Crypto World

Chainlink Holder Count Nears 900K as Wallet Growth Picks Up

TLDR:

- Chainlink holder count climbed to 892.8K Ethereum wallets after adding more than 8K holders in five days.

- Recent wallet growth accelerated sharply and pushed LINK closer to the 900K holder milestone.

- Santiment linked the increase to growing interest in tokenized assets and institutional blockchain projects.

- LINK holder growth continued even while the token traded near recent local price lows.

Chainlink has surpassed another important adoption milestone amid the recent surge in wallet growth over the last few days. The network now has 892,800 non-empty Ethereum wallets, which have swelled by over 8,000 in the last five days, according to fresh on-chain data.

The boost is part of a growing spotlight on the crypto market on tokenized assets and institutional blockchain projects. Despite LINK trading near recent lows, the latest stats suggest more people are joining the network.

Chainlink Holder Count Rises as More Wallets Join the Network

On-chain analytics platform Santiment reported that Chainlink’s holder count has entered a much steeper growth phase. The platform tracks non-empty Ethereum wallets holding LINK.

Its latest data shows the network added more than 8,000 holders over five days. That pushed the total number of wallets holding LINK to roughly 892,800.

The recent increase stands out from previous growth trends. According to Santiment, Chainlink could move beyond the 900,000-holder mark before the week ends if the current pace continues.

Holder growth remains one of the clearest ways to measure network adoption. A larger holder base often reflects increasing participation across an ecosystem, regardless of short-term market movements.

While price often attracts the headlines, wallet data can tell a different story. In Chainlink’s case, more users continue entering the network even as LINK remains close to recent local lows.

Institutional Blockchain Activity Keeps Chainlink in Focus

Santiment linked the recent wallet expansion to several developments involving real-world assets and institutional finance.

These include Project Pangea, DTCC’s collateral initiatives, tokenized assets, and 24/5 equity data streams.

Chainlink has become part of a growing number of blockchain projects supporting tokenized financial infrastructure.

Its oracle network provides external data that decentralized applications and financial platforms rely on. The latest wallet figures arrived during a period when institutional blockchain projects continue expanding.

Real-world asset tokenization has also remained one of the industry’s most active development areas throughout the year.

Although LINK has yet to stage a major price recovery, wallet growth has continued moving higher.

Santiment noted that the increase in holders has taken place while the token trades near local lows, suggesting network participation continues to build despite subdued market conditions.

Chainlink’s expanding holder base adds another metric to watch as adoption develops across the ecosystem. The latest on-chain figures show users continue accumulating LINK while institutional blockchain and tokenized asset initiatives remain active across the broader crypto market.

For years the XRP community has promised that XRP would flip SWIFT, the messaging network behind global banking. In 2026 the reality is stranger than the slogan. SWIFT is building its own blockchain ledger that pointedly leaves XRP out, even as XRP gets wired into SWIFT through a side door.

Summary

- The long-running claim that XRP will replace SWIFT has given way to a more complicated 2026 reality in which the two systems both compete and connect.

- SWIFT is a messaging network used by more than 11,000 institutions to move trillions of dollars a day, and it completed its migration to the ISO 20022 data standard in late 2025 and is now building its own blockchain shared ledger.

- That SWIFT ledger deliberately excludes public-network assets like XRP, keeping settlement in tokenized bank deposits, which undercuts the idea that XRP becomes the settlement rail.

- At the same time, a SWIFT integration with the payments firm Thunes gives banks optional access to Ripple’s liquidity products, including XRP as a bridge asset, so XRP is wired in as an option rather than a requirement.

- Ripple itself has hedged by pushing its RLUSD stablecoin as speed without volatility, pointing toward a future where XRP is one optional liquidity leg in a fragmented, interoperable system rather than the network that replaces SWIFT.

The single most durable promise in the XRP community is that XRP will one day replace SWIFT, the messaging network that sits behind nearly every international bank transfer on earth. It is a powerful story, the idea that a fast, cheap digital asset will sweep away a slow, decades-old system and capture the enormous value flowing through global payments, and it has motivated XRP holders for years. The trouble is that the story has always blurred two very different things: SWIFT, which is a messaging system that tells banks how to move money, and XRP, which is an asset that can actually move value.

In 2026, the relationship between the two has become more interesting and more complicated than the slogan suggests. SWIFT is not standing still, having finished a major data-standard overhaul and begun building its own blockchain ledger. Ripple, for its part, has quietly softened its rhetoric from replacing SWIFT to complementing it, and has hedged its own bets by leaning into a dollar stablecoin alongside XRP. The blunt replacement narrative no longer fits the facts.

What makes the question genuinely worth examining now is that both systems are making concrete moves that reveal how they actually see each other. SWIFT has built a blockchain ledger that deliberately leaves XRP out, a telling choice. Yet through a separate integration, XRP has been wired into SWIFT as an optional liquidity tool, an equally telling choice in the other direction.

The result is neither the clean replacement the bulls predicted nor the irrelevance the skeptics expected, but something messier: a fragmented, interoperable landscape in which XRP is one option among several, available but not required. This piece works through what SWIFT actually is and what Ripple actually built, the reality behind the ISO 20022 hype, SWIFT’s own blockchain project and why it excludes XRP, the side door through which XRP gets connected anyway, Ripple’s pivot toward its stablecoin, and an honest verdict on whether XRP is complementing the banking network or replacing it. The answer matters because so much of the XRP investment case rests on which of those two things is true.

What SWIFT actually is, and is not

To judge the rivalry clearly, you have to be precise about what SWIFT does, because the replacement narrative often gets this wrong. SWIFT is not a payment system that moves money; it is a messaging network that moves instructions about money. When a bank in one country needs to send funds to a bank in another, SWIFT carries the standardized message that says, in effect, pay this amount to this account.

The actual money moves separately, through the banks’ own accounts and the correspondent banking system. More than eleven thousand financial institutions use SWIFT, and the value of payments it helps coordinate runs into trillions of dollars every day, which makes it the central nervous system of cross-border finance. It is, above all, a trusted standard and a network, deeply embedded in how banks talk to one another.

The weaknesses the replacement narrative points to are real, but they live in the settlement layer beneath SWIFT, not strictly in SWIFT itself. Because a cross-border payment often hops through a chain of correspondent banks, each holding pre-funded accounts in various currencies and each taking a fee and adding delay, the traditional process can take one to three business days and is closed on weekends and holidays. A payment from Japan to Brazil might pass through three or four intermediaries before arriving.

SWIFT has worked to improve this. Its gpi service, launched in 2017, sped things up so that a large share of payments now credit within thirty minutes and effectively all within a day, with tracking along the way. But gpi modernized the messaging and tracking without changing the underlying correspondent-banking architecture, which still relies on pre-funded accounts and intermediaries. So SWIFT is best understood as the messaging and standards layer of a settlement system whose plumbing is slow, and the question is whether a blockchain alternative can replace that plumbing, the messaging layer, or both.

What Ripple actually built

Ripple’s pitch is aimed squarely at the settlement plumbing, and understanding its core product clarifies where XRP fits. Ripple is a blockchain financial-technology company built around the XRP Ledger, and its enterprise network, historically called RippleNet, lets financial institutions send payments to one another more directly than the correspondent system allows.

The mechanism that actually involves XRP is called On-Demand Liquidity, or ODL, and it is the heart of the XRP value proposition. Instead of a bank pre-funding accounts in every destination country, ODL converts the sending currency into XRP on a crypto exchange, moves that XRP across the XRP Ledger in three to five seconds, and converts it into the destination currency on the other side. The XRP acts as a bridge asset, a momentary carrier of value between two currencies, which removes the need for the expensive pre-funded accounts that slow the traditional system.

The advantages are concrete. An XRP Ledger transaction settles in seconds rather than days, costs a fraction of a cent, and runs around the clock, including weekends, with the network having processed billions of transactions cumulatively and supported tens of billions of dollars in liquidity volume. For a bank or payment provider, ODL promises to free up the capital that would otherwise sit idle in pre-funded foreign accounts, while settling far faster.

This is the genuine innovation behind the XRP thesis: not a new messaging standard, but a new way to handle the settlement leg, using a digital asset as a bridge so value can move without the correspondent-banking overhead. Whether this complements SWIFT or replaces it depends on whether banks adopt the bridge for the settlement leg while keeping SWIFT for messaging, or whether something more wholesale occurs. And as the rest of this piece shows, the 2026 evidence points firmly toward the former.

The ISO 20022 reality check

No discussion of Ripple versus SWIFT is complete without addressing ISO 20022, because few topics generate more confusion and hype in the XRP community. ISO 20022 is a global standard for the format of financial messages, replacing older, less structured message types with a richer format that carries far more data, such as detailed remittance information, compliance data, and structured identifiers.

It improves automation, transparency, and anti-money-laundering monitoring, and it has become the common language toward which the world’s major payment systems are migrating. SWIFT completed its full migration to ISO 20022 in November 2025, ending the long coexistence with legacy message types, a genuine milestone for global finance.

Here is where the confusion sets in. A persistent claim in XRP circles holds that XRP is ISO 20022 compliant in a way that guarantees it a central role once banks adopt the standard. The reality is more limited. Ripple did join the ISO 20022 standards body, becoming one of the first blockchain firms to do so, and RippleNet is built to send and receive ISO 20022 messages, which lets it interoperate cleanly with banks using the standard.

That is a real advantage for Ripple’s network. But the XRP token itself is not ISO 20022 certified, because ISO 20022 standardizes messaging formats and does not certify cryptocurrencies or blockchains at all. The standard governs how payment information is structured, not which asset settles a payment. So while RippleNet’s compliance gives Ripple a seat at the table and makes integration easier, the idea that ISO 20022 anoints XRP as the chosen settlement asset is a misreading.

The standard raises the bar for every payment solution, traditional or crypto, and SWIFT, as the established messaging hub that helped shape the standard, arguably benefits at least as much as Ripple does. ISO 20022 is a prerequisite for interoperability, not a victory for any single token.

SWIFT is not standing still

The replacement narrative tends to picture SWIFT as a static, aging incumbent waiting to be disrupted, but the 2026 reality is that SWIFT is actively building its own path into the blockchain era. After completing the ISO 20022 migration, SWIFT moved on to a more ambitious project: a blockchain-based shared ledger designed to enable round-the-clock cross-border settlement. Having run trials since 2025 with a group of more than forty banks, SWIFT completed the design phase of this ledger in early 2026 and began building its first working version, with the aim of processing real transactions before the end of the year.

The ledger is permissioned and compatible with common smart-contract tooling, and it is tied closely to the ISO 20022 messaging SWIFT already runs, so banks can plug into it through SWIFT’s trusted infrastructure instead of adopting an entirely new public blockchain.

Crucially, SWIFT has been explicit that this is about extending its existing role, not handing the rails to a competitor or issuing new money. Its chief innovation officer framed the effort as preserving settlement in central-bank money, commercial-bank money, or tokenized deposits, while adding the ability to lock in commitments, execute complex cross-border transactions atomically, and share a single auditable record across networks. In other words, SWIFT wants to keep value inside the regulated banking system while gaining the speed and programmability of a blockchain.

To get there, it has been stress-testing nearly every digital-asset rail available, running trials with major banks on tokenized deposits, tokenized bonds, and stablecoins, including a March 2026 interoperability trial that tested several stablecoins. The picture this paints is not of an incumbent asleep at the wheel, but of a network methodically absorbing blockchain technology into its own infrastructure, on its own terms, while keeping its central position as the orchestrator of global banking. That ambition sets up the most consequential detail for XRP holders.

The detail XRP holders cannot ignore

If SWIFT is building its own blockchain ledger, the obvious question for the XRP thesis is whether XRP is part of it, and the answer, pointedly, is no. SWIFT’s shared-ledger project is designed around tokenized bank deposits in currencies such as dollars, euros, and Canadian dollars, transferred between banks under the same regulations that govern wires, and it deliberately avoids public-network assets like XRP.

The design principle is that no value should escape regulated accounts, so reaching a public-ledger asset would require an additional step outside the system’s perimeter, a step the project intentionally does not take. SWIFT’s ledger is permissioned and built for the control and auditability that central banks and supervisors demand, which is precisely the opposite of XRP’s open, public network.

This is a genuinely important development that much of the bullish commentary glosses over. If banks get the round-the-clock, blockchain-based settlement they want from SWIFT’s own ledger, using tokenized deposits they already trust and within the regulated perimeter they are comfortable with, then a significant part of the problem ODL was meant to solve gets solved without XRP. SWIFT is, in effect, building a competitor to the settlement innovation that underpins the XRP thesis, and building it in a way that keeps XRP out by design.

For an XRP holder, this should temper any expectation that banks will inevitably route settlement through XRP simply because blockchain is faster. The institutions have a path to blockchain settlement that does not touch XRP at all, offered by the network they already use and trust. That does not mean XRP is shut out of the banking system entirely, because there is a side door, but it does mean the headline rail SWIFT is building is, by deliberate choice, an XRP-free one.

The side door: how XRP gets wired in anyway

The story has another turn, because even as SWIFT’s own ledger excludes XRP, XRP has been connected to SWIFT through a separate channel, and understanding this optionality is essential to an honest verdict. Through an integration involving the payments firm Thunes, the more than eleven thousand banks on the SWIFT network gain optional access to Ripple’s liquidity products, including XRP as a bridge asset.

The routing works in sequence: a company sends a payment via SWIFT, SWIFT can route it through Thunes, Thunes offers access to Ripple’s ODL infrastructure, and XRP settles that leg. The critical word in that sequence is optional. No step forces a bank to use XRP; the connection makes XRP available as one liquidity choice among others, not a mandated part of the flow.

This optionality is structurally meaningful, but it is a double-edged thing for XRP holders, and the distinction matters enormously for how to read the narrative. On one hand, being wired into SWIFT, even optionally, gives XRP distribution at a scale it could never reach through Ripple’s direct partnerships alone, putting an XRP settlement option in front of thousands of institutions. On the other hand, optional access creates demand optionality, not guaranteed volume.

The banks can use the XRP rail, but nothing compels them to, and many will default to the rails and assets they already know. So the SWIFT connection is real and potentially valuable, but it is a long way from the mandatory, network-wide adoption the replacement narrative imagined. The accurate way to hold it is that XRP now has a foot in the door of the world’s dominant banking network, as one option a bank can choose, while SWIFT simultaneously builds its own settlement ledger that bypasses XRP. Both things are true at once, which is exactly why the simple replace-or-die framing fails.

Ripple’s own pivot tells the story

Perhaps the clearest signal about whether XRP is replacing SWIFT comes from Ripple itself, which has been quietly repositioning in a way that speaks volumes. Alongside its push for XRP-based settlement, Ripple has been aggressively advancing its dollar-pegged stablecoin, RLUSD, and the rationale reveals how Ripple now sees the landscape.

RLUSD is fully reserved with cash and short-term government securities, audited regularly, and positioned as enterprise-grade infrastructure that offers the speed of blockchain rails without the price volatility of XRP. In effect, Ripple is offering banks and payment firms stablecoin-as-a-service: a way to get fast, programmable settlement while holding a stable dollar value instead of a fluctuating token. This directly complements SWIFT’s own tokenized-deposit strategy instead of trying to overthrow it.

The significance of this pivot is hard to overstate for the replacement debate. A company that truly believed XRP was on the verge of replacing SWIFT and capturing all that settlement value would have little reason to build a competing stablecoin product that settles without XRP. Ripple is hedging, building rails that work whether or not banks choose XRP, because it understands that enterprises often want stability over a bridge asset and that the future is more likely to be a fragmented mix of instruments than a single winner.

This is the same complementary posture Garlinghouse has signaled in softening from earlier replace-SWIFT rhetoric toward language about Ripple complementing existing systems. Ripple, in other words, has read the room. It is positioning itself as a provider of modern settlement infrastructure, of which XRP is one component and RLUSD is another, instead of betting everything on XRP displacing the incumbent network. When the company most invested in XRP’s success diversifies away from pure-XRP settlement, holders should take note of what that says about the realistic ceiling of the replacement thesis.

Complement or replace: the honest verdict

So where does this leave the question at the heart of the matter? The honest verdict is that XRP is complementing the banking network far more than replacing it, and that the 2026 evidence has largely retired the clean replacement narrative. The landscape that is actually forming is not winner-takes-all but fragmented and interoperable, a world in which several systems coexist and connect instead of one sweeping the others away.

SWIFT retains its position as the standards-setter and messaging hub of global finance, and it is extending that position into blockchain on its own terms, with a settlement ledger that keeps value inside the regulated banking system and deliberately excludes XRP. Ripple, meanwhile, controls a suite of modern settlement tools, including the XRP Ledger, the optional XRP bridge liquidity now reachable through SWIFT, and the RLUSD stablecoin, and it is selling all of them into a market that increasingly wants choice instead of a single rail.

Within that landscape, XRP’s realistic role is as one optional liquidity leg among many, valuable where it is chosen but never mandated, available to thousands of institutions through the SWIFT connection yet competing against tokenized deposits, stablecoins, and SWIFT’s own XRP-free ledger for each transaction. That is a meaningful role, and it is not nothing: a foot in the door of global banking, with genuine speed and cost advantages, is a real asset. But it is a long way from the world the slogan promised, in which XRP becomes the settlement rail of international finance and captures the value flowing across it.

For holders, the practical takeaway is to replace the binary replace-or-die framing with a more accurate one. XRP’s banking future is about optionality and adoption rates: how often institutions actually choose the XRP rail when given the option, and whether ODL volume grows enough to matter against the token’s large supply. The replacement dream made XRP a bet on inevitability. The complementary reality makes it a bet on competition, in which XRP must win each transaction against capable rivals, including the incumbent it was supposed to replace. That is a more sober thesis, but it is the one the facts now support.

Frequently Asked Questions

Is XRP going to replace SWIFT?

The 2026 evidence strongly suggests no, at least not in the wholesale way the community long predicted. SWIFT is a messaging network used by over eleven thousand institutions, and instead of being swept away, it has modernized, completing its ISO 20022 data-standard migration and building its own blockchain settlement ledger. That ledger deliberately excludes XRP, keeping value in tokenized bank deposits. XRP has been connected to SWIFT optionally through a Thunes integration, giving banks access to XRP as one liquidity choice, but participation is not required. The realistic picture is XRP complementing the banking network as one optional settlement tool, not replacing the network that coordinates global payments.

What is the difference between SWIFT and Ripple?

SWIFT is a messaging network that carries standardized instructions about payments between banks; it does not move the money itself, which travels separately through correspondent banking. Ripple is a blockchain company whose On-Demand Liquidity product actually moves value, converting a sending currency into XRP, moving it across the XRP Ledger in seconds, and converting it to the destination currency, which removes the need for pre-funded accounts. So SWIFT is primarily the messaging and standards layer, while Ripple targets the settlement layer beneath it. They operate at different points in the payment process, which is part of why they can complement each other instead of being pure substitutes.

Is XRP ISO 20022 compliant?

This is widely misunderstood. RippleNet, Ripple’s payment network, is built to handle ISO 20022 messages and Ripple joined the standards body, which helps its network interoperate with banks adopting the standard. But the XRP token itself is not ISO 20022 certified, because ISO 20022 is a messaging-format standard that does not certify cryptocurrencies or blockchains at all. It governs how payment data is structured, not which asset settles a payment. So the popular claim that ISO 20022 guarantees XRP a central role is a misreading. The standard raises the bar for all payment solutions and arguably benefits SWIFT, the established messaging hub, at least as much as it benefits Ripple.

Does SWIFT’s blockchain ledger use XRP?

No, and this is one of the most important developments for XRP holders. SWIFT’s blockchain shared ledger, which moved into its building phase in 2026, is designed around tokenized bank deposits and deliberately avoids public-network assets like XRP. It is permissioned, keeps value inside regulated accounts, and is built for the control and auditability central banks require. This means SWIFT is creating a path to round-the-clock blockchain settlement that does not involve XRP, solving much of the problem ODL was meant to address without the token. Banks wanting blockchain settlement have an XRP-free option from the network they already trust, which meaningfully tempers the case for inevitable XRP adoption.

How does XRP connect to SWIFT then?

Through a separate integration involving the payments firm Thunes. The arrangement gives the more than eleven thousand banks on SWIFT optional access to Ripple’s liquidity products, including XRP as a bridge asset. A payment can route from SWIFT through Thunes to Ripple’s ODL infrastructure, where XRP settles the leg. The key point is that this access is optional, not mandated. It gives XRP exposure to a vast network of institutions, which is truly valuable for distribution, but it creates demand optionality instead of guaranteed volume, since banks can choose the XRP rail but are never forced to use it over the alternatives available to them.

What does this mean for XRP’s value?

It reframes the XRP thesis from inevitability to competition. The replacement narrative implied XRP would automatically capture global settlement value; the complementary reality means XRP is one optional liquidity tool that must win each transaction against tokenized deposits, stablecoins, including Ripple’s own RLUSD, and SWIFT’s XRP-free ledger. XRP retains real advantages in speed, cost, and round-the-clock settlement, and its optional presence on SWIFT gives it broad distribution. But its value will depend on how often institutions actually choose the XRP rail and whether that volume grows enough to matter against XRP’s large supply, instead of on a wholesale replacement of SWIFT that the current evidence does not support.

This article is information, not investment advice. Details of SWIFT’s and Ripple’s products, integrations, and strategies reflect reporting available as of June 27, 2026, and can change. The competitive landscape in cross-border payments is evolving quickly. Nothing here is a recommendation to buy or sell XRP or any asset. Verify current details from primary sources and consider your own circumstances before making any decision.

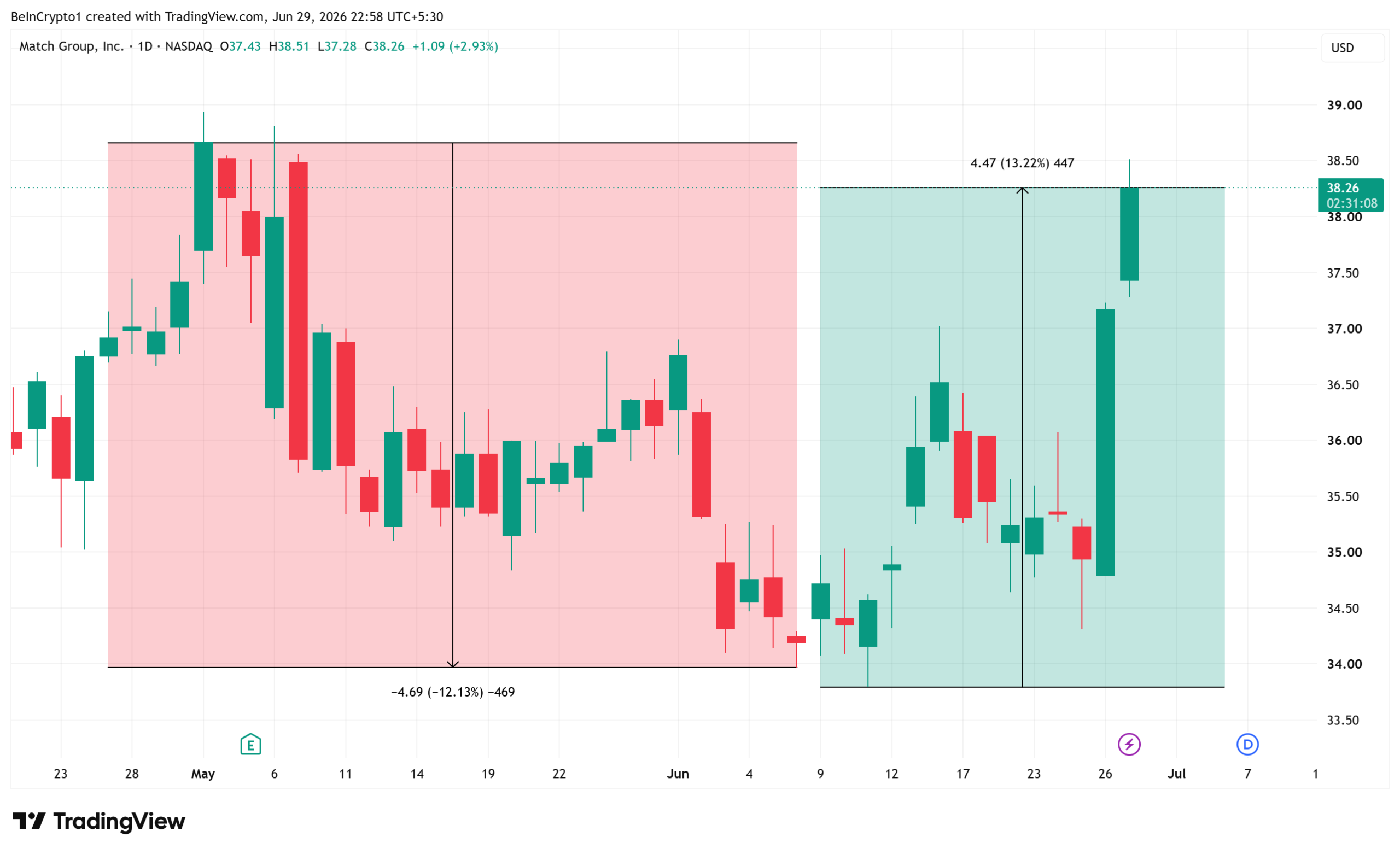

The most profitable World Cup trade this month was not a Polymarket bet on Spain or France. It was a Tinder boom that helped lift Match Group (MTCH) stock.

The stock had slumped about 12% before the tournament began on June 11. It has since climbed roughly 13%, erasing those losses and pushing back near its highs for the year.

Prediction Markets Grabbed the Headlines

Sports betting drove most of the World Cup money story. On Polymarket, the tournament winner market has drawn hundreds of millions of dollars in wagers, with Spain and France the narrow favorites.

The buzz around World Cup prediction markets was easy to see. Sector open interest hit a record $1.48 billion in mid-June as fans piled into match outcomes.

Yet the smarter equity trade ran through dating apps. Match Group, the parent of Tinder and Hinge, watched its shares rebound as fresh engagement data reached investors.

Inside Tinder’s World Cup jump

Tinder logged its gains in the tournament’s first six days, from June 11 to 16. Compared with June 2025, US matches jumped almost 60%, while total users rose 15%.

Follow us on X to get the latest news as it happens

Across the 16 host cities in the United States, Mexico, and Canada, activity from international fans climbed 47%, according to data reported by Fast Company. The figures track the influx of traveling supporters.

That timing mattered. The data circulated in late June, just as Match Group shares closed at $37.17 on June 26 after a 6.4% jump.

The Quieter World Cup Trade

The rebound lands on a longer turnaround story. Tinder had shed users for nearly two years, drawing activist investors Elliott Investment Management and Starboard Value, who pushed for change and a new chief executive.

In March, Tinder registrations returned to year-over-year growth for the first time in almost two years, while Hinge revenue grew 28%. New CEO Spencer Rascoff framed the shift in the company’s first-quarter results.

Tinder works better today than it did before. Our product changes are resonating with Gen Z and driving improvements in leading indicators.

A World Cup engagement bump fits that narrative, which is why investors rewarded it. While bettors split their money between Polymarket and Kalshi, Match Group offered a calmer way to trade the same event.

Even so, the average analyst target sits near $40, a consensus Moderate Buy that leaves limited room above current levels.

The caution is in Match Group’s own numbers. Tinder paying users still fell 5% in the first quarter, so engagement has not yet become revenue.

With the final set for July 19, the test is whether the swiping outlasts the tournament. A few traders banked millions on Polymarket, but the cleaner bet was the stock.

The post The Hottest World Cup Trade Wasn’t Sports Betting, It Was Tinder appeared first on BeInCrypto.

The EU’s Markets in Crypto-Assets Regulation (MiCA) is now shaping crypto licensing across Europe—but the rollout is uneven, with some jurisdictions moving quickly while others are still absent from the authorization map. According to an ESMA interim register compiled on Friday, Germany has issued the largest number of MiCA authorizations so far, even as the new EU framework begins to take effect this Wednesday.

ESMA’s data shows Germany has approved 57 crypto-asset service providers (CASPs) under MiCA. That figure represents about 23% of the 244 total MiCA licenses issued across the EU and EEA jurisdictions tracked in the register. France is next, with 26 CASP authorizations (around 11% of the total), placing it alongside the Netherlands as one of the bloc’s leading hubs for late-June licensing.

Key takeaways

- Germany leads MiCA authorizations: 57 CASPs approved—roughly 23% of all licenses reported in ESMA’s interim register.

- France accelerated late-June: five CASP approvals between June 18 and June 22, the highest in that specific window among the jurisdictions listed.

- Several EU states have yet to issue any MiCA licenses: ESMA interim data indicates Greece, Hungary, Poland, Portugal, and Romania reported zero authorizations as of June 26.

- Fragmentation persists before the July 1 transition deadline: implementation speed varies, despite MiCA’s aim to standardize rules across the EU.

- Regulator expectations differ: Germany’s BaFin said it is difficult to predict whether Germany’s dominance will hold as other countries’ processes mature.

Germany’s licensing lead—and what BaFin says explains it

Germany’s dominant share of MiCA-approved CASPs comes at a time when the market is preparing for MiCA’s July 1 transitional deadline. BaFin, Germany’s financial regulator, told Cointelegraph that the country’s comparatively high number of authorizations is influenced by the size of its financial sector. BaFin specifically pointed to the presence of many credit institutions, which can provide crypto-asset services under MiCA.

BaFin also highlighted a second factor: Germany’s earlier national licensing regime. Under MiCA transition rules, some providers were able to rely on simplified authorization pathways, which may have helped accelerate approvals compared with jurisdictions without the same pre-existing structures.

However, BaFin cautioned against assuming Germany will keep leading indefinitely. The regulator said it is difficult to forecast whether Germany’s dominant share will remain as MiCA implementation progresses. BaFin noted that outcomes will depend on broader market developments, innovation patterns, and the number of pending applications in each member state. It added that authorizations in other EU countries are expected to rise over time, generally tracking the size of their national financial sectors.

France pushes a late-June approval wave

While Germany leads overall, France’s recent behavior stands out for speed. ESMA interim data indicates France issued five CASP approvals between June 18 and June 22—more than any other jurisdiction in that window. In total, 11 approvals were reported across EU and EEA jurisdictions during the June 18 to June 22 period, with Malta following France with two authorizations.

Among the CASPs included among France’s approvals were Bpifrance Investissement, RCUBE Asset Management, Paymium, Leonod, and Meria.

The late-cycle rush in France matters because MiCA’s enforcement timeline is compressing the window for firms that want a fully authorized operating environment under the new regime. Even where the rules are harmonized at EU level, differences in how quickly regulators process applications can translate into real competitive advantages for providers that secure approvals earlier.

Not all jurisdictions are moving at the same pace

ESMA interim register data also shows that MiCA licensing has not yet reached every part of the EU. Five EU member states—Greece, Hungary, Poland, Portugal, and Romania—had issued no MiCA licenses as of June 26, according to ESMA.

Greece is particularly notable because Binance had applied for authorization in the country but later withdrew its application, shifting its licensing plans to another MiCA jurisdiction. (Earlier coverage from Cointelegraph reported both the application and the subsequent withdrawal.)

Poland presents a different dynamic. ESMA’s data leaves the country without a MiCA licensing framework by the time of the EU deadline, and Cointelegraph previously reported that delays in MiCA implementation legislation were followed by three reported presidential vetoes—contributing to uncertainty around the timing of regulatory readiness.

This kind of patchwork rollout underscores an important point for market participants: MiCA is intended to create a single EU-wide market framework, but regulatory capacity, domestic legislative timing, and transitional mechanics are still producing uneven outcomes. That mismatch is likely to remain a meaningful factor for businesses choosing where to seek authorization and for traders assessing which platforms may have smoother compliance paths in the run-up to full application of the rules.

Italy’s non-compliant register dominates—while others show sparse entries

Alongside the list of approved CASPs, ESMA also maintains a separate view of CASPs that are considered non-compliant. In that register, Italy dominates by far, accounting for 160 out of 162 entries as of Friday. By comparison, the Netherlands and Slovakia recorded one entry each, linked to MEXC and LWEX, respectively.

While the approved-license figures show where regulators are actively issuing authorizations, the composition of the non-compliant register hints at how unevenly firms are positioned to meet MiCA requirements—either because they are still in process, facing compliance gaps, or operating under different transitional assumptions. For providers, the practical question becomes how quickly regulators can move from non-compliant listings to approvals—and what guidance will narrow compliance uncertainty.

As MiCA’s effects roll in, the main uncertainty is whether Germany and France’s early momentum will persist or whether the authorization map will broaden as other regulators scale their processes. Readers should watch for changes in ESMA’s interim register in the days following the regime’s effective date, particularly which of the currently inactive jurisdictions begin issuing CASP licenses and whether the volume of pending applications reshapes the regional ranking.

Launching a memecoin used to be a one-time event. Now, on platforms like Pump.fun, the person who creates a token can earn a cut of every trade, potentially for as long as it trades. That single change has reshaped who launches coins, why, and how the money flows. Here is how creator fees work, how they are evolving, and where they go wrong.

Summary

- Creator fees are a share of trading activity that a memecoin launchpad routes to the person who created a token, turning a launch into a potential ongoing income stream rather than a one-time event.

- On Pump.fun, the dominant Solana launchpad, creator fees can reach a small percentage of each transaction, and the system has evolved from rewarding coin creation to trying to reward genuine trading.

- A 2026 update introduced creator-fee sharing, letting teams split fees across multiple wallets, transfer token ownership, and assign percentages to community administrators.

- The mechanic has produced a new playbook in which some creators airdrop their fees back to holders to build loyalty, while the same tools can sustain hype around a token the creator profits from.

- Creator fees align incentives in theory but introduce real risks in practice, from incentivizing spam launches to enabling fee extraction at the expense of retail traders.

Creator fees are payments that a memecoin launchpad routes to the person who created a token, taken as a small percentage of the trading activity in that token, which turns launching a coin from a one-time act into a potential source of ongoing income. This is a genuinely important shift in how memecoins work, and it is easy to miss if you only watch token prices. In the older model, someone who launched a token might profit only by holding and selling their own allocation; the act of creating the coin itself paid nothing directly. Modern launchpads changed that by sharing a slice of every trade with the token’s creator, so that a coin which trades actively can pay its creator continuously, sometimes substantially, regardless of whether the creator buys or sells.

That single mechanic reshaped the incentives of the entire memecoin economy: it changed who launches coins, why they launch them, how they behave afterward, and increasingly how communities and influencers are paid. Understanding creator fees is therefore central to understanding why the memecoin space looks the way it does. The mechanic also sits at the heart of recent flashpoints in crypto, from launchpads redesigning their fee systems to influencers pledging to airdrop their accumulated fees back to traders. To make sense of those stories, you need to understand what creator fees are, how launchpads make money around them, how the systems have evolved from rewarding mere coin creation toward rewarding real trading, the newer fee-sharing tools that let creators split and redistribute their take, the community playbook this has enabled, a concrete worked example of the money involved, and the real risks and abuses the model invites.

This guide walks through each. The goal is not to encourage launching coins or chasing fees, but to explain a mechanism that now shapes the behavior of nearly every memecoin you might encounter, so that you can read the incentives behind a token rather than just its price chart. Once you see who gets paid and how, a great deal of otherwise baffling memecoin behavior starts to make sense.

What creator fees actually are

At the simplest level, a creator fee is a cut of trading taken automatically and paid to a token’s creator. When a launchpad hosts a token, it typically charges fees on trades, and it can direct a portion of those fees to the wallet associated with whoever created the coin. Because the fee is a percentage of trading volume, the creator earns more when the token trades more, which ties the creator’s income to the activity around the coin rather than to a single sale of their own holdings. This is structurally different from the traditional way token creators made money, which was to hold an allocation and sell it, an approach that aligns the creator with dumping on buyers.

A creator fee, by contrast, pays the creator from the flow of trading itself, which in principle gives them a reason to want sustained activity instead of a quick exit. It helps to separate the creator fee from the other fees in the system, because a launchpad’s economics involve several layers. When you trade a memecoin on a launchpad, the fees on that trade can be split among multiple parties: the protocol, meaning the platform itself; the liquidity providers who supply the pool the token trades against once it has graduated to a normal market; and the creator. Each takes a defined slice.

The creator fee is the portion earmarked for the token’s originator, and on the leading Solana launchpad it can reach a small but meaningful percentage of each transaction. Multiplied across high trading volume, even a fraction of a % per trade can add up to large sums for a coin that catches fire. So the basic picture is this: every trade in a launchpad memecoin pays a toll, and one slice of that toll flows to whoever created the coin, for as long as people keep trading it. That simple arrangement is the engine behind much of what follows.

How launchpads make money around fees

To understand creator fees, it helps to understand the business of the launchpad itself, because the two are intertwined. A memecoin launchpad is, at its core, a fee machine: it earns from the enormous volume of trading that flows through the tokens it hosts, regardless of whether any individual token succeeds or fails. This is a crucial point that explains much of the industry’s behavior. The platform benefits from activity and speculation in aggregate, so its incentive is to maximize the number of coins launched and the volume traded, even though the vast majority of those coins will lose nearly all their value.

The launchpad wins on volume; the individual trader usually does not. The leading Solana launchpad illustrates the scale of this. It has captured a dominant share of Solana’s memecoin launches, on the order of three-quarters of them, and it has generated very large revenues from platform fees. Notably, it has directed the overwhelming majority of its platform revenue, well over 90%, into buying back its own token, retiring a substantial portion of that token’s supply, one of the most aggressive buyback programs in crypto.

That detail matters because it shows how the fee flows ultimately circulate: trading fees fund the platform, which funds buybacks of the platform’s token, which benefits the platform’s token holders. Creator fees are one branch of this larger fee economy, the branch earmarked for the people who create the coins. Seen this way, the whole system is an arrangement for converting speculative trading volume into revenue and distributing it among the platform, its token holders, liquidity providers, and creators. The traders supplying the volume are the source of all of it.

From rewarding creation to rewarding trading

Creator-fee systems have not stood still; they have evolved in response to the problems they created, and that evolution is instructive. An earlier generation of the dominant launchpad’s fee system, introduced in late 2025 as part of a broader program, was designed to reward successful token creators, and it worked in the sense that it pulled in a wave of new participants, many of whom had never used a crypto application before, who began launching coins to earn fees. Platform activity surged, with trading volumes reportedly doubling. But the design had a flaw that its own operators came to recognize: by rewarding the act of creating coins, it skewed incentives toward low-risk coin creation instead of toward the high-risk trading that actually sustains a launchpad’s health.

In other words, it paid people to mint tokens, which produced a flood of low-quality launches, when what the platform needed was active trading and liquidity. This led to a rethink. The platform’s operators concluded that creator fees needed to change so that they rewarded genuine trading activity and the people who provide liquidity, instead of simply rewarding deployment. They signaled a shift toward what they described as a market-based approach, in which traders, not the people deploying coins, would effectively determine whether a token’s narrative deserved fee support, moving the reward toward the activity that generates real volume.

The operators also made a pointed cultural statement, indicating that no member of the platform’s own team would accept creator fees, and framing the feature as being for the active traders the community calls trenchers. That is why who the fees are aimed at matters in the broader Solana memecoin culture. The direction of travel, then, is away from paying people merely to launch tokens and toward channeling fees in a way that supports trading and liquidity. Whether that fully works in practice is open to question, but the evolution itself reveals the central tension in creator fees: a reward meant to encourage good behavior can easily encourage the wrong behavior, and designing it well is genuinely hard.

Creator-fee sharing and the newer tools

The most consequential recent change to creator fees was the introduction, in early 2026, of a fee-sharing system that gave creators far more flexibility in how their fees are handled, and understanding it clarifies several recent headlines. Under the older model, directing fees to a specific person or address was cumbersome, and the system sometimes required users to trust others to allocate fees properly, which weakened transparency. The fee-sharing update addressed this by letting a token’s team split its creator fees across multiple wallets, up to ten of them, and assign specific percentages to each, as well as transfer ownership of a coin and revoke certain authorities over it. Importantly, the update also let community administrators, the people who take over a coin in what is called a community takeover, assign fee percentages after a token has launched, opening the fee stream to community structures instead of only the original deployer.

This may sound like a technical plumbing change, but its effects are significant. By making it easy to split and redirect creator fees, the update turned the fee stream into something that could be shared among a team, distributed to a community, or routed to specific purposes, instead of flowing solely to one anonymous creator. It enabled coordinated projects to pay multiple contributors, allowed communities that revive an abandoned coin to capture the fees, and, as the next section describes, made it practical for creators to redistribute their fees back to holders as a loyalty mechanism. The broader significance is that creator fees stopped being a simple, single-recipient reward and became a flexible tool that could be programmed to serve different incentive structures.

That flexibility is powerful, and like most powerful tools in this space, it can be used to align a community or to manufacture loyalty around a token the controllers profit from. The mechanics are neutral; the uses are not. This is why creator fees should be read as the incentive design behind tokens rather than as a simple reward feature. The question is never only whether fees exist; it is who controls them, where they flow, and what behavior they encourage.

The community playbook this enabled

The fee-sharing tools, combined with the sheer size of fees a viral coin can generate, gave rise to a new playbook that has reshaped how influencers and communities interact with memecoins. The traditional influencer-coin pattern was extractive: an influencer launches or promotes a token, the price spikes on their attention, and they sell into it, leaving followers with losses. The newer playbook inverts part of that. Instead of pocketing accumulated creator fees, some creators now airdrop portions of those fees back to the community of holders and traders, framing it as sharing the rewards with the people who drove the coin’s success.

This redistribution, returning earned fees to holders instead of extracting and exiting, has been received notably well in a culture long cynical about influencers benefiting at retail’s expense. A high-profile instance brought this playbook to wide attention when a prominent Solana influencer, amid a memecoin frenzy built on his name, publicly criticized the launchpad over its handling of rewards and pledged to airdrop his accumulated creator fees, reported in the hundreds of thousands of dollars, back to traders, framing it in the community’s own slang as giving them a boost the platform would not. That was the fee-airdrop playbook in action. The move generated goodwill and reinforced a narrative that the influencer had alignment and skin in the game.

But the same episode illustrates the playbook’s double edge. A fee-airdrop program is a truly community-friendly gesture, and it is also a powerful tool for sustaining attention and buying pressure around a token the creator holds a large position in and profits from. Redistributing fees can align a creator with holders, and it can also be a sophisticated way to keep a speculative coin alive a little longer. Both readings are valid, and the honest view is that creator-fee redistribution is a real improvement over pure extraction while remaining a tool whose ultimate effect depends on the intentions and holdings behind it.

The mechanic does not, by itself, make a memecoin safe. It may reduce one type of extraction while preserving others. It may prove genuine alignment, or it may simply extend the life of a trade that still depends on fresh buyers arriving. The difference depends on the creator’s holdings, transparency, and behavior after the airdrop.

A worked example: where the money goes

To ground the abstraction, walk through a simplified example of how creator fees flow, using round numbers for clarity instead of precision. Imagine a creator launches a memecoin on a launchpad where the creator fee is set at a small fraction of 1% of each trade, and the coin catches a wave of attention. Suppose that over a busy stretch the token does $50 million in cumulative trading volume as buyers and sellers churn through it. Even at a creator-fee rate of, say, around 0.5% of trading, that volume would generate on the order of a couple of hundred thousand dollars in creator fees flowing to the wallet associated with the coin, entirely separate from any gain or loss on the creator’s own token holdings.

This is why a single viral coin can pay its creator a life-changing sum from fees alone, and why the prospect of those fees draws so many people to launch tokens. Now layer on the fee-sharing tools. With the newer system, that creator could split the fee stream across multiple wallets, perhaps paying several contributors who help run the project, or assign a percentage to a community administrator after a takeover, or set aside a portion to airdrop back to holders. So the same $200,000 might be divided among a small team, partly redistributed to the community to build loyalty, and partly retained.

The numbers here are illustrative, not a claim about any specific coin, but they capture the real dynamic: meaningful sums, generated from the trading volume of ordinary buyers, flowing to creators and increasingly programmable into splits and redistributions. The essential point the example makes is where the money originates. Every dollar of creator fees comes from the trading activity of the people buying and selling the coin. The fee is a transfer from traders to creators, dressed up in various ways.

Understanding that is the key to reading any claim about creator fees with clear eyes, because it locates who pays and who is paid. A fee can be redistributed, split, or framed as community alignment, but it still begins as a toll on trading activity. That does not make it automatically abusive. It does mean the economic direction of the flow should be clear before anyone treats it as a benefit.

Risks, abuses, and what to watch

Creator fees, for all their cleverness, introduce a set of risks and potential abuses that anyone interacting with memecoins should understand. The first is that fees incentivize spam. When launching a coin can pay, people launch enormous numbers of low-quality coins purely to chase fees, flooding the market with tokens that have no purpose beyond generating trades, which is precisely the problem the launchpads themselves identified and tried to redesign around. The second is fee extraction layered on top of other extraction.

A creator can earn substantial fees while also holding a large token position, and the combination gives them strong tools and strong motives to pump attention around a coin, sustain trading, and benefit regardless of whether holders ultimately profit, which can shade into the pump-and-dump dynamics that critics attribute to influencer-driven micro-caps. That is where how fee extraction can shade into abuse becomes relevant. Not every creator-fee model is a rug pull, but the same environment that supports fee extraction also supports scams, liquidity drains, and insider exits. The difference often lies in wallet concentration, transparency, and whether the creator can profit while holders are left with the downside.

The third risk is trust and transparency in how fees are allocated. Because fee streams can be split, redirected, and assigned to various wallets, it is not always clear who is actually receiving a coin’s fees or what they will do with them, and earlier systems were criticized for requiring users to trust others to allocate fees properly. The fourth is that the entire structure is funded by retail traders, the people supplying the volume, most of whom lose money on the highly volatile tokens involved, while fees flow to creators and platforms regardless. There are also broader integrity questions hanging over the dominant launchpad, including a major lawsuit alleging an insider-driven system that favored privileged participants at retail’s expense, a reminder that the fee economy operates in a lightly regulated and contested environment.

The practical guidance that follows from all this is to read creator fees as an incentive structure, not a feature that benefits you. When you encounter a memecoin, ask who earns its fees, how large their position is, and whether the activity around it is organic or manufactured by people who profit from the trading. Creator fees explain a great deal of memecoin behavior, and almost none of it is designed in the interest of the trader supplying the volume. They are part of the launch mechanism fees ride on, and understanding both the curve and the fee stream is how you see the full extraction path.

Frequently asked questions

What is a creator fee in crypto?

A creator fee is a share of trading activity that a memecoin launchpad routes to the person who created a token, taken as a percentage of each trade. It turns launching a coin into a potential ongoing income stream, because the creator earns from the flow of trading instead of only from selling their own holdings. On the leading Solana launchpad, the creator fee can reach a small percentage of each transaction, which can add up to large sums for a coin that trades heavily. It is one of several fees on a trade, alongside the protocol’s cut and the fees paid to liquidity providers, and it is specifically the slice earmarked for the token’s originator.

How much can a creator earn from fees?

It depends entirely on trading volume, since the fee is a percentage of trading. For a coin that fails to attract attention, the fees are negligible. For a coin that goes viral and trades tens of millions of dollars in volume, even a fraction of a % per trade can generate hundreds of thousands of dollars in fees, separate from any gain on the creator’s own holdings. This is why viral coins can pay their creators life-changing sums from fees alone, and why the prospect draws so many people to launch tokens. The flip side is that the overwhelming majority of launched coins generate almost nothing, because most never attract meaningful trading.

What is creator-fee sharing?

Creator-fee sharing is a system introduced on the leading Solana launchpad in early 2026 that lets a token’s team split its creator fees across multiple wallets, up to ten, and assign specific percentages to each, as well as transfer a coin’s ownership and revoke certain authorities. It also lets community administrators who take over a coin assign fee percentages after launch. The effect is to turn the creator fee from a single-recipient reward into a flexible tool that can pay a team, fund a community, or be redistributed to holders. It made the fee stream programmable, which enabled new uses like airdropping fees back to a community, while also raising questions about who actually controls a coin’s fees.

Why do some influencers airdrop their creator fees?

Because it builds goodwill and a narrative of alignment. The traditional influencer-coin pattern is extractive, with the influencer selling into the hype they create. Airdropping accumulated creator fees back to holders inverts part of that, framing the influencer as sharing rewards with the community that drove the coin, which plays well in a culture cynical about influencer extraction. A prominent example saw a Solana influencer pledge to airdrop his fees back to traders during a frenzy built on his name. The honest read is that this is both a truly community-friendly gesture and a tool for sustaining hype around a token the influencer profits from, since the same move keeps attention and buying pressure alive.

Are creator fees bad for traders?

Creator fees are funded by traders, since every dollar of fees comes from the trading volume of people buying and selling the coin, so they represent a transfer from traders to creators and the platform. They also create incentives that often work against traders: they reward spamming low-quality coins, they give creators tools and motives to manufacture hype around tokens they profit from, and they fund a system in which platforms and creators earn regardless of whether holders win or lose. They are not inherently fraudulent, and redistribution can return some value to communities, but they are best understood as an incentive structure that benefits creators and platforms. That structure is funded by the speculative activity of retail traders who mostly lose.

Which launchpad pays creator fees?

The most prominent is the dominant Solana memecoin launchpad, which captured roughly three-quarters of Solana’s memecoin launches and built an elaborate creator-fee system, including the 2026 fee-sharing tools described here. It directs a small percentage of each trade to a coin’s creator and has evolved its system from rewarding coin creation toward trying to reward genuine trading and liquidity. Other launchpads on Solana and other chains have their own fee models, and the specifics vary. But the general concept, routing a slice of trading fees to token creators, has become a standard feature of the memecoin launchpad model instead of something unique to any single platform.

This article is educational information, not financial advice or an endorsement of launching or trading any token. Details of launchpad fee systems, rates, and features reflect reporting available as of June 29, 2026, and can change. Memecoins are extremely high-risk and frequently lose most or all of their value, and the fee structures described are funded by trading activity that mostly results in losses for participants. Verify current platform terms independently and consult a qualified professional before making any decision.

Strategy has unveiled a revised capital management plan that allows the company to sell part of its Bitcoin holdings to strengthen liquidity, support shareholder payouts and repurchase securities.

Summary

- Strategy has approved a new capital framework that allows up to $1.25 billion in Bitcoin sales to support dividends, cash reserves and share buybacks.

- The company raised the STRC dividend to 12% and increased its protected cash reserve to $2.55 billion while reporting no new Bitcoin purchases last week.

- The changes came after growing scrutiny of Strategy’s funding model as investors questioned its liquidity, preferred stock structure and capital raising plans.

According to a Form 8-K filed with the U.S. Securities and Exchange Commission on Monday, filed alongside the company’s latest weekly Bitcoin update, the new Digital Credit Capital Framework authorizes Strategy to monetize up to $1.25 billion worth of Bitcoin if needed.

Per the filing, proceeds may be used to increase cash reserves, fund preferred stock dividends, meet debt obligations, and buy back both preferred securities and Class A MSTR shares.

At the same time, Strategy increased the annual dividend rate on its STRC perpetual preferred stock to 12% from 11.5%. The company also disclosed that its dedicated cash reserve has reached $2.55 billion, enough to cover roughly 17 months of preferred dividends and interest payments. Under the new policy, the reserve can only be used for those obligations and must remain above 12 months of coverage unless the board approves otherwise.

Executive chairman Michael Saylor said the existing reserve, combined with the newly authorized Bitcoin monetization capacity, provides about $3.8 billion of dividend coverage, equivalent to nearly 26 months. Saylor also said Strategy intends to remain disciplined when issuing new MSTR shares, particularly when the stock trades near one times its modified net asset value, or mNAV.

Nevertheless, Strategy shares appeared to respond positively to Monday’s announcement. Ahead of the Nasdaq opening bell, investors had pushed MSTR shares up more than 3.2% and another 2.69% in after-hours trading.

MSTR shares. Source: Google Finance.

Focus turns to liquidity instead of new Bitcoin purchases

Although Saylor had hinted at another Bitcoin acquisition over the weekend by posting Strategy’s Bitcoin tracker, the company reported no purchases during the week ended Sunday. Holdings remained unchanged at 847,363 BTC acquired for a combined $64.1 billion at an average purchase price of $75,651 per Bitcoin.

Even without a new weekly purchase, Strategy has added a net 3,625 BTC so far in June after buying 3,657 BTC and selling 32 BTC earlier in the month. The filing also showed the company raised about $1.15 billion in net proceeds through the sale of 12.67 million MSTR shares.

The revised framework follows several days of growing debate around Strategy’s funding model. Earlier this month, CryptoQuant warned that Strategy should pause Bitcoin purchases and strengthen its balance sheet, estimating that the company would need about $2.8 billion in cash to restore around two years of dividend coverage after annualized preferred dividend obligations rose to approximately $1.2 billion.

Other critics had questioned whether Strategy should continue relying on capital markets to fund Bitcoin purchases while its securities weakened. For instance, Ripple CEO Brad Garlinghouse has recently argued that issuing securities to acquire more Bitcoin does not create lasting value, while Bitcoin critic Peter Schiff suggested the company might eventually need to sell part of its Bitcoin holdings to finance share buybacks.

Strategy’s mNAV falling below 1 for the first time this cycle has also drawn attention to the economics of its fundraising model. The company had previously indicated that issuing common shares below roughly 1.22x mNAV could dilute Bitcoin per share for existing shareholders.

A wave of Solana memecoins carrying the name of influencer Ansem has gone parabolic, with one version running to tens of millions in market cap in under two weeks. But Ansem did not create most of them, has publicly disavowed several, and the eye-catching pump figures often do not survive a look at the chain. Here is what $ANSEM actually is, why it is trending, and what it teaches about influencer coins.

Summary

- $ANSEM is not a single coin but a cluster of competing Solana memecoins built around the online identity of crypto influencer Ansem, real name reported as Zion Thomas, who created none of them.

- The dominant “Black Bull” version on Pump.fun ran from a market cap in the tens of thousands to tens of millions of dollars within roughly 10 to 12 days in mid-to-late June 2026.

- Ansem amplified the frenzy by criticizing the launchpad Pump.fun and pledging to airdrop his creator fees to the community, while at the same time disavowing other $ANSEM tokens as impersonations.

- Several viral pump figures circulating on aggregator trackers did not hold up against live on-chain data, a reminder to verify the actual contract before trusting a headline number.

- $ANSEM is best understood not as a coin to buy but as a live case study in how an influencer’s name spawns a swarm of speculative and copycat tokens, and how easily retail buyers get hurt.

$ANSEM is the name shared by a cluster of competing Solana memecoins that sprang up around the online identity of the crypto influencer known as Ansem, whose real name is reported as Zion Thomas and whose verified account is @blknoiz06, and the single most important fact about it is that Ansem did not create these tokens and has publicly distanced himself from several of them. That makes $ANSEM less a single coin than a phenomenon: a recognizable name in crypto that, the moment it started trending, spawned a swarm of tokens using it, some promoted heavily, some outright impersonations, and no single official one among them. In late June 2026, one version branded as “The Black Bull” went parabolic on the launchpad Pump.fun, climbing from a market cap in the tens of thousands of dollars to tens of millions within roughly 10 to 12 days, while traders fought in what the culture calls the trenches over which $ANSEM coin, if any, was the real one. The story drew enormous attention, and it is a near-perfect illustration of how influencer memecoins actually work, who tends to benefit, and who tends to get hurt.

This guide treats $ANSEM the way it deserves to be treated: not as a coin to evaluate buying, but as a case study to learn from. Understanding it requires understanding who Ansem is and why his name carries weight, why there is no single official $ANSEM coin, how the frenzy unfolded and what catalyzed it, the disavowal and the copycats that complicate the story, the creator-fee twist that made it unusual, the gap between viral pump figures and on-chain reality, and the genuine risks that influencer memecoins carry for the people who chase them. The aim is that by the end, a reader could recognize the pattern the next time a famous name starts trending and a wall of tokens appears using it, because that pattern repeats constantly, and $ANSEM is simply its latest and loudest example. The lesson is in the mechanics, not the ticker.

Who Ansem actually is

To understand why a memecoin built on his name could run so far so fast, you have to understand the standing Ansem holds in crypto. Zion Thomas, who goes by Ansem and is sometimes called “The Solana Guy,” is one of the most-followed voices in the space, with roughly a million followers on the platform X. His reputation rests on a real track record: he was an early and vocal supporter of Solana and of memecoins like Dogwifhat and Bonk, and he is widely credited with calling Solana’s enormous 2023 rally, when the token climbed from around $8 to nearly $300. He has a background in computer science from Georgia Tech and worked as a software engineer before moving into crypto full time, and he holds a research role at an investment firm.

That combination of early correct calls, technical credibility, and a massive audience is why his name carries weight, and why a token attached to it can attract a flood of speculative buying on attention alone. But the picture is not uniformly flattering, and an honest explainer has to include the criticism, because it is directly relevant to the risks of any coin bearing his name. Ansem has drawn sustained accusations that he uses his influence to promote low-cap memecoins that spike and then collapse. In late 2024, the prominent on-chain investigator ZachXBT publicly accused him of promoting micro-cap coins in a way that resembled pump-and-dump dynamics, hyping risky tokens to a large following, watching them briefly surge, and leaving late buyers with losses.

These remain accusations rather than proven findings, and Ansem has his defenders, but the pattern they describe is exactly the danger retail buyers face with influencer coins. Notably, Ansem himself has at times acknowledged the problem: he has publicly admitted that supporting some celebrity-backed memecoins was a mistake, citing misaligned incentives that hurt retail investors. That admission is worth holding onto, because it comes from the very person whose name is now attached to a fresh memecoin frenzy, and it captures the core risk better than any outside critic could. In influencer memecoins, the audience is often the liquidity, and the audience is usually the last to understand that.

There is no single $ANSEM coin

The most common and costly misunderstanding about $ANSEM is the assumption that it refers to one coin. It does not. When Ansem’s name began trending, multiple distinct Solana tokens using the $ANSEM name appeared at the same time, and there is no single official one that Ansem created or endorsed as the canonical version. This is not unusual; it is the standard sequence in crypto. A well-known name starts trending, and within minutes a swarm of tokens appears using it, deployed by different anonymous creators all hoping their version becomes the one the market settles on.

The result was a chaotic competition, with the trading community flipping between rival $ANSEM coins and no clear winner crowned as the real one for a stretch, a dynamic participants describe as a player-versus-player battle in the trenches. Out of that scramble, one version did come to dominate the narrative: a coin branded as “The Black Bull,” launched on the Pump.fun launchpad in mid-June 2026, which became the token most associated with the headlines as it ran to tens of millions in market cap. Even so, the existence of that dominant version does not change the underlying reality that the name was contested and that other $ANSEM tokens continued to circulate alongside it, including ones Ansem explicitly disavowed. For anyone encountering the trend, the practical implication is severe: there is no safe assumption that a token labeled $ANSEM is the one being discussed, is endorsed by Ansem, or is anything other than an opportunistic deployment by a stranger.

The name on the token tells you almost nothing about who made it or whether it is connected to the person it references. That single fact, that the name is not the coin, is the first and most important thing to internalize about $ANSEM and about every influencer memecoin like it. This is whyverifying contracts and accounts matters before believing any viral ticker. A famous name can become a trap when anyone can attach it to a contract.

How the frenzy unfolded

The timeline of the $ANSEM surge shows how quickly attention converts into market cap in this corner of crypto, and what lit the fuse. The dominant Black Bull version gained real traction around the middle of June 2026 and then, over roughly 10 to 12 days, went parabolic, rising from a starting market cap reportedly in the tens of thousands of dollars to a level above $50 million and then $60 million at its peak, accompanied by gains measured in thousands of %. On-chain trackers recorded enormous short-window moves, with one tracker reporting a single-day surge of well over a hundredfold at one point, the kind of move that draws the entire trading community’s attention and pulls in waves of new buyers chasing the run.

A specific catalyst supercharged the move. Ansem publicly criticized Pump.fun over how it handled rewards to users, and declared that he would deliver a financial boost directly to retail traders, a gesture he framed in the community’s own language. In a widely shared post on June 28, 2026, he wrote that he “had to give the trenches a stimmy since pump refuses to,” using slang for handing money to on-chain traders. That narrative, an influencer taking the side of small traders against the platform, spread rapidly across crypto social media and triggered a fresh wave of speculative buying that lifted the token’s valuation further.

The frenzy also minted dramatic individual outcomes that became their own marketing: in one widely reported case, a trader who put roughly $2,300 into an ANSEM-named token saw the position balloon to more than $600,000 after a parabolic rally, a return of tens of thousands of %. Stories like that, true but extraordinarily rare, are exactly what pull more people into the next frenzy, which is why they deserve to be read with as much caution as excitement. The setup also show how the launch pricing worked, because these early Solana memecoin moves often begin on bonding curves before attention pushes them toward graduation or collapse. The bigger the screenshot gain, the more important it becomes to ask who bought before the crowd and who is left buying after the move.

The disavowal and the copycats

Running directly against the bullish narrative is a fact that anyone tempted by $ANSEM needs front and center: Ansem publicly disavowed tokens trading on his name. According to posts reported from his verified account, he distanced himself from the activity, indicating that the coin being promoted was not him and that he was not endorsing any micro-cap tokens, and he clarified that he had only linked his account to a launchpad address to prove that he could, not to bless any particular coin. In other words, the person whose name was driving tens of millions of dollars in speculative value was, at the same time, telling people he had not created these tokens and was not endorsing them. That is a glaring contradiction at the heart of the trend, and it is the single clearest warning sign attached to it.

The disavowal points to the deeper pattern, which is the real lesson of $ANSEM. A recognizable crypto name reliably spawns a cluster of copycat and impersonation tokens, the overwhelming majority of which the named person never touched, because on a permissionless launchpad anyone can deploy a token and call it whatever they want. The Ansem case is a textbook instance: a swarm of $ANSEM tokens, no official one, and the real Ansem distancing himself from the activity even as it raged. The danger goes beyond merely buying the wrong version.

Ansem’s identity has been abused by outright impersonators before; reports describe a 2024 impersonation that phished roughly $2.5 million from victims, an event that had nothing to do with Ansem himself but used his name and likeness to steal. The takeaway is blunt: when a name is trending, impersonation and copycatting are not edge cases but the norm, and a token carrying a famous name should be treated as unaffiliated and unsafe until proven otherwise, a standard that becomes absolute when the person has publicly disavowed it, as Ansem did. The same pattern has appeared around other high-profile names and brands, including fake tokens designed to mimic official launches. That is why the first question should never be “how much is it up?” but “who actually created this contract?”

The creator-fee twist that made it unusual

One feature did set the $ANSEM episode apart from the typical influencer-coin story and helps explain both its momentum and the debate around it. Rather than simply launching his own token to capture the speculative interest, which is the usual influencer playbook, Ansem leaned into a different mechanic tied to how the Pump.fun launchpad pays out fees. Pump.fun routes a share of trading fees to a token’s associated creator account, and screenshots of Ansem’s launchpad profile indicated he had accumulated substantial creator fees, reported in the area of several hundred thousand dollars. In response to community suggestions, he announced that, instead of pocketing those fees, he would airdrop portions of them back to the community of traders, framing it as giving the trenches the boost the platform would not.

This redistribution, returning earned fees to holders rather than extracting and exiting, was received notably well in a culture used to influencers benefiting at retail’s expense, and it reinforced the narrative that Ansem had “skin in the game.” Indeed, reporting on his launchpad wallet suggested a very large exposure to the token, with a holding worth tens of millions of dollars making up the overwhelming majority of that wallet’s value. Supporters read this as alignment: the influencer profiting only if holders profit. Skeptics read it differently, noting that a huge personal position and a fee-airdrop program are also powerful tools for sustaining hype around a token the influencer benefits from, and that the same dynamics ZachXBT criticized, an influencer’s attention inflating a coin’s price, are present whether or not fees are shared.