David Campbell Transport is taking Aurizon to court in an attempt to recoup some $8 million it says it’s owed over haulage at Glencore’s Murrin Murrin operations.

‘Varney & Co.’ host Stuart Varney comments on King Charles’ visit to the U.S. and the growing split between the U.S. and Europe during his ‘My Take.’

President Donald Trump announced Friday he was raising tariffs on European cars to 25%, citing the European Union’s noncompliance with the U.S.-EU trade deal.

“I am pleased to announce that, based on the fact the European Union is not complying with our fully agreed to Trade Deal, next week I will be increasing Tariffs charged to the European Union for Cars and Trucks coming into the United States. The Tariff will be increased to 25%,” Trump wrote in a Friday morning Truth Social post.

Advertisement

He did, however, indicate that he would drop the tariffs if European companies agreed to manufacture their cars in the U.S.

“It is fully understood and agreed that, if they produce Cars and Trucks in U.S.A. Plants, there will be NO TARIFF,” Trump also wrote.

President Donald Trump speaks to the press before departing the White House for Florida on May 1, 2026, in Washington, D.C. (Celal Gunes/Anadolu via Getty Images / Getty Images)

He reiterated the point while speaking to reporters at the White House on Friday.

“We raised the tariffs on cars coming in from the European Union because the European Union was not adhering to the trade deal we have. So based on that now, when they build their plants on which they’re spending over $100 billion for countries, not just the Union, but when those plants open, there won’t be any tariffs,” Trump told reporters.

Cars are loaded onto the car carrier ship Polaris Liberty at the automotive terminal on Aug. 11, 2025, in Bremerhaven, Germany. The U.S. will apply a 25 percent tariff to all European vehicles, U.S. President Donald Trump announced May 1, 2026. (Focke Strangmann/Getty Images / Getty Images)

He also touted ongoing U.S. manufacturing of car plants.

“We have right now in the United States over $100 billion of car plants being built. That’s a record. We’ve never had anything like it, from all countries, Japan, South Korea, every, by the way, Canada, Mexico, they’re all building plants in the United States. But the European Union was not adhering to the deal that we made,” Trump said.

Advertisement

President Donald Trump walks with Executive chair of Ford Motor Company Bill Ford Jr. and CEO of Ford Motor Company Jim Farley as they tour the Ford River Rouge Complex on Jan. 13, 2026, in Dearborn, Michigan. (Getty Images / Getty Images)

The U.S. and EU reached a landmark trade deal in July that saw the President agree to lower tariff rates on EU cars and trucks from its previous 27.5% to 15%.

By its most generic description, the 2x Bitcoin Strategy ETF (BITX) is a leveraged product that tries to give you twice the daily price action of Bitcoin (BTC-USD). Chasing the price of Bitcoin in a leveraged way for more than a day can lead to a complete loss of your investment, so that’s the first thing you need to know about this and other leveraged ETFs.

Inside BITX

Incepted by Volatility Shares on June 27, 2023, BITX is not a Bitcoin holder, so there’s no direct or indirect exposure as such. The exposure comes from futures contracts on Bitcoin. Using cash, treasuries, repo agreements, etc. for collateral, the fund buys monthly rolling contracts that are one and two months out, and these contracts are rolled over before expiration.

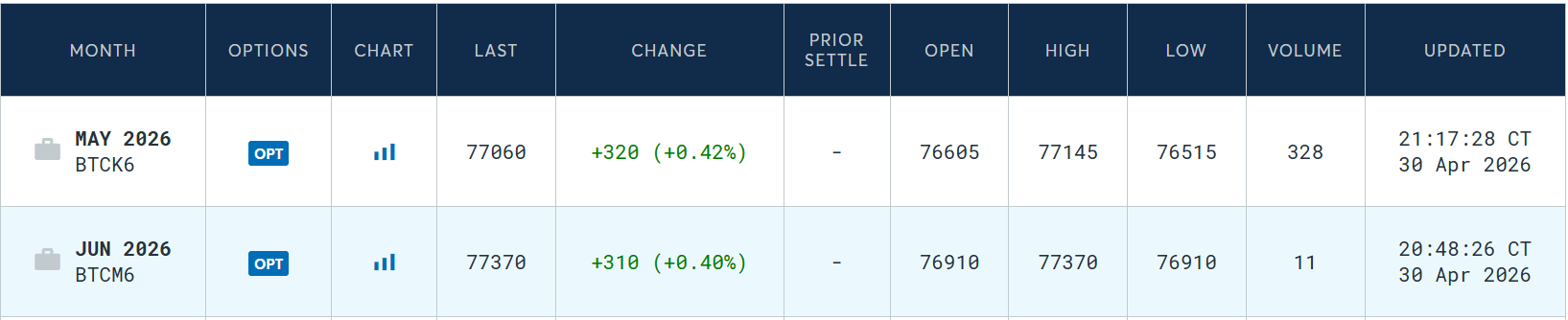

To illustrate this, this is what their annual report showed as of February 28, 2026.

Advertisement

BITX website

Since it’s now May at the time of writing, these contracts would have been rolled over to April and May, then May and June, and eventually to June and July futures later this month when July contracts are available. Let’s see how that’s going.

CME Group

What’s happening here is that the Bitcoin futures contract values show us where the market thinks the Bitcoin USD (BTC-USD) price will go over whatever period the contracts cover. When the market is bullish, longer-expiration contracts are more expensive, like in the screenshot above. Because of that, rolling over to the next month’s contracts is a net loss exercise for the ETF. The bet they’re making is that BTC prices will rise by the time they sell the older-month contracts so the net loss can be rolled over into a net gain position.

Advertisement

There’s a problem associated with this approach. Since the ETF is on the buy side of these contracts, these oscillations between net gain and net loss are amplified 2x and can lead to volatility drag. Here’s the example the fund gives in its prospectus.

…if Bitcoin futures were to rise 10% on day one, fall 5% on day two, and then rise 7% on day three, the expected leveraged performance of a fund like BITX over the three days would be = 1.2 * 0.9 * 1.14 = 1.23, or 23%, while the simple sum of the leveraged daily returns +20% – 10% +14% = 24%. This 1% lag is due to volatility drag.

That’s the cost long-term holders of BITX are paying on top of the 2.38% ER. Why would anyone do that? The answer is the potential upside during bitcoin bull cycles, because the ETF also does this.

…if Bitcoin futures were to rise 20% a day for three consecutive days, then BITX’s expected performance could be calculated as = 1.4 *1.4 * 1.4 = 2.74, or an impressive 174% increase over three days – a whopping 54% more than the simple sum of the three 40% returns (40% + 40% + 40% = 120%).

If you’re looking at this from a risk-reward angle, it looks like a no-brainer, but it’s not. Be careful here. This is just the gain/loss on the derivatives amplifying the movement of Bitcoin, and looking at just a couple of examples doesn’t give us the higher-level perspective.

The bigger risk that overshadows the derivatives risk is Bitcoin’s market value. As an extremely volatile and news-sensitive asset, even holding bitcoin alone can lead to sleepless nights. Imagine doubling that trouble, and what you get is BITX.

Advertisement

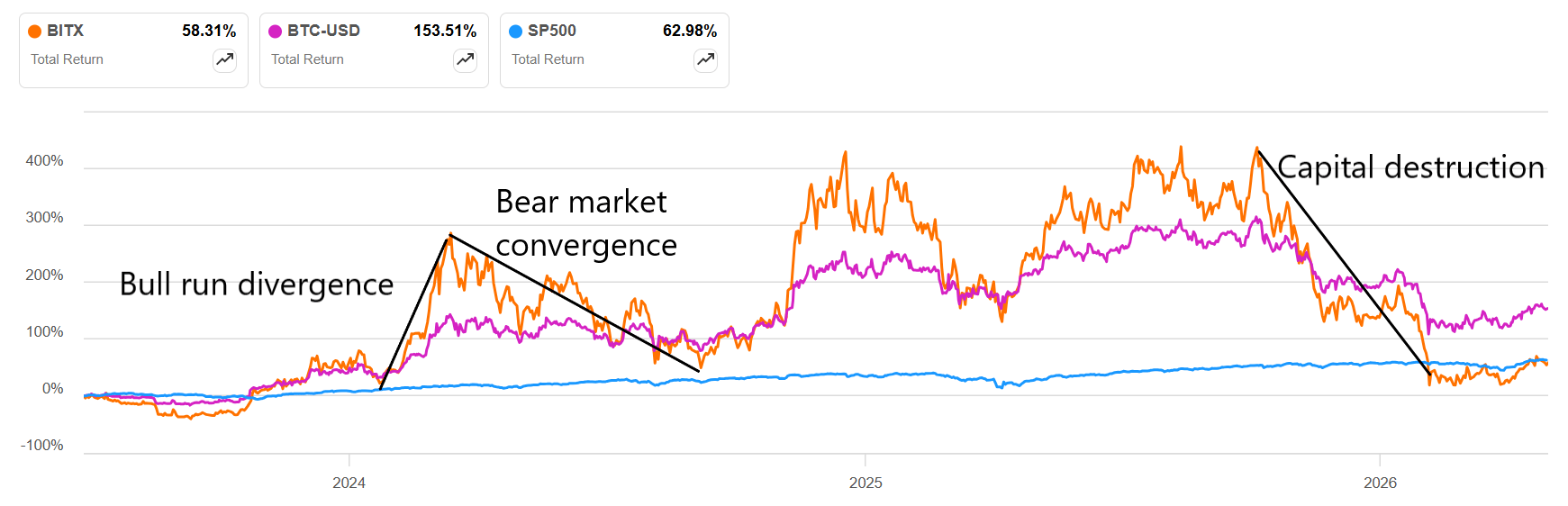

On the bright side, when bitcoin rallies, holding BITX can give you those tasty leveraged returns. For a moment, forget about the one-day-only warning of the ETF and imagine you held BITX from the time of inception until now.

SA

If you ignore the fact that BTC’s price movements since 2023 (June 27), when BITX was launched, make the S&P look like the kiddie ride in your neighborhood park, you’ll probably also see that BITX hasn’t given any hint of 2x leverage other than during the bull run divergences. Actually, the opposite is true—the divergence is caused by the leverage. This is where the real money is to be made if you’re looking at an investment horizon of longer than a day.

Then there’s the other side of the coin. I’m sure you haven’t missed the fact that your capital could be wiped out even more quickly. This isn’t an ETF where you accrue your wins and losses. It’s a daily reset. It’s aggressive. It’s potentially very rewarding, but it’s as risky as it is attractive.

Advertisement

Who Should Consider Using BITX?

I used the word “Using” and not “Holding” here on purpose, and the SEC warns investors about leveraged ETFs because of the volatility decay. That’s what you’re seeing in that screenshot two paragraphs ago. That entire period is volatility decay in action, and it should be obvious that the gains made during multiple and separate bull runs were almost zeroed out, leaving the investor with returns that were even less than the S&P500’s.

BITX can be handy for certain investors:

Price capture enthusiasts: Those who like participating in the price of Bitcoin during longer rallies periodically can be quite advantageous when coupled with leverage.

Those who opt out of Bitcoin (non-adopters) but want to benefit from its price action: investors who don’t want to hold Bitcoin but are keen on participating in rallies.

Portfolio diversifiers: those who need diversification and are willing to pay the risk premium but don’t really want to own any actual crypto assets.

If this looks interesting, you need to do your due diligence about your entry and exit points.

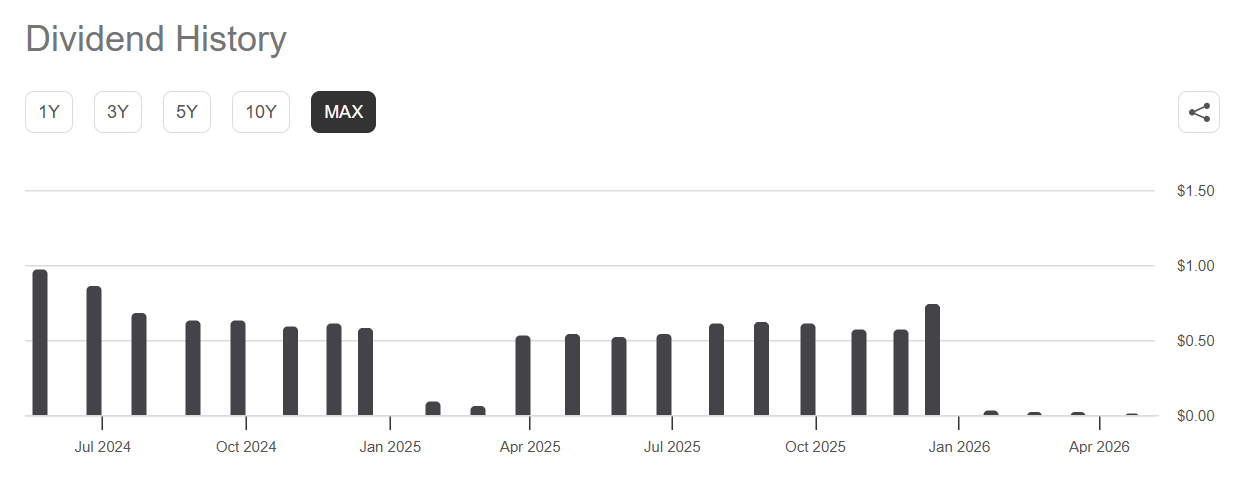

One last thing. Don’t be taken in by the sky-high distributions. Over the past three years, the ETF has paid out strong monthly dividends, but as of 2026, it’s run out of steam, and the monthly payout is now a paltry 1.5 cents a share.

SA

Advertisement

Unless you have a strong conviction that there’s another bitcoin rally on the horizon, it doesn’t look like you can depend on the high yield to resume anytime soon. That’s still not too bad if you think BTC is prepping for another bull run.

SA

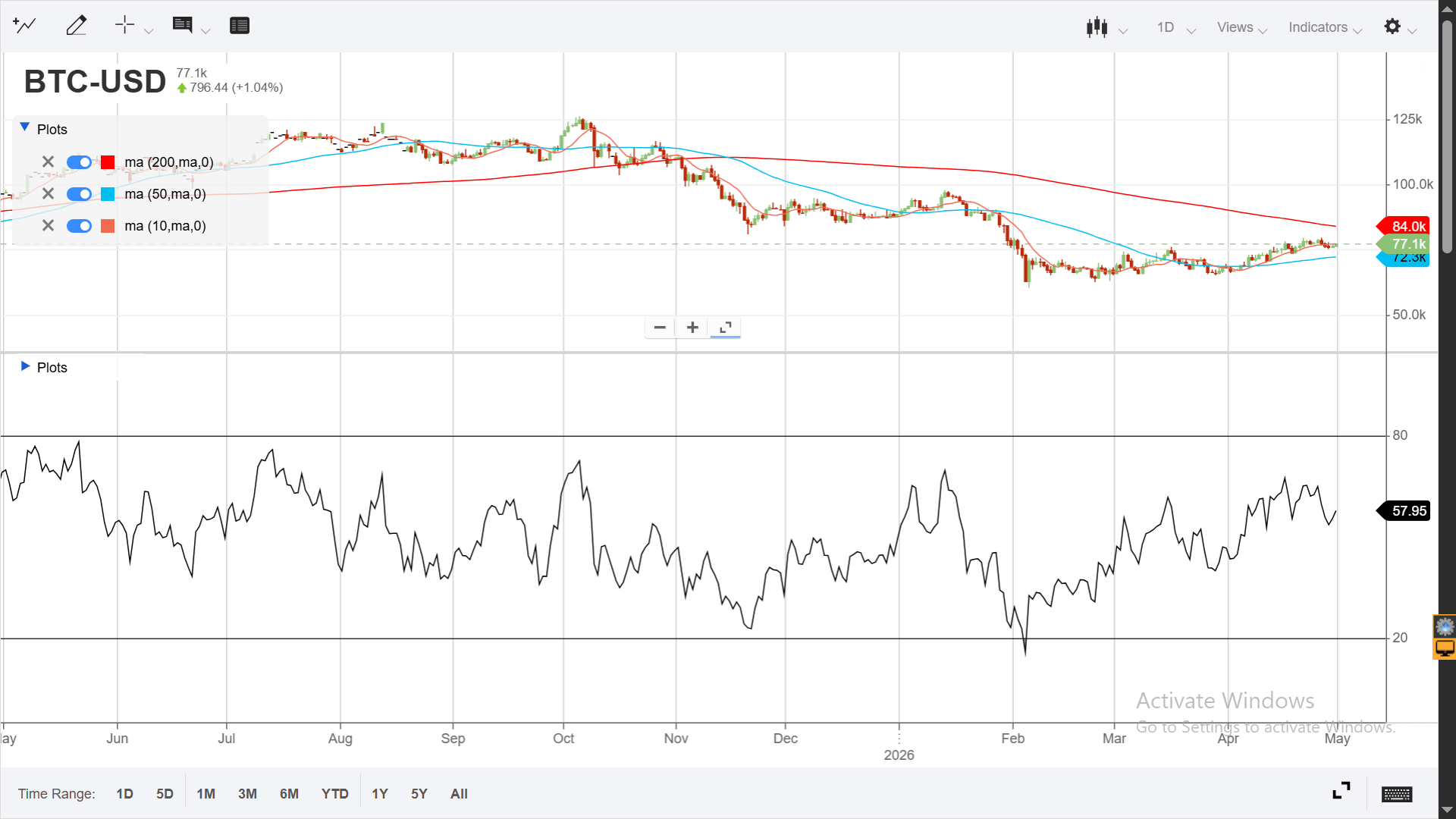

Using current context to illustrate potential use cases, the 10-day SMA has crossed over the 50-day SMA, but there’s still not enough momentum to force a turnaround in the 200-day SMA. It could go either way, and the RSI bears that out. There’s been an increase since the February low, but it’s been very cautious, hence the lack of momentum. It could have more room to run, but the best entry points for BITX are the ones where it bounces off 30 or under. Once it approaches 70, that’s a warning sign to sell.

As a final thought, I’d recommend thoroughly researching the leverage concept and how technical indicators can show you the best entry and exit points. From an academic perspective, I hope the article has given you at least some of what you came for. Thanks for reading!

Advertisement

This article answers three questions about BITX:

How does BITX reflect the price of Bitcoin?

What risks are involved in using BITX?

Which investors is BITX appropriate for?

Editor’s note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

Linde plc (LIN) Q1 2026 Earnings Call May 1, 2026 9:00 AM EDT

Company Participants

Juan Pelaez – Vice President of Investor Relations Matthew White – Executive VP & CFO

Advertisement

Conference Call Participants

Laurent Favre – BNP Paribas, Research Division Patrick Cunningham – Citigroup Inc., Research Division Vincent Andrews – Morgan Stanley, Research Division Patrick Fischer – Goldman Sachs Group, Inc., Research Division David Begleiter – Deutsche Bank AG, Research Division Joshua Spector – UBS Investment Bank, Research Division Matthew DeYoe – BofA Securities, Research Division Michael Sison – Wells Fargo Securities, LLC, Research Division Jeffrey Zekauskas – JPMorgan Chase & Co, Research Division John Ezekiel Roberts – Mizuho Securities USA LLC, Research Division Kevin McCarthy – Vertical Research Partners, LLC Laurence Alexander – Jefferies LLC, Research Division Arun Viswanathan – RBC Capital Markets, Research Division

Presentation

Advertisement

Operator

Ladies and gentlemen, good day, and thank you for standing by. Welcome to the Linde First Quarter 2026 Earnings Call and Webcast. [Operator Instructions] Please be advised that today’s conference is being recorded.

I would now like to hand the conference over to Mr. Juan Pelaez, Head of Investor Relations. Please go ahead, sir.

Advertisement

Juan Pelaez Vice President of Investor Relations

Abby, thank you. Good morning, everyone, and thanks for attending our 2026 first quarter earnings call and webcast. I’m Juan Pelaez, Head of Investor Relations, and I’m joined this morning by Matt White, Chief Financial Officer. Today’s presentation materials are available on our website at linde.com in the Investors section.

Please read the forward-looking statement disclosure on Page 2 of the slides and note that it applies to all statements made during this teleconference. The reconciliations of the adjusted numbers are in the appendix of this presentation. Matt will provide some opening remarks, I’ll give an update on Linde’s first quarter financial performance, and then Matt will finish the updated outlook, after which we will wrap up

TPG Inc. (TPG) Q1 2026 Earnings Call May 1, 2026 10:00 AM EDT

Company Participants

Gary Stein – Head of Investor Relations Jon Winkelried – CEO & Director Jack Weingart – Chief Financial Officer Todd Sisitsky – President, Managing Partner of North America and Head of North American & Europe Private Equity James Coulter – Founder & Executive Chairman

Advertisement

Conference Call Participants

Glenn Schorr – Evercore ISI Institutional Equities, Research Division Alexander Blostein – Goldman Sachs Group, Inc., Research Division Craig Siegenthaler – BofA Securities, Research Division Brian Bedell – Deutsche Bank AG, Research Division Kenneth Worthington – JPMorgan Chase & Co, Research Division Brian Mckenna – Citizens JMP Securities, LLC, Research Division Michael Brown – UBS Investment Bank, Research Division Benjamin Budish – Barclays Bank PLC, Research Division Steven Chubak – Wolfe Research, LLC Arnaud Giblat – BNP Paribas, Research Division Bart Dziarski – RBC Capital Markets, Research Division Michael Cyprys – Morgan Stanley, Research Division

Presentation

Advertisement

Operator

Good morning, and welcome to the TPG’s First Quarter 2026 Earnings Conference Call. [Operator Instructions] Please be advised that today’s call is being recorded. Please go to TPG’s IR website to obtain the earnings materials. I will now turn the call over to Gary Stein, Head of Investor Relations at TPG. You may begin.

Gary Stein Head of Investor Relations

Advertisement

Great. Thanks, operator, and welcome, everyone. Joining me today are Jon Winkelried, Chief Executive Officer; and Jack Weingart, Chief Financial Officer. In addition, our Executive Chairman and Co-Founder, Jim Coulter; and our President, Todd Sisitsky, are here with us for the Q&A portion of this call.

I’d like to remind you this call may include forward-looking statements that do not guarantee future events or performance. Please refer to TPG’s earnings release and SEC filings for factors that could cause actual results to differ materially from these statements. TPG undertakes no obligation to revise or update any

The world’s largest music company said revenue for the three months to the end of March grew 8.1% on year at constant currency to 2.90 billion euros, equivalent to $3.39 billion. Analysts had forecast 2.94 billion euros in revenue, according to Visible Alpha.

MOUNTAIN VIEW, Calif. — Alphabet Inc. shares edged lower in midday trading Friday, trading around $384 after the tech giant delivered robust first-quarter results that underscored its dominance in search advertising and accelerating growth in artificial intelligence-powered cloud services. The modest decline of roughly 0.13 percent came amid broader market fluctuations as investors digested strong earnings against ongoing antitrust scrutiny.

Alphabet Stock Dips Slightly as Q1 Earnings Highlight AI Cloud Boom and Regulatory Risks

Alphabet reported consolidated revenue of $109.9 billion for the quarter ended March 31, a 22 percent increase from the prior year and beating Wall Street expectations. The performance marked the company’s 11th consecutive quarter of double-digit growth, driven largely by Google Search and YouTube advertising alongside surging demand for Google Cloud infrastructure. Operating income rose 30 percent to $39.7 billion, with margins expanding to 36.1 percent, reflecting operational discipline amid heavy AI investments.

Net income jumped 81 percent to $62.6 billion, translating to earnings per share of $5.11 — a significant beat over analyst forecasts. Chief Executive Sundar Pichai highlighted AI’s pervasive impact, stating it is “lighting up every part of the business.” Google Cloud revenue climbed 63 percent year-over-year, fueled by Gemini AI tools and enterprise adoption, while Search revenue grew 19 percent despite competitive pressures from generative AI chatbots.

The results sent shares higher in after-hours trading Wednesday before Friday’s slight pullback. Analysts praised the “full-stack” AI strategy integrating hardware, software and services, positioning Alphabet to capitalize on the next wave of technological transformation. Capital expenditures rose sharply as the company ramps data center capacity for AI training and inference, with guidance signaling further increases into 2027.

Yet regulatory clouds loom large. European Union authorities continue probing Alphabet under the Digital Markets Act, recently providing guidance on opening services to rivals including AI developers. In the United States, the Department of Justice seeks structural remedies following monopoly findings in search and ad tech markets, potentially forcing changes to default agreements and data practices that could reshape Google’s core business. Brazil’s antitrust authority has also deepened its review of journalistic content practices.

Advertisement

These legal battles represent both risk and distraction as Alphabet invests tens of billions in AI infrastructure. Pichai and other executives have emphasized compliance while advocating for innovation-friendly regulation. The company maintains strong cash flow and a fortress balance sheet to weather potential fines or remedies, but prolonged uncertainty could pressure margins or force business model adjustments.

Alphabet’s advertising ecosystem remains resilient despite economic headwinds and AI disruption fears. YouTube Shorts and performance advertising products delivered robust growth, while the company’s focus on responsible AI deployment helps differentiate Gemini from competitors. Enterprise customers increasingly choose Google Cloud for its security, scalability and integrated AI capabilities, contributing to backlog expansion.

Dividend news provided another positive signal. The board approved a 5 percent increase to the quarterly payout, now $0.22 per share, reflecting confidence in sustained cash generation. Share repurchases continue as part of a disciplined capital return program, supporting shareholder value amid volatility.

Wall Street reactions were largely bullish. Several firms raised price targets, citing AI momentum and cloud acceleration as reasons for optimism. Consensus forecasts project continued double-digit revenue growth through 2026, with cloud margins expanding as scale efficiencies materialize. However, elevated capital spending — potentially reaching $190 billion this year — will test near-term profitability even as long-term positioning strengthens.

Advertisement

Competitive dynamics in AI remain fluid. OpenAI, Anthropic and Microsoft partnerships influence the landscape, yet Alphabet’s vast data assets, distribution reach through Android and Search, and hardware efforts like custom TPUs provide distinct advantages. Gemini’s multimodal capabilities and integration across products position it well for consumer and enterprise use cases.

Broader market context shows Big Tech navigating similar themes — innovation versus regulation, growth versus profitability. Alphabet’s results compare favorably to peers, with cloud growth outpacing many rivals and advertising holding steady. The modest Friday dip may reflect profit-taking or rotation rather than fundamental concerns following the earnings beat.

Looking ahead, investors will monitor AI monetization progress, regulatory developments and macroeconomic impacts on advertising spend. Alphabet’s diversified portfolio — from Waymo autonomous vehicles to Pixel devices and subscription services — provides multiple growth vectors beyond core search. Executives express confidence that AI investments will yield substantial returns over time.

For retail investors, Alphabet remains a cornerstone holding in tech portfolios, offering exposure to search dominance, cloud computing and emerging AI opportunities. The company’s scale, brand strength and engineering talent underpin long-term optimism despite short-term volatility from legal and spending pressures.

Advertisement

As the second quarter unfolds, focus shifts to product launches, partnership announcements and further regulatory clarity. Alphabet’s ability to balance aggressive AI investment with financial discipline will determine whether the current momentum sustains through 2026 and beyond. Friday’s trading action, while slightly negative, does little to dim the overall positive narrative emerging from the earnings report.

The biggest horse race in the country, the Kentucky Derby, takes place Saturday in Louisville. If you’re looking to make a wager on Kalshi, Polymarket or another prediction platform around the event — you’re out of luck.

There are no Kentucky Derby event contracts offered on the major prediction platforms, which host contracts on everything from sports outcomes to geopolitical events to reality TV show moments, but not horse racing.

Bill Carstanjen, CEO of Churchill Downs, which owns the Kentucky Derby and the racetrack where it’s held, told CNBC it’s unlikely that horse racing will ever show up on prediction markets because the race track owners don’t want it.

“You need to actually go to us, those who own the race tracks, to cut a deal,” Carstanjen said in an interview this week. “And from our perspective, that’s not something we’re interested in doing.”

Advertisement

Horse racing has long been something of its own little fiefdom. Betting on the races, America’s original form of sports betting dating back to the colonial era, enjoyed special status even before the Supreme Court in 2018 struck down a law that prevented states other than Nevada from offering sports betting.

By law, under the Interstate Horseracing Act of 1978, offering wagers on horses requires explicit permission from the host race track, the horsemen’s group made up of owners and trainers and the state racing commission where the race is held.

That’s left the burgeoning prediction markets industry on the outs.

“Prediction markets are not something that that would be good for horse racing, or the economic paradigm under which our industry works, which involves funding purses for the winners of the horse race,” Carstanjen said.

Kalshi declined to comment on the absence of horseracing on its platform. Polymarket didn’t respond to a request for comment. And representatives for the Commodity Futures Trading Commission, which regulates event contracts, likewise didn’t respond to a request for comment.

Advertisement

The tension raises an interesting question of when — and in what context — permission is needed for prediction market platforms to offer contracts on a given event.

U.S. states have argued companies like Kalshi and Polymarket need their permission (via a license) to offer wagers on sports. Prediction platforms have maintained they don’t need licenses because their platforms offer investing and trading activity, not gambling, and because they’re regulated by the CFTC.

The CFTC has filed multiple lawsuits against states seeking to prevent them from taking action against prediction platforms.

Kentucky, for its part, has taken a tough stance on predictions. Lawmakers in the state have proposed legislation that would ban any of its gambling licensees from offering predictions. It’s also proposed a 17.5% tax on prediction market fees.

Advertisement

Meanwhile, there’s still old-fashioned gambling set for Saturday’s Derby. Churchill Downs said it’s seeing increased betting during Derby Week leading up to the big race.

Caesars, too, said the amount of money wagered on the Kentucky Derby is pacing ahead of expectations.

— CNBC’s Jessica Golden contributed to this report.

Disclosure: Kalshi and CNBC have a commercial relationship which includes a minority investment.

Its head of consumer protection policy Sue Davies said: “It is deeply concerning that another children’s craft product, particularly from a major brand like Crayola, which is sold by big-name retailers, has been recalled due to potential asbestos contamination, continuing a worrying trend of recalls involving this deadly substance.

The Lanier Law Firm lead attorney Mark Lanier joins Varney & Co. to discuss the social media addiction trial verdict against Meta and Google, comparing it to tobacco litigation.

Tech giant Meta is threatening to cut off access to its social media platforms in New Mexico as a response to the state’s legal effort to compel changes to child safety protocols on the platform.

Meta and the state of New Mexico are expected to proceed to the second stage of their trial next week after a jury recently issued a $375 million award to the state after finding that the company misled consumers about the safety of its platforms and protections for children against sexual predators.

Advertisement

The next phase of the trial will concern what actions the parent company of Facebook, Instagram and WhatsApp must take to address those issues.

Among the remedies New Mexico is seeking is to impose a requirement that Meta meet a 99% accuracy threshold in verifying that children on its platform are at least 13 years old. Meta has pushed back on that requirement, arguing in a court filing that it’s unfeasible and would require it to “comply with impossible obligations.”

Meta is warning that it may be forced to pull its apps from New Mexico if the state prevails in requiring the social media giant to implement certain safeguards. (Arda Kucukkaya/Anadolu via Getty Images)

Meta’s legal team said in a filing that New Mexico’s “requests for relief are so broad and so burdensome, that if implemented it might force Meta to withdraw its apps entirely from the State of New Mexico as an alternative way of complying with the injunction.”

Advertisement

“It does not make economic or engineering sense for Meta to build separate apps just for New Mexico residents,” Meta’s lawyers added. “Nor could Meta guarantee the perfection the State demands, making it impractical for Meta to operate in New Mexico.”

The company has argued that it’s being unfairly singled out in comparison to other social media platforms that are popular with young people. It also previously signaled it will appeal the $375 million civil judgment against it.

New Mexico pushed back on Meta’s assertion that it would be impractical to comply with the safeguards it’s seeking for social media apps.

Meta is the parent company of apps including Facebook, Instagram and WhatsApp. (Reuters/Dado Ruvic/Illustration)

“Meta is showing the world how little it cares about child safety,” said New Mexico Attorney General Raúl Torrez. “Meta’s refusal to follow the laws that protect our kids tells you everything you need to know about this company and the character of its leaders.”

“We know Meta has the ability to make these changes. For years the company has rewritten its own rules, redesigned its products, and even bent to the demands of dictators to preserve market access. This is not about technological capability. Meta simply refuses to place the safety of children ahead of engagement, advertising revenue, and profit,” Torrez added.

New Mexico is also seeking that Meta implement safer recommendation algorithms that don’t prioritize engagement over child well-being, restrictions on end-to-end encryption for minors, prominent warning labels about the platform’s risks, permanent bans for adults engaging in or facilitating the exploitation of children, and an independent oversight regime through a court-appointed child safety monitor.

You must be logged in to post a comment Login