Editor’s note: This article is intended to provide a general overview of the ETF for educational purposes only and, unlike other articles on Seeking Alpha, does not offer an investment opinion about the ETF.

Business

Understanding WQTM: Investing In The Quantum Computing Opportunity (BATS:WQTM)

onimate/iStock via Getty Images

The WisdomTree Quantum Computing Fund ETF (WQTM) is an exchange-traded fund that aims to give investors access to a diversified portfolio of companies engaged in, or with exposure to, various aspects of quantum computing, such as the development of quantum hardware and software, enabling technologies, and necessary supporting infrastructure.

What Is WQTM?

WQTM is a U.S.-listed thematic equity ETF designed to provide investors with targeted exposure to companies participating in the emerging quantum computing ecosystem. WQTM started trading on October 9, 2025, and seeks to track the WisdomTree Classiq Quantum Computing Index, which was created through a collaboration between WisdomTree and Classiq, a quantum software firm. The investment strategy outlined by WisdomTree covers quantum hardware, quantum software, quantum infrastructure, and enabling technologies, as well as companies that focus on quantum technology and larger companies that offer a diversified range of technologies.

WQTM is essentially a frontier-technology fund, not a broad technology ETF or a simple semiconductor or AI proxy. It is instead designed to capture companies associated with the long-term commercialization of quantum computing through its mandate. While this is potentially appealing, it is also speculative because quantum computing is new, and most of its business models are still developing rather than mature.

What Does the Wisdom Tree Quantum Computing Fund Offer Investors?

Instead of forcing investors to pick specific quantum-related stocks on their own, the WQTM ETF is designed to provide exposure to a rules-based basket of companies that WisdomTree views as relevant to the quantum value chain. As a result, this fund is primarily for capital appreciation, with a distribution yield of 0.00%, and not for income purposes.

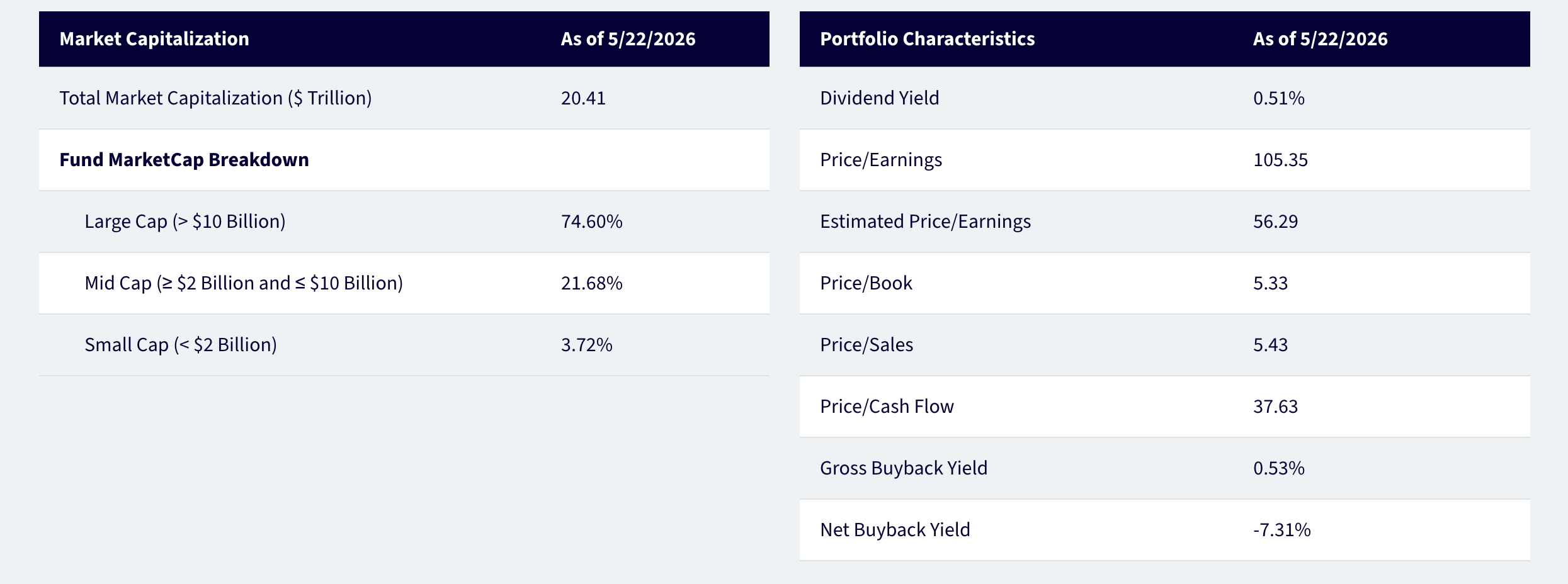

WQTM’s Market Capitalization and Portfolio Characteristics (WisdomTree Product Sheet)

As the portfolio exhibits a financial profile consistent with a high-growth thematic strategy, WisdomTree’s reported portfolio characteristics reflect higher valuation metrics, including a price-to-earnings ratio greater than 100 and an estimated price-to-earnings ratio greater than 50, based on the underlying holdings. This does not mean the fund is unattractive; however, it does raise the bar for future growth.

As of May 22, 2026, WisdomTree reported that roughly three-quarters of the fund’s market-cap exposure was to large-cap stocks, with most of the remainder in mid-cap names. This large-company focus may lessen some of the single-company risks inherent in fully speculative technology plays. All the same, this does not remove thematic risk. Should enthusiasm for quantum computing wane, or should commercialization take longer than expected, WQTM could experience volatility.

Who Might Consider WQTM?

WQTM may work for investors with broad-based, diversified core positions who want a more specific satellite investment in a long-duration technology theme. WQTM is best considered a focused, specialized investment rather than a substitute for a broad stock-market fund. It gives investors more direct exposure to quantum computing than many traditional technology ETFs.

The fund may be most relevant for investors who expect quantum computing research and experimentation to ultimately trend toward commercial adoption but prefer diversified ETF exposure rather than individually selecting particular companies or stocks. The fund may also suit investors who are prepared to bear early-stage uncertainty, high valuations, and limited operating history at the fund level. As WQTM is newly created, it has a very limited performance history.

More cautious investors, investors looking for income, or investors who are not comfortable with big price swings may find WQTM too focused or too risky.

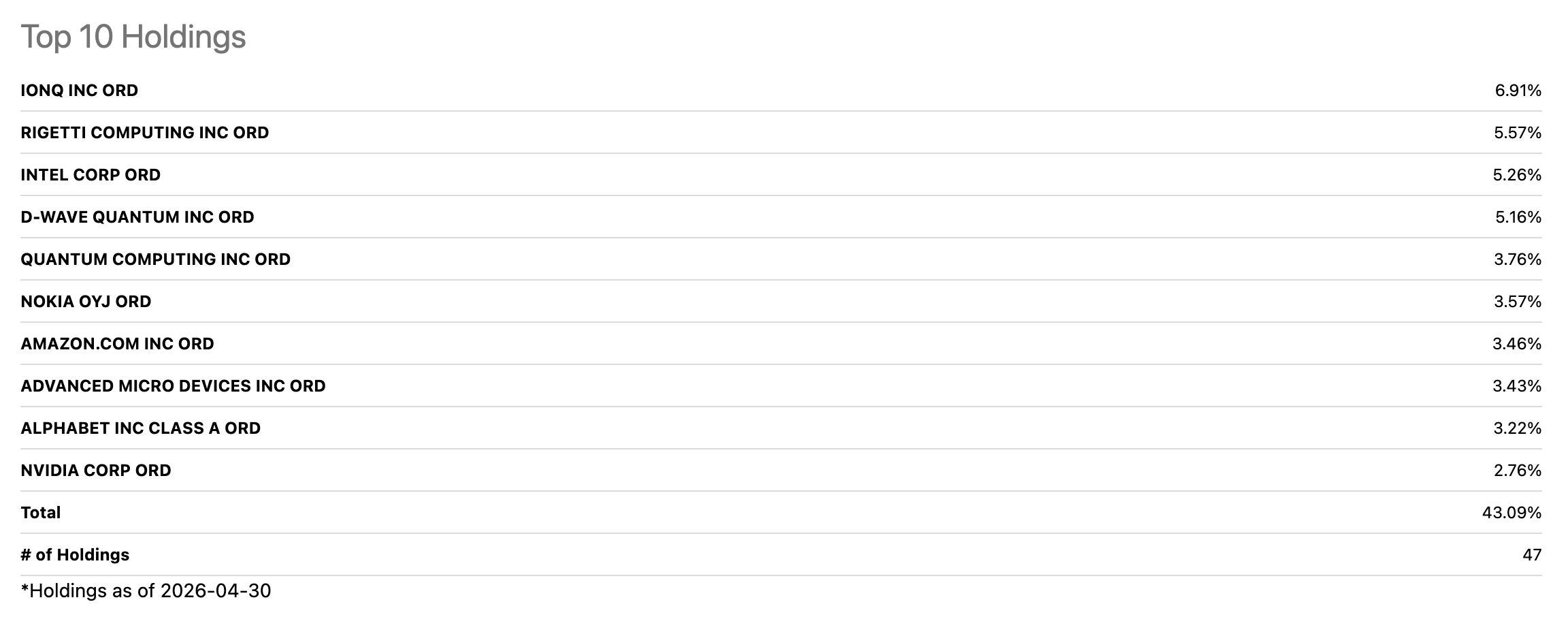

What’s Inside WQTM? A Closer Look at Its Top Holdings

WQTM’s Top 10 Holdings (Seeking Alpha )

1) IonQ Inc. (IONQ) – 6.91%

The largest company held by WQTM is IonQ, making it one of WQTM’s most direct connections to the stand-alone quantum computing industry. IonQ is focused on developing trapped-ion quantum systems, offering cloud-based access to quantum computers, and developing business applications for quantum computing. This makes it more closely connected to the quantum-computing theme than other larger and more diversified technology companies included in the fund.

2) Rigetti Computing Inc. (RGTI) – 5.57%

Rigetti Computing is a quantum-computing company focused on building quantum-computer hardware. The company produces superconducting quantum processors and supplies quantum systems to local research organizations, national laboratories, and quantum research centers. The reason Rigetti has such appeal as a stock investment is that it is directly addressing one of the largest obstacles facing quantum computing right now: hardware.

3) Intel Corp. (INTC) – 5.26%

Intel contributes to WQTM through a distinct type of exposure. Although Intel is not considered a pure quantum computing business, it has still made itself valuable to the overall quantum-computing market through its role in the semiconductor manufacturing industry, its lengthy history in chip design, and its extensive research and development activities.

4) D-Wave Quantum Inc. (QBTS) – 5.16%

Over several years, D-Wave has remained commercially active in quantum systems. The company is primarily associated with quantum annealing, a specialized approach aimed at solving optimization-based problems; yet, D-Wave has also positioned itself as a company focused on providing enterprise-level services and developing applications based on quantum technologies.

5) Quantum Computing Inc. (QUBT) – 3.76%

Quantum Computing Inc. is a higher-risk stock, as it is a smaller and more volatile company that adds another level of pure-play exposure to the quantum computing sector. The company develops integrated photonics-based quantum computers for use in computing, artificial intelligence, cybersecurity, and sensing. While the company’s progress is notable, it remains early-stage by public-market standards.

6) Nokia Oyj (NOK) – 3.57%

Nokia may seem less obvious at the outset, but its inclusion in the fund reflects quantum’s involvement with networks, security, and advanced communications through Bell Labs and its related research activities. It gives the fund exposure to quantum-computing infrastructure and related research. This can help balance out the smaller, riskier companies in the fund that focus more directly on quantum computing.

7) Amazon.com Inc. (AMZN) – 3.46%

Thanks to its cloud infrastructure and quantum access, Amazon.com gives WQTM exposure to quantum computing. The Amazon Braket managed service allows researchers and developers to run experiments on quantum computers, use simulators, and run hybrid workflows through AWS.

8) Advanced Micro Devices Inc. (AMD) – 3.43%

Within the context of an enabling technology company, AMD fits WQTM because of its position in supporting quantum innovation through the use of its chips, GPUs, FPGAs, and system components in high-performance computing environments. These technologies allow scientists to simulate, control, and integrate quantum workloads. AMD is not selling a mainstream quantum computer. Nevertheless, progress in quantum computing may still depend on the powerful traditional computing technology that AMD provides.

9) Alphabet Inc. Class A (GOOG) – 3.22%

WQTM has access to one of the deepest corporate quantum research initiatives globally through Alphabet’s Class A shares. Google Quantum AI is focused on developing large-scale, error-corrected quantum computers, and Alphabet has positioned itself as a serious long-term competitor in quantum computing. Alphabet is certainly not a pure-play quantum stock. Advertising, cloud, and its other businesses account for the majority of its earnings. However, the research being done in quantum computing provides investors with meaningful research-backed exposure.

10) NVIDIA Corp. (NVDA) – 2.76%

NVIDIA’s place in the top ten is representative of acceleration rather than direct quantum ownership. Its CUDA-Q platform allows quantum processors to connect with both GPUs and CPUs, allowing developers to create hybrid quantum-classical applications before fully mature quantum hardware exists. Quantum computing will most likely need classical computing for simulation, control, and error correction.

WQTM Performance Overview

WQTM’s Momentum Stats (Seeking Alpha)

The data signals to investors that WQTM is a newer ETF with strong near-term momentum, reasonable fees, and a risk profile with many unknowns. The most recent returns are likely what will primarily catch investor attention, as they have been very large for an exchange-traded fund. The one-month return of 22.24% and six-month return of 58.31% are extremely high compared to median returns for other ETFs of 1.34% and 9.58%, respectively. Additionally, the YTD price return of 48.03% is significantly greater than the S&P 500’s (SP500) gain of 9.17%.

WQTM’s Momentum Stats (Seeking Alpha)

Basically, WQTM is built to capture one specific technology theme. When that theme is working, the returns can move quickly. The one-week price return of 12.64% makes that clear.

Market sentiment can change quickly in favor of high-growth tech, speculative innovation, and quantum-related stocks, which may lead to a sharp rise in WQTM and therefore a significant return. Nonetheless, the downside also cuts both ways.

WQTM Dividend Scorecard

The fund’s lack of a dividend also clarifies how it should be viewed. Instead, most of the potential return depends on the fund’s price going up. This is common for funds focused on emerging technologies.

WQTM: Expenses

WQTM’s Expense Stats (Seeking Alpha)

0.45% is a fair expense ratio for a specialized thematic ETF, and it falls below the 0.50% median for all ETFs. Most thematic funds will have higher fees than broad-index ETFs, and these higher costs can reduce returns over time.

State Street SPDR S&P 500 ETF Expenses (Seeking Alpha)

In this case, it will not be as cost-effective as a broad-based S&P 500 ETF (SPY). Investors are essentially paying for narrow exposure to a particular idea rather than basic market exposure.

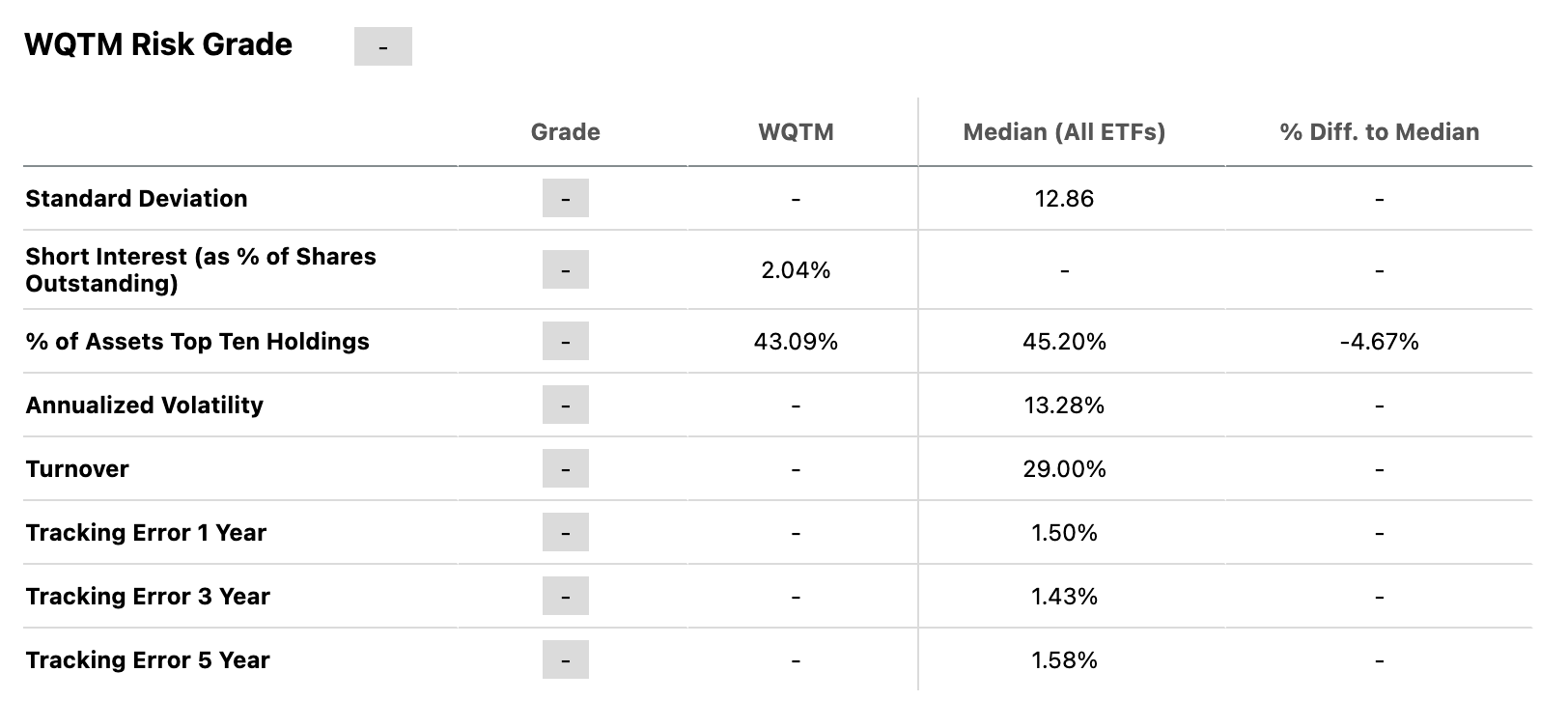

WQTM: Risks

Here are the downsides to WQTM: risk metrics are mixed and incomplete. Standard deviation, annualized volatility, turnover, and tracking error are missing, making it difficult to assess the level of risk with the same confidence as a traditional ETF that has existed for many years.

WQTM’s Risk Metrics (Seeking Alpha)

Even so, we do have a concentration figure. The top ten holdings represent 43.09% of the fund’s assets, which is just under the overall ETF median of 45.20%. Therefore, while WQTM does not seem to be especially concentrated when compared to other ETFs, this may not be a good comparison for evaluating WQTM because many of its top ten holdings have similar investment themes.

Short interest at 2.04% of shares outstanding is not a high percentage. Nevertheless, it is enough to show that some investors have taken positions against the ETF. It suggests these investors are either hedging their exposure to the fund or speculating that there may be a downturn. This does not prove that investors are becoming strongly negative on WQTM. Notwithstanding, it does show that the market is not treating WQTM as a safe, widely agreed-upon investment.

Should You Invest In WQTM?

Investors interested in having a small slice of quantum computing without picking their own quantum stocks can use WQTM. Although quantum computing is still an early-stage technology, it is making progress. The best opportunity to take advantage of WQTM investments may come if you have already built an established, diversified portfolio and are comfortable with the possibility that this investment may drop sharply and stay down for an extended period during the time required for the fund’s strategy to prove itself, which may take years. WQTM provides no meaningful income. Therefore, if you need a source of dividend income or steady returns, you may need to find other investment vehicles.

This article answers three main questions about WQTM:

- What are the benefits and risks of investing in WQTM?

- How volatile is WQTM compared to the overall market?

- Are there concentration risks with WQTM?

Continue Reading

Cardiff-based edtech venture GroupEd said that closed frameworks are locking many Welsh SMEs out of Welsh public sector contracts

GroupEd

An education software company is calling on the Welsh Government to support indigenous firms by ending a practice of public bodies in Wales procuring through closed frameworks in England.

Cardiff-based GroupEd said its growth trajectory has been affected by a growing number of Welsh councils opting to procure management information systems (MIS) software via Kent County Council’s arm’s-length procurement vehicle, KCS Procurement Services.

Under these arrangements, Welsh councils can award contracts directly to suppliers already listed on a closed framework, with no obligation to run an open competition or invite Welsh businesses to bid.

GroupEd said frameworks are opened to new applicants only intermittently, and in some cases not for years, meaning companies offering better technology and better value for money are structurally barred from consideration. GroupEd said the earliest opportunity to join the KCS education software framework is 2030.

The company said the practice is at odds with Welsh legislation in the Procurement (Wales) Act 2023 and the Procurement (Wales) Regulations 2024, which it says place clear duties on Welsh public bodies to maximise spending with Welsh businesses and consider the wider economic impact of their purchasing.

Yet it added when councils use closed English frameworks – classified as “reserved procurement arrangements” under Welsh law – those duties do not apply to the original supplier selection, which was conducted under UK Government rules, leaving “Welsh SMEs without any meaningful seat at the table.”

According to GroupEd, of the 455 approved suppliers across all 50 KCS frameworks, only two are headquartered in Wales, representing just 0.4% of the total supplier base. Of the 12 framework categories, 10 contain no Welsh suppliers.

The two Welsh businesses are listed on the highways (signage) and people and professional services (training) frameworks. GroupEd said there are no Welsh firms on other categories, including technology, education, legal services, ICT and facilities management.

Cerys Furlong.

Chief executive of GroupEd, Cerys Furlong, said: “Our founders have invested millions of pounds into building world-class software for Welsh schools and created highly skilled jobs here in Wales. The irony is that several Welsh councils conducted their own open procurement processes, showing it is possible.

“But too many others are defaulting to a closed English framework because it requires the least effort from their procurement teams. That may be convenient for councils, but it means Welsh public money is flowing to places like Kent invisibly, year after year, while better and cheaper Welsh alternatives are locked out entirely.”

GroupEd is calling on the new Welsh Government to issue a formal direction stating that closed English frameworks should not be used where open Welsh procurement would satisfy the requirement.

It also says the new administration should:

- Engage directly with Section 151 officers and local authority procurement teams on the true cost of closed frameworks, including management fees, compared with open Welsh tenders.

- Establish an accountability mechanism to monitor compliance; and

- Provide a public register showing which Welsh public bodies are using reserved procurement arrangements, and why.

Ms Furlong said: “We are not asking the new Welsh Government to do something difficult. We are asking it to enforce a law it already has, act on a manifesto it has just won, and send a signal that Welsh public money belongs in Wales. A closed framework has no mechanism for merit – it simply reflects who was in a room somewhere in England years ago. The new government has the power to end that. We are watching to see if it will.”

Despite the framework challenge, GroupEd, founded by Andrew Cooksley, who also established leading training provider ACT, is aiming to have its software platform in 10,000 schools by 2030. It is also pursuing international expansion.

In its Senedd manifesto, Plaid Cymru committed to increasing Welsh public procurement spending with Welsh SME suppliers from 55% to at least 70% over the next four years, with a stated aim of creating more than 35,000 new jobs.

However, Plaid has not clarified what jobs could be lost among non-Welsh SMEs and Welsh corporates that currently provide publicly procured contracts, nor has it estimated how many staff could transfer from existing suppliers to new providers under TUPE rules.

Responding to the concerns raised by GroupEd, a Welsh Government spokesman said: “We want to increase the local economic impact of public procurement in Wales — currently worth more than £11bn a year — to embed that economic activity in Wales, supporting our home-grown small and medium-sized businesses.

“Schools, colleges and local authorities have the discretion to enter into contracts of their own choice with third-party suppliers in order to meet and support their own data needs and ensure they can meet their statutory obligations. We do not advocate any single supplier so that there is competition in the market and schools and local authorities are able to attain the best contractual terms and conditions for their needs.”

The Welsh Government liaises with school and local authority software suppliers through the Software Development Forum (SDF), which usually meets three or four times a year to discuss technical specifications for statutory data collections and other ways in which systems support schools’ obligations. GroupEd is a member of the forum.

A spokesman for the Welsh Local Government Association said: “Councils use a range of procurement routes, including frameworks, to secure value for money and meet local needs. Councils are committed to supporting Welsh businesses and supply chains, and recent procurement reforms, including open frameworks and dynamic markets, are intended to improve SME access.

“Frameworks can offer important efficiencies, but they must be designed and used in ways that reflect Welsh priorities, support fair competition and deliver the best outcomes for communities.”

Oracle has cut around 21,000 roles worldwide over the past year, a stark sign of how quickly artificial intelligence is reshaping the cost base of the world’s largest technology firms, the US software and cloud computing giant’s latest annual report shows.

The company employed roughly 141,000 full-time staff as of 31 May 2026, down from about 162,000 a year earlier, according to Reuters. The reduction amounts to roughly 13 per cent of its global workforce.

In unusually candid language, Oracle told investors that the “deployment of AI technologies across our operations have resulted, and may continue to result, in reductions to our workforce”. The admission, buried in the firm’s annual filing, makes Oracle one of the few blue-chip employers to explicitly link headcount cuts to automation rather than the usual corporate shorthand of “efficiency” or “streamlining”.

The cuts have not come cheap. Oracle said it booked about $1.8bn (£1.36bn) in severance and other restructuring costs over the year, nearly five times the $374m it spent the year before. The figures are set out in the company’s annual report filed with the US Securities and Exchange Commission.

The bulk of the reductions appear to have landed in April, when senior employees began posting online about “significant” job losses, though the full scale only became clear once the annual report was published.

Oracle was careful to flag the risks. It acknowledged that the reorganisation “can be disruptive” and warned that thinning out certain teams could leave it short of skilled workers in particular roles, denting productivity and, ultimately, earnings.

The pattern at Oracle, cutting people while pouring money into machines, is becoming the defining trade-off of the AI era. The company has been racing to build data centres for the likes of OpenAI and Meta, and plans to spend at least $50bn on infrastructure this year alone. Co-founder Larry Ellison, one of the world’s richest people and the group’s chief technology officer, has staked Oracle’s future on becoming the plumbing behind the AI boom.

For a sector where staff are typically the single biggest expense, the maths is increasingly hard to ignore. Across the industry, more than 100,000 technology workers have lost their jobs in the past year, according to employment trackers, even as the giants commit eye-watering sums to the technology. Google, Amazon and Meta alone plan to invest some $650bn between them this year.

Oracle is far from alone. Facebook-owner Meta has been cutting roles while ramping up its AI budget, as Business Matters reported when Meta moved to axe 8,000 jobs to fund its $145bn AI push. Amazon, meanwhile, has signalled the deepest cuts of all, with plans to shed around 30,000 corporate roles in several rounds, detailed when the retailer axed 16,000 jobs to “remove bureaucracy”. Amazon, which employs more than 1.5 million people globally, intends to spend $200bn on AI over the next year, the largest commitment of any big technology company.

A senior Amazon executive captured the prevailing mood in an internal note last October, arguing that the company needed to be organised “more leanly” because AI was “enabling companies to innovate much faster than ever before”.

For all the talk of innovation, the human cost is mounting, and it is being felt well beyond Silicon Valley boardrooms. The squeeze is now reaching the bottom of the career ladder too, with entry-level vacancies in the UK down by almost a third since ChatGPT launched. Oracle’s frank acknowledgement that AI is directly displacing workers may prove a watershed: where one of the world’s most powerful software firms leads in its disclosures, others may feel obliged to follow.

The question for businesses watching from the sidelines is no longer whether AI will reshape their workforces, but how openly they are prepared to say so.

Amy Ingham

Amy is a newly qualified journalist specialising in business journalism at Business Matters with responsibility for news content for what is now the UK’s largest print and online source of current business news.

Business

Vedanta Power, Oil & Gas, and Iron shares rally up to 5%; Aluminium sheds 3%. Should you buy, sell or hold?

Shares of Vedanta Oil & Gas, Vedanta Iron & Steel and Vedanta Power, which were recently spun off from Vedanta following the demerger, surged up to 5% on Tuesday, extending their winning streak to six consecutive sessions.

Among the demerged entities, Vedanta Oil & Gas hit its 5% upper circuit at Rs 36.40 on the BSE, while Vedanta Power was also locked in the 5% upper circuit band at Rs 45.25. Vedanta Iron & Steel, the best-performing stock among the spun-off businesses since listing, extended its winning streak to a sixth straight session and traded at its 5% upper circuit limit of Rs 28.10.

In contrast, Vedanta Aluminium Metal, often regarded as the group’s crown jewel, declined 3.3% to Rs 464.

Which stock are you betting on?

Last week, Citi initiated coverage on Vedanta Aluminium shares with a ‘Buy’ rating and a target price of Rs 560 apiece, naming the newly listed stock its top Indian metals pick. The latest target price implies an upside potential of more than 17% from the stock’s previous closing price.Citi listed key drivers for its bullish call, which include a positive aluminium outlook, growth potential (Balco expansion, Vedanta Aluminium debottlenecking), cost focus (higher captive alumina, domestic bauxite and captive coal), and improving leverage. It expects the company to have a net cash position by FY28.

Expecting aluminium prices to hover around $3,400 in FY27-28, Citi explained that every $100 per ton change in LME can impact the company’s EBITDA by 4-5.5%, and subsequently fair value by nearly Rs 30 per share. “We open a 90-D positive CW: Our commodities team believes the aluminium market is in deficit and will draw inventories sharply over the next 3-6 months, driving prices up 15-20% to $4,000 per ton in the base case,” it added.

Also read: Vedanta Aluminium vs Power vs Oil & Gas vs Iron & Steel: Which stock should you buy?

Vedanta Oil & Gas share price

According to Sunny Agrawal, Head of Fundamental Research at SBI Securities, Vedanta Oil & Gas commands a fair value of Rs 42 per share.

Vedanta Oil & Gas, which houses Cairn Oil & Gas, claims to be India’s leading private-sector upstream player and is targeting production of 300,000 to 500,000 barrels per day through a planned investment of $5 billion. “A little over a decade ago, Cairn was valued at $14.5 billion. When we acquired Cairn, its market capitalisation was half of the asset value. Today, Cairn has grown manifold, adding more reserves as well as a natural gas portfolio,” the company had said in a press release earlier this year.

Vedanta Power share price

Brokerages remain divided on valuations for Vedanta Power. Domestic brokerage Emkay estimates a value of around Rs 51.7 per share, while Kotak Institutional Equities pegs it at Rs 60 per share. Nuvama’s valuation implies a value of around Rs 47 per share, while CLSA’s estimate corresponds to roughly Rs 35 per share.The company has more than 4 GW of installed power generation capacity across Punjab, Andhra Pradesh, Chhattisgarh and Odisha. Its portfolio includes the Talwandi Sabo Thermal Plant, Meenakshi Energy, Sakti Power and the Jharsuguda Thermal Plant.

Management has outlined plans to become one of India’s top three private thermal power producers by FY33 through capacity expansion and asset turnarounds. The business also benefits from several long-term and medium-term power purchase agreements with state utilities, providing a degree of revenue visibility.

Read more: Vedanta demerger: How will the mega restructuring impact dividend payouts for shareholders?

Vedanta Iron and Steel share price

The company’s share price has recorded the sharpest gains so far among the four Vedanta Group companies, rallying for a sixth consecutive session. Vedanta Iron & Steel has operations spanning India and Africa and focuses on iron ore exploration, mining, and processing. It also produces high-quality steel, wire rods, TMT bars, pig iron, ductile iron (DI) pipes, ferro-silicon, cement and metallurgical coke.

Sunny Agrawal said that Vedanta Iron & Steel offers cyclical upside and carries higher commodity and execution risks, especially given weaker listing traction and greater earnings volatility. Hence, on a forward SOTP basis, Aluminium stands out as a structural compounder with favourable operating leverage, while the rest are more tactical or cyclical plays.

Vedanta block deal

Billionaire Anil Agarwal-led Vedanta fell 6% on Tuesday after media reports claimed that promoter entity Twin Star Holdings likely pared its stake through a block deal. About 7.3 crore shares worth Rs 2,149 crore changed hands at Rs 292 apiece in the transaction.

The Economic Times couldn’t verify the buyers and sellers in the transaction. Twin Star Holdings is Vedanta’s largest promoter shareholder, holding a 40% stake in the company as of March 31, 2026. The overall promoter group owned 56.38% of Vedanta at the end of the March quarter. The number of shares that changed hands amounts to 1.7% of the company’s outstanding equity.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of The Economic Times)

India’s rural economy may not be as strong as headline wage numbers suggest. While official data indicates a sharp rise in rural wages, a closer look reveals that the improvement may largely be the result of statistical changes rather than genuine income growth. According to Dhananjay Sinha from Systematix Group, the combination of weaker wage growth, rising inflation, reverse migration, and an uncertain monsoon could create fresh challenges for rural demand and consumer-focused companies.

Sinha said his team’s analysis of Labour Bureau data found that the reported 17% year-on-year increase in rural wages for March 2026 was misleading because of changes in the government’s sampling methodology.

“The underlying wage growth could be in the region of 4-4.2% instead of 17%. This 17% essentially comes on the back of additional coverage of north-eastern states, Delhi, and Goa, where the average wages are 50% higher than the earlier sample. Adjusting for that, we find a concerning trend, and the wage and income situation in rural areas might be much more modest compared to what the headlines are actually telling us,” he said.

He added that the slowdown in wage growth had emerged even before the recent geopolitical tensions in West Asia. According to him, higher living costs in cities have encouraged workers to return to rural areas, increasing dependence on agriculture, which typically offers lower productivity and income than urban employment.

“Because of the rise in the urban cost of living, there has been reverse migration from urban centres to rural areas. There is increased dependence on agriculture, which is less productive compared to urban occupations. This will likely impact the rural demand scenario,” he said.

Sinha warned that the improving volume growth seen by consumer companies in the previous quarter may not be sustained. He believes companies have started raising product prices as input costs increase, while slowing wage growth and rising inflation could squeeze consumers’ purchasing power.

“A combination of higher end-product prices, decelerating nominal wage growth, and inflation starting to rise might imply negative or flat real wage growth. You have rising prices and real wages actually coming down. This combination will impact the profitability and volume growth of consumer companies.”On inflation, Sinha said rising fuel prices are already pushing up the cost of living, adding that shortages of LPG have further intensified price pressures.

“Because of the LPG crisis and shortages, prices have informally gone up by almost four times. Generally, because of the increase in fuel prices, there is a generalised inflation, and we are seeing that in the numbers as well.”

He also cautioned that delayed monsoon rains and El Niño conditions could add another layer of stress to rural incomes. Lower rainfall could reduce cultivation acreage and agricultural productivity, making government support even more important.

“There has been a deficiency of almost 40% in the monsoon during the first month. Lower acreage under cultivation and higher dependence on agriculture could reduce productivity, and it will require governments to provide larger support in rural areas,” he said.

Discussing labour migration, Sinha noted that workers returning to villages are largely coming back from regions where wages are significantly above the national average, including Kerala, Delhi-NCR, Goa, and parts of the North-East. This, he said, could weaken household incomes and reduce remittance flows to rural families.

“The reverse migration is essentially happening from urban centres that have higher wages. This will have a significant impact on workers’ earnings and remittances. It is quite likely that, as we enter July or thereabouts, wage growth could actually come down close to zero. That is a concern that I have for the rural demand scenario,” he said.

The findings suggest that while official wage data paints a picture of robust rural recovery, underlying income trends remain fragile. If inflation continues to accelerate, rainfall remains below normal, and migration trends persist, rural consumption could face renewed pressure in the coming quarters, posing challenges for companies that rely heavily on demand from India’s villages.

Jefferies has initiated coverage on GE Vernova T&D with a Hold rating, while reiterating its bullish stance on Hitachi Energy India and Siemens Energy India on the back of a multi‑year upcycle in power transmission capex and outsized earnings growth visibility for the latter two names.

Jefferies’ call: Hold on GE Vernova, Buy on Hitachi and Siemens

Jefferies has started coverage on GE Vernova T&D India (GE Vernova) with a “Hold” and a target price of Rs 6,000 per share, implying limited upside from the current levels and valuing the stock at 65 times FY28 estimated earnings. In contrast, the brokerage has retained “Buy” ratings on Hitachi Energy India and Siemens Energy India, with target prices of Rs 43,145 and Rs 4,500 per share, respectively, both implying around 17% upside.

“We retain Buy on Hitachi Energy (Hitachi) and Siemens Energy (SE) given their strong 40%+ earnings CAGR on operating leverage backed by strong revenue visibility. We initiate coverage on GE Vernova T&D (GE) with a Hold,” Jefferies said.

Jefferies expects GE Vernova to deliver about 35–36% EPS CAGR over FY26–29E, but sees even faster profit compounding in Hitachi and Siemens, which justifies higher or similar multiples and a more constructive rating on those stocks.

The house view is anchored in a strong and prolonged capex cycle in India’s power transmission and distribution segment, where annual transmission project awards have more than doubled and are expected to sustain at elevated levels.

Transmission project bids have already jumped from an annual run rate of about Rs 390–400 billion in FY24 to over Rs 800 billion from FY25 onwards, and management commentary from Power Grid and Adani Energy suggests this pipeline could stay above Rs 800 billion through FY27–28 and potentially cross Rs 1 trillion on a sustainable basis.

The brokerage estimates a USD 100 billion‑plus transmission capex pipeline over FY27–36, translating into over Rs 14 trillion of national transmission opportunity when combining the Central Electricity Authority’s plan to integrate 900 GW of non‑fossil capacity by FY36 and the Brahmaputra basin HVDC development. With only a handful of qualified high‑voltage equipment suppliers and transformer manufacturing capacity expected to rise 80–90% versus FY25 levels—still lagging the demand trajectory—the brokerage believes “supply shortages should continue and pricing should remain firm,” supporting margins for key OEMs.

Jefferies estimates that roughly 40% of India’s transmission spend is addressable to equipment suppliers, pointing to a sizeable and long‑duration order funnel for names such as GE Vernova, Hitachi Energy, Siemens Energy, and CG Power.

Against this backdrop of tight domestic manufacturing capacity, rising HVDC intensity and favourable pricing, the brokerage is positioning investors towards companies where the combination of order‑book visibility, margin upside and valuation still offers meaningful risk‑reward.

Analysis-Can Pakistan’s peacekeeping role in Iran war give it an economic dividend?

“Hitting customers with hidden fees is illegal. It’s not fair to draw people in with what looks like a good deal, only for them to find the real price is higher when they get to the checkout due to extra charges that can’t be avoided,” said Emma Cochrane, executive director of consumer protection at the CMA.

Shares of Syrma SGS Technology surged 4.84% to Rs 1,400.90 in Tuesday’s trading session after the electronics manufacturing services (EMS) company announced a strategic joint venture with Japan-based Kaga Electronics India Pvt. Ltd. to establish a state-of-the-art EMS manufacturing facility in India.

The partnership marks a significant step in Syrma’s efforts to strengthen its presence in the high-value electronics manufacturing segment while catering to the growing requirements of Japanese customers looking to expand their sourcing footprint in India.

According to the company’s regulatory filing, Syrma and Kaga signed an agreement to jointly establish, develop, and operate an advanced EMS manufacturing facility in India. The proposed venture will primarily focus on serving Japanese clients and leveraging the technical expertise and market reach of both partners.

Under the agreement, Syrma SGS Technology will hold up to a 60% stake in the proposed joint venture company (JVCo), while Kaga Electronics India will own up to 40%. Syrma plans to invest approximately Rs 15 crore in the venture, with Kaga contributing around Rs 10 crore. The transaction remains subject to customary regulatory approvals, conditions precedent, and closing requirements.

The governance structure of the JVCo will comprise a four-member board, with both partners nominating two directors each. The agreement also includes standard joint venture provisions such as rights of first refusal on share transfers, reserved matter protections, future funding mechanisms, rights issues, and capital structure safeguards.

Importantly, the company clarified that Kaga is not related to Syrma’s promoter or promoter group, and the transaction does not qualify as a related-party transaction.

Market participants viewed the collaboration positively, as it strengthens Syrma’s manufacturing capabilities and positions the company to benefit from increasing global supply-chain diversification and the growing trend of Japanese companies expanding production and sourcing operations in India.The announcement triggered buying interest in the counter, pushing Syrma SGS Technology shares nearly 5% higher during the session.

Share Price Performance

Syrma SGS Technology has delivered a strong rally over recent periods, gaining nearly 80% in the last three months and surging around 165% over the past year. The company currently commands a market capitalisation of approximately Rs 25,766 crore. During intraday trade today, the stock also touched a fresh 52-week high of Rs 1,410, reflecting strong bullish momentum.

From a technical standpoint, the stock appears stretched in the short term. The 14-day Relative Strength Index (RSI) stands at 76, a level typically considered overbought, suggesting the possibility of near-term consolidation or a pullback. However, the broader trend remains firmly positive, with the stock trading above all 8 key simple moving averages (SMAs), underscoring sustained bullish strength across timeframes.

(Disclaimer: Recommendations, suggestions, views and opinions given by the experts are their own. These do not represent the views of Economic Times)

A multi-storey apartment block, estimated to cost $22 million, is set to be built next to a lot that was once owned by Victor Goh and is now selling to Edge Visionary Living.

OPINION: There’s an urgent need to proceed with the Henderson and Western Trade Coast developments.

Business59 seconds ago

Welsh Government urged to end public procurement through closed English frameworks

Crypto World2 minutes ago

OpenAI Pitches Chatbot Ads at Cannes as $1 Trillion IPO Looms

Politics3 minutes ago

All Tube Lines Affected As London Thunderstorms Cause Floods

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Miami – Corporette.com

-

Tech7 days ago

Tech7 days agoThe Adder At The Heart Of Intel’s 8087 FPU

-

Entertainment2 days ago

Entertainment2 days agoRenter of Home in Anne Heche Crash Denies Settlement With Son

-

Tech20 hours ago

Tech20 hours agoMicrosoft accidentally kills epic Outlook email threads

-

Business2 days ago

Business2 days agoSoccer-U.S. defends Iran World Cup travel restrictions, says discussions ongoing

-

Politics5 days ago

Politics5 days agoBBC Reporter Discusses Cross Party Criticism Of Trumps Iran Deal

-

Business3 days ago

Business3 days agoWall Street Week Ahead: Investors see Micron earnings as pulse check of AI rally momentum

-

Tech5 days ago

Tech5 days agoAWS enters the context layer race with a graph that learns from agents, not manual curation

-

Crypto World3 days ago

Crypto World3 days agoHIVE shares jump as $220M AI deal speeds Bitcoin mining pivot

-

Crypto World3 days ago

Crypto World3 days agoCan Charles Hoskinson Really Rescue Cardano?

-

Crypto World3 days ago

Crypto World3 days agoJake Chervinsky accuses CME of protecting derivatives monopoly

-

Tech13 hours ago

Tech13 hours agoNearly 7,000 fake Amazon domains registered ahead of Prime Day 2026, researchers warn

-

Sports4 days ago

Sports4 days agoFIFA World Cup 2026: Canada beat 9-men Qatar 6-0 to register first ever win | FIFA World Cup 2026

-

Business2 days ago

Business2 days agoMHP SE 2026 Q1 – Results – Earnings Call Presentation (OTCMKTS:MHPSY) 2026-06-20

-

Politics3 days ago

Politics3 days agoAndy Burnham and the meaning of Makerfield

-

Business4 days ago

Business4 days agoBrexit cost 6% of UK economy, Bank of England company data suggests

-

Tech2 days ago

Tech2 days agoSignal’s Meredith Whittaker says AI chatbots ‘are not your friends’ and calls Copilot agents a backdoor

-

Crypto World5 days ago

Crypto World5 days agoAnthropic’s Dario Amodei Urged AI Unity at G7, Even as US Banned His Models

-

Entertainment3 days ago

Entertainment3 days agoJose Alvarado Wants Taylor Swift at More Knicks Games

-

Tech6 days ago

Tech6 days agoWeeks Of In-The-Field Testing And A Verdict

You must be logged in to post a comment Login