Business

Making the case for cereal as healthy, clean and functional

Earnings call transcript: Camden Property Trust beats Q1 2026 earnings estimates

NEW YORK — Procter & Gamble Co. (NYSE: PG) remains a cornerstone holding for income-focused investors in 2026, offering consistent dividend growth and defensive qualities in an uncertain economy, but slower organic sales growth and elevated valuations are prompting some analysts to recommend trimming positions or waiting for a better entry point. With shares trading near all-time highs, the question of whether to buy or sell Procter & Gamble stock this year depends heavily on an investor’s time horizon, risk tolerance and outlook for consumer staples giants.

P&G has delivered reliable performance through economic cycles thanks to its portfolio of essential everyday brands including Tide, Pampers, Gillette, Bounty, Crest and Head & Shoulders. The company has increased its dividend for 69 consecutive years, making it a Dividend King with a current yield around 2.4%. In the first half of 2026, PG shares have returned roughly 11%, slightly lagging the broader S&P 500 but providing stability during periods of market volatility.

First-quarter 2026 results showed organic sales growth of 3%, in line with company guidance but below some investor expectations. Pricing power helped offset volume softness in certain categories, particularly in North America where consumers remain price-sensitive. CEO Jon Moeller highlighted continued strength in health care and beauty segments while noting challenges in fabric and home care due to competitive pressures and retailer inventory management.

Analysts at firms like Goldman Sachs and Morgan Stanley maintain mostly positive outlooks. Goldman rates PG as Buy with a $178 target, citing its unmatched brand strength and ability to navigate inflation and supply chain issues. Morgan Stanley holds a Hold rating, arguing that while the company is a high-quality business, current valuations leave limited upside in the near term. The consensus price target sits around $165–$170, suggesting modest single-digit upside from current levels.

Strong Fundamentals Support Long-Term Ownership

Procter & Gamble benefits from several enduring advantages. Its diversified global portfolio spans beauty, grooming, health care, fabric care and baby care, reducing reliance on any single category. International markets, particularly emerging economies, continue to offer growth potential as rising middle classes adopt premium branded products. The company’s focus on innovation — such as new sustainability initiatives and premium product lines — helps maintain pricing power and customer loyalty.

P&G’s balance sheet remains fortress-like with strong free cash flow generation supporting both dividends and share repurchases. The company returned more than $15 billion to shareholders in the trailing 12 months through dividends and buybacks. This capital return discipline appeals to retirement accounts and conservative investors seeking predictable income streams.

Defensive characteristics also shine during economic uncertainty. Consumer staples demand remains relatively stable even in slowdowns, as people continue purchasing toiletries, detergents and diapers. This resilience has helped PG outperform during previous recessions and periods of high inflation.

Challenges and Reasons for Caution

Despite its strengths, several factors give pause to growth-oriented investors. Organic sales growth has moderated to the low-to-mid single digits after stronger post-pandemic gains. Intense competition from private-label brands and nimble challengers in categories like oral care and personal grooming has pressured market share in some segments. Rising input costs and the need for continued marketing investment have also compressed margins at times.

Valuation remains a key concern. PG trades at a forward price-to-earnings multiple in the mid-20s, a premium to historical averages and many consumer staples peers. This leaves limited margin of safety if economic conditions deteriorate or if the company misses earnings expectations. Some analysts argue that slower long-term growth prospects — projected around 4-5% annually — do not fully justify the current multiple.

Another risk involves changing consumer preferences toward natural and sustainable products. While P&G has invested heavily in this area, execution challenges and higher costs could weigh on results. Regulatory scrutiny on pricing, environmental impact and advertising practices also represents a background risk for large consumer goods companies.

Buy Case: Stability and Income in Uncertain Times

Investors considering buying PG stock in 2026 point to its role as a defensive anchor in diversified portfolios. In an environment of geopolitical tensions, potential recession risks and volatile equity markets, P&G’s predictable cash flows and growing dividend provide ballast. The stock has historically performed well during periods of market stress, offering downside protection while still participating in broader rallies.

Long-term compounding through reinvested dividends has created substantial wealth for patient shareholders. Those with a 5-10 year horizon may view current levels as reasonable for accumulating a high-quality business with global scale and pricing power. Upcoming product launches in premium segments and continued emerging market expansion could drive incremental growth.

Sell Case: Limited Upside and Better Opportunities Elsewhere

Those recommending selling or underweighting PG argue that better risk-reward opportunities exist elsewhere. Technology, healthcare and select industrial stocks offer higher growth potential at comparable or lower valuations. With PG trading at a premium, any slowdown in consumer spending or margin pressure could lead to multiple contraction and disappointing returns.

Investors who bought at lower levels in previous years may consider trimming positions to lock in gains and reallocate capital toward faster-growing sectors. Short-term traders might wait for a pullback closer to the 200-day moving average before re-entering.

Analyst Consensus and Market Sentiment

Wall Street’s overall stance leans Hold to Buy. The average rating from 18 analysts tracked by major platforms is Moderate Buy, with price targets implying limited but positive upside. Institutional ownership remains high, reflecting confidence in the company’s long-term prospects. However, activist investor attention has been minimal, suggesting the market views P&G as a steady compounder rather than a turnaround story.

Technical analysis shows PG in a long-term uptrend but approaching resistance levels. A break above recent highs could signal continued momentum, while failure to hold key support might trigger profit-taking.

Investment Considerations for 2026

For dividend growth investors, Procter & Gamble remains attractive. The company’s commitment to annual dividend increases, combined with a reasonable payout ratio, supports continued income growth. Retirement portfolios and income funds often include PG as a core holding for stability.

Growth investors may find the stock less compelling unless valuations compress or the company demonstrates accelerated top-line growth. Those building diversified portfolios might consider pairing PG with higher-growth consumer names or using it as a defensive satellite position.

Risk management remains important. While P&G is a high-quality business, no stock is immune to market downturns or company-specific challenges. Position sizing, regular monitoring of fundamentals and maintaining a long-term perspective are key to successful investment in consumer staples.

Final Outlook

Procter & Gamble stock in 2026 offers a classic choice between stability and growth potential. For conservative investors seeking reliable dividends and downside protection, PG deserves consideration as a core holding. For those chasing higher returns in a dynamic market, other sectors may provide more compelling opportunities.

The company’s strong brand portfolio, global reach and disciplined capital allocation support a positive long-term view. However, elevated valuations and moderating growth rates suggest patience may be rewarded for new buyers. Whether you ultimately decide to buy, hold or sell Procter & Gamble stock should align with your individual financial goals, risk tolerance and portfolio construction strategy.

As always, investors should conduct thorough due diligence and consider consulting a financial advisor before making investment decisions. The consumer staples sector will continue playing a vital role in portfolios, and Procter & Gamble remains one of its most respected leaders.

Business

Earnings call transcript: CubeSmart Q1 2026 reports earnings beat with cautious market response

Earnings call transcript: CubeSmart Q1 2026 reports earnings beat with cautious market response

Two new passive mutual funds are launching this week to expand fund houses’ offerings. DSP Nifty FMCG ETF opens May 12-14 with a Rs 5,000 minimum, while HDFC Gold Silver Passive FoF opens May 15-29 with a Rs 100 minimum. Investors should choose based on their risk appetite and goals.

The Investment Doctor is a financial writer, highlighting European small-caps with a 5-7 year investment horizon. He strongly believes a portfolio should consist of a mixture of dividend and growth stocks.

He is the leader of the investment group European Small Cap Ideas which offers exclusive access to actionable research on appealing Europe-focused investment opportunities not found elsewhere. The a focus is on high-quality ideas in the small-cap space, with emphasis on capital gains and dividend income for continuous cash flow. Features include: two model portfolios – the European Small Cap Ideas portfolio and the European REIT Portfolio, weekly updates, educational content to learn more about the European investing opportunities, and an active chat room to discuss the latest developments of the portfolio holdings. Learn more.

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I currently have no position but am interested in the common stock and preferred stock although it is unlikely I will establish a long position within the next few weeks.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Brad Thomas has over 30 years of real estate investing experience and has acquired, developed, or brokered over $1B in commercial real estate transactions. He has been featured in Barron’s, Bloomberg, Fox Business, and many other media outlets. He’s the author of four books, including the latest, REITs For Dummies. Brad, along with HOYA Capital, lead the investing group iREIT®+HOYA Capital. The service covers REITs, BDCs, MLPs, Preferreds, and other income-oriented alternatives. The team of analysts has a combined 100+ years of experience and includes a former hedge fund manager, due diligence officer, portfolio manager, PhD, military veteran, and advisor to a former U.S. President. Note: Brad is also related to Nicholas Thomas who contributes to Seeking Alpha. Learn more

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Earnings call transcript: Rubis Q1 2026 sees robust growth, stock dips

Earnings call transcript: IPC’s Q1 2026 results show solid performance

Equity mutual funds saw a strong performance last week, with over 8% returns for the category. Among the top performers, international funds like Mirae Asset Global X Artificial Intelligence & Technology ETF FoF led the pack with an 8.49% gain.

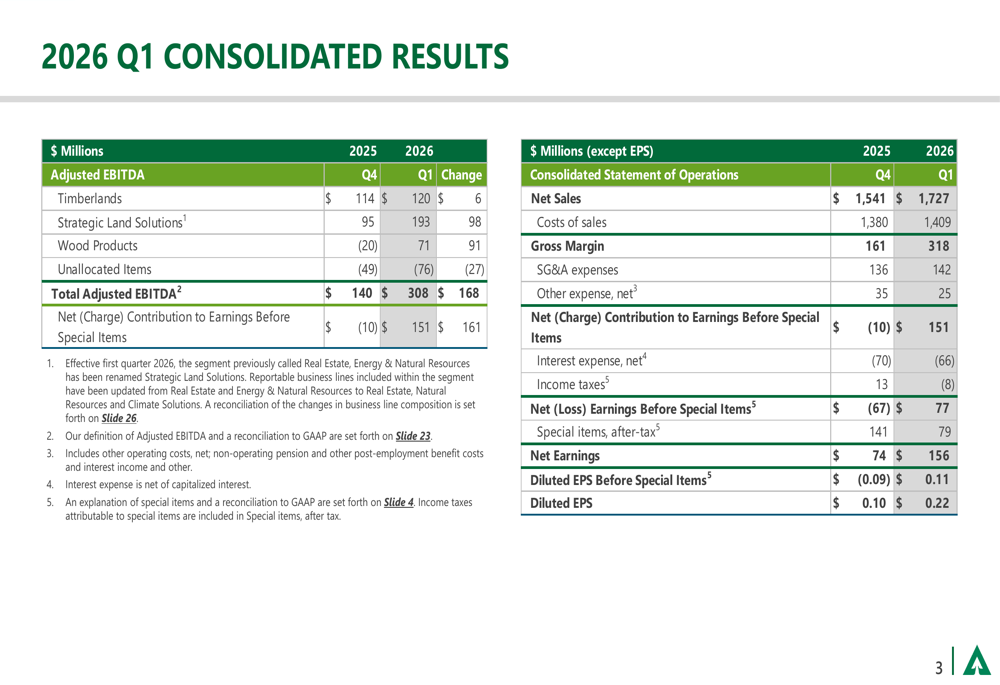

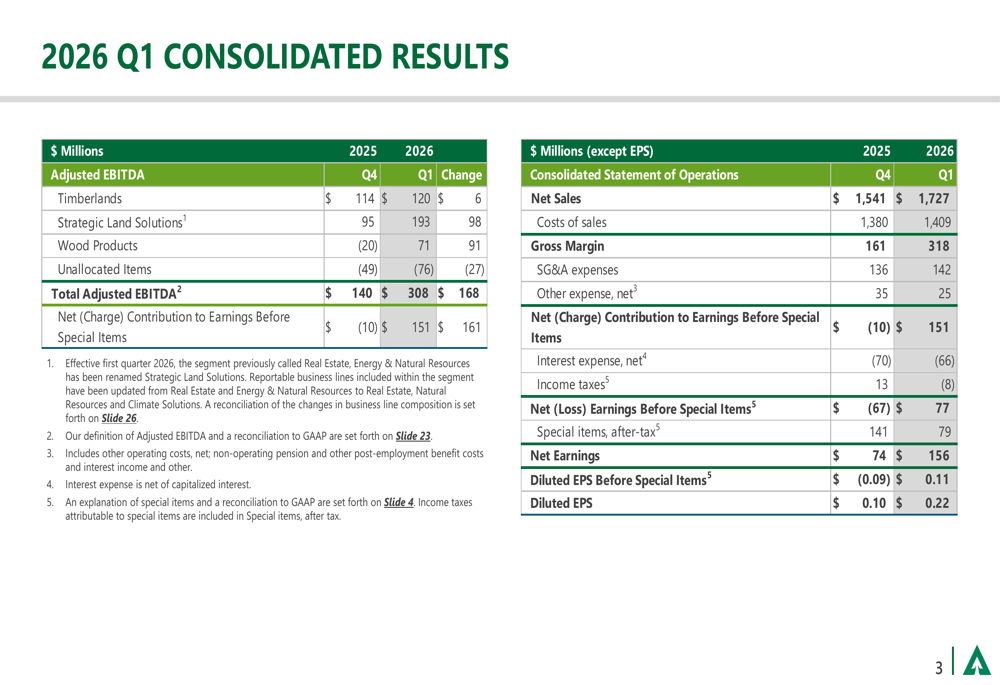

Weyerhaeuser Q1 2026 slides: EBITDA surges on climate deal

BeInCrypto Institutional Research: 15 Fintechs Bridging Fiat and Digital Assets

Hugh Jackman’s Wild New Murder Mystery Is the Surprise Box Office Hit of the Year

Michael Saylor DROPS BOMBSHELL on Bitcoin Holders!! (What Now?)

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World2 days ago

Crypto World2 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

NewsBeat7 days ago

NewsBeat7 days agoChannel 5 – All Creatures Great and Small series 7 new post

-

Crypto World3 days ago

Crypto World3 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Marianne Dress

-

Tech6 days ago

Tech6 days agoImage AI models now drive app growth, beating chatbot upgrades

-

NewsBeat3 days ago

NewsBeat3 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Business1 day ago

Business1 day agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Politics1 day ago

Politics1 day agoPolitics Home Article | Starmer Enters The Danger Zone

-

Crypto World7 days ago

Crypto World7 days agoBlackRock Buys $284M In Bitcoin On May 1 As The Best Crypto To Invest In For 2026 Sits Below A Pending Binance Listing

-

Entertainment6 days ago

Entertainment6 days agoOlivia Wilde Reacts To Viral ‘Corpse’ Comparison

-

Sports6 days ago

Sports6 days agoInter Milan Win Serie A Title After Victory Over Parma

-

Sports7 days ago

Sports7 days agoKofi Kingston and Xavier Woods reportedly released by WWE along with others

-

Business7 days ago

Business7 days agoCan LeBron James Lead LA Past OKC Without Injured Luka Doncic?

-

Sports6 days ago

Sports6 days agoEvery word of Arne Slot’s heated rant after Manchester United win vs Liverpool

-

Crypto World5 days ago

Crypto World5 days agoUAE Free Zone Deploys Blockchain IDs to Verify Registered Firms

-

Entertainment7 days ago

Entertainment7 days agoOther Bennet Sister Love Triangle Cast: Ella Bruccoleri, Donal Finn

-

Sports7 days ago

Sports7 days agoJoel Embiid urges Sixers fans not to sell playoff tickets to Knicks fans

-

Sports7 days ago

Sports7 days agoLa Liga: Vinicius Jr scores twice as Real Madrid win to keep Barcelona waiting for title

-

Entertainment7 days ago

Jennifer Lawrence’s Mary Jane Sneakers Are Spring’s It-Girl Shoe

-

Sports6 days ago

Sports6 days ago2026 NHL playoff picks: Second-round predictions, series odds, Stanley Cup bracket

You must be logged in to post a comment Login