Crypto World

Bitcoin ETFs See $331M Inflows as BTC Recovers Above $70K

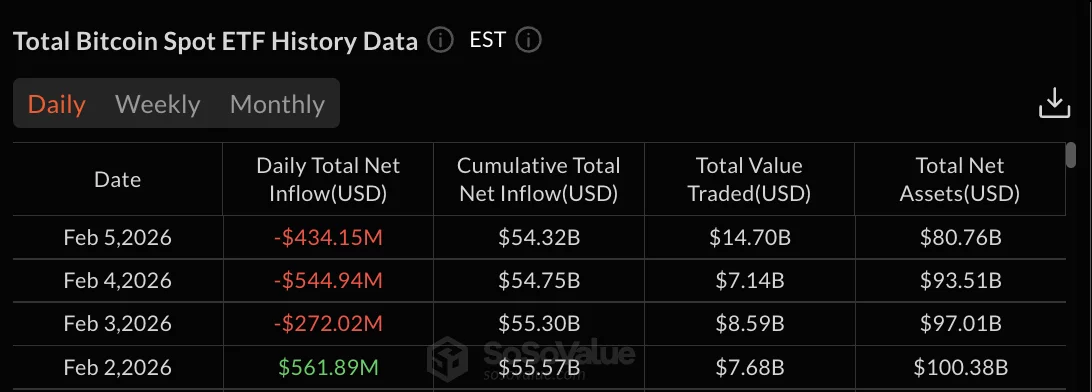

Bitcoin ETFs recorded $330.67 million in net inflows on February 6, ending a three-day outflow streak that drained $1.25 billion from products.

Summary

- Bitcoin ETFs recorded $330.7M in inflows on Feb. 6, ending a $1.25B outflow streak.

- BlackRock’s IBIT led with $231.6M as BTC rallied 6.6% above $70,000.

- Ethereum ETFs diverged with $21.4M in outflows, led by BlackRock’s ETHA.

BlackRock’s IBIT led with $231.62 million in inflows. At the same time, Ark & 21Shares’ ARKB has brought in $43.25 million and Bitwise’s BITB posted $28.70 million in inflows.

The reversal came as Bitcoin (BTC) price climbed 6.6% over 24 hours and quickly fell to the $67,000 level.

Total net assets under management rose to approximately $105 billion from $80.76 billion on February 5, while cumulative total net inflow reached $54.65 billion. VanEck’s HODL and Fidelity’s FBTC showed no updated data for the trading session.

February 2-5 posted $1.25B in Bitcoin ETFs redemption

The three-day selling wave began February 3 with $272.02 million in outflows, followed by the streak’s largest single-day withdrawal of $544.94 million on February 4.

February 5 recorded $434.15 million in Bitcoin ETFs redemptions before buying pressure resumed.

February 2 briefly interrupted the selling with $561.89 million in inflows, but failed to establish sustained surge.

Total net assets fell from $100.38 billion on February 2 to a low of $80.76 billion on February 5 before recovering with February 6’s inflows.

Grayscale’s mini BTC trust attracted $20.13 million while the primary GBTC product recorded zero flows. Invesco’s BTCO posted $6.97 million in inflows. Valkyrie’s BRRR, Franklin’s EZBC, WisdomTree’s BTCW, and Hashdex’s DEFI all recorded zero activity.

BlackRock’s IBIT maintains $61.84 billion in cumulative net inflows. Grayscale’s GBTC holds -$25.88 billion in net outflows since converting from a trust structure.

Fidelity’s FBTC has accumulated approximately $11.08 billion in cumulative inflows based on available data.

Ethereum posts $21 million in outflows as BlackRock withdraws

Ethereum spot ETFs recorded $21.37 million in net outflows on February 6 despite Bitcoin’s reversal to positive flows.

BlackRock’s ETHA accounted for $45.44 million in redemptions, offsetting positive flows from four other products.

Bitwise’s ETHW led Ethereum inflows with $11.80 million, followed by Grayscale’s mini ETH trust at $6.80 million, VanEck’s ETHV at $3.01 million, and Invesco’s QETH at $2.45 million. Grayscale’s ETHE, Franklin’s EZET, and 21Shares’ TETH recorded zero flows.

Total net assets for Ethereum products fell to $10.90 billion from $13.69 billion on February 2. Cumulative total net inflow dropped to $11.80 billion.

Ethereum has posted outflows in three of the past four trading days, with February 4 and 5 recording $79.48 million and $80.79 million in withdrawals respectively.

February 3 provided brief relief with $14.06 million in inflows before redemptions resumed.

Crypto World

Zcash’s (ZEC) upside hinges on a repricing of financial privacy in an AI-driven world, Grayscale says

Zcash (ZEC) is a wager that the rise of AI surveillance will make financial privacy more valuable, and the crypto market is underpricing that possibility, according to asset manager Grayscale.

“Zcash is nearly 10 years old but may be entering a new chapter. Use of its shielding technology is increasing, and new capital is entering the ecosystem to support wallet development and Zcash mining,” analyst Michael Zhao wrote in a Friday report.

ZEC is a privacy-focused cryptocurrency that uses zero-knowledge proofs to hide transaction details, allowing users to shield the sender, receiver and amount, while still verifying transfers on a public blockchain.

Designed as a more confidential alternative to bitcoin , the largest cryptocurrency, it aims to function as a closer approximation to digital cash in an otherwise transparent crypto ecosystem.

The token has seen multiple boom-and-bust cycles, most notably during crypto bull markets when its privacy narrative gained traction. In late 2025, ZEC surged to nearly $700, sharply outperforming much of the market as investors switched into smaller-cap assets with differentiated use cases.

The move proved short-lived. Prices retraced quickly, falling more than 60% in the following months as momentum faded and larger assets like bitcoin regained favor. The volatility underscores a recurring pattern for Zcash: sharp upside during narrative-driven rallies, followed by steep drawdowns when that narrative loses urgency.

ZEC makes up about 0.3% of the $1.6 trillion crypto “currencies” segment, according to Grayscale, a share it said reflects expectations that privacy stays marginal. If that view changes, even slightly, the upside could be significant.

Grayscale pointed to rising use of Zcash’s shielded transactions, now the majority of activity, as evidence that demand for privacy already exists onchain. But the firm said the market still treats privacy as an afterthought rather than a core monetary feature.

This is part of a broader structural shift. Just as digitization and the internet reshaped financial privacy debates in prior decades, Zhao argued AI and blockchain transparency could trigger a third wave, one where confidential transactions become more valuable.

In that scenario, Zcash’s design positions it as a direct analogue to cash, a property the analyst said is increasingly scarce in digital finance.

Still, there are risks, the report cautioned. Regulatory treatment remains uncertain despite Zcash’s selective disclosure tools. Execution risk persists given the network’s reliance on complex upgrades, and long-term concerns like quantum computing that apply across crypto, including ZEC, the report added.

ZEC was trading 5% higher over 24 hours, around $224.80, at publication time.

Read more: AI rout hits software stocks, but Grayscale says blockchains stand to benefit

Geopolitics and energy constraints shaped Bitcoin’s landscape in March as a notable drop in hashrate coincided with a geopolitical flare-up tied to Iran. Analysts estimated Iran accounts for a meaningful slice of global mining activity, with some figures placing it around 6–8% of hashrate, while military-linked operations reportedly account for a large portion of mining. Following a late-February cross-border operation involving the United States and Israel, the network’s total hashrate slid about 6% over the month, underscoring how disruptions to energy infrastructure and competing strategic priorities can ripple into crypto production.

Against this backdrop, Bitcoin’s price movement remained muted. Bitcoin traded near the $67,000 level as five-year U.S. Treasury yields rose roughly 4% in March, sharpening a risk-off mood and encouraging cash preservation among traders. In parallel, the ecosystem’s appetite for crypto-native forecasting marketplaces surged, with March transactions on prediction platforms hitting a record pace of about 192 million—an uptick of 24% from February and a staggering 2,880% year over year, highlighting a growing, crypto-adjacent activity thread even as regulatory headwinds persist.

Beyond price and hashrate, drivers of liquidity shifted toward euro-denominated stablecoins. A March report found that euro-backed stablecoins now account for about 85% of non-dollar stablecoin transfer volume, with participation by users also concentrated in euros (roughly 78%). The shift is widely interpreted as institutional comfort with euro-pegged coins growing under the Markets in Crypto-Assets framework, which has elevated regulatory clarity for euro-focused crypto liquidity.

On the corporate side of the crypto economy, Robinhood’s stock price weakened in March, sliding about 16% as uncertainty around new regulatory regimes and softer crypto trading revenues weighed on sentiment. The company’s crypto business has faced headwinds in recent quarters, with reports indicating a notable year-over-year decline in crypto-related revenue and app volumes. In response, Robinhood announced a $1.5 billion stock buyback program to be executed over the next three years, a move aimed at bolstering investor confidence amid a broader market pullback.

Within the alt-crypto strategies space, Strategy reported an 11% drawdown on its Bitcoin holdings for March, with an average entry cost near $75,669 and Bitcoin trading around $67,800 at the time of writing. Yet the firm pressed on with purchases, revealing two substantial Beaufort-style adds in March—about 17,994 BTC on March 9 and 22,337 BTC on March 16, totaling roughly $2.7 billion at the relevant prices. Financing these acquisitions, Strategy has leaned on high-yield stock issuances such as Stretch (STRC) to avoid diluting its primary common shares. Chairman Michael Saylor has highlighted that retail investors make up a large share of STRC buyers, framing the instruments as a way to access high-yield digital credit with relatively low volatility.

Key takeaways

- Bitcoin’s hashrate declined about 6% in March, reflecting Iran’s pivotal yet strained role as a mining hub amid energy and security pressures following the February operation against Iran.

- The BTC price hovered near $67,000 as five-year U.S. Treasury yields rose around 4% for the month, contributing to a cautious risk posture among traders.

- Prediction markets posted a record March, with roughly 192 million transactions—up 24% from February and about 2,880% year over year—indicating rising interest in crypto-native forecasting tools.

- Euro-stablecoins now dominate non-dollar liquidity, accounting for about 85% of non-dollar stablecoin transfer volume, with strong user participation, aided by MiCA-aligned regulatory clarity.

- Robinhood’s stock weakness continued into March amid crypto-revenue headwinds, even as the firm advanced a sizable buyback. Strategy’s ongoing BTC accumulation remained sizable but came with an 11% month-long drawdown on holdings.

Hashrate, geopolitics, and the mining cliff

March’s mining dynamics underscored how geopolitical shocks can directly influence the security and economics of Bitcoin’s network. The U.S.–Israel operation in Iran, dubbed by some observers as a pivotal event for regional stability, coincided with a sustained drag on Iran’s mining capacity. Bloomberg’s crypto and digital assets coverage has highlighted Iran as a major mining contributor—estimated at roughly 6–8% of global hashrate—with a large portion of mining activity tied to state or military entities. When energy infrastructure is strained or redirected toward defense, the country’s ability to sustain large-scale Bitcoin mining tightens, creating ripples across the global hashrate figure and potentially affecting network difficulty and block times in the near term.

As miners contend with energy constraints and shifting priorities, the broader mining landscape remains sensitive to policy and geopolitical developments. The global network’s resilience, measured by hashrate, continues to reflect a balance between mining economics, energy costs, and regulatory conditions across jurisdictions. While the immediate impact is a modest hashrate pull for March, it is a reminder of how external forces ultimately shape Bitcoin’s security fabric and the distribution of mining power around the world.

Macro currents, markets, and the march of crypto demand

Bitcoin’s price path in March did not showcase a strong breakout even as macro conditions shifted. The yield curve’s repricing—five-year Treasuries climbing toward a 4% monthly gain—fed a preference for cash or less risky yield assets, weighing on new capital inflows into high-volatility assets like BTC. The combination of macro pressure, a cautious risk stance, and a sense of regulatory caution contributed to a lack of sustained upside for Bitcoin during the month. Yet, the same environment also drew attention to non-price-driven activity, such as prediction markets, where participants speculate on outcomes across events and often use these markets as hedges against broader macro risk. The March surge in such activity indicates a growing appetite for crypto-native financial primitives beyond spot and futures trading.

Stablecoins, MiCA, and strategic balance sheets

The euro-dominated stablecoin footprint—now representing about 85% of non-dollar stablecoin volume and a dominant share of participant activity—reflects a notable shift in liquidity preferences. The trend is closely tied to regulatory clarity introduced by the European Union’s Markets in Crypto-Assets framework, which has elevated institutional comfort with euro-pegged tokens and cross-border use cases. Market participants point to MiCA as a catalyst for more predictable, compliant stablecoin operations, encouraging institutions to integrate euro-denominated liquidity into their crypto rails while reducing some of the regulatory ambiguities that previously constrained non-dollar activity.

On the corporate side, Robinhood’s ongoing struggle with crypto trading revenue underscores the challenge of sustaining a diversified platform in a regulatory-tightening environment. The firm’s decision to deploy a $1.5 billion buyback program signals an attempt to shore up equity value despite a softening revenue trajectory. Meanwhile, Strategy’s Bitcoin program continues to reflect a high-stakes approach to crypto accumulation, funded through high-yield instruments that offer an alternate route to expand BTC holdings without diluting existing equity. The company’s commentary on STRC buyers—where a large portion are retail investors—frames a broader narrative about retail participation in crypto-linked structures and the perceived advantages of branded digital credit offerings in volatile markets.

What to watch next is how MiCA’s rollout further shapes non-dollar liquidity and whether tail risks—ranging from geopolitical shifts to regulatory changes—alter the trajectory of euro-stablecoins and related market activity. Additionally, with prediction markets facing ongoing regulatory scrutiny at the state and federal levels, observers will be watching for any concrete moves that could curb or clarify their role in the broader financial ecosystem.

Markets continue to react to a blend of macro signals, geopolitical developments, and evolving regulatory regimes. The coming weeks will be telling for Bitcoin’s leadership in a climate where liquidity, risk appetite, and institutional confidence are being recalibrated in near real time.

Readers should stay tuned for updates on Iran’s energy and mining dynamics, the pace of MiCA implementation and its practical impact on euro-denominated liquidity, and the evolving regulatory stance on prediction markets in U.S. states. These factors will help determine whether the current risk-off tone persists or shifts toward renewed crypto demand driven by macro reorientation and regulatory clarity.

U.S. spot Bitcoin ETFs bled roughly $296 million in net outflows between March 24 and March 27, as a broad risk-off shift tightened its grip on global markets. The reversal was sharp – Monday opened with $167.2 million in inflows before sentiment collapsed entirely by week’s end.

Friday delivered the killing blow: $225.5 million in single-day outflows, led by heavy redemptions from BlackRock’s IBIT. The week’s total marks one of the most decisive institutional de-risking episodes since the ETF products launched in January 2024.

- $296M in net outflows recorded across U.S. spot Bitcoin ETFs, March 24–27, led by IBIT redemptions of $225.5M on Friday alone.

- Macro pressure is compounding – triple-digit oil, fading ceasefire hopes, and end-of-quarter rebalancing all cited as drivers by multiple analysts.

- BTC price support sits at $65,600–$65,107; a break below that zone would signal structural deterioration rather than tactical repositioning.

Discover: The best pre-launch token sales

ETF Flow Data Points to Institutional De-Risking – But Is It Structural?

Thursday, March 26, alone saw $171.12 million exit across all 11 spot Bitcoin ETF products – the largest single-day outflow in over three weeks. BlackRock’s IBIT shed $41.92 million that day, while Fidelity’s FBTC, Grayscale’s GBTC, Bitwise’s BITB, and ARK’s ARKB each recorded $20–30 million in redemptions. The breadth matters: this wasn’t an issuer-specific bleed – it was coordinated institutional de-risking across the board.

That distinction matters. When outflows concentrate in a single fund, the read is operational or reputational. When every major product sells simultaneously, the signal is macro.

Josh Gilbert, market analyst at eToro, put it plainly: “Risk-off is clearly the mood amongst markets,” pointing to Bitcoin’s slide to a three-week low and the S&P 500’s fifth consecutive weekly loss – its longest losing streak since 2022. “The macro forces working against it are compounding,” he added. “Triple-digit oil is fuelling inflation fears, which pushes rate cut expectations further out, which in turn removes the very catalyst that risk assets need to find a floor.”

Bitcoin’s slide below $67,000 amid rising treasury yields had already flagged deteriorating risk appetite before the ETF data confirmed it. Geopolitical escalation compounded the pressure – President Donald Trump’s comments to the Financial Times, suggesting the U.S. could “take the oil in Iran” and potentially seize Kharg Island, rattled commodity and risk markets simultaneously.

Peter Chung, head of research at Presto Labs, said the risk-off tone was the primary driver, though he noted the outflow “doesn’t seem that dramatic compared to the recent trends.”

Pratik Kala, head of research at Apollo Crypto, echoed that read, calling the $290 million figure “quite normal” and attributing it to “risk-off sentiment and end-of-quarter rebalancing.”

Long-term holder balances remain stable, indicating tactical repositioning rather than a structural exit from Bitcoin exposure. Cumulative ETF investments had surpassed $2 billion in recent weeks before this pullback, underscoring how quickly institutional adoption accelerated through early 2026.

Can Bitcoin ETFs Demand Recover – Or Is More Outflow Pressure Coming?

The price structure gives traders a clear framework. Key support sits at $65,631–$65,107, the February 12–19 lows, with a secondary floor at $65,619 – the March 8 low.

A clean break below $65,600 would shift the read from tactical reset to something more concerning for demand structure. Resistance is parked at $71,880, the March 25 high.

Gilbert flagged a ceasefire as the most immediate catalyst for a “strong relief rally,” but warned that without credible de-escalation, markets face “more choppy sessions ahead.” The Fed rate outlook is the second variable – geopolitical factors weighing on Bitcoin are compressing any near-term case for policy relief.

Three scenarios are live. A ceasefire or dovish Fed signal reopens inflow momentum, and BTC reclaims the $71,000 zone. Base case: choppy, range-bound flow data through April as macro uncertainty persists and ETF demand stays muted. Bear case: a break below $65,100 triggers forced selling and a second wave of institutional outflows that dwarfs last week’s total.

The week’s Monday-to-Friday reversal – from $167.2 million inflows to $225.5 million single-day outflows – is the clearest signal that institutional conviction is conditional right now, not structural. Traders navigating this environment should watch weekly ETF flow totals as a leading indicator for BTC price direction, not a lagging one.

Discover: The best crypto to diversify your portfolio with

The post Bitcoin ETFs See $290M in Outflows as Risk-Off Sentiment Intensifies appeared first on Cryptonews.

The ECB now accepts tokenized securities as collateral, lifting DLT into its toolkit while X erupts over Axiology’s XRP Ledger roots and “no XRP” disclaimer.

Summary

- The European Central Bank now accepts DLT‑issued tokenized securities as collateral for Eurosystem credit operations, effective March 30, 2026.

- Axiology, one of the first eligible platforms, is built on XRP Ledger open‑source code, but the ECB says this does not mean it uses public XRP.

- The distinction has split Crypto X, with XRP supporters trying to frame the move as de facto XRP adoption while critics push back.

The European Central Bank has started accepting tokenized securities issued on distributed ledger technology as eligible collateral for Eurosystem credit operations, in what many in European markets see as a watershed moment for on‑chain finance. The change, effective March 30, 2026, follows months of preparation under the ECB’s digital finance and wholesale DLT experimentation agenda, and gives banks a way to post properly structured tokenized assets against central bank liquidity. The decision has quickly become the most discussed topic on Crypto X, in part because one of the early platforms in focus, Axiology, is built using open‑source XRP Ledger code.

The nuance that is driving arguments is simple but politically charged. In documentation and technical clarifications around its collateral framework, the ECB has stressed that using XRP Ledger–based infrastructure “does not imply the use of the public XRP token” and that all eligible collateral must meet existing eligibility and risk‑control criteria regardless of the technology used. That has not stopped XRP‑aligned accounts from trying to spin the development as proof that “XRP is now ECB collateral,” while critics point out that the central bank is explicitly separating the underlying open‑source code base from the freely traded XRP asset tracked on the XRP price page.

Behind the social‑media noise, the policy shift fits into a broader pattern of European experimentation with DLT in wholesale markets. The ECB has run multiple trials on tokenized bonds and central bank money settlement, and has signalled that its collateral framework can be “technology‑neutral” as long as legal, operational and risk standards are met. According to a January discussion that first went viral when X user IOV_OWL highlighted the upcoming change, the new rules open the door for banks to use DLT‑issued securities from approved platforms as if they were conventional collateral, subject to familiar haircuts and eligibility checks.

Market participants say the move could gradually expand eligible pools of repo collateral and support the emerging real‑world asset segment, where tokenized bonds and funds aim to compress settlement cycles and reduce intermediaries. In a previous crypto.news story on tokenization, European pilots of tokenized government bonds were framed as a way to test whether on‑chain settlement can safely plug into the ECB’s monetary operations without undermining stability. Another crypto.news story on RWAs noted that infrastructure built on public‑chain code, including variants of ethereum and XRP Ledger, is increasingly being adapted for permissioned institutional contexts.

For XRP holders, any association between the XRP Ledger and a major central bank is fuel for a long‑running narrative that the token could one day sit at the heart of cross‑border settlement. XRP maximalists on X have seized on Axiology’s architecture to claim that “the ECB now backs XRP,” even as the official documents underline that collateral eligibility is tied to the legal issuer and risk profile of the tokenized security, not to XRP itself.

From a market‑structure perspective, analysts warn that conflating open‑source code usage with token adoption risks misleading investors about what central banks are actually doing. In another crypto.news story on central bank digital currency pilots, legal experts stressed that most wholesale DLT experiments are designed to remain walled off from public tokens such as bitcoin, ethereum or XRP, even when they borrow code or concepts. As the ECB’s framework beds in, the more substantive question will be how quickly volumes in tokenized collateral grow—and whether other central banks follow—rather than how far social‑media narratives can stretch the XRP connection.

Crypto World

Crypto News: Is the Market Dead Again ? While Pepeto Shows High Growth Potential and ETH and XRP Keep Building

Every crash produces the same headline: crypto is dead. The crypto news cycle printed that claim after FTX collapsed, after the 2022 bear wiped $2 trillion, and after Bitcoin fell 50% from its October 2025 high. Wallets that bought during peak fear built the returns the crowd paid a premium for later.

With over $8 million in presale capital and a Binance exchange debut drawing closer, Pepeto offers both real exchange tools and a clear path to early positioning. For anyone tracking crypto news, this presale gives the rare chance to lock in 150x potential before exchange trading begins.

Crypto News Says the Market Is Dead, but Three Events This Week Prove the Opposite

Strategy holds 762,099 BTC purchased for $57.69 billion and added another $76.6 million last week below its own cost basis (CoinDesk).

Square auto enabled Bitcoin Lightning payments for four million merchants on March 30, and BNP Paribas launched six crypto ETNs the same day (LiveBitcoinNews).

Crypto news calling the market dead while the largest corporate buyer, a major payment processor, and Europe’s biggest bank all expand crypto operations in the same week is noise, not signal.

Market Headlines, Presale Capital, and the Entry Fear Is Hiding

Why Pepeto Is the Crypto News Story the Headlines Have Not Written Yet

With the Binance exchange debut drawing closer, Pepeto is emerging as the presale the crowd discovers after the window closes, and committed wallets are already taking notice. Rounds are filling faster than projected, and passing on this entry risks losing the only presale with a confirmed exchange listing and working tools behind it.

Pepeto is not another token built on hype alone. The risk scorer catches scams and surfaces contract problems before a trade costs money, protecting capital the way no meme token has before. Every contract check flows through a transparent verification layer for holders who need answers before the trade, not after the loss.

That protection does not fade when narratives shift. Whether capital chases memes, DeFi, or AI tokens, the demand for contract verification before buying stays constant. That is why Pepeto attracts committed capital even while fear keeps the index at 9. PepetoSwap processes every trade at zero cost across multiple chains, and the bridge connects networks without charging a cent on transfers, both live before the exchange debut. A SolidProof review locked down every smart contract, and a former Binance expert on the dev team secured the exchange path that most presales chase for years without finding.

Staking at 191% APY compounds for wallets inside, building positions while the crypto news audience reads about recovery timelines. For wallets searching for the right entry, this is the moment to act because the presale at $0.000000186 gives the 150x distance from entry to exchange that the Pepe ATH math confirms, and the Binance debut closes that window permanently.

Ethereum (ETH)

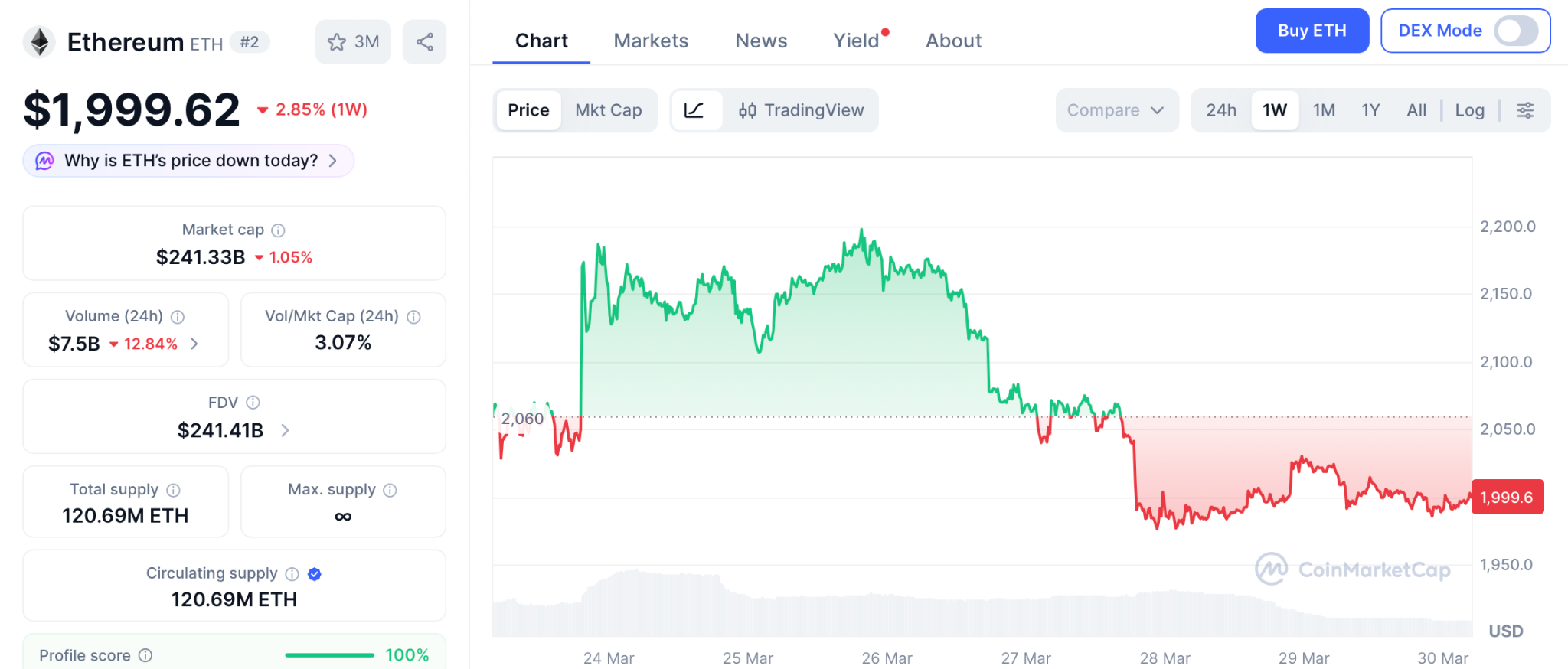

Ethereum trades near $1,999 according to CoinMarketCap, down more than 60% from its October 2025 peak, with the ETH to BTC ratio at multi year lows.

Pectra in April could shift sentiment. Declaring ETH dead ignores $233 billion in market cap, but recovery requires months of rotation the presale entry today does not need.

XRP

XRP holds $1.32 after the SEC classified it as a digital commodity on March 17, ending a five year legal battle (24/7 Wall St).

Spot ETFs hold $1.44 billion in inflows and Standard Chartered targets $2.80 to $8.00. From $1.32 with an $80 billion cap, returns measure in percentages while the presale multiplier measures in multiples.

Crypto News Will Shift From Fear to FOMO, and the Presale Closes Before It Does

With ETH underperforming and XRP waiting for institutional flows, Pepeto is clearly the crypto news entry the market has not priced yet. The listing approaches fast, marking the close of the entry early wallets acted on before the crowd had reason to look.

Searching for answers in the market news led here, and Pepeto through the Pepeto official website is the answer that search was pointing toward because a working exchange backs every token the listing will price.

Over $8 million flowing in during extreme fear proves the investors inside already see where this is going, and the ceiling on a project with real exchange tools has no comparison to anything built on hype alone. The investors who lock in their position before this presale closes are the ones who will remember this exact moment as the day everything changed, and the ones who hesitate will spend the rest of this cycle watching those returns belong to someone else.

Click To Visit Pepeto Website To Enter The Presale

FAQs:

What is the biggest crypto news story right now?

Strategy adding BTC below cost, Square enabling Lightning for four million merchants, and BNP Paribas launching ETNs all in one week proves crypto is expanding, not dying.

Why is Pepeto the crypto news entry to watch this cycle?

Over $8 million committed during extreme fear, the original Pepe cofounder, and a Binance debut make the Pepeto official website the presale institutional products cannot access.

Is it smart to enter crypto during extreme fear?

Every cycle’s biggest returns came from entries made during fear, and Pepeto at presale pricing with a SolidProof audit and exchange tools gives the verified entry serious wallets are choosing.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

The Senate Banking Committee is targeting the week of April 13 for Kevin Warsh confirmation hearing as Federal Reserve chair, citing two sources familiar with the matter.

The timeline puts Warsh on a direct path to replace Jerome Powell before his May 15 term expiration – and it puts a known rate hawk one confirmation vote away from the world’s most influential monetary policy seat.

For crypto traders, that distinction matters.

- Confirmation Timeline: Senate Banking Committee hearing expected the week of April 13, contingent on Warsh completing his paperwork submission; hearing date described as “fluid.”

- Policy Implications: Warsh has publicly called for “regime change” in Fed rate and balance sheet policy, flagging the current Fed’s “hesitancy to cut rates” as a mark against it – signaling a more aggressive easing posture if confirmed.

- Market Signal: Confirmation resistance from Senators Warren and Tillis introduces delay risk; a stalled timeline past May 15 extends policy uncertainty that has historically pressured risk assets including BTC.

Warsh’s Rate Doctrine and What It Means for the Fed’s Next Move

Warsh is not a caretaker appointment.

The 55-year-old served on the Fed’s Board of Governors from 2006 to 2011, the youngest governor in the institution’s history, and helped navigate the 2008 financial crisis. Trump transmitted his dual nomination to the Senate on March 30: a 4-year term as Chairman and a 14-year term as Board Member. This is a structural reshaping of Fed leadership.

Warsh has already signaled the direction. He told CNBC in July that the Fed’s reluctance to cut rates was a mark against them and called for regime change in how the institution manages both rates and its balance sheet. That is not a continuation of Powell’s measured approach. It is an accelerant toward easier policy.

Political resistance is the live variable. Senator Elizabeth Warren is pushing back on structural grounds. Senator Thom Tillis has said he will oppose Fed nominees until a DOJ probe into Powell over renovation expenses at Fed office buildings reaches a resolution. Two opposition holds create a real confirmation drag risk.

For crypto, the directional read is constructive. Elevated Treasury yields have repeatedly compressed Bitcoin valuations during prior tightening cycles.

A Warsh-led Fed pivoting toward faster cuts relieves that pressure structurally. Every week of Senate delay extends Powell’s tenure and preserves the current cautious posture. Traders pricing in a Warsh pivot need to account for both wildcards. A stalled hearing pushes the inflection point into May and compresses the window before Powell’s term expires.

The Fed’s regulatory posture toward crypto is also in play. A new chairman with a mandate for institutional reform could reset how the Fed engages with digital asset firms seeking master account access and regulatory clarity.

Discover: The best pre-launch token sales

What to Watch

The April 13 week is the first hard date on the calendar. Warsh’s paperwork completion is the gating item – any delay in submission slides the hearing and tightens the confirmation window ahead of Powell’s May 15 exit. Watch for the Senate Banking Committee to formally schedule the hearing, which locks in the timeline.

After the hearing, the committee will vote next. A successful committee vote followed by Senate floor scheduling could deliver confirmation by late April. A hold from Tillis – or procedural delay driven by the DOJ-Powell probe – extends the process and leaves rate policy in Powell’s hands past the May deadline. Powell has confirmed he will remain chair until his successor is officially confirmed, meaning there will be no gap. But every day of delay is a day the current rate posture remains in place.

If Warsh clears the committee and reaches a floor vote without holds, confirmation before May 15 is achievable. That outcome would represent the clearest macro catalyst for risk assets – including crypto – since the rate cycle began.

Discover: The best crypto to diversify your portfolio with

The post Fed Nominee Kevin Warsh Confirmation Hearing Expected Week of April 13 appeared first on Cryptonews.

Siren (SIREN) price has surged 109% in 24 hours to a $1.21B cap, up 9,095% from its low, as traders on X argue over “real DeFi” versus a coordinated pump.

Summary

- Siren (SIREN) price has jumped 109% in 24 hours, lifting its market cap to about $1.21 billion with $164.5 million in daily volume, according to CoinGecko.

- The token has now risen roughly 9,095% from its March 2025 all‑time low and is trading near $1.75.

- The move has sparked heated debate on X over whether SIREN is a real DeFi success story or a coordinated pump.

Siren’s SIREN price has exploded into the top‑60 crypto assets by market capitalization after a 109% single‑day gain, putting the project at the center of one of this week’s most polarizing debates on X. CoinGecko data show SIREN changing hands at about $1.75, with a market cap around $1.21 billion and 24‑hour trading volume of roughly $164.5 million, numbers more commonly associated with established DeFi names than relative newcomers. At current levels, the token is up an eye‑catching 9,095% from its March 2025 all‑time low, prompting some traders to draw comparisons with earlier cycle hyper‑performers that went from obscurity to multi‑billion‑dollar valuations in a matter of months.

On X, one of the main threads tracking the move has framed the question bluntly: “Is this an actual DeFi protocol gaining traction, or just another coordinated pump?” That split tone captures the mood in trading circles, where some accounts point to rising on‑chain activity around SIREN’s contracts and liquidity pools, while others note that a large share of volume is concentrated on a small number of venues—often a red flag in past episodes of aggressive, short‑term speculation. For now, concrete protocol metrics remain sparse compared to more established DeFi platforms, leaving traders reliant on price, volume and address growth rather than audited revenue or fee data.

SIREN is marketed as a DeFi‑focused token, with community advocates describing it as part of a new wave of permissionless trading and liquidity tools rather than a meme coin or simple governance wrapper. That puts it, at least thematically, in the same broad category as tokens tied to platforms like Uniswap or GMX, where value is supposed to accrue from trading fees, liquidity incentives and protocol usage. But where those projects publish detailed dashboards and historical metrics, the information around SIREN’s underlying economics and roadmap is still patchy, which helps explain why the X debate has tilted so sharply toward the “pump versus traction” framing.

In previous crypto.news coverage of sudden DeFi rallies, similar patterns have emerged: thin float, concentrated holdings and aggressive social media campaigns can combine with low liquidity to produce triple‑digit daily moves, only for prices to retrace once early buyers take profits. Another crypto.news story on whale‑driven breakouts documented how large wallets moving into and out of small‑cap tokens can amplify these swings, especially when retail traders are chasing green candles without clear fundamentals. A separate crypto.news story on market structure highlighted how fragmented liquidity and high funding rates in derivatives can further magnify upside and downside in these episodes.

With SIREN now sitting near $1.75 and a $1.21 billion market cap, the immediate question is whether the token can sustain its top‑60 status or whether it will follow the pattern of past parabolic moves that faded once attention shifted elsewhere. Traders will be watching for signs of organic growth—such as rising unique users, protocol fees and total value locked—rather than just continued spikes in volume and social mentions. If SIREN does evolve into a genuine DeFi protocol with durable usage, this week’s 109% jump could be remembered as the moment it was “discovered.” If not, it risks joining the long list of tokens whose charts tell the story of a spectacular, but ultimately short‑lived, pump.

President Trump has rescheduled his planned Beijing state visit to May 14–15, 2026, after the escalating Iran conflict forced the White House to pull its diplomatic bandwidth away from US-China diplomacy and toward managing a rapidly deteriorating Middle East crisis. The postponement puts the 2025 trade truce – the architecture holding tariff ceilings and tech export frameworks in place since October – under immediate structural stress.

Beijing’s response has been blunt. Chinese officials, according to reporting by Modern Diplomacy, are operating at what sources describe as “low expectation and zero enthusiasm,” with internal frustration mounting over what they characterize as a pattern of US-initiated delays on high-level engagement. That framing matters because a trade framework without a summit to anchor it is just a handshake agreement – and handshakes expire.

- Postponement Trigger: The Trump Beijing Visit has been rescheduled to May 14–15, 2026, with the White House citing the Iran conflict and Strait of Hormuz volatility as the primary cause for pulling the President’s travel calendar.

- China’s Response: Beijing officials are signaling frustration, describing the delay as part of a pattern of US sidelining – a posture that directly threatens the stability of the Trade Truce 2026 framework negotiated at the October 2025 Busan summit.

- What to Watch: Whether White House planning for the Beijing trip solidifies ahead of May 14, and whether tech CEO intervention keeps EV battery and AI chip supply chain talks on the summit agenda despite the Iran-driven distraction.

Discover: How Iran Deadline Extension Is Weighing on Bitcoin and Risk Assets

What the Beijing Delay Actually Means for Trade Truce 2026

The October 2025 Busan meeting between Trump and Xi – a 90–100 minute session that Trump rated “12 out of 10” – was always understood as the opening act, not the deal itself.

The Beijing state visit was supposed to be the closing ceremony: bilateral commitments on EV battery manufacturing quotas, AI chip export ceilings, and reciprocal tech supply chain disclosures that Busan outlined but never formalized.

None of that gets done over a phone call. The May postponement doesn’t just push dates – it compresses the negotiating window at precisely the moment that Strait of Hormuz disruptions are already squeezing maritime supply chains that run through both US and Chinese manufacturing ecosystems.

Internal leaks cited by Modern Diplomacy describe White House planning for the trip as “scattershot,” with several high-profile tech CEOs reportedly attempting to intervene and keep trade interests on the agenda despite the administration’s Iran-driven distraction.

That is not a healthy diplomatic posture heading into the most consequential bilateral summit of 2026.

The Iran conflict’s direct market mechanics compound the problem. Geopolitical risk-off pressure has already driven BTC below key support levels, as elevated Treasury yields and energy price uncertainty push institutional capital away from risk assets.

A prolonged diplomatic vacuum between Washington and Beijing – two economies accounting for roughly 43% of global GDP – deepens that risk repricing across equity, commodity, and crypto markets simultaneously.

Beijing’s “forever wait” framing is a negotiating signal, not just a complaint. Chinese officials are telegraphing that patience for US-China Diplomacy has a price, and that price is being paid in eroding confidence in the Trade Truce 2026 architecture.

Discover: BTC USD Price Action Under Geopolitical Pressure

What to Watch Before May 14

The critical variable is whether the Iran conflict produces a durable ceasefire or negotiated pause before the rescheduled Beijing dates. If Strait of Hormuz tensions de-escalate sufficiently for the White House to shift diplomatic attention eastward, the May 14–15 summit window holds – and markets will read that as a stabilizing signal for risk assets tied to US-China trade continuity.

If the Iran conflict runs past April with no resolution in sight, the Trump Beijing Visit faces a second postponement. A second delay would almost certainly fracture the goodwill built at Busan and hand Beijing’s skeptics the political argument they need to slow-walk the Trade Truce 2026 implementation. Watch specifically for whether US tech sector lobbying produces any concrete agenda items in White House briefings before May 1 – that’s the deadline by which summit logistics need to be confirmed to hold the May dates.

The summit is still on the calendar. But a calendar entry and a functioning diplomatic framework are not the same thing. Right now, only one of those exists with confidence.

The post Trump’s Beijing State Visit in Doubt as Iran Conflict Drags On appeared first on Cryptonews.

What you get back from a gambling platform matters just as much as what you put in. Bonuses, rakeback, fees, withdrawal speeds, and loyalty perks all determine whether a platform is working for you or just taking your money efficiently. FanDuel dominates the regulated US market with a massive brand and a slick product. ZunaBet is a 2026 arrival that has been picking up steam among crypto gamblers looking for better returns. These two platforms target overlapping audiences but deliver very different experiences. Here is where your money actually goes further.

What FanDuel Offers

FanDuel grew out of daily fantasy sports and became one of the biggest legal sportsbooks and online casinos in the United States. It is owned by Flutter Entertainment and operates under individual state licenses wherever it is available. That regulatory framework gives it legitimacy in the US market but also limits what it can offer depending on where you live.

The sportsbook is one of FanDuel’s strongest assets. It covers NFL, NBA, MLB, NHL, soccer, tennis, golf, MMA, and other major sports with competitive odds and a well-designed betting interface. The mobile app is consistently rated among the best in the industry for speed and usability.

The casino side includes slots, table games, and live dealer options, though the game library is smaller than what many offshore or crypto platforms carry. Available titles depend on the state, and the provider list is more limited than what players on unregulated platforms have access to.

Welcome promotions on FanDuel rotate based on the time of year and the sport in season. Typical offers include no-sweat first bets, bet-and-get promotions, and bonus bet credits. Casino-specific bonuses tend to be more conservative, often topping out at a few hundred dollars in matched play depending on the state. These promotions are fine as introductory offers but do not deliver the kind of value that some competing platforms now provide.

FanDuel handles payments through traditional channels: bank transfers, debit and credit cards, PayPal, Venmo, and similar options. Withdrawal processing can take anywhere from a few hours to multiple business days depending on the method. Some options carry fees.

The rewards program lets players accumulate points through wagering, which can be exchanged for bonus bets or casino credits. It functions as expected but does not offer tiered benefits, escalating returns, or any particularly memorable progression structure.

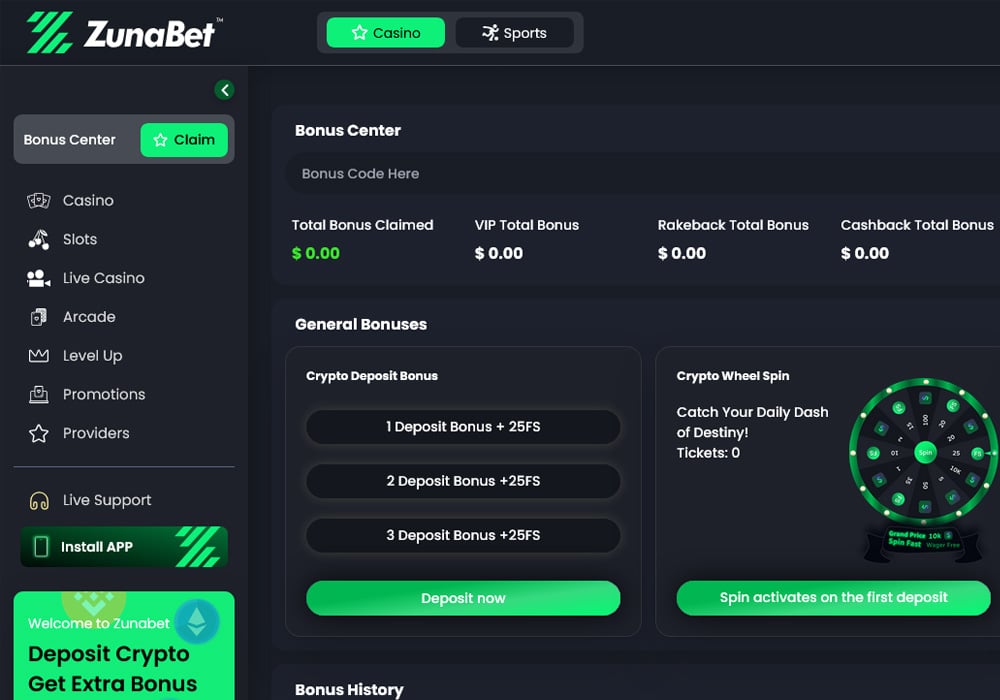

What ZunaBet Offers

ZunaBet went live in 2026. It is owned by Strathvale Group Ltd, carries an Anjouan gaming license, and was constructed by a team with over two decades of collective online gambling experience. The platform was not converted from a fiat casino. It was designed from the ground up with cryptocurrency as the backbone of every transaction.

The game library immediately stands out. Over 11,000 titles from 63 providers are available, spanning slots, RNG table games, and live dealer experiences. Providers include Pragmatic Play, Hacksaw Gaming, Yggdrasil, BGaming, and Evolution. That kind of selection dwarfs what most traditional platforms offer, including FanDuel, where state regulations and a narrower provider list keep the catalog significantly smaller.

Sports betting is fully embedded in the platform. The sportsbook handles football, basketball, tennis, NHL, combat sports, and virtual sports alongside esports markets covering CS2, Dota 2, League of Legends, and Valorant. A single account manages both casino and sportsbook activity, making it simple to move between the two without juggling balances or logins.

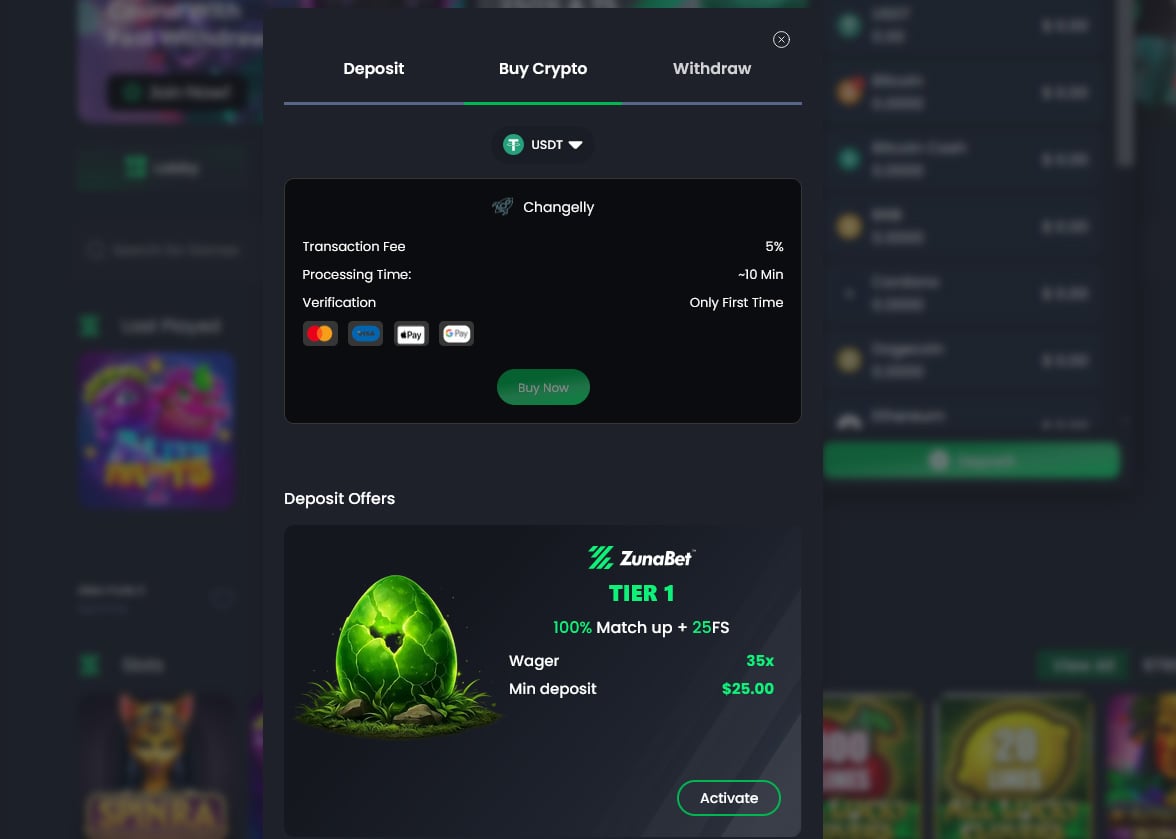

More than 20 cryptocurrencies are accepted: BTC, ETH, USDT across several blockchain networks, SOL, DOGE, ADA, XRP, and others. ZunaBet applies no processing fees on its end, and withdrawals are built to clear fast. Dedicated apps exist for iOS, Android, Windows, and MacOS, with live chat available 24 hours a day.

Bonus Value: Modest vs Generous

FanDuel’s promotions are decent for a regulated platform but modest by broader industry standards. A no-sweat first bet up to $1,000 on the sportsbook side means you get bonus credits back if your initial wager loses, but you do not receive matched deposit funds to play with. Casino welcome bonuses vary by state and typically land in the low hundreds. These offers serve as a nice introduction but do not dramatically extend your bankroll.

ZunaBet opens with a welcome package totaling up to $5,000 plus 75 free spins delivered across three deposits. The first deposit receives a 100% match up to $2,000 and 25 free spins. The second gets a 50% match up to $1,500 and 25 spins. The third gets a 100% match up to $1,500 and another 25 spins. This staggered approach means bonus funds and free spins keep arriving across your first several visits, which encourages continued engagement rather than front-loading everything into one session.

The gap in upfront value is wide. A player looking to maximize their starting position gets meaningfully more from ZunaBet. A $5,000 bonus ceiling with free spins on top is several times what FanDuel typically provides, giving new players far more room to explore games and find their footing.

Long-Term Rewards: Flat vs Progressive

How a platform rewards you after the welcome bonus runs out is where the real financial impact shows up.

FanDuel uses a points-based system. You earn points as you play and redeem them for bonus bets or credits. The structure is flat and predictable in a way that does not offer much upside. There are no major tier jumps, no increasing percentages, and no system that meaningfully rewards you more the longer you stay.

ZunaBet built its loyalty program around a dragon evolution concept with six clearly defined tiers. Squire returns 1% rakeback. Warden returns 2%. Champion returns 4%. Divine returns 5%. Knight returns 10%. Ultimate returns 20%. Free spins increase with each tier up to 1,000 spins. VIP club access and double wheel spins add further value at the higher levels. A dragon character named Zuno ties the whole experience together, making progression feel more like leveling up than collecting generic points.

Every part of ZunaBet’s loyalty program is visible from the day you sign up. Tiers, rewards, and requirements are all laid out clearly. There is no ambiguity and no hidden criteria. At 20% rakeback at the top tier, the long-term return on wagering is substantial. FanDuel’s rewards system does not approach that level of ongoing value for regular players.

The Transaction Gap

Money moving in and out of a platform is where hidden costs live, and this is an area where the two platforms could not be more different.

FanDuel relies on traditional payment infrastructure. Bank transfers, cards, and digital wallets are the available options. Withdrawal times range from same-day for certain methods to several business days for others. Processing fees depend on what you use. Every transaction passes through banking systems and regulatory verification, which adds time and occasionally creates delays, particularly for larger cashouts.

ZunaBet operates entirely on cryptocurrency. Deposits arrive quickly. Withdrawals process without waiting for banks to open. No processing fees are applied by the platform. Supporting over 20 coins, including USDT on multiple blockchain networks, means players can move funds using whichever cryptocurrency is most convenient for them at the time.

Over the course of regular play, these differences compound. A FanDuel player making weekly deposits and occasional withdrawals absorbs transaction delays and potential fees that a ZunaBet player simply does not face. The cost savings and time savings on a crypto-native platform are not dramatic on any single transaction, but they are meaningful over months of play.

Two Platforms, Two Eras

FanDuel is a strong product within its lane. For American players who want a legally regulated sportsbook with a great mobile app and name-brand trust, it delivers. The product is polished, the sportsbook odds are sharp, and the brand carries weight. If operating within the regulated US market is your priority, FanDuel does that job well.

ZunaBet operates outside that regulatory framework but offers more at nearly every other touchpoint. A bigger welcome bonus, a vastly larger game library, broader cryptocurrency support with no fees, faster payouts, and a loyalty program that returns up to 20% rakeback with complete transparency. For players who are comfortable with crypto and want their platform to match how they actually handle money, ZunaBet delivers more tangible value from the first deposit onward.

FanDuel represents where online gambling has been for the past several years — polished, regulated, and built for the fiat world. ZunaBet represents where it is going — crypto-powered, globally accessible, and designed for a new generation of players who measure a platform by how much it gives back rather than how familiar its name is. When the question is where your money goes further, ZunaBet answers it convincingly.

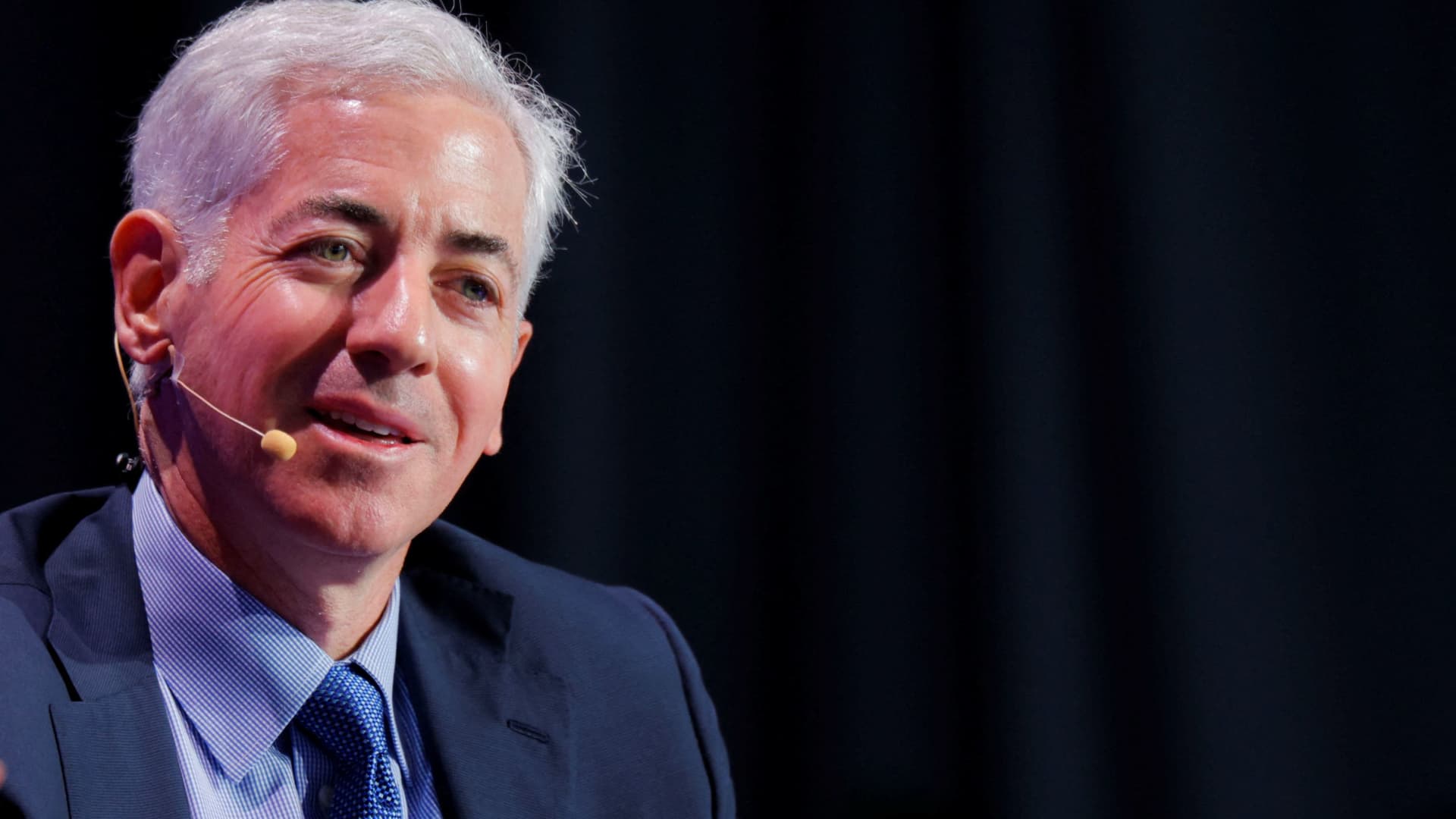

Bill Ackman, founder and CEO of Pershing Square Capital Management, attends the Milken Conference 2025 in Beverly Hills, California, U.S., May 6, 2025.

Mike Blake | Reuters

Billionaire investor Bill Ackman said the current market dislocation has created one of the most attractive entry points for high-quality companies in years, urging investors to look past macro fears and lean into what he sees as deeply discounted opportunities.

“Some of the highest quality businesses in the world are trading at extremely cheap prices,” Ackman wrote in a post on X late Sunday. “One of the best times in a long time to buy quality. Ignore the bears.”

The founder of Pershing Square Capital Management pointed to what he described as a highly asymmetric setup in select names, singling out U.S. mortgage giants Fannie Mae and Freddie Mac as “stupidly cheap,” with the potential to deliver outsized returns in a relatively short period.

Ackman’s bullish stance comes at a time when markets have been rattled by rising energy prices, sticky inflation concerns and shifting expectations around Federal Reserve policy. The recent bout of volatility has pushed valuations lower across a range of sectors, even as economic uncertainty continues to cloud the outlook.

“One of the most one-sided wars in history that will end well for the U.S. and the world. And we have the potential for a large peace dividend,” Ackman wrote.

President Donald Trump offered investors hope that an end to the war against Iran is drawing near. While the president added that “great progress has been made,” he also said that if a peace deal is not reached “shortly” and the Strait of Hormuz is not “immediately” reopened, the U.S. would attack key Iranian energy infrastructure.

Pershing Square Holdings, the firm’s London-listed closed-end fund, is down 19% year to date as of last Tuesday, its website showed.

Earlier this month, Pershing Square filed to list on the New York Stock Exchange under the ticker “PS,” a move that would give public investors direct exposure to the firm’s concentrated portfolio of large-cap investments.

The listing would effectively turn Ackman’s investment vehicle into a permanent capital structure, echoing the model used by Warren Buffett‘s Berkshire Hathaway.

Zcash’s (ZEC) upside hinges on a repricing of financial privacy in an AI-driven world, Grayscale says

Poverty can’t be solved by lifting the two-child benefit cut alone

IS XRP ABOUT TO CRASH HARD?!?! (I HAVE THE DATA)

-

NewsBeat5 days ago

NewsBeat5 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

News Videos5 days ago

News Videos5 days agoParliament publishes latest register of MPs’ financial interests

-

NewsBeat3 days ago

NewsBeat3 days agoThe Story hosts event on Durham’s historic registers

-

Business4 days ago

Business4 days agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

NewsBeat5 days ago

NewsBeat5 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Tech7 days ago

Tech7 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

Entertainment2 days ago

Entertainment2 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Fashion6 days ago

Fashion6 days agoDoes It Matter What You Wear When You’re Laid Off and Looking?

-

Business6 days ago

Business6 days agoMore women enter wealth management, but few in advisory roles: study

-

Politics7 days ago

Politics7 days agoHow Media Platforms Balance Performance and Accessibility in Image Delivery

-

Tech4 days ago

Tech4 days agoIntercom’s new post-trained Fin Apex 1.0 beats GPT-5.4 and Claude Sonnet 4.6 at customer service resolutions

-

NewsBeat6 days ago

NewsBeat6 days agoNASA Artemis II Astronauts enter 14-Day quarantine as moon rocket reaches launchpad

-

Business6 days ago

Business6 days agoLate-paying firms face multimillion-pound fines under new crackdown

-

NewsBeat6 days ago

NewsBeat6 days agoEntrepreneurs Forum survey reveals optimism in North East

-

Tech6 days ago

Tech6 days agoEmbedding compliance in AI adoption

-

Sports5 days ago

Sports5 days agoFantasy Baseball Week 1 Preview: Top sleeper hitters for both five- and 12-day period led by Munetaka Murakami

-

Tech5 days ago

Tech5 days agoUS FCC Prohibits Approval Of New Foreign-Made Consumer Routers

-

Crypto World6 days ago

Crypto World6 days agoBTC gives up $70,000 level as markets mull higher interest rates

-

Fashion6 days ago

Fashion6 days agoCoffee Break: Korean Skincare Set

-

Fashion6 days ago

Fashion6 days agoAlthea Mink: Patrice Taylor’s Atlanta Couture Brand Built on Legacy, Resilience, and Architectural Glamour

You must be logged in to post a comment Login