Business

Budget 2026: 7 high speed corridor plan lifts Jupiter Wagons, IRFC and other railway stocks up to 3%

The BSE and National Stock Exchange held a live trading session on Sunday to coincide with the presentation of the Union Budget 2026–27, drawing attention to railway linked counters, particularly technology and wagon manufacturing stocks. Quadrant Future Tek led the gains, rising 3%. Jupiter Wagons followed with a 1.87% increase. Railway PSUs IRFC and RITES also traded higher, gaining 1.20% and 1.19%, respectively, while RailTel was up 1.08% during the session.

During her Budget speech, Sitharaman announced plans to develop seven high speed rail corridors to act as key growth connectors between major cities, aimed at improving inter city connectivity, reducing travel time and supporting economic activity along key urban and industrial clusters.

The proposed corridors include Mumbai–Pune, Hyderabad–Pune, Hyderabad–Bengaluru, Chennai–Bengaluru, Delhi–Varanasi, Varanasi–Siliguri and others. The government also outlined the plan as part of efforts “to promote environmentally sustainable passenger travel” through high speed rail links connecting major cities.

Also Read | Gold ETFs crash 16% on stronger dollar, silver ETFs follow suit. What should investors do?

Market participants said the Budget’s emphasis on high speed corridors sharpened expectations of stronger order inflows across rolling stock, signalling, rail financing and project execution segments over the medium term.

The proposal announced by Finance Minister Nirmala Sitharaman to develop seven high speed rail corridors represents a structural push towards decongested, high capacity rail infrastructure, said Divyam Mour, Research Analyst, SAMCO Securities, adding that dedicated high speed corridors are likely to accelerate project execution, improve asset utilisation, and unlock large EPC order inflows across track laying, electrification, signalling and station development.”This is materially positive for railway infrastructure players such as Rail Vikas Nigam Limited and IRCON International Limited, while electrification and civil contractors like KEC International Limited, NCC Limited and Ashoka Buildcon Limited should see sustained order momentum. Financing support from Indian Railway Finance Corporation further strengthens funding visibility for long term rail expansion,” said Mour.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

Fox News chief national security correspondent Jennifer Griffin reports on the state of Strait of Hormuz traffic, Irans demand for a toll on passing ships and ceasefire negotiations on Varney & Co.

This story on the March 2026 CPI inflation report is developing and will be updated with further details.

Inflation surged in March as consumer prices jumped amid the economic disruptions caused by the Iran war’s impact on the energy market.

The Bureau of Labor Statistics on Friday said that the consumer price index (CPI) – a broad measure of how much everyday goods like gasoline, groceries and rent cost – rose 0.9% from a month ago and is 3.3% higher than last year. The annual figure jumped from last month’s 2.4% reading, while the monthly increase also rose markedly from last month’s 0.3% reading.

Expectations vs. reality

Both the 0.9% monthly increase and 3.3% annual rise were in line with the expectations of economists polled by LSEG.

So-called core prices, which exclude volatile measurements of gasoline and food to better assess price growth trends, were up 0.2% on a monthly basis and 2.6% from a year ago. Both of those figures were slightly cooler than economists’ predictions of 0.3% and 2.7%, respectively.

The core CPI figures were slightly hotter than February’s readings, which showed prices rose 0.2% on a monthly basis and 2.5% from the prior year.

Economists have noted that inflation data from December 2025 through April 2026 will be affected due to data collection interruptions resulting from last fall’s 43-day government shutdown.

During the shutdown, the BLS wasn’t able to gather data and used a carry-forward methodology to make up for the lack of an October CPI report and missing data in November’s report. Economists say this is likely to impart a downward bias on inflation data until this spring, when fresh data will negate the discrepancy.

The cost of living breakdown

High inflation has created severe financial pressures in recent years for most U.S. households, which are forced to pay more for everyday necessities like food and rent. Price hikes are particularly difficult for lower-income Americans, because they tend to spend more of their already-stretched paychecks on necessities and have less flexibility to save.

Food prices were flat on a monthly basis in March, and were up 2.7% from a year ago. The food at home index declined 0.2% for the month and is up 1.9% over the last year, while the food away from home index is 3.8% higher than a year ago after a 0.2% increase on a monthly basis.

Meats, poultry and fish prices were down 0.5% for the month but remain 5.6% higher than a year ago. Beef and veal prices fell 0.6% in March and are 12.1% higher than last year. Egg prices continued to decline following an avian flu outbreak that impacted supply, with prices down 3.4% for the month and 44.7% from a year ago. The fruits and vegetables index rose 1% in March and is up 4% on an annual basis.

Expert analysis

Texas-based company acquires Les Aliments Mejicano.

LyondellBasell: North America's Cost Advantage Is Just Getting Started

Thousands of small investors who piled into one of London’s best-known green investment vehicles are staring down the barrel of losses running well beyond 50 per cent, after the board of SDCL Efficiency Income Trust (SEIT) bowed to pressure from a New York activist and abandoned its rescue plan in favour of a managed wind-down.

The FTSE 250 trust, which has raised more than £1.1 billion from retail backers since its 2018 launch, confirmed today that it has shelved plans to convert itself into a conventional operating company and will instead begin selling off its portfolio of energy-efficiency assets.

SEIT becomes the latest London-listed trust to change course under the gaze of Saba Capital, the aggressive New York hedge fund run by Boaz Weinstein, which is understood to hold a stake of more than 10 per cent. Saba has built positions in dozens of British investment trusts over the past eighteen months, agitating for boards to be replaced and cash to be returned to shareholders.

For the army of private investors who subscribed to SEIT’s nine capital raisings between 2018 and 2022, the decision marks the bitter end of a story that once looked like a copper-bottomed route into the green transition. They were lured by an anticipated yield of 5 per cent or more at a time when base rates were on the floor, and placings were frequently several times oversubscribed. Their money went into projects ranging from rooftop solar arrays at Tesco supermarkets to electric-vehicle charging infrastructure and district heating schemes.

The trust’s fortunes reversed sharply once interest rates began their steep climb, and the market has grown increasingly sceptical about the values SEIT has placed on its unquoted holdings. The shares, which were issued at £1 or more, closed at 45p yesterday, a punishing 49 per cent discount to stated net asset value. If the portfolio is eventually liquidated anywhere close to recent market prices, the collective hit to shareholders could exceed £500 million.

Tony Roper, SEIT’s chairman, said the board had held intensive talks with wealth managers, retail platforms and other large holders, and that the feedback had been clear. Many had expressed what he described as “a clear preference for liquidity” over the proposed run-on plan. Saba is believed to have been among those consulted.

The directors, he said, had “unanimously concluded” that a managed wind-down of the portfolio was now in the best interests of shareholders taken as a whole. Roper acknowledged the pain felt by loyal backers, saying the board was “acutely aware of the reduction in share price in recent years” and recognised the frustration and uncertainty that had caused.

The alternative on the table had been to delist the investment trust wrapper, retain the stock market listing as an ordinary trading company and carry on running the assets. Roper conceded that, in theory, such a route “could have created value significantly in excess of the current share price”, but said it carried meaningful execution risk that shareholders were unwilling to stomach.

SDCL, the manager founded and led by energy-efficiency evangelist Jonathan Maxwell, has agreed to what the trust described as minimised termination fees, a nod to the sensitivity around what retail backers might otherwise regard as rewards for failure.

Analysts at Barclays said the activist presence on the shareholder register had made an orderly wind-down the more probable outcome all along. In their view, the shift “provides clearer line of sight to value realisation”, though they warned that the process would stretch out over an extended period and that disposal pricing remained a live risk.

There is already a cautionary data point. SEIT recently offloaded a batch of assets for £105 million, a 9 per cent discount to the value at which they had been carried in the books, a reminder that the private market for infrastructure assets remains sticky and that further haircuts are likely as the wind-down gathers pace.

The SEIT decision lands squarely within a broader assault by Saba on the £270 billion investment trust sector. Edinburgh Worldwide Investment Trust and Impax Environmental Markets are both midway through exit tender offers that their boards have argued are necessary to prevent ordinary shareholders being trapped in vehicles increasingly controlled by the American fund. Several other trusts have pre-emptively announced buybacks, continuation votes or strategic reviews in an attempt to keep Saba at bay.

For SME owners and retail savers who were encouraged to view specialist investment trusts as a low-drama way of backing the energy transition, the unravelling of SEIT is a sobering lesson. A yield that looks generous in a zero-rate world can evaporate quickly when gilts start paying 4 per cent, and unlisted infrastructure values that held up well on paper do not always survive contact with a real buyer. With Saba now a fixture on share registers from Leith Walk to Bishopsgate, more boards are likely to find themselves weighing whether to fight, fold or hand the cheque book back to investors.

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

A surge in prices at the pump due to the Iran war has pushed the inflation rate to 3.3%.

Business

Trump Furious Over NATO ‘Betrayal’ as He Weighs Pulling US Troops From Europe in Major Rift

WASHINGTON — President Donald Trump, seething over what he calls NATO allies’ failure to support U.S. efforts in the Iran conflict and stalled plans for Greenland, has discussed with advisers the possibility of withdrawing some American troops from Europe, a senior White House official said Thursday.

The deliberations, reported first by Reuters, mark the latest escalation in trans-Atlantic tensions that have pushed the 77-year-old military alliance into one of its rockiest periods. No final decision has been made, and the Pentagon has not been tasked with concrete planning, but the mere discussion signals Trump’s deepening frustration with European partners he accuses of freeloading on American security guarantees while offering little in return during critical moments.

Trump’s anger boiled over after a tense White House meeting Wednesday with NATO Secretary General Mark Rutte. In an all-caps Truth Social post afterward, the president declared: “NATO WASN’T THERE WHEN WE NEEDED THEM, AND THEY WON’T BE THERE IF WE NEED THEM AGAIN. REMEMBER GREENLAND, THAT BIG, POORLY RUN, PIECE OF ICE!!!” He followed up Thursday by calling the alliance “very disappointing” and saying its members only respond to pressure.

The troop withdrawal idea would serve as a targeted punishment short of the full U.S. exit from NATO that Trump has repeatedly floated — a move that would require congressional approval and faces legal hurdles. Instead, officials are eyeing a realignment: pulling forces from countries viewed as “unhelpful,” such as Germany and Spain, and shifting them toward more supportive eastern flank nations like Poland, Romania, Lithuania and Greece, according to reports citing administration sources.

The United States currently stations roughly 84,000 troops across Europe, with major bases in Germany playing a central logistical role for operations from the Middle East to Africa. Any significant drawdown would reshape America’s forward military posture on the continent and send shockwaves through European capitals already grappling with Russia’s ongoing threat and energy security concerns.

Roots of Trump’s Fury: Iran War and Hormuz

Trump’s latest grievances trace directly to the U.S.-Israeli military campaign against Iran that began in late February 2026. The conflict disrupted shipping through the Strait of Hormuz, a vital chokepoint for global oil and gas flows, sending energy prices soaring. European allies largely declined to commit naval forces to help reopen the waterway, a decision Trump branded as abandonment.

“They turned their backs on the American people,” White House press secretary Karoline Leavitt said ahead of the Rutte meeting. Trump has repeatedly labeled NATO a “paper tiger” and suggested in interviews that he is “absolutely” considering pulling the U.S. out of the alliance once the Iran situation stabilizes.

The Greenland issue adds another layer. Trump has long expressed interest in acquiring the Danish territory for strategic reasons, but progress has been nonexistent, further fueling his irritation with European partners.

A Strategy of Punishment Without Full Withdrawal

The troop repositioning plan, first detailed by The Wall Street Journal, stops short of a complete NATO exit but would still dramatically reduce Washington’s security commitments in western and central Europe. Countries with higher defense spending and quicker support during the Hormuz crisis could see increased U.S. presence, while others face base closures or force reductions.

Defense analysts note that such a move would test NATO’s Article 5 collective defense pledge in practice, even if not formally abandoned. Eastern European nations, already wary of Russian aggression, have generally met or exceeded the 2% of GDP defense spending target that Trump has long demanded. Western European powers like Germany have increased spending in recent years but remain below what the president considers adequate.

NATO officials and European leaders responded with a mix of calm and concern. Rutte described his meeting with Trump as “very frank” and “very open,” acknowledging disagreements without elaborating. Poland and other frontline states urged unity, while Germany reaffirmed its commitment to the alliance. British Prime Minister Keir Starmer suggested Europe may need to strengthen intra-continental defense ties.

Congressional barriers could complicate any large-scale withdrawal. The National Defense Authorization Act includes provisions aimed at preventing sharp reductions in U.S. forces in Europe below certain thresholds, reflecting bipartisan support for maintaining the trans-Atlantic link.

Historical Echoes and Strategic Stakes

Trump’s threats echo his first term, when he repeatedly criticized NATO spending and briefly considered troop cuts from Germany. This time, the context is more volatile: a recent U.S.-Iran conflict, disrupted global energy markets and a NATO already strained by Russia’s war in Ukraine.

European officials worry that any U.S. drawdown could embolden adversaries and force rapid, costly increases in their own defense budgets. Some have quietly begun contingency planning for greater European strategic autonomy, including joint procurement and enhanced EU defense initiatives.

For the Pentagon, repositioning tens of thousands of troops would involve enormous logistical challenges, base negotiations and potential strains on readiness. Supporters of Trump’s approach argue it finally forces Europe to shoulder more of the burden after decades of underinvestment.

Critics, including former national security officials, warn that signaling wavering U.S. commitment could weaken deterrence against Russia and China while damaging America’s global credibility.

What Comes Next

As of Friday, April 10, no orders for troop movements have been issued. White House officials emphasize that discussions remain internal and that Trump continues to use leverage to extract concessions on spending and burden-sharing.

Trump is expected to keep pressure on allies in coming weeks, potentially tying future U.S. support to concrete actions on defense budgets and Hormuz-related cooperation.

The episode underscores the fragile state of trans-Atlantic relations in 2026. While NATO has survived previous Trump-era turbulence, the combination of the Iran conflict fallout and longstanding spending disputes has exposed deep fault lines.

For now, the president’s anger serves as both venting and negotiating tactic. Whether it leads to actual force reductions — or simply compels European capitals to boost contributions — will shape the alliance’s future for years to come.

European leaders face a delicate balancing act: responding to Trump’s demands without appearing to capitulate, while preparing for a security landscape with potentially less reliable American backing.

As one senior European diplomat put it privately, “Pressure works with Trump, but permanent damage to trust could outlast any single administration.”

State-owned energy provider Synergy has launched an investigation into claims of a massive data breach allegedly involving over 900,000 sensitive document, including the personal records of customers.

Vista House, a private home in Westlake, Georgia, sponsored by Vista Global during the Masters.

Credit: VistaJet

A version of this article first appeared in CNBC’s Inside Wealth newsletter with Robert Frank, a weekly guide to the high-net-worth investor and consumer. Sign up to receive future editions, straight to your inbox.

Private jet companies are rolling out the red carpet for their top clients at the Masters Tournament, as competition shifts from the air to the ground with lavish hospitality events and experiences.

Thousands of private jets are expected to fly in and out of Augusta, Georgia, and nearby airports for the Masters in the coming days, making it one of the most important events of the year. NetJets, the industry leader, expects more than 775 flights into and out of Augusta, marking a 35% to 40% increase from last year, the company said. Flexjet is projecting about 350 to 400 flights, and Vista projects over 20 flights a day.

“Demand is off the charts,” said Mike Silvestro, CEO of Flexjet. “The Masters is like nothing else.”

On the private jet calendar, Davos, the Super Bowl, Cannes, the Kentucky Derby, the Monaco Grand Prix and Art Basel all attract plenty of private jets and wealthy attendees. But the Masters has a unique combination of tens of thousands of well-heeled attendees and a full week of events, creating a constant flow of clients flying in and out.

The swarm of Gulfstreams, Phenoms and Challengers is straining Augusta Regional Airport. Kenneth Hinkle, director of aviation services at the airport, said it had 3,294 flights last year and he expects an increase this year. The airport raised its “special event fee” this year by 25%, to between $150 and $4,000 per plane, depending on size, and expanded its jet parking area to accommodate 200 jets at a time.

The competition among private jet companies for landing slots, parking spaces and access to and from the terminal has grown so fierce that many companies have moved to nearby airports in Thomson, Georgia, or Aiken, South Carolina.

A photo rendering of NetJets’ new Augusta terminal.

Credit: Courtesy of NetJets

The real battle however, begins after the jets land. Jet companies are renting out mansions to create branded pop-up clubs, hiring Michelin-star chefs and well-known mixologists, hosting nightly parties with the biggest names in golf, and vying to attract the top players and announcers as headliners. Many are even staging private concerts with Grammy-winning country stars.

The spending is all part of a new race in the private jet business.

Private jet flights hit an all-time record in 2025, with 3.9 million departures, up 34% from pre-Covid levels. Recent U.S. government shutdowns and airport delays have only increased demand, jet companies say.

“We want to stay connected with our customers beyond just when they’re the air with us,” said Pat Gallagher, President of NetJets. “We’re a world lifestyle business. We’re a luxury business. If somebody asks me what business I’m in, I don’t say I’m in the travel or aviation space. I’m in the hospitality business.”

Longtime Masters fans say the hottest ticket of the week outside the Augusta National Golf Club is the NetJets Friday night party. NetJets won’t disclose any details on the location or entertainment for this year’s bash. But past parties have been hosted by sports commentator Jim Nantz and featured musical guests like Noah Kahan, Chris Stapleton and Zac Brown.

For the rest of the week, NetJets clients can use the brand’s hospitality venue to relax, grab a meal or drink, or hold a meeting. Some of NetJets’ more than 30 golf ambassadors who are playing at the Masters are also expected to pass through. Gallagher said the Masters is one of nearly 100 events a year now hosted by NetJets.

The company also just announced a new private jet terminal at Augusta Regional. The project, still under construction, includes 432,000 square feet of ramp space for jet parking.

“The number of jets that are parked on the [Augusta] runways, it’s like nothing you’ve ever seen from a from an aviation perspective,” Gallagher said.

Vista Global will be hosting clients at Vista House, a private home in Westlake, Georgia, that will be transformed into a branded hospitality venue in its signature silver and red. It will have nightly dinners, entertainment and special appearances by Vista brand ambassadors Gary Player, Jon Rahm, Phil Mickelson and Patrick Reed.

Vista hosted its big welcoming party Wednesday night with a private concert. The company said the goal is to give Vista House the same brand feel of its planes, from flight attendants serving in their Moncler-designed uniforms, to Vista’s signature scent designed by Le Labo to its ever-popular Vista beach towels. Clients of VistaJet and XO — both owned by Vista Global — will get access to Vista House as well hospitality space at the Double Eagle Club, close to the Augusta National Golf Club.

Vista said some of its clients fly in from as far away as Japan, South Korea, Singapore, India and Brazil.

“I think the Masters, especially in the past five years, has become more pronounced for us,” said Leona Qi, president of VistaJet U.S. “It’s a place where our clients — the ultra-high-net-worth individuals and corporate executives — go to not just to watch the game, but to really connect with each other and get deals done. And to share the passion and the experience with each other.”

Wheels Up will open the “Wheels Down Club” in Augusta, just a 10-minute walk from the entrance to Augusta National. The club, a temporary structure built around an existing home, will offer 11,000 square feet of hospitality space. Guests can valet their cars, get snacks and drinks in between rounds and check in their phones (a prized service since no cellphones are allowed on the course).

Wheels Up is running a “Wheels Down Club,” just a 10-minute walk from the entrance to Augusta National at the Masters.

Credit: Wheels Up

Wheels Up, now controlled by Delta Air Lines, expects to host 600 guests a day at the club. Big names on the program include Delta CEO Ed Bastian; Eric Kutcher, the North America chair of McKinsey & Co.; and Apple executive Eddy Cue, along with pro golfers. Chef José Andrés will host a “Jamon and Caviar” tasting and mixologist Tyler Zielinski will be making his signature “tiny cocktails.”

“The Masters has really become our tentpole event,” said Kristen Lauria, chief marketing officer for Wheels Up. “Whether it’s for members, whether it’s for prospects, or whether it’s for our partners who entertain their clients on the ground, it’s becoming bigger and bigger and bigger.”

Lauria said Wheels Down events will continue to expand into other sports, like tennis, equestrian and motorsports, as well as culinary and luxury lifestyle events. She said the clubs also help attract new clients who come in as guests of existing members.

“As I look at different ways to create demand, it’s really about going to where our customers are and where our members are,” she said. “Time is of the essence for our members. So showing up where they’re already going or where they’re planning to be, is a return in and of itself.”

Flexjet is taking a different approach. Rather than joining the spending spree of pop-up clubs and parties, the fractional jet company says it’s focused solely on its core business of getting clients to and from the event.

With Augusta Regional Airport highly congested during Masters week, Flexjet decided this year to move its operations to the Thomson-McDuffie Regional Airport in Thomson, Georgia. The airport is a short drive to the course at Augusta, is closer to the areas where attendees usually stay, and will allow Flexjet clients to get in and out quickly.

“The infrastructure in Augusta is taxed,” Silvestro said. “We’re trying to stay ahead of the curve and have the experience that we deliver to our customers be as seamless and stress-free as possible.”

Silvestro said clients will have an exclusive executive area at Thomson and can be picked up and dropped off right in front of their planes. He said the Masters has become so oversaturated with parties and events that Flexjet’s clients already have too many events to choose from.

“I shake my head at some of the hospitality extravagances from some of the people that are operating our space,” he said. “We see people doing certain things in and around our space that don’t make a lot of sense to us.”

Innovation will focus on premium, functional, multisensorial and personalization.

Form S-1/A Bitcoin Depot Inc For: 10 April

Nigel Farage unveils ‘Vote Reform. Get Starmer out’ slogan

March 2026 CPI: Inflation surged as Iran war took a toll on consumer prices

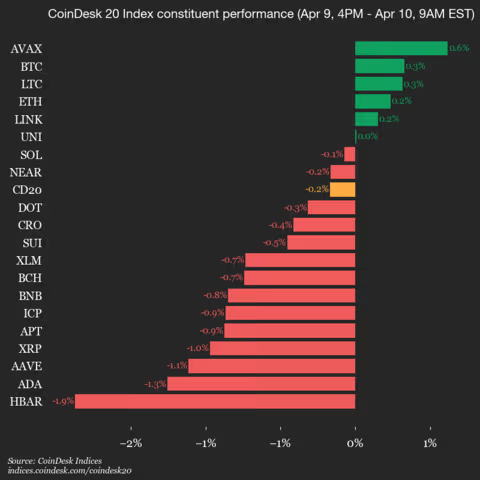

Hedera (HBAR) drops 1.9%, leading index lower

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Alan Cumming Brands Baftas Ceremony A ‘Triggering S**tshow’

Daily Market Coverage Apr. 8, 2026 9AM-11AM (ET) | Yahoo Finance

What is Finance? | Definition Financial Company|Financial Information| Accounts Video #financial

Psalm 23 Prayer for Financial Prosperity and Abundance #Psalm23 #DivineProtection #FaithInGod

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business5 days ago

Business5 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports6 days ago

Sports6 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business6 days ago

Business6 days agoExpert Picks for Every Need

-

Tech3 days ago

Tech3 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business5 days ago

Business5 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion4 days ago

Fashion4 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Fashion3 days ago

Fashion3 days agoLet’s Discuss: DEI in 2026

-

Crypto World2 days ago

Crypto World2 days agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Business6 days ago

Business6 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Crypto World1 day ago

Crypto World1 day agoCanary Capital Files SEC Registration for PEPE ETF

-

Politics6 days ago

Politics6 days agoThe UK should not pay a penny in slavery reparations

-

Tech4 days ago

Tech4 days agoSamsung just gave up on its own Messages app

-

Tech4 days ago

Tech4 days agoHaier is betting big that your next TV purchase will be one of these

-

Fashion7 days ago

Fashion7 days agoWeekly News Update, 4.3.26 – Corporette.com

-

Sports7 days ago

A Kevin O’Connell Theory Can Now Be Retired

-

NewsBeat7 days ago

NewsBeat7 days agoKemi Badenoch talks ‘spring cleaning’ Reform defections

-

Tech4 days ago

Tech4 days agoGamer Restores the Original PlayStation Portal From Two Decades Ago

-

Tech7 days ago

Tech7 days agoFlat tire? Dead battery? Speedy’s serves stranded Seattle riders as a quicker e-bike picker-upper

-

Tech4 days ago

Tech4 days agoThe Xiaomi 17 Ultra has some impressive add-ons that make snapping photos really fun

You must be logged in to post a comment Login