Crypto World

What is Robinhood Chain? The broker’s L2 explained

Robinhood launched its own blockchain in July 2026, an Ethereum layer 2 where tokenized stocks trade around the clock and plug into DeFi as collateral. This guide explains what Robinhood Chain actually is, how it works under the hood, what Stock Tokens are and who can use them, how the chain differs from Base and the other corporate networks, and what it means for users, builders, and the industry’s biggest open questions.

On July 1, 2026, one of the largest retail brokers in the United States switched on its own blockchain. Robinhood Chain launched its public mainnet at a London keynote, carrying 95 tokenized stocks that trade 24 hours a day, a suite of DeFi protocols live from day one, and access wired directly into the Robinhood Wallet used across 120 countries. Within a week the chain had processed roughly 4 million transactions, gathered over $240 million in deposits, and produced a launch statistic, $570 million of day-one volume against $21.68 million of liquidity, that made the entire industry look twice.

A brokerage running a blockchain would have sounded absurd for most of crypto’s history, and it now sounds inevitable: Coinbase runs Base, Stripe backs Tempo, and the era of consumer giants renting neutral rails is visibly ending. But Robinhood Chain is a distinct species within that trend, because it was built around one specific product no other chain ships: real-world equities as native, composable on-chain assets, the thing crypto has promised since the first tokenized-stock experiments and never delivered at brokerage scale.

This guide explains the chain from the ground up: what it technically is and how the Arbitrum-based architecture works, what Stock Tokens are and what holders actually get, the DeFi ecosystem that launched with it and why composability is the entire point, who can access what and where the regulatory lines sit, how the chain compares to Base and the corporate-chain field, the fee economics including the unusual revenue-sharing deal with Arbitrum, and the honest open questions, control, liquidity, and law, that will decide what the chain becomes.

The architecture: an Ethereum layer 2, built to order

Robinhood Chain is a layer 2 blockchain: a network that executes transactions on its own fast, cheap environment while posting records to Ethereum, inheriting the base chain’s security for its history. It is built using Arbitrum’s Orbit technology, the chains-as-a-service framework from the team behind Arbitrum One, which means Robinhood did not invent a blockchain so much as commission one: Orbit supplies the rollup machinery, proofs, data posting, Ethereum settlement, and Robinhood configures the network, operates its infrastructure, and decides what it is for.

Three design choices define it. First, it is permissionless: any developer can deploy contracts using standard Ethereum tooling, without Robinhood’s approval, which is why an uninvited memecoin economy appeared on day one and why first-tier DeFi protocols could arrive at launch. That openness distinguishes it sharply from the private bank chains of the last decade and puts it in the same public-network category as Base. Second, it is EVM-compatible: everything built for Ethereum ports over directly, wallets, contracts, developer tools, so the chain starts with the industry’s entire software ecosystem instead of an empty room. Third, it is purpose-tuned for real-world assets: fast block times via Alchemy infrastructure, Chainlink as the official oracle for prices, cross-chain messaging, and proof-of-reserve on Robinhood-issued assets, and BitGo integration on the custody side, the specific plumbing tokenized equities require and general-purpose chains bolt on as afterthoughts.

The trust profile follows from the architecture, and it is the standard corporate-chain bargain. User funds are secured by Ethereum: the sequencer that orders transactions cannot forge them or steal assets, and the chain’s history settles to the base layer. Access and ordering, though, run through infrastructure Robinhood operates, the centralized-sequencer chokepoint every major rollup currently carries, which means outages, ordering policy, and censorship capacity sit with one regulated company. For everyday users the distinction rarely surfaces; for anyone evaluating the chain seriously, it is the first line of the risk section.

Stock Tokens: the product the chain was built around

The headline asset class is Stock Tokens: on-chain representations of equities, NVDA, GOOG, AAPL among the 95 at launch, issued by Robinhood, priced by Chainlink feeds, and tradable every hour of every day, not just during exchange sessions. They are the chain’s reason for existing, and understanding precisely what they are, and are not, is the guide’s most practical section.

A Stock Token delivers price exposure to the underlying equity in a token that behaves like any other crypto asset: hold it in the Robinhood Wallet or self-custody, trade it around the clock on the chain’s exchanges, transfer it, and, most consequentially, use it inside DeFi. What it does not deliver is shareholder status: token holders do not vote, and corporate rights stay with the issuance structure, with dividend economics passed through per the product’s terms, the standard trade-off of every tokenized-equity model. The tokens descend from Robinhood’s 2025 European pilots, which tokenized exposure to private names like SpaceX and OpenAI as proof of concept, and the lineage matters: the legal wrappers were tested under European rules before the chain bet on them.

Availability is the sharpest edge. Stock Tokens ship through the Robinhood Wallet in more than 120 countries, and conspicuously not to United States users, where the line between a compliant synthetic instrument and an unregistered security remains undrawn. The result is one of the strangest compliance objects in crypto: a permissionless network, built by an American broker, whose flagship assets are geofenced away from Americans, with enforcement living at the issuance and app layers while the rails underneath stay open. Whether that architecture satisfies regulators, or attracts them, is among the chain’s defining open questions.

The 24/7 dimension carries its own mechanics worth knowing. When the underlying stock market is closed, nights, weekends, holidays, the tokens keep trading, drifting on expectation with no live reference price, then reconverging when the real market opens. Weekend token prices function as forecasts of Monday’s open, gaps can be violent when news breaks during the closure, and anyone using the tokens in leveraged or collateralized positions inherits that gap risk in full.

The DeFi layer: why composability is the point

Tokenized stocks existed before Robinhood Chain. What the chain adds, and what its launch ecosystem was assembled to prove, is composability: the tokens plug into open financial protocols as first-class assets, which converts a brokerage line item into a programmable building block.

The day-one roster was deliberately first-tier. Uniswap deployed a dedicated AMM as the chain’s core public liquidity venue; Arcus, built by the team behind dYdX, runs a zero-fee exchange purpose-built for the stock tokens; 1inch, Rialto, and Lighter round out trading, with Lighter adding perpetual futures and pledging $11 million of its token to Robinhood users; Pleiades operates a proprietary market-making AMM; and Morpho’s lending markets opened the loop that matters most: stock tokens as loan collateral. That last integration is the chain’s genuinely novel product, a holder borrowing stablecoins against tokenized NVDA, automatically, no paperwork, with liquidation machinery enforcing the loan against oracle prices, and it is also the chain’s most delicate engineering: equity collateral marked by feeds from a market that closes means health factors computed against stale or reconstructed prices for two-thirds of every week, gap-risk liquidations at Monday opens, and corporate-action handling no DeFi risk framework has stress-tested at scale.

The deposits that flowed in during week one, past $240 million, concentrated in exactly these venues, drawn by a 7% yield incentive and points programs, and the composition question, how much collateral is actually stock tokens versus recycled farm assets, is the single best indicator of whether the composability thesis is converting, the launch-week forensics this publication’s feature examined in depth.

Using the chain: access, wallets, and what a first session looks like

For a user, the chain’s front door is the Robinhood Wallet, the company’s self-custody app, which added native Robinhood Chain support at launch: bridging assets in from Ethereum and other networks, swapping tokens, and reaching the chain’s applications happen from inside an interface tens of millions of people already carry. That distribution is the launch’s real innovation, one tap from an existing consumer app to an on-chain economy, no seed-phrase ceremony, no network-configuration ritual, and it is why the chain gathered users at a pace organic launches never match.

Nothing about the chain requires Robinhood’s app, though, and the permissionless design means the standard crypto path works identically: add the network to any EVM wallet, bridge funds across, and interact with the protocols directly. A typical first session looks like any L2’s, bridge a stablecoin or ETH, pay negligible fees, swap or deposit into a venue, with two chain-specific wrinkles worth knowing in advance. The first is that asset availability depends on who you are and where: the DeFi protocols and general tokens are open, while Stock Tokens and certain products check jurisdiction at the issuance and interface layers, so two users on the same chain can see different shelves. The second is incentives literacy: the launch period’s yields and points programs are bootstrap subsidies with published terms and step-down schedules, and treating them as permanent rates is the classic new-chain mistake, since incentive-driven deposits reprice the day the programs do.

Builders face an even lower bar: the chain is standard EVM, deploys with familiar tooling, and offers what no other network can, proximity to a brokerage user base and an asset class, the stock tokens, that exists nowhere else as a composable primitive. The day-one protocol roster arrived for exactly that reason, and the open question for every subsequent builder is the same one the chain itself faces: whether the mission assets acquire the liquidity that makes building against them worthwhile.

The launch by the numbers, and how to read them

The chain’s opening week produced statistics worth recording precisely, because they will be the baseline every future assessment measures against. Day-one volume of $570 million against $21.68 million of total value locked, a 26-to-1 turnover ratio without precedent at scale, driven overwhelmingly by speculative memecoin trading rather than the stock tokens the chain was built for. Roughly 4 million transactions in the first week against about $57,000 of protocol revenue, deliberately subsidized throughput. Deposits growing past $240 million within days, concentrated in Morpho and Ethena strategies farming a 7% incentive. And an 8% rally in HOOD stock on launch, the equity market pricing the option the chain represents.

Read together, the numbers say the launch proved distribution and deferred everything else: the crowd arrived instantly, the crowd was the wrong crowd by the mission’s definition, and the company visibly did not mind, because speculative bootstrap is how every successful chain, Base included, actually started. The figures to watch from here are the boring ones, stock-token volume as a share of activity, collateral composition in the lending markets, deposit retention through incentive step-downs, and they will decide, over quarters rather than weeks, whether the launch statistics were a foundation or a fireworks show.

Fees, economics, and the Arbitrum deal

The chain’s business model is subsidy now, franchise later. Transaction fees are deliberately negligible, roughly $57,000 of protocol revenue against the first week’s 4 million transactions, because the chain is priced as customer acquisition: Robinhood monetizes the surrounding stack, wallet, custody, order flow, spreads, and the eventual financialization of assets its 28 million customers already hold. The structure echoes the company’s zero-commission brokerage playbook precisely.

The launch’s most consequential economic detail belongs to someone else: 10% of Robinhood Chain’s fees flow to the Arbitrum ecosystem, with 8% going directly to the treasury controlled by ARB token holders, confirmation that sent ARB up double digits. The deal matters twice over: it prices Orbit’s chains-as-a-service model with its biggest customer to date, and it sets the template every future corporate chain will negotiate against, the sell-shovels economics underneath the land grab, whose full competitive map this publication has drawn.

One further piece of the economics deserves its own paragraph because it inverts the usual chain-token question: Robinhood Chain has no token, and the company has signaled nothing about one. The network’s fees are paid in ETH-denominated gas, its incentives are paid in dollars and partner tokens, and the value the chain generates is designed to accrue to HOOD equity through the brokerage’s ordinary lines rather than to a new crypto asset. The choice is strategically legible, a token would add regulatory surface exactly where the company has least room, and it makes the chain a useful natural experiment: the corporate-chain model’s economics, tested without the token variable that confounds every other network’s numbers. It also concentrates the ecosystem’s token exposure in unexpected places, ARB through the fee-sharing deal, and the partner protocols’ tokens through their deployments, which is why the launch’s clearest market beneficiaries were assets Robinhood does not issue.

How it compares: Robinhood Chain versus the field

Against Base, the reigning corporate chain, the comparison clarifies both. Base is a general-purpose network that grew an economy organically, memecoins first, then consumer apps, then everything, monetized through sequencer margin at enormous scale; its differentiation is Coinbase’s distribution applied to an open playground. Robinhood Chain is a product-led network: the stock tokens are the anchor tenant, the DeFi roster was recruited around them, and the bet is that one asset class nobody else ships outruns a general platform’s breadth. Base runs on the OP Stack, Robinhood on Arbitrum Orbit, a meaningful choice mostly for the fee-sharing counterparty and the proving roadmap. Against Tempo, Stripe’s payments-first chain, the contrast is anchor product again, payments versus equities, and against the neutral L1s both compete with, the corporate chains share the same offer and the same objection: distribution no neutral chain can match, control no neutral chain would accept.

Where the chain came from: the two-year assembly

The launch’s polish reflects deliberate sequencing worth knowing, because it explains both the chain’s capabilities and its ambitions. Robinhood spent 2025 acquiring the pieces: Bitstamp, one of the oldest crypto exchanges, for trading and institutional infrastructure; WonderFi for Canadian licensing; and the European tokenized-equity pilots, including exposure products on private names like SpaceX and OpenAI, as legal and product rehearsal. Early 2026 brought the quiet phase: a public testnet from February that processed millions of transactions, and the European expansion of crypto perpetuals that became one of the company’s fastest-growing lines. The July launch composed the pieces into one architecture, assets tokenized on its own network, traded through its own wallet and partnered venues, financed through integrated lending, custodied through its own stack, and the composition, more than any single component, is the product: a vertically integrated on-chain brokerage, with each layer feeding the others.

The assembly also explains the chain’s geography. The launch happened in London, the stock tokens ship internationally first, and the European perps expansion runs under MiCA-era rules, because the regulatory groundwork was laid where frameworks exist. The United States, the company’s home market, receives the chain, the wallet, and the crypto products, and waits on the equity tokens until American classification law settles, a sequencing that reads as strange until it reads as strategy: build the global product under workable rules, and let the home market’s framework catch up to a working precedent instead of a proposal.

The honest open questions

Three questions will decide what the chain becomes, and none is answerable yet. Control: a permissionless network whose sequencing, issuance, and flagship interface all route through one regulated broker is decentralized at exactly one layer, and the pressure point regulators or litigants would reach for first is obvious. Liquidity: 24/7 equity trading and stock-collateral lending are only as real as their depth, and week-one depth in the mission assets was thin against the speculative noise; the products exist as listings and must become markets. And law: the geofence paradox, the CLARITY-era classification of the tokens, and the first serious corporate action or exploit on tokenized equities are all uncharted, and each is capable of reshaping the chain’s product overnight.

What is not in question is significance. A top American broker building a public blockchain around real-world assets, and populating it with DeFi’s first tier on day one, is the clearest single marker yet of traditional finance and crypto converging on shared rails, and whichever way the open questions resolve, the experiment’s data, on tokenized-equity demand, on corporate-chain economics, on regulated assets in permissionless systems, will shape what every institution builds next.

A short reader’s guide to following the chain closes the picture, because the story is young and the sources are all public. The chain’s explorer and the standard TVL dashboards carry the activity and deposit series; the incentive programs publish their terms and step-down dates; the stock-token venues report the volumes that measure the mission; and Robinhood’s quarterly disclosures will, over time, reveal what the company chooses to say about economics it is currently subsidizing in silence. The corporate-chain era is being decided by exactly this kind of unglamorous series, retention curves and collateral mixes, not keynotes, and Robinhood Chain, whatever it becomes, has committed to being graded in public. For a technology that spent a decade arguing about whether traditional finance would ever really arrive on-chain, the most informative thing about this chain may simply be its existence: the argument is over, the arrival is operational, and the remaining questions, control, liquidity, and law, are the practical kind that get answered by data, not debate.

And a sizing footnote for perspective: a week after launch, the chain’s deposits already exceeded what most of the previous cycle’s venture-funded L2s gathered in their lifetimes, and its flagship product had transacted less than its accidental memecoin economy, both facts true at once, which is the corporate-chain era in a single sentence.

The chain is a week old; this guide will age accordingly, and its framework, architecture, assets, access, economics, questions, is built to be refilled with each quarter’s numbers.

Disclaimer: This article is for educational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Product availability varies by jurisdiction, and details are current as of July 9, 2026, and changing quickly. Always do your own research.

Frequently asked questions

What is Robinhood Chain in simple terms?

Robinhood Chain is a public blockchain launched by the brokerage Robinhood in July 2026. It is an Ethereum layer 2 built with Arbitrum’s technology, designed for tokenized real-world assets: its flagship product is Stock Tokens, on-chain versions of equities like NVDA and AAPL that trade 24/7 and plug into DeFi applications. Anyone can build on it, and users access it primarily through the Robinhood Wallet.

Is Robinhood Chain its own blockchain or part of Ethereum?

Both, in the way all layer 2 networks are: it executes transactions on its own fast, cheap network, and it posts records to Ethereum, inheriting the base chain’s security for its history. It is built on Arbitrum Orbit, the same technology family as Arbitrum One, and is fully compatible with Ethereum wallets, tools, and smart contracts.

What are Stock Tokens and do they make me a shareholder?

Stock Tokens are Robinhood-issued tokens tracking specific equities, tradable around the clock and usable in DeFi as collateral. They deliver price exposure and pass through dividend economics per their terms, but holders are not shareholders of record: no voting rights, and corporate rights remain with the issuance structure. They are exposure instruments, not shares.

Can US users trade Stock Tokens on Robinhood Chain?

No. Stock Tokens are available through the Robinhood Wallet in more than 120 countries, with availability varying by jurisdiction, and the United States is excluded pending regulatory clarity on how such tokens are classified. US users can access the chain itself, which is permissionless, but not its flagship equity products.

What DeFi protocols run on Robinhood Chain?

The launch ecosystem included Uniswap with a dedicated AMM as core public liquidity, Arcus, a zero-fee stock-token exchange from the dYdX team, 1inch, Rialto, and Lighter for trading and perpetuals, Pleiades as a proprietary market-making venue, and Morpho for lending, where stock tokens can serve as loan collateral. Chainlink provides the oracle and cross-chain infrastructure throughout.

What happens to Stock Tokens when the stock market is closed?

They keep trading. With no live reference price overnight and on weekends, the tokens float on traders’ expectations of the next open and reconverge when the real market resumes, sometimes with sharp gaps if news broke during the closure. Anyone borrowing against stock-token collateral carries that gap risk, since positions can be liquidated against prices that jump at the open.

How is Robinhood Chain different from Coinbase’s Base?

Base is a general-purpose corporate chain that grew a broad economy organically and runs on the OP Stack. Robinhood Chain is product-led: built on Arbitrum Orbit specifically around tokenized real-world assets, with the stock tokens as anchor tenant and a DeFi roster recruited to serve them. Base sells an open playground with Coinbase’s distribution; Robinhood sells an asset class nobody else ships.

Who controls Robinhood Chain?

The network is permissionless to build on and its assets are secured by Ethereum, but Robinhood operates the core infrastructure, including the sequencer that orders transactions, issues the flagship assets, and controls the primary wallet interface. Funds cannot be stolen by the operator, but access, uptime, and ordering depend on it, the standard trade-off of the corporate-chain model.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Nancy Pelosi and Cathie Wood rank among the market’s most-watched stock pickers. They time their bets in opposite ways, and a decade of data shows one clearly ahead.

This month made the contrast concrete. ARK bought Circle stock one day before the company won a landmark bank charter.

Pelosi vs Cathie Wood by the numbers

Quiver Quantitative runs a hypothetical “Nancy Pelosi” strategy that rebuilds a portfolio from her family’s disclosed filings. As of mid-July 2026, it had compounded near 21% a year since May 2014.

That figure is a backtest, not a live account, and it recalculates daily. At the same date, the model showed a win rate close to 73% across 731 trades. Its maximum drawdown was near 37%.

ARK’s flagship fund, the ARK Innovation ETF (ARKK), returned about 13.4% annualized since its October 2014 launch. Its total gain since then tops 300%.

On Quiver’s math, the Pelosi backtest more than doubles that figure. It also outpaces the S&P 500 over the same span.

How Paul Pelosi’s Trades Keep Winning

Nancy Pelosi does not place the trades herself. Her husband, Paul Pelosi, a longtime investor, runs the account.

His method is consistent. It centers on call options in large technology companies.

The results have been hard to ignore. In 2024, Pelosi’s portfolio rose about 70.9%, by Unusual Whales’ estimate, against a 24.9% gain for the S&P 500.

The report singled her out as a standout options trader. Even so, only about half of Congress’s active traders beat the market that year.

The edge is not new, either. A 2011 study found a portfolio copying House members’ buys beat the market by about 6% annually. That analysis covered 1985 to 2001.

The evidence is not one-sided, though. A 2022 paper found no proof that members beat the market once the STOCK Act forced disclosure.

There is a catch for anyone hoping to copy it. The STOCK Act lets lawmakers disclose trades as late as 45 days after the fact.

By the time filings appear, the entry price is often gone. Other well-timed congressional stock buys have kept the same debate alive.

ARK’s Transparent Bets and the Circle Call

Cathie Wood built ARK in 2014 and made her name with an early, outsized bet on Tesla. The firm publishes every trade the day it happens and stakes its name on public conviction.

Circle (CRCL) is the latest test. The stock is barely a year old. It closed 168% above its $31 IPO price on its June 2025 debut, then slid.

On July 9, ARK bought about 217,900 Circle shares, worth close to $13.7 million, per its daily disclosures. That day it also sold about $9.8 million of Robinhood stock. One day later, Circle secured final OCC approval to form a national trust bank.

The stock climbed roughly 15% in pre-market trading on the news. Circle CEO Jeremy Allaire framed the charter as a turning point.

“OCC approval to establish Circle National Trust marks a defining step in bringing blockchain technology and digital assets into the core of the U.S. financial system,” Allaire said in the announcement.

Transparency cuts both ways, though. ARKK rode the 2020 growth boom, then lost about 67% in 2022 as rates rose. Circle’s post-IPO swings show how quickly the mood can flip.

The Verdict

The two are not a clean match. One is a concentrated, options-heavy strategy rebuilt from delayed filings. The other is a diversified fund priced in real time.

Both lean on the same technology and crypto themes. That shared tilt powered much of the edge during a long bull market.

On the raw numbers, the Pelosi strategy still wins. Its options leverage, though, is hard for a small investor to copy.

The real divide is access. ARK’s moves are public within hours, while Pelosi’s surface weeks later.

That gap may soon matter less. Pelosi will retire when her term ends in January 2027, which would end one of the market’s most-watched disclosure trails.

Her trades also face a political clock. Senator Josh Hawley’s bill, first branded the PELOSI Act, cleared a Senate committee in 2025. There it was renamed the Honest Act and widened to cover presidents. It would bar lawmakers and their spouses from holding individual stocks.

The pressure is bipartisan. Treasury Secretary Scott Bessent has urged Congress to curb congressional stock trading.

For now, the scoreboard favors Pelosi on returns and Wood on transparency. The next year may decide whether the comparison even survives.

The post Nancy Pelosi vs Cathie Wood: Whose Trades Timed It Better? appeared first on BeInCrypto.

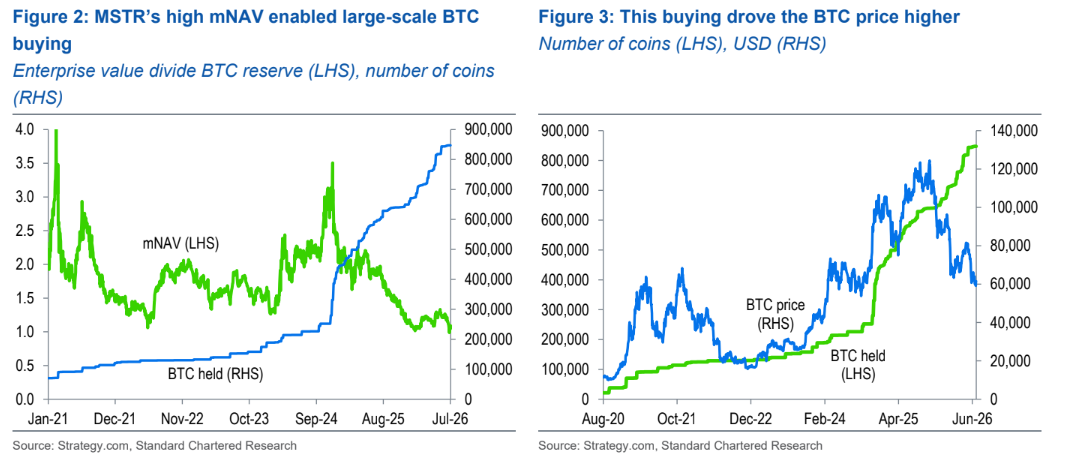

Michael Saylor, the Strategy founder and long-time Bitcoin advocate, posted a new chart on Sunday meant to reinforce how investors should interpret his firm’s latest moves. The message—“Orange dots tell only part of the story”—drew attention because it follows a shift at Strategy toward using Bitcoin to support dividends and maintain cash reserves, an approach that differs from its earlier messaging.

The debate matters for markets because Strategy’s Bitcoin treasury has often served as a proxy for broader institutional demand. But in a note to clients, Standard Chartered’s Geoff Kendrick said Strategy’s evolving communications are “muddying the waters” for Bitcoin in the near term—particularly regarding whether or not the company is likely to sell large amounts of BTC.

Key takeaways

- Strategy’s recent filings and disclosures show a move away from strict “never sell” messaging, including BTC sales to fund dividends and replenish cash.

- Standard Chartered’s Geoff Kendrick argues the company’s market signaling lacks clarity and can weigh on Bitcoin sentiment in the short term.

- Kendrick believes clearer messaging tied to backing STRC with Bitcoin could reduce pressure for wholesale BTC selling.

- Strategy’s STRC preferred shares and common stock have underperformed sharply over the past year, adding pressure ahead of its July 30 earnings report.

Saylor’s latest post and the question of what investors should infer

Saylor’s Sunday post shared a chart via Saylortracker.com, continuing a pattern in which similar messages have preceded announcements of Strategy’s Bitcoin purchases. In this case, however, the context is different: Strategy has recently signaled that Bitcoin may be sold when needed for shareholder dividends and corporate liquidity.

According to a July 6 filing with the U.S. Securities and Exchange Commission, Strategy sold $216 million worth of Bitcoin earlier this month. The filing also states that the company’s total holdings declined to 843,775 tokens.

That development comes after Strategy introduced a capital framework earlier in the month that contemplates Bitcoin sales as part of funding dividends. The same initiative included an increased annual dividend rate on Strategy’s STRC preferred stock to 12% and reported U.S. dollar reserves of $2.55 billion.

Standard Chartered: the “never sell” story is no longer straightforward

In Standard Chartered’s view, the central issue is not only what Strategy does, but how investors interpret what it does. Kendrick argued that Strategy’s older “never sell” framing limited how the market could understand—and therefore price—the economic role of its Bitcoin treasury.

“The problem with the ‘never sell’ approach is that it limits what MSTR’s BTC holdings can do—or, perhaps more importantly, what they are perceived to be doing,” Kendrick wrote in a Friday client note. He added that Strategy has already begun changing how it communicates this strategy in recent months, pointing to two BTC sales and the disclosure of a BTC monetization program.

Kendrick’s concern is that ambiguous signals may cause near-term uncertainty about whether BTC sales are an infrequent backstop or an ongoing feature of the business model. That ambiguity can, in turn, affect how investors gauge Bitcoin’s near-term demand picture, especially when Strategy is viewed as one of the most prominent corporate Bitcoin holders.

Why the messaging shift could still matter for Bitcoin prices

Despite his critique, Kendrick also suggested there could be a constructive path forward if Strategy communicates more clearly how STRC’s structure connects to Bitcoin economics. In his note, he said the market needs reassurance that wholesale selling is unlikely.

He argued that “effective communication” of Strategy’s new approach—specifically using Bitcoin to back STRC—could help remove the market’s incentive to assume large-scale sales are the only way the dividend mechanism works. Kendrick said that if the signaling is effective, it should support Bitcoin prices, and it may even reduce the need for Strategy to sell BTC by helping maintain STRC’s value through price support.

Standard Chartered also reaffirmed that it maintains a $100,000 year-end forecast for Bitcoin, though the bank framed the immediate concern as about interpretation and clarity rather than a direct change to its outlook.

Strategy shares face pressure ahead of earnings

Investors who have followed Strategy’s Bitcoin narrative have not been met with a smooth ride. The STRC preferred shares were initially structured with a $100 par value, but that par value effectively fell out of focus last month, reaching the lowest level since the preferred stock was introduced a year ago.

Meanwhile, Strategy’s common shares (trading under the MSTR ticker) have declined dramatically over the past year. The stock closed at $94.64 per share on Friday, according to the article’s figures, down from a 52-week high of $457.22—representing more than a 70% loss since July 2025.

With expectations also a concern, Strategy is scheduled to report second-quarter earnings on July 30. Consensus for earnings per share is $4.28, based on Yahoo Finance data. The company has missed analyst forecasts in six of the last eight quarters, Fintel.io data shows, including a 33.76% negative surprise in the first quarter of 2026.

For traders and long-term investors alike, the combination of earnings risk and evolving treasury policy is likely to keep attention on both Strategy’s disclosures and the way Saylor frames them publicly—especially after Sunday’s chart post reminded markets that interpretation remains contested.

Going forward, readers should watch whether Strategy’s next communications become more explicit about how its Bitcoin-backed dividend strategy reduces the likelihood of large sales, and whether the July 30 earnings report offers additional signals on cash flows and execution—areas that could sharpen the market’s understanding of the “orange dots” narrative.

South Korea’s crypto trading volume hit a two-year low, dropping below 10 trillion won ($6.7 billion) for the first time since September 2023.

The slump coincides with a dramatic collapse across the country’s stock markets.

Is South Korea Losing Its Crypto Market?

Trading volume measures the total value of assets bought and sold across exchanges over a set period. Weekly volume across South Korea’s five main fiat exchanges hit a two-year low, signaling a sharp cooling in overall market activity.

The five platforms include Upbit, Bithumb, Coinone, Korbit, and Gopax. In the week of July 3 to July 10, combined volume reached roughly 9.97 trillion won ($6.65 billion). Furthermore, that marks a 25.75% drop from the prior week’s 13.4 trillion won total ($8.9 billion).

The decline deepens over time. The current volume is about 43.5% below early June levels, according to WuBlockchain.

It marks the fifth consecutive weekly drop, reflecting a broad retreat in retail speculation nationwide.

Follow us on X to get the latest news as it happens.

Structural challenges add to the pressure. During the first quarter of 2026, combined volume had already fallen notably, with Bithumb dropping over 30%.

Furthermore, an operational error at Bithumb earlier this year damaged trust among cautious retail investors.

Tighter regulation compounded the caution. New limits on exchange ownership stakes reinforced a defensive mood. Consequently, many retail traders pulled back from the major platforms, deepening the multi-week slide in overall trading activity.

Why Are Crypto and the KOSDAQ Falling Together

The synchronized decline is no coincidence, given how South Korean investors move between tech stocks and crypto. Many traders speculate across both markets, so a decline in risk appetite in one quickly spreads to the other.

The KOSDAQ index has crashed 31% over the past 9 weeks, erasing nearly a full year of gains. That correction rivals the 2020 crash, when it fell 32% in five weeks.

Meanwhile, the KOSPI dropped 20% over three weeks, entering technical bear-market territory.

The AI trade sits at the center of the turmoil. Optimism around artificial intelligence is fading, especially after doubts over chip and semiconductor spending. Samsung and SK Hynix, along with leveraged ETFs, account for over 70% of traded market value, amplifying volatility.

Regulators are now watching closely. South Korea’s finance minister announced tighter oversight of leveraged single-stock ETFs, acknowledging the sector’s risk concentration.

As a result, that intervention adds pressure and pushes capital toward more defensive positions.

Analysts see the contraction as a reallocation, not an exit. Some activity may be migrating toward smaller platforms, DEXs, or traditional assets.

However, lower liquidity on major exchanges means wider spreads, higher volatility, and pressure on platform fee revenue.

The post South Korea Crypto Volume Hits a Two-Year Low Amid the KOSDAQ Crash appeared first on BeInCrypto.

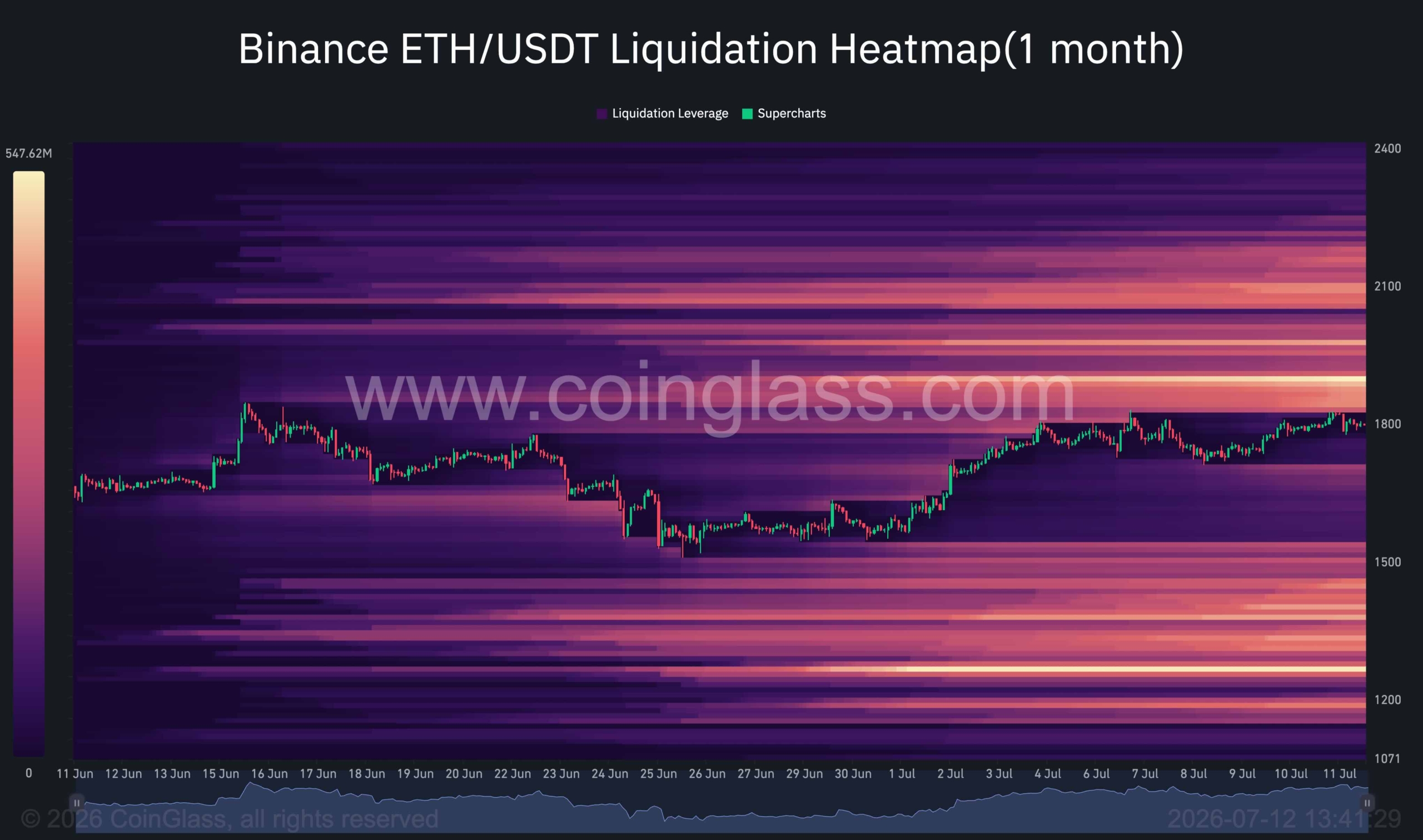

Ethereum has continued its recovery from the June lows and is now approaching a major technical inflection point. While the recent rally has improved short-term sentiment, the asset is still trading beneath a confluence of long-term resistance levels.

Interestingly, the liquidation landscape aligns closely with these technical barriers, suggesting that ETH could first target overhead liquidity before the market decides whether a larger trend reversal is underway or another corrective leg lower remains ahead.

Ethereum Price Analysis: The Daily Chart

On the daily timeframe, ETH remains within a broader descending structure in place since the beginning of the year. It has recovered strongly from the major demand zone around $1.45K-$1.55K and is currently testing the key resistance region around $1.80K-$1.85K.

This area is particularly significant because it coincides with the descending trendline that has capped price action since May. The level also represents a major horizontal resistance that previously acted as support before the June breakdown.

Despite the recent strength, ETH remains below the 100-day and 200-day moving averages, both of which continue to trend lower. The 100-day MA is positioned around the $2K-$2.1K resistance zone, while the 200-day MA remains considerably higher near $2.2K, reinforcing the broader bearish market structure.

As long as ETH remains below the descending trendline and the $1.80K-$1.85K resistance zone, the current move can still be viewed as a recovery rally within a larger downtrend. A decisive breakout above this area would shift focus toward the next major resistance at $2K-$2.1K.

ETH/USDT 4-Hour Chart

The 4-hour chart highlights a clear ascending structure that has developed since the late-June low. Price has respected the rising channel boundaries while forming higher highs and higher lows, reflecting improving short-term momentum.

The market has already reclaimed the $1.62K-$1.64K demand zone and subsequently established another support area around $1.72K-$1.74K. These zones have repeatedly attracted buyers during pullbacks and continue to define the short-term bullish structure.

However, the rally is now approaching the upper boundary of the channel and the major resistance band around $1.83K-$1.85K. This creates a natural area where profit-taking and seller activity could emerge.

From a structural perspective, ETH remains constructive above the $1.72K-$1.74K support region. Losing this level would be the first sign that bullish momentum is fading and could expose the lower channel boundary and the broader support zone around $1.55K.

Sentiment Analysis

The Binance ETH/USDT liquidation heatmap provides an important clue regarding the next likely move.

The most significant concentration of short-side liquidity sits above the current market price, particularly within the $1.95K-$2.1K region. This cluster aligns remarkably well with the daily chart resistance zone, the 100-day moving average, and the broader supply area visible on the higher timeframe.

Meanwhile, substantial liquidity pools remain below the market around the $1.45K-$1.55K region, which corresponds closely with the major daily demand zone that has supported ETH throughout the recent recovery.

The alignment between the liquidation map and the technical structure suggests that the market may first be drawn toward the overhead liquidity cluster. A move into the $2K-$2.1K area would effectively sweep a large concentration of short liquidations while simultaneously testing one of the most important resistance zones on the chart.

The reaction at that region will likely determine the next major directional move. If buyers manage to reclaim the $2K-$2.1K resistance area and establish acceptance above it, the recovery could evolve into a broader bullish trend reversal. However, if the liquidity sweep is followed by strong selling pressure and rejection from resistance, ETH could enter another notable decline, potentially targeting the large liquidity pools resting beneath the market around the $1.45K-$1.55K support zone.

The post Ethereum Price Analysis: ETH Reaches Its Biggest Obstacle on the Road to $2K appeared first on CryptoPotato.

Strategy founder and chairman Michael Saylor again took to social media on Sunday to offer his latest signal to investors as one analyst sees Saylor’s messaging as needing more clarity to help Bitcoin regain its momentum.

“Orange dots tell only part of the story,” was Saylor’s message on Sunday in a post that accompanied a chart from Saylortracker.com, similar to previous social media messages that have preceded news of Strategy’s Bitcoin (BTC) purchases, typically announced the day after his posts.

In recent weeks, the largest digital asset treasury company and a major BTC holder, has moved away from its long-time “never sell Bitcoin” approach to a willingness to sell the biggest crypto as needed to fund dividends for holders of its STRC preferred stock and to replenish its cash reserves. Earlier this month, Strategy sold $216 million worth of Bitcoin, reducing its total holdings to 843,775 tokens, according to a July 6 filing with the US Securities and Exchange Commission.

“Orange dots tell only part of the story.” Source: Michael Saylor

Days earlier, Strategy unveiled a capital framework allowing Bitcoin sales to fund dividends, increased the annual dividend rate on its STRC preferred stock to 12%, and disclosed that its US dollar reserve had grown to $2.55 billion.

Standard Charter’s global head of digital assets research, Geoff Kendrick, believes recent Strategy’s actions — and Saylor’s manner of communicating them — “are muddying the waters for BTC near-term.”

“We think effective communication of MSTR’s new strategy (using BTC to back STRC) is key to reassuring markets that wholesale selling is unlikely; this should in turn support BTC prices,” Kendrick wrote in a note to clients on Friday. “Indeed, if this signalling proves effective, it should remove the need for MSTR to actually sell any BTC by supporting STRC’s price,” he said.

Related: Crypto Biz: Did Michael Saylor buy the Bitcoin bottom for once?

StanChart sees inconsistencies in “never sell” approach

Kendrick said that Strategy’s long-held “never sell” approach limited what the company could with its industry-biggest digital asset treasury.

“The problem with the ‘never sell’ approach is that it limits what MSTR’s BTC holdings can do — or, perhaps more importantly, what they are perceived to be doing,” the StanChart analyst said. “MSTR has started to shift its communication strategy on this in recent months. It has sold BTC twice and recently announced a BTC monetization program.”

Source: Standard Chartered Bank

Still, he sees Strategy’s “market signaling” will improve soon. He expects that to bring clarity to the outlook for Bitcoin, on which StanChart maintains its $100,000 year-end forecast.

Shares struggle from year low ahead of earnings report

Investors who bought into the Strategy narrative have not had an easy time in the past 12 months. The STRC preferred shares were formulated to hold a price of $100 apiece. Shareholders saw that par value fall to the wayside last month, to the lowest value since the preferred stock was introduced a year ago.

The common shares, trading under the MSTR ticker, have lost more than 70% of their value since July 2025, closing at $94.64 per share on Friday, down from a 52-week high of $457.22.

The company is slated to report second-quarter earnings on July 30, with analysts consensus of $4.28 per share, according to Yahoo Finance data. Earnings have fallen short of analyst forecasts in six of the last eight quarters, according to Fintel.io data, including a 33.76% negative surprise in the first quarter of 2026.

Magazine: Will the crypto lobby’s $189M campaign get CLARITY over the line?

HDFC Bank ended the March financial year with 3,343 fewer employees, a major contraction for India’s biggest private lender.

Total headcount stood at 211,178 as of March 31, down from 214,521 a year earlier. The lender said it is steadily moving routine processing onto digital and automated systems.

AI Automation Hits Back-Office Jobs Hardest

The greatest impact fell on operational staff. Non-supervisory employees, classified as workmen or clerical, and subordinate staff fell by more than 8,000 to 162,797. New hiring also slowed, dropping by 3,811 across the period.

Higher tiers moved the other way. Middle-level headcount rose by 1,252, junior-level by 3,543, and senior management added 15 roles.

The bank tied the shift to strategy. The report said it is steadily shifting routine tasks, such as cash deposits, to Cash Recycler Machines and other automated channels.

That effort runs on Neev, the bank’s in-house AI platform for model access, governance, and workflow integration. Chief Executive Officer Sashidhar Jagdishan said the bank is “consciously redeploying talent from backend functions” toward customer-facing roles as technology takes over routine work.

“As we accelerate the transformation toward becoming a technology-led, customer-centric bank, employees need to keep pace,” he said.

Follow us on X to get the latest news as it happens

Banks Worldwide Lean on AI to Trim Staff

HDFC Bank is not alone. Standard Chartered plans to trim 15% of corporate function roles by 2030 as it scales automation. The trend is now evident in the data. AI drove 38,579 US job cuts in May, roughly 40% of the monthly total, according to Challenger, Gray & Christmas.

However, not every leader shares the gloom. Jeff Bezos argues AI will lift productivity and living standards rather than erase work.

For HDFC Bank, the math already favors fewer hands. Profit after tax rose 10.9% to ₹74,671.3 crore, about $7.83 billion, in FY26, even as the workforce shrank.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post India’s Largest Private Bank Lost Over 3,000 Employees to AI appeared first on BeInCrypto.

Japanese lender CRYL has launched Bitcoin-backed loans ranging from 1 million yen to 1 billion yen, or about $6,200 to $6.2 million.

Summary

- CRYL offers Bitcoin-backed loans from $6,200 to $6.2 million for individuals and businesses across Japan.

- Borrowers pay annual rates between 3.5% and 7%, with collateral ratios ranging from 40% to 60%.

- Japan’s Bitcoin credit market is expanding as lenders and securities firms test new collateral products nationwide.

The service allows individuals, sole traders and companies to obtain yen without selling their Bitcoin. CRYL began offering the product on July 9, according to its official launch announcement.

CRYL offers loans at annual rates from 3.5%

CRYL set annual borrowing rates between 3.5% and 7%. The company applies collateral ratios of 40% to 60%, depending on the borrower and loan terms.

The loans run for one year and may be extended. Most contracts require borrowers to repay the principal and interest in one lump sum at maturity. CRYL also allows additional borrowing under some credit-line agreements if the loan-to-value ratio remains below 60%.

Borrowers can use the funds for tax payments, living costs, business expenses and property purchases. The company offers separate plans for individuals, sole traders, property buyers and corporate customers.

However, CRYL requires applicants to pass its screening process. The lender also charges a 20% annual rate on overdue balances and warns customers that Bitcoin price changes may affect their collateral position.

Bitcoin serves as the only accepted collateral

CRYL accepts only Bitcoin as collateral. Borrowers transfer BTC to the lender while receiving the approved amount in Japanese yen.

The structure gives Bitcoin holders a way to access cash while keeping exposure to the asset. Selling Bitcoin can also create a taxable event in Japan when the holder records a gain.

CRYL described the product as an alternative to either holding or selling crypto. Still, taking a loan creates interest costs and repayment duties, while a decline in Bitcoin’s price can reduce the value of the pledged collateral.

The firm operates as a registered money lender in Tokyo and belongs to the Japan Financial Services Association. It is also part of the J-CAM group, which runs the BitLending crypto lending service.

Fintertech already offers crypto-backed lending

CRYL enters a market where Fintertech has offered digital asset-backed loans since 2020. Fintertech is a financial technology company linked to Daiwa Securities Group and Credit Saison.

Fintertech initially launched its service for companies and sole traders using Bitcoin collateral. The original product offered annual rates from 4% to 8%, a 50% collateral ratio and a one-year term.

The lender later expanded the service to individuals and added Ether as eligible collateral. Its current loans range from 5 million yen to 500 million yen, making CRYL’s advertised 1 billion yen ceiling twice as high.

In October 2025, Daiwa Securities began referring customers from branches across Japan to Fintertech. The expanded service offers loans for personal use, business funding and property purchases at annual rates of 4% to 8%.

Japan explores wider uses for Bitcoin credit

CRYL’s launch comes as more firms test ways to use Bitcoin in lending and capital markets. As previously reported by crypto.news, Metaplanet is studying Bitcoin-backed digital credit with JPYC and tokenization infrastructure provider Progmat.

That project will examine whether BTC can serve as collateral or credit support for digital corporate bonds. However, the companies have not launched a product or confirmed any issuance terms.

Crypto-backed borrowing is also expanding outside Japan. Strike recently launched Bitcoin-backed loans without price-triggered margin calls, although borrowers may pay rates of up to 14.2%.

Meanwhile, institutional platforms are offering larger financing products. Crypto.news previously reported that BitGo launched a unified crypto financing platform for institutions seeking to borrow against assets held in custody.

CRYL’s product gives Japanese Bitcoin holders another regulated route to obtain yen without selling their holdings. Its use will depend on borrower demand, screening decisions and how the lender manages collateral during sharp market moves.

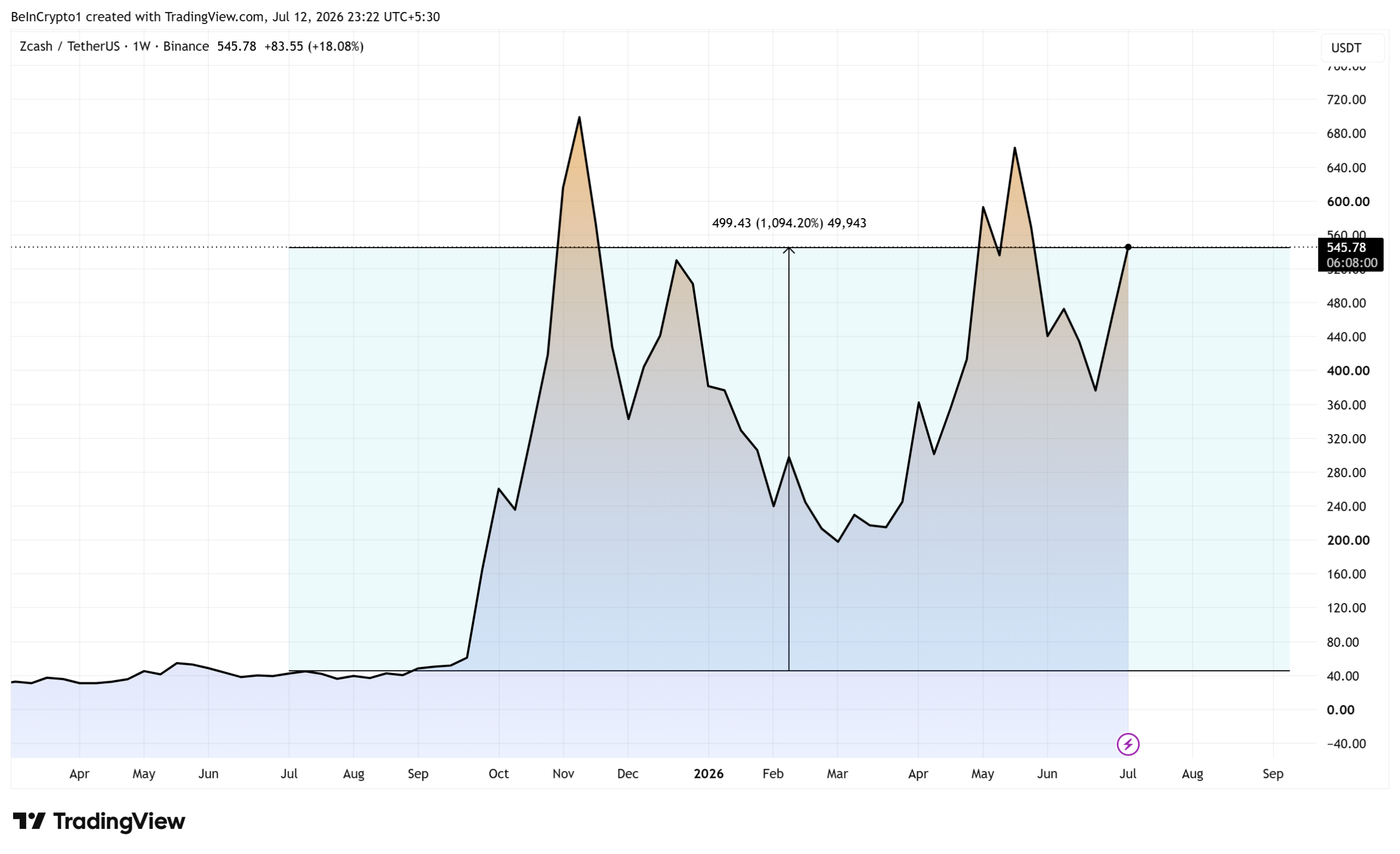

The Zcash (ZEC) price has climbed roughly 1,190% over the past year, earning it a spot on Forbes’ new top 10 list of the best cryptocurrencies to buy.

The privacy coin trades near $545 after rising about 17% in a week. It is one of just 10 names Forbes picked, beside Bitcoin (BTC), Ethereum (ETH), and Hyperliquid (HYPE).

Why Zcash Is Climbing

To make Forbes’ shortlist, a token had to top $5 billion and pass a utility or store-of-value screen. Zcash cleared both, and its rally rests on more than sentiment.

On-chain supply is tightening. By early June, a record shielded supply held about 5.1 million ZEC. That is close to a third of all coins, and those holdings sit outside the liquid market.

A November 2024 halving added to the squeeze. It cut the block reward in half, from 3.125 to 1.5625 ZEC, slowing new issuance.

Regulatory pressure eased at the same time. The Zcash Foundation said in January that the SEC closed a two-year investigation into crypto asset offerings without enforcement. The probe had followed a 2023 subpoena.

The Case Against the Run

The risks are just as concrete. In late May, a researcher found a critical flaw in Zcash’s Orchard shielded pool. The bug had gone undetected for about four years, and in theory it could have minted counterfeit ZEC.

Electric Coin Company and the Zcash Foundation patched it through an emergency hard fork within days. Network accounting showed no fake coins were created. Still, ZEC fell about 38% on the news, and on-chain data flagged lingering stress. Gemini’s Winklevoss twins later backed formal verification, a math-based check meant to make such bugs impossible.

Europe poses the clearest threat. Under MiCA, the bloc’s crypto rulebook, platforms cannot list assets with built-in anonymity features. That provision takes effect in 2027, and some exchanges have already dropped privacy coins.

Will It Hold?

The honest answer is a qualified yes, with caveats. This run has firmer footing than past Zcash pumps. A shrinking liquid supply, slower issuance, and named institutional backers are structural, not hype. Momentum also points up, with gains across the weekly and monthly windows.

Durability is a separate question. Zcash still trades far below its 2016 record high. Adoption stays thin, and Forbes flagged volatility as a core weakness. The Orchard scare showed how fast confidence can crack.

“Given crypto’s higher volatility, we chose a more conservative cutoff: screening only for projects with a market cap of at least $5 billion,” Forbes stated.

The takeaway is that Zcash’s rally rests on firmer ground than its history suggests, yet it is far from safe. Its longer-term price outlook now turns on a single question. Can privacy demand outlast the regulation it invites?

The post Zcash Price Climbs 1,190%, Joins Forbes’ 2026 Top 10 List: Will It Hold? appeared first on BeInCrypto.

But the 2026 midterm election is coming up quite soon — Nov. 3, so less than four months from now — and lawmakers will have to face their own base and flanks after they break for the summer recess and go into the final campaign swing.

That means that U.S. President Donald Trump and the $1.4 billion he made off crypto will be a key factor in the floor vote. More specifically, if there isn’t an ethics provision, it’s unlikely that sufficient Democrats will vote for the bill in the Senate. If the text that drops next week doesn’t even include a placeholder to address the ethics portion, that may even be counterproductive to getting full bipartisan support for the bill, an individual said.

That means that Trump will still need to sign off on an ethics agreement. Several of the sources CoinDesk spoke to last week said the White House had not been as engaged recently as it had earlier in the summer, but another individual told CoinDesk in early July that it may just be a matter of waiting to see whether all the other outstanding issues are resolved first.

One bright side for the bill’s proponents: Assuming the President did not veto the housing bill sitting on his desk sometime between this newsletter’s filing and 12:00 a.m. on Saturday, a provision banning the Federal Reserve from issuing a central bank digital currency for at least four years will have taken effect. There was concern from industry players that House lawmakers might push to include a CBDC ban in Clarity if the Senate advanced the bill, which would further strain the negotiation process and timeline. But that issue should be resolved for now through at least until 2030, with the inclusion in the housing bill.

The x402 standard revives a dormant corner of the web’s original design, the 402 Payment Required status code, to let AI agents pay for services autonomously, per call, with no accounts and no cards. Ripple has moved to put the XRP Ledger and RLUSD inside that standard, betting that when machines become the economy’s newest customers, they will settle on its rails.

Summary

- Ripple is integrating the XRP Ledger and RLUSD with the x402 payment standard to support autonomous AI agents making on chain payments.

- The analysis finds RLUSD is likely to handle most settlement flows while XRP could benefit through transaction fees, liquidity routing and wallet reserve requirements.

- The long term opportunity depends on whether machine to machine payments gain broad adoption and whether Ripple can capture enterprise settlement activity ahead of competing networks.

This is the honest examination of the machine-to-machine thesis: what x402 actually is, what Ripple is actually doing, which asset captures the flow, and how large the agent economy really is today.

Buried in the original specification of the web, written before online payments existed, sits HTTP status code 402: Payment Required, reserved for future use. It waited three decades for its future to arrive, and the future turned out not to be human. The x402 standard, incubated at Coinbase and now backed by a widening coalition, activates that dormant code as a native payment layer for the internet: a server answers a request with 402 and a price, the client pays in stablecoins on-chain, retries the request with proof of payment, and receives the service, no account creation, no card on file, no subscription, no human. It is a payment protocol shaped precisely for software that buys things, which is to say, for AI agents, and the demand curve behind it is the least speculative trend in technology: autonomous agents already generate a majority-adjacent share of web traffic and a rising share of transaction volume across venues.

Ripple’s entry into this push is the development worth examining, because Ripple does not adopt standards; it positions for settlement flows. The company has moved to make the XRP Ledger an x402-capable network with RLUSD as a settlement asset, slotting the machine-to-machine economy into the institutional-payments architecture it has spent a decade and several billion dollars assembling. The community’s reading was immediate and predictable, agents paying on XRPL means demand for XRP, and the honest analysis is, as usual with this company, more layered: the same empire-and-token gap that runs through every Ripple story runs through this one, with a truly new variable, because machine customers may reshape which asset the flow actually touches.

This piece takes the bet apart properly: how x402 works and why agents need it, what Ripple has concretely done versus announced, the XRP-versus-RLUSD question applied to machine flows, the competitive field, since every settlement network wants the same customers, the honest sizing of an agent economy that is enormous in forecasts and embryonic on-chain, and the tells that would show the bet paying.

Why machines need their own payment rail

The case for x402 begins with a mismatch: the internet’s payment stack was built for humans, and every piece of it assumes one. Accounts assume an identity to onboard; cards assume a holder to authenticate; subscriptions assume a relationship that outlives the transaction; fraud systems assume human behavioral patterns; and checkout flows assume someone is looking at them. An autonomous agent, a piece of software tasked with, say, researching a market, needs none of that and breaks all of it: it wants to pay four cents for one API call, from one service it has never used and may never use again, ten thousand times a day across a thousand services, instantly, with a budget its principal set and cryptographic proof of everything.

That workload profile, micropayments, no relationships, machine speed, global by default, is unservable by card rails, whose fixed fees exceed the transaction sizes and whose fraud systems flag exactly this behavior, and it maps precisely onto what stablecoins on fast ledgers do well. x402’s contribution is standardization: by embedding the payment negotiation in HTTP itself, the protocol every web service already speaks, it lets any API monetize per-call and any agent pay per-call without bilateral integration, the same role payment standards have always played, reducing a many-to-many integration problem to one spec. The design is chain-agnostic and asset-agnostic in principle, which is exactly why the interesting competition is happening one layer down: everyone agrees machines will pay through something like x402; the war is over which networks and which dollars they pay with, the agentic-payments landscape this publication’s explainer maps in full.

What Ripple has actually done

Strip the announcements to verifiable substance and Ripple’s x402 position has three components. The first is protocol enablement: work to make the XRP Ledger and its EVM-compatible sidechain function as x402 settlement networks, so that services quoting 402 prices can accept payment on Ripple’s rails. The second is asset positioning: RLUSD as the settlement instrument for those flows, the regulated, natively-issued dollar that institutional counterparties can hold, now past $1.7 billion in circulation with the majority living on the XRPL itself. The third is distribution: folding agentic payments into the institutional stack, custody, prime brokerage, treasury tooling, that Ripple sells, so that a corporate deploying agents can pay and get paid through infrastructure it already contracts for, the empire whose accounting this publication has done piece by piece.

Read against Ripple’s pattern, the move is characteristic: the company arrives early to settlement standards, positions its regulated dollar at the center, and lets the token’s role ride on second-order effects. It is also, notably, a fast-follower play rather than a founding one: x402’s gravity well is Coinbase’s, the standard’s flagship deployments run on Base, and Ripple is doing what it did with tokenization and custody, joining a standard it did not write and betting its institutional distribution outweighs its lateness. That bet has a respectable record in payments, where standards commoditize and distribution decides, and an unresolved tension at its center, which is the next section.

The mechanics in one worked loop

A concrete walk-through makes the standard tangible. An agent tasked with compiling a market report calls a data API it has never used. The server responds not with data but with status 402 and a machine-readable price: four cents, payable in a listed stablecoin, to a listed address, on a listed network. The agent’s payment module checks its budget policy, spending caps, approved networks, approved counterparties, set by its human principal at deployment, signs a stablecoin transfer from its wallet, and retries the request with the payment proof attached. The server, or the facilitator service verifying payments on its behalf, confirms settlement and returns the data. Elapsed time: seconds. Human involvement: zero. Relationship created: none, and none needed, because the next call, from this agent or any other, repeats the loop statelessly.

Multiply the loop and the economic texture emerges. The agent runs thousands of such calls per task across dozens of services; the services meter revenue per call instead of per subscription, opening business models, pay-per-query data, per-inference AI, per-request compute, that card economics never permitted; and the wallets involved are ephemeral, numerous, and policy-governed, an account structure no banking system was built to serve and every fast ledger was accidentally built to serve. The design also relocates trust: the service trusts the chain’s finality instead of a card network’s chargeback apparatus, the agent trusts the response because payment and delivery are cryptographically coupled, and the principal trusts the budget policy code, which is why the standard’s real dependencies are wallet security and policy tooling, the unglamorous infrastructure where most of the coalition’s engineering actually happens.

The asset question: what machines actually hold

Here the story meets the fork every Ripple analysis meets: does the flow touch XRP, or does RLUSD capture it? For agentic payments the answer has structurally new features, because machine customers differ from human ones in exactly the dimensions that decide asset selection.

The case for the stablecoin is the base case, and it is strong. Agents denominate budgets in dollars because their principals do; services price API calls in dollars because costs are; and a volatile asset in the settlement loop imposes hedging complexity on software whose entire virtue is simplicity. x402’s flagship implementations settle in stablecoins for this reason, and RLUSD exists precisely to be the compliant dollar in such loops. If agentic flows scale on the XRPL, the mechanical demand lands on RLUSD, whose float income lands on Ripple, the same pattern as every institutional product in the stack: the ledger wins, the company wins, the token’s share is the residual.

The residual, though, is less trivial here than usual, through three channels. Fees: every XRPL transaction burns XRP, and machine-to-machine traffic is the first plausible source of transaction counts large enough to make burn arithmetic visible, since agents transact at volumes humans never will; the counterargument is the same as ever, fees are fractions of a cent, and even billions of calls burn modest sums. Liquidity and bridging: agents paying across currencies and chains need routing liquidity, and XRP’s designed role as a bridge asset inside XRPL’s exchange gets a genuinely new customer class if agent flows require it, though stablecoin-to-stablecoin routing may bypass it entirely. And reserves: every XRPL account holds an XRP reserve, so an agent economy of millions of machine wallets implies structural token lockup, an effect real in direction and, at current reserve sizes, modest in magnitude.

Summed honestly: the machine economy hands XRP its most plausible utility-demand story in years, and the story’s magnitude at today’s parameters is small, which is exactly the shape of every XRP utility argument, and why the supply side still dominates the price question.

What could kill it: the honest risk register

The bet’s failure modes deserve equal billing, because several are structural rather than executional. The first is that metering never scales: the web’s services might answer the agent-traffic squeeze with licensing deals, walled APIs, and enterprise contracts, the pattern already visible in the data-licensing agreements between AI labs and publishers, rather than per-call micropayments, in which case x402 remains a niche protocol for the long tail while the economically meaningful flows settle through invoices, exactly as B2B payments always have. The second is the incumbent-absorption scenario: agent commerce standardizes around protocols the payments giants control, with stablecoin settlement as a feature inside their stacks, leaving crypto-native rails as interchangeable back-ends competing on basis points, a commodity position that rewards the largest and cheapest, which is not obviously the XRPL. The third is regulatory: autonomous wallets transacting at machine speed across borders are an anti-money-laundering novelty no framework yet addresses, agent payments concentrate exactly the properties, pseudonymity, velocity, volume, that supervisors flag, and one high-profile abuse case could impose compliance requirements that reintroduce, at the wallet-policy layer, all the friction the standard exists to remove. Ripple’s compliance-first positioning is partly a hedge against this third risk, and partly evidence of how seriously insiders take it.

The fourth risk is quieter and belongs to the token specifically: even complete success of the thesis can bypass XRP. Every channel in the residual case, fees, routing, reserves, has a plausible engineering workaround, batched settlement compressing transaction counts, stablecoin-pair routing skipping the bridge asset, account abstraction pooling reserves, and machine economics, precisely because they are pure, will adopt every workaround that saves a basis point. The machine customer that makes the token’s utility case possible is the same customer most certain to optimize it away where it can, a symmetry the honest version of the bull case has to carry.

One adjacent Ripple asset completes its hand and rarely gets counted: the identity and compliance layer. Machine payments at enterprise scale will require exactly what human payments require, sanctioned-party screening, transaction monitoring, auditable trails, applied at speeds no manual process survives, and Ripple’s acquisitions in custody and its bank-grade compliance tooling are as relevant to winning enterprise agent flows as the ledger’s speed. The competitive lane, properly drawn, is not fast chains versus card networks but compliant machine-payment stacks versus each other, a framing in which Ripple’s decade of regulatory scar tissue converts from cost into inventory. It is the same conversion the company executed in stablecoins, where being the slow, licensed issuer became the selling point, and the agent economy, whose first enterprise deployments will be lawyered to death, is built to reward it again.

The field: everyone wants the machine customer

Ripple’s bet lands in the most crowded strategic lane in crypto, because the agent economy is the rare thesis every faction shares. Coinbase built x402 and runs its center of gravity on Base; the major stablecoin issuers are wiring agent frameworks to their dollars; Google, Stripe, and the payments incumbents are building agent-commerce protocols of their own, some interoperating with x402 and some competing; and every fast ledger, Solana’s consumer stack, the corporate chains, Robinhood’s new venue explicitly markets itself as AI-native, pitches the same machine customers. The standard itself is designed to be multichain, which converts the competition into exactly the game Ripple knows: not protocol wars but distribution wars, where the winner is whoever already banks the enterprises that deploy agents at scale.

That framing is Ripple’s genuine edge and its honest limit. Edge, because agent deployments that matter economically will come from corporations with treasury policies, compliance requirements, and existing banking relationships, the customers Ripple’s entire stack was built for, and a compliant, bank-adjacent agent-payments offering is differentiated against crypto-native rivals, particularly while the American classification framework stays unsettled. Limit, because the same enterprises are precisely the customers the traditional payments giants will not surrender, and a Stripe-scale incumbent adding stablecoin settlement to its agent tooling competes with Ripple’s offering from a distribution position an order of magnitude stronger. The machine-to-machine bet, for every participant, reduces to a wager on which side domesticates the other: crypto rails acquiring enterprise distribution, or enterprise payment networks acquiring crypto settlement. Ripple, characteristically, is built to profit from either, so long as the settlement asset is its dollar.

The deeper Ripple pattern, and why this bet differs

Placing the move inside Ripple’s decade-long pattern clarifies what is and is not new. The company’s strategic constant has been settlement adjacency: identify where institutional value will move next, cross-border payments, custody, tokenized Treasuries, prime brokerage, stablecoin rails, arrive with compliant infrastructure before the flow arrives, and monetize the plumbing regardless of which asset the flow denominates in. The pattern’s track record on the corporate side is excellent, a private valuation around $50 billion says the market agrees, and its track record for the token is the permanent controversy, because at every prior junction the settlement asset the institutions chose was the dollar instrument, not XRP, a divergence the market has priced with years of underperformance against the company’s wins.

The agentic bet fits the pattern and breaks it in one respect worth isolating. Every prior Ripple market was made of human institutions, whose asset choices are governed by mandate, accounting, and habit, forces that reliably select the stablecoin. The machine market’s asset choices will be governed by code responding to cost, and code is indifferent: it will hold whatever the policy permits and route through whatever is cheapest, which means, for the first time, the token’s utility case does not require persuading a treasurer of anything, only being the cheapest path often enough at sufficient volume. That is a materially better competitive position than arguing with risk committees, and it is also a knife’s edge, as the risk register above notes, because the same indifference disqualifies XRP the moment a cheaper path exists. Ripple’s bet, reduced to one sentence, is that owning the rails lets it keep its token on the cheapest path by construction, and the machine economy will be the first market large enough, and neutral enough, to test whether that is a strategy or a hope.

Sizing honestly: forecasts versus chains

The agent-economy numbers deserve the same forensic treatment as every crypto narrative, because the gap between projection and production is currently the widest in the industry. The projections are enormous: agentic commerce forecasts run to trillions in transaction value within the decade, and the traffic data, agents as a majority-adjacent share of web requests, non-human activity dominating volumes on several trading venues, makes the direction unarguable. The on-chain production is embryonic: x402 transaction counts, while growing fast from launch, measure in the millions cumulatively, settled values are a rounding error against any payment network, and most agent activity today pays for nothing, scraping and querying services that have not yet metered themselves. The bet, precisely stated, is that metering arrives, that the internet’s services, squeezed by agent traffic they currently serve free, adopt per-call pricing at scale, and that when they do, the standard and rails already in place capture the flow. That is a real and possibly rapid adoption curve, and it has not happened yet, which is why every participant’s positioning, Ripple’s included, costs little and claims much.

The tells that would show the bet paying are concrete. Watch x402 settlement values, not transaction counts, and their distribution across chains, the series that shows whether XRPL captures share. Watch RLUSD supply and velocity for a machine-payments signature, high-frequency small-value flows distinct from institutional settlement lumps. Watch for a marquee enterprise agent deployment settling through Ripple’s stack, the proof-of-distribution the thesis requires. Watch XRPL transaction counts and reserve growth for the token’s residual effects. And watch the incumbents’ agent-commerce launches, because the week Stripe or a card network ships native stablecoin agent settlement is the week this lane’s competitive map redraws.

The conclusion is the one Ripple stories converge on, with a new twist worth stating. The company has again positioned its rails and its dollar at a plausible future’s settlement layer, cheaply, early, and with the institutional framing its competitors lack; the token again holds the residual claim, fees, routing, reserves, on flows designed to run through the stablecoin. What is new is the customer: machines transact at frequencies and account counts that could, for the first time, make the residual arithmetically interesting, and machines have no brand loyalty, no habits, and no friction tolerance, which means this market, unlike every human one, will be won purely on rails. That is the actual bet, that in a customer base of pure economics, the best settlement infrastructure wins by default, and it is the first Ripple bet in years where the token’s role, however secondary, scales with the thesis instead of beside it.

Two closing observations frame the story’s real timescale. The first is that agent payments are a rare crypto narrative whose demand side is being built by forces entirely outside crypto: every improvement in model capability, every enterprise agent deployment, every service buckling under automated traffic advances the thesis without a single coin changing hands, which makes it structurally different from narratives that require crypto to bootstrap its own demand. The infrastructure being positioned today, Ripple’s included, is a bet on a customer whose growth curve belongs to the AI industry’s capex cycle, the best-funded demand engine on earth, and the positioning costs are trivial against the option value if even the conservative forecasts land.