Diesel prices are jumping every day. The cost for a gallon nearing the highest recorded average of $5.816 back in 2022. Some heating oil businesses are having to change their day-to-day operations because of price hikes.

LONDONDERRY, NH – Home heating oil firms are facing mounting cost pressures as rising crude and diesel prices tied to Middle East tensions squeeze margins and disrupt operations across New England.

The recent spike follows a cold winter that boosted demand for heating oil, leaving both consumers and suppliers exposed to higher costs. Businesses say they are trying to avoid passing those increases on to customers, even as expenses climb sharply.

Advertisement

“We had to lower our prices to be able to get the phones to start ringing more. People are holding off on auto deliveries because the prices are so high, and we can’t blame them on that,” said Andrew Chesney, owner of Southern New Hampshire Energy.

Heating oil providers say volatility in energy markets is complicating planning, as rising crude prices coincide with surging diesel costs needed to fuel delivery fleets.

Chesney said a month ago it cost around $8,000 to fill up one of their delivery trucks with diesel, and today it’s between $12,000 and $15,000. Between filling up four trucks and getting all the necessary oil and fuel, it costs Southern New Hampshire Energy around $50,000 a day.

The cost of filling up a delivery truck jumped thousands over the past month. (Kailey Schuyler / Fox News)

“We’re trying to cut corners where we can to save the people money, but it’s hard to also on our end. We’re not making a huge profit at all,” said Chesney.

Some companies are implementing new policies to manage rising costs. In Massachusetts, Atlantic Oil Company posted a disclaimer on their website saying: “Due to recent and ongoing events in the Middle East, we have currently suspended any deliveries below 125 gallons. We have also added a surcharge of $40 for any orders that take less than the 125 gallon minimum.”

Atlantic Oil company sets limit on oil delivery amid Middle East conflict (Kailey Schuyler / Fox News)

“I have people come in, long-time customers saying, ‘you know, I can’t really pay for this,’ and we try to help them. We say, ‘you know, we could, take some payment now,’ because in the summer you won’t need to pay for your oil, typically,” said Ted Triandafilou, General Manager of Atlantic Oil Company.

Advertisement

Triandafilou said his company is experiencing a similar jump in diesel costs.

“Depending on the size of the truck, we have multiple trucks of different sizes. So it could be over. As of now, it’s over $12,000 to fill the truck up as it may have been, you know, $5,000-$6,000 about a month ago.”

“We really don’t know where it’s going to go from here and prices are increasing and decreasing anywhere from 10 cents to 25 cents a day right now with everything going on in the world,” said Chesney.

Advertisement

“Prices change daily just like gas prices typically do, and a lot of time, I’ve seen … the prices go up in the morning – let’s say, jump 20, 30 cents, crazy numbers – and then slowly during the day, they’ll drop back down, but by the close of the market, they’re back up again,” said Triandafilou. “It’s getting to the point where I don’t even bother displaying the price outside because I’d just be running out and changing it again.”

According to AAA, the average cost for a gallon of diesel on March 20 was $5.15, approaching the record average of $5.80 in 2022.

“The last time we saw diesel prices this high was in 2022 after Russia invaded Ukraine,” said AAA spokesperson Mark Schieldrop. “The current situation is a little bit different because we’re seeing significant impacts on production. We are also seeing all those cargo flows out of the Strait of Hormuz being impacted. So, there are some long-term impacts here.”

Schieldrop said that the record could be broken if the conflict continues. Even if the conflict ended today, the prices wouldn’t drop tomorrow.

Advertisement

“It is true that prices shoot up like a rocket and then tend to drift down like a feather,” said Schieldrop. “It’s going to take a sustained period of time, and many analysts believe that the impact could be lasting for more than a year, even if the conflict ends in the short term.”

Schieldrop says it can be tough to cut corners on gasoline prices to save money.

“We urge folks to try to drive less. That’s a tough bargain for folks who have to drive, but stacking your trips, trying to drive more economically,” said Schieldrop. “Easing up on the gas pedal, drive a little slower, follow the speed limit, and you can increase your fuel economy pretty dramatically.”

Advertisement

For homeowners, demand may ease in the coming months as warmer weather reduces heating needs. But for businesses, the seasonal slowdown brings its own challenges.

Southern New Hampshire Energy heating oil cost seen at $4.89 on March 20. (Kailey Schuyler / Fox News)

“We’re actually coming into our slower season. So everyone’s going to be holding off on getting home heating oil till winter,” said Chesney.

“So it’s going to start slowing down for our employees, and we’re going to go through a struggle ourselves running a business and keeping things going till the prices lower down.”

Companies like Southern New Hampshire Energy are relying on other services, including plumbing, heating and cooling, to offset seasonal declines in fuel demand.

“Support local. We’re a family-owned and operated company. We’re not a corporate company, so we structure our business on family. And we’re just a small business trying to make our way through life right now,” said Chesney.

FTSE 100 DIY retailer Kingfisher saw an uplift in the UK but reported a dip in France and Poland

Felix Armstrong www.cityam.com

10:02, 24 Mar 2026

A B&Q store(Image: Stu Forster/Getty Images)

B&Q and Screwfix owner Kingfisher saw the performance of its UK operations undermined by difficulties abroad, as revenues in France and Poland declined. The FTSE-100 company experienced falling sales across its French Castorama (-2.2 per cent) and Brico Depot (-2.3 per cent) divisions and in Poland (-1.1 per cent), whilst sales climbed by more than three per cent at UK operations B&Q and Somerset-based Screwfix.

Advertisement

The DIY retailer has been grappling with stagnant sales in Poland and France – where Castorama ranks among Kingfisher’s most persistently underperforming operations, according to analysts.

Kingfisher’s share price rose by two per cent during Tuesday’s early trading to 302p, leaving the stock up eight per cent over the past year but down more than 10 per cent since the pandemic-era DIY surge.

The business has concentrated on reducing costs in recent years, having shed £120m in excess expenditure last year, as reported by City AM.

The company recorded an adjusted pre-tax profit of £560m, up six per cent from last year and in line with analysts’ expectations. Total sales across Kingfisher’s operations edged up by only 0.2 per cent.

Advertisement

B&Q and Screwfix will be anticipating the DIY surge that arrives each spring, as rivals suggest the UK’s ageing housing stock maintains demand for home improvement elevated.

However, Kingfisher’s operations, like its competitor Wickes, have struggled in recent years to shift big-ticket purchases such as kitchen renovations, with Britons reducing discretionary spending as they feel the squeeze. The French Castorama brand is bearing the brunt of declining demand for major purchases, with sales for these products falling 4.5 per cent year on year.

Kingfisher attributed B&Q and Screwfix’s robust performance to an emphasis on e-commerce, powerful seasonal sales periods and B&Q’s purchase of several Homebase stores.

Kingfisher pressed ahead with its physical expansion in the UK, with Screwfix launching 32 new sites whilst shutting five.

Advertisement

B&Q opened 10 new outlets – eight of which were transformed from former Homebase properties – and closed three, as Kingfisher recorded 41 net openings across its international brands.

Kingfisher said it aims to drive growth by concentrating on sales to tradespeople because they shop more regularly and spend more than the typical customer.

The company has established dedicated trade zones in each of its outlets and recorded growth in trade sales of five and four per cent at B&Q and Screwfix, and as much as 47 per cent in Castorama Poland.

The firm unveiled a new £300m share buyback programme, having repurchased £1.2bn in shares since 2021.

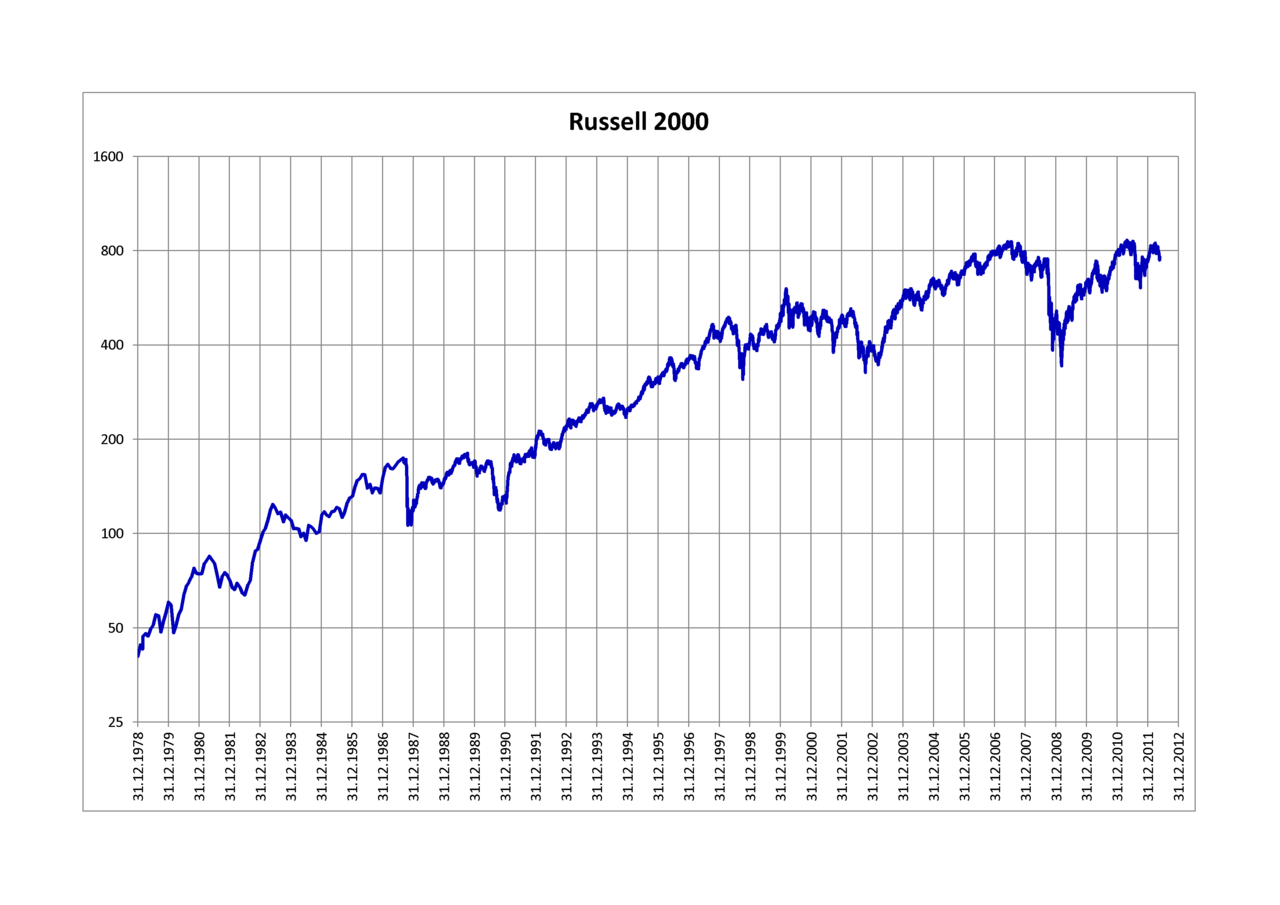

NEW YORK — Russell 2000 futures traded modestly lower in overnight and early Tuesday trading on March 24, 2026, pulling back slightly after a robust session for small-cap stocks the previous day that saw the benchmark index surge more than 2% and futures contracts post solid gains.

Russell 2000 Futures

The front-month E-mini Russell 2000 futures contract for June 2026 settlement hovered around 2,486 to 2,492 in early Asian and European hours, down roughly 0.7% to 0.9% from Monday’s settlement levels near 2,516. The cash Russell 2000 index itself closed Monday at approximately 2,516, up more than 77 points or 3.19% in one of its strongest daily performances in recent weeks.

Monday’s rally reflected continued investor rotation into small-cap names, which have shown relative strength amid expectations of steady Federal Reserve policy and potential fiscal support for domestic-focused companies. The Russell 2000, which tracks about 2,000 smaller U.S. companies, often benefits when investors shift away from mega-cap technology stocks toward more economically sensitive sectors such as regional banks, industrials and consumer discretionary firms.

Analysts noted that small caps entered correction territory earlier in March after a pullback but have since staged a comeback, supported by lower interest rate sensitivity compared with larger growth stocks. The index remains one of the few major U.S. benchmarks in positive territory year-to-date as of late March, though it has lagged the broader market’s record highs in prior months.

Trading volume in E-mini Russell 2000 futures was active Monday, with more than 280,000 contracts changing hands in the June contract alone. Open interest remains elevated as traders position for potential volatility around upcoming economic data, including consumer confidence readings and housing market indicators later this week.

Advertisement

The June 2026 contract, the most actively traded near-term future, opened Monday near 2,510 before climbing as high as 2,574 in intraday action and settling around 2,516. Overnight action Tuesday showed some profit-taking, with the contract dipping toward the 2,480 level at times before stabilizing.

Market participants cited several factors influencing small-cap sentiment. The Federal Reserve’s recent decision to hold rates steady in the 3.5% to 3.75% range, combined with a patient outlook for future cuts, has eased pressure on borrowing costs for smaller businesses. Additionally, expectations around fiscal measures — including potential infrastructure or domestic manufacturing incentives — have fueled optimism for companies heavily weighted in the Russell 2000.

However, headwinds persist. Elevated geopolitical tensions, fluctuating commodity prices and lingering inflation concerns have kept some investors cautious. Small-cap valuations, while still below historical averages relative to large caps in some metrics, have risen during the recent rebound, prompting warnings from chart analysts not to chase the momentum too aggressively.

The Russell 2000 futures contract serves as a key barometer for risk appetite in the equity market. Each point in the E-mini contract is worth $50, making it a popular tool for both hedgers and speculators. Micro E-mini versions, valued at $5 per point, have also seen growing participation from retail traders seeking exposure to small-cap moves with lower capital requirements.

Advertisement

Broader market context Tuesday showed mixed signals. Major indices futures pointed to a subdued open on Wall Street after Monday’s mixed session, with focus shifting to corporate earnings season progress and fresh inflation data. Small caps’ outperformance Monday stood in contrast to more modest moves in the S&P 500 and Nasdaq, underscoring the ongoing “size rotation” theme that has characterized parts of 2026 trading.

Technical levels to watch include support near 2,450–2,465 for the June futures and resistance around 2,550–2,575. A break above recent highs could signal further upside for small caps, while a decisive drop below 2,450 might test recent correction lows.

Economists and strategists remain divided on the sustainability of the small-cap rally. Some argue that improving earnings visibility for domestic-oriented firms, combined with any softening in the U.S. dollar, could provide tailwinds. Others caution that persistent higher-for-longer interest rates and potential slowdowns in consumer spending could weigh on smaller companies with less pricing power or balance sheet strength.

The Russell 2000’s composition — heavy in financials, industrials, health care and consumer stocks — makes it particularly sensitive to domestic economic conditions. Recent strength in regional bank stocks and cyclical names has helped lift the index, even as technology-heavy large caps face scrutiny over high valuations.

Advertisement

As trading progresses Tuesday, investors will monitor any updates from the Federal Reserve or comments from officials that could influence rate expectations. Housing data due later in the week may also offer clues about the health of the broader economy, given small caps’ exposure to real estate and construction-related businesses.

For traders, Russell 2000 futures provide an efficient way to gain or hedge exposure without trading hundreds of individual stocks. The contract’s liquidity and tight spreads make it a staple in institutional portfolios seeking small-cap beta.

Looking ahead, the June 2026 contract will eventually roll to September, with typical roll activity expected in coming weeks. Market participants are already positioning for potential volatility around key events later in the spring, including more Fed meetings and quarterly earnings from small-cap heavy sectors.

Overall, while early Tuesday action showed some consolidation, the underlying narrative for small caps remains one of cautious optimism. The Russell 2000 futures’ performance continues to be closely watched as a gauge of whether the long-awaited small-cap resurgence can gather further momentum in 2026.

Large UK companies that repeatedly delay paying suppliers will face multimillion-pound fines under sweeping new legislation aimed at tackling late payment practices and protecting small businesses.

The reforms, announced by the Department for Business and Trade, will grant enhanced enforcement powers to the Small Business Commissioner, enabling it to investigate poor payment behaviour and penalise persistent offenders.

At the centre of the new rules is a mandatory 60-day payment window for all commercial contracts involving companies with annual revenues above £54 million.

Suppliers will also gain the right to charge statutory interest on overdue invoices at a rate of 8 percentage points above the Bank of England base rate, significantly increasing the cost of late payments for larger firms.

Companies found to be consistently breaching payment standards will be required to publicly disclose their practices in annual reports, including explanations and steps taken to improve.

Advertisement

Business Secretary Peter Kyle said the measures represent the most significant overhaul of payment laws in a generation.

“It is simply unacceptable that so many businesses are forced to shut due to late payments,” he said. “These are the strongest, most robust changes to payment laws in over a generation.”

The government also confirmed it will consult on reforms to retention payments in the construction sector, a long-standing issue where funds are withheld and sometimes lost if a contractor becomes insolvent.

Industry bodies have broadly welcomed the reforms, describing them as a long-overdue intervention in a problem that has plagued SMEs for decades.

Advertisement

Federation of Small Businesses policy chair Tina McKenzie said the measures would help prevent large companies from using smaller suppliers as a source of “free credit”.

However, she cautioned that a 60-day payment window still falls short of best practice, arguing that a 30-day standard should remain the long-term goal.

Late payments are widely seen as one of the biggest barriers to SME growth, affecting cash flow, investment and hiring decisions. Government research suggests that dozens of businesses close each year as a direct result of delayed payments.

Emma Jones, the Small Business Commissioner, said the new powers would help reduce the administrative burden on smaller firms.

Advertisement

“Less time chasing debt means more time focused on growth,” she said, adding that stronger enforcement will help shift behaviour across the market.

The legislation is expected to be introduced when parliamentary time allows, with ministers indicating they will assess the readiness of businesses before mandating contractual changes.

The reforms mark a clear shift towards a more interventionist approach to payment practices, as policymakers seek to rebalance relationships between large corporations and their smaller suppliers.

For big businesses, the message is increasingly clear: late payment is no longer just a commercial issue, it is becoming a regulatory and reputational risk.

Advertisement

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

Gold traded higher on Tuesday amid positive global cues, rising by over Rs 1,200 per 10 grams intraday to hit the day’s high of Rs 1,40,482 on the MCX. Gold’s safe-haven appeal has taken a hit since the onset of the Iran–Israel/US war, contrary to expectations of a bull rally during a time of crisis.

April gold futures slipped below the Rs 1,40,000 mark on Monday on the MCX. The metal has sharply corrected from its all-time peak of Rs 1,93,096, falling by Rs 56,800 or about 29%.

Meanwhile, COMEX gold is hovering around the $4,420.10 per ounce mark. With the war now in its fourth week, spot gold is down 15%, while it has fallen 22% from its January record high, according to a Reuters report.

The rupee’s continued weakness has also failed to support bullion prices, despite the INR hitting new lifetime lows almost daily.

Advertisement

Trivedi said its volatility against the US dollar amplifies moves in MCX gold, and even minor global price shifts translate into sharper domestic swings, increasing intraday and weekly volatility.

Live Events

Commenting on the current trends, Jateen Trivedi, Vice President and Research Analyst at LKP Securities, said gold has witnessed a sharp corrective decline after recent highs, breaking below key short-term supports and entering a volatile phase. The market is now reacting to mixed geopolitical signals — initial escalation between the US–Israel, and Iran followed by unconfirmed de-escalation talks — creating sharp two-way moves, he said. In his view, gold is currently caught between supportive factors such as geopolitical risk premiums and negative factors like de-escalation talks reducing safe-haven demand, along with inflation concerns keeping rate cuts uncertain. “This creates a high-volatility, non-directional environment,” he added.Annualized Actual Volatility (AAV), which measures gold’s volatility on the MCX, has risen 43% over the past five trading sessions.

Trivedi suggested the following near-term strategy for traders based on gold’s current price performance:

1) Key support & resistance

Prices have broken down from the Rs 1,60,000+ zone and are now trading near Rs 1,39,000, indicating a clear short-term downtrend with panic unwinding. Immediate resistance is seen at Rs 1,42,500, while major resistance is at Rs 1,45,000. Immediate support is placed at Rs 1,38,000, with major support at Rs 1,37,500.

The current structure suggests range-bound volatility after the breakdown, rather than an immediate trend reversal, he opined.

Advertisement

2) Momentum indicator

The RSI is near 29, entering oversold territory. This indicates selling exhaustion may emerge, but does not confirm a reversal — it only increases the probability of sharp pullback rallies. Prices have moved to the lower band with expansion, indicating strong volatility and trend acceleration. Such moves are typically followed by short-term mean reversion or sideways consolidation.

3) Technically speaking

EMA 8: Sharp downward slope, acting as immediate resistance

EMA 21: Also turning down, confirming a bearish structure

Prices trading well below both EMAs signal trend weakness and a sell-on-rise bias.

Advertisement

4) MACD

The MACD is in negative territory with a widening histogram, indicating strong bearish momentum. There are no signs of a reversal yet, but oversold conditions may trigger short-covering.

Gold trading strategy

Gold is likely to remain highly volatile within this band as markets react to conflicting geopolitical updates and macro signals.

The expected trading range is Rs 1,37,500 – Rs 1,42,500.

Selling pressure is expected in the Rs 1,42,000 – Rs 1,42,500 range.

Advertisement

Short covering or buying support is likely to emerge at Rs 1,37,500 – Rs 1,38,000.

He suggested that traders adopt a range-bound approach rather than aggressive directional bets, and maintain strict risk management, given headline-driven volatility.

(Disclaimer: The recommendations, suggestions, views and opinions given by the experts are their own and do not represent the views of The Economic Times.)

Pacific Energy has been contracted for work on the second stage of the Kwinana Energy Transformation Hub as the multi-user hydrogen technology testbed project progresses.

Climate tech firm Zevero has secured $7 million in new funding as global demand for robust carbon data and ESG reporting continues to accelerate.

The latest investment, which brings the company’s total funding to $14 million, includes backing from Spiral Capital, Gazelle Capital and Deep 30. It follows a period of rapid expansion, with Zevero reporting 400% year-on-year growth in annual recurring revenue and a doubling of its customer base.

The company has also strengthened its offering through the recent acquisition of sustainability advisory firm Inhabit, enabling it to move beyond emissions tracking into active decarbonisation support for clients.

Zevero’s platform uses artificial intelligence to automate the collection and calculation of emissions data across Scope 1, 2 and 3 — the three key categories used to measure an organisation’s carbon footprint.

By building a continuous, reusable dataset, the platform allows companies to integrate sustainability metrics into core business functions such as product design, procurement and investment planning, rather than treating them as standalone reporting exercises.

Advertisement

Chief executive Shigeo Taniuchi said the shift reflects a broader transformation in how organisations approach sustainability.

“Businesses are increasingly being asked to manage sustainability the way they manage finance,” he said. “Yet many are still treating it as an annual project rather than a continuous system. Our goal is to make climate data actionable, reliable and embedded in decision-making.”

The funding comes amid tightening global regulatory requirements around climate disclosure. Frameworks such as the UK Sustainability Reporting Standards and Japan’s SSBJ standards are pushing companies to apply the same level of rigour to environmental reporting as they do to financial accounts.

This shift is increasing demand for platforms capable of delivering auditable, real-time data, particularly as supply chain transparency and carbon border adjustment mechanisms (CBAM) begin to affect international trade.

Advertisement

George Wade, co-founder and chief commercial officer, said carbon data is rapidly becoming a strategic input rather than a compliance obligation.

“Organisations don’t just need software to collect the data, they need guidance to turn it into something the business can act on,” he said.

The new funding will be used to accelerate product development and support Zevero’s international expansion, particularly across Asia-Pacific and continental Europe, where regulatory and commercial pressures are intensifying.

The company is already working with major organisations including Asahi Group and the Tokyo Metropolitan Government, as well as a growing number of clients in manufacturing, FMCG and consumer sectors.

Advertisement

Investors say the company’s combination of technology and embedded expertise gives it a strong position in a market that is becoming increasingly crowded but also more critical to business operations.

Spiral Capital’s Tomokazu Okuno said the platform addresses one of the most pressing challenges facing organisations today, gaining visibility into emissions and acting on that insight.

The investment highlights a broader trend in climate technology, where funding is increasingly flowing towards solutions that deliver measurable operational value rather than purely compliance-focused tools.

As businesses navigate the transition to a low-carbon economy, the ability to track, verify and act on emissions data is becoming a core capability.

Advertisement

For Zevero, the next phase will be scaling its platform globally while maintaining the balance between automation and expert insight, a combination it believes is essential to turning climate data into meaningful action.

With regulatory demands rising and investor scrutiny intensifying, platforms that can bridge the gap between reporting and real-world impact are likely to play a central role in the next stage of the sustainability transition.

Jamie Young

Jamie is Senior Reporter at Business Matters, bringing over a decade of experience in UK SME business reporting.

Jamie holds a degree in Business Administration and regularly participates in industry conferences and workshops.

When not reporting on the latest business developments, Jamie is passionate about mentoring up-and-coming journalists and entrepreneurs to inspire the next generation of business leaders.

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

Professor Dylan Jones-Evans has undertaken an analysis as part of an alternative strategy for the future of the game in Wales

Welsh rugbyy.(Image: 2025 Getty Images)

Welsh rugby is far more than a sport – it is a national economic asset, but for far too long, the debate around Welsh rugby has been framed as if it were simply about results on the pitch, boardroom rows, or the latest financial crisis at the Welsh Rugby Union.

But the evidence now makes clear that this is much bigger than that, and Welsh rugby is not just a sporting institution; it is one of Wales’s most significant national economic assets.

Recently, Rob Regan, who is currently working on an alternative strategy for Welsh rugby, asked me to examine its economic impact on the nation. While most of the data was available, some had to be extrapolated from other sources because various organisations here in Wales had not conducted the necessary research. Nevertheless, the overall results are striking, and for the first time, we now possess information on this important subject.

The available data indicate that Welsh rugby provides a direct annual economic impact of at least £225m and up to £250m through the professional game and matchday activity alone. When a cautious estimate for the grassroots game is included, this amount increases to between £240m and £270m. Furthermore, if the broader social and well-being benefits of the community game are considered, the total national value of Welsh rugby could plausibly range from £370m to £430m annually.

That matters because it shifts the conversation, as it is no longer solely about whether Welsh rugby is managed well enough to win matches, but about whether a nationally significant asset is being adequately protected.

At the core of the direct economic case is the professional game. The Welsh Rugby Union (WRU) had a turnover of £106.1m in 2024-25, while the broader regional professional game is estimated to add another £40m to £60m annually. Together, this creates a direct professional rugby economy of approximately £150 million each year.

But the true significance of Welsh rugby goes far beyond the WRU’s balance sheet. International matches at the Principality Stadium generate one of Wales’s strongest visitor economies, with each major home international contributing approximately £10.5m to £11m in matchday economic impact at current prices. This results in an annual visitor economy of about £63m to £66m from six major fixtures. Of course, this does not include income from other events hosted at the stadium, such as concerts.

Crucially, much of this is new money entering Wales, with about 35% of visitors coming from outside Wales, and their spending accounts for around 70% of total economic output. It is also worth noting that the WRU is apparently holding a more recent report on the stadium’s impact from last year and has yet to publish it, so this estimate could be revised once it finally does.

Advertisement

That is why the stadium is so important, as the Principality is not just a venue but a key gateway for outside money into the Welsh economy. Data indicates it supports around one in ten tourism jobs in Cardiff and also sustains hospitality, retail, and broader city-centre activity. Building a replacement stadium to similar standards today would probably cost close to or over £1 billion, making it effectively irreplaceable.

Then there is the issue that few public discussions have properly addressed, which is Welsh rugby’s “hidden” asset base. The WRU’s share of the retained commercial interest in Six Nations Rugby Limited is estimated to be worth between £500m and £570m.

That value does not appear transparently in the way most people understand a balance sheet, but it is real in economic terms. It originates from the CVC deal in 2021, which implied a valuation of about £2.55bn for Six Nations Rugby, with later estimates suggesting the competition might now be worth between £3.5bn and £4bn. On that basis, the WRU’s effective economic interest is substantial.

The Wales rugby brand is valued at around £109m in 2023, but that figure should probably now be seen as a ceiling rather than a current valuation, due to Wales’s decline on the field over the past three years. This also indicates that the worth of Welsh rugby’s commercial assets is not assured but relies on maintaining competitiveness, public trust, and a healthy development pipeline.

Advertisement

And that is where the findings become most uncomfortable, as despite all the large numbers associated with Welsh rugby, community rugby remains underfunded. The grassroots game is described as the foundation upon which the professional game, the national team, the brand, and the matchday economy all ultimately depend.

Yet the WRU directly allocates only £3.3m of its own funds to community clubs and affiliated organisations, around 3% of annual revenue. Even when the wider community rugby department is included, spending remains modest compared with the economic and social value grassroots rugby appears to generate.

That imbalance lies at the heart of the argument, and the report emphasises that Welsh rugby’s governance issues are inseparable from its economic challenges. They are one and the same problem. If the community game continues to weaken, the pathway becomes narrower. A narrower pathway leads to poorer national performance, which in turn results in declining audiences, weakened brand value, and reduced commercial worth of Welsh rugby’s stake in the Six Nations.

Hence, the key conclusion is unavoidable. Welsh rugby is not just a sport facing significant difficulties, but a vital national asset under pressure, with its economic value encompassing the visitor economy, regional development, the community club network, and Wales’s international profile. Once these assets diminish, many of them cannot be easily restored.

Advertisement

The question, therefore, is no longer whether Welsh rugby has economic significance, as the evidence shows it does, but whether the current structures and management can protect something so vital to Wales before further damage occurs.

“The Middle East war continues to trigger a broad macroeconomic shock across global markets, forcing investors to reprice inflation, rates, growth, and liquidity conditions simultaneously,” analysts at Saxo Bank said. “Gold is being sold because it remains one of the few liquid assets still showing gains over the past year.”

![BITCOIN: 24 HOURS LEFT!!!! [I WENT LONG]](https://wordupnews.com/wp-content/uploads/2026/03/1774346399_maxresdefault-80x80.jpg)

You must be logged in to post a comment Login