Crypto World

How STON.fi’s Omniston Scaled DeFi on TON

Building a swap DApp is relatively straightforward. Running it under real market conditions — with bots, arbitrageurs, and volatile liquidity — is not. BeInCrypto sat down with Andrey Fedorov, CMO & CBDO at STON.fi Dev at Consensus Hong Kong to hear what that process actually looked like.

STON.fi launched as an AMM (automated market maker) on TON Blockchain — a swap interface with liquidity pools. Omniston, its liquidity aggregation protocol, came later as a response to fragmentation: multiple DEXs on TON meant users had to manually compare prices across protocols. Omniston was supposed to fix that by aggregating liquidity into a single access point.

Aggregation worked. But scale exposed new constraints.

Three Lessons From Production

Fedorov is candid about what went wrong early on. “First there was just one token, and it was very easy to provide the technology. Activity levels were minimal, and the user base was still small. But over time it exploded.”

The first lesson was scaling. Both the front end and back end buckled under unexpected demand. The second was subtler: multi-hop swaps — routing trades through intermediate tokens — worked in testing but revealed edge cases under live conditions. “In theory, both hops execute seamlessly,” Fedorov explains. “In practice, you have simultaneous transactions, liquidity shifting across pools, and multiple DEXs updating state at once. The first hop can succeed while the second fails.”

The third lesson was about complexity itself. The initial model assumed a simple set of actors: users swap, liquidity providers provide. Reality added arbitrageurs, bots, and more complex interaction patterns that hadn’t yet been fully anticipated. “I don’t think it is actually possible to work out all these things in the beginning. You need to launch it, see how it goes, then fix something if it breaks.”

STON.fi now accounts for 80 to 90 percent of DEX activity on TON, underscoring its dominant share of swap volume on the chain. But cross-chain swaps, next on the roadmap, will reset that counter. “The fundamentals will be the same, but I’m sure we will see new challenges.”

Why Aggregation Wasn’t Enough

Omniston’s original proposition was to connect all TON DEX pools and find the best route. But aggregating public liquidity has a ceiling. If nobody has added liquidity to a particular pair, no amount of smart routing helps.

“Sometimes people just don’t want to provide liquidity in a specific pool,” Fedorov says. “When a user wants to swap a token in this pool, they can’t get a good price because there is no liquidity.”

The answer was escrow swaps — a parallel execution path that taps into private liquidity from professional market makers, or “resolvers.” Instead of relying solely on AMM pools, Omniston now evaluates both public and private sources and routes each swap through whichever delivers the better outcome.

“It’s not a silver bullet, because we need to have both. The combination provides the best experience.”

Tokenized Equities as a Stress Test

The escrow model proved its value when STON.fi integrated xStocks — tokenized representations of US equities issued by Backed Finance. These are technically TON jettons, but they behave differently from crypto-native tokens in ways that matter for execution.

The harder challenge was liquidity: unlike established crypto pairs, xStocks don’t yet have deep AMM pools across pairs. Technically, AMM support is there. But we also introduced an additional execution path — escrow swaps — so users can access deeper liquidity. Today, most xStocks volume executes through escrow.

From the user’s perspective, Fedorov insists the experience should feel identical to any other swap. “We want our users to forget about technical complexity. Under the hood it is different, but users don’t see it.”

The Self-Custody Trade-off

Fedorov is direct about the constraints of remaining fully non-custodial.

“Sometimes we see solutions with strong traction — big user bases, high volume. From a business standpoint, integrating them would boost our growth immediately. But many of them are centralized. When I bring those options to our technical team, the answer is simple: it doesn’t work like that.” STON.fi is non-custodial. Users keep their assets in their wallets. Swaps are executed by smart contracts.

Centralized integrations are faster and simpler — often just an API connection. DeFi integrations require trustless, contract-level logic where assets never leave the user’s wallet. “We could grow faster if we compromised on custody. But then we wouldn’t be building DeFi infrastructure — we’d be building another fintech layer.”

The trade-off isn’t only technical. It’s educational. Sometimes this creates a marketing and communication challenge. Self-custody shifts responsibility to the user — something many newcomers underestimate. “If someone loses their seed phrase, we can’t restore access. We don’t have it. We’ve never had it. But quite often users still come to us expecting support, like they would from a bank or centralized exchange.”

In centralized systems, there’s a safety net — password reset, account recovery, customer service with override power. In DeFi, security comes from not having that backdoor. The same mechanism that protects users also removes our ability to intervene.

For STON.fi, that means investing more in onboarding, education, and clearer UX — without diluting the core principle of self-custody.

“It’s a long-term bet. In the short term, education is harder. But in the long term, users understand the value of ownership. Especially in Web3, that’s the point.”

Distribution First, Then Depth

Fedorov frames TON not only as a blockchain choice but also as a distribution strategy because of its integration with Telegram. STON.fi and Omniston integrate with wallets, apps, games, and bots across the Telegram ecosystem — each one a potential swap surface. “They want to use the protocol because they want to enable swaps in their applications. But it is also our distribution network. It’s a win-win.”

The next phase is cross-chain aggregation — starting with Tron, then expanding to EVM chains — to unify liquidity across ecosystems rather than just across DEXs on a single chain.

“Make things easier for those who don’t want to think about technical stuff. Get wider distribution by integrating into all the apps. And aggregate liquidity from multiple blockchains, not just one,” Fedorov says. “That’s the roadmap. Now it’s about scaling it.”

This week, Google published a paper describing how a quantum computer could theoretically derive a bitcoin private key in 9 minutes, with ramifications that stretch to Ethereum, other tokens, private banking, and potentially everything in the world.

Quantum computing is easy to mistake for a faster version of a regular computer. But it is not a more powerful chip or a bigger server farm. It is a fundamentally different kind of machine, different at the level of the atom itself.

A quantum computer starts with a very cold, very small loop of metal where particles begin to behave in ways they do not behave under normal conditions on Earth, ways that alter what we think of as the basic rules of physics.

Understanding what that means, physically, is the difference between reading about the quantum threat and actually grasping it.

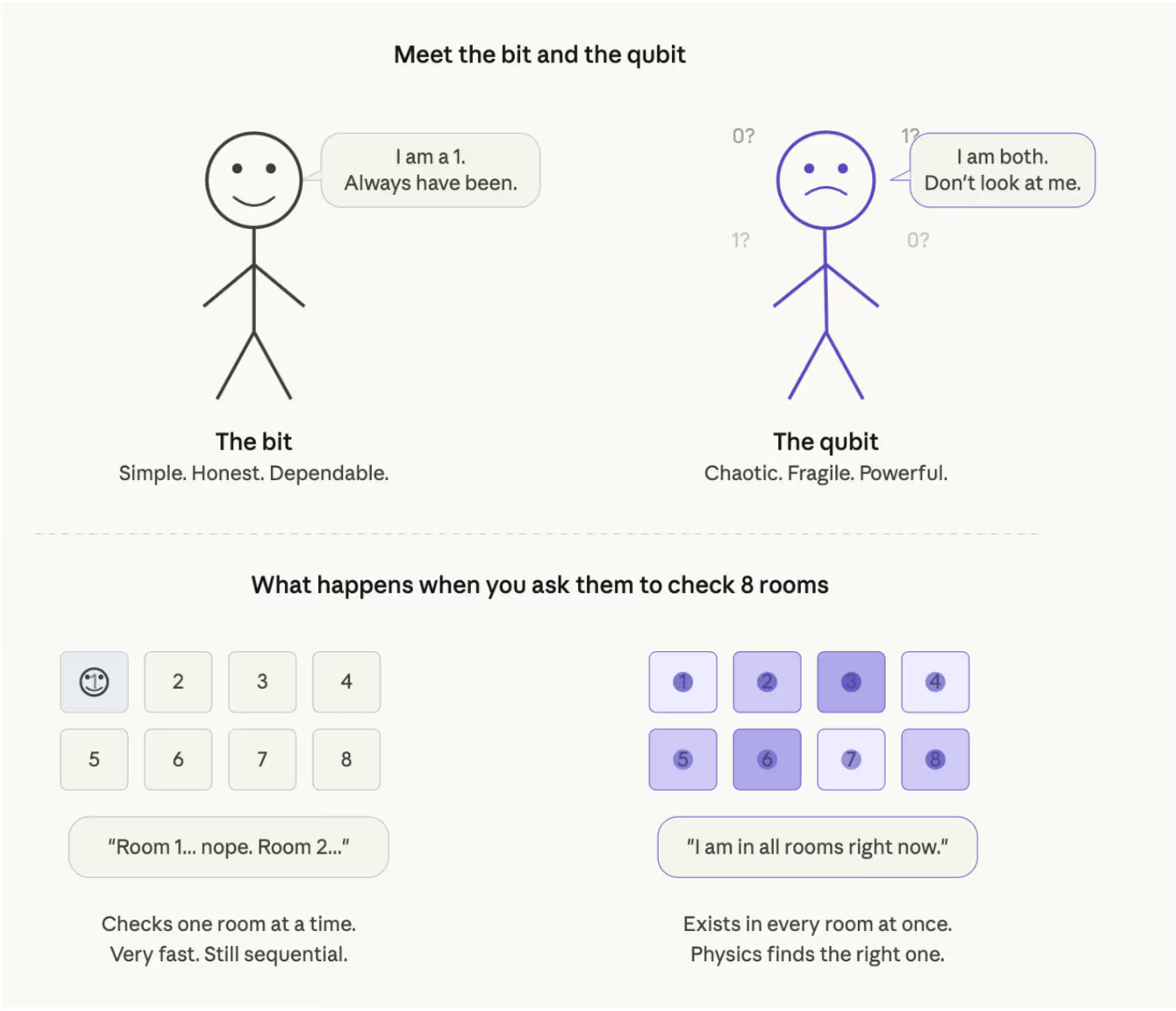

How computers and quantum computers actually work

Regular computers store information as bits — each is either a 0 or a 1. A bit is a tiny switch. Physically, it’s a transistor on a “chip” — a microscopic gate that either lets electricity through (1) or doesn’t (0).

Every photo, every bitcoin transaction, every word you’ve ever typed is stored as patterns of these switches being on or off. There is nothing mysterious about a bit; it is a physical object in one of the two definite states.

Every calculation is just shuffling these 0s and 1s around really fast. A modern chip can do billions of these per second, but it still does them one at a time, in sequence.

Quantum computers use something known as qubits instead of bits. A qubit can be 0, 1, or — and this is the weird part — both at the same time!

This is possible as a qubit is a completely different kind of physical object. The most common version, and the one Google uses, is a tiny loop of superconducting metal cooled to about 0.015 degrees above absolute zero, colder than outer space but here on Earth.

At that temperature, electricity flows through the loop without any resistance, and the current is said to exist in a quantum state.

In the superconducting loop, current can flow clockwise (call that 0) or counterclockwise (call that 1). But at quantum scales, the current does not have to pick one direction and actually flows in both directions simultaneously.

Don’t mistake it for switching between the two really fast. The current is measurably, experimentally and verifiably in both states simultaneously.

Mind-bending physics

With us so far? Great, because here’s where it gets genuinely strange, because the physics behind how it works isn’t immediately intuitive, and it is not supposed to be.

Everything someone interacts with in daily life obeys classical physics, which assumes that things are in one place at one time. But particles do not behave this way at the subatomic scale.

An electron does not have a definite position until you look at it. A photon does not have a definite polarization until you measure it. A current in a superconducting loop does not flow in a definite direction until you force it to pick.

The reason we don’t experience this in everyday life is decoherence. When a quantum system interacts with its environment, air molecules, heat, vibrations and light, the superposition collapses almost instantly.

A football cannot be in two places at once because it is interacting with trillions of air molecules, dust, sound, heat, gravity, etc., every nanosecond. But isolate a tiny current in a near-absolute-zero vacuum, shield it from every possible disturbance, and the quantum behavior survives long enough to compute with.

That’s why quantum computers are so hard to build. People are engineering physical environments where the laws of physics that normally prevent this stuff from happening are held at bay for just long enough to run a calculation.

Google’s machines operate in dilution refrigerators the size of huge rooms, colder than anything in the natural universe, surrounded by layers of shielding against electromagnetic noise, vibration, and thermal radiation.

And the qubits are fragile even then. They lose their quantum state constantly, which is why “error correction” dominates every conversation about scaling up.

So quantum computing is not a faster version of classical computing. It is exploiting a different set of physical laws that only apply at extremely small scales, extremely low temperatures, and extremely short timeframes.

Now stack that up.

Two regular bits can be in one of four states (00, 01, 10, 11), but only one at a time (since current flows in only one direction). Two qubits can represent all four states at once, as the current is flowing in all directions at the same time.

Three qubits represent eight states. Ten qubits represent 1,024. Fifty qubits represent over a quadrillion. The number doubles with every qubit that is added, which is why the scaling is so exponential.

The second trick is something called entanglement. When two qubits are entangled, measuring one instantly tells an observer something about the other, no matter how far apart they are. This lets a quantum computer coordinate across all those simultaneous states in a way that regular parallel computing cannot.

And these quantum computers are set up so that wrong answers cancel each other out (like overlapping waves that flatten) and right answers reinforce each other (like waves that stack higher). By the end of the computation, the correct answer has the highest probability of being measured.

So it’s not brute-force speed. It’s a fundamentally different approach to calculation — one that lets nature explore an exponentially large space of possibilities and then collapses to the right answer through physics rather than logic.

A monumental threat to cryptography

This mind-bending physics is why it is terrifying for encryption.

The math protecting bitcoin relies on the assumption that checking every possible key would take longer than the age of the universe.

But a quantum computer doesn’t check every key. It explores all of them simultaneously and uses interference to surface the right one.

That is where it ties into Bitcoin. Going one direction, from private key to public key, takes milliseconds. Going the other direction, from public key back to private key, would take a classical computer a million years, or even longer than the age of the universe. That asymmetry is the only thing proving that a person is holding their coins.

A quantum computer running an algorithm called Shor’s can go through that trapdoor in reverse. Google’s paper this week showed it could do so with far fewer resources than anyone previously estimated, and within a timeframe that races against bitcoin’s own block confirmations.

This is why the threat of quantum computers breaking blockchain encryption is genuinely making everyone very worried.

How that attack works step by step, what Google’s paper specifically changed, and what it means for the 6.9 million bitcoin already exposed, is the subject of the next piece in this series.

Crypto World

Top 10 Crypto Hacks Total $5.7 Billion, But Proposed DeFi Fix Would Only Have Helped One

The 10 largest crypto hacks have drained a combined $5.68 billion from the industry, yet a structural defense proposed by a DeFiLlama developer would have applied to just one of them.

Data places the $285 million Drift Protocol exploit alongside legacy disasters such as Mt. Gox and FTX. The list has renewed debate over whether Decentralized Finance (DeFi) security is improving fast enough.

Lending Protocols Face Higher Risk

A DeFiLlama developer proposed combining cross-protocol tranching with 24-hour withdrawal rate limits. The idea splits depositor capital into senior and junior tranches, then caps daily withdrawals at the junior tranche’s size.

According to the developer’s data, 3.92% of lending protocols with peak total value locked above $50 million have suffered an 80%-plus drain.

That rate is 4.6 times higher than the 0.85% observed across all protocol categories. Cross-protocol tranching could reduce the probability of total loss for senior depositors by roughly 80%, the developer estimated.

The combination would enforce that senior-tranche capital can always be made whole, provided the hack does not exceed the junior buffer within a single day.

Most Losses Fall Outside DeFi Lending

However, the top-10 list exposes the proposal’s limits. Drift Protocol, the largest DeFi hack of 2026, lost $285 million through a governance takeover that drained vaults in roughly 12 minutes.

Tranching plus rate limits could have slowed that drain and preserved senior depositor funds.

The remaining nine incidents fall into two categories that tranching does not address. Five were centralized exchange failures, including the $1.5 billion Bybit breach and the collapses of FTX and Mt. Gox.

Four were cross-chain bridge exploits affecting Ronin Network, Poly Network, Wormhole, and the BNB Bridge.

Security experts say DeFi protocol code is becoming harder to exploit, shifting the main attack surface to people and operational security weaknesses.

“I really hope Hyperliquid is in a war room right now, assuming they’ve already been compromised and reviewing every last thing they’ve done for the last year and a half,” quipped Laura Shin, host of the Unchained podcast.

While the data suggests that tranching strengthens one layer of defense for lending, the industry’s largest dollar losses remain tied to centralized infrastructure and human error.

The post Top 10 Crypto Hacks Total $5.7 Billion, But Proposed DeFi Fix Would Only Have Helped One appeared first on BeInCrypto.

Crypto World

Ripple (XRP) Corporate Treasury Expands, Yet Taurox (TAUX) Pre-KYA Opening Boosts AI Agents Developments

Ripple trades near $1.32 right now. The company just made a significant move by integrating XRP and its stablecoin RLUSD directly into its enterprise treasury management system (through its 2025 acquisition of GTreasury). This allows corporate CFOs to manage digital assets alongside traditional fiat money in a single dashboard for the first time. On top of that, Ripple announced a major partnership with Convera, a $190 billion payments giant, to settle cross-border payments using RLUSD on the XRP Ledger.

Taurox, an AI-driven trading protocol, is designed to help regular stakers benefit from this growing corporate adoption through smart autonomous agents that focus on steady, risk-managed returns.

Even when Ripple announces big institutional partnerships and treasury tools, XRP often still swings 20-30% on normal market noise. Many holders feel like the real-world progress doesn’t always show up in the price right away. Taurox was built to solve that disconnect. It pools deposits of USDT, BTC, or XRP into one shared trading pool and lets a global team of developers, quants, and AI engineers run multiple diversified strategies at once.

Each strategy is strictly limited to 2% of the total pool to keep risk controlled, and smart built-in rules automatically maintain balance. The result is much smoother performance, without the constant stress of trying to guess how the market will react to every new partnership.

Taurox has opened the Pre-KYA Registration Table ahead of schedule. This early window lets developers, quants, and AI builders submit their trading agents before the full system launches. The first ones in get priority testing in the Proving Ground, faster access to pool capital, and extra rewards from the Agent Creator Fund (10% of total TAUX supply). If you already have a working trading strategy, this is your chance to get positioned ahead of the crowd.

When you stake, your funds go into one shared trading pool and you receive txTokens that represent your share of the pool’s value, starting at $1.00 each. The protocol keeps 15% in stablecoins as a safety buffer and puts the rest to work through autonomous agents. These agents only go live after passing strict tests in the Proving Ground. Daily loss limits of 2%, single-trade caps of 5%, and an automatic pause if the pool drops 5% all help protect your capital. Everything is on-chain and fully transparent.

TAUX has a hard-capped supply of 2 billion tokens that can never be increased after launch. Taurox charges zero upfront fees, it only takes 5% of the profits the agents make, buys TAUX on the open market, and permanently burns 30% of it. The rest is shared between stakers, the DAO, and the strategy creators. This setup creates real scarcity: the bigger and more successful the pool becomes, the more valuable TAUX can get over time.

The Taurox Presale has entered Phase 4 and has already raised over $950K. TAUX is currently priced at $0.018. Investors joining in this phase are positioned for nearly 4.5x returns when the token lists at $0.08. If Taurox reaches its $1 billion pool target, these early participants could see up to 103x gains as TAUX potentially climbs to $1.85. For example, a $500 investment today would grow to roughly $2,220 at listing and approach $28,000 if TAUX hits the $1 level.

The presale includes a 1-month cliff and 20% monthly unlocks from month 2 to 5, so you can start staking quickly while limiting early selling. Combined with 30% burns and strong reserves, it offers real potential for both short-term and long-term upside.

As Ripple quietly brings XRP and RLUSD into mainstream corporate treasury and payments infrastructure, Taurox gives you a practical way to stay exposed without the usual volatility and guesswork. It combines intelligent AI agents with clear risk controls and a token that actually becomes scarcer as the protocol grows. If you’re watching Ripple’s shift into enterprise finance and want simpler returns, Taurox is built for exactly this kind of moment.

Buy TAUX: https://taurox.io

Whitepaper: https://docs.taurox.io/

Official Telegram: https://t.me/tauroxlabs

Official X/Twitter: https://x.com/TauroxProtocol

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Key Highlights

- First inflation measurements since Iran conflict began: March CPI and February PCE reports scheduled

- March employment report showed 178,000 new positions, surpassing the 65,000 forecast

- Crude prices surged more than 50% following war outbreak, pushing gasoline beyond $4 nationwide

- Delta Air Lines earnings Wednesday will reveal jet fuel expense impact on carrier profitability

- Major indices snapped five consecutive weeks of declines, climbing at minimum 3%

Investors are preparing for a pivotal week featuring critical inflation measurements, quarterly corporate results, and continued monitoring of the Iran conflict’s economic ramifications.

Last week’s trading session saw the S&P 500 advance 1.6%, while the Dow Jones climbed 1.2%, and the Nasdaq Composite surged 2.2%. The rally ended a five-week decline for all three benchmarks. Year-to-date, the S&P 500 and Dow remain lower by 3.8% and 3.2%, respectively.

Friday’s employment data for March significantly exceeded analyst projections. The report revealed 178,000 nonfarm payroll additions versus consensus estimates of 65,000. This represented a sharp reversal from February’s 92,000 job losses.

“The message here is equilibrium,” noted Gina Bolvin, president of Bolvin Wealth Management Group. “Robust employment growth diminishes pressure for immediate rate reductions, though it doesn’t alter the overall deceleration pattern.”

Michael Feroli, JPMorgan Chase’s chief US economist, indicated the figures provided “somewhat greater assurance that economic expansion can absorb the current energy cost surge without substantial lasting harm.”

Critical Inflation Measurements Approaching

Thursday delivers the February Personal Consumption Expenditures index, an inflation gauge the Federal Reserve prioritizes. Analyst consensus projects a 0.4% monthly advance and 2.8% annual growth.

Friday presents the more significant release: March’s Consumer Price Index. Forecasters anticipate a 0.9% monthly increase and 3.4% annual rise. February’s CPI registered 2.4% annually. This upcoming report represents the initial measurement incorporating Iran war-related pricing effects.

National average gasoline prices exceeded $4 per gallon last week, per AAA data. Goldman Sachs analyst Ben Shumway noted escalating costs are “contributing to further deterioration in consumer sentiment from previously depressed readings.”

Andy Schneider, senior US economist at BNP Paribas, observed that “supply disruptions in the Strait of Hormuz have materialized while tariff impacts continue spreading,” noting that “initial petroleum price transmission will be reflected in March figures.”

Goldman economist Manuel Abecasis characterized the present supply disruption as “less worrisome than previous instances that generated inflation challenges,” pointing to its constrained scope and range.

Corporate Results and Conflict Implications

Delta Air Lines releases quarterly results Wednesday morning before market open. The carrier’s performance will illuminate how elevated aviation fuel expenses are impacting airline sector margins. Constellation Brands and Levi Strauss additionally report during the period.

#earnings for the week of April 6, 2026 https://t.co/hLn2sKQhEY $APLD $STZ $AEHR $DAL $BB $SMPL $GBX $LEVI $NEOG $KRUS $SKIL $WDFC $RELL $ERGP $LOT $XELB $RPM $SLP $CLIR $EVO $IQST $BYRN $PXED pic.twitter.com/aKqX72tj9u

— Earnings Whispers (@eWhispers) April 2, 2026

Street analysts forecast earnings expansion exceeding 13% across the S&P 500 overall, per FactSet data.

Oil prices have climbed over 50% during the five weeks since hostilities commenced. Shipping activity through the Strait of Hormuz remains virtually nonexistent. Trump conducted a Monday briefing alongside military leadership as his self-established deadline for strait reopening nears.

Capital.com analyst Daniela Hathorn observed that “investors have shifted from pricing in de-escalation scenarios to assessing escalation likelihood.”

Paola Rodriguez-Masiu, Rystad Energy’s chief oil analyst, indicated the temporary cushion that initially contained price increases from pre-conflict petroleum inventories is now depleting.

The Federal Reserve’s March policy meeting minutes release Wednesday at 2 p.m. ET. Market participants broadly anticipate the Fed will maintain current interest rates at its upcoming April session.

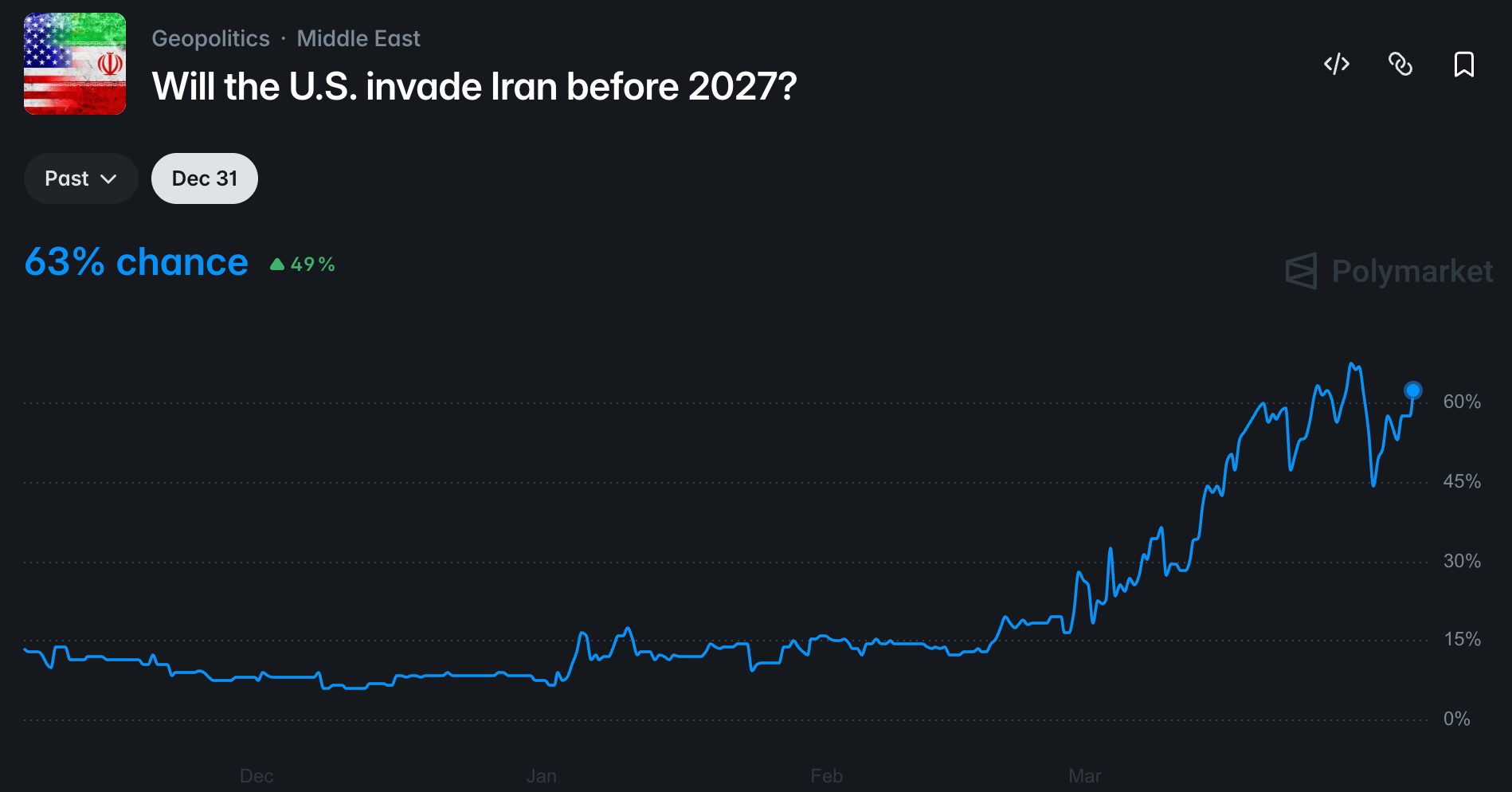

The odds of the United States invading Iran this year surged to 63% on the Polymarket prediction platform on Sunday, following comments made by US President Donald Trump on social media.

Despite the surge, the odds of an invasion before 2027 are still down from the high of 68% on March 29, due to a US troop buildup in the region and comments from the Trump administration that the United States was considering capturing Kharg Island, a major Iranian oil shipping station.

Volume on that prediction was about $3.74 million at the time of publication.

On Tuesday, after Trump signaled that the US might leave Iran in the next two to three weeks, Bitcoin (BTC) jumped by about 2.6% and the S&P 500 index to added about 2.91%. However, Trump reversed course with his latest statement on Sunday. He wrote:

“Tuesday will be power plant day, and bridge day, all wrapped up in one, in Iran. There will be nothing like it! Open the fuckin’ strait, you crazy bastards, or you’ll be living in hell.”

At last look, BTC was little changed, trading up less than 0.1% in the past 24 hours, remaining anchored around the $67,500 level, according to data from TradingView.

The mixed signals from the Trump administration on the war and how long it will last continue to create investor uncertainty and an impact on all risk asset prices, as market analysts, traders and economists attempt to forecast the effects of the war.

Related: Polymarket takes down market on missing US pilot after backlash

Trump’s comments draw a wave of online backlash, but asset prices barely budge

“I wish Trump would stop threatening Iranian civilian infrastructure. It’s a lose-lose for us: backing down hurts his negotiating credibility,” economist Peter Schiff said in response to Trump’s comments.

“Carrying it out escalates the war, damages US standing, generates sympathy for Iran and fuels Iranian hatred for America,” Schiff continued.

“I assumed this was a fake, it isn’t — wild,” podcaster and Bitcoin advocate Peter McCormack said.

Brent crude oil, the most widely used pricing benchmark for the international spot oil market, remains elevated, closing Thursday at more than $109 per barrel. Trading is scheduled to resume on Monday following the Easter holiday weekend.

The relationship between Bitcoin and US dollar–denominated liquidity is shaping how crypto markets behave in 2026. According to Sam Lyman, head of research at the Bitcoin Policy Institute, the coexistence of BTC with dollar-backed stablecoins like USDT has become a mutually reinforcing dynamic that benefits both sides of the ecosystem. In practice, the leading BTC trading pairs are anchored in USD, a reality that helps sustain demand for dollar liquidity even as crypto markets expand globally.

More than a simple trading pattern, the dynamic sits at the intersection of market structure, regulation, and geopolitics. Lyman argues that the BTC-dollar relationship mirrors the broader role the dollar plays in commodity and macro markets — a framework that has long been embedded in the way crypto trades are priced and settled. In his view, Bitcoin’s strongest leverage point remains its liquidity expressed in dollars, which challenges the notion that BTC could undermine the dollar system. The observation is supported by data showing the dominance of dollar-based markets for Bitcoin, a trend that Kaiko highlighted in its 2024 analyses of on-chain and off-chain activity.

Key takeaways

- Bitcoin’s liquidity core is anchored to USD trading, with BTC/USD pairs supported by stablecoins like USDT that maintain dollar-denominated rails for buyers and sellers.

- Regulatory direction in the United States — notably GENIUS Act-aligned stablecoin policy — could shape how dollar-pegged tokens operate within crypto markets without sacrificing the dollar’s role in liquidity provision.

- China’s stance remains a paradox: while Beijing reiterates a ban on permissionless crypto activity and push for a CBDC, Chinese mining pools still command a sizable share of global hashrate, underscoring control dynamics beyond formal prohibitions.

- The rise of the digital yuan and capital controls continue to influence cross-border flows, illustrating how policy choices in major economies can impact crypto market structure and risk exposure for miners and validators.

- Investor and builder attention should focus on regulatory clarity, mining geography shifts, and the evolving balance between centralized fiat rails and permissionless borderless networks.

The dollar–Bitcoin nexus in a changing regulatory and geopolitical landscape

At the heart of the current narrative is the “symbiotic” relationship between Bitcoin and dollar liquidity. Lyman notes that the largest BTC trading pair remains USD-based, a reality that makes dollar stability and regulatory certainty influential for crypto markets. Stablecoins pegged to the dollar, particularly USDT, act as a bridge for traders seeking quick exposure to BTC without stepping into traditional bank rails. This arrangement creates a feedback loop: as more capital flows into dollar-denominated BTC markets, the dollar’s role in crypto deepens, and stablecoins gain further prominence as liquidity vehicles.

The discussion around stablecoins is not purely technical; it sits squarely within a regulatory framework that currently anchors many of the market’s most important rails. Advocates of prudent regulation argue that stablecoins, if backed by robust reserves and transparent governance, can provide stable liquidity channels that bolster market depth and resilience. In this framing, policy proposals such as the GENIUS Act aim to codify oversight and guardrails for stablecoins. For observers and participants, the question is not whether stablecoins are here to stay, but how the rules of the road will shape innovation, settlement speed, and cross-border payments in the crypto economy.

On the data side, independent researchers have flagged the dollar’s dominance in BTC markets in 2024, with analyses from Kaiko illustrating the extent to which dollar-based trading pairs anchor liquidity. This backdrop matters for traders who rely on predictable settlement assets, and it informs long-term bets on infrastructure that underpins dollar-denominated trading, such as stablecoin liquidity pools, exchange markets, and on-chain custody solutions.

Policy, control, and China’s ongoing paradox

Policy tensions also extend beyond the United States. China has repeatedly framed Bitcoin and stablecoins as threats to the country’s capital controls, a central feature of its economic management. Lyman emphasizes that Beijing’s approach reflects a broader objective: to keep financial activity within the country’s regulatory perimeter while guiding capital flows through a state-backed mechanism. In 2025, China reaffirmed its stance on stablecoins even as it advances a separate digital yuan project designed to exert tighter control over foreign exchange and capital movements.

Yet regulatory bans have not eliminated crypto activity in practice. While China maintains a blanket ban on Bitcoin mining and other permissionless crypto activities, mining pools within the country continue to represent a substantial portion of the global hashrate. Hashrate Index places Chinese pools at more than 36% of the worldwide hashrate, underscoring a disconnect between formal prohibitions and actual network participation. The outcome is a nuanced mining map: a political impulse to restrict is in tension with economic incentives and cross-border capital flows that crypto miners leverage wherever policy allows.

These dynamics intersect with the broader push toward a centralized, programmable digital currency framework. The CBDC landscape, led by China’s digital yuan, is often cited as a tool for precision control over capital movements and monetary policy transmission. Proponents argue CBDCs can offer programmable features that improve settlement efficiency and cross-border interoperability, while critics warn they could erode financial privacy and curb the openness that has driven permissionless innovation in crypto markets.

What investors and builders should watch next

As policy debates evolve in the US and abroad, the crypto market stands at a crossroads where liquidity, regulatory clarity, and governance will shape momentum more than any single price move. The dollar-centered liquidity regime is likely to persist in the near term, reinforcing the role of dollar-denominated stablecoins as the primary conduit for BTC trading. For investors, the key questions relate to how changes in stablecoin regulation could affect market depth, settlement speed, and counterparty risk in major exchanges and over-the-counter desks.

From a construction and infrastructure perspective, the ongoing emphasis on stablecoin resilience, transparent reserve management, and compliance will influence which platforms gain network effects. Traders and institutions may prioritize products and services that align with GENIUS Act principles—namely, clarity around custody, reserve standards, and reporting—without compromising the efficiency that makes USD-based crypto liquidity compelling.

On the geopolitical front, observers should monitor how the CBDC push interacts with global capital flows and whether central banks will pursue interoperability initiatives that either complement or complicate existing crypto rails. The tension between centralized, programmable fiat and permissionless networks will continue to shape debates about financial sovereignty, market accessibility, and the future of cross-border payments.

For now, the market appears to be navigating a period of regulatory refinement and strategic repositioning. The next few quarters will test how well dollar-denominated liquidity and stablecoins can adapt to evolving rules and shifting mining geographies, while the ongoing CBDC experiments and capital-control policies will help illuminate the long-term balance between centralized control and decentralized finance.

Readers should watch for updates on GENIUS Act developments and any concrete regulatory guidance around stablecoins, as well as continued data on mining geography and hashrate distribution. These factors will shape liquidity availability, market depth, and the resilience of the BTC ecosystem as it matures within a complex regulatory and geopolitical landscape.

Community Banks Increase Compliance Issues

The Independent Community Bankers of America has been critical of the application and its compliance framework has been challenged. The group stated that the proposal does not meet required standards on risk management and profitability. Also, banks claimed that crypto companies must be subject to the same stringent regulations as their conventional counterparts. Bank representatives emphasized that companies cannot be given charter benefits without being regulated in full. They cautioned that unequal requirements might pose dangers to customers and the institutions. In addition, this issue is symptomatic of a broader conflict between digital asset companies and traditional financial organizations.

Nevertheless, Coinbase declared that it is not interested in being a traditional bank. The company stated that the charter of the trust would facilitate custody services and not deposits or lending. In addition, it seeks to enhance legal safeguards and facilitate financial activities that are under federal supervision. The National Community Reinvestment Coalition also protested against the approval and had concerns about the public interest. Its representatives claimed that the action would allow access to federal systems without fulfilling greater duties. They also referred to threats associated with previous enforcement measures and cybersecurity attacks.

Americans for Financial Reform Education Fund also commented on the decision and cautioned against risks to financial stability. The group raised issues related to fraud, money laundering, and market volatility in relation to crypto activities. Therefore, the charter’s revision continues to be debated in policy circles. Simultaneously, Coinbase continues to oppose regulations proposed by the US Securities and Exchange Commission concerning tokenized securities. The company argued that these restrictions could inhibit innovation and run contrary to how the market actually operates. Additionally, this conflict adds another dimension to its regulatory participation. The struggle between Coinbase and US banks underscores growing tension over crypto companies’ entry into the financial system.

James Wynn, the high-leverage crypto trader known for turning $7,600 into $25 million on PEPE, warned traders that markets will deteriorate further before recovering. Wynn outlined a multi-asset defensive strategy, shorting US equities and going long on oil while selectively buying Bitcoin (BTC) dips with spot capital.

All these is amid the US President Donald Trump’s fiery geopolitical message on Sunday against Iran and the Strait of Hormuz.

James Wynn’s Macro Bets and the Iran Factor

The trader’s positioning reflects a broader macro thesis tied to geopolitical escalation. James Wynn said he is short the S&P 500 and Nasdaq, long on WTI crude oil, and accumulating BTC on pullbacks.

He also flagged positive expected value in the Singapore dollar, Chinese yuan, euro, and British pound. He expects gold to hold its price or reach new all-time highs soon.

On real estate, Wynn acknowledged his own exposure to the sector, calling it a losing position while stressing the importance of diversification.

His strategy aligns with the current geopolitical environment. President Donald Trump gave Iran a 48-hour ultimatum on Truth Social, threatening to strike power plants and bridges if Tehran does not reopen the Strait of Hormuz by Tuesday.

Iran has kept the Strait effectively closed since the US-Israel military operation began on February 28, disrupting roughly 20% of the world’s oil supply.

Low Liquidity Wicks and Liquidation Hunts

Separately, James Wynn warned about Bitcoin price action. He flagged a Sunday manipulation wick on BTC that occurred during low trading volume, calling it further proof of what is coming next.

“Another classic low-volume manipulation wick on Bitcoin on a Sunday further proves what’s about to come,” he indicated.

Indeed, a $1,000 BTC price pump within 10 minutes on Sunday liquidated $28 million in short positions in a single hour, amid continued low-liquidity leverage hunting.

BTC is trading near $67,201 as of this writing, with the Fear and Greed Index stuck at 12, deep in extreme fear territory. The token has held a $65,000 to $73,000 range for weeks despite sustained bearish sentiment.

With Trump’s self-imposed Tuesday deadline approaching and oil prices hovering above $100 per barrel, the macro backdrop for risk assets remains volatile.

The post James Wynn Reveals His Defensive Play Amid Trump’s Fiery Iran Message appeared first on BeInCrypto.

Polymarket has removed a betting market tied to the rescue of U.S. service members in Iran, after intense backlash and criticism from lawmakers this weekend.

The market allowed users to wager on when the U.S. would confirm the rescue of two airmen after an F-15E fighter jet was shot down over Iran. The crew members have since been rescued.

Rep. Seth Moulton, a Democrat from Massachusetts, criticized the listing in a post on X, calling it “disgusting” and arguing it reduced a military rescue effort to a financial trade.

Moulton has taken a hard line on prediction markets, recently banning his staff from using platforms such as Polymarket and Kalshi over concerns that financial incentives could influence policy decisions.

A Polymarket spokesperson said the listing did not meet its integrity standards removed shortly after it appeared. The company added that it is reviewing how the market passed internal safeguards.

The incident comes as prediction markets face rising pressure in Washington. A group of congressional Democrats last month introduced legislation that would ban contracts tied to elections, war and government actions.

Separately, several senators have urged the Commodity Futures Trading Commission to prohibit markets linked to individual deaths, citing national security concerns.

Regulators are also asserting authority over the sector. The CFTC said this week it filed lawsuits against three states over efforts it believes attempt to bypass federal oversight of prediction markets.

Industry scrutiny has expanded beyond politics. The NFL has asked operators to avoid offering contracts it views as objectionable or open to manipulation, including bets tied to officiating decisions or events known in advance.

Still, the market is expanding. Kalshi has late last month secured a license to offer margin trading to institutional investors, while new players are entering the market. Among them is JPMorgan, whose CEO, Jamie Dimon, has signaled that it is looking to enter the fray.

Latest Acquisitions Drive Overall Holdings To Greater Heights

The recent purchase comes after a huge one announced last week. Bitmain has already accumulated more than 71,000 ETH, boosting total holdings to more than 4.7 million ETH. It now holds nearly 4 percent of the total Ethereum supply. The company still aims to own five percent of Ethereum’s supply in the market. In addition, the strategy signals a long-term accumulation plan that targets market positioning. The aggressive buying has, however, exposed it to price volatility.

Statistics indicate that Bitmain has a large unrealized loss on its Ethereum investment at present. The average purchase price is above current market rates, which has impacted portfolio value. This puts the firm under pressure as market conditions remain uncertain. Since the beginning of the year, Bitmain’s stock has fallen more than 30 percent. Nonetheless, it posted a small profit in the last week along with a slight uptick in Ethereum’s price. Moreover, this movement suggests a more favorable mood even amid ongoing geopolitical threats.

According to Tom Lee, the company will continue purchasing at current levels despite the unstable markets. He explained that the plan rests on optimism about the broader economic outlook. Therefore, current pricing is seen as an opportunity rather than a risk for the firm. Lee noted that present oil prices are lower than historical highs when adjusted for inflation. He compared current levels with those observed in previous market cycles. He added that this analogy supports the belief that the economy can sustain higher energy prices.

Notably, the leading cryptocurrencies have remained relatively stable even amid geopolitical tension. Both Bitcoin and Ethereum have avoided further losses during the recent conflict period. Consequently, Bitmain is still consolidating its assets in line with the long-term plan.

Ryan O’Hearn homers and drives in 4 to lift Pirates over Orioles 8-2 for 5th straight win

This Android phone can run Windows games locally, no PC required

Goodbye, Bahama Breeze: Caribbean-themed restaurant officially closes all locations

-

NewsBeat3 days ago

NewsBeat3 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business3 days ago

Business3 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Spanx – Corporette.com

-

Entertainment6 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World4 days ago

Crypto World4 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech7 days ago

Tech7 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World5 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech7 days ago

Tech7 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Sports23 hours ago

Sports23 hours agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business4 days ago

Business4 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech6 days ago

Tech6 days agoApple will hide your email address from apps and websites, but not cops

-

Tech5 days ago

Tech5 days agoEE TV is using AI to help you find something to watch

-

Sports5 days ago

Sports5 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Politics6 days ago

Politics6 days agoShould Trump Be Scared Strait?

-

Tech6 days ago

Tech6 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Fashion6 days ago

Fashion6 days agoThe Best Spring Trends of 2026

-

Sports6 days ago

Sports6 days agoWomen’s hockey camp eyes fitness boost, tactics ahead of WC 2026 campaign | Other Sports News

-

Crypto World6 days ago

Crypto World6 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech6 days ago

Daily Deal: StackSkills Premium Annual Pass

-

Tech5 days ago

Tech5 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

You must be logged in to post a comment Login