Crypto World

SEC Regulation Crypto: $75m exemption explained

While Washington’s attention fixes on whether the CLARITY Act can find seven Democratic votes before the August recess, the Securities and Exchange Commission has been quietly assembling the framework that governs American crypto if the bill dies, and much of it even if the bill passes.

Summary

- Regulation Crypto would create a four-year startup exemption for crypto projects raising up to 5 million dollars per year.

- A separate fundraising exemption would let more mature issuers raise up to 75 million dollars annually with lighter disclosure than full registration.

- The safe harbor would give tokens a defined path out of securities classification once issuer-led managerial efforts permanently end.

- The rule could operate alongside the CLARITY Act, but if the bill fails, it may become the main US crypto capital-formation framework.

- The biggest fights ahead are over dollar thresholds, decentralization standards, investor protections, and litigation risk.

On July 7, the agency confirmed plans to formally propose Regulation Crypto, its first major crypto-specific rulemaking under Chair Paul Atkins. The proposal, expected to run past 400 pages, sits under review at the White House Office of Information and Regulatory Affairs, the final gate before publication for public comment, and Atkins has said release is expected shortly after that review completes.

The package does three concrete things. It gives new crypto projects a startup exemption from full securities registration for up to four years while they build toward network maturity, raising up to 5 million dollars annually against whitepaper-style disclosures. It creates a fundraising exemption allowing more mature issuers to raise up to 75 million dollars in any 12-month period with audited financials and semiannual reporting, a burden far lighter than full registration. And it writes an investment contract safe harbor: a rules-based path for a token to exit securities classification entirely once its issuer has permanently ceased the essential managerial efforts that made it an investment contract in the first place.

Atkins has repeatedly described the framework as a bridge to the CLARITY Act. The description is honest and incomplete at the same time. A bridge implies something temporary that the statute replaces; in reality, Regulation Crypto answers questions the bill does not reach, will operate for years regardless of the Senate outcome, and, if the bill fails, becomes the entire de facto constitution of American crypto capital formation. This feature decodes what the rule actually does, where it came from, why Senate Democrats consider it an end-run, and what it means for the market that one of these two frameworks is arriving no matter what happens in the next three weeks.

The taxonomy underneath: five buckets instead of one question

Regulation Crypto did not appear from nothing. Its foundation is a joint SEC and Commodity Futures Trading Commission interpretive release from March 17, 2026, which replaced the enforcement era’s single endless question, is this token a security, with a working taxonomy of five categories: digital commodities, digital collectibles, digital tools, stablecoins, and digital securities. Under the interpretation, only digital securities, tokenized versions of traditional financial instruments, remain fully subject to the securities laws. The other categories may still trigger securities obligations if sold as part of an investment contract, which is where the Howey analysis survives, but the default presumption flipped: most tokens are not securities by nature, and the legal question becomes how they were sold, not what they are.

Atkins introduced the exemption framework the same day, in a speech at the DC Blockchain Summit titled Regulation Crypto Assets: A Token Safe Harbor, and the agency submitted the proposed rules to the White House within the week. The sequencing matters for understanding what kind of project this is. The interpretive release stated how the agency reads existing law; interpretations bind nobody and evaporate with the next chair. The proposed rule converts the reading into formal regulation, with notice, comment, and the full Administrative Procedure Act process, which makes it dramatically harder to unwind. The past year’s accommodations, staff guidance, no-action letters, dropped enforcement actions, carry no binding force at all; a future commission could reverse them by memo. A finalized Regulation Crypto could only be undone by a new rulemaking that survives its own comment period and litigation. Durability is the entire point, and durability is exactly what the industry has said it needs.

The chair’s broader agenda frames the rule as one panel of a triptych. Atkins has described crypto market structure, custody, and capital formation as the agency’s three crypto priorities, with the stated goal of making the United States the leading crypto capital. He has asked staff to evaluate letting non-security crypto assets that were sold under investment contracts trade on venues not registered with the Commission, to clear paths for state-licensed platforms to list such assets, and to let CFTC-regulated platforms offer them with margin. He also shut down the agency’s crypto innovation hub, arguing the Gensler-era version was so tainted that industry participants feared subpoenas after visiting, a symbolic demolition that tells its own story about how completely the agency’s posture has inverted.

The three exemptions, decoded

The startup exemption is the on-ramp. A new project receives up to four years of relief from full registration while it develops its network, during which it can raise up to 5 million dollars per year. The disclosure standard is principles-based and deliberately modeled on what serious projects already publish: whitepaper-style documentation of the technology, the token economics, and the team, plus required financial statements to investors. The four-year clock is the regulatory embodiment of an idea the industry has argued since 2018, that decentralization takes time, and that forcing registration at launch, when a network is inescapably centralized, guarantees either noncompliance or offshoring. The exemption’s wager is that a project given four lawful years will either mature into something the safe harbor releases or grow into something the fundraising tier can carry.

The fundraising exemption is the growth pathway, and its design is more conservative than the headline suggests. The 75 million dollar annual cap is borrowed directly from Regulation A+, the existing exemption for smaller public offerings by conventional issuers; Atkins adapted a tested framework instead of inventing one. The obligations scale accordingly: audited financial statements and ongoing semiannual reporting, meaningfully heavier than the startup tier’s whitepaper standard, meaningfully lighter than a full registration. For the mid-sized token issuer, the practical effect is a lawful domestic alternative to the offshore foundation structures that became the industry’s default architecture, with a compliance bill measured in hundreds of thousands of dollars instead of tens of millions.

The investment contract safe harbor is the philosophical core and the piece with no statutory parallel. It answers the question the Torres ruling in the Ripple case raised but could not settle: when does a token that was sold as a security stop being one? The safe harbor’s answer is a rule-based test keyed to managerial effort. Once an issuer has permanently ceased the essential managerial functions that investors relied on, the token exits securities classification, full stop. That converts decentralization from a rhetorical claim into a compliance milestone with legal consequences, and it gives every project in the startup tier a defined destination. It is also, not coincidentally, the provision that most directly generalizes the industry’s hardest-won litigation outcomes into standing law, the same conceptual territory Ripple spent 150 million dollars mapping, as the token-versus-sale distinction moved from courtroom argument to regulatory architecture.

The objection: an agency legislating around the legislature

Senate Democrats have noticed that the SEC is building, by rule, much of what Congress has not agreed to build by statute, and their objection deserves a full hearing because it is not frivolous.

Elizabeth Warren and Chris Van Hollen wrote to Atkins directly, charging that the agency plans to exempt most cryptocurrencies from the securities laws with significant potential harm to investors, and calling on Congress to close the loopholes as it considers market structure legislation. Financial industry commenters have warned that broad exemptive relief could import cybersecurity risks, illicit-finance exposure, and flash-crash volatility into markets stripped of their traditional guardrails. The constitutional-order version of the critique is sharper still: an agency whose chair previously advised crypto firms is using administrative discretion to deliver, in advance, the deregulatory half of a bill the elected branch has not passed, while the accountability provisions Democrats attached to that bill, the ethics rules aimed at the president’s 2.3 billion dollars in crypto exposure, have no administrative equivalent and can only exist in statute. Regulation Crypto, on this reading, is not a bridge to CLARITY. It is a mechanism for harvesting CLARITY’s benefits without paying CLARITY’s political price, and every week it advances reduces the industry’s urgency to compromise on the ethics language currently blocking the bill, a standoff crypto.news has followed into its decisive month.

The rebuttal has two layers. Legally, exemptive authority is not a loophole; Congress wrote it into the securities laws deliberately, and Regulation A+, Regulation D, and Regulation Crowdfunding are all products of the same power. An agency tailoring registration requirements to a novel asset class through notice-and-comment rulemaking is the administrative state working as designed, and the courts, not letters, will test whether this rule exceeds the statute. Practically, the alternative to Regulation Crypto is not the status quo Democrats prefer; it is the pre-2025 regime of regulation by enforcement that a federal judge partially repudiated and that nearly dissolved companies later vindicated. Between an imperfect rule with a comment period and an enforcement lottery with none, the rule is the more accountable instrument, whatever one thinks of its content.

What both sides quietly agree on is the stakes of reversibility. Democrats want the ethics and consumer provisions in statute because statutes bind future administrations; the industry wants the exemptions in a finalized rule for precisely the same reason. The entire fight, in Congress and at the agency simultaneously, is about who gets to make their preferences durable first.

How the agency got here: from Hinman speech to Howey off-ramp

The rule reads differently with a decade of institutional history attached, because every one of its provisions answers a specific wound.

The startup exemption answers the original sin of the ICO era. In 2017 and 2018, hundreds of projects raised capital from Americans with no disclosure standard at all, the agency responded with a wave of enforcement that treated every token sale as an unregistered offering, and the surviving industry drew the obvious lesson: incorporate in Zug, exclude Americans, and disclose nothing. The exemption’s whitepaper-based standard is a wager that a lawful middle existed all along, and that the agency’s refusal to build it, not the industry’s refusal to use it, drove a decade of capital formation offshore.

The safe harbor answers the Hinman problem. In 2018, a senior SEC official famously suggested in a speech that Ether, whatever its origins, had become sufficiently decentralized that its sales were no longer securities transactions. The industry spent years trying to hold the agency to that logic, the agency spent years insisting the speech was one man’s opinion, and the internal documents Coinbase later pried loose in litigation showed officials themselves could not agree on what the standard was. Commissioner Hester Peirce proposed a formal token safe harbor twice, in 2020 and 2021, and was ignored by her own agency both times. The current safe harbor is Peirce’s idea with Atkins’ signature, arriving seven years after the speech that made everyone realize the question had no answer.

And the fundraising tier answers the enforcement era’s quietest casualty: the mid-sized compliant issuer that never existed because there was no rule to comply with. Between the 5 million dollar seed rounds that Regulation D could awkwardly cover and the public listings that only exchanges and miners attempted, an entire capitalization band of the industry simply had no American on-ramp. Borrowing Regulation A+’s 75 million dollar ceiling is the agency conceding that the band was a regulatory artifact, not a market verdict.

The arc from Gensler to Atkins, from an agency that sued first and declined to write rules even under court order, to an agency proposing 400 pages of them, is the sharpest institutional reversal in modern financial regulation, and it happened without a single statute changing. That fact is the strongest argument for the rule and the strongest argument against relying on it, at the same time.

What can still change: the comment period is not a formality

Between OIRA clearance and a final rule stand months of process in which the package’s most important parameters remain genuinely contestable, and market participants pricing the framework as finished are early.

The dollar thresholds are the obvious pressure point. Consumer advocates and Senate Democrats will push the 75 million dollar ceiling down and load the startup tier with conditions; industry commenters will push for inflation indexing and aggregate-cap clarity, since the current design names annual limits without a publicly specified lifetime ceiling. The decentralization test inside the safe harbor is the subtle one. Permanently ceased essential managerial efforts is a phrase that will absorb tens of thousands of comment pages, because it decides whether the off-ramp is a real destination or a mirage: too strict, and no foundation-supported network ever qualifies; too loose, and every project theatrically dissolves its team on paper while running development through affiliates. The illicit-finance overlay is the political one. The same law enforcement coalition currently fighting the CLARITY Act’s developer protections, a split crypto.news dissected as the Senate vote approached, will demand that exempted issuers carry monitoring obligations the statute never imposed, and the agency’s answer will determine whether the exemptions are usable by actually decentralized projects or only by companies that look like broker-dealers with extra steps.

Litigation risk frames all of it. A finalized rule this consequential draws challenges from both flanks: investor-protection groups arguing the agency exceeded its exemptive authority by hollowing out registration, and, conceivably, industry plaintiffs attacking whatever conditions survive comment. Post-Chevron, courts owe the agency’s statutory reading no deference, and a single adverse circuit decision could stay the framework for years. This is the structural reason Atkins keeps calling the rule a bridge and pressing Congress to act anyway: he is building the most durable thing an agency can build while publicly acknowledging it is the second-most durable thing available.

Regulation Crypto versus the CLARITY Act: substitutes, complements, or race

Mapping the two frameworks against each other shows they overlap less than the political rhetoric implies, which is why the with-or-without framing in this feature’s title is literal.

The CLARITY Act’s center of gravity is market structure: which agency supervises trading, how exchanges and brokers register, how the CFTC gains spot authority over digital commodities, how developers escape money transmitter liability. Regulation Crypto’s center of gravity is capital formation: how tokens are launched, funded, and eventually released from securities status. The bill barely touches primary issuance mechanics; the rule barely touches secondary market supervision. A world with both is coherent: CLARITY sorts the assets and assigns the regulators, Regulation Crypto governs how new assets are born. Atkins’ bridge metaphor undersells his own product; the honest description is that the rule is the bill’s missing chapter, written by the agency because the legislature never drafted one.

The substitution effect appears only in the failure scenario, and there it is nearly total. If the Senate misses the August window and the 2030 warnings prove accurate, Regulation Crypto plus the March taxonomy plus the CFTC’s stretched existing authority become the entire American framework: token launches under the exemptions, classifications under the five buckets, trading under a patchwork the rule’s platform provisions try to rationalize. That regime would function, and its existence is precisely what Galaxy Research and others cite when they note that CLARITY’s failure would be a slow bleed rather than a catastrophe. But it would be a framework resting on one commission’s rulemaking, contestable in court, reversible by a hostile successor with patience, and silent on everything from illicit finance funding to the ethics questions that stalled the bill. The GENIUS Act fight already previewed what statute-versus-regulator arguments look like when real money is at stake, with state and federal authorities wrestling over stablecoin turf in a battle crypto.news covered throughout its Senate run, and the yield wars that followed passage show how much conflict survives even a signed law, a standoff crypto.news has tracked between banks and issuers over 6 trillion dollars in deposits.

There is also a timing race with the bill’s own politics. The rule’s OIRA review and comment period run on an administrative calendar indifferent to the Senate’s. If the merged CLARITY draft stalls on ethics while Regulation Crypto publishes for comment, the industry’s cost of legislative failure drops in real time, which weakens the coalition pressing moderate Democrats and strengthens the members arguing the bill can wait. Agency action meant as a bridge can function as an off-ramp. The three weeks in which both instruments reach their decisive stages, the merged bill text and the published rule, will reveal which metaphor the market believes.

What it means for issuers, and the European mirror

Before the issuer decision tree, the market implications deserve a paragraph of their own, because the rule reprices assets that already exist, not just launches that have not happened. Tokens whose largest discount is classification ambiguity, the mid-cap layer ones, the DeFi governance assets, the infrastructure tokens that trade below comparable revenue because American institutions cannot categorize them, gain a defined path to non-security status through the safe harbor even if the CLARITY Act never assigns them a commodity label. Exchange listing committees, which spent the enforcement era rationing US availability by litigation risk, get a compliance framework to point to. And the venture pipeline reopens domestically: funds that structured around offshore token warrants for a decade can underwrite American issuance with actual rules attached, which changes where the next cycle’s projects incorporate, hire, and pay taxes. None of this requires the rule to be generous. It requires the rule to exist, because the binding constraint was never severity. It was undefined risk, the one input no allocation committee can price.

For anyone actually launching a token, the practical decision tree changes shape the moment the rule publishes. A credible path now exists to raise seed capital domestically under the startup tier, scale through the 75 million dollar pathway with audit-grade disclosure, and target the safe harbor as the legal finish line where the token sheds its securities character by verifiable decentralization. The offshore foundation, the airdrop-to-avoid-sale contortions, and the deliberate exclusion of American buyers, the entire defensive architecture of the past eight years, become choices rather than necessities. The projects most affected are the serious middle: too big for a fair launch to fund, too small to carry registration costs, which describes most of the infrastructure layer the industry claims to want.

The comparison that will define the rule’s success is the one across the Atlantic. Europe’s MiCA regime just completed its transition, locking unlicensed firms out of a 30-country market and elevating the licensed few, a sorting crypto.news documented as the deadline hit. MiCA’s strength is comprehensiveness backed by statute; its weakness is rigidity, a stablecoin regime severe enough to expel the largest issuer on earth. Regulation Crypto inverts the trade: flexible, innovation-forward, and administratively fast, but resting on agency authority in a country where agencies change hands every four years. An American founder in 2026 chooses between a European rulebook that cannot easily be improved and an American one that cannot easily be trusted. The CLARITY Act is, among everything else, an attempt to give the American framework the one property it lacks, and the rule arriving with or without it is both the industry’s insurance policy and the bill’s quiet competitor.

The decode, compressed: Regulation Crypto is the most consequential piece of American crypto policy that almost nobody outside Washington is reading, precisely because it advances on the boring calendar of administrative law while the Senate supplies the drama. Four-year runways, 75 million dollar raises, and a legal exit from securities status are arriving through the Federal Register, on a timeline no filibuster can touch and no recess interrupts. The comment period will bend the parameters, the courts may test the boundaries, and a future commission could someday attempt the long unwind. What no plausible scenario now delivers is a return to the world where the only American rulebook was a lawsuit. The only question the Senate’s three weeks will answer is whether the new rulebook arrives as a chapter of a statute or as the whole book.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

In Utah, which passed State-Endorsed Digital Identity (SEDI) legislation, Cardano Foundation-built Veridian has already shown that digital identity can be delivered in a privacy-preserving way, allowing users to prove that they are over or under a specific age without exposing any other data. It’s a working model of what responsible verification can look like and shows trust does not require unnecessary disclosure. Privacy can be designed into the system from the start.

That is the standard bills like KIDS or KOSA should favor.

If the goal is to protect children, the tools should be narrow, purposeful, and minimally invasive. Broad mandates that push every platform toward more data, more retention, and greater dependence on identity are too blunt and risk creating a multitude of other problems alongside the ones they claim to solve.

A better approach is straightforward. Build for data minimization, limit retention, and use privacy-preserving verification where verification is truly needed. If digital trust can be established without exposing personal data, lawmakers should prefer that path. If safety can be improved without turning the internet into an identity checkpoint, that should be the only option.

Children deserve protection online. But they do not need a policy framework that makes everyone more visible in order to make the internet, and the companies that thrive on it, more accountable.

EU AML watchdog has warned that the end of MiCA’s transitional period has increased the risk of compliance pressure on crypto firms as customers move to licensed providers across the bloc.

Summary

- EU anti money laundering chief warned that customer migration after MiCA could strain compliance at crypto firms.

- AMLA said licensed providers should maintain strong anti money laundering controls as they onboard new users.

- The authority plans to publish a crypto money laundering risk report this year while expanding its blockchain analytics capabilities.

According to Bruna Szego, chair of the Authority for Anti-Money Laundering and Countering the Financing of Terrorism (AMLA), crypto companies exiting the European Union market could face a surge in customer withdrawal requests, while licensed virtual asset service providers (VASPs) may struggle to onboard large numbers of new users without weakening compliance standards.

Speaking during a Wednesday briefing before the European Parliament’s Committee on Economic and Monetary Affairs, Szego said firms winding down operations should be prepared for increased customer activity as users transfer their assets before services end. She added that licensed providers absorbing those customers should keep anti-money laundering procedures effective throughout the transition.

The warning comes after the European Union’s 18-month Markets in Crypto-Assets (MiCA) transitional period ended on July 1, requiring crypto-asset service providers (CASPs) to obtain authorization to continue serving customers in the bloc.

Earlier, the European Securities and Markets Authority (ESMA) instructed firms that remained unauthorized after the deadline to take immediate steps to wind down their EU operations, leaving customers to migrate to licensed providers.

AMLA prepares next stage of MiCA oversight

Before the July 1 deadline, AMLA issued an advisory note outlining money laundering risks linked to the end of the transitional period. According to the authority, the guidance sets out expectations for both firms closing their EU businesses and licensed providers accepting new customers so that anti-money laundering controls remain effective during the migration.

During the parliamentary briefing, Szego said AMLA plans to publish a report before the end of the year examining money laundering risks across the crypto sector alongside supervisory practices used by national authorities. She added that the authority is expanding its blockchain analytics capabilities to strengthen oversight of crypto-asset service providers.

According to Szego, the report will compare how regulators supervise CASPs across member states and identify differences that could require coordinated follow-up work between AMLA and national authorities.

The latest comments build on Europe’s post-licensing supervisory efforts. On July 11, ESMA launched a Common Supervisory Action covering a sample of MiCA-authorized crypto custodians to examine operational resilience in areas including private key management, transaction controls, incident response and reliance on third-party technology providers.

ESMA said the review is intended to test whether authorized firms can maintain effective operational safeguards in practice rather than relying solely on their MiCA licenses, making it one of the first coordinated supervisory exercises after the transition period expired.

Robinhood’s newly launched Ethereum layer-2, built on Arbitrum technology, has quickly become one of the busiest rollups in the ecosystem—prompting fresh debate over a familiar question in Ethereum scaling: do successful L2s ultimately lift demand for ETH, or do they mainly capture value for themselves?

According to Cointelegraph’s reporting and data it cites, more than $141 million in Ether was bridged to Robinhood Chain in its first two weeks. DeFiLlama’s Ether distribution data also indicates that more than half a million wallets now hold ETH on the network. Activity has spilled into trading as well: Robinhood Chain has reportedly surpassed Ethereum L1 and Coinbase’s Base L2 in 24-hour DEX volume.

Key takeaways

- Robinhood Chain’s rollout has boosted attention on whether L2 adoption can translate into stronger ETH demand.

- Bridged Ether and wallet growth on the L2 are clear early signals, but that does not automatically mean higher L1 fee revenue or burn.

- Industry participants differ on what drives ETH upside: fee-share economics versus ETH’s role as “money” across L2 ecosystems.

- Even if major institutions build on Ethereum, it remains uncertain how much of that activity requires users to hold ETH directly.

Robinhood Chain’s rapid traction puts institutions in the spotlight

Robinhood Chain launched on July 1 and, per the activity figures cited above, has rapidly drawn users and liquidity. In its first two weeks, the network drew meaningful Ether bridging volumes and grew to more than 500,000 wallets holding ETH on the chain, according to DeFiLlama.

What has drawn more interest than the underlying rollup concept is the sponsor: Robinhood is a publicly listed retail brokerage with tens of millions of customers. Prior waves of L2 growth—often associated with crypto-native teams—failed to materially shift market pricing for ETH, largely because much of the economic action stayed on the rollups rather than flowing back to Ethereum L1.

This time, the narrative is different: Robinhood has brought a mainstream financial brand into the L2 arena, and early signals suggest it is integrating into broader real-world asset (RWA) activity. Within days of launch, Robinhood Chain reportedly accounted for 6.9% of all tokenized stockholders, based on Token Terminal data referenced in the coverage.

Why some see the launch as a stronger “ETH is money” thesis

Ether’s price reaction has added fuel to the optimism. The article notes that Ether rose roughly 15% from $1,582 on July 1 to $1,825 by July 13, citing Coingecko price data.

Commentators linked the price strength to Robinhood Chain as reinforcement of an “ETH is money” argument—one that emphasizes ETH’s role as the base asset underpinning Ethereum settlement and collateral usage rather than just its share of transaction fees.

On July 11, World Liberty Financial’s Eric Trump posted on X that “ETH is pumping hard,” while Tom Lee, chairman of BitMine Immersion Technologies, argued on X that the launch supports the idea that “ETH is money,” pointing to Ethereum’s native gas role and L2 finality on the mainnet.

Developer commentary also leaned toward a milestone framing. Alex Gluchowski, founder and CEO of Matter Labs (the developer behind zkSync), described Robinhood Chain as a milestone showing L2 infrastructure has moved from experimentation by crypto teams to usage by regulated, publicly listed companies. He also characterized Robinhood’s approach as tailoring an Ethereum rollup for privacy, compliance, and performance while inheriting Ethereum’s security and staying connected to its liquidity.

Bitwise’s Max Shannon, quoted in the article, suggested the significance goes beyond prior L2 deployments. He argued it reflects growth of the Ethereum ecosystem among major institutions and arrives as Ethereum broadens its push toward institutional engagement through initiatives referenced in the report.

But value-accrual questions remain unresolved

Even with institutional participation, the core investment question has not been fully answered: how does rising L2 usage translate into measurable economic value for ETH holders?

The coverage highlights a key tension between two ways of thinking about ETH upside. One view treats ETH as a revenue-generating asset tied to L1 fee capture and burn. The other treats ETH as money—gaining value as it becomes the widely accepted collateral and settlement asset across a growing number of L2 systems.

Ark Invest’s Lorenzo Valente posted on July 14 that Robinhood Chain generated $816,000 in revenue since launch, with Arbitrum taking a 10% cut and only about 0.15% of the total reportedly paid back to Ethereum. The article also includes pushback from GrowThePie, which argued Valente’s numbers were off by a factor of four and that 0.6% is the correct share.

Regardless of which proportion is accurate, the broader point remains: even if Robinhood Chain is among the busiest L2s, the portion of fees attributed to Ethereum L1 appears small in the near term. The article adds that, while Robinhood generated more gas fees than any other L2 in the past week (citing a post referencing “Matze” and GrowThePie), Ethereum’s L1 only received $4,400 from that activity.

Gluchowski argued that ETH’s appreciation likely would not hinge on fee revenue alone. Instead, he said the asset’s value could strengthen as ETH becomes more widely used as a base monetary asset across the L2 environment—particularly as value settles through Ethereum and ETH becomes less “just a fee token.” He also suggested that users might pay for activity with stablecoins or not think about gas directly, yet ETH could still benefit from its underlying role in settlement and collateralization.

Institutional builders may not mean users hold ETH directly

Shannon acknowledged that upgrades such as Fusaka have improved Ethereum’s scaling capabilities, but he said rising transaction activity hasn’t yet translated into meaningfully higher L1 fees or ETH burn. In his view, Robinhood Chain won’t “solve this problem,” and neither will the aggregate growth of L2s without a broader shift in developer incentives and in Ethereum’s token economics.

The coverage also flags another practical uncertainty: whether institutional users actually need to hold ETH themselves. As tokenized stocks and other RWAs increasingly trade against stablecoins, some users may interact less with ETH day to day—despite ETH’s role in running settlement and securing the ecosystem behind the scenes.

Robinhood Chain therefore appears to be both a promising signal and a reminder of the gap between adoption and accrual. It demonstrates that a large, regulated financial brand is willing to build on Ethereum’s infrastructure, but it does not yet provide a conclusive pathway for how that activity should translate into stronger demand for ETH from end users.

For investors and builders, the next watch items are straightforward: whether L2 growth continues to expand Ether collateral and usage over time, whether L1 fee and burn effects move meaningfully beyond current baselines, and whether Ethereum’s economics evolve enough to ensure value from institutional L2 activity doesn’t get stranded entirely on the rollups.

[The stream is slated to start at 10 a.m. ET. CNBC Television will start the stream when the event begins. Please refresh the page if you do not see a player above.]

Federal Reserve Chairman Kevin Warsh testifies Wednesday before the Senate Banking Committee, facing questions over the the economy and how various factors might impact interest rates.

Part of congressionally mandated Capitol Hill appearances for the central bank leader, Warsh spoke Tuesday to the House Financial Services Committee. During his remarks, he reaffirmed the Fed’s commitment to fighting inflation though he gave few clues about the direction of monetary policy.

Legislators tried baiting Warsh into commenting on fiscal and political matters, but he largely avoided the topics, stressing the importance of the Fed staying focused on its assigned responsibilities.

Read more:

Warsh pledges Fed policy ‘regime change’ to rid inflation ‘tax’ on American people

Kevin Warsh names members of his Federal Reserve task forces, including Marc Andreessen, Doug McMillon

Fed meeting minutes to show ‘family fight’ over rates. The squabble could drag on for a while

Circle has secured a court-backed arbitration win after records made public in a Boston federal court detailed why the stablecoin issuer suspended Heka Funds’ USDC minting and redemption services over suspected market manipulation involving Tether.

Summary

- Circle has won an arbitration case after an arbitrator ruled it lawfully suspended Heka Funds’ USDC minting and redemption services.

- Court records said Heka did not disclose Tether’s role as the fund’s main investor and Circle reasonably suspected possible market manipulation.

- The ruling comes as Circle continues expanding its institutional business with new banking initiatives and partnerships in the United States and South Korea.

Court filings submitted by Circle on Tuesday as part of its petition to confirm a February arbitration award said the company concluded the Malta-based arbitrage fund had failed to disclose Tether’s role as its principal investor and reasonably suspected trading activity that could have manipulated the USDC market.

Retired judge Robert L. Dondero, who served as arbitrator, ruled in Circle’s favor on the remaining contract claims, finding the company acted within the rights granted under its agreements with Heka.

Hidden Tether ties became central to the dispute

At the center of the case was Heka Funds, managed by London-based Abraxas Capital Management, which opened a Circle account in January 2022 for its Elysium Global Arbitrage Fund.

According to the arbitration record, Heka disclosed only investor Simon Grima during onboarding, while Tether had become the fund’s dominant capital provider. Testimony from Heka founder Fabio Frontini showed Tether’s investment reached about $800 million by the time of arbitration, accounting for roughly 75% of Elysium’s assets.

Dondero concluded the omission was intentional and wrote that the missing disclosure appeared designed to avoid revealing Tether’s involvement in the fund. Circle Chief Business Officer Kash Razzaghi testified that the company would not have approved the account had it known of Tether’s role when the relationship began.

The trading dispute emerged after Silicon Valley Bank’s collapse in March 2023 temporarily pushed USDC below its dollar peg. According to the filings, Heka bought discounted USDC in secondary markets and redeemed the tokens with Circle at face value after many other arbitrage firms had stopped once the spread narrowed.

Internal Circle communications presented during arbitration showed executives disagreed over whether the trades represented legitimate arbitrage. Razzaghi described the activity as “a manufactured arb not a market-driven one,” attributing it to Tether waiving its normal fees, while Circle employee David Norton initially argued the trades appeared commercially rational.

Circle allowed Heka to redeem more than $587 million in USDC over a two-week period while testing whether the trading opportunity depended on Heka’s activity. Court records said Norton later changed his position after asking Heka to pause its trades and observing that the market spread tightened instead of widening. Coinbase also informed Circle it was uncomfortable working with Heka because of the fund’s Tether relationship and fee structure, leading the exchange to place restrictions on the account, according to the filings.

Arbitrator upholds Circle’s contractual rights

Court documents showed Circle reduced Heka’s minting and redemption limits to zero in November 2023 before suspending the account on Dec. 1 under Section 9(c) of the parties’ master services agreement after Frontini threatened legal and regulatory action.

Heka’s request to redeem $100 million in February 2024 was rejected, and the master services agreement expired the following month. Testimony presented during arbitration said Tether invested another $500 million in Elysium during the same month before Heka filed its arbitration claim.

Another issue raised during the proceedings involved Frontini’s application for an account with Circle France shortly before the hearing. According to the arbitration award, he did not disclose the ongoing dispute and submitted a board resolution stating Heka maintained an active Circle relationship, later testifying he expected his U.S. application to fail.

Applying Delaware law, Dondero found Circle did not breach either agreement because the user terms allowed the company to adjust transaction limits and suspend services at its discretion. The arbitrator also ruled Circle was not required to prove market manipulation had occurred, only that it had reached a reasonable conclusion that such activity might be taking place.

Although Circle requested about $5.15 million in legal fees and costs, Dondero awarded only $166,643.25 related to expert work after finding Heka continued pursuing a $49 million lost-profits claim that had already been excluded from the case.

A Heka spokesperson told the Financial Times the fund had never engaged in market manipulation and had never been the subject of a regulatory investigation involving such conduct. The spokesperson also said Circle sought to make the arbitration record public to divert attention from its refusal to process USDC redemptions.

The disclosure comes as Circle continues expanding its institutional business globally. The company recently received final approval from the U.S. Office of the Comptroller of the Currency to establish Circle National Trust and is preparing to host its invitation-only Current Seoul event on July 23, where executives from banks, crypto exchanges, and payments companies are expected to discuss future partnerships as Circle pursues wider USDC adoption in South Korea.

Crypto World

High-level White House meeting said to be planned to hash out Clarity Act ethics section

The most contentious piece of the crypto market structure bill is unresolved in the final weeks of Senate runway, and administration officials are expected to meet on it.

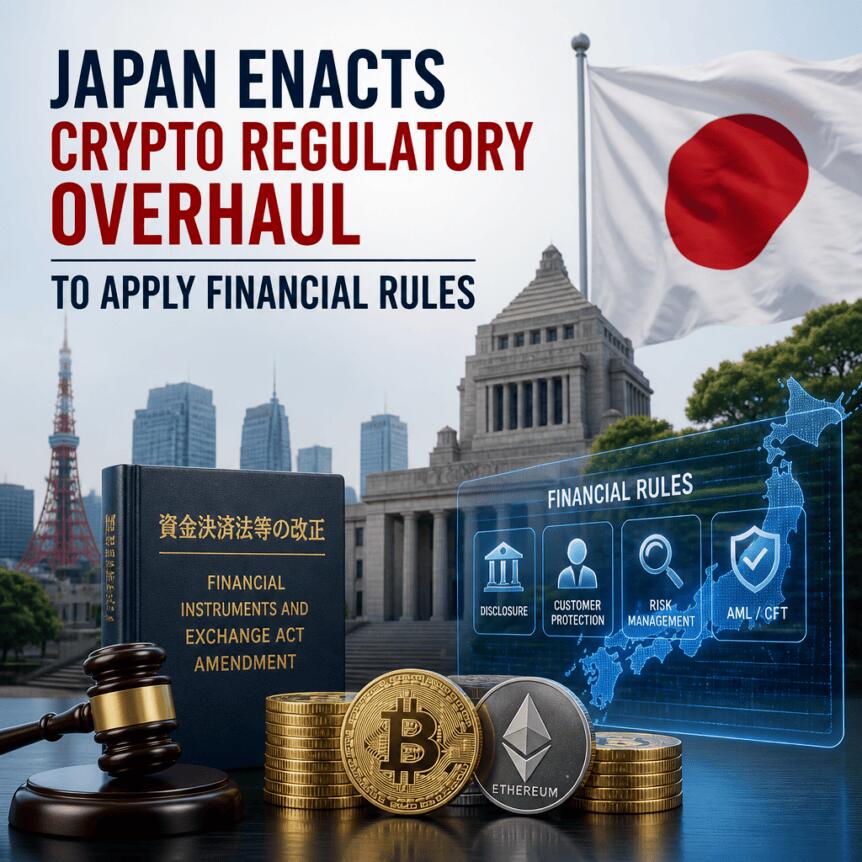

Japan has approved revisions to its cryptocurrency law, reshaping how digital assets are treated under the Financial Instruments and Exchange Act (FIEA). According to a report by Nikkei, the changes passed in parliament on Wednesday mark a major regulatory shift away from the country’s earlier approach under the Payment Services Act.

The updated framework aims to place crypto closer to traditional finance, adding market-integrity measures and strengthening oversight for businesses operating in Japan. It also introduces insider trading restrictions and tighter controls around registration and compliance.

Key takeaways

- Japan’s parliament passed revisions that treat crypto assets as financial assets under the FIEA, moving the sector away from Payment Services Act rules.

- The overhaul introduces insider trading restrictions for issuers, exchanges, and other market participants who have undisclosed material information.

- Penalties are expected to increase substantially for companies that operate without proper registration.

- Registered crypto firms may be reclassified under the law, reflecting a broader effort to align terminology and oversight with traditional financial regulation.

From payment-focused rules to a financial-assets framework

Under Japan’s previous regulatory approach, crypto assets were largely treated through the lens of the Payment Services Act (PSA), which framed digital assets primarily as payment-related instruments. The revisions now classify crypto assets as financial assets under the Financial Instruments and Exchange Act (FIEA), according to Nikkei.

That distinction matters for compliance design. When regulators bring crypto into the FIEA perimeter, firms typically need to follow expectations associated with market conduct, disclosure, and supervision—areas that are more familiar to traditional brokerage and trading environments than to payment processors.

Insider trading limits and stronger market-integrity expectations

The revised rules tighten conduct requirements across the ecosystem. As described in the Nikkei report, issuers, exchanges, and other market participants are prohibited from trading while aware of undisclosed material information.

The legal structure is intended to mirror insider trading restrictions used in traditional finance (TradFi). For exchanges and other intermediaries, this can change day-to-day controls—such as how material information is documented, who can access it, and how trading is managed around significant corporate events.

While the details of enforcement mechanisms are not laid out in the excerpt provided, the existence of an insider trading rule signals regulators’ intent to treat crypto markets as subject to the same fairness and integrity standards expected in regulated securities and derivatives markets.

Heavier penalties for operating without registration

Japan’s revisions also reportedly increase the consequences for firms that conduct business without the required registration. Nikkei reports that the maximum prison term could rise from three years to 10 years, and fines could increase from roughly 3 million yen (about $19,000) to around 10 million yen.

The report further notes that insider trading violations could lead to penalties of up to five years in prison, fines of up to 5 million yen, or both. In practical terms, these changes elevate legal risk for firms that fail to meet compliance obligations—or for employees who trade or influence trades without controls that align with the new rules.

For traders and investors, stronger penalties can also shift how firms approach internal governance, potentially affecting market behavior and the reliability of corporate and exchange disclosures over time.

Reclassification of crypto businesses and the “TradFi alignment” trend

Alongside the substantive changes, the revised framework reportedly adjusts the wording used for registered entities. The terminology may move from “cryptocurrency exchange” to “cryptocurrency trading company,” reflecting the broader role regulators now associate with the sector.

Japan’s approach fits a wider global pattern: rather than crafting entirely separate legal regimes for crypto, many jurisdictions are mapping digital asset activity onto existing financial regulation categories. That trend is visible in other policy work described in related coverage from Cointelegraph, including a report noting South Africa’s tax authority draft guidance on how existing tax rules apply to crypto assets.

In the United States, regulators have similarly continued clarifying how existing securities and commodities frameworks can apply to different kinds of digital asset activity, underscoring that the “crypto-as-finance” direction is not unique to Japan.

What Japan’s shift means for market participants

For crypto exchanges and other intermediaries, the immediate challenge is operational: aligning compliance systems with a legal regime that more closely resembles traditional market regulation. That likely includes stronger oversight processes, clearer documentation around material information, and more robust controls over who may trade and when.

For investors, the change is primarily about predictability. When conduct rules and penalties look closer to those used in established financial markets, participants may have more confidence that trading behavior is subject to comparable integrity standards. The longer-term question is how strictly and consistently the new rules will be applied as the market adapts.

Readers should watch for subsequent guidance on implementation—particularly around registration requirements, compliance expectations for exchanges and issuers, and how authorities will interpret “material information” in practice. Those details will determine how quickly Japan’s crypto market can transition into the new framework and what compliance gaps, if any, remain to be addressed.

EU crypto compliance is entering a potentially turbulent phase after the Markets in Crypto-Assets Regulation (MiCA) transitional period ended on July 1, pushing more businesses—and more customers—into the post-transition licensing environment. Bruna Szego, chair of the EU’s anti–money laundering authority AMLA, warned that a wave of user migration could create operational and compliance strain for virtual asset service providers (VASPs) across the bloc.

Speaking during a briefing with the European Parliament’s Committee on Economic and Monetary Affairs on Wednesday, Szego said providers should expect pressure as customers “rush to withdraw” and as licensed firms take on new users. Her comments underline a key risk for the next stage of EU crypto supervision: whether firms can keep anti–money laundering controls effective while business models and customer flows shift quickly.

Key takeaways

- AMLA chair Bruna Szego warned that end-of-transition customer movement could intensify operational and compliance pressure on EU crypto VASPs.

- As MiCA’s transitional period ended on July 1, firms that are not properly authorized were expected to wind down EU activities “immediately,” per ESMA guidance.

- AMLA has advised both licensed providers onboarding new customers and firms winding down to keep anti–money laundering controls functional through the transition period.

- AMLA says it will publish a report before year-end assessing money laundering risks and supervisory practices, including differences between EU member states.

- The authority is also expanding its blockchain analytics capabilities to strengthen oversight of crypto-asset service providers.

Why MiCA’s transition ending raises compliance stress

MiCA’s transitional period was designed to give the market time to adapt to a new regulatory framework. But with the clock now fully expired, Szego suggested the change could trigger behavior that compliance departments may not be able to absorb smoothly at scale.

In her remarks, she focused on two pressure points. First, entities winding down their EU operations may face customer withdrawal surges, which can strain internal processes and monitoring systems. Second, licensed crypto firms that remain active under MiCA may see onboarding volumes increase as they absorb users migrating away from less-compliant platforms.

The practical implication is straightforward: even if firms are formally compliant, rapid customer migration can still challenge the day-to-day execution of know-your-customer and transaction monitoring controls—especially if migration happens faster than expected.

AMLA’s advisory note and the compliance balancing act

Ahead of the July 1 deadline, AMLA published an advisory note highlighting money laundering risks linked to the end of the transitional period. According to the advisory guidance, firms should take targeted steps depending on where they sit in the transition—either scaling down EU activities or onboarding customers within the licensed perimeter.

Szego emphasized that AMLA expects providers to maintain efficient compliance procedures during the transition rather than treating the changeover as a mere administrative milestone. For winding-down firms, the focus is on ensuring controls do not degrade during periods of change. For licensed providers, the concern is that adding customers rapidly should not dilute anti-money laundering safeguards.

AMLA’s positioning also suggests a supervisory priority: AMLA is effectively drawing attention to “transition risk”—the idea that business continuity and compliance discipline can be hardest during periods of structural adjustment.

ESMA’s wind-down expectation after the deadline

MiCA’s end-state requirement is that crypto asset service providers must be licensed to keep serving EU customers after the transitional period. The deadline was paired with expectations for what unauthorized providers must do next.

Cointelegraph previously reported on the July 1 transition ending, citing ESMA’s view that service providers still not authorized by then must take “immediate” steps to wind down their EU activities. That regulatory posture matters for Szego’s concern because wind-down periods can produce concentrated customer actions—such as withdrawals—that may test operational readiness.

In other words, even if the licensing rule is clear on paper, the market’s adjustment phase can create real-world friction points that AMLA intends to monitor closely.

What AMLA plans to publish—and what to watch next

AMLA chair Bruna Szego said the authority will publish a report before the end of the year covering money laundering risks in the crypto sector and describing supervisory practices across the EU. She added that AMLA is expanding blockchain analytics capabilities to improve its ability to oversee crypto-asset service providers.

The report is also expected to assess how national authorities supervise crypto-asset service providers and highlight differences in supervisory approaches across member states. For market participants, this matters because uneven enforcement can translate into uneven compliance expectations and timelines—particularly during periods of rapid migration and customer churn.

Szego indicated AMLA intends to use the findings to coordinate follow-up work with national regulators where needed, aiming for more consistent anti-money laundering oversight throughout the bloc.

For investors, traders, and users, the main question for the coming months is whether licensed platforms can maintain strong onboarding and monitoring standards as they absorb new customers—and whether winding-down firms can handle withdrawal waves without compliance controls becoming secondary. AMLA’s year-end assessment and its growing analytics focus will likely determine how regulators refine expectations for the post-transition phase.

Welcome to The Protocol, CoinDesk’s tech newsletter covering the most important stories in blockchain. I’m Margaux Nijkerk, a reporter at CoinDesk.

We’re giving you a deeper look at the biggest trends, breakthroughs and debates shaping blockchain technology each week.

This week, we’re unpacking the timeline of all the changes at the Ethereum Foundation since the year began.

Crypto World

Open USD poses new threat to Circle by challenging USDC’s core business model, CoinShares says

USDC’s circulating supply has fallen to about $73 billion from nearly $80 billion in March, trimming its share of the roughly $312 billion stablecoin market as competition from newly regulated issuers intensifies.

Circle shares fell more than 17% on the day Open USD was announced, though CoinShares said the decline was likely amplified by technical selling linked to the Russell index reconstitution.

Still, the report argued the market may be overreacting. Open USD has yet to launch, important details remain unresolved and Circle retains a significant advantage through USDC’s deep liquidity and years of integrations across exchanges, DeFi and payments.

Open USD is unlikely to pose a major threat to Tether, whose dominance in emerging markets and offshore dollar liquidity gives USDT, the largest stablecoin by far, a different competitive moat, the report added.

For now, investors should watch whether Circle changes its distribution strategy and whether Open USD can convert its high-profile backing into adoption, CoinShares said. Until then, the project remains a credible, but unproven, challenge to USDC.

CoinShares is not alone in noting the challenge posed by Open USD. Japanese investment bank Mizuho downgraded Circle to underperform from neutral and slashed its price target to $50 from $85 in a note to clients on Tuesday, arguing that the new rival’s business model threatens the stablecoin issuer’s long-term economics.

Protesters confront NatureScot at biodiversity conference over guga hunt licence

Wayne Rooney’s cheating scandals, arrest at US airport and huge BBC salary

Ada Kejutan Keuangan Untukmu

-

Fashion6 days ago

Fashion6 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports5 days ago

Sports5 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Politics3 hours ago

Politics3 hours agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

News Videos19 hours ago

News Videos19 hours agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech1 day ago

Tech1 day agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech19 hours ago

Tech19 hours agoDark Secrets Emerge When Jailbreaking LLMs

-

News Videos7 days ago

News Videos7 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

NewsBeat6 days ago

NewsBeat6 days agoMajor update after Huntingdon train attack as man enters plea

-

Tech6 days ago

Tech6 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Tech2 days ago

Tech2 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Tech7 days ago

Tech7 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Crypto World7 days ago

Crypto World7 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

Crypto World6 days ago

Crypto World6 days agoMark Cuban-Backed DeFi Dashboard Zapper Shuts Down After 7 Years

-

Tech6 days ago

Tech6 days agoClaude’s New Reflect Dashboard Wants To Help You Log Off Of Claude

-

Crypto World7 days ago

Crypto World7 days agoFed minutes June 2026: officials split on rates

-

Entertainment2 days ago

Entertainment2 days agoKathryn Newton and Lana Condor Are Caught in the Maw of Prime Video’s Chilling Survival Thriller in New Look [Exclusive]

You must be logged in to post a comment Login