Crypto World

What is a multisig wallet? How crypto’s biggest treasuries get secured, and robbed

Multisignature wallets guard most of the serious money in crypto: DAO treasuries, exchange cold storage, protocol funds, and the savings of the security-conscious. They are also at the center of the industry’s biggest heists, from Bybit’s $1.5 billion to this year’s UXLINK breach, because attackers stopped picking locks and started fooling the people holding the keys. This guide explains how multisig actually works, the M-of-N design choices, how the famous multisig hacks really happened, and how to run one without becoming a case study.

Summary

- Multisig wallets protect crypto funds by requiring multiple approvals, reducing the risk of a single compromised key.

- Major breaches such as Bybit and Ronin exposed human error and interface attacks rather than weaknesses in multisig technology itself.

- Strong operational practices including independent verification and separate key management remain essential for multisig security.

Ask where crypto’s serious money lives, and the answer, overwhelmingly, is behind multiple signatures. A majority of institutional custodians run multisignature arrangements; DAO treasuries holding billions coordinate through them; exchanges guard cold storage with them; custody chains behind institutional products depend on them; and protocols park their upgrade keys and reserve funds inside them, most commonly in Safe, the contract system formerly known as Gnosis Safe, which alone secures values rivaling large banks. The idea is old, borrowed from bank vaults and nuclear launch protocols: no single person, key, or machine should be able to move what matters. Require M signatures out of N keys, 2-of-3, 3-of-5, and a thief must compromise several independent guardians instead of one.

And yet the largest theft in crypto’s history, Bybit’s $1.5 billion, walked out through a multisig. So did this year’s $11.3 million UXLINK breach, and the Ronin bridge’s $600 million before them. The pattern is the most instructive fact in modern crypto security: the multisig math has never been broken; the humans and interfaces around it are broken constantly. Multisig eliminates the single point of failure and replaces it with a subtler question, whether your several points of failure are actually independent, and the industry’s disaster record is a catalog of discovering they were not.

This guide covers the mechanism and its failure modes with equal seriousness: how multisignature schemes actually work on Bitcoin and on smart-contract chains, how to choose M and N and what each choice trades, the anatomy of the great multisig heists and the blind-signing problem at their core, multisig against its modern rivals, MPC and smart accounts, and the operational playbook that separates the treasuries that survive from the ones that headline.

The mechanism: M-of-N, on two architectures

A multisig wallet requires a threshold of signatures, M, from a set of authorized keys, N, before any transaction executes. A 2-of-3 personal setup might split keys across a hardware wallet at home, a second device in a bank box, and a trusted relative; a 4-of-7 DAO treasury spreads keys across council members on different continents. The threshold is the design’s dial: security against compromise rises with M, resilience against key loss rises with the gap between N and M, and operational friction rises with both.

Under the hood, two architectures implement the idea. On Bitcoin, multisig is native to the protocol’s scripting: an address encodes the M-of-N requirement itself, and spending requires the signatures to be presented and verified by the network. It is minimal, battle-tested, and rigid, changing signers means moving funds to a new address. On Ethereum and similar chains, multisig lives in smart contracts: a program, such as a Safe, holds the funds and enforces the policy, collecting signatures until the threshold is met and then executing. The contract approach is vastly more flexible, signers can be rotated, thresholds changed, daily limits and timelocks and module extensions added, and that flexibility is double-edged: the policy is code, code can have flaws, and, as the disaster section will show, the richness of what a contract wallet can execute is exactly what modern attackers exploit.

The transaction flow in both worlds follows the same rhythm. Someone proposes a transaction, recipient, amount, and, on contract wallets, arbitrary program calls. The proposal circulates to signers, each of whom reviews and cryptographically approves it with their own key, on their own device. When approvals reach the threshold, the transaction becomes executable and is broadcast. Every step is auditable: the chain records exactly which keys approved what, creating the accountability trail that makes multisig the governance tool of choice for DAO treasuries whose control is otherwise contested through token votes, for corporate funds requiring officer sign-off, and for escrow arrangements where a neutral third key arbitrates disputes, the human-governed cousin of the time-locked contracts that automate escrow on-chain.

Choosing M and N: the design space

The threshold choice is a risk allocation, and the standard configurations each answer a different question. 2-of-2 is a partnership with no tiebreaker and no recovery, one lost key strands the funds, and is mostly used with one key held by a service. 2-of-3 is the individual’s workhorse: it survives the loss of any one key, resists the compromise of any one key, and keeps signing friction tolerable; the classic personal build spreads three hardware keys across locations, and the classic collaborative-custody build gives one key to a professional service that can co-sign recovery but can never move funds alone. 3-of-5 and up is institutional territory, tolerating multiple losses and requiring multiple corruptions, at the price of coordination overhead that, in practice, tempts organizations into the worst sin of the genre: concentration, several keys held by one person, one office, one laptop, or one cloud account. A 3-of-5 whose keys live in three browsers and two drawers of the same office is a 1-of-1 with extra steps, and post-mortems of real losses find this shape constantly. The rule the design space reduces to: the security of a multisig is the security of its most correlated keys, and independence, of people, devices, software, and geography, is the entire point of the exercise.

Key-holder policy matters as much as the numbers. Every signer is a target the moment the arrangement is visible on-chain, and large treasuries are visible by definition, tracked by the same wallet-attribution lens that maps every whale. Serious operations therefore treat signers as an attack surface: hardware keys only, dedicated signing devices, no signer identities published unnecessarily, and procedures rehearsed before they are needed, because the day a treasury must move funds under pressure is the worst day to discover the third signer’s key is in a safe nobody can open.

How multisigs actually get robbed

The heist record is where this subject earns its place in a security curriculum, because the attacks share an anatomy and it is not the one intuition expects. No major multisig loss has come from breaking the cryptography. They come from making the right people sign the wrong thing.

The Bybit theft, $1.5 billion, the largest in industry history, is the canonical case. The exchange’s cold storage sat behind a multisig with executives as signers, exactly as best practice prescribes. Attackers, attributed to North Korea’s Lazarus Group, compromised the infrastructure of the wallet interface the signers used, so that when the executives performed a routine, scheduled transfer, their screens showed the legitimate transaction while their hardware keys signed a different payload, one that handed the attackers control of the wallet’s logic. Every signature was genuine. Every signer was diligent by the standard of what they could see. The vault held; the vault’s window lied. The Ronin bridge before it fell differently but rhymes: a 5-of-9 arrangement whose keys were insufficiently independent, with one organization controlling enough of them that compromising it, via a social-engineered employee, crossed the threshold, the key-compromise pattern behind the largest bridge disasters. And this year’s UXLINK breach showed the small-scale version: attackers who gain threshold control do not just drain, they use the wallet’s own administrative powers, adding themselves as signers, ejecting the owners, because on a contract multisig, governance of the wallet is itself just another transaction.

The common thread is blind signing. A hardware key protects the signature; it does not tell the signer, in honest human terms, what they are signing, and complex contract-wallet payloads are unreadable hashes on a tiny screen. Attackers therefore aim at the layer between intention and signature: the web interface, the signer’s laptop, the proposal pipeline, the human’s routine. The defenses that address this are specific and increasingly standard: independent verification of every payload on a second channel before signing, signing devices that decode and display transaction meaning, simulation tools that preview a transaction’s actual effects, timelocks that delay large movements long enough for review, and the simple institutional rule that no transaction is routine, because routine is precisely the state of mind the Bybit attackers were waiting for.

From Bitcoin script to Safe: how the standard was built

Multisig’s history is the history of crypto custody growing up, and its milestones explain today’s defaults. The capability is nearly as old as Bitcoin itself, formalized in the protocol’s early years through pay-to-script-hash addresses that let spending conditions, including M-of-N signature requirements, be encoded on-chain. The first institutional era was built directly on it: the early exchange and custody pioneers ran Bitcoin multisig vaults, and the first collaborative-custody businesses sold 2-of-3 arrangements to individuals a decade ago. The idea crossed to Ethereum as smart-contract wallets, where the flexibility of code produced both the triumphs and the scars: an infamous 2017 library bug in a widely used contract wallet froze hundreds of millions permanently, the formative lesson that flexible custody code is itself an attack surface, and the survivor of that era’s consolidation, Gnosis Safe, hardened through years of audits and adversarial value into the default it is now.

Today Safe-style contracts secure treasuries whose combined value rivals major banks, the DAO era having made the multisig council crypto’s standard governance executive, and Bitcoin’s own multisig lineage continues in parallel, favored for deep cold storage precisely because its rigid, minimal script surface offers so little to exploit.

The standardization has a consequence worth naming: concentration of a different kind. When one contract system secures the majority of on-chain treasuries, its code, its interface, and its upgrade process become systemic infrastructure, and the Bybit attack’s compromise of interface infrastructure was, among other things, a demonstration that the ecosystem’s eggs share more baskets than the M-of-N math suggests. The response, interface diversity, independent transaction verification services, signing-device decoding, is effectively the community rebuilding independence one layer up the stack, the same principle the wallets encode, applied to the tooling around them.

Setting one up: the individual’s path

For an individual reader, the practical on-ramp deserves concreteness. A personal 2-of-3 today is a weekend project: three hardware keys, ideally from two different vendors to avoid a shared firmware flaw; a contract wallet on an inexpensive network or a native Bitcoin multisig, depending on holdings; owner addresses triple-checked before deployment, because a mistyped owner is a permanent stranger with signing power; and the three keys distributed across genuinely separate locations, home, bank box, trusted party, with recovery instructions that someone other than you can follow.

The recurring costs are minor, deployment gas and slightly larger transaction fees, and the recurring disciplines are not: test the setup with small amounts first, rehearse a lost-key migration before losing one, keep a small gas balance where the contract needs it, and revisit the arrangement whenever a signer, device, or living situation changes. The friction is real, every transaction becomes a small ceremony, and the friction is the feature: a wallet that requires deliberation cannot be drained by one bad click, which, given that a single mistaken approval is how most individual losses now happen, is the entire value proposition in one sentence.

Multisig and its rivals: MPC and smart accounts

Two adjacent technologies answer the same single-point-of-failure problem, and choosing among them is a real decision, not branding.

Multi-party computation, MPC, splits one key into mathematical shares held by different parties, who jointly compute a signature without the full key ever existing anywhere. To the blockchain, the result looks like an ordinary single signature: cheaper, private, chain-agnostic, and revealing nothing about the policy behind it. The trade is opacity and dependence: the threshold logic lives in the providers’ off-chain software rather than in public code, there is no on-chain trail of who approved what, and the institutional MPC market is dominated by vendors whose systems must be trusted. Institutions increasingly use both, MPC for operational hot flows, multisig for deep cold governance.

Smart accounts, account abstraction, generalize the contract-wallet idea: programmable accounts with recovery guardians, spending policies, session keys, and multisig as merely one available policy among many. They are the likely long-term home of these ideas for individuals, folding multisig-grade protection into interfaces normal users can operate. For treasuries today, the audited, battle-hardened dedicated multisig remains the standard, precisely because its decade of scars, documented above, produced a decade of hardening.

Between the architectures sits a question every treasury eventually asks: how many signers is too many? The coordination cost of thresholds grows faster than linearly, five signers across five time zones can turn a routine payment into a week, and organizations respond with delegation structures that deserve scrutiny because they quietly re-centralize. Common patterns include a small operational multisig with spending limits for daily flows, governed by a larger cold council for everything above the limit; module systems that pre-authorize specific recurring actions; and role separation between proposers, who prepare transactions, and signers, who approve them, narrowing what any single compromised seat can initiate. Each pattern trades purity for function, and the honest evaluation standard is the same one the thresholds themselves answer to: enumerate what the compromise of each seat, device, and interface enables, and check that no enumeration ends in everything. Treasury security is not a product purchased once; it is that enumeration, repeated, forever, against adversaries who read the same post-mortems.

One misconception deserves explicit correction before the playbook: multisig does not protect against approving a bad idea unanimously. If all required signers are deceived by the same forged interface, the same fraudulent counterparty, or the same internal fraudster’s paperwork, the threshold is met and the mathematics executes the mistake faithfully. Signature independence protects against compromised keys; only verification independence, different signers checking the payload through different tooling and channels, protects against compromised information, and the great heists were failures of the second kind wearing the confidence of the first.

The operational playbook

Everything in this guide compresses into a practice list, and the list is the difference between the mechanism and its reputation. Choose thresholds for both compromise and loss: 2-of-3 personal, 3-of-5 or higher institutional. Make independence real: different people, devices, vendors, physical locations, and no key in a browser. Verify what you sign: second-channel confirmation of every payload, simulation before approval, and a standing suspicion of anything urgent. Add time as a defense: timelocks on large transfers turn a successful deception into a recoverable one. Rehearse recovery: a lost-key drill and a signer-rotation drill, run before either is needed. And treat the wallet’s own governance, adding or removing signers, changing thresholds, as the crown jewels, because the UXLINK lesson is that whoever can edit the signer set owns everything the signatures guard.

Multisig, honestly summarized, is the most successful security primitive crypto has deployed: it moved the industry’s treasuries from single hackable keys to arrangements that require conspiracies to rob, and the conspiracies, note, have had to grow to nation-state sophistication to succeed. Its failures are not refutations but curriculum, each one converting a blind spot into a checklist item, and the checklist is public. The vault works. Guard the window.

Two closing perspectives round out the subject. The first is the defender’s asymmetry, and it is encouraging: every major multisig loss has produced a specific, adoptable countermeasure, payload verification after Bybit, key-independence audits after Ronin, signer-set timelocks after the takeover breaches, and the countermeasures compound while the attacks must be reinvented. A treasury running the current playbook is not facing the same odds its predecessors did; it is facing adversaries who must now defeat every lesson previous victims paid for. Security in this domain is cumulative, and the cumulation is public.

The second is the philosophical point hiding in the mechanism, worth one paragraph because it explains multisig’s cultural weight in crypto. A multisignature arrangement is a constitution in miniature: a written rule about who may act, enforced by mathematics instead of courts, visible to everyone it governs. That is why the technology became the executive branch of the DAO era, why its failures feel like institutional scandals rather than mere thefts, and why its steady hardening matters beyond the funds it guards. Crypto’s founding claim was that agreements could be enforced without trusted enforcers, and the multisig, requiring humans to agree while preventing any of them from betraying the agreement, is the claim’s most widely deployed, most thoroughly attacked, and most durably successful embodiment. The vaults hold more than money.

For further orientation, the study list is mercifully practical: the post-mortems of the major incidents named above, each a free masterclass in one failure mode; the documentation of the dominant contract systems, whose security recommendations encode the industry’s accumulated scar tissue; the transaction-simulation and payload-decoding tools that address blind signing directly; and, for organizations, the published treasury-operations frameworks that DAOs and custodians have converged on. Multisig is the rare corner of crypto where the best practices are written down, battle-tested, and free, and where the distance between the average outcome and the best outcome is almost entirely a matter of reading them.

And if this guide leaves a single instinct behind, let it be this one: in multisig, the question is never whether the mathematics will hold, because it will. The question, every time, for every transaction, is whether the humans holding the keys know what they are signing, and every practice in the playbook above is, in the end, a different way of making sure the answer is yes.

Disclaimer: This article is for educational purposes only and does not constitute investment or security advice. Digital asset custody carries significant risk, and no arrangement eliminates it. Details are current as of July 9, 2026. Always do your own research.

Frequently asked questions

What is a multisig wallet in simple terms?

A multisig wallet is a crypto wallet that requires multiple private keys to approve any transaction, following an M-of-N rule such as 2-of-3 or 3-of-5. No single person or device can move the funds alone: a proposal must collect the threshold number of signatures, each from an independent key, before it executes. This removes the single point of failure that defines ordinary wallets.

How does a 2-of-3 multisig work?

Three keys are created and stored independently, for example on a hardware wallet at home, a second device in another location, and with a trusted party or service. Any two of the three must sign for a transaction to execute. One key being lost does not strand the funds, and one key being stolen does not endanger them, which is why 2-of-3 is the standard personal configuration.

Are multisig wallets actually safe if Bybit lost $1.5 billion through one?

The mathematics has never been broken; the famous losses came from deceiving the signers. In the Bybit case, attackers compromised the signing interface so executives approved a malicious payload their screens displayed as routine. The lesson is that multisig secures the signatures, while operational discipline, verifying payloads independently, using devices that decode transactions, adding timelocks, must secure what gets signed.

What happens if I lose one of my keys?

If your threshold still allows it, for example losing one key of a 2-of-3, the remaining keys can move the funds, and best practice is to migrate promptly to a fresh setup with a full key set. If losses exceed the tolerance, the funds are permanently inaccessible, which is why the gap between N and M exists and why recovery drills matter.

What is the difference between multisig and MPC?

Multisig uses several complete keys with the threshold enforced on-chain, visible and auditable. MPC splits a single key into shares that jointly produce one ordinary-looking signature, with the policy enforced in off-chain software. Multisig offers transparency and battle-tested public code; MPC offers privacy, lower fees, and chain flexibility at the cost of trusting provider infrastructure. Institutions commonly use MPC for hot operations and multisig for cold governance.

Who should use a multisig wallet?

Anyone holding more crypto than they could bear to lose to a single mistake: individuals with significant savings, and, essentially without exception, organizations, DAOs managing community treasuries, companies with crypto on the balance sheet, protocols holding upgrade keys, and groups needing escrow. For small everyday balances, the coordination friction usually outweighs the benefit.

What is blind signing and why is it dangerous?

Blind signing is approving a transaction whose true contents you cannot read, typically a complex smart-contract payload shown as an opaque hash. It is the vector behind the largest multisig heists: attackers compromise the interface so signers see a legitimate transaction while approving a malicious one. Defenses include devices that decode payloads, independent second-channel verification, and simulation tools that preview effects.

Can the signers of a multisig be changed?

On smart-contract multisigs, yes: adding or removing signers and changing the threshold are themselves transactions requiring threshold approval. That flexibility enables rotation and recovery, and it is also a target, since an attacker reaching the threshold can eject the rightful owners entirely, as recent breaches showed. Treat signer-set changes as the most sensitive operation the wallet performs.

STRC by Strategy (formerly MicroStrategy) is now offering investors more than 28% upside potential if it returns to par and pays its dividends over the next year. But investors keep selling it anyway.

Over the last week, STRC has declined 2% and is down 11% in 30 days. These sales in the face of Strategy’s generous offer are votes of diminishing confidence in management, including founder Michael Saylor.

As of today, STRC was paying a 12% annualized dividend at full par value of $100 yet was on sale for under $86 per share.

If that stock returns to Strategy’s intended $99-100 trading range and pays its dividends, investors would earn a total return of at least 15% on their stock price appreciation plus a stream of semi-monthly dividends.

Even better, those dividends have beneficial tax treatment as return of capital, meaning that 12% is even higher than 12% for many investors on a tax-adjusted basis.

Read more: Michael Saylor wants $100 STRC — the market says different

Moreover, the rally from sub-$86 to over $99 per share could occur anytime, not simply at a 12-month maturity. This would make the time-weighted value of any early 15% rally worth even more than if it rallied evenly across 12 months.

In addition, as if the offer wasn’t already sweet enough, Strategy pays its 12% dividend rate on each share’s full $100 par value, not based on the USD value of investors’ STRC holdings.

That means that an investor buying STRC below $86 per share is actually earning an effective dividend yield over 14% plus return of capital tax treatment.

Adding these numbers — 15% plus a tax-advantaged 14% — makes the offer sound almost too good to be true.

For many investors, an opportunity over 28% probably is.

Corporate objective for STRC to trade at $99–$100

Michael Saylor keeps saying he wants STRC to trade at $99-100, and investors could earn over 28% if it does within a year. Yet the market keeps selling.

The risk to counterbalance STRC’s incredible offer is, of course, that the price of STRC keeps declining anyway.

There is, after all, no guarantee by Strategy that STRC will ever rally back above $99. In fact, it could trade at any price down to $0.

It’s simply a preferred stock that Saylor’s company issued to fund BTC purchases. It’s changed hands for as low as $71.25 on the Nasdaq.

In other words, management has promised to defend $99-100 over the long term, yet they allowed it to trade 28.75% below par in the meantime. Not good.

Its own filings say its board intends to maintain the trading price of STRC near $100.

Yet even as the company funds an effective yield of roughly 14%, a return dwarfing junk bond yields and rivaling credit card rates, investors are still wary.

Read more: STRC crashes as Strategy’s unrealized BTC losses exceed $13 billion

STRC traders refuse to bid at par

Strategy built STRC to behave like a high-yield bank account or money market with a fatter payout rate, even though it’s nothing like an insured savings product.

No FDIC insured bank account or money market is allowed to lose money like the price of STRC.

Were a rational investor to have full confidence in Strategy to sustain its above-average dividend payouts, they should pay up to the full $100. Yet no one is doing that right now.

In an attempt to reinstill confidence, Strategy has hiked it dividend rate from 9% at STRC’s July 2025 debut through a long series of hikes to 12%, yet the price of STRC continues to deteriorate.

Each increase in dividend and decrease in stock price concedes that demand is too weak and uncertainty is still too high.

Paying $1.25 billion and STRC still in the mid-$80s

The cost of a quasi-peg that won’t hold is costing Strategy $1.25 billion annually in dividend payouts. And this figure is rising rapidly.

The reason bidders stay away sits in Strategy’s own disclosures. The company can change or suspend the dividend at will, guarantees nothing about the share price, and gives holders no way to redeem STRC for the $100 they want.

Worse, Strategy is now selling the asset meant to make its whole scheme work.

On July 6, Saylor disclosed that Strategy sold 3,588 BTC to fund dividends. Strategy’s stocks like STRC are, in theory, supposed to be supported by a growing treasury of BTC that has, in recent weeks, shrunk.

BTC was trading on thursday near $62,700, down 28% year to date. MSTR, Strategy’s common stock, opened for trading today down 38% year to date, amplifying BTC’s losses to the downside.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

SpaceX shares have gained fresh momentum after Raymond James initiated coverage with an $800 price target, implying about 440% upside from current levels.

Summary

- Raymond James initiated SpaceX with a Strong Buy rating and an $800 price target, implying about 440% upside.

- Wall Street support strengthened as Morgan Stanley, Goldman Sachs, Citigroup, UBS, and Wells Fargo also issued bullish ratings.

- SpaceX expanded its Starlink plans, Ark Invest added shares, and the company’s Bitcoin holdings remained in focus.

According to Raymond James, the brokerage has started coverage of SpaceX with a Strong Buy rating and an $800 price target, making it one of the most optimistic forecasts issued by a major Wall Street firm.

The target came as SPCX traded around the $153 level on Thursday after rising about 3.2%, following a difficult stretch in which the stock had fallen more than 25% from recent highs despite joining the Nasdaq-100, as previously reported by crypto.news.

The brokerage linked its bullish outlook to three long-term businesses that it believes could support future growth. Raymond James pointed to the continued development of Starship, the expanding Starlink satellite internet network, and the company’s potential to become a major global infrastructure provider through its launch and communications operations.

Wall Street support for SpaceX continues to grow

Fresh optimism from Raymond James builds on a series of positive ratings issued by other investment banks in recent days. Morgan Stanley began coverage with an Overweight rating, assigning a base-case price target of $300 and a bull-case target of $600.

Goldman Sachs also initiated coverage with a Buy rating and a $205 target, while Citigroup started coverage with a Buy recommendation and a 12-month target of $200. UBS and Wells Fargo also launched coverage with positive recommendations, adding to institutional support for the newly listed company.

Although Raymond James’ forecast stands well above those targets, the latest recommendation has added to expectations that analysts continue to see substantial upside even after SpaceX’s recent share price volatility.

Separately, Cathie Wood’s Ark Invest has continued increasing its exposure to SpaceX. According to reports, the investment firm bought 153,084 shares across its ARKK, ARKQ, and ARKX exchange-traded funds. Based on SpaceX’s closing price of $148.30, the purchase was valued at roughly $22.7 million.

Starlink expansion and Bitcoin holdings stay in focus

Operational developments have also remained active. SpaceX has filed an application with the U.S. Federal Communications Commission seeking approval to deploy as many as 100,000 third-generation Starlink satellites, a move that would significantly expand its satellite internet network if approved.

The company has also maintained a rapid launch schedule. Reports show SpaceX deployed 1,589 Starlink satellites during the first half of 2026, surpassing the previous first-half record of 1,489 launches achieved in 2025.

Outside its space business, SpaceX recently drew attention in the cryptocurrency market. As crypto.news reported, a wallet linked to the company transferred $88 worth of Bitcoin on July 8, ending six months without on-chain activity.

Data from Arkham Intelligence showed SpaceX still holds about 18,712 BTC, valued at roughly $1.16 billion, while the receiving wallet contains 614 BTC worth about $38 million.

Investors are also tracking developments tied to Elon Musk’s artificial intelligence ecosystem after SpaceXAI disclosed plans to release Grok 4.5 to the public.

Despite the growing list of bullish analyst calls, some investors remain cautious. Critics argue that SpaceX’s valuation already prices in much of its expected expansion, while others say the company’s first public earnings report will provide a clearer basis for assessing whether current expectations can be justified.

The Trump White House has rejected accusations that it is refusing to nominate Democratic commissioners to the Securities and Exchange Commission and Commodity Futures Trading Commission as the Senate moves closer to debating the CLARITY Act.

Summary

- White House says it requested Democratic nominees for the SEC and CFTC but has not received any names.

- CLARITY Act negotiations continue as lawmakers debate ethics rules, DeFi provisions, and regulatory appointments.

- Senators Cynthia Lummis and Ron Wyden have defended different parts of the bill ahead of a Senate vote.

According to a letter sent by the White House to Senate Majority Leader John Thune and Senate Democratic Leader Chuck Schumer, the administration said it had already asked for suitable Democratic nominees for both the SEC and the CFTC but had not received any names in response.

The letter pushes back against criticism that the administration is deliberately leaving seats vacant at two agencies expected to oversee large parts of the digital asset market if the CLARITY Act becomes law.

With the Senate still yet to schedule a floor vote on the market structure bill, the exchange over regulatory appointments has added another issue to negotiations already facing time pressure. As crypto.news reported earlier, lawmakers are working against the Senate’s Aug. 7 recess, leaving a limited window to move the legislation forward.

Senate negotiations continue before floor vote

Although the White House defended its position on the nominations, it remains unclear whether the disagreement will influence support for the CLARITY Act. Lawmakers from both parties are still negotiating several outstanding provisions, including an ethics section that has become part of the broader talks.

Separately, law enforcement organizations have argued that the bill’s decentralized finance provisions could make investigations into illicit finance more difficult. Those concerns have become another point of discussion as senators continue to negotiate the final language before any vote is scheduled.

At the same time, debate over protections for blockchain developers has continued. As crypto.news reported earlier today, Democratic Sen. Ron Wyden urged Thune and Schumer to preserve Section 604, known as the Blockchain Regulatory Certainty Act, in any future version of the CLARITY Act.

In a letter to the Senate leaders, Wyden argued that legal protections for non-custodial blockchain developers should remain part of the legislation as negotiations continue.

Pro-crypto senators defend key provisions

Meanwhile, Sen. Cynthia Lummis publicly defended the CLARITY Act after Sen. Elizabeth Warren criticized the proposal, arguing that it would create opportunities for sanctions evasion.

In a post on X, Lummis responded that both lawmakers want bad actors held accountable but differ on how to achieve that outcome. She pointed to Section 303, saying it would authorize new crypto sanctions targeting Iran, while Section 305 would allow major cryptocurrency exchanges to stop illicit funds before they reach North Korea.

Lummis has also warned that Congress may not get another opportunity to pass comprehensive digital asset legislation before the end of the decade. In an earlier X post, she argued that failing to pass the CLARITY Act would leave the United States following rules written by other countries instead of establishing its own regulatory framework.

For now, the White House’s defense of its nomination process, ongoing negotiations over key provisions, and competing arguments from lawmakers have all become part of the political backdrop as the Senate prepares for its next steps on one of the crypto industry’s most closely watched bills.

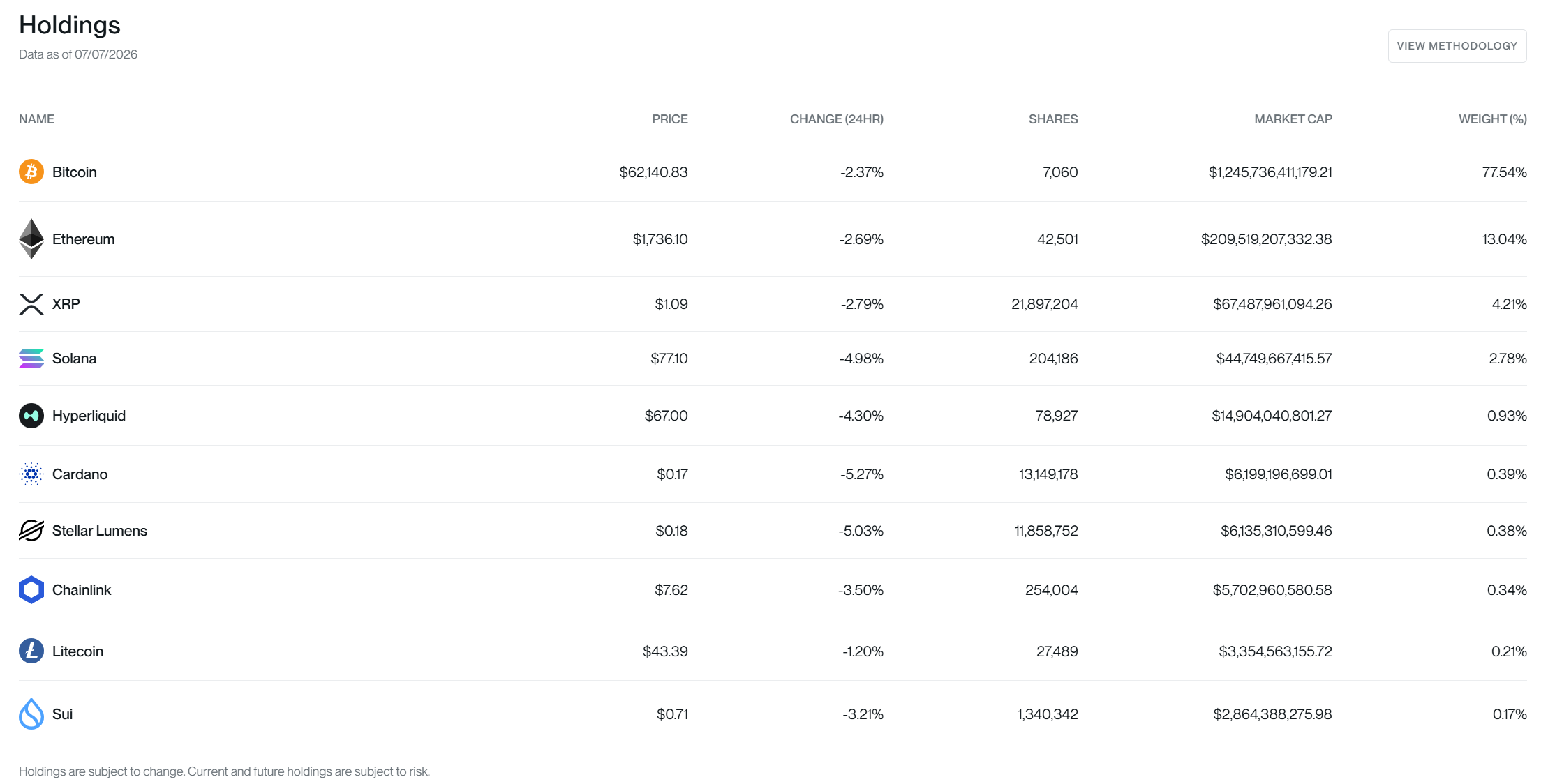

Bitwise has dropped Polkadot (DOT) and Avalanche (AVAX) from its flagship Bitwise 10 Crypto Index ETF (BITW). Hyperliquid (HYPE) and Stellar (XLM) were added to the fund’s latest monthly rebalance.

BITW works like a crypto stock index fund. It automatically holds the 10 largest eligible coins by market cap, so investors gain exposure to HYPE and XLM without buying them directly.

Why Hyperliquid and Stellar Entered the Bitwise 10 Crypto Index ETF

Bitwise’s rebalance results show HYPE entering at a 0.93% weight and XLM at 0.38%. That makes HYPE the fund’s fifth-largest holding, ahead of Cardano (ADA), Chainlink (LINK), Litecoin (LTC), and Sui (SUI). Bitcoin (BTC) still accounts for 77.54% of the fund.

Hyperliquid earned its seat through sheer size. The token ranks 10th among all cryptocurrencies at roughly $15 billion, according to BeInCrypto Markets data. HYPE trades near $67.92, weeks after hitting a new all-time high of $76.70 on June 16.

The project runs the dominant decentralized exchange for perpetual futures, a popular type of crypto derivative. It leads that perp DEX race by a wide margin.

Stellar ranks 18th overall, but Bitwise’s eligibility screens lift XLM into the qualifying group.

What the Exit Means for DOT and AVAX

The removals reflect rankings, not a verdict on either project. Both tokens led the 2021 bull market. DOT peaked at $54.98 in November 2021 but now trades near $0.83, a 98% fall that leaves it ranked 53rd. AVAX topped $144 the same month and has since lost 95%, sitting at $6.76, 32nd.

Neither network loses anything on-chain. Staking, development, and payments continue unaffected. Both coins had joined BITW at its NYSE Arca debut in December 2025 and lasted roughly six months.

Will Hyperliquid Keep Its Seat?

The near-term answer looks like yes. HYPE’s $15 billion market value is 10 times DOT’s, five times AVAX’s, and more than double Stellar’s $6.2 billion. A challenger would need to close that gap before the rankings flip.

Demand signals also point the right way. Recent crypto ETF flows showed HYPE products drawing fresh capital while Bitcoin funds recorded outflows. Bitwise even runs a dedicated spot Hyperliquid ETF, BHYP.

The main threat comes from within. Only about 22% of HYPE’s 1 billion maximum supply is circulating today, and its fully diluted value of nearly $64 billion is over four times its market cap.

BeInCrypto’s Hyperliquid price outlook flags those scheduled unlocks as the key risk, since new supply can pressure prices.

DOT’s slide from launch roster to 53rd shows how fast the table can turn. For now, HYPE holds the strongest hand among BITW’s smaller holdings, provided demand keeps outrunning its unlock schedule.

The post Bitwise Drops 2 Altcoins From Flagship Crypto ETF: Will Hyperliquid Keep Its Seat? appeared first on BeInCrypto.

![World's daily on-chain volume, showing the pre-prank peak, Source: Dune/ario_57]](https://wordupnews.com/wp-content/uploads/2026/07/9bf00bf07a9042d7bfc0990ea56902d6.webp)

World, a week-old Solana (SOL) prediction market, staged a fake exit. On July 8, it said it was leaving Solana for Robinhood Chain, then admitted the whole thing was a crypto prank the following day.

The gag drew millions of views and briefly fooled parts of the crypto industry. It also divided opinion on whether staged deception is smart marketing or a costly gamble for a young platform.

How the Crypto Prank Spread

World went live on Solana on July 1 inside the Phantom wallet, with Chainlink (LINK) handling data and settlement. Solana’s official account had promoted the debut just a week earlier.

Days later, the project told followers it was leaving for Robinhood Chain. It thanked the Solana Foundation and posted a polished logo for the supposed move.

The target made the fake believable. Robinhood Chain is a real Arbitrum-based Layer 2 that launched on July 1 for tokenized stocks.

That same week, the network set a record daily volume of $563.9 million, according to DefiLlama. Meme coins, not tokenized stocks, drove the frenzy. It was arguably crypto’s hottest new chain.

Several outlets reported the migration as fact. Within a day, World revealed the joke.

The reception split. Solana co-founder Anatoly Yakovenko amplified the gag, and CoinGecko co-founder Bobby Ong called it sharp marketing.

“I’m still trying to figure out if they moved to Robinhood Chain or staying at Solana. I think this is a parody and they are actually staying on Solana. I guess it triggered many folks and got them the attention that they really want, which is all that matters in consumer tech,” Ong remarked.

Critics, however, saw a bait-and-switch that erodes trust in a product handling real bets.

Follow us on X to get the latest news as it happens

Did the Joke Pay Off?

The on-chain record complicates any victory claim. An independent dashboard built by analyst ario_57 tracks World’s activity. It shows roughly $4.37 million in notional volume. Daily users peaked near 3,000 since the July 1 launch.

![World's daily on-chain volume, showing the pre-prank peak, Source: Dune/ario_57]](https://assets.beincrypto.com/img/-avHN9_82Fzf-o66hJTGVAYBSIg=/smart/9bf00bf07a9042d7bfc0990ea56902d6)

Yet that volume crested around July 6, two days before the stunt. The cumulative totals cover the full launch week, not one viral afternoon. The prank coincided with World’s momentum. It did not create it.

The 2.3 million views were World’s own tally, a measure of attention rather than adoption. Meanwhile, prediction markets face fresh scrutiny, raising the cost of any misstep in trust.

For now, World has crypto’s attention and a working product behind the gag. Whether that attention becomes lasting users is the question the coming weeks will answer.

The post Worst Crypto Prank Ever? Viral Prediction Market Pulls Off Shocking Joke appeared first on BeInCrypto.

- Solana (SOL) is up 18.5% over the past 30 days.

- Analysts are watching the $85–$90 resistance zone.

- B3 futures and FullSend add to Solana’s momentum.

Solana has regained momentum after a difficult stretch earlier this year, with the token climbing back above the $77 mark and extending its monthly recovery.

At the time of writing, SOL is trading at $77.73, up 0.8% over the past 24 hours after moving between $76.25 and $78.62 during the session.

Over the past month, the cryptocurrency has gained 18.5%, while its two-week performance stands at 21.6%.

The recent recovery has renewed interest in Solana’s outlook, particularly as technical indicators, institutional activity, and network developments begin to align.

While the token remains well below its all-time high of $293.31, several analysts believe the current trend has created room for further upside if key resistance levels are cleared.

Technical picture points to key breakout levels

SOL’s latest rally follows a rebound of roughly 38% from its recent low near $60, bringing renewed attention to the asset’s technical structure.

The recovery also marked Solana’s first positive monthly performance in several months, suggesting that selling pressure has eased.

Market analyst Ali Martinez has identified the $85 to $90 region as an important resistance zone.

A sustained move above that range would bring the psychologically significant $100 level back into focus.

SOLANA: BIG SUPPLY WALL

Solana is currently attempting to reclaim a resistance zone between $79 and $85.

According to URPD data, roughly 105 million SOL were transacted within this range, establishing a dense supply cluster.

Reclaiming this zone as support clears the overhead… https://t.co/CZXB9kPtOz pic.twitter.com/jiZI3GJ8z4

— Ali Charts (@alicharts) July 8, 2026

Another closely watched analyst, Michaël van de Poppe, has highlighted the importance of the $73- $76 area, describing it as a major support zone that continues to underpin the broader recovery.

According to Poppe, as long as that area remains intact, the longer-term structure remains constructive from a technical standpoint.

Things start to become interesting here for $SOL.

If it is able to hold between $ 73- $ 76 and bounce back upwards, it is a strong signal that the markets are ready to run to higher than $100.

If that doesn’t happen, boy, we’ll be seeing new lows across the board. pic.twitter.com/XRz4iMfxY6

— Michaël van de Poppe (@CryptoMichNL) July 8, 2026

Attention has also shifted to Solana’s performance against Bitcoin.

The SOL/BTC trading pair has shown signs of strengthening after spending months in decline.

According to technical analysis, a breakout above the long-term resistance around 0.00140–0.00145 BTC could indicate improving relative strength for Solana compared with Bitcoin.

If that breakout is confirmed, technical projections place the next major value area between $140 and $150.

Those levels are based on historical trading activity rather than guaranteed price targets, meaning further confirmation would still be needed before the market could sustain such a move.

At the same time, focus is on the $75 to $78 range as an important near-term support area.

Holding above that zone would help preserve the current recovery, while a break below it could slow bullish momentum.

Institutional adoption continues to expand

Beyond price action, Solana has also benefited from growing institutional participation.

Brazil’s stock exchange, B3, recently expanded its regulated cryptocurrency derivatives offering by introducing Solana futures alongside Ethereum futures and Bitcoin options.

The contracts are settled in US dollars and reference Nasdaq’s digital asset benchmark prices.

Each Solana futures contract represents 5 SOL, giving professional investors another regulated instrument for gaining exposure to the asset or managing risk through hedging strategies.

B3 also reduced the size of its Bitcoin futures contracts to improve accessibility, a move that reflects broader efforts to increase participation in regulated crypto derivatives.

The expansion places Solana alongside Bitcoin and Ethereum within one of Latin America’s largest regulated exchange environments.

While derivatives products do not directly determine price direction, they typically improve market efficiency by expanding trading and hedging opportunities for institutional participants.

Recent infrastructure developments have also focused attention on Solana’s ability to support high-volume financial applications.

Privy, the wallet infrastructure provider acquired by Stripe, has partnered with Jito Labs to launch FullSend, a transaction routing system designed specifically for the Solana blockchain.

Instead of relying solely on traditional RPC infrastructure, FullSend routes transactions directly to the validator responsible for producing the next block.

According to the companies, the system has been operating in production since January and has processed millions of transactions with 99.999% landing reliability.

The technology also reduces transaction inclusion latency to approximately 50 milliseconds, compared with roughly 200 milliseconds or more under conventional routing methods.

For developers building payment platforms, trading applications, or financial services, those improvements reduce failed transactions during periods of network congestion while simplifying transaction management.

Developers using Privy’s wallet infrastructure receive these routing improvements without implementing additional software.

The announcement also highlights Privy’s growing reach following its acquisition by Stripe.

The company supports approximately 140 million accounts across applications that collectively process billions of dollars in monthly transaction volume.

The immediate focus now remains on whether buyers can push the token above the $85–$90 resistance range.

A successful breakout would place $100 at the centre of market attention, while continued strength in the SOL/BTC pair could reinforce the view that Solana is beginning to outperform Bitcoin once again.

Crypto World

Billions flowing out of bitcoin ETFs and private credit funds suggest rising market risks

Average requests rose to 10.3% of shares from 9.7% in Q1, but ranged widely (1.3%–38.1% at Blue Owl’s OTIC), Fitch said. Many requests were follow-ups from investors who were only partly satisfied last quarter. New inflows fell by about 56% on average, so most funds saw net outflows of roughly 3% of the prior quarter’s net asset value.

What’s concerning, for private credit, is that Fitch expects continued redemptions in the months ahead.

“With BDCs capping redemptions at 5% quarterly, unfulfilled requests will lead to persistent elevated redemptions for many firms in the coming quarters,” ratings agency Fitch warned,” the ratings agency said.

Same story, different structures

Bitcoin ETFs are liquid, exchange-traded vehicles, where outflows directly impact the spot price of BTC. Private credit BDCs are the opposite: illiquid, long-duration lending vehicles with built-in quarterly gates.

Still, the fact that investors rushed for exit in both at the same time does point to broader caution around liquidity and risk appetite.

Amid all this, energy markets continue to send risk-off signals, with the U.S. Strategic Petroleum Reserve at its lowest level since 1983. So, if the energy market remains disrupted, the government now has significantly less buffer to flood the market with oil and keep prices lower.

Bitcoin’s market appears to be in the later stages of a bear market, but the signals confirming a broader turnaround have not yet emerged. On-chain data shared by Glassnode shows the asset has recovered from $57,800 to nearly $63,000 over the past week, but it remains below both the True Market Mean of $76,600 and the Short-Term Holder Cost Basis of $72,200.

This leaves the asset in a “deep value” zone.

BTC Bottoming

Bitcoin has now spent about five months trading below both of these levels – one of the longest discount periods in its history. According to Glassnode, such long periods have historically provided the foundation for cyclical bottoms as investors accumulate at prices below the average cost of recent buyers and the broader active market. However, a further decline toward the Realized Price of roughly $53,000 remains possible.

The report identified long-term holders as the primary source of current selling pressure. Since early February, the share of realized value attributed to long-term holder losses has increased from 15% to 43%, which makes this cohort’s capitulation the largest contributor to downside pressure. These investors largely bought near the cycle peak and, after holding through months of losses, are increasingly selling as the downturn tests their conviction.

Glassnode said that this steady wave of distribution has prevented Bitcoin from reclaiming the upper end of its current trading range. The report added that long-term holders’ realized losses, measured on a 30-day moving average basis, recently climbed to around $280 million per day, which is the highest level since December 2022. This was the second major spike recorded during the current bear market.

Unlike the previous spike, however, this wave of capitulation has not yet begun to cool. Glassnode believes that a decline in this metric will be necessary before a credible transition back to bullish conditions can be considered.

Off-chain indicators also continue to point to weak institutional demand despite exhibiting modest improvement. The 30-day average of US spot Bitcoin ETF net flows has remained negative since mid-May. The average daily outflows declined from a peak of $193 million in early June to approximately $88.9 million.

While the slower pace of withdrawals is viewed as a “tentative positive,” institutions are still reducing exposure overall, which means demand has yet to stabilize. ETF trading activity also remains low, as daily volume ranges between $650 million and $950 million, roughly 80% below the $4.4 billion daily peak recorded in October 2025.

According to the report, both stronger trading activity and a return to neutral or positive ETF flows would be needed to confirm renewed institutional participation.

Defensive Positioning

Derivatives markets present a mixed picture. The options put/call ratio has fallen to 0.56, its lowest level this year, while perpetual futures funding rates indicate traders have cautiously rebuilt long positions after earlier de-risking. Despite this, the options market remained defensive.

“The 25-delta skew, the premium of downside protection over upside, is bid across every tenor. Every selloff since the winter has re-bid it, and late June’s spike to 24% was the most defensive the front end has been since the February selloff. Traders are still paying up to hedge each dip, even as the book leans long.”

Bitcoin also trades about 6% below the options market’s aggregated max pain level of $66,000, the price at which the greatest number of outstanding options would expire worthless and around which spot price has often gravitated as expiry approaches.

The post Bitcoin Is in Deep Value Zone, Yet $53K Drop Cannot Be Ruled Out appeared first on CryptoPotato.

Key Highlights

- Milwaukee Bucks forward Kyle Kuzma toured IBM’s Thomas J. Watson Research Center, sharing his quantum computing experience with his 1.3 million X platform followers.

- The tech giant clarified the laboratory visit wasn’t sponsored — Kuzma initiated contact after publicly showing interest in quantum technology on social platforms.

- Wall Street consensus rates IBM as “Moderate Buy” with a $306.47 average price target; Bank of America recently upgraded its forecast to $330.

- Sumitomo Mitsui Trust Group decreased its IBM holdings by 3.8% during Q1, divesting 91,570 shares, while institutional investors maintain 58.96% ownership.

- The company announces Q2 2026 financial results on July 22; shares began Thursday trading at $302.18, declining 1.3% intraday.

International Business Machines enters earnings reporting season amid a distinctive convergence of events — including a high-profile facility tour, dividend increases, and active analyst coverage.

International Business Machines Corporation, IBM

Kyle Kuzma, who plays forward for the Milwaukee Bucks, recently explored IBM’s Thomas J. Watson Research Center and documented the experience for his 1.3 million X platform audience. He expanded on the visit through a Monday LinkedIn update, stating: “Quantum could end up being the foundation that expands what AI is even capable of.”

IBM informed Barron’s that Kuzma’s visit materialized after the athlete publicly demonstrated curiosity about quantum computing technology via social channels. Company representatives verified no financial arrangement supported the visit.

Shares commenced Thursday’s session at $302.18, registering approximately 1.3% decline during trading. This valuation positions the stock considerably below its 52-week peak of $332.46, while maintaining distance above the $212.34 annual low.

The technology giant schedules its Q2 2026 earnings announcement for July 22. During the previous quarter, IBM delivered earnings per share of $1.91, surpassing analyst expectations of $1.81 by $0.10. Total revenue reached $15.92 billion, exceeding the projected $15.60 billion and representing 9.5% year-over-year growth.

Wall Street’s Perspective

Current analyst coverage includes sixteen Buy recommendations and nine Hold ratings. The overall consensus classification stands at “Moderate Buy” with a $306.47 average price objective.

Bank of America elevated its price forecast to $330 in recent activity. Barclays commenced coverage during June with an “overweight” designation and $350 target. JPMorgan upgraded from neutral to overweight in late June, increasing its projection from $270 to $291.

Bearish sentiment exists among some analysts. KeyCorp downgraded to “sector weight” coinciding with JPMorgan’s upgrade. HSBC transitioned from “reduce” to “hold” during April, adjusting its target upward from $218 to $231.

Sumitomo Mitsui Trust Group reduced its IBM allocation by 3.8% throughout Q1, liquidating 91,570 units to conclude the quarter holding 2,348,360 units valued at approximately $569 million. Institutional investors collectively control 58.96% of outstanding shares.

Quantum Computing Enters Mainstream Consciousness

Kuzma’s facility tour represents another indicator that quantum computing technology is penetrating broader public awareness. A $2 billion federal government investment package materialized in May, accompanied by two executive directives addressing quantum advancement. IBM separately unveiled plans for an independent quantum chip manufacturing facility supported by $1 billion Commerce Department funding — an announcement that propelled the stock to its strongest weekly performance in over twenty years.

Kuzma maintains an established pattern of technology company visits. He toured Meta’s corporate headquarters in late June and recently shared photographs featuring equipment from Lunar Outpost, an emerging company holding a $220 million NASA agreement.

Industry analysts and quantum computing executives consistently emphasize that genuine sector validation originates from revenue-generating customers — not celebrity endorsements. Current end users predominantly comprise academic institutions and government agencies, rendering consumer-oriented publicity primarily a brand awareness strategy.

IBM additionally increased its quarterly dividend distribution to $1.69 per share, distributed June 10, up from the previous $1.68. The annualized dividend yield currently stands at 2.2%.

The corporation also introduced compact z17 and LinuxONE 5 computing systems this week, alongside unveiling Project Lightwell, an open-source security framework addressing software supply-chain vulnerabilities.

StarkWare co-founder Eli Ben-Sasson argues that quantum-safety for Bitcoin is more likely to arrive through ZK STARKs—especially when used to compress the huge signature data expected from post-quantum (PQ) schemes—rather than by simply expanding blocks or accepting slower throughput. He also suggested that Adam Back, founder of Blockstream, aligns with the core idea, though Cointelegraph reported no response from Back to its outreach.

The broader debate has resurfaced this week as Ben-Sasson also drew attention for a separate, contentious proposal on X: raising Bitcoin inflation to 4% annually. However, his technical case for ZK STARK aggregation rests on a concrete concern—PQ signatures are far larger than today’s ECDSA/Schnorr signatures—and the resulting trade-offs for network capacity and decentralization.

Key takeaways

- Post-quantum signatures are much larger than Bitcoin’s current signature schemes, potentially forcing major capacity changes.

- ZK STARK aggregation could compress many large signatures from a block into a much smaller proof, reducing on-chain data pressure.

- Simply increasing block size is an alternative, but it may raise costs for nodes and revive decentralization concerns.

- Bitcoin’s governance and Script limitations are the main bottlenecks for adding native STARK verification at the base layer.

- StarkWare’s roadmap points to a different approach via account abstraction, making post-quantum upgrades operationally easier on systems like Starknet.

The core constraint: PQ signatures don’t fit like today’s

Ben-Sasson’s argument starts with the mismatch between Bitcoin’s existing cryptographic footprint and the expectations around post-quantum schemes. Adding PQ signatures “by itself,” he says, does not make the chain quantum-safe in a practical sense; it introduces an engineering problem first: the new signatures are orders of magnitude larger.

According to the article, the current set of PQ signatures approved by the US-based National Institute of Standards and Technology (NIST) are roughly 10 to 100 times larger than Bitcoin’s prevailing ECDSA and Schnorr signatures. The practical risk is throughput and verification overhead—one oft-cited concern is that a block could end up supporting far fewer transactions.

Ben-Sasson’s counterproposal is to move the bulk of that data off the chain and replace it with a compact cryptographic statement. In his view, the signatures for all transactions in a block could be aggregated into a single ZK STARK proof, which would be significantly smaller than including the original signatures. That, he argues, could preserve or even improve effective efficiency compared with a naive on-chain PQ upgrade.

“If they don’t allow for ZK STARK aggregation, then definitely it will be a very unfortunate move because it won’t really solve the problem … where the problem is ‘can everyone actually use Bitcoin?’” Ben-Sasson said.

“So for that you need massive scale. And for that, you need things like signature aggregation and just increasing the block size isn’t enough.”

Block size as the “simple engineering” fix—and why it’s controversial

One alternative Ben-Sasson acknowledges, via commentary from other experts, is increasing Bitcoin’s block size. The dispute is not about whether it works—it’s about the cost structure and the governance path.

Marin Ivezic, author of PostQuantum.com and founder of Applied Quantum, told Cointelegraph that Bitcoin’s SegWit scheme reduced the impact of larger signatures by up to 75%. But Ivezic’s modeling of NIST’s ML-DSA-44 scheme (described in the article as having 2,420 bytes per signature) suggests block capacity could drop to roughly 500 to 700 transactions under those conditions—down from 2,500 to 3,000 “today.”

That figure is what makes block-size debates feel inevitable: if PQ signatures drive transaction sizes sharply upward, the network needs somewhere for that data to go. Yet, as the article notes, critics see block growth as a blunt instrument because it pushes more storage, bandwidth, and verification work onto all nodes. Over time, that can mean higher operating costs and potentially less hardware diversity—an outcome that opponents argue could shift Bitcoin toward centralization.

The article also points to Blockstream Research’s recent experiments compressing hash-based post-quantum signature schemes for Bitcoin. It cites SHRINCS and SHRIMPS, with “everyday” signatures said to be around five times larger than current Bitcoin signatures, and up to 40 times larger in recovery scenarios such as wallet resurrection. The implication is that even with compression, larger signatures remain a throughput challenge unless block sizes increase.

“Raising capacity natively is the simple engineering answer and the hardest governance answer,” Ivezic said. “We just don’t have time for those debates.”

Why ZK aggregation could matter more than capacity alone

The attraction of ZK STARK aggregation is not simply that it is smaller. It’s that it changes the economics of what must be stored and verified by nodes.

At a high level, ZK proofs let one side prove that some statement holds without exposing all underlying details. In the Bitcoin setting described in the article, a STARK proof could certify that the necessary conditions for multiple transactions—tied to signatures—are satisfied, without requiring the chain to carry the full set of individual signature bytes.

The operational claim from Ben-Sasson is that generating a proof for a single block is a job that likely needs to be done once (with optional redundancy), and that the proving hardware could be far cheaper than commercial mining setups. The article further notes that verifying proofs could be feasible on very modest devices, pointing to Lean Ethereum’s specification benchmarks—where proving equipment is described as potentially under $100,000 and verification could run on almost any equipment, even something like a Raspberry Pi.

Ben-Sasson also argues the momentum for ZK STARKs existed among early Bitcoin developers. He claimed that figures such as Greg Maxwell and Mike Hearn were “very bullish about ZK STARKs,” citing their belief that STARKs provide post-quantum security without trusted setup. In the article, he adds that he thinks Bitcoin Core developer Luke Dashjr and Adam Back are aligning more with the idea, though Cointelegraph states it did not receive a response from Back.

One complication raised in the article is that Ethereum researcher Justin Drake has described a desire for Bitcoin to adopt Lean Ethereum’s ZK proof aggregation approach. However, political constraints might make that difficult to implement in practice—even if the technical path exists.

What would it take for Bitcoin to verify STARKs?

The question for Bitcoin is less about whether ZK STARKs are cryptographically credible and more about whether Bitcoin can verify them in a practical, acceptable way. That brings the discussion to Bitcoin Script and governance.

The article suggests a more politically pragmatic starting point may be re-enabling OP_CAT, an opcode Satoshi introduced and later removed. Ben-Sasson argues that if OP_CAT is enabled, it could unlock capabilities needed for STARK proofs and aggregation and thereby support post-quantum security.

Still, while OP_CAT drew attention in earlier months (as the article frames it, 12 to 24 months ago), it has “lost momentum” more recently. It remains a governance-dependent path, with Bitcoin’s deliberative culture cited as a key factor.

Beyond OP_CAT, the article mentions other proposals such as OP_STARK_VERIFY, an opcode-oriented idea designed to verify STARKs more efficiently on Bitcoin, and a concept called BitZip associated with Ethan Heilman. Heilman’s framing (as quoted in the article) outlines two broad routes: enhancing Bitcoin with general-purpose opcodes to support rollup-like constructions, or supporting STARKs at the consensus layer. He also referenced weaker aggregation schemes—like CISA (Cross Input Signature Aggregation)—as potential partial help.

Even if the crypto is strong, the practical gating factor is that Bitcoin Script cannot verify STARKs today. The article quotes Ivezic’s assessment that a base-layer STARK verifier is realistically a 2030s governance conversation, noting that consensus-layer changes carry far more surface area than small signature-related opcodes—even ones like OP_CAT that have already faced years of debate.

By contrast, the article highlights that other networks may find post-quantum transitions easier. It notes that Ethereum is targeting 2029 for post-quantum transition and that Solana has experimented with post-quantum signatures. For Starknet specifically, the article ties StarkWare’s three-phase quantum-secure transition to native account abstraction, which allows upgrades of underlying cryptography without forcing every user to migrate accounts manually.

“On Starknet, we have this big advantage that we have already native account abstraction and smart wallets, which means that nothing is enshrined so its very easy to upgrade the wallets and the infrastructure to be post quantum.“

The strategic implication, as Ben-Sasson presents it, is that post-quantum roadmaps on networks without flexible account layers could be “extremely hard,” while Starknet’s design choices reduce lock-in risk.

For Bitcoin readers, the next watchpoints are straightforward: whether any OP_CAT-related or STARK-verification discussions regain momentum, and whether the community gravitates toward aggregation-first proposals that preserve decentralization—rather than defaulting to block-size increases that may raise node burdens. The cryptography may be solvable, but Bitcoin’s ability to verify it at scale hinges on governance and Script capabilities.

Mexico to file criminal complaints over deaths in US custody

Top 10 US Cities Attracting the Biggest Corporate Headquarters Moves in 2026, Led by Dallas-Fort Worth

Buy STRC and make 28%? Traders say no thanks

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Weekend Open Thread: Staud – Corporette.com

Warren Buffett’s 7 Simple Money Habits That Can Make You Wealthy | Financial Wisdom Everyone Should

BREAKING : CRYPTO REGULATION IN INDIA || UPDATE

Devenir millionnaire en travaillant chez Costco ! #costco #management #finance #salaire

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: High Hopes

-

NewsBeat5 days ago

NewsBeat5 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Crypto World6 days ago

Crypto World6 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

Fashion3 days ago

Fashion3 days agoOpen Thread: What Great Books Have You Read Recently?

-

Politics6 days ago

Politics6 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Fashion8 hours ago

Fashion8 hours agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

News Videos3 days ago

News Videos3 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Tech2 days ago

Tech2 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Crypto World6 days ago

Crypto World6 days agoESMA Expands Crypto Register by 37 Firms Following MiCA Transition Period

-

Business3 days ago

Business3 days agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports2 days ago

Sports2 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Crypto World3 days ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

Crypto World4 days ago

Crypto World4 days agoSouth Africa proposes crypto tax guidance under existing rules

-

News Videos3 days ago

News Videos3 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech4 days ago

Tech4 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business7 days ago

Business7 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Sports2 days ago

We have punished the disrespect

-

Crypto World7 days ago

Crypto World7 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

-

News Videos3 days ago

News Videos3 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

-

Crypto World6 days ago

Crypto World6 days agoAlibaba bans Claude Code over alleged backdoor security concerns

You must be logged in to post a comment Login