’s own warning that yields could be volatile early on.

What remains uncertain is how quickly incentives will translate into measurable changes in on-chain activity—such as fees, application revenue, and TVL—after the upgrade. With recent data showing BERA and TVL trending downward, the post-fork period will be the real test of whether the new incentive system meaningfully boosts participation.

All eyes will be on Wednesday’s block upgrade and the days immediately afterward: whether APR stabilizes, how reward vault and liquid staking behavior changes as BGT-linked incentives are phased out, and whether chain usage improves enough to offset the current softness in TVL and token performance.

Key Highlights

- Base introduces B20 standard for native issuance of stablecoins, RWAs, and digital tokens.

- Developers can create tokens without deploying custom ERC-20 smart contracts.

- Built-in issuer controls include minting, burning, pausing, and transaction restrictions.

- Full ERC-20 compatibility ensures seamless integration with existing infrastructure.

- Deployment comes after Base sequencer disruptions and the Beryl network upgrade.

Base has unveiled its B20 standard on the mainnet, offering developers a streamlined approach to creating stablecoins, real-world assets, and fungible tokens. This protocol eliminates the requirement for custom ERC-20 contract deployment while introducing enhanced issuer management capabilities and preserving full ERC-20 compatibility.

Base Activates B20 for Streamlined Token Creation

Base deployed the B20 standard to its mainnet at 6:00 pm UTC, establishing a protocol-native framework for token issuance. This infrastructure enables developers to mint stablecoins, tokenized securities, real-world assets, and various fungible digital tokens.

The B20 protocol offers two distinct token configurations tailored to issuer requirements. Asset tokens accommodate decimal precision ranging from six to 18 places. Meanwhile, the stablecoin configuration defaults to six decimals and mandates fiat currency denomination.

Base engineered B20 with backward compatibility for existing ERC-20 infrastructure. Consequently, digital wallets, cryptocurrency exchanges, and blockchain indexers can integrate these tokens with minimal technical modifications. The standard additionally incorporates ERC-2612 permit capabilities for gasless approvals.

Enhanced Issuer Controls and Regulatory Features

The B20 architecture provides token issuers with comprehensive operational controls. Available management functions encompass token minting, burning operations, protocol pausing, supply caps, transfer restrictions, and transaction metadata. These features allow issuers to govern their assets through Base’s native infrastructure layer.

Previous Base technical documentation described an Issuer Toolkit designed for regulated asset creators. This toolkit delivers role-based access control alongside optional compliance mechanisms. It further accommodates asset freezing and seizure capabilities for jurisdictions with applicable regulatory requirements.

Base deployed B20 as part of the Beryl upgrade package, which launched on mainnet June 26. This upgrade simultaneously reduced Base-to-Ethereum withdrawal timeframes from seven days to five days. Additionally, the upgrade incorporated Reth V2 implementation to optimize node storage efficiency.

B20 Debut Comes After Sequencer Interruptions

The B20 standard launch arrives following two consecutive disruptions affecting Base’s sequencer operations. On June 25, an invalid block halted block production across the network. This incident persisted for approximately 116 minutes before Base engineers restored normal operations.

A subsequent outage materialized on June 26 when a system restart triggered a race condition. This technical issue prevented sequencers from synchronizing properly and lasted roughly 20 minutes. Base subsequently attributed both disruptions to sequencer software defects.

The first disruption occurred mere hours before the scheduled Beryl upgrade deployment. Nevertheless, Base postponed the upgrade by 24 hours due to an unrelated B20 activation registry timing conflict. Base clarified that the sequencer outage had no connection to the upgrade implementation.

Dunamu, the operator of South Korean cryptocurrency exchange Upbit, has been selected as the preferred bidder for the Korean National Police Agency’s one-year seized digital asset custody contract.

Summary

- Dunamu has been selected as the preferred bidder to manage digital assets seized by South Korea’s National Police Agency under a one year custody contract.

- Procurement results placed Dunamu ahead of K DAC and Hecto Wallet One after it received the highest combined technical and price evaluation score.

- Some industry participants questioned whether the tender requirements gave large exchange operators an advantage, while police said the operator was selected through a fair competitive process.

Procurement records published by South Korea’s Public Procurement Service showed that Dunamu ranked first in the bidding process for the project, which will transfer custody of cryptocurrencies seized during police investigations to an external institution.

As the preferred negotiating bidder, Dunamu will secure the contract if negotiations are completed successfully without requiring talks with lower-ranked participants.

Dunamu leads technical and price evaluation

Scoring released through the procurement platform showed Dunamu receiving the maximum 10 points for its bid price and 84.73 points in the technical assessment, giving it a total score of 94.73. Korea Digital Asset Custody (K-DAC) placed second with 91.29 points, while Hecto Wallet One finished third with 87.27 points.

Valued at 267 million won (about $195,000), the contract will run for one year and cover the storage and management of digital assets confiscated by police during criminal investigations.

Industry participants, however, questioned whether the tender requirements made it difficult for smaller custody providers to compete.

According to local media reports, the National Police Agency required bidders to immediately accept full custody of seized cryptocurrencies, maintain a round-the-clock response system, and guarantee full compensation if assets were lost due to hacking.

Several industry officials told local media that those conditions, while reasonable for safeguarding government-held assets, were easier for a large exchange operator such as Dunamu to satisfy than for standalone custody firms with fewer resources.

One custody industry official said competing against a major exchange under those requirements “wasn’t an easy game from the start.”

Evaluation process draws criticism

Some market participants also expressed disappointment with the evaluation process itself. According to local media, an industry official said Dunamu was likely assessed favorably because of its experience operating a 24-hour exchange infrastructure and handling multiple digital assets, but added that a proposed on-site inspection of competing firms’ security systems and operating infrastructure was not included in the evaluation.

The National Police Agency rejected suggestions that the outcome favored a large company from the outset, with local media reporting that the agency said the operator had been selected through a fair competitive process.

The decision follows previous incidents involving the handling of seized cryptocurrencies by law enforcement agencies. Local reports noted that the need for an external custody provider gained attention after Bitcoin seized by the Gwangju District Prosecutors’ Office was lost, while police also later confirmed that seized Bitcoin had gone missing in a separate 2022 incident.

The latest development comes as Dunamu continues to navigate regulatory scrutiny on other fronts. Earlier this month, the company disclosed that the completion of its planned all-stock share swap with Naver Financial had been postponed for a second time until Dec. 31 as several regulatory approvals remain pending.

Key Takeaways

- Alibaba’s American Depositary Receipts climbed 11% in premarket sessions on Wednesday, reaching $109.38

- A pre-earnings analyst briefing revealed that the company’s instant-commerce division is experiencing reduced losses

- Hong Kong’s Hang Seng Tech Index surged approximately 5%, while Tencent and JD.com both gained around 4%

- South Korea’s KOSPI tumbled 5.4% as capital flowed away from semiconductor stocks including Micron and SK Hynix

- Nasdaq 100 futures declined 1.1% amid concerns over deteriorating U.S.-Iran cease-fire conditions

Alibaba’s American Depositary Receipts rocketed 11% to $109.38 during Wednesday’s premarket session, representing the stock’s most significant single-session rally in Hong Kong trading since September.

Alibaba Group Holding Limited, BABA

The driving force behind this surge was an analyst briefing conducted ahead of the company’s official earnings release. According to Chinese media outlet Jiemian News, Alibaba informed analysts that its rapidly expanding instant-commerce segment experienced narrowing losses during the June quarter, while the company maintained stable profitability across its operations. Market participants responded enthusiastically to these developments.

Shares traded in Hong Kong jumped as much as 12.5% during peak trading, positioning the stock among the strongest performers on the Hang Seng Tech Index, which rallied approximately 5%.

This wasn’t an isolated Alibaba phenomenon. JD.com climbed 3.8%, Baidu advanced 6.4%, and Tencent posted gains of nearly 4%. Chinese technology giants, which had underperformed throughout much of 2026, suddenly recaptured investor interest.

Capital Reallocation Dynamics

The larger narrative involves a meaningful shift in capital allocation patterns. Throughout recent months, artificial intelligence investment themes concentrated heavily on semiconductor manufacturers — especially South Korean companies like SK Hynix and American giant Micron. These equities fueled substantial gains in Korea’s KOSPI index and Taiwanese markets.

Wednesday reversed that trend dramatically. The KOSPI plunged as much as 5.4% as capital rotated away from chip-heavy markets. Micron declined 4.7%, while SK Hynix dropped 5.7%.

Market participants appear to be seeking more attractive valuations within the AI investment theme. Chinese internet companies, which had tumbled into bear market territory in Hong Kong, present lower price-to-earnings multiples compared to their elevated U.S. and Korean peers.

Contributing to the optimistic sentiment surrounding Chinese AI capabilities: Reuters disclosed that DeepSeek is developing proprietary chip technology to support AI infrastructure. The Information separately reported that Zhipu is evaluating the design of its own AI processors — indications that China’s artificial intelligence sector is advancing into hardware development.

American Technology Sector Faces Headwinds

While Chinese technology stocks attracted buying interest, American markets indicated weakness. Nasdaq 100 futures fell 1.1% after President Trump suggested the cease-fire arrangement between the United States and Iran may be unraveling. Rising oil prices unsettled investors across multiple sectors.

Alibaba’s ADRs had experienced significant pressure throughout 2026, declining 33% year-to-date prior to Wednesday’s rally. The weakness stemmed from investor anxiety regarding the company’s substantial expenditures on artificial intelligence infrastructure, including its Qwen large-language model, which management has positioned as a competitor to ChatGPT.

A Barron’s analysis published Monday contended that Chinese AI enterprises are strategically positioned to compete effectively, highlighting the comparatively low pricing of their chatbot services relative to offerings from OpenAI, Anthropic, and Alphabet.

Alibaba is scheduled to release comprehensive earnings results within the coming days. Wednesday’s preliminary briefing indicated that financial results, particularly regarding profitability metrics, may exceed conservative expectations.

The Hang Seng Tech Index had previously entered bear market territory earlier this year due to declining confidence in Chinese e-commerce operations and apprehensions about China’s macroeconomic conditions.

The Reserve Bank of India (RBI) has reiterated its support for a crypto policy, which is “leaning towards prohibition,” according to internal government documents reviewed by Reuters.

They show that the institution continues to be concerned about financial stability, monetary sovereignty, and the role of privately issued stablecoins.

RBI Wants Crypto Outside Regulated Finance

According to the report, the RBI said that banks and financial institutions should be prohibited from holding, trading, or gaining any exposure to cryptocurrencies and to privately issued stablecoins (such as USDT and USDC). The bank also considers a prohibition a means of keeping digital assets outside the regulated financial system and reducing further risks.

RBI also flags stablecoins as a specific concern. The main stance is that foreign currency-pegged coins could pose a risk to domestic monetary sovereignty, while rupee-backed stablecoins could affect the government’s income from issuing fiat currency and create problems for financial stability during periods of stress.

It’s important to note that India hasn’t fully banned crypto trading. However, the sector remains in a regulatory grey zone. Major lenders generally avoid direct crypto exposure after receiving multiple warnings from the central bank, even though there is no direct prohibition on dealing in digital assets.

But that’s not all.

Tax Department Also Piles On

The country’s tax department also warned that crypto transactions are becoming a lot harder to track – in a separate statement. This is particularly true when transactions are routed through offshore exchanges, peer-to-peer rupee trades, or originate from private self-custody wallets.

The department found that fewer than a quarter of 645,000 individuals who made crypto transactions who made any kind of crypto transactions back in 2023 reported them on their tax returns.

India currently taxes crypto gains at 30%. However, overseas platforms, valuation gaps, and unclear ownership tend to complicate compliance, according to officials.

The post India’s Central Bank Renews Push for Crypto Ban: Report appeared first on CryptoPotato.

Futures for the Dow Jones Industrial Average and the other major stock indexes traded mixed ahead of Tuesday’s open. Nasdaq-100 futures dropped in overnight trading after South Korean memory giant Samsung Electronics reported preliminary earnings. Astera Labs (ALAB), Bloom Energy (BE), Nvidia (NVDA) and Tesla (TSLA) were winners Monday. Space Exploration Technologies (SPCX), known as SpaceX, dropped ahead of its…

Copyright ©2026 Investor’s Business Daily, LLC. All rights reserved. 87990cbe856818d5eddac44c7b1cdeb8

Crypto World

Apple (AAPL) Inks Massive $30B+ Chip Deal with Broadcom (AVGO) for Domestic Manufacturing

Key Highlights

- Apple has entered into a major multiyear partnership with Broadcom exceeding $30 billion in value, focused on custom semiconductor components and wireless connectivity solutions.

- Over 15 billion chips will be manufactured domestically as part of this arrangement.

- Broadcom plans to commit $1.5 billion toward upgrading its Fort Collins, Colorado production plant.

- The agreement centers on FBAR radio frequency filtering technology, a product line the two companies have jointly engineered since 2023 at minimum.

- This represents Apple’s most substantial American Manufacturing Program (AMP) initiative yet, contributing to its comprehensive $600 billion domestic investment plan spanning four years.

Apple has finalized its most significant U.S.-based manufacturing partnership to date, entering into a multiyear collaboration with Broadcom valued at over $30 billion to manufacture specialized semiconductors and wireless components domestically.

Revealed this Wednesday, the partnership will lead to the domestic fabrication of no fewer than 15 billion semiconductor units, creating employment opportunities for hundreds of Americans throughout the manufacturing ecosystem.

Shares of Apple (AAPL) declined 0.64% during trading, while Broadcom (AVGO) dropped 0.83%, though neither movement seemed directly connected to the partnership reveal.

Broadcom initially revealed the extended supply arrangement this past Monday, verifying it had finalized a contract with Apple extending to 2031. Wednesday’s statement provided the comprehensive specifics.

The semiconductors forming the partnership’s foundation are FBAR filters — specialized radio frequency elements that enable wireless connectivity in Apple’s product lineup. The two technology giants have jointly developed these components since 2023 or earlier.

This partnership falls under Apple’s American Manufacturing Program, an initiative the corporation introduced previously to strengthen domestic supply chain capabilities. This latest agreement represents Apple’s most significant undertaking within that framework.

To accommodate the increased manufacturing capacity, Broadcom will allocate $1.5 billion for renovating and enhancing its Fort Collins, Colorado manufacturing campus. This location will manufacture the FBAR filters alongside other sophisticated wireless connectivity solutions.

Tim Cook described the Fort Collins-produced components as “essential to delivering the incredible performance and connectivity our customers expect.” He additionally expressed appreciation to the Trump administration for backing the initiative.

Broadcom’s CEO Hock Tan stated the company is “pleased to expand our manufacturing footprint in Fort Collins,” emphasizing that the facility manufactures technology that “connects people around the world.”

Apple’s $600 Billion Domestic Investment Strategy

The Broadcom deal forms part of a broader financial pledge Apple has undertaken regarding the American economy. The technology leader has committed to directing $600 billion domestically across four years, encompassing manufacturing operations, employment generation, and technological advancement.

Wednesday’s revelation furthers Apple’s declared objective of establishing a comprehensive silicon supply infrastructure within U.S. borders — an initiative that has gained increased importance amid continuing trade tensions and tariff considerations.

A Multi-Decade Collaboration

Apple and Broadcom have maintained a collaborative relationship spanning many years, with Broadcom furnishing wireless semiconductor solutions utilized throughout iPhone models and additional Apple hardware. This latest agreement substantially strengthens that partnership and prolongs it considerably into the coming decade.

The supply contract running through 2031 provides Broadcom with demand forecasting certainty and validates the capital expenditure in Colorado. From Apple’s perspective, it secures a reliable domestic supplier for critical components during a period when American semiconductor production capacity ranks as a strategic imperative.

Apple verified the partnership on Wednesday, July 8, 2026, with manufacturing of the Fort Collins-produced components anticipated to expand across multiple Apple product categories moving forward.

Ethereum has weakened for a second straight session as a bearish rounding-top pattern and renewed selling pressure threaten a move toward $1,650.

Summary

- Ethereum fell below $1,750 after failing to break above key resistance near the 50-day EMA around $1,800.

- A bearish rounding-top pattern, weakening momentum indicators, and liquidation clusters point to $1,650 as the next support.

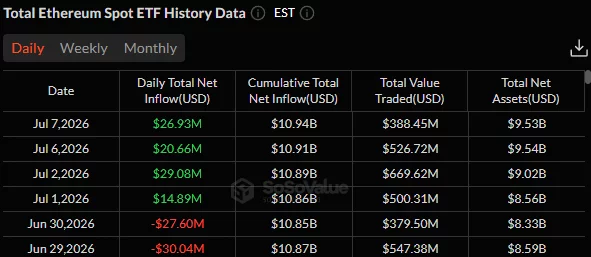

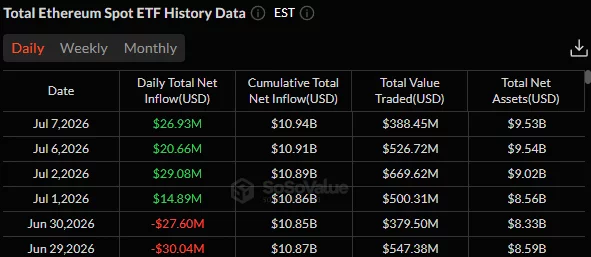

- Despite four straight days of spot ETF inflows, analysts say the recent rally has been driven mainly by spot demand rather than leverage.

According to data from crypto.news, Ethereum (ETH) was trading near $1,737 at press time, down nearly 2% over the past 24 hours after a wallet linked to a large holder transferred roughly $26.9 million worth of Ether to a centralized exchange.

The move triggered fresh profit-taking after Ethereum’s recent recovery stalled just below a major technical resistance zone between $1,800 and $1,806, where the daily Supertrend indicator and the 50-day exponential moving average converged.

Geopolitical tensions have added another layer of pressure. Oil prices climbed after fresh U.S. military action targeting Iranian energy infrastructure, reviving inflation concerns and lifting Treasury yields. Risk assets weakened across global markets as technology stocks retreated, with cryptocurrencies moving lower alongside equities.

Exchange-traded fund demand has nevertheless remained constructive. U.S. spot Ethereum ETFs have now posted four consecutive days of net inflows, while Coinbase Premium has continued recovering from recent lows, suggesting institutional demand has improved even as price struggles to reclaim overhead resistance.

Derivatives positioning also paints a mixed picture. According to analyst Rain, Ethereum’s recent advance has come primarily from spot buying rather than leveraged speculation.

“$ETH is up 10% this week and open interest barely moved: the actual signal,” Rain wrote on X. “Leverage ratio hasn’t recovered from June, this bounce comes from spot demand.”

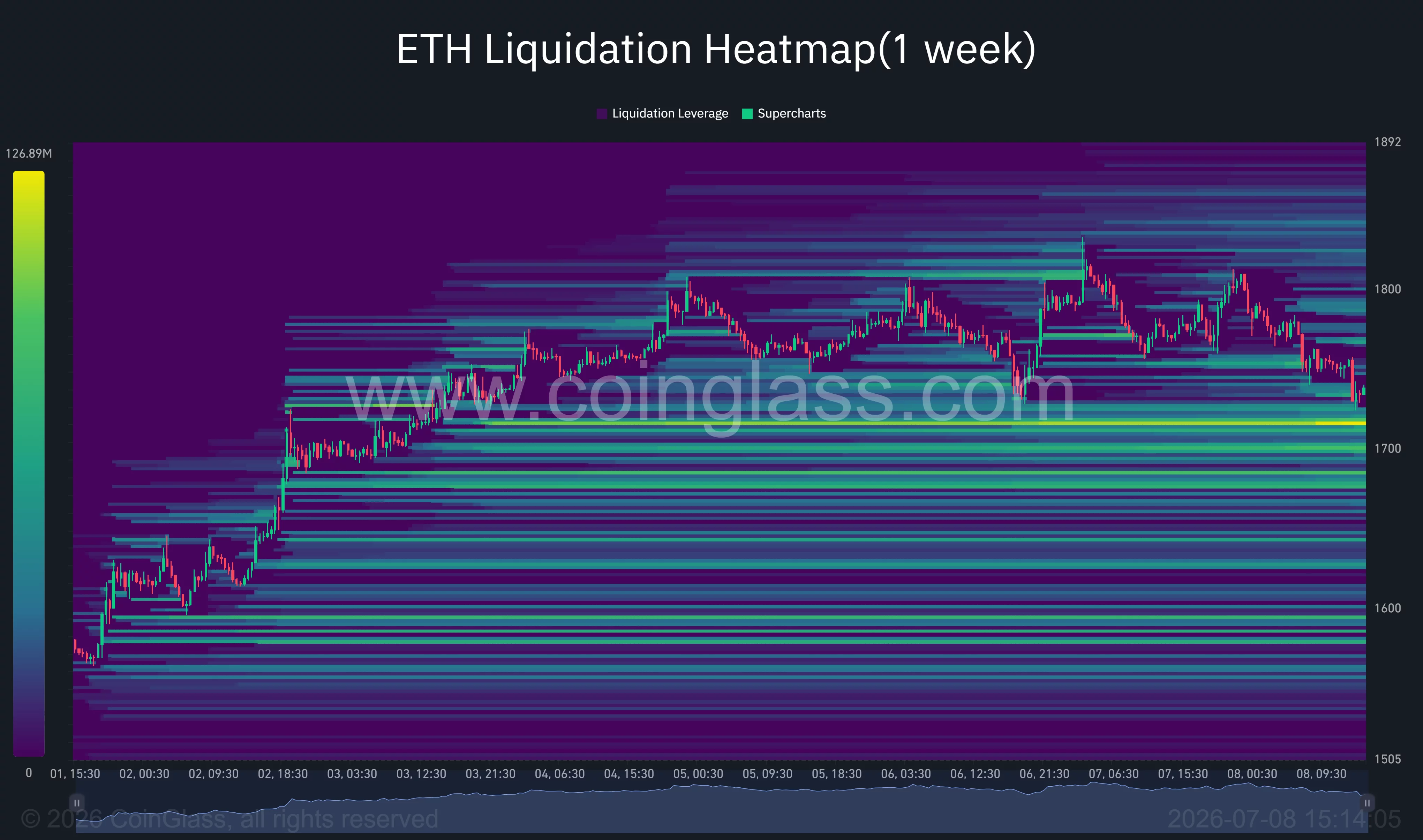

Rain added that net taker volume turned positive on June 28, while roughly $76.2 million in positions were liquidated over the past day, with long traders accounting for most of the losses after ETH failed to hold above $1,800.

Ethereum technical structure favors a move toward $1,650

Ethereum’s 4-hour chart has formed a bearish rounding-top pattern after the recovery from late June stalled near $1,830. Price has already broken below the ascending trendline that supported the rally and slipped beneath the 61.8% Fibonacci retracement level around $1,724 after repeated rejection near the 78.6% level at roughly $1,772.

Momentum indicators have also turned weaker. The 4-hour RSI has fallen to around 44 after approaching overbought territory earlier this week, while the MACD remains below its signal line with expanding negative histogram bars. If sellers maintain control, the next major technical objective sits near the 0.382 Fibonacci retracement at approximately $1,657, aligning closely with the projected rounding-top target around $1,650.

The daily chart offers little relief for bulls. Ethereum remains below the 50-, 100-, and 200-day moving averages near $1,789, $2,025, and $2,247, respectively, keeping the medium-term trend under pressure. Chaikin Money Flow has stayed slightly above zero, suggesting spot demand has not disappeared entirely, but buyers have yet to generate enough momentum to reclaim key moving averages.

CoinGlass liquidation data also identifies an important support zone between $1,700 and $1,720, where a large concentration of leveraged long positions remains. A decisive break below that range could force another wave of liquidations and accelerate a decline toward the $1,650 region.

Holding above $1,700 remains critical for bulls

Analyst Ted Pillows believes Ethereum has already lost an important technical level.

“$ETH has lost the $1,750 support zone. A daily close below the level would be really bad for Ethereum.”

A sustained close below the $1,700-$1,720 support band would strengthen the bearish setup and expose Ethereum to additional losses toward $1,650, with the June low near $1,550 becoming the next major support. Renewed geopolitical tensions, elevated bond yields, or another wave of whale selling could add further pressure if risk appetite weakens again.

The bearish outlook would lose momentum if ETH quickly reclaims the $1,800-$1,806 resistance area. A breakout above that zone would invalidate the rounding-top pattern, shift attention back to the recent high near $1,833, and improve the chances of another attempt toward the psychological $1,900 level, particularly if ETF inflows continue and leverage returns to the futures market.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

The Reserve Bank of India (RBI), the country’s central bank, has reiterated its support for a cryptocurrency policy that favors a prohibition-oriented approach.

The RBI wants banks and financial institutions barred from any exposure to crypto assets and privately issued stablecoins.

Why India’s Central Bank Leans Toward Crypto Prohibition

The RBI has warned about crypto risks repeatedly and now argues for policies “leaning towards prohibition,” according to documents reviewed this week by Reuters. It wants digital assets kept outside the regulated financial system. Officials say the aim is to limit contagion risks to lenders.

The stance revives a fight the RBI lost in 2018, when a court struck down policies that had effectively banned crypto dealings. Since then, digital assets have existed in a grey zone.

Indian banks are currently allowed to engage with cryptocurrencies. However, most major lenders have stayed away from the sector after repeated cautionary statements from the RBI.

The containment line echoes caution seen across global frameworks, though most now favor regulation over isolation.

Government figures put the number of crypto traders at nearly 39 million. They held about $2.1 billion in digital assets at the end of May, according to the tax department estimates.

Follow us on X to get the latest news as it happens

Stablecoins and Offshore Trading Raise the Stakes

The RBI extended its warning to stablecoins, tokens pegged to fiat currencies. It said foreign-currency versions threaten monetary sovereignty. Rupee-backed tokens could cut the government’s currency income and strain stability during market stress.

It added that permitting stablecoins could make it harder to identify and tax cryptocurrency profits, as users would have less need to convert their holdings into fiat currencies.

Moreover, the tax department flagged offshore exchanges and private wallets as issues for tracking. Those channels make it harder to identify beneficial owners. Peer-to-peer trades in rupees also make taxable income difficult to trace.

Compliance already lags. Fewer than a quarter of the 645,000 people who traded crypto in the year ending March 2023 reported it on tax returns. India taxes crypto gains at 30% and levies a 1% tax on each trade.

The coming months will show whether the government turns the RBI’s prohibition lean into law or keeps crypto in limbo.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post India’s Central Bank Renews Push to Keep Crypto Out of the Financial System appeared first on BeInCrypto.

Hot French startup ZML releases free product to speed inference across lots of AI chips

Her spending made her lose her control over it #podcast #finance #makingmoney

Nottingham fire live: ‘Avoid area’ warning with evacuation after scrapyard blaze

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Weekend Open Thread: Staud – Corporette.com

Her spending made her lose her control over it #podcast #finance #makingmoney

Earn More Money with These 3 Powerful Habits | Daily Success Tips That Actually Work

LIVE: BITCOIN CRASHING? Michael Saylor on BTC & MSTR Prediction 2026

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: High Hopes

-

NewsBeat3 days ago

NewsBeat3 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Crypto World7 days ago

Airdrop Registration Becomes Key Focus For Remittix As RTX Launch Updates Approach

-

Fashion2 days ago

Fashion2 days agoOpen Thread: What Great Books Have You Read Recently?

-

Politics5 days ago

Politics5 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World5 days ago

Crypto World5 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Sports7 days ago

Sports7 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Business2 days ago

Business2 days agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Crypto World6 days ago

Crypto World6 days agoBinance stock trading tops $1B in first month after launch

-

News Videos1 day ago

News Videos1 day agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Crypto World6 days ago

Crypto World6 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

Crypto World3 days ago

Crypto World3 days agoSouth Africa proposes crypto tax guidance under existing rules

-

Crypto World2 days ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

News Videos2 days ago

News Videos2 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech1 day ago

Tech1 day agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Tech3 days ago

Tech3 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business7 days ago

Business7 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

NewsBeat6 days ago

NewsBeat6 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

Business5 days ago

Business5 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World6 days ago

Crypto World6 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

You must be logged in to post a comment Login