Business

Wall Street Week Ahead: AI disruption hangs over US markets as investors wary of risks

The disruptive potential of AI has consumed investors in recent weeks, with shares in industries such as software, wealth management and real estate services pummeled by concerns about business upheaval.

“There continues to be this…back and forth about who might be the victim and those that will actually emerge winners because they are harnessing AI as opposed to being replaced by it,” said Kristina Hooper, chief market strategist at Man Group.

“There is very little definitive right now about that, and so I think that will continue to be a concern.”

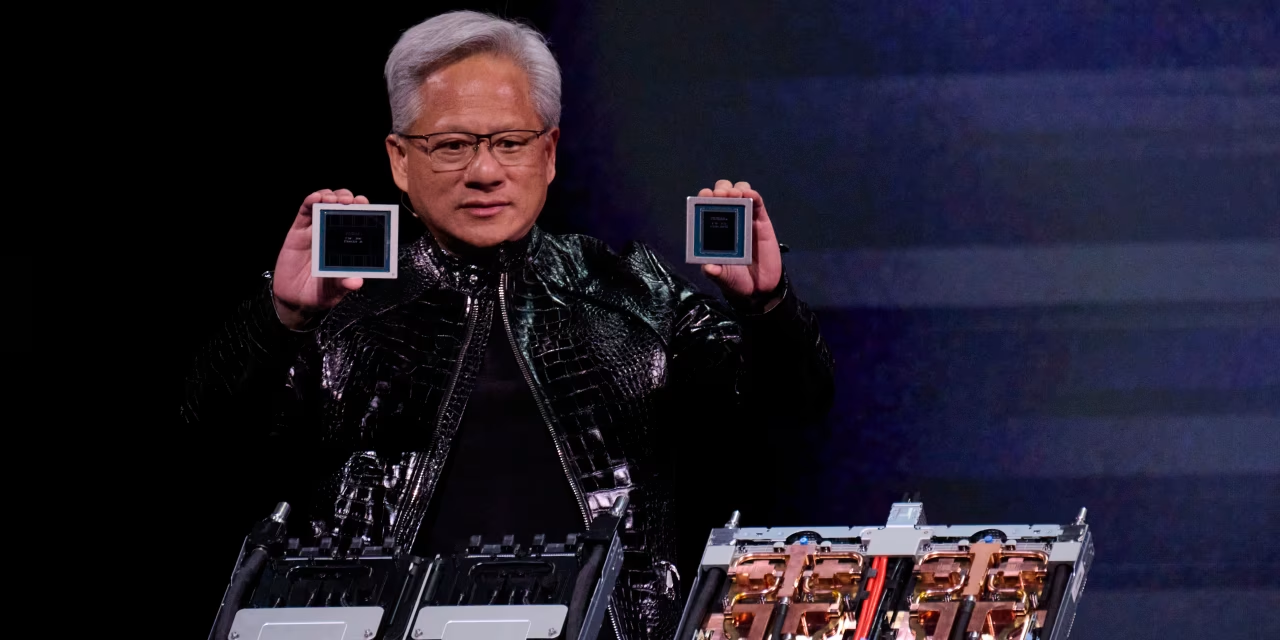

Stock prices in areas such as software remain acutely sensitive to AI-related developments. AI bellwether Nvidia’s highly anticipated quarterly report failed to calm nerves, with the semiconductor giant’s shares falling over 5% on Thursday and weighing on the technology sector. Investors are concerned about whether Nvidia’s “hyperscaler” customers will garner sufficient returns to justify their massive spending on data centers and other infrastructure.

Despite the tech sector’s struggles, gains this year in other areas such as industrials and consumer staples have helped buoy major equity indexes. The benchmark S&P 500 was up 0.9% in 2026 as of Thursday.

“The U.S. equity market is sort of in its late cycle, trying to find the winners and losers of this new disruptive technology and pretty much treading water,” said John Velis, Americas macro strategist at BNY.

WILL FEBRUARY JOBS BACK JANUARY’S STRENGTH?

The U.S. jobs report for February, due on March 6, is expected to show an increase of 60,000 jobs, according to a Reuters poll. It comes after January’s surprisingly robust report, with an increase of 130,000 jobs and the unemployment rate falling to 4.3%.

The January report allayed worries about a weakening labor market, but “the concern is that January is a one-off,” said Paul Nolte, senior wealth adviser and market strategist at Murphy & Sylvest Wealth Management.

“We saw a good January jobs report, but we also have seen a really weak 2025 for the job market,” Hooper said. “And so the question becomes, where do we go from here?”

Investors will also seek clues from the report about when the Federal Reserve may next cut interest rates. Fed funds futures suggest the next reduction will come in June or July, after Fed Chair Jerome Powell’s term ends in May and his nominated replacement Kevin Warsh could be in charge.

The Fed cut rates last year in the face of a weakening employment backdrop but paused the easing cycle in January, and solid jobs data could prompt investors to push back their expectations for further cuts. Investors generally associate lower interest rates with higher prices for stocks and other assets.

BNY’s Velis said the market’s reaction to the jobs data will be telling for which factors are prominent for equity investors. For example, strong data followed by weak stock performance is “going to be a sign that the rate argument is important,” Velis said.

RETAIL SALES, BROADCOM EARNINGS ALSO UP NEXT

Other economic releases due in the coming week include reports on manufacturing and services sector activity. The retail sales report for January is expected on March 6.

Aside from Broadcom’s quarterly report on Wednesday, results are expected from retailers Best Buy and Target.

Wall Street is eager for any evidence of AI’s impact on the economy, both positive and negative. In an interview with Reuters this week, outgoing Atlanta Fed President Raphael Bostic said the U.S. may be entering a period of structurally higher unemployment as firms deploy AI tools to save labor. “Major technological shifts provoke both excitement and anxiety,” Keith Lerner, chief investment officer at Truist Advisory Services, said in a research note on Thursday. “More recently… optimism has begun to give way to heightened anxiety and increasingly bleak narratives about AI’s impact on work, productivity, and economic outcomes.”

Israel says it launched pre-emptive attack against Iran

Edited excerpts from a chat with the senior fund manager:

The market has been stuck in a consolidation phase for the last 1.5 years. Now that earnings downgrades have slowed and US trade deal uncertainty is gone, what is holding the market back?

Over the past few weeks, India has secured a trade agreement with two of its largest trading partners, ie EU and US, which have a combined share of ~37% in India’s total goods exports. Overall, it is anticipated that the trade deals would be particularly beneficial in expanding market access and improving export competitiveness for India.

Secondly, incoming data indicates that the growth momentum seen in 3QFY26 has sustained into 4Q as well. Overall, the growth outlook remains constructive, with the RBI raising the FY2026 GDP forecast to 7.4% and the Economic Survey projecting 7.4% in FY2026 and 6.8–7.2% in FY2027, supported by domestic demand and ongoing reforms.

While we do not take top-down views on the market, the recent correction means that, on a relative basis, Indian equity markets are trading at or close to 10 year averages while the relative premium to EMs have narrowed to 45%, below the long term historical range, and far off its highs of 90% observed between 2022-2024. Over the past five years, India has recorded the highest annualised earnings growth among peers at ~10%, and is expected to sustain a healthy 14–15% growth trajectory going forward, although admittedly it is not significantly ahead of other major EMs over the next couple of years.

Although the macro implications of technological evolution remain uncertain, India’s diversified sectoral composition and relatively lower market volatility support a more stable and resilient earnings cycle.

Consumption was touted as a big theme after GST cuts were introduced before Diwali. Since then auto appears to be the only winner in the consumption cycle. Are you disappointed with the impact that GST is having on overall consumption in India?

Consumer-facing sectors saw a sequential improvement in earnings this quarter, although the recovery remains somewhat mixed across categories. In autos, revenue growth was supported by festive demand and GST rationalization, along with recovery in CVs. Consumer staples delivered sequentially a decent set of numbers, led by rural growth. Premiumization trends continue to stay strong and emerging channels such as e-commerce and quick commerce are continuing to scale well. Jewelry companies reported stellar performance at the back of rising gold prices which is a both headwind and tailwind at the same time for the category, coupled with the sustained trend of formalization of the sector in India. There is a view among the relatively smaller ticket discretionary lifestyle consumption category companies that the customers appear to have prioritized purchase of bigger ticket products with higher GST reduction benefits initially, which should change in the coming times aiding demand for their products.

Media and retail sector trends have been largely company- and event-driven with seasonality playing a role in some companies. More importantly, the earnings revision cycle remains uneven — autos are seeing early signs of estimated upgrades, but upward revisions across other consumer segments have been relatively muted.

Smaller sized private and PSU banks have reported a double-digit gold loan mix. Is this a healthy trend for their balance sheets?

Gold loans are regarded as among the lower risk retail products as (1) they are collateralized, (2) recovery is relatively quicker via auction and (3) borrower behavior tends to be disciplined and guided by emotional and sentimental value attached to their pledged items. Recent asset quality trends with CRIF data showing PAR >90 days below 1% across the system is far better than unsecured retail or MFI loans.

That said, we believe that any outsized exposure to a single segment increases lender risk, particularly if collateral values are affected during periods of volatility, as can occur with precious metals. While most private and PSU banks have robust risk management frameworks in place to mitigate such risks through prudent LTVs and monitoring mechanisms, concentration risk remains an important consideration.

As with any product, gold loans can be attractive from a margin standpoint, provided exposures remain well-calibrated and contained within a diversified portfolio framework.

Credit growth in many PSU banks has been higher than their private peers in Q3. Are PSU bank stocks looking more attractive? Are valuations good enough to buy?

Yes, recent asset quality trends and growth at large PSU banks have been comparable to those of large private sector peers. However, with any sub-segment, rather than taking a top-down view, we prefer to identify bottom-up opportunities.

Historically, the valuation gap between PSU and private banks has reflected differences in RoAs, as well as governance and capital allocation constraints. Also, it should not be missed that over time well-run private sector banks have gained market share when compared to PSU banks.

On an aggregate basis, the banking sector offers opportunities across the market-cap spectrum, and valuations do not appear stretched, with earnings expectations in the mid-teens.

Which sectors appear structurally well-positioned over the next three to five years, and why?

We are very stock selection driven as a house and do not make top down thematic or sectoral calls, as those are fraught with risk without adding returns in our view. Our sectoral over weights and underweights are an outcome of bottom-up stock picking opportunities at any given point in time, rather than an input to our portfolio construction. For the all-cap portfolio, from a bottom-up perspective, there are certain sectors where we consistently find more opportunities. Currently we see more promising prospects within private sector financials, consumer discretionary, communication services, healthcare, REITs and Invits. While not generalising, it is certain sub-segments and individual companies within them that find favour with the team.

Do you think that the sell-off in small caps we saw in last 1.5 years is done and that we will see gradual recovery in next 2 quarters?

Since its peak in Sep 2024, small caps have corrected meaningfully due to a combination of tighter liquidity, higher interest rates, and earnings downgrades. Much of this adjustment appears to have already played out and recent earnings trends within the small and mid-caps have been ahead of large caps. Having said that, a broad-based recovery in share prices usually requires sustained improvement in earnings momentum, cash flows, and risk appetite, which tends to lag market corrections, especially after prolonged periods of adjustment.

Historically, we find greater number of opportunities in the mid and small market cap and off-benchmark companies. We believe these segments of the market are typically less well researched and hence more inefficient, thereby providing strong alpha generation potential.

Although we tend to be bottom up focussed, looking ahead over the next couple of quarters, a gradual and selective recovery is a reasonable base case rather than a sharp rebound.

What stood out for you in the Q3 earnings season? Are you more hopeful of broad-based growth than before?

Earnings growth in Q3 has been stronger than recent quarters, with aggregate Nifty-500 Index earnings at 14%, with SMIDs outpacing large cap earnings. We note healthy earnings growth delivered by autos, capital goods and utilities, while consumption was gradual but uneven.

However, we would like to see a few more quarters of consistent earnings trends before gaining greater confidence in a sustained recovery in the earnings trajectory.

Form 144 ALNYLAM PHARMACEUTICALS For: 27 February

Form DEF 14A Adobe Inc. For: 27 February

Lithium bottom is in: global demand set to jump 25% as EV market recovers

Business

Berkshire Maven Bloomstran Says Stock Is Cheap Versus Intrinsic Value, Can Deliver 10%-Plus Returns

Berkshire Maven Bloomstran Says Stock Is Cheap Versus Intrinsic Value, Can Deliver 10%-Plus Returns

Nvidia NVDA -4.16%decrease; red down pointing triangle now makes more revenue in a single quarter than most other chip companies generate in an entire year. In a turbulent market awash in a new class of AI fears, that’s no longer enough.

The chip maker’s fiscal fourth-quarter results Wednesday showed why the company remains the undisputed leader in artificial-intelligence computing. Revenue of $68.1 billion was up 73% from the same period a year earlier and represented the company’s best growth rate in four quarters. Nvidia projected an even higher growth rate for the current quarter, and that forecast actually beat Wall Street’s consensus target by the widest range in two years, according to FactSet data.

Copyright ©2026 Dow Jones & Company, Inc. All Rights Reserved. 87990cbe856818d5eddac44c7b1cdeb8

Form 144 CONSOLIDATED EDISON INC For: 27 February

Pakistan, Afghan Taliban forces clash as diplomatic efforts intensify

Netflix Declines to Match Paramount’s Offer for Warner Bros.

Top 10 Altcoins Investing in Crypto Market Crash 2026 – DCA cryptocurrency coins list / Hindi Urdu

Bridgerton’s 10 best-rated episodes with a surprising winner

Israel says it launched pre-emptive attack against Iran

-

Politics6 days ago

Politics6 days agoBaftas 2026: Awards Nominations, Presenters And Performers

-

Sports5 days ago

Sports5 days agoWomen’s college basketball rankings: Iowa reenters top 10, Auriemma makes history

-

Fashion12 hours ago

Fashion12 hours agoWeekend Open Thread: Iris Top

-

Politics5 days ago

Politics5 days agoNick Reiner Enters Plea In Deaths Of Parents Rob And Michele

-

Business3 days ago

Business3 days agoTrue Citrus debuts functional drink mix collection

-

Politics1 day ago

Politics1 day agoITV enters Gaza with IDF amid ongoing genocide

-

Crypto World4 days ago

Crypto World4 days agoXRP price enters “dead zone” as Binance leverage hits lows

-

Business6 days ago

Business6 days agoMattel’s American Girl brand turns 40, dolls enter a new era

-

Business6 days ago

Business6 days agoLaw enforcement kills armed man seeking to enter Trump’s Mar-a-Lago resort, officials say

-

Tech4 days ago

Tech4 days agoUnsurprisingly, Apple's board gets what it wants in 2026 shareholder meeting

-

NewsBeat2 days ago

NewsBeat2 days agoCuba says its forces have killed four on US-registered speedboat | World News

-

NewsBeat2 days ago

NewsBeat2 days agoManchester Central Mosque issues statement as it imposes new measures ‘with immediate effect’ after armed men enter

-

NewsBeat5 days ago

NewsBeat5 days ago‘Hourly’ method from gastroenterologist ‘helps reduce air travel bloating’

-

Tech6 days ago

Tech6 days agoAnthropic-Backed Group Enters NY-12 AI PAC Fight

-

NewsBeat6 days ago

NewsBeat6 days agoArmed man killed after entering secure perimeter of Mar-a-Lago, Secret Service says

-

Politics6 days ago

Politics6 days agoMaine has a long track record of electing moderates. Enter Graham Platner.

-

Business2 days ago

Business2 days agoDiscord Pushes Implementation of Global Age Checks to Second Half of 2026

-

NewsBeat3 days ago

NewsBeat3 days agoPolice latest as search for missing woman enters day nine

-

Sports5 days ago

Sports5 days ago2026 NFL mock draft: WRs fly off the board in first round entering combine week

-

Business1 day ago

Business1 day agoOnly 4% of women globally reside in countries that offer almost complete legal equality