Crypto World

Chainlink Price Holds Near $8.0 as FIFA Partner Adopts Oracles

TLDR:

- Chainlink price traded near $7.91 as LINK remained under short-term selling pressure despite the new FIFA World Cup partnership.

- ADI Predictstreet adopted Chainlink as its exclusive oracle infrastructure for FIFA World Cup 2026 prediction markets.

- Chainlink Runtime Environment will help automate market creation, resolution, and settlement using high-quality FIFA data.

- The partnership expands Chainlink’s real-world utility, but LINK still needs stronger demand to confirm a price recovery.

Chainlink price traded near $7.91 on June 9 as ADI Predictstreet adopted Chainlink as its exclusive oracle infrastructure for FIFA World Cup 2026 prediction markets. LINK was down 0.87% in 24 hours, while trading volume fell 5.99% to about $320.65 million.

The announcement added a major sports-related use case for Chainlink. However, LINK’s chart remained weak after its recent decline from higher levels. The token was still trading below the $8 area, with market capitalization near $5.75 billion.

Chainlink Price Stays Weak Despite FIFA World Cup Deal

Chainlink price remained under pressure even after a major integration tied to the FIFA World Cup 2026. Chainli price analysis reveals LINK is struggling to rebuild momentum after a sharp drop in early June.

The token recently moved near the lower end of its short-term range. The RSI stood near 34.75, showing that sellers still held control. This level also suggested that LINK was close to oversold territory.

LINK/USD 1-day chart | Source: TradingView

ADI Predictstreet announced that it had adopted Chainlink to support prediction markets for the FIFA World Cup 2026. The platform is the official prediction market partner of the tournament.

The deal gives Chainlink a role in market resolution, settlement, and data orchestration. ADI Predictstreet said Chainlink would help reduce slow manual resolution and outcome disputes.

ADI Predictstreet Uses Chainlink for Prediction Markets

ADI Predictstreet will use the Chainlink Runtime Environment to automate market creation, resolution, and settlement. The system will rely on high-quality FIFA data to support accurate outcomes.

The 2026 FIFA World Cup is expected to span 48 teams, 104 matches, and 16 host cities. The event will take place across Canada, Mexico, and the United States.

This scale creates a major test for prediction market infrastructure. Fast settlement matters because users expect quick payouts after match outcomes are known. Chainlink’s oracle system is designed to provide that source of truth.

ADI Predictstreet CEO Dimitrios Psarrakis said the integration would support transparent outcome resolution and efficient settlement. Chainlink Labs Chief Business Officer Johann Eid said the partnership could help redefine live sports prediction markets.

The Chainlink has expanded its reach beyond DeFi and tokenized finance. The network has already been used across lending, payments, stablecoins, and institutional blockchain projects.

As reported, the Chainlink network has enabled over $30 trillion in transaction value, and its infrastructure powers more than 70% of the global DeFi market.

Still, Chainlink’s price has not yet reflected a strong market reaction. LINK needs renewed spot demand and stronger broader crypto conditions to confirm a rebound.

A move above $8.00 would be the first sign of short-term strength. Further upside could bring attention back to the $8.50 and $9.00 areas. A failure to hold near $7.80 may keep sellers active.

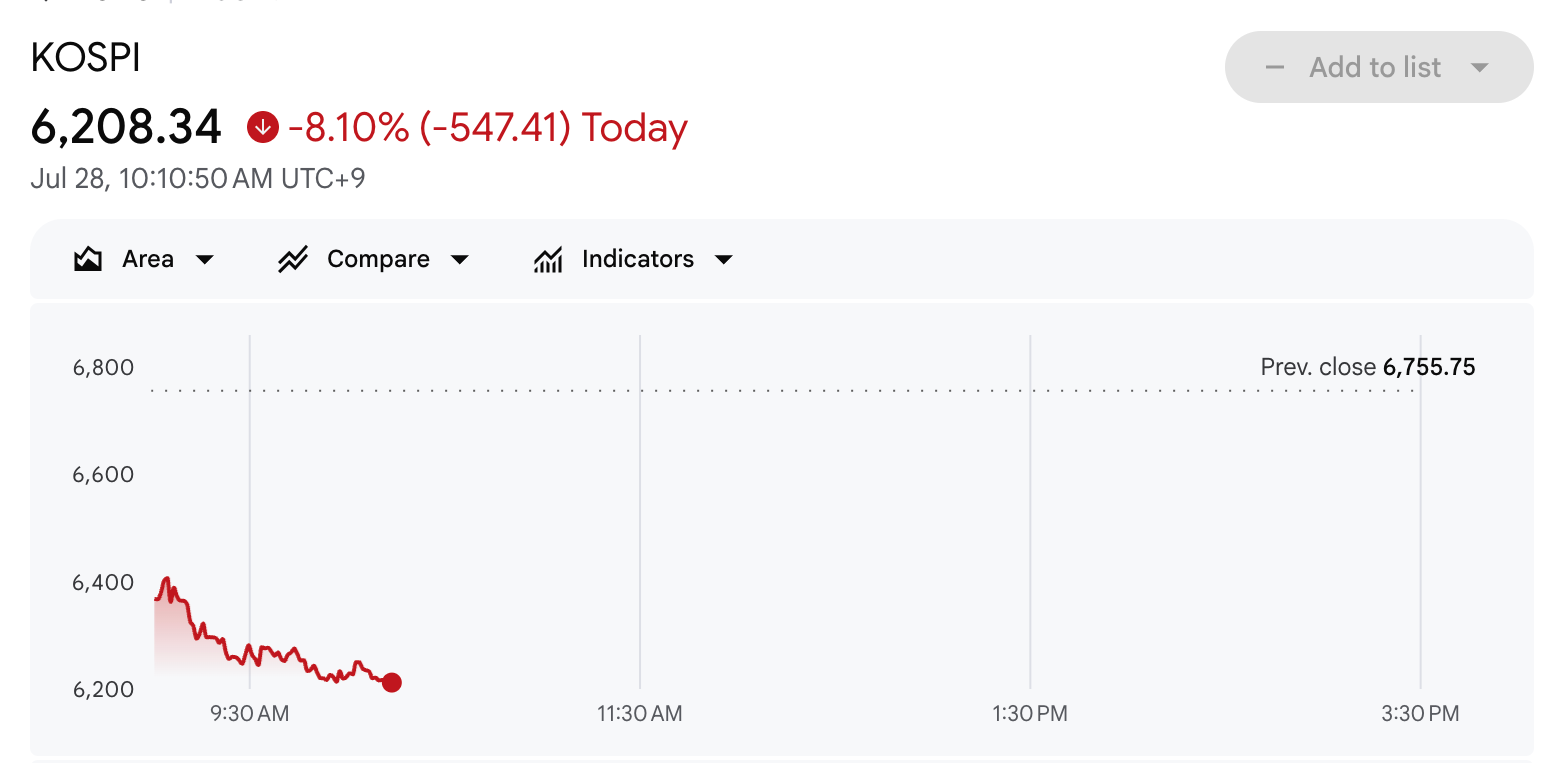

The KOSPI plunged 8.10% to 6,208.34 on Tuesday morning, deepening a global semiconductor rout.

SK Hynix sank 11.01%, and Samsung Electronics dropped 9.45%, a day before the memory giant reports quarterly earnings.

Follow us on X to get the latest news as it happens

Chip Selloff Spreads From Wall Street to Seoul

The Korea Exchange triggered a sell-side sidecar after the open, its 22nd this year. A similar mechanism tripped on the Kosdaq shortly afterward. The index was down 6.6% at press time.

Japan followed Seoul lower. Kioxia cratered 16.5%, Tokyo Electron dropped over 9%, and Advantest slid 8%.

SoftBank Group, an AI proxy through its Arm stake, fell nearly 5%. Overall, the Nikkei 225 lost 3.90%, while the Topix shed 2.49%.

The rout extends Monday’s weakness in US chip stocks, where the VanEck Semiconductor ETF lost over 2%, according to CNBC. AMD and Teradyne led declines, falling 5% and 4% respectively.

Investors remain skeptical about tech giants’ heavy AI spending. The selloff comes days after SK Hynix and Samsung announced $950 billion AI deals.

Earnings Gauntlet Meets Crypto Spillover

The timing raises the stakes. SK Hynix reports on Wednesday, July 29, its first earnings since a record Nasdaq debut. Microsoft, Meta, and a Fed rate decision land the same day. Apple and Amazon close Big Tech’s earnings week on Thursday.

The pressure has spilled into crypto markets. Bitcoin (BTC) traded near $63,199, down 2.9% over 24 hours. Meanwhile, US futures pointed to further weakness, with S&P 500, Nasdaq 100, and Dow futures down 0.1%, 0.42%, and 0.04%, respectively.

Whether Wednesday’s results from SK Hynix restore confidence or confirm the doubts driving the unwind may set the tone for the week.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post KOSPI Crashes 8% as AI Chip Selloff Slams Asian Markets appeared first on BeInCrypto.

Binance says it has been running simulated phishing attacks on its own staff every month for the past four years, using the results to measure whether its security practices are improving. The exchange’s chief security officer, Jimmy Su, told Cointelegraph that the internal “red team” carries out the exercises and that employees who repeatedly fail may be sent for remediation training.

Meanwhile, the crypto sector also faces policy and compliance pressures across Asia: an Internet rights group in India challenged a government-backed order to remove repositories related to Jack Dorsey’s BitChat, while other developments—from stablecoin payment pilots in the Philippines to shifting retail behavior in South Korea—highlight how technology adoption and regulation are moving in parallel.

Key takeaways

- Binance conducts monthly internal phishing tests via its red team and uses the outcomes to trigger remediation training.

- India’s Internet Freedom Foundation says a recent order to GitHub to disable BitChat repositories is unconstitutional and threatens open-source and free speech.

- CoinShares-related social-engineering concerns remain in focus, with prior industry estimates suggesting a large share of crypto incidents are driven by manipulation rather than pure technical exploits.

- South Korea’s five largest crypto exchanges reported a sharp year-over-year drop in combined trading volume, despite growth in equities.

- Several countries are exploring real-world payment use cases for stablecoins and blockchain rails, even as governance scrutiny tightens.

Binance uses internal phishing drills to test security hygiene

According to Cointelegraph, Binance’s security approach includes ongoing, controlled attempts to trick employees with phishing-style tactics. Jimmy Su, Binance’s chief security officer, said the company runs these exercises “on a monthly basis” to determine whether day-to-day security hygiene is improving.

The tests are carried out by Binance’s internal ethical hacking unit—its “red team”—which is tasked with breaking into systems in order to identify vulnerabilities. Su said employees who fail the phishing simulations are not simply tracked; they are expected to undergo remediation training.

The broader relevance is that attackers often target human behavior rather than exploiting only software bugs. In February, AMLBot estimated that 65% of crypto security incidents in 2025 were driven by social engineering, underscoring why organizations have increasingly prioritized employee training alongside technical controls. (AMLBot estimate referenced by Cointelegraph: https://cointelegraph.com/news/amlbot-2025-crypto-incidents-social-engineering-phishing-impersonation)

India challenges GitHub takedown order over BitChat repositories

In India, the Internet Freedom Foundation (IFF) condemned a government order directing GitHub to remove or disable repositories related to BitChat, describing the move as unconstitutional. The group warned that the decision could undermine free speech and the open-source ecosystem.

IFF’s statement, according to Cointelegraph, followed a cybercrime agency directive that ordered GitHub to disable access to three BitChat repositories within three hours. The agency’s rationale was that BitChat could be used to bypass internet shutdowns, evade lawful surveillance, and facilitate unlawful activities.

BitChat is described as a decentralized messaging app designed to route encrypted messages between nearby devices over Bluetooth, without relying on internet connectivity or centralized servers. Cointelegraph also noted that since BitChat’s July 2025 release, it has gained traction during periods of unrest and internet outages in countries including Madagascar, Nepal, Uganda, Jamaica, and Iran. (Cointelegraph links referenced by the original report: https://cointelegraph.com/news/jack-dorsey-launches-bluetooth-relayed-decentralized-messaging-app-bitchat, https://cointelegraph.com/news/48000-nepalis-install-jack-dorseys-bitcoin-amid-protests, https://cointelegraph.com/news/bitchat-second-ranked-app-jamaica-as-hurricane-strikes, https://cointelegraph.com/news/decentralized-messaging-adoption-global-unrest)

For developers and users, the dispute raises a familiar tension in crypto and open-source technology: platforms and code repositories can become collateral in broader concerns about communications infrastructure and governance. What remains to be seen is whether GitHub’s handling of the order, and any potential legal challenge in India, changes how decentralized tools are distributed—or whether similar requests spread to other repositories.

Retail crypto interest cools in South Korea while equities surge

Separately, South Korea’s crypto trading activity has deteriorated sharply even as its stock market climbed. Cointelegraph reports that the combined trading activity across five major won-based exchanges—Upbit, Bithumb, Coinone, Korbit, and Gopax—fell by 89% year over year.

The figure comes from Cointelegraph’s review of CoinGecko’s historical 24-hour volume readings. The comparison used seven-day averages in July 2025 versus July 2026. On a combined basis, average daily volume declined to $305 million from $2.82 billion over the comparable July 2025 period.

Cointelegraph also stated that the KOSPI benchmark more than doubled during the same stretch. While volume has dropped for crypto, the divergence suggests that some retail liquidity may be rotating toward stocks—or that risk appetite and participation in crypto are being influenced by factors beyond token prices alone, such as market structure or broader macro sentiment.

Traders and investors watching South Korea will likely want to focus on whether this pattern persists beyond July and whether exchange-level initiatives or regulatory developments affect participation. The next question is whether lower volumes reflect temporary sentiment shifts or a more durable change in retail allocation decisions.

Stablecoin rails and exchange restructures signal continued build-out

Beyond security and policy disputes, adoption-oriented developments continued. In the Philippines, the Bank of the Philippine Islands (BPI) plans a stablecoin-based settlement rail for cross-border payments to freelancers, virtual assistants, and other workers receiving overseas income. Cointelegraph reports that the project is being developed with Meridian, with the intent to reduce processing cost and time while retaining safeguards associated with traditional banking transactions.

According to Cointelegraph’s reporting, stablecoins would be used as a settlement instrument before funds are converted to Philippine pesos and credited to recipients’ BPI accounts. (Cointelegraph referenced coverage from ABS-CBN and Philippine Daily Inquirer.)

In Singapore, Coinbase is also reported to be expanding its local presence, planning to grow headcount from 150 to about 200 staff members by the end of 2026 and prioritizing roles including engineers and institutional sales. Cointelegraph cited comments from Hassan Ahmed, Coinbase’s country director for Singapore, to the Business Times about the city-state’s role as a strategic hub for crypto innovation. (Cointelegraph referenced link: https://www.businesstimes.com.sg/singapore/coinbase-expand-singapore-operations-grow-headcount-200-despite-global-restructuring)

Elsewhere in Asia, HashKey Holdings said it has merged HashKey Exchange and HashKey Global into a single platform and application, with the goal of giving users a consistent app experience while compliance is managed through local regulatory frameworks. (Cointelegraph link referenced: https://cointelegraph.com/news/hong-kong-crypto-giant-hashkey-merges-its-exchanges-into-one)

Taken together, these stories point to a sector split between defensive maturity—like Binance’s ongoing internal phishing drills—and front-of-house expansion, such as stablecoin payment settlement testing and exchange platform consolidation. The common thread is governance: whether it’s security enforcement inside companies, repository access decisions by governments, or compliance-heavy product rollouts in banking systems, the “how” of crypto adoption is increasingly as important as the “what.”

For the weeks ahead, watch how India’s BitChat repository dispute develops and whether it affects other open-source or decentralized tools, while South Korean trading volume trends indicate whether retail activity is temporarily shifting or settling into a new baseline.

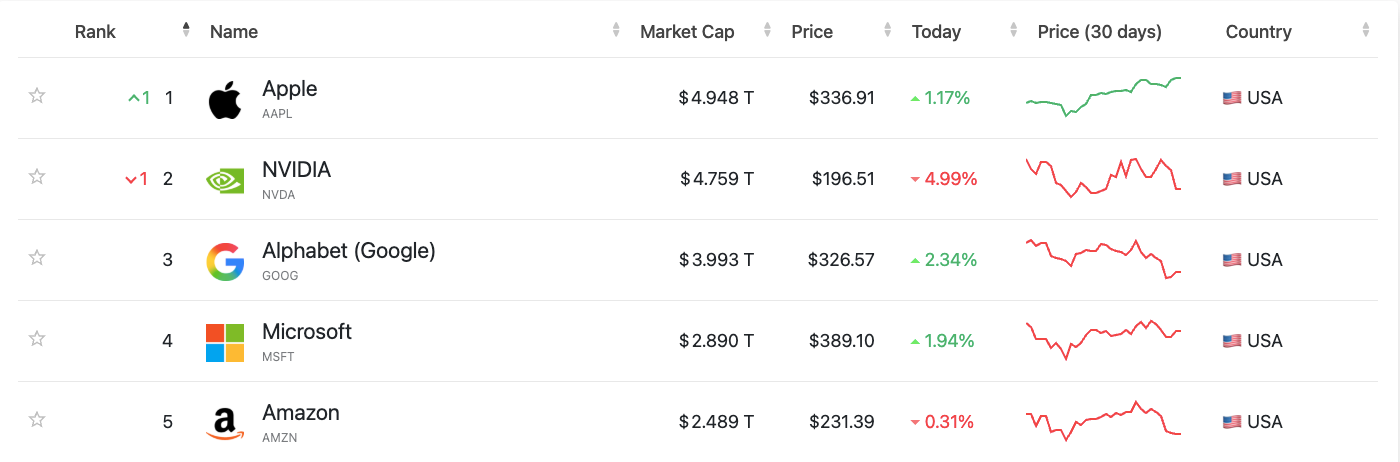

Dan Niles, founder of Niles Investment Management, says Apple’s (AAPL) slow start on artificial intelligence (AI) turned into an accidental advantage, even as he flags valuation risk ahead of its earnings report this week.

Apple’s stock recently reached new all-time highs, hitting a record closing price of $336.91 on July 27. This surge pushed Apple’s market capitalization to roughly $4.93 trillion, allowing it to reclaim the title of the world’s most valuable public company from Nvidia. The company reports fiscal third-quarter results on July 30.

Apple’s AI Delay Was Actually a Lucky Break

Speaking on CNBC’s Squawk on the Street, Niles said Apple avoided the AI spending spree that has hit rivals’ cash flow.

“Sometimes you get lucky for being incompetent,” Niles said, adding that Apple was “horrible” at getting AI onto iPhones.

That weakness now looks like an edge. Alphabet has raised its 2026 capital expenditure (capex) guidance to $195 billion to $205 billion for AI infrastructure. The spending pushed Alphabet’s free cash flow negative in the second quarter, the first such quarter since its 2004 initial public offering (IPO), the process by which a private company first sells shares to the public.

Apple takes a different path. It reportedly pays Google around $1 billion a year to license a custom Gemini model for Siri’s AI upgrade. That fee covers a fraction of what rivals spend building their own AI models from scratch.

Apple briefly passed Nvidia as the world’s most valuable company earlier this month. Its stock has kept climbing since, partly on the view that it can benefit from AI demand without carrying the balance-sheet risk.

The Valuation Catch

Niles was less comfortable with where the stock trades today. Apple’s price-to-earnings (P/E) ratio, a measure of stock price relative to earnings, sits in the high 30s. That’s well above the S&P 500’s roughly 22 times earnings.

He warned that could leave Apple exposed if Thursday’s numbers disappoint, particularly if rising semiconductor prices squeeze margins. Memory chip costs have surged this year, a trend already forcing price hikes across the phone market.

“You can’t put all the money in the world into this one stock because they’re just not spending on AI,” Niles said. “It doesn’t make sense at a certain valuation.”

Wall Street expects Apple to post revenue near $108.9 billion and earnings per share (EPS) of $1.89 for the quarter, up from $1.57 a year earlier. Thursday’s report also lands in the middle of a packed earnings week for Big Tech, with Meta and Amazon reporting the same week under similar AI spending scrutiny.

Niles said he plans to stay largely on the sidelines for those names too, citing his own concerns about capex tied to each.

The post Dan Niles Says Apple Was ‘Incompetent’ With AI, So Why Is The Stock at All-Time Highs? appeared first on BeInCrypto.

Binance ‘red teams’ its own staff every month to keep hackers out

Cryptocurrency exchange Binance has been running simulated phishing attacks against its own employees for the past four years and can fire staff who repeatedly fail the tests, according to Binance chief security officer Jimmy Su.

The fake attacks are conducted by Binance’s red team, an internal ethical hacking unit whose job is to break into systems to identify vulnerabilities.

“We do phishing attacks on our own employees on a monthly basis just so we understand if our security hygiene is improving,” Su told Cointelegraph. “The ones that have failed it, we will do remediation training.”

In February, AMLBot estimated that 65% of crypto security incidents in 2025 were driven by social engineering.

India’s BitChat GitHub takedown order ‘unconstitutional’

India’s Internet Freedom Foundation (IFF) has condemned a government order directing GitHub to remove repositories for Jack Dorsey’s decentralized messaging app BitChat, calling the move unconstitutional and warning it threatens free speech and open-source software.

The statement came a day after India’s cybercrime agency ordered GitHub to disable access to three BitChat repositories within three hours, saying the decentralized messaging app could be used to bypass internet shutdowns, evade lawful surveillance and facilitate unlawful activities.

BitChat is a decentralized messaging app that routes encrypted messages between nearby devices over Bluetooth without relying on internet connectivity or centralized servers.

Since its release in July 2025, the app has gained traction during periods of unrest and internet outages in countries including Madagascar, Nepal, Uganda, Jamaica and Iran.

More crypto news from India:

— India’s Central Board of Direct Taxes (CBDT) has issued guidance directing crypto exchanges to report all transactions on their platforms to the Income Tax department.

Balaji’s Network School turns to Kazakhstan amid Malaysian setback

Balaji Srinivasan’s utopian Network School looks set to move to Kazakhstan after Malaysian authorities revoked its business license over alleged premises-use violations.

A memorandum of understanding was signed between Kazakhstan’s Minister of Digital Development and Srinivasan to establish a campus in the country which has been positioning itself as an emerging technology hub, and has plans for Central Asia’s first “crypto city” in Alatau.

The Network School had been at the centre of a scandal involving hosting Israeli citizens given the Muslim majority country has no diplomatic relations with Israel. The US State Department called in the Malaysian envoy to ask for an explanation about the country’s apparent policy of deporting dual citizens with Israeli passports.

Source: The Times of Israel/Reuters

South Korea crypto volumes shrink as retail investors shift to stocks

South Korea’s five major crypto exchanges have seen their combined trading activity fall by 89% year over year, even as the country’s stock market surged.

The Korea Composite Stock Price Index (KOSPI) benchmark more than doubled over the period, while volumes across the country’s largest won-based crypto platforms fell off a cliff.

Cointelegraph reviewed CoinGecko’s historical 24-hour volume readings for Upbit, Bithumb, Coinone, Korbit and Gopax, comparing seven-day periods in July 2025 and July 2026.

On a combined basis, average daily volume fell about 89%, to $305 million from $2.82 billion in the comparable July 2025 period.

More crypto news from Korea:

— South Korean crypto exchange Korbit will reportedly rebrand as Digital X after becoming part of Mirae Asset Group.

— South Korea’s KB Kookmin Bank will launch a blockchain-based cross-border payment service for import and export businesses in August using JPMorgan’s Kinexys network.

— South Korean regulators have removed 29 unlicensed crypto exchange apps from the Google Play store. Affected apps include those from OKX, Bybit, MEXC, Kucoin, Gemini, Backpack, and BitMEX.

— North Korean authorities have reportedly arrested a group of former state cyber operators and IT specialists accused of hacking two state banks and laundering stolen funds through cryptocurrency.

Thailand SEC files complaint against Bitkub over alleged false disclosures

Thailand’s SEC filed a criminal complaint against Bitkub and two former directors over alleged false disclosures linked to a 2021 cyberattack involving $50 million in assets.

The complaint names former Bitkub directors Sakolkorn Sakavee and Thaweesap Rawan, who the SEC said were responsible for submitting company reports during the period under investigation.

The case comes as Bitkub’s parent company considers a potential public listing, putting renewed attention on transparency and governance at one of Thailand’s most prominent crypto businesses.

More crypto news from Thailand:

— Thailand’s Kbank has signed a memorandum of understanding with BPMG and HashKey Group to develop stablecoin-based cross-border remittance services.

— Thailand authorities have raided seven illegal Bitcoin mining operations after uncovering large scale electricity theft. More than 1900 crypto mining machines were seized.

One of two Bitcoin mining warehouses in Samut Sakhon alleged to be stealing power. Source: DSI Facebook page.

Philippine bank BPI plans stablecoin payments pilot

The Bank of the Philippine Islands (BPI) is planning to pilot a stablecoin-based settlement rail for cross-border payments to freelancers, virtual assistants and other workers receiving overseas income.

Developed with global digital clearinghouse Meridian, the system is intended to reduce the cost and processing time of inbound payments while retaining safeguards used in traditional banking transactions, according to ABS-CBN and the Philippine Daily Inquirer.

Stablecoins would be used as a settlement instrument before the funds are converted to Philippine pesos and credited to recipients’ BPI accounts.

Coinbase to expand Singapore office headcount by 25%: Report

Cryptocurrency exchange Coinbase plans to expand its presence in Singapore and grow its headcount from 150 to about 200 staff members by the end of 2026.

The cryptocurrency exchange is mainly looking to hire more engineers, customer service, relationship management staff and institutional sales representatives for its Singapore office, which opened at One Raffles Quay on Wednesday.

Hassan Ahmed, Coinbase’s country director for Singapore, told the Business Times the exchange plans to expand its operations in Singapore because the city state is increasingly becoming a strategic hub for cryptocurrency innovation.

More Singapore crypto news:

— The Singapore Police Force and the U.S. FBI signed a memorandum of understanding to strengthen joint operations on online scams including crypto related scams, cyber fraud, and money laundering cases.

— Singapore based payments firm Triple-A reportedly lost $11.8 million after its hot wallet was drained. The firm said it was investigating but no customer funds were affected.

— The Monetary Authority of Singapore has tightened monetary policy, which will lead to the Singapore dollar appreciating by about 1% per year.

Hong Kong crypto giant HashKey merges regional exchange into one

Hong Kong digital asset services business HashKey Holdings has merged its HashKey Exchange and HashKey Global exchanges into a single platform and application.

Core jurisdictional hubs including Hong Kong, Singapore, the Middle East (Dubai) and Bermuda have been merged under a single platform.

The idea is that all users download the same application wherever they are, while the platform manages compliance on the back end with local regulatory frameworks.

News in brief from China

— A Hunan man was penalized under the Anti-Telecom and Online Fraud Law for reselling virtual currency for profit and for lending out his relative’s payment accounts to others so they could receive and transfer funds.

—Authorities in Shenzen have closed down numerous social media accounts for hyping up cryptocurrencies.

Cointelegraph publishes long-form journalism, analysis and narrative reporting produced by Cointelegraph’s in-house editorial team with subject-matter expertise. All articles are edited and reviewed by Cointelegraph editors in line with our editorial standards. Content published in here does not constitute financial, legal or investment advice. Readers should conduct their own research and consult qualified professionals where appropriate. Cointelegraph maintains full editorial independence.

Tether holds 97,141 bitcoin, enough to rank second among corporate holders if it were listed anywhere. It is not. There is no share, so there is no multiple, no premium, no discount, and no market referee on the largest private Bitcoin position in existence, funded by a business that earns more per employee than any company on earth.

Summary

- Tether holds 97,141 BTC, worth roughly $6 billion at current prices, accumulated under a 2023 policy of allocating up to 15% of realized quarterly operating profits to Bitcoin, most recently an 8,888 BTC transfer on New Year’s Day.

- If Tether were public, ranking services place it second among corporate holders behind Strategy’s 672,497 BTC. It is private, so every metric built to value Bitcoin treasuries, mNAV above all, simply does not compute.

- The funding model inverts the treasury-company template: Strategy and its imitators raise capital to buy Bitcoin, while Tether buys with retained profits from a reserve business that reported over $10 billion in net income for 2025.

- Bitcoin is one leg of a diversified reserve: roughly 116 metric tons of gold worth more than $17 billion, around $135 billion in US Treasuries by the issuer’s account, against approximately $185 billion of USDT in circulation.

- The same diversification cuts both ways: S&P downgraded USDT to its lowest stablecoin rating in December, citing disclosure gaps and a rising share of high-risk assets, meaning the accumulation that makes Tether a Bitcoin power is what a rating agency counts against it.

Every large corporate Bitcoin position in the world has a price attached to it, and not the price of the coins. Strategy has an mNAV. So does every listed treasury company, tracked in real time across a hundred names by analytics platforms that publish thirty metrics apiece: enterprise value over Bitcoin net asset value, premium or discount, diluted variants, debt-adjusted variants, the entire apparatus a market builds when it needs to decide what a pile of Bitcoin inside a corporate wrapper is worth. That apparatus has one conspicuous blind spot, and it happens to contain the second-largest corporate stack on earth. Tether holds 97,141 BTC, roughly $6 billion at current prices, accumulated quarter after quarter since 2023 under a policy of committing up to 15% of realized operating profits to the asset. Ranking services note that if Tether were a public company it would sit second behind Strategy, and then they file it on a separate page for private companies, holdings listed, valuation column blank, because there is no share, no float, no enterprise value, and therefore no multiple to compute. The most-watched metric in corporate Bitcoin cannot be applied to one of corporate Bitcoin’s largest holders. This piece is about that gap: what Tether actually holds, how the accumulation is funded, why the absence of a market price is more consequential than it sounds, and what a rating agency sees when it looks at the same balance sheet.

The position, itemized

Start with the stack and the pattern, because the pattern is more informative than any single figure.

The current disclosed holding is 97,141 BTC. The most recent visible additions trace a consistent rhythm: an 8,888.8 BTC transfer to the treasury wallet on January 1, worth roughly $778 million at the time and described by the chief executive as the Q4 2025 profit allocation, taking holdings above 96,000, followed by a smaller addition in April that brought the total to its present level. The policy behind the rhythm dates to May 2023: up to 15% of realized quarterly operating profits committed to Bitcoin, executed as periodic purchases and consolidated near quarter-end, a mechanical program, not a discretionary trade.

Bitcoin is one leg of a three-legged reserve strategy, and the other two are larger. Gold: roughly 116 metric tons as of the third quarter of 2025, valued above $17 billion by early this year, a position that makes Tether one of the largest private gold holders in existence. US government debt: approximately $135 billion by the chief executive’s own framing, which he described as positioning the company as the seventeenth-largest holder of US debt, with later reporting citing exposure figures around $141 billion. Against those reserves sits roughly $185 billion of USDT in circulation, and around the whole structure, per its Q3 2025 attestation, approximately $184.5 billion in stablecoin reserves against $215 billion in total assets, with roughly $23 billion in retained earnings and about $30 billion in group equity.

The scale comparison worth holding onto: Strategy’s 672,497 BTC is nearly seven times Tether’s stack, built with more than $50 billion of raised capital at an average cost around $75,000 per coin, and it constitutes that company’s entire reason for existing. Tether’s 97,141 BTC is a side position, roughly 3% of its total assets, accumulated from spare profit by a company whose actual business is something else entirely. That difference in kind, not the difference in size, is what makes the valuation problem interesting.

The machine that funds it

The accumulation model is the inverse of the sector it is usually grouped with, and the inversion explains why Tether can keep buying when the treasury companies cannot.

The digital asset treasury template, which this publication has covered from Strategy’s flywheel through the newer entrants, runs on capital markets. A company issues equity or convertible debt, buys Bitcoin with the proceeds, and depends on trading above its net asset value so that each issuance is accretive rather than dilutive. When the premium compresses, as it has across the sector this year, the machine stalls: raising becomes value-destroying, purchases stop, and the equity story unwinds. It is a leveraged bet on both Bitcoin and continued market enthusiasm for the wrapper.

Tether buys with cash it already earned. The reserve business generates income by holding predominantly short-term US government debt against tokens the public holds without interest, which produced more than $10 billion in net profit for 2025 and, on the company’s own account, roughly $500 million a month from Treasury holdings alone at one point last year. Fifteen percent of realized profits into Bitcoin is an allocation decision made after the money is in the door. No premium is required, no issuance, no market permission. The purchases continue at $63,000 exactly as they continued at $100,000, because the input is profit, not sentiment, which is why Tether kept accumulating through a drawdown that stopped much of the treasury-company sector cold.

That funding structure also makes Tether the clearest single illustration of stablecoin economics that this publication’s stablechain coverage has traced from the other direction. The float pays for everything: the Bitcoin, the gold, the chain investments, the venture portfolio, and the free-transfer subsidies underwriting the purpose-built USDT networks. A business that earns on other people’s dollar balances converts monetary demand into a balance sheet, and the Bitcoin position is simply the most visible artifact of that conversion.

The metric that cannot be computed

Now the gap, which is the piece’s actual subject.

For public treasury companies, mNAV is the governing number. It divides enterprise value, market capitalization plus debt and preferred equity, by the market value of the Bitcoin held. Above 1.0 means the market pays a premium for the wrapper, its strategy, its access to capital, its operating business. Below 1.0 means the market discounts even the coins. Analytics platforms track it across more than a hundred companies with real-time variants for dilution and capital structure, and the ratio has become the sector’s price-to-earnings equivalent, the number that decides whether a treasury company can raise, whether it should buy back, and whether its strategy is working.

Apply that to Tether and every input goes missing. There is no market capitalization, because there is no traded share. There is no enterprise value, because there is no market to compute it. There is no premium or discount, because nobody is bidding for a claim. The company has moved toward the edges of price discovery, a share buyback program was initiated last autumn and reporting has described interest from major investors in a private placement raising up to $20 billion, which would imply a valuation, but a negotiated private round is not a market price. It is one number agreed by a few parties under confidentiality, revealed selectively, and untested by anyone who might disagree.

The consequences are more than academic, and they run in both directions. Nobody can express a view: an investor who believes Tether’s Bitcoin is worth more than the market credits, or that the whole structure is worth less than claimed, has no instrument to trade. Nobody can be corrected: without a price, the company’s own attestations, disclosures, and framings are the primary information, and there is no continuously updated second opinion of the kind a share price provides. And nothing is disciplined: public treasury companies discovered this year that a compressing mNAV forces strategy changes, halted purchases, buybacks, defensive disclosure, because the market votes daily. Tether faces no such vote. The largest private Bitcoin position on earth is, in the most literal sense, unmarked, and the only external referees are the attestation firms and the rating agencies, which is where the story turns uncomfortable.

What the rating agency sees

S&P Global looked at the same balance sheet in December and reached a conclusion the accumulation narrative rarely mentions: it downgraded USDT to 5, the weakest grade on its five-point stablecoin stability scale, citing persistent gaps in disclosure and a rising share of high-risk assets in the reserves. The high-risk assets named include Bitcoin, gold, corporate bonds, and secured loans.

Sit with the symmetry, because it is the sharpest fact in this piece. Every headline celebrating Tether as a top-tier Bitcoin holder is describing, in the rating agency’s framework, the growth of the reserve component least suitable for backing a dollar-pegged liability. Both readings follow from the same asset. The company’s case, argued publicly by its chief executive against the downgrade, is that excess reserves and group equity absorb the volatility: roughly $7 billion in excess reserves and about $30 billion in group equity stand between a Bitcoin drawdown and the tokens, meaning the volatile assets are funded by capital rather than by the money backing USDT. That is a real argument and, on the disclosed figures, a substantially cushioned position.

The counter is equally real. The cushion is disclosed by the company and verified by attestation rather than by audit, a distinction this industry has debated for a decade; a Bitcoin drawdown of the severity Bitcoin has repeatedly produced would consume a large share of the stated excess in a single quarter; and the correlation problem is the one nobody models publicly, since the conditions that would trigger mass USDT redemption are precisely the conditions in which Bitcoin and gold would be falling and least convenient to sell. A reserve that is diversified in normal times can be concentrated in the only scenario that matters. That is not a prediction of failure. It is the reason a rating agency’s job exists, and the reason the missing market price matters: for a public company, a market would price that tail risk continuously and visibly. Here, one agency’s letter grade and the issuer’s rebuttal are the entire public debate.

What would make it pricable

Three developments would convert this position from an unmarked holding into a valued one, and each is at least plausible.

A completed private placement at scale, the reported raise of up to $20 billion with institutional participation, would produce a negotiated valuation for the whole enterprise. It would not be a market price, but it would be the first external number against which the Bitcoin, gold, and Treasury legs could be measured, and it would create shareholders with an interest in eventual liquidity.

Regulatory convergence is the second. The US stablecoin framework and its implementation, covered across this publication’s regulatory reporting, is steadily raising the disclosure floor for issuers serving American users, and Tether’s domestic-market vehicle brings part of the group inside that perimeter. Disclosure requirements are how private balance sheets become legible, and legibility is the precondition for valuation.

And a listing, the possibility every private financial company of this scale eventually faces, would resolve everything at once: a share price, an enterprise value, and finally an mNAV for the second-largest corporate Bitcoin holder in the world. There is no indication one is planned. But the buyback program, the private placement discussions, and the group-equity disclosures are the standard sequence of a company assembling the furniture a valuation event requires.

Until one of those lands, the situation stands as described: 97,141 bitcoin, roughly $6 billion, inside a company earning more than $10 billion a year, sitting on a spreadsheet somewhere with no multiple attached, in a sector that has built an entire analytical apparatus for exactly this question and cannot point it at the biggest private target in the field.

What to watch

The quarterly transfer. The 15% allocation makes each quarter’s profit-driven purchase a schedule, and the size of each transfer is a live read on the reserve business’s profitability, one of the few genuinely informative numbers a private issuer emits.

The next attestation. Excess reserves and group equity are the cushion the entire high-risk-asset debate turns on. Watch whether both grow with the Bitcoin position or lag it, since the ratio between them is the honest version of the risk question.

Any rating movement. S&P’s grade is the closest thing to an external referee. An upgrade on improved disclosure, or a further downgrade, moves the only public scorecard that exists.

The raise. Confirmation, size, and valuation of the reported private placement would supply the first external number for the enterprise, and with it the first opportunity to ask what the market thinks all that Bitcoin is worth inside this particular wrapper.

One final calibration, because Tether is not quite alone in this category and the comparison sharpens the point. Ranking services list at least one private entity with a larger claimed Bitcoin position, a technology company whose holdings, unlike Tether’s, cannot be verified on-chain at all, which produces a three-tier structure of corporate Bitcoin knowledge worth naming. Public companies disclose in filings and are priced continuously by markets. Tether discloses in attestations and is verifiable on-chain but priced by nobody. And a third tier claims holdings that are neither audited nor observable, existing purely as assertion. The industry’s data infrastructure, the trackers, the leaderboards, the dashboards with thirty metrics per company, handles the first tier well and quietly degrades across the other two, which means every statement about how much Bitcoin corporations own carries an error bar that grows as you move away from the listed names. That is worth remembering the next time a leaderboard is cited as though all its rows were equivalent evidence. Tether’s row is unusually good by the standards of private disclosure, on-chain verifiable, regularly attested, publicly discussed by its chief executive, and it still lacks the single thing that makes a corporate holding legible to markets: someone, somewhere, willing to state a price and be wrong about it in public.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. Holdings, reserve figures, and profit numbers reflect company statements, attestations, and third-party reporting that cannot be independently verified against audited financials, and asset values change continuously. Nothing here is a recommendation to buy, sell, or hold any asset. Always do your own research. Information is accurate as of July 26, 2026.

Frequently Asked Questions

How much Bitcoin does Tether hold?

97,141 BTC, worth roughly $6 billion at current prices. The position was built under a policy adopted in May 2023 of allocating up to 15% of realized quarterly operating profits to Bitcoin, with recent additions including 8,888.8 BTC transferred on January 1 as the Q4 2025 allocation and a smaller purchase in April.

Where does that rank among corporate holders?

Second, if it counted. Ranking services note Tether would sit behind only Strategy’s 672,497 BTC if it were a public company, but list it separately because it is private. Strategy’s position is nearly seven times larger and constitutes that company’s entire business model, while Tether’s is roughly 3% of total assets.

How is Tether’s accumulation different from a treasury company’s?

Funding. Treasury companies raise equity or convertible debt to buy Bitcoin and depend on trading above net asset value for issuance to be accretive, so purchases stall when the premium compresses. Tether buys with retained profits from its reserve business, which reported more than $10 billion in net income for 2025, so its purchases continue regardless of market sentiment toward any wrapper.

What is mNAV and why can it not be applied to Tether?

mNAV divides a company’s enterprise value by the market value of its Bitcoin, showing whether investors pay a premium or discount for the wrapper. It requires a traded share price, which Tether does not have. With no market capitalization, no enterprise value, and no float, every input is missing, so the sector’s governing metric simply does not compute for one of its largest holders.

Why does the absence of a market price matter?

Because a price is a continuous external opinion. Without one, no investor can express a view on whether Tether is over- or undervalued, no daily second opinion checks the company’s own disclosures, and no market discipline forces strategy changes the way a compressing mNAV has forced them across the public treasury sector this year. Attestations and rating agencies are the only external referees.

What else is in Tether’s reserves?

Predominantly US government debt, around $135 billion by the company’s own account, described by its chief executive as making Tether the seventeenth-largest holder of US debt, plus roughly 116 metric tons of gold valued above $17 billion, against approximately $185 billion of USDT in circulation. Bitcoin is the smallest of the three headline legs.

Why did S&P downgrade USDT if the reserves are diversified?

S&P cut USDT to 5, the weakest grade on its stablecoin scale, in December, citing persistent disclosure gaps and a rising share of high-risk assets including Bitcoin, gold, corporate bonds, and secured loans. The agency’s framework treats volatile assets backing a dollar-pegged liability as a risk, so the same accumulation celebrated as treasury strength counts against the stability rating. Tether’s response points to roughly $7 billion in excess reserves and about $30 billion in group equity as the buffer.

Could Tether ever be valued publicly?

Possibly, through three routes: the reported private placement of up to $20 billion, which would produce a negotiated enterprise valuation; regulatory convergence raising disclosure requirements as US stablecoin rules are implemented; or an eventual listing, which would supply a share price and, finally, an mNAV. None is confirmed, though a share buyback program and private-placement discussions are the customary preliminaries. This is educational analysis, not investment advice.

Ethereum price rallied 5% to $1,966 on July 27 as surging spot demand, short liquidations, and tighter available supply pushed ETH toward the key $2,000 barrier.

Summary

- Ethereum price gained 5% to $1,966, while 24-hour spot trading volume jumped 118.53% to $9.21 billion.

- The daily chart places $1,981.50 and $2,000 as the next major resistance zones.

- 4-hour RSI reached 73.36, showing strong momentum but raising the risk of a short-term pullback.

- Liquidation data shows large leverage clusters near $1,980–$2,000, with downside liquidity around $1,930.

- Analysts see $2,350–$2,500 as possible targets if ETH establishes support above $2,000.

Ethereum price rally targets $2,000

According to data from crypto.news, Ethereum (ETH) price climbed to around $1,966 after trading near $1,870 during the previous session, extending a recovery that began from its June low near $1,512. The latest move brought ETH within 2% of the psychological $2,000 level.

Spot trading volume increased 118.53% over 24 hours to $9.21 billion, according to the supplied market data. Rising volume alongside price suggests buyers supported the advance rather than the move occurring during thin trading conditions.

The daily chart shows ETH reaching an intraday high of $1,981.24 before easing toward $1,964. That high closely matches the 100% Fibonacci retracement level at $1,981.50, making the $1,981–$2,000 area the first major test for the recovery.

Ethereum has already reclaimed the 78.6% Fibonacci level at $1,880.97. Below that price, the next retracement levels sit at $1,802.05, $1,746.62, and $1,691.19.

The daily Supertrend has also switched to bullish support at approximately $1,772.31. ETH would need to fall below that level before the broader recovery structure faces a more serious invalidation risk.

Spot demand and supply pressure support ETH

Ethereum’s rally coincided with a sharp increase in market activity and a reported rise in its staking rate to a record 34%. Staked tokens cannot immediately enter the spot market, reducing the liquid supply available to buyers during periods of stronger demand.

Higher Layer 2 throughput and decentralized finance activity have also increased smart contract execution. Under Ethereum Improvement Proposal 1559, part of each transaction’s base fee is burned, removing ETH from circulation when network usage rises.

These supply conditions do not guarantee further gains, but they can magnify price movements when demand accelerates. A smaller pool of liquid ETH means buyers may need to bid at progressively higher prices to complete large spot purchases.

US spot Ethereum exchange-traded funds provide another source of demand. The supplied market context indicates that the products recovered from volatile outflows earlier in July and began recording more consistent net inflows.

For US investors, sustained ETF inflows would offer evidence that regulated demand is strengthening alongside activity in native crypto markets. However, the upcoming Federal Reserve interest-rate decision remains a key risk because a hawkish policy signal could reduce demand for high-beta assets such as ETH.

Technical indicators warn of short-term overheating

Ethereum’s 4-hour chart shows the price moving inside an ascending parallel channel that has guided the recovery since early July. ETH recently rebounded from the channel’s lower boundary near $1,850 and returned to the $1,965 region.

The Aroon Up indicator stands at 92.86%, compared with Aroon Down at 14.29%. That wide gap indicates that recent highs are arriving more frequently than recent lows, supporting the bullish short-term structure.

Momentum is becoming stretched, however. 4-hour relative strength index reached 73.36, above the conventional overbought threshold of 70 and well above its moving average at 55.41. This reading does not require an immediate reversal, but it raises the chance of consolidation or profit-taking near $2,000.

The daily moving average convergence divergence indicator remains constructive. Its MACD line sits at 46.51, above the 40.75 signal line, while the positive histogram reads 5.76. Those values show that upward momentum remains active despite ETH approaching resistance.

A daily close above $1,981.50 would clear the full Fibonacci recovery level shown on the chart. Bulls would then need to reclaim $2,000 as support before targeting the upper portion of the 4-hour channel near $2,050–$2,100.

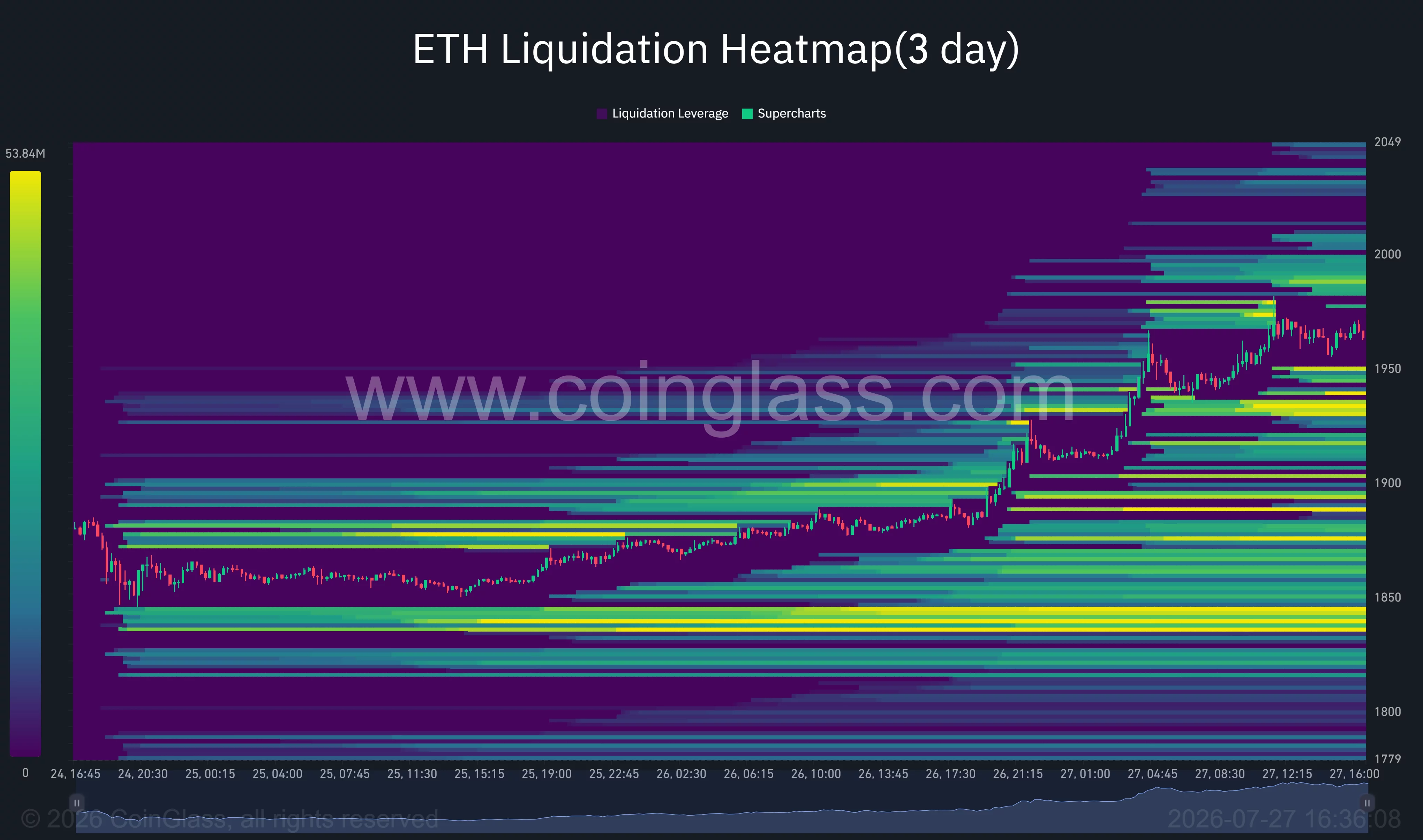

Ethereum liquidations could accelerate the breakout

CoinGlass’s three-day liquidation heatmap shows concentrated leverage immediately above the current price. The strongest nearby clusters appear around $1,980–$2,000, with additional liquidity extending toward $2,040.

A move into those levels could force leveraged short positions to close through market purchases. That process may create another short squeeze and help ETH move through resistance, particularly if spot volume remains elevated.

The heatmap also maps downside liquidity around $1,945–$1,930, followed by larger concentrations near $1,900–$1,880. A rejection from $2,000 could attract price toward those areas as leveraged long positions unwind.

The largest lower cluster appears around $1,835–$1,850. That zone aligns with the 4-hour channel floor and gives bulls a major defensive area if ETH loses $1,880. A break below it would expose $1,802, followed by the daily Supertrend near $1,772.

Analysts map $2,350 to $2,500 ETH targets

According to market commentator Michaël van de Poppe, Ethereum may consolidate before beginning another upward leg.

“Matter of time until it runs towards $2,500 (which is the other side of the range).”

Analyst Ted Pillows also pointed to rising spot demand but placed the immediate condition at $2,000.

“If Ethereum manages to break and reclaim $2,000 here, it could rally to May highs.”

Pillows’ chart places intermediate resistance near $2,191 and a larger supply zone around $2,350–$2,400. These targets remain conditional on ETH closing above $2,000 and holding that level during a retest.

Failure to reclaim $2,000 would favor short-term consolidation toward $1,930 or $1,881. The bullish structure remains intact above the ascending channel floor, while a decisive loss of $1,850 would weaken the current recovery thesis.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Jim Cramer says Washington will not let Nvidia lose the artificial intelligence race to China. He frames the US government as a quiet backstop behind the chipmaker’s biggest bets.

Commerce Secretary Howard Lutnick controls power access to a federal site in Ohio. Nvidia is negotiating a $250 billion guarantee there for OpenAI, tying the chipmaker to a government decision.

Nvidia’s Backstop Meets Washington’s Power Switch

Nvidia is in talks to guarantee roughly $250 billion in financing for OpenAI’s lease, the Wall Street Journal reported. The deal covers a 10-gigawatt data center campus in Piketon, Ohio.

The site sits on decommissioned federal land. The full project, including chips, could exceed $500 billion.

Electricity for the campus flows from a natural gas plant that Japan is funding with a $33 billion investment. That investment is part of a recent US trade deal.

Lutnick decides which company gets access to that power. OpenAI, Anthropic, Microsoft, and Google have all approached him about the site.

Washington in Deep with Nvidia, Says Cramer

On Monday night’s episode of “Mad Money,” Cramer linked Nvidia’s financial strength to Washington’s stake in the outcome.

“They have the best balance sheet of any company in the world,” Cramer said. He added that the government is a “subtle backstop” so China does not win the AI race.

Nvidia’s cash and a government hand on the power switch make a powerful combination. That combination helps explain why Cramer still calls Nvidia a stock to own even as shares slide.

Not everyone agrees the setup is healthy. Investor Michael Burry has called the arrangement circular.

He argues Nvidia’s guarantees would fund OpenAI’s purchases of Nvidia’s own chips. Nvidia is discussing that separate chip financing package, which could reach $350 billion. OpenAI also lacks its own investment-grade credit rating, a gap that already caused other financing troubles this year.

The bigger question is what happens if Washington’s role in AI infrastructure becomes the industry’s financing template. That role already includes Jensen Huang’s open-model push and Nvidia’s new security alliance.

The post Jim Cramer Says the US Government Is Nvidia’s Silent Backstop appeared first on BeInCrypto.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

As economic pressures rise, XRPPower is drawing attention with AI-powered digital asset services and questions about its platform model.

Summary

- XRPPower gains attention as investors explore AI-powered digital asset services amid rising economic uncertainty and market volatility.

- The platform highlights its AI-driven digital asset platform as users seek new income opportunities in the evolving fintech landscape.

- It has expanded its digital asset services, promoting automated solutions as financial uncertainty drives demand for alternative income tools.

The ever-changing global situation and economic and financial market uncertainties are impacting the lives of more and more ordinary people. Rising prices, increased living costs, and financial market volatility have made “how to protect one’s income and savings” a pressing issue for many families.

For salaried workers, monthly salaries may increasingly struggle to cover rising living expenses; for ordinary businesses, operating costs and market changes bring new pressures; and for retirees, how to better utilize their accumulated savings to cope with future living expenses is also a real problem.

When existing income cannot meet expenses, some people choose credit cards, loans, or other borrowing methods to alleviate short-term financial pressure. However, borrowed money must eventually be repaid, and interest and debt may further increase long-term burdens. Therefore, finding additional sources of income besides wages is becoming a growing concern.

Entering 2026, with the rapid development of artificial intelligence and fintech, various automated digital asset services are also gaining attention. Against this backdrop, XRPPower has come into the public eye, proposing to provide 365-day-a-year digital asset services through an intelligent system.

However, for those hearing the name for the first time, the most important question might not be the number of features it advertises, but rather: What kind of platform is XRPPower? Does it actually exist? And can its described services and revenue model withstand scrutiny?

Yes, XRPPower is a genuine platform that offers long-term returns

According to publicly available information from XRPPower, it has been operating since 2023 and will continue to grow until 2026, entering its third year of operation. For a digital asset platform, long-term stable operation is sufficient proof of its reliability.

Meanwhile, XRPPower-related content has also been disseminated through multiple international internet and financial information channels, including GlobeNewswire, Yahoo, and The Globe and Mail. Users can search for the XRPPower name to find past press releases, company updates, and related information, gaining a deeper understanding of the platform’s true development trajectory from publicly available records at different times.

How to Get Started with XRPPower

1. Free Account Registration

2. Choose a suitable contract

The platform offers contract options ranging from $100 to $100,000, allowing users to choose flexibly according to their needs. Before purchasing, they can view the corresponding period, yield rules, and related terms.

3. Deposits and withdrawals

XRPPower supports deposits and withdrawals in major cryptocurrencies such as BTC, XRP, and USDC. Users can choose based on the supported currencies.

4. Daily contract earnings check

During contract execution, earnings generated according to the corresponding product rules will be automatically credited to an account balance, which can then be withdrawn.

5. Earn rewards by inviting friends

Users can share their invitation codes or links. After friends register and meet the corresponding conditions, you can receive referral rewards; according to the platform’s published plan, some referral rewards can reach up to 5%. Transparency, Intelligence, and Security: How Does XRPPower Lower the Barrier to Entry for Users?

Why are more and more people choosing XRPPower?

According to publicly available information, XRPPower is headquartered in London, UK, and prioritizes compliance with relevant laws, regulations, and requirements during its operations. Regarding contract issues, which are of great concern to users, the platform emphasizes transparency: the period, amount, profit rules, and related conditions of different yield contracts are displayed before purchase, allowing users to understand the rules before deciding whether to participate.

In terms of user experience, XRPPower applies an intelligent AI system to the platform. Whether a new user or an existing user, there is no need for frequent operations or long-term monitoring. After a user selects and purchases a contract, the system automatically runs according to the corresponding rules, making digital asset management simpler.

Regarding security and risk management, XRPPower states that it implements the auditing, risk management, and internal control concepts adopted by international professional institutions such as PwC, and enhances the platform’s protection capabilities through multi-layered account and fund security mechanisms.

Summary: Opportunities come from understanding and choice

Since 2023, XRPPower has reported over 3 million registered users. After three years of development, the platform has continuously improved its intelligent system, contract mechanisms, and digital asset services, providing global users with a simpler and more transparent way to participate.

For those seeking additional income opportunities, the first step is not blind investment, but understanding. Register NOW for XRPPower for free to view the platform’s contract rules, profit mechanisms, deposit and withdrawal processes, and related risks, and then decide whether to participate based on personal circumstances.

In today’s world of rising living costs and a constantly changing financial environment, more choices mean more possibilities.

Choice is sometimes more important than effort, and opportunities often favor those who are willing to learn in advance and prepare.

For more information, visit the official website.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Bitmine Immersion Technologies reported that it added nearly 10,000 Ether (ETH) over the past week, lifting its total ETH holdings to 5.79 million. The company disclosed the purchases in an update released Monday, with Ether now forming a substantial part of its overall treasury.

According to Bitmine, it holds 5.79 million ETH, representing about 4.8% of Ether’s total supply. Roughly 4.9 million ETH—about 85% of its position—is staked via the company’s validator operations, and Bitmine projected annualized staking rewards of around $299 million once all of its Ether is deployed across its staking infrastructure and partner validators. The company also said its total crypto assets, cash, and marketable securities total $11.8 billion as of July 26.

Key takeaways

- Bitmine Immersion Technologies increased its Ether holdings by nearly 10,000 ETH to 5.79 million.

- About 85% of Bitmine’s Ether position is staked through its validator operations.

- Bitmine projects annualized staking rewards of approximately $299 million once its full stake is deployed.

- The buys follow a week in which Ether outperformed Bitcoin, supporting a stronger ETH/BTC ratio.

- Bitmine’s accumulation approach appears to be diverging from Strategy, which has paused Bitcoin purchases in recent weeks.

Bitmine’s Ether treasury grows, with most coins staked

Bitmine’s latest disclosure centers on the continued expansion of its corporate Ether treasury. The company said it now holds 5.79 million ETH after purchasing nearly 10,000 ETH during the previous week.

Staking is a central part of that story. Bitmine stated that about 4.9 million ETH—around 85% of its holdings—are staked through its validator operations. In addition to describing its current staking footprint, the company gave an outlook for when its entire Ether balance will be placed across its staking infrastructure and partner validators. Bitmine projected annualized staking rewards of roughly $299 million once that process is complete.

From an investor perspective, the staking-heavy structure matters because it changes how treasury value may be expressed over time. Instead of relying solely on spot appreciation, Bitmine is explicitly tying a large portion of its ETH exposure to ongoing network rewards.

Why the timing looks strategic as ETH leads BTC

Bitmine’s purchases arrive during a period when Ether has been comparatively stronger against Bitcoin. According to CoinGecko data, ETH gained about 2.4% over the past seven days, while Bitcoin fell roughly 0.7% in the same timeframe.

In Monday’s announcement, Bitmine Chairman Tom Lee pointed to the rising ETH/BTC ratio as a signal. He characterized the ratio as being at a three-month high and said it indicated strengthening momentum for Ether.

Even if the immediate magnitude of daily price moves remains difficult to forecast, corporate buying decisions often reflect a broader view of relative positioning—particularly for firms seeking to build a dominant share of a given asset exposure. In this case, Bitmine’s continued accumulation coincides with a week where Ether has outpaced Bitcoin, reinforcing the narrative that its ETH thesis may be gaining traction across the market.

Bitmine vs. Strategy: accumulation strategies diverge

Bitmine has positioned itself as one of the most active corporate ETH treasuries. The company said it has built the world’s largest corporate Ether treasury and noted that it trails only Strategy among public companies by the value of its digital asset holdings.

However, the update also highlights a divergence from Strategy’s more recent approach. Bitmine’s accumulation strategy has recently differed from Strategy’s, which has paused Bitcoin purchases in recent weeks.

Earlier this month, Strategy announced it had raised $544.5 million through stock sales, repurchased $25 million of its STRC preferred shares, and increased its US dollar reserve to $3.75 billion, while maintaining holdings of 843,775 BTC.

That contrast matters because it underscores that “treasury strategy” is not uniform across the sector. While Bitmine appears to be leaning further into ETH accumulation and staking deployment, Strategy’s recent communications suggest a shift toward capital and reserve management around its BTC exposure. For observers, the key question is whether Strategy’s pause reflects timing, liquidity needs, or a longer-term recalibration of how it wants to allocate capital.

Total treasury size and staking deployment remain what to watch

Beyond the ETH purchase itself, Bitmine provided a snapshot of its broader balance sheet. The company said its crypto holdings, cash, and marketable securities total $11.8 billion as of July 26. This figure may help explain how firms sustain large, ongoing purchases without disrupting other liquidity priorities.

Looking ahead, two items are likely to draw attention. First, Bitmine’s projection of annualized staking rewards depends on full deployment of its Ether across its staking infrastructure and partner validators. Second, market participants will watch whether Bitmine continues adding ETH after this week’s purchases—especially given the near-term strength in ETH relative to Bitcoin and Bitmine’s interpretation of that movement via the ETH/BTC ratio.

For now, Bitmine’s disclosures reinforce that corporate Ether treasuries are increasingly paired with staking operations, turning holdings into a long-running revenue mechanism rather than a purely directional bet. The next signals to monitor are the pace of further ETH acquisitions and the timing of complete staking deployment relative to the company’s stated plan.

Strategy, the business intelligence firm best known for holding one of the largest corporate Bitcoin treasuries, continued reshaping its capital structure last week by combining common stock sales with buybacks of its preferred shares.

According to company disclosures, Strategy sold 5,429,160 shares of its Class A common stock through its at-the-market (ATM) program between July 20 and July 26, bringing in $544.5 million in net proceeds. In parallel, it repurchased 288,930 shares of its STRC preferred stock for $25 million, as detailed in a Form 8-K filed with the U.S. Securities and Exchange Commission on Monday.

Key takeaways

- Strategy raised $544.5 million in net proceeds via its July 20–26 ATM common stock sales.

- In the same period, the company repurchased $25 million worth of its STRC preferred stock through buybacks.

- Despite the capital activity, Strategy reported no Bitcoin buys or sales for July 20–26, keeping holdings steady at 843,775 BTC.

- Strategy’s U.S. dollar reserve increased to $3.75 billion as of July 26, up from $3.225 billion the previous week.

- Recent remarks by Michael Saylor on X fueled speculation about Strategy’s preferred-stock strategy, though the filings show only what the company actually executed.

ATM stock sales and preferred buybacks

Strategy’s latest capital moves were carried out through both of the mechanisms it has relied on to fund its broader financial strategy. First, the company used its at-the-market offering program to sell additional shares. The reported sale volume—5,429,160 shares of Class A common stock—translated into $544.5 million in net proceeds over the July 20–July 26 window.

Separately, Strategy used preferred share repurchases to alter its balance-sheet composition. The company repurchased 288,930 shares of STRC preferred stock for $25 million, according to the Form 8-K filed Monday.

Market reaction followed the news as traders digested the mix of issuance and repurchases. Yahoo Finance data referenced by the original reporting indicated STRC preferred shares were up about 2.3% to $88.90 ahead of the Nasdaq open, while Strategy’s common shares were also higher in Monday’s premarket activity.

Why the cash reserve matters for Strategy’s structure

Following additional fundraising through its ATM program, Strategy increased its U.S. dollar reserve to $3.75 billion as of July 26. The company’s prior reserve level was $3.225 billion the week before, meaning the latest funding cycle added roughly half a billion dollars to the cash buffer over a short period.

Just as important for investors is that Strategy reported no Bitcoin purchases or sales during July 20–26. Its Bitcoin holdings remained unchanged at 843,775 BTC, acquired at an average purchase price of $75,476 per bitcoin, for $63.69 billion in aggregate. In other words, the week’s financing activity appears to have been directed toward liquidity and capital structure rather than changing the size of the treasury.

Strategy’s growing cash reserve reflects an operational need that goes beyond flexibility in market conditions. The reserve is intended to support dividend payments on its preferred stock and interest payments on its outstanding debt—requirements that make near-term liquidity particularly relevant for a company balancing treasury strategy with obligations across its capital stack.

Saylor’s posts reignite debate on Bitcoin and banks

These financial filings arrived in the wake of renewed debate sparked by Strategy executive chairman Michael Saylor on X. Earlier in the week, Saylor’s comments pushed the same discussion back to the forefront: whether Bitcoin’s long-term growth depends on integration with traditional financial institutions.

On Sunday, Saylor wrote that rejecting Bitcoin’s links to financial infrastructure would deny access to most potential users. The argument drew criticism from some Bitcoin supporters, who argue that greater reliance on banks runs counter to Bitcoin’s original goal as a peer-to-peer electronic cash system designed to minimize the need for financial intermediaries.

Supporters and critics both claim alignment with Bitcoin’s fundamentals, but they emphasize different layers of adoption. For those skeptical of bank involvement, the concern is that mainstream routing through established institutions could undermine the network’s decentralized promise. For those taking Saylor’s position, the focus is on distribution—how institutions can act as conduits for broader user access.

The renewed discussion also followed an earlier Saylor post in which he wrote, “We’re gonna need another color,” prompting speculation among market observers about possible adjustments to Strategy’s preferred stock approach. While the speculation highlighted investor attention to Strategy’s preferred instrument strategy, the week’s documented actions remain tied to the specific transactions reported in regulatory filings.

What to watch next

With Strategy maintaining a steady Bitcoin position during the July 20–26 window while simultaneously building cash reserves and adjusting preferred shares, the next signals to monitor are whether future filings show additional preferred share changes, further increases in the dollar reserve, or a shift back toward Bitcoin purchases. The balance between financing activity and treasury execution is likely to remain the key question for investors tracking how Strategy translates capital markets access into long-term Bitcoin exposure.

Why Jackson Koivun’s unorthodox swing is so effective

Why is China cracking down on AI-powered companions?

KOSPI Crashes 8% as AI Chip Selloff Slams Asian Markets

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Brooks Brothers

-

Crypto World7 days ago

Crypto World7 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

NewsBeat6 days ago

NewsBeat6 days agoHow a former Blue Peter presenter stunned America’s Got Talent judges

-

Tech1 day ago

Tech1 day agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Tech7 days ago

Tech7 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

Business6 days ago

Business6 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Entertainment6 days ago

Entertainment6 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

Crypto World5 days ago

Crypto World5 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics15 hours ago

Politics15 hours agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

NewsBeat7 days ago

NewsBeat7 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Sports4 days ago

Sports4 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Sports1 day ago

Sports1 day agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Fashion4 days ago

Fashion4 days ago16 Dresses for the High Summer Event

-

News Videos4 days ago

News Videos4 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Politics2 days ago

Politics2 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Entertainment4 days ago

Entertainment4 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

Crypto World7 days ago

Crypto World7 days agoAndrew Cuomo joins OKX board as crypto exchange expands in U.S.

-

News Videos1 day ago

News Videos1 day agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Crypto World2 days ago

Crypto World2 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

NewsBeat7 days ago

NewsBeat7 days agoNADINE DORRIES: I have witnessed first-hand what happens to new Prime Ministers when they enter No 10… and this is why Andy Burnham will be out by May

You must be logged in to post a comment Login