Business

Girls’ Generation’s Tiffany Young, Byun Yo Han Are Now Married

K-Pop star and Girls’ Generation member Tiffany Young and actor Byun Yo Han are officially married.

The couple has registered their marriage, which means that they are legally considered married despite not holding any wedding ceremony.

Tiffany Young and Byun Yo Han Are Married

According to The Korea Times, Byun’s agency TEAMHOPE confirmed the marriage in a statement to the couple’s fans.

“Actors Tiffany Young and Byun Yo Han completed their marriage registration today, based on deep trust in and love for one another,” TEAMHOPE said in the statement.

“We also feel cautious and concerned that the continuing news might cause some fatigue,” the company continued. “However, the two actors told us they wanted to share the news first with their fans, who have always watched over them with great love, and we are informing you of this out of respect for their wishes.”

The couple met when they co-starred in the Disney+ drama “Uncle Samsik.” They confirmed their relationship last December.

Will They Hold a Wedding Ceremony?

While no wedding ceremony has held upon the registration of their marriage, the couple is planning to hold a small ceremony, according to Korea JoongAng Daily.

This, again, was confirmed by TEAMHOPE.

“They are carefully considering holding a small wedding with family members in order to pay their gratitude, in the form of a [church] service,” the company said.

LAS VEGAS — CleanSpark Inc. shares climbed more than 5% Thursday to trade around $10.38 as investors cheered the Bitcoin miner’s robust March production numbers and accelerating pivot toward artificial intelligence and high-performance computing infrastructure in Texas.

The NASDAQ-listed company (CLSK) rose as high as $10.50 intraday amid renewed enthusiasm for crypto-related stocks and easing geopolitical tensions after a U.S.-Israel-Iran ceasefire. The stock has delivered a year-to-date gain of roughly 2% in 2026 while recovering from earlier volatility, with a market capitalization now hovering near $2.6 billion.

CleanSpark, one of the largest and most efficient U.S. Bitcoin miners, released its unaudited March 2026 operational update on April 7, reporting production of 658 Bitcoin for the month. That brought calendar-year 2026 output to 1,799 BTC through the first quarter. The company achieved a peak single-day production of 23.01 BTC and an average daily rate of 21.24 BTC.

Operational hashrate reached a record 50.0 EH/s at month-end, with an average of 47.3 EH/s during March. Fleet efficiency hit a peak of 16.07 J/Th, reflecting ongoing optimizations. CleanSpark held 13,561 BTC as of March 31, up from 13,363 at the end of February. It utilized 808 MW of its 1.8 GW of contracted power capacity.

The strong mining metrics helped offset lingering effects from a disappointing fiscal first-quarter earnings report released in early February. For the quarter ended Dec. 31, 2025, CleanSpark posted revenue of $181.2 million, up 11.6% sequentially but missing analyst expectations of about $194 million. The company reported a net loss of $378.7 million, or $1.35 per share — heavily impacted by non-cash unrealized losses on its Bitcoin holdings amid price volatility — compared with year-earlier net income.

Adjusted EBITDA turned negative at $295.4 million, underscoring the accounting swings common in the sector. Despite the miss, management highlighted a strengthened balance sheet with $458.1 million in cash and over $1 billion in Bitcoin holdings at quarter-end, providing dry powder for expansion.

CleanSpark has aggressively positioned itself at the intersection of Bitcoin mining and the AI boom. In January, the company announced a major land and power acquisition in Brazoria County, Texas, near Houston, for up to 447 acres with transmission-level access supporting an initial 300 MW demand load and potential expansion to 600 MW total. The deal closed in February, marking CleanSpark’s second strategic site in the greater Houston region after an earlier Austin County acquisition with 285 MW approved capacity.

Together, the Texas projects give CleanSpark more than 890 MW of aggregate potential utility capacity aimed at large-scale AI and high-performance computing data centers. CEO Matthew Schultz has emphasized building a “hyperscale-ready infrastructure platform” that can dynamically support both Bitcoin mining and AI workloads depending on profitability and demand.

The company controls 1.8 GW of power across its portfolio, powered by competitive energy prices, and continues to optimize sites for rapid deployment of compute resources. Executives have signaled advanced discussions for AI/HPC leases, though no major contracts comparable to peers’ multi-billion-dollar deals have been announced yet.

Analysts remain broadly bullish on CleanSpark despite recent earnings volatility and a Cantor Fitzgerald price target cut to $14 from $17 in early April. Consensus ratings lean toward Strong Buy or Moderate Buy, with an average 12-month price target around $19 to $20 — implying significant upside from current levels. Some firms see even higher potential if AI monetization accelerates.

Chardan Capital reiterated a Buy rating with a $16 target as recently as April 8, while the overall Wall Street view highlights CleanSpark’s operational efficiency and power portfolio as key differentiators in a capital-intensive industry.

The miner has maintained one of the lowest all-in sustaining costs in the sector through disciplined fleet management and energy procurement. Its deployed fleet stood at more than 224,000 miners by late March. Plans include further efficiency gains via technologies like liquid immersion cooling to reach sub-15 J/Th levels.

Next earnings for the fiscal second quarter ending March 31, 2026, are expected around early May, with analysts projecting continued revenue growth from higher hashrate but potential pressure from Bitcoin price fluctuations and network difficulty adjustments.

CleanSpark’s strategy reflects a broader industry trend: Bitcoin miners with access to cheap, scalable power are repurposing infrastructure for AI workloads amid explosive demand from hyperscalers. Electricity shortages and grid constraints have made permitted sites with ready power a scarce and valuable asset.

Risks abound. The company remains heavily exposed to Bitcoin’s price, which influences both mining economics and the value of its treasury holdings. Non-cash accounting volatility can produce headline-grabbing losses even in operationally strong quarters. Execution on large Texas data center builds faces typical challenges, including equipment lead times, regulatory approvals and competition for talent and components in the AI supply chain.

Broader sector dynamics also play a role. Rising network hashrate across Bitcoin could compress margins unless offset by efficiency gains or higher BTC prices. Geopolitical or macroeconomic shifts that pressure risk assets could weigh on the stock.

Still, momentum appears supportive. Shares jumped more than 9% on April 8 following positive options activity and broader crypto tailwinds, with Thursday’s gains extending the rebound. Volume has remained elevated, signaling sustained investor interest.

CleanSpark, founded in 1987 and reoriented toward Bitcoin mining in recent years, now describes itself as a data center developer optimizing low-cost energy for compute. It employs a growing team focused on AI infrastructure alongside its core mining operations and maintains facilities across multiple states.

As artificial intelligence capital spending by major tech firms surges — with combined forecasts exceeding $650 billion for 2026 — companies controlling gigawatt-scale power like CleanSpark are attracting fresh attention. Its Texas footprint positions it to potentially capture leasing revenue from GPU clusters while retaining Bitcoin mining as a flexible hedge.

Whether the current rally can build further will depend on upcoming earnings, progress on AI site development and the trajectory of Bitcoin. For now, investors appear willing to look past accounting noise and bet on CleanSpark’s dual-track growth story in energy, crypto and AI.

The stock closed Wednesday at $9.88 before climbing Thursday. By mid-afternoon, it traded near $10.38 with strong volume.

CleanSpark continues to emphasize capital stewardship, local grid support and sustainable operations. Its March update showed average Bitcoin sale prices around $71,396, reflecting strategic treasury management.

As the company prepares for its next quarterly report, focus will center on hashrate growth, power utilization trends and any updates on AI/HPC pipeline conversion. With a robust balance sheet and expanding infrastructure, CleanSpark aims to deliver shareholder value across volatile market cycles.

AMSTERDAM — Nebius Group N.V. shares surged more than 7% Thursday to trade around $134.60 as investors bet big on the fast-growing AI cloud provider’s landmark infrastructure contracts with hyperscalers and fresh Wall Street coverage highlighting its role in the artificial intelligence buildout.

The NASDAQ-listed company (NBIS) climbed as high as $141 intraday Thursday, extending a blistering rally that has seen the stock deliver more than 430% gains over the past year. The momentum accelerated this week following Cantor Fitzgerald’s initiation of coverage with an Overweight rating and a $129 price target, while broader optimism around AI infrastructure spending lifted related names amid easing geopolitical tensions.

Nebius, the restructured international AI infrastructure business formerly tied to Yandex, has emerged as a pure-play beneficiary of exploding demand for GPU-powered cloud capacity. The company operates advanced data centers optimized for large-scale AI training and inference, leveraging high-density compute clusters built around NVIDIA hardware.

In its most recent earnings released Feb. 12, Nebius reported explosive fourth-quarter 2025 revenue of $227.7 million, up 547% from a year earlier, though it missed analyst expectations of roughly $243 million to $247 million. Full-year 2025 revenue reached $529.8 million, a 479% jump from $91.5 million in 2024. The company swung to an adjusted EBITDA profit of $15 million in the quarter from a prior loss, while posting a net loss of $249.6 million driven by heavy capital expenditures.

Management highlighted strong execution, with year-end annualized recurring revenue (ARR) hitting $1.25 billion — beating its own guidance range of $900 million to $1.1 billion. Active power capacity stood at 170 MW by year-end, ahead of internal targets.

For 2026, Nebius guided to revenue between $3 billion and $3.4 billion, with ARR projected at $7 billion to $9 billion and adjusted EBITDA margins approaching 40% in the back half of the year as utilization ramps. The aggressive outlook reflects rapid deployment of new GPU clusters and long-term capacity agreements.

The biggest catalyst has been a string of mega-deals underscoring Nebius’s growing clout in the neocloud space. In March, the company announced a landmark agreement with Meta Platforms valued at up to $27 billion over five years. The pact includes $12 billion in committed dedicated AI infrastructure capacity starting in 2027, plus up to $15 billion in additional capacity purchases. The deal ranks among the largest infrastructure commitments Meta has made and validates Nebius’s ability to secure hyperscale anchor tenants.

Nebius has also secured significant business with Microsoft and other large customers, contributing to a reported backlog of committed capacity deals exceeding $45 billion when including potential expansions. In March, NVIDIA made a $2 billion strategic investment in Nebius to support next-generation hyperscale AI cloud infrastructure, providing both capital and a powerful endorsement from the GPU market leader.

The company is aggressively scaling its footprint. Plans include construction of one of Europe’s largest AI campuses in Finland with 310 MW capacity and multiple new data centers across Europe and North America. Nebius aims to deploy advanced systems including NVIDIA’s Vera Rubin NVL72 platforms in 2026. Capital expenditures are expected to run between $16 billion and $20 billion this year to fuel the expansion, funded in part by a $4.3 billion convertible notes offering completed in March and its strong cash position of approximately $3.68 billion.

Analysts have grown increasingly bullish. Consensus ratings lean toward Moderate Buy to Strong Buy, with an average price target around $154 to $171, implying 15% to 27% upside from recent levels. Some firms see even higher potential, with targets reaching $215 or more if execution on capacity deployment stays on track. Northland Securities and BofA have issued positive calls, while Cantor’s fresh Overweight initiation Thursday helped spark the latest leg higher.

“Nebius is one of the few scaled players capable of delivering dedicated AI infrastructure at the speed and density hyperscalers require,” one analyst noted following the Meta announcement. The company’s vertically integrated approach — controlling power, facilities, networking and GPU clusters — gives it an edge over traditional cloud providers facing allocation constraints.

Still, risks are substantial. Nebius remains deeply unprofitable on a GAAP basis and is burning significant cash on capex. Free cash flow turned deeply negative in recent quarters as the company races to bring new capacity online. Execution challenges include securing sufficient NVIDIA GPUs amid industry-wide shortages, navigating regulatory and grid hurdles for data center builds, and delivering on ambitious utilization targets.

Competition is intensifying from established players like CoreWeave as well as hyperscalers expanding their own infrastructure. Nebius’s heavy reliance on a handful of large customers also introduces concentration risk, though long-term contracts provide revenue visibility.

The stock’s valuation has expanded dramatically alongside its growth narrative. Trading at elevated multiples on forward sales, the shares reflect expectations of triple-digit revenue growth for several years. Market capitalization now exceeds $30 billion, up sharply from levels seen just months ago.

Thursday’s gains came on elevated volume, with shares breaking toward recent highs near $141. The rally builds on a more than 25% year-to-date advance in 2026 and follows positive commentary from market influencers, including Jim Cramer highlighting data center expansion trends.

Nebius executives expressed confidence in the outlook. Founder and CEO Arkady Volozh has described 2025 as the company’s “first full year of operations” marked by exceptional growth. Management is focused on converting its massive pipeline into contracted revenue while maintaining capital discipline where possible.

The company continues to innovate on its AI Cloud platform, recently introducing serverless AI capabilities and acquiring assets like Tavily to enhance agentic search features. These moves aim to broaden appeal beyond raw compute to higher-value AI services.

As artificial intelligence capital spending by Big Tech surges — with combined forecasts for major hyperscalers topping hundreds of billions in 2026 — providers like Nebius that can deliver scarce, high-performance GPU capacity are commanding premium attention.

Whether the current momentum sustains will depend on upcoming milestones: progress on data center deployments, potential new customer wins, and the May earnings report (estimated around late April to mid-May) that could provide further color on 2026 ramp. Analysts will scrutinize utilization rates, gross margins and capex efficiency.

Nebius Group employs a growing global team and operates from its base in Amsterdam while maintaining data centers across multiple continents. Originally emerging from the international assets of the former Yandex group after geopolitical restructuring, the company has fully repositioned as an independent AI infrastructure leader.

For investors, Nebius represents a high-beta play on the AI theme — offering explosive upside potential but with commensurate volatility and execution risk. The combination of secured mega-deals, NVIDIA backing and aggressive capacity buildout has turned it into one of the more compelling stories in the AI supply chain.

As Thursday’s trading showed, sentiment remains firmly in growth mode. With power capacity expanding rapidly and long-term contracts providing a foundation, Nebius appears well-placed to capture a meaningful slice of the AI infrastructure market — provided it can navigate the capital-intensive path ahead.

Shares closed Wednesday near $125 before powering higher. By mid-afternoon Thursday, they traded around $134.60 with strong participation from momentum and growth-oriented funds.

The EU’s much-delayed Entry/Exit System will change the way UK passengers travel to 29 countries.

TV channels for dogs are multiplying but research is mixed on whether dogs are watching.

Operator

Good day, ladies and gentlemen, and welcome to AmpliTech Group’s Quarterly Investor Update Call, where the company will discuss its FY 2025 Financial Results. Present in this call, we have the executive team of AmpliTech Group, Fawad Maqbool, CEO, CTO and Board Chair; Jorge Flores, COO; and Louisa Sanfratello, CFO. [Operator Instructions]

As a reminder, today’s conference is being recorded. I would now like to turn the call over to AmpliTech’s COO, Jorge Flores.

Jorge Flores

Chief Operating Officer

Thank you, operator, and thank you, everyone, for joining today’s call to review the progress of AmpliTech’s growth initiatives and to answer investors’ questions. Following initial management comments, we will open the call to investors’ questions as well. An archived replay of today’s call will be posted to the Investor Relationship section of AmpliTech’s corporate website. This call is taking place on Thursday, April 9, 2026.

Remarks that follow and answers to questions may include statements that the company believes to be forward-looking within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements generally include words such as anticipate, believe, expect or words of similar importance. Likewise, statements that describe future plans, objectives or goals are also forward-looking. These forward-looking statements are subject to various risks that could cause actual results to be materially different than expected. Such risks include, among others, matters that the company has described in its press releases and in its filings with the Securities and Exchange Commission. Except as described in these filings, the company disclaims any obligation to

CORNING, N.Y. — Corning Inc. shares climbed more than 3% Thursday to trade around $170.30 as investors rewarded the materials science giant’s deepening role in powering artificial intelligence data centers with high-density optical fiber, cable and connectivity solutions amid explosive hyperscale demand.

The NYSE-listed company (GLW) rose as high as $172.22 intraday Thursday, building on a series of strong sessions that have propelled the stock sharply higher in recent weeks. Corning has delivered roughly 89% year-to-date gains in 2026, turning it into one of the standout performers in the broader technology supply chain as AI infrastructure spending accelerates.

Corning, a 175-year-old innovator in specialty glass, ceramics and optical physics, has repositioned itself as a critical enabler of next-generation data center networks. Its Optical Communications segment — which includes fiber, cable and connectivity products — has seen surging enterprise sales driven by Gen AI adoption, with hyperscalers requiring far more fiber density and bandwidth than traditional cloud setups.

The momentum intensified in January when Corning announced a multiyear agreement with Meta Platforms valued at up to $6 billion. Under the deal, Corning will supply advanced optical fiber, cable and connectivity solutions to support Meta’s AI data center buildout across the United States. The partnership includes a major expansion of Corning’s optical cable manufacturing capacity in Hickory, North Carolina, with Meta serving as the anchor customer. Construction on the expansion officially began in late March.

“Building the most advanced data centers in the U.S. requires world-class partners and American manufacturing,” Meta’s Joel Kaplan said in the announcement. The pact underscores Corning’s commitment to domestic production while addressing the massive connectivity needs of AI training and inference clusters.

Corning showcased additional AI-focused innovations at the Optical Fiber Communication Conference (OFC) 2026 in March. Highlights included a multicore fiber solution that delivers four times the capacity per fiber strand within a standard footprint, reducing the number of connectors by up to 75%, cable mass by 70% and installation time by 60%. The company also introduced the Contour Flow micro cable for denser inter-data-center links, next-generation connectors and co-packaged optics systems designed to scale GPU density in AI networks.

These products address the “nervous system” of AI infrastructure, where fiber optics handle the enormous data movement between thousands of GPUs. Demand for such connectivity is growing at more than 50% annually in some estimates, creating a sustained tailwind for Corning’s optical business.

Financially, Corning delivered record results for full-year 2025. Core sales rose 13% to $16.41 billion, while core EPS jumped 29% to $2.52. In the fourth quarter, core sales grew 14% to $4.41 billion and core EPS increased 26% to $0.72, exceeding expectations. Management highlighted margin expansion, with core operating margin reaching 20.2% in the quarter.

The company upgraded its Springboard growth plan, now targeting an additional $11 billion in incremental annualized sales by the end of 2028 — up from the original $8 billion goal. For 2026 specifically, internal plans call for $6.5 billion in incremental sales, with a high-confidence figure of $5.75 billion.

For the first quarter of 2026, Corning guided for core sales of $4.2 billion to $4.3 billion, representing about 15% year-over-year growth, with core EPS expected in the range of $0.66 to $0.70. The outlook reflects accelerating momentum in optical communications and other segments.

Analysts have grown increasingly bullish. Recent price target hikes include Mizuho raising its target to $160 from $155, BofA moving to $155 from $144 earlier, and UBS to $171. Consensus ratings lean toward Moderate Buy, with average targets in the $130-$150 range, though some firms see potential well above current levels if AI demand sustains. Zacks recently upgraded the stock to a #2 Buy rank on improving earnings estimates.

Corning’s broader portfolio continues to contribute. Its Specialty Materials segment, home to Gorilla Glass used in consumer electronics, benefits from innovations like the new Gorilla Glass Ceramic 3 for foldable devices. Display Technologies and Environmental Technologies segments provide diversification, though Optical Communications has been the standout growth driver tied to AI.

The company maintains a healthy balance sheet and returned capital to shareholders through a quarterly dividend of $0.28 per share. Adjusted free cash flow nearly doubled in 2025, supporting both growth investments and shareholder returns.

Still, risks remain. Corning’s valuation has expanded significantly with the rally, trading at elevated multiples that assume continued strong AI spending. Competition in optical components could intensify, and any slowdown in hyperscaler capex — or shifts in technology architectures that reduce fiber needs — could pressure results. Broader supply chain issues for data center equipment also pose execution challenges.

Management expressed confidence in the outlook. CEO Wendell Weeks noted the transformed financial profile since launching Springboard two years ago, with meaningful margin and return on invested capital gains providing a strong base for future expansion.

“AI growth is expected to be unprecedented,” Weeks and other executives have emphasized, positioning Corning’s 175 years of materials innovation as uniquely suited to solve the density, power and scalability challenges of massive GPU clusters.

The stock’s recent surge accelerated in early April amid broader market optimism and sector tailwinds, with Thursday’s gains coming on solid volume. By mid-afternoon, shares traded near $170.30, up about 3.1% on the session.

Corning employs thousands worldwide and operates manufacturing facilities across North America, Europe and Asia. Its optical products are deployed in data centers globally, but the Meta partnership highlights a strategic push to strengthen U.S.-based production amid national focus on AI leadership and supply chain security.

As hyperscalers including Meta, Microsoft, Google and Amazon pour hundreds of billions into AI infrastructure in 2026, suppliers like Corning that provide the essential “plumbing” for high-speed, high-density interconnects are drawing fresh investor attention.

Upcoming first-quarter 2026 earnings, expected around late April, will be closely watched for further color on optical demand trends, margin performance and any updates to the upgraded Springboard targets.

For now, sentiment favors continued growth. With record backlog visibility from major AI deals, innovative new products and a proven ability to scale manufacturing, Corning appears well-positioned to capitalize on what many describe as a multi-year AI infrastructure supercycle.

Whether the blistering pace can persist will depend on execution, sustained hyperscaler spending and the company’s ability to convert innovation into profitable, recurring revenue streams.

Corning Inc., headquartered in Corning, New York, traces its roots to 1851 and has evolved from early glassmaking to a global leader in materials science. Its technologies touch everything from smartphone screens and automotive emissions control to the fiber optic networks that increasingly form the backbone of the AI economy.

Deborah Honig

Adelaide Capital

All right. Good morning or good afternoon, depending on where you’re dialing in from. Thanks for joining us today. We have a very exciting update with iFabric. They just put out their Q4 and full year 2025 numbers, which were fantastic and offered some guidance on Q1 ’26 as well.

With me today, I have Hylton Karon, CEO; Hilton Price, CFO; and Giancarlo Beevis, COO. We’re not going to work off a presentation. The format will be a quick overview of the company for anyone that’s new to the story, then we’re going to get right into the financial numbers and then open it up for Q&A. There is a Q&A box at the bottom of your screen, so feel free to use that. And even though we’re not working off a presentation, this session will contain forward-looking statements. If you’d like to know more about those, you can find them on the presentation on the company’s website.

With that out of the way, I’d like to introduce and hand the mic over to Giancarlo Beevis, who’s COO of the company and CEO of Intelligent Fabrics division.

Giancarlo Beevis

President & CEO of Intelligent Fabric Technologies (North America) Inc. and Director

Thanks, Deb, very much. Hi, how are you?

Deborah Honig

Adelaide Capital

I’m good, I’m good. Yes, why don’t you tell us a little bit about the company for people that are less familiar?

The brokerage notes that the recent macro-led selloff has dragged down Indian banks, NBFCs and affordable housing finance companies (AHFCs) alike, but contends that “beyond now-attractive valuations, we see several compelling reasons to turn constructive on the segment, driven by an impending inflection in both growth and asset quality.”

It adds that the current correction “is a favorable entry point” and reiterates its Outperform ratings on HomeFirst, Aadhar and Aptus, while maintaining Market-Perform on Aavas and PNB Housing Finance.

What makes Bernstein bullish on housing finance stocks?

Bernstein flags that AHFCs have already undergone a sharp derating over the last 6-9 months, with stock price declines steeper than those of larger NBFC peers. Current price-to-earnings multiples are now at three-year lows despite comparable or superior earnings growth.

“The sharp derating has also meant that valuations are at the lowest point in the last three years, with PE multiples now significantly lower than those of larger NBFCs despite earnings growth being comparable or superior,” the report says, highlighting the valuation gap as a key part of the upside argument.

On fundamentals, the analysts argue that both growth and asset quality are “now approaching an inflection point,” pointing to 3QFY26 data where disbursement growth showed sequential improvement and early-stage delinquencies (1+ DPD) began to stabilise or improve across most lenders. While AHFCs had earlier faced a slowdown in disbursements and a marginal rise in credit costs, Bernstein emphasises that return on assets has stayed above 3% for the segment, supported by improving net interest margins and stable operating expenses.

The report also underlines structural advantages that could help AHFCs ride out any prolonged macro stress. In an environment of tighter liquidity and higher inflation, “AHFCs are better positioned versus their larger NBFC peers,” it says, citing the secured nature of their loan books in both home loans and loan-against-property, and a funding profile marked by longer-tenor borrowings, a high floating-rate share, and access to National Housing Bank (NHB) funding.This combination, Bernstein argues, reduces the risk of sharp margin compression and insulates asset quality relative to unsecured-focused NBFCs.

At a thematic level, Bernstein reiterates that “the long-term thesis remains intact,” anchored in India’s still-low mortgage penetration as a share of GDP and the need for an operationally intensive, opex-heavy model to serve the mass-market borrower that many banks are reluctant to adopt.

The report notes that this model has translated into healthy earnings growth of around 20% and RoAs above 3% even in recent quarters, underscoring the medium-term potential of the affordable housing theme despite near-term volatility.

Top 2 stock picks

Within its coverage, Bernstein’s top picks are HomeFirst and Aadhar Housing Finance, which it describes as “the best franchises in this segment” thanks to diversified geographic presence and a proven ability to scale across markets.

It values HomeFirst using a 22x FY27 earnings multiple with a target price of Rs 1,430, and Aadhar at 20x FY27 earnings with a target of Rs 600, implying strong upside from current levels.

“While valuations are attractive across the sector, we continue to prefer HomeFirst and Aadhar,” the analysts say, adding that Aptus also looks attractive on low valuations, even as structural concerns keep them more cautious on Aavas and PNB Housing for now.

Check out what’s clicking on FoxBusiness.com.

The United States Postal Service is suspending employer pension contributions for workers beginning Friday, citing a looming cash shortfall, the agency announced Thursday.

The move, which affects the Federal Employees Retirement System (FERS), comes just weeks after the Postal Service warned Congress it could run out of cash in under a year without significant reforms, including changes to pension funding and stamp prices.

USPS emphasized that the pause will have no immediate impact on current or future retirees.

“There will not be any immediate detrimental impact to our current or future retirees if normal FERS cost payments are temporarily withheld,” Postal Service Chief Financial Officer Luke Grossmann said.

POSTAL SERVICE SAYS CASH COULD RUN OUT IN UNDER A YEAR WITHOUT CHANGES

A United States Postal Service worker delivers packages on Cyber Monday in New York Dec. 1, 2025. (Bess Adler/Bloomberg via Getty Images / Getty Images)

USPS has previously reported mounting losses over the years, totaling $118 billion since 2007, as volumes of its most profitable product, first-class mail, fell to their lowest levels since the late 1960s.

The financial strain was further exacerbated by global tariffs, high inflation and recent spikes in gasoline prices, along with growing competition from private carriers such as Amazon, which now delivers many of its own packages.

USPS said it typically sends the Office of Personnel Management (OPM), which oversees federal retirement accounts, about $200 million every two weeks to cover pension costs.

By suspending the payments, the agency expects to free up roughly $2.5 billion in the current fiscal year.

While the agency has suspended its employer contributions, it said it will continue transferring employee payroll deductions into retirement accounts.

USPS COULD SLOW SERVICE IN CERTAIN AREAS AS IT SEEKS TO CUT COSTS

An Amazon Inc. package sits on a conveyor belt at the United States Postal Service Merrifield processing and distribution center in Merrifield, Va., Dec. 19, 2018. (Andrew Harrer/Bloomberg via Getty Images / Getty Images)

Separately, the agency said its Thrift Savings Plan (TSP), a separate retirement savings program similar to a government 401(k), remains unaffected.

USPS will continue processing employee-funded contributions and matching funds into the Thrift Savings Plan (TSP), and noted that workers will be able to contribute more in 2026 under new IRS limits.

Postmaster General David Steiner testified before Congress on the current state of the U.S. Postal Service. (Pool)

In March, Postmaster General David Steiner told a House Oversight subcommittee that the Postal Service could run out of cash within a year without major changes.

Steiner outlined potential cost-cutting steps, including reducing six-day delivery, raising first-class mail prices from 78 cents to $1 or more and expanding borrowing authority after USPS hit its $15 billion debt cap.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

“In order to survive beyond the next year, we need to increase our borrowing capacity so that we don’t run out of cash,” Steiner said in prepared testimony. “The failure to do this could lead to the end of the Postal Service as we know it now.”

The rise in energy prices has hit Asia particularly hard as many nations are heavily reliant on Gulf oil.

Anthropic revenue just hit a $30 billion run rate

Richard Riakporhe prays for Jeamie TKV ahead of British title fight

New ‘LucidRook’ malware used in targeted attacks on NGOs, universities

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Spanx – Corporette.com

-

Business4 days ago

Business4 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Business6 days ago

Business6 days agoExpert Picks for Every Need

-

Sports5 days ago

Sports5 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Tech2 days ago

Tech2 days agoHow Long Can You Drive With Expired Registration? What Florida Law Says

-

Business5 days ago

Business5 days agoNo Jackpot Winner, Prize to Climb to $231 Million

-

Fashion4 days ago

Fashion4 days agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Politics6 days ago

Wings Over Scotland | The quality of mercy

-

Fashion2 days ago

Fashion2 days agoLet’s Discuss: DEI in 2026

-

Business5 days ago

Business5 days agoAkebia Therapeutics, Inc. (AKBA) Discusses Pipeline Progress and Strategic Focus on Kidney Disease Treatments at R&D Day – Slideshow

-

Crypto World1 day ago

Crypto World1 day agoBitcoin recovers as US and Iran Agree a Ceasefire Deal

-

Politics7 days ago

Politics7 days agoEast Jerusalem Palestinian families eviction orders

-

Politics7 days ago

Politics7 days agoWhy so many children are now classified as ‘disabled’

-

Crypto World12 hours ago

Crypto World12 hours agoCanary Capital Files SEC Registration for PEPE ETF

-

Politics6 days ago

Politics6 days agoThe UK should not pay a penny in slavery reparations

-

Politics7 days ago

Politics7 days agoNuclear rockets, moon bases and NASA’s Mars plan

-

Tech7 days ago

Tech7 days agoThe Threadless Ball Screw Never Took Off, But Don’t Write It Off

-

Business7 days ago

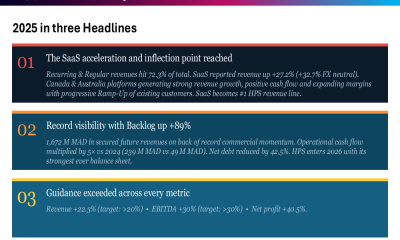

Business7 days agoHPS FY 2025 slides: SaaS inflection drives 22% revenue growth

-

Fashion7 days ago

Fashion7 days agoTory Burch’s Spring 2026 Campaign Goes on a Getaway

-

Fashion6 days ago

Fashion6 days agoFrugal Friday’s Workwear Report: Hammered Metallic Button Sweater Vest

You must be logged in to post a comment Login