Business

Why a Rs 72,000 crore fund manager refuses to chase power and defence rally now

In this interview with ET Markets, he warns that current valuations have already priced in future growth, leaving little margin of safety for aggressive new bets. Edited excerpts from a chat on market outlook, sectoral bets and stock picking in a tough macroeconomic environment.

How has your allocation between equity and debt changed over the last year in ICICI Prudential Equity & Debt Fund?

We do not maintain a static allocation between equity and debt. The allocation is dynamically managed based on valuations and certain macroeconomic factors, with valuations being the primary driver. Over the last year, our equity allocation has moved between approximately 65% and 75%. Currently, it is around 73-75%. Whenever valuations become attractive, we increase equity exposure, while expensive valuations prompt us to reduce it. The fund’s mandate allows us to operate within a 65-80% equity range.Which sectors currently offer the best opportunities from a valuation and growth perspective?

Valuations are close to their long-term averages, expectations are reasonable, and fundamentals remain healthy. Banking is one sector we find attractive from a valuation perspective. We also like certain discretionary consumption businesses, particularly those with pricing power. In an inflationary environment, companies that can pass on costs tend to maintain profitability better. This includes select automobile and consumer discretionary businesses. On the export side, we like pharmaceutical companies and exporters of manufactured goods. Currency depreciation can enhance their competitiveness globally. We also find opportunities among companies benefiting from import substitution.

The consumption narrative has been strong over the last year. Do you still remain positive?

We were not very positive on consumption as a broad theme. Consumption is not a homogeneous category. Different segments perform differently depending on demand conditions and competitive intensity. We prefer specific discretionary categories where either competitive dynamics are improving or pricing power remains strong. While GST reductions have supported consumption, inflation has partially offset some of those benefits. However, in most categories, price increases have not fully negated the gains from lower GST rates.

What is your outlook on PSU banks?

The key question is whether current profitability levels are sustainable. PSU banks benefited from treasury gains and lower credit costs. Going forward, treasury income may moderate and credit costs could increase marginally. The strong earnings upgrade cycle that PSU banks enjoyed is largely behind them. While valuations remain reasonable, the scope for meaningful re-rating depends on whether economic conditions improve again. Currently, we have very limited exposure to PSU banks.

What is your view on the broader PSU space, particularly defence, power and energy?

Within PSUs, we continue to like the power sector. The underlying business cycle remains favourable, although there could be some seasonal fluctuations. Defence remains an attractive long-term theme, but valuations in many defence stocks already reflect a significant portion of future growth expectations. Execution will now become critical. Companies must deliver on order books and profitability. While we like some individual defence names, we are not broadly positive on the entire sector at current valuations.

There has been a shift in investor preference from PSU defence companies to private defence companies. How do you view this?

The theme remains intact, but valuations across both PSU and private defence companies have become expensive. From a thematic perspective, defence remains attractive, but valuation comfort is limited.

Your dividend yield fund owns IT stocks. There are concerns that AI could significantly disrupt IT services companies. How do you think about that risk?

The growth environment for IT remains challenging. Economic growth globally is moderating, and AI introduces additional uncertainty regarding future demand pattern. However, valuations have corrected, dividend yields have improved and cash flow generation remains strong. This creates a case for owning the sector, although we are not taking a significant overweight position.

This is a contrarian opportunity, but unlike some previous contrarian calls, it is not one where investors can take very large bets. AI is not a temporary phenomenon. It is a structural change and has the potential to be disruptive. That said, disruption often takes longer than people expect. Traditional newspaper companies, for example, continue to operate profitably despite digital disruption. However, their valuation multiples have compressed significantly over time. Something similar could happen in IT. Even if earnings remain resilient, valuation multiples could continue to de-rate. Therefore, while there is a case for investing in the sector, position sizing becomes very important.

Have you increased your allocation to IT over the last year?

Compared to eight or nine months ago, our allocation is higher. At one point, we were significantly underweight in the sector. Today, we are closer to benchmark weight. The combination of attractive valuations, strong cash generation and increasing shareholder returns through dividends and buybacks has improved the investment case.

What is the starting point for stock selection in your dividend yield fund?

The first filter is yield. We evaluate both dividend yield and operating cash flow yield. However, yield alone is not enough. We focus equally on the sustainability of those yields and the probability that they can grow over time. Our process combines yield, sustainability and growth potential to identify the most attractive opportunities.

How is the portfolio constructed?

The portfolio is built through two approaches. The first is a systematic ranking framework that combines dividend yield, operating cash flow yield and sustainability metrics. The second is a bottom-up approach where we identify businesses undergoing positive cyclical change. In such situations, current yields may not appear attractive, but future cash flows could improve significantly. We have used this framework successfully in sectors such as telecom, automobiles and power in the past.

Why has your allocation to REITs reduced over time?

There was a period when REIT valuations were significantly more attractive, and our allocation was higher. Over time, valuations improved and yields compressed. Relative to other opportunities available in equities, REITs became less attractive. As a result, our allocation has reduced.

What is your outlook on the power sector, particularly power equipment companies?

The underlying theme remains strong. Global AI-related capital expenditure is driving demand for power infrastructure and equipment. However, valuations have become quite rich. The market has increasingly priced in the growth opportunity. However, there could be a possibility that these companies could surprise positively. We have seen similar cycles in the past where strong demand supported earnings growth for several years. That said, given the elevated valuations, it would be risky to have a very large allocation to the sector. Any slowdown in global capex could quickly affect sentiment and valuations.

From a value perspective, where do you currently find opportunities in the market?

Banks remain attractive from a valuation standpoint. Beyond banks, we see opportunities in pharmaceutical companies and export-oriented manufacturing businesses. These are the areas where we currently find the best combination of valuation comfort and business visibility.

Regis Aged Care has submitted a plan to build a facility in Shenton Park’s Montario Quarter precinct, estimated to cost $50 million.

Amazon: Long-Term Bullish But Short-Term Neutral (Rating Downgrade)

OPINION: Local producers are likely to face a new competitor in the form of Chinese wine.

More than 800 million tonnes of trade passed through Pilbara’s ports last financial year, delivering $150 billion in export value to the state.

Business

Prince Harry Surprises Meghan Markle With Video Call During Her MasterChef Australia Guest Judge Stint

Prince Harry made a sweet surprise appearance on the July 26 episode of “MasterChef Australia,” phoning in to check on wife Meghan Markle while she served as a guest judge on the reality cooking competition.

The Duke of Sussex made the appearance while his wife was doing a stint as a guest judge on the show. The surprise call came during the episode as the judges were reviewing a contestant’s dish, catching the contestants and other judges in the room off guard.

“My Husband’s Here”

The video call kicked off with a lighthearted greeting from Harry, who appeared unsure of exactly what he had dialed into. “G’day,” Harry began in the video call as Meghan turned the phone to the crowd, excitedly saying, “My husband’s here.” Harry then asked his wife, “What’s going on? Have I interrupted something important?”

Meghan quickly brought her husband up to speed, introducing him to the judging panel and explaining what the group was in the middle of. “Well, we are actually in the middle of tasting all the dishes,” she told him. “We have four incredible cooks here.” She went on to gush about the contestants’ skills, telling her fellow judges, “It’s amazing, they’re so talented. We wish you were here,” before noting that Harry was in Canberra at the time, spending time with veterans.

Judges Get in on the Fun

Harry also took a moment to compliment the show’s set design during the call, telling the judges, “The chandeliers in the background, that’s very nice.” One of the judges quipped back, “Yeah, we fancied the joint up for your beautiful wife,” before Harry signed off warmly. “Go and enjoy it,” he said. “I’m very sorry to disturb you. All is well here and I’ll see you later.”

During the same segment, just as Meghan was tasting the competitors’ dishes, she referred to her husband as “my love” while lamenting that he couldn’t try the food himself. “I wish you could try this,” she said. “These dishes are fantastic.”

A Playful Nod to Meghan’s Cooking

The Duchess of Sussex also used her time on set to tease the judges about one particular dish. Meghan later called her husband “a charmer” after his surprise video call during the guest judging appearance. Describing a hot sauce among the dishes she sampled, Meghan said, “There’s a hot sauce that — well you know me, it’s a sambal and it is so good,” before adding playfully, “I think it might be too much for you, though. It’s spicy.”

Filmed During the Couple’s April Trip to Australia

Meghan filmed her guest-judging appearance during a recent trip to Australia with Prince Harry, with the cameo initially teased after being shot during their visit to the country in April. The As Ever founder introduced the contestants to their challenge for the day, which involved picking a “hero” ingredient to spotlight in a dish that told a personal story or family memory.

During the episode, four contestants were challenged to create a dish using a set of Meghan’s favorite seasonal ingredients, including Brussels sprouts, local Australian honey, quince and strawberries, with the goal of crafting something “fit for a duchess.”

Family Stories and a More Casual Approach

Meghan used her introduction of the ingredients as an opportunity to share glimpses into her family life. She shared that her children, Prince Archie, 7, and Princess Lilibet, 5, are big fans of Brussels sprouts, and that she personally grows strawberries and mandarins on her farm in California.

The “With Love, Meghan” host also opted for a more informal approach to her role on the show, telling the judges they did not need to address her as Duchess and could instead simply “call me Meghan.”

Part of a Broader Australian Visit

The Duke and Duchess of Sussex’s four-day Australian trip in April included a mix of private, business and philanthropic engagements. The couple had previously visited the country eight years earlier on their first official joint royal tour as newlyweds, before stepping back from their senior royal roles two years after that visit.

A Well-Known Format for Australian Viewers

“MasterChef Australia,” based on the original British format, features amateur home cooks competing for the chance to publish their own cookbook, along with a cash prize of 250,000 Australian dollars, worth roughly $174,500 in U.S. currency. Meghan’s cameo added a celebrity spotlight to a show already known for drawing prominent guest judges throughout its run.

No Stranger to Surprise Calls

This is not the first time the couple has used a well-timed video call to surprise one another publicly. During a 2019 visit to Nalikule College of Education in Malawi as part of a royal tour of Africa, Harry was surprised when Meghan appeared unexpectedly on a video call to a room full of young women he was meeting with, delighting both Harry and the group in attendance.

A Continued Public Presence

Meghan’s MasterChef appearance arrives amid a steady stream of public projects for the couple, including her Netflix lifestyle series “With Love, Meghan,” which ran for two seasons and featured a rotating cast of celebrity guests joining her for cooking and lifestyle segments. The MasterChef Australia episode aired just after Meghan shared new photos on social media from a recent family vacation with Harry and their two children, continuing the couple’s pattern of blending personal milestones with their public-facing projects.

For fans of the couple, Monday’s viral clip offered a rare, unscripted glimpse of their relationship playing out on a reality television set, a lighthearted moment that quickly circulated online following the episode’s broadcast.

Anduril Executive Chairman and co-founder Trae Stephens joins ‘Mornings with Maria’ to discuss the future of autonomous warfare, how technology is changing the battlefield and scaling America’s defense base.

Mercedes-Benz faces a potential ban on selling connected vehicles in the U.S. under legislation targeting automakers with significant ownership ties to China.

The Senate Commerce Committee advanced a measure last week that would bar the sale of connected vehicles in the U.S. by companies with more than 15% ownership by Chinese entities, potentially affecting German automaker Mercedes-Benz, in which two Chinese investors hold stakes totaling nearly 20%.

Sens. Elissa Slotkin, D-Mich., and Bernie Moreno, R-Ohio, sponsored the bipartisan legislation, which would codify and expand restrictions established under the Biden administration, arguing that it “closes the door on Chinese-origin vehicles, software, and key components at every stage, from production, importation, to sale, so that data gathered on U.S. roads can’t be funneled back to the Chinese government.”

“Chinese cars are surveillance packages on wheels, with the ability to collect on American citizens and transmit that data back to Beijing,” Slotkin said in a statement.

FORD ENTERS COMPETITION TO DEVELOP NEW US ARMY TACTICAL TRUCK

Mercedes-Benz faces a potential ban on selling connected vehicles in the U.S. under legislation targeting automakers with significant ownership ties to China. (Eric Thayer/Bloomberg via Getty Images / Getty Images)

Moreno said the measure aims to prevent “an absolute, total, and complete destruction of our industrial base.”

“China’s auto industry was not built to compete, it was built to destroy American manufacturing, gut the middle class, and undermine our national security,” he said.

But Sen. Ted Cruz, R-Texas, who chairs the Commerce Committee, warned that Mercedes-Benz could effectively be shut out of the U.S. market if the legislation becomes law without changes and said the bill needed changes.

Cruz accused General Motors of pushing for the measure to cut Mercedes-Benz out of the market and make its Cadillac brand more appealing.

“We would never consider” banning Mercedes-Benz sales in the U.S., he said.

GM contended that the legislation does not attempt to target an individual automaker, saying it “supports policies that protect and strengthen American manufacturing and the global competitiveness of U.S. automakers.”

The Senate Commerce Committee advanced a measure last week that would bar the sale of vehicles in the U.S. by companies with more than15% ownership by Chinese entities. (ANDREW CABALLERO-REYNOLDS/AFP via Getty Images / Getty Images)

“As we have said many times, we can compete with anyone in the world when we are given a level playing field,” GM said.

Mercedes-Benz highlighted its extensive U.S. operations while stressing that it “continues to support legislation designed to protect U.S. national security.”

“Mercedes-Benz also remains committed to ensuring that any legislation does not impact our operations. The company will continue to safeguard its employees, dealers, suppliers, and customers,” the automaker said.

The bill includes a process through which manufacturers could seek Commerce Department authorization for vehicles that otherwise would be prohibited.

Moreno said GM intends to move production of its Chinese-made Buick Envision to the U.S. for the 2028 model year and that Ford has agreed to transfer Chinese-made Lincolns to the U.S.

“I view that as a big victory,” Moreno said.

JAGUAR LAND ROVER RECALLS MORE THAN 15,000 VEHICLES OVER VISIBILITY-LIMITING DEFECT

Sen. Ted Cruz warned that Mercedes-Benz would be removed from the U.S. market if the legislation becomes law. (Artur Widak/NurPhoto via Getty Images / Getty Images)

CLICK HERE TO GET FOX BUSINESS ON THE GO

He also said Google’s self-driving vehicle company, Waymo, which had been in talks with Chinese automaker Geely about platforms coming from China, has committed to looking at a Detroit-based manufacturer for its future platforms.

Cruz said another bill provision backed by GM would require automakers to purchase more expensive batteries from GM, adding $5,000 to the vehicles’ cost.

This comes after the Trump administration last month banned Polestar from selling new connected vehicles in the U.S. starting in the 2027 model year due to the Sweden-based automaker being majority-owned by Geely.

Polestar’s sister brand and co-founder, Volvo Cars, said in May that it was given a green light to continue selling cars in the U.S.

The legislation must still pass the full Senate and House and be signed by the president before becoming law.

Reuters contributed to this report.

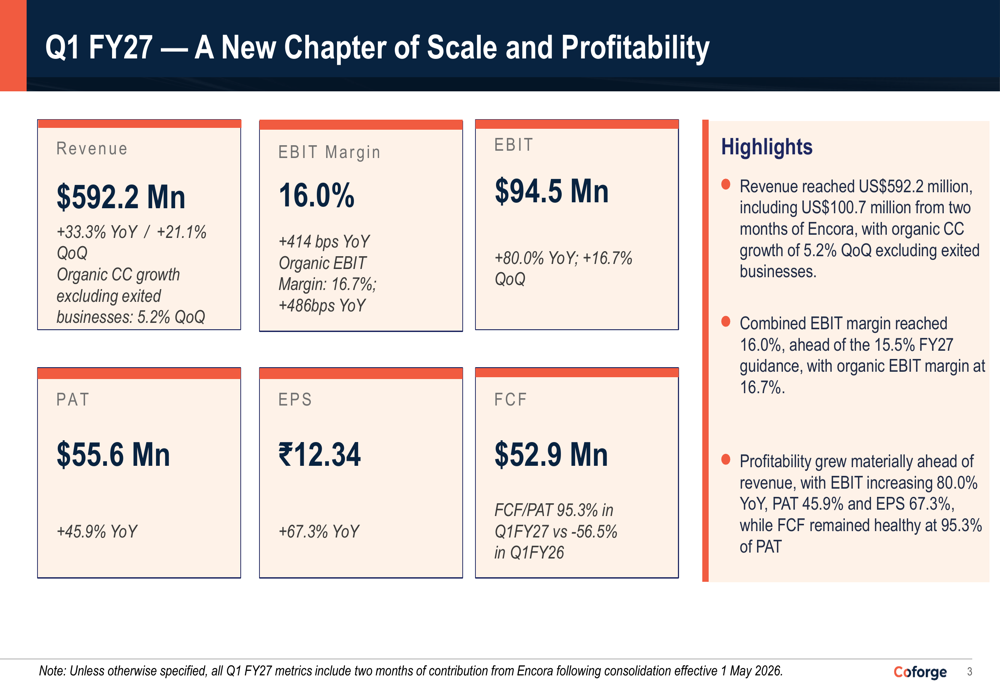

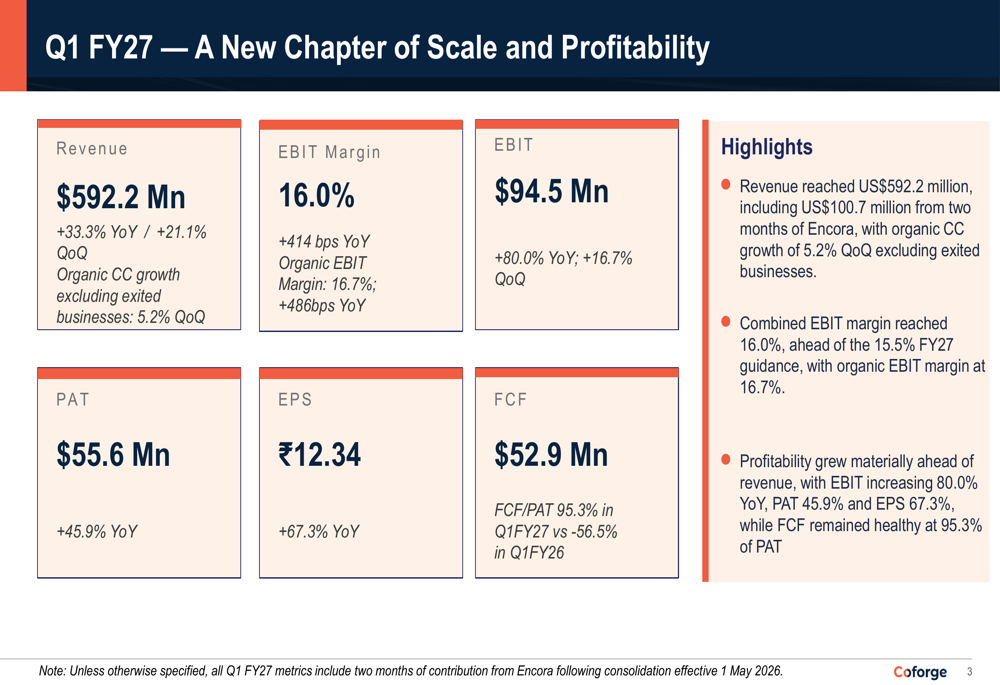

Coforge Q1 FY27 slides: Encora deal drives 33% revenue surge

AI supplier Zhongji Innolight raises $6.8 billion in Hong Kong’s biggest IPO since

Business

DroneShield Shares Sink 12% to a Fresh Low as Middle East Tensions Ease and Ongoing Governance Woes Persist

DroneShield Ltd. shares tumbled sharply Tuesday, falling 12.02% to $1.83, marking another painful session for the once high-flying Australian counter-drone technology company as easing Middle East tensions and lingering governance concerns continued to weigh on the stock.

The decline of $0.25 comes amid a broader retreat in oil prices and defense-sector sentiment following a weekend pause in hostilities between the United States and Iran, a development that has sharply reduced the geopolitical risk premium that had driven a defense-stock rally across the ASX earlier in the year.

A Stock That Has Fallen Dramatically From Its Peak

Tuesday’s slide extends a brutal stretch for DroneShield shareholders that has now stripped away the vast majority of the stock’s once-spectacular gains. The stock reached its all-time high of $6.71 on Oct. 9, 2025, a level far above where shares now trade. Shares have fluctuated anywhere between $4.74 in January and a low of $2.14 in late July, leaving the stock down roughly 35% year to date and 54% below its January 2026 peak, and about 41% below trading levels from a year earlier.

A Rally Fueled by Global Defense Spending, Then Reversed

DroneShield’s meteoric rise earlier this year was driven by a powerful narrative around rising global defense budgets and geopolitical instability. There had been a strong start to the year for DroneShield shares, supported by higher global defense budgets and geopolitical volatility following conflict in the Middle East, with investors flocking to defense-related shares as governments around the world hiked their defense budgets and geopolitical risk worsened.

The stock rallied from around 56 cents in early 2024 to its all-time high above $6.71 by October 2025, a gain of more than 1,000% during that primary uptrend. But that momentum began reversing sharply in the following months. A combination of governance and regulatory concerns dampened investor sentiment beginning in mid-May, when DroneShield announced it had received a notice from the Australian Securities and Investments Commission requesting assistance with an investigation under the Corporations Act, related to market announcements and share trading between Nov. 1 and Nov. 20, 2025.

Regulatory Cloud Continues to Weigh on Sentiment

That ASIC investigation has remained a persistent overhang on the stock in the months since it was first disclosed. Reuters reported that Australia’s corporate regulator was investigating DroneShield’s disclosures and share trading, contributing to the stock’s decline even as the company continued to report strong underlying business results.

Wall Street Turns More Cautious

As the governance concerns have persisted, analyst sentiment on DroneShield has grown increasingly split. Jefferies Financial Group lowered its revenue projections for DroneShield across 2026 through 2028 by roughly 9% and cut its earnings-per-share estimates by a range of 5% to 16%, reducing its price target by 27% to 2.05 Australian dollars. The level of short positioning in DroneShield shares was nearly double that of peer Electro Optic Systems Holdings, with short interest climbing by 7.01 million shares since July 1 while the number of shares outstanding remained steady at around 924.1 million.

Other analysts remain divided on the stock’s outlook. Out of four analysts tracked by TradingView, two hold a strong buy rating while two hold a sell or strong sell rating, though all agree there is some element of potential upside ahead, with an average price target of $3.41 implying about 49% upside and a maximum target of $4.80 implying the stock could climb another 110% from recent levels.

Strong Contract Wins Have Failed to Offset Selling Pressure

The declines have come despite the company continuing to secure notable new business. Among its recent wins, DroneShield secured a $24.9 million contract with a U.S. defense customer combining mobile and fixed counter-drone systems with software subscriptions and ongoing support services, reflecting the company’s shift toward higher-margin recurring revenue. A separate roughly $50 million European military contract secured via a reseller, with substantial hardware deliveries weighted to the first quarter of 2026, briefly drove the share price above $2.80 before those gains evaporated, while an additional $6.2 million Asia-Pacific military contract further validated the global breadth of demand for the company’s AI-enabled electronic warfare systems.

Despite that operational strength, the stock has failed to find insulation from selling pressure, in large part due to the ongoing governance cloud, with DroneShield having established a reputation as a high-beta, momentum-driven play within the defense technology space that tends to lead sector moves in both directions.

Business Fundamentals Remain Solid

Beyond the near-term share price volatility, DroneShield’s underlying financial performance has continued to show substantial growth. The company reported fiscal 2025 revenue of $216.5 million, up 276% year-over-year, along with $104 million in secured fiscal 2026 revenue and $21.7 million in new contracts. DroneShield has also been expanding its manufacturing footprint, announcing in March an EU manufacturing facility targeting annual production capacity of about $2.4 billion Australian dollars by the end of 2026.

A Cooling Geopolitical Backdrop

Tuesday’s decline also fits within the broader pullback across defense-linked assets following the weekend pause in U.S.-Iran hostilities, which has sharply reduced the acute geopolitical risk that had underpinned demand for counter-drone and defense technology stocks throughout the first half of the year. As tensions in the region have shown signs of easing and oil prices have retreated sharply from their recent highs, investors appear to be reassessing how much of a risk premium defense stocks like DroneShield deserve.

DroneShield is scheduled to release its next earnings report on Sept. 1, 2026, a date that could offer investors a clearer read on how the company’s underlying business is performing amid the ongoing volatility in its share price. Until then, DroneShield’s stock is likely to remain caught between genuinely strong operational momentum, including a growing pipeline of international military contracts, and a market increasingly focused on the unresolved ASIC investigation and the broader cooling of the geopolitical backdrop that originally fueled the stock’s dramatic rise. For now, investors appear to be pricing in considerably more caution than conviction, leaving the stock trading well below both its all-time high and the levels many analysts still consider achievable over the next 12 months.

The Reserve Bank governor says interest rates may need to go higher, as Australia’s weak productivity problem locks households in for lower living standards.

Regis Aged Care submits $50m Shenton Park plan

BNY unit wins MiCA entry as Europe’s crypto register hits 309

LeBron James to Wear No. 23 After Completing Move to Philadelphia 76ers

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World7 days ago

Crypto World7 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat7 days ago

NewsBeat7 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech1 day ago

Tech1 day agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Business6 days ago

Business6 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment6 days ago

Entertainment6 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Crypto World5 days ago

Crypto World5 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics19 hours ago

Politics19 hours agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Sports1 day ago

Sports1 day agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Sports4 days ago

Sports4 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Fashion4 days ago

Fashion4 days ago16 Dresses for the High Summer Event

-

News Videos4 days ago

News Videos4 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Politics2 days ago

Politics2 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Entertainment4 days ago

Entertainment4 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

News Videos1 day ago

News Videos1 day agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Crypto World5 days ago

Crypto World5 days agoUniswap (UNI) pushes deeper into tokenized RWAs with permissioned trading pools

-

Crypto World6 days ago

Crypto World6 days agoSablier Labs Enters Maintenance Mode, Halts Development

-

Crypto World5 days ago

SEC Agrees to Overhaul Recordkeeping After Settling Coinbase Lawsuit Over Gensler’s Lost Texts

-

Business4 days ago

Business4 days agoAlliance Entertainment Holding Corporation (AENT) Discusses Evolution Into Omnichannel Distribution and Fulfillment Platform for Media and Collectibles Transcript

You must be logged in to post a comment Login