Business

American Airlines raises checked bag fees, trims economy perks amid soaring fuel prices

Julian Lin is a financial analyst. He finds undervalued companies with secular growth that appreciate over time. His approach is to look for companies with strong balance sheets and management teams in sectors with long growth runways.

Julian is the leader of the investing group Best Of Breed Growth Stocks where he only shares positions in stocks which have a large probability of delivering large alpha relative to the S&P 500. He also combines growth-oriented principles with strict valuation hurdles to add an additional layer to the conventional margin of safety. Features include: exclusive access to Julian’s highest conviction picks, full stock research reports, real-time trade alerts, macro market analysis, individual industry reports, a filtered watchlist, and community chat with access to Julian 24/7. Learn more.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of TTD, META either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

The BSE Focused IT is a sector index that measures the performance of the 14 companies belonging to the Information Technology sector that are also BSE 500 firms.

The index constituents are Coforge, Cyient, HCL Technologies, Infosys, KPIT Technologies, LTIMindtree, Mphasis, Oracle Financial Services Software, Persistent Systems, Tata Consultancy Services (TCS), Tata Elxsi, Tata Technologies, Tech Mahindra and Wipro.

BSE Focused IT index was launched on October 7, 2024. The index has delivered negative 24% returns between January and March.

BSE shares ended 3% up on the NSE today at Rs 3,260 despite weak markets. Nifty plunged 222.25 points or 0.93% to finish at 23,775.10. Meanwhile, Sensex declined 947.22 points or 1.22% to settle at 76,615.68.

The stock also hit a fresh 52-week high of Rs 3,285.70. The capital market stock has seen a stellar run on the D-Street, delivering 76% returns in the past year. These returns came at a time when Indian markets faced multiple headwinds including rich valuations leading to FII outflows, tariff issues, a falling rupee and weak earnings. The latest setback for global markets including India has been the Iran-Israel war.

BSE shares are currently trading above their 50-day and 200-day simple moving averages (SMAs) of Rs 2,851 and Rs 2,609, respectively.The multibagger counter has delivered 2,070% returns in the past three years.

(Disclaimer: The recommendations, suggestions, views, and opinions given by the experts are their own. These do not represent the views of The Economic Times.)

Kia plans to release a pickup truck for American consumers in the coming years, as the South Korean automaker plots continued growth domestically and globally.

The company said Thursday it will add a pickup truck that includes hybrid variants by 2030 as a major expansion of its brand into the highly lucrative U.S. market. At least one hybrid variant is expected to be produced in the U.S., according to a presentation from Kia’s CEO investor day.

Detroit automakers General Motors, Ford Motor and Chrysler parent Stellantis dominate U.S. full-size pickup truck sales, however Kia reportedly plans to have its pickup be a smaller, midsize model.

That would position the vehicle against the industry-leading Toyota Tacoma as well as the Ford Ranger and GM’s Chevrolet Colorado and GMC Canyon, among other entrants.

“Accounting for approximately 20% of total demand, the U.S. pickup market represents a key strategic segment. Given its strategic importance, Kia will launch a new Body-on-Frame pickup model to broaden our customer base,” Kia CEO Ho Sung Song said, according to the presentation.

Kia expects to sell 90,000 pickups a year in North America and claim 7% of the midsize pickup segment by 2034, according to Automotive News.

Kia last year entered the global pickup truck market with a vehicle called Tasman. It’s not immediately clear whether the company would use that name or any parts from it for the planned “U.S.-specific” pickup truck or how much its U.S. vehicle would cost.

Kia did not immediately respond for request for comment about the sales targets or whether all variants of the planned pickup would be produced in the U.S.

Its pickup truck plans were announced during the automaker’s 2026 CEO investor day, where it also said it’s anticipating growing annual U.S. sales to 1.02 million vehicles and reaching 6.2% market by 2030. That compares with sales of more than 850,000 units last year and a roughly 5% market share.

Kia CEO Ho Sung Song on April 9, 2026 during the company’s CEO Investor Day in South Korea.

Courtesy Kia

The U.S. is key to Kia’s growth globally. The company said its global sales jumped from less than 2.8 million vehicles in 2021 to 3.14 million last year. Kia on its own is the world’s eighth-largest automaker, but ranks third when combined with its parent company, Hyundai Motor.

Kia said Thursday it’s targeting global sales of 4.13 million units and a 4.5% market share by 2030. That would be up from expectations of 3.35 million units in global sales this year and a 3.8% market share.

The company also announced plans to continue releasing new all-electric vehicles as well as a major push into hybrid and electric extended-range vehicles, or EREVs, including the planned pickup truck for the U.S.

Monthly grocery spend would rise 32% with full adherence, Numerator finds.

Luggage is prepared for an American Airlines flight at O’Hare International Airport in Chicago, Illinois.

Scott Olson | Getty Images News | Getty Images

American Airlines joined other airlines in raising its bag fees Thursday, but the luggage will be even more expensive for customers who buy basic economy tickets.

United Airlines, JetBlue Airways, Delta Air Lines and Southwest Airlines have all hiked the fee to check a bag in the past two weeks as the industry grapples with a jump in jet fuel expenses from the war in the Middle East.

American is raising the cost more for its no-frills option, while the other airlines had across-the-board increases.

The airline will hike the fee by $10 to check a first piece of luggage at the airport on domestic or short-haul international flights starting with tickets booked Thursday. That brings the price for one bag to $50, and a second bag will cost $60 for most tickets. There’s a $5 discount for checking a bag on American’s website or app, making the prices $45 and $55, respectively.

Customers with a basic economy ticket, meanwhile, will have to pay $55 for their first checked bag and $65 for a second bag starting with tickets purchased on May 18. The $5 online discount also applies to those fees, bringing the prices to $50 and $60, respectively, for those who pay in advance.

All customers in basic economy, even those with status, will also have to pay to pick a seat starting on May 18 and will not be eligible for complimentary and system-wide upgrades.

Airline executives have said travel demand is still high, but it’s not clear that carriers will be able to cover the entirety of the fuel price run-up. The effective closure of the Strait of Hormuz is choking off supplies of both crude and refined products like jet fuel, further driving up the price.

Jet fuel is airlines’ second-biggest cost, coming after labor.

Meanwhile, airlines have been leaning into premium offerings and making their basic fares more restrictive as the growth from higher-end options outpaces sales from regular economy. American has fallen behind large rivals Delta and United in seeking out luxury customers, profit and more.

Mane, Arzeda bringing together technologies to scale ViaLeaf Reb M.

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead. We’re sorry we can’t reply to individuals’ comments.Content disclaimer: The information in the publication is not an investment recommendation and it is not investment, legal or tax advice or an offer or solicitation to purchase or sell any financial instrument.This publication has been prepared by ING solely for information purposes without regard to any particular user’s investment objectives, financial situation, or means. For our full disclaimer please click here.

Nick Ackerman is a former financial advisor using his experience to provide coverage on closed-end funds and exchange-traded funds. Nick has previously held Series 7 and Series 66 licenses and has been investing personally for over 14 years.He contributes to the investing group CEF/ETF Income Laboratory along with leader Stanford Chemist, and Juan de la Hoz and Dividend Seeker. They help members benefit from income and arbitrage strategies in CEFs and ETFs by providing expert-level research. The service includes: managed portfolios targeting safe 8%+ yields, actionable income and arbitrage recommendations, in-depth analysis of CEFs and ETFs, and a friendly community of over a thousand members looking for the best income ideas. These are geared towards both active and passive investors. The vast majority of their holdings are also monthly-payers, which is great for faster compounding as well as smoothing income streams. Learn More.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BOE, GOOGL either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Business

Intel Stock Surges Past $60 as Analyst Upgrade, Terafab Partnership and Foundry Momentum Fuel Turnaround Hopes

SANTA CLARA, Calif. — Intel Corp. shares climbed more than 2.5% Thursday, breaking above $60 for the first time in years, as renewed optimism around the chipmaker’s foundry business, a high-profile partnership with Elon Musk’s Terafab project and a fresh analyst upgrade lifted sentiment amid a broader technology sector rebound.

The stock rose as high as $61.08 during the session before settling near $60.44 midday, up $1.49 or 2.54% on strong volume exceeding 60 million shares. That extended a sharp rally that saw Intel gain more than 11% on Wednesday alone and push the shares to a new 52-week high, marking one of the strongest runs in recent memory for the longtime semiconductor giant.

Intel, once the undisputed leader in PC and server processors, has spent years battling manufacturing delays, lost market share to rivals like AMD and Nvidia, and heavy losses in its foundry operations. Under CEO Lip-Bu Tan, who took the helm in early 2025, the company has pursued an aggressive turnaround focused on cost discipline, workforce reductions, improved process technology execution and external foundry customers.

Recent catalysts have accelerated the narrative. On April 7-8, Intel announced it would join Elon Musk’s ambitious Terafab initiative alongside Tesla, SpaceX and xAI to help manufacture advanced AI chips, a move that signaled potential high-volume demand for Intel’s 18A and future process nodes. The partnership sent shares surging as investors bet on renewed relevance in the AI infrastructure race.

Analysts also turned more constructive. Wells Fargo raised its price target on Intel from $45 to $55 while maintaining an Equal Weight rating, citing improved financial flexibility and progress on key nodes. The upgrade helped propel the stock to intraday highs near $59.17 on Wednesday before Thursday’s continuation.

The company’s balance sheet has strengthened noticeably. In early April, Intel agreed to repurchase Apollo Global Management’s 49% stake in its Fab 34 joint venture in Ireland for $14.2 billion, regaining full control over a critical advanced manufacturing facility. The move, financed in part by a healthier cash position, underscored management’s confidence in its long-term manufacturing strategy after years of joint-venture reliance.

Intel’s foundry business remains the centerpiece of the recovery story. The company reported a backlog exceeding $15 billion and is in advanced discussions with hyperscalers including Google and Amazon for advanced packaging services on custom AI chips. CFO Dave Zinsner has highlighted the potential for billion-dollar annual revenue streams from packaging alone, which could deliver attractive 40% gross margins and serve as an earlier bridge to profitability than traditional wafer fabrication.

The Intel 18A process node — a critical bet for regaining process leadership — has shown monthly yield improvements of 7-8% in recent quarters. First 18A shipments occurred in late 2025, with high-volume production targeted for later in 2026. Microsoft and AWS are confirmed customers for custom AI silicon on 18A, providing anchor validation even as the company eyes broader external wins.

Yet challenges persist. Intel’s first-quarter 2026 guidance, issued in January, called for revenue of $11.7 billion to $12.7 billion with breakeven adjusted earnings per share and gross margins around 32-34%, reflecting ongoing supply constraints and the heavy cost of ramping new nodes. Q1 2026 results are scheduled for release April 23, with analysts watching closely for updates on yield progress, supply availability from Q2 onward and any commentary on 14A customer pipeline development.

Data Center and AI (DCAI) revenue showed sequential acceleration in late 2025, growing 15% quarter-over-quarter — the fastest in a decade for that segment. Custom AI ASIC business crossed a $1 billion annualized run rate, though it still represents a small fraction of the overall $100 billion-plus addressable market for such silicon.

The PC client group continues to face headwinds from a maturing market and competition, but Intel is positioning its Lunar Lake and Panther Lake platforms for AI PC leadership, aiming to capture a majority share of next-generation Copilot+ PCs.

Financially, Intel has made progress. Full-year 2025 operating cash flow reached $9.7 billion, and the company expects positive adjusted free cash flow in 2026 despite continued heavy capital spending. Workforce reductions of roughly 30% and disciplined capex have helped stabilize the balance sheet, with cash reserves bolstered by strategic investments and divestitures.

Wall Street’s view remains mixed. Consensus ratings hover around Hold, with average price targets in the mid-$40s to low $50s, though bullish voices see potential for $65 or higher if 18A execution succeeds and foundry external revenue materializes. The stock trades at an elevated forward multiple, reflecting hopes for a multi-year recovery rather than near-term perfection.

Geopolitical tailwinds have also helped. U.S. government support for domestic semiconductor manufacturing, including CHIPS Act incentives, aligns with Intel’s “Made in America” push and has drawn positive attention from the White House. CEO Tan’s engagement with policymakers has reinforced Intel’s role in reducing reliance on overseas foundries.

Longer term, Intel aims to return to 40%+ gross margins as yields improve and higher-value products ramp. Success in advanced packaging, custom silicon for hyperscalers and potential 14A foundry wins could transform the company from a struggling IDM into a competitive player across design and manufacturing.

For investors, the recent surge reflects growing belief that the worst of the process technology crisis may be behind Intel and that Tan’s “time and resolve” approach is yielding tangible results. Thursday’s move lacked major new company-specific news but benefited from carryover momentum, technical breakout above key resistance levels and rotation into beaten-down tech names.

Intel’s market capitalization has climbed back toward $250 billion territory in recent trading, still well below its pandemic-era peaks but reflecting renewed respect for its manufacturing scale and U.S.-based capabilities.

As the April 23 earnings report approaches, focus will center on whether supply constraints are truly easing, any acceleration in foundry customer announcements and updated full-year guidance. Execution risks remain high — yields, competition from TSMC and Samsung, and macroeconomic pressures on capex spending could all influence the trajectory.

Yet for a company once written off as permanently behind in the AI era, the combination of Terafab exposure, regained fab control, packaging momentum and analyst support has reignited the turnaround narrative. Whether Intel can convert that optimism into sustained profitability and market share gains will define its path through the remainder of 2026 and beyond.

People gather at the Magic Kingdom theme park before the “Festival of Fantasy” parade at Walt Disney World in Orlando, Florida, U.S. July 30, 2022.

Octavio Jones | Reuters

Disney is planning to begin its next phase of cost cutting, which will include as many as 1,000 layoffs, according to a person familiar with the matter.

The cost-cutting initiative comes shortly after Josh D’Amaro took the helm as CEO in mid-March.

The layoffs are expected to mostly affect Disney’s marketing department, according to the person, who requested to speak anonymously because the moves had not yet been made public. That department was recently consolidated under Asad Ayaz, who was named chief marketing and brand officer in January.

Ayaz, who reports directly to D’Amaro and Dana Walden, Disney’s president and chief creative officer, oversees marketing for all of Disney’s divisions — entertainment, experiences and sports — in the newly created role. It’s the first time that Disney brought all of its units under one marketing chief.

Disney’s stock was slightly down in afternoon trading on Thursday. The layoffs were first reported by The Wall Street Journal.

The changes to the marketing department structure occurred in January, when Bob Iger was still CEO of the company. Disney announced shortly after that that D’Amaro would take take over the top job — a long-awaited decision for the company.

D’Amaro, who previously was chairman of Disney Experiences, succeeded Iger after a period of uncertainty for the media and theme park giant — which had included a succession race and recent reorganization and turnaround of the business.

Iger reclaimed the Disney CEO role in late 2022, about two years after his initial departure. He was immediately tasked with a turnaround of the business as its stock price had fallen and earnings began to miss expectations.

By February 2023, Disney had announced sweeping plans that reorganized the structure of the company, cut $5.5 billion in costs and eliminated 7,000 jobs from its workforce.

On D’Amaro’s first official day as CEO in March, he noted the work Iger had done to get the company past one of its most difficult periods.

“When Bob returned to the company a few years ago, his goal was to fortify our business and lay the groundwork for long-term growth, by reigniting creativity and improving performance at our studios, building a robust and profitable streaming business, transforming ESPN for a digital future, and turbocharging our parks and experiences,” D’Amaro said on stage at the company’s investor day.

“We’ve accomplished all of those things, and we’re operating from a place of strength, with ample opportunity for growth.”

Child dies from dog bite at property in North Yorkshire

The Trade Desk Is Now A Deep Value Stock (NASDAQ:TTD)

Binance’s CZ Offers OKX Founder $1 Billion Bet Over Divorce Dispute

-

Business7 days ago

Business7 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business6 days ago

Business6 days agoExpert Picks for Every Need

-

Sports5 days ago

Sports5 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech2 days ago

Tech2 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business4 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Fashion3 days ago

Fashion3 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Politics6 days ago

Wings Over Scotland | The quality of mercy

-

Fashion2 days ago

Fashion2 days agoLet’s Discuss: DEI in 2026

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Fashion7 days ago

Fashion7 days agoStatement Sunglasses: The Accessory Shaping Modern Fashion

-

Crypto World1 day ago

Crypto World1 day agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics7 days ago

Politics7 days agoEast Jerusalem Palestinian families eviction orders

-

Politics7 days ago

Politics7 days agoWhy so many children are now classified as ‘disabled’

-

Fashion7 days ago

Fashion7 days agoFor Love & Lemons’ Spring 2026 Line is for the Romantics

-

Politics7 days ago

Politics7 days agoNuclear rockets, moon bases and NASA’s Mars plan

-

Tech7 days ago

Tech7 days agoThe Threadless Ball Screw Never Took Off, But Don’t Write It Off

-

Business7 days ago

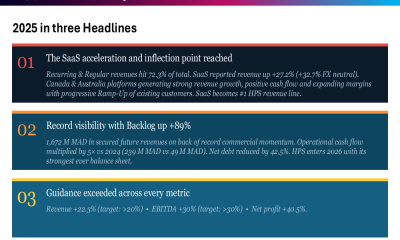

Business7 days agoHPS FY 2025 slides: SaaS inflection drives 22% revenue growth

-

Fashion6 days ago

Fashion6 days agoFrugal Friday’s Workwear Report: Hammered Metallic Button Sweater Vest

You must be logged in to post a comment Login