Crypto World

SEC Regulation Crypto: $75m exemption explained

While Washington’s attention fixes on whether the CLARITY Act can find seven Democratic votes before the August recess, the Securities and Exchange Commission has been quietly assembling the framework that governs American crypto if the bill dies, and much of it even if the bill passes.

Summary

- Regulation Crypto would create a four-year startup exemption for crypto projects raising up to 5 million dollars per year.

- A separate fundraising exemption would let more mature issuers raise up to 75 million dollars annually with lighter disclosure than full registration.

- The safe harbor would give tokens a defined path out of securities classification once issuer-led managerial efforts permanently end.

- The rule could operate alongside the CLARITY Act, but if the bill fails, it may become the main US crypto capital-formation framework.

- The biggest fights ahead are over dollar thresholds, decentralization standards, investor protections, and litigation risk.

On July 7, the agency confirmed plans to formally propose Regulation Crypto, its first major crypto-specific rulemaking under Chair Paul Atkins. The proposal, expected to run past 400 pages, sits under review at the White House Office of Information and Regulatory Affairs, the final gate before publication for public comment, and Atkins has said release is expected shortly after that review completes.

The package does three concrete things. It gives new crypto projects a startup exemption from full securities registration for up to four years while they build toward network maturity, raising up to 5 million dollars annually against whitepaper-style disclosures. It creates a fundraising exemption allowing more mature issuers to raise up to 75 million dollars in any 12-month period with audited financials and semiannual reporting, a burden far lighter than full registration. And it writes an investment contract safe harbor: a rules-based path for a token to exit securities classification entirely once its issuer has permanently ceased the essential managerial efforts that made it an investment contract in the first place.

Atkins has repeatedly described the framework as a bridge to the CLARITY Act. The description is honest and incomplete at the same time. A bridge implies something temporary that the statute replaces; in reality, Regulation Crypto answers questions the bill does not reach, will operate for years regardless of the Senate outcome, and, if the bill fails, becomes the entire de facto constitution of American crypto capital formation. This feature decodes what the rule actually does, where it came from, why Senate Democrats consider it an end-run, and what it means for the market that one of these two frameworks is arriving no matter what happens in the next three weeks.

The taxonomy underneath: five buckets instead of one question

Regulation Crypto did not appear from nothing. Its foundation is a joint SEC and Commodity Futures Trading Commission interpretive release from March 17, 2026, which replaced the enforcement era’s single endless question, is this token a security, with a working taxonomy of five categories: digital commodities, digital collectibles, digital tools, stablecoins, and digital securities. Under the interpretation, only digital securities, tokenized versions of traditional financial instruments, remain fully subject to the securities laws. The other categories may still trigger securities obligations if sold as part of an investment contract, which is where the Howey analysis survives, but the default presumption flipped: most tokens are not securities by nature, and the legal question becomes how they were sold, not what they are.

Atkins introduced the exemption framework the same day, in a speech at the DC Blockchain Summit titled Regulation Crypto Assets: A Token Safe Harbor, and the agency submitted the proposed rules to the White House within the week. The sequencing matters for understanding what kind of project this is. The interpretive release stated how the agency reads existing law; interpretations bind nobody and evaporate with the next chair. The proposed rule converts the reading into formal regulation, with notice, comment, and the full Administrative Procedure Act process, which makes it dramatically harder to unwind. The past year’s accommodations, staff guidance, no-action letters, dropped enforcement actions, carry no binding force at all; a future commission could reverse them by memo. A finalized Regulation Crypto could only be undone by a new rulemaking that survives its own comment period and litigation. Durability is the entire point, and durability is exactly what the industry has said it needs.

The chair’s broader agenda frames the rule as one panel of a triptych. Atkins has described crypto market structure, custody, and capital formation as the agency’s three crypto priorities, with the stated goal of making the United States the leading crypto capital. He has asked staff to evaluate letting non-security crypto assets that were sold under investment contracts trade on venues not registered with the Commission, to clear paths for state-licensed platforms to list such assets, and to let CFTC-regulated platforms offer them with margin. He also shut down the agency’s crypto innovation hub, arguing the Gensler-era version was so tainted that industry participants feared subpoenas after visiting, a symbolic demolition that tells its own story about how completely the agency’s posture has inverted.

The three exemptions, decoded

The startup exemption is the on-ramp. A new project receives up to four years of relief from full registration while it develops its network, during which it can raise up to 5 million dollars per year. The disclosure standard is principles-based and deliberately modeled on what serious projects already publish: whitepaper-style documentation of the technology, the token economics, and the team, plus required financial statements to investors. The four-year clock is the regulatory embodiment of an idea the industry has argued since 2018, that decentralization takes time, and that forcing registration at launch, when a network is inescapably centralized, guarantees either noncompliance or offshoring. The exemption’s wager is that a project given four lawful years will either mature into something the safe harbor releases or grow into something the fundraising tier can carry.

The fundraising exemption is the growth pathway, and its design is more conservative than the headline suggests. The 75 million dollar annual cap is borrowed directly from Regulation A+, the existing exemption for smaller public offerings by conventional issuers; Atkins adapted a tested framework instead of inventing one. The obligations scale accordingly: audited financial statements and ongoing semiannual reporting, meaningfully heavier than the startup tier’s whitepaper standard, meaningfully lighter than a full registration. For the mid-sized token issuer, the practical effect is a lawful domestic alternative to the offshore foundation structures that became the industry’s default architecture, with a compliance bill measured in hundreds of thousands of dollars instead of tens of millions.

The investment contract safe harbor is the philosophical core and the piece with no statutory parallel. It answers the question the Torres ruling in the Ripple case raised but could not settle: when does a token that was sold as a security stop being one? The safe harbor’s answer is a rule-based test keyed to managerial effort. Once an issuer has permanently ceased the essential managerial functions that investors relied on, the token exits securities classification, full stop. That converts decentralization from a rhetorical claim into a compliance milestone with legal consequences, and it gives every project in the startup tier a defined destination. It is also, not coincidentally, the provision that most directly generalizes the industry’s hardest-won litigation outcomes into standing law, the same conceptual territory Ripple spent 150 million dollars mapping, as the token-versus-sale distinction moved from courtroom argument to regulatory architecture.

The objection: an agency legislating around the legislature

Senate Democrats have noticed that the SEC is building, by rule, much of what Congress has not agreed to build by statute, and their objection deserves a full hearing because it is not frivolous.

Elizabeth Warren and Chris Van Hollen wrote to Atkins directly, charging that the agency plans to exempt most cryptocurrencies from the securities laws with significant potential harm to investors, and calling on Congress to close the loopholes as it considers market structure legislation. Financial industry commenters have warned that broad exemptive relief could import cybersecurity risks, illicit-finance exposure, and flash-crash volatility into markets stripped of their traditional guardrails. The constitutional-order version of the critique is sharper still: an agency whose chair previously advised crypto firms is using administrative discretion to deliver, in advance, the deregulatory half of a bill the elected branch has not passed, while the accountability provisions Democrats attached to that bill, the ethics rules aimed at the president’s 2.3 billion dollars in crypto exposure, have no administrative equivalent and can only exist in statute. Regulation Crypto, on this reading, is not a bridge to CLARITY. It is a mechanism for harvesting CLARITY’s benefits without paying CLARITY’s political price, and every week it advances reduces the industry’s urgency to compromise on the ethics language currently blocking the bill, a standoff crypto.news has followed into its decisive month.

The rebuttal has two layers. Legally, exemptive authority is not a loophole; Congress wrote it into the securities laws deliberately, and Regulation A+, Regulation D, and Regulation Crowdfunding are all products of the same power. An agency tailoring registration requirements to a novel asset class through notice-and-comment rulemaking is the administrative state working as designed, and the courts, not letters, will test whether this rule exceeds the statute. Practically, the alternative to Regulation Crypto is not the status quo Democrats prefer; it is the pre-2025 regime of regulation by enforcement that a federal judge partially repudiated and that nearly dissolved companies later vindicated. Between an imperfect rule with a comment period and an enforcement lottery with none, the rule is the more accountable instrument, whatever one thinks of its content.

What both sides quietly agree on is the stakes of reversibility. Democrats want the ethics and consumer provisions in statute because statutes bind future administrations; the industry wants the exemptions in a finalized rule for precisely the same reason. The entire fight, in Congress and at the agency simultaneously, is about who gets to make their preferences durable first.

How the agency got here: from Hinman speech to Howey off-ramp

The rule reads differently with a decade of institutional history attached, because every one of its provisions answers a specific wound.

The startup exemption answers the original sin of the ICO era. In 2017 and 2018, hundreds of projects raised capital from Americans with no disclosure standard at all, the agency responded with a wave of enforcement that treated every token sale as an unregistered offering, and the surviving industry drew the obvious lesson: incorporate in Zug, exclude Americans, and disclose nothing. The exemption’s whitepaper-based standard is a wager that a lawful middle existed all along, and that the agency’s refusal to build it, not the industry’s refusal to use it, drove a decade of capital formation offshore.

The safe harbor answers the Hinman problem. In 2018, a senior SEC official famously suggested in a speech that Ether, whatever its origins, had become sufficiently decentralized that its sales were no longer securities transactions. The industry spent years trying to hold the agency to that logic, the agency spent years insisting the speech was one man’s opinion, and the internal documents Coinbase later pried loose in litigation showed officials themselves could not agree on what the standard was. Commissioner Hester Peirce proposed a formal token safe harbor twice, in 2020 and 2021, and was ignored by her own agency both times. The current safe harbor is Peirce’s idea with Atkins’ signature, arriving seven years after the speech that made everyone realize the question had no answer.

And the fundraising tier answers the enforcement era’s quietest casualty: the mid-sized compliant issuer that never existed because there was no rule to comply with. Between the 5 million dollar seed rounds that Regulation D could awkwardly cover and the public listings that only exchanges and miners attempted, an entire capitalization band of the industry simply had no American on-ramp. Borrowing Regulation A+’s 75 million dollar ceiling is the agency conceding that the band was a regulatory artifact, not a market verdict.

The arc from Gensler to Atkins, from an agency that sued first and declined to write rules even under court order, to an agency proposing 400 pages of them, is the sharpest institutional reversal in modern financial regulation, and it happened without a single statute changing. That fact is the strongest argument for the rule and the strongest argument against relying on it, at the same time.

What can still change: the comment period is not a formality

Between OIRA clearance and a final rule stand months of process in which the package’s most important parameters remain genuinely contestable, and market participants pricing the framework as finished are early.

The dollar thresholds are the obvious pressure point. Consumer advocates and Senate Democrats will push the 75 million dollar ceiling down and load the startup tier with conditions; industry commenters will push for inflation indexing and aggregate-cap clarity, since the current design names annual limits without a publicly specified lifetime ceiling. The decentralization test inside the safe harbor is the subtle one. Permanently ceased essential managerial efforts is a phrase that will absorb tens of thousands of comment pages, because it decides whether the off-ramp is a real destination or a mirage: too strict, and no foundation-supported network ever qualifies; too loose, and every project theatrically dissolves its team on paper while running development through affiliates. The illicit-finance overlay is the political one. The same law enforcement coalition currently fighting the CLARITY Act’s developer protections, a split crypto.news dissected as the Senate vote approached, will demand that exempted issuers carry monitoring obligations the statute never imposed, and the agency’s answer will determine whether the exemptions are usable by actually decentralized projects or only by companies that look like broker-dealers with extra steps.

Litigation risk frames all of it. A finalized rule this consequential draws challenges from both flanks: investor-protection groups arguing the agency exceeded its exemptive authority by hollowing out registration, and, conceivably, industry plaintiffs attacking whatever conditions survive comment. Post-Chevron, courts owe the agency’s statutory reading no deference, and a single adverse circuit decision could stay the framework for years. This is the structural reason Atkins keeps calling the rule a bridge and pressing Congress to act anyway: he is building the most durable thing an agency can build while publicly acknowledging it is the second-most durable thing available.

Regulation Crypto versus the CLARITY Act: substitutes, complements, or race

Mapping the two frameworks against each other shows they overlap less than the political rhetoric implies, which is why the with-or-without framing in this feature’s title is literal.

The CLARITY Act’s center of gravity is market structure: which agency supervises trading, how exchanges and brokers register, how the CFTC gains spot authority over digital commodities, how developers escape money transmitter liability. Regulation Crypto’s center of gravity is capital formation: how tokens are launched, funded, and eventually released from securities status. The bill barely touches primary issuance mechanics; the rule barely touches secondary market supervision. A world with both is coherent: CLARITY sorts the assets and assigns the regulators, Regulation Crypto governs how new assets are born. Atkins’ bridge metaphor undersells his own product; the honest description is that the rule is the bill’s missing chapter, written by the agency because the legislature never drafted one.

The substitution effect appears only in the failure scenario, and there it is nearly total. If the Senate misses the August window and the 2030 warnings prove accurate, Regulation Crypto plus the March taxonomy plus the CFTC’s stretched existing authority become the entire American framework: token launches under the exemptions, classifications under the five buckets, trading under a patchwork the rule’s platform provisions try to rationalize. That regime would function, and its existence is precisely what Galaxy Research and others cite when they note that CLARITY’s failure would be a slow bleed rather than a catastrophe. But it would be a framework resting on one commission’s rulemaking, contestable in court, reversible by a hostile successor with patience, and silent on everything from illicit finance funding to the ethics questions that stalled the bill. The GENIUS Act fight already previewed what statute-versus-regulator arguments look like when real money is at stake, with state and federal authorities wrestling over stablecoin turf in a battle crypto.news covered throughout its Senate run, and the yield wars that followed passage show how much conflict survives even a signed law, a standoff crypto.news has tracked between banks and issuers over 6 trillion dollars in deposits.

There is also a timing race with the bill’s own politics. The rule’s OIRA review and comment period run on an administrative calendar indifferent to the Senate’s. If the merged CLARITY draft stalls on ethics while Regulation Crypto publishes for comment, the industry’s cost of legislative failure drops in real time, which weakens the coalition pressing moderate Democrats and strengthens the members arguing the bill can wait. Agency action meant as a bridge can function as an off-ramp. The three weeks in which both instruments reach their decisive stages, the merged bill text and the published rule, will reveal which metaphor the market believes.

What it means for issuers, and the European mirror

Before the issuer decision tree, the market implications deserve a paragraph of their own, because the rule reprices assets that already exist, not just launches that have not happened. Tokens whose largest discount is classification ambiguity, the mid-cap layer ones, the DeFi governance assets, the infrastructure tokens that trade below comparable revenue because American institutions cannot categorize them, gain a defined path to non-security status through the safe harbor even if the CLARITY Act never assigns them a commodity label. Exchange listing committees, which spent the enforcement era rationing US availability by litigation risk, get a compliance framework to point to. And the venture pipeline reopens domestically: funds that structured around offshore token warrants for a decade can underwrite American issuance with actual rules attached, which changes where the next cycle’s projects incorporate, hire, and pay taxes. None of this requires the rule to be generous. It requires the rule to exist, because the binding constraint was never severity. It was undefined risk, the one input no allocation committee can price.

For anyone actually launching a token, the practical decision tree changes shape the moment the rule publishes. A credible path now exists to raise seed capital domestically under the startup tier, scale through the 75 million dollar pathway with audit-grade disclosure, and target the safe harbor as the legal finish line where the token sheds its securities character by verifiable decentralization. The offshore foundation, the airdrop-to-avoid-sale contortions, and the deliberate exclusion of American buyers, the entire defensive architecture of the past eight years, become choices rather than necessities. The projects most affected are the serious middle: too big for a fair launch to fund, too small to carry registration costs, which describes most of the infrastructure layer the industry claims to want.

The comparison that will define the rule’s success is the one across the Atlantic. Europe’s MiCA regime just completed its transition, locking unlicensed firms out of a 30-country market and elevating the licensed few, a sorting crypto.news documented as the deadline hit. MiCA’s strength is comprehensiveness backed by statute; its weakness is rigidity, a stablecoin regime severe enough to expel the largest issuer on earth. Regulation Crypto inverts the trade: flexible, innovation-forward, and administratively fast, but resting on agency authority in a country where agencies change hands every four years. An American founder in 2026 chooses between a European rulebook that cannot easily be improved and an American one that cannot easily be trusted. The CLARITY Act is, among everything else, an attempt to give the American framework the one property it lacks, and the rule arriving with or without it is both the industry’s insurance policy and the bill’s quiet competitor.

The decode, compressed: Regulation Crypto is the most consequential piece of American crypto policy that almost nobody outside Washington is reading, precisely because it advances on the boring calendar of administrative law while the Senate supplies the drama. Four-year runways, 75 million dollar raises, and a legal exit from securities status are arriving through the Federal Register, on a timeline no filibuster can touch and no recess interrupts. The comment period will bend the parameters, the courts may test the boundaries, and a future commission could someday attempt the long unwind. What no plausible scenario now delivers is a return to the world where the only American rulebook was a lawsuit. The only question the Senate’s three weeks will answer is whether the new rulebook arrives as a chapter of a statute or as the whole book.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

SpaceX stock is attempting to stabilize near $110 ahead of its first post-IPO earnings report, but a $100 billion share unlock could limit any recovery.

Summary

- SPCX has fallen 52% from its June intraday peak of $225.64.

- Analysts expect $6.88 billion in revenue and a loss of $0.23 per share.

- The 4-hour chart shows improving momentum after SPCX exited a descending channel.

- Up to 911.5 million shares become eligible for sale on Aug. 6.

- A recovery requires SPCX to reclaim $120, followed by the $130 resistance area.

SpaceX will report its second-quarter results after the US market closes on Aug. 4, giving investors their first detailed look at the company since its June initial public offering.

The report arrives at a difficult point for SPCX stock. Shares recently traded at $110.41, down about 18% from their $135 IPO price and roughly 52% below the June intraday high of $225.64.

That decline has reduced some of the valuation premium created by the IPO’s limited float. However, the company is still valued at roughly 35 to 37 times projected 2026 revenue, leaving little room for weak results or cautious guidance.

SpaceX earnings face unusually high expectations

Wall Street expects SpaceX to report approximately $6.88 billion in second-quarter revenue, according to FactSet data. Analysts forecast a loss of $0.23 per share and adjusted earnings before interest, taxes, depreciation and amortization of about $2.1 billion.

Full-year expectations stand near $39 billion in revenue and $17.3 billion in EBITDA.

These estimates place considerable pressure on SpaceX’s three main businesses: Starlink, rocket launches and artificial intelligence. Investors will assess whether revenue growth from Starlink and launch contracts can support the company’s spending on Starship, satellites and AI infrastructure.

Cantor Fitzgerald analyst Colin Canfield has warned that the first report could contain an “extreme expectation bias,” reflecting the potential gap between Wall Street forecasts and SpaceX’s actual performance.

Starlink is likely to receive the most attention because its recurring subscription revenue could help offset the more volatile economics of rocket development. Analysts expect the connectivity segment to remain SpaceX’s largest revenue source, supported by more than 10 million users.

The launch business also enters earnings with a substantial order pipeline. SpaceX recently secured a $1.6 billion US Space Force contract covering 18 Falcon 9 launches through 2027, adding visibility to its government-related revenue.

AI presents a less certain outlook. Investors will want details on spending, revenue and expected returns following SpaceX’s expansion into AI infrastructure. High capital expenditure without a clear path to positive free cash flow could renew concerns about the company’s valuation.

SPCX stock shows early signs of stabilization

The 4-hour chart shows SPCX stock moving out of a descending channel that guided prices lower throughout July. Shares recently rebounded from an intraday low of $104.85 and reached $112.70 before settling near $110.41.

That breakout suggests the decline may be losing momentum. However, it does not yet confirm a wider trend reversal because the stock remains close to its record low and well below several former support levels.

The Moving Average Convergence Divergence indicator has produced an early bullish crossover. The MACD line stood at minus 6.99, above its signal line at minus 7.80, while the histogram turned positive at 0.81.

Because both lines remain below zero, the signal points to improving short-term momentum rather than an established bullish trend.

The Average Directional Index stood at 32.82. An ADX reading above 25 normally indicates a relatively strong trend, but the indicator does not determine its direction. In this case, it primarily confirms the strength of the decline that preceded the latest stabilization attempt.

A strong earnings report could provide the catalyst needed to validate the channel breakout. Weak results, however, could turn the move into a temporary pause within the larger downtrend.

SPCX needs to reclaim $120 to extend its recovery

Immediate resistance sits between $112.70 and $115, an area that has repeatedly limited rebounds since late July. A 4-hour close above that zone could allow SPCX to test $120.

The $120 level previously acted as short-term support before the latest breakdown. Reclaiming it would improve the technical structure and could expose the stock to resistance between $127 and $130, near the upper boundary of the former descending channel.

A move above $130 would offer stronger evidence that SPCX has formed a short-term bottom. The next major resistance area would then sit between $140 and $150, where sellers controlled several July rebounds.

On the downside, $104.85 is the first support level. A break below that intraday low would place the psychological $100 mark at risk.

Falling below $100 after earnings would invalidate the latest channel breakout and leave SPCX without a clear historical support level because the stock has traded publicly for less than two months. That lack of price history could increase volatility as investors search for a new valuation floor.

The Aug. 6 unlock could limit an earnings rally

Even an earnings beat may not remove the stock’s most immediate supply risk.

Up to 911.5 million shares held by employees and some early investors become eligible for sale on Aug. 6, the second trading day after the earnings release. At $110.41 per share, the tranche is worth about $100.6 billion.

The release exceeds the approximately 639 million shares initially available for public trading. If every eligible share entered the market, the tradable supply would rise to roughly 1.55 billion shares. Eligibility does not mean holders must sell, but the size of the tranche creates the potential for considerable selling pressure.

A second tranche of 455.8 million shares could have qualified for early release if SPCX closed at or above $175.50 on at least five of the 10 trading days through earnings. The stock’s decline means that condition will not be met.

SpaceX’s staggered lock-up structure will release additional shares over the coming months. By Dec. 8, the number of potentially tradable shares could reach approximately 5.33 billion, compared with fewer than 640 million following the IPO. Elon Musk’s holdings remain subject to a longer restriction extending into mid-2027.

Can SpaceX earnings revive SPCX stock?

The bullish scenario requires SpaceX to beat revenue expectations, demonstrate strong Starlink margins and give investors a credible plan for funding AI and Starship investments. Those results could push SPCX through $115 and toward $120 or $130.

The bearish case centers on continued losses, elevated capital spending and weak guidance. Those concerns would become more damaging when combined with the Aug. 6 unlock, particularly if employees and early investors use the earnings window to sell.

SPCX’s improving MACD and channel breakout provide an early technical basis for a rebound. Still, the stock must reclaim $120 before the move can be treated as more than a relief rally.

Earnings could revive SPCX in the short term, but holding those gains may prove harder. The company must satisfy high operating expectations just two days before its available share supply begins to expand.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

The odds of the Digital Asset Market Clarity Act’s (CLARITY) passage are dwindling as the US Senate is scheduled to begin summer recess at the end of this week, threatening another leg down for cryptocurrency valuations, according to wealth manager Bernstein.

Bernstein said that the Senate’s failure to pass the legislation could trigger an immediate negative “industry knee-jerk reaction,” which may result in another leg down for Bitcoin and the broader crypto market.

“From a tactical standpoint, we expect the crypto market to bottom and start showing momentum towards late Q3 and early Q4 prior to the mid-terms,” Bernstein analysts wrote in a Monday report shared with Cointelegraph.

At the same time, however, the analysts said that Senate failure to pass the legislation may bring more proactive policy support from regulators, including the Commodity Futures Trading Commission (CFTC) and the Securities and Exchange Commission (SEC), which may accelerate rulemaking initiatives under Project Crypto.

Project Crypto is a regulatory initiative first announced by SEC Chairman Paul Atkins in July 2025, which was later expanded into a joint staff initiative between the SEC and CFTC in September 2025. The initiative aims to create a workable regulatory framework for digital assets using existing agency authority while Congress finalizes crypto market legislation under the CLARITY Act.

Bernstein said that the two agencies could provide more interpretive releases tied to the taxonomy of tokens, clear rules around decentralized finance (DeFi) and accelerate the innovation exemption for issuing tokens that would be exempted from securities status during a finite period.

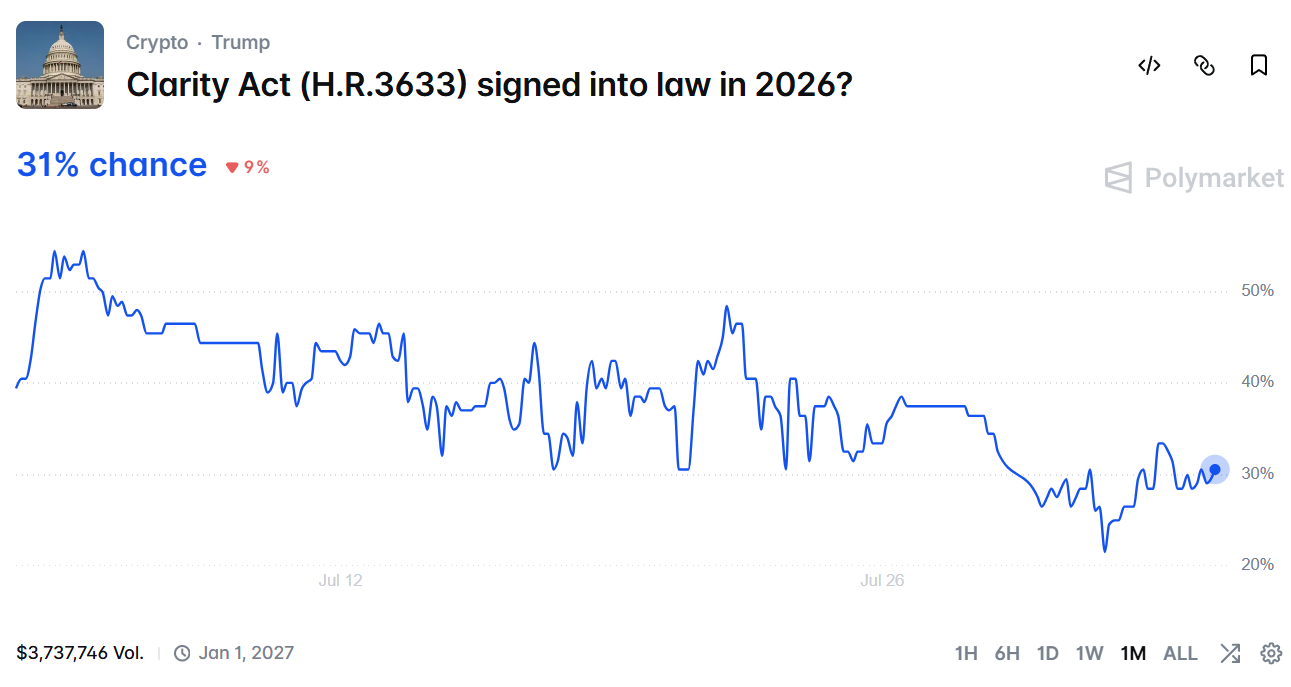

CLARITY Act odds decline to 31%

Bernstein’s skepticism is supported by prediction market traders who are betting against the passage of the CLARITY Act before the end of 2026.

Odds of the legislation’s passage before the end of the year are now at 31%, down 7% in the past week and down 9% in the past month, according to Polymarket, which shows about $3.7 million has been wagered on that prediction.

Prediction market odds of the CLARITY Act being signed into law by the end of 2026. Source: Polymarket

Meanwhile, White House officials are reportedly weighing a bipartisan ethics counterproposal received on Thursday, following weeks of negotiations between Republican Senator Thom Tillis and Arizona Democrat Ruben Gallego.

The proposal would enable state attorneys general to sue the Department of Justice if it fails to enforce ethics laws against federal officials, three sources familiar with the matter told crypto journalist Eleanor Terrett.

Related: ABA, state banking groups push back on CLARITY Act stablecoin yield provisions

The CLARITY Act aims to establish the first regulatory framework for digital assets in the US, but it has been met with pushback from the banking industry, which argued that the current draft would allow crypto firms to offer yields on stablecoins without facing the same requirements as traditional financial institutions.

On June 26, Galaxy Digital cut its odds of the CLARITY Act becoming law in 2026 to 50%, warning that the US Senate is running out of time to move the crypto market structure bill before its August recess.

Magazine: How the EU’s crypto tax rules are expected to work for users and platforms

BlackRock has launched two tokenized money market products as the world’s largest asset manager expands its blockchain-based cash management and real-world asset strategy.

Summary

- BSTBL will issue tokenized shares on Ethereum that approved investors can transfer between compliant wallets.

- BRSRV will support multiple blockchains and automatically reinvest dividends each day.

- Both products will hold cash, short-term U.S. Treasuries and Treasury-backed overnight repurchase agreements.

- BlackRock’s cash management group oversees nearly $1.1 trillion across its broader liquidity strategies.

BlackRock launches BSTBL shares on Ethereum

The BlackRock Select Treasury Based Liquidity Fund, or BSTBL, will introduce tokenized shares of an existing money market fund on Ethereum.

Institutional investors will be able to move the shares between approved wallets, subject to regulatory and compliance requirements. This structure brings transferability onto a public blockchain while retaining controls commonly applied to regulated financial products.

BNY Mellon will serve as BSTBL’s transfer agent and tokenization service provider. Its role will connect the fund’s shareholder records and transaction processes with the infrastructure used to issue and transfer the on-chain shares.

BSTBL will invest in cash, short-term U.S. Treasury securities, and overnight repurchase agreements backed by Treasuries. The portfolio aims to preserve principal and liquidity while generating returns from short-duration government debt.

The model differs from a stablecoin because investors hold fund shares rather than tokens designed to maintain a fixed redemption value. Returns will depend on the income generated by the underlying portfolio.

BRSRV targets stablecoin reserve management

BlackRock’s second product, the BlackRock Daily Reinvestment Stablecoin Reserve Vehicle, or BRSRV, is designed for digitally native institutional investors.

Unlike BSTBL’s initial Ethereum-based structure, BRSRV will support access across multiple blockchains. The fund will also reinvest dividends daily, allowing income generated by its assets to remain within the product.

BlackRock said BRSRV could be used in several digital-asset settings, including stablecoin reserve management. Stablecoin issuers typically need liquid, low-risk assets to support redemptions, making Treasury bills and Treasury-backed repurchase agreements common reserve instruments.

Securitize will act as the fund’s transfer agent and tokenization service provider. The company already supplies infrastructure for tokenized securities and previously worked with BlackRock on its blockchain-based investment products.

BRSRV will use the same core asset categories as BSTBL: cash, short-term U.S. government debt and overnight repurchase agreements collateralized by Treasuries.

BlackRock expands its role in tokenized U.S. markets

The two launches extend BlackRock’s involvement in real-world asset tokenization beyond individual blockchain products.

crypto.news reported in July that BlackRock joined a Depository Trust & Clearing Corporation pilot testing tokenized stocks and U.S. Treasuries. The initiative involves securities already held within DTCC’s custody framework, which safeguards about $114 trillion in assets.

JPMorgan, Goldman Sachs, Vanguard, the New York Stock Exchange and nearly 40 other financial firms are also participating. The pilot lets institutions test blockchain-based representations of traditional securities without moving the underlying assets outside established market infrastructure.

For U.S. institutions, that model may reduce the operational gap between conventional securities and on-chain markets. However, wallet transfers, investor eligibility and access will remain subject to regulatory requirements rather than operating as permissionless crypto transactions.

BlackRock’s cash management group now oversees close to $1.1 trillion for corporations, banks, insurers, foundations and public institutions. Its scale could help introduce tokenized fund shares to investors already using its traditional liquidity products.

BlackRock builds across crypto and traditional finance

BlackRock has also expanded its position in regulated cryptocurrency markets through the iShares Bitcoin Trust, its U.S. spot Bitcoin exchange-traded fund.

As previously reported by crypto.news, the U.S. Securities and Exchange Commission approved an increase in the position limit for options tied to the fund. The limit rose fourfold from 250,000 to 1 million contracts, giving eligible traders room to hold larger options positions linked to IBIT.

The tokenized fund launches represent a separate part of BlackRock’s digital-asset strategy. Rather than providing Bitcoin exposure, BSTBL and BRSRV place traditional cash-management assets on blockchain infrastructure.

Their adoption will depend on institutional demand, regulatory access, and whether on-chain transfers provide meaningful operational advantages over existing money market fund systems.

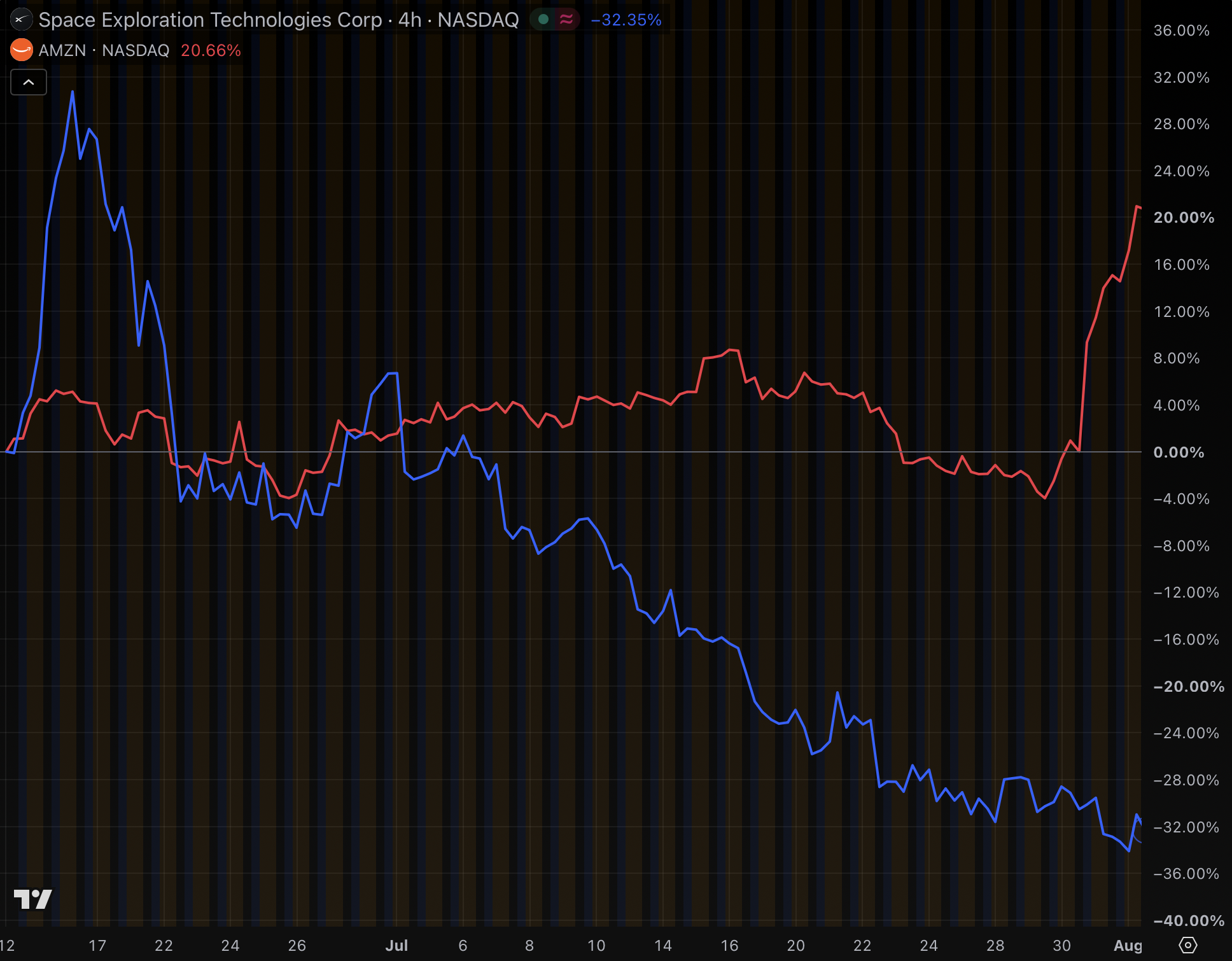

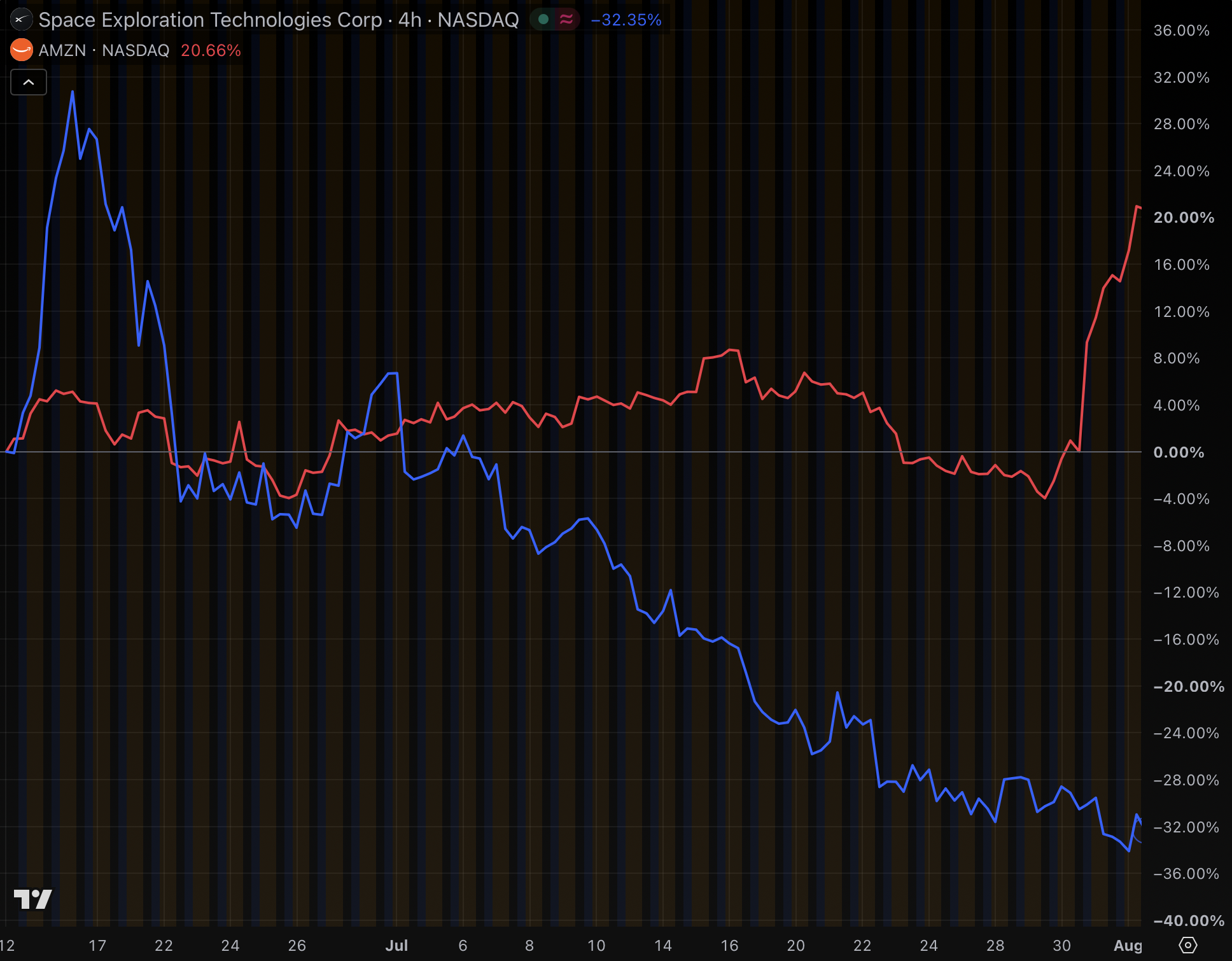

In less than six weeks, Amazon has gained almost as much market capitalization as SpaceX has lost. Since June 26, both companies have swapped precisely $560 billion in market cap.

Believe it or not, as recently as June 16, both companies had the same valuation, each being a $2.65 trillion company.

Since then, however, their valuations have trended in opposite directions.

Shares of Amazon climbed above $284 today, carrying the online retailer’s market value past $3 trillion for the first time. Only four publicly traded companies had ever reached that mark before.

Elon Musk’s rocket, internet, and AI conglomerate SpaceX had a great start after its IPO, running above $2.9 trillion within three days and briefly eclipsing the value of Amazon for one glorious week.

Stock in SpaceX then crashed, crashed, and crashed some more. Over the past month, the stock has lost 32% of its value.

Today, Amazon’s $3.06 trillion market cap is more than twice as valuable as SpaceX’s $1.44 trillion.

A good earnings report from Amazon

Last week, Amazon reported second quarter net sales of $200 billion and operating income up an impressive 43%, largely due to tariff refund checks and an increase in its Anthropic investment.

Its Amazon Web Services division grew at its fastest rate in 18 quarters.

The company posted adjusted earnings of $1.97 per share that beat Wall Street’s $1.82 estimate, on impressive revenue of $200 billion versus an expected $196 billion.

Accelerating cloud-computing growth eased investors’ concerns about Amazon’s heavy AI spending, with analysts framing its AI expenditures as bets that were starting to pay off.

The stock surged 15% the day after the report and was up about 5% again on Monday, marking another record high.

CEO Andy Jassy said, “There’s a lot to be excited about, and we have much more coming for customers in the second half of the year and beyond.”

Some of that excitement came from outside the business. Roughly $53 billion of the quarter’s $62.6 billion net income arrived as non-operating gains, largely on Amazon’s stake in Anthropic.

Amazon even nudged capital spending guidance toward $220 billion, and investors were happy to oblige — bidding up its stock 22% over the past week despite its plans to spend more cash on AI.

Wall Street raised its Amazon price targets. Analysts at JPMorgan raised their price target to $365 from $330, Wells Fargo reiterated its overweight recommendation and $328 price target, and TD Cowen said buy up to $350.

Read more: Some SpaceX bonds have already sunk to junk-like territory

SpaceX reports Tuesday, more stock unlocks Thursday

All of that good news for Amazon contrasts starkly with a terrible few weeks for SpaceX, which priced shares of the largest IPO in history at $135 apiece in June.

Within three trading sessions, it touched an intraday peak near $2.95 trillion — a level it would never regain. In fact, its value has halved since that high.

By this morning, SpaceX traded down to a fresh all-time low near $105. The stock sits well below the price its own underwriters set less than two months ago.

The calendar offers no relief.

SpaceX posts its first quarterly results as a public company after the close of regular trading tomorrow. Investors are obviously not optimistic, given the poor stock performance.

Two days after earnings, a share unlock will free 911 million additional shares for sale. That will more than double the tradable float, adding sell pressure on shares already under steady pressure over the past month.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

The asset manager introduced two blockchain-based money market funds designed to qualify as stablecoin reserve assets under the US GENIUS Act.

Kenya has anchored more than 15 million academic records to the Avalanche C-Chain as it replaces slow, paper-based certificate checks with a national electronic verification system.

Summary

- Kenya has anchored over 15 million records dating to 1989 on Avalanche.

- Nearly 1 million 2025 KCSE certificates are available exclusively through the electronic platform.

- KNEC expects the system to eventually cover about 35 million verifiable records.

- The platform cuts some certificate checks from months to seconds, according to Ava Labs.

Kenya moves academic verification onto Avalanche

The Kenya National Examinations Council launched the system through a local technology provider, according to an Ava Labs announcement published on Aug. 3.

The initial rollout covers more than 15 million historical examination records dating back to 1989. It also includes certificates for nearly 1 million candidates who took the Kenya Certificate of Secondary Education examination in 2025.

Those certificates are now issued exclusively through KNEC’s electronic certificate platform. Students can access and download their credentials, while employers, universities and other institutions can verify them online.

“Candidates no longer have to rely solely on physical certificates. Instead, they can securely access, download and verify their KCSE certificates online, providing a faster, more reliable and more convenient way of managing academic credentials in the digital age,” KNEC CEO David Njengere said.

KNEC plans to expand the system to about 35 million records. Its expected scope includes primary and secondary qualifications, advanced diplomas and government teacher-training certifications.

Avalanche system targets certificate fraud

Academic verification in Kenya previously depended on manual requests, physical files and centralized databases. Ava Labs said individual checks could take a month, while large verification requests from recruiters could take up to six months.

The new platform is designed to reduce that process to seconds. Anchoring certification data on Avalanche creates a tamper-resistant reference that authorized users can check against records presented by candidates.

KNEC also aims to reduce certificate forgery and the use of fraudulent verification websites. However, the announcement did not provide detailed information about which data fields are stored directly on-chain, how personal information is protected, or the cost of operating the platform.

The rollout extends Avalanche’s use in government record systems. In the United States, California’s Department of Motor Vehicles has digitized 42 million vehicle titles using Avalanche, while Bergen County, New Jersey, is using the network in a project covering 370,000 property deeds valued at about $240 billion, according to Ava Labs.

AVAX sees no clear boost from Kenya rollout

The announcement did not produce a clear breakout in AVAX, Avalanche’s native token. crypto.news data showed the token trading near $6.54, with a market capitalization of roughly $2.82 billion.

Its 24-hour trading volume stood near $170 million, down about 35% from the previous day. That suggests the Kenya announcement had not yet generated a sustained increase in market activity.

KNEC’s platform nevertheless adds a nationwide public-sector use case to the Avalanche C-Chain. Its long-term effect will depend on whether the system reaches the planned 35 million records and continues processing new certifications at scale.

Kenya expands blockchain use amid cyber risks

The academic project arrives as Kenya develops broader oversight of digital assets. As crypto.news previously reported, the Capital Markets Authority moved in July to procure surveillance software capable of monitoring Bitcoin, Ethereum and more than 20 other blockchain networks.

The regulator wants the system to trace funds, flag suspicious wallets and identify offshore crypto platforms serving Kenyan users without authorization.

Kenya’s digital expansion also faces cybersecurity risks. Hackers temporarily defaced President William Ruto’s official website on July 18 and demanded five Bitcoin as ransom. Authorities opened an investigation, but the incident was separate from KNEC’s Avalanche deployment.

The next test will be whether KNEC can expand the certification platform while protecting student data, maintaining access and preventing the digital system from creating new points of failure.

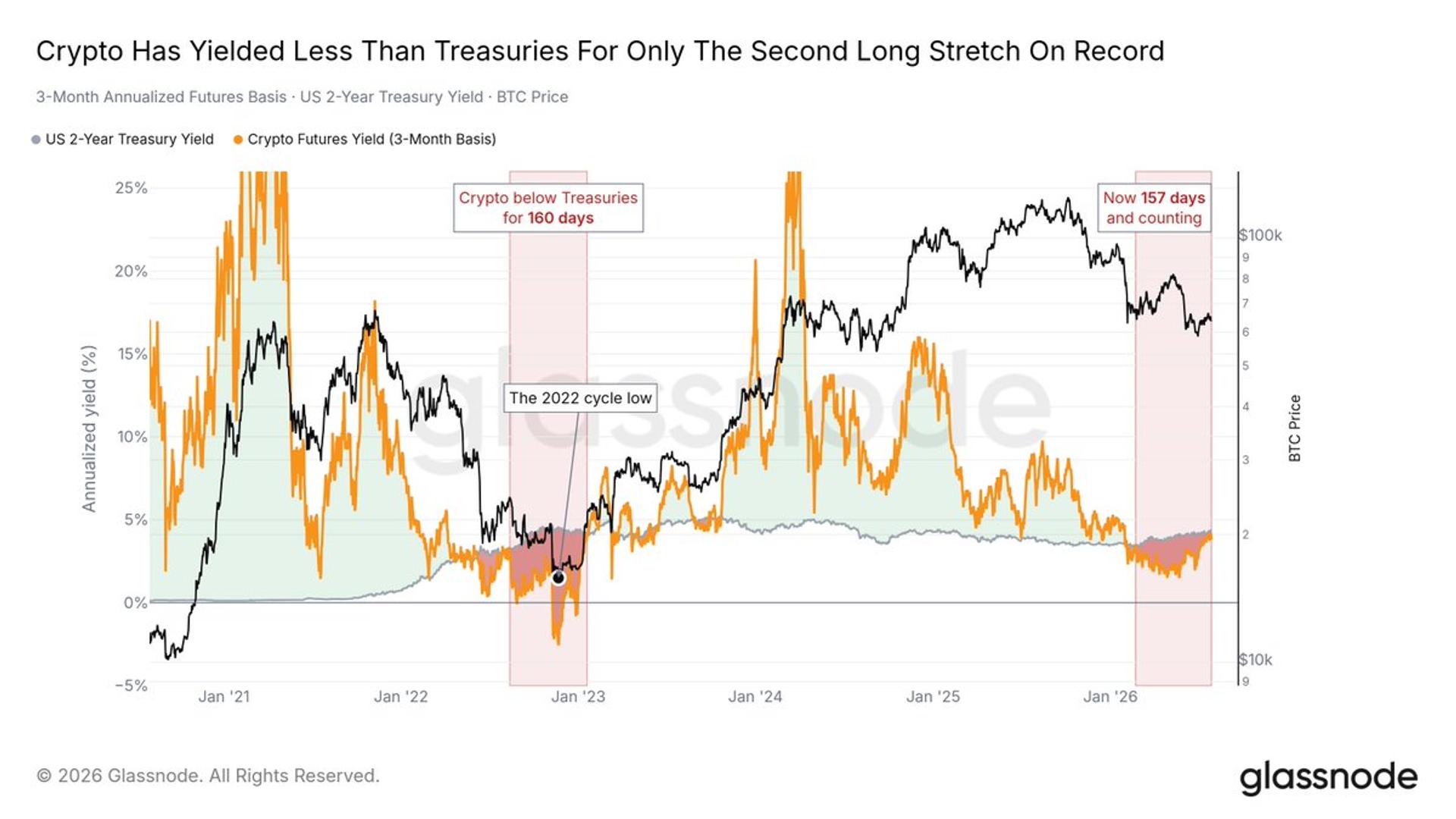

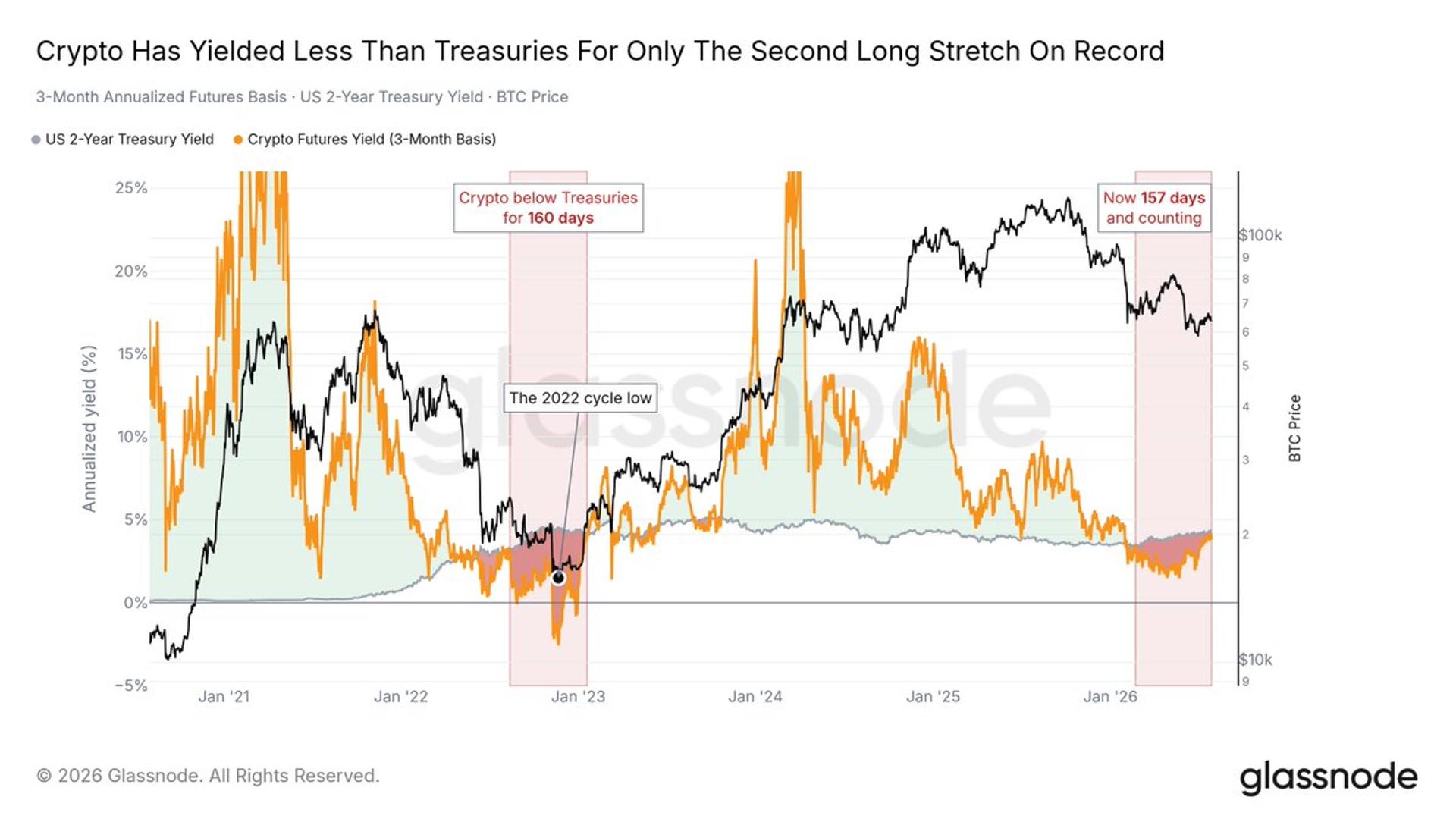

Once a goldmine for carry traders, bitcoin futures have flipped, consistently underperforming plain‑vanilla U.S. Treasuries every month since February.

Carry trades consistently yielded 20% or more across regulated and unregulated crypto exchanges during the 2021 bull market. The strategy involved shorting bitcoin futures while simultaneously buying a spot exchange-traded fund (ETF). Now they return just 3% compared with an average 3.8% yield on two-year Treasuries.

Traders have long used futures, agreements to buy or sell an asset at a set price on a specific date, to set up trades that profited from the gap between futures and spot prices, known as basis. That basis, in annualized terms, has been lower than the two‑year Treasury note continuously for more than five months, according to data source Glassnode.

“Three-month futures basis has paid less than a two-year Treasury since February. Only one other stretch on record has run this long: August 2022 into January 2023. It ended at the cycle low,” Glassnode said in a post on Telegram.

The three-month basis has been yielding less than the two-year Treasury note for 157 days, according to Glassnode’s Sunday chart.

Bitcoin analysts are pointing to August as a potential inflection point, hinging on whether the asset can secure a key monthly close that would confirm a technical bear-market bottom signal. Separately, Grayscale research suggests the bottom could have occurred earlier than the typical four-year cycle implies, pushing the focus to macro conditions rather than the calendar.

According to a Monday report shared with Cointelegraph by 10x Research founder Markus Thielen, Bitcoin’s July performance did not meet the threshold needed to validate a technical bottom. However, the firm argues that a monthly close near $63,000 in August could flip several of its cycle indicators to a bullish configuration.

Key takeaways

- 10x Research says a July monthly close failed to confirm its technical bottom signal, but an August monthly close near $63,000 could trigger a reversal indication.

- 10x Research continues to favor long positions, but would turn more neutral if Bitcoin breaks key support levels and moving averages.

- Grayscale’s Zach Pandl told investors in a July 22 report that Bitcoin may have bottomed earlier than the four-year cycle would suggest, potentially placing the cycle low in September or October.

- Macro variables—especially Fed policy and changes in the 10-year Treasury yield—remain central to timing both analysts’ outlooks.

- Other market participants highlight supply-side stress indicators, including the share of Bitcoin held at a loss.

What needs to happen for a 10x Research bottom signal

10x Research’s technical framework centers on cycle indicators tied to Bitcoin’s monthly price behavior. Thielen said in the Monday report that Bitcoin closed July below the level required to confirm the firm’s bear-market bottom setup.

When the analysis was prepared, Bitcoin was trading at $63,140. That matters because 10x Research argues the distance from the July closing level to the next confirmation threshold may be small. In its view, if Bitcoin prints an August monthly close around $63,000, the change could be sufficient to turn multiple cycle indicators bullish.

Importantly, 10x Research is not treating the signal as unconditional. The firm said it continued to favor long positioning, but would shift to a neutral stance if Bitcoin breaks key support levels and moving averages—an acknowledgement that technical confirmation can fail if price action deteriorates before the month ends.

Macro risks remain the timing driver

While the chart-based trigger is specific, 10x Research frames macro policy as the overriding variable. Its base case assumes the Federal Reserve holds interest rates steady. But the firm also flagged two key uncertainties: further increases in the 10-year Treasury yield could raise the probability of a September rate hike, and the Iran conflict adds geopolitical risk that could disrupt risk assets more broadly.

That emphasis on the macro backdrop is also echoed by Grayscale. In a July 22 report, Grayscale head of research Zach Pandl argued that Bitcoin’s timing might not match the traditional four-year cycle pattern, but that macroeconomic conditions—including Fed policy—still represent the primary mechanism shaping Bitcoin’s price.

Grayscale: a bottom may have come early—cycle low could be later

Grayscale’s view diverges from a strict reliance on the four-year cycle. Pandl told investors that Bitcoin may have bottomed earlier than the traditional four-year cycle would suggest. Under that interpretation, the cycle low would still fall in September or October, even if the earliest “bottoming” signals appeared sooner.

For traders and portfolio managers, the practical difference is not just the date—it is what to monitor. If bottoming can occur in phases, then early relief rallies or stabilization periods may not immediately complete the cycle, and investors may need to watch macro catalysts that can either sustain or reverse the improvement.

Supply-side pressure and the loss-held supply signal

In addition to technical and macro narratives, market structure indicators are contributing to the debate about how close Bitcoin may be to a durable bottom.

Earlier in July, crypto brokerage K33 pointed to a supply-side stress measure: more than half of Bitcoin’s supply was held at a loss. K33 described this as another sign that the market could be approaching a bottom, because prior periods with similar loss concentration were followed by strong subsequent returns.

K33 also reported that Bitcoin bottomed within 13 to 31 days of when that threshold was reached in 2017, 2018, and 2022. The key takeaway for investors is that the timeline is not only about price resistance or moving averages—distribution and holder pain can compress into a short window that may precede a broader trend reversal.

Another data point referenced in the broader discussion is long-term holder behavior. In a June interview, Swan Bitcoin CEO Cory Klippsten told Cointelegraph that long-term holders’ record balance of 14.7 million BTC was an indication Bitcoin was nearing a bottom. The idea aligns with a broader pattern often seen during bear markets: if long-term holders absorb supply while not distributing into weakness, downside pressure may eventually fade.

What to watch as the month turns

For now, the near-term question is straightforward: can Bitcoin produce an August monthly close around $63,000 in a way that validates 10x Research’s cycle indicators, while macro conditions do not undermine the setup. Investors should also monitor how supply-side stress measures evolve and whether the market behavior stays consistent with the historical windows flagged by K33—because that combination of technical confirmation and shifting holder dynamics is what will determine whether “bottoming” turns into a sustained trend.

Cointelegraph is committed to providing independent, high-quality journalism across the crypto, blockchain, AI, and fintech industries.

All news, reviews, and analyses are produced with full journalistic independence and integrity. For more details on our standards and processes, please read our Editorial Policy.

Other easily missed breeding spots include a tiny pocket of water beneath the soil in a potted plant, a discarded tire, or a planter saucer. Maintained, chlorinated pools and fountains with moving water generally aren’t the problem. Mosquitoes want still water—and the smaller the pool, the easier it is to miss.

They never walk past a container without glancing inside

Once mosquito experts learn what a breeding spot looks like, they see them everywhere.

In her own yard, a tarp left crumpled over some lumber became a collection of tiny pools after it rained. Buckets and cups forgotten after parties are equally inviting. Then there’s her neighbor’s wheelbarrow, which is full of weeds and refills whenever it rains. “I keep sneaking over there and emptying it out,” Bartholomay says. “The mosquitoes just love it.”

Where you live determines where else you need to look. In parts of Florida, some plants, like ornamental bromeliads, collect water in the cups of their leaves, allowing mosquitoes to breed several feet above the ground. Daniel Markowski, technical advisor with the American Mosquito Control Association, flags children’s toys—dump trucks, sand pails, plastic cups—and buried downspouts that aren’t draining properly. Mosquitoes can breed in the trapped water underground, then fly in and out through the top.

Prison officer claims colleagues ‘broke down’ over ‘nasty bullying’ culture

Douglas Dynamics, Inc. (PLOW) Q2 2026 Earnings Call Transcript

Can SpaceX earnings revive SPCX stock after its 52% plunge?

Renter of Home in Anne Heche Crash Denies Settlement With Son

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Weekend Open Thread: Staud – Corporette.com

NEW XRP RICHLIST MAKES YOU A MILLIONAIRE WITH 1000 XRP **YES IM SERIOUS** THE CLARITY ACT IS A TRAP

All financial advisors HATE this man! @CRED_club #LLAShorts 561

Matt Hougan :”My NEW Prediction For The 2026 Crypto Bull Run” (Prepare Now)

-

Business5 days ago

Business5 days agoWhy Trees Belong on the Risk Register

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Wit & Wisdom

-

Politics3 days ago

Politics3 days agoMeta enters AI-training agreement with far-right ‘propaganda rag’ Newsmax

-

Entertainment6 days ago

Entertainment6 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Crypto World2 days ago

Crypto World2 days agoMicroStrategy Post-Earnings CLARITY Act Push Could Add New Catalyst for Its Stock

-

Politics6 days ago

Politics6 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Business6 days ago

Business6 days agoMajor shareholder moves on Canyon

-

Crypto World3 days ago

Crypto World3 days agoXRP Ledger v3.3.0 brings five institutional features

-

News Videos4 days ago

News Videos4 days agoBitcoin Enters the 3rd Stage of the Bear Market

-

Crypto World6 days ago

Crypto World6 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech7 days ago

Tech7 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos6 days ago

News Videos6 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics4 days ago

Politics4 days agoLuke Littler’s dominance sparks GOAT debate

-

Sports4 days ago

Sports4 days agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

-

Business6 days ago

Business6 days agoJohnson & Johnson agrees to $5.5B settlement over talc cancer claims

-

Crypto World1 day ago

Crypto World1 day agoCrypto PAC spending tops $2M in Michigan House race

-

Business3 days ago

Business3 days agoTrump Announces Hamas Disarmament Agreement as Iran Strikes Kuwait Air Base and US Attacks Pause Overnight

-

Crypto World3 days ago

Crypto World3 days agoNew York sues Kalshi over prediction market gambling

-

Tech5 days ago

Tech5 days agoGemini can now summarize the messiest comment threads in Google Docs

-

Tech2 days ago

Tech2 days agoESET tracks rise in malicious AI skills and adaptable malware

You must be logged in to post a comment Login