Business

Nebius Stock Surges. It Got This Huge New AI Deal With Meta.

Russia says US should abandon ’language of ultimatums’ on Iran

I’m a full-time investor with a strong focus on the tech sector. I graduated with a Bachelor of Commerce Degree with Distinction, major in Finance. I’m also a proud lifetime member of the Beta Gamma Sigma International Business Honor Society. My core values are: Excellence, Integrity, Transparency, & Respect. I always, to the best of my ability, hold true to these values which I believe are key for long-term success. I would like to invite all of my readers to leave their constructive criticism and feedback in the comments section so that I can further enhance the quality of my work moving forward. Thank you and God Bless America!

Analyst’s Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Genesis Energy: Cash Flow Growth Likely To Slow Down Going Forward (Rating Downgrade)

RIO DE JANEIRO — Brazilian soccer star Neymar Jr. faces a potential lengthy suspension and widespread backlash after making a sexist remark about referee Sávio Pereira Sampaio following Santos’ 2-0 victory over Remo in the Brazilian league on Saturday, April 3, 2026.

In post-match comments, the 34-year-old forward, who returned to boyhood club Santos after stints in Europe and Saudi Arabia, criticized the official’s decisions and reportedly said the referee “woke up on his period” or used a colloquial Brazilian slang phrase equivalent to suggesting the referee was menstruating and therefore officiated poorly. The comment, widely interpreted as misogynistic for linking emotional instability or bad judgment to women’s menstrual cycles, quickly sparked outrage on social media and among women’s rights advocates, players and officials.

Neymar expressed frustration during the interview, complaining that he was fouled unnecessarily from behind late in the match and that communication with the referee was lacking. “It’s the same every time. It’s unfair,” he said before adding the controversial remark about the referee’s supposed “period.” The phrase in Brazilian Portuguese slang carries strong sexist undertones and has been condemned as discriminatory.

The Brazilian Football Confederation’s disciplinary body, under the Código Brasileiro de Justiça Desportiva, is investigating the incident. Precedents suggest Neymar could face a ban of up to 12 matches, which would sideline him for a significant portion of the domestic season and potentially derail any remaining hopes of selection for the 2026 FIFA World Cup in the United States, Mexico and Canada.

Brazil coach Carlo Ancelotti has already expressed reservations about Neymar’s fitness and consistency. The former Real Madrid and Everton manager has emphasized that only fully fit players will be considered for the Seleção squad, and Neymar has not featured in recent call-ups for friendlies. Reports indicate Ancelotti views the squad as largely defined, with younger, more reliable attackers prioritized amid Neymar’s recurring injury issues that have limited him to just five appearances for Santos in 2026 so far.

The controversy adds another layer to Neymar’s turbulent recent years. Once hailed as the heir to Pelé in Brazilian soccer, the five-time Ballon d’Or nominee has battled serious knee and ankle injuries since 2023, spending more than 600 days on the sidelines at times. His return to Santos was seen as a chance for redemption and a final push toward the 2026 World Cup, but fitness doubts and off-field incidents continue to cloud his prospects.

Women’s groups and female referees in Brazil reacted swiftly. The Brazilian Association of Women’s Soccer and several prominent players denounced the remark as reinforcing harmful stereotypes. Social media platforms filled with calls for accountability, with hashtags highlighting misogyny in Brazilian football trending within hours. Some commentators noted that similar sexist comments by other players, such as a defender from Red Bull Bragantino who received a 12-match ban last month, set a clear precedent for punishment.

Neymar’s representatives have not issued a formal apology as of Sunday, though sources close to the player suggested he may address the matter in coming days. In past controversies, Neymar has sometimes downplayed remarks as “heat of the moment” or attempted to clarify intent, but the explicit nature of this comment has left little room for deflection.

The incident occurred after Santos secured the win, with Neymar involved in the buildup play despite receiving a yellow card late in the match for dissent or a foul. The referee’s decisions became a flashpoint for Neymar, who has a history of clashing with officials throughout his career, including tunnel incidents and on-field disputes.

Brazilian media outlets like Chosun Biz, GOAL and Marca reported extensively on the backlash, with some labeling it a “disgraceful” moment that could define the twilight of Neymar’s international career. Former players and pundits weighed in, with many urging the Brazilian Football Confederation to act decisively to protect the sport’s image.

The timing is particularly damaging. With the 2026 World Cup less than three months away, Brazil sits among the favorites but has shown vulnerability in recent friendlies. Ancelotti has favored a squad built around fit, in-form players rather than relying on past glory. Neymar’s limited playing time and this latest off-field issue make a recall increasingly unlikely, even if he avoids the maximum suspension.

If handed a lengthy ban, Neymar would miss key matches for Santos, further hampering his match sharpness and physical condition. Brazilian league rules and potential appeals could stretch the process, but a suspension starting in the coming weeks would effectively end his domestic season early.

Neymar has 79 goals in 128 appearances for Brazil, making him one of the nation’s all-time leading scorers behind only Pelé. He played a key role in the 2014 and 2018 World Cups but has yet to lift the trophy, with Brazil exiting in the quarterfinals in 2018 and suffering early disappointment in 2022 under different circumstances.

The forward has spoken in the past about his desire to compete in 2026 and potentially retire afterward, but persistent fitness struggles and now this disciplinary cloud have dimmed those prospects. Supporters point to flashes of brilliance in recent Santos appearances, including assists and creative play, as evidence he could still contribute if selected.

Critics, however, argue that Neymar’s off-field behavior and injury history make him a liability for a high-stakes tournament. Ancelotti has been frank in assessments, noting the need for reliability in a squad preparing for the expanded 48-team World Cup.

FIFA and CONMEBOL have not commented directly, but the case falls under national disciplinary procedures unless it escalates to international level. The Brazilian Football Confederation faces pressure to demonstrate zero tolerance for discriminatory language, aligning with global campaigns against sexism and discrimination in soccer.

Women’s soccer advocates in Brazil have used the moment to call for broader education and cultural change within the men’s game. Referees’ unions echoed concerns that such remarks undermine officials’ authority and create a hostile environment, particularly when directed at male referees using misogynistic tropes.

As the investigation proceeds, Neymar remains with Santos, where he serves as captain and a symbolic figure for the club. Club officials have stayed largely silent, focusing on on-field matters while the disciplinary process unfolds.

The episode highlights ongoing challenges in Brazilian football regarding player conduct, respect for officials and gender sensitivity. Previous high-profile cases have resulted in bans and fines, setting expectations for a firm response.

For Neymar, the stakes extend beyond one match or season. At 34, with a history of dazzling talent tempered by injuries and controversies, this latest incident risks cementing a narrative of unfulfilled potential on the international stage. Brazil’s 2026 campaign, hosted in part on familiar American soil for many Brazilian fans, represents what could be his final realistic shot at World Cup glory.

Whether Neymar issues a meaningful apology, receives a reduced sanction or faces the full weight of disciplinary action remains to be seen. In the meantime, the football world watches as one of the game’s most gifted players navigates yet another self-inflicted obstacle on the road to what was once considered his destiny.

Analysts suggest that even a shorter ban could disrupt momentum at Santos and further erode trust from national team selectors. With Ancelotti prioritizing squad harmony and fitness, the path back to the Seleção appears narrower than ever.

As April 2026 progresses, Brazilian soccer fans and global observers await the outcome of the disciplinary hearing. The remark has already damaged Neymar’s public image, reigniting debates about accountability for star athletes and the need for cultural shifts in how players express frustration.

Neymar’s talent remains undeniable when fit, but consistency and conduct have become defining questions as the World Cup draws near. For a player who once carried the hopes of a nation, this controversy adds a painful chapter to a career marked by brilliance, injury and now, potentially, self-sabotage.

Fredrik Arnold is a former quality service analyst. He is now reporting investment ideas with a primary focus on dividend yields by utilizing free cash flow and one-year total returns as trading indicators. He is the leader of the investing group The Dividend Dog Catcher, where he shares a minimum of one new dividend stock idea per week with focus on yield or extraordinary financial circumstances. All ideas are archived and available after weekly announcement. Learn more.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of T either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Business

Is McDonald’s Open on Easter Sunday 2026? Most US Locations Serving Burgers with Varying Hours

McDonald’s restaurants across the United States will largely remain open on Easter Sunday, April 5, 2026, providing Big Macs, fries and drive-thru service for families and travelers despite the major Christian holiday.

Unlike some retailers and restaurants that close entirely for Easter observances, the fast-food giant maintains a flexible approach. Hours vary by location based on local demand, staffing and franchisee decisions, McDonald’s has confirmed in statements to multiple outlets.

A company spokesperson told USA TODAY that “hours vary by location, but most McDonald’s in the U.S. are open on holidays.” This policy has held consistent in recent years, allowing the chain to serve customers seeking quick meals amid Easter brunches, egg hunts and family gatherings.

Easter 2026 falls on Sunday, April 5, commemorating the resurrection of Jesus Christ. While many Americans attend church services or enjoy home-cooked feasts, others look for convenient dining options. McDonald’s positions itself as a reliable choice, with its widespread network of company-operated and franchised locations operating in nearly every community.

Most locations are expected to follow typical Sunday hours, often opening as early as 5 a.m. or 6 a.m. for breakfast and closing around 10 p.m. or 11 p.m., though some drive-thrus may extend later. High-traffic sites near highways, airports and tourist areas tend to maintain extended availability, while neighborhood spots might adjust for anticipated lighter morning crowds due to religious services.

In previous Easter observances, including 2025, the majority of U.S. McDonald’s stayed open with only minor variations. Media reports from TODAY.com, USA TODAY and regional outlets confirm the chain ranks among fast-food options likely to welcome patrons on April 5, 2026. Some locations could see reduced hours or rare closures tied to low expected volume rather than a corporate directive.

For context, competitors show mixed patterns. Chipotle Mexican Grill plans full closures on Easter Sunday 2026, while Wendy’s, Taco Bell, Burger King and Dairy Queen generally remain open with potential adjustments. Starbucks and Dunkin’ also expect strong availability. In contrast, major retailers like Costco, Target and some grocers will shutter for the day, though Walmart and Walgreens plan to operate.

Customers seeking certainty should verify details directly:

- Use the McDonald’s mobile app to locate nearby stores and view real-time hours.

- Visit the official website at mcdonalds.com and access the restaurant locator by entering a ZIP code or city.

- Call the specific location, as franchisees have autonomy over operations.

The app supports mobile ordering, contactless payments and access to deals, including current value menu promotions and any limited-time offers that may appeal during the holiday weekend. McDonald’s Rewards members can earn points toward future visits, with no major Easter-specific promotions announced as of April 5.

McDonald’s operates more than 13,000 locations in the United States, a mix of corporate and independent franchise sites. Franchisees often tailor hours to community needs, meaning a store inside a shopping mall or travel plaza might align with venue schedules, while standalone outlets follow local patterns.

Industry observers note that fast-food chains like McDonald’s benefit from holiday demand as families seek breaks from cooking or quick stops during travel. The company has emphasized accessibility, keeping most doors open even on other observances such as Memorial Day or Labor Day. Widespread closures typically occur only on Thanksgiving and Christmas.

Weather forecasts for Easter Sunday 2026 suggest spring conditions across much of the country, potentially increasing drive-thru traffic at locations with outdoor features or in warmer regions like the South and West Coast. Northern states might experience slower early hours aligned with church attendance.

Travelers receive particular value from McDonald’s strategy. Locations at major airports, highway rest areas and gas stations frequently extend hours to accommodate passengers and road trippers, even on holidays. However, confirmation via the app or website remains essential, as transportation hubs occasionally modify operations.

The chain has navigated recent challenges, including labor shortages, inflation pressures and evolving consumer preferences toward healthier or plant-based options. Yet McDonald’s continues innovating with menu updates, digital enhancements and value deals that resonate during family-oriented weekends like Easter.

Dietary accommodations include breakfast all day at participating sites, customizable orders and alternatives such as McPlant or salad options at select locations. Mobile ordering helps minimize wait times during potentially busier periods when other dining choices are limited.

Parents coordinating Easter activities may find a local McDonald’s a practical refueling point after morning services or before afternoon gatherings. The chain’s presence in urban centers, suburbs and rural areas makes it one of the most accessible options nationwide.

While McDonald’s does not publish precise nationwide holiday statistics, surveys and anecdotal evidence from past years indicate that well over 90% of locations typically serve customers on Easter Sunday. Individual exceptions usually reflect franchisee choices tied to staffing or community dynamics rather than policy.

Crew members, as employees are known, often staff holiday shifts, with some locations offering incentives. The company has not released specific 2026 staffing details, focusing instead on delivering consistent service as the “golden arches” symbol of convenience.

For those preferring to stay home, the McDonald’s app enables delivery through partners like DoorDash or Uber Eats, subject to local participation and third-party availability. Gift cards and at-home menu-inspired products offer additional flexibility.

As Easter unfolds, McDonald’s aims to balance respect for the holiday’s significance with its mission to feed communities. With billions of annual visits globally, the chain plays a quiet but steady role in both everyday routines and special occasions.

In bustling cities like New York, Los Angeles and Chicago, downtown and 24-hour locations often maintain robust activity. Smaller towns or rural outlets might adopt more conservative hours, again highlighting the need to check ahead.

McDonald’s decentralized model empowers local operators to respond to real-time conditions, a strategy that has sustained relevance amid shifting retail and dining landscapes. This flexibility contrasts with chains enforcing uniform closures.

Looking forward, McDonald’s 2026 holiday guidance lists Easter as open with varying hours, consistent with other non-major dates. Only Thanksgiving and Christmas typically trigger broad reductions or shutdowns.

Families blending traditions with convenience can incorporate a McDonald’s stop seamlessly. Whether grabbing breakfast sandwiches post-church or Happy Meals for children after egg hunts, the chain stands prepared at thousands of sites.

In conclusion, yes — McDonald’s is open today, Easter Sunday, April 5, 2026, at the vast majority of U.S. locations. Hours are not standardized nationwide, so consulting the official app or website for your nearest restaurant ensures an accurate plan and prevents any holiday inconvenience.

The fast-food leader continues prioritizing customer access while operating within the realities of a vast franchise system on a day filled with religious and familial meaning for millions of Americans.

Business

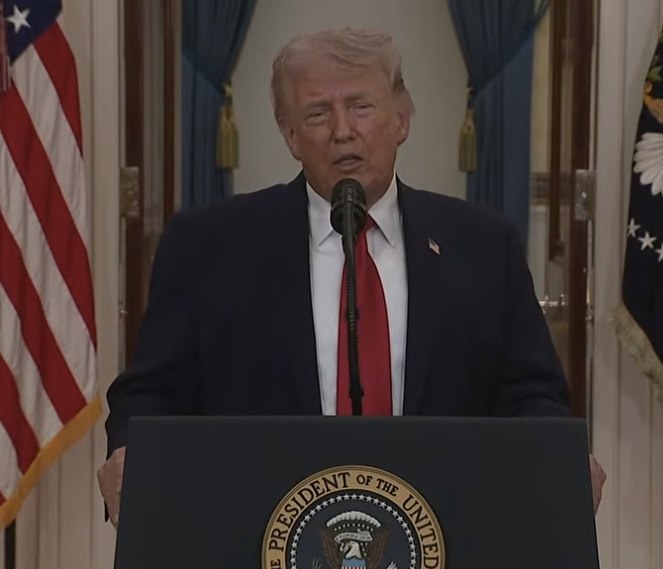

Trump Threatens Strikes on Iranian Power Plants and Bridges in Expletive-Laden Truth Social Post

WASHINGTON — President Donald Trump issued a blunt warning to Iran on Easter Sunday, April 5, 2026, declaring that Tuesday would bring unprecedented attacks on the country’s power plants and bridges unless Tehran opens the Strait of Hormuz.

In a Truth Social post at 12:03 p.m. EDT, Trump wrote: “Tuesday will be Power Plant Day, and Bridge Day, all wrapped up in one, in Iran. There will be nothing like it!!! Open the Fuckin’ Strait, you crazy bastards, or you’ll be living in Hell – JUST WATCH! Praise be to Allah. President DONALD J. TRUMP.” The message quickly drew thousands of reactions, with more than 39,000 likes and 9,000 re-truths within hours.

The post escalates longstanding tensions over the strategic waterway, a critical chokepoint through which about one-fifth of global oil passes. Disruptions there have contributed to recent fuel shortages and price spikes in the United States and worldwide, including diesel shortages affecting Australian farmers and broader economic ripple effects.

White House officials did not immediately comment on the president’s language or whether the post signals imminent military action. National Security Council spokespeople referred questions to the Pentagon, which also declined immediate comment on operational matters.

The blunt rhetoric comes amid ongoing conflict involving Iran that has already disrupted global energy markets. Earlier reports indicated U.S. concerns over Iran’s role in regional instability and its impact on shipping lanes. Trump has repeatedly criticized previous administrations for what he calls weak policies toward Tehran.

The timing of the message — posted on Easter Sunday — drew mixed reactions. Some supporters viewed it as a strong show of resolve from the president, while critics questioned the tone and choice of day for such a stark warning. Trump had issued a separate Easter message earlier in the weekend emphasizing faith and hope.

The Strait of Hormuz reference ties directly to the current fuel supply challenges. Australia, heavily reliant on imported refined fuels, has faced diesel shortages at hundreds of service stations, with national reserves hovering around 29-39 days for key products. Energy experts link part of the crunch to disruptions in Middle Eastern supply routes and Asian refining capacity affected by regional tensions.

Trump’s post echoes his long-standing “maximum pressure” approach toward Iran, which he first pursued during his initial term. He has accused Iran of destabilizing the region through proxy groups and nuclear ambitions. Tehran has denied seeking nuclear weapons and blamed U.S. sanctions for economic hardship.

Military analysts noted that targeting power plants and bridges would represent a significant escalation, potentially affecting civilian infrastructure and energy production. Iran’s power grid and transportation network could face severe disruption, though experts caution that such strikes carry risks of broader regional conflict and retaliation.

The colorful language — including an expletive and the closing “Praise be to Allah” — is characteristic of Trump’s unfiltered social media style. He frequently uses Truth Social to bypass traditional media and speak directly to supporters. The platform, which he launched after being banned from major sites following the Jan. 6, 2021, Capitol riot, remains his primary online outlet.

Reactions poured in quickly across platforms. Supporters praised the tough stance, with some calling it necessary deterrence against Iranian aggression. Critics, including some foreign policy experts, expressed concern that provocative rhetoric could undermine diplomatic efforts or escalate into unintended conflict.

The Biden administration had pursued a mix of sanctions and limited diplomacy with Iran. Trump has repeatedly vowed a harder line, promising to prevent Iran from acquiring nuclear capabilities and to protect vital shipping routes.

The post comes as global oil markets remain sensitive. Any actual closure or threat to the Strait of Hormuz could send energy prices soaring further, exacerbating inflation concerns in the U.S. and abroad. Recent U.S. fuel excise cuts and government efforts to secure alternative shipments reflect attempts to mitigate domestic impacts.

Pentagon officials have previously confirmed heightened naval presence in the region to safeguard maritime traffic. U.S. Central Command has conducted freedom-of-navigation operations in the area for years.

Iranian officials had no immediate public response to the specific post, though state media often denounces Trump’s comments as bluster or warmongering. Tehran has warned that any attack on its territory would provoke a strong response, potentially targeting U.S. interests or allies.

Congressional leaders from both parties were briefed on regional developments in recent weeks, though details remain classified. Some lawmakers have urged restraint while others support a firm posture against Iran.

The president’s message also touches on broader themes of American strength. Trump has positioned himself as a leader who restores respect for the U.S. on the world stage, frequently contrasting his approach with predecessors.

As of Sunday afternoon, no additional details had emerged about specific military plans for Tuesday. Defense Secretary and Joint Chiefs of Staff declined to confirm or deny operational timelines when asked by reporters.

The incident highlights the intersection of social media, presidential communication and foreign policy. Trump’s direct style has both energized his base and drawn criticism for lacking traditional diplomatic nuance.

Energy traders monitored the situation closely, with some futures contracts showing volatility in response to the post. Analysts cautioned that actual military action would have far-reaching consequences for global supply chains already strained by recent events.

Domestically, the fuel situation has drawn attention from farmers, truckers and consumers facing higher prices at the pump. The administration has pointed to incoming shipments and policy measures aimed at stabilizing supplies.

Trump’s Easter Sunday activity extended beyond the Iran post. He had shared messages focused on faith earlier, aligning with the holiday’s religious significance for Christians celebrating the resurrection.

The full context of U.S.-Iran relations involves decades of hostility, including the 1979 hostage crisis, nuclear negotiations, sanctions and periodic military confrontations. Trump withdrew from the 2015 nuclear deal during his first term, citing its deficiencies.

Supporters argue his pressure campaign brought Iran to the negotiating table previously, while detractors say it isolated the U.S. and empowered hardliners in Tehran.

As Tuesday approaches, international observers watch closely for any signs of movement on the Strait of Hormuz or military posturing in the Persian Gulf. Diplomatic channels reportedly remain active, though public statements suggest hardened positions on both sides.

The president’s post, while informal in tone, carries the weight of his office and has already reverberated through global media and financial markets. Whether it serves as effective deterrence or risks escalation remains a subject of intense debate among policymakers and analysts.

For now, the message stands as another example of Trump’s willingness to use bold, unconventional communication to address international challenges. The coming days will clarify whether it leads to diplomatic breakthroughs, heightened tensions or direct action in one of the world’s most volatile regions.

MIAMI — As the expanded 2026 FIFA World Cup approaches, soccer legends Lionel Messi and Cristiano Ronaldo stand on the brink of what is widely expected to be their last dance on the global stage, with both players eyeing participation in a record sixth tournament despite advanced ages and fitness questions.

Messi, who will turn 39 in June 2026, and Ronaldo, who turns 41 in February, have already qualified with Argentina and Portugal respectively. The tournament, co-hosted by the United States, Mexico and Canada from June 11 to July 19, features 48 teams and a new format that could offer more opportunities for deep runs. Yet experts and recent analyses suggest their paths to lifting the trophy differ sharply due to team quality, personal form and physical demands.

Messi, the reigning World Cup champion after Argentina’s triumph in Qatar 2022, has repeatedly emphasized that his participation hinges on feeling “100 percent” and remaining useful to coach Lionel Scaloni’s squad. Speaking in late 2025, the eight-time Ballon d’Or winner said he would assess his condition day-by-day during preseason with Inter Miami. Teammates like Cristian Romero have expressed confidence that Messi will “easily” make the squad, citing his enduring football intelligence even as physical speed declines.

Argentina sits among the top favorites, ranked third in the latest FIFA men’s rankings behind France and Spain. The Albiceleste boast a deep, balanced roster with stars such as Julian Alvarez, Lautaro Martinez and a solid defensive core. Recent power rankings and betting odds place Argentina near the top for outright victory, bolstered by Copa America success and consistent qualifying dominance. Many analysts argue Messi’s presence elevates the team’s chances significantly, even if his role shifts toward playmaking and leadership rather than carrying the full attacking burden.

Predictions from outlets like CBS Sports envision strong showings for Argentina, with some forecasting a potential semifinal clash against Portugal that could deliver the long-awaited Messi-Ronaldo showdown. However, questions linger about Messi’s ability to sustain elite performance across a grueling schedule in North American summer heat. Reports indicate he has intensified physical preparation, including specialized training sessions in Rosario, to arrive in peak condition.

For Ronaldo, the narrative centers on unfinished business. The all-time leading international goalscorer has confirmed that 2026 will “definitely” be his final World Cup, describing it as his last major tournament at age 41. Playing for Al-Nassr in the Saudi Pro League, Ronaldo maintains sharp goal-scoring form and insists he still feels “quick and sharp.” Portugal coach Roberto Martinez has downplayed recent injury concerns, stating the captain is recovering well and that the issue does not threaten his participation.

Portugal ranks fifth in the FIFA standings and possesses talent including Bruno Fernandes, Bernardo Silva and young prospects, yet many observers note the team performs differently with and without Ronaldo on the pitch. Former teammate Ricardo Quaresma believes Ronaldo’s “last dance” motivation could inspire the squad, while others suggest his impact may come more as a super-sub or inspirational figure. A 2002 World Cup winner with Brazil claimed a Portuguese title would elevate Ronaldo above Messi and Diego Maradona in the greatest-of-all-time debate, though such views remain subjective.

The expanded format offers both players a buffer. With 12 groups of four and the top two plus the eight best third-place teams advancing, early exits are less likely for seeded sides like Argentina and Portugal. Their group-stage opponents appear manageable based on the December 2025 draw, setting up potential knockout-path meetings later. A Messi-Ronaldo semifinal has become a popular dream scenario in media forecasts, though actual bracket outcomes depend on results.

Realistically, Messi’s chances of winning a second World Cup appear stronger. Argentina’s squad depth and recent pedigree provide a platform where his genius can shine without requiring him to dominate every minute. Former Brazil international Kleberson noted that “Argentina has more chance of winning the World Cup with Messi than any other country” due to the supporting cast. Betting markets and expert predictions frequently list Argentina among the top three contenders alongside France and England.

Ronaldo’s path is steeper. Portugal reached the quarterfinals in 2022 but fell short, and the 2026 edition represents his final realistic shot at the one major trophy missing from his cabinet. While his leadership and clutch moments remain valuable, the physical toll of a month-long tournament at 41 raises questions. Some tactical analyses suggest Portugal plays more fluidly without him starting every match, potentially limiting his minutes in high-stakes games.

Both players could achieve historic milestones. Participation would make them the first men to feature in six World Cups, joining Mexico goalkeeper Guillermo Ochoa in that pursuit. Ronaldo could become the oldest player to win the tournament if Portugal triumphs, surpassing Italy’s Dino Zoff who lifted the trophy at 40 in 1982. Messi, already a champion, could cement his legacy further with back-to-back titles.

Fitness remains the wildcard. Messi has managed minor setbacks in MLS but continues producing moments of brilliance for Inter Miami. Ronaldo’s Saudi league campaign provides consistent match rhythm, though the level of competition differs from European or international intensity. Both have defied age expectations throughout their careers, adapting roles as needed — Messi evolving into a deeper creator, Ronaldo leveraging positioning and finishing.

The expanded 48-team field and North American venues add variables. Matches span 16 host cities with varying climates, travel demands and pitch conditions. The final at MetLife Stadium in New Jersey on July 19 could host a fairy-tale ending if either captain lifts the trophy.

Public and media fascination centers on the rivalry’s final chapter. For two decades, Messi and Ronaldo defined an era through club battles at Barcelona and Real Madrid before their international paths diverged. A 2026 encounter, whether in the group stage or knockouts, would captivate billions. Yet many experts caution against over-romanticizing, noting younger stars like those at France, England or Brazil may dominate headlines.

Ultimately, Messi holds the clearer route to glory. Argentina’s cohesion and his proven ability to elevate teammates in major tournaments give the defending champions an edge. Ronaldo’s Portugal boasts talent but lacks the same recent silverware pedigree, making a title run more dependent on collective performance and perhaps his inspirational presence.

As April 2026 preparations intensify, both icons train with characteristic dedication. Messi assesses his body daily while Ronaldo channels trademark hunger for one more shot at history. The 2026 World Cup promises emotion, records and possibly one last unforgettable chapter in the greatest individual rivalry soccer has known.

Whether either lifts the trophy remains uncertain, but their mere presence ensures the tournament will carry extra magic. For Messi, a second star could seal his status as the undisputed greatest. For Ronaldo, a maiden World Cup would complete the ultimate collection and spark endless debate. Fans worldwide await the summer drama that could define their legacies one final time.

LOS ANGELES — Travelers passing through Los Angeles International Airport on Easter Sunday, April 5, 2026, are encountering unusually short TSA security wait times, with many checkpoints reporting waits of just 1 to 5 minutes as of mid-morning, according to official airport data and real-time trackers.

The flyLAX.com security wait times page showed Tom Bradley International Terminal general boarding at approximately 2 minutes and TSA PreCheck at 1-2 minutes early Sunday, with similar low figures across multiple sources. Other monitoring sites reported blended estimates around 3 minutes for standard lanes during off-peak morning hours.

This smooth flow comes amid a busy Easter holiday travel period, when passenger volumes typically rise as families head out for spring break getaways or return home after weekend celebrations. LAX, one of the world’s busiest airports handling more than 60 million passengers annually, has seen lighter-than-expected congestion at security on this Sunday, contrasting with broader concerns about TSA staffing strains from the ongoing partial government shutdown affecting some operations nationwide.

Airport officials and TSA representatives recommend that passengers still arrive at least two hours before domestic flights and three hours for international departures. Even with current short lines, factors like flight volume, checked baggage processing and gate boarding can add time to the overall experience.

Real-time data from the official LAX website and third-party trackers such as takeofftimer.com and onairparking.com indicate that waits remain minimal outside traditional peak windows. Typical busy periods at LAX include early mornings from 6:30 to 9 a.m., midday from 11 a.m. to 2 p.m., and evenings from 8 to 11 p.m. On April 5, however, many travelers reported breezing through checkpoints in under 10 minutes, especially those with TSA PreCheck, CLEAR or airline-specific expedited programs.

The lighter lines may reflect a combination of factors: Easter falling on a Sunday when some business travelers stay home, strategic flight scheduling by airlines, and effective staffing at checkpoints despite national challenges. Recent Reddit reports from early April noted smooth experiences at Terminal B (the new international facility) with waits under 5 minutes for international departures.

LAX features nine passenger terminals with security checkpoints that vary in layout and technology. The Tom Bradley International Terminal often handles the heaviest international traffic, while domestic terminals 1 through 8 serve major carriers like American, Delta, United and Southwest. Travelers should check their specific terminal via the LAX app or website, as wait times can differ slightly by location.

To stay informed, passengers can visit flyLAX.com/wait-times for official updates refreshed periodically throughout the day. The MyTSA mobile app from the Transportation Security Administration also provides crowdsourced and estimated wait times, along with reminders about the 3-1-1 liquids rule and prohibited items. Additional tools like airline apps from Delta, United or American sometimes integrate real-time security data.

For those without expedited screening, standard lanes involve removing shoes, laptops and liquids, with TSA officers conducting thorough checks. PreCheck members enjoy faster processing with shoes and light jackets often kept on, while CLEAR uses biometric verification to skip document checks.

Easter travel at LAX coincides with spring break surges that began in late March, when some reports noted occasional longer lines during peak hours. However, on this holiday Sunday, the combination of holiday timing and possibly fewer early departures has kept congestion low. Social media posts from travelers described security experiences as “seamless” or under 10 minutes even without PreCheck.

Broader TSA context includes reports of elevated absenteeism and longer lines at some major hubs due to the partial government shutdown, with wait times exceeding two to four hours at airports like Atlanta in recent weeks. LAX appears to have avoided the worst of those delays so far, thanks in part to local staffing adjustments and the airport’s multiple checkpoints distributing passenger flow.

Travelers with disabilities or needing assistance can request TSA Cares support in advance by calling 855-787-2227. Families with young children or elderly passengers should factor in extra time for strollers, car seats and mobility aids, even when general lines move quickly.

Parking and ground transportation add another layer. LAX offers economy, central terminal area and valet options, but traffic around the airport can spike during holiday periods. Rideshares, shuttles and public transit via the LAX shuttle or Metro connections help avoid congestion. The airport strongly advises against circling terminals and encourages using the cell phone waiting lot for pickups.

Flight status remains another key variable. Easter Sunday saw some delays earlier in the weekend due to weather or mechanical issues in certain markets, but security itself has not been a major bottleneck today. Passengers should monitor their airline app or flightaware.com for gate and departure updates.

Experts recommend several strategies for smooth LAX travel:

- Enroll in TSA PreCheck or Global Entry for frequent flyers to cut wait times dramatically.

- Use CLEAR biometric lanes where available for even faster entry.

- Pack efficiently: Place liquids in a quart-sized bag and electronics in an accessible spot.

- Download digital boarding passes and use mobile check-in.

- Arrive early enough to enjoy the airport’s dining and shopping options if time allows.

LAX has invested heavily in modernization, including the new Terminal B, automated screening lanes and improved signage. These upgrades help process passengers more efficiently even during busier periods.

For international travelers, additional steps like customs and border protection upon arrival or departure add time. The Tom Bradley terminal features enhanced facilities, but waits there can vary based on flight banks.

As the day progresses, wait times could increase if afternoon and evening departures ramp up. Historical patterns suggest monitoring mid-to-late afternoon for potential moderate rises, though current indicators point to continued light traffic.

In a year when national TSA operations face challenges from staffing and funding issues, LAX’s performance on Easter Sunday offers a positive note for Southern California travelers. The airport continues to rank among the busiest globally, serving as a major gateway to Asia, Europe, Latin America and domestic destinations.

Travelers departing later today or connecting through LAX should check live data closer to their arrival. Conditions can change rapidly with sudden surges or operational adjustments.

For those arriving at LAX, immigration and baggage claim represent separate processes, with reported waits sometimes longer than security for international flights.

Overall, Easter Sunday 2026 at LAX security appears traveler-friendly so far, with short lines allowing more time for relaxation or last-minute purchases before boarding. Still, the standard advice holds: build in a buffer for the unexpected, confirm flight status and prepare documents in advance.

The TSA emphasizes that safety remains the priority, and thorough screening ensures secure skies even when lines move quickly. Passengers are encouraged to report any concerns or helpful feedback through official channels.

As families celebrate Easter with travel plans, LAX demonstrates that holiday surges do not always translate to chaos at security when volumes and staffing align favorably.

In summary, current TSA wait times at Los Angeles International Airport on Easter Sunday, April 5, 2026, are short — generally under 5 minutes at many checkpoints — providing a smoother experience than typical peak holiday travel. Travelers should still plan conservatively, use available apps for real-time updates and take advantage of expedited programs to minimize stress.

With the airport operating efficiently amid national headwinds, LAX offers a relatively stress-free start to journeys on this spring holiday.

Prime Capital Financial Chairman and managing partner Scott Colangelo breaks down his bullish outlook for the markets on ‘Varney & Co.’

For the first time on record, average diesel prices in San Francisco have surged past $8 per gallon, according to new data from GasBuddy—marking an unprecedented milestone for any U.S. city.

The jump comes as the war with Iran pushes global oil prices higher, underscoring the volatility in fuel markets and how California-specific factors—like stricter regulations, higher taxes and limited supply—can drive prices well above the national average.

San Francisco has long had some of the highest fuel costs in the country, but crossing the $8 threshold for diesel represents a new benchmark—even for a state accustomed to elevated energy prices.

BUYING A HOME JUST GOT MORE EXPENSIVE AS THE IRAN WAR DRIVES UP MORTGAGE RATES

A person grabs the nozzle for diesel fuel at a gas station. (Rebecca Noble/Bloomberg/Getty Images)

Diesel, which powers much of the nation’s freight, shipping and public transportation systems, is especially sensitive to refining capacity and global supply disruptions.

The surge is expected to ripple beyond the Bay Area. Higher diesel costs often translate into increased transportation and shipping expenses, which can ultimately push up prices for goods and services nationwide.

Meanwhile, gas prices are rising across nearly every region, with some states already well above the national average.

As of April 5, the national average for regular gasoline stood at $4.11 per gallon, according to AAA – up 86 cents from a month earlier. On the West Coast, drivers are seeing the highest costs, with prices reaching $5.92 per gallon in California and $5.37 in Washington.

MAPPED: WHERE GAS PRICES ARE RISING THE FASTEST FROM THE IRAN CONFLICT

On the East Coast, gas prices are exceeding $4 in several areas, including $4.27 in Washington, D.C., and $4.06 in New York.

In the Midwest, Illinois stands out at $4.29 per gallon, while much of the region remains in the mid-$3 range. Southern states remain cheaper overall, though prices are rising. Texas averages about $3.82 and South Carolina at $3.82, while Florida is higher at $4.20.

President Donald Trump on Sunday directed a profanity-laced message to Iran, saying the U.S. will target the regime’s power plants and bridges this week if the Strait of Hormuz is not reopened.

The Strait of Hormuz, a waterway between Iran, the United Arab Emirates and Oman, is a critical energy choke point.

GET FOX BUSINESS ON THE GO BY CLICKING HERE

A satellite image shows the Strait of Hormuz, a key maritime passage connecting the Persian Gulf to the Gulf of Oman, vital for global energy supply. (Amanda Macias/Fox News Digital)

“Tuesday will be Power Plant Day, and Bridge Day, all wrapped up in one, in Iran,” Trump’s post read. “There will be nothing like it!!!”

“Open the F—– Strait, you crazy bastards, or you’ll be living in Hell – JUST WATCH!” read Trump’s message to Iran’s leaders. “Praise be to Allah.”

While prices may fluctuate in the coming weeks, the milestone signals how vulnerable fuel markets remain to supply shocks—and how quickly costs can climb to historic levels.

Spanish media still unconvinced despite Marcus Rashford scoring crucial Barcelona goal

Fitness tracking under scrutiny as Strava military data leak exposes personnel

Waitrose worker sacked after ‘stopping thief stealing Easter eggs’

-

NewsBeat3 days ago

NewsBeat3 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business3 days ago

Business3 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Spanx – Corporette.com

-

Entertainment6 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World4 days ago

Crypto World4 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech7 days ago

Tech7 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World5 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech7 days ago

Tech7 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Sports20 hours ago

Sports20 hours agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business4 days ago

Business4 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech6 days ago

Tech6 days agoApple will hide your email address from apps and websites, but not cops

-

Tech5 days ago

Tech5 days agoEE TV is using AI to help you find something to watch

-

Sports5 days ago

Sports5 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Politics6 days ago

Politics6 days agoShould Trump Be Scared Strait?

-

Tech6 days ago

Tech6 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Fashion6 days ago

Fashion6 days agoThe Best Spring Trends of 2026

-

Sports6 days ago

Sports6 days agoWomen’s hockey camp eyes fitness boost, tactics ahead of WC 2026 campaign | Other Sports News

-

Tech5 days ago

Tech5 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Crypto World7 days ago

Crypto World7 days agoBitcoin’s Six-Month Losing Streak: What On-Chain Data Says About the Market’s Next Move

-

Politics6 days ago

Politics6 days agoBBC slammed for ignoring author of The Fraud

You must be logged in to post a comment Login