Crypto World

Draft bill in Turkey Seeks 10% Crypto Tax and Tighter Oversight of Exchanges

TLDR

- Turkey proposed a new bill that introduces a 10% tax on cryptocurrency income and gains.

- Lawmakers stated that platforms must withhold the tax on a quarterly basis for all users.

- The bill allows the president to adjust the withholding rate between 0% and 20%.

- Service providers would pay a 0.03% transaction tax on every crypto trade they facilitate.

- Authorities confirmed that tax enforcement will rely on detailed records kept by platforms.

- The bill connects all crypto definitions to the existing Capital Markets Law for consistency.

Turkey’s ruling party advanced a new plan that would introduce a 10% tax on cryptocurrency gains, and lawmakers presented the draft to parliament as they moved to update current tax laws while outlining new rules for service providers.

Proposed Crypto Tax Framework

Turkey introduced a draft bill that creates a new structure for crypto taxation, and lawmakers placed the proposal before the Grand National Assembly as they sought clear rules for the sector. They stated that platforms regulated under the Capital Markets Law must withhold a 10% tax on quarterly income and gains, and officials confirmed that this applies to residents and non-residents.

The bill grants the president the power to adjust the withholding rate, and officials said it could move between 0% and 20% depending on asset type. They also linked the tax rate to holding periods and wallet usage, and they highlighted that different token categories may face different rules.

The legislation introduces a 0.03% transaction tax for service providers, and it applies to the sale amount or market value of assets. Lawmakers said this measure covers platforms that facilitate trades, and they reported that brokers must maintain detailed records.

Authorities emphasized that incomplete user information may trigger enforcement, and the tax agency would pursue shortfalls directly from the user. The bill ties terms such as “crypto asset,” “wallet,” and “platform” to existing financial regulations, and it ensures consistent definitions across the law.

Market Context and International Comparisons

Chainalysis reported that Turkey recorded $200 billion in crypto activity between July 2024 and June 2025, and analysts stated that rising volumes followed economic pressure in recent years. They wrote that Turkey’s economic conditions pushed many users toward digital assets, and the report said people used crypto for alternative savings.

Turkey experienced inflation that peaked at 85% in late 2022, and the rate later stabilized near 30% by early 2025. Officials believe tax reform can support regulatory oversight, and they said the new framework aims to match existing market behavior.

Lawmakers referenced international trends, and they pointed to a Dutch plan that proposed a 36% capital gains tax on digital holdings. They acknowledged that the Dutch proposal awaits a Senate vote, and they said the measure could start in 2028.

The Turkish draft includes a VAT exemption for crypto deliveries covered by the transaction tax, and lawmakers confirmed that service providers fall under the updated expenditure rules. They also stated that foundation university hospitals will lose corporate tax exemptions in 2027, and they kept this clause in the broader bill.

The International Monetary Fund (IMF) lowered its global growth forecast for 2026 to 3.1% in its April update. This marks a 0.2 percentage point downgrade from its January estimate.

The Fund noted that the latest downgrade largely reflects economic disruptions stemming from the ongoing Middle East conflict. It added that in its absence, the outlook would have instead been revised upward by 0.1 percentage point to 3.4%.

IMF Cuts Growth, Lifts Inflation Forecast in 2026

The report added that the global growth forecast for 2027 remains unchanged from the January 2026 World Economic Outlook update.

Follow us on X to get the latest news as it happens

Meanwhile, global headline inflation is expected to edge higher in 2026 before resuming its downward trajectory in 2027. It is currently projected at 4.4% this year, before easing to 3.7% in 2027.

The economic impact remains uneven across regions. Emerging markets saw their 2026 growth outlook downgraded by 0.3 percentage points. Yet, projections for advanced economies were largely unchanged.

“Crucially, there is a high degree of cross-country dispersion in the reference forecast. While the growth and inflation revisions seem relatively modest at the global level, the toll on the conflict region and more vulnerable economies elsewhere—in particular, commodity-importing emerging market and developing economies with preexisting fragilities—is much more pronounced,” the report read.

The IMF also outlined additional downside risks. In a scenario where energy prices rise more sharply and persistently, global growth could slow to 2.5% in 2026.

At the same time, inflation may climb to 5.4%. A more severe disruption, particularly involving damage to energy infrastructure in the conflict region, would deepen the impact, dragging global growth to around 2% and pushing inflation above 6% by 2027. Emerging and developing economies would be disproportionately affected again, with nearly twice the impact as advanced economies.

The IMF said its latest World Economic Outlook uses a “reference forecast” rather than a traditional baseline. This reflects the difficulty of forming stable assumptions amid ongoing uncertainty.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post IMF Cuts 2026 Global Growth Forecast by 0.2 Points as Middle East War Hits Momentum appeared first on BeInCrypto.

Bitcoin is absorbing the return of Middle East risk better than oil or equities.

Bitcoin traded at $74,335 on Monday morning, down 1.6% over 24 hours but still up 4.8% on the week after the U.S. Navy seized an Iranian ship over the weekend and Tehran reimposed controls on the Strait of Hormuz.

Ether slipped 2.6% to $2,272, Solana fell 1.5% to $84, and BNB held flat at $618, with the broader top-10 showing red across the board but none of the moves breaching 3%.

Brent crude jumped 5.7% to $95.50 a barrel, European natural gas futures surged as much as 11%, S&P 500 futures fell 0.6% after Friday’s record close, and European equity futures indicated a 1.2% drop at the open. Gold fell 0.8% to $4,790, and the dollar edged up as traditional war-hedge demand returned.

The weekend flare-up reversed a three-week unwind of war risk premium. Iran had declared the Strait “completely open” on Friday, prompting the S&P 500’s record close and a broad rally across emerging markets.

By Sunday morning, Trump was threatening to destroy every power plant and bridge in Iran if negotiations fail, and Tehran was signaling it may skip a second round of talks while the U.S. maintains its naval blockade.

This is the fourth major Iran-related risk event crypto has absorbed since the conflict began, and the pattern of shrinking sell-offs continues. Earlier escalations produced sharper drawdowns in bitcoin than this one, with each successive flare-up compressing the magnitude of the crypto reaction even as oil and equities continue to price each headline fresh.

The divergence suggests crypto has largely finished pricing the geopolitical tail risk that traditional markets are still reacting to, either because holders who were going to sell on Iran headlines have already sold, or because the spot ETF bid has become a more reliable floor than the futures-driven weekend gaps that defined earlier cycles.

What traders will watch through the U.S. session is whether the 10-year Treasury yield holding near 4.27% and the dollar bid pull bitcoin lower through the risk-parity channel, or whether the equity correlation that dominated Q1 loosens on a day when the driver is explicitly geopolitical rather than macro-liquidity.

If bitcoin holds $74,000 through the European open and the Strait of Hormuz situation deteriorates further, the asset’s emerging reputation as a geopolitical shock absorber gains another data point. If the move extends below $73,000 on any incremental Iran headline, the shrinking-sell-off thesis breaks.

Geopolitical tensions surrounding the Strait of Hormuz renewed a risk-off mood across cryptocurrency markets over the weekend, pressuring Bitcoin after a brief rally earlier in the week. On Friday, Bitcoin surged above $78,300 on Coinbase — its highest level since early February — but the rally faded as broader developments escalated. By weekend’s end, BTC had retreated to the $75,000–$76,000 zone, and late Sunday slid further to briefly dip below $74,000 in the wake of a U.S. military operation in the region.

The U.S. military announced that it opened fire on and later seized an Iranian cargo ship it said was attempting to breach a blockade of Iranian ports, a move that Tehran characterized as a violation of a two-week ceasefire between the two nations. The ceasefire, which had contributed to a calmer backdrop for energy markets and crypto trading alike, is due to expire this week, with investors watching how any renewal or breakdown could influence risk assets.

As tensions escalated, Tehran signaled retaliation and reportedly rejected a new round of peace talks slated for Monday in Islamabad, citing the U.S. blockade. The combined stance from Washington and Tehran underscored the fragility of a de-escalation path, complicating the outlook for both oil and crypto markets in the near term.

The broader market backdrop reflected the tension. U.S. stock futures opened Sunday night lower, with S&P 500 futures down about 0.8%, Nasdaq-100 futures off 0.6%, and Dow futures down roughly 0.9% (around 450 points). Oil markets reacted in kind, with crude futures rising more than 4.5% and trading above $95 a barrel as supply concerns and geopolitical risk re-entered the narrative.

Crypto market sentiment also shifted. The Crypto Fear & Greed Index edged higher to 29 out of 100 on Monday, signaling a return to fear after a period of relative calm, though it remained in the cautious end of the spectrum rather than outright panic.

Bitcoin’s price trajectory over the weekend underscores how sensitive the crypto market remains to macro-driven risk factors in addition to its own supply-and-demand dynamics. The move back toward the mid-$70,000s after a weekend foray into the mid-$70k range highlighted the potential for renewed volatility should the conflict persist or escalate around Hormuz and related channels.

Cointelegraph has previously noted how macro tensions, including geopolitical flare-ups and oil price swings, have historically fed into bitcoin’s price action, offering a potential liquidity tilt during periods of global uncertainty. The current sequence — a Friday peak followed by a weekend retreat and a Sunday plunge tied to military actions — illustrates the ongoing intersection between energy markets, geopolitical risk, and crypto liquidity.

Looking ahead, the key question for traders is whether the ceasefire holds long enough for markets to re-price risk more calmly or if renewed escalation magnifies volatility. The end-date of the current two-week ceasefire looms large for both oil markets and digital assets, as any renewal terms or new conflict dynamics could reintroduce abrupt shifts in sentiment, liquidity, and hedge demand.

Analysts will also be watching how the U.S. and Iranian sides approach diplomacy in the coming days. Tehran’s rejection of new talks and its vow of retaliation, alongside the U.S. military actions, suggests that any easing in risk appetite may depend heavily on clear signals of de-escalation rather than the mere absence of headlines.

In the near term, Bitcoin and other major cryptocurrencies may continue to trade within a risk-off framework so long as geopolitical headlines dominate. Traders will likely weigh potential upside toward prior resistance levels against the risk of renewed volatility if tensions intensify or the ceasefire breaks down again. As always, liquidity, macro cues, and the evolving diplomatic calculus will shape the path forward for BTC and the broader crypto market.

What to watch next: the timing and outcome of any renewed discussions around the ceasefire, ongoing responses from both Tehran and Washington, and the corresponding reactions in oil and traditional equity markets. The coming days could reveal whether this episode marks a temporary pause in risk appetite or a more sustained shift in how investors price geopolitical risk into digital assets.

Crypto World

LayerZero blames Kelp’s setup for $290 million exploit, attributes it to North Korea’s Lazarus

LayerZero has placed responsibility for the $290 million Kelp DAO exploit on Kelp’s own security configuration, saying the liquid restaking protocol ran a single-verifier setup that LayerZero had previously warned against.

The attack used a novel vector targeting the infrastructure layer rather than any protocol code.

Attackers, whom LayerZero attributed with preliminary confidence to North Korea’s Lazarus Group and its TraderTraitor subunit, compromised two of the remote procedure call (RPC) nodes that LayerZero’s verifier relied on to confirm cross-chain transactions.

RPC nodes are the servers that let software read and write data on a blockchain, and LayerZero’s verifier used a mix of internal and external ones for redundancy.

The attackers swapped the binary software running on two of those nodes with malicious versions designed to tell LayerZero’s verifier that a fraudulent transaction had occurred, while continuing to report accurate data to every other system querying those same nodes.

That selective lying was engineered to keep the attack invisible to LayerZero’s own monitoring infrastructure, which queries the same RPCs from different IP addresses.

Compromising two nodes was not enough. LayerZero’s verifier also queried uncompromised external RPC nodes, so the attackers ran a distributed denial-of-service attack on those to force failover to the poisoned ones.

Traffic logs LayerZero shared show the DDoS running between 10:20 a.m. and 11:40 a.m. Pacific Time on Saturday. Once the failover triggered, the compromised nodes told the verifier a valid cross-chain message had arrived, and Kelp’s bridge released 116,500 rsETH to the attackers. The malicious node software then self-destructed, wiping binaries and local logs.

The attack only worked because Kelp ran a 1-of-1 verifier configuration, meaning LayerZero Labs was the sole entity verifying messages to and from the rsETH bridge.

LayerZero’s public integration checklist and direct communications to Kelp had recommended a multi-verifier setup with redundancy, where consensus across several independent verifiers would be required to confirm a message. Under that configuration, poisoning one verifier’s data feed would not have been enough to forge a valid message.

“KelpDAO chose to utilize a 1/1 DVN configuration,” LayerZero wrote, using the protocol’s term for decentralized verifier networks. “A properly hardened configuration would have required consensus across multiple independent DVNs, rendering this attack ineffective even in the event of any single DVN being compromised.”

LayerZero said it has confirmed zero contagion to any other application on the protocol. Every OFT-standard token and application running multi-verifier setups was unaffected.

The LayerZero Labs verifier is back online, and the company said it will no longer sign messages for any application running a 1-of-1 configuration, forcing a protocol-wide migration off single-verifier setups.

The architectural distinction matters for how DeFi prices LayerZero risk going forward.

A protocol-level bug would have implied every OFT token on every chain was potentially at risk. However, a configuration failure by a single integrator, combined with a targeted infrastructure attack, implies the protocol worked as designed and that Kelp’s security choices, not LayerZero’s code, created the opening.

Kelp has not yet publicly responded to LayerZero’s framing or addressed why it operated a 1-of-1 verifier setup despite the explicit recommendations against it.

Lazarus Group has been linked to the Drift Protocol exploit on April 1 and now Kelp on April 18, meaning the same North Korean unit has drained more than $575 million from DeFi in 18 days through two structurally different attack vectors: social engineering governance signers at Drift and poisoning infrastructure RPCs at Kelp.

The group is adapting its playbook faster than DeFi protocols are hardening their defenses.

Crypto protocols lost over $606 million to hacks in just 18 days of April 2026. That makes it the single worst month for exploits since February 2025.

The surge comes from two attacks on KelpDAO and Drift Protocol. Together, they account for 95% of April’s losses and 75% of 2026’s total of $771.8 million.

April 2026 Crypto Hack Losses Dwarf Q1 Combined

According to data from DefiLlama, April’s $606.2 million total across 12 incidents, it has already eclipsed the first quarter’s $165.5 million haul. That makes the month roughly 3.7 times as large as January, February, and March combined.

Follow us on X to get the latest news as it happens

| Month | Number of Hacks | Amount Lost |

| January | 12 | $100.1M |

| February | 8 | $24.2M |

| March | 15 | $41.3M |

| April (to April 18) | 12 | $606.2M |

| YTD Total | 47 | $771.8M |

Every month since February 2025 has held under $240 million, per DefiLlama’s tracker. That earlier figure was skewed by the $1.4 billion Bybit breach, which drove February 2025’s total to $1.466 billion.

April 2026’s losses arrived without any headline exchange hack of that size. The pattern shows how quickly attackers pivoted to Decentralized Finance (DeFi) infrastructure.

BeInCrypto reported that KelpDAO lost over $290 million on April 18, now the year’s largest single hack. Drift Protocol sits just behind at $285 million.

The damage has stacked up in recent days. Incidents at Vercel, Hyperbridge, Grinex Exchange, and Rhea Finance have piled in 2026.

“None of these accounts for the collateral damage seen across TVL, user trust, valuations, and the space’s morale. DeFi remains a niche market until risk can be properly priced; at this time, we’re far from it,” an anlyst wrote.

DeFi TVL Slides as Sentiment Cracks

DeFi total value locked (TVL) fell by more than 7% over the past 24 hours following the Kelp exploit. Aave alone dropped from $26.4 billion to near $17.9 billion.

“Every protocol is taking a hit now,” analyst Ted Pillows wrote.

Hack frequency is also climbing sharply. DeFi recorded 47 incidents in the first 4.5 months of 2026, compared with 28 over the same period in 2025. That works out to a roughly 68% year-over-year rise.

The reactions point to rising concern that DeFi’s risk pricing has not caught up with infrastructure-layer exploits. Dollar losses sit below 2025’s Bybit-skewed pace, yet incidents keep stacking. The next few weeks will show whether DeFi can tighten security before April’s trend defines the year.

The post April 2026 Becomes Worst Month for Crypto Hacks Since February 2025 appeared first on BeInCrypto.

The decentralized finance (DeFi) ecosystem is experiencing a sharp capital outflow following the weekend exploit of the KelpDAO protocol.

Leading DeFi lending platform Aave has lost $8.45 billion in deposits over the past 48 hours, driving a broader $13.21 billion decline in total value locked (TVL) across DeFi. TVL refers to the combined dollar value of crypto assets deposited across DeFi protocols, such as Aave, and is widely used as to measure liquidity and overall market activity.

Total value locked across DeFi fell from $99.497 billion to $86.286 billion, while Aave’s TVL declined by $8.45 billion to $17.947 billion over the same period, according to DefiLlama. Protocol-level data shows double-digit percentage drops across platforms, including Euler, Sentora, and Aave, with losses concentrated in lending, restaking, and yield strategies tied to the affected collateral.

The move stems from a $292 million exploit of Kelp’s bridge that allowed attackers to use stolen rsETH, a liquid re-staking token widely used in DeFi, as collateral to borrow funds on lending platforms.

Because these stolen tokens lacked legitimate collateral backing, borrowing against them created potential shortfalls for lenders. It’s similar to conning a traditional bank by depositing fake fiat and taking out loans against it, ultimately leaving the lender with bad debt.

Protocols responded by freezing affected markets, while panicked users withdrew funds, leading to a broad decline in total value locked.

Token prices have moved less sharply than deposits. The AAVE token is down about 2.5% over 24 hours, while UNI and LINK are down less than 1% over the same period, according to CoinDesk market data.

Peter Chung, head of research at Presto Research, said in a note the incident highlights risks in cross-chain infrastructure, particularly in verification systems used by bridges.

Early analysis suggests the issue may have originated in the verification layer rather than in smart contracts themselves.

Chung added that the episode also shows how interconnected DeFi protocols can transmit shocks beyond the initial point of failure, with withdrawal activity and market freezes extending to platforms without direct exposure to the exploit.

Bitcoin erased its weekend gains as it fell below $74,000 on Sunday after the US military seized an Iranian cargo ship, putting pressure on a ceasefire between the two countries.

Bitcoin (BTC) had soared above $78,300 late Friday on Coinbase, its highest price since early February, but dropped to between $75,000 and $76,000 over the weekend after Iran said it would close vital oil routes in the Strait of Hormuz.

The cryptocurrency then sank sharply late on Sunday to briefly trade below $74,000 after the US military said it opened fire on, and later seized, an Iranian cargo ship it claimed tried to run its blockade of Iranian ports, with Tehran accusing the US of violating an agreed ceasefire.

The two-week ceasefire between the US and Iran, which had helped boost the markets and temper oil prices, is set to end on Wednesday.

Tehran has vowed to retaliate over the US military’s seizure of the ship and has rejected a new round of peace talks slated for Monday in Islamabad, Pakistan, due to the US blockade, Iranian state media reported.

Related: Bitcoin eyes $90K as whales absorb 20x daily BTC supply in 30 days

US stock futures sank Sunday night amid rising tensions, with S&P 500 futures dropping 0.8%, Nasdaq-100 futures falling 0.6% and Dow Jones futures declining 0.9%, or about 450 points.

Oil futures also soared amid the hostilities and Iran’s threat to close the Strait of Hormuz, with crude oil futures rising over 4.5% to over $95 a barrel.

The Crypto Fear & Greed index rose by two points to a score of 29 out of 100 on Monday, its highest score since late January, but which still indicated a sentiment of “fear.”

Magazine: Bitcoin will not hit $1M by 2030, says veteran trader Peter Brandt

Crypto analyst Ansem argues that Ethereum (ETH) is in a “worse spot” in 2026 than it was in 2023, pointing to a thesis he says has been eroding for years.

His bearish take drew rebuttals from some members of the community. Meanwhile, on-chain activity and technical indicators elsewhere on the network flash bullish signals.

Ansem Lists Cracks in the ETH Thesis

Ansem argues that Solana (SOL) has dominated retail activity this cycle. Hyperliquid has taken the lead in perpetual futures trading, while rollups have failed to gain traction.

He also noted that Vitalik Buterin “publicly abandoned” the general-use rollup thesis. The ongoing Aave (AAVE) situation around the KelpDAO rsETH exploit, Ansem said, is a mark on Ethereum’s core value proposition of “safety + security of defi & insto interest.

“ETH thesis has been weakening consistently for years,” the analyst wrote. ETH in 2026 is in a worse spot than it was in 2023, amplified by AI doing extremely well & tech stocks being much more favorable investments with real revenues / emerging narratives / increasing momentum, ETH is a $300B asset with a ton of overhang from Tom Lee topblasting + complacent ETH holders sitting idle in defi protocols.”

Follow us on X to get the latest news as it happens

Technically, the analyst noted that ETH remains in a sustained downtrend after failing to break multi-year resistance. He projected that the second-largest cryptocurrency could slip to 2025 lows near $1,300 and to the bear-market lows from 2022.

“Tight invalidation 2377 assuming problems worsen if you want to play it loose assuming other risk assets continues doing well & drags it up probably somewhere around 2700/2800 invalidation fundamentals wise would want to see breakout activity from some new vertical,” the post read.

Community Members Push Back

The take triggered notable pushback. Ryan Berckmans accused Ansem of not understanding fundamentals. Leo Lanza went further, sharply dismissing the analyst’s bearish case on X.

Another user pointed to a 56% drop in the SOL/ETH pair this cycle.

“Soleth is down 56% after being up 12x+ *this cycle* because one guy decided to buy 5% of the eth supply after it had underperformed all cycle. idk why you guys act like i dont also bearpost solana i havent posted anything bullish about sol in over a year,” Ansem replied.

Not everyone shares the bearish view on Ethereum. BeInCrypto recently highlighted that network activity remains strong, while technical indicators like the Rainbow Chart and MACD are also flashing bullish signals.

With macro and geopolitical uncertainty still in play, the question is whether ETH slides further this year or stages a renewed rally.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Ansem Says Ethereum Is in a Worse Spot Than 2023 as Thesis Weakens appeared first on BeInCrypto.

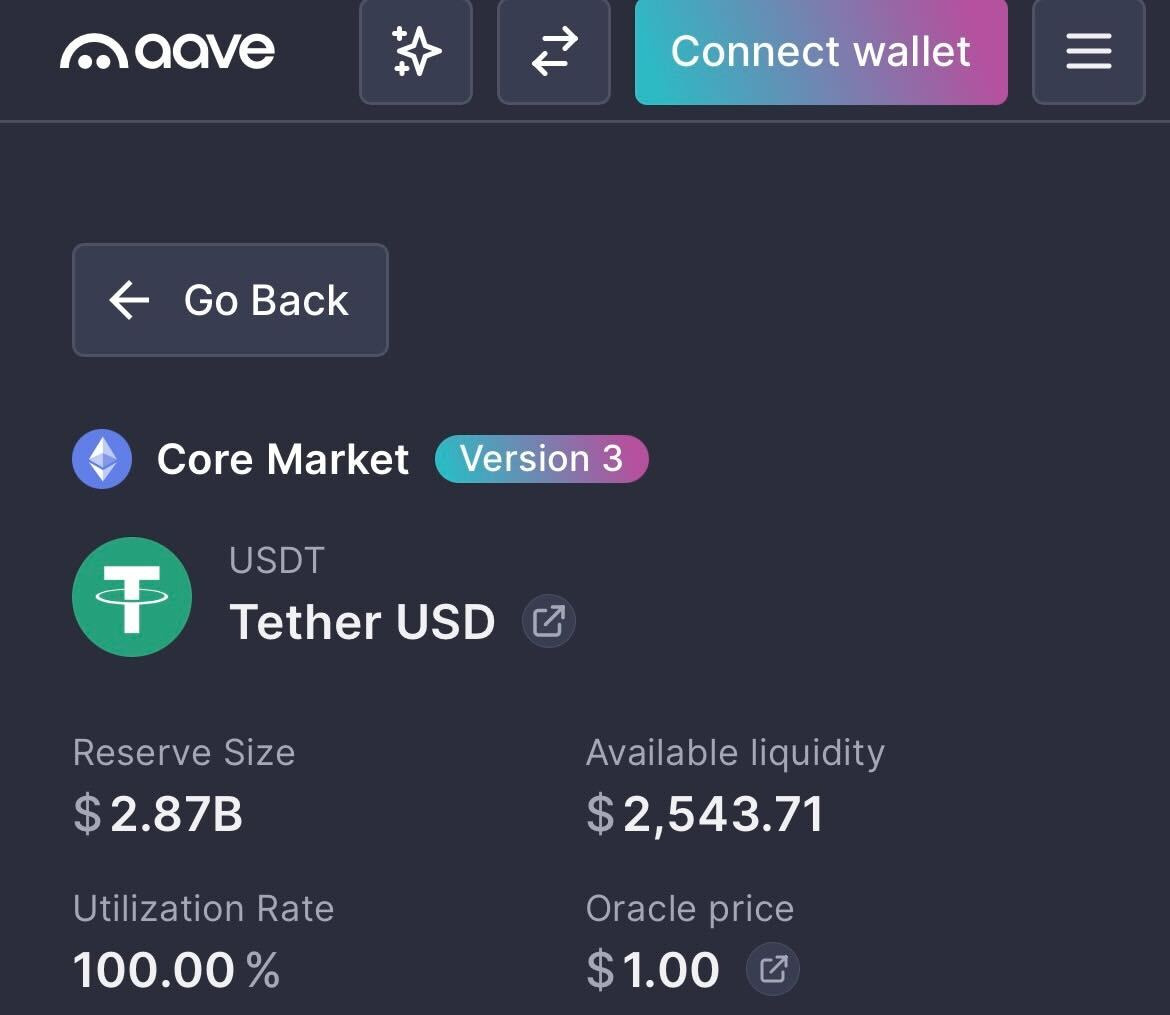

Total value locked on decentralized lending protocol Aave dropped by nearly $8 billion over the weekend after hackers behind the $293 million Kelp DAO exploit borrowed funds on Aave, leaving roughly $195 million in “bad debt” on the protocol and triggering withdrawals.

Data from DeFiLlama shows that Aave’s TVL fell from about $26.4 billion to $18.6 billion by Sunday, losing the top spot as the largest DeFi protocol.

Aave v3’s lending pools for USDt (USDT) and USDC (USDC) are now at 100% utilization, meaning that more than $5.1 billion worth of stablecoins cannot be withdrawn until new liquidity arrives or borrows are repaid.

Aave’s TVL fall shows how rapidly risk from a single security incident can spread throughout the broader, interconnected DeFi lending market, potentially leading to a severe liquidity crisis.

The incident began on Saturday when hackers stole 116,500 Kelp DAO Restaked ETH (rsETH) tokens worth about $293 million from Kelp DAO’s LayerZero-powered bridge and used them as collateral on Aave v3 to borrow wrapped Ether (wETH).

Crypto analytics platform Lookonchain said the move created about $195 million in “bad debt” on Aave, which contributed to the Aave (AAVE) token tanking nearly 20% from $112 on Saturday at 6:00 pm UTC to $89.5 about 25 hours later.

Lookonchain noted that some of the largest crypto whales to withdraw funds from Aave were the MEXC crypto exchange and Abraxas Capital at $431 million and $392 million, respectively.

Several crypto networks and protocols tied to rsETH or the LayerZero bridge have paused use of the bridge until the problem is resolved, including DeFi platform Curve Finance, stablecoin issuer Ethena and BitGo’s Wrapped Bitcoin (WBTC).

Aave has frozen several rsETH, wETH markets

Shortly after the Kelp DAO exploit, Aave said it froze the rsETH markets on both Aave v3 and v4 to prevent any suspicious borrowing and later stated that rsETH on Ethereum mainnet remains fully backed by underlying assets.

WETH reserves also remain frozen on Ethereum, Arbitrum, Base, Mantle and Linea, Aave said.

This incident marks the first significant stress test of Aave’s “Umbrella” security model, which was introduced in June 2025 to provide automated protection against protocol bad debt while enabling users to earn rewards.

Related: Aave DAO backs V4 mainnet plan in near-unanimous vote

Earlier this month, the Bank of Canada found that Aave avoided bad debt in its v3 market by using overcollateralization, automated liquidations and other strategies that shifted risk to borrowers.

In comments to Cointelegraph, Aave defended its liquidation-based model, framing it as a core safety mechanism that protects lenders while limiting downside for borrowers.

It comes as Aave parted ways with its longest-standing DeFi risk service provider, Chaos Labs, on April 6, following disagreements over the direction of Aave v4 and budget constraints.

Magazine: Are DeFi devs liable for the illegal activity of others on their platforms?

A breach at web infrastructure provider Vercel is forcing crypto teams to rotate API keys and do a deep inspection of their underlying code.

In a bulletin, Vercel said the hacker was able to grab behind-the-scenes settings that weren’t locked down, potentially exposing API keys — the digital credentials apps use to connect to other services. Those credentials act like digital passwords, allowing software to connect to databases, crypto wallets, and external services. In the wrong hands, they can be used to impersonate an app, burn through usage limits, or manipulate how it runs.

A post on cybercrime forum BreachForums claimed to be selling Vercel data for $2 million, including access keys and source code, though those claims have not been independently verified. Vercel said it has engaged incident response firms and law enforcement and is continuing to investigate whether any data was exfiltrated.

The company traced the intrusion to Context.ai, a third-party AI tool used by an employee, its CEO said in an X post, where a compromised Google Workspace connection allowed attackers to escalate access into Vercel’s internal environments. Vercel said environment variables marked as “sensitive” are stored in a way that prevents them from being read, and that there is no evidence that they were accessed.

The incident is drawing scrutiny because Vercel underpins frontend infrastructure for many crypto applications and is the primary steward of Next.js, one of the most widely used web development frameworks. Many Web3 teams host wallet interfaces and decentralized app dashboards on Vercel, relying on environment variables to store credentials that connect their frontends to blockchain data providers and backend services.

Solana-based decentralized exchange Orca said its frontend is hosted on Vercel and that it has rotated all deployment credentials as a precaution. The project added that its on-chain protocol and user funds were not affected.

Crash victim, 86, was determined to walk again, court hears

Opinion: Hunker down for a trifecta of trouble

IMF Cuts 2026 Global Growth Forecast by 0.2 Points as Middle East War Hits Momentum

-

Crypto World6 days ago

Crypto World6 days agoThe SEC Conditionalises DeFi Platforms to Be Avoided for Broker Registration

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Theodora Dress

-

NewsBeat6 days ago

NewsBeat6 days agoTrump and Pope Leo: Behind their disagreement over Iran war

-

Crypto World6 days ago

Crypto World6 days agoSEC Signals Exemption for Crypto Interfaces From Broker Registration

-

News Videos5 days ago

News Videos5 days agoSecure crypto trading starts with an FIU-registered

-

Sports3 days ago

Sports3 days agoNWFL Suspends Two Players Over Post-Match Clash in Ado-Ekiti

-

Crypto World6 days ago

Crypto World6 days agoSEC Proposes Certain Crypto Interfaces Don’t Need to Register as Brokers

-

Business15 hours ago

Business15 hours agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Politics2 days ago

Politics2 days agoPalestine barred from entering Canada for FIFA Congress

-

Crypto World2 days ago

Crypto World2 days agoRussia Pushes Bill to Criminalize Unregistered Crypto Services

-

Sports7 days ago

Sports7 days agoNWFL opens Pathway for new Clubs ahead of 2026 Season

-

Business3 days ago

Business3 days agoCreo Medical agree sale of its manufacturing operation

-

Entertainment6 days ago

Entertainment6 days agoBrand New Day’ Footage Reveals the Devastating Impact of ‘Now Way Home’

-

Politics20 hours ago

Politics20 hours agoZack Polanski demands ‘council homes not luxury flats for foreign investors’

-

Crypto World7 days ago

Crypto World7 days agoTrump whales load up ahead of Mar-a-Lago luncheon.

-

Business7 days ago

Kering slides after Morgan Stanley downgrade, Gucci woes loom

-

Tech7 days ago

Tech7 days agoApple glasses won’t go brand shopping like Meta did with Ray-Ban and Oakley

-

Tech7 days ago

Tech7 days agoGoogle adds E2E encryption to Gmail for iOS and Android enterprise users

-

Tech5 days ago

Tech5 days agoMicrosoft adds Windows protections for malicious Remote Desktop files

-

Entertainment6 days ago

Entertainment6 days agoKarol G’s ‘Ultra Raunchy’ Coachella Set Gave ‘Satanic Vibes’

You must be logged in to post a comment Login