Some institutional investors who had grown accustomed to outperforming the broader private equity composites are finding they have not done so consistently in recent years. Their diagnoses of the problem often center on specific decisions or biases they made in their recent manager selection, whereas a likely culprit is a falloff in the persistence of outperformance among private equity managers.

While wide performance dispersion persists among private equity funds of a given vintage, academic research suggests that the tendency for a manager’s prior strong performance to persist into subsequent funds has largely disappeared, particularly when prior performance is based on the interim measures used to compare funds less than 10–15 years old. If this lack of persistence is the “new normal,” it will be very difficult for investors to expect to outperform the private equity composites by meaningful amounts going forward.

Investment committees should encourage institutions to raise the bar for hiring private equity managers, as putting money to work relatively cheaply in the public markets is a better investment than paying high fees for private equity managers they have less than full confidence in.

My day job at GMO does not directly involve private equity beyond being an observer. But I do wind up discussing private equity reasonably regularly, both with investment committees that I serve on and when invited to speak to the investment committees of other institutions. And in those situations, I’ve started to notice something a little jarring that may not be as obvious to investment committee members who only experience the performance of one or two institutions.

It is well known that private equity has failed to keep up with the public markets over the last several years. But I also seem to be hearing from a number of institutions that the performance of their particular PE portfolio, which in the past might have done substantially better than the Preqin, Cambridge Associates, or other composite, no longer seems to be doing so. There is usually an excuse that feels specific to the institution in question—“we focused too much on co-investment opportunities and failed to keep a high enough bar on our expectations for the actual fund performance,” or “we were too slow to react to our GPs’ loss of focus and mission creep.”

The implication of those explanations is that fixing a particular problem they diagnose will lead to better relative performance in the future. But there is another explanation for this phenomenon that is less fixable and feels awfully plausible to me: if the persistence of performance for PE managers has gone away, or even significantly deteriorated, the performance difference between the best institutional PE portfolios and the mean is doomed to collapse to low levels. 1 For private equity allocations predicated on a belief in the investment staff’s ability to find and secure the very best private equity managers, such an explanation would call into question the rationale for the allocation in the first place.

The original handbook for the endowment model, David Swensen’s Pioneering Portfolio Management (2009), made no claims about an inherent return premium for private equity. While Swensen acknowledged some advantages of private equity in principle—better alignment with investors, longer time horizons, the focus on operating efficiency that comes along with a greater debt load—he pointed out that private equity also suffers from high fees, principal-agent problems, and the tendency for successful managers to raise ever-larger funds only for them to underperform their earlier, smaller ones.

Advertisement

He concluded that private equity was riskier than public equities due to its high leverage and, to the best of his knowledge, achieved disappointing median returns over its history (pp. 220–235). 2 The case for private equity, rather than resting on some vague “illiquidity premium,” 3 was all about finding extraordinary managers. He believed private assets were a good place to do that, given their much wider range of performance across managers relative to public equities or fixed income.

In practice, generating this alpha for an institution would involve finding extraordinary portfolio managers or firms who can consistently outperform their peers. So the first question any investment committee should ask when discussing an allocation to private equity or any other private asset is: what makes us confident we can find these extraordinary managers and get meaningful allocations to their funds?

If the committee can’t credibly answer that question, it makes little sense for them to try to replicate the asset allocation of institutions that can. But even for institutions that have reason to claim such a selection ability, private equity fund performance really needs to be significantly persistent for the game to work. And it is far from clear that such persistence exists.

Several academics have done interesting work on the topic, noting that persistence of performance has fallen notably since 2000, and more so for private equity than venture capital. 4 A particularly relevant finding is that the interim performance of funds that have not completed their life cycles is entirely unhelpful in predicting future fund returns, a real problem since those are the only returns recent enough to feel relevant when considering a manager’s next fund.

Advertisement

While we all know “past performance is not indicative of future results,” it is extremely hard to overstate how central past performance is to investors’ decision-making when choosing private asset managers. You are buying into a blind pool, and almost the only thing you know is what the manager did in the past.

While the performance of the investments in that previous pool is not the only thing you can analyze, it feels like the most salient piece of data there is. But what if that is an illusion? A mature private equity portfolio will consist of multiple funds from multiple managers, so the total number of different funds owned by an institution will generally be pretty large, easily a couple of dozen or more, even if the institution has relationships with a relatively small number of firms.

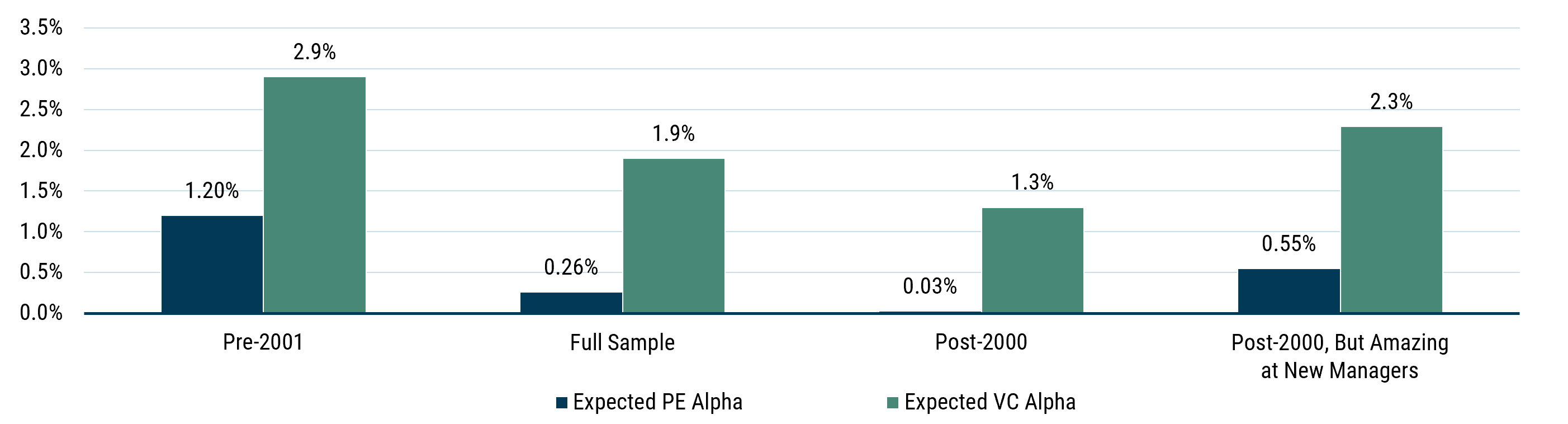

If there truly is little persistence in private equity fund returns, it implies that even if the range of returns between the best- and worst-performing funds remains large, the aggregate returns for an institution will almost always be close to the median. The chart below shows the implied alpha of a diversified PE portfolio across several levels of performance persistence (Braun, Jenkinson, and Stoff 2017).

Effect of Performance Persistence on Expected PE and VC Alpha

Source: Braun, Jenkinson, and Stoff (2017) Assumed alpha for quartiles of performance is 8%/3.5%/-3.5%/-8% for PE and 12%/4%/-4%/-12% for VC. “Amazing at New Managers” assumption is 40%/30%/20%/10% odds of new managers being in each alpha quartile, and 20% of assets in PE/VC invested in such new managers.

Advertisement

I’ve put the venture capital results in as well. While there was basically no evidence of persistent performance in the post-2000 sample for private equity, venture capital did show a decent amount of persistence, even if it, too, shows substantially less persistence than the early sample. I added a fourth column in which I made a friendly assumption about the new funds that an institution hires. I assumed that the institution had an amazing record in backing new managers, and that those new managers had a 40%/30%/20%/10% chance of being in the 1st through 4th quartiles of performance.

I further made the (probably insanely friendly) assumption that the institution’s full 20% PE or VC allocation was invested in such funds (such an institution could still not expect very much alpha from a PE portfolio, though 55 basis points is a whole lot better than the 3 basis points of implied alpha for an institution that simply reupped with its strongest performers).

It’s possible I’m being unfair in assuming that the basic due diligence in choosing to invest in the new funds of current managers is to look at the interim performance of their previous funds, but for institutions whose current alpha relative to the PE composite does not look particularly impressive, I think it’s fair to ask why you think it will get better in the future.

I’m not trying to make the case that institutions should abandon private equity. Actually, if one believes, as I do, that private equity is choosing from a small, junky group of firms, the industry’s performance has been somewhat better than it looks over the last decade. 5 I also believe that investing skill exists, 6 and that it makes sense for well-resourced institutions to invest with private equity managers they truly have high conviction in. The difference between the best and worst performers among private equity funds remains large, and an institution that can truly tilt the odds in favor of top-quartile results will reap substantial benefits.

Advertisement

But the bar to invest in a private equity manager should be high—arguably even higher than it is for active public asset managers, since you’ll be stuck paying PE managers high fees for a long time, even if you lose conviction in the interim. And if individual fund allocations truly do have a high bar, a target PE allocation may not even make sense (at least not beyond establishing an upper limit).

If, for example, you target 25% of your portfolio in U.S. public equities and can only come up with 10% worth of allocations to active managers you truly believe in, you have the option to allocate the other 15% passively. That passive option is not available to you in private equity. If you max out on high-caliber PE managers short of an overall allocation target, you will wind up investing the rest of your allocation in managers you have less confidence in. Paying high fees to managers you have less confidence in is unlikely to be a good use of capital.

How can the investment committee help? I think a good start would be for the investment committee to ask the investment staff to discuss their beliefs about each asset class in which the institution invests, the purpose each serves in the portfolio, how much (if any) alpha they expect to add in each asset class, and, crucially, how they intend to test those beliefs over time. They should document their beliefs for each asset class and compare them periodically, perhaps every three to five years. 7

At the end of the day, the role of the investment committee is to help the investment staff do a better job managing the portfolio. That should not be about second-guessing individual manager decisions, but pushing the investment staff to think critically about what they do and why is absolutely in the committee’s wheelhouse. Private equity programs are not meant to run on autopilot; there are critical questions to answer and, for many institutions, disappointing results to grapple with.

Advertisement

1 There will still be a fair bit of performance dispersion, since most investors invest with a relatively small number of PE managers, and there will still be plenty of variability in actual fund returns. But without persistence of returns, that variability will wind up mostly owing to chance, and longer-term returns will tend to converge.

2 Paraphrased from the 2009 edition, which made basically the same points as the original 2000 edition (pp. 224–233) with some updated data.

3 An illiquidity premium for leveraged buyouts (LBOs), at least, never made any sense in the first place. If you voluntarily take a public company private and pay a premium to do so, there is no plausible mechanism by which you could possibly get paid for taking on the illiquidity. The illiquidity might be a means to an end for some other mechanism to achieve higher returns, but the idea that you would generally get paid for the fact that the asset is no longer liquid is just silly when the illiquidity is entirely self-imposed.

4 I’m not going to pretend to give a comprehensive listing of the research, but a couple of studies that stood out to me included Braun, Jenkinson, and Stoff (2017), which looked at performance by deal rather than by fund, helping to abstract away from some of the fund return calculation problems; and Harris, Jenkinson, Kaplan, and Stucke (2023), which looked at the problem of interim performance calculations that investors are forced to rely on given the long lives of funds.

6 Admittedly, I’m highly likely to be biased toward such a belief.

7 The risk in doing this is that it just turns into a referendum on which assets have done well or badly in the trailing period, which would be a profound mistake. There is already too much performance chasing in the investment world. But putting your beliefs down on paper is extremely important to avoid the narrative creep that it is all too easy to fall into. If ”private real estate is a great place to add alpha” turns into “private real estate is an inflation hedge,” then into “private real estate is an under-owned asset class,” and so on—each rationale replacing the last as the thesis fails to play out—while the target allocation remains fairly static, something has gone very wrong.

References

Braun, R., Jenkinson, T., & Stoff, I. (2017). How persistent is private equity performance? Evidence from deal level data. Journal of Financial Economics, 123 (2), 273–291. https://doi.org/10.1016/j.jfineco.2016.01.033

Advertisement

Harris, R.S., Jenkinson, T., Kaplan, S.N., & Stucke, R. (2023). Has persistence persisted in private equity? Evidence from buyout and venture capital funds. Journal of Corporate Finance, 81 (102361). https://doi.org/10.1016/j.jcorpfin.2023.102361

Swensen, D. (2009). Pioneering Portfolio Management: An Unconventional Approach to Institutional Investment, Fully Revised and Updated. Free Press.

Disclaimer: The views expressed are the views of Ben Inker through the period ending May 2026 and are subject to change at any time based on market and other conditions. This is not an offer or solicitation for the purchase or sale of any security and should not be construed as such. References to specific securities and issuers are for illustrative purposes only and are not intended to be, and should not be interpreted as, recommendations to purchase or sell such securities.

Choosing the right roofing style is one of the most important decisions for any property owner in the UK. The roof plays a vital role in protecting a building from rain, wind, temperature changes, and other environmental factors.

When planning a new build, extension, or roof replacement, many homeowners find themselves deciding between a flat roof and a pitched roof.

Both roofing systems have distinct advantages and limitations. The best choice often depends on factors such as property design, budget, maintenance expectations, and local weather conditions. Understanding how each option performs in the UK’s climate can help property owners make an informed decision.

Understanding Flat Roofs

A flat roof is designed with a very slight slope that allows rainwater to drain away. Although referred to as “flat,” these roofs are not completely level. Modern flat roofing systems are commonly constructed using materials such as EPDM rubber, fibreglass, or high-performance felt. Flat roofs have become increasingly popular for home extensions, garages, garden rooms, and contemporary residential properties. Their clean, modern appearance makes them attractive for modern architectural designs. This growing demand can be seen in areas such as flat roofing Watford projects, where homeowners often choose flat roof systems for their practicality, cost-effectiveness, and sleek appearance.

One of the primary advantages of a flat roof is affordability. Installation costs are generally lower because fewer materials are required, and construction is typically faster than a pitched roof. Flat roofs also provide easy access for inspections, repairs, and maintenance. Another benefit is the potential use of roof space. Many property owners choose to incorporate roof terraces, solar panels, or green roofing systems on flat roof structures.

Advertisement

Understanding Pitched Roofs

A pitched roof features two or more sloping sides that create an angled structure. This traditional roofing design is commonly seen across the UK and has been used successfully for centuries. Pitched roofs are particularly effective at directing rainwater away from the property. Their steep angles help prevent water accumulation and reduce the risk of leaks caused by standing water.

These roofs also offer additional attic or loft space, which can be used for storage or converted into living accommodation. For homeowners seeking long-term value, a pitched roof often provides greater durability and lifespan compared to many flat roofing systems.

The classic appearance of a pitched roof complements a wide range of architectural styles, making it a preferred choice for many traditional homes.

Flat Roof vs Pitched Roof Comparison

Feature

Flat Roof

Pitched Roof

Cost

Lower installation cost

Higher initial cost

Lifespan

25–40 years

50+ years

Rain Performance

Needs drainage system

Excellent natural runoff

Maintenance

Easier access, more frequent checks

Less frequent but harder access

Energy Efficiency

High with proper insulation

High with loft insulation

Usable Space

Can be used for terrace/solar panels

Provides loft/attic space

Weather Resistance

Good when properly installed

Excellent in heavy rain/snow

Aesthetic Style

Modern, minimal

Traditional, classic

Performance in UK Weather Conditions

The UK climate includes frequent rainfall, strong winds, frost, and occasional snowfall. These conditions place constant pressure on roofing systems throughout the year.

Advertisement

Rainfall Performance

Pitched roofs perform extremely well in heavy rainfall because water naturally flows down the slopes into guttering systems. Flat roofs rely on drainage systems, and while modern materials are highly effective, proper installation is essential to avoid water pooling.

Wind Resistance

Both roof types can perform well in windy conditions when properly designed. Pitched roofs may experience more wind uplift on exposed areas, while flat roofs can benefit from a more aerodynamic surface. Installation quality is the most important factor in both cases.

Snow and Ice

Pitched roofs allow snow and ice to slide off easily, reducing structural load. Flat roofs can retain snow for longer periods, which may increase weight. Modern structural design accounts for this, but proper engineering is essential.

Energy Efficiency

Energy efficiency is becoming increasingly important for homeowners looking to reduce energy costs.

Advertisement

Pitched roofs often provide additional insulation opportunities through loft spaces. These air pockets can help regulate indoor temperatures throughout the year.

Flat roofs can also achieve excellent thermal performance when fitted with modern insulation systems. In many cases, the overall energy efficiency depends more on insulation quality than roof shape alone.

Maintenance Requirements

Every roofing system requires ongoing maintenance to maximise its lifespan.

Flat roofs typically need more frequent inspections to ensure drainage systems remain clear and that membranes remain intact. Because the surface is accessible, maintenance is often simpler and safer to carry out.

Advertisement

Pitched roofs generally require less routine attention. However, repairs can be more complex due to height and accessibility challenges. Missing tiles, damaged flashing, and gutter issues should be addressed promptly to prevent water ingress.

Professional inspections help identify minor problems before they develop into costly repairs.

Lifespan Comparison

Roof longevity is a major consideration for property owners making long-term investments.

A well-installed pitched roof can often last 50 years or more, depending on the materials used. Slate and clay tile systems may last significantly longer with proper maintenance.

Advertisement

Modern flat roofing systems have also improved dramatically in recent decades. High-quality EPDM and fibreglass roofs commonly achieve lifespans of 25 to 40 years when professionally installed and maintained.

The lifespan of either roofing system depends heavily on workmanship, materials, and regular maintenance.

Cost Considerations

Budget frequently influences roofing decisions.

Flat roofs generally have lower installation costs because they require fewer structural components and less labour. This makes them particularly attractive for extensions and smaller structures.

Advertisement

Pitched roofs involve more complex construction and greater material usage, resulting in higher upfront costs. However, many homeowners view the increased durability and longevity as a worthwhile long-term investment.

When evaluating costs, it is important to consider both initial installation expenses and future maintenance requirements.

Which Roof Is Best for UK Weather?

There is no universal answer because the ideal roofing solution depends on individual property requirements.

For homeowners seeking a traditional appearance, excellent rainwater management, and maximum longevity, a pitched roof is often the preferred choice.

Advertisement

For modern properties, extensions, and projects where budget efficiency and usable roof space are priorities, a flat roof can provide excellent performance when installed using high-quality materials and proper drainage systems.

Many experienced roofing professionals, including reputable roofers in St Albans, recommend choosing a roofing solution that aligns with the property’s design, functional requirements, and long-term maintenance goals, rather than making a decision based solely on current trends.

Frequently Asked Questions

1. Are flat roofs suitable for heavy UK rainfall?

Yes. Modern flat roofing systems are designed with slight slopes and efficient drainage systems that allow water to drain effectively when installed correctly.

2. Which roof type lasts longer?

Generally, pitched roofs have a longer lifespan and can last 50 years or more. Modern flat roofs can also provide decades of service with proper maintenance.

Advertisement

3. Is a flat roof cheaper than a pitched roof?

In most cases, yes. Flat roofs typically require fewer materials and less labour, making them more cost-effective to install.

4. Which roof is more energy efficient?

Both roof types can achieve excellent energy efficiency. The quality of insulation and installation has a greater impact than the roof design itself.

Rahul Tandon is joined by Rebecca Choong Wilkins in Singapore and Walter Todd in South Carolina, USA. They discuss which jobs may be most resistant to the rise of AI and whether skilled trades such as plumbing and locksmithing could offer greater job security. They also compare the challenges facing the US and Chinese economies in light of the latest data releases. And can Toy Story 5 match the box-office success of its predecessors?

Producers: Neil Morrow and Bisi Adebayo

Executive Producer: Justin Bones

Somewhere in a Vancouver boardroom, a team approved a drum.

The instrument that Lululemon wheeled onto the Great Wall of China last month, framed by rows of contented yogis and a hired celebrity, turned out to be Japanese, or near enough that those who analysed the footage online could make the case. The timing is unfortunate, with Beijing and Tokyo trading accusations over Taiwan, and the Chinese internet primed to interpret any slight as a national one. Lululemon has since apologised to the celebrity and the public, and attempted to erase the campaign from existence, admitting that it suffered “limitations in [their] professional knowledge”.

That phrase deserves pause. It is the most honest thing any brand has said in this situation in years. Nobody in the room knew enough to see the problem, but, fundamentally, the room was built so that nobody could have.

This is a failure that no amount of talent inside a brand’s office can fix, because it’s a failure not of competence but instead almost certainly of composition. A capable in-house team shares a language, a set of reflexes and a mutual understanding of what is acceptable. The more cohesive a team becomes, the more efficiently it navigates. As such, those instead best placed to analyse whether a message, narrative or a campaign reads as intended – several zones away, to an audience carrying a history no one in the room had considered – are precisely those not invited to the meeting.

The recent record is not short. The most instructive case belongs to fellow Canadian apparel manufacturer Arc’teryx – a brand whose entire identity rests on reverence for the wild – and who, in September, set off an enormous fireworks display across a Tibetan ridge at eighteen thousand feet. In an attempt to honour the landscape, they were instead accused of desecrating it. Over 90 million engaged with the government’s announcement of an investigation into the stunt, and China’s Advertising Association concluded the stunt had destroyed years of trust in the firm’s eco credentials. A company that sells itself on protecting nature was seen to set light to it, and nobody had registered the contradiction, because everybody believed the same flattering thing about what they were doing.

Advertisement

As recently as last month, Starbucks released a range of “Tank” tumblers in South Korea – the company’s third largest market – on the anniversary of the Gwangju uprising, when in 1980, paratroopers crushed pro-democracy protests against military strongman Chun Doo-hwan. Prada spent much of last year explaining sandals it had paraded down a runway that were, to any Indian eye, the Kolhapuri design that artisans in Maharashtra and Karnataka have made for centuries, credited to no one. None of these was the work of fools. Each was formed by a clever and well-intentioned team – certain of a good idea – with no one whose job was to flinch first.

What the external specialist sells, then, is not creativity – of this, the internal team usually has a surplus. It is the deliberate importation of a missing perspective. Those who have, by nature of the role, seen a mistranslation turn into a scandal and whose wider market knowledge can predict how a celebration to one may read as provocation to another.

Companies pay lawyers to read contracts and auditors to verify accounts precisely because the downside of skipping them is so much larger than the fee. Cultural risk is no different, except brands have not yet naturally learned to budget for it.

Lululemon will likely survive its version: China is its fastest-growing market and accounts for a sixth of global sales, and the misjudged drum might even be forgotten by Autumn. But surviving a mistake is not the same as avoiding one, and the firms that keep treating cultural risk as a detail are the ones who end up paying for it.

Advertisement

Alex Gilmore

Alex is Head of Digital at Farrant Group, a strategic communications agency in London and Dubai. He advises brands, family offices and high-profile principals on reputation and narrative in unfamiliar and challenging markets.

Northern Trust Asset Management is a global investment manager that helps investors navigate changing market environments in efforts to realize their long-term objectives.

Entrusted with $1.2 trillion in assets under management as of March 31, 2024, we understand that investing ultimately serves a greater purpose and believe investors should be compensated for the risks they take — in all market environments and any investment strategy. That’s why we combine robust capital markets research, expert portfolio construction and comprehensive risk management in an effort to craft innovative and efficient solutions that seek to deliver targeted investment outcomes.

As engaged contributors to our communities, we consider it a great privilege to serve our investors and our communities with integrity, respect and transparency.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company. Note: This account is not managed or monitored by Northern Trust Asset Management, and any messages sent via Seeking Alpha will not receive a response. For inquiries or communication, please use Northern Trust Asset Management’s official channels.

Weardale Lithium secured grant funding earlier this year and is looking to scale up its operations

From left: Paul Bradley, chief financial officer; Sharon Bennett, assistant principal (Advanced Manufacturing and Partnerships); Stewart Dickson, managing director of Weardale Lithium, Alison Maynard, deputy principal of New College Durham.(Image: New College Durham)

The company behind plans to draw valuable lithium deposits from underneath the County Durham countryside has partnered with a college to create the skills necessary for the vision.

Weardale Lithium hopes to use lithium carbonate-rich geothermal waters in the North Pennine Ore Field to extract the material which is critical to battery manufacturing and energy storage. The project – which has secured grant funding from the Government’s Drive35 competition – could create jobs that will require technical skills.

That has led to a partnership with New College Durham, which is already active in the area following the launch of its National Battery Training & Skills Academy (NBTSA) which delivers specialist training in battery technology and prepares learners for careers in electric vehicles, energy storage and advanced manufacturing.

Alison Maynard, deputy principal of New College Durham, said: “This partnership with Weardale Lithium marks an important milestone for both our students and the wider regional economy. By working in close collaboration with industry, we are equipping learners with the advanced technical knowledge and specialist skills required to succeed in a rapidly evolving energy sector, while supporting the development of sustainable, high-value careers across the North East.

Advertisement

“The strength of our curriculum, the depth of our employer partnerships, and our clear focus on future workforce needs have recently been recognised at a national level. We are extremely proud to have been confirmed as one of only four Technical Excellence Colleges for Advanced Manufacturing in the country, an achievement that reflects both the quality of our provision and our commitment to delivering skills that align with industry demand.”

Planning approval was granted last year for Weardale Lithium’s demonstration plant at its Eastgate cement works site. The firm is now looking to scale up its operation and will work with New College Durham on training programmes.

Stewart Dickson, managing director of Weardale Lithium, added: “By connecting education, research and industry, this partnership will play a vital role in ensuring the North East workforce is equipped with the advanced skills needed to support the clean energy sector’s rapid expansion. With significant progress being made locally, including our planned lithium extraction projects in County Durham, the region is quickly emerging as a key contributor to the UK’s critical minerals and battery supply chain.

“Through this collaboration, we are not only responding to immediate skills demands but also helping to build a sustainable talent pipeline that aligns with national priorities around energy security and the development of domestic lithium production. By aligning education with cutting-edge innovation and industrial growth, we are positioning the North East and its workforce at the forefront of the UK’s transition to a low-carbon, high-value economy.”

Ministers are weighing up whether parts of a clampdown on the low-value imports that power Shein and Temu could arrive sooner than planned, after sustained lobbying from British retailers who say the current timetable leaves the high street exposed.

The government confirmed last year that reform of the so-called de minimis regime, which lets goods worth less than £135 enter the UK without customs duties, would not be fully in place until 2029 because of the complexity of building a new customs system from scratch. Now, officials are understood to be examining whether elements of that reform can be brought forward while still keeping goods flowing freely at the border.

The consultation on the design of a replacement system closed in early March, and ministers are still working through the responses. For retailers who have spent the better part of two years arguing that the relief tilts the pitch against them, even that assessment period feels too slow.

The de minimis exemption has become one of the defining battlegrounds in the contest between established British retailers and the fast-growing overseas platforms snapping at their heels. Shein and Temu, both founded in China, have expanded rapidly in Britain by shipping low-cost goods directly from manufacturers to shoppers, sidestepping the duties and overheads that domestic firms shoulder when they import through conventional supply chains.

Names including Sainsbury’s, Currys and AO World have argued that the carve-out hands overseas rivals a structural advantage. It is an argument that has steadily gained volume, with UK retailers calling on the government to end China’s tax-free advantage and warning that the playing field has been tilted for too long.

Advertisement

The government has already said it intends to abolish the exemption, a position set out when Rachel Reeves moved to review the import tax loophole in its crackdown on cheap overseas goods. But it has insisted that a phased transition is needed to avoid disruption at ports and customs checkpoints. Officials say a new system for collecting duties on low-value parcels has to be built, in their words, “from the ground up” to cope with the sheer volume of packages arriving in the country, and that businesses moving and selling food will also need time to prepare. The full design is set out in the Treasury’s consultation on reforming the customs treatment of low-value imports.

The timetable has frustrated retailers, who have stepped up their lobbying in recent months. Last week Andrew Murphy, chief executive of toy seller The Entertainer, wrote to the government urging ministers to accelerate the reforms, describing the current schedule as “unacceptable”.

Industry groups have also warned that Britain risks becoming an outlier as other major economies move faster. The United States scrapped its own low-value import exemption last year, while the European Union is preparing to introduce a temporary customs duty on low-value parcels from next month before bringing in wider reforms, a shift confirmed by the European Commission’s taxation and customs directorate. The fear among executives is that, as doors close elsewhere, more low-cost and potentially unsafe goods will simply be redirected towards the UK, a concern that has already prompted warnings that delay risks turning Britain into a ‘dumping ground’.

The Treasury, for its part, is holding the line on both the destination and the pace. “The rapid growth in low-value imports is hurting our high streets and retailers,” it said. “We are removing the customs duty relief for low-value imports and reforming the way these goods are declared into the UK to ensure all goods are appropriately controlled.

Advertisement

“This is a significant reform which backs our businesses to compete and grow, controls safety and flow of goods at our border, and keeps the UK in line with our international partners.”

For Britain’s retailers, the principle is now settled. The fight, increasingly, is over the clock.

Jamie Young

Jamie is Senior Reporter at Business Matters, bringing over a decade of experience in UK SME business reporting.

Jamie holds a degree in Business Administration and regularly participates in industry conferences and workshops.

When not reporting on the latest business developments, Jamie is passionate about mentoring up-and-coming journalists and entrepreneurs to inspire the next generation of business leaders.

You must be logged in to post a comment Login