Crypto World

Amazon: Record Earnings Are Priced In as the Trend Loses Momentum

Fundamental backdrop

In the first quarter of 2026, Amazon (AMZN on FXOpen) reported a 17% increase in net sales to $181.5 billion. AWS revenue grew by 28% — its fastest pace in 15 quarters — while operating margin reached a record 13.1%. These results provided a solid fundamental foundation for the rally in Amazon shares seen from February through early May.

Now that the positive impact of the quarterly earnings release has likely been fully priced in, the market appears to be shifting its focus towards second-quarter prospects. A key event for the period will be the annual Prime Day sales event, scheduled for June 2026.

Technical picture

Since 27 March, Amazon shares have posted a sharp advance, forming a short-term uptrend. The move was supported by an ascending trendline connecting the 200 area with the 278 region, where local resistance emerged. At present, the price is testing this trendline for a potential downside break and has already moved below the lower boundary of the profile located at 260, signalling weakening bullish structure.

The point of control (POC) is situated in the 263–264 area, close to the lower boundary of the profile. Should the stock attempt to recover, this boundary may become the first obstacle for buyers. The upper boundary of the profile at 273 may also attract market attention if the price returns to the range. Above it lies a resistance level near 278.

The RSI and its moving averages currently stand at 39, 45 and 49. All three readings remain below the 50 mark, indicating the development of a bearish phase and weakening upward momentum. The 248 area, where the green support level is located, remains the nearest downside target should the decline continue.

Key takeaways

Amazon shares have undergone a strong upward move supported by record financial results; however, the technical picture now points to a potential trend reversal. Further developments will largely depend on whether sellers can maintain control below the current volume profile.

Buy and sell stocks of the world’s biggest publicly-listed companies with CFDs on FXOpen’s trading platform. Open your FXOpen account now or learn more about trading share CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

The past several months have not been kind to XRP. After it marked a new all-time high in mid-July 2025, it has been mostly downhill, losing over 70% of its value, dumping toward $1.00, being surpassed by BNB and USDC in terms of market cap, and registering six consecutive months in the red at one point.

Amid all of these adverse developments, some analysts have turned highly bearish on the asset. While the dominant belief is that XRP has reached its most crucial moment during this cycle, some, such as Ali Martinez, pointed to potential drops to the next crucial support levels at $0.80, $0.62, or $0.51 if the $1.00 floor gives in.

Glassnode warned that XRP token holders continue to realize more losses than profits, indicating intensifying selling pressure even among investors in the red. Even ChatGPT made some worrying predictions if the asset indeed flips $1.00 from support into resistance soon. But maybe such low sentiment is what is needed for XRP to turn things around.

Run Up Instead?

Paradoxically, history shows that the markets rarely reward such consensus. In fact, Warren Buffett has said it best, “Be fearful when others are greedy, and be greedy when others are fearful.”

Extreme pessimism has frequently appeared near important turning points across the crypto market. BTC, ETH, and XRP have all experienced periods where sentiment collapsed and remained there for a while before major recoveries began. This is generally possible when weak hands exited, and long-term investors quietly accumulated.

For XRP, this accumulation appears to be coming from ETF investors, as the funds tracking its performance have seen a green-only streak of eight consecutive weeks, while the BTC and ETH ETFs have bled out heavily.

The recent sell-off also pushed several on-chain and technical metrics into historically oversold territory. Some analysts argue that XRP may be approaching a zone where risk-reward begins to improve, even if short-term volatility persists.

History is indeed on XRP’s side. Recall that the asset’s sentiment had plunged to similar levels in mid-June but skyrocketed by double digits within 24 hours as the analytics company Santiment attributed that rally to the deteriorating investor behavior.

July Agrees

Current data show that XRP is on track to close June with a decline of over 20%, its worst monthly performance since February 2025. Data from CryptoRank suggests that this aligns with previous performances, as June has been a predominantly bearish month for the asset.

On the contrary stands July. XRP has closed each of the past six editions in the green, showing some impressive gains. Five out of the six have seen double-digit price increases, including massive 45%+ pumps in 2020 and 2023. The median gain for July stands at close to 11%.

The post Everyone Expects XRP to Crash Further: Is Ripple About to Surprise the Market? appeared first on CryptoPotato.

SBI Holdings is a financial services group with businesses spanning securities, banking, insurance, asset management and venture investing with a market capitalization of about $11 billion. The Tokyo-based company is one of Japan’s most active traditional-finance participants in digital assets, with stakes and partnerships across crypto trading, liquidity, tokenization, stablecoins and blockchain-based settlement.

Bitbank is one of the country’s largest licensed cryptocurrency exchanges, offering spot trading, custody and other digital-asset services to retail and institutional clients.

Cheaper, quicker to buy

Crypto mergers and acquisitions have remained brisk in 2026 as banks, payments firms and exchanges race to build regulated digital asset businesses rather than develop them in-house.

The industry has recorded 144 deals worth $11.8 billion so far this year, according to data from Architect Partners, with buyers increasingly targeting exchanges, custody providers, data firms and stablecoin infrastructure as regulatory clarity draws more institutional capital into the sector.

According to Payne, the Bitbank acquisition is about more than customer growth. The deal brings a Financial Services Agency-licensed exchange, one of Japan’s deepest altcoin liquidity pools and an institutional custody business, Japan Digital Asset Trust, giving SBI capabilities that would be far more costly and time-consuming to build internally.

The acquisition comes at a pivotal moment for Japan’s crypto industry. Legislation passed by the country’s lower house on June 11 would shift crypto assets under the Financial Instruments and Exchange Act, aligning them with securities regulation. The reforms lower the tax rate on crypto gains to a flat 20% and pave the way for spot bitcoin , ether (ETH) and XRP exchange-traded funds, while simultaneously imposing more stringent capital, custody and disclosure requirements on exchanges.

Mow is not the first to argue that bitcoin’s traditional four-year cycle has changed. After bitcoin climbed to a then-all-time high before the April 2024 halving, several analysts suggested growing institutional demand following the launch of U.S. spot bitcoin ETFs could alter the pattern that has historically followed each halving. Others, however, argued it was too early to conclude the cycle had changed.

$55,000 more likely

Not everyone agrees. Several analysts have recently argued that bitcoin is either close to a market bottom or still has further to fall, although they rely on different indicators and models.

CoinDesk market analyst Omkar Godbole recently wrote that if you were “wondering just how much lower bitcoin is likely to drop, the answer, at least according to one historically accurate contrarian indicator, is not much.”

That indicator is based on bitcoin’s 50-week and 100-week simple moving averages. The 50-week average, representing roughly one year, is very close to dropping below the 100-week line, forming what analysts call a “bear cross.” Historically, similar signals coincided with market bottoms, leading some analysts to see the pattern as bullish.

More recently, Markus Thielen, the founder of 10x Research, said he believes the bottom is more likely at $55,000 and not until somewhere between August and October. Arthur Hayes, the BitMex co-founder, took a more bearish position, saying bitcoin would bottom at around $40,000 within the next six months.

Michael Saylor shared a StrategyTracker chart on X this Sunday showing Strategy holds 847,363 bitcoin valued at $50.88 billion as of June 28, 2026, with 113 purchase events and an average cost basis of $75,653 per BTC.

That chart displays orange bubbles for MSTR’s buys overlaid on bitcoin price history, highlighting aggressive accumulation especially in 2024-2025 with the average purchase price line trending upward.

“We’re gonna need more charts” signals Saylor’s intent for continued bitcoin purchases, generating more data points as Strategy maintains its position as a leading corporate BTC holder.

Last week, Ripple CEO Brad Garlinghouse said he remains bullish on bitcoin but that Saylor’s approach to funding bitcoin purchases has damaged the wider cryptocurrency market, as the preferred stock at the center of Strategy’s model fell to a record low.

Strategy’s (MSTR) stock fell 8% lower Thursday to $86, amid concerns about its ability to meet dividend obligations. However, Saylor’s treasury still has 10 months of dollar reserves available to cover STRC’s dividend obligations. MSTR is currently priced at $82.31 following a further 3.54% drop. STRC hovers around $74.57 after a 1.48% increase on Sunday.

XRP is trading near $1.05 as buyers continue to defend the $1 level after a weak month.

Summary

- XRP trades near $1.05 after falling sharply over the past week and month.

- ETF inflows remain positive while Bitcoin and Ethereum funds continue showing heavy weekly outflows.

- Analysts watch $1 support, rising active addresses, and possible rebound signals toward the $1.30 zone.

The token is down more than 7% over the past week and about 19% over the past 30 days, while its 24-hour range sits between $1.04 and $1.07.

The price action remains weak, but several market signals show that XRP has not lost all support. ETF inflows remain positive, daily active addresses are rising, and some analysts now point to early reversal patterns on the daily chart.

XRP trades near $1 after sharp monthly decline

XRP holds a market rank of #6, with market capitalization near $65.4 billion. Its 24-hour trading volume stands above $1.1 billion, showing that activity remains strong even as price stays near recent lows.

The token remains far below its all-time high of $3.65 from July 2025. It has also fallen more than 50% over the past year and about 49% over the past 200 days, showing that the current weakness is part of a longer downtrend.

A recent XRP price prediction noted that XRP is trading near a 20-month low. The same report said $1 has become the key level to watch, with downside support near $0.85 and $0.70 if that area fails.

That makes the current setup simple. XRP needs to hold $1 to avoid a deeper technical breakdown. A strong move above $1.12 and then $1.27 would be needed before traders can argue that momentum is shifting back toward buyers.

ETF demand stays positive despite weak price

XRP fund flows continue to stand out against Bitcoin and Ethereum. On June 26, XRP ranked first in single-day net inflows at about $15.63 million, while spot Bitcoin ETFs saw about $444.51 million in outflows and Ethereum funds lost about $12.85 million.

The weekly trend also remains positive. XRP spot ETFs have now posted seven straight green weeks, with roughly $144.69 million in net inflows over that stretch, according to SoSoValue data.

This is not the same pattern seen in Bitcoin and Ethereum. Over the same seven-week stretch, Bitcoin ETFs recorded about $7.73 billion in outflows, while Ethereum ETFs lost around $1.18 billion.

A previous fund flow report showed XRP products had already beaten Bitcoin and Ethereum for five straight weeks. Another CLARITY Act analysis said XRP ETFs had drawn roughly $1.44 billion in cumulative inflows through six weeks of buying, even as price remained weak.

That contrast is important for the current XRP price analysis. It suggests that fund demand has not been enough to lift the token yet, but it may be helping to slow deeper losses near $1.

On-chain activity and chart signals improve

Analyst Ali Charts said XRP network activity has risen over the past two weeks. Daily active addresses climbed from about 23,000 on June 14 to nearly 39,500, pointing to higher on-chain participation.

Rising active addresses can show more users interacting with the network. It does not guarantee a price recovery, but it gives traders another data point at a time when price is testing a key support level.

Ali also pointed to two bullish reversal signals on the daily chart. He said the Tom DeMark Sequential indicator printed a “9” buy signal, which can sometimes appear before a short relief rebound lasting one to four daily candles.

He also said the past three daily sessions formed a Morning Star Doji pattern. That pattern is often used by technical traders to identify a local bottom after a downtrend.

If buying volume rises from here, Ali said XRP could move toward $1.30. That level also lines up with earlier resistance areas from recent price action.

A prior XRP technical report said traders were watching $1.20 as a recovery level, with $1.24 and $1.30 as the next zones if buyers pushed through resistance.

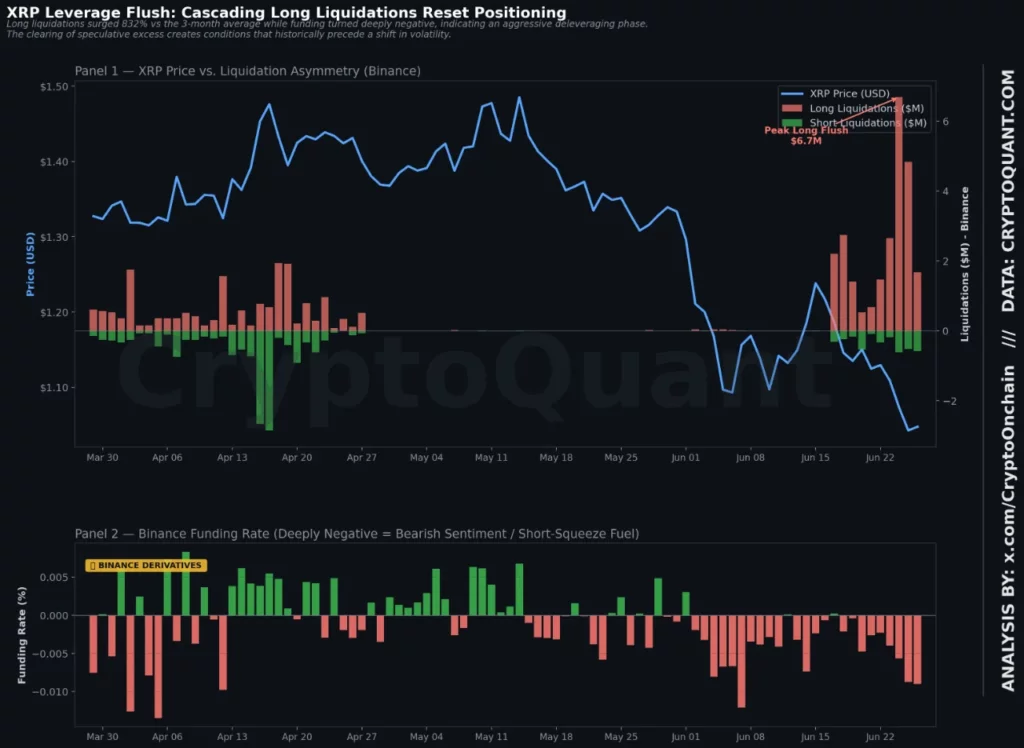

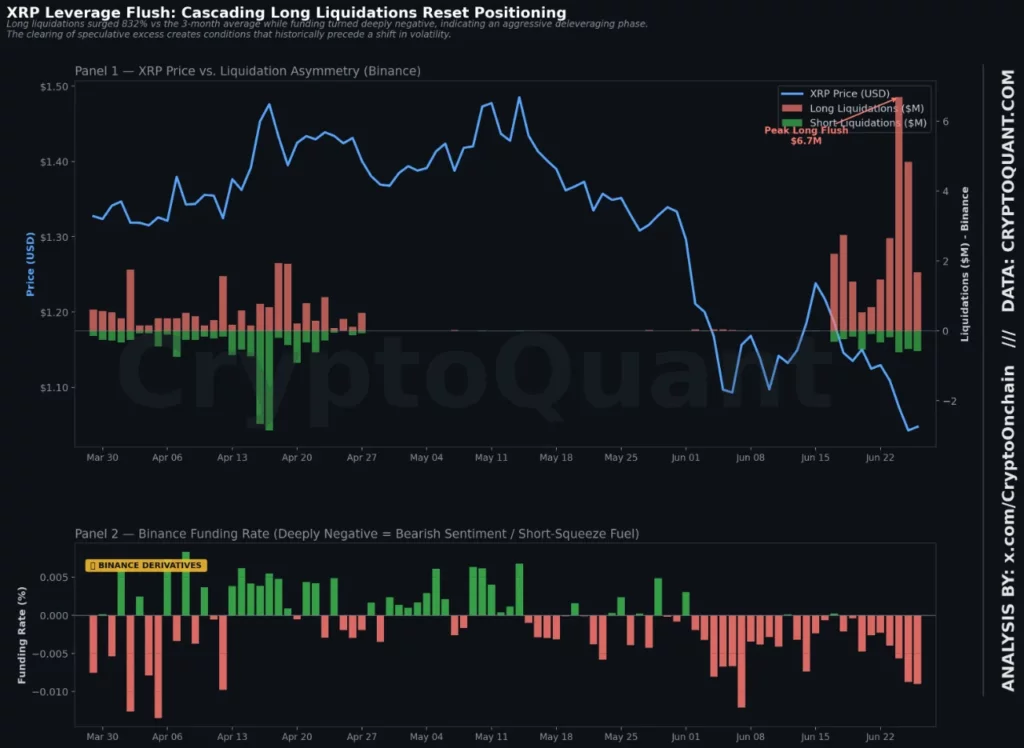

Derivatives reset may shape the next move

Acccording to CryptoOnchain, XRP derivatives have gone through a heavy deleveraging phase. Long liquidations jumped to nearly $3 million over the past week, up more than 800% from the prior month.

Open interest also fell from about $1.18 billion to roughly $1.04 billion. At the same time, funding rates turned deeply negative, showing that traders who were positioned for upside have been forced out.

That type of reset can cut speculative excess from the market. It can also create conditions for a sharp move if short sellers become crowded and spot buyers remain steady.

The spot side looks calmer than futures. Binance reserves were nearly flat over the week, suggesting holders are not rushing to move XRP to exchanges for immediate sale.

The next signal will come from open interest and funding rates. If open interest starts to recover while price holds $1, traders may read it as a healthier reset. If XRP loses $1 with rising volume, the market may shift back toward $0.85 and $0.70 support.

Ripple’s wider ecosystem also remains in focus after RLUSD became available in Japan through SBI VC Trade. The stablecoin launch gives Ripple a new regulated channel in Asia, though XRP’s short-term direction still depends on price action, fund flows, and whether buyers can defend the $1 level.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

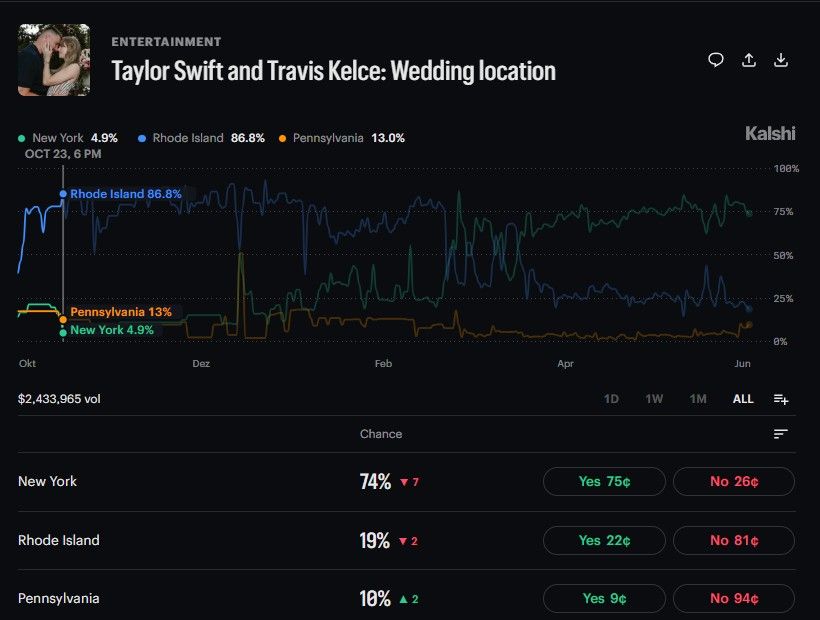

Taylor Swift and Travis Kelce’s unannounced wedding has already generated more than $4 million in trading volume on prediction platform Kalshi, with bettors wagering on the venue, the date, and even the bridesmaids.

According to Kalshi, entertainment trading grew from $43 million in 2024 to over $300 million in 2025. Music markets alone surpassed $400 million in Q1 2026, putting total 2026 entertainment volume on pace for $1 billion.

Location and Timing Drive the Biggest Bets

The location market has drawn $2.26 million in volume, making it Kalshi’s largest Swift-Kelce trading category. New York holds 80% odds, with Rhode Island trailing at 21%. Polymarket narrows the call further, placing Manhattan at 85%.

A street-closure permit filed near Madison Square Garden for July 3 has intensified speculation about the date. Neither Swift nor Kelce appears on the permit.

Kalshi gives 95.5% odds that the wedding will occur this year. Polymarket sets the chance of it occurring before August 31 at 96%. The permit reportedly calls for tenting outside the arena to accommodate between 500 and 999 guests.

New York City will simultaneously host July 4 celebrations and FIFA World Cup matches that weekend.

Separate markets track the wedding party. Jason Kelce leads the odds of being a groomsman at 89%, followed by Patrick Mahomes at 72%.

On the bridesmaid’s side, Abigail Anderson Berard holds 85% odds for maid of honor. Selena Gomez follows at 76%, with Gigi Hadid at 54%. Blake Lively and Brittany Mahomes, meanwhile, have both fallen to 8% odds.

Celebrity Markets Break Records as Kalshi Eyes $40 Billion

The Swift-Kelce surge arrives as prediction markets post record monthly transactions. Monthly active users reached 865,411 in March 2026, up 118% from the prior year. Monthly notional volume hit $23.89 billion, a 1,107% year-over-year increase.

The sector grew from roughly $1.2 billion in monthly volume in April 2025. By March 2026, that figure had exceeded $25 billion. Kalshi is targeting a $40 billion valuation in an ongoing funding round, up from $22 billion a month earlier.

The platform has also expanded through a World Cup prediction partnership, broadening its market categories.

Female Traders Reshape the Prediction Market Audience

Kalshi reports the share of female traders on its platform has doubled over the past year. That shift suggests celebrity-focused markets attract users well beyond the typical trading audience. Research also shows US voters consult prediction markets alongside conventional polling.

A bill seeking to ban prediction markets has circulated in Congress, though it has yet to clear both chambers. Despite that, Kalshi’s reach across sports, politics, and pop culture continues to grow.

The post Swifties Storm Prediction Markets: Over $4 Million Wagered on Taylor Swift’s Wedding appeared first on BeInCrypto.

Whether a token is a security or a commodity decides almost everything about how it can be traded, listed, and held in the U.S. In March 2026 regulators called sixteen major tokens “digital commodities,” but only on interpretive footing a future administration could undo. The CLARITY Act would turn that label into law. Here is what a digital commodity actually is, and how the bill would reclassify crypto.

Summary

- A digital commodity is a crypto asset whose value comes from the workings of a functional blockchain and from supply and demand, not from the expectation of profit from a company’s managerial efforts.

- The distinction matters enormously: a security falls under the securities regulator’s heavy registration and disclosure regime, while a commodity falls under the commodities regulator’s lighter-touch oversight.

- In March 2026 the SEC and CFTC jointly classified sixteen major tokens, including Bitcoin, Ethereum, XRP, and Solana, as digital commodities, but that was an interpretation, not a law, and a future administration could reverse it.

- The CLARITY Act would write the digital-commodity category into federal statute, making the classification durable, and create a maturity test that lets a token move from security to commodity as its network decentralizes.

- Reclassification changes what products can be built, especially exchange-traded funds, how exchanges list assets, how institutions hold them, and how much investor protection applies.

A digital commodity is a crypto asset whose value comes from the workings of its blockchain and from supply and demand, rather than from the promised efforts of a company or team, which is the legal distinction that places it under the lighter-touch oversight of the commodities regulator instead of the heavier hand of the securities regulator. That sentence contains the entire stakes of one of the most consequential questions in crypto: for any given token, is it a security or a commodity. The answer determines which federal agency has authority over it, what financial products can be built around it, how exchanges can list it, whether large institutions can comfortably hold it, and how aggressively the government can act against the people who issue and trade it. For more than a decade, the U.S. had no clear way to answer that question for most tokens, leaving the entire industry in a gray zone, and the fight over how to draw the line, and who gets to draw it, has shaped the regulation of crypto in America more than any other issue.

In 2026 that long-running question reached a turning point on two fronts at once, and understanding both is essential to understanding what a digital commodity is and why it matters. On the regulatory front, the two relevant agencies, the securities regulator and the commodities regulator, took the unprecedented step of jointly declaring sixteen major tokens to be digital commodities, ending years of ambiguity for those specific assets. On the legislative front, Congress has been working on the CLARITY Act, a bill that would take the digital-commodity concept and write it into permanent federal law, with a mechanism for deciding which tokens qualify and how a token can move from one category to another over time. This guide explains what a digital commodity actually is, why the security-versus-commodity distinction decides so much, the test at the heart of classification, what the 2026 regulatory interpretation did and why it was not enough on its own, how the CLARITY Act would reclassify crypto by statute, the clever maturity mechanism that lets a token change categories, what reclassification practically changes, and the real limits and risks that remain.

What a digital commodity actually is

Start with the precise definition, because the legal language is doing specific work. A digital commodity, in the formulation regulators have adopted, is a crypto asset that is intrinsically linked to and derives its value from the programmatic operation of a functional crypto system, as well as from supply and demand dynamics, rather than from the expectation of profits from the essential managerial efforts of others. That is a dense sentence, so it helps to unpack it: the key idea is the source of the asset’s value. A digital commodity is valuable because of how its blockchain works and because of ordinary market forces of supply and demand, not because some company is promising to do work that will make the token go up.

Crucially, regulators have added that a digital commodity does not carry intrinsic economic rights such as generating a passive yield or conveying a claim on the future income, profits, or assets of a business, which is exactly the kind of feature that would make something look like a security. The contrast that makes this concrete is the traditional commodity. Think of oil, wheat, or gold: these are produced by many different parties around the world, not issued by a single company to raise money for itself, and one unit is interchangeable with another, so one barrel of a given grade of oil is worth the same as any other. Their value comes from supply and demand and from their inherent usefulness, not from anyone’s promise of profit.

Regulators have long treated Bitcoin the same way, reasoning that it is produced by many disparate miners around the world, is fungible, and has no central issuer making promises, which makes it commodity-like rather than security-like. The digital-commodity category extends that logic to other tokens whose networks are sufficiently decentralized and functional that no central enterprise is driving their value through promised efforts. A digital commodity, then, is the crypto equivalent of gold or oil instead of the crypto equivalent of a company’s stock. That single distinction is what determines how it is regulated.

Security or commodity: the question that decides everything

To see why this classification carries such weight, you have to understand how differently the two categories are regulated. Securities, which include stocks and bonds, fall under the securities regulator, whose regime is built around investor protection through heavy obligations: companies issuing securities must register their offerings, provide extensive ongoing disclosures, and operate within a tightly controlled system of registered broker-dealers and exchanges, all backed by the threat of enforcement for non-compliance. The logic is that when people invest money expecting profit from someone else’s efforts, they need protection and information, so the law imposes a demanding framework. Commodities, by contrast, fall under the commodities regulator, whose regime is far lighter.

The commodities regulator oversees the derivatives markets for commodities, such as futures and options, and can pursue fraud and manipulation, but it does not impose the same registration-and-disclosure burden on the underlying asset. It also has limited direct authority over spot markets where commodities are bought and sold for immediate delivery, which is why the jurisdictional split codified by the CLARITY Act matters so much. The practical consequences of which bucket a token lands in are enormous, which is why the industry has fought over classification for years. If a token is a security, its issuer faces registration and disclosure requirements, the exchanges listing it face securities-law obligations, and institutions weighing whether to hold it confront the heavier compliance and restrictions that come with securities.

If the same token is a commodity, those burdens largely lift: listing is easier, compliance is lighter, and the path to building products around it, especially exchange-traded funds, becomes far more direct. Classification also determines which regulator writes the rules, who pays which fees, how custody is handled, and how much room institutions have to participate. Calling a token a security or a commodity is not a technicality; it is a decision that shapes whether a project can operate smoothly in the U.S. or faces a wall of regulatory friction. It also influences the token’s accessibility to the institutional capital that can move its price, which is why the definition of a digital commodity, and the process for deciding which tokens qualify, became one of the central battles in crypto policy.

The Howey test and the efforts of others

At the heart of the security-versus-commodity question sits a legal test that has governed it for decades: the Howey test. Derived from a Supreme Court case, the Howey test defines an investment contract, which is a type of security, as an investment of money in a common enterprise with an expectation of profits derived from the efforts of others. That last phrase, the efforts of others, is the crux. If you buy a token primarily because you expect a company or team to do work that will increase its value, the arrangement looks like a security, because your profit depends on their efforts.

If, instead, the token’s value comes from a decentralized network and market forces with no central party whose efforts you are relying on, it looks more like a commodity. The Howey test is why the same token can be treated differently depending on how it is sold and how mature its network is. This is also where one of the most important and confusing features of crypto classification comes from: a token’s status is not necessarily permanent. The Howey analysis depends on facts that can change as a project evolves.

A token might begin its life as a security, sold by a founding team to raise money for a network that does not yet exist, where buyers are clearly relying on the team’s efforts. Over time, if the network becomes genuinely functional and decentralized, with no central team driving its value, the same token can stop looking like a security and start looking like a commodity, because the efforts-of-others element fades away. This transition is the key conceptual move that everything else builds on, and it explains why regulators and lawmakers have struggled to draw clean lines: the line itself moves as a project matures. The 2026 regulatory interpretation adjusted the Howey analysis for crypto by requiring that an issuer affirmatively make representations or promises about its essential managerial efforts for there to be an investment contract, which sharpened the test in a way favorable to treating mature, decentralized tokens as commodities.

The March 2026 interpretation: a label, not a law

In March 2026 the security-versus-commodity question got its most significant answer yet, though an incomplete one. The securities regulator and the commodities regulator, which had spent years disagreeing over jurisdiction, jointly issued a formal interpretation that, for the first time, set out an agreed framework for classifying crypto assets. The interpretation sorted crypto into a taxonomy of categories, most of which are not securities: digital commodities, digital collectibles such as certain non-fungible tokens, digital tools that perform a utility function like membership or access, stablecoins, which sit in their own lane governed by separate stablecoin legislation, and digital securities, the one category that clearly is a security. Within that framework, the agencies named sixteen major tokens as examples of digital commodities, including Bitcoin, Ethereum, Solana, and XRP, alongside others such as Cardano, Litecoin, and even some memecoins, explicitly declaring that these assets are not securities and that their spot trading falls primarily under the commodities regulator.

This was a landmark moment, the first time the two top financial regulators agreed in writing on how to treat these assets, and it brought real clarity to the named tokens. But it carried a critical limitation that defines why the story does not end there. The interpretation is exactly that, an interpretation: a statement of how the agencies read existing law, binding on the agencies themselves in how they administer the law, but not a new statute passed by Congress. That distinction matters enormously, because an interpretation issued by agencies can be modified or reversed by those same agencies under a future administration.

The clarity it provides is real but conditional, resting on the current regulators’ chosen reading instead of on durable law. This is precisely why, even as the industry welcomed the interpretation, many participants, and even one of the regulators involved, called for Congress to act, because only legislation can turn a reversible interpretation into permanent law. Stablecoins sit in their own separate lane, which is why the law governing the stablecoin category matters alongside the CLARITY Act rather than inside the same commodity bucket. Digital securities, meanwhile, remain a separate class, and the rise of the digital-securities category shows why not every on-chain asset belongs under commodity-style treatment.

How the CLARITY Act reclassifies crypto

The CLARITY Act, formally the Digital Asset Market Clarity Act, is the legislative effort to take the digital-commodity concept and write it into federal statute, giving it the permanence the 2026 interpretation lacks. The bill would create a statutory framework that sorts digital assets into categories and assigns them to regulators, with digital commodities placed under the commodities regulator and securities remaining with the securities regulator. In doing so, it would codify the jurisdictional split that the interpretation expressed, so that the division of authority between the two agencies rests on law instead of on an agreement that could be undone. A companion measure moving through the agriculture committee, sometimes called the Digital Commodity Intermediaries Act, would give the commodities regulator formal jurisdiction over the spot markets for digital commodities, addressing the long-standing gap in which that regulator could oversee derivatives but had limited authority over everyday spot trading.

The conceptual heart of how the CLARITY Act reclassifies crypto is a principle of separating the asset from the way it is offered and sold. Under this approach, the act recognizes that a token can be sold in a transaction that is an investment contract, and therefore a security at the point of that sale, while the underlying token itself can be a digital commodity. This separation is what allows the law to handle the awkward reality that the same token can look like a security in one context and a commodity in another. It means the securities regulator retains authority over primary-market fundraising, when a project first sells tokens to raise capital and buyers are relying on the team’s efforts, as well as over assets that truly function as investment contracts, while the commodities regulator takes over the secondary-market trading of digital commodities once a token’s network is mature.

By writing this structure into statute, the CLARITY Act would replace the case-by-case, lawsuit-driven approach of the past, in which classification was fought out one enforcement action at a time, with a predictable framework that issuers and exchanges can read in advance. That shift, from regulation by enforcement to regulation by clear rule, is what the industry treats as the bill’s central promise. It is also why the bill’s contested path matters so much: until the bill becomes law, the digital-commodity framework remains partly dependent on agency interpretation rather than statutory permanence. The category may now be easier to understand, but it still needs Congress to make it durable.

The maturity test: how a token moves from security to commodity

The cleverest and most important mechanism in the CLARITY Act is the one that lets a token change categories as its network matures, because it directly addresses the moving-line problem that Howey created. The bill creates a maturity test, a set of criteria for determining when a blockchain system has become decentralized and functional enough that its token should be treated as a digital commodity instead of as part of a securities offering. The underlying idea follows directly from the efforts-of-others principle: a token sold early in a project’s life, when a central team is building the network and buyers are betting on that team’s success, fits the securities framework. Once the network is truly up and running and no longer dependent on a central group’s managerial efforts, the justification for securities treatment fades, and the token can graduate to commodity status.

This creates what is sometimes called a maturity on-ramp, a path by which a token can begin under securities oversight and, as its network decentralizes and meets the maturity criteria, transition to commodity oversight. The criteria for maturity center on decentralization: roughly, whether the system operates without any single person or affiliated group exercising outsized control over the network or its value, whether it is functional, and whether its governance and operation are truly distributed. A blockchain that meets the test is treated as mature, and its native token is treated as a digital commodity. This mechanism is what makes the CLARITY Act more sophisticated than a simple fixed list of which tokens are commodities.

Instead of freezing classifications in place, it provides a rule for how a token earns commodity status by becoming the kind of decentralized network that commodity treatment is meant for. It is also, as the limits section notes, one of the most contested parts of the bill, because deciding exactly how decentralized is decentralized enough is truly difficult, and the definition the bill uses has been criticized from multiple directions. But the basic design, a test that lets status follow the reality of a network’s maturity instead of being fixed at launch, is the conceptual engine of how the CLARITY Act would reclassify crypto. It gives projects a legal path from fundraising-stage oversight to mature-network treatment, rather than forcing every dispute into the courts.

What reclassification actually changes

For everyday holders and for the market, the abstract question of classification translates into concrete consequences, so it is worth being specific about what changes when a token is treated as a digital commodity. The most immediate effect is on financial products, above all exchange-traded funds. An asset classified as a commodity follows a far more direct regulatory path to a spot ETF than a security does, which is why the digital-commodity designation has been linked to a surge of pending ETF applications across many tokens. For an investor, this matters because spot ETFs are often the most convenient and trusted way for both retail and institutional money to gain exposure to an asset, so commodity status can widen access and bring in new demand.

Reclassification also eases how exchanges list a token, since listing a commodity does not carry the securities-law obligations that listing a security does, and it lowers the compliance burden across the board. The change extends to institutions and to specific crypto activities. Large institutions, including asset managers and pension funds, generally face fewer restrictions holding commodity-classified assets than security-classified ones, so commodity status can unlock institutional participation that securities treatment would discourage. The 2026 interpretation also clarified that certain activities long shadowed by securities-law uncertainty, including protocol staking and the wrapping of tokens, are not in themselves securities transactions when conducted within defined boundaries, which removed legal risk that had pushed some platforms to suspend staking services.

To make the journey concrete, consider a token’s path under this framework: it might launch through a sale that is an investment contract, a security at that moment, with its issuer subject to securities obligations. Then, as its network grows decentralized and functional and meets the maturity test, the token itself comes to be treated as a digital commodity, its spot trading moves under the commodities regulator, exchanges can list it more easily, an ETF becomes feasible, and institutions grow more comfortable holding it. That arc, from security at birth to commodity at maturity, is the practical shape of what the CLARITY Act’s reclassification is designed to enable. It is why the industry views statutory clarity as the gateway to the next phase of adoption.

Limits, risks, and what is still unsettled

For all its significance, the digital-commodity framework comes with real limits and unresolved tensions that an honest account must address. The first and most important is the gap between interpretation and law. The 2026 classification of sixteen tokens as digital commodities is an agency interpretation, binding on the agencies but reversible by a future administration, which means the clarity it provides is conditional instead of permanent until Congress acts. And the legislation meant to make it durable, the CLARITY Act, has not become law; it has advanced through the House and a Senate committee but still faces a contested path, so the statutory permanence the industry wants is not yet secured.

Beyond the interpretation-versus-statute problem, several substantive concerns persist. The definition of decentralization at the core of the maturity test is truly hard to pin down, and critics argue the version in play is too narrow or too vague, which could lead to inconsistent or contestable classifications. There is a meaningful investor-protection tradeoff: moving an asset out of the securities regime and into the commodity regime means lighter disclosure requirements and fewer of the protections securities law provides, which supporters see as appropriate for decentralized assets but critics warn could leave holders more exposed, particularly because crypto can be more susceptible to manipulation than registered securities and direct crypto holdings do not carry the same regulatory safeguards. Classification can also remain context-dependent: even a token treated as a commodity in secondary trading could be part of a securities transaction if it is later sold subject to an investment-contract arrangement promising profits.

The whole area remains politically contested, with the CLARITY Act facing objections over its decentralized-finance provisions, its treatment of stablecoin yield, and ethics questions, any of which could reshape or stall it. The honest summary is that the digital-commodity category represents real and welcome progress toward clarity, but it currently stands on reversible interpretive ground, depends on legislation that has not passed, relies on a maturity test that is hard to define, and carries genuine investor-protection tradeoffs. It is a meaningful step in defining how crypto is regulated, not a finished or settled answer.

Frequently asked questions

What is a digital commodity in simple terms?

A digital commodity is a crypto asset whose value comes from how its blockchain works and from ordinary supply and demand, instead of from a company promising to do work that makes the token go up. That makes it the crypto equivalent of gold or oil instead of a company’s stock. Because no central enterprise is driving its value through promised efforts, it is treated like a commodity under the lighter-touch commodities regulator instead of as a security under the heavier securities regulator. Regulators have long treated Bitcoin this way and, in 2026, extended the label to other sufficiently decentralized tokens such as Ethereum, XRP, and Solana.

Why does it matter whether a token is a security or a commodity?

Because the two are regulated completely differently, and the difference shapes nearly everything. A security falls under the securities regulator’s heavy regime of registration, disclosure, and trading restrictions designed to protect investors. A commodity falls under the commodities regulator’s far lighter regime, which oversees derivatives and pursues fraud but imposes much less burden on the underlying asset. Commodity status makes a token easier to list, lighter to comply with, more accessible to institutions, and far closer to qualifying for a spot exchange-traded fund.

Which cryptocurrencies are digital commodities?

In March 2026 the securities and commodities regulators jointly named sixteen major tokens as examples of digital commodities, including Bitcoin, Ethereum, Solana, and XRP, along with others such as Cardano, Litecoin, Stellar, and some memecoins. The list was described as not closed, meaning other assets could qualify. The common thread is that these tokens derive their value from decentralized, functional networks instead of from a central team’s promised efforts. It is important to note this came from an agency interpretation instead of a law, so while it gave real clarity to those tokens, the classification rests on interpretive footing that could change until Congress passes durable legislation.

How does the CLARITY Act reclassify crypto?

The CLARITY Act would write the digital-commodity category into federal statute, placing digital commodities under the commodities regulator and securities under the securities regulator, codifying the jurisdictional split so it rests on law instead of a reversible interpretation. Its key mechanism is separating the asset from how it is sold: a token can be sold in a securities transaction while the underlying token is a digital commodity. The securities regulator keeps authority over fundraising and genuine investment contracts, while the commodities regulator takes over secondary trading of mature digital commodities. This replaces the old case-by-case enforcement approach with a predictable, statutory framework.

What is the maturity test?

The maturity test is the CLARITY Act’s mechanism for letting a token move from security to commodity as its network matures. The idea follows from the principle that a token sold early, when a central team is building the network and buyers rely on that team’s efforts, fits the securities framework, but once the network is truly decentralized and functional, no longer dependent on a central group, the token can graduate to digital-commodity status. The criteria center on decentralization: whether any single person or group exercises outsized control, whether the system is functional, and whether its operation is truly distributed. It creates a maturity on-ramp instead of freezing a token’s status at launch, though defining decentralization precisely remains contested.

Is a digital commodity safer or less regulated than a security?

It is less heavily regulated, which cuts both ways. Commodity status means lighter compliance, easier listing, and broader access, which the industry views as appropriate for decentralized assets and a driver of adoption. But it also means fewer of the disclosure requirements and investor protections that securities law provides, so holders may be more exposed, particularly because crypto can be more susceptible to manipulation than registered securities and direct crypto holdings lack the same safeguards. Commodity status is also not a permanent, blanket shield, since a token could still be part of a securities transaction if later sold with profit promises.

This article is educational information, not legal, financial, or tax advice. The classification of crypto assets, the status of the 2026 regulatory interpretation, and the progress of the CLARITY Act reflect information available as of June 28, 2026, and can change. Regulatory classifications can be modified, and the legal treatment of any specific token may differ by context and jurisdiction. Verify current details from primary sources and consult a qualified professional before making any decision.

Tether is expanding the use of Tether Gold as crypto lender Ledn adds support for XAU₮.

Summary

- Tether is expanding XAU₮ utility by bringing tokenized gold into Ledn’s lending platform this year.

- XAU₮ holders will be able to borrow against gold without selling the underlying tokenized bullion.

- The move follows Tether’s wider shift toward gold, Bitcoin mining, AI, and infrastructure assets.

The move will let users hold and trade tokenized gold on Ledn, with gold-backed loans expected later this year.

The plan extends Tether’s wider gold strategy at a time when tokenized bullion is gaining more use in crypto markets. Each XAU₮ token represents one fine troy ounce of physical gold stored in Swiss vaults.

XAU₮ joins Ledn’s lending platform

Ledn said it has added support for XAU₮ alongside Bitcoin, USD₮ and USA₮. The platform said users can now hold and trade XAU₮, while borrowing against the tokenized gold product will come later in 2026.

The product follows the same structure Ledn has used for Bitcoin-backed loans. Users can access liquidity while keeping exposure to the underlying asset instead of selling it for cash.

Ledn said client collateral remains held 1:1 and is not lent out or used to generate yield. That point matters after the 2022 crypto lending failures, when weak risk controls and rehypothecation hurt many customers.

The company said demand is growing for services that combine long-term asset ownership with financial flexibility.

“As digital assets become an increasingly important part of the global economy, demand is growing for solutions that combine long-term ownership with financial flexibility,” Tether CEO Paolo Ardoino said.

Tether expands its gold strategy

Tether Gold has grown sharply over the past year as demand for tokenized gold increased. Tether said XAU₮ reserves reached 707,747.139 fine troy ounces by March 31, 2026.

That was up from 520,089.350 fine troy ounces at the end of 2025. Tether said XAU₮’s market value rose from about $2.25 billion to more than $3.3 billion during the first quarter.

The wider $23 billion gold figure refers to Tether’s broader bullion position across its products. Reuters reported that Tether held about 132 metric tons of gold for USDT reserves at the end of March, valued near $19.8 billion, while XAU₮ accounted for about 22 tons.

Tether has also moved to focus more on XAU₮ after closing Alloy and aUSDT. As previously reported, users can redeem aUSDT and recover XAU₮ until Sept. 17 before Alloy support ends.

Gold-backed loans mirror Bitcoin lending

Gold-backed lending is not new in traditional finance. Banks, bullion dealers and large financial firms have long used physical gold as collateral.

Tether and Ledn are trying to bring that model into digital asset markets. Tokenized gold can move on blockchain rails while still tracking ownership of physical bullion held in custody.

This setup may appeal to users who want to keep gold exposure but still need liquidity. A borrower could use XAU₮ as collateral and receive stablecoins without selling the gold-backed asset.

The model also gives Tether another way to add use cases around XAU₮. Instead of acting only as a tokenized gold holding, XAU₮ could become collateral inside crypto lending markets.

Tokenized gold push widens

The Ledn plan follows other recent moves around Tether Gold. Tether and Fasset launched a Visa card with XAU₮ rewards, allowing eligible users to spend through the card and earn up to 6% cashback in tokenized gold.

That product placed XAU₮ closer to everyday payments. It also showed how Tether is testing uses for tokenized gold beyond storage and trading.

The company has also invested beyond stablecoins. Tether has backed Bitcoin mining, renewable energy projects, AI infrastructure, Gold.com and Antalpha as part of a wider technology and infrastructure push.

For Tether, the Ledn deal gives XAU₮ another practical role. Users may soon be able to borrow against tokenized gold in a structure closer to Bitcoin-backed lending, without giving up exposure to the underlying bullion.

Polymarket’s latest security incident has grown larger after blockchain intelligence firm AMLBot updated the estimated losses to about $3.1 million.

Summary

- Polymarket’s frontend phishing attack now shows $3.1 million in losses across 11 user wallets.

- The platform says a compromised third-party vendor injected malicious code into parts of its frontend.

- The refund pledge comes as lawmakers press regulators over alleged deceptive prediction market advertising practices.

The prediction market platform had earlier promised to refund affected users after saying a third-party vendor compromise allowed malicious code to reach some users through its frontend.

Hack losses rise to $3.1M

AMLBot said hackers stole about $3.1 million in PUSD from 11 user wallets. The firm said the funds were taken from Polygon and quickly bridged to Ethereum.

The update raises the loss figure from earlier estimates near $2.94 million. Specter Analyst had first flagged the attack as a phishing campaign that drained funds from at least 11 wallets holding PUSD.

Polymarket said in a June 25 post that it found a third-party vendor had been compromised. The company said the vendor issue allowed attackers to inject a malicious script into the platform’s frontend for some users.

“We’ve contained it & removed the affected dependency.” It also said it was contacting affected users and “refunding them in full,” the platform said.

Frontend attack targeted user wallets

The attack appears to have targeted users through the website interface rather than the core protocol. That type of attack can trick users into approving harmful wallet activity while they believe they are using the normal platform.

PeckShield said the attacker bridged stolen funds from Polygon to Ethereum and swapped them into about 1,893 ETH. Specter also said the funds were consolidated into an Ethereum address after the phishing activity.

A frontend attack can be difficult for users to detect in real time. The site may look normal, but the code loaded in the browser can create unsafe wallet prompts.

The incident also puts focus on third-party dependencies. Even if a platform’s smart contracts remain unchanged, outside code used in a website can create risk for users who connect wallets.

Earlier incidents add pressure

The latest incident follows other Polymarket security issues. In March, blockchain investigator ZachXBT flagged a suspected breach after more than $520,000 was reportedly drained from two Polygon smart contracts.

Polymarket later said funds were safe in that case. In December, the platform also confirmed an incident on its Discord channel after users reported missing funds and suspicious login attempts.

A previous report said the latest attack was recorded by DefiLlama as the 89th crypto security breach of the second quarter. The same report said that count made the quarter the highest on record by number of reported incidents.

The growing incident count shows why platforms now face closer checks across smart contracts, wallets, login systems, frontend code and outside vendors.

Regulatory scrutiny widens

The hack also arrives as Polymarket faces new regulatory attention. A recent report said U.S. Senators Adam Schiff and John Curtis urged the CFTC to review allegations tied to deceptive advertising practices.

The senators asked whether Polymarket promoted markets through simulated trading websites, staged transactions and undisclosed paid influencer campaigns. They also questioned whether the CFTC has enough tools to oversee prediction markets and protect users.

Polymarket and Kalshi are also part of a wider legal fight over sports event contracts. Kentucky has accused prediction market firms of offering unlicensed sports betting, while the CFTC has argued that federally regulated event contracts fall under its authority.

As previously reported, the cases may help decide whether sports-linked prediction markets answer mainly to federal derivatives rules or state gambling laws.

Binance founder Changpeng “CZ” Zhao says the crypto market’s weak 2026 cannot be blamed on one event.

Summary

- CZ says crypto’s 2026 sell-off has no single cause behind Bitcoin’s sharp yearly decline.

- AI funding, global tension and the four-year cycle now sit at the center of debate.

- CZ remains long-term bullish, saying demand for financial technology should keep growing across crypto markets.

He pointed to capital moving into AI, global tension and the usual crypto market cycle as possible reasons for the downturn.

Bitcoin has fallen sharply from its October 2025 peak above $126,000 and now trades near $60,000. The wider market has also struggled as investors reduce risk and move capital into other high-growth sectors.

CZ says there is no single cause

In a CoinDesk interview, CZ said there is no simple answer for why crypto has fallen so much in the first half of 2026. He said geopolitical tension, the AI boom and the four-year crypto cycle may all be weighing on prices.

The comments come after Bitcoin opened 2026 near $89,000, briefly moved above $96,000, and then dropped toward $60,000. That fall has raised new questions about whether the current market is following an old cycle or entering a new structure.

CZ said his long-term view has not changed. He said, “Over the long run, the industry will develop,” pointing to rising demand for financial technology and more digital transactions over time.

His view lines up with earlier comments that blockchain could become part of daily life within five years. As previously reported, CZ has argued that countries that fail to adopt blockchain and AI may face economic disadvantages.

AI draws capital from crypto

CZ said “new industries like AI” are taking some “hot money” away from crypto. He framed that movement as a temporary capital rotation, not a long-term rejection of digital assets.

The AI boom has become one of the strongest competing themes in global markets. Investors have pushed money into AI infrastructure, chips, cloud computing and robotics while crypto prices have weakened.

This shift has also changed market attention. A recent report on crypto search interest found that public interest fell to a one-year low even though Bitcoin remained far above its 2022 bear market bottom.

That weaker attention matters because retail demand often helps drive crypto rallies. When AI stocks attract more attention, crypto may struggle to find the same level of fresh demand.

Four-year cycle debate grows

CZ also pointed to the four-year crypto cycle as one reason for the decline. Bitcoin has often moved through boom-and-bust cycles linked to halving periods, liquidity shifts and investor behavior.

The question now is whether that cycle still works in 2026. A recent Bitcoin price prediction report noted that Bitcoin trades near $60,000, more than 50% below its 2025 peak, while traders debate whether the old cycle remains useful.

Another cycle analysis said Bitcoin’s drawdown from the October peak looked severe but still fit parts of past market behavior. The report also noted that analysts remain split over whether the downturn marks a normal cycle reset or the end of the bull market.

That debate remains open because institutional flows have changed Bitcoin’s market structure. Spot ETFs, corporate treasuries and derivatives now play a larger role than in earlier cycles.

Policy and prediction markets stay in focus

CZ also said U.S. crypto policy remains important, though he described bills such as the CLARITY Act as tactical steps rather than the only driver of long-term growth. A related report said the CLARITY Act could help bring more crypto activity back to the U.S. by giving firms clearer rules.

He also spoke about prediction markets, saying they can help price events and provide liquidity. CZ said prediction markets could be “good for the population,” while also noting that speculation exists in many financial products.

As previously reported, CZ has supported activity in the BNB Chain prediction-market sector. He praised Predict.fun’s acquisition of Probable as a move that could combine liquidity and talent.

For now, CZ’s message is cautious but not bearish on the long term. He sees the 2026 slump as the result of several pressures hitting the market at once, while still expecting the crypto industry to keep growing as financial technology demand expands.

Ben Stokes retirement: England captain’s former teammate pays tribute to England ‘talisman’ after shock retirement announcement

Why Wear Anything Other Than a Sun Hoodie This Summer? Our Picks for the Best

Thirty-three people rescued, thousands still missing after Venezuela quakes

-

Sports5 days ago

Sports5 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Tech6 days ago

Tech6 days agoMicrosoft accidentally kills epic Outlook email threads

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics2 days ago

Politics2 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics3 days ago

Politics3 days agoPotential 2028er World Cup attendee leaderboard

-

Business2 days ago

Business2 days agoAsia stock markets slide as tech shares slump

-

Tech3 days ago

Tech3 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World4 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World3 days ago

Crypto World3 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World4 days ago

Crypto World4 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Business5 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World1 day ago

Crypto World1 day agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports2 days ago

Sports2 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Crypto World2 days ago

Crypto World2 days agoRTX holders must register wallets before token distribution begins

-

Crypto World2 days ago

Crypto World2 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Sports3 days ago

Sports3 days agoIndia vs Bangladesh LIVE Score, Women’s T20 World Cup: Bangladesh Opt To Bat; India Enter ‘Do-Or-Die’ Stage As Semi-Final Race Heats Up

-

Crypto World23 hours ago

Crypto World23 hours agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Crypto World2 days ago

The DATA Foundation Launches to Tackle AI’s Multi-Billion Dollar Training Data Bottleneck

-

Crypto World3 days ago

Crypto World3 days agoStrategy (MSTR) has a 10-month cash runway for dividends, but retail investors are losing faith

-

Crypto World3 days ago

Crypto World3 days agoAAVE price tests 9-month trendline after 17% rebound as breakout hopes build

You must be logged in to post a comment Login