Crypto World

5 Undervalued AI Stocks for 2026: Oracle (ORCL), AMD, Micron (MU), TSMC and Dell Lead the Pack

While the artificial intelligence revolution has minted numerous success stories, many headline-grabbing companies now carry valuations that price in years of perfect execution. The real opportunities may lie with the less glamorous players—those providing the essential building blocks of AI infrastructure, from semiconductors and memory to cloud platforms and enterprise servers. Here are five stocks trading at attractive valuations despite their critical roles in the AI ecosystem.

Oracle’s Transformation Into an AI-Driven Cloud Giant

Once dismissed as a dinosaur in the database industry, Oracle is rewriting its narrative with impressive momentum.

The company’s most recent quarterly results showed total revenue climbing 22%, while cloud revenue surged 44% and Oracle Cloud Infrastructure accelerated an impressive 84% year-over-year. Perhaps most striking was the 325% jump in remaining performance obligations to $553 billion—representing committed future revenue already in the pipeline. Management has confidently raised its fiscal 2027 revenue guidance to $90 billion.

Wall Street may still be valuing Oracle through the lens of its legacy software business, but the reality is dramatically different. As the company’s revenue composition shifts increasingly toward high-margin AI cloud services, the valuation gap becomes more apparent. Should Oracle successfully monetize its massive backlog, significant upside potential remains.

AMD Emerges as a Legitimate Nvidia Competitor

While AMD is not Nvidia, the narrative that it’s perpetually behind is outdated.

Advanced Micro Devices, Inc., AMD

AMD delivered record quarterly revenue of $10.3 billion in Q4 2025, maintaining a healthy 54% gross margin. The data center division generated $5.4 billion in revenue—a 39% increase from the prior year—fueled by robust adoption of both EPYC server processors and Instinct AI accelerators.

The compelling case for AMD lies in its valuation relative to peers and its diversified revenue streams. Unlike pure-play AI chip companies, AMD benefits from multiple growth vectors including AI GPUs, traditional server CPUs, embedded solutions, and general cloud infrastructure expansion. Investors who believe AMD will continue capturing market share in high-performance computing may find today’s valuation attractive.

Micron: The Essential Memory Provider Wall Street Overlooks

Artificial intelligence infrastructure demands massive quantities of high-bandwidth memory, and Micron stands among the select few manufacturers capable of delivering at volume.

First-quarter fiscal 2026 results showcased revenue of $13.6 billion—a 57% year-over-year increase. Micron also achieved record free cash flow and announced increased capital expenditures to expand production capacity for next-generation HBM (high-bandwidth memory).

Memory chip manufacturers historically face cyclical demand patterns, making investors hesitant to assign premium valuations. However, AI workloads may be establishing a structural shift in memory demand that defies traditional cycles. If HBM remains in tight supply as expected, Micron could command a higher valuation multiple than legacy memory producers typically receive.

TSMC: The Indispensable Manufacturer Behind AI’s Biggest Names

TSMC fabricates the cutting-edge processors that enable virtually every significant AI innovation. Companies from Nvidia and AMD to Apple depend entirely on TSMC’s manufacturing capabilities.

Fourth-quarter 2025 results demonstrated revenue growth of 25.5% in U.S. dollar terms, accompanied by a 62.3% gross margin and 54% operating margin. The momentum continued into 2026, with January and February revenue climbing 29.9% compared to the same period in the previous year.

TSMC shares have traditionally traded at a discount to American semiconductor peers due to geopolitical risks associated with Taiwan. Yet from a pure operational and financial perspective, TSMC rivals or exceeds nearly any large-cap chip company. As AI hardware demand keeps advanced node capacity fully utilized, the company’s earnings trajectory appears increasingly robust.

Dell’s Explosive AI Server Growth Flies Under the Radar

Dell has transformed into a critical supplier of AI infrastructure, though many investors haven’t yet recognized this evolution.

Fiscal fourth-quarter 2026 results revealed overall revenue growth of 39%, but the real story was in AI-optimized servers, where revenue exploded 342% to reach $9 billion. Dell entered the current year with an extraordinary $43 billion backlog of AI server orders—providing revenue visibility that few hardware manufacturers can match.

The market continues pricing Dell largely as a personal computer company, creating a disconnect between perception and reality. With AI servers representing an expanding portion of total revenue, the valuation gap between Dell’s legacy image and its actual business composition is becoming harder to ignore. Value-oriented investors seeking AI exposure are increasingly recognizing this opportunity.

Final Thoughts

Oracle, AMD, Micron, TSMC, and Dell may not generate the same headlines as the most prominent AI stocks, but they’re providing the essential infrastructure—processors, memory chips, manufacturing capacity, cloud platforms, and complete systems—that enables the entire AI revolution. For investors concerned that the obvious AI beneficiaries already reflect lofty expectations, these five companies offer an alternative pathway to capitalize on the same secular growth trend.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

BlockDAG stands out among the top crypto gainers with a limited $0.000022 entry price, as the Pippin crypto price drops and the Dogecoin price prediction remains uncertain.

Sentiment across crypto sits at extreme fear right now, with the Fear & Greed Index barely scraping double digits and altcoins absorbing the worst of it. Pippin is a clear example: whale exits hammered the price over 10% in 24 hours, volume dried up, and key support near $0.0427 is now holding by a thread. Dogecoin is in a similar holding pattern, stuck inside a descending triangle after a near-30% slide since February.

Neither coin is broken, but neither is giving traders much reason to feel confident right now. That’s actually the context that makes BlockDAG (BDAG) worth slowing down on. Priority access at $0.000022 closes April 8. CoinMarketCap already shows $0.40. That’s a 39,900% difference. Global listings on BitMart, Coinstore, and P2B open the same day, bringing real exchange exposure. Analysts called $0.30 to $0.40 months ago. That range already happened. Now $0.70 is the number people are watching.

Pippin Plummets 10% Amid Whale Sell-Off

Pippin (PIPPIN), a Solana-based memecoin, has dropped over 10% in the past 24 hours, driven by a whale sell-off and growing bearish sentiment among traders. On March 29, PIPPIN fell 10.52% to $0.0512, while trading volume slid 18% to $40.20 million, reflecting reduced market interest. Analytics from Nansen showed whales cut holdings by 25%, even as the top 100 wallets slightly increased theirs.

Major players, including Solana co-founder Raj Gokal, reportedly rotated into PUNCH, signaling weakening momentum. The Pippin crypto price currently trades near key support at $0.0427, consolidating between $0.047 and $0.0599. If support holds, recovery is possible, but a break could trigger sharper declines.

Overall, short-term bearish pressure continues, and the Pippin crypto price remains volatile, with bulls struggling. Traders are eyeing $0.0467 and $0.0605 for key activity, shaping the Pippin crypto price outlook.

Dogecoin Faces Critical Support as Market Awaits Next Move

The DOGE price is at a critical juncture as the chart compresses within a descending triangle, with highs dropping while support near $0.0886 holds. Since mid-February, DOGE has fallen almost 30%, from $0.1280 to $0.0905, putting pressure on this key level. Analysts note that if support holds, a bounce toward $0.1050 is possible, but a break could drive prices down to $0.0820.

Historical cycles suggest DOGE has repeated accumulation and breakout phases, with prior gains of 190% and 480%. This has traders watching closely. Short-term momentum is mixed, making the Dogecoin price prediction uncertain. Current conditions suggest that Dogecoin price prediction hinges on reclaiming higher ranges, and the next decisive move could shape the broader trend. Overall, the Dogecoin price prediction remains volatile but watchful.

BlockDAG Unveils 85x Price Jump Chance

BlockDAG has emerged as one of the top crypto gainers this year thanks to an exceptional rise in price and a limited-time priority access offer. The current priority access at $0.000022 remains available but only until April 8 which can guarantee at least 85x price jumps as compared to BDAG lowest price on the open market, while today’s CoinMarketCap price reached $0.4, representing a 39,900% increase from Stage 1 and 700% above the listing price.

This massive gap between the entry price and the current market price highlights an opportunity few investors ever encounter. The three-month head start before community deposits open in June allows early participants to secure positions far below market levels.

Global trading opens on April 8, with listings across BitMart, Coinstore, and P2B, exposing BlockDAG to millions of traders worldwide. The combination of limited priority access and broad exchange exposure has accelerated interest and amplified the sense of urgency.

Market analysts had projected the $0.3–$0.4 range, which has already been achieved, and now attention has shifted to $1 prediction for the near future. For those holding priority access at $0.000022, the ROI potential is nearly unimaginable, reaching hundreds of thousands of percent if prices move as predicted.

Network fundamentals support the growth story. Developer engagement continues to rise, mining hardware distribution strengthens the system between April and June, and futures markets add depth to liquidity. The combination of strong infrastructure, early gains, and priority access highlights an opportunity to enter the market at $0.4 or higher, allowing participants to benefit from early positioning.

Final Thoughts

Pippin’s support at $0.0427 is doing a lot of work right now, and whether it holds or breaks will define the Pippin crypto price outlook for the next few weeks. Dogecoin is in a similar wait-and-see spot. The Dogecoin price prediction stays clouded until bulls actually reclaim ground, not just defend it.

BlockDAG is where the math gets interesting. Buying at $0.000022 when CoinMarketCap shows $0.40 is a gap most people stumble across after it closes. April 8 is when global listings go live, and that $0.000022 entry goes with it. Among top crypto gainers this year, few offer a closing window this specific. Specific tends to matter.

For more information, visit the official website, presale, Telegram, and Discord.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

TLDR:

- Kiyosaki ties the 1974 petrodollar system to today’s rising oil prices and growing global conflict risks.

- The shift from pensions to 401(k)s after ERISA left millions of baby boomers without guaranteed retirement income.

- Kiyosaki recommends gold, silver, and Bitcoin as real stores of value amid dollar weakness and inflation.

- He calls on schools to teach financial literacy, a message he has repeated since writing Rich Dad Poor Dad in 1997.

Robert Kiyosaki, author of Rich Dad Poor Dad, has renewed his warnings about the U.S. economy. He links two major 1974 policy shifts to today’s financial instability.

The “Rich Dad” author points to the petrodollar system and the passage of ERISA as turning points. According to Kiyosaki, those decisions have now created conditions that threaten millions of Americans, particularly retiring baby boomers facing an uncertain financial future.

The Petrodollar and Rising Oil Prices

In 1974, the U.S. dollar moved away from the gold standard and became backed by oil. This shift created the petrodollar system, which has shaped global trade for decades. However, Kiyosaki argues that this arrangement is now under serious pressure in 2026.

He posted on X, warning that “the world stands on the edge of world war over oil.” Rising oil prices are pushing inflation higher across food and fuel markets. These increases are hitting everyday consumers hard as purchasing power continues to weaken.

The U.S. also carries one of the largest debt burdens in its history. Kiyosaki notes that whole countries and individuals are deeply in debt simultaneously. This convergence of debt and rising commodity prices creates a fragile economic environment.

He continues to recommend holding gold, silver, and Bitcoin as alternatives to fiat currency. These assets, in his view, represent real money that retains value over time. His long-standing position has not changed, even as market conditions shift.

ERISA, Retirement Insecurity, and Financial Education

The 1974 passage of ERISA marked a major transition in how Americans save for retirement. Before that year, most employees received guaranteed lifetime income through pension plans. After ERISA, the shift toward 401(k)s, IRAs, and RRSPs transferred investment risk to individuals.

Kiyosaki warns that millions of baby boomers will soon discover their retirement savings fall short. Social Security and Medicare are also facing serious funding challenges, he says. Many retirees may find themselves without stable income once they stop working.

He raises a broader concern about financial literacy in schools. “Why do our schools not teach the subject of money to students?” he wrote. This question, which he first raised in Rich Dad Poor Dad in 1997, remains central to his message today.

Kiyosaki encourages people to invest in their personal financial education. He acknowledges that while many credible teachers exist on YouTube, there are also unreliable sources. He advises people to stay alert and verify the information they consume carefully.

MicroStrategy co-founder Michael Saylor says Bitcoin (BTC) has won the global narrative war, but flags BIP-110 protocol changes as the asset’s greatest remaining threat.

Meanwhile, Bitcoin Conference organizer David Bailey extends an invitation to BIP-110 supporters, invigorating debate that has split the Bitcoin community into opposing camps.

BIP-110 is a proposal to change how new Bitcoin blocks are selected by allowing miners to vote on which valid block to accept, rather than strictly following the longest-chain rule.

In simple terms, it tries to make Bitcoin’s consensus more flexible and resistant to certain mining attacks.

Why the BIP-110 Debate Matters Now

Saylor argues that the BTC price is now driven by institutional capital flows rather than halving cycles.

He describes the four-year cycle as “dead” and emphasized that bank lending and digital credit will shape Bitcoin’s growth going forward.

However, the most provocative line targeted protocol development. The MicroStrategy executive calls “bad ideas driving iatrogenic protocol changes” the single biggest risk to Bitcoin.

“Iatrogenic” is a medical term meaning harm caused by medical examination, treatment, or advice from health professionals.

That warning lands squarely on the BIP-110 controversy. The Bitcoin Improvement Proposal, introduced by developer Dathon Ohm and backed by the Bitcoin Knots team, seeks a temporary one-year soft fork to restrict non-monetary data in Bitcoin transactions.

It targets Ordinals inscriptions, BRC-20 tokens, and large OP_RETURN payloads that critics say bloat the blockchain and burden node operators.

A Community Split in Two

The first block signaling support for BIP-110 was mined by the Ocean pool in March 2026.

Proponents frame it as a necessary defense of Bitcoin’s identity as sound money. They argue that arbitrary data competes unfairly with payments and drives up fees for ordinary users.

Opponents see a different picture entirely. Blockstream CEO Adam Back warned that consensus-level intervention could damage Bitcoin’s credibility as a store of value.

He argued the proposal risks setting a precedent for future transaction censorship.

The activation threshold itself remains contentious. BIP-110 proposes a 55% hash power requirement, far below the traditional 95% consensus standard for Bitcoin upgrades.

Bailey, CEO and Chairman of Nakamoto and founder of BTC Inc., acknowledged his own role in mocking BIP-110 supporters online.

Several BIP-110 supporters dismissed the gesture as a PR move tied to ticket sales rather than genuine bridge-building.

Notwithstanding, the Bitcoin 2026 Conference and a Federal Reserve meeting are both scheduled for late April, creating a dense catalyst window for BTC.

The BIP-110 signaling process remains active, with a potential activation decision approaching later in 2026.

It is a contest over whether Bitcoin should remain a minimal monetary tool or allow broader on-chain experimentation.

The post Michael Saylor Calls BIP-110 Bitcoin’s Biggest Self-Inflicted Risk appeared first on BeInCrypto.

TLDR:

- The IRGC collected Hormuz transit tolls in USDT via Tron, settling payments in seconds outside U.S. banking systems.

- Chainalysis reported the IRGC moved $3 billion through cryptocurrency in 2025, with over 50% of Iranian crypto activity linked to it.

- TRM Labs traced $1 billion in IRGC flows through Zedcex and Zedxion, both later designated by OFAC on January 30, 2026.

- Iran’s Central Bank held $507 million in USDT per Elliptic, while its Defence Ministry accepted crypto for arms exports in January 2026.

USDT, the dollar-pegged stablecoin, has become central to a documented IRGC financial operation. The token settles transactions on the Tron blockchain in under three seconds.

It bypasses American banking infrastructure entirely and cannot be frozen by the Federal Reserve. Bloomberg reported on April 1 that the Islamic Revolutionary Guard Corps collects tolls from tankers transiting the Strait of Hormuz. Payments are accepted in Chinese yuan or stablecoins, including USDT.

IRGC Toll Collection at Hormuz Runs on Crypto Rails

According to Bloomberg, tanker operators contact an IRGC-linked intermediary to begin the process. The operator submits vessel ownership, flag, cargo, crew list, and destination for review.

Hormozgan Provincial Command screens submissions using a one-to-five friendliness ranking toward the U.S. and Israel. If cleared, the operator negotiates a toll starting at one dollar per barrel.

Rates can reach up to two million dollars per supertanker, depending on the agreement reached. Payment settles either in Chinese yuan through CIPS or in USDT through the Tron blockchain.

Once payment is confirmed, a VHF passcode is issued to the vessel. An IRGC patrol boat then escorts the tanker safely through the Larak corridor.

Analyst Shanaka Anslem Perera posted on X that the toll system is “live and collecting revenue tonight.” He described the setup as the first conflict in history where an enemy’s currency funds both sides.

In January 2026, Iran’s Ministry of Defence also began accepting cryptocurrency for arms exports. Drones, missiles, and defense equipment were all settled on the same blockchain rails.

The toll system did not require new technology to operate at the Strait of Hormuz. It applied existing stablecoin infrastructure that was already running at global industrial scale.

The Central Bank of Iran had accumulated $507 million in USDT, according to Elliptic. That reserve was already in place well before the current conflict escalated further.

Blockchain Analytics Firms Documented Billions in IRGC Crypto Flows

Chainalysis reported that the IRGC moved $3 billion through cryptocurrency in 2025 alone. IRGC-linked wallet addresses accounted for over 50 percent of all Iranian crypto activity by Q4 2025.

TRM Labs traced approximately $1 billion in IRGC flows through two UK-registered exchanges. Those exchanges, Zedcex and Zedxion, conducted transactions almost entirely in USDT on Tron.

TRM described the operation as “a sanctioned military organization operating exchange-branded crypto infrastructure offshore.” The firm further called it “infrastructure-level control” over offshore stablecoin exchange activity.

The U.S. Office of Foreign Assets Control designated both exchanges on January 30, 2026. Twenty-nine days after those designations, military strikes on Iran began.

The U.S. Treasury issues bonds to fund its own war effort against Iran. Those bonds finance aircraft carriers, interceptors, and the 2,400 sorties flown over Iran in five weeks.

Meanwhile, USDT — a token bearing “USD” on its face — funds toll payments on the opposing side. Both instruments denominate in dollars yet operate on entirely separate financial rails.

One rail runs through the Federal Reserve; the other through a British Virgin Islands-registered blockchain. Both systems settle in seconds and reference the same dollar.

The IRGC captures revenue from dollar-denominated tolls without needing access to American financial systems. Neither party controls how the other side uses the dollar’s name in this ongoing conflict.

Crypto World

Gold Reserves Top $4 Trillion, Surpassing Foreign-Held U.S. Treasuries for the First Time

TLDR:

- Central bank gold holdings crossed $4 trillion, exceeding $3.9 trillion in foreign-held U.S. Treasuries in early 2026.

- Global central banks purchased 863 tonnes of gold in 2025, marking three consecutive years of record-level buying.

- Gold dropped from $5,608 to $4,676 amid Iran war inflation pressures, yet institutional price targets remain above $5,400.

- The 2022 freeze of $300 billion in Russian reserves triggered a structural move by central banks toward unfreezable gold assets.

Gold reserves held by the world’s central banks have crossed a critical threshold in early 2026. For the first time, the collective value of sovereign gold holdings — roughly $4 trillion — now exceeds the $3.9 trillion in U.S. Treasury securities held by foreign governments.

The shift represents the most consequential change in global reserve composition since the dollar displaced the British pound sterling decades ago.

Central Banks Drive Structural Gold Accumulation

The scale of central bank gold purchases has been consistent and growing. In 2025, central banks collectively bought 863 tonnes of gold. That marks the third consecutive year above 1,000 tonnes when unreported purchases estimated by the World Gold Council are factored in.

Poland added 20 tonnes in February alone. China’s central bank has maintained purchases for over 15 consecutive months.

Meanwhile, global gold ETF holdings reached an all-time high of 4,171 tonnes, reflecting broad institutional participation beyond sovereign buyers.

As analyst Shanaka Perera noted on social media: “The buying is not speculative. It is structural. It is central banks replacing the asset that can be frozen with the asset that cannot.”

The catalyst for this shift traces back to February 2022. That month, the United States and Europe immobilized approximately $300 billion in Russian central bank reserves held in Western financial institutions. The message to non-aligned central banks was direct — reserves held in foreign bonds carry political risk.

Gold Price Correction Masks Long-Term Momentum

Gold currently trades at $4,676, down from $5,608 in January. The decline stems largely from short-term war-driven market mechanics.

The Iran conflict pushed oil above $140, driving inflation and keeping the U.S. Federal Reserve’s rates at 3.50 to 3.75 percent. Higher real yields have temporarily made the dollar more attractive relative to gold.

The same conflict that is straining U.S. strategic influence at the Strait of Hormuz is, at least in the near term, supporting dollar strength through inflationary channels. Gold is therefore caught between short-term rate pressures and longer-term reserve diversification trends.

Major financial institutions have not revised their bullish outlook. JPMorgan and Wells Fargo project targets between $6,100 and $6,300. Goldman Sachs forecasts $5,400 by year-end. Institutional buyers appear to be accumulating during the dip rather than exiting positions.

The broader context remains unchanged. Gold cannot be frozen by executive order, does not settle through SWIFT, and requires no foreign custodian.

That combination of properties, rather than any speculative thesis, continues to drive sovereign demand. The $4 trillion crossover reflects a measured, ongoing rebalancing of global reserve strategy — one tonne at a time.

Crypto World

Taurox (TAUX) Pre-KYA Opening Announcement Secures Renewed Interest From (Ripple) Investors

XRP trades near $1.32. April has recorded the highest average monthly returns for XRP since 2014 at 24.8%. The OCC final rule took effect on April 1, enabling Ripple’s conditionally approved National Trust Bank to move forward with expanded digital asset custody operations, while the Senate Banking Committee markup of the CLARITY Act remains scheduled for the second half of the month.

Taurox, an AI-driven trading protocol, is equipped to respond to these developments through autonomous agents that deliver diversified, risk-managed returns to stakers.

Handling XRP Supply Dynamics and Regulatory Timelines with Taurox’s Methodical Framework

XRP faces ongoing pressure from the April 1 escrow release of 1 billion tokens combined with regulatory milestones, resulting in moderate volatility and repeated 20-30% price movements for holders despite institutional progress. Taurox presents a steadier solution by uniting deposits of USDT, BTC, or XRP inside one central trading pool guided by autonomous agents. These agents are created by an international network of developers, quants, and AI engineers to achieve reliable proportional profits.

Each agent is limited to no more than 2% of total pool assets to reduce concentration risk, with KYA tiers ensuring strategies stay within conservative, moderate, or aggressive categories. Demanding Sharpe ratios of at least 1.5 and drawdown limits below 15%, Taurox generates more consistent outcomes than direct asset ownership or standard hedge funds that charge 2% management fees under any market circumstance.

Early Agent Submission Portal Open: Accelerating Strategy Integration

Taurox recently achieved an important roadmap acceleration by launching the Pre-KYA Registration Table. This gateway enables developers, quants, and AI specialists to submit trading agents early, before the full Know Your Agent framework activates. Early registrants gain front-of-line access to the Proving Ground for quicker testing and faster capital deployment. They also qualify for additional rewards from the Agent Creator Fund, which accounts for 10% of total TAUX supply. Strategists with proven systems now have a prime window to secure early positioning inside the Taurox ecosystem.

Taurox Operational Framework: AI Strategies with Layered Risk Protections

Taurox collects staker contributions into one central trading pool and issues txTokens valued at the current net asset value per share, starting at $1.00. The protocol reserves 15% of assets in stablecoins to support liquidity and allocates the balance through a performance-weighted system. Agents implement strategies such as statistical arbitrage using secure on-chain vaults or limited-access CEX accounts.

Before activation, each agent completes evaluation in the Proving Ground with sponsor capital until it satisfies statistical thresholds, such as a minimum of 500 trades for high-frequency approaches. Protective measures consist of 2% daily loss limits, 5% single-trade exposure caps, and an automatic 5% pool-wide drawdown halt. Gradual reallocation procedures help prevent abrupt liquidations, and KYA classification confirms that agents adhere strictly to their designated risk parameters within a transparent and auditable structure.

TAUX Economic Model: Capped Supply Enhanced by Systematic Burns

TAUX maintains a fixed supply of 2 billion tokens with no possibility of additional minting after launch, removing any dilution risk. In contrast to standard hedge funds, Taurox imposes no base fees and retains only 5% of gross profits, acquired directly on the open market. Thirty percent of this revenue is sent permanently to a dead address for burning, while seventy percent is directed to the DAO treasury.

The remaining profit share follows a tiered model that prioritizes stakers, allocating 80% for returns between 0-20% and reducing progressively to 43% once returns surpass 300%, with all calculations based on high-water mark net gains. Allocations assign 40% to the presale, 15% to ongoing block-by-block staking rewards, 10% to milestone-based agent incentives, and 5% to the team under a six-month cliff vesting schedule.

Taurox Presale Progress: Entry Opportunity with Defined Growth Projections

The Taurox Presale has advanced into Phase 4 and surpassed $950K raised. TAUX is currently available at $0.018. Phase 4 participants can expect nearly 4.5x upside at listing when the token debuts at $0.08. If the protocol reaches a $1 billion pool, early backers could realize up to 103x returns with TAUX at $1.85. A $500 investment today would grow to roughly $2,220 at listing and approach $28,000 at the $1 valuation.

The presale includes a one-month cliff and 20% monthly releases from months two to five, allowing immediate staking while limiting early transfers. Combined with 30% revenue burns, tiered profit sharing, 15% staking rewards, and an 8% security allocation, it presents attractive potential across both near-term and extended horizons.

Final Assessment: Taurox Establishing Reliable Yield Mechanisms in Dynamic Markets

Taurox integrates advanced AI autonomy with rigorous on-chain risk protocols and a built-in deflationary mechanism to establish a new benchmark in decentralized finance. Supported by contributions from developers around the world and sustained by ongoing token burns, the protocol maintains a clear path for measured growth as the need for consistent and transparent yield generation increases across market cycles.

Learn More

Buy TAUX: https://taurox.io

Whitepaper: https://docs.taurox.io/

Official Telegram: https://t.me/tauroxlabs

Official X/Twitter: https://x.com/TauroxProtocol

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Kwasi Kwarteng, the UK’s former Chancellor of the Exchequer who served just weeks in September 2022, is re-emerging with a new focus on bitcoin, monetary history, and long-term economic thinking.

Reflecting on the infamous mini-budget in an interview with CoinDesk, he was candid about the missteps. “The mini budget was literally two weeks after we took office, it was just very, very rushed business,” he said, referring to the period immediately after taking office on Sept. 6, followed by the death of Queen Elizabeth II two days later. The compressed timeline left little room for coordination or scrutiny. The fallout was severe, sending gilt yields sharply higher and helping expose the UK’s Liability-Driven Investment pension crisis.

Kwarteng still defends the intent behind the policy, warning the UK is now stuck in a fiscal “doom loop” where “you’re spending more money than you can raise in taxation,” and rising taxes ultimately “kill incentives in the economy.”

He also criticised the short-termism dominating both politics and markets. “Everything’s quarterly driven, people are either euphoric or freaking out. And actually, you’ve got to take a longer view.”

That longer view now shapes his thinking on bitcoin and money more broadly. While in office, he said, “the Treasury, the Bank of England are certainly aware of bitcoin and digital assets, but its still incredibly small,” highlighting what he sees as the UK’s reluctance to embrace innovation.

He also pointed to a cultural gap with Europe, noting Paris is becoming “quite forward leaning on digital assets.”

Kwateng also pushed back on criticism from Boris Johnson, after the former prime minister claimed Bitcoin was a “Ponzi,” arguing instead for a more open-minded view of emerging forms of money.

A new bitcoin treasury venture

Now involved with UK bitcoin treasury firm Stack BTC (STAK) as executive chairman, Kwarteng is putting those ideas into practice, with the company holding 31 BTC on its balance sheet.

The firm has drawn increasing political attention, with Reform UK leader Nigel Farage taking a 6% stake in the company.

For Kwarteng, the shift reflects a move away from reactive policymaking toward what he sees as a more resilient monetary future grounded in long-term thinking.

Crypto World

The Infrastructure Behind the Next Era of Capital Markets Is Being Built on Chainlink and Swift

TLDR:

- Swift completed a tokenized bond interoperability trial with BNP Paribas, Intesa Sanpaolo, and Société Générale using Chainlink.

- Chainlink CCIP enabled cross-chain settlement of tokenized assets across 12+ major financial institutions including Citi and BNY Mellon.

- AI models achieved nearly 100% data consensus on corporate actions records validated through the Chainlink Runtime Environment.

- GLEIF and Chainlink partnered to deliver verifiable, cross-jurisdictional identity and compliance tools for institutional blockchain transactions.

Chainlink is building the infrastructure behind the next era of capital markets through a series of landmark partnerships and technical milestones.

Working alongside Swift, DTCC, Euroclear, and dozens of major financial institutions, the platform is connecting traditional finance with blockchain networks.

From tokenized bond settlements to AI-powered corporate actions processing, the groundwork for a new financial system is taking shape across both legacy and emerging infrastructure.

Connecting Traditional Finance to Blockchain Networks

Swift, the messaging standard connecting over 11,500 financial institutions across 200+ countries, recently completed a major digital asset interoperability trial.

The initiative involved tokenized bond transactions with BNP Paribas Securities Services, Intesa Sanpaolo, and Société Générale (FORGE).

It demonstrated how Swift can orchestrate tokenized asset transactions across blockchains and existing enterprise systems.

This trial marks a turning point in how traditional banking infrastructure interacts with distributed ledger technology.

The foundation for this milestone was laid through earlier collaboration between Swift, Chainlink, and UBS Asset Management. That work demonstrated cross-chain settlement of tokenized assets using existing Swift fiat payment rails.

More than 12 world-leading financial organizations participated, including Citi, BNY Mellon, Euroclear, Clearstream, and Lloyds Banking Group. The results established a replicable framework now being extended across Swift’s global network.

Chainlink’s Cross-Chain Interoperability Protocol (CCIP) serves as the technical backbone enabling settlement across public and private blockchains. Banks can now access on-chain environments while operating within familiar Swift messaging standards.

This removes the need for institutions to rebuild existing infrastructure from the ground up. Instead, blockchain connectivity becomes an extension of systems already trusted by thousands of institutions worldwide.

At Sibos 2024, Chainlink Co-Founder Sergey Nazarov presented these capabilities to capital markets participants. The showcase demonstrated how Swift integration with blockchains works through existing standards and Chainlink infrastructure.

Institutions can streamline interoperability without sacrificing the compliance frameworks they already operate within. This approach directly addresses one of the most persistent barriers to institutional blockchain adoption.

As part of the Monetary Authority of Singapore’s Project Guardian, Swift, UBS Asset Management, and Chainlink went further. They demonstrated the issuance and settlement of tokenized funds using traditional Swift fiat payment rails.

Digital asset transactions settled through infrastructure already used by institutions across more than 200 countries. That proof of concept confirmed that tokenized finance and conventional payment systems can operate as one unified layer.

Building a Shared Data Foundation for Capital Markets

At Sibos 2025, Chainlink and 24 of the world’s largest financial institutions announced Phase 2 of their corporate actions initiative. Partners include Swift, DTCC, Euroclear, UBS, and Wellington Management.

The phase introduces a production-grade system with new data attestor and contributor roles assigned to trusted institutions. These roles allow participating organizations to validate and enrich AI-extracted corporate actions records with verifiable accuracy.

The Chainlink Runtime Environment (CRE) managed the orchestration of multiple AI model outputs throughout the testing period. Confirmed results were converted into ISO 20022-compliant messages and delivered through the Swift Network.

At the same time, Chainlink CCIP distributed identical records across DTCC’s blockchain ecosystem and additional chain environments. Post-trade systems, smart contracts, and custodians could all access the same data simultaneously.

During testing, AI models reached nearly 100% data consensus across all evaluated corporate actions records. The system processed multilingual disclosures written in Spanish and Chinese, broadening its global coverage across jurisdictions.

Cryptographic attestation by designated institutions created a verifiable chain of custody for each corporate action. Data accuracy for confirmed records reached 100%, establishing a new reliability standard for the industry.

This infrastructure produces what the initiative calls an on-chain golden record. It functions as a real-time, attested source of truth accessible by both blockchain platforms and traditional financial systems.

Tokenized equities can now reference the same confirmed data across public and private chains. That synchronization creates the conditions for greater automation across on-chain markets going forward.

The Global Legal Entity Identifier Foundation (GLEIF) extended this infrastructure further through a strategic partnership with Chainlink. Their combined solution integrates GLEIF’s verifiable Legal Identity Identifier with Chainlink’s Cross-Chain Identity and Automated Compliance Engine.

Institutions can now verify asset provenance, enforce compliance policies programmatically, and meet regulatory requirements across multiple jurisdictions. Taken together, these layers of infrastructure form the backbone of a capital markets system built for the era ahead.

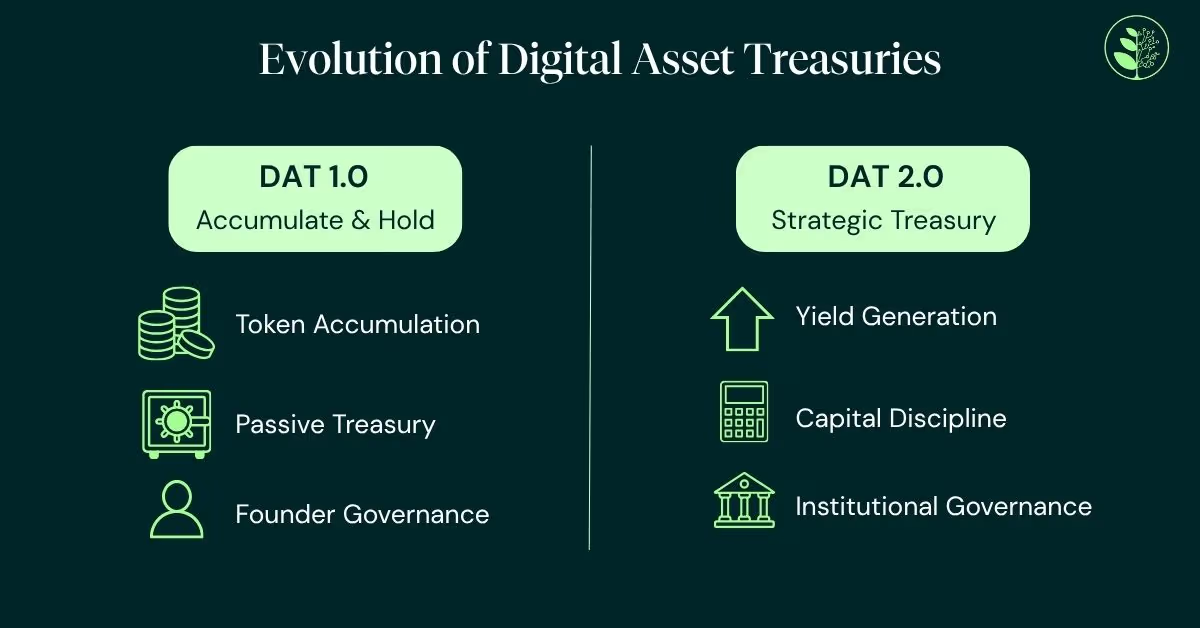

The era of buying bitcoin and calling it a treasury strategy is over.

By early 2026, more than 200 publicly listed companies hold digital assets on their balance sheets, collectively managing over $115 billion (DLA Piper, October 2025). The total market capitalization of these companies reached approximately $150 billion by September 2025 – a nearly fourfold increase from the year before. Yet several of these companies now trade at discounts to the value of the assets they hold. The market is sending a clear signal: accumulation alone is no longer enough.

Investors want to see capital discipline and economic return. Management teams have responded with share repurchase programs and transparency metrics such as “BTC per share,” designed to show the value a treasury adds beyond the token price (AMINA Bank Research, 2026). The shift from passive accumulation to active yield generation – from “DAT 1.0” to “DAT 2.0”—is now the defining theme of the sector.

Three broad models are emerging. Each carries a different risk – return profile and places distinct demands on governance, technical capability and infrastructure.

Infrastructure participation and staking

The most protocol-native approach involves staking tokens to support network consensus and earning rewards in return. For bitcoin-focused treasuries, this increasingly extends to the Lightning Network and other native infrastructure that generates routing and liquidity-based fees. Staking requires careful analysis of the technical security and smart contract risks.

The numbers have grown quickly. Bitmine Immersion Technologies reported over 3 million staked ETH by early 2026, with total holdings of $9.9 billion and annualized staking revenue of approximately $172 million (SEC Filing, March 2026). Its proprietary validator network marginally outperformed the Composite Ethereum Staking Rate, demonstrating the edge that institutional-grade infrastructure can deliver even in a protocol-level yield environment.

SharpLink Gaming deployed $200 million in ETH into restaking infrastructure via EigenCloud, targeting higher yields by securing applications ranging from AI workloads to identity verification (SEC Filing, 2025). Restaking – where already-staked ETH is used to secure additional services, with careful governance.

Active trading and market-driven income

A second set of strategies leverages market structure – funding-rate arbitrage, basis trading and options premiums. These can be effective and often market-neutral, but they demand trading expertise, robust risk controls and round-the-clock monitoring. The governance implications are significant: this approach effectively converts a treasury function into a trading operation. Like any trading function, it can be difficult to find skilled staff required to monitor complex positions and correlation risks.

One prominent Japanese listed company illustrates both the potential and the complexity. Holding over 35,000 BTC by the end of 2025, it generated the equivalent of approximately $55 million in bitcoin income revenue through option-based strategies, with operating profit growth exceeding 1,600% year-on-year. Yet the same company recorded a substantial net loss due to non-cash mark-to-market revaluations under local accounting standards (TradingView; Kavout, 2026). For investors, this disconnect between operational cash flow and reported earnings makes evaluation materially harder – and underscores why governance and transparency matter as much as headline returns.

Galaxy Digital offers a contrasting hybrid model, combining its own digital asset treasury with institutional services including collateralized lending, strategic advisory, and infrastructure. In Q3 2025, Galaxy posted a record adjusted gross profit of over $730 million (Mint Ventures Research, 2025). Notably, the firm has diversified its yield sources beyond pure crypto by repurposing its Helios mining facility as an AI compute campus secured by long-term contracts – a signal that the most resilient treasuries may be those that derive income from multiple, uncorrelated sources.

Credit deployment and net interest margin

A third route treats digital assets as productive balance-sheet capital. The model involves borrowing against crypto holdings on a non-recourse basis, receiving stablecoin liquidity, and deploying it into higher-yielding private credit. It preserves long-term exposure to the underlying asset while generating recurring interest income from short-duration, real-economy lending. In particular, this strategy demands expertise in yield, credit risk and fixed income.

The mechanics draw directly from traditional banking: liquidity management, underwriting, governance and controlled leverage. Under this type of model, a company acquires bitcoin, borrows against those holdings on a non-recourse basis—meaning the downside is limited to the collateral—and deploys the proceeds into diversified private credit portfolios supporting real-economy lending. If bitcoin appreciates, the company retains the upside after repaying the loan, combining potential capital gains with recurring interest income.

For credit deployment models to work credibly, they need to be grounded in operational financial infrastructure rather than built from scratch. The approach is most effective when it extends from an existing platform with real lending relationships and established client accounts. In our view at Greenage, this is also an area where governance and due diligence frameworks are particularly important, given that capital is being deployed into third-party credit opportunities that must be assessed on a counterparty-by-counterparty basis.

The success of this model is also tied to the maturation of stablecoins as institutional infrastructure. By 2026, stablecoins underpin cross-border payments, real-time settlement and T+0 clearing (same-day settlement) for enterprises (Foley & Lardner, January 2026). Coinbase Institutional projects total stablecoin market capitalization could reach $1.2 trillion by 2028 (Coinbase Institutional, August 2025). For credit deployment strategies, stablecoins provide a sound medium for capital deployment in lending markets.

The new measure of maturity

Recent market conditions have reinforced a simple truth: price appreciation alone is not a treasury strategy. The growing range of yield solutions reflects a sector learning from its own history—sustainable income generation makes digital assets more productive components of a corporate balance sheet.

No single model is definitive. The most effective treasuries will blend approaches depending on risk appetite, operational capability and governance structure. But the direction of travel is clear. Passive holding is no longer sufficient to justify digital assets’ place on the balance sheet. Yield is becoming the central measure of treasury maturity –and the core factor in how the market values companies with digital asset exposure.

The winners in this next phase will not be the largest holders. They will be the most disciplined operators.

Important Notice:

This article has been prepared by Greengage & Co. Limited for informational and thought leadership purposes only. It is intended solely for use by businesses, professional counterparties and institutional market participants and is not directed at retail consumers. It does not constitute financial advice, investment advice, a financial promotion, or a recommendation or inducement to buy, sell, or hold any asset, security, or financial instrument.

Digital assets are subject to significant price volatility and regulatory change. Past performance is not indicative of future results. All investments carry risk, including the potential loss of capital. Forward-looking statements and market projections referenced herein are sourced from third-party research and do not represent the views or predictions of Greengage & Co. Limited.

Greengage & Co. Limited is not authorized or regulated by the Financial Conduct Authority for investment business. Greengage acts solely as an introducer to independent third-party service providers and does not arrange investments, provide lending, custody, or investment management services.

Readers should seek independent professional advice before making any investment decision.

Prediction markets are pushing into Asia’s largest economies even as local gambling laws impose strict limits on traditional betting activities. The region’s combination of scale, active retail participation, and limited local alternatives creates a compelling case for prediction markets to grow, though regulatory risk remains a defining factor.

That dynamic mirrors a broader pattern in crypto where technology often outpaces licensing and oversight. Polymarket, one of the fastest-growing platforms, is already recording weekly volumes above $1 billion and has added Chinese-language support. New entrants like PredicXion are betting that region-focused events will help unlock adoption in markets where localization matters just as much as the product itself.

Yet Asia’s landscape is fragmented and legally intricate, with access, language, and regulation not always aligning with the sector’s global ambitions. As platforms push forward, the legal framework—rather than technology—could ultimately shape how quickly prediction markets scale in the region.

Key takeaways

- Asia’s largest economies show robust demand for prediction markets, but India’s heavy taxation on undisclosed gains and China’s outright ban on crypto activities create a complex regulatory backdrop.

- Japan and South Korea—two leading crypto markets in Asia—maintain strict gambling rules, which narrows access yet leaves room for localized efforts and experimentation.

- Polymarket remains a reference point for the model, with weekly volume surpassing $1 billion and expansion into Chinese-language support, while regional players like PredicXion emphasize Asia-centric events.

- Regulatory classification—whether these platforms are treated as gambling, information markets, or financial instruments—will largely determine their future in Asia and beyond.

Asia’s market pull and regulatory headwinds

GDP scale matters in the appeal of prediction markets. In 2024, major Asian economies such as China, India, Japan, and South Korea ranked among the world’s top five by gross domestic product, underscoring why the region is a focal point for growth in data-driven prediction tools. While India and China do not have explicit frameworks addressing blockchain-based prediction markets, both maintain restrictive environments for crypto. India imposes heavy taxation on gains, while China enforces an outright ban on several crypto activities, including trading and mining.

South Korea’s example is particularly instructive: it is one of the world’s largest economies by GDP, and its won (KRW) consistently features among the most active fiat currencies in crypto markets. Kaiko’s data highlight the KRW’s prominence in on-chain trading activity, a reminder that local currency liquidity can play a pivotal role in any regional expansion of prediction markets.

From a market perspective, Korea is often cited as a fertile ground for retail crypto adoption. Yet the local market’s gambling laws create a nuanced environment for prediction-market operators. Heechang Kang, co-founder of research firm Four Pillars, told Cointelegraph that while the Korean market could offer significant opportunities, platforms must address audiences beyond Western-focused themes to achieve broader traction.

The regulatory lens: gambling vs information markets

The regulatory question is at the heart of Asia’s prediction-market push. In several markets, authorities classify activities tied to wagering on uncertain outcomes as gambling, a category that is tightly controlled or prohibited outside state-run frameworks. Andy Cheung, founder and CEO of PredicXion, stresses that this creates a “significant concern” for operators operating in jurisdictions where gambling rules are opaque or stringent.

Despite these realities, some analysts argue that prediction markets are not simply gambling. Jaewon Kim, a researcher at Four Pillars, has framed the distinction around output: gambling is a closed loop of bets against a house, while prediction markets aggregate collective expectations about real-world events. Kim noted that during the 2024 U.S. presidential election, prediction markets gained traction and, in some cases, proved more accurate than polls or expert forecasts, underscoring the informational value they can offer beyond pure wagering.

China’s strict online policy complicates access, with many users turning to VPNs to reach platforms like Polymarket. However, this circumvents controls rather than resolves the legal risk, and authorities’ stance on whether prediction-market-like activity falls under gambling or a distinct information-market category remains unsettled. In Korea and Japan, regulators have yet to issue clear guidance specific to blockchain-based prediction markets, but both countries maintain rigorous gambling restrictions that can constrain user participation and operator growth.

Localized platforms, regional focus, and the path forward

Against this backdrop, Asian-anchored platforms are emphasizing localization as a core strategy. PredicXion is attempting to tailor markets toward events familiar to Asian retail audiences, seeking to avoid directly traversing heavily restricted markets where possible. Cheung notes that in several jurisdictions, operators must navigate a maze where wagering on uncertain outcomes is often treated as gambling, potentially limiting the range of acceptable products and geographies.

Polymarket’s approach illustrates the regional tension between global platforms and local realities. The platform has returned to activity levels comparable to those seen during the U.S. presidential election, a signal of resilience in a market where regulatory clarity remains uneven. Its expansion into Chinese-language support aims to widen accessibility, while its presence in Asia continues to test how far a global model can travel when local rules push back.

At the same time, the industry’s argument that prediction markets offer value beyond wagering hinges on their ability to aggregate real-world expectations. Jaewon Kim’s assessment points to an informational utility that could align with regulated financial-like instruments if policymakers converge on a workable classification. The question for investors and builders is whether regulators will carve out a distinct lane for prediction markets as information markets or keep them tethered to gambling frameworks with narrow licensing pathways.

In practice, the next steps will be defined by regulatory decisions across Asia’s largest economies. Platforms that can demonstrate responsible governance, transparent operation, and robust consumer protections may find a path forward even as others retreat to clearer, more tightly controlled markets.

As Asia weighs these choices, observers should watch regulatory statements and licensing developments in India, China, Korea, and Japan—along with evolving cross-border approaches to information markets. The outcome will shape not just where prediction markets can operate, but how they are structured, marketed, and perceived by everyday users seeking to gauge the pulse of real-world events.

28 Years Later, Steven Spielberg’s WWII Masterpiece Returns to Streaming

Brit dad facing jail in Thailand after mistakenly picking up stranger’s phone in bar

DOG: Hedging ETF With Positive Drift

-

NewsBeat2 days ago

NewsBeat2 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business2 days ago

Business2 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion23 hours ago

Fashion23 hours agoWeekend Open Thread: Spanx – Corporette.com

-

Entertainment5 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World3 days ago

Crypto World3 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Tech6 days ago

Tech6 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Crypto World4 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Entertainment7 days ago

Entertainment7 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Tech6 days ago

Tech6 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Sports4 days ago

Sports4 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Business3 days ago

Business3 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech4 days ago

Tech4 days agoEE TV is using AI to help you find something to watch

-

Fashion7 days ago

Fashion7 days agoAmazon Sundays: Soft Spring Layers

-

Tech6 days ago

Tech6 days agoElon Musk’s last co-founder reportedly leaves xAI

-

Fashion5 days ago

Fashion5 days agoThe Best Spring Trends of 2026

-

Tech4 days ago

Tech4 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech5 days ago

Tech5 days agoApple will hide your email address from apps and websites, but not cops

-

Politics5 days ago

Politics5 days agoShould Trump Be Scared Strait?

-

Crypto World5 days ago

Crypto World5 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech5 days ago

Tech5 days agoFlipsnack and the shift toward motion-first business content with living visuals

You must be logged in to post a comment Login