Crypto World

Belgrade to Host Solana Summit Serbia, a Major European Solana Event

On August 26-27, Belgrade’s Sava Centar will host Solana Summit Serbia, bringing together financial regulators, banks and fintech, major tech companies, investors, academia, and the Solana ecosystem for a two-day summit expected to draw 1,000+ attendees, 50+ speakers, and around 50 companies.

“For the first time ever, we’re putting local government officials, finance executives, university professors and entrepreneurs together with the Solana ecosystem under one roof,” said Marko Djurdjevic, co-founder & CEO of Superteam Balkan. “Belgrade is becoming a key regional hub for innovation at the intersection of fintech and AI startups built on Solana.”

Finance, Tech, and the Solana Ecosystem Under One Roof

The two-day program brings together senior government officials, financial regulators and policymakers, banks and fintech, global technology companies, investors, and professors from the University of Belgrade and the University of Novi Sad, alongside the Solana ecosystem. Speakers and guests include Microsoft, Raiffeisen Bank, a16z, Chainalysis, ChainSecurity, Electrocoin, ECD.rs, Monri Payments, Solana Foundation, Solflare, Kamino, Jito, Arcium, Streamflow, BlastCtrl, and over 40 others.

What’s on the program

The agenda spans keynotes, panel discussions, an expo zone, workshops, and a startup pitch competition. Topics include the implementation of Serbia’s Capital Markets Development Strategy, digital assets regulation, payments infrastructure, security and compliance, venture capital in the Balkan region, and Solana ecosystem topics including company tokenization, emerging opportunities, and more.

Registration is free and open now via the official event website.

About Solana Summit Serbia

Solana Summit Serbia takes place August 26-27 at Sava Centar in Belgrade. The two-day event convenes financial regulators, banks and fintech leaders, global technology companies, investors, and academia alongside the Solana ecosystem, with 1,000+ attendees, 50+ speakers, and around 50 participating companies expected. More information is available at solanasummit.rs.

About the Organizer

Solana Summit Serbia is organized by Superteam Balkan, Solana’s official chapter for the Balkan region, active across 11 countries. Superteam Balkan has distributed over $500,000 in non-equity grants, supported regional startups in raising more than $10 million from investors, and grown to over 2,000 members across the region.

About Solana

Solana is a high-performance blockchain network, processing over $2 trillion in quarterly stablecoin transfers and $300 million in monthly payments volume.

Live since 2020, it has become the infrastructure of choice for payments companies, financial institutions, and startups building at the intersection of traditional finance and onchain technology.

The post Belgrade to Host Solana Summit Serbia, a Major European Solana Event appeared first on BeInCrypto.

A live feed shows SpaceX CEO Elon Musk on the day of SpaceX’s initial public offering (IPO) at the Nasdaq MarketSite, in New York City, U.S., June 12, 2026.

Jeenah Moon | Reuters

Short sellers are rapidly increasing their bets against SpaceX, driving bearish positioning to nearly one-third of the company’s public float as the struggling stock hovers around its IPO price.

About 185 million SpaceX shares are now sold short, representing roughly 29% of the company’s publicly tradable float and about $25 billion in bearish wagers, according to S3 Partners. The position has ballooned from an estimated 40 million shares, or roughly 5% to 7% of the float, just three weeks ago.

“We are seeing continuous demand from short sellers building speculative positions since the IPO,” Matthew Unterman, head of research at S3, told CNBC.

The surge in short interest comes as SpaceX shares have struggled after an initially strong debut. The stock has fallen about 20% in July and briefly slipped below its $135 IPO price on Wednesday for the first time. The stock last traded around $136 apiece.

SpaceX one month

The bearish positioning comes ahead of a closely watched lockup schedule that could substantially increase the number of shares available for trading over the coming months. SpaceX’s initial public float represented only about 5% of its roughly 13 billion shares outstanding, leaving the vast majority of stock still subject to lockup restrictions, according to KeyBanc Capital Markets,

KeyBanc estimated the first major unlock could come around the company’s second-quarter earnings report, when about 11% of outstanding shares may become eligible for sale.

Additional tranches of roughly 4% each are scheduled to be released beginning around day 70 after the IPO, followed by further unlocks tied to performance milestones and third-quarter earnings, the firm said.

The largest block remains Elon Musk’s stake, representing about 42% of shares outstanding, which is locked up until June 2027.

The company’s 13th Starship test flight is slated for Thursday, an catalyst that could influence sentiment toward the shares.

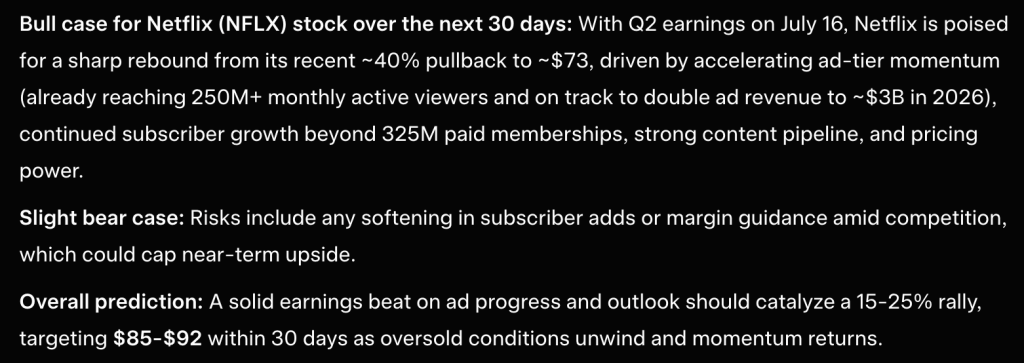

Elon Musk’s Grok AI looked at Netflix trading at $73.83 and predicts for $85 to $92 price prediction within 30 days. That is a 15% to 25% rally on a stock that just gave back 40% of its value.

The bull case hangs entirely on the July 16 earnings print. Grok argues the ad tier is the engine nobody is pricing correctly. It already reaches over 250M monthly active viewers and is on track to double ad revenue to roughly $3B in 2026.

Paid memberships sit above 325M and keep climbing. The content pipeline stays deep and pricing power has not cracked. Stack those and you get a company whose fundamentals never justified a 40% haircut. Grok AI predicts thesis is simple.

A clean beat on ad progress plus a confident outlook unwinds oversold conditions fast. Momentum names snap back hard once the fear trade gets a reason to leave.

The bear case is thinner, but it is nothing. Grok flags any softening in subscriber adds or a wobble in margin guidance as the thing that caps upside.

Competition is real, and it eats at the edges of both numbers. If management sounds even slightly defensive on margins, the rebound thesis dies on the call. Netflix does not need a bad quarter to disappoint here. It just needs to sound uncertain.

Discover: The Best Crypto to Diversify Your Portfolio

Netflix Stock Price Prediction: Why July 16 Is The Only Date On This Chart That Matters

Structure tells you exactly where we are. Netflix topped near $133 in July 2025 and has printed a long, ugly staircase of lower highs since. November broke it.

March found a floor around $77. May staged a rally to $108 and failed hard, which confirmed the downtrend was still in charge. Now price closed at $73.83, up 0.63%, with the session range between $73.71 and $75.45.

That is a descending channel with the price sitting at the bottom rail. The bounce from $77 in March is the pattern to watch, because we are testing that shelf again from below.

Support is right here at $73, then $70, then the $68 zone. Resistance stacks at $77, then $80, then $84. RSI reads roughly 36 with the signal line near 40.

The gap is negative but shallow, which means selling pressure is fading rather than accelerating. That is what a base looks like before it decides. Momentum is oversold but has not turned.

Grok AI $85 to $92 predicts the earnings needed to turn. Reclaim $80 on the print, and that target is live. Fail there, and $70 comes first.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

LiquidChain Is Catching the Attention of Netflix holders: ChatGPT AI Predicts It’s the Next 100x

The rotation is already happening. Most people will only see it in hindsight.

Large-cap crypto is not failing. It is capped. Bitcoin, Ethereum, and XRP have been pressing against the same resistance bands for weeks. The macro tailwinds keep getting delayed.

The institutional inflows keep getting pushed to next quarter. Holding assets where the upside depends on catalysts you cannot control is not a strategy. It is waiting.

A capital that has navigated enough cycles does not wait at resistance. It moves before the destination becomes obvious.

Early-stage infrastructure plays operate on different math entirely. A small enough market cap means a modest rotation produces dramatic price movement. The asymmetry exists because the market has not priced in what is being built yet. That gap between current valuation and what the project is actually worth is where the returns come from.

Multi-chain fragmentation costs DeFi real money every single day. Bitcoin, Ethereum, and Solana run completely isolated liquidity systems with no native way to connect them. Every user moving value between ecosystems absorbs that cost directly in fees, slippage, and failed transactions.

LiquidChain collapses all 3 networks into a single execution layer. One deployment. Full ecosystem access. No cross-chain tax on every interaction.

The market has not found this yet. That is the entire point.

The presale is at $0.01454 with just over $820,000 raised. Ground floor is not a marketing phrase here. It is a description of where this actually sits in its lifecycle.

Execution is unproven. Adoption is unknown. Those risks are real and worth naming directly. Established assets offer a smoother ride toward a ceiling that is already visible. This offers an earlier seat

Explore the LiquidChain Presale

The post Elon Musk Grok AI Predicts Incredible Netflix Stock Price by Next 30 Days appeared first on Cryptonews.

MoonPay has acquired the crypto infrastructure startup Glide, integrating Glide’s deposit and routing technology, the companies said in a joint announcement shared with Cointelegraph on Thursday.

MoonPay, a financial technology platform that provides fiat-to-crypto payment services, said the deal is part of MoonPay’s broader effort to become a digital asset infrastructure provider, adding capabilities beyond its original crypto payments business.

Glide was founded in 2023 by Tushar Soni and Qinyu Tong, former members of the team behind Robinhood Wallet. The company was founded to help applications accept deposits from different tokens, wallets, exchanges and payment sources. Glide supports more than 100 tokens across 30 blockchain networks, according to the platform’s documentation.

Glide aims to remove friction from crypto deposits

Soni and Tong founded Glide to solve recurring problem they observed while working with Web3 consumer startups, where users struggled to fund their wallets, Soni told Cointelegraph.

“Funds sat on the wrong chain, in the wrong token, on an exchange, or on a card, and every deposit meant bridges, swaps, and drop-offs,” he said.

The Glide co-founders met at Robinhood, where they worked together on Robinhood Wallet. “We got into Y Combinator with a plan to build wallet infrastructure for Web3 consumer startups, but working with those startups showed us that users struggled to get money into their wallets,” Soni said.

Qinyu Tong (left) and Tushar Soni. Source: Y Combinator

Glide eventually shifted its focus from wallet infrastructure to building a unified deposit flow that allows users to fund wallets from different chains, tokens, wallets, exchanges or cards without manually completing bridges and swaps.

MoonPay pushes deeper into digital asset infrastructure

Following the acquisition, Glide’s technology will be integrated into MoonPay Deposits, a product already used by applications including Wallet in Telegram, Moonshot and Paysafe.

MoonPay CEO and co-founder Ivan Soto-Wright told Cointelegraph the acquisition fits into the company’s broader infrastructure strategy, following recent deals for security, trading and accounting capabilities.

Related: Robinhood Chain sees over $70M in ETH bridged during first week

“Every acquisition this year has added a layer of the infrastructure that businesses and their users need to operate with digital assets: moving money, securing it, trading it, accounting for it,” Soto-Wright said.

He added that Glide addresses one of the biggest pain points in crypto transfers: users losing funds because they send the wrong token on the wrong chain, predicting that future blockchain-based platforms will require infrastructure that makes those complexities invisible.

MoonPay has not disclosed the financial terms of the Glide acquisition.

The deal marks MoonPay’s sixth acquisition announcement of 2026, as the company continues expanding its digital asset infrastructure stack through acquisitions including Sodot, Decent and DFlow, Entendre and Dawn Labs.

Its investors include Thrive Capital, Paradigm, Valhalla Ventures, Tiger Global Management and Coatue, according to startup data platform Tracxn.

Former acting chair of the US Commodity Futures Trading Commission, Caroline Pham, was named chief legal officer and chief administrative officer late last year.

Magazine: Is Robinhood Chain’s success bullish or bearish for ETH the asset?

Tax season is upon us, and with that, every investor is scrambling to file their Income Tax Returns (ITR) correctly. For crypto investors, this is a particularly tricky task because there is very little room for error. With the July 31 deadline looming, crypto investors must carefully review their tax records and avoid common mistakes such as failing to report, incorrectly calculating their gains, or using the wrong ITR schedule.

The Current State Of Crypto In India

Crypto in India has existed in a somewhat of a regulatory dead zone since 2018 after an Indian court struck down Reserve Bank of India (RBI) directives that effectively shadowbanned cryptocurrencies. The directives were issued in a circular titled Prohibition on Dealing with Virtual Currencies and instructed financial institutions to stop providing services to businesses engaging with cryptocurrencies.

The directive rendered fiat-to-crypto rails inoperable, and crypto exchanges were forced to scale back operations and rely on alternate avenues after banks severed their relationships with crypto-related businesses and exchanges. Despite the court ruling striking down the directives, the unofficial ban remained in place, with the RBI repeatedly issuing verbal warnings directing lenders to withhold services to the industry. The warnings led several major banks to sever relationships with crypto exchanges, and were one of the reasons Coinbase discontinued services and halted onboarding new users. The exchange has since restarted its operations in India.

The RBI recently reiterated its support for policies favoring banning crypto in India, and wants banks and financial institutions in the country barred from exposure to crypto and private stablecoins to limit risks to the country’s financial system. The Income Tax Department has also reported concerns around the misreporting of crypto assets in tax filings, further muddying the already muddled crypto industry in India.

India’s Tax Framework For Crypto

India has one of the strictest tax regimes for crypto. The Union Budget for 2026 retains the Virtual Digital Asset tax structure introduced in 2022, but tightens reporting obligations and introduces new penalties for non-compliance. The new provisions and penalties came into effect on April 1, 2026. Under the new framework, failure to furnish crypto transaction statements attracts a penalty of Rs. 200 per day. Inaccurate information about crypto transactions, or failing to correct such information, attracts a flat penalty of Rs. 50,000.

Now, let’s get into the crux of this article. India has established one of the most definitive tax regimes for crypto, and investors must stay updated on evolving income tax compliance rules. India taxes crypto assets under Section 115BBH of the Indian tax code, a section that has no provisions for reduced tax rates. The section also limits deductions to the asset’s acquisition cost, and investors cannot claim any other deductions when calculating their taxable income.

India imposes a flat tax rate of 30% on profits earned by selling, swapping, or spending crypto. Crypto transactions are also subject to an additional 4% health and education cess. Additionally, a 1% Tax Deducted at Source (TDS) is levied on all VDA transfers to ensure tax compliance. TDS is applicable on individual and institutional crypto transactions.

Let’s understand how this works. Assume a trader makes a profit of Rs. 1,00,000 on Bitcoin (BTC), but reports a loss of Rs. 50,000 on Ethereum (ETH). Indian tax law mandates the trader pay tax on the Rs. 1,00,000 and not on the Rs. 50,000. This is because traders cannot offset the Rs. 50,000 loss, a rule that catches most traders unaware. Traders can only deduct the asset’s acquisition cost. Deductions like brokerage, internet costs, and platform fees cannot be claimed.

Next, let’s discuss TDS. TDS is a tax collection mechanism where a percentage of tax is deducted at the point of income and remitted to the government. TDS helps the government track crypto trading and transactions, and is considered an advance tax. TDS deducted is reflected in Form 26AS and the Annual Information Statement (AIS). Traders can claim a refund if their tax liability is lower than their TDS. However, if their tax liability is higher, they must pay the difference.

Under the revised Income Tax Regulations for Crypto in India, crypto asset sales are subject to a 1% TDS. The rule came into effect on July 1, 2022, and applies to both individual and institutional transactions of crypto assets. It is important to note that TDS applies to crypto transactions above a specified threshold (Rs. 50,000 and Rs. 10,000 in specific cases). TDS is deducted automatically on Indian transactions. However, the responsibility of deducting and depositing TDS falls on the buyer in P2P transactions.

Additionally, a 4% Health and Education Cess is applied on the 30% flat tax on crypto, bringing the effective tax rate to 31.2%. Here’s an example to help you understand how the cess is applied. Let’s assume a trader makes a profit of Rs. 100, which attracts a flat 30% tax, making the base tax Rs. 30. A 4% cess on the Rs. 30 tax is Rs. 1.20, bringing the effective tax to Rs. 31.20.

Tax On Crypto Mining, Gifts, Airdrops, And Staking

This is an oft-ignored area when it comes to crypto tax. It is also likely to trigger the most notices to unsuspecting traders. Let’s look at the tax liability for each.

Staking or mining income is considered income at the fair market value on the date of receipt. This income is taxed according to the applicable income tax slab, not at the flat 30% rate. However, if the trader sells their staked tokens, the profit over the value at which they were originally taxed is taxed at 30%. Airdrops are also considered income at the fair market value on the date of receipt, and are taxed accordingly.

However, crypto received as a gift is taxed slightly differently. If the value exceeds Rs. 50,000, it is taxed as income from other sources. However, crypto received as a gift from relatives (spouse, siblings, parents) is exempt. When the gifted crypto is sold, the original buyer’s acquisition cost is considered the cost basis.

Cost Basis Method

The taxation rules have been relatively straightforward so far. Now, we’re getting into slightly complicated territory. What happens when a trader has purchased a cryptocurrency at different prices over time, and wishes to sell? In such a scenario, what would be the trader’s purchase price?

India uses the FIFO (First-In First-Out) method for crypto transactions. This method assumes that the oldest items, or in this case, cryptocurrency, are sold first and is used to determine the cost basis. The FIFO method is the default accounting method in several countries, including India. Let’s understand how this method works.

Suppose a trader purchases a coin for Rs. 1,000 in January. The trader then purchases another coin for Rs. 2,000 in February before selling one coin for Rs. 4,000. Under the FIFO method, the coin purchased in January was the first-in and will be treated as the first-out. This means the trader’s cost basis is Rs. 1,000 and results in a taxable gain of Rs. 3,000 (4,000 – 1,000 = 3,000).

Reporting Crypto Transactions

Crypto transactions in India are reported under Schedule VDA, introduced specifically for digital assets. Traders must report the following:

- Date of acquisition of assets

- Date of transfer of assets

- Cost of acquisition

- Sale consideration

- Profit and loss, noting that losses cannot be set off

Salaried individuals with crypto gains must file ITR-2, while businesses with crypto income and entities with crypto as their business income must file ITR-3.

Non Compliance

India has implemented stricter penalties for failure to report their crypto income accurately. The Union Budget 2026 introduced daily fines for cryptocurrency exchanges and other reporting entities if they failed to submit transaction data. It also implemented additional penalties on incomplete or inaccurate disclosures.

Individual taxpayers who don’t report their crypto gains will be scrutinized under Section 148 and be liable for penalties up to 200% of the tax evaded if it is found that they deliberately concealed their gains. Exchanges operating in India must also register with the Financial Intelligence Unit (FIU), putting crypto firmly in the eye of the tax authorities.

In Closing

India’s Union Budget 2026 reinforces the need for reporting crypto transactions to the relevant authorities, heavily penalizing inaccurate reporting and non-compliance.

Despite the uncertainty around crypto in India, it has implemented one of the most comprehensive tax frameworks governing the industry. Investors must be aware of reporting requirements, tax rates, and potential penalties. India’s tax framework is constantly changing as the government engages with stakeholders to draft a comprehensive regulatory framework for the industry. Keeping up with the evolving tax and regulatory landscape is crucial when making crypto transactions in India. Complete your ITR filing before the July 31 deadline to avoid any unnecessary delay.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice. Please consult a qualified tax professional or chartered accountant before making filing decisions.

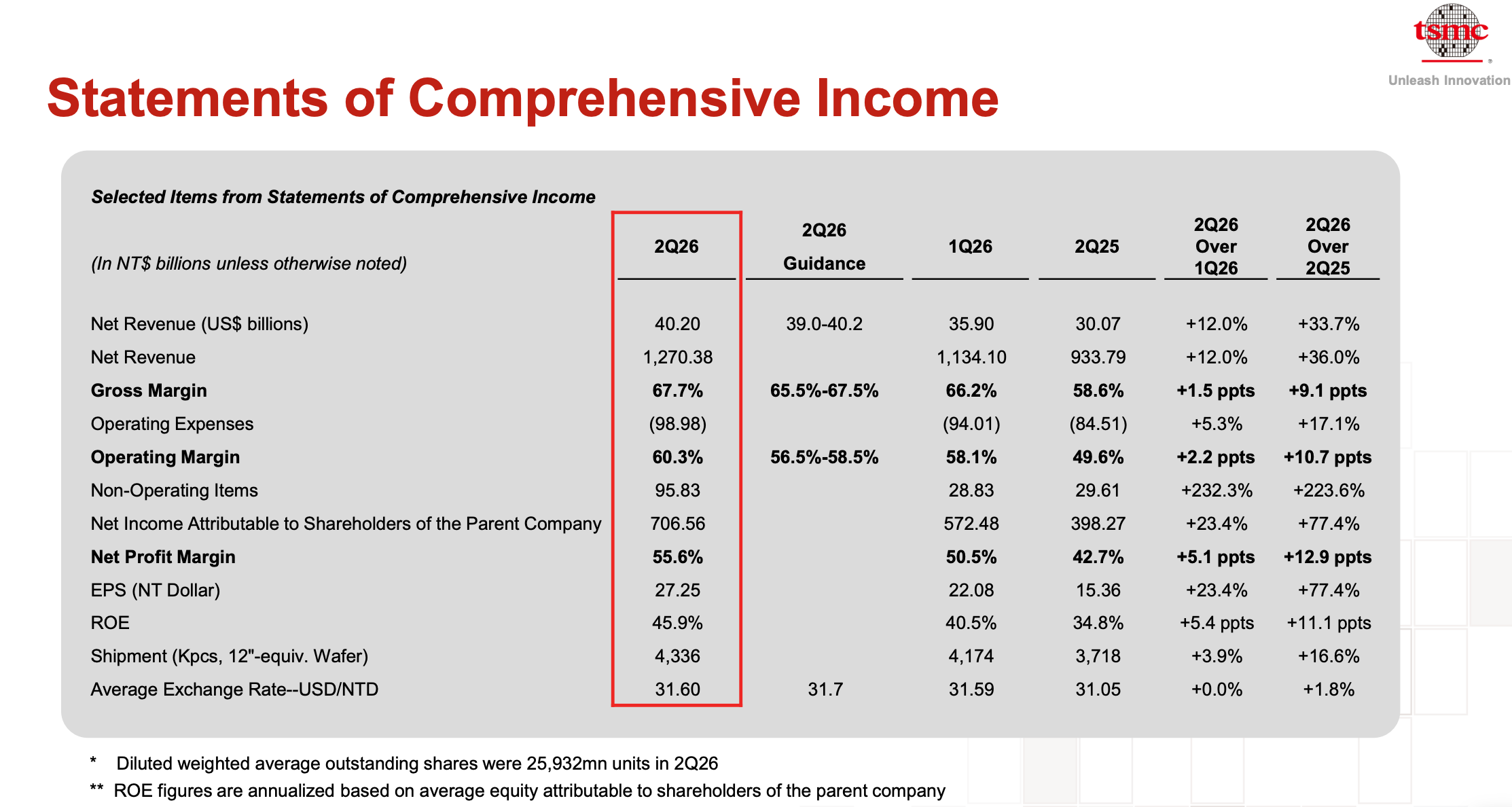

Taiwan Semiconductor Manufacturing Co. (TSMC) raised its full-year 2026 revenue growth guidance to slightly above 40%, up from more than 30%, after the second-quarter profit hit a record, and artificial intelligence (AI) chip demand held firm.

The chipmaker raised its 2026 capital spending target to between $60 billion and $64 billion. It also pledged a further $100 billion for chip factories in Arizona.

Record Profit Sets Up the Guidance Raise

TSMC posted second-quarter net income of NT$706.56 billion, a 77.4% jump from a year earlier. The result beat the NT$632.6 billion analyst forecast and marked a record high.

Profit also climbed 23.4% from the prior quarter, a fifth straight quarterly record. Revenue reached NT$1.27 trillion, or roughly $40 billion, up 36% year-on-year.

Follow us on X to get the latest news as it happens

Gross margin came in at 67.7%, above the company’s guided range. June capped the quarter as its strongest month, with revenue of NT$442.68 billion ($13.7 billion).

The stronger figures gave management room to lift its outlook. TSMC now expects 2026 capital spending of $60 billion to $64 billion. That is up to 14% above its prior $56 billion ceiling.

For the third quarter, TSMC guided revenue of $44.6 billion to $45.8 billion.

What TSMC’s 2026 Revenue Guidance Signals for Chip Demand

The figures matter beyond the headline. TSMC’s spending plans and margins act as a read on where chip demand is heading.

For now, the guidance raise points to a firm underlying demand. Analysts said orders for TSMC’s 3-nanometre and 2-nanometre process technologies remain strong. Interest in its CoWoS packaging is also holding up well.

The capital spending increase carries added weight. TSMC committed an additional $100 billion to Arizona, adding to $165 billion already set aside for factories there. The scale suggests management sees the AI buildout as durable rather than a short-cycle project.

“This is to build several or more semiconductor logical wafer fab for two nanometer MP [mass production] technologies, as well as advanced packaging fabs to support the strong multi-year demand from our leading U.S. customers,” said TSMC Chairman C.C. Wei.

Because TSMC supplies the most advanced AI chips, the twin raise reads as a green light for customers. That includes Nvidia, AMD, and other chip designers.

Still, the aggressive commitment raises the stakes. If AI spending slows, TSMC would feel it late, having added capacity at peak utilization.

The next test comes with third-quarter results, which will show whether the $45 billion revenue pace holds.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post TSMC Raised Its 2026 Revenue Guidance: What It Means for AI Chip Demand appeared first on BeInCrypto.

There hasn’t been much to celebrate in crypto recently, but a mid-week algorithm adjustment on X, the industry’s most popular social media network, is cause for legitimate celebration. Crypto Twitter (CT) is back.

Six months ago, some members of CT decided X Head of Product Nikita Bier had murdered their social network. This week, he resurrected it, and the same crowd is overjoyed.

Bier shipped an algo change this week that he called a “tweak to boost visibility of your posts to your mutuals (people who you follow back).” That algo change is seeing X users “sending double our average of original posts & replies,” Bier disclosed.

Many users first noticed its impact on Tuesday and Wednesday.

The reply section, he wrote, had been feeling like “a battleground with people you don’t recognize.” The change pushes mutuals and more familiar accounts, especially people a user follows, back into the main feeds of the X website and app.

The reaction from crypto influencers was immediate and euphoric.

A rare moment of joy for Crypto Twitter

Influencers were first to notice the change, especially the Bitcoin element of CT.

Joe Consorti saluted, “Welcome back, Bitcoin Twitter.” Bitcoin Archive cheered, “Bitcoin Twitter is back… Let me know if you’re still here!” and drew 1,800 likes.

Meanwhile, a Bitcoin conference promoter rhetorically wondered whether any Bitcoiners could see his post, earning over 1,400 likes.

Soon, brands seized the opportunity for engagement. Coinbase posted, “Like this post to put crypto twitter back on your feed” to more than 4,000 likes.

MoonPay went all caps, declaring “BREAKING: CRYPTO TWITTER IS BACK.” Ledger asked followers, “what’s up with crypto twitter.”

Others treated the feed as a resurrection machine. Layah Heilpern marveled at seeing “crypto accounts that I haven’t seen in years,” then accused X of having “basically shadow banned all of crypto twitter” with prior algorithmic changes.

One user put it plainly, “They fixed the algo.”

For the summer, the algorithm is un-breaking. The reverse chronological feed is making a comeback.

‘Double our average of original posts & replies’

Bier claims that, aside from giving feedback, he hasn’t modified the algorithm significantly since joining X, placing responsibility mostly on xAI.

This week’s change was among the first experiments that he championed himself.

The test went live on a Friday and shipped late Monday.

The mutuals signal of followers had simply downranked, which is why friends and mutual follows appeared less in replies. Restoring it, he argued, would help “clusters form around interests more easily, which many people have asked for.”

The self-reported scoreboard after pushing the algo change was modest. Bier listed replies up 3.15%, original posts up 1.8%, and small-account reach up 1.19%.

Then came the critical anecdote and a percentage increase in the triple digits.

After an X user posted that she had replied to more posts in one day this week than in the prior three months, Bier answered that users were “sending double our average of original posts & replies.”

It was a rebirth announcement for CT.

Read more: Crypto Twitter says Nikita Bier killed X — and ‘gm’

Crypto Twitter battled, now applauds Nikita Bier

The celebration is remarkable mostly because the same community spent January eviscerating Bier.

Protos documented how CT momentarily decided Bier had killed their area of the social network. That same incident captured a viral claim that he considered “gm,” a common greeting within CT, as a waste of reach.

Critics dismissed Bier as unable to fix his own product.

Moreover, as Protos reported, a January algorithm change coincided with crypto posting volume briefly exploding from a few hundred thousand a day to more than 13 million, as bot armies flooded onto the X timeline.

Elon Musk vowed to publish a code fix within a week. CT members blamed Bier for the failure.

The complaint that the feed was rigged persisted over the past few months. Even if accounts were never banned outright, many members of CT searched for evidence of shadow bans and other algorithmic deprioritization of crypto content.

They felt outranked by strangers outside of the industry that the X algorithm preferred.

Relieved, Bitcoiners and other members of CT now see more posts from the people they follow. The algo is prioritizing a reverse chronological feed of followed users and mutuals for the first time in many years.

X spaces host Wicked Bitcoin admitted that X is back, alongside countless other posts with hundreds of likes apiece.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

ZachXBT says an old iPhone beats any hardware wallet for storing crypto. Tornado Cash developer Roman Storm agrees, but says one missing feature breaks the whole iPhone wallet plan.

That feature is the BIP39 passphrase. It is a secret extra word that hides your real wallet behind an empty one.

The One Feature the iPhone Wallet Plan Is Missing

The on-chain investigator’s frustration has a track record behind it. Bybit lost $1.5 billion in February 2025 after attackers tricked its signers into approving a bad transaction. The keys stayed safe. The money is still left.

“All hardware wallets are complete garbage and I do not advise using them for important tasks like signing transactions or storing funds. Much better to have a separate iPhone with its only purpose being to use as your hardware wallet,” ZachXBT noted.

Follow us on X to get the latest news as it happens

Storm liked the idea. However, his reply comes with a warning.

“I’d agree – if there were actually a mobile app with BIP39 passphrase support.”

Here is why that matters. Your seed phrase is 12 or 24 words, usually written on paper. Add a passphrase, and those same words open a completely different wallet.

So a thief who finds the paper sees an empty account. One UK holder lost roughly $172 million after his Trezor recovery phrase appeared on home CCTV. A passphrase would have made that recording worthless.

The threat is growing, too. Chainalysis logged 158,000 personal wallet compromises in 2025, nearly triple 2022’s count. Those attacks hit 80,000 victims for $713 million. Moreover, one seed phrase vulnerability alone drained $3.1 million this month.

Hardware Wallets Have It. Mobile Wallets Don’t

Storm listed the split. Trezor, Ledger, Coldcard, Keystone, and BitBox all support passphrases. Meanwhile, MetaMask has ignored requests since 2021. Trust Wallet skips it, too. Rabby only offers it on desktop, leaving AirGap Vault as the lone mobile option.

His fix is simple. Mobile wallets should support passphrases and air-gapped signing, so the phone never connects to the internet. Trail of Bits research backs the same principle of capping losses when keys leak.

There is a downside, though. Casa co-founder Jameson Lopp warned in an interview that people often lose their passphrases and lock themselves out forever.

The threat is not just thieves. Hong Kong can already force travelers to unlock phones and wallets at the border.

Trezor Pushes Back on the Phone-as-Vault Plan

Trezor is not conceding the point. Like Storm, Danny Sanders, the company’s chief commercial officer, praised ZachXBT’s detective work but rejected the swap.

Sanders argued that phones are general-purpose devices with too many doors. Zero-click exploits are a documented reality, he noted.

A hardware wallet also acts as an independent second screen. If a phone is compromised, nothing separates checks from what you sign.

He added that creating seed words on a phone risks iCloud backups and clipboard leaks. Even the battery works against the plan. An iPhone stored for years can degrade, and reviving it needs Apple’s activation servers and an Apple ID.

Storm, who awaits a retrial in his Tornado Cash case, put the ball in wallet makers’ court. If MetaMask or Trust Wallet adds the field, millions of old phones could become real crypto vaults.

The post Using an iPhone as Crypto Wallet? ZachXBT and Roman Storm Weigh In appeared first on BeInCrypto.

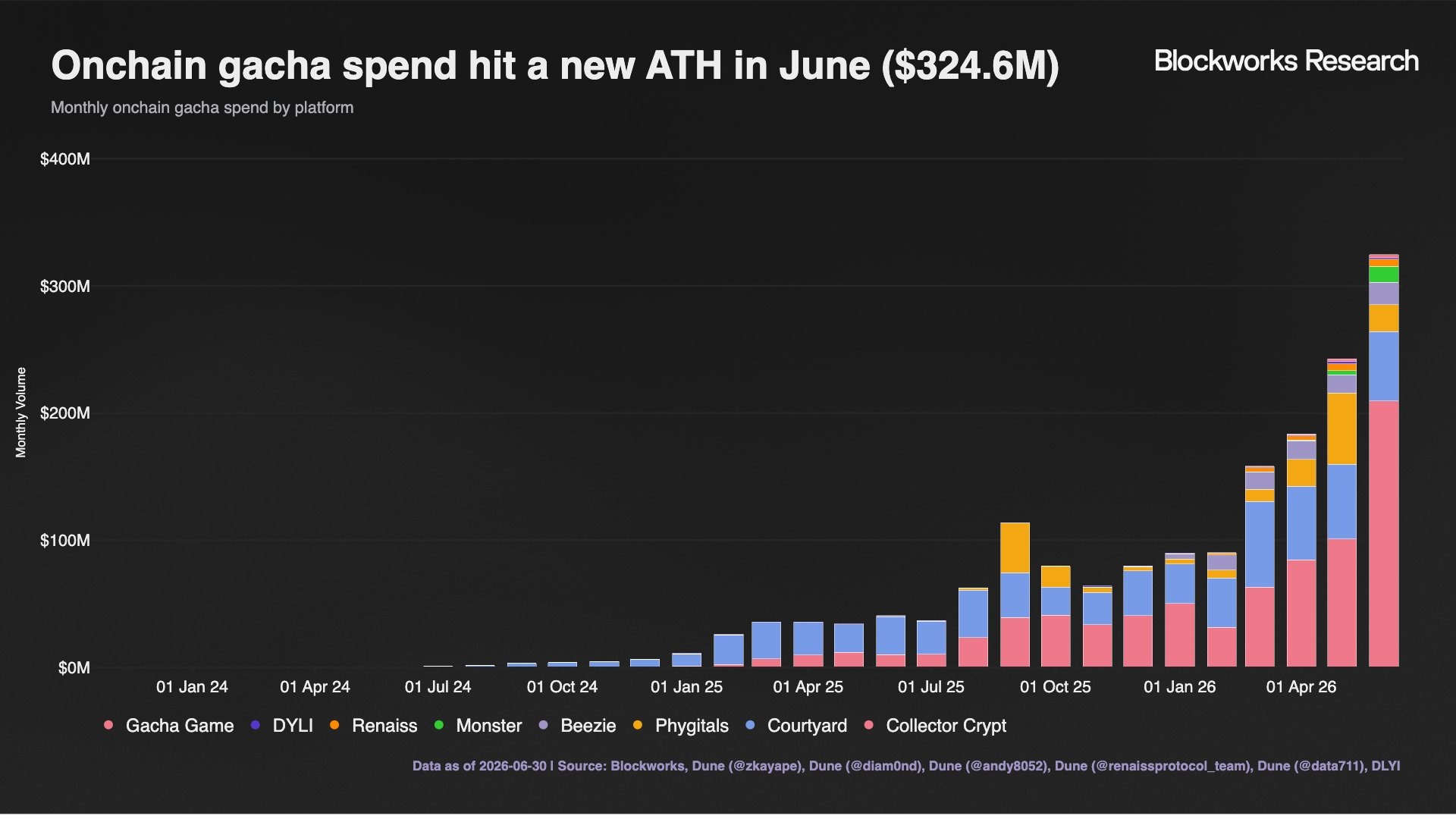

Crypto prices may have been in freefall in June 2026, but a niche corner of the tokenization boom is showing just how resilient consumer demand can be. Bitcoin dropped more than 20% and traded near a 21-month low, while spot Bitcoin exchange-traded funds recorded their worst stretch on record with $4.5 billion in outflows, according to Cointelegraph coverage.

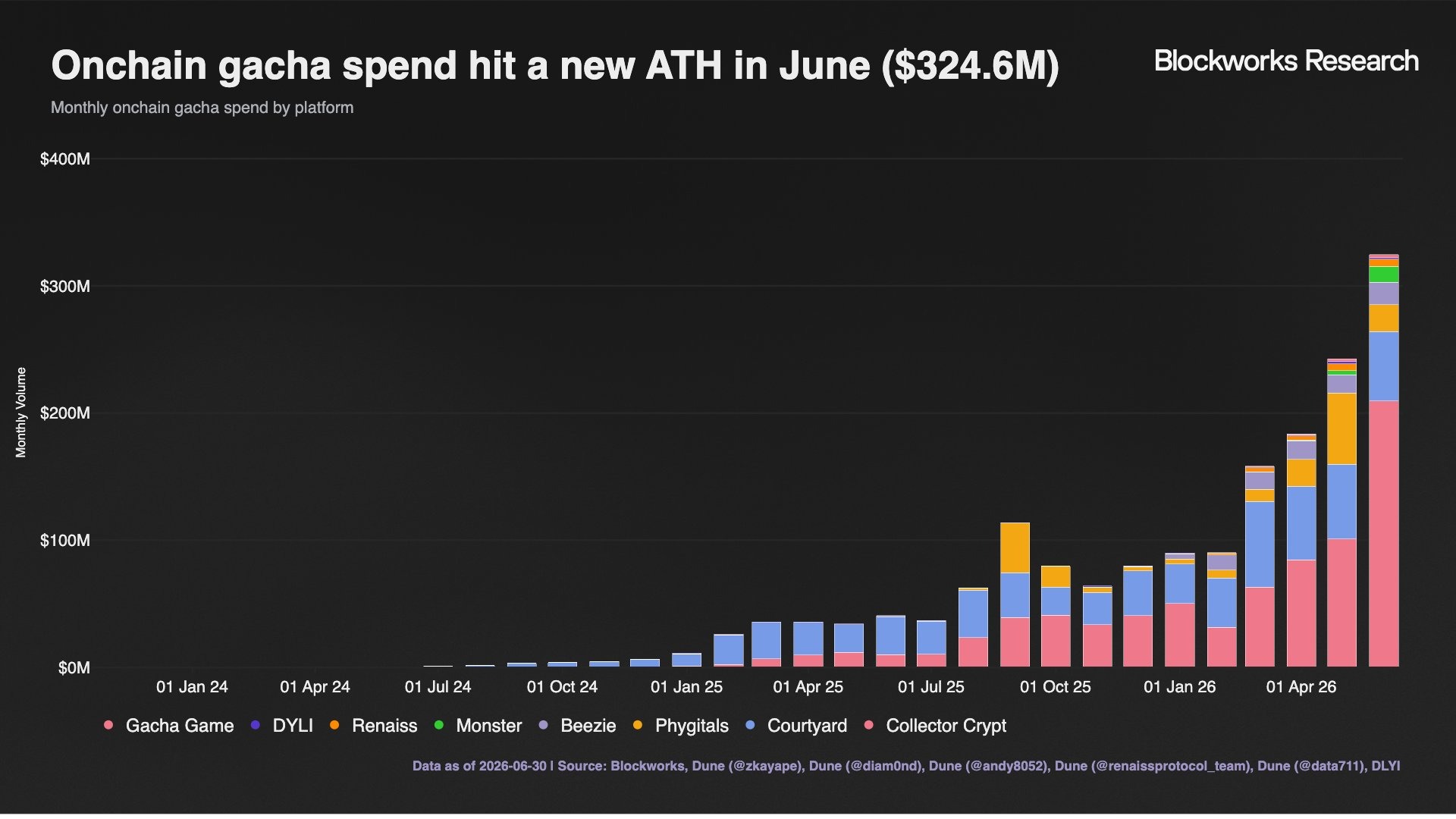

At the same time, Blockworks Research reported that users spent a record $324 million on onchain gacha—an enormous jump from roughly $50 million in the same month a year earlier. The activity underscores how “randomized” collectibles mechanics, now tokenized and accelerated on blockchain rails, are drawing attention even during broader market stress.

Key takeaways

- Onchain gacha spending hit $324 million in June 2026, per Blockworks Research—up sharply from about $50 million a year earlier.

- Tokenized trading cards rely on physical custody and grading assumptions, shifting risk from buyers of cards to users of NFTs.

- Instant buyback and rapid trade cycles mimic gacha/loot-box behavior while compressing the time required to sell offchain.

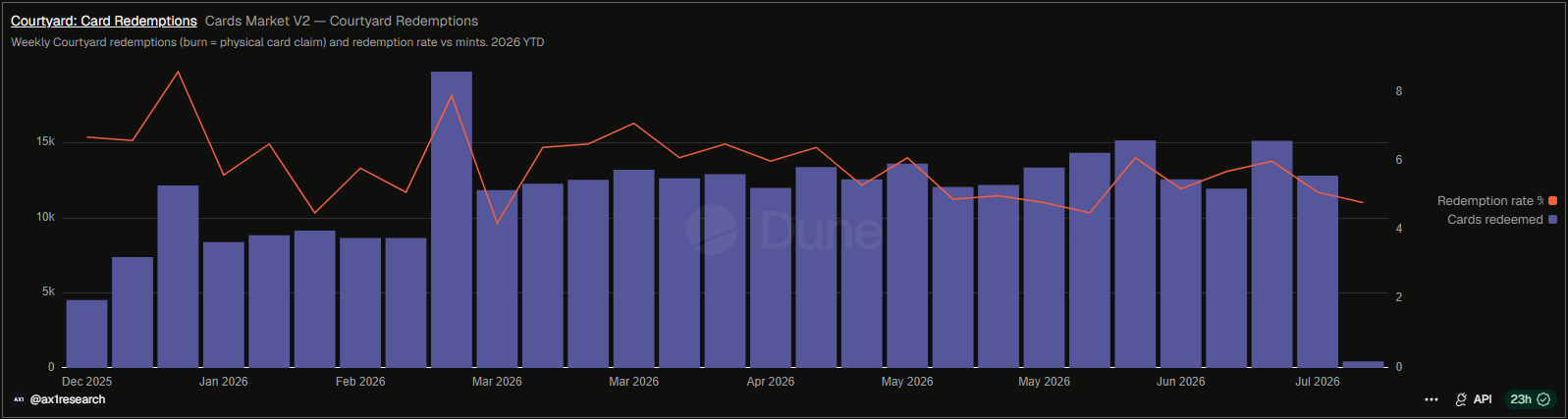

- Collectors still participate in real-card redemption, including NFT burns that represent claims to physical assets on platforms like Courtyard, based on Dune.

From booster packs to blockchain packs

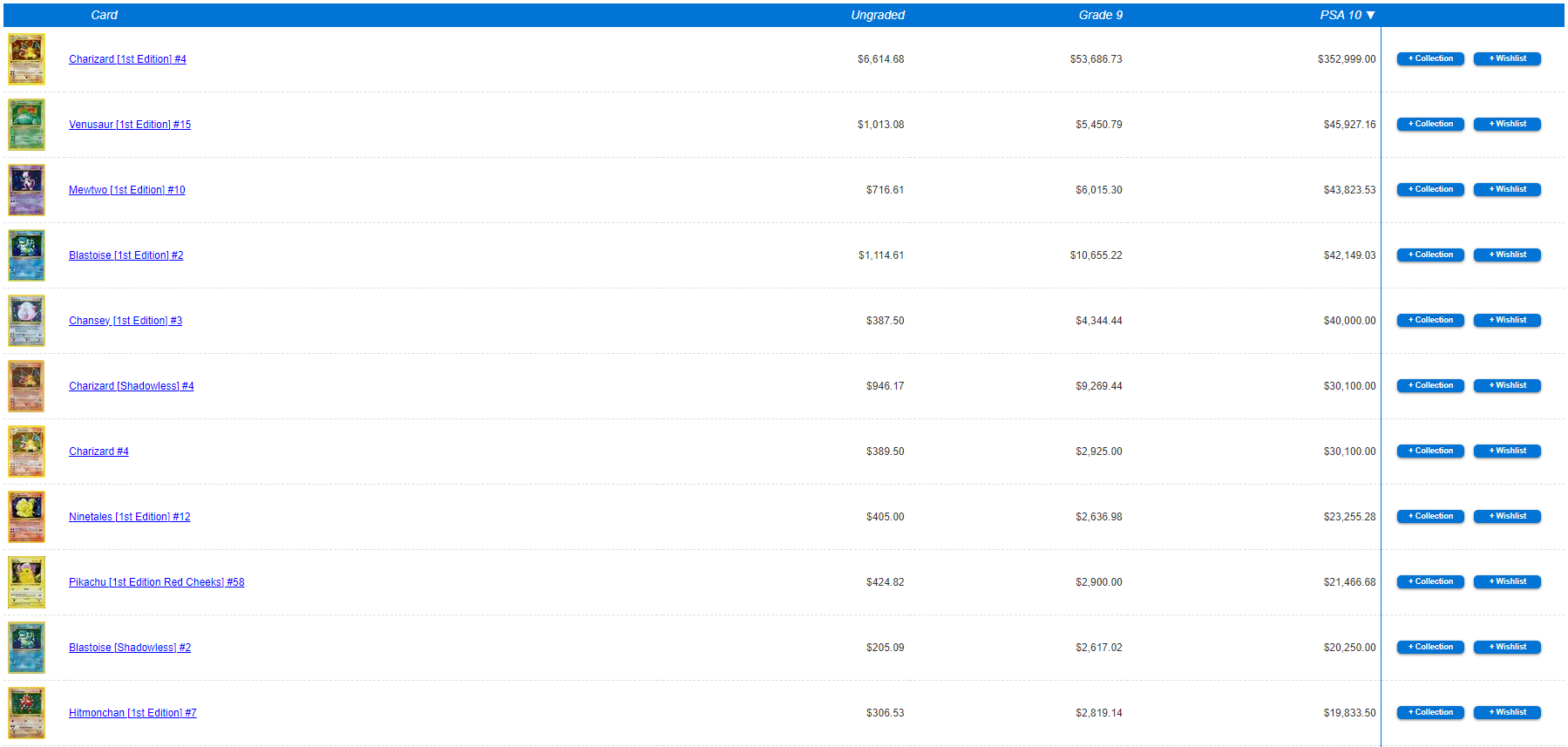

Gacha traces its roots to Japanese vending machines: pay a fixed amount and receive a randomized item. In traditional trading card games, this typically takes the form of sealed booster packs that contain an unpredictable assortment. The value of the cards inside can vary dramatically based on rarity, condition, print run, and the year of release—creating a market where prices can span from very small amounts to prices that reach the hundreds of thousands of dollars for pristine copies.

Because condition and authenticity matter so much at the high end, grading has become central to how these collectibles trade. Independent graders such as PSA, Beckett, or CGC evaluate attributes like centering, wear on corners and edges, and surface imperfections, then encapsulate the card in a sealed holder (“slab”). Two visually similar cards can command very different prices once graded.

That is the gap blockchain projects aim to bridge. According to the article, platforms such as Collector Crypt and Courtyard tokenize real collectibles by accepting physical cards (often already graded), storing them in vaults, and issuing NFTs tied to specific cards and stated grades. When a user opens a pack, the system delivers a token backed by a corresponding physical asset held in custody. Users can keep the NFT, trade it on marketplaces, sell it back to the platform, or redeem it for the physical card.

The core dependency is straightforward but important: the NFT value depends on whether the vault truly holds the exact card in the claimed condition. That places custodial and integrity risk on platform operators—risk that the article notes is not theoretical, as grading companies themselves report fraud and counterfeits.

What drove the June surge

Tokenized gacha’s rise is unlikely to be explained by one variable. The report points to several converging factors, including strong brand momentum in Pokémon and an onchain infrastructure that makes buying, trading, and verification feel immediate.

On the consumer side, the article cites Circana research saying Pokémon became the most popular toy brand in the U.S. in 2025, generating $2.5 billion in sales—up 87% year over year. It also points to interest from older collectors, not just children, alongside heightened demand for card grading.

That grading demand appears to have spilled into operations. In June, PSA reportedly suspended new submissions across four basic service levels while working through a backlog of nearly 10 million cards, according to the service-level update referenced in the article. Tokenization, in this framing, plugs into a market where collectors want liquidity and frictionless access, but where traditional channels can be slow and expensive.

The article also draws a direct line between tokenized packs and mainstream excitement around trading cards, noting that high-profile buyers such as Logan Paul have helped keep Pokémon in the public spotlight.

The mechanics: speed, buybacks, and speculation

While the collectibles are physical, the market behavior is increasingly shaped by how fast users can cycle positions. A major friction in the traditional offchain trading-card market is liquidity. Selling a card often requires finding a counterparty, confirming authenticity and grade, and arranging shipping.

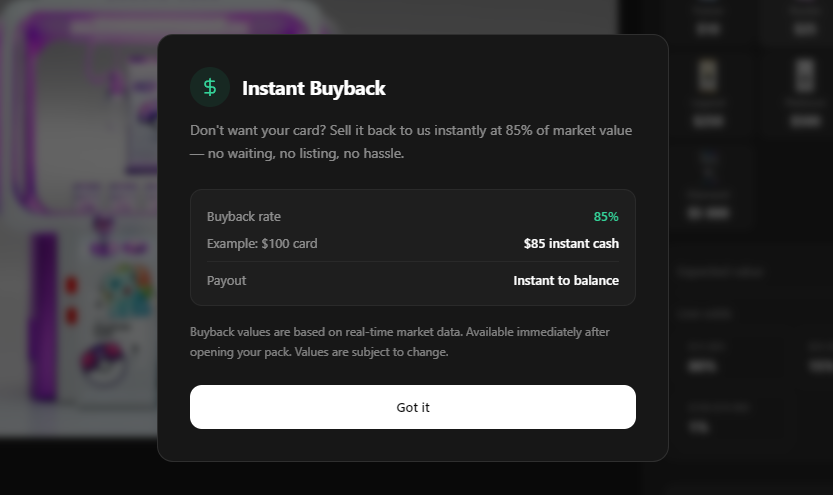

Onchain tokenized trading cards can reduce that friction by offering built-in pathways for trading. The article specifically describes an “instant buyback” mechanism: many platforms allow users to sell packs/cards back shortly after opening—so if the outcome disappoints, users can cash out quickly (for example, at a discount such as 85% of value in the article’s description) and open another pack. If the card is desirable, users can list it or hold it.

This creates a “gacha loop” that compresses what can take weeks offchain into minutes or seconds onchain. The article compares the effect to loot boxes in video games—where users pay for randomized outcomes and the appeal often includes the dopamine and uncertainty around rare pulls.

There are regulatory implications in the background. The article notes that some jurisdictions have tried to bring loot boxes under gambling frameworks. Whether tokenized TCG mechanics fall into similar categories could depend on how large the sector becomes and how platforms structure odds, marketing, and redemption terms. For now, the key operational difference highlighted is tempo: the same gacha logic plays out faster in the onchain environment.

Collectors haven’t disappeared—redemption still exists

Despite the gambling-like loop, tokenized trading cards also serve a less flashy purpose: enabling real collectors to hold and redeem physical assets. According to Dune data cited in the article, users burn 5% to 8% of NFTs issued on Courtyard each week, with each burn representing a claim to a physical card.

Collector Crypt’s head of marketing, Dakota Campbell, is cited as saying that around 30% of its users eventually redeem a card. He also claims that many users choose to hold rather than constantly flip, often beyond the 72-hour buyback window described in the article.

Campbell further reports that, in the prior 30 days referenced in the piece, 5,400 assets were shipped to 634 unique users with a total insured value of $3.29 million. That detail matters because it anchors the story in actual custody and logistics, not only trading behavior.

Why this matters beyond one record month

Blockchain startups are essentially taking an established collectibles playbook—tokenizing and routing demand through faster rails. But the sustainability of onchain gacha is an open question. The article emphasizes that inflows can reverse quickly, since the gacha loop runs in both directions and user engagement can be sensitive to broader sentiment.

For readers and market participants, the key thing to watch next is whether platforms can maintain trust and real-world custody at scale—especially as counterfeit risk and consumer protection concerns remain persistent themes in graded-card markets—while also building durable collector communities that go beyond short-term speculation.

BlackRock’s BUIDL looks like a stablecoin, pays interest like a bond fund, and is legally neither. Tokenized money market funds are the fastest-growing real-world asset in crypto, and almost nobody who talks about them can explain what you actually own.

Summary

- A tokenized money market fund is a regulated fund holding short-term instruments such as Treasury bills, repo, and cash, whose shares circulate as tokens on public blockchains instead of sitting only in a traditional register.

- They look like stablecoins and are legally the opposite. Payment stablecoins are barred from paying holders interest; tokenized money market funds are securities that distribute money market returns.

- Tokenized Treasury products grew from under $1 billion in early 2024 to more than $15 billion by April 2026, led by BlackRock’s BUIDL at roughly $2.5 to $3 billion.

- Access is permissioned. Wallets must be allow-listed by a transfer agent after identity checks, and transfers to unapproved addresses fail at the contract level. This is not a permissionless crypto asset.

- The uncomfortable data: roughly 90% of BUIDL and WisdomTree’s WTGXX sits in about four wallets each, and the main holders are DeFi protocols using the tokens as collateral, not retail savers.

For a decade, crypto’s answer to the question of where to park idle dollars was a stablecoin, and stablecoins had one glaring flaw as a savings instrument: they paid you nothing while the issuer collected the interest on the reserves. Tokenized money market funds are the industry’s response, and they have quietly become the most successful real-world asset category in existence. BlackRock, JPMorgan, Franklin Templeton, and Circle all now run one. The category went from essentially nothing to over $15 billion in about two years. And yet the basic question of what a holder actually owns, and what rights come with the token in the wallet, is answered wrong constantly, including by people trading them. This guide covers the structure, the mechanics, the major products, and the concentration problem sitting underneath the growth story.

What a tokenized money market fund is

A money market fund is one of the oldest and dullest products in finance. It pools money, invests it in very short-term, very low-risk instruments, and pays out the interest those instruments generate. Treasury bills with weeks to maturity, overnight repurchase agreements secured by Treasuries, and cash. The fund targets a stable value per share, conventionally one dollar, and the return comes from the underlying yield.

A tokenized money market fund is that same product with one change: the shares are represented as tokens on a blockchain, and the ownership record is maintained on-chain through a permissioned system rather than solely in traditional book-entry form. The fund still holds the same T-bills. The manager still runs the same mandate. The custodian bank still holds the underlying securities. What changes is the settlement rail.

That change is smaller than the marketing suggests and more consequential than the skepticism allows. It is not a reinvention of the product. It is a decades-old instrument moved onto infrastructure that settles in minutes instead of on a T+1 or T+2 cycle, operates continuously, and lets the share itself be programmable. Managers cut operational cost, holders gain around-the-clock mobility, and regulators get an auditable real-time record. Nobody involved is promising a revolution. They are removing settlement friction from cash management, which is a real if unglamorous prize.

Legally, these are securities. They are regulated and supervised by securities authorities, and the classification is what separates them from the thing they resemble.

Why they are not stablecoins

This is the distinction everything else depends on, and it is a legal one rather than a technical one.

A payment stablecoin such as USDC is designed as a settlement asset: a token that holds a dollar and moves. Under the GENIUS Act, US payment stablecoin issuers must hold full reserves in liquid assets, and they are prohibited from paying interest to holders. The issuer earns the yield on the reserves. You get the dollar.

A tokenized money market fund is designed as an investment: a token representing a share in a regulated fund that distributes returns in line with money market rates. Holders receive the yield. BlackRock’s OnChain Shares filing disclosed a 3.61% seven-day yield as of the end of 2025, which gives a concrete sense of the difference between holding a share and holding a stablecoin.

The odd part is that the two instruments are often backed by nearly identical assets. Both hold short-term Treasuries and cash. The economic substance is close to the same, and the legal classification is completely different, which determines who receives the interest and what rules apply. As one analyst framed it, these are essentially the same asset with different legal classifications and limitations.

The categories are also converging from both directions. The GENIUS Act permits eligible reserve assets, including money market funds, to be held in tokenized form, which means a tokenized fund can sit inside a stablecoin’s reserves. USDS, the third-largest stablecoin globally, reportedly holds BUIDL and JTRSY among its reserves, and Mountain Protocol’s stablecoin and frxUSD have done the same. JPMorgan launched JLTXX in May 2026 explicitly engineered as a GENIUS-compliant reserve asset for stablecoin issuers, seeded with $100 million alongside Anchorage Digital. The tokenized fund is becoming the thing that backs the stablecoin.

How one actually works

The operational flow has five steps and is considerably more controlled than a typical crypto transaction.

Step one: identity. The investor completes know-your-customer and sanctions screening with the transfer agent or an authorized platform. There is no anonymous participation.

Step two: allow-listing. The investor’s wallet address is added to an on-chain allow list maintained by the token contract. This is the critical departure from permissionless assets. An unapproved wallet cannot receive or hold the token, and a transfer to a non-approved address reverts at the contract level. The BIS has noted that these products rely on wallet allow-listing to constrain peer-to-peer trading and meet compliance requirements.

Step three: subscription. The investor sends cash, stablecoin, or another approved instrument. Payment methods vary: some funds accept only fiat wires, some accept USDC, some accept both. For BUIDL, investors wire dollars to the fund’s bank account at BNY Mellon.

Step four: issuance. The transfer agent confirms the subscription and the smart contract mints tokens to the whitelisted wallet, while the official ownership record is updated. The trade settles in minutes, bypassing the traditional clearing cycle.

Step five: yield. The interest earned by the underlying assets flows to holders through one of two designs. Accruing tokens hold price at $1.00 and pay rewards by minting additional tokens into holder wallets on a daily or monthly cadence, which is BUIDL’s model. Rebasing tokens grow the balance in each wallet automatically, so a wallet holding 1,000 tokens might hold 1,003.5 a month later.

Redemption reverses the path. Tokens go to the issuer’s contract, the contract burns them, and the administrator pays out dollars or, increasingly, a regulated stablecoin.

Four parties make this work, and it is worth naming them because the marketing tends to omit most. On the traditional side: a manager running the portfolio, a custodian bank holding the underlying securities, and a transfer agent keeping the official ownership record. On the tokenization side: a platform such as Securitize or Tokeny operating the smart contracts, and an oracle, typically Chainlink, publishing the fund’s net asset value on-chain so the token reflects its price.

What you actually own

Here is the part that gets stated backwards most often. The token in your wallet is not the ownership record.

The beneficial ownership of the fund shares remains recorded in the transfer agent’s official register. The token functions as a digital receipt that enables on-chain mobility. When a token moves between two authorized wallets, the system updates the off-chain ownership record to match. JPMorgan, among others, retains the authority to correct discrepancies between the on-chain ledger and the legal record, so that the technological holding never diverges from the legal reality.

Read that again, because it inverts the usual crypto assumption. In Bitcoin, the ledger is the truth. Here, the ledger is a mirror of the truth, and if the two disagree, the off-chain register wins and the chain gets corrected. Holding the token does not by itself prove ownership. Your rights flow from the fund documents, the transfer agent’s register, and the product’s redemption terms.

Access rules vary by product and are restrictive almost everywhere. BUIDL is a Securities Act Rule 506(c) private fund limited to qualified purchasers, with subscriptions starting around $5 million. USYC is available only to non-US persons. Some products carry institutional minimums far above any retail threshold. Acquiring exposure through a secondary market or an unapproved wallet may not carry the same rights as subscribing directly.

Legal structures differ too, in ways that matter. Some tokenized funds are digital representations of shares in a conventional US government money market fund, which allows broader participation but imposes strict liquidity constraints, including the requirement that 99.5% of assets sit in cash, government securities, or repo collateralized by them. Others are not money market funds at all in the regulatory sense, but private funds for accredited investors, exempt from many of the disclosure and liquidity risk management requirements that apply to registered funds. Treating BENJI, BUIDL, USYC, and WTGXX as interchangeable is a mistake, because their legal wrappers are not the same.

The major products

BUIDL is the BlackRock USD Institutional Digital Liquidity Fund, launched on Ethereum on March 20, 2024, with Securitize as transfer agent. It sits around $2.5 to $3 billion across at least eight networks, making it the largest single tokenized Treasury product. Each token targets $1.00, dividends accrue daily and pay monthly as newly minted BUIDL, and holders can custody at Anchorage, Coinbase Custody, Fireblocks, BitGo, Komainu, Copper, or their own multisig provided the wallet is whitelisted. Major derivatives platforms including OKX and Deribit accept it as collateral.

BENJI is the Franklin OnChain US Government Money Fund, the first tokenized money market fund, launched in 2021 on Stellar and since expanded to Polygon, Canton, Ethereum, Arbitrum, Base, Aptos, Avalanche, and Solana. One FOBXX share equals one BENJI token, with the transfer agent maintaining the official record through the Benji platform.

USYC was launched by Hashnote and later folded into Circle. It briefly overtook BUIDL on January 22, 2026 at roughly $2.98 billion, helped by deep integration as collateral on crypto-native venues.

OUSG and USDY, both from Ondo, show the structural creativity. OUSG is a fund-of-fund whose underlying allocation flows substantially through BUIDL, letting an issuer market a token under its own brand with its own fee and minimum structure. USDY is a reward-bearing note for non-US holders.

JLTXX and MONY are JPMorgan’s entries, with MONY launching on Ethereum in December 2025 and JLTXX following in May 2026 as a purpose-built stablecoin reserve asset.

WTGXX is WisdomTree’s Government Money Market Digital Fund, and USTB is Superstate’s short-duration Treasury product.

BlackRock also filed a registration statement in May 2026 for a fund whose OnChain Shares would have their official ownership record maintained through Securitize Transfer Agent using a permissioned system connected to multiple public blockchains. That filing was subject to completion, and the securities cannot be sold until it becomes effective.

What the tokens are used for

Demand does not come from savers. It comes from three institutional use cases.

Collateral. This is the largest driver. A tokenized fund share earns yield while sitting as margin, which a stablecoin cannot do. Crypto prime brokers allow clients including hedge funds to post BUIDL as collateral for derivatives trading, and DeFi protocols such as Aave’s Horizon accept tokenized funds as collateral against stablecoin borrowing. Capital that would otherwise sit idle in USDC now earns Treasury yield without leaving the trading system.

Stablecoin reserves. As covered above, tokenized funds are moving into the reserve baskets of stablecoins, a structural linkage that barely existed two years ago.

Fund-of-fund wrappers. OUSG is the model: build a product on top of another issuer’s fund, tailor the fees and minimums, market it under your own brand.

Notice what is absent from that list. Nobody is buying these to save for retirement. The BIS found that companies operating DeFi protocols are the main investors in BUIDL, and that fact explains the concentration data below.

How the yield actually reaches you

The yield mechanics deserve their own walkthrough, because they are where the tokenized wrapper does something a traditional fund share cannot, and where most confusion about these products lives.

Start with the source. The fund holds Treasury bills, overnight repo, and cash. Those instruments pay interest. That interest accrues to the fund and raises the value of the portfolio. In a conventional money market fund, the manager either lets the share price float slightly or, far more commonly, holds the share at a constant dollar and distributes the accrued income to holders on a schedule. Nothing about tokenization changes this part. The yield comes from short-term government debt, and it is whatever short-term government debt happens to pay.

Now the delivery, which is where the designs diverge. Accruing token models keep the token price pinned at $1.00 and pay rewards by minting additional tokens into holder wallets. BUIDL works this way: dividends accrue daily based on the fund’s net yield and are distributed monthly as freshly minted BUIDL. Your token count rises; each token stays worth a dollar. Rebasing models take the other route, growing the balance in each wallet automatically as rewards accrue, so a wallet holding 1,000 tokens at the start of a month might hold 1,003.5 by the end without any transaction appearing.

The distinction sounds cosmetic and is not, for two reasons. First, integrations break differently. A DeFi protocol that assumes a fixed balance will mishandle a rebasing token, and one that assumes a fixed supply will mishandle an accruing one. Second, the tax and accounting treatment of receiving new tokens is not obviously the same as the treatment of a balance silently increasing, and that difference belongs to the holder.

Then the part that has no traditional analogue at all: the share keeps earning while it works. This is the entire commercial case for the category, and it is worth stating precisely.

In the old arrangement, capital posted as margin sat idle. You wanted yield, so you held a money market fund; you wanted to trade, so you posted cash; you could not do both with the same dollar without a settlement cycle standing between them. A tokenized share collapses that. BlackRock structures BUIDL so exchanges including OKX and Deribit accept it as collateral for derivatives trades, and DeFi lending markets accept tokenized funds as collateral against stablecoin borrowing. The same dollar earns roughly the Treasury rate and backs a leveraged position at the same time.

That is not a marketing flourish. It is a genuine improvement in capital efficiency, and it explains the growth curve better than any narrative about democratized access.

Institutions did not adopt these products because they are on a blockchain. They adopted them because the blockchain let a yield-bearing security move at the speed of collateral, and collateral that earns is strictly better than collateral that does not.

It also explains the concentration. If the product’s killer feature is posting yield-bearing margin against derivatives positions, then the natural buyer is a trading desk or a protocol treasury, not a saver. The design selected its holders. Four wallets is not an accident of a young market; it is the predictable result of building an institutional collateral instrument and describing it as a savings revolution.

The concentration nobody advertises

The growth chart is genuinely impressive: under $1 billion in early 2024 to more than $15 billion by April 2026, with Boston Consulting Group and Standard Chartered projecting the broader tokenization market could reach $16 trillion by 2030. Set against a stablecoin market above $300 billion, tokenized funds are roughly 5% of the on-chain dollar economy, which is small but no longer trivial.

Now the part that appears in the BIS data and almost nowhere in the promotional material. For BUIDL, and also for WTGXX, around 90% of total holdings sit in the hands of only four wallet holders each, according to blockchain data. Demand from DeFi protocols has produced high concentration and limited trading activity.

That is a different product from the one being described in press releases. A category marketed as democratizing access to institutional cash management is, in practice, a handful of protocols and trading desks using an instrument that retail cannot legally touch. The allow-list model guarantees it: if wallets require qualified-purchaser status and $5 million minimums, the holder base will be institutional by construction.

The concentration has a practical consequence beyond optics. Four holders means redemption risk is lumpy. If one of four wallets holding a quarter of a fund decides to exit, the fund must liquidate a meaningful share of its portfolio at once. Money market funds are built for diversified redemption patterns, and a book with four holders does not have one. That risk has not been tested, partly because, as the ECB has observed, the tokenization market is still young enough that stress behavior has not yet been observed.

There is also a regulatory gap worth naming. In the EU, tokenized money market funds fall within the existing Money Market Fund Regulation, but whether they are permitted under MiCA is unclear, since the relevant implementing regulation has not been adopted. And the largest product by assets, BUIDL, is a private fund, which means it is exempt from many of the disclosure and liquidity risk management requirements that registered money market funds must meet. Regulators and the public have limited visibility into whether private tokenized funds have adopted the same liquidity tools, such as portfolio maturity maximums and liquid asset minimums, that registered funds are required to run.

The honest assessment

Tokenized money market funds are the clearest example in crypto of tokenization doing something real. They are not a narrative waiting for adoption. They hold actual Treasuries, pay actual yield, settle faster than the traditional rail, and have found genuine product-market fit as yield-bearing collateral. Compare that to most real-world asset projects, and the difference is stark.

The honest caveats are equally clear. This is not decentralized finance in any meaningful sense: access is permissioned, the ledger defers to an off-chain register, and an intermediary can correct your balance. The holder base is four wallets deep on the largest products. The retail access the category is marketed on does not exist for most of these funds. And the newest use case, sitting inside stablecoin reserves, quietly builds a linkage between the tokenized fund market and the $300 billion stablecoin market that regulators have not yet stress-tested.

The right way to hold both thoughts is this: tokenization worked here because it was applied to a product that did not need reinventing, only rewiring. That is the lesson, and it is a rebuke to every project trying to tokenize something that has no settlement problem to solve.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. Tokenized money market funds are securities subject to access restrictions, and eligibility, minimums, and terms vary by product and jurisdiction and can change at the manager’s discretion. Nothing here is a recommendation to buy any product. Always do your own research. Figures are accurate as of July 16, 2026.

Frequently Asked Questions

What is a tokenized money market fund?

It is a regulated fund holding short-term, low-risk instruments such as Treasury bills, overnight repo, and cash, whose shares are issued and recorded as tokens on public blockchains instead of only in a traditional register. Legally the shares are securities. The fund holds the same assets and follows the same mandate as a conventional money market fund; what changes is the settlement infrastructure.

How is it different from a stablecoin?

Legally and economically. Payment stablecoins are settlement assets and, under the GENIUS Act, US issuers are prohibited from paying interest to holders, so the issuer keeps the reserve yield. Tokenized money market funds are securities that distribute money market returns to holders. Both are often backed by nearly identical assets, which is why the distinction is legal classification instead of substance.

What is BUIDL?

The BlackRock USD Institutional Digital Liquidity Fund, launched on Ethereum in March 2024 with Securitize as transfer agent. It is the largest tokenized Treasury product at roughly $2.5 to $3 billion across at least eight networks. It is a Rule 506(c) private fund limited to qualified purchasers, with subscriptions starting around $5 million, targeting $1.00 per token with daily accrued yield paid monthly as new tokens.

Can anyone buy one?

Generally no. Access is permissioned and varies by product. BUIDL is limited to qualified purchasers with multi-million dollar minimums. USYC is restricted to non-US persons. Wallets must pass identity screening and be added to an on-chain allow list before they can hold the token, and transfers to unapproved addresses fail at the contract level.

Do I own the fund shares if I hold the token?

Not by itself. The authoritative ownership record is the register maintained by the transfer agent. The token acts as a digital receipt enabling on-chain mobility, and when it moves between approved wallets the off-chain record updates to match. Some administrators retain authority to correct discrepancies between the chain and the legal record. Your rights flow from the fund documents and the register.

How big is the market?

Tokenized US Treasury products and similar money market funds grew from under $1 billion in early 2024 to more than $15 billion by April 2026. For scale, the stablecoin market sits above $300 billion, making tokenized funds roughly 5% of the on-chain dollar economy. Boston Consulting Group and Standard Chartered project the broader tokenization market could reach $16 trillion by 2030.

Who actually holds these tokens?

Overwhelmingly institutions, and very few of them. The BIS found that companies operating DeFi protocols are the main investors in BUIDL, and blockchain data indicates roughly 90% of BUIDL and WisdomTree’s WTGXX holdings sit with about four wallet holders each. The dominant use is as yield-bearing collateral for derivatives and lending, not as a savings product.

What are the risks?

Concentration is the most immediate: a handful of holders creates lumpy redemption risk that diversified money market funds do not carry. The largest products are private funds exempt from many disclosure and liquidity requirements that registered funds must meet. Regulatory treatment is unsettled in the EU under MiCA. And the growing use of these funds inside stablecoin reserves creates linkages between two markets that have not been stress-tested together.

June 2026 was brutal for the crypto market. Bitcoin (BTC) fell more than 20%, hitting a 21-month low, while spot Bitcoin ETFs saw a record $4.5 billion in outflows.

That did not stop users from spending a record $324 million on onchain gacha during the month, according to Blockworks Research. A year earlier, the monthly figure was closer to $50 million.

Spending hit a new all time high in the depths of a bear market. While crypto prices were tanking, people were opening more and more packs of tokenized Pokémon cards — driven by the thrill, the hope of a profit or the urge to expand a collection.

It’s an entire randomized Real World Asset (RWA) sector that’s flown under the radar… until now.

Onchain gacha spending hit an all-time high in June 2026. Source: Blockworks.

Booster packs, grades and slabs

Gacha is a mechanism borrowed from Japanese vending machines, where a fixed payment yields a random item. In the trading card game (TCG) market, it usually works through booster packs: sealed packs holding a random assortment of cards. The buyer does not know in advance what they will get.

The cards inside a booster are not created equal. Print run, rarity, condition and year of release drive prices orders of magnitude apart: from cents for an ordinary card, to hundreds of thousands of dollars for a rare copy in pristine condition. A market has grown up around those collectibles, which Global Market Insights values at $9.2 billion and Mordor Intelligence at $15.11 billion.

Some cards can fetch several hundred thousand dollars. Source: PriceCharting.

When a card can cost as much as a car, its authenticity and condition have to be assessed.

Related: Logan Paul sells Pokémon card for $16.5M, years after fractional NFT row

That is what grading is for — a process in which an independent company such as PSA, Beckett or CGC checks a card against several criteria. The card is inspected for image centering, the condition of its corners, edges and surface, and for scratches and stains, after which it is assigned a grade and sealed in a plastic case known as a slab.

The grade directly affects the price: two identical cards can be worth completely different amounts, while a raw, ungraded card sells as a riskier asset.

A Pokémon card sealed in a PSA slab. Source: eBay.

Projects such as Collector Crypt and Courtyard are moving these real world assets onto the blockchain. They accept physical cards — usually ones that have already been graded — hold them in vaults and issue NFTs tied to a specific copy.

When a user buys and opens a pack, they receive a token backed by a real card in a real vault. The token can be kept, listed on a marketplace, sold back to the platform or redeemed for the physical card.

Crucially, the value of these NFTs rests on the assumption that the partner vault really does hold that exact card in the stated grade. The user takes on custodial risk — the safety of the asset, the integrity of the authentication and the durability of the platform itself — and with grading companies themselves reporting a rise in counterfeits, that assumption is far from trivial.

Why now?

The growing popularity of onchain gacha, and of TCG-focused blockchain platforms more broadly, is probably down to several factors.

Pokémon cards are the core product for many of these projects, and the franchise is on a roll right now.

According to research firm Circana, Pokémon became the most popular toy brand in the US in 2025, with $2.5 billion in sales, up 87% from a year earlier.

The interest is not coming from children alone. Wealthier members of Generations Y and Z sometimes prefer cards to expensive paintings. Demand for grading is so high that in June, PSA temporarily suspended card submissions across four basic service levels as it tried to work through a backlog of almost 10 million cards.

Tokenization simply plugged into this frenzy by providing a useful service and removing friction.

High-profile buyers like Logan Paul have helped push Pokémon cards into the spotlight. Source: Logan Paul.

The real world trading card market suffers from a problem common to all collectibles markets: the absence of instant liquidity. To sell a card offchain, the owner has to find a counterparty, verify its authenticity and grade, and ship the item.

Related: The 5 types of real world assets being tokenized fastest onchain

“Traditional marketplaces are slow and expensive,” Dakota Campbell, head of marketing at Collector Crypt, told Cointelegraph. “With tokenized trading cards, collectors can buy, sell, trade, and verify ownership instantly while the physical asset remains securely vaulted until they want it shipped.”

Collector Crypt has tokenized roughly $40 million worth of cards and comic books, according to Campbell. About $23 million of that inventory belongs to the platform itself, while the rest sits in user wallets or has already been redeemed. To keep up with demand, the company buys around $2 million worth of cards every week.

Gambling on collectibles

As with the NFT boom, it’s hard to deny that price speculation and gambling-style dopamine hits from the random prizes are part of the appeal.

The instant buyback mechanism, available on most platforms, creates an almost perfect “gacha loop”: Buy a pack, and if the card is unappealing or not worth much, sell it back for, say, 85% of its value and go open the next one. Pull something rare, and either list it on a marketplace or keep it. Unlike with physical cards, there’s no searching for a buyer, no shipping, no waiting.

The “instant buyback” option is available on nearly all TCG platforms. Source: Phygitals.

The gagcha mechanism is similar to loot boxes within video games: The user pays for a random outcome, knowing only the odds. Some jurisdictions have already tried to bring loot boxes under gambling regulations. Whether that logic will reach tokenized TCGs probably depends on how big the sector grows.

Either way, this is exactly how the traditional TCG market works. The only difference is speed: Offchain, closing the gacha loop takes weeks. Onchain, it takes a few seconds.

Sometimes users are driven by nothing more than the desire to “try their luck.” Source: X.

“There is always speculation in an emerging market, especially in the crypto sector,” Campbell said, while arguing that the platform benefits most from committed collectors hunting for their next “grail.”

No country for collectors?

Genuine collectors of physical cards still make up a proportion of the market. According to Dune, users burn 5% to 8% of the NFTs issued on Courtyard each week, with each burn representing a real physical claim.

Users burn 5% to 8% of Courtyard’s issued NFTs each week for physical cards. Source: Dune.

Collector Crypt reports that around 30% of its users eventually redeem a card, according to Campbell, and many more hold their cards in their onchain inventory past the 72-hour buyback window rather than flipping them.

“In just the last 30 days, 5,400 assets shipped to 634 unique users at $3.29 million insured value,” he said.

New tracks for an old train

Essentially, blockchain startups are running the classic tokenization play: moving a proven business model onto more efficient rails and removing some of the friction.

Concerns about the speculative nature of this market, or the role of gambling in it, are warranted to the extent that platforms build their marketing around this aspect.

Beyond that, this is simply how gacha works. People sift through the “junk” in pursuit of a rare card. And if there are complaints to be made, they should be addressed to the entire TCG industry, not just its onchain segment.

As for June’s records, they are the result of several factors converging. The traditional card market is booming, tokenization has proved mature enough to plug into it, and the gacha mechanic sits neatly on blockchain rails.

How sustainable that is remains an open question. The gacha loop runs fast in both directions, and record inflows can reverse just as fast.

Features: Will the crypto lobby’s $189M campaign get CLARITY over the line?

Trump’s CFPB overhaul cost Americans $26.5 billion, Sen. Warren says

Short sellers load up against SpaceX as stock retreats back to IPO price

Virat Kohli breaks Ricky Ponting’s record, enters all-time top-five elite list | Cricket News

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports7 days ago

Sports7 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports6 days ago

Sports6 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Politics1 day ago

Politics1 day agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

News Videos2 days ago

News Videos2 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech2 days ago

Tech2 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech2 days ago

Tech2 days agoDark Secrets Emerge When Jailbreaking LLMs

-

Entertainment22 hours ago

Entertainment22 hours agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

Sports18 hours ago

Sports18 hours agoNew Cornerback Enters Vikings Trade Rumor Mill

-

Crypto World14 hours ago

Crypto World14 hours agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

News Videos3 days ago

News Videos3 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Tech3 days ago

Tech3 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Entertainment21 hours ago

Entertainment21 hours agoVicki Gunvalson Defends Discussing Heather Dubrow’s Money

-

Crypto World2 days ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

-

NewsBeat18 hours ago

NewsBeat18 hours agoWatch: Is Donald Trump facing a popular backlash on immigration?

-

Sports15 hours ago

Sports15 hours agoMichigan officials not expected to discuss AD Warde Manuel at Thursday meeting

-

Business2 days ago

Business2 days agoACCC warns AI could lift insurance costs in risk-prone areas

-

NewsBeat17 hours ago

NewsBeat17 hours agoFirefighters issue update on Dovestone moorland blaze as fire enters fourth day

-

Business12 hours ago

Business12 hours agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Entertainment4 days ago

Entertainment4 days agoHollywood’s Biggest Director Just Called Out AI, And It’s Glorious

You must be logged in to post a comment Login