Business

Sell The S&P 500 And Buy Gold Mining Stocks

style-photography/iStock via Getty Images

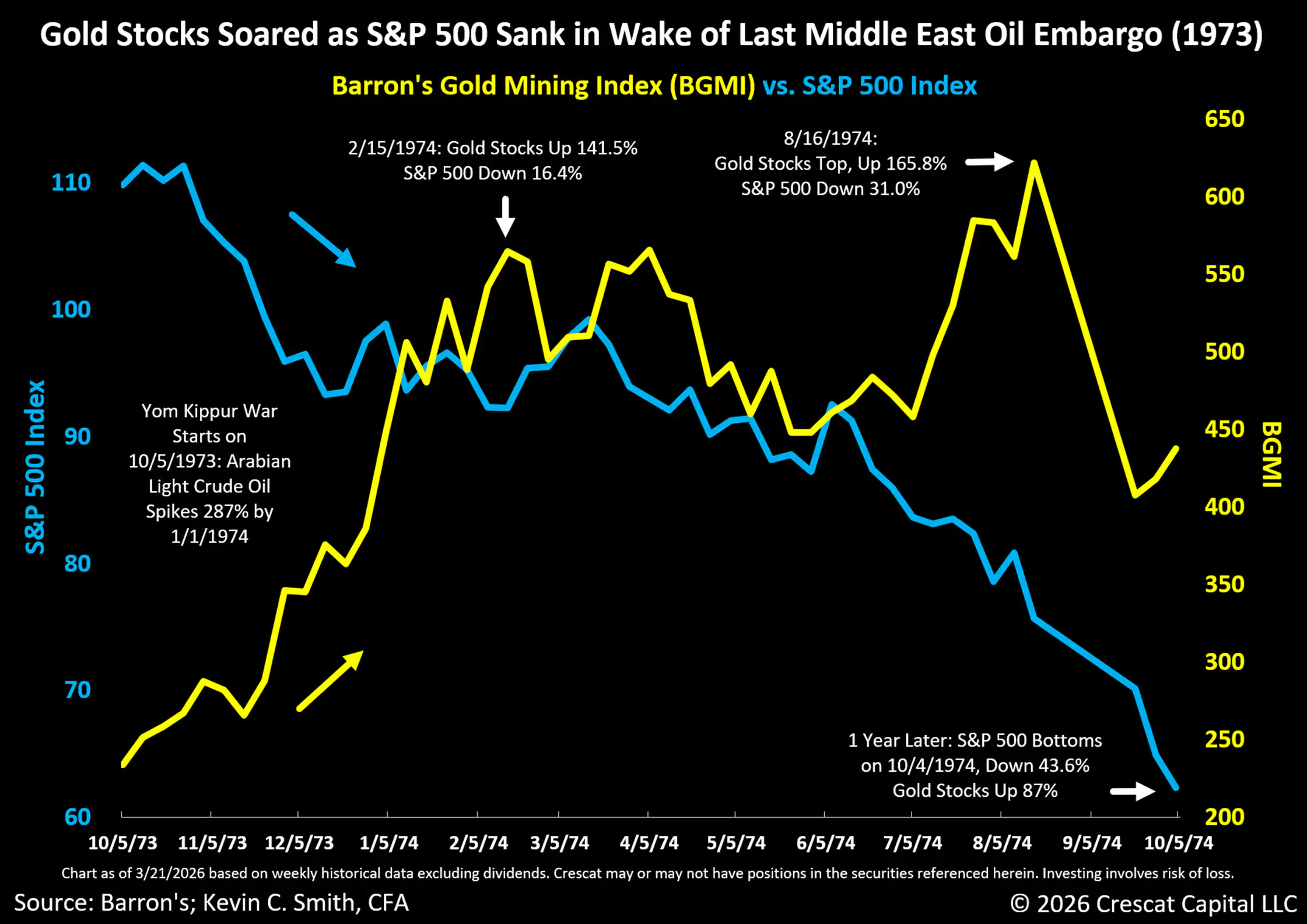

We think the recent correction in gold mining stocks presents a timely buying opportunity. For the reasons we outline in this research letter, we believe now is a great time for investors to consider selling their S&P 500 Index (SPY) funds and buying gold mining stocks. Since February 28, when Israel and the United States began a series of missile strikes against Iran, front-month West Texas Intermediate crude oil futures have risen 46.7%. On Thursday, CNBC ran the headline: “Gold and silver sell-off accelerates as inflation fears grip global markets.” It reads like an oxymoron. Normally, we would expect new inflation fears, even from an oil shock, to be a bullish catalyst for gold and mining equities. Such fears can also be a trigger for a selloff in an overvalued large cap US equity market. That was the case on both counts from the start of the 1973 Yom Kippur War and ensuing Arab Oil Embargo, as we show in the chart below.

Rising Interest Rates Send a Potentially False Signal for Gold

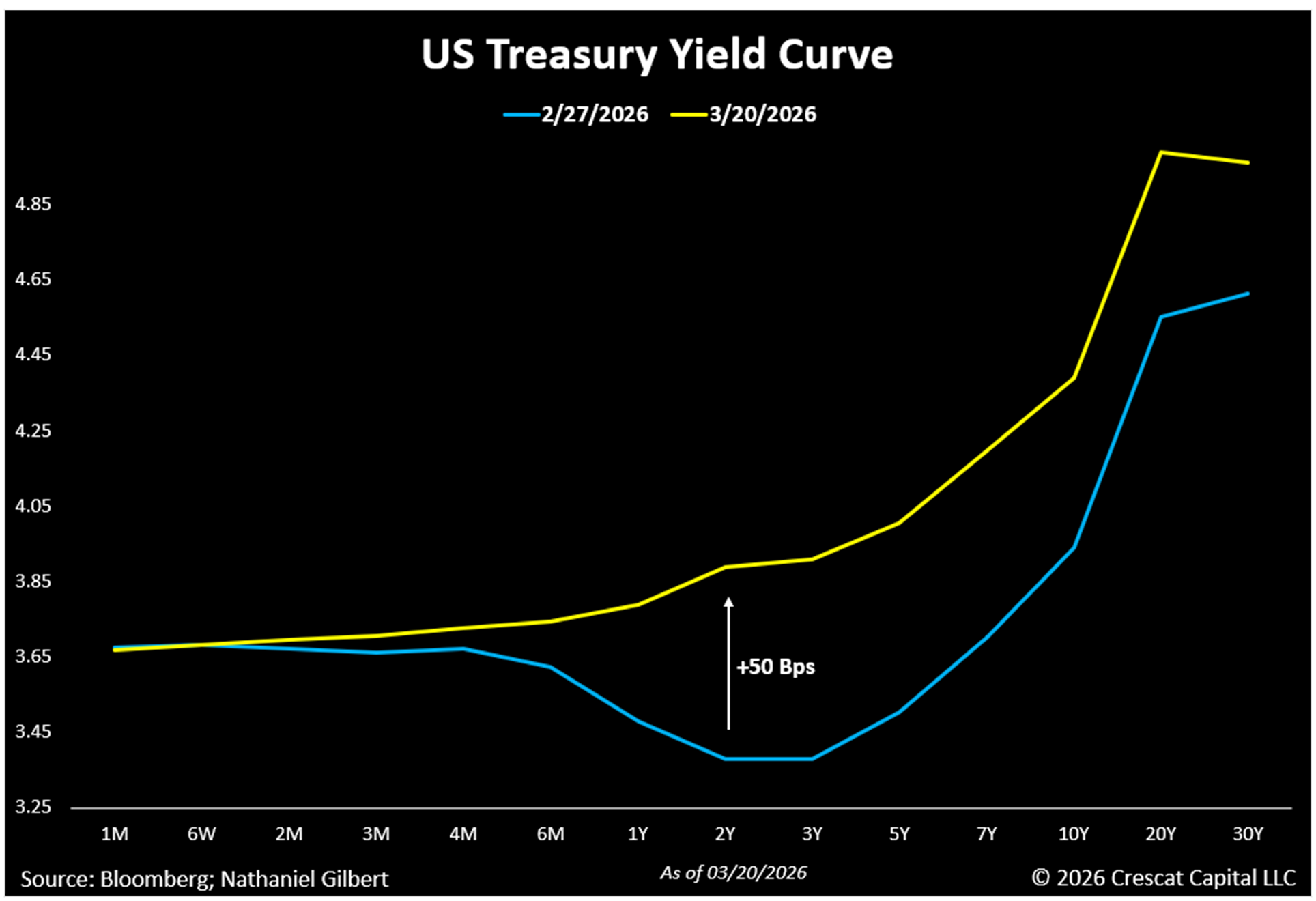

Normally, rising inflation expectations would be looked at as a glass half full for steadfast gold bulls. But it seems that gold bears and perhaps weak-handed gold investors today are seeing rising interest rate expectations as a reason to look at the gold market as a glass half empty. The overwhelming narrative today is that rising interest rates are bad for gold, but we think this is a false narrative. Indeed, with the oil spike fueling new inflationary concerns in the US, the Fed rate cuts that had been priced into the futures curve for the remainder of 2026 now appear off the table. The entire US Treasury yield curve has shifted higher over the last three weeks. The 2-year yield has risen the most, up a full 50 basis points, reversing the recent inversion at the short end of the curve.

We think today’s gold mining investors would be wise not to panic at today’s low levels of interest rates and inflation expectations, especially given the historic US debt and deficit imbalances, which in our view portend at least as high and sustained inflation rates in the decade still ahead as in the 1970s. On the fiscal deficit front, the war has already cost more than a billion dollars a day, with the first 100 hours alone costing $3.7 billion. Speaking of oxymorons, the Pentagon sent a request to the White House for more than $200 billion in supplemental war funding on March 18, and gold and silver sold off hard the next day. Earlier in the week, the US national debt quietly crossed $39 trillion, less than 5 months after hitting $38 trillion. With the current war in Iran, the thesis for precious and critical metals mining stocks has not broken; it has only gotten stronger.

Precious Metals Outpaced Rising Oil in the 1970s, Even as Interest Rates Rose

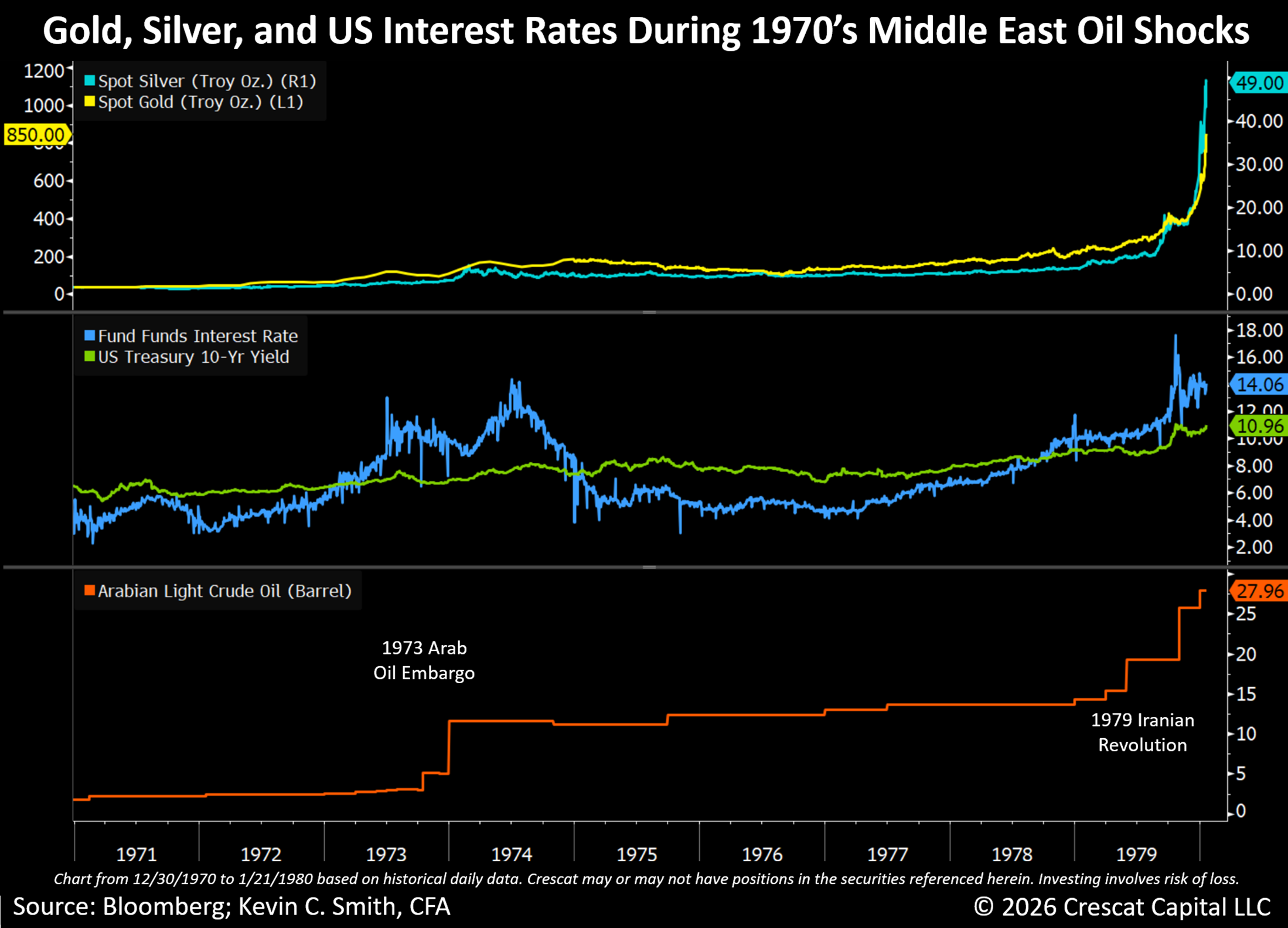

We need to look at the most comparable time in history, which in our opinion is the 1970’s decade, to see if rising interest rates are truly bad for gold or not. We think the current geopolitical climate is extremely bullish for precious metals prices, just as it was at the outset of that period. Remember, that was a stretch that included two major oil price shocks in the Middle East: the 1973 Yom Kippur War, and then later the 1979 Iranian Revolution. Inflation expectations, interest rates, and oil prices all rose substantially throughout the entire decade. Rising interest rates over this time were not a valid reason to be bearish on gold.

Gold rose 2,329% from US$35/oz. at the beginning of the decade to a high of US$850/oz on January 21, 1980. Silver rose even more than gold over the same time period, up 2,888% from US$1.64 to US$49.00. Oil rose substantially too, but even less than gold and silver. Arab Light Crude Oil climbed 1,553% from US$1.80/barrel to US$27.96/barrel over that time period. If gold and silver investors had feared rising interest rates from the outset, it would have caused them to miss this historic runup in the entire precious metals complex. US Fed Funds interest rate rose from 3% to over 14.1% over the entire period, reaching a high of 17.6% on 10/22/1979, three months before gold would finally top.

Rising interest rates in the 1970s did nothing to stop the trend of secular rising inflation expectations until Fed Chair Paul Volcker would later raise the Fed Funds rate all the way to 22.4% on 7/22/1981, creating a double-dip recession that finally broke both inflation and gold’s back. In our opinion, today’s meager 3.6% Fed Funds rate and 4.4% 10-year US Treasury yield are well poised to ignite a new inflationary era, not to quash one, even if the Fed were to allow rates to rise.

Gold Mining Stocks Crushed the S&P 500 Index in the 1970s

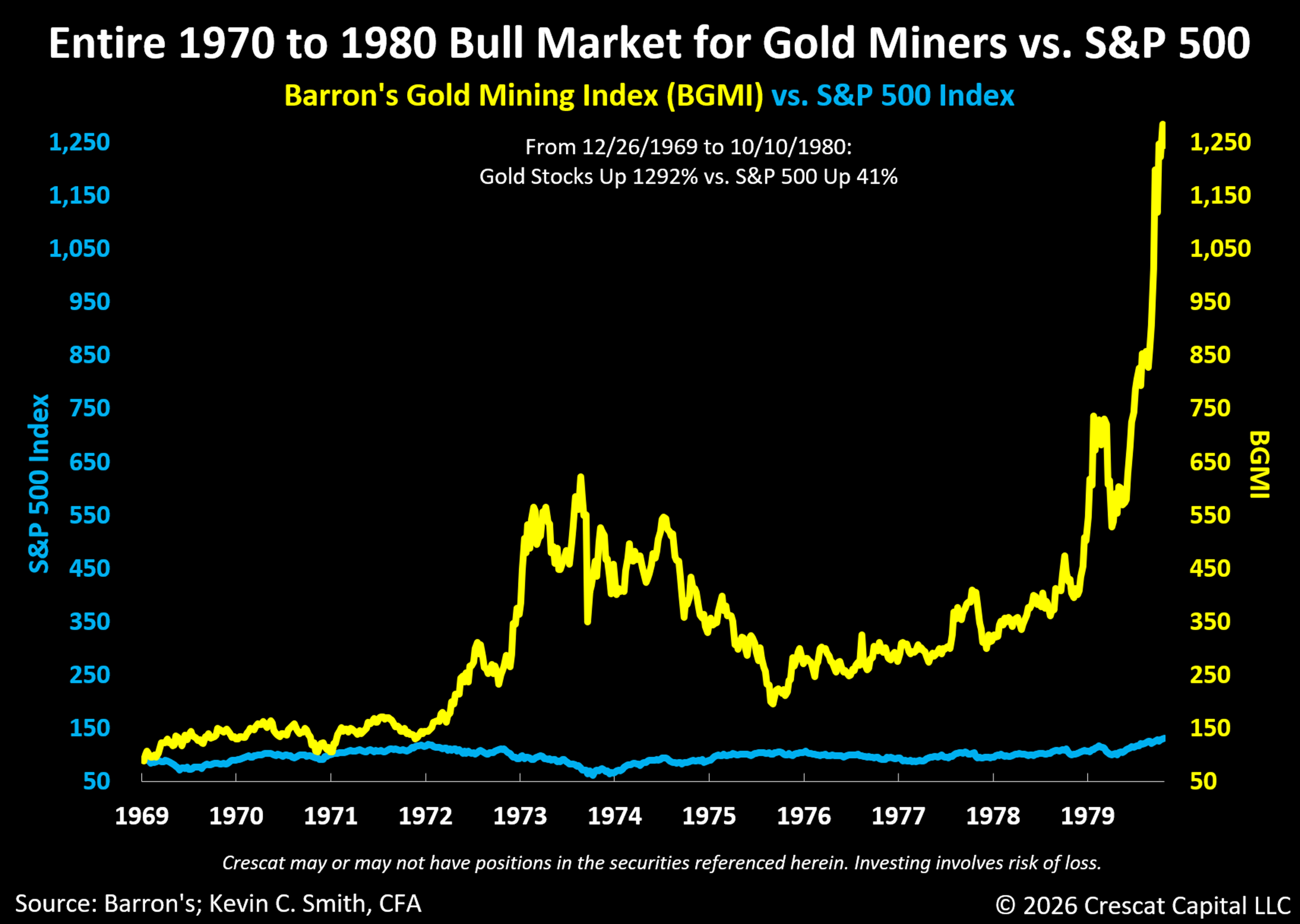

Gold mining equities did extremely well over the 1970s decade, especially compared to the S&P 500 Index. The Barron’s Gold Mining Index rose 1,292% from its low on 12/26/1969 to its high on October 17, 1980, based on weekly data from Barron’s. The S&P 500 was up a mere 41% over that long stretch. Starting from today’s high Shiller CAPE ratios for the S&P 500, forward-10-year returns for the S&P 500 should be similarly low in comparison to that decade. On the other hand, starting from today’s low valuations for countercyclical mining stocks, and given the favorable macro supply-and-demand backdrop for metals, we think the forward 10-year returns for the miners should be similarly high compared to that decade.

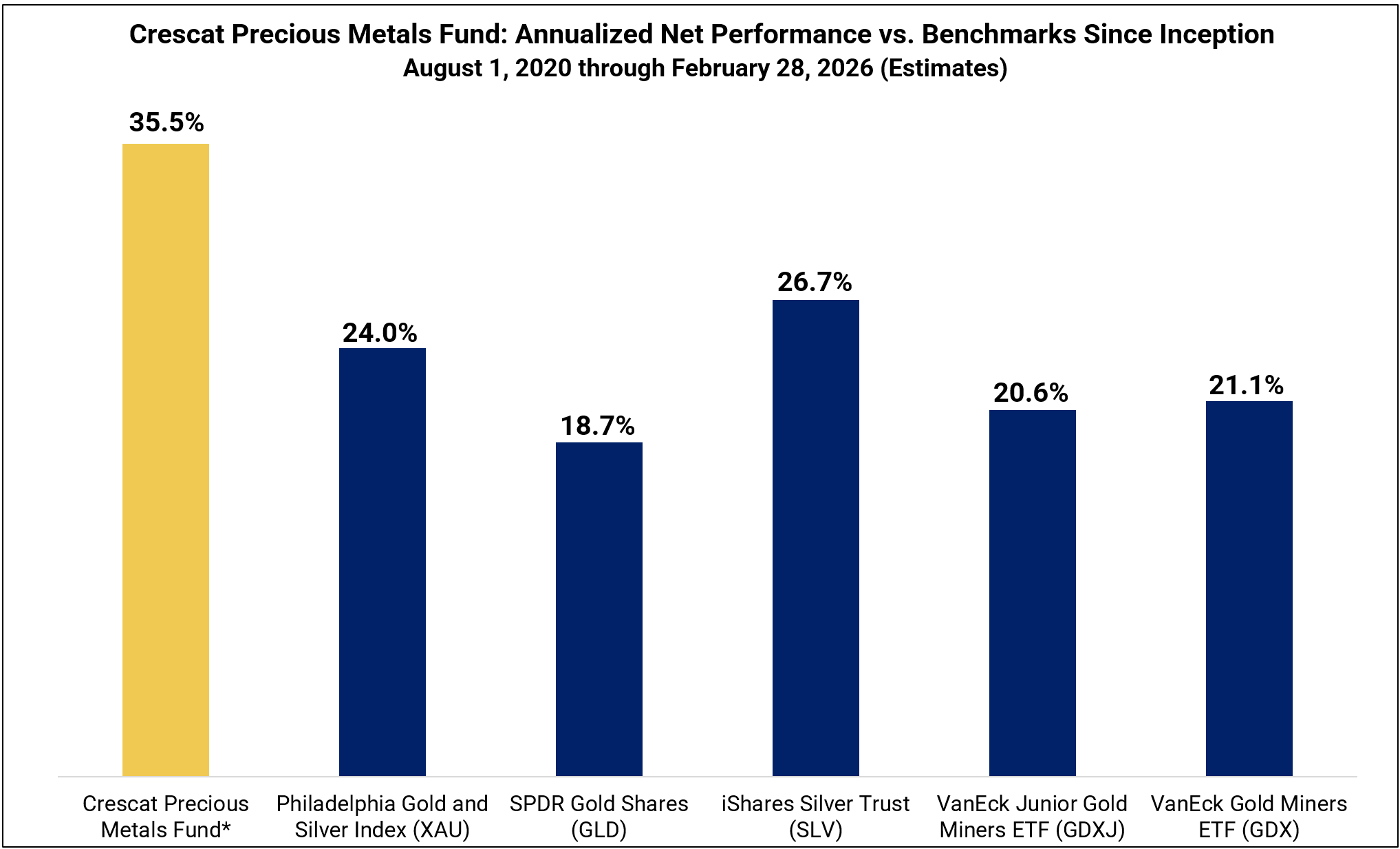

Yes, there is volatility in mining stocks, but the rewards in the right macro environment can be well worth it. We prefer mining stocks relative to owning outright gold and silver today because, in our valuation models, the equities are ultra-cheap relative to the metal prices, especially in our highly curated activist metals portfolio, the largest thematic exposure across all five Crescat funds. Furthermore, our portfolio is heavily tilted toward the exploration companies that control some of the world’s most attractive new gold, silver, and copper discoveries. These are the types of companies that the major miners will need to buy at a significant premium to current market prices to replace their dwindling reserves after a long trend of underinvestment in exploration spending and capital investment over the last 14 years.

At the same time, it takes about 15 years on average to advance a mining project from discovery to production. The world needs more metals now for AI datacenters, electrification, new US manufacturing onshoring, and defense, but the pipeline of new economic discoveries and viable development projects is scarce. These are the primary reasons we believe the cycle has strong legs for an entire decade ahead and this is why we favor the small cap explorers at this stage of the cycle. These companies carry risk and should be held in a professionally managed diversified portfolio, such as through our funds, but offer significantly more upside than the large-cap mining indices and ETFs in our view.

Technical Support for Gold Stocks; Resistance for the S&P 500

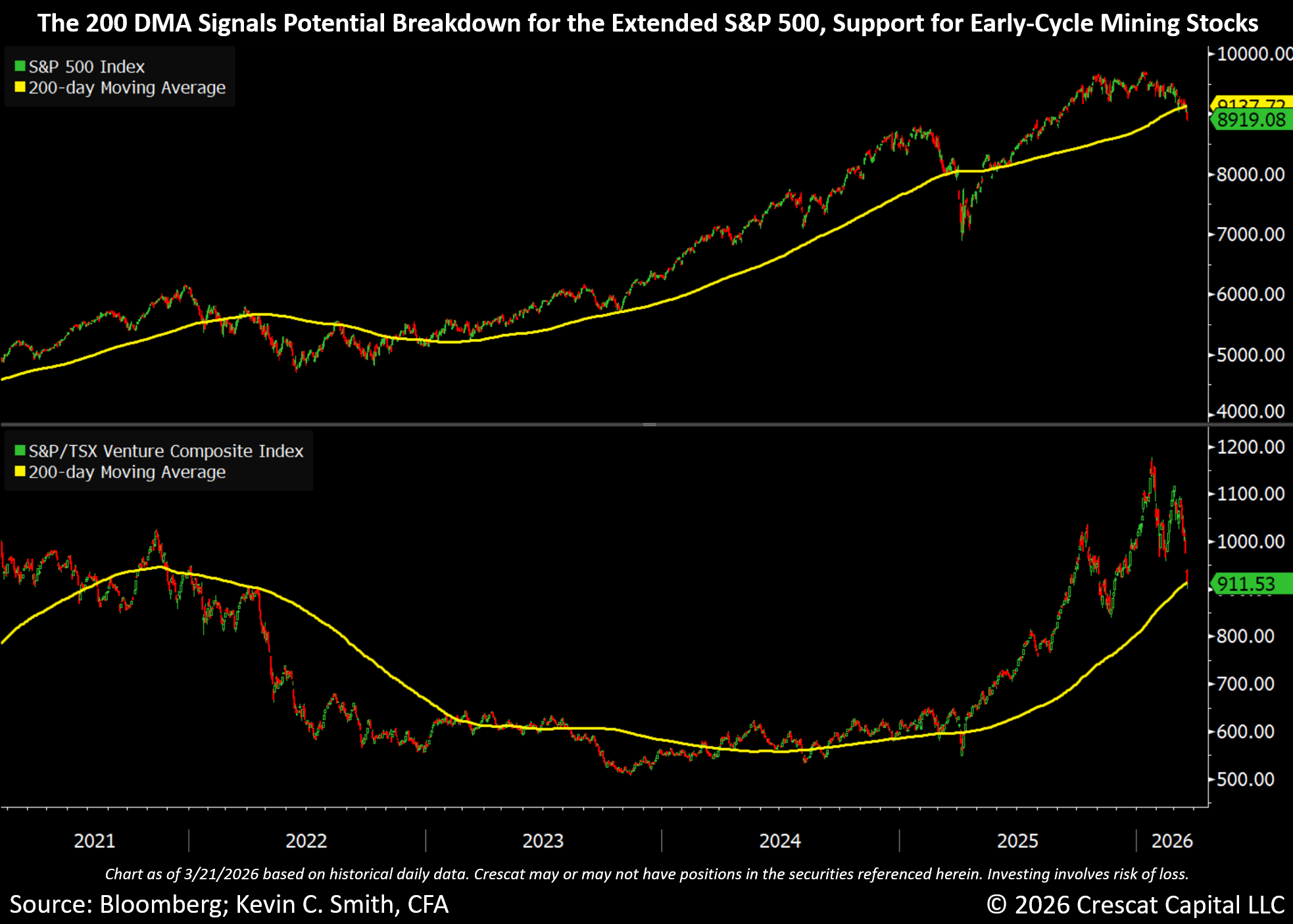

The large cap S&P 500 and Nasdaq 100 (QQQ) indices finally appear to be just starting to break down from record valuations, as we would expect with the new geopolitical conflict and resulting likely inflation and higher interest rates, but gold, silver, and mining stocks have sold off significantly more than these indices since Israel and the US first struck Iran on February 28. We think that presents an incredible short-term buying opportunity for the undervalued and still uncrowded mining stocks, especially the premier small cap explorers that we favor in our portfolios. Meanwhile, we see the long-slowing momentum, and now breakdown from the 200-day moving as a potential sell trigger for late-cycle, overcrowded, and overvalued US large cap equity indices and megacap tech stocks.

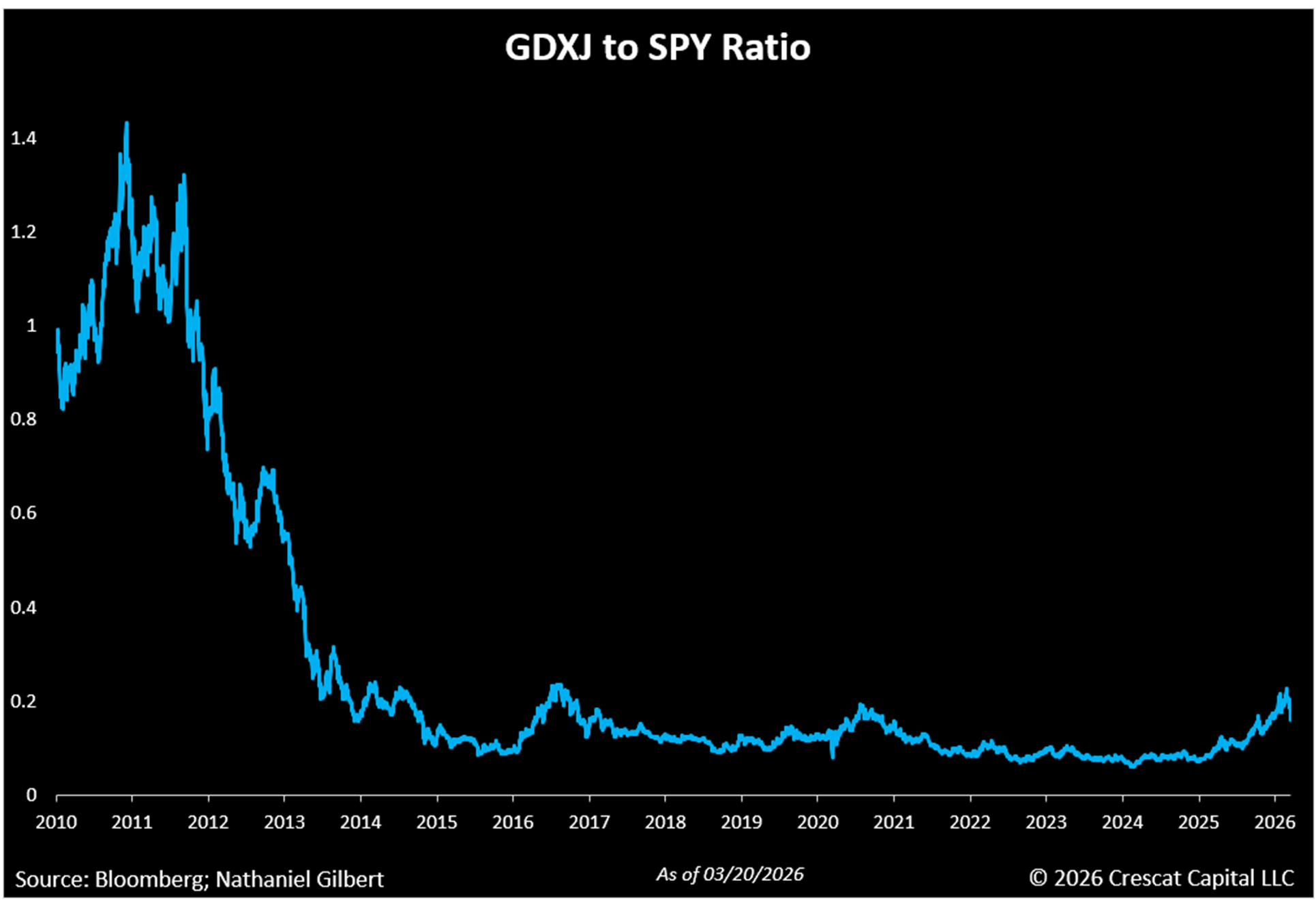

Interestingly, both mining stocks and the large cap indices are near their critical 200-day moving average support and resistance levels, but the two groups have highly divergent valuation and growth profiles. The indices of the high-growth, undervalued mining stocks are deeply oversold and hover at or above their 200-day moving average. The S&P/TSX Venture Composite Index, a proxy for small cap exploration focused miners, has already come down 23% from its January 23 recent high and could find strong support. It is now right on the 200-day moving average. The small cap exploration focused miners where Crescat is tilted have been outperforming the larger cap producing miners in the current pullback. From February 27 through March 20, the large cap VanEck Gold Miners ETF (GDX) (GDX) has declined 31%, while the VanEck Junior Gold Miners ETF (GDXJ) (GDXJ), a mid-tier producer index, is down 33%. Both of these ETFs hover just above the 200-day moving average now.

The S&P 500 and Nasdaq 100, however, look like they have just critically broken the 200-day moving averages. Yet, the S&P 500 is down only 6.8% from its recent January 28 high. In our view, it has substantially further downside ahead to get to reasonable valuations based on market history. The broad US large cap indices could finally be poised to break down hard from historically high fundamental valuations, which, in our analysis, are comparable to those at prior major market tops in 1929 and 2000.

Both the GDX and GDXJ ETFs have 14-day Relative Strength Index (“RSI”) readings below 30, a level typically associated with oversold conditions suggestive of a potential for a near-term rebound. Note, the last two times GDXJ 14-day RSI was sub 30 in March 2023 & October 23, there was a 34.6% and a 27.9% rally, respectively, within just two months. For an industry that just led the entire stock market in 2025, such a sharp rebound would not surprise us at all.

Although pullbacks can be painful and unsettling in the moment, they often create some of the most attractive opportunities for disciplined investors. When it comes to mining stocks today, these aphorisms apply:

“Buy when there’s blood in the streets, even if the blood is your own.” – Baron Rothschild

“The time of maximum pessimism is the best time to buy.” – Sir John Templeton

“Be fearful when others are greedy and greedy only when others are fearful.” – Warren Buffett

Oil Price Future Less Clear than Gold

Importantly, mining equities have come under pressure not only from the decline in underlying precious metals prices, but also from growing concerns around operating-cost inflation, particularly the risk that a sustained rise in oil prices could compress margins across the sector, especially among the producers who have been enjoying strong margins.

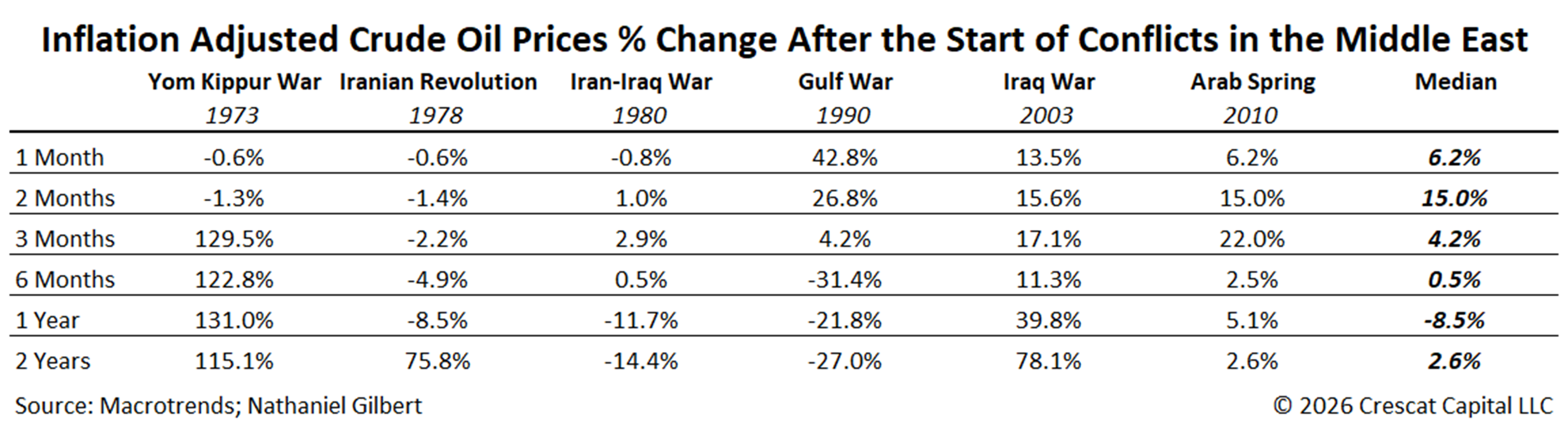

We have shown that higher oil prices do not mean that metal prices cannot go even higher. At this stage, however, the ultimate effect of recent geopolitical developments on the long-term path of oil prices remains unclear. The US is the largest oil-producing country in the world today and is now a net exporter, unlike in the 1970s when it was dependent on Middle East oil. Although the market has understandably responded to the risk of higher energy costs, it is too early to conclude whether the current move in crude reflects a lasting shift in fundamentals or a shorter-term geopolitical premium. To provide perspective, the table below illustrates the inflation-adjusted percentage change in crude oil prices following the onset of past major Middle East conflicts over various time horizons.

Still Early Innings in a New Secular Bull Market for Mining Stocks

We launched our precious metals fund in 2020 and began allocating heavily to exploration mining companies at that time because we believed the sector was entering the early innings of a major multi-year bull cycle. That view was, and continues to be, driven by our conviction that the industry faces deep structural supply shortages. At the same time, a macro backdrop characterized by inflationary pressures and unsustainable sovereign debt burdens has set the stage for a gold super cycle. More than a decade of underinvestment in mining has created a favorable supply and demand imbalance for metal prices at a time when the world needs more metals than ever. This argues for strong growth ahead for the mining industry revenues, earnings, and new investment dollars poised to pour into the industry for exploration and mine development. Meanwhile, investors’ love affair with big technology stocks and apprehension toward mining still leaves the crucial mining industry with valuations that are ultra depressed. Such is a formula for much higher stock prices for precious and critical metals miners in the years ahead, in our view.

Crescat Performance and Call to Action

For our existing investors, we want to first thank you for your continued trust and support. In January of this year, we heard from a number of you who wished you had added at the end of 2024. This pullback is that moment again. The same macro environment that rewarded your conviction in 2025 has not reversed, it has deepened. We believe this is the time to consider an additional allocation. And for those who are comfortable where they are, staying put with a thesis this intact is equally the right call.

For those who stayed on the sidelines feeling that 2025 was too strong a year to come in after, this is your opportunity to get positioned. The 2025 performance was significant, but the case for precious metals and mining equities was never a one-year story. The pullback has reset prices without resetting the thesis. We believe this is a cleaner setup than most investors get and an opportunity to be positioned ahead of the next leg. April 1 is the date to get positioned.

*See important disclosures below. Past performance does not guarantee future results. Investing involves risk, including risk of loss.

Sincerely,

Kevin C. Smith, CFA, Founder & CEO

Nathaniel Gilbert, Analyst

References

- 1 – Net returns reflect the performance of an investor who invested from inception and is eligible to participate in new issues and side pocket investments. Net returns reflect the reinvestment of dividends and earnings and the deduction of all expenses and fees (including the highest management fee and incentive allocation charged, where applicable). An actual client’s results may vary due to the timing of capital transactions, high watermarks, and performance.

- 2 – Performance figures presented Excluding SCM SP represent the fund’s net returns calculated without the impact of the San Cristobal Mining, Inc. side pocket that was designated on July 1st, 2024. The side pocket includes a private equity asset that is not available to new investors in the funds on or after July 1, 2024. Excluding these assets provides a clearer view of the performance to investors coming into the funds after that date. New investors cannot participate in the SCM Side Pocket and will not share in its potential gains or losses. Investors should consider both the overall performance and the performance excluding the side pocket when evaluating the fund’s returns.

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

A Perth-founded diving company has reinvented itself and is now delivering world-leading resource-recovery results.

Kaynar Group founder Kyle Ringin has been named the First Amongst Equals at the 2026 40under40 business awards, taking out the top honour recognising Western Australia’s emerging business leaders.

More than 600 people took to Crown to celebrate the tradie-turned-entrepreneur and 39 others in the 25th year of the Business News awards gala on Friday evening.

Attendees were entertained with a night of performances by Williams Creative Co, Japanese Wadaiko ensemble Taiko On and DJ crossed with live music duo, The New Now.

Having judged most of the 40under40 awards since its inception in 2002, Business News senior journalist and chief judge Mark Pownall said WA has continued to offer up a diverse cohort of excellent candidates.

Choosing the winners, he said, remained a challenge from the beginning.

“In our first year of 40under40, the judging panel caused a bit of angst for the event organisers by deciding to name two winners, because we could not split the tied pair,” Mr Pownall said.

“One was from a family business, the other from corporate WA.

“I felt that start set the tone for 40under40.”

Now, a total of 1,000 of WA’s business leaders have been inducted as 40under40 winners.

“It is not about any one sector in this state – it isn’t just small business, or family business, or startup founder, or careerists who have made it on St Georges Terrace,” Mr Pownall said.

“All of those can have a crack, and they have.”

Having undertaken an extensive interview and application process, Mr Ringin was recognised as both First Amongst Equals and the winner of the Family Business category.

Working as an apprentice auto electrician and workshop foreman in Broome, he identified a gap in the Kimberley for a reliable, locally skilled trades provider.

That led him to establish maintenance, mining and civil solutions provider Kaynar Group with his wife and co-founder Shaylee Greechan in 2020.

Mr Ringin has turned operating in extreme remoteness into a competitive advantage, all while delivering real impact for WA’s north.

Kaynar Group has grown rapidly over the past five years in both revenue and staff, employing more than 130 people.

But Mr Ringin‘s secret to success is simple – to seize any opportunity when it comes.

“One of our clients had a need for a mining provider when their current mining provider left,” he said after receiving the top honour.

“We stepping in without any right to be doing that, and delivered a mining program for six months to an exceptional standard that taught us we can deliver other disciplines as well.”

Using a people-first approach, Mr Ringin continues to build his local workforce and create opportunities for both Indigenous and non-Indigenous remote youth through apprenticeships, TAFE and community partnerships.

“We are a people business and we trade in time but our product is trust, and this represents that,” Mr Ringin said.

First Amongst Equals finalists Jessica Wilson, Ben Smith and Kyle Hoath missed out on the top honour, but all won in other categories.

Ms Wilson, a Yindjibarndi and Njamal entrepreneur and artist, took home the Indigenous Business award.

As the founder of Seven Sisters Collective, she helps find opportunities for Indigenous artists on large projects and builds education among businesses.

After a career spanning hyper-growth consumer brands, Mr Smith’s leadership as chief executive of alcohol, drug and mental health support provider Holyoake earned him the Community, Social Enterprise or Not for Profit award.

And Dr Hoath, a defining voice in the state’s medical and civil leadership, won the Small or Start-Up Business award.

The consultant psychiatrist and newly elected President of the Australian Medical Association WA co-founded Oqea – a technology platform modernising mental health care.

The Pantry Group founder Sam Kaye was recognised with the People’s Choice award – recognising his journey which went from working at Daisies Cottesloe to owning the cafe alongside three other hospitality venues.

The other major category winners include:

You can read more about each of the winners in the May 18 edition of Business News’ print magazine, which will also be available online.

Congratulations to all of 2026’s 40under40 winners:

Jessica Wilson: Seven Sisters Collective

Sam Kaye: The Pantry Group

Zoran Aleksic: PCH Civil

Stephen Tormey: Bennco Engineering

David Gozzard: The University of Western Australia

Justin Barnes: Rocket Launcher

Tandin Dorji: Kingston International College

Joshua Wigley: Hyperion Systems

Mathew Wilson: Wilco Maintenance Solutions

Rowan Streater: Mayfair Building Co

Kane Smith: Smartfix

Alastair Mackenzie: Buddiup

Benn Ellard: White Spark Pictures / Surround Sync

Jo Gibb: Coliving Collective

Mark Bond: Consolidated Electrical Solutions

Luke Whelan: Perth is OK! / Social Meteor

Michael Agostino: Trendsetter Homes / Select Living

Damien Wragg: Trainwest

Ashley McGrath: CEOs for Gender Equity

Isabelle Charter: Betterlabs

Jeroen van Dalen: Integral Development Associates

Catherine Hyde: Amity Resources

Rachel Falzon: Women in Defence Association

Eli Barlow: Funday Entertainment Group / Lavender Estate

Jonathan Cover: JPS Management and Execution / Safe Isolation Australia

Mark D’Alessandro: Contec Australia / JCM Property Group

Samantha Johnson: Sexual Health Quarters

The S&P 500 and the Nasdaq have advanced to record closing highs, boosted by robust earnings and a dip in crude prices.

The Investment Doctor is a financial writer, highlighting European small-caps with a 5-7 year investment horizon. He strongly believes a portfolio should consist of a mixture of dividend and growth stocks.

He is the leader of the investment group European Small Cap Ideas which offers exclusive access to actionable research on appealing Europe-focused investment opportunities not found elsewhere. The a focus is on high-quality ideas in the small-cap space, with emphasis on capital gains and dividend income for continuous cash flow. Features include: two model portfolios – the European Small Cap Ideas portfolio and the European REIT Portfolio, weekly updates, educational content to learn more about the European investing opportunities, and an active chat room to discuss the latest developments of the portfolio holdings. Learn more.

Analyst’s Disclosure: I/we have a beneficial long position in the shares of BAC either through stock ownership, options, or other derivatives. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

I also have a long position in BAC.PR.L. I may add to both positions, but this is unlikely to happen in the next 72 hours

Seeking Alpha’s Disclosure: Past performance is no guarantee of future results. No recommendation or advice is being given as to whether any investment is suitable for a particular investor. Any views or opinions expressed above may not reflect those of Seeking Alpha as a whole. Seeking Alpha is not a licensed securities dealer, broker or US investment adviser or investment bank. Our analysts are third party authors that include both professional investors and individual investors who may not be licensed or certified by any institute or regulatory body.

Q1: 2026-04-29 Earnings Summary

EPS of $4.17 misses by $0.16

| Revenue of $2.44B (9.84% Y/Y) misses by $65.83M

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

A $2 billion investment in housing promises to ensure young people have the opportunity to buy a home, with 34,000 new dwellings to be built.

Ronojoy Banerjee

Communications Lead – Finance

Good morning, and a very warm welcome to this Volvo Cars press conference, where we will be talking about our first quarter financial results and our strategic direction as a company.

My name is Ron. And as always, this morning, I’m joined by our President and Chief Executive, Hakan Samuelsson; our Chief Financial Officer, Fredrik Hansson; and we’re also joined by our Chief Commercial Officer, Erik Severinson. At the start of this press conference, Hakan, Erik and Fredrik will walk us through our performance. And thereafter, we’ll throw it open for a question-and-answer round.

You can participate in the Q&A around in two ways. [Operator Instructions ] I’ll come back with more information ahead of the Q&A round.

But for now, I’ll hand it over to you, Hakan.

Hakan Samuelsson

CEO, President & Director

Thank you, Ron, and welcome to the presentation of our quarter 1 result. It has been a mixed bag quarter. I mean external factors, extremely turbulent geopolitical situation, tariffs, currency also has been negative for us. Altogether, that has given us a revenue drop of 12%, 11% volume drop.

But we have also seen a very successful internal work with cost and cash. And that is really the reason why we have closed the quarter. Despite 11% volume drop, we have a profitability level more or less equal to first quarter last year. And that is thanks

Abel took a moment to reflect on Berkshire’s values. He started by talking about a letter he sent to the company’s 400,000 employees when he took over as CEO in January.

The letter, he said, talked about how important Berkshire’s values were–and are. Integrity is at the top of the list.

Then, Abel cut to a video of Buffett’s 1991 testimony to Congress, which Abel called “Berkshire’s anthem.”

Abel said Berkshire’s insurance underwriting results benefited from light catastrophes in the first quarter. He added that property and casualty market conditions are becoming more “challenging” in what insurers call a softening market. He’s echoing comments from other insurers recently.

Q1: 2026-04-29 Earnings Summary

EPS of $5.11 beats by $2.48

| Revenue of $109.90B (21.79% Y/Y) beats by $2.86B

Seeking Alpha’s transcripts team is responsible for the development of all of our transcript-related projects. We currently publish thousands of quarterly earnings calls per quarter on our site and are continuing to grow and expand our coverage. The purpose of this profile is to allow us to share with our readers new transcript-related developments. Thanks, SA Transcripts Team

#SpiritAirlines is facing potential collapse after years of financial pressure. #airlines #ustravel

Games Inbox: What’s the best video game to play when it’s sunny?

Dredge does the dirty work, makes it pay

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

#SpiritAirlines is facing potential collapse after years of financial pressure. #airlines #ustravel

NYC Mayor Zohran Mamdani Slams Trump | The Financial Disaster Hidden Behind The War | 99TV

Bitcoin Going to $15k – TA Expert Says Crash Is Just Getting Started | Jason Pizzino

-

Tech6 days ago

Tech6 days agoRegister Renaming | Hackaday

-

Politics6 days ago

Politics6 days agoDrax board avoid their own AGM, accused of greenwashing & environmental racism

-

Fashion5 days ago

Fashion5 days agoKylie Jenner’s KHY Enters a New Era with ‘Born in LA’

-

Tech7 days ago

Tech7 days agoWhy Blue Badges Disappeared From Toyota Hybrids

-

Tech6 days ago

Tech6 days agoImages of Samsung’s rumored smart glasses have leaked

-

Tech2 days ago

Tech2 days agoTrump’s 25% EU auto tariff breaches Turnberry Agreement that also covers semiconductors and digital trade

-

NewsBeat8 hours ago

NewsBeat8 hours agoChannel 5 – All Creatures Great and Small series 7 new post

-

Business5 days ago

Business5 days agoMost Commercial Energy Audits Miss the Real Losses

-

Business7 days ago

Business7 days ago(VIDEO) Charlize Theron Climbs Times Square Billboard to Promote New Netflix Thriller ‘Apex’

-

Crypto World6 days ago

Crypto World6 days agoCFTC’s AI will review U.S. crypto registration applications, chairman tells CoinDesk

-

Sports2 days ago

Sports2 days agoPaul Scholes issues Marcus Rashford reality check as agreement emerges over Man United star

-

Business5 days ago

Business5 days agoBarclay Brothers Avoid Bankruptcy: HSBC Drops High Court Petitions After IVA Deal

-

Business4 days ago

Business4 days agoTesla Officially Registers Elon Musk’s Stock: What Investors Need to Know

-

Entertainment7 days ago

Entertainment7 days agoAlicia Keys Calls Out Music Industry ‘Boys Club’

-

Tech5 days ago

Tech5 days agoGet Ready for More Brain-Scanning Consumer Gadgets

-

Crypto World6 days ago

Crypto World6 days agoRobinhood Phishing Scam Exploits Gmail Dot Feature to Bypass Security

-

Entertainment6 days ago

Entertainment6 days agoSister Wives: Janelle Posts New Scary Warning

-

Crypto World6 days ago

Crypto World6 days agoGmail Dot Trick Underpins Robinhood Phishing, Sending Real-Looking Emails

-

Business3 days ago

Business3 days agoTwo Powerball Tickets Split $143 Million Jackpot in Indiana and Kansas

-

Tech7 days ago

Tech7 days agoThe next iPhone moment might come from an AI company, not Samsung or Apple

You must be logged in to post a comment Login