Cyclist Shaun Reilly had come off his bike and was standing at the side of the road in East Whitburn, West Lothian, when he was involved in the collision early on Saturday.

15:54, 15 Feb 2026Updated 15:55, 15 Feb 2026

Tributes have been paid to a “proud” Scots dad who died in a collision involving a van.

The cyclist, named locally as Shaun Reilly, had come off his bike and was standing at the side of the road on Main Street in East Whitburn, West Lothian, when he was involved in the collision with the white Vauxhall van just after 6am on Saturday.

Emergency crews were called to the scene but the 34-year old tragically died at the scene.

Advertisement

The driver of the vehicle, a white Vauxhall van, was uninjured.

Police appealed for anyone with information on the crash to come forward as loved ones paid tribute to the married dad on Sunday.

One friend said on Facebook that “heaven has gained a proper angel”.

They wrote: “I don’t even have the right words to express how much I’m gonna miss you.”

Advertisement

In a message to Shaun’s partner, who he wed three years ago, they wrote: “I can’t begin to imagine what your going through my hearts broken for you but you and those boys were his world he was so so proud.”

A loved one also paid tribute on Facebook, saying: “Still can’t believe this is real! Your gonna be sadly missed.

“Rest easy buddy. You’ll never be forgotten.”

Advertisement

Another tribute read: “Sleep tight my wee pal.”

Police taped off the road following the early hour crash and motorists were asked to use alternative routes.

Photos taken from the scene showed a large cordon in place and multiple police vehicles in attendance.

Anyone with any information, or who may have seen the white Vauxhall van or the cyclist in the area around the time of the crash are urged to get in touch.

Advertisement

Sergeant Fraser Mitchell said: “Our thoughts are with the family and friends of the man who died in this crash. Enquiries are ongoing to establish the full circumstances of what happened.

“I am appealing to anyone who has information to come forward. If anyone saw the white Vauxhall van or a cyclist on or off a black pedal cycle in the area around the time of the collision, please contact us.

“I would also urge anyone who has dash-cam or personal footage to please review it and get in touch if there is anything that may be relevant to our investigation.”

Get more Daily Record exclusives by signing up for free to Google’s preferred sources. Click HERE

Race Across the World is back with five teams racing from Sicily to Mongolia for a £20,000 prize.

Courtney Eales Trends writer and Hayley Anderson Screen Time TV Reporter

16:20, 02 Apr 2026

The BBC’s beloved travel competition Race Across the World is set to return for its sixth series tonight.

The forthcoming season has been billed as “the toughest journey yet” as five teams cover more than 12,000km across Europe and Asia.

Advertisement

Stripped of smartphones and bank cards, and armed only with the cash equivalent of an economy flight along the route, the competition will challenge five teams both physically and emotionally, pushing each to their absolute limits. Just one team will cross the finish line and take home the £20,000 prize.

The teams will set off from Palermo on the island of Sicily, heading all the way to the remote village of Hatgal on the shores of Lake Hövsgöl in northern Mongolia.

The route will pass through eight countries: Italy, Greece, Turkey, Georgia, Kazakhstan, Uzbekistan, Kyrgyzstan and Mongolia.

The 2025 series of Race Across the World concluded with mother and son duo Caroline and Tom becoming the first pair to reach the final checkpoint in Kanniyakumari and scoop the £20,000 prize. This series, a fresh set of contestants will be hoping to emulate their achievement.

In what promises to be the most gruelling race to date, conditions could swing from scorching 30-degree Mediterranean heat to subarctic lows of –20°C.

Each pair will be allocated a budget of under £26 per person per day. Details of the contestants and the show’s broadcast time can be found below.

Advertisement

How to watch Race Across the World 2026 and what time is it on?

Race Across the World returns with series 6 on Thursday April 2, 2026, at 8pm on BBC One and iPlayer.

Following the opening episode, the nine-episode series will continue every Thursday through to the finale, which airs on Thursday May 28, 2026. Episodes are also available to stream on BBC iPlayer.

Meet the Race Across the World 2026 cast

Jo and Kush

Jo and Kush are lifelong best mates from Liverpool. Jo is a 19 year old college student while Kush is a 19 year old gap-year student.

Advertisement

They are the youngest participants in the forthcoming series. Both are still residing at home with their families and chose to take part because they were “at a sort of standstill in deciding what to do” with their futures.

Kush told BBC: “So, when the opportunity came up, we thought it would be a fantastic experience and something we could look back on and learn from.”

Jo added: “We had just finished sixth form, got our A-Levels and the opportunity to travel with the race before we go to university, made it even more exciting for us.”

Katie and Harrison

Katie is a 21 year old account manager while her older brother Harrison is a 23 year old finance assistant from Manchester.

Discussing the motivation for participating in the programme, Harrison said: “It was an opportunity to travel that I wouldn’t have given myself the opportunity to do.

“I would have just gone down the standard life path of work, university, carrying on working and buying a house. I would never have given myself an opportunity to go out there and travel and take that time off from being responsible.”

Molly and Andrew

Junior doctor Molly, 23, and her father Andrew, a 54 year old geography teacher, are eagerly anticipating the forthcoming series.

Molly explained: “We keep calling it a joke gone too far. We were sitting watching it on TV one night, and the option to apply came up and every time we watch it, we always say that we would love to do it.

“The next day, the ad popped up on daddy’s Facebook, and so we put an application in thinking nothing of it, and it’s kind of just been a whirlwind since then.”

Andrew informed the BBC he is “living the dream” and it’s something he’s always aspired to do.

Advertisement

Puja and Roshni

Doctor Puja, 31, and her cousin Roshni, 32, a software engineer, both hail from London. Having dedicated their twenties to establishing thriving careers, they’ve now chosen to take a gamble.

Puja revealed: “I’ve been a massive fan of the show for years, since the first season came out. During the time I applied, I had hit a career block, and I decided that if I was hitting a career block, I would do something that I wanted to do for a very long time and so decided to apply for the race.

“That was the predominant reason why I just wanted to do something that was for myself, for my personal life, and something that will give me memories to last the rest of my life.”

Advertisement

Mark and Margo

Mark, a 66 year old retired architect from London, and Margo, a 59 year old hypnotherapist from Liverpool, have navigated a typically turbulent in-law dynamic over the past 40 years.

However, having recently set aside their differences while uniting to care for a loved one, the pair have discovered a newfound appreciation for one another’s company.

Reflecting on the programme, Margo said: “Someone told me about the series, and I watched it and went, ‘that’s got me written all over it’. I just love impulsive, crazy things and adventure. I said, ‘I’m going to do that’ and the first person who came to mind was Mark.’

Advertisement

“It seemed like a good time in our lives. We’ve been through this experience with losing my big sister and him losing his wife.

“It seemed like a celebratory thing that we could do together. This was a new journey that could be exciting and like a renewal.”

Race Across the World 2026 premieres on Thursday, April 2, at 8pm on BBC One and BBC iPlayer.

A personal trainer has revealed a simple hack to reduce blood pressure that can be done anytime and anywhere.

High blood pressure is often called the silent killer, quietly affecting millions until serious health problems emerge. If left unchecked, it can significantly increase the risk of heart attacks and strokes. Yet, its impact is not always obvious.

Advertisement

Day-to-day health can suffer in less noticeable ways, from circulation issues to erectile problems and reduced overall wellbeing. While medications and professional treatments remain the primary approach, experts are highlighting a simple item that costs just 77p.

Personal trainer Toby King, speaking to adult website SoloFun, explains that regularly squeezing a tennis ball over a few weeks may contribute to lowering blood pressure. “When you get diagnosed with high blood pressure, you are often told to exercise, and while exercising will help, it can be confusing to know what to do,” Toby says.

“Squeezing a tennis ball or a stress ball if you have one is known as an isometric handgrip exercise that anyone can do, whether they are commuting on the train or sitting at their desk in the office.”

The exercise works through isometric handgrip training, which involves contracting muscles without movement. This contraction increases blood flow and encourages the expansion of blood vessels, which can help reduce blood pressure.

Advertisement

Research has shown that performing these exercises several times a week can lower readings by more than five millimetres of mercury.

Toby adds: “When you squeeze and hold the tennis ball, your muscles will stay under tension without performing a whole exercise. This control puts pressure through your muscles and blood vessels for a short period and helps the blood vessels to become more efficient.”

The method is straightforward.

Advertisement

Grab a tennis ball in one hand and squeeze it at roughly 50 percent of your maximum grip strength.

Hold this grip for two minutes, rest briefly, then repeat the process three times in total.

Toby emphasises: “The best way to think about this is to take a firm grip rather than trying to crush the ball. If you use too much force, then you won’t be able to grip for the full two minutes.”

While the exercise is not a substitute for medical treatment, it offers a practical, natural way to support cardiovascular health.

Advertisement

Studies suggest that consistent use of handgrip exercises can reduce blood pressure by between five and twenty millimetres of mercury, depending on the individual.

Advertisement

“You won’t see overnight results with this, but this small habit that takes a few minutes to perform will make a difference over time,” Toby says.

Lowering blood pressure can have a number of health benefits, but it can also improve sexual health, which is often overlooked.

In men, high blood pressure can contribute to erectile dysfunction. In women, it may reduce arousal, cause vaginal dryness, and make orgasms more difficult to achieve.

Toby highlights the broader benefits: “When you improve your blood pressure, you improve your overall health, which can affect your energy, confidence and your overall quality of life.”

Neil Mackinnon spent almost 24 hours in the saddle for the cycle challenge over four days to raise money for the charity set up in the name of former Scotland rugby international Doddie Weir.

A Stagecoach worker has completed an extraordinary endurance cycling challenge across the UK and Ireland to raise funds for the My Name’5 Doddie Foundation, supporting research into Motor Neurone Disease (MND).

Advertisement

Neil Mackinnon, insight lead based at Stagecoach’s Perth head office in Dunkeld Road, spent almost 24 hours in the saddle over four days, covering more than 500km and climbing 4911 metres as part of Doddie’s Triple Crown 2026.

The challenge, led by former Scotland rugby captain Rob Wainwright, saw teams travel approximately 800 miles from Melrose to Dublin between March 10 and 13, passing through Scotland, England, Wales and Ireland.

And the event builds on the success of previous fundraising rides, which have collectively raised over £1 million for MND research.

Neil, who lives in Guildtown, cycled alongside record-breaking long-distance cyclist Mark Beaumont during his epic voyage.

Advertisement

Despite facing severe weather conditions, including high winds and torrential rain, participants continued their journey, stopping at rugby clubs along the route to raise awareness and support for the cause.

Neil’s personal contribution saw him complete nine demanding cycling segments, demonstrating significant endurance and commitment to the charity’s mission.

Neil said: “It was certainly a challenge; we were a small team of five cyclists so everyone was going to be pedalling over 100 miles a day.

“Within an hour-and-a-half the sunshine was replaced by rain and strong headwinds, so resilience, teamwork and adjusting plans to suit conditions came to the fore.

Advertisement

“For a small team I’m proud of how we pulled together; days of discomfort for us will hopefully contribute to hope for those with Motor Neurone Disease.”

The group’s efforts have raised over £8,500 for charity.

The My Name’5 Doddie Foundation was established by former Scotland international Doddie Weir and is committed to funding research to find effective treatments and ultimately a cure for MND.

Reaching net zero is no longer a distant ambition for the UK, it’s an urgent national priority that is reshaping how cities operate, build, and grow. But while the conversation often focuses on cutting emissions, the reality on the ground is far more complex. From electric vehicle infrastructure to energy consumption and renewable uptake, some areas are clearly better equipped than others to make the transition.

The exact number of impacted vehicles is unclear, but one officer said it was between 100 and 200 (Picture: JamPress)

Motorists said they saw several of the lone robocabs while driving through Wuhan (Picture: JamPress)

‘I called their customer service number nearly 20 times from my own phone and still couldn’t get through,’ the user, Luka, said, with a video showing the button not working.

‘Is there any way to file a complaint? I’m speechless.’

She added in a second video that customer service representatives offered her a 50% coupon as compensation.

Advertisement

One dashcam recording posted to Rednote shows a car passing 16 autonomous vehicles parked on the road in only 90 minutes.

One police officer told local media that between 100 and 200 robotaxis stalled, which is a ‘common problem’ with Apollo Go cars.

The fleet of robotaxi autonomous vehicles was developed for Baidu’s Apollo Go self-driving project in Wuhan (Picture: AFP)

The officer added: ‘Passengers can press a button and the door can open, but they can’t get off or get off the ring road. We saved many people today.’

Police have not revealed what caused the malfunctions along the Second and Third Ring Roads and the Baishazhou Bridge at 8.57pm.

Advertisement

No one was injured and all passengers have exited the vehicles.

The police added: ‘Following established contingency plans, the public security traffic control and transportation departments quickly mobilised forces to the scene to dispose of the situation in coordination with Apollo Go company staff.’

But these trials haven’t been without speed bumps. Passengers of self-driving Waymo cars in San Francisco say that their trips have been cut short because of vandals or those opposed to robot cars.

Footage from the scene shows two men driving against the flow of traffic through the Williamsburg neighbourhood when a man sitting on the back of the motorbike takes out a gun and fires “at least two rounds”, New York City Police Commissioner Jessica Tisch told a news conference.

The King and Queen visited Wales for the annual Royal Maundy service and gave out presents after the service

Taite Johnson Audience and Trending Writer and Eleanor Barlow Press Association

15:45, 02 Apr 2026

During his visit to Wales, King Charles gifted presents at the annual Maundy service. The traditional Easter service was held in north Wales for the first time, and only the second time ever in Wales.

Charles, accompanied by the Queen, arrived at St Asaph Cathedral on Thursday, April 2 for the ceremony, which was last held in Wales in 1982. During the visit gifts were given as part of a tradition, and the people who received them are recommended to hold on to them.

The King presented Royal Maundy gifts to 77 men and 77 women as part of the tradition, which happens on the Thursday before Easter every year and recognises people who have showed outstanding Christian service and made a difference to the lives of people in their communities.

Advertisement

Recipients chosen from dioceses in Wales or close to the English border, were presented with two leather purses. From superstar gigs to cosy pubs, find out What’s On in Wales by signing up to our newsletter here

In a white purse was a set of specially minted silver Maundy coins totalling 77 pennies, to match the King’s age, and in the red purse was a £5 coin commemorating 100 years since Queen Elizabeth II’s birth, and a 50p coin that celebrates the 50th anniversary of The King’s Trust.

Together this gift is valued at hundreds of pounds as the coins are rarely made. The Royal Mint currently stocks Maundy Money with coins priced at as much as £785 and the least expensive being £120.

Advertisement

Jean Carthy, 81, from Towyn, told the Press Association she had thought it was a scam when she received a letter telling her she had been nominated to receive the gift. She said: “Even this morning I was wondering why I was there. It was just so, so special and especially because it was the first time it has been in north Wales.

“He gave me the purses and said ‘thank you for the work you do’ and that was really something.”

Colin Pengelly, 77, from Castle Caereinion, near Welshpool, said: “It has been an amazing, humbling experience.The King put the purses in my hand and said ‘thank you for all you have done over the years’. I said to him ‘thank you too, keep doing it’.”

Supporters with Union flags and Welsh flags lined the street outside the cathedral to greet the royal couple.

Further up the road, behind barriers separating them from the rest of the crowd, were a group of protesters with yellow flags from Republic, an anti-monarchy campaign group.

They held a banner which had photos of Charles, his brother Andrew Mountbatten-Windsor and the Prince of Wales, and the slogan “What are you hiding? Royal Epstein inquiry now”.

Advertisement

Hours before Charles and Camilla’s arrival, graffiti saying “Not our King” was cleaned off a wall in the grounds of the building, which is the UK’s smallest ancient cathedral.

The first recorded Royal Maundy service was held in 1210 by King John commemorating the Last Supper of Jesus Christ, and the distribution of alms has become a tradition.

Speaking to recipients before the King ‘s arrival, Bishop of Norwich the Right Rev Graham Usher said: “It’s an act of humility on the part of the monarch in which a small representative group of people who have lived an exemplary life of service to their church and community is honoured. Enjoy this moment. It’s your moment.”

The bilingual service, in English and Welsh, included specially composed anthem A Sacred Benediction which was sung by soprano Rebecca Evans.

As they left the cathedral, Charles and Camilla were greeted by schoolchildren, many of whom had bunches of flowers to present to them, and then spoke to people on the High Street outside who had been waiting while the service took place.

Camilla wore a hat by Philip Treacy, a navy blue silk crepe pleated dress and navy blue wool crepe embroidered coat, both by Christian Dior, and accessorised with a sapphire and diamond brooch which belonged to the late Queen.

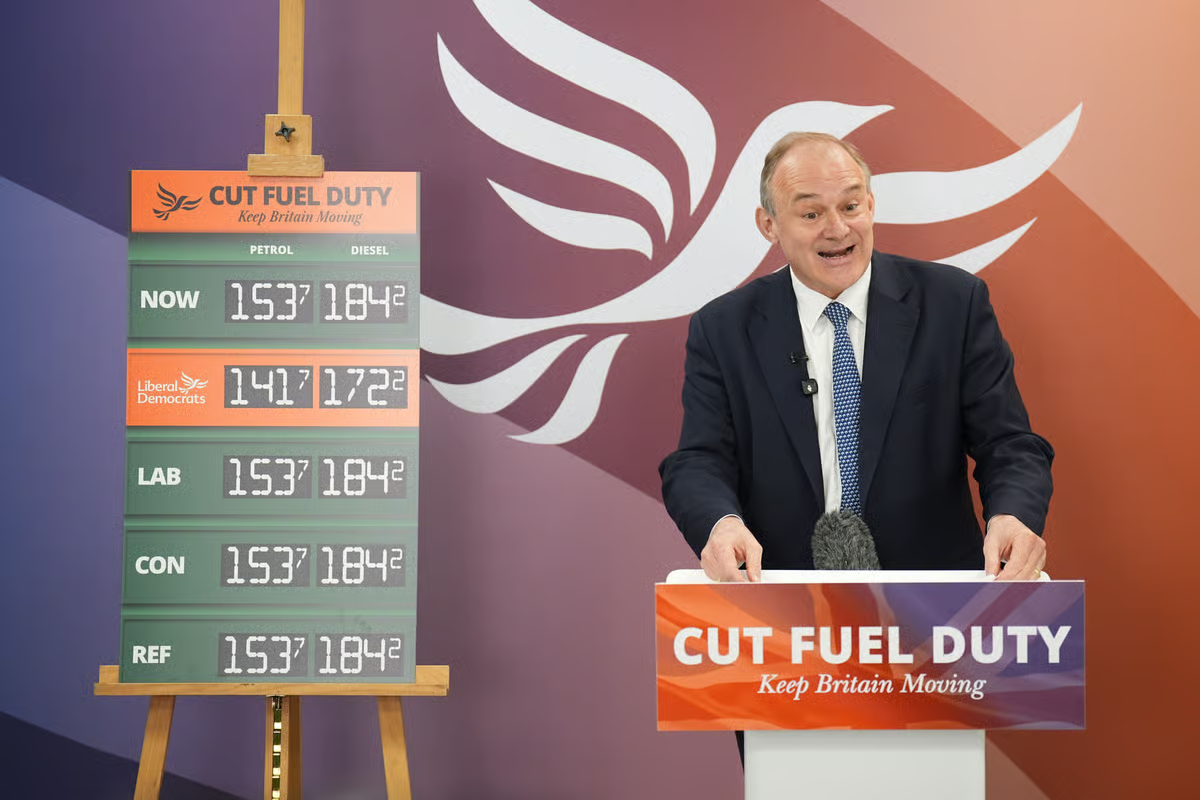

He said taking action on petrol and diesel prices, cutting fuel duty “now, not by 1p, not by 5p, by 10p a litre”, was “especially important today as people set off to join families and friends for the Easter weekend – 21 million trips – the busiest weekend on British roads in years”.

“Shortly afterwards, a 19-year-old man was detained and arrested nearby on suspicion of common assault, grievous bodily harm, threats to kill, theft of a bike, theft of a motor vehicle, possession of an offensive weapon, driving while disqualified and possession of drugs.

Officers and paramedics attended the scene. The person was pronounced dead at the scene.

Trains between Cambridge and Hitchin were disrupted while emergency services responded. However, lines have reopened and disruption is expected until around 4pm.

A National Rail spokesperson said: “The emergency services have completed their work following an earlier incident between Hitchin and Cambridge allowing all lines to reopen. Whilst service recovers, trains may still be revised or cancelled.”

You must be logged in to post a comment Login