Crypto World

What is a transfer agent in tokenized securities?

Crypto spent fifteen years arguing the ledger is the truth. Tokenized securities quietly reversed it. The token in your wallet is a receipt, and a company you have never heard of keeps the record that actually decides who owns what.

Summary

- A transfer agent maintains the official register of who owns a security, processes subscriptions and redemptions, issues and cancels shares, and pays out distributions. In the United States they must register with the SEC.

- In tokenized securities, the transfer agent’s off-chain register remains the authoritative legal record of ownership. The token is a digital representation that enables on-chain mobility, not the source of truth.

- If the blockchain and the register disagree, the register wins. Administrators including JPMorgan retain authority to correct the on-chain ledger against the legal record.

- Transfer agents run the allow-list. They screen identity, add approved wallets to an on-chain list, and the token contract blocks transfers to any address that is not on it.

- This inverts crypto’s founding assumption. Whether that is a betrayal or the precise reason institutions will tokenize anything at all is the argument worth having.

Every crypto explainer starts from the same premise: the blockchain is the record, possession of the key is ownership, and no intermediary can reverse it. That premise is true for Bitcoin. It is false for essentially every tokenized security in existence, including the ones BlackRock and JPMorgan are issuing right now. In those products, the authoritative record of who owns what is a database maintained by a company called a transfer agent, and the token in your wallet is a mirror of that database. If the two diverge, the database is right, and the chain gets corrected. Understanding this is not a technicality. It is the difference between understanding what tokenized securities are and repeating a marketing claim about them.

What a transfer agent does

The transfer agent is one of the least glamorous and most load-bearing roles in traditional finance. It exists because a company issuing shares needs someone to answer a deceptively hard question: who owns them right now?

The core functions are these. The transfer agent maintains the register of security holders, the official list of names and balances. It processes transfers when securities change hands, updating that register. It issues new shares when investors subscribe and cancels them when investors redeem. It distributes dividends, interest, and other payments to the holders on the register. And it handles corporate actions, communications, and the reconciliation that keeps everything consistent.

In the United States, transfer agents must register with the SEC under the Exchange Act and operate under its rules. This is not an informal bookkeeping role. It is a regulated function with legal consequences, because the register the agent maintains is what a court would consult to determine ownership.

Traditionally, shares in most listed securities are recorded through a central securities depository, with the Depository Trust and Clearing Corporation performing that function in the US. Each institution keeps its own books, and post-trade steps such as confirmation, clearing, and settlement require multiple intermediaries and repeated reconciliation between those books. The transfer agent sits inside that architecture as the issuer’s official record-keeper.

What changes when a security gets tokenized

The pitch for tokenization is that a shared, consensus-validated ledger replaces fragmented books and eliminates the reconciliation. Instead of every institution maintaining a separate record that must be checked against every other record, all participants read one ledger.

In practice, tokenized securities did not do that. They did something more modest and more interesting.

Tokenized funds use distributed ledger technology to issue and maintain their shares instead of recording them solely through a central depository. That is a real change: settlement collapses from a T+1 or T+2 cycle to minutes, and the share becomes programmable. But the transfer agent did not disappear. It moved.

The structure now looks like this. The transfer agent still maintains the official ownership record. A tokenization platform, most prominently Securitize and also Tokeny, runs the smart contracts that mint tokens on subscription and burn them on redemption. An oracle, typically Chainlink, publishes the fund’s net asset value on-chain. And the token contract enforces the transfer restrictions that the transfer agent’s compliance rules require.

Securitize Transfer Agent LLC is the reference example. It is an SEC-registered transfer agent and broker-dealer, and it maintains the official record for BlackRock’s BUIDL fund. BlackRock’s filing for its OnChain Shares describes Securitize Transfer Agent as maintaining the official record through a permissioned system connected to multiple public, permissionless blockchains, with wallets linked to off-chain identity records.

Franklin Templeton’s structure works the same way: one FOBXX share links to one BENJI token, while the transfer agent maintains the official ownership record through the Benji platform.

Read those descriptions carefully and the architecture becomes clear. A permissioned system, connected to public blockchains, with wallets linked to off-chain identity. The chain is a distribution and mobility layer bolted onto a conventional register. It is not the register.

The token is not the record

This is the single most important idea here, and it is stated backwards in most coverage.

The beneficial ownership of tokenized fund shares remains recorded in the transfer agent’s official register. The token acts as a digital receipt that enables on-chain movement. When a token transfers between two authorized wallets, the system updates the off-chain ownership record to reflect the change. The chain does not replace the register; it triggers an update to it.

And when they disagree? The register wins. JPMorgan, among others, retains the authority to correct discrepancies between the on-chain ledger and the legal record, so that the technological holding never diverges from the legal reality. There is a company with a button that can change what your wallet says, because your wallet was never the authority.

Holding the token does not, by itself, prove ownership. The exact rights depend on the fund’s legal documents, the official ownership record maintained by the transfer agent, and the product’s wallet and transfer rules. The official record is generally the authoritative source.

Consider what that means for a scenario crypto users take for granted. You send tokens to a friend’s wallet. In Bitcoin, that is final and your friend owns them. In a tokenized security, either the transfer fails because the wallet is not allow-listed, or it succeeds and the transfer agent updates the register to reflect the new holder, which happens only because the wallet was pre-approved and identity-linked. There is no version of that transaction where a stranger acquires the security by receiving the token.

Who controls the allow-list

The transfer agent’s most consequential power in tokenized securities is not record-keeping. It is the gate.

Before any subscription, the transfer agent runs know-your-customer and sanctions screening on the wallet owner. The wallet address is then added to an on-chain allow list maintained by the token contract. Smart contracts enforce restrictions from that list: any transfer to an address that is not allow-listed reverts. The BIS has noted that these products rely on the allow-listing of blockchain wallets to constrain peer-to-peer trading and meet regulatory compliance requirements.

The enforcement lives in the token standards. Where stablecoins typically use plain fungible standards such as ERC-20 with unrestricted transfers, tokenized securities often employ security token standards such as ERC-1400 or ERC-3643. Under ERC-3643, a function called isVerified confirms that a recipient appears in the register of allow-listed investors, and canTransfer enforces any additional conditions required before a transfer proceeds. As compliance needs evolve, programmable checks let more complex rules be applied in code.

That is the whole architecture in one sentence: compliance rules, written by a regulated intermediary, enforced automatically by a smart contract, on a public blockchain that anyone can read and almost nobody can transact on.

The practical consequences are worth spelling out. Moving a token to a wallet not on the allow list may be blocked at the protocol or transfer agent level, which is why verifying transfer eligibility before attempting to move a position is not optional. Access through secondary markets or unapproved wallets may not carry the same rights as subscribing directly through the fund or its authorized platform. And restrictions vary sharply by product: some funds are limited to qualified purchasers, some exclude US persons entirely, some impose institutional minimums.

Why this exists

It would be easy to read all of this as institutions gutting the point of a blockchain. The steelman is stronger than that, and it deserves stating properly.

Securities law does not care what technology you use. If an instrument is a security, then rules about who may hold it, how ownership is evidenced, what disclosures are owed, and how sanctions screening works all apply regardless of whether the record sits in Oracle or Ethereum. A tokenized fund that let anonymous wallets hold shares would not be an innovation. It would be an unregistered securities offering with an anti-money-laundering failure attached.

The allow-list model is what makes tokenized funds work inside existing securities and AML frameworks. Without it, none of these products would exist, because no regulated manager would issue them and no regulator would permit it. The choice was never between a permissioned tokenized fund and a permissionless one. It was between a permissioned tokenized fund and no tokenized fund.

And the benefits are real even with the gate in place. Settlement in minutes instead of days. Around-the-clock operation. Shares usable as collateral without leaving the fund, which is why crypto prime brokers accept BUIDL as margin. Real-time auditable records for regulators. Programmability that lets a share do things a book entry cannot. None of that requires the ledger to be the final authority. It only requires the ledger to be fast, shared, and honest about what it is.

The counterargument is equally real. If an intermediary maintains the authoritative record, screens participants, and can reverse the chain, then the blockchain is performing the role of a message bus, and a permissioned database could deliver most of the benefits with less complexity. The transparency argument weakens too, since the interesting record is off-chain. What you are left with is faster settlement and composability with other on-chain assets, which is genuinely valuable but a long way from disintermediation.

Where the two worlds are colliding

The most interesting developments sit exactly at this seam.

The DTCC, the central node in US securities infrastructure, ran its Smart NAV pilot with Chainlink, showing how mutual fund net asset value data can be published on-chain using cross-chain interoperability infrastructure, with multiple global asset managers participating. It has also unveiled a platform for real-time tokenized collateral management. The depository is not being disintermediated. It is tokenizing.

Meanwhile some tokenized funds are pushing the other way. Products including Superstate’s short-duration government securities fund and Franklin’s OnChain US Government Money Fund enable peer-to-peer transactions among approved holders, and BUIDL has been listed on Uniswap’s decentralized exchange for eligible traders. Each step widens the set of things an allow-listed holder can do without going through the issuer, which is a slow migration of function toward the chain without ever surrendering the register.

The tension shows up plainly in retail products. Robinhood’s Stock Tokens are structured as tokenized debt securities that track a stock’s economic performance but confer no voting rights, no shareholder rights, and no direct legal ownership claim on the shares, and they are unavailable to US persons. That is a different structure from a tokenized fund share, and it exists because building a token that conveys actual equity ownership across borders runs straight into the transfer agent and registrar architecture that governs real shares. It is easier to issue a derivative of a stock than to tokenize the stock.

What a failure would look like

A useful way to test whether you understand an architecture is to ask how it breaks, and the transfer agent model has failure modes that differ sharply from the ones crypto users are trained to watch for.

The register and the chain diverge. This is the mundane one and it will happen. A subscription is recorded off-chain but the mint fails. A transfer succeeds on-chain but the register update does not process. For a period, the two records disagree about who owns what. In a permissionless system this would be a crisis with no resolution path. Here it is a reconciliation task, because the hierarchy is defined in advance: the register is authoritative, the chain gets corrected, and administrators such as JPMorgan hold explicit authority to do exactly that. The failure is contained precisely because the system is not decentralized. That is the trade in one sentence.

The transfer agent itself fails. This is the interesting one, and it has no on-chain answer.

If the entity maintaining the register suffers an outage, an insolvency, or a compromise, the authoritative record of ownership is impaired. The tokens still sit in wallets, still display balances, still move between allow-listed addresses. And none of that settles what anyone owns, because the record that decides ownership is the impaired register. Traditional finance has procedures for transfer agent succession, because this risk predates blockchains by a century. But the crypto instinct, which is to point at the chain and say the record is right there, is precisely wrong here. The chain is a mirror. A mirror does not help when the original is gone.

The allow-list becomes the attack surface. Whoever controls which addresses may hold the token controls the asset in a way no key holder does. A compromised allow-list could add unauthorized addresses or, more disruptively, remove legitimate ones, freezing holders out of transfers they are entitled to make. The smart contract will faithfully enforce whatever the list says, because faithful enforcement is its only job. Decentralization does not protect you here; it is what is being enforced against.

Composability breaks at the edge. Tokenized fund shares are increasingly used as collateral across DeFi. But a permissioned token cannot be liquidated to an arbitrary buyer, because arbitrary buyers are not allow-listed. A lending protocol that accepts BUIDL as collateral must have a liquidation path that terminates in an approved wallet, which means its liquidation mechanism depends on a whitelist maintained by a company that has no obligation to that protocol. The composability that makes these tokens attractive is conditional on a permission layer sitting outside the protocol using them, and that dependency has not been tested during a genuine stress event.

None of these are arguments against the model. They are the actual risk register, and it is a different register from the one crypto is used to reading. Nobody is going to lose a tokenized fund position because they mismanaged a seed phrase. They would lose it because an intermediary’s database, an approval list, or a reconciliation process failed, which are exactly the risks tokenization was supposed to have removed and instead relocated.

The question underneath

Strip away the mechanics and one question remains, and it is the one that decides whether tokenization matters.

If the transfer agent’s register is the truth, and the token is a receipt, what exactly has been tokenized? The optimistic answer: the settlement layer, and that alone is worth billions in operational savings and unlocks collateral mobility that did not previously exist. The skeptical answer: nothing important, because the trust assumptions are identical to the ones we had, and we added a blockchain to a system that already worked.

The honest answer is probably that this is a transitional architecture. Right now the register is authoritative and the chain is a mirror, because the law requires a registered intermediary to keep the record and the law has not changed. If it ever does, if a properly regulated on-chain register were permitted to be the record itself, the transfer agent function would not vanish. It would become code plus a compliance oracle, and something would be genuinely different.

Until then, the useful discipline for anyone touching tokenized securities is to hold the correct mental model. The wallet shows you a balance. The register decides whether that balance is yours. Those are two different claims, and only one of them is enforceable in a courtroom.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or legal advice. Tokenized securities are subject to access restrictions and securities regulation, and eligibility, rights, and terms vary by product and jurisdiction. Nothing here is a recommendation to buy any product. Always do your own.

Frequently Asked Questions

What is a transfer agent?

A transfer agent maintains the official register of who owns a security, processes transfers between holders, issues shares on subscription and cancels them on redemption, distributes dividends and interest to registered holders, and handles corporate actions and reconciliation. In the United States, transfer agents must register with the SEC and operate under its rules, making it a regulated function rather than informal bookkeeping.

What does a transfer agent do in tokenized securities?

The same things, plus two more. It maintains the authoritative off-chain ownership register that the tokens mirror, and it controls the allow-list: screening investor identity, adding approved wallets to an on-chain list, and thereby determining which addresses can legally hold the token. The smart contract enforces those decisions automatically, blocking transfers to addresses that have not been approved.

If I hold the token, do I own the security?

Not by itself. The authoritative record is the register maintained by the transfer agent. The token functions as a digital receipt enabling on-chain mobility, and when it moves between approved wallets the off-chain record updates to match. Your actual rights flow from the fund’s legal documents, the register, and the product’s transfer and redemption rules.

What happens if the blockchain and the official record disagree?

The official record wins. Administrators including JPMorgan retain authority to correct discrepancies between the on-chain ledger and the legal record, so the technological holding never diverges from the legal reality. This inverts the usual crypto assumption that the ledger is the final source of truth, and it is the defining characteristic of tokenized securities as currently structured.

Why can I not send tokenized fund shares to any wallet?

Because the token contract enforces an allow-list maintained by the transfer agent. Security token standards such as ERC-1400 and ERC-3643 build the restrictions into the token itself. Under ERC-3643, isVerified checks whether a recipient appears in the register of allow-listed investors and canTransfer enforces additional conditions. A transfer to an unapproved address reverts at the contract level.

Who are the major transfer agents in tokenization?

Securitize is the most prominent. Securitize Transfer Agent LLC is an SEC-registered transfer agent and broker-dealer and maintains the official record for BlackRock’s BUIDL and its OnChain Shares filing. Tokeny is another tokenization platform operating in this space. Franklin Templeton maintains the official record for BENJI through its own Benji platform.

Does this defeat the purpose of using a blockchain?

That is the genuine argument. Critics note that if an intermediary keeps the authoritative record, screens participants, and can reverse the chain, a permissioned database could deliver similar benefits more simply. Supporters note that securities law requires a registered record-keeper regardless of technology, that the allow-list is what makes these products legal at all, and that faster settlement, continuous operation, and collateral mobility are real gains that do not require the ledger to be authoritative.

How does this differ from Robinhood’s Stock Tokens?

Considerably. Robinhood’s Stock Tokens are structured as tokenized debt securities that track a stock’s economic performance but confer no voting rights, no shareholder rights, and no direct ownership claim on the underlying shares, and they are unavailable to US persons. A tokenized fund share represents an actual registered fund position recorded by a transfer agent. It is easier to issue a derivative referencing a stock than to tokenize the stock itself, precisely because of registrar architecture.

A macOS information-stealing malware can hijack Telegram Desktop sessions and compromise cryptocurrency wallets, according to blockchain security firm SlowMist.

The malware harvests data from the macOS Keychain, Safari cookies, Apple Notes, Telegram Desktop and databases associated with more than a dozen cryptocurrency wallets.

After collecting passwords and authenticated sessions, the malware copies users’ authenticated Telegram Desktop session data, wallet databases and browser wallet extension data.

SlowMist said attackers can then attempt to decrypt the stolen wallet databases offline using passwords harvested from the infected device or replace legitimate Ledger and Trezor applications with fake versions that trick users into entering their recovery phrases. The security firm reproduced the attack chain in an isolated environment.

MacOS malware code used to steal keys and passwords. Source: SlowMist

Related: AI has not triggered DeFi ‘hackpocalypse,’ Dragonfly partner says

MacOS malware targets popular crypto wallets

According to SlowMist, the malware combines multiple techniques into a coordinated attack chain, allowing attackers to pursue different methods of compromising cryptocurrency accounts and wallets.

The malware targets software wallets including Exodus, Atomic, Electrum, Wasabi and Monero, as well as hardware wallet applications such as Ledger Live and Trezor Suite, according to SlowMist. It also searches for wallet data stored by full-node clients including Bitcoin Core, Litecoin Core, Dash Core and Dogecoin Core.

Telegram two-step verification does not prevent the attack because the malware reuses an authenticated local session instead of creating a new login, according to SlowMist. In tests, researchers restored stolen Telegram Desktop session data on another Mac without entering a phone number, verification code or two-step verification password.

SlowMist urged users who suspect their devices have been compromised to immediately terminate existing Telegram sessions, establish a new trusted login and change both their Telegram two-step verification password and Telegram Desktop Passcode. The company also recommended generating a new recovery phrase on a clean device and transferring all assets to new addresses.

Magazine: Does Botanix’s failure prove Bitcoiners don’t care about DeFi?

DeFi platform Spreadefi has reported that the total volume of funds users placed in liquidity pools topped $25 million in the second quarter. For a relatively young project, that’s a significant milestone, especially with interest in the decentralized finance sector only gradually picking back up after a long stretch of subdued activity.

Growth in total value locked (TVL) is traditionally seen as one of the key health indicators for a DeFi platform. The more capital users are willing to trust a protocol with, the deeper the liquidity, the more stable the service runs, and the wider the opportunities for further ecosystem development.

What drove the growth?

According to market participants, several factors fed into the increase.

Over the past year, the Spreadefi team has been actively building out the platform’s infrastructure, regularly rolling out technical updates and improving the user experience. A lot of focus went into optimizing liquidity pool management, making smart contracts more efficient, and sharpening the internal algorithms that handle capital allocation.

Beyond the technical side, the project significantly dialed up its public presence. Over the past year, the team has regularly published product development reports, maintained an official blog, shown up at industry conferences, and expanded its footprint inside the crypto community.

For users, that kind of openness is a major trust factor, especially against the backdrop of the countless anonymous projects popping up across the DeFi landscape.

The platform’s growth in 2025

Last year was a period of active scaling for Spreadefi. The team broadened the platform’s functionality, kept pushing liquidity pool staking solutions forward, and put a premium on infrastructure stability.

One of the standout moments was the formal establishment of the company in the United States, coming after more than two years of project development. That step made it possible to boost business transparency and strengthen trust from both users and potential partners.

At the same time, the platform’s community kept growing. The user base expanded, the audience across official channels widened, and the product gradually became more visible alongside other DeFi projects.

Why TVL is considered an important metric

For most decentralized financial platforms, the amount of funds sitting in liquidity pools is one of the primary development indicators.

TVL growth typically signals that users are willing to entrust their assets to a protocol over the long haul. Larger pools also have a positive knock-on effect on platform efficiency, cutting slippage, making trading operations more resilient, and opening up more ways to deploy capital.

That’s why a lot of analysts look at TVL dynamics as one of the most objective measures of a DeFi project’s health.

What’s next?

Spreadefi representatives note that the increase in liquidity pool volume is just one stage of the platform’s development. The team’s immediate plans include further infrastructure expansion, the rollout of new investment instruments, a growing number of supported networks, and ongoing work to sharpen the user experience.

If the current pace holds, Spreadefi will be in a position to strengthen its standing among emerging DeFi platforms and pull in even more users interested in staking and earning through liquidity pools.

In the second quarter, the project has already shown it can attract significant capital. Where things go from here will depend on how well the team keeps the community’s trust, advances its technology base, and adapts to a decentralized finance market that never stands still.

The post Spreadefi Users Deploy Over $25 Million in Liquidity Pools in the Second Quarter appeared first on BeInCrypto.

- 64 billion SHIB have left crypto exchanges today, so far.

- SBI inherited 1.111 trillion SHIB through the Coinhako acquisition.

- Exchange reserves climbed to 86.497 trillion SHIB.

Shiba Inu (SHIB) is navigating two very different stories at the same time.

On one side, the token is gaining more exposure in Asia through a major corporate acquisition involving one of Japan’s largest financial groups.

On the other, fresh on-chain data points to renewed selling pressure as more SHIB moves onto exchanges.

The conflicting signals have left the token under pressure, with buyers struggling to regain momentum despite positive adoption news.

Exchange outflows add pressure to SHIB price

Shiba Inu traded around $0.00000409 after extending its recent decline, reflecting a broader period of weakness across the cryptocurrency market.

The latest on-chain data suggests that exchange activity has become a key factor behind the token’s muted performance.

Data from CryptoQuant showed that 173.45 billion SHIB flowed into cryptocurrency exchanges over the latest 24-hour period, while 271.09 billion SHIB left exchanges.

That resulted in a negative exchange netflow of 97.64 billion SHIB, indicating that more tokens exited trading platforms than entered them.

The latest figures also showed that exchange reserves climbed to 86.497 trillion SHIB, highlighting a larger pool of tokens sitting on trading venues.

During the previous 10-day period, on-chain data showed more than 1.4 trillion SHIB leaving centralised exchanges.

Those outflows had reduced the amount of SHIB immediately available for sale and were viewed as a stronger accumulation signal.

Instead, the latest data points to a reversal in that trend.

Combined with the recent decline in price, the higher exchange balances illustrate the increased selling activity that has weighed on SHIB over recent trading sessions.

Japan expansion strengthens SHIB’s long-term visibility

While on-chain data has turned less favourable in the short term, Shiba Inu has simultaneously received a significant boost in institutional exposure through developments in Japan and Singapore.

SBI Holdings, one of Japan’s largest financial services companies, recently completed its acquisition of Coinhako after receiving approval from the Monetary Authority of Singapore (MAS).

The acquisition also transferred custody of approximately 1.111 trillion SHIB, valued at roughly $4.5 million at the time of the transaction.

The holdings were already part of Coinhako’s customer and exchange reserves, meaning the acquisition did not represent a fresh purchase of SHIB from the open market.

Coinhako manages a digital asset portfolio worth more than $164 million, with SHIB ranking among its larger cryptocurrency holdings.

Following the acquisition, SBI expanded its footprint in Southeast Asia while adding another regulated platform that offers SHIB trading against both the Singapore dollar (SGD) and the US dollar (USD).

The transaction adds to Shiba Inu’s growing presence within regulated Asian cryptocurrency markets.

However, the increased visibility has yet to translate into stronger price performance as traders continue to focus on short-term market activity.

Ripple’s win over the US Securities and Exchange Commission (SEC) had a hidden weapon. Attorney John Deaton says nearly 4,000 XRP holders helped swing the case by telling their stories to the court.

Deaton represented those holders as a friend of the court. He shared how they shaped the outcome, with the revelation coming only days after the ruling turned three years old.

The Judge Read the Holders’ Stories

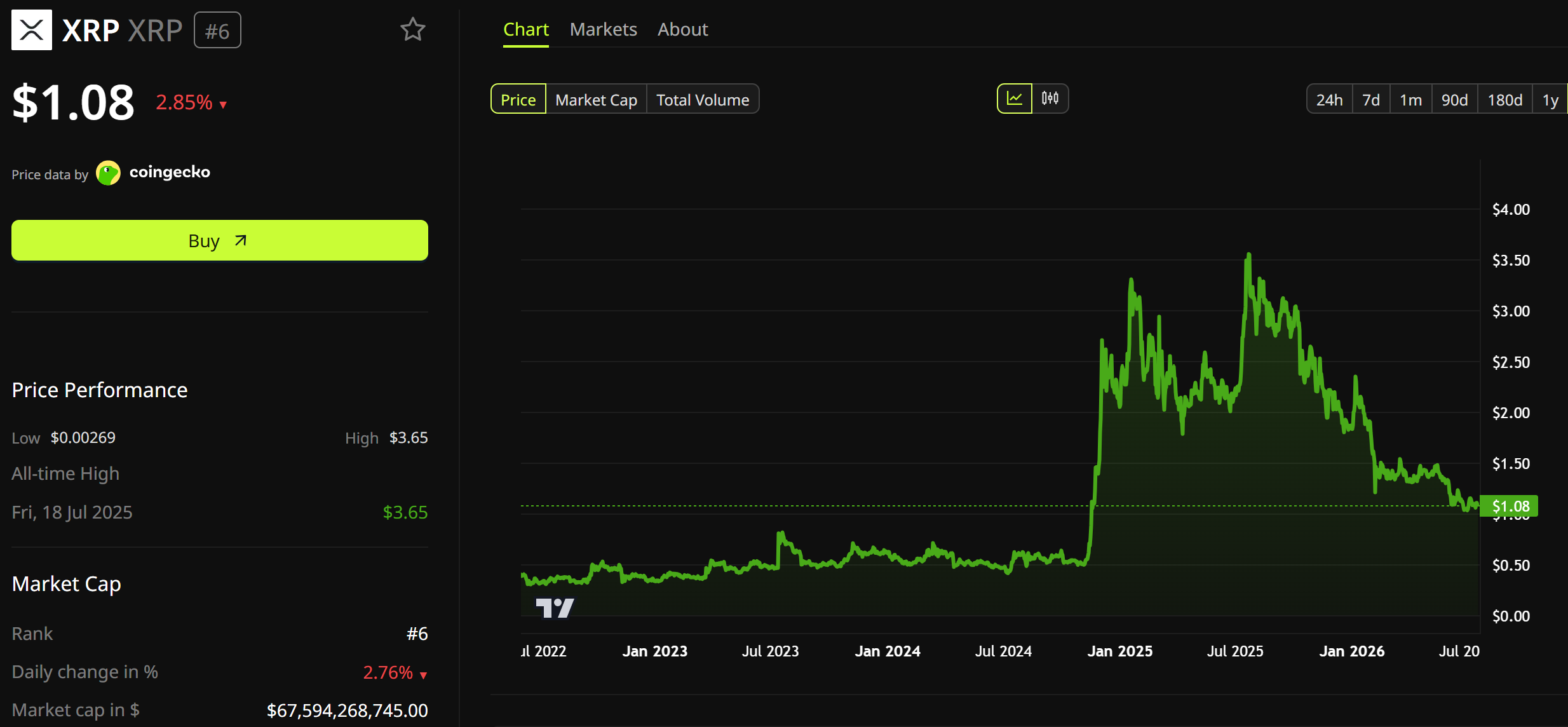

Judge Analisa Torres issued her order on July 13, 2023. XRP itself is not a security, she ruled. However, $728.9 million in direct sales to institutions broke securities law. Sales to everyday buyers on exchanges did not.

Ripple paid a $125 million fine in 2024. The case formally closed in August 2025, when both sides dropped their appeals. The fight almost killed the company first. CEO Brad Garlinghouse admits Ripple nearly shut down rather than face the SEC in court.

So where do the holders come in?

Deaton collected sworn statements from almost 4,000 of them. By his account, Torres cited those statements in her decision and very little else.

“Out of the thousands of exhibits submitted in the case overall, in her final summary judgment decision, she only cited to several dozens exhibits. XRP holder affidavits was one of those exhibits,” Deaton finally revealed.

Follow us on X to get the latest news as it happens

He says the judge also cited his amicus brief and his courtroom exchange in the LBRY case, another SEC crypto lawsuit.

Why Small Holders Made a Big Difference

John Deaton made one simple argument. XRP is just computer code. Code cannot be a security on its own, even if someone sells it like one.

He pointed to orange groves, and that choice was no accident. The Howey test, which is the standard for determining whether something is a security, stems from a 1946 Supreme Court case about Florida orange groves. The groves were sold as investments, yet the fruit itself was never a security. Torres took the same view on XRP.

Meanwhile, Ripple Chief Legal Officer Stuart Alderoty marked the anniversary with a celebratory post declaring an unofficial holiday in honor of the ruling.

The token itself has less to celebrate. XRP traded near $1.08 at press time, down about 3% in a day, per BeInCrypto Markets data.

Still, the ruling shapes US crypto policy today, and Congress is now weighing crypto market structure rules. The bigger lesson may be simpler. Ordinary XRP holders showed up, and a federal judge listened.

The post John Deaton Says 4,000 XRP Holders Helped Secure Ripple’s SEC Victory appeared first on BeInCrypto.

Crypto World

Virtual Protocol Sees Breakout Opportunity Amid Increasing Momentum in the AI Ecosystem Expansion

Virtual Protocol is being closely monitored by traders to see if improved technical strength and ecosystem development could help the cryptocurrency move past important resistance levels. Despite VIRTUAL still trading below its downtrend line, constant defense of key support levels is helping drive the accumulation bias.

However, the positioning in derivatives markets is also neutral, which indicates that market participants are waiting for more proof before taking more leveraged bets. This, coupled with continued development in AI infrastructure, agent commerce, and robotics, keeps the overall outlook interesting.

Technical Structure Suggests Critical Turning Point

Virtual Protocol could continue trading below value due to its prolonged correction, according to recent market analyst Tanaka. Rather than dwelling on its price movements in the short term, it is worth mentioning the ecosystem expansion and development plan that the project is building. The weekly chart provides additional evidence for this viewpoint.

After dropping by almost 90% since its peak levels, VIRTUAL slowly stabilized, creating a downtrend in the form of a descending resistance trendline with consecutive lows. The price is currently trading right under the persistent resistance level, which brings us to a critical turning point for the token.

Price action keeps squeezing between the resistance and the solid support area. Buyers keep entering the market in the accumulation zone, whereas selling activity looks much weaker than before the start of the correction.

Currently, Virtual Protocol is priced at $0.6357, representing an increase of 5.13% over the previous day and 21.73% within the last week. Trading volume for the day amounts to about $102.44 million.

Expanding the AI Ecosystem Serves to Strengthen the Long-Term Narrative

Other than price movements, Virtual Protocol continues to expand the ecosystem of the protocol focusing on AI. One of the primary goals of the protocol is the creation of a system for intelligent AI agents where they can transact autonomously. The process of agent payments, task execution, and autonomous interactions forms an important part of the project’s long-term plan.

The other notable development is the Agent Commerce Protocol, which aims to enable independent AI agents to find each other, negotiate services, and make payments autonomously. This commerce layer might prove to be one of the most useful long-term aspects of the protocol, according to Tanaka.

VIRTUAL also acts as the key asset in the entire ecosystem. The agent tokens make use of the VIRTUAL trading pairs for their liquidity, whereas transactions made between AI agents through commerce are done using the token.

Further growth of the ecosystem is continuing via integrations with Base, Robinhood Chain, and robotics programs. Eastworlds is also collaborating with Unitree Robotics to experiment with the physical implementation of AI. Although this will contribute to making the future outlook of the platform more positive, validation of adoption and revenue generation is still needed.

Funding Rates Are Evidence of Well-Balanced Positioning

The analysis of derivatives data reveals a similarly balanced view of the prevailing market positioning. OI-weighted funding rates stayed relatively neutral despite prolonged market weakness. There was neither any domination of bulls nor bears during the latest period of trading activities, implying balanced market participation in perpetual futures trading.

Previously, in case of the price decline, there were occasional moments when funding rates went below the zero level due to increasing bearish positioning. But these were never extremely low values that indicate a state of market capitulation. Recently, funding rates moved around the equilibrium point along with the price consolidation in a narrow range.

Resistance Breakout Is the Critical Technical Level

For now, the key technical factors for Virtual Protocol are the positive improvement in technical stability, ecosystem development, and the neutral derivatives sentiment. Virtual Protocol still builds infrastructure through AI agents, autonomous commerce, and robotics and enjoys positive support from the long-term accumulation area.

Despite that, the falling resistance trendline is the main technical barrier at the moment. Its breakout might confirm bullish momentum and change the market structure, while inability to do that will keep the ongoing range. Until this critical move takes place, traders will watch whether accumulation, ecosystem development, and stable market positioning can help form the next trend for Virtual Protocol.

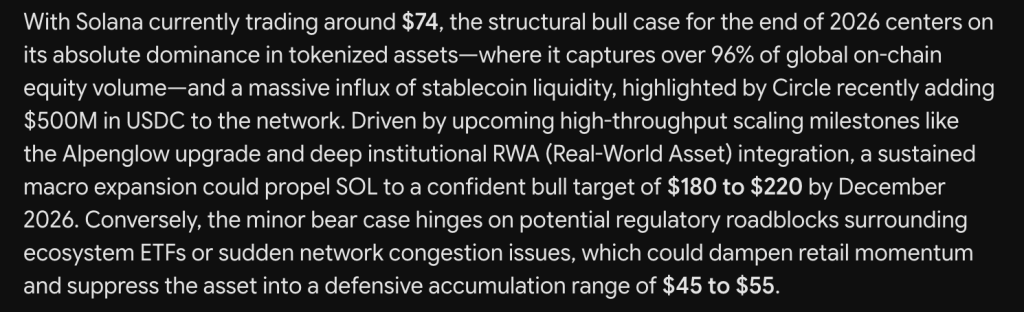

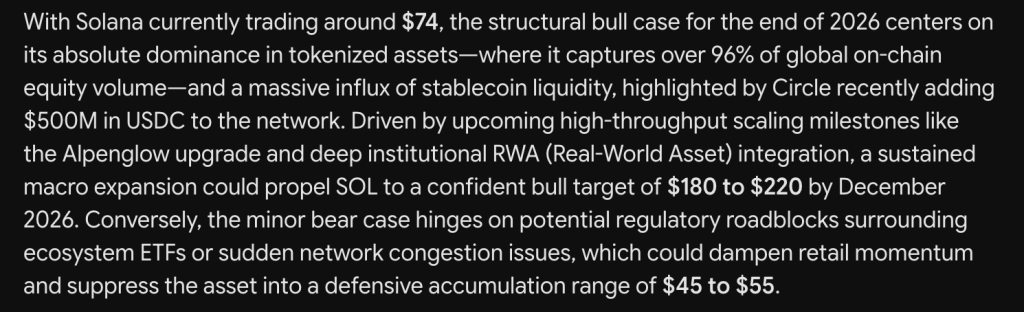

Google Gemini AI predicts a Solana price target that skips the usual talking points and goes straight to a number that made us pause.

Over 96% of global on-chain equity volume runs through Solana right now. That is not a growing market share story; that is a market that has already been won.

From $74, Gemini puts the December 2026 target at $180 to $220. Stablecoin liquidity is doing real work here too, with Circle adding $500M in USDC to the network in a single move.

The forward-looking piece is the Alpenglow upgrade, aimed at pushing throughput into territory that makes high-frequency use cases viable on chain for the first time. Pair that with deep institutional integration into real-world assets, and Gemini’s thesis is less about speculation and more about infrastructure quietly becoming unavoidable.

A sustained macro expansion is the condition attached to all of it. Without a broader risk appetite returning, even dominant infrastructure sits underpriced.

The bear case Gemini offers is almost an afterthought by comparison. Regulatory roadblocks around ecosystem ETFs or a sudden bout of network congestion could dampen retail momentum and push SOL into a defensive range of $45 to $55.

That is a specific, bounded downside rather than a collapse scenario. It reads more like a pause than a reversal.

Discover: The Best Token Presales

Solana Price Prediction: SOL RSI Just Crossed A Line It Has Not Held Since October

Price closed at $74.67, down 0.78%, with the session ranging between $74.12 and $75.69. On its own, that is an unremarkable day, but the chart underneath it tells a longer and more interesting story.

SOL peaked near $257 in September 2025, and the decline from there was almost uninterrupted through the February crash below $80. Since that crash, price has spent five months carving a wide range between roughly $60 and $100, with three separate rally attempts, March, May, and now July, each stalling near the same $95 to $100 ceiling.

That repetition matters. A level that rejects price three times stops being a coincidence and starts being the market’s actual opinion on fair value.

Support sits at $70, then the June low near $60 that has held twice now. Resistance stacks at $80, then $85, then that stubborn $95 to $100 zone.

The RSI panel shows something worth pausing on. RSI reads 46.03 with the signal line at 54.63, and that signal line has been climbing steadily since the June bottom, tracking the price recovery closely.

The current gap is negative, meaning short-term momentum has cooled slightly after the recent bounce, but the broader trend in the signal line itself is the more telling detail. It has not been this elevated since October, back when SOL was still trading above $200.

For Gemini AI, as it predicts, a $180 prediction becomes plausible. Solana needs to finally close above $100 with conviction, something it has failed to do three separate times since February. The infrastructure case may already be true. The chart has not been asked to agree with it yet.

Discover: The best crypto to diversify your portfolio with

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

You Might Like What Gemini AI Predicts About This New Layer 3 Called LiquidChain

The money that wins cycles never waits at resistance.

Large caps are stuck. Bitcoin, Ethereum, and XRP keep testing the same ceilings with nothing breaking through. Every macro catalyst has a new arrival date. Every institutional wave has a new quarter attached. Waiting on someone else’s decision is not a trade.

Small market cap infrastructure plays operate on completely different physics. A rotation that vanishes as noise at Bitcoin’s scale reprices an undiscovered project by multiples. The opportunity lies in the gap between what something is genuinely worth and what the market has assigned it. That gap closes permanently the moment discovery happens.

Multi-chain fragmentation is one of the most expensive unsolved problems in DeFi. Bitcoin, Ethereum, and Solana run as completely isolated systems. No shared architecture. No native interoperability. Every time value crosses those boundaries it pays in fees, slippage, and failed transactions.

LiquidChain makes the crossing free. Gemini AI predicts and agrees. All 3 networks inside one execution environment. Single deployment. Complete ecosystem access. No tax on any interaction.

The presale is at $0.01454 with just over $900,000 raised. Early and undiscovered. That combination does not last long.

Explore the LiquidChain Presale

The post Google Gemini AI Reveals Shocking Solana Price Target for 2026 appeared first on Cryptonews.

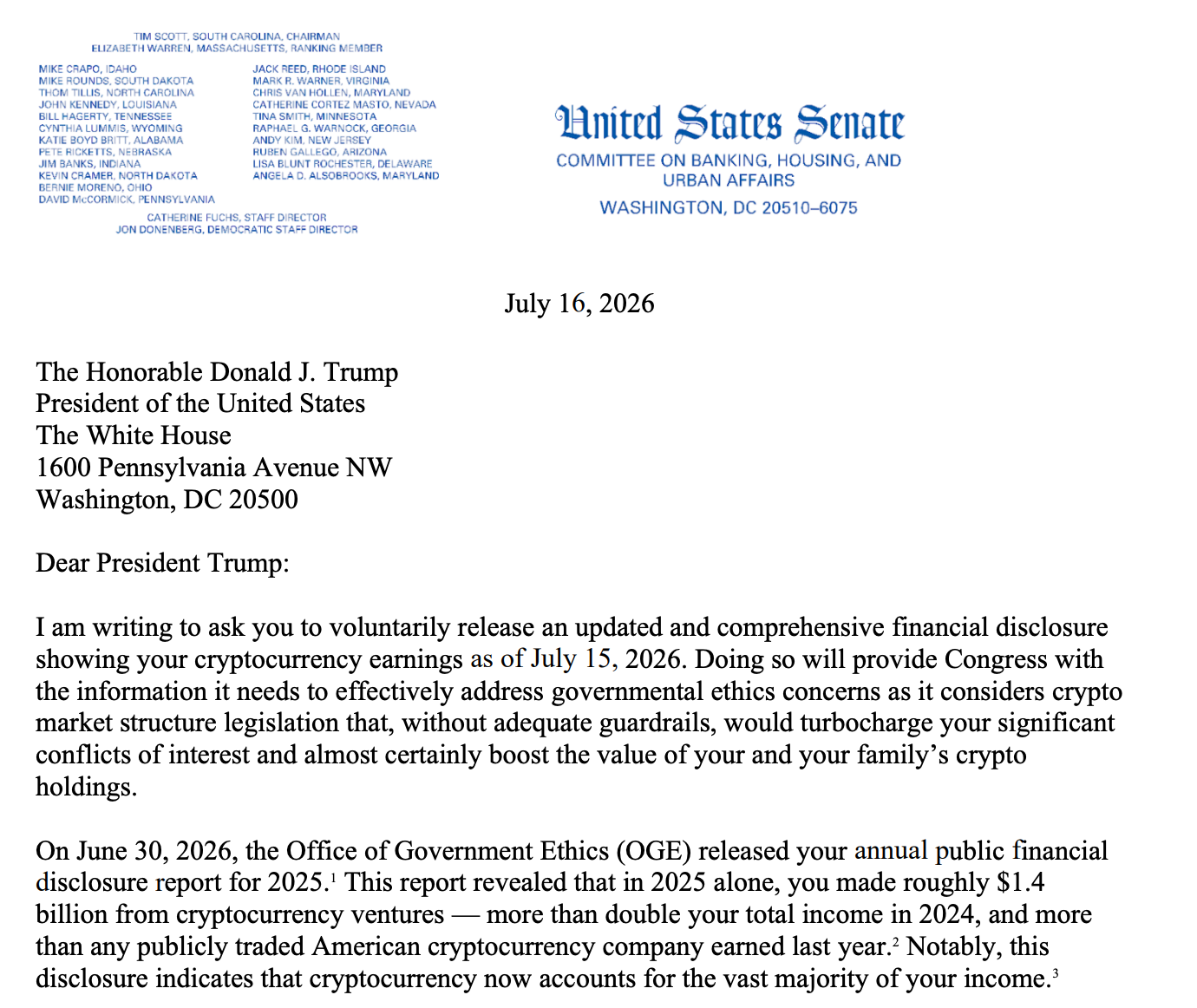

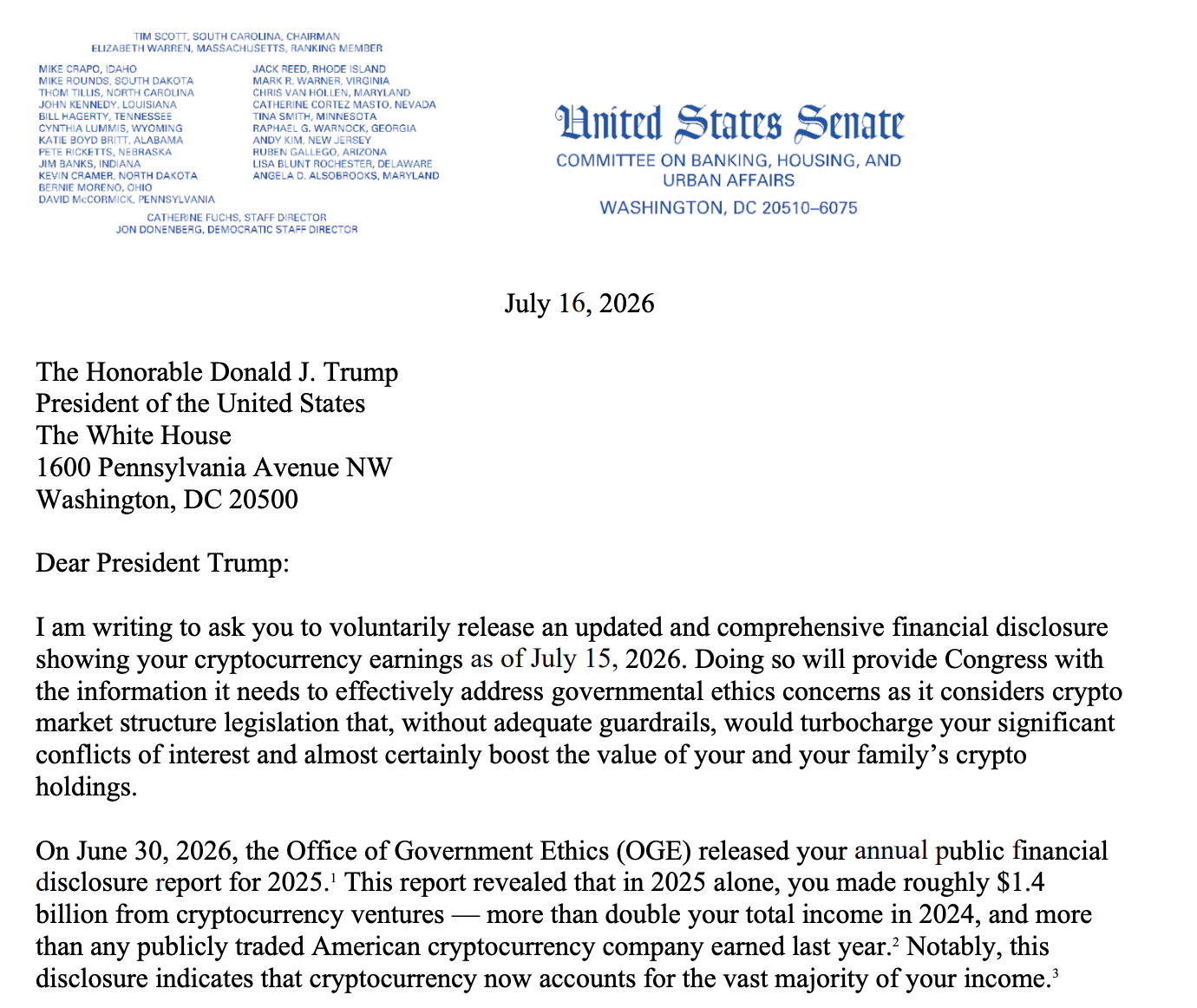

Senator Elizabeth Warren has urged President Donald Trump to provide updated financial disclosures covering his cryptocurrency earnings for the first half of 2026, arguing the information is especially important as the US Senate weighs legislation that could reshape the crypto market.

In a letter sent on Thursday, Warren requested that Trump voluntarily release a report detailing crypto-related income between Jan. 1 and July 15. The request comes amid heightened scrutiny of how crypto policy might affect the value of the president’s and his family’s reported holdings.

Key takeaways

- Elizabeth Warren is asking Trump to disclose crypto earnings for Jan. 1–July 15, ahead of the president’s normal filing timeline for 2026.

- Warren pointed to Trump’s 2025 disclosures, which reportedly showed $1.4 billion in crypto-related earnings.

- The senator’s concern ties directly to pending Senate action on the Digital Asset Market Clarity (CLARITY) Act.

- Majority Leader John Thune indicated the Senate aims to hold a vote on the bill before August states work periods begin.

- On the House side, a CLARITY hearing was held in New York, while some Democrats have signaled they will require stronger ethics guardrails before supporting the bill.

Warren presses for earlier crypto earnings disclosures

Warren’s letter asks Trump to publish updated financial disclosures covering crypto earnings for the period from Jan. 1 to July 15. She framed the timing as crucial because the Senate is considering the Digital Asset Market Clarity (CLARITY) Act, legislation intended to clarify rules for digital assets and market structure.

Warren said Trump’s disclosure raises “key questions” about whether presidents, senior administration officials, members of Congress, and their families should profit from the crypto industry while the federal government debates rules that could influence market outcomes.

She also emphasized that, under current disclosure requirements, Trump is not expected to file his full 2026 annual report until May 2027. Still, Warren requested voluntary publication by July 23 so it aligns with the Senate’s consideration of the CLARITY bill.

What Warren cited from Trump’s 2025 disclosures

The pressure is grounded in disclosures Warren referenced from Trump’s 2025 earnings reporting. Earlier coverage cited filings showing Trump earned $1.4 billion from crypto-related ventures in 2025, including through his memecoin, Official Trump (TRUMP), and through World Liberty Financial, according to the reporting linked in the article.

That point is central to Warren’s argument: she contends that legislation under debate could “turbocharge” conflicts of interest if ethics guardrails are not tightened, potentially increasing the value of holdings held by the president and his family.

“[W]ithout adequate guardrails, [CLARITY] would turbocharge the President’s significant conflicts of interest and almost certainly boost the value of his and his family’s crypto holdings.”

House and Senate movement on CLARITY, with ethics concerns looming

The Warren letter arrives as Congress advances CLARITY through committee and floor planning. According to Senate Majority Leader John Thune, the chamber intends to hold a vote on the crypto bill before the Senate breaks for August states work periods.

At the same time, the political dynamics around the bill appear closely tied to ethics conditions. The article notes that many Democrats have said they would not support any legislation without clear ethics provisions, with some pointing to potential conflicts of interest linked to Trump’s crypto investments.

Earlier in the process, Trump has publicly denied wrongdoing related to his crypto activity. The article references a July 2 interview in which Trump said there was “nothing illegal” and “nothing wrong” with profiting from his crypto investments while in office.

House committee hearing highlights bipartisan claims—and missing Democrats

While the Senate focuses on timing for a full-vote window, House activity has been moving in parallel. On Friday, the House Financial Services Committee’s Subcommittee on Digital Assets, Financial Technology, and Artificial Intelligence held a field hearing in New York City on the CLARITY Act.

The bill has already passed the House, in July 2025. If the Senate approves it with 60 votes, it would return to the chamber for final consideration. Representative French Hill, who chairs the full committee and attended the hearing, described CLARITY as a “bipartisan priority” for Congress.

However, the hearing reportedly did not include Democratic representatives from the committee. Cointelegraph reached out to Democratic lawmakers for comment but did not receive an immediate response, according to the article.

With the Senate vote reportedly targeting a pre-August window, the immediate question for investors and policy watchers is whether ethics requirements—especially disclosures and guardrails—will be strengthened enough to address concerns raised by Warren and other Democrats. The requested July 23 disclosure deadline may become an early test of how closely market structure legislation and conflict-of-interest scrutiny will be linked in practice.

OKX Europe has introduced a “one-way conversion” option that allows customers to deposit USDT and convert it into USDC within the exchange, creating a regulated off-ramp as Europe’s Markets in Crypto-Assets (MiCA) framework restricts support for non-authorized stablecoins.

In a company announcement provided to Cointelegraph, OKX Europe said users can send Tether’s USDt (USDT) to their OKX Europe account and then convert the deposit into USDC, a stablecoin that is among the major options compliant with MiCA’s requirements. The feature is positioned as a migration path for customers whose existing platforms no longer accept USDT or are moving them to alternatives.

Key takeaways

- OKX Europe lets customers convert deposited USDT into USDC on the exchange, rather than keeping USDT balances active.

- The change reflects MiCA constraints: Tether has not obtained authorization for USDT issuance under MiCA.

- OKX Europe says conversions are initiated at the customer’s discretion, not pushed through a platform-imposed deadline.

- The decision underscores how USDT accessibility in Europe is tightening even as it remains the largest stablecoin globally.

- OKX Europe operates for users across 30 EU and European Economic Area (EEA) countries under its MiCA license.

MiCA’s stablecoin licensing pressure reaches everyday flows

MiCA’s rollout has affected how European platforms handle stablecoins—particularly those whose issuers have not secured authorization to issue the relevant asset under the new regime. According to OKX Europe’s announcement, its new one-way conversion feature is aimed at customers who are dealing with service changes elsewhere and still want to maintain stablecoin exposure, but in an asset that fits the MiCA-compliant environment.

The core problem stems from the fact that Tether has not obtained MiCA authorization for USDT issuance. As MiCA took full effect across the EU on July 1 (per the article’s timeline), many crypto platforms moved to restrict USDT deposits, remove or limit trading pairs, or automatically shift customer balances toward compliant alternatives.

OKX Europe’s approach is notable because it does not present conversion as an after-the-fact compliance step imposed by a fixed cutoff. Instead, the exchange said conversions can be completed at the customer’s discretion, which may help reduce forced timing decisions for users managing their own balances.

Why USDT still matters—even as platforms reroute users

The rollout comes as USDT remains dominant in global stablecoin usage. DefiLlama data cited in the announcement indicates Tether controls roughly 59% of the stablecoin market, with market capitalization around $184 billion out of nearly $310 billion in total stablecoin value. By comparison, Circle’s USDC is shown at about $73 billion market cap.

This imbalance helps explain why MiCA-compliant migration tools are likely to remain in demand: even if a region limits USDT functionality, USDT still represents a large portion of users’ circulating balances and trading inventory. Features that allow “in-exchange” conversion can therefore act as a bridge—keeping liquidity moving into compliant stables without forcing users to seek off-platform solutions.

Tether’s stance on MiCA—and the ripple effect in Europe

Tether’s decision not to seek MiCA authorization for USDT has been a persistent point of contention. Tether has defended that position even as exchanges across the EU adjusted their offerings in response to the regulatory framework’s start in late 2024, according to earlier reporting attributed to Cointelegraph.

In a May 2025 interview with Cointelegraph, Tether CEO Paolo Ardoino criticized MiCA’s reserve requirements. He argued the framework could introduce unnecessary risk for stablecoin issuers by requiring part of reserves to be held with European credit institutions. In that context, Ardoino suggested Tether chose not to pursue authorization despite the likelihood that USDT would lose support on European exchanges.

Ardoino has reiterated a similar posture since then. In a July 2025 post on X referenced in the original reporting, he said Tether would reconsider applying for MiCA authorization only “when MiCA becomes safer for consumers and stablecoin issuers,” signaling that the company views the current structure as fundamentally unfavorable rather than merely temporary.

Meanwhile, other companies have already acted on the basis of regulatory and operational risk. Earlier coverage cited in the article notes that digital banking platform Revolut said it would stop supporting USDT for customers in the EEA and Switzerland, giving users until Aug. 31 to sell or withdraw their holdings before any remaining balances are automatically converted into their base currency. That kind of consumer-facing change illustrates how MiCA’s stablecoin restrictions are not confined to exchanges but can propagate through payment and custody layers as well.

What OKX Europe’s conversion feature changes for users

For OKX Europe customers, the practical implication is straightforward: if they hold USDT, they can still move value into the exchange and then convert into USDC—potentially preserving stablecoin utility without running into deposit restrictions or trading-pair limitations that some platforms have applied.

OKX Europe also framed the tool as a way for users to adapt when “existing platforms” no longer accept USDT or when migration happens automatically. By allowing conversions at the customer’s discretion rather than attaching them to a strict, platform-set deadline, OKX Europe appears to be trying to reduce friction around the timing of stablecoin transitions.

Still, the change is a reminder that USDT access in Europe is increasingly conditional on regulatory structure. Until Tether’s USDT issuance becomes MiCA-authorized—or until the regulatory posture of specific platforms changes—users should expect more “migration” mechanics like this to appear across major trading venues.

As MiCA licensing expands and platforms continue adjusting their stablecoin support, readers should watch whether more exchanges adopt similar conversion-only flows and whether any shift occurs in Tether’s stance on seeking authorization; the next wave will likely depend on both regulatory decisions and how quickly compliant stablecoins can absorb migrating liquidity.

Crypto World

Senator Warren Requests 2026 Reporting for Trump’s Crypto Earnings after $1.4B Disclosure

Senator Elizabeth Warren, one of the more outspoken voices in the US Congress associating digital assets with illicit activities, has called on President Donald Trump to release additional information on his crypto investments ahead of a mandated deadline.

In a Thursday letter, Warren requested Trump voluntarily release a financial disclosure report on his earnings related to cryptocurrency between Jan. 1 and July 15. The request came after Trump’s 2025 financial disclosures showed he had earned $1.4 billion from crypto-related ventures in 2025, including through his memecoin, Official Trump (TRUMP), and his family’s company World Liberty Financial.

“Your financial disclosure raises key questions about the appropriateness of Presidents, Vice Presidents, senior administration officials, members of Congress, and their families profiting off the crypto industry, just as the US Senate debates crypto market structure legislation that has the potential to increase the value of your crypto holdings,” said Warren.

Thursday letter from Elizabeth Warren requesting financial disclosures from Donald Trump. Source: Senate Banking Committee

Trump’s 2025 disclosure was filed on June 30 as part of a US Office of Government Ethics mandate to prevent conflicts of interest with elected officials. Warren noted that the president was not required to file his 2026 annual report until May 2027, but requested that he do so voluntarily by July 23 as the Senate considers a crypto market structure bill, the Digital Asset Market Clarity (CLARITY) Act.

Warren added:

“[W]ithout adequate guardrails, [CLARITY] would turbocharge the President’s significant conflicts of interest and almost certainly boost the value of his and his family’s crypto holdings.”

Related: US indicts crypto investor over alleged $20M fraud scheme

Cointelegraph reached out to the White House and Warren’s office for comment but did not receive an immediate response. In a July 2 interview, Trump said that there was “nothing illegal” and “nothing wrong” with profiting from his crypto investments as president.

According to Senate Majority Leader John Thune, the chamber will hold a vote on the crypto bill before the Senate breaks for August states work periods. However, many Democrats have publicly said that they will not support any legislation without clear provisions on ethics, with some citing Trump’s potential conflicts of interest.

House Republicans hold CLARITY hearing as Senate debates bill

On Friday, the House Financial Services Committee’s Subcommittee on Digital Assets, Financial Technology, and Artificial Intelligence held a field hearing in New York City on the CLARITY Act. Although the bill was already passed by the House of Representatives in July 2025, it will return to the chamber if approved with 60 votes in the Senate.

Representative French Hill, who chairs the full committee and attended on Friday, said CLARITY has been “a bipartisan priority” for Congress. However, no Democratic representatives appeared to be present at the hearing. Cointelegraph reached out to Democratic lawmakers on the committee for comment but did not receive an immediate response.

Magazine: Crypto’s CLARITY Act faces partisan fight over ethics on Senate floor

![]()

The lack of an ethics provision remains one of the biggest sticking points. Sen. Ruben Gallego (D-Ariz.), one of two Democrats who voted to advance the bill out of the Senate Banking Committee, has repeatedly said he will not support the legislation on the Senate floor without a bipartisan ethics provision. Other Democrats have raised similar concerns over conflicts of interest involving public officials and digital assets.

As of Friday, there had been no public readout from Thursday’s White House meeting, and no bipartisan ethics language had emerged, leaving one of the bill’s largest obstacles unresolved.

If passed, the Clarity Act would establish a federal framework for digital asset markets by drawing a clearer line between assets regulated by the Securities and Exchange Commission (SEC) and those overseen by the Commodity Futures Trading Commission (CFTC). Supporters argue the measure would replace years of regulation through enforcement with rules written by Congress.

Industry executives reiterated that message during a House hearing Friday marking one year since the chamber passed the legislation.

“The community has already done the hard work,” Nova Labs executive Sarah Aberg told lawmakers, arguing that regulatory uncertainty delayed investment in the Helium wireless network after the SEC sued the company in a case that was later settled. “Clarity is not a call for deregulation; it is a call for the right regulation from the right regulator.”

WATCH LIVE: Vought testifies on Consumer Financial Protection Bureau in Senate hearing

Andy Burnham’s five big pledges ‘to change Britain’: From public ownership to devolving power

8 Great Sci-Fi Shows Overshadowed by ‘Lost’

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

NewsBeat1 day ago

NewsBeat1 day agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Crypto World2 days ago

Crypto World2 days agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Politics2 days ago

Politics2 days agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

Business2 days ago

Business2 days agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Entertainment2 days ago

Entertainment2 days agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

News Videos3 days ago

News Videos3 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech4 days ago

Tech4 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Crypto World22 hours ago

Crypto World22 hours agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

NewsBeat7 hours ago

NewsBeat7 hours agoRegistration is now open for March for Men with Kev 2026

-

Tech3 days ago

Tech3 days agoDark Secrets Emerge When Jailbreaking LLMs

-

Business2 days ago

Business2 days agoPalantir Shares Rise After Expanded Nvidia Partnership and Fresh Analyst Upgrades Ahead of Earnings Day

-

News Videos12 hours ago

News Videos12 hours agoMoney | Class 12 Economics | CBSE Board Exam 2026-27

-

Sports2 days ago

Sports2 days agoNew Cornerback Enters Vikings Trade Rumor Mill

-

Fashion1 hour ago

Fashion1 hour agoWeekend Open Thread – Corporette.com

-

Business18 hours ago

Business18 hours agoBanco Bilbao Vizcaya Argentaria, S.A. (BBVA) Discusses Global Macro Environment and Economic Outlook for Core Markets Transcript

-

Tech4 days ago

Tech4 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

News Videos4 days ago

News Videos4 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Entertainment2 days ago

Entertainment2 days agoVicki Gunvalson Defends Discussing Heather Dubrow’s Money

-

Crypto World3 days ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

You must be logged in to post a comment Login