Crypto World

What is the Howey test? Crypto securities explained

The most important legal test in crypto was written in 1946 to settle a dispute about orange groves. That single sentence explains most of the past decade of American crypto regulation: the confusion, the lawsuits, the exodus of projects to friendlier jurisdictions, and the legislative fight now playing out in the United States Senate.

\Every argument about whether a token is a security eventually arrives at the same four questions, and those questions come from a Supreme Court case decided before the transistor was invented.

The Howey test is the legal standard American courts and regulators use to decide whether an arrangement counts as an investment contract, one of the categories of security defined in federal law. If a crypto token sale meets the test, the full weight of securities regulation applies: registration, disclosure, liability, and the jurisdiction of the Securities and Exchange Commission. If it does not, the token falls outside the SEC’s core authority and, increasingly, into the hands of the Commodity Futures Trading Commission. Billions of dollars, entire business models, and the architecture of pending legislation turn on which side of the line an asset lands.

This guide explains where the test came from, what its four prongs actually require, how the SEC applied it to crypto through a decade of enforcement, what the landmark cases decided and left undecided, how the March 2026 joint SEC and CFTC interpretation reshaped the analysis, and how the CLARITY Act now moving through Congress would change the rules again.

The orange groves that defined a security

In the 1940s, the W. J. Howey Company owned large citrus groves in Florida. To raise money, it sold small tracts of the groves to visitors, mostly tourists with no farming experience, and offered each buyer a service contract under which Howey’s own company would cultivate the land, harvest the oranges, pool the fruit, and remit a share of the profits. Buyers owned land on paper, but in substance they were handing money to a business and waiting for returns.

The Securities and Exchange Commission sued, arguing that these land sales were unregistered securities. The case, SEC v. W. J. Howey Co., reached the Supreme Court in 1946, and the Court agreed with the regulator. It held that an investment contract exists when there is an investment of money in a common enterprise with an expectation of profits derived from the efforts of others. The Court stressed that substance beats form: it does not matter what a scheme is called, what asset is nominally being sold, or how the paperwork is dressed. If the economic reality matches the definition, it is a security.

That flexibility was the point. Congress wrote the securities laws of 1933 and 1934 broadly, after a crash fueled by opaque investment schemes, and the Howey test gave courts a tool that could reach any new packaging of the same old arrangement: money in, promises made, profits expected from someone else’s work. Eighty years later, that packaging includes tokens, and the same interpretive flexibility that let the test reach franchise schemes, whiskey warehouse receipts, and payphone leaseback programs across the twentieth century is what let regulators reach token sales in the twenty first.

The four prongs, one at a time

The test has four elements, and all four must be satisfied. The first is an investment of money. Courts read this liberally: cash qualifies, but so do other crypto assets, property, services, or anything else of value given up in exchange. Buying a token with ether is an investment of money. Even effort, in some framings, can qualify, which is why free distributions raise their own questions, discussed below.

The second prong is a common enterprise. The investor’s money must be pooled with others, or the investor’s fortunes must be tied to those of the promoter, such that everyone rises and falls together. Courts have developed competing doctrines here, horizontal commonality focusing on pooled funds and shared outcomes, vertical commonality focusing on the link between investor and promoter, and the disagreement matters in crypto cases because token buyers do not always have any formal relationship with each other or with the issuer.

The prongs interact, which is why the test resists mechanical application. A strong showing on reliance can compensate for a fuzzy common enterprise; a purely consumptive purchase can defeat the whole analysis even where a promoter exists. Courts weigh the total mix of facts, and small factual differences flip outcomes, which is exactly what makes the test flexible for regulators and maddening for anyone trying to comply in advance.

The third prong is an expectation of profits. The buyer must be motivated primarily by the prospect of financial return, capital appreciation, dividends, yield, instead of by consumption or use. Someone who buys a token to pay for computation on a network looks like a customer; someone who buys the same token because they expect the price to rise looks like an investor. The same asset can be both things to different buyers, which is one of the deep awkwardnesses of applying Howey to tokens.

The fourth prong is that profits must come from the efforts of others. If returns depend predominantly on the managerial or entrepreneurial work of a promoter, a founding team, a company, the arrangement points toward a security. If value arises from broad market forces or the holder’s own activity, it points away. This prong carries most of the weight in crypto disputes: the more a token’s value story depends on a specific team shipping a roadmap, the more it resembles the orange grove.

Why crypto and Howey collided

For its first decade, crypto mostly sold itself as something new, and the law mostly did not care. That ended with the initial coin offering boom of 2017, when thousands of projects raised money by selling tokens to the public on the strength of whitepapers and roadmaps. Functionally, many of these sales were indistinguishable from Howey’s service contracts: money in, a team promising to build, buyers expecting the token to appreciate through that team’s efforts.

The SEC responded first with the DAO Report of 2017, concluding that tokens sold by a decentralized fundraising vehicle were securities, then with a 2019 staff framework listing dozens of factors relevant to applying Howey to digital assets, and then with years of enforcement. The commission’s central position hardened into a slogan associated with its then chairman: nearly every token except Bitcoin looked to the agency like a security, because nearly every token had a team whose efforts buyers relied on. The industry’s counterargument was equally simple: a token is just an asset, like a commodity or a collectible, and an asset is not a contract. The sale of a token might create an investment contract in some circumstances, but the token itself, trading hands years later between strangers on an exchange, carries no promises with it.

Courts spent years sorting between these views, one enforcement action at a time, in what the industry came to call regulation by enforcement. The commission brought actions against issuers over unregistered sales, against exchanges over listing alleged securities, against staking services over yield programs, and against promoters over undisclosed paid touting, naming along the way dozens of specific tokens it considered securities in complaint after complaint. The pattern imposed enormous costs: projects could not know their legal status without being sued, exchanges could not know which listings were lawful, and the question of who regulates crypto, the SEC or the CFTC, stayed unresolved because the answer depended on an asset by asset legal test from 1946.

The cases that drew the map

A handful of decisions define the current terrain. The fundraising cases came first and went badly for issuers. Telegram raised 1.7 billion dollars selling contracts for future tokens and was enjoined in 2020; Kik lost on summary judgment the same year over its token sale; LBRY lost in 2022 despite arguing its token had genuine utility. Together they settled the easy half of the question: selling tokens to fund development, with buyers expecting profit from that development, satisfies Howey.

The hard half arrived with the Ripple litigation. In 2023, a federal judge split the difference in a way that reorganized the entire debate: Ripple’s direct sales of XRP to institutional buyers were securities transactions, because those buyers knew they were funding Ripple’s efforts, but programmatic sales on exchanges to anonymous buyers were not, because a purchaser on an exchange has no idea whether their money goes to Ripple at all and relies on no specific promises. The decision was contested and other judges pushed back on parts of its reasoning, but the core distinction, between a primary sale that creates an investment contract and a secondary trade in the bare asset, became the intellectual center of the reform argument. The token is not the security; the transaction might be. Readers following the XRP saga watched this distinction move billions of dollars in market value in a single afternoon.

The later enforcement wave against exchanges, targeting the listing of dozens of alleged securities, raised the stakes further, because it put the secondary market question directly in play. If tokens themselves were securities, most of the American crypto market was operating illegally. If only certain sales were, most of it was fine. That was the unstable equilibrium the current reform era inherited. Notably, the courtroom record itself stayed mixed: judges in different districts reached different conclusions about secondary sales, some rejecting the Ripple court’s programmatic sales reasoning outright, which guaranteed that without either a definitive appellate ruling or a statute, the question would stay open indefinitely. Uncertainty, not hostility, became the binding constraint on the American market.

The March 2026 interpretation: Howey, narrowed

On March 17, 2026, the SEC issued a formal interpretation of how Howey applies to crypto assets, with the CFTC issuing companion guidance the same day, and it marked the most significant regulatory repositioning since the enforcement era began. The interpretation runs in the industry’s direction on almost every contested point, and although it is not legislation and not binding rulemaking, a Commission level interpretation carries real weight with courts and total weight with the agency’s own staff.

Three moves matter most. First, the interpretation centers the analysis on the issuer’s own representations and promises. A buyer’s expectation of profit counts only if it rests on what the issuer said and did, not on hype from third parties, influencers, or the market at large. Second, it reaffirms that a common enterprise is a genuine, independent requirement, narrowing a prong the agency had previously treated as nearly automatic, and making it harder for secondary market transactions between strangers to satisfy the test. Third, and most consequentially, it describes a pathway for separation: a token born inside an investment contract can shed that status once the issuer’s original promises have been fulfilled or abandoned and no reasonable buyer still relies on them. The asset and the contract can come apart over time, which is exactly what the industry had argued since the Ripple decision.

The interpretation also addressed activities. Protocol mining, protocol staking without discretionary management or guaranteed returns, wrapping of assets, and airdrops generally do not involve the offer or sale of securities when conducted as described. Alongside the interpretation, the agencies jointly classified a first group of sixteen assets, including Bitcoin, Ethereum, and XRP, as digital commodities falling under CFTC jurisdiction. The classification was a watershed and also a warning: what an interpretation gives, a future commission can take back. Only statute is permanent, which is why the legislative fight matters more than any agency document.

What Howey does not cover

Understanding the test also means understanding its limits, because three misconceptions do most of the damage in public debate. The first is that Howey is the whole definition of a security. It is not. Federal law lists dozens of instruments that are securities on their face, stocks, bonds, notes, options, and the investment contract category that Howey defines is the catch all at the end of the list. Tokenized stocks are securities because they are stocks, no Howey analysis required. The test matters for crypto because most tokens resemble nothing on the enumerated list, so everything turns on the catch all.

The second misconception is that failing the Howey test makes an asset unregulated. A digital commodity escapes SEC registration requirements, but it lands in CFTC territory, where fraud and manipulation rules still apply, and it remains subject to tax law, sanctions law, and money transmission rules regardless. The Howey question decides which regulator and which rulebook, not whether rules exist.

The third is that passing or failing is permanent. Because the analysis attaches to transactions, an asset’s status can change as facts change. A network that decentralizes can grow out of its investment contract origins, which the 2026 interpretation now recognizes explicitly, and a dormant project that resumes making promises can walk back into securities territory. Lawyers describe tokens as existing on a spectrum with a direction of travel, not in fixed categories.

One more boundary matters in practice: the test only reaches offers and sales. Simply holding a token, building software, or validating a network is not a securities transaction. This is why so much legal engineering in crypto concentrates on the moment of distribution, the single point where the securities laws attach or do not.

The CLARITY Act: replacing the test with a statute

The Digital Asset Market Clarity Act is Congress’s attempt to answer by statute the question Howey answers by litigation. The bill passed the House in July 2025 by a bipartisan 294 to 134 vote and cleared the Senate Banking Committee in May 2026, and as of mid July 2026 it awaits a Senate floor vote that must clear a sixty vote threshold. Its core mechanism is a formal division of the asset universe: digital commodities, defined largely by reference to decentralization and function, fall to the CFTC, while tokens sold as part of capital raising remain with the SEC, with defined pathways for assets to migrate from one category to the other as networks mature.

In effect, the bill writes the Ripple distinction and the 2026 interpretation into law: primary fundraising is securities territory, sufficiently decentralized assets trading in secondary markets are commodities territory, and the boundary is defined by criteria a project can evaluate in advance instead of a four part test applied after the fact by a court. Supporters call this the end of regulation by enforcement. Opponents, including state securities regulators, argue it weakens investor protection by letting issuers structure their way out of disclosure obligations. Prediction markets currently price passage this session as roughly a coin flip, and the market’s live odds, which fell sharply through early July as the Senate calendar tightened, have become the industry’s real time barometer of whether the Howey era is actually ending, a story crypto.news has tracked closely in its coverage of the CLARITY Act’s odds and what they mean for major assets.

Until a statute passes, Howey remains the operative standard. Committee votes do not reclassify tokens, and interpretations do not bind future commissions. The 1946 test is still the law of the land, which is precisely why it is still worth understanding.

Why free tokens still raise Howey questions

Airdrops look like the easy case, no money changes hands, so the first prong fails, but the analysis proved more tangled than that. The SEC argued in several matters that free distributions can still involve an investment of value, because recipients often provide something, promotional activity, network usage, personal data, or because the issuer benefits by creating a trading market for the remainder of its supply. Courts entertained versions of this theory as far back as internet stock giveaways in the 1990s, and the uncertainty was severe enough that some projects excluded American users from airdrops entirely for years, a self imposed geofence that became a running symbol of the enforcement era.

The 2026 interpretation defused most of this. Airdrops conducted as genuine distributions, without payment and without the issuer soliciting value in return, generally do not involve the offer or sale of securities under the interpretation, and the same logic extends to network rewards from protocol mining and staking. The reasoning follows the interpretation’s core move: securities law attaches to the issuer’s representations and the exchange of value, and a distribution lacking both sits outside the perimeter.

The practical consequence arrived quickly. Projects that had walled off American users began including them again, and airdrop design shifted from legal risk management back toward marketing mechanics. The episode stands as a compact illustration of how much economic behavior a single legal test can shape: for half a decade, the geography of free token distribution on the internet was drawn by a 1946 precedent about oranges.

How to think about any token under Howey

For a practical read on any asset, walk the prongs in order and be honest about the facts. Was there a sale in which buyers handed over value? Almost always yes. Were funds pooled toward a shared venture whose success buyers share? Usually yes for fundraising sales, murkier for secondary trades. Did buyers primarily expect profit? Marketing tells you: materials emphasizing price potential, scarcity, and listings point one way, materials emphasizing use point the other. And do those profits depend on a specific team’s ongoing efforts? This is where decentralization matters legally, not aesthetically: a network that would keep functioning and accruing value if its founding team vanished makes a weak Howey case, and a token whose entire value story is a company’s roadmap makes a strong one.

Two cautions complete the picture. First, labels are irrelevant. Calling something a utility token, a governance token, or a meme changes nothing; courts look at economic reality, and the regulatory history is littered with projects that discovered this in court. Second, the analysis is transaction by transaction, not asset by asset. The same token can be sold as a security in a fundraising round, trade as a non security on an exchange years later, and be offered as a security again if the issuer restarts making promises. The question is never what is this token. The question is always what was this transaction, and that is the insight the orange groves have been teaching for eighty years.

Frequently asked questions

What is the Howey test in simple terms?

It is the four part legal standard American courts use to decide whether an arrangement is an investment contract, and therefore a security. The four elements are an investment of money, in a common enterprise, with an expectation of profits, derived from the efforts of others. All four must be met.

Where does the name Howey come from?

From SEC v. W. J. Howey Co., a 1946 Supreme Court case about a Florida company that sold citrus grove plots along with service contracts to manage them. The Court ruled the packages were investment contracts, creating the test that still applies today.

Is Bitcoin a security under the Howey test?

No. Regulators have consistently treated Bitcoin as a commodity, because there is no central issuer or promoter whose efforts drive returns. The March 2026 joint SEC and CFTC action formally listed Bitcoin among the first group of digital commodities.

Why did the SEC treat most other tokens as securities?

Because most tokens were originally sold by identifiable teams to raise money, with buyers expecting the token to appreciate through those teams’ work, a fact pattern that maps closely onto the Howey prongs. That view drove years of enforcement actions against issuers and exchanges.

What did the Ripple ruling actually decide?

A federal court held in 2023 that Ripple’s direct institutional sales of XRP were securities transactions while its anonymous exchange based sales were not. The decision popularized the distinction between a token sale that creates an investment contract and the token itself trading later.

What changed in March 2026?

The SEC issued a formal interpretation narrowing how Howey applies to crypto: profit expectations must rest on the issuer’s own representations, common enterprise is a real requirement, and tokens can separate from their original investment contracts over time. Mining, staking, wrapping, and airdrops conducted as described generally fall outside securities offerings.

Would the CLARITY Act replace the Howey test?

For crypto assets, largely yes. The bill creates statutory categories, digital commodities under CFTC oversight and capital raising tokens under SEC oversight, with defined criteria replacing case by case Howey analysis. Until it becomes law, Howey remains the operative standard.

Does the Howey test apply outside the United States?

No. It is a doctrine of American federal law. Other jurisdictions use their own frameworks, such as the European Union’s MiCA regulation, though the underlying question of whether a token functions as an investment product appears in some form almost everywhere.

This article is for educational purposes only and does not constitute legal or investment advice. Securities law is fact specific, and regulatory positions change. Details are accurate as of July 14, 2026.

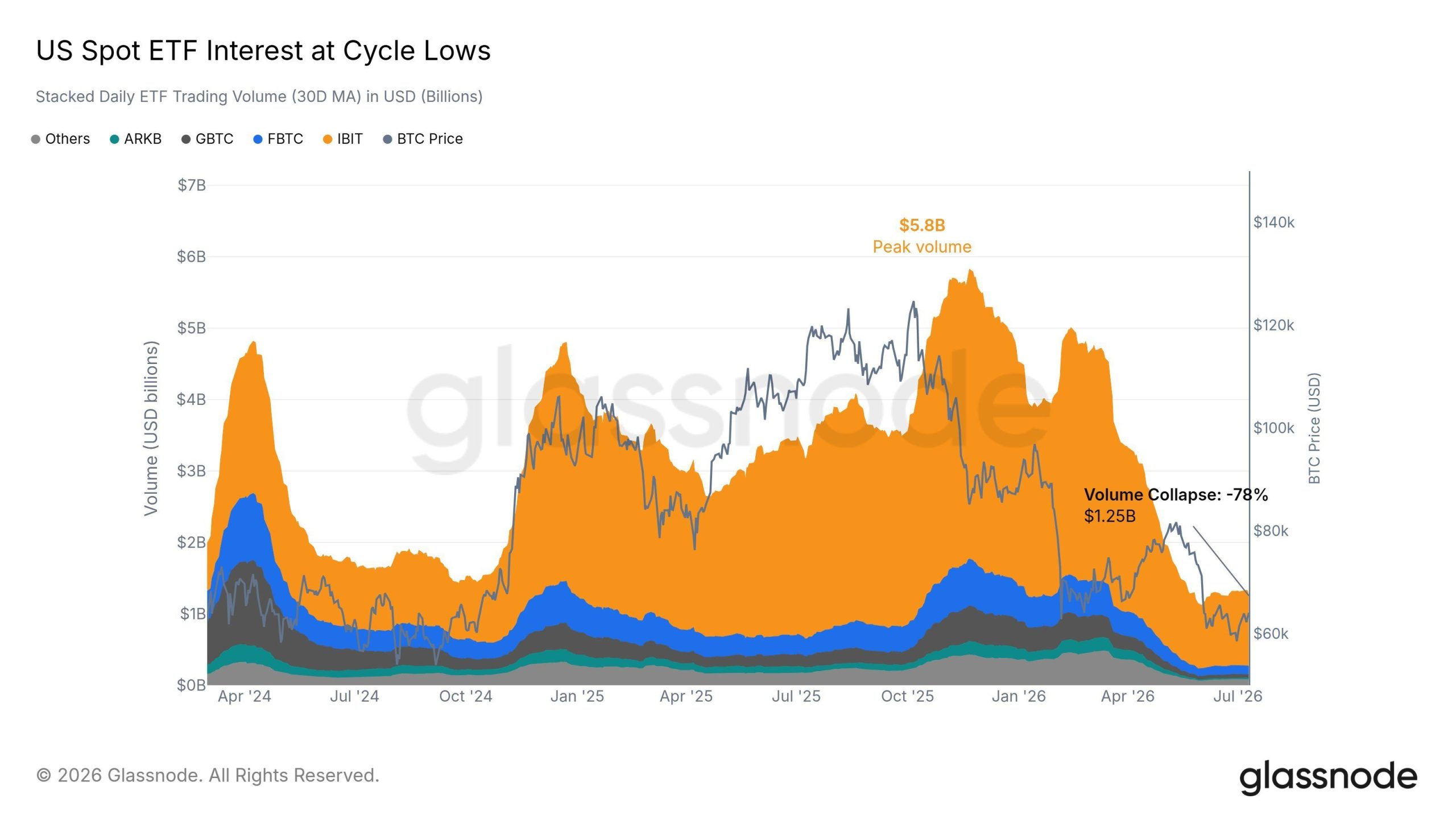

US spot Bitcoin (BTC) ETF outflows reached roughly $430 million on July 13. Fidelity’s FBTC lost $246.3 million and BlackRock’s IBIT shed $186.1 million, according to Glassnode data.

The redemptions hit a market already trading at its quietest levels this cycle. ETF volumes have collapsed 78% from their peak, and analysts warn that attention has rotated to other asset classes.

ETF Trading Volumes Collapse 78% From Peak

Glassnode’s 30-day moving average of daily trading volume across US spot Bitcoin ETFs now sits at $1.25 billion. That marks a 78% collapse from the $5.8 billion peak recorded in late 2025.

Activity has also slipped below 2024 levels. BlackRock’s IBIT still accounts for most of the remaining turnover. However, even its share has thinned in recent months.

The on-chain analytics firm framed the slowdown as a loss of attention rather than a temporary lull. Glassnode shared the observation in a post on X:

“Trading activity in US spot ETFs sits in a quiet regime. Volumes are down 78% from the peak and below 2024 levels. A sustained recovery in $BTC price momentum would likely require attention and market participation to return from other asset classes.”

Bitcoin ETF Outflows Top $430 Million in One Day

Monday’s session showed how one-sided flows have become. Fidelity’s FBTC led the exit with $246.3 million in redemptions. IBIT followed with $186.1 million, while VanEck’s HODL bucked the trend with a $3.5 million inflow.

Grayscale’s GBTC and Franklin Templeton’s EZBC posted smaller losses. Combined, the funds bled roughly $430 million in a single day.

The IBIT figure drew loud reactions. Evan Luthra, entrepreneur and BeInCrypto Experts Council member, reacted to the data in a post on X.

The framing deserves nuance, however. ETF outflows reflect investors redeeming shares, which forces issuers to sell bitcoin held in trust. BlackRock did not liquidate a proprietary position, and Fidelity’s outflow was the larger of the two.

The reversal also stings because of its timing. Bitcoin funds had just attracted $197.4 million in net inflows during the week ending July 10, snapping eight straight losing weeks. June, in contrast, produced record monthly outflows of $4.5 billion.

BTC Price Prediction Hinges on the $58,000 Support

BTC trades near $64,681, up 4.4% over the past 24 hours, per BeInCrypto market data. Glassnode’s flows chart tracks the token’s slide from roughly $78,000 in mid-May to a June 30 low near $58,000.

That $58,000 area remains the level to defend. A daily close below it would put the cycle floor near $57,500 in play, roughly an 11% drop from current prices.

On the upside, bulls must reclaim $68,000, the zone where the early June breakdown began. A recovery above that level would suggest institutional demand is returning after a two-month drought.

There are early signs of absorption elsewhere. Long-term holders flipped back to accumulation on July 11 and 12, adding a net 5,912 BTC.

Sustained positive flows and a volume recovery would confirm renewed participation. Until then, BTC either rebuilds momentum above $68,000 or retests $58,000 with little institutional cushion beneath it.

The post ‘BlackRock Dumped $185M in Bitcoin’ Claim Fuels ETF Panic as Trading Hits Cycle Lows appeared first on BeInCrypto.

Three Democratic senators have opposed the Digital Asset Market Clarity Act unless lawmakers add stronger ethics rules covering senior officials and their families.

Summary

- Murphy, Merkley and Van Hollen oppose the CLARITY Act unless lawmakers add strict ethics safeguards.

- John Thune pledged a Senate vote before recess, but timing and Democratic support remain uncertain.

- The bill needs 60 votes, making bipartisan support essential amid disputes over ethics and DeFi.

Senators Chris Murphy, Jeff Merkley and Chris Van Hollen raised their objections during a July 14 press conference organized with Americans for Financial Reform and Indivisible.

The lawmakers tied their opposition to President Donald Trump’s crypto businesses, including his memecoin and the World Liberty Financial project. Murphy claimed Trump earned $1.4 billion from crypto in 2025. Trump has rejected claims of wrongdoing involving his digital asset interests.

Senators demand conflict-of-interest protections

Murphy said Congress should not create a new crypto framework without rules that prevent officials from profiting from the industry they regulate. He said, “There is no reason to pass a new regulatory system for crypto if this system does not stop Trump’s corruption.”

Merkley called for restrictions covering the president, vice president, Cabinet officials, members of Congress and their families. Van Hollen also argued that the bill needs stronger consumer, anti-crime and conflict-of-interest provisions before he can support it.

The lawmakers did not reject digital asset regulation as a general goal. Their position centers on whether the final Senate text includes enforceable ethics language. Senator Elizabeth Warren has made a similar demand, calling for restrictions on crypto profits involving senior government officials.

Thune commits to vote before August recess

Senate Majority Leader John Thune told Bloomberg Government that the chamber will vote on the CLARITY Act during the current work period. He said leaders had not fixed the exact date and added that Democratic support remains the main question.

The press conference organizers listed July 20 as the expected vote date. However, Thune only committed to action before the recess and said the exact timing remained undecided.

The Senate’s official calendar starts its state work period on Aug. 10, leaving Aug. 7 as the final scheduled session day before the break. As of July 15, the public Senate floor schedule did not list a CLARITY Act vote, leaving the reported timing still subject to change.

The bill needs 60 votes, so Republicans cannot pass it without Democratic support. The House approved the CLARITY Act in July 2025 by a 294-134 vote. The measure would divide digital asset oversight between the SEC and CFTC while setting registration and custody rules for crypto firms.

Ethics dispute adds to unresolved policy fights

As previously reported, ethics rules are one of three disputes shaping the Senate negotiations. Lawmakers also remain divided over protections for non-custodial developers and whether crypto platforms may offer rewards tied to stablecoin balances.

The ethics debate has gained urgency as senators prepare a combined draft from the Banking and Agriculture committees. Supporters want a durable federal framework, while opponents say the bill should not move without clear limits on financial conflicts involving public officials.

Bill also gains law enforcement support

The National Organization of Black Law Enforcement Executives and Federal Law Enforcement Officers Association have backed the bill. FLEOA also requested tighter DeFi accountability rules and language preserving federal investigative powers.

As reported by crypto.news, the two endorsements give supporters added backing before the Senate vote. However, the ethics opposition shows that the bill still lacks the bipartisan coalition needed for passage. The final wording and vote date remain unsettled.

The European Central Bank is moving the digital euro from planning into testing, with dozens of payment companies joining the next stage of the project.

The ECB selected 36 payment service providers (PSPs) to participate in a digital euro pilot, according to an official announcement published Tuesday.

The list of selected PSPs includes fintechs Stripe and Revolut alongside traditional banks including Deutsche Bank, UniCredit and BPCE. Revolut has recently adjusted some cryptocurrency services for EU users by phasing out support for Tether USDt.

The pilot comes as governments take different approaches to digital currencies. While Europe is expanding testing of its proposed central bank digital currency (CBDC), the US has moved to block the Federal Reserve from issuing a CBDC.

Italy tops list of digital euro pilot providers

The ECB began selecting providers from across the euro area for its digital euro pilot earlier this year, with the 12-month trial set to begin in the second half of 2027.

The central bank said it received more than 50 applications from payment companies after opening a call for interest in March 2026. The selected participants include traditional banks, payment processors and non-bank service providers.

Source: ECB

Italy has the largest number of selected participants, with seven companies joining the pilot, including UniCredit, Poste Italiane, Nexi Payments, Banca Sella, Banca Monte dei Paschi di Siena, Isybank and Numia.

Germany follows with five selected providers, while Portugal and Greece each have three. The ECB said the mix of countries is designed to create a broad testing environment, with selected providers able to offer pilot services outside their home markets.

Strong interest in digital euro pilot

ECB Executive Board member Piero Cipollone, who chairs the high-level task force on a digital euro, said the level of participation shows private-sector interest in helping develop it, adding that the Central Bank expects deeper cooperation with payment providers during the pilot.

“We look forward to deeper engagement as we work with and learn alongside European payment service providers in developing a secure, efficient and inclusive digital euro,” Cipollone said.

Related: South Korea to test tokenized government bonds with CBDC in 2027

The pilot will involve the ECB and the central banks of 19 bloc-members, including Belgium, Germany, France, Italy, Spain and the Netherlands, alongside payment companies and merchants testing the system before any potential token issuance.

Selected providers will have different responsibilities during the trial, with some focused on supporting user access to beta digital euro services and others helping merchants accept payments. Several companies will take on both roles, the ECB said.

Magazine: The 5 types of real world assets being tokenized fastest onchain

Chinese AI startup DeepSeek has begun preparing for an initial public offering (IPO) and has also opened early talks with new investors for another funding round.

The moves come only weeks after DeepSeek closed its first external round, signaling that investors are aggressively chasing top Chinese artificial intelligence (AI) plays.

DeepSeek Eyes IPO Filing This Year as It Sounds Out New Investors

According to Bloomberg, DeepSeek could file its IPO paperwork late this year or in early 2027. That timeline would clear the way for a debut next year.

The company is working with accounting and banking advisers. It wants to finish its financial report by the end of December.

The Hangzhou firm has also opened preliminary talks with new investors this week. The Financial Times reported that DeepSeek is seeking fresh funds in another round, targeting a pre-money valuation of about $71 billion.

Follow us on X to get the latest news as it happens

That tops the roughly $50 billion figure from its first external round. That raise closed nearly a month ago and drew Tencent and battery maker CATL. Founder Liang Wenfeng put about $3 billion of his own money into it.

The rapid return to fundraising reflects DeepSeek’s expectation of higher spending ahead. The company plans to build its own data center and buy more AI chips. DeepSeek is also developing its own AI chip, which could cut reliance on Nvidia and Huawei, Reuters reported earlier this month.

Plans remain fluid, and both the IPO timing and the funding could shift. Much depends on market conditions and the company’s performance.

DeepSeek’s IPO push comes as US rivals move in the same direction. Anthropic and OpenAI both filed confidential IPO prospectuses in June. Anthropic said any offering would depend on market conditions and other factors, keeping the timing open.

OpenAI’s timeline looks less settled. CFO Sarah Friar floated the idea of waiting until 2027 to go public. She cited heavy cash burn, large compute commitments, and the burden of public reporting.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post DeepSeek May File for IPO This Year as It Weighs Fresh Fundraising appeared first on BeInCrypto.

Corporate treasury demand remains one of Bitcoin’s most important structural sources of support, but experts suggest that the market is no longer treating it as a permanent, price-insensitive floor.

Instead of focusing solely on how much BTC companies hold, QCP Capital stated that investors are increasingly evaluating whether the funding conditions behind those holdings can continue to support accumulation.

Funding Model Matters More

In its latest report, QCP said that the trend became clear in Q2 after Strategy’s late-May sale of 32 BTC. Although the sale was “immaterial” relative to its 846,842 BTC holdings, it challenged the long-held belief that corporate Bitcoin treasuries would only keep buying, never sell.

It also prompted the market to reassess whether treasury holdings were truly untouchable. Even as Strategy resumed buying within weeks, there has been no meaningful positive reach for Bitcoin, which essentially suggests that the market had become more focused on funding capacity, balance-sheet liquidity, and confidence in the treasury model than on accumulation alone.

QCP explained that while public companies collectively hold about 1.26 million BTC, roughly two-thirds belong to Strategy. This leaves the corporate treasury narrative heavily concentrated around a single company. As a result, its purchases, issuance conditions, and reserve policy continue to influence Bitcoin sentiment well beyond their direct impact on the spot market.

The financial structure supporting corporate accumulation has come to attention in Q2. Rather than judging treasury demand through purchase announcements, investors are now watching factors such as mNAV, equity issuance, preferred demand, convertible capacity, and cash reserves.

When funding conditions remain favorable, companies can raise capital, expand their Bitcoin reserves, and reinforce confidence in the treasury model. On the other hand, when conditions tighten, recurring preferred-stock obligations create cash needs, as seen with the Strategy’s May sale.

QCP went on to add that the company’s equity still trades above the combined value of its Bitcoin net asset value and US dollar reserves, which indicates a premium on its ability to continue raising capital, even as around $22.2 billion in preferred securities and convertible instruments rank ahead of common equity.

Looking ahead to Q3, continued net accumulation by Strategy and other public companies, particularly alongside stabilizing ETF inflows, would strengthen Bitcoin’s absorption channel and help repair the confidence damage from Q2. However, QCP warned that slower purchases, weaker preferred pricing, a compressed mNAV premium, or declining cash reserves would point to growing stress, which would end up making the corporate treasury bid more selective and increasing sentiment risk.

Besides, Bitwise CIO Matt Hougan recently said that Strategy is unlikely to have the same influence on Bitcoin demand in the next market cycle as it did previously. Hougan does not expect the company to become a major seller and still sees it remaining a net buyer if the crypto asset’s prices recover.

Scenarios For BTC

QCP outlined three possible paths for Bitcoin in Q3. Its base case calls for the crypto asset to remain between $60,000 and $75,000 as ETF flows stabilize and corporate treasury demand supports the market.

A steady reclaim of $75,000 could drive prices toward $80,000-$82,000, while renewed ETF outflows, a stronger dollar, or rising real yields could trigger a break below $58,000-$60,000 and confirm a more bearish outlook.

The post Why Strategy’s Tiny 32 BTC Sale Changed How Investors View Corporate Bitcoin Buying appeared first on CryptoPotato.

![]()

Reed Smith has launched an automated MiCA compliance platform as crypto firms across the European Union have entered full regulatory supervision following the end of the bloc’s transition period.

Summary

- Reed Smith has launched an automated platform to help crypto companies comply with the European Union’s MiCA regulation.

- The platform automates crypto asset classification, regulatory filings, due diligence and ESG disclosures for firms entering the EU market.

- The launch comes as European regulators move from MiCA licensing to operational supervision and consider future changes to the framework.

According to global law firm Reed Smith, the new platform, called Aquarius, automates key compliance tasks under the European Union’s Markets in Crypto-Assets (MiCA) regulation, including crypto-asset classification, regulatory white paper generation, due diligence and environmental, social and governance (ESG) disclosures.

Designed for companies entering the European market or expanding existing crypto services, the platform combines automated compliance workflows with legal support to simplify MiCA requirements. Reed Smith said future versions will also support crypto compliance regimes in the United Kingdom, the United Arab Emirates, Hong Kong, and Singapore.

The launch comes shortly after the European Union’s MiCA transition period ended on July 1, when crypto companies could no longer rely on temporary national exemptions in member states that adopted the full grandfathering period. The framework now requires crypto-asset service providers to meet common licensing, consumer protection, and operational standards across all 27 EU member states.

Reed Smith has continued expanding its digital asset practice through its “On Chain” initiative. The firm acted as legal counsel to the placement agents in Trump Media’s $2.5 billion Bitcoin treasury financing and also advised Nakamoto Holdings on its merger with KindlyMD to establish a Bitcoin treasury company.

Focus moves from licensing to supervision

Recent regulatory activity indicates that European authorities are now concentrating on how licensed firms operate after receiving approval.

Last week, the European Securities and Markets Authority (ESMA) began a Common Supervisory Action covering selected MiCA-authorized crypto-asset service providers. According to ESMA, the review examines custody operations, including private key management, transaction controls, incident response procedures and reliance on third-party technology providers.

Sebastien Dessimoz, co-founder and managing partner of digital asset infrastructure provider Taurus, previously said obtaining a MiCA licence is only the starting point for custodians because regulators now expect firms to demonstrate that their operational controls can withstand real-world risks. He added that supervision increasingly focuses on cybersecurity, governance and protection of client assets rather than licensing alone.

Institutional expectations have also increased. Jody Mettler, chief operating officer of BitGo and president of BitGo Trust, previously said clients are paying closer attention to how custodians segregate customer assets, control access, respond to security incidents and maintain business continuity during periods of market stress.

Meanwhile, European policymakers continue discussing possible changes to MiCA after its rollout. According to a Euronews report, officials are considering future revisions to stablecoin rules, including the treatment of non-euro-denominated stablecoins, following the passage of the United States’ GENIUS Act.

The European Parliament has also asked the European Commission to examine whether decentralized finance, staking, crypto lending and borrowing, non-fungible tokens and tokenized financial assets should receive more specific treatment under the EU’s crypto framework. Parliament’s position does not change the law but provides political support for further reviews, while any expansion of MiCA would still require separate legislative proposals.

US Treasury Secretary Scott Bessent confirmed the US government ordered the freezing of more than $130 million in cryptocurrency held in wallets linked to Iran on Tuesday, as hostilities ramped up in the Middle East.

Earlier on Tuesday, blockchain investigator Specter pointed to onchain data showing Tether froze four Tron wallets holding $131 million worth of USDt (USDT). Bessent confirmed on X that the wallets were tied to the Central Bank of Iran.

“US Treasury is committed to disrupting and degrading Iran’s illicit financial activities, including its abuse of digital assets,” Bessent said Tuesday. “We will continue to aggressively follow the money and deny the Iranian regime access to the proceeds of its illicit revenue schemes.”

The asset freeze comes amid a collapse in the ceasefire between the US and Iran. The US said it has renewed its blockade of Iranian ports, while the US military’s Central Command announced a new wave of strikes on Iran. Meanwhile, Iran’s military claimed on Tuesday that it carried out drone strikes against US military facilities at Jordan’s Al Azraq Air Base.

Source: Scott Bessent

The move follows a similar freeze in April, when stablecoin issuer Tether confirmed it had frozen more than $344 million in USDT at the request of US authorities.

In May, Bessent said the US has seized around $1 billion in Iranian crypto assets as part of the US financial pressure campaign against Iran known as Operation Economic Fury, which launched in March 2025.

Related: Iran-linked entities moved $3.8B through CoinEx, TRM says

“Through Economic Fury, the Treasury Department is disrupting the foreign procurement networks that support the Iranian military’s efforts to acquire weapons,” Bessent said in a statement in June.

“Treasury has frozen the Iranian regime’s assets, severely disrupted its economy, and dismantled the Iranian war machine. Treasury will not tolerate any support of the Iranian military.”

Magazine: Thai scammer’s $122M wallet, Japan embraces crypto credit: Asia Express

Confirmo has launched a stablecoin subscription payment service that supports automated recurring billing across more than 700 self-custody wallets and exchange accounts.

Summary

- Confirmo has launched Subscribe to let businesses automate recurring stablecoin payments through wallets and exchange accounts.

- The service supports USDC and USDG on Solana and Polygon, with more than 700 WalletConnect compatible wallets available.

- The launch comes as stablecoin payments continue expanding across business subscriptions, cross border settlements and enterprise payment services.

According to a July 14 press release shared with crypto.news, Subscribe allows enterprise businesses such as SaaS providers, trading platforms, and subscription services to add recurring stablecoin payments to their existing payment systems without developing the infrastructure internally.

The product has arrived as the global subscription economy is projected to reach $1.2 trillion by 2030, while Confirmo said more than 700 million people, or about 8.5% of the global population, now hold digital assets.

Built on Solana and Polygon, Subscribe initially supports Circle-issued USDC and Paxos-issued USDG. Paxos also serves as Confirmo’s US infrastructure partner, with the companies working together on stablecoin infrastructure and market access.

Subscribe supports wallets and exchange accounts

Unlike services limited to self-custody wallets, Subscribe accepts payments from both wallets and exchange accounts. WalletConnect integration gives customers access through more than 700 supported wallets, according to Confirmo.

Once a customer approves a subscription, the system automatically pulls stablecoins from the selected wallet or account on each billing date. Every payment is recorded from the outset, allowing merchants to monitor completed and scheduled transactions.

Existing Confirmo clients can view subscription activity through the same dashboard used for their other stablecoin payment products. The combined view removes the need to manage recurring transactions through a separate system.

Subscription plans are priced in US dollars to limit exposure to digital asset price changes. Confirmo said stablecoin settlement can also lower cross-border costs and reduce unexpected charges for customers.

Card declines and failed billing attempts can cause subscribers to lose access to a service without choosing to cancel. The company said wallet-based pull payments remove some of those failure points by collecting funds automatically after the customer grants approval.

Anna Kratky Strebl, Group CEO at Confirmo, said the service was developed around the payment needs of the company’s business customers.

“Built in collaboration with our long-term customers, it gives merchants a more transparent, cost-effective way to manage subscription and recurring revenue models, while making it easier for consumers worldwide to pay with the wallets and accounts they already use,” Strebl said.

She added that Confirmo would continue adapting its services as stablecoins become part of mainstream financial infrastructure and businesses seek new digital payment models.

FTMO helped design the payment system

Confirmo developed Subscribe with proprietary trading firm FTMO, which served as the product’s design partner. The collaboration allowed the infrastructure provider to test the system against the operational requirements of an existing merchant before launch.

Milan Flosman, Head of Finance Operations at FTMO, said the service would allow the company to introduce automated stablecoin billing without building its own payment system.

“Subscribe will give us something that didn’t exist before, a way to run automated, recurring stablecoin billing without building it ourselves,” Flosman said.

He added that Confirmo understood FTMO’s setup through the companies’ existing relationship and built the service to integrate with its operations.

“We’re not just looking to accept a new payment method; we’re preparing to launch a new payment model entirely,” Flosman said.

Stablecoin payments continue expanding beyond trading

The launch comes as businesses continue adopting stablecoins for commercial payments instead of limiting their use to crypto trading.

As previously reported by crypto.news, stablecoin cross-border payments were priced below interbank foreign exchange rates throughout the second quarter of 2026, Borderless.xyz highlighted in its Q2 2026 benchmark.

The firm tracked 260 payment corridors across 108 countries using nearly three million exchange rate observations and found stablecoin transfers maintained predictable pricing while provider selection became the largest factor affecting payment costs.

Borderless.xyz also reported that real-world stablecoin payment volume doubled to about $400 billion in 2025 as business-to-business payments, payroll and cross-border settlement gained traction.

The report said payment providers have continued expanding stablecoin services across new markets, with companies including dLocal and SBI Remit increasing support for international payment corridors.

XRP traded near $1.07 on July 14 after losing about 1% over 24 hours.

Summary

- XRP trades near $1.07 as negative Binance CVD data shows sellers still control spot demand.

- The $1.08 resistance level remains crucial, while $1.05 and $1.00 form the nearest downside supports.

- Bullish XRP social sentiment may increase short-term risk because prices often move against crowded expectations.

The token moved between $1.06 and $1.08, with daily volume near $955 million and market capitalization around $66.7 billion. Ripple’s native token remained the sixth-largest cryptocurrency.

The price has fallen nearly 6% over seven days and about 7% over one month. It also sits more than 70% below its July 2025 record of $3.65. The latest data shows weak price action near a support area defended several times since late June, while buyers still lack a clear breakout signal.

XRP price remains below key resistance

The XRP/USDT daily chart shows a broader decline from the $1.40 to $1.50 region. Price has stabilized between $1.05 and $1.10, but buyers have not reclaimed the recent recovery zone near $1.15 to $1.20. Analyst Cryptorphic said lower levels remain possible “as long as $1.08 remains resistance.”

The nearest downside level sits around $1.05. A daily close below that area could expose the psychological $1.00 mark. A recovery above $1.08 would ease immediate pressure, while a move through $1.10 could open another test of $1.14 and $1.18.

The relative strength index stood near 40.30, below its signal average of 45.68. The MACD histogram turned slightly positive, but the MACD and signal lines stayed below zero. That setup points to minor stabilization rather than a confirmed trend change, because both momentum lines remain in negative territory.

Binance order flow continues to favor sellers

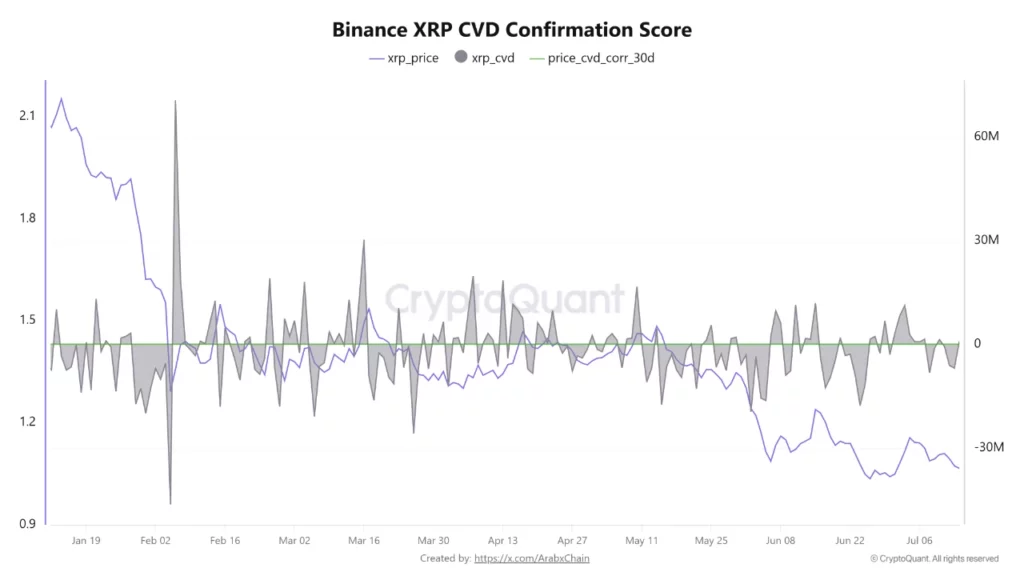

A CryptoQuant analysis by Arab Chain found that XRP’s Binance Cumulative Volume Delta remained negative at about 6.93 million. CVD measures the difference between market buy and sell orders. A negative reading means sellers executed more volume than buyers.

The 30-day Price-CVD Confirmation Score held near 0.84. The analyst said the reading confirms that price and order flow continue to move together, but does not show enough buying demand for a reversal. A sustained move in CVD above zero, with a rising score, would offer clearer evidence that buyers have returned.

The data supports the short-term chart structure. The token has stayed close to $1.07 while spot sellers limit rebounds. Binance remains one of the largest XRP markets, making its order flow useful for judging whether price moves have support from spot demand.

Bullish social sentiment creates a mixed signal

Santiment said XRP recorded 3.02 bullish comments for every bearish comment on Monday. Ether followed at 2.31, while Bitcoin posted a more balanced ratio of 1.40. XRP therefore carried the strongest level of optimism among the three assets.

Santiment warned that crowded optimism can work against prices when markets already trade lower. “Crypto typically moves opposite to what the crowd is loudly expecting,” the firm wrote. It said strong bullish discussion around XRP and Ether could slow a rebound or create short-term downside risk.

The reading follows an earlier rise in XRP network growth and social interest near the $1 support region. New activity can attract buyers, but sentiment alone does not confirm demand. The split between positive commentary and negative Binance order flow keeps attention on both price and liquidity.

$50 XRP scenario depends on a $100 trillion crypto market

Crypto commentator Moon Lambo calculated that XRP could reach $50.10 if the total cryptocurrency market grew to $100 trillion and XRP retained a 3.13% share. That outcome would assign about $3.13 trillion in value to XRP, based on its circulating supply.

Moon Lambo stated, “I’m not making a prediction.” The calculation only shows price under fixed assumptions. At a 1% share of a $100 trillion market, XRP would trade near $16.01. A 5% share would place it around $80.08, while 10% would imply about $160.15.

Those figures do not describe XRP’s current market setup. The global crypto market would need to expand many times, while XRP would need to retain or increase its share. Supply changes, adoption, regulation and market structure would also affect future valuation.

XRP entered July between support around $1.00 to $1.06 and resistance near $1.18 to $1.20. Spot XRP exchange-traded funds also recorded $7.29 million in net outflows on July 8, their largest daily withdrawal since March.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

A former Los Angeles County Sheriff’s Department deputy has been sentenced to 18 months in federal prison after admitting he lied to federal investigators about threats made by a cryptocurrency businessman during a 2021 extortion incident.

Summary

- A former Los Angeles sheriff’s deputy was sentenced to 18 months in prison for lying to federal investigators in a crypto-related extortion case.

- Prosecutors said the deputy witnessed Adam Iza threaten a victim with live ammunition before demanding a $25,000 payment.

- Iza remains in federal custody after multiple guilty pleas, including his role in a bitcoin-linked kidnapping conspiracy in Connecticut.

The U.S. Attorney’s Office for the Central District of California said U.S. District Judge Percy Anderson also imposed a $10,000 fine on Scott Allen Simpkins, who pleaded guilty on March 17 to one count of obstruction of justice. Simpkins resigned from the Los Angeles County Sheriff’s Department’s Special Enforcement Bureau after entering his felony plea, according to the office.

Federal prosecutors said Simpkins falsely denied witnessing cryptocurrency businessman Adam Iza threaten a victim with live ammunition during an incident at Iza’s Bel Air home in 2021.

Court records cited by the U.S. Attorney’s Office said Simpkins was working private security at the residence with fellow former LASD deputy Christopher Michael Cadman. Both men were employed by Saavedra & Associates, a private security company owned by then-LASD Deputy Eric Chase Saavedra.

According to prosecutors, Iza placed four or five live 9mm rounds on his desk, spun one of the bullets while threatening the victim, and demanded a $25,000 transfer before Simpkins and Cadman escorted the victim off the property.

The U.S. Attorney’s Office said the two deputies received $1,400 each for their work that day. After helping Saavedra & Associates secure a longer-term security contract with Iza, the company paid each of them about 10% of its profits from the contract’s first month, prosecutors added.

Iza still awaits sentencing

Separate federal cases against Iza have continued to move forward.

The U.S. Attorney’s Office said Iza has remained in federal custody since September 2024 after pleading guilty in California in January 2025 to conspiracy against rights, wire fraud, and tax evasion. He has not yet been sentenced in that case.

In a separate prosecution, the U.S. Department of Justice announced in June that Iza also pleaded guilty in federal court in Connecticut to conspiracy to interfere with commerce by robbery. The charge carries a maximum prison sentence of 20 years.

According to the Justice Department, the Connecticut case involved a 2024 kidnapping plot targeting the parents of Veer Chetal, a man accused of participating in the theft of about 4,100 bitcoin. Prosecutors said Iza and his brother, Saif Faiq, organised the scheme in an attempt to extort cryptocurrency.

As pre DOJ records, Faiq pleaded guilty on June 9, when he admitted recruiting six men from Florida, arranging their travel to Connecticut, and coordinating surveillance before the attack in Danbury. Prosecutors said the group allegedly forced Sushil and Radhika Chetal from their vehicle after staging a collision, assaulted them, and briefly held them captive. The six alleged attackers later pleaded guilty to kidnapping and carjacking offences, according to the department.

Federal records cited by the DOJ show Veer Chetal separately pleaded guilty in November 2025 to charges connected to the theft of approximately 4,100 bitcoin and is awaiting sentencing.

‘BlackRock Dumped $185M in Bitcoin’ Claim Fuels ETF Panic as Trading Hits Cycle Lows

Todd Graves Reveals Rare Gift Chuck Norris Once Gave Him

Samsung launches new SSD 990: reviews praise the performance, question the price

-

Fashion6 days ago

Fashion6 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports5 days ago

Sports5 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports5 days ago

Sports5 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

News Videos9 hours ago

News Videos9 hours agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech24 hours ago

Tech24 hours agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech9 hours ago

Tech9 hours agoDark Secrets Emerge When Jailbreaking LLMs

-

News Videos6 days ago

News Videos6 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

NewsBeat6 days ago

NewsBeat6 days agoMajor update after Huntingdon train attack as man enters plea

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Sports7 days ago

Sports7 days ago39-year-old Djokovic wins five-hour thriller to enter Wimbledon semis | Other Sports News

-

Tech6 days ago

Tech6 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

Tech1 day ago

Tech1 day agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Tech6 days ago

Tech6 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Crypto World6 days ago

Crypto World6 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

Crypto World6 days ago

Crypto World6 days agoMark Cuban-Backed DeFi Dashboard Zapper Shuts Down After 7 Years

-

Tech6 days ago

Tech6 days agoClaude’s New Reflect Dashboard Wants To Help You Log Off Of Claude

-

Crypto World7 days ago

Crypto World7 days agoMicrosoft Cuts AI Bill by Replacing OpenAI and Anthropic in Software Products

-

Crypto World6 days ago

Crypto World6 days agoFed minutes June 2026: officials split on rates

You must be logged in to post a comment Login