Crypto World

16 million stolen ADA and crypto’s restitution experiment

An exploit drained roughly 16 million ADA, about $2.4 million, from 374 Cardano wallets in late June. What happened next is the interesting part: EMURGO, one of Cardano’s founding entities, announced a recovery path to return the assets within two weeks, while an independent forensic team including Mt. Gox veterans published competing findings. Crypto has spent fifteen years insisting stolen funds are gone forever. Cardano is running a live experiment in whether that has to be true, and every chain is watching the precedent.

Summary

- A Cardano linked exploit drained about 16 million ADA from 374 wallets, with EMURGO outlining a two week plan to return affected users’ funds.

- Independent investigators challenged parts of the official account, putting competing forensic findings at the centre of how victims could qualify for restitution.

- The recovery effort is testing whether a blockchain ecosystem can compensate theft victims without reversing the ledger or compromising decentralization principles.

Between June 21 and 23, an exploit connected to a protocol called SecondFi drained approximately 16 million ADA, worth about $2.4 million, from 374 addresses on Cardano. As crypto thefts go, it barely registers: the industry loses that much most weeks, and 2026’s running total makes $2.4 million a rounding error. The theft is not the story.

The story is the response. Within days, EMURGO, the commercial arm among Cardano’s founding entities, announced it had identified a recovery path for affected users and would begin returning assets within roughly two weeks, one week to build the recovery mechanism and one to test it. Simultaneously, an independent forensic team, Tibane Labs, whose personnel include investigators from the Mt. Gox case, crypto’s original catastrophic theft, published a competing analysis of what actually happened, disputing elements of the official account. And the affected community, 374 wallets whose owners did nothing wrong beyond using a protocol, became the test population for one of the most consequential questions in the industry: whether a blockchain ecosystem can make theft victims whole without breaking the properties that make it a blockchain.

That question has a fifteen-year history of being answered no, at enormous cost, and a handful of famous exceptions that each bent the rules in a different way. Ethereum rolled back its ledger once, in 2016, and the decision split the chain permanently. Exchanges have reimbursed hacks from their own treasuries. Protocols have negotiated with attackers, paying bounties for returns. But a founding entity engineering restitution for users of a third-party protocol, on a chain whose ledger will not be rolled back, through a mechanism built and tested in two weeks, is a new entry in the genre, and its outcome, success, failure, or messy middle, will be cited in every post-exploit governance fight for years. This piece covers the exploit as best the competing forensics allow, the anatomy of the recovery mechanism and the hard constraints it must respect, the restitution genre’s history and where this attempt sits in it, the moral-hazard and precedent questions that make recovery controversial even when it works, and what the two-week experiment will actually prove.

What happened, as far as the forensics agree

The reconstruction begins with an unusual feature: there are two of them. The official account, from EMURGO and ecosystem responders, describes an exploit connected to SecondFi that extracted funds from user wallets across a three-day window, with 374 affected addresses and roughly 16 million ADA taken. The independent account, from Tibane Labs, a forensic team whose resume includes the Mt. Gox investigation, examines the same on-chain evidence and disputes elements of the official narrative, a disagreement whose specifics matter less, for this piece’s purposes, than its existence: three weeks after the event, the ecosystem’s official and independent investigators have not converged on a single story of what occurred.

That divergence is itself a finding about the state of crypto incident response.

On-chain data is perfectly preserved and public, which is why blockchain forensics can achieve certainties conventional financial investigation cannot; but the interpretation layer, which contract behavior was intended, which approvals were informed, where the boundary between exploit and design flaw sits, remains contested terrain where reputations, liability, and recovery eligibility all hang on the framing. The pattern is familiar from the anatomy of every major protocol disaster: the chain records what happened with perfect fidelity and no opinion, and the fight is always over what it meant. For the 374 wallet owners, the practical consequence is concrete: the recovery mechanism’s design, and who qualifies for it, depends on which reconstruction prevails, which is why competing forensics are not academic but constitutive of the restitution itself.

The scale deserves honest framing too. Sixteen million ADA is about 0.04% of circulating supply; $2.4 million is small enough that EMURGO could plausibly reimburse it from corporate resources without any mechanism at all. The choice to build a recovery process instead, engineered, tested, documented, signals that the exercise is understood by its architects as infrastructure, a template being built at low stakes for use at higher ones, which is exactly why it merits the scrutiny this piece gives it.

The mechanism: what recovery can and cannot mean

Every recovery attempt on a public blockchain operates inside the same iron constraint: the ledger does not go backward. Cardano’s history will not be rewritten; the stolen ADA sits wherever the attacker moved it, validly, as far as the protocol is concerned. Whatever EMURGO’s two-week build produces, it is not an undo button, and enumerating what it can be maps the entire design space of crypto restitution.

The first family is interception: if stolen funds sit on exchanges or touch regulated venues, they can be frozen and clawed back through compliance channels, the path that has recovered the largest sums industry-wide and the reason attackers launder through mixers and cross-chain routes, the bridge-hopping playbook every major theft now follows. Its reach ends where the attacker’s operational security begins. The second is negotiation: bounty offers converting attackers into white hats retroactively, effective embarrassingly often, and dependent entirely on the attacker’s incentives.

The third is replacement: making victims whole from some treasury, corporate funds, protocol reserves, an ecosystem pool, without touching the stolen assets at all, which is restitution in the economic sense and abandons recovery in the literal one. The fourth, rarest and most Cardano-specific in this instance, is mechanism-level remediation: where the exploited system itself, a protocol’s contracts, a wallet standard, retains any authority over the affected assets or their derivatives, that authority can sometimes be repurposed to restore balances, the approach that requires exactly the one-week-build-one-week-test cadence EMURGO described.

The announced timeline suggests a combination weighted toward the third and fourth families, and the details, at this writing, remain unpublished, which is appropriate caution and also part of the test: restitution mechanisms revealed before deployment invite gaming by exactly the adversaries they respond to. What can be evaluated in advance is the constraint set any design must satisfy. It must distinguish victims from opportunists, on-chain, against forensics that are themselves disputed. It must not create authority that persists after the emergency, because a standing power to reassign user balances is a bigger vulnerability than any exploit. It must not require the base protocol to special-case the event, the line Cardano’s own decentralization principles, governed by DReps precisely to prevent unilateral intervention, will not permit crossing. And it must complete fast, because every week of delay compounds the harm and shrinks the interceptable share. Two weeks, against those constraints, is aggressive, and the aggressiveness is the announcement’s real content: EMURGO believes the mechanism exists and is discoverable on a schedule.

The victims’ fortnight: what waiting inside a recovery is like

The 374 addresses deserve a section of their own, because restitution debates chronically abstract the people they are about, and this population is unusually legible. The affected wallets skew small: the $2.4 million total across 374 addresses averages under $6,500 per victim, savings-scale money for the retail holders who dominate Cardano’s famously loyal base, not fund-scale positions with legal departments and insurance. Their fortnight is a specific experience the industry has never bothered to design for: funds visibly gone, an official promise of return on a stated schedule, competing expert accounts of what even happened, and no action available except watching announcements, a limbo in which every day of official silence gets read as bad news and every community rumor moves through the victim population at chat speed.

Two features of this experience matter beyond sympathy. The first is that victim behavior during recovery windows is itself an attack surface: fake recovery portals, phishing campaigns impersonating the restitution process, and advance-fee scams targeting exactly this population appear within days of every publicized exploit, harvesting victims a second time, and the quality of official communication, clear channels, signed announcements, explicit warnings that no one will DM them, is as much a part of the mechanism’s success as its code. The second is that the fortnight sets the template for what users can expect from the ecosystem, and expectations are load-bearing: an institution-courting chain whose retail base learns that infrastructure failures get handled competently retains those users through the next incident, while a botched communication cycle converts a $2.4 million exploit into a permanent trust discount far more expensive than the theft. The recovery’s architects are, whether they framed it this way or not, running crypto’s first serious customer-service operation for a decentralized loss event, and the industry’s notes on it will be as valuable as the mechanism itself.

The genre: how crypto has answered theft before

The SecondFi experiment enters a genre with a defined canon, and its position in that canon is what gives a $2.4 million incident industry-wide stakes.

The founding text is Ethereum’s 2016 DAO intervention: facing the theft of a double-digit share of all ETH, the community altered the ledger to reverse it, and the decision’s price was permanent schism, the unaltered chain persisting as Ethereum Classic and the precedent haunting every subsequent governance debate. The lesson the industry took was that base-layer intervention works exactly once, at existential scale, and costs a chain’s neutrality forever; no major network has repeated it, through losses orders of magnitude larger. The second tradition is the exchange model: centralized custodians from the Mt. Gox estate through the modern majors have run reimbursements, creditor processes, and insurance funds, restitution as a corporate liability question, effective where custody was centralized and irrelevant where it was not. The third is the protocol-treasury model: DeFi projects reimbursing exploits from token treasuries or negotiated bounties, case by case, with outcomes ranging from full restoration to governance-vote refusals that left victims holding the loss, a genre in which the liquidation-era bad-debt socializations supplied some of the bitterest chapters.

What the canon lacks, and what SecondFi supplies, is the founding-entity model on a decentralization-first chain: an ecosystem steward, not the thief’s counterparty, not the ledger’s operator, engineering restitution for a third-party protocol’s users without touching the base layer. Cardano is, in one sense, the natural venue for the attempt, its culture prizes formal process and its governance apparatus is unusually explicit, and in another sense the hardest one, because the same culture treats ledger neutrality as close to sacred, and the community debate around the recovery has featured exactly the voices, on exactly the lines, the DAO fight canonized: make victims whole versus code is law, with a decade of intervening history sharpening both sides.

The timing layer: why this experiment, this month

The recovery’s context supplies half its meaning, because the experiment is running inside the most delicate month Cardano has had in years, and every audience the mechanism performs for is watching for its own reasons.

The institutional audience arrived the same week: Clearstream, Deutsche Borse’s post-trade arm with trillions in custody, added ADA to its regulated custody services on July 7, the most significant institutional on-ramp in the asset’s history, landing days into the recovery window. Institutions selecting crypto assets audit precisely the thing SecondFi tests, how an ecosystem behaves when its infrastructure fails, and the recovery’s execution is, functionally, a live due-diligence exhibit for every custody and ETF conversation the ecosystem hopes to have. The market audience is watching a fragile turn: ADA rebounded roughly 30% from multi-year lows in the same fortnight, whale wallets accumulated through the crash while on-chain usage thinned, and the recovery sits inside a sentiment window where a competence story compounds the bounce and an incompetence story validates the lows. And the governance audience is internal: Cardano’s DRep apparatus and its constitutional culture have spent two years building the machinery of collective decision-making, the Van Rossem fork is moving through exactly that machinery this month, and a founding entity executing an emergency restitution adjacent to, but not through, the formal governance process is itself a constitutional data point, read closely by everyone who cares where the ecosystem’s real authority lives.

The timing also explains the two-week aggression. A recovery that completes before the news cycle moves on is an asset; one that drags into autumn is a liability regardless of outcome, because unresolved incidents metastasize in exactly the audiences above. The schedule is the strategy, and its keeping or slipping is the first verdict the experiment will render.

Moral hazard, precedent, and the case against success

The strongest objections to the recovery deserve their full weight, because they are not callousness; they are the accumulated lessons of the genre.

The moral-hazard argument runs: every successful restitution teaches users that losses get reversed, which erodes the diligence that self-custody requires, subsidizes risk-taking on unaudited protocols, and converts founding entities into implicit insurers of an ecosystem they cannot actually underwrite, a liability that compounds until an exploit arrives at a scale no one can cover, whereupon the implicit promise defaults at the worst moment. The precedent argument runs deeper: a proven capability to restore balances is a proven capability to reassign them, and every government, litigant, and pressure group learns from the proof; the neutrality that makes public chains valuable is precisely the credible inability to do favors, and each benevolent exception prices that credibility down. And the selection argument is the practical edge of both: 374 wallets got a recovery mechanism because their loss was legible, bounded, and adjacent to a founding entity’s reputation, while the ecosystem’s countless smaller victims, of rug pulls, drainers, and their own mistakes, get nothing, which converts restitution from a principle into a lottery whose winners are chosen by newsworthiness.

The answers, from the recovery’s defenders, are also serious. Users harmed by infrastructure failures they could not have evaluated are not moral-hazard cases but consumer-protection ones, and an industry courting mainstream adoption cannot tell mainstream users that their diligence should have included auditing smart contracts. Precedent cuts both ways: an ecosystem that visibly cares for its users compounds trust, the asset every chain claims to optimize, and the intervention line, no base-layer changes, no persistent authority, can be held publicly and verifiably. The honest synthesis is that both sides are describing real gradients, and the experiment’s value is precisely that it will convert the argument into evidence: a recovery that completes cleanly, inside its constraints, without scope creep, is a data point the make-whole side has never had on a decentralization-first chain, and a recovery that fails, stalls, or requires quiet rule-bending is the strongest code-is-law exhibit since the DAO.

The forensics fight: why the second opinion matters

The Tibane Labs dimension deserves fuller treatment before the conclusion, because independent forensics entering a live recovery is nearly as novel as the recovery itself, and its implications outlast this incident.

Crypto incident analysis has historically been a monopoly of the responding party: the exploited protocol, the affected foundation, or the security firm they retain writes the post-mortem, and the community consumes it as fact, with no institution playing the adversarial-review role that accident investigation runs on in every mature industry. The entry of an unaffiliated team, staffed by investigators whose formative case was Mt. Gox, the theft whose decade of creditor litigation taught crypto what unresolved forensics cost, breaks the monopoly on exactly the incident where the official account carries financial consequences: eligibility for restitution flows from the accepted reconstruction, and a disputed reconstruction means disputed eligibility, appeals, and the exact procedural morass the two-week schedule cannot absorb.

The dispute’s existence, whatever its resolution, teaches two durable lessons. The first is that restitution mechanisms need an evidentiary standard before they need code: who adjudicates victimhood, against which account of events, with what appeal path, questions the traditional financial system answers with courts and regulators and that a decentralized recovery must answer with something, publicly, in advance, or improvise under fire. The second is that a market for adversarial blockchain forensics is forming, funded by exactly these disputes, and its emergence is unambiguously healthy: official accounts that expect independent review are written more carefully, mechanisms designed under scrutiny are designed better, and the industry’s post-mortem culture, long a public-relations genre, acquires the beginnings of a discipline. If the SecondFi fortnight produces nothing else, a precedent that serious incidents get second opinions would justify the episode’s place in the canon by itself.

What the two weeks will actually prove

The experiment resolves into observable outcomes on a short clock, and the reading guide is worth writing in advance. Completion on schedule, with victims restored and the mechanism’s design published for audit, proves the founding-entity model viable at small scale and makes it the reference implementation every future incident invokes, on Cardano and beyond. Partial completion, some victims, disputed eligibility, timeline slippage, proves the harder truth that restitution’s binding constraint is not engineering but forensics, and elevates the Tibane-versus-official divergence from footnote to headline. Failure or quiet abandonment feeds the code-is-law canon and, less obviously, damages the specific asset that motivated the attempt: Cardano’s institutional courtship, the Clearstream custody listing landing the same week, leans on the ecosystem’s reputation for process, and a botched recovery is a process failure in the one arena institutions watch.

Beyond the fortnight, the durable questions are two. Whether the mechanism, whatever it is, gets generalized, documented, criticized, and hardened into ecosystem infrastructure, or remains a one-off that future victims cite and cannot access. And whether the precedent’s boundary holds: the recovery’s architects have implicitly drawn a line, exceptional response, no base-layer change, no standing power, and the entire value of the experiment, for Cardano and for the industry, depends on that line surviving its own success. Crypto has proven, exhaustively, that it can build systems where theft is final. The SecondFi fortnight is a test of something the industry has barely attempted: whether it can build justice on top of finality without dissolving the finality, and 374 wallets, $2.4 million, and one founding entity’s reputation are the stakes of the first controlled trial.

Beyond Cardano, the audiences with the most to learn are the ones building the systems where this question arrives at a thousand times the scale. The tokenized-asset rails now carrying equities and Treasuries onto public chains inherit, with the assets, traditional finance’s non-negotiable expectation that errors and thefts get remediated, and every institution wiring real-world value into blockchain settlement is implicitly betting that something like the SecondFi mechanism, generalized, standardized, and legally legible, will exist when it is needed. The corporate chains have answered the question by centralizing it, their operators can intervene, and everyone knows it, which is exactly the answer the decentralized ecosystems cannot give and the reason this experiment matters disproportionately: it is a test of whether the neutral chains can offer remediation without becoming the corporate ones. Regulators, meanwhile, read incidents like this in their own dialect: a shown industry capacity for orderly restitution is an argument against prescriptive consumer-protection mandates, and a shown incapacity is the argument for them, which places the fortnight’s outcome, improbably, inside the same policy conversations deciding the industry’s classification and custody rules.

The final word belongs to proportion, which has been this piece’s method throughout. Two point four million dollars is nothing; 374 wallets are a village; two weeks is a news cycle. And the question the village and the fortnight are answering, whether a system built so that no one can reverse anything can still, when it matters, make things right, is the oldest and largest open question in the industry, older than the DAO, as large as adoption itself. Small experiments that answer large questions are the best bargains in institutional history. This one cost sixteen million ADA, none of it EMURGO’s, and its findings, either way, will be cited for a decade.

For readers tracking the experiment live, the checklist is short: the mechanism’s technical publication, the first restored balances on-chain, the treatment of disputed addresses, the Tibane findings’ final form, and whether any authority created for the recovery is verifiably dismantled afterward. Five items, two weeks, one precedent, and the rare crypto story whose ending will be a matter of public record rather than public argument.

And a housekeeping note befitting a live experiment: this piece freezes a moving story at the midpoint of its two-week window, the mechanism’s details were unpublished at this writing, and the account above should be read against the recovery’s actual outcome, which, by the time most readers arrive here, will be a matter of on-chain record. That the story can be checked against the chain is, fittingly, the whole point of the system being tested.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile, and you can lose your entire investment. Incident details reflect public reporting as of July 9, 2026, and the recovery process described is ongoing; verify current status before relying on any account of it. Always do your own research.

As analysts have predicted for July based on historical data, BTC is off to a strong start. The leading digital currency has rebounded from its most recent low of $57,700 to $64,000, a major support and pivot level.

According to the latest CryptoQuant weekly report, bitcoin’s rebound can be attributed to July’s positive seasonality and recovering demand. These factors are likely to contribute to a significant pump before the month runs out.

July Starts Strong, Bitcoin Sees Recovery

To substantiate the claims, CryptoQuant analysts cited past data that showed that the seasonal tailwind is strongest in July during bear markets. July has become bitcoin’s reliable positive month over the last decade. During previous bear cycles in 2018 and 2022, BTC closed the month with 20% and 17% surges, respectively.

So far this month, BTC has risen 11% from its lows of $57,700, trading above $64,000. The positive momentum witnessed in July usually happens regardless of how weak the broader market trend is. Since BTC entered July fresh off a bear market low, there is a higher chance of further upside, thanks to positive seasonality.

Moreover, total bitcoin demand is recovering and has climbed back towards neutral after its sharpest contraction since 2022. Analysts noted a recovery in 30-day total demand metrics after the indicator fell to -650,000 BTC in early June as the asset declined toward $58,000.

“It has since recovered to near neutral, with speculative futures demand turning slightly positive while spot apparent demand contracts at its slowest pace since mid-May. A move back into positive territory would confirm that the demand engine is re-igniting,” analysts explained.

Stronger Demand Still Needed

Furthermore, investor demand in the United States is improving, as seen in the Coinbase Premium Index, which has recovered from deeply negative readings to -0.062. The rebound was aided by BTC rebounding from the $57,000 level. It signals that selling pressure on U.S. trading platforms is easing and institutional appetite is stabilizing.

Unfortunately, market conditions are still extremely bearish despite these recent developments, as seen in the CryptoQuant Bull Score Index hovering at 20, which is the bearish zone. Even though BTC has reached short-term undervalued territory and more price recovery is possible, stronger demand is needed.

In fact, the Bull Score Index needs a reading above 60 for a sustainable rally. Until this happens, every rebound will be treated as a bear-market recovery, not a trend reversal.

The post Bitcoin’s Recovery Gains Momentum, Putting July Off to a Strong Start appeared first on CryptoPotato.

Kevin Warsh’s arrival at the Federal Reserve, renewed geopolitical tensions, and the AI investment boom have pushed stocks, gold, and Bitcoin onto sharply different paths this year, according to a new report from crypto trading firm BIT.

The report argues that investors are no longer responding to a single macro theme, with markets instead swinging between shifting catalysts that have repeatedly changed where capital flows.

Warsh, Iran, and a Fed That Won’t Budge

According to BIT, traditional relationships between equities, gold, and BTC have broken down as investors continuously reprice assets around changing macro narratives.

Its report noted that the S&P 500 has climbed 9% year to date, while gold has fallen 6% and Bitcoin has dropped 31%. Rather than moving together, the three assets have responded differently as expectations around monetary policy, geopolitical events and AI have taken turns dominating investor attention.

BIT traced the first major shift to expectations surrounding Federal Reserve policy. After President Donald Trump proposed Kevin Warsh to lead the central bank, markets abandoned earlier expectations of three interest rate cuts this year and instead began pricing in a more hawkish policy path. The June Federal Open Market Committee meeting reinforced those expectations, keeping pressure on assets that typically benefit from easier liquidity, including Bitcoin and gold.

Then there was Iran, which closed off the Strait of Hormuz following strikes against it by the United States and Israel, sending oil prices jumping and equities falling. Gold also fell, since, according to BIT, markets expected central banks in the Middle East to redirect funds toward financing reconstruction of infrastructure affected by the conflict instead of buying more bullion.

With all that happening, BTC hit a downward patch of its own, dipping below the $60,000 level and breaking what the crypto firm described as its previous resilience during geopolitical crises.

Once the Iran arc cooled, attention then shifted almost entirely to artificial intelligence, with Nvidia’s reported $2 billion stake in Marvell Technology and Anthropic’s annual revenue beating the $30 billion mark, ahead of the $20 billion OpenAI had previously reported. That combination made the AI market’s dominant investment theme, lifting tech shares while drawing capital away from other assets.

Where BIT Thinks This Goes

However, the enthusiasm around AI started fading around June, with what BIT called the “tokenmaxxing” trade losing steam as companies began to notice the true cost of AI tokens, while cheaper open-source models out of China added more pressure.

The report also noted that spot Bitcoin ETFs became heavy sellers during that period, cutting holdings by about $9 billion while BTC itself went from about $82,000 to near $63,000.

Gold, in the firm’s view, is already technically oversold, and Bitcoin is closing in on a cycle bottom somewhere between $50,000 and $55,000. But it believes the current divergence will not last, especially if the September FOMC meeting brings a change in the Fed’s hawkish stance and AI spending demand picks back up while inflation cools. In that scenario, gold, BTC, and AI trades could all turn higher together.

The post Report: AI, Warsh, and Geopolitics Break Bitcoin Correlation With Stocks and Gold appeared first on CryptoPotato.

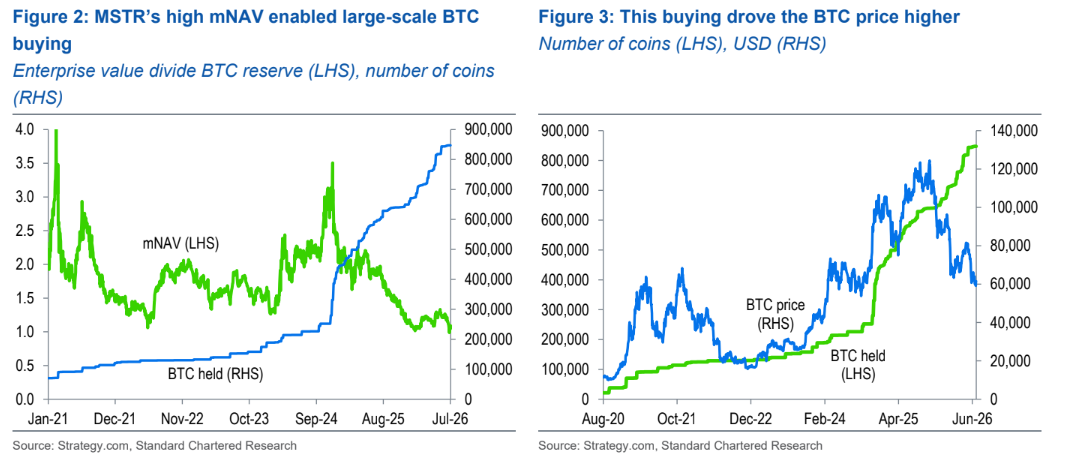

Michael Saylor, Strategy’s founder and chairman, used social media Sunday to refine how investors should interpret his company’s latest Bitcoin-related messaging. In a post built around a chart from Saylortracker.com, he said the “orange dots” indicate only part of the story—an apparent attempt to frame what markets may be inferring from his prior signals.

That clarification comes as Strategy has shifted from its long-running “never sell Bitcoin” narrative to a more flexible approach. The company has disclosed Bitcoin sales used to support dividends for holders of its STRC preferred stock and to bolster its U.S. dollar reserves. For investors, the immediate question is whether Strategy’s communications reduce uncertainty around the likelihood of further large-scale selling that could weigh on Bitcoin sentiment.

Key takeaways

- Strategy’s recent SEC filing shows it sold $216 million worth of Bitcoin earlier this month, reducing holdings to 843,775 BTC.

- Saylor’s Sunday post—linking “orange dots” to only part of the picture—adds another layer to how traders interpret Strategy’s Bitcoin signaling.

- Standard Chartered’s Geoff Kendrick argues Strategy’s messaging has become “muddy” for Bitcoin near-term, mainly because it complicates expectations around selling.

- Kendrick believes better communication could reassure markets enough that Strategy may not need to sell more Bitcoin to support STRC.

- Strategy’s common shares and STRC preferred shares have both faced pressure over the past year, with the company scheduled to report earnings on July 30.

Saylor’s new “signal” and what it may change

Saylor’s Sunday message, posted alongside a chart from Saylortracker.com, referenced “orange dots” that, he said, “tell only part of the story.” According to the post, the chart is meant to contextualize Strategy’s Bitcoin-related actions and announcements that have historically followed similar social media updates.

In prior cycles, Saylor’s public posts have often been followed by announcements of Strategy Bitcoin purchases—typically the next day. This time, however, the context is different: the market is already reacting to evidence that Strategy is willing to sell Bitcoin when required for funding priorities tied to its preferred equity structure and cash management.

From “never sell” to monetization for dividends and reserves

In recent weeks, Strategy has moved away from a strict “never sell Bitcoin” stance. The company has indicated that selling may be necessary to fund dividends for holders of its STRC preferred stock and to replenish cash reserves.

Earlier this month, Strategy sold $216 million worth of Bitcoin, according to a July 6 filing with the U.S. Securities and Exchange Commission. The filing states that the sale reduced Strategy’s total Bitcoin holdings to 843,775 tokens. Alongside that disclosure, Strategy also earlier laid out a capital framework that authorizes Bitcoin sales as a mechanism to support dividends.

Just days before Sunday’s post, Strategy increased its annual dividend rate on STRC preferred stock to 12% and disclosed that its U.S. dollar reserve had grown to $2.55 billion. Taken together, those changes suggest Strategy is attempting to create a more repeatable funding path for shareholders—one that may involve Bitcoin monetization rather than treating holdings as purely “hold forever” collateral.

Standard Chartered: communications are “muddying the waters”

Standard Chartered’s Geoff Kendrick argued that Strategy’s recent actions—and the way they are being communicated—could be undermining confidence in Bitcoin’s near-term outlook. In a note to clients released on Friday, Kendrick said Strategy’s updated approach is “muddying the waters for BTC near-term.”

Kendrick’s central point is about signaling credibility. He suggested that investors need clarity on how Strategy intends to use Bitcoin to back its STRC preferred stock without implying frequent or “wholesale” selling of BTC. He wrote that effective communication of the new strategy—using Bitcoin to back STRC—is important to reassuring markets that wholesale selling is unlikely, which he said should support Bitcoin prices.

He also made a specific conditional argument: if the messaging works and is interpreted as credible by markets, it could reduce the need for Strategy to actually sell additional Bitcoin by supporting STRC’s price dynamics.

Why the “never sell” narrative is harder to maintain

According to Kendrick, the company’s earlier “never sell” posture limited how its Bitcoin holdings could be used—both operationally and in terms of how the market perceives their purpose. He said the main issue is that “never sell” frames BTC holdings as something the company cannot put to broader financial use, making it harder for investors to interpret changes when they eventually occur.

Kendrick noted that Strategy has sold Bitcoin twice and has announced a BTC monetization program, implying the communications have been shifting for “several months” rather than just recently. For traders, this sequence matters: once markets begin to price in monetization as a regular tool for funding, the burden shifts to management messaging to explain when sales are likely versus when holdings will remain intact.

Even so, Kendrick expects the messaging—and therefore market signaling—will improve, and he anticipates that the clearer communication will improve the outlook for Bitcoin. Standard Chartered continues to maintain a $100,000 year-end forecast for Bitcoin, per the analyst’s note.

Equity pressure ahead of earnings

Strategy’s equity markets have not reflected a smooth acceptance of the narrative shift. Investors who bought into the “Strategy story” have faced losses over the past year, and the preferred stock and common stock structures have both shown stress.

The STRC preferred shares were originally designed to hold a par value of $100, but shareholders saw that par value fall last month to the lowest level since the preferred stock was introduced a year ago. Meanwhile, Strategy’s common shares—trading under the MSTR ticker—have declined sharply. The stock closed at $94.64 per share on Friday, down from a 52-week high of $457.22 and down more than 70% since July 2025.

Looking ahead, Strategy is scheduled to report second-quarter earnings on July 30. Yahoo Finance data cited in the source article points to a consensus expectation of $4.28 per share. Separately, Fintel.io data indicates earnings have missed analyst forecasts in six of the last eight quarters, including a 33.76% negative surprise in the first quarter of 2026.

With the earnings date approaching, investors will likely focus on whether Strategy’s dividend funding plan and Bitcoin sales approach align with the market expectations built around its communications—especially after Sunday’s attempt to clarify what certain chart cues are meant to represent.

For now, the key watch items are how markets interpret Saylor’s “orange dots” framing, whether Strategy’s next disclosures add detail to the monetization plan, and what management signals ahead of July 30—particularly regarding the balance between supporting STRC and minimizing further Bitcoin selling pressure.

Peter Schiff says the next major market crash will begin in the bond market, not in Bitcoin (BTC). The longtime gold proponent argues that rising U.S. Treasury yields, not crypto volatility, pose the real threat to global markets.

On his latest podcast, Schiff warned that a breakdown in Treasuries could ripple through stocks, housing, and cryptocurrencies. He expects investors to eventually flee into gold as those risk assets unwind together.

Why Schiff Says the Market Crash Starts With Bonds

The warning centers on a bond market that Schiff says has already begun to break. The 10-year Treasury yield sits near 4.5%, while the 30-year has climbed toward 5%, according to Treasury figures. He expects both to head sharply higher.

Rising yields lift borrowing costs everywhere. Schiff argues that this would pressure stocks, deepen a housing affordability problem, and slow growth. The average 30-year mortgage already sits at 6.49%, according to Freddie Mac’s weekly survey, a level that keeps many buyers away.

A deeper housing slump would then force the Federal Reserve to step in, he says. That would mean more money printing and higher inflation.

Both outcomes, in his view, favor precious metals. Gold now trades above $4,100 an ounce, having recovered after it slipped below $4,000 in June.

Why He Says Bitcoin Won’t Be Spared

Bitcoin has held up better than many of Schiff’s critics expected. The token trades near $64,200, with a market cap around $1.29 trillion. Even so, it sits roughly 49% below its record of $126,080 from October 2025.

That drawdown, Schiff argues, already shows Bitcoin does not behave like a safe haven. He expects it to fall further when stocks drop, rather than hold firm like gold.

“Although I believe that when tech stocks go down, Bitcoin will be correlated. It just doesn’t go up when tech stocks go up. But when tech stocks go down, it’s gonna go down a lot more,” he said in the podcast.

He also doubts Wall Street’s public optimism. Major banks still hold bullish Bitcoin targets, yet the weak performance of Strategy’s preferred shares suggests investors privately question those calls.

The strain runs deeper at MicroStrategy itself. Michael Saylor’s firm is the largest corporate holder, with more than 840,000 BTC.

It has started selling Bitcoin to fund dividends on those securities. Schiff has long warned the model would buckle, including a controversial call for a steeper decline to $20,000.

“I do believe that the precious metals market is setting up for a major move up and the stock market is setting up for a major move down,” he stated.

Whether the bond market cracks the way he predicts remains far from certain. Many analysts still expect yields to ease if inflation cools.

In the meantime, however, his thesis hands investors a clear signal to watch. The next few weeks of Treasury moves may test it.

The post Peter Schiff Says the Biggest Market Crash Will Not Start With Bitcoin, But Here appeared first on BeInCrypto.

Nancy Pelosi and Cathie Wood rank among the market’s most-watched stock pickers. They time their bets in opposite ways, and a decade of data shows one clearly ahead.

This month made the contrast concrete. ARK bought Circle stock one day before the company won a landmark bank charter.

Pelosi vs Cathie Wood by the numbers

Quiver Quantitative runs a hypothetical “Nancy Pelosi” strategy that rebuilds a portfolio from her family’s disclosed filings. As of mid-July 2026, it had compounded near 21% a year since May 2014.

That figure is a backtest, not a live account, and it recalculates daily. At the same date, the model showed a win rate close to 73% across 731 trades. Its maximum drawdown was near 37%.

ARK’s flagship fund, the ARK Innovation ETF (ARKK), returned about 13.4% annualized since its October 2014 launch. Its total gain since then tops 300%.

On Quiver’s math, the Pelosi backtest more than doubles that figure. It also outpaces the S&P 500 over the same span.

How Paul Pelosi’s Trades Keep Winning

Nancy Pelosi does not place the trades herself. Her husband, Paul Pelosi, a longtime investor, runs the account.

His method is consistent. It centers on call options in large technology companies.

The results have been hard to ignore. In 2024, Pelosi’s portfolio rose about 70.9%, by Unusual Whales’ estimate, against a 24.9% gain for the S&P 500.

The report singled her out as a standout options trader. Even so, only about half of Congress’s active traders beat the market that year.

The edge is not new, either. A 2011 study found a portfolio copying House members’ buys beat the market by about 6% annually. That analysis covered 1985 to 2001.

The evidence is not one-sided, though. A 2022 paper found no proof that members beat the market once the STOCK Act forced disclosure.

There is a catch for anyone hoping to copy it. The STOCK Act lets lawmakers disclose trades as late as 45 days after the fact.

By the time filings appear, the entry price is often gone. Other well-timed congressional stock buys have kept the same debate alive.

ARK’s Transparent Bets and the Circle Call

Cathie Wood built ARK in 2014 and made her name with an early, outsized bet on Tesla. The firm publishes every trade the day it happens and stakes its name on public conviction.

Circle (CRCL) is the latest test. The stock is barely a year old. It closed 168% above its $31 IPO price on its June 2025 debut, then slid.

On July 9, ARK bought about 217,900 Circle shares, worth close to $13.7 million, per its daily disclosures. That day it also sold about $9.8 million of Robinhood stock. One day later, Circle secured final OCC approval to form a national trust bank.

The stock climbed roughly 15% in pre-market trading on the news. Circle CEO Jeremy Allaire framed the charter as a turning point.

“OCC approval to establish Circle National Trust marks a defining step in bringing blockchain technology and digital assets into the core of the U.S. financial system,” Allaire said in the announcement.

Transparency cuts both ways, though. ARKK rode the 2020 growth boom, then lost about 67% in 2022 as rates rose. Circle’s post-IPO swings show how quickly the mood can flip.

The Verdict

The two are not a clean match. One is a concentrated, options-heavy strategy rebuilt from delayed filings. The other is a diversified fund priced in real time.

Both lean on the same technology and crypto themes. That shared tilt powered much of the edge during a long bull market.

On the raw numbers, the Pelosi strategy still wins. Its options leverage, though, is hard for a small investor to copy.

The real divide is access. ARK’s moves are public within hours, while Pelosi’s surface weeks later.

That gap may soon matter less. Pelosi will retire when her term ends in January 2027, which would end one of the market’s most-watched disclosure trails.

Her trades also face a political clock. Senator Josh Hawley’s bill, first branded the PELOSI Act, cleared a Senate committee in 2025. There it was renamed the Honest Act and widened to cover presidents. It would bar lawmakers and their spouses from holding individual stocks.

The pressure is bipartisan. Treasury Secretary Scott Bessent has urged Congress to curb congressional stock trading.

For now, the scoreboard favors Pelosi on returns and Wood on transparency. The next year may decide whether the comparison even survives.

The post Nancy Pelosi vs Cathie Wood: Whose Trades Timed It Better? appeared first on BeInCrypto.

Michael Saylor, the Strategy founder and long-time Bitcoin advocate, posted a new chart on Sunday meant to reinforce how investors should interpret his firm’s latest moves. The message—“Orange dots tell only part of the story”—drew attention because it follows a shift at Strategy toward using Bitcoin to support dividends and maintain cash reserves, an approach that differs from its earlier messaging.

The debate matters for markets because Strategy’s Bitcoin treasury has often served as a proxy for broader institutional demand. But in a note to clients, Standard Chartered’s Geoff Kendrick said Strategy’s evolving communications are “muddying the waters” for Bitcoin in the near term—particularly regarding whether or not the company is likely to sell large amounts of BTC.

Key takeaways

- Strategy’s recent filings and disclosures show a move away from strict “never sell” messaging, including BTC sales to fund dividends and replenish cash.

- Standard Chartered’s Geoff Kendrick argues the company’s market signaling lacks clarity and can weigh on Bitcoin sentiment in the short term.

- Kendrick believes clearer messaging tied to backing STRC with Bitcoin could reduce pressure for wholesale BTC selling.

- Strategy’s STRC preferred shares and common stock have underperformed sharply over the past year, adding pressure ahead of its July 30 earnings report.

Saylor’s latest post and the question of what investors should infer

Saylor’s Sunday post shared a chart via Saylortracker.com, continuing a pattern in which similar messages have preceded announcements of Strategy’s Bitcoin purchases. In this case, however, the context is different: Strategy has recently signaled that Bitcoin may be sold when needed for shareholder dividends and corporate liquidity.

According to a July 6 filing with the U.S. Securities and Exchange Commission, Strategy sold $216 million worth of Bitcoin earlier this month. The filing also states that the company’s total holdings declined to 843,775 tokens.

That development comes after Strategy introduced a capital framework earlier in the month that contemplates Bitcoin sales as part of funding dividends. The same initiative included an increased annual dividend rate on Strategy’s STRC preferred stock to 12% and reported U.S. dollar reserves of $2.55 billion.

Standard Chartered: the “never sell” story is no longer straightforward

In Standard Chartered’s view, the central issue is not only what Strategy does, but how investors interpret what it does. Kendrick argued that Strategy’s older “never sell” framing limited how the market could understand—and therefore price—the economic role of its Bitcoin treasury.

“The problem with the ‘never sell’ approach is that it limits what MSTR’s BTC holdings can do—or, perhaps more importantly, what they are perceived to be doing,” Kendrick wrote in a Friday client note. He added that Strategy has already begun changing how it communicates this strategy in recent months, pointing to two BTC sales and the disclosure of a BTC monetization program.

Kendrick’s concern is that ambiguous signals may cause near-term uncertainty about whether BTC sales are an infrequent backstop or an ongoing feature of the business model. That ambiguity can, in turn, affect how investors gauge Bitcoin’s near-term demand picture, especially when Strategy is viewed as one of the most prominent corporate Bitcoin holders.

Why the messaging shift could still matter for Bitcoin prices

Despite his critique, Kendrick also suggested there could be a constructive path forward if Strategy communicates more clearly how STRC’s structure connects to Bitcoin economics. In his note, he said the market needs reassurance that wholesale selling is unlikely.

He argued that “effective communication” of Strategy’s new approach—specifically using Bitcoin to back STRC—could help remove the market’s incentive to assume large-scale sales are the only way the dividend mechanism works. Kendrick said that if the signaling is effective, it should support Bitcoin prices, and it may even reduce the need for Strategy to sell BTC by helping maintain STRC’s value through price support.

Standard Chartered also reaffirmed that it maintains a $100,000 year-end forecast for Bitcoin, though the bank framed the immediate concern as about interpretation and clarity rather than a direct change to its outlook.

Strategy shares face pressure ahead of earnings

Investors who have followed Strategy’s Bitcoin narrative have not been met with a smooth ride. The STRC preferred shares were initially structured with a $100 par value, but that par value effectively fell out of focus last month, reaching the lowest level since the preferred stock was introduced a year ago.

Meanwhile, Strategy’s common shares (trading under the MSTR ticker) have declined dramatically over the past year. The stock closed at $94.64 per share on Friday, according to the article’s figures, down from a 52-week high of $457.22—representing more than a 70% loss since July 2025.

With expectations also a concern, Strategy is scheduled to report second-quarter earnings on July 30. Consensus for earnings per share is $4.28, based on Yahoo Finance data. The company has missed analyst forecasts in six of the last eight quarters, Fintel.io data shows, including a 33.76% negative surprise in the first quarter of 2026.

For traders and long-term investors alike, the combination of earnings risk and evolving treasury policy is likely to keep attention on both Strategy’s disclosures and the way Saylor frames them publicly—especially after Sunday’s chart post reminded markets that interpretation remains contested.

Going forward, readers should watch whether Strategy’s next communications become more explicit about how its Bitcoin-backed dividend strategy reduces the likelihood of large sales, and whether the July 30 earnings report offers additional signals on cash flows and execution—areas that could sharpen the market’s understanding of the “orange dots” narrative.

South Korea’s crypto trading volume hit a two-year low, dropping below 10 trillion won ($6.7 billion) for the first time since September 2023.

The slump coincides with a dramatic collapse across the country’s stock markets.

Is South Korea Losing Its Crypto Market?

Trading volume measures the total value of assets bought and sold across exchanges over a set period. Weekly volume across South Korea’s five main fiat exchanges hit a two-year low, signaling a sharp cooling in overall market activity.

The five platforms include Upbit, Bithumb, Coinone, Korbit, and Gopax. In the week of July 3 to July 10, combined volume reached roughly 9.97 trillion won ($6.65 billion). Furthermore, that marks a 25.75% drop from the prior week’s 13.4 trillion won total ($8.9 billion).

The decline deepens over time. The current volume is about 43.5% below early June levels, according to WuBlockchain.

It marks the fifth consecutive weekly drop, reflecting a broad retreat in retail speculation nationwide.

Follow us on X to get the latest news as it happens.

Structural challenges add to the pressure. During the first quarter of 2026, combined volume had already fallen notably, with Bithumb dropping over 30%.

Furthermore, an operational error at Bithumb earlier this year damaged trust among cautious retail investors.

Tighter regulation compounded the caution. New limits on exchange ownership stakes reinforced a defensive mood. Consequently, many retail traders pulled back from the major platforms, deepening the multi-week slide in overall trading activity.

Why Are Crypto and the KOSDAQ Falling Together

The synchronized decline is no coincidence, given how South Korean investors move between tech stocks and crypto. Many traders speculate across both markets, so a decline in risk appetite in one quickly spreads to the other.

The KOSDAQ index has crashed 31% over the past 9 weeks, erasing nearly a full year of gains. That correction rivals the 2020 crash, when it fell 32% in five weeks.

Meanwhile, the KOSPI dropped 20% over three weeks, entering technical bear-market territory.

The AI trade sits at the center of the turmoil. Optimism around artificial intelligence is fading, especially after doubts over chip and semiconductor spending. Samsung and SK Hynix, along with leveraged ETFs, account for over 70% of traded market value, amplifying volatility.

Regulators are now watching closely. South Korea’s finance minister announced tighter oversight of leveraged single-stock ETFs, acknowledging the sector’s risk concentration.

As a result, that intervention adds pressure and pushes capital toward more defensive positions.

Analysts see the contraction as a reallocation, not an exit. Some activity may be migrating toward smaller platforms, DEXs, or traditional assets.

However, lower liquidity on major exchanges means wider spreads, higher volatility, and pressure on platform fee revenue.

The post South Korea Crypto Volume Hits a Two-Year Low Amid the KOSDAQ Crash appeared first on BeInCrypto.

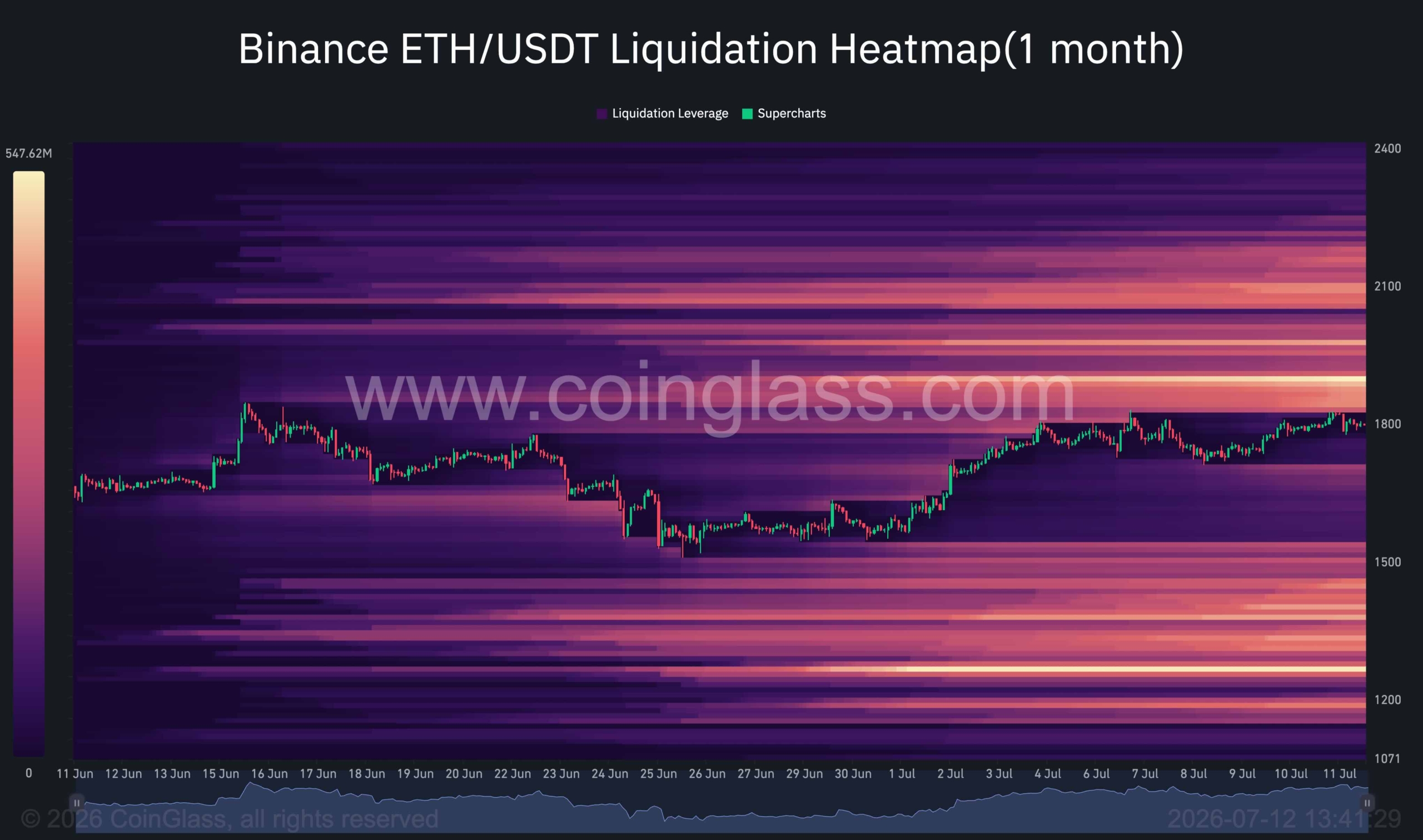

Ethereum has continued its recovery from the June lows and is now approaching a major technical inflection point. While the recent rally has improved short-term sentiment, the asset is still trading beneath a confluence of long-term resistance levels.

Interestingly, the liquidation landscape aligns closely with these technical barriers, suggesting that ETH could first target overhead liquidity before the market decides whether a larger trend reversal is underway or another corrective leg lower remains ahead.

Ethereum Price Analysis: The Daily Chart

On the daily timeframe, ETH remains within a broader descending structure in place since the beginning of the year. It has recovered strongly from the major demand zone around $1.45K-$1.55K and is currently testing the key resistance region around $1.80K-$1.85K.

This area is particularly significant because it coincides with the descending trendline that has capped price action since May. The level also represents a major horizontal resistance that previously acted as support before the June breakdown.

Despite the recent strength, ETH remains below the 100-day and 200-day moving averages, both of which continue to trend lower. The 100-day MA is positioned around the $2K-$2.1K resistance zone, while the 200-day MA remains considerably higher near $2.2K, reinforcing the broader bearish market structure.

As long as ETH remains below the descending trendline and the $1.80K-$1.85K resistance zone, the current move can still be viewed as a recovery rally within a larger downtrend. A decisive breakout above this area would shift focus toward the next major resistance at $2K-$2.1K.

ETH/USDT 4-Hour Chart

The 4-hour chart highlights a clear ascending structure that has developed since the late-June low. Price has respected the rising channel boundaries while forming higher highs and higher lows, reflecting improving short-term momentum.

The market has already reclaimed the $1.62K-$1.64K demand zone and subsequently established another support area around $1.72K-$1.74K. These zones have repeatedly attracted buyers during pullbacks and continue to define the short-term bullish structure.

However, the rally is now approaching the upper boundary of the channel and the major resistance band around $1.83K-$1.85K. This creates a natural area where profit-taking and seller activity could emerge.

From a structural perspective, ETH remains constructive above the $1.72K-$1.74K support region. Losing this level would be the first sign that bullish momentum is fading and could expose the lower channel boundary and the broader support zone around $1.55K.

Sentiment Analysis

The Binance ETH/USDT liquidation heatmap provides an important clue regarding the next likely move.

The most significant concentration of short-side liquidity sits above the current market price, particularly within the $1.95K-$2.1K region. This cluster aligns remarkably well with the daily chart resistance zone, the 100-day moving average, and the broader supply area visible on the higher timeframe.

Meanwhile, substantial liquidity pools remain below the market around the $1.45K-$1.55K region, which corresponds closely with the major daily demand zone that has supported ETH throughout the recent recovery.

The alignment between the liquidation map and the technical structure suggests that the market may first be drawn toward the overhead liquidity cluster. A move into the $2K-$2.1K area would effectively sweep a large concentration of short liquidations while simultaneously testing one of the most important resistance zones on the chart.

The reaction at that region will likely determine the next major directional move. If buyers manage to reclaim the $2K-$2.1K resistance area and establish acceptance above it, the recovery could evolve into a broader bullish trend reversal. However, if the liquidity sweep is followed by strong selling pressure and rejection from resistance, ETH could enter another notable decline, potentially targeting the large liquidity pools resting beneath the market around the $1.45K-$1.55K support zone.

The post Ethereum Price Analysis: ETH Reaches Its Biggest Obstacle on the Road to $2K appeared first on CryptoPotato.

Strategy founder and chairman Michael Saylor again took to social media on Sunday to offer his latest signal to investors as one analyst sees Saylor’s messaging as needing more clarity to help Bitcoin regain its momentum.

“Orange dots tell only part of the story,” was Saylor’s message on Sunday in a post that accompanied a chart from Saylortracker.com, similar to previous social media messages that have preceded news of Strategy’s Bitcoin (BTC) purchases, typically announced the day after his posts.

In recent weeks, the largest digital asset treasury company and a major BTC holder, has moved away from its long-time “never sell Bitcoin” approach to a willingness to sell the biggest crypto as needed to fund dividends for holders of its STRC preferred stock and to replenish its cash reserves. Earlier this month, Strategy sold $216 million worth of Bitcoin, reducing its total holdings to 843,775 tokens, according to a July 6 filing with the US Securities and Exchange Commission.

“Orange dots tell only part of the story.” Source: Michael Saylor

Days earlier, Strategy unveiled a capital framework allowing Bitcoin sales to fund dividends, increased the annual dividend rate on its STRC preferred stock to 12%, and disclosed that its US dollar reserve had grown to $2.55 billion.

Standard Charter’s global head of digital assets research, Geoff Kendrick, believes recent Strategy’s actions — and Saylor’s manner of communicating them — “are muddying the waters for BTC near-term.”

“We think effective communication of MSTR’s new strategy (using BTC to back STRC) is key to reassuring markets that wholesale selling is unlikely; this should in turn support BTC prices,” Kendrick wrote in a note to clients on Friday. “Indeed, if this signalling proves effective, it should remove the need for MSTR to actually sell any BTC by supporting STRC’s price,” he said.

Related: Crypto Biz: Did Michael Saylor buy the Bitcoin bottom for once?

StanChart sees inconsistencies in “never sell” approach

Kendrick said that Strategy’s long-held “never sell” approach limited what the company could with its industry-biggest digital asset treasury.

“The problem with the ‘never sell’ approach is that it limits what MSTR’s BTC holdings can do — or, perhaps more importantly, what they are perceived to be doing,” the StanChart analyst said. “MSTR has started to shift its communication strategy on this in recent months. It has sold BTC twice and recently announced a BTC monetization program.”

Source: Standard Chartered Bank

Still, he sees Strategy’s “market signaling” will improve soon. He expects that to bring clarity to the outlook for Bitcoin, on which StanChart maintains its $100,000 year-end forecast.

Shares struggle from year low ahead of earnings report

Investors who bought into the Strategy narrative have not had an easy time in the past 12 months. The STRC preferred shares were formulated to hold a price of $100 apiece. Shareholders saw that par value fall to the wayside last month, to the lowest value since the preferred stock was introduced a year ago.

The common shares, trading under the MSTR ticker, have lost more than 70% of their value since July 2025, closing at $94.64 per share on Friday, down from a 52-week high of $457.22.

The company is slated to report second-quarter earnings on July 30, with analysts consensus of $4.28 per share, according to Yahoo Finance data. Earnings have fallen short of analyst forecasts in six of the last eight quarters, according to Fintel.io data, including a 33.76% negative surprise in the first quarter of 2026.

Magazine: Will the crypto lobby’s $189M campaign get CLARITY over the line?

HDFC Bank ended the March financial year with 3,343 fewer employees, a major contraction for India’s biggest private lender.

Total headcount stood at 211,178 as of March 31, down from 214,521 a year earlier. The lender said it is steadily moving routine processing onto digital and automated systems.

AI Automation Hits Back-Office Jobs Hardest

The greatest impact fell on operational staff. Non-supervisory employees, classified as workmen or clerical, and subordinate staff fell by more than 8,000 to 162,797. New hiring also slowed, dropping by 3,811 across the period.

Higher tiers moved the other way. Middle-level headcount rose by 1,252, junior-level by 3,543, and senior management added 15 roles.

The bank tied the shift to strategy. The report said it is steadily shifting routine tasks, such as cash deposits, to Cash Recycler Machines and other automated channels.

That effort runs on Neev, the bank’s in-house AI platform for model access, governance, and workflow integration. Chief Executive Officer Sashidhar Jagdishan said the bank is “consciously redeploying talent from backend functions” toward customer-facing roles as technology takes over routine work.

“As we accelerate the transformation toward becoming a technology-led, customer-centric bank, employees need to keep pace,” he said.

Follow us on X to get the latest news as it happens

Banks Worldwide Lean on AI to Trim Staff

HDFC Bank is not alone. Standard Chartered plans to trim 15% of corporate function roles by 2030 as it scales automation. The trend is now evident in the data. AI drove 38,579 US job cuts in May, roughly 40% of the monthly total, according to Challenger, Gray & Christmas.

However, not every leader shares the gloom. Jeff Bezos argues AI will lift productivity and living standards rather than erase work.

For HDFC Bank, the math already favors fewer hands. Profit after tax rose 10.9% to ₹74,671.3 crore, about $7.83 billion, in FY26, even as the workforce shrank.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post India’s Largest Private Bank Lost Over 3,000 Employees to AI appeared first on BeInCrypto.

Teen Speaks On Argument, New Pic Surfaces

The locations where Blue-Green algae has been reported this year in Northern Ireland

Formula 1 congratulates ‘Friend of F1’ Jannik Sinner after Wimbledon title defence

-

Fashion6 days ago

Fashion6 days agoOpen Thread: What Great Books Have You Read Recently?

-

News Videos6 days ago

News Videos6 days agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Fashion4 days ago

Fashion4 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Tech6 days ago

Tech6 days agoAnthropic’s new “J-lens” reveals a silent workspace inside Claude that mirrors a leading theory of consciousness

-

Crypto World6 days ago

Crypto World6 days ago$1,000 Credit Alert! BlockDAG X Exchange Pre-Registration Now Officially Open, Polkadot Dips & Zcash Rebounds

-

Business6 days ago

Business6 days agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports5 days ago

Sports5 days agoJoshua Pacio ‘more complete’ ahead of ONE rematch vs Malachiev

-

Sports3 days ago

Sports3 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

News Videos6 days ago

News Videos6 days agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech5 days ago

Tech5 days agoAnthropic brings Claude Cowork to mobile and web as usage data shows most users aren’t coding

-

Crypto World6 days ago

Crypto World6 days agoSK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

News Videos6 days ago

News Videos6 days agoAvoid entering in FOMO #bitcoin #cryptocurrency #trading #scalping

-

Sports3 days ago

Sports3 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Sports5 days ago

We have punished the disrespect

-

Crypto World6 days ago

Crypto World6 days agoBinance lists Strategy’s STRC stock as company expands Bitcoin funding

-

Tech3 days ago

Tech3 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Tech6 days ago

Tech6 days ago9 Best Keyboards (2025), Tested and Reviewed

-

Business6 days ago

Business6 days agoEnbridge: AI Tailwind Priced In (Rating Downgrade)

-

News Videos6 days ago

News Videos6 days ago“What’s going on?!” Carl Froch discusses Floyd Mayweather Jr financial issues

You must be logged in to post a comment Login