Crypto World

Binance formally denies Iran sanctions violation allegations

Binance has rejected allegations that its platform allowed transactions linked to entities in Iran.

Summary

- Binance issued a formal response to a U.S. Senate inquiry denying claims that it allowed transactions linked to Iran.

- The exchange said media reports cited in the inquiry contain false and unsupported allegations about its compliance program.

- Binance pointed to investigations that led to the removal of certain entities and its expanded compliance measures.

The exchange issued a response on March 6 to a letter sent by Richard Blumenthal regarding sanctions compliance and anti-money laundering controls. The inquiry referenced several recent media reports. Binance said those reports contain false and unsupported claims about its compliance program.

Binance said it runs a large compliance operation to prevent sanctioned users from accessing the platform. Identity verification is required for every user, and individuals located in Iran are not allowed to use the exchange.

Compliance program and monitoring systems

According to the company, millions of dollars have been invested in compliance infrastructure in recent years. The compliance team now includes more than 1,500 professionals around the world. Many focus on sanctions monitoring, financial crime investigations, and counter-terrorism financing checks.

More than 25 monitoring tools are used to screen users and review transactions. Customer onboarding checks, sanctions screening, and behavioral analysis are also applied to detect suspicious activity. When concerns appear, cases are reviewed and information can be shared with law enforcement.

The company also pointed to its cooperation with investigators. In 2025 alone, Binance handled more than 71,000 law-enforcement requests. Over the past three years, authorities seized more than $752 million with assistance from the exchange.

Blockchain analytics data cited by Binance shows a decline in exposure to wallets linked to illicit activity. Between January 2024 and July 2025, the share of exchange volume connected to such wallets dropped from 0.284% to 0.009%.

Investigations involving flagged entities

The inquiry also mentioned two trading entities, Hexa Whale and Blessed Trust, which were reported to have indirect exposure to wallet addresses with possible links to Iran.

Binance said it became aware of those concerns after receiving requests from law enforcement in 2025. Investigations were then carried out by the exchange’s internal team. Transaction records were reviewed and user information was provided to authorities.

After the reviews were completed, both entities were removed from the platform. Hexa Whale was offboarded in August 2025, while Blessed Trust was removed in January 2026. Binance said it is not aware of any account on the exchange that directly transacted with an Iran-based entity.

The company also rejected claims that it had identified thousands of Iranian-linked accounts. Binance said it never made such a determination and noted that any attempt to bypass location restrictions using a VPN violates its terms of service.

Binance said it investigates credible risks, removes accounts when necessary, and works with authorities to address potential misuse of its platform.

Bitcoin fell to $67,960 by Saturday morning, down 3.4% over the past 24 hours and retreating sharply from the past week’s high. The move fits what has become a recurring script in recent months, with late-week selling dragging prices toward the lower end of the range heading into Saturday.

Majors took the harder hit again. Ether dropped 4.4% to $1,974, solana fell 4% to $84.31, dogecoin lost 2.9% to $0.09, and BNB slid 2.6% to $627. XRP fell 2.2% to $1.37.

The weekly picture tells a more nuanced story though. Bitcoin is still up 3.6% over seven days. Ether has gained 2.6%. BNB added 2.1%. The mid-week surge absorbed the war shock and then some, even if Friday’s pullback took the shine off.

Meanwhile, the dollar posted its steepest weekly gain in a year, strengthening as markets priced in higher energy costs, stickier inflation, and a Fed that has even less room to cut rates. That’s a direct headwind for bitcoin and every other asset denominated against the dollar.

“As tensions escalated in the Middle East last week, investors moved quickly to the safety of the U.S. dollar, which strengthened as markets began pricing in higher energy prices and reignited inflation fears, potentially delaying Federal Reserve rate cuts,” said Björn Schmidtke, CEO of Aurelion, in an email to CoinDesk.

The on-chain data paints a fragile picture beneath the surface. Glassnode data shows 43% of bitcoin’s total market supply is now sitting at a loss. That’s a significant overhang.

As bitcoin recovers, those underwater holders have an incentive to sell into any rally to break even, creating persistent resistance on the way up. It’s one reason the push to $74,000 on Thursday couldn’t hold. Every bounce toward higher prices runs into supply from people who’ve been waiting months to get out.

One bright spot came from stablecoin flows. Messari recorded a 415% jump in net stablecoin inflows to $1.7 billion over the week, with daily transfers up nearly 10%. That’s potentially dry powder waiting to be deployed, and it suggests retail isn’t entirely absent despite the fear-heavy sentiment. Whether that capital rotates into bitcoin or waits for lower prices is the question.

The war continues to set the tempo. The U.S.-Iran conflict showed no signs of resolution this week. Oil remains elevated. The Strait of Hormuz is still disrupted. And the macro backdrop of strong dollar, sticky inflation, and delayed rate cuts is the worst combination for risk assets.

Bitcoin’s week looked impressive in headlines, touching $74,000 mid-week, but the round trip from $68,000 to $74,000 and back to $68,000 is just another lap of the range.

Retail investors have been scooping up Bitcoin after it slipped below $70,000, but whale activity suggests the price could still head lower if past patterns repeat, according to crypto sentiment platform Santiment.

“The moment Bitcoin hit $74k, these key stakeholders began taking profit,” Santiment said in a report on Friday.

Santiment explained that whales — those holding between 10 and 10,000 Bitcoin (BTC) — “accumulated heavily” between Feb. 23 and Mar. 3, when Bitcoin was trading between $62,900 and $69,600.

Since Wednesday, when Bitcoin climbed past $70,000 and touched $74,000, the cohort has offloaded around 66% of their recent purchases, Santiment said. Meanwhile, retail investors — those holding below 0.01 Bitcoin — have been increasing their positions.

Correction may not be over yet, says Santiment

“When retail buys while whales sell, it typically signals that the correction is not yet over,” Santiment said. Bitcoin is trading at $67,984 at the time of publication, according to CoinMarketCap.

Bitcoin’s price decline led the Crypto Fear & Greed Index to fall 6 points, pushing it further into “Extreme Fear” territory with a score of 12 on Saturday.

MN Trading Capital founder Michael van de Poppe shared a similar outlook, saying a further decline is possible. “If Bitcoin doesn’t find support in this $67-68K region, then we’re likely going to retest the lows for liquidity before bouncing back upwards,” van de Poppe said in an X post on Friday.

Spot Bitcoin ETFs post largest outflow day in three weeks

The decline coincided with US-based spot Bitcoin ETFs posting their largest outflow day since Feb. 12, with a total of $348.9 million in net outflows across the 11 ETF products, according to Farside data.

Related: Trump’s National Cyber Strategy pledges to support crypto and blockchain

Bitcoin’s price fell as low as $60,000 on Feb. 6 during its downtrend from the October all-time high of $126,000 before showing a modest recovery. Economist Timothy Peterson suggests this level could be the floor for the time being.

“This valuation level has always marked a bottom for Bitcoin. About 99.5% chance it stays above $60k,” Peterson said in an X post, referring to the Bitcoin Price to Metcalfe Value chart.

Magazine: The debate over Bitcoin’s four-year cycle is over: Benjamin Cowen

The US administration released its National Cyber Strategy on Friday, signaling that crypto and blockchain technologies are now explicitly targeted for protection and secure integration within the nation’s digital infrastructure. Industry executives say the emphasis could shape policy levers ranging from funding for security research to potential enforcement actions. The six-page document frames the crypto ecosystem not only as a financial frontier but as a critical layer in national security, calling for secure supply chains and privacy protections from design to deployment. As crypto firms digest the implications, questions linger about how the administration will balance innovation with controls on privacy tools, mixers, and unregulated off-ramps.

Among the bold lines, the strategy states a commitment to “build secure technologies and supply chains that protect user privacy from design to deployment, including supporting the security of cryptocurrencies and blockchain technologies.” That clause, highlighted by industry observers as a first for a US cybersecurity framework, signals a potential opening for closer public-private collaboration on security standards. Yet, the policy also contains tougher language about criminal infrastructure and the denial of financial exits for illicit actors, a section that some analysts say could justify crackdowns on privacy-focused tools and crypto mixers in the longer run.

“We will build secure technologies and supply chains that protect user privacy from design to deployment, including supporting the security of cryptocurrencies and blockchain technologies.”

For Galaxy Digital’s head of firmwide research, the wording is a telling shift. Alex Thorn argued that explicitly naming crypto and blockchain as technologies to be protected marks a milestone in how Washington views the sector’s role in national security. The broader document, the industry veteran noted in a post, maps a future where cybersecurity risk management dovetails with crypto governance, potentially guiding federal engagement with crypto firms and infrastructure projects.

Another thread running through the document concerns resilience against emerging threats, notably quantum computing. Castle Island Ventures founder Nic Carter has been vocal about quantum risk to Bitcoin and the broader crypto ecosystem. In a take that aligns with the strategy’s emphasis on modernizing federal information systems, Carter pointed to the section calling for “post-quantum cryptography, zero-trust architecture, and cloud transition” as proof that policymakers are taking quantum threats seriously. “Sure seems like they’re taking quantum seriously. Nothing to worry about, I’m sure,” he said on X.

Bitcoin’s quantum risk lens tightens policy dialogue

The strategy’s posture toward quantum resilience comes at a time when the industry has debated how close practical quantum computing is to undermining current cryptographic underpinnings. Carter’s views reflect a broader tension inside the crypto community: balancing the need for robust, future-proof security with the practicalities of ongoing network upgrades and governance. The document’s emphasis on post-quantum cryptography is not merely an academic exercise; it foreshadows potential standards for federal and industry-grade security that could ripple through crypto custody, exchanges, and other critical components of the ecosystem.

In the same breath, the strategy reframes AI as a frontier technology that warrants careful risk management and innovation safeguards. The document states, “We will secure the AI technology stack—including our data centers—and promote innovation in AI security.” For crypto developers and asset managers, that phrasing suggests a growing overlap between AI-enabled security tooling, data integrity, and the safeguarding of sensitive financial information within crypto networks.

Beyond technology, the strategy highlights the importance of recruiting the next generation of cyber professionals to design and deploy advanced cyber technologies. This workforce emphasis mirrors a broader policy objective of aligning national security priorities with a vibrant tech economy, including the crypto sector, which relies on sophisticated cryptography, secure software supply chains, and resilient cloud infrastructure.

Market context

Market participants are watching how this policy direction translates into practical steps. The strategy’s emphasis on secure technologies and anti-criminal enforcement may influence risk sentiment, regulator expectations, and capital flows within crypto markets. While the document stops short of prescribing specific new rules, its signaling—particularly around post-quantum security, zero-trust architectures, and secure supply chains—could shape future standards, audits, and compliance requirements for crypto firms and their service providers.

Why it matters

For crypto users and investors, the strategy’s framework could translate into clearer security expectations and potentially more formal coordination between government agencies and the private sector on safeguarding digital assets. Acknowledging crypto and blockchain as technologies warranting protection might open avenues for collaboration on security research, testing, and standard-setting, helping to reduce systemic risk in the space.

For builders and operators, the document signals that security-by-design will be a central theme in any future regulatory guidance. Post-quantum readiness, zero-trust adoption, and robust cloud migration plans could become de facto prerequisites for governmental contracts, subsidies, or public-private partnerships, shaping how wallets, exchanges, and custody solutions structure their software, audits, and incident-response playbooks.

From a policy perspective, the juxtaposition of safeguarding innovation with criminal offense enforcement creates a dynamic tension. The “uproar against criminal infrastructure” language may push policymakers to balance privacy rights with anti-money-laundering goals, a debate that will likely surface in regulatory conversations and legislative proposals in the months ahead. Market participants will need to watch not only for new rules but for how agencies interpret and implement the strategy’s guardrails across different fiscal cycles and political winds.

What to watch next

- Implementation details on the post-quantum cryptography rollout and zero-trust adoption across federal information systems.

- Guidance or proposed regulations related to privacy-focused tools, mixers, and off-ramps for digital assets.

- Standards development and collaboration efforts between government agencies and crypto industry participants on secure supply chains.

- Budget allocations or policy actions that fund cybersecurity research relevant to crypto infrastructure.

Sources & verification

- President Trump’s Cyber Strategy for America (White House PDF): https://www.whitehouse.gov/wp-content/uploads/2026/03/President-Trumps-Cyber-Strategy-for-America.pdf

- Galaxy Digital’s Alex Thorn on crypto security in the strategy: https://x.com/intangiblecoins/status/2030078133303455922?s=20

- Nic Carter on quantum readiness and policy emphasis: https://x.com/nic_carter/status/2030091238742053115?s=20

- Bitcoin quantum risk discussion and institutional concerns: https://cointelegraph.com/news/bitcoin-quantum-computing-risk-institutions-developers

- Bitcoin price context referenced in coverage: https://cointelegraph.com/bitcoin-price

National Cyber Strategy reframes crypto under security and quantum guardrails

The six-page document makes it clear that the administration views cryptography, digital assets, and blockchain as components of critical national infrastructure rather than peripheral technologies. While the exact regulatory path remains to be seen, the emphasis on post-quantum readiness and secure, privacy-conscious design sets a baseline for how federal agencies intend to engage with the crypto ecosystem. Industry voices have already started parsing the strategy’s language for practical implications—ranging from research funding opportunities to potential investigations into privacy-preserving architectures and on-ramps.

The strategy’s commitment to privacy-by-design, coupled with its tough stance on combatting illicit financial activity, positions the policy as a pivot point for the sector. Whether this translates into collaboration on cryptographic standards or a tightening of enforcement around privacy tools remains to be seen. What is clear is that the policy framework now recognizes crypto and blockchain as central to national security considerations, not just speculative technologies with speculative risk profiles.

TLDR:

- Former CFO diverted $35M into DeFi lending platforms despite company policy requiring conservative investments.

- Crypto investments promising 20% yields collapsed within weeks, wiping out nearly all of the company funds.

- The software firm laid off 60 employees after the financial losses triggered a major restructuring.

- A federal court sentenced the executive to two years and ordered repayment of the full $35,000,100.

A former chief financial officer has received a two-year prison sentence after diverting $35 million in company funds into risky cryptocurrency investments.

U.S. federal prosecutors said the executive secretly transferred the money to a DeFi platform he controlled. The funds quickly collapsed in value after being placed in high-yield crypto lending protocols.

The case exposes how unauthorized crypto bets can devastate corporate finances.

CFO Moves $35M Into DeFi Lending Platforms

Nevin Shetty served as chief financial officer at a private software company beginning in March 2021. The firm raised capital to support growth and product development.

Company leadership adopted an investment policy designed to protect those funds. The policy restricted investments to conservative instruments such as money market accounts.

According to the U.S. Attorney’s Office for the Western District of Washington, Shetty helped draft that policy. However, he later transferred company funds into a cryptocurrency venture he secretly controlled.

Court records show Shetty launched a side company called HighTower Treasury in early 2022. The business had no outside customers.

Between April 1 and April 12, 2022, Shetty ordered wire transfers totaling $35,000,100 from a Chase branch near his home. The funds moved into HighTower Treasury accounts.

Prosecutors said Shetty then deployed the money across decentralized finance lending protocols. These platforms advertised yields exceeding 20 percent.

HighTower planned to return a smaller fixed payment to the software company. Shetty and his partner would keep the remaining profits.

Federal prosecutors stated the arrangement allowed Shetty to personally benefit from returns generated with company funds.

Crypto Investments Collapse Within Weeks

Initial results appeared profitable. According to court filings, the strategy generated roughly $133,000 in profits during the first month.

However, the DeFi investments soon deteriorated. Crypto market losses rapidly erased the value of the positions.

By May 13, 2022, the investment portfolio had nearly reached zero value. Almost the entire $35 million disappeared.

After the collapse, Shetty informed two fellow executives about the transfers. The company dismissed him immediately.

The financial damage forced the firm to restructure operations. Court documents state the company laid off around 60 employees after the loss.

The U.S. Attorney’s Office described the scheme as a calculated fraud carried out over several months. Prosecutors argued Shetty misled colleagues and financial institutions during the transfers.

Following a nine-day trial, a jury convicted Shetty in November 2025 on four counts of wire fraud. Federal investigators from the FBI’s Seattle field office supported the case.

A federal judge sentenced Shetty to two years in prison and ordered repayment of $35,000,100. He will serve three years of supervised release after prison.

The court also barred him from serving as a corporate officer without approval from a probation officer.

Bitcoin is firmly in the deepest phase of the bear market and the pain may worsen, according to CK Zheng, founder of crypto investment firm ZX Squared Capital.

“Bitcoin’s price is convincingly in deep bear market territory now. We expect a further 30% price drop during 2026 as the Iran war started,” Zheng told CoinDesk in an email, citing the “four-year cycle” as one of the key catalysts.

The world’s largest cryptocurrency has already nearly halved since hitting a record high of over $126,000 in October last year, according to CoinDesk data. As of writing, it changed hands at around $68,000.

The four-year bitcoin cycle

Crypto investors often talk about the “four-year cycle” – a pattern in which prices surge, crash, and then recover, centred on the quadrennial mining reward halving.

The halving, most recently implemented in April 2024, is a programmed event that halves bitcoin’s supply expansion rate every 4 years. As of today, 3.125 BTC are emitted as rewards for each block mined on the Bitcoin network, down from the original 50 BTC at launch after four halving events to date.

Historically, bitcoin’s price has tended to peak about 16–18 months after a halving, followed by a bear market that typically lasts about a year.

BTC topping out in October last year, roughly 18 months after the April 2024 halving, means the cycle is playing out again. So, the bear market could deepen in the near term.

Zheng said that the cycle is proving very difficult to break. According to him, the reason is simple: human psychology.

“The “Four-year crypto cycle” momentum is gaining strength and is extremely difficult to break due to individual investors’ psychological behaviors,” Zheng said.

Individual investors tend to behave in predictable ways — buying during hype and selling during panic. That behavior reinforces the boom-and-bust four-year pattern that has defined crypto markets for more than a decade.

Because of this, Zheng said bitcoin still trades more like a speculative asset than a safe haven like gold.

He added that the institutional adoption of bitcoin remains very slow and limited in scope at this stage and warned that some firms that have purchased bitcoin as a treasury asset may be forced to sell, leading to a deeper price sell-off.

“The total size of crypto ETFs and Digital Asset Treasury companies is only around 10% of the whole crypto market. Some Digital Asset Treasury firms may be forced to sell cryptos to meet certain debt servicing requirements during this bear market, which may create a vicious cycle,” Zheng said.

For now, Zheng’s outlook is clear: crypto’s bear market may have further to run before the next cycle begins.

“Our long-term target is $0.9000,” one analyst stated.

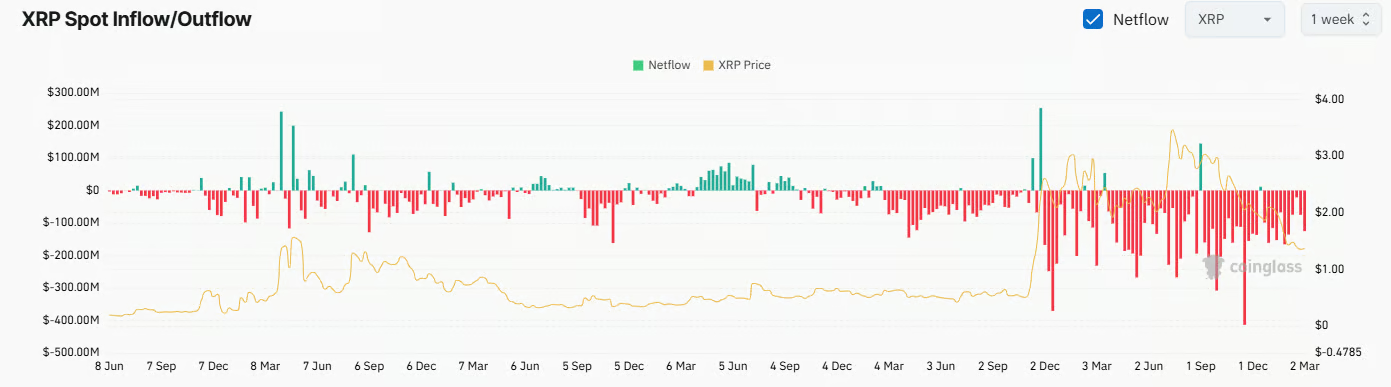

Ripple’s XRP has registered a minor uptick over the past week, coinciding with the broader cryptocurrency market’s revival.

However, some analysts believe its price may decline sharply in the near future and even fall below the psychological $1 level.

New Pullback Ahead?

Earlier this week, XRP tried to reclaim the $1.50 mark but failed and now trades at around $1.39 (per CoinGecko’s data). The asset’s market capitalization stands at approximately $85 billion, making it the fourth-biggest cryptocurrency, trailing behind BTC, ETH, and USDT.

One person who has been closely monitoring its performance is the X user TradingShot. In their view, XRP has been moving within a downward channel throughout its entire bear cycle, which, according to the chart, began in July 2025 – shortly after the price reached its all-time high of over $3.65.

TradingShot noted that the severe decline in February this year hit the previous target on the 1W MA200, suggesting the asset’s next potential pullback may lead to a further drop to the 1M MA100 support, set at under $0.90.

“This level is critical as it formed the June 2022 bottom of the previous Bear Cycle. Our long-term Target is $0.9000,” the X user concluded.

X user WealthManager also presented a bearish forecast. They believe XRP looks “very dangerous” right now, warning that a “huge drop could be imminent.”

Meanwhile, the prominent Bitcoin educator and advocate Adam Livingston spoke sharply against Ripple’s native cryptocurrency. He said he would rather have $100,000 in FTX customer refund claims than $100,000 in XRP.

You may also like:

“At least SBF might send a heartfelt apology from prison before he dies of old age,” Livingston added.

The Bullish Scenario

Despite the pessimistic views some express toward XRP, many indicators suggest its price may head north soon. Numerous market observers pointed out that large investors have purchased almost 4.2 billion tokens (worth a whopping $5.7 billion at current rates) since the October 10 crash.

This development reduces the amount of XRP tokens available on the open market, and economic principles dictate that the valuation should rise if demand doesn’t diminish. Moreover, this shows that whales are confident in the asset and view lower prices as an opportunity, a signal that could encourage smaller players to follow suit.

XRP’s exchange netflow is next on the list. Over the past several weeks, outflows have consistently exceeded inflows, indicating that investors are moving their holdings off centralized platforms and into self-custody. This shift reduces the amount of coins immediately available for sale, easing short-term selling pressure.

The asset’s Relative Strength Index (RSI) is also worth mentioning. It has fallen to around 30 on a weekly scale, marking oversold territory that can sometimes be a precursor to a rally. On the other hand, ratios above 70 are considered bearish.

Binance Free $600 (CryptoPotato Exclusive): Use this link to register a new account and receive $600 exclusive welcome offer on Binance (full details).

LIMITED OFFER for CryptoPotato readers at Bybit: Use this link to register and open a $500 FREE position on any coin!

Crypto industry executives are combing through US President Donald Trump’s National Cyber Strategy after it was released on Friday, searching for hints about what it could signal for government support of the crypto industry.

“Crypto and blockchain are explicitly named as technologies to be ‘protected and secured.’ This is a first for any US cybersecurity strategy,” Galaxy Digital’s head of firmwide research Alex Thorn said in an X post on Friday.

Crypto and blockchain were mentioned once in the six-page report:

“We will build secure technologies and supply chains that protect user privacy from design to deployment, including supporting the security of cryptocurrencies and blockchain technologies.”

However, industry executives have also been interpreting other parts of the document to see how they relate to crypto.

Thorn pointed to a section pledging to “uproot criminal infrastructure and deny financial exit and safe haven.” “This language could easily justify crackdowns on mixers, privacy coins, and unregulated off-ramps,” he said.

Bitcoin VC points out that quantum has been taken “seriously”

Castle Island Ventures founder Nic Carter, who has been vocal about the threat of quantum computing to Bitcoin (BTC) in recent times, pointed to the section saying the government “will accelerate the modernization, defensibility, and resilience of federal information systems by implementing cybersecurity best practices, post-quantum cryptography, zero-trust architecture, and cloud transition.”

“Sure seems like they’re taking quantum seriously. Nothing to worry about, I’m sure,” Carter said in an X post.

It comes as the crypto industry continues to debate about how close quantum computing is to being a serious threat to Bitcoin. On Feb. 15, Carter said that major Bitcoin-holding institutions may eventually lose patience with Bitcoin developers for not addressing quantum computing concerns quickly enough.

Trump points to the next generation as a priority

Trump said that the National Cyber Security outlines his priorities for “ensuring that America remains unrivaled in cyberspace.” Artificial intelligence was a key focus of the report.

“We will secure the AI technology stack—including our data centers—and promote innovation in AI security,” it said.

Related: Community banks and crypto industry ‘are allies’ in CLARITY Act debate: Exec

Trump also emphasized the importance of recruiting the next generation of workers in the cyber workforce to “design and deploy exquisite cyber technologies and solutions.”

The US typically releases a national cybersecurity strategy every administration, outlining the government’s priorities for emerging technologies.

Magazine: The debate over Bitcoin’s four-year cycle is over: Benjamin Cowen

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

The man behind the pseudonym Mark Zuckerfart has resurfaced after months of speculation. In an exclusive interview, the marketer explains why he left the Solfart project and why he now believes Patos Meme Coin has the team, strategy, and momentum to dominate the next wave of Solana meme tokens.

crypto.news presents an exclusive look at the man behind the pseudonym: Mark Zuckerfart. With a track record of scaling meme coins into the hundreds of millions, Zuckerfart has long been a silent engine in the marketing and creative space.

But his latest chapter came with a cost. After a dispute over Solfart’s financial transparency and the team’s treatment, MZ walked away from his previous brand last November, leaving behind one final, cryptic Reddit post. Now, with the ducks flying high, it’s clear what the image meant. He has found a new home as the Marketing and Creative Head for Patos Meme Coin and a project leader.

For the first time, he’s addressing the rumors regarding Solfart and explaining why the move was necessary —and how Patos Meme Coin is a band of unrivaled Crypto Rock Stars.

MZ, let’s start with the basics. Why did you leave Solfar (SOLF) Token?

I was a co-creator of solfart but I wasn’t the owner. I never handled wallets and payments, etc, I just made sure the internet was littered with content and provided connections to all the major news outlets. I left because we had a $15k sale, and the money was mishandled. Neither the team under me nor I were compensated, while the owner squandered money. The writing on the wall was clear; he was not ‘cutting the cheese’.

But hey, I made that slogan and concept for him. Makes sense. If he doesn’t believe in the idea/concept, he has no reason to. He didn’t make the creative concepts nor share the belief

What do you think will happen to the Solfart token now, and what did you learn from the experience?

Hopefully, Fart McSatoshi learns and keeps moving forward. I wish no negatives on anyone and believe he can steer his own vision as he chooses.

I do see he’s still shilling the work I did back in November of 2025, however. I think investors should demand more. That’s it. He’s a brilliant developer. Every time I see people asking “what happened to Mark Zuckfart” or wanting my work back, I feel more inspired to continue creating with Patos.

What made you move on to Patos Meme Coin?

More control allows me to exercise greater budgetary restraint and have a firm handle on the project’s direction. To make sure there’s a fair opportunity for everyone.

My belief in building something that will spread wealth to those who invest will be honored by this project. I also believe in the developer & marketing team’s ideas. We have a crew of people from 4 countries who are absolute Rock Stars at their craft. The Beatles of the Crypto space!

Everyone shares one belief, structured around math fundamentals. Everyone works just as hard as I do, and results are showing already.

Ducks eat bread together. Ducks fly high together. “PATOS” is all that, but also a potential catalyst to Pump All Tokens on Solana by creating a FOMO for the SPL ecosystem.

Do you believe Patos Meme Coin is better than Solfart?

Undoubtedly. Our team has far more reach in the actual crypto industry. Look at what we’ve achieved in 2 months compared to Solfart.

Patos Meme Coin has more crypto exchange listings, we’re on Google News on a new site every few days, and our first round of presale is nearly sold out.And recently, we released the first dAPP with more to come. Patos.games is a play-to-earn GameFi hub launched to help anyone earn $PATOS while boosting trading volumes and, in turn, brand visibility. Speaking of after the presale, of course. If you go point for point, the facts are clear.

What makes you confident in Patos Meme Coin’s execution?

Experience. Connections. Power. Consistency. Scaling ability.

The 111 Crypto exchange idea wasn’t just to compete with my old ideas at Solfart. It’s because I, myself, and a teammate conducted an analysis of crypto exchanges’ effects on the market cap of previously listed tokens, on average; tokens on a similar scale to what Patos Meme Coin is destined to be, if not less.

That 111 Cex theory puts those averages together, and along with support from our rising “Patos Flock” following, should create an excess of momentum in the opening week, and our team, keyword ‘teamwork,’ can handle all aspects of what needs to be done to convert that momentum into a parabolic market cap increase. And 111 is a bit ‘over the top’ of where the actual math suggested, but we want to aim for Mars, not the Moon.

Parabolic increases in market cap turn into parabolic token price explosions. We even have connections with Pop Culture celebrities and influencers that will aid our growth at the right time. Our collective reach really separates us from any other presale currently live.

On PatosMemeCoin.com, it shows that the token presale’s first round is almost closed, with 9 remaining; 10 total. This means PATOS should have around 11 crypto exchange listings confirmed per round. Is this accurate?

Something like that. For instance, we expect to add 4, possibly 6, more crypto exchange listing confirmations to our resume before round 1 closes. That will boost our total CEX confirmations to 12 or 14. Our team likes to be ahead of the ball, ahead by as far as possible.

The doors are open to many people as they trust the team involved and me. The faster funding comes in, the faster listings will grow, and in compounding fashion, vs. speed.

But of course, the price of tokens goes up with each round, with the 10th-round price 47% higher than the first. The fastest duck gets the most bread.

You mentioned earlier that you have the GameFi dAP “Patos Games.” What other applications can investors expect?

We like to keep most things very much hush. As you can see from the Patos Games references, there was no mention of the actual project before it launched. There are too many energy & idea thieves in this industry, and I want to keep as many surprises for investors as possible.

Just know, we’re looking to make an impact in a way that will make Patos Meme Coin a meme coin with utility that’s used for years to come. That’s the goal.

Our team would much rather ‘show’ than talk. But at this point, we have more CEX support, a GameFi pixel game launched, and so much visibility. Changpeng Zhao, aka CZ, responded to us indirectly on X.

With just what we have now, a 50x increase in value from today’s token price is possible. comes, the faster listings will grow, and in compounding fashion vs speed increase.

Thank you for your time, Mark Zuckerfart. Wishes of great fortune and materialization of your vision for Patos Meme Coin.

Wishes aren’t needed. Just hard work If you’re ready to win, come join the Flock.The first round has 18% left, and we’re still in the 2nd month of this token presale. Check others’ ages to notice how fast we are moving by comparison.

We’re going to go even faster soon. Get your first bag holdings during the genesis round at PatosMemeCoin.com. And to all of those invested right now: Patos Fock, let’s fly Mother Quackin’ high.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

A crypto executive has pushed back against claims by the president of a community banking association that any compromise between the banking sector and the crypto industry on the CLARITY Act would be a mistake. Austin Campbell, founder of Zero Knowledge Consulting, argued in a Friday X post that success or failure won’t be dictated by the players who stand to lose the most. “If community banks and crypto can’t find a way to work together, we already know who the winners are. It’s not the community banks. It’s not consumers. It’s not the crypto industry,” Campbell said, framing a potential collaboration as a win for local economies over the entrenched interests of large lenders. He went on to stress that the real opportunity lies in using stablecoins to address persistent technology and regulatory gaps that have hindered community banks from embracing crypto-enabled solutions.

Key takeaways

- Austin Campbell argues that cooperation between community banks and crypto firms is essential to avoid a decisive win by large banks, implying a missed opportunity for local lenders and consumers if cooperation fails.

- The exchange centers on the CLARITY Act, with proponents of flexibility arguing concessions could bolster liquidity and economic activity in smaller markets, while opponents warn of deposit leakage and regulatory risk.

- Banking lobbyists contend that a broad adoption of stablecoins could siphon deposits from traditional banks, citing a Standard Chartered note that predicts a potential drop in deposits tied to growing stablecoin use.

- Political figures, including Eric Trump and Donald Trump, have weighed in on the debate, urging speed on related legislation and arguing that banks are throttling crypto policy to preserve profits.

- Policy discussions are playing out against a backdrop of ongoing regulatory scrutiny, growing acceptance of stablecoins as liquidity tools, and the broader question of how to regulate a rapidly evolving payments ecosystem.

Tickers mentioned:

Market context: The CLARITY Act debate sits at the intersection of regulatory clarity, stablecoin usage, and local lending dynamics, illustrating how policy choices may affect both consumer access to higher-yield options and the resilience of regional banks.

Sentiment: Neutral

Market context: The discussions frame liquidity and regulatory risk as central to crypto’s interaction with traditional finance, underscoring how policy signals could influence participation by smaller lenders and crypto firms alike.

What to watch next: 1) Movement on CLARITY Act amendments in Congress; 2) Public statements from community bank associations and their members; 3) Upticks in stablecoin adoption and related liquidity tooling; 4) Public commentary from major banks on crypto policy; 5) Regulatory updates on stablecoins and payments infrastructure.

Why it matters

The core of the debate centers on whether stablecoins and other crypto-enabled liquidity tools can be harnessed by community banks without eroding traditional deposit bases. Campbell’s argument positions community banks as potential beneficiaries if they partner with crypto firms to offer compliant, technology-enabled services. In his view, the real threat comes not from crypto or consumers, but from capital and lobbying power concentrated among the largest banks, which he says have incented competing factions to undermine collaboration. The framing challenges the assumption that regulatory concessions are inherently risky for local lenders and instead suggests they could unlock new channels for funding and lending in smaller markets.

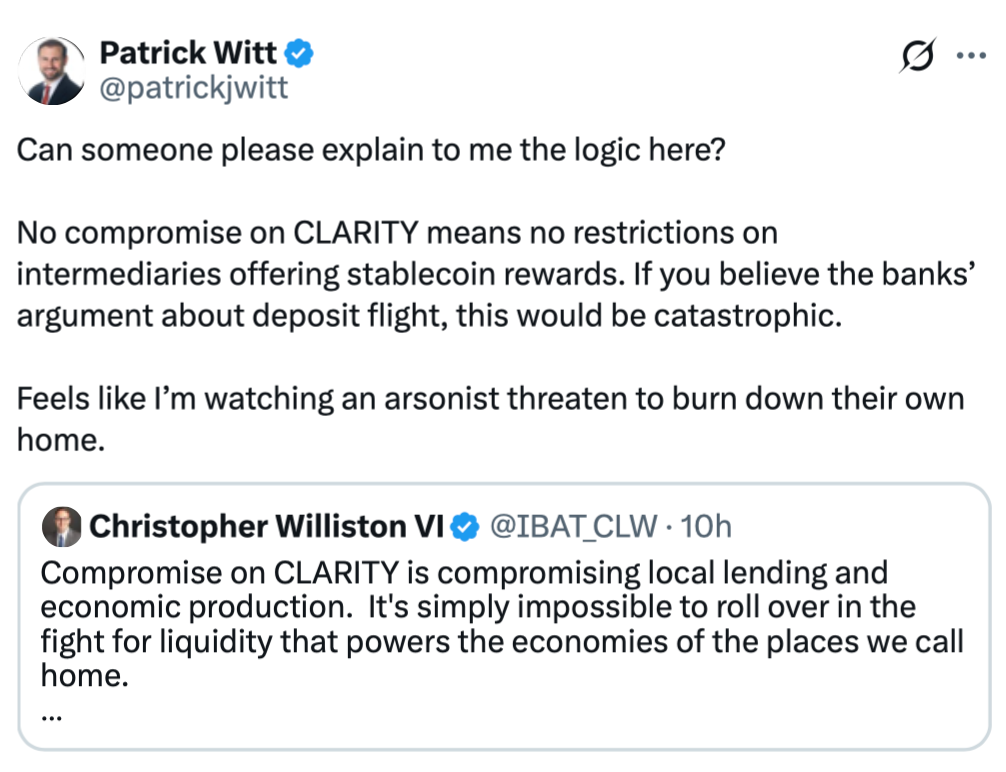

On the other side, Christopher Williston, president of the Independent Bankers Association of Texas, has warned that concessions in the CLARITY Act could undermine local lending by shifting liquidity away from traditional banks. Williston argues that “it’s simply impossible to roll over in the fight for liquidity that powers the economies of the places we call home.” The argument underscores a broader fear among lenders that stablecoins, if not properly regulated, might draw away customer funds or complicate reserve management. The debate has drawn in perspectives from the broader banking lobby, with Standard Chartered’s note highlighting potential deposit declines as stablecoin adoption grows, a claim that adds material weight to calls for thoughtful design and robust safeguards in any proposed framework.

The policy dialogue has also intersected with political commentary this week. Eric Trump criticized large banks on X for allegedly blocking Americans from earning higher yields on savings, while Donald Trump pressed for swift action on a Market Structure bill and argued that banks should not obstruct crypto policy. The political dimension adds urgency to lawmakers’ considerations about how to balance investor protection, financial stability, and innovation in a rapidly evolving payments landscape. A broader conversation about the regulatory underpinnings of stablecoins—how they are issued, backed, and used for on-ramps and off-ramps—remains central to building a framework that protects consumers while supporting responsible innovation.

In the background, the debate unfolds as policymakers weigh how to integrate stablecoins into a compliant, secure financial system. The tension between liquidity needs in local economies and the banks’ concerns about deposits and reserve adequacy illustrates the complexity of crafting policy that does not stifle competition or slow the adoption of technology that could enhance efficiency and inclusion. With the CLARITY Act and related market-structure discussions occupying congressional calendars, the path forward will likely hinge on how well negotiators can translate public policy into practical reforms that serve both communities and investors.

The discourse also mirrors a broader industry trend: the growing importance of stablecoins as tools for settlement, liquidity provisioning, and cross-border transactions. As more institutions explore regulated, compliant implementations, the emphasis remains on transparent, auditable designs that align incentives across participants—from small community banks to the largest money-center institutions. The YouTube discussion linked below captures a snapshot of these tensions, featuring perspectives from industry observers and policymakers as they navigate the trade-offs between innovation, risk, and stability. Video discussion

In parallel, the political discourse has featured statements from prominent figures, including Eric Trump and Donald Trump, urging lawmakers to move promptly on the crypto agenda. The narrative underscores a broader theme: the policy environment is actively shaping the strategic calculus of counterparty risk, liquidity provisioning, and the pace at which the crypto sector can integrate with traditional banking rails.

As the CLARITY Act debate continues, observers will be watching for how congress evaluates stability, consumer protection, and the risk of deposit outflows under different design choices. The tension between the desire for innovation and the need for prudent oversight remains at the heart of policy discussions, with industry voices insisting that collaboration between community banks and crypto firms could unlock benefits for local economies—if guided by clear, enforceable rules.

What to watch next

- Legislative updates on the CLARITY Act, including potential amendments that balance liquidity with deposit protection.

- Statements from independent bankers’ associations and regional banks on the proposed framework and liquidity impacts.

- Regulatory guidance on stablecoins, disclosures, and reserves that could influence adoption by smaller lenders.

- Public commentary from influential industry figures and lawmakers ahead of key votes or hearings.

- Verification of deposit-flow projections tied to stablecoin use and cross-border settlement experiments.

Sources & verification

- Independent Bankers Association of Texas president Christopher Williston’s remarks on X: https://x.com/IBAT_CLW/status/2029950462649057749?s=20

- Patrick Witt’s commentary related to the discussion: https://x.com/patrickjwitt/status/2030102472417489373?s=20

- Standard Chartered note on stablecoins and deposits: https://cointelegraph.com/news/stablecoins-real-threat-us-bank-deposits-says-standard-chartered

- Eric Trump’s X post on banks and yields: https://x.com/EricTrump/status/2029309823423009211

- Trump’s call for Market Structure action and related coverage: https://cointelegraph.com/news/trump-takes-swipe-banks-over-stalled-crypto-bill

- YouTube video discussion: https://www.youtube.com/watch?v=ry9MI57Pbjs

- Independent context on the CLARITY Act and liquidity debates (general references within the reporting):

Community banks, crypto, and the CLARITY Act: the policy battle shaping liquidity

The CLARITY Act debate places community banks at the center of a larger question about how crypto-enabled liquidity should integrate with traditional financial rails. Austin Campbell’s critique centers on the idea that the most durable gains for local economies will come from partnerships rather than adversarial standoffs. He emphasizes that stablecoins—when designed with robust risk controls—could bridge operational and regulatory gaps that have long hindered community banks from accessing the efficiencies and speed of digital payment rails. In this framing, cooperation between smaller lenders and crypto companies becomes a pragmatic path to improving service offerings and expanding financial inclusion, rather than a theoretical contest over who controls the new payments paradigm.

However, the opposing view, as articulated by Williston and other banking lobbyists, highlights a legitimate concern: if policy is perceived as too lenient, the safety and soundness of traditional deposits could be compromised. Their argument rests on the premise that deposits are a fragile resource that must be safeguarded, especially in times of rising interest rates and macro uncertainty. The Standard Chartered projection, cited in coverage of the debate, adds a quantitative dimension to this concern by warning that widespread stablecoin adoption could translate into meaningful deposit declines for US banks. Such projections reinforce calls for careful governance, reserve standards, and transparency to ensure any crypto-enabled framework strengthens, rather than destabilizes, the banking system.

The political dimension adds urgency to the policy conversation. With voices from the White House and Congress weighing in—alongside public commentary from figures like Eric Trump and Donald Trump—the push to finalize a coherent market-structure and payments framework grows stronger. The discourse suggests that supporters see an opportunity to advance crypto policy in a way that complements innovation while addressing consumer protection and financial stability concerns. As policymakers examine potential concessions, the role of community banks could hinge on the availability of regulatory guardrails that enable responsible experimentation without undermining essential lending activities in local communities.

In sum, the current moment captures a critical crossroads for the crypto ecosystem and traditional finance. The CLARITY Act, the stability and resilience of local banks, and the pace of crypto-enabled liquidity tools will collectively shape how the sector evolves over the next 12 to 24 months. Stakeholders on both sides are advocating for a design that preserves consumer choice and market competition while ensuring that reserve management, disclosure, and oversight keep pace with the speed of innovation. As noted, the path forward will depend on concrete policy language, precise regulatory expectations, and the willingness of varied actors to collaborate in service of broader economic vitality rather than narrow interests.

A crypto executive has pushed back against claims by the president of a community banking association that any compromise between the banking sector and the crypto industry on the US CLARITY Act would be a mistake.

“If community banks and crypto can’t find a way to work together, we already know who the winners are. It’s not the community banks. It’s not consumers. It’s not the crypto industry,” Zero Knowledge Consulting founder Austin Campbell said in an X post on Friday.

“It is the big banks,” Campbell said.

“There is a very straight line between the value community banks bring,” he said, explaining that they face technological and regulatory issues that can be solved by stablecoins.

The major banks “have tricked both sides”

“These are not enemies,” Campbell said of stablecoin-yield providers and community banks, adding that “they are allies.”

“The big banks and the bank lobbies they fund have tricked both sides into fighting each other so that the ultimate winner is Jamie Dimon’s bonus,” he said.

Campbell’s comments came in response to Independent Bankers Association of Texas president Christopher Williston, who said that making concessions in the CLARITY Act debate would risk harming local lending and economic production.

“It’s simply impossible to roll over in the fight for liquidity that powers the economies of the places we call home,” he said.

Banking lobby groups have argued that if the CLARITY Act passes in its current form, stablecoins could siphon deposits from the banking system. Major US bank Standard Chartered recently estimated in a research note that increasing stablecoin adoption could lead to US bank deposits decreasing “by one-third of stablecoin market cap.”

The debate has also drawn comments from the Trump family this week.

Eric Trump, the son of US President Donald Trump, said in a X post on Thursday that large banks are not acting in the best interests of US citizens. “Big Banks (think JPMorgan Chase, Bank of America, Wells Fargo, etc.) are lobbying overtime to block Americans from getting higher yields on their savings.”

Donald Trump urges the bill to pass “ASAP”

US President Donald Trump also criticized banks for stalling the Senate’s crypto market-structure bill amid ongoing disagreements over stablecoin yield payments.

Related: Revolut makes second attempt at US bank charter, names new CEO for US business

“The U.S. needs to get Market Structure done, ASAP,” Trump said. “The Banks are hitting record profits, and we are not going to allow them to undermine our powerful Crypto Agenda,” he added.

Magazine: The debate over Bitcoin’s four-year cycle is over: Benjamin Cowen

F1 2026 Australia GP live: Qualifying result, lap times and schedule

Form 4 Century Aluminum Company For: 7 March

BTC slips below $68,000 as dollar posts steepest weekly gain

-

Politics4 days ago

Politics4 days agoAlan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

-

Tech6 days ago

Tech6 days agoUnihertz’s Titan 2 Elite Arrives Just as Physical Keyboards Refuse to Fade Away

-

Business15 hours ago

Form 8K Entergy Mississippi LLC For: 6 March

-

NewsBeat6 days ago

NewsBeat6 days agoAbusive parents will now be treated like sex offenders and placed on a ‘child cruelty register’ | News UK

-

Fashion12 hours ago

Fashion12 hours agoWeekend Open Thread: Ann Taylor

-

NewsBeat7 days ago

NewsBeat7 days agoDubai flights cancelled as Brit told airspace closed ’10 minutes after boarding’

-

NewsBeat7 days ago

NewsBeat7 days agoThe empty pub on busy Cambridge road that has been boarded up for years

-

NewsBeat6 days ago

NewsBeat6 days ago‘Significant’ damage to boarded-up Horden house after fire

-

Tech2 days ago

Tech2 days agoBitwarden adds support for passkey login on Windows 11

-

Entertainment5 days ago

Entertainment5 days agoBaby Gear Guide: Strollers, Car Seats

-

Sports2 days ago

Sports2 days ago499 runs and 34 sixes later, India beat England to enter T20 World Cup final | Cricket News

-

NewsBeat6 days ago

NewsBeat6 days agoEmirates confirms when flights will resume amid Dubai airport chaos

-

Politics6 days ago

FIFA hypocrisy after Israel murder over 400 Palestinian footballers

-

NewsBeat5 days ago

NewsBeat5 days agoIs it acceptable to comment on the appearance of strangers in public? Readers discuss

-

Tech6 days ago

Tech6 days agoViral ad shows aged Musk, Altman, and Bezos using jobless humans to power AI

-

Video5 days ago

Video5 days agoHow to Build Finance Dashboards With AI in Minutes

-

Fashion6 days ago

Fashion6 days agoOn the Scene at the 57th Annual NAACP Image Awards: Teyana Taylor in Black Ashi Studio, Colman Domingo in Yellow Sergio Hudson, Chloe Bailey in Christian Siriano, and More!

-

Business3 days ago

Business3 days agoGuthrie Disappearance Enters Fifth Week as Family Visits Memorial

-

NewsBeat5 days ago

NewsBeat5 days agoUkraine-Russia war latest: Belgium releases video showing forces boarding Russian shadow fleet oil tanker

-

Crypto World6 days ago

Crypto World6 days agoUS Judge Lets Binance Unregistered Token Class Action Proceed