Crypto World

Circle Enlists Sasai to Expand USDC for Africa Cross-Border Payments

Circle is expanding the use of its USD Coin (USDC) across Africa through a strategic partnership with Sasai Fintech. The collaboration aims to weave USDC into Sasai’s payments fabric, covering cross-border transfers, enterprise payments, and consumer wallets, with the goal of lowering costs and shortening settlement times for users across multiple markets.

In a Business Wire release, Circle and Sasai described integrating USDC into Sasai’s infrastructure to unlock practical on-chain use cases for the stablecoin within Sasai’s network. Sasai operates digital payments services across several African markets, and the partnership would connect Circle’s on-chain rails with Sasai’s cross-border and mobile-payment ecosystem.

Circle CEO Jeremy Allaire framed the collaboration as part of the company’s broader focus on high-growth payment corridors in emerging markets, while Cassava Technologies Chairman Strive Masiyiwa highlighted the potential to broaden access to digital financial services for both businesses and consumers.

Data from DefiLlama shows USDC remains the second-largest stablecoin by market capitalization, at roughly $78.6 billion, trailing only Tether’s USDT, which sits around $184.1 billion. The size of USDC liquidity underscores the potential scale that could flow into Africa’s payments rails as the ecosystem grows.

The rise of crypto and stablecoins in Africa

Africa has witnessed a notable uptick in crypto activity, with Sub-Saharan Africa showing a 52% year-over-year increase in on-chain activity in the 12 months through June 2025, tallying more than $205 billion in on-chain value, according to Chainalysis data cited in recent market coverage. Nigeria accounted for the largest share of that activity—over $92 billion—followed by South Africa, Kenya, Ethiopia, and Ghana. Remittances, cross-border payments, and hedging against currency volatility are among the leading use cases driving this surge.

The region’s crypto expansion is drawing attention from global players expanding into Africa. For example, Blockchain.com announced Ghana-focused expansion as part of its broader push across the continent, reflecting growing demand for retail and institutional access to digital assets and stablecoins as a payment and settlement layer.

Regulatory developments are also beginning to mature alongside growth. Ghana’s Securities and Exchange Commission approved 11 crypto trading platforms to operate within a regulatory sandbox framework under the country’s Virtual Asset Service Providers Act, signaling a structured pathway for crypto services to scale with oversight.

Beyond the technology itself, policymakers and industry participants emphasize stablecoins as a faster, lower-cost alternative to traditional remittance routes. The World Bank continues to highlight an urgent cost challenge: while the global target is to bring average remittance costs below 3%, many economies in Sub-Saharan Africa still register higher levels. A World Bank analysis noted that in 2023 several economies, including Sierra Leone, Uganda, Angola, Botswana, and Zambia, faced remittance costs above 7%.

What this partnership signals for investors and users

The Circle–Sasai collaboration arrives as Africa’s payments ecosystem matures, with an emphasis on onboarding more people into digital finance through stablecoins and mobile-first services. For investors, the deal highlights a growing preference among builders and operators to anchor on-chain liquidity with regionally relevant rails. By anchoring USDC into Sasai’s breadth of services—cross-border transfers, enterprise payments, and consumer wallets—the collaboration could reduce settlement times and processing costs for a broad set of use cases, from small-business payments to worker remittances.

For users, the on-ramp to digital finance in Africa can become more accessible and affordable as stablecoin rails are integrated with everyday payment flows. The combination of Sasai’s regional reach and Circle’s global on-chain platform could create a more seamless experience for individuals and businesses moving money across borders or paying suppliers in other countries, with USDC serving as the common settlement asset.

On the regulatory front, the Ghana sandbox move demonstrates how governments are approaching crypto infrastructure with a combination of oversight and opportunity. This framework can help standardize participation for exchanges and wallets while preserving consumer protections, a development that could encourage broader adoption and more predictable interoperability between on-chain assets and traditional payment rails.

Another dynamic to watch is the broader regional push by established crypto firms into Africa. The combination of rising adoption, improving regulatory clarity, and the entry of global players into local ecosystems could accelerate the velocity of stablecoin use, especially in corridors where remittances and cross-border payments have historically been costlier and slower. If the trend continues, we could see more enterprise-grade solutions built on USDC that specifically target Africa’s fragmented payment landscape, potentially unlocking new business models for remittance corridors, supplier payments, and consumer wallets alike.

The next few quarters will be critical for measuring impact. Key questions include how quickly Sasai can operationalize USDC rails across its markets, what the actual cost savings look like for end users, and how regulators across the region balance supervision with innovation. Market participants will also be watching for concrete usage metrics—volume, settlement times, and cross-border transaction costs—as real-world adoption begins to take hold. As Africa’s crypto infrastructure evolves, collaborations like Circle and Sasai’s could lay the groundwork for a more inclusive digital economy where stablecoins help bridge traditional finance and mobile-first financial services.

Readers should watch for updates on deployment milestones, regulatory progress, and early usage data from Sasai’s network as USDC-enabled services begin to roll out across the continent. The collaboration represents more than a single partnership; it signals a notable shift toward scalable, on-chain payment rails tailored for Africa’s distinctive market dynamics.

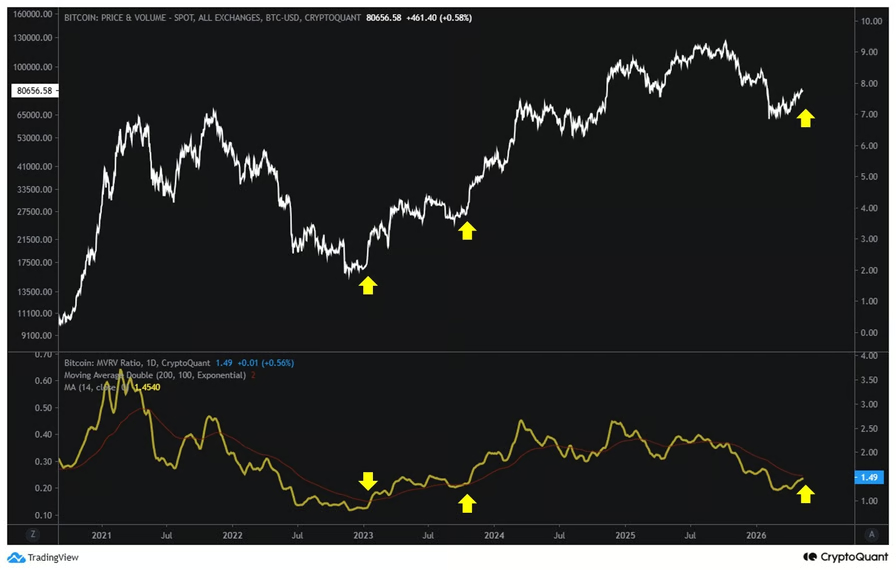

Bitcoin (BTC) could be set for an extended uptrend, with a pending bullish signal from a key valuation metric suggesting that BTC prices might go “much higher,” according to crypto analysts.

Key takeaways:

- Bitcoin’s MVRV golden cross signals a shift to bullishness, historically preceding prolonged price rallies.

- Bitcoin traders argue $60,000 was the bear market bottom, see “huge” BTC price breakout next.

Bitcoin MVRV momentum sends a “trend reversal signal”

Bitcoin’s Market Value to Realized Value (MVRV) ratio, an indicator that measures whether the asset is overvalued, is about to print a “golden cross,” an occurrence that has previously preceded massive price rallies, according to CryptoQuant analyst CW8900.

Related: Saylor signals another Bitcoin buy after hinting at selling in Q1 earnings call

“A golden cross between the $BTC MVRV Ratio and the 200D EMA line is imminent,” the analyst said in an X post on Sunday, adding:

“This signal is a representative trend reversal signal and is a bullish indicator.”

Bitcoin MVRV momentum indicator. Source: CryptoQuant

The last time the indicator produced this bullish crossover was just after the 2022 cycle bottom, preceding a 90% BTC price rally to $31,000 from $16,300 in Q1 2023. Another cross in September 2023 was followed by a 400% bull run to the current all-time high of $126,000 reached in October 2025.

In an earlier analysis, CW8900 highlighted a golden cross when the 30-day simple moving average (SMA) of Bitcoin’s MVRV ratio crossed above its 90-day SMA in late April, saying:

“$BTC has completely turned to a bullish trend.”

Source: CW8900

Meanwhile, Bitcoin’s recent rally to $83,000 boosted the short-term holder (STH) cost basis level as newer buyers returned to profitability.

STH cost basis refers to the average purchase price of investors who have held Bitcoin for less than 155 days.

The chart below shows that the price could rise higher to touch the “heated” band of this metric, currently at $92,000.

Despite profit-taking at current prices, the STH risk zone suggests BTC can go higher in the short term with the “heated” band at $92,000 and the overheated band at $104,000.

Bitcoin short-term cost basis bands. Source: Glassnode

Bitcoin analysts say BTC’s “huge breakout” is coming

As Cointelegraph reported, analysts say Bitcoin is at a make-or-break point as it retests the 200-day moving average at $82,500.

A break above this level could end the multi-month downtrend, while a rejection could result in a fresh sell-off toward $50,000.

Analyst Shib Spain argues that BTC’s break above a multi-month downtrend line on the weekly chart marked a structural shift from bearish dominance, reinforced by a bullish crossover from the MACD indicator.

“Bitcoin’s huge breakout is coming. MACD bullish reversal forming,” the analyst said in a recent post on X, adding:

“The bull run is just getting started.”

BTC/USD daily weekly chart. Source: Shib Spain

Fellow analyst Moustache highlights the BTC market cap and its RSI bouncing off multi-year support lines on the monthly time frame, as shown in the chart below.

“Just like in 2022, I’ve called the bottom for $BTC again this cycle,” the analyst said in an X post on Monday, adding:

“Prices will go much, much higher. We’ve got something big to look forward to.”

Bitcoin market cap, USD. Source: X/Moustache

As Cointelegraph reported, several analysts predict a “supercycle” rally toward $180,000-$250,000 as early as this year, supported by institutional accumulation and a strengthening technical setup.

TLDR

- The Senate Banking Committee scheduled May 14 for the markup of the CLARITY Act.

- Lawmakers will debate amendments before voting on whether to advance the bill to the Senate floor.

- The House previously passed the CLARITY Act with a 294–134 bipartisan vote.

- The bill would define regulatory boundaries between the SEC and the CFTC.

- The Senate version expands the legislation to nine titles, including stablecoin oversight and bankruptcy protections.

The Senate Banking Committee will meet May 14 to mark up the Digital Asset Market Clarity Act. Lawmakers will debate amendments and decide whether to send the measure to the Senate floor. However, bank lobbyists and some Democrats now threaten to block the bill before it advances.

CLARITY Act Faces Senate Test After House Approval

The committee will hold the executive session at 10:30 a.m. in Room 538 of the Dirksen Senate Office Building. Chairman Tim Scott confirmed the schedule last week and opened the meeting to public livestream. Lawmakers will consider amendments before voting on whether to advance the bill.

The House passed H.R. 3633 on July 17, 2025, with a 294–134 bipartisan vote. All 216 Republicans supported the measure, while 78 Democrats joined them. Since then, the Senate delayed two markup sessions and extended talks over stablecoin oversight.

The CLARITY Act would define regulatory boundaries between the SEC and the CFTC. The bill grants the CFTC authority over spot markets for digital commodities. Meanwhile, the SEC would retain control over investment contract assets and primary offerings.

Senators expanded the Senate draft to nine titles covering decentralized finance safeguards and illicit finance rules. The text also includes bankruptcy protections for crypto customers and the Blockchain Regulatory Certainty Act. That provision would provide safe harbors for blockchain software developers.

Banking Lobby and Democratic Ethics Dispute Intensify

Major banks have increased lobbying efforts in recent weeks as the vote approaches. At the same time, Democrats demand ethics rules covering crypto holdings by public officials. Republicans argue that such provisions could derail the measure entirely.

Senators Cynthia Lummis and Bernie Moreno warned about tight legislative deadlines. They said failure to clear committee before the May 21 Memorial Day recess could delay action until 2030. The White House has set July 4 as its target for presidential approval.

SEC Chair Paul Atkins urged Congress on April 9 to advance the bill. He said both agencies stand ready to implement the framework once enacted. Atkins referenced “Project Crypto” as an internal readiness initiative.

Treasury Secretary Scott Bessent framed the legislation as a national security issue in a Wall Street Journal op-ed. He warned that regulatory gaps push blockchain firms toward Singapore and Abu Dhabi. White House crypto adviser Patrick Witt said negotiations over stablecoin yield have concluded.

Senator Lummis reiterated support after the Easter recess and wrote “Clarity” on X.

Speaking at the Bitcoin Conference, she stated, “We are gonna markup the CLARITY Act in May.” She added, “We are gonna get it to the finish line.”

Chairman Scott previously targeted September 2025 for a floor vote. He later moved the timeline to late 2025 and then to June or July 2026. The May 14 markup now represents the Senate’s first formal committee vote on the bill.

A comparative analysis published on May 11 by XWIN Japan tracked how Bitcoin, Ethereum, XRP, BNB, and Solana held up during the six months of market stress between October 2025 and April 2026.

According to the report, that downturn was less about panic selling alone and more about “internal selection,” with investors separating Bitcoin from the broader altcoin market amid macro stress and shrinking liquidity.

Bitcoin Stayed Ahead While Altcoins Took Deeper Losses

Going by XWIN’s data, BTC dropped 52.5% in that period, going from a peak of around $126,000 to roughly $60,000. And while that was a brutal fall in absolute terms, compared to the rest of the group, the flagship crypto held up better.

Solana got battered the most. It fell 71.6% from its highest level of $238 to $67. At the same time, Ethereum and XRP declined by 63%, while Binance Coin dropped 59%.

In terms of recovery from their bottom prices, SOL enjoyed the biggest bounce at 38%, with Bitcoin the second-best at 34.7%.

XWIN Japan’s analysis divided the six-month period into three phases, namely a derivatives-driven unwind in late 2025, a macro fear and liquidity contraction phase in early 2026, and an institutional-led recovery this spring.

What it found, broadly, is that BTC’s relative resilience wasn’t accidental, with the report pointing to ETF inflows, corporate treasury buying, and demand as a geopolitical hedge as ongoing sources of support through the worst of the selling.

“Even during market stress, capital consistently returned to Bitcoin,” the analysis stated, describing BTC as having become a global macro asset rather than just a crypto token.

ETH, by contrast, saw its price collapse despite network activity holding up. The report noted that staking growth, Layer-2 usage, and stablecoin settlement stayed strong throughout the drawdown period, even as the price fell from around $4,700 to below $1,800.

On the other hand, XRP’s relative performance was tied mostly to regulatory narrative and ETF expectations around cross-border payment themes, while BNB stayed somewhat steadier due to activity within the Binance ecosystem.

Where Things Stand

We can get an indication of how much progress has been made so far by looking at present-day prices for the assets XWIN quoted in its research. For instance, Bitcoin is trading at around $81,000, which is an 11% increase from the previous month.

ETH is around $2,300, up about 4% on the month, while XRP gained some 7.5% in the same period and was changing hands near $1.45 at the time of writing.

Solana, however, has had the strongest performance of them all, up more than 12% in the past month and about 12% on the week, and is currently trading near $95.

The post How Bitcoin Outperformed ETH, XRP, BNB, and SOL During 2025-2026 Market Stress appeared first on CryptoPotato.

The collision of AI innovation and crypto lobbying is shaping how voters view both industries as the United States edges toward potential policy changes. A Politico/Public First survey signals growing public skepticism about crypto and cautious scrutiny of AI, even as lawmakers and advocacy groups accelerate efforts to influence Washington before the next election cycle.

Poll findings suggest policymakers face a tough audience: while the crypto sector has amassed substantial funding in political action committees, a broad swath of voters remain unconvinced about the sector’s benefits or risks associated with artificial intelligence. The dialogue around a formal regulatory framework, including considerations around the CLARITY Act, has become a focal point in how industry interests intersect with voter sentiment.

Key takeaways

- Public trust gaps persist: 47% of Americans prefer traditional banks to crypto platforms, while only 17% express a level of trust comparable to banks in crypto services.

- AI skepticism runs deep: 43% believe AI risks outweigh its benefits, with just 33% seeing the opposite.

- Low awareness of lobbies: awareness of major crypto and AI lobbying groups remains limited, with only 9% having heard of the AI Super PAC Leading the Future and 3% aware of the pro-crypto Fairshake PAC.

- Grassroots resistance to tech infrastructure: across seven states, local movements have delayed or blocked substantial data-center investments, with Maine considering a statewide ban.

- Partisan dynamics complicate advocacy: while crypto voices frame their cause as bipartisan, the policy reality shows deep ties to executive and regulatory arms of government, complicating the political calculus for both parties.

Voter sentiment: crypto trust and AI doubts shape the narrative

The Politico/Public First poll paints a nuanced picture of public opinion on crypto and AI. A plurality still regards traditional financial institutions as more trustworthy than crypto platforms, and only a minority views crypto as having comparable reliability to banks. The same survey indicates that opinion on AI is uneven, with a sizable portion of the electorate wary of potential risks even as others point to benefits.

Michael Beckel, director of money-in-politics reform at Issue One, summarized the mood to Cointelegraph: voters across ideological lines are expressing concerns about corporate influence and how campaign money shapes policy outcomes. He noted that some candidates are attempting to capitalize on this frustration, a signal that the political calculus around tech lobbying is shifting.

For crypto, the numbers look especially wary. Republicans show slightly higher affinity toward crypto than Democrats, but the gap remains broad. The survey highlights a key tension: voters’ skepticism toward lucrative lobbying efforts may override partisan lines when it comes to accepting industry-friendly messaging.

Lobbying, awareness, and the politics of influence

The broader political discourse around AI and crypto is being shaped not just by policy proposals but by who finances the campaigns and how that money is framed to voters. Rick Claypool, research director at Public Citizen, emphasized a long-standing norm: voters generally oppose heavy corporate money shaping politics. He noted that post-Citizens United, the expectation has been that big brands do not straightforwardly fund campaigns, or they do so through opaque channels that obscure the funding origins.

In the 2024 cycle, industry actors—ranging from major exchanges to prominent venture firms—were active in campaign finance. Yet, the messaging directed at voters did not center on crypto per se. Advertisements and mailers often aligned with candidates’ broader positions, sometimes framing the contest as a defense against regulation or a push for deregulatory priorities rather than a crypto-first debate. The takeaway is clear: even when an industry pushes for policy, it must translate complex technical issues into relatable political narratives that the electorate can parse.

Ohio Rep. Jim Renacci summed up a practical concern for lawmakers: if a candidate is heavily backed by crypto money, the local electorate may react negatively due to limited understanding of the technology. The sentiment underscores a risk for representatives who rely on industry fundraising in a climate where voters are increasingly wary of corporate influence in politics.

Grassroots pushback and the regulatory map

The political environment around AI and crypto is further complicated by a growing grassroots movement that targets the physical footprint of technological infrastructure. Data Center Watch has documented a wave of local actions—across California, Oregon, Arizona, Texas, Missouri, Indiana, and Virginia—where new data-center projects were delayed or blocked. A recent report notes that these efforts have stalled more than $64 billion in planned data-center investment and that Maine is weighing a statewide ban as a potential policy precedent.

Claypool framed this as a potentially fertile ground for campaign messaging, particularly for Democrats seeking to capitalize on grassroots energy against what many see as energy-hungry, resource-intensive tech infrastructure. He argues that opposition to data centers can be a mobilizing issue, one that may help candidates align with voters who perceive tech expansion as a local environmental or community concern rather than a purely national policy matter.

Meanwhile, the crypto industry has tried to position itself as a bipartisan issue, arguing that policy clarity and reasonable regulation would benefit consumers and investors alike. Coinbase’s leadership and other notable venture backers have publicly framed crypto as a cross-partisan concern in Washington. Yet, on the ground, enforcement priorities and regulatory posture often track more with party leadership and executive agencies than with partisan labels. The intertwining of crypto advocacy with the Trump political orbit adds another layer of complexity. As Trump’s relevance in the broader political landscape fluctuates, ties to the industry carry new political risk for candidates who rely on that support.

A recent Illinois Democratic primary illustrated the potential political consequences of money in crypto circles. Lieutenant Governor Juliana Stratton cited opponent Raja Krishnamoorthi as being backed by “MAGA-backed crypto bros,” highlighting how the perception of money in politics can become a campaign issue. Stratton’s victory underscored that the electorate can scrutinize the sources of campaign contributions as much as the policy positions themselves.

Looking ahead: what matters for voters, investors, and builders

As midterm dynamics and regulatory debates unfold, observers should watch how legislative momentum around the CLARITY Act evolves and whether it gains broader bipartisan support. The public’s growing skepticism about crypto and AI could influence lawmakers to pursue tighter disclosures, clearer enforcement guidelines, and more transparent lobbying practices, even as proponents argue for a clear framework that benefits investors and users.

For market participants, the key takeaway is not a sudden shift in policy, but a gradual recalibration of risk around policy risk. Investors and builders should monitor two threads: first, the trajectory of regulatory clarity and how it aligns with consumer protections and innovation; second, the ability of the crypto and AI industries to articulate tangible benefits to the public in a way that resonates beyond the fundraising apparatus.

In the coming months, the interplay between voter sentiment, grassroots activism, and political endorsements will shape how Washington treats crypto and AI. If voters increasingly view industry money as a potential conflict of interest, candidates may distance themselves from big-ticket funding, potentially narrowing the policy window for industry-backed initiatives. Conversely, if policymakers offer credible, accessible frameworks that address consumer protection and innovation, the sector may find a more stable path forward.

Readers should keep an eye on regulators’ statements, legislative committee hearings, and any new public-facing campaigns from major lobbies and consumer groups. The political weather surrounding crypto and AI is shifting, and the path to policy clarity may hinge on how convincingly proponents connect technical progress with everyday benefits for the American public.

Michael Burry attends “The Big Short” New York screening Ziegfeld Theater on Nov. 23, 2015 in New York City.

Astrid Stawiarz | Getty Images

Michael Burry urged investors to scale back exposure to surging technology stocks, saying the current market environment has reached historically dangerous extremes reminiscent of prior speculative bubbles.

The famed investor, best known for predicting the 2008 housing collapse, said investors should “reject greed” as enthusiasm around artificial intelligence and momentum-driven trades pushes valuations sharply higher.

“An easier way for most is to simply reduce exposure to stocks, to tech stocks in particular. For any stocks going parabolic reduce positions almost entirely,” Burry wrote in a Sunday Substack post.

Burry has been warning for months that the stock market’s AI fixation increasingly resembles the final stages of the dot-com bubble. Last week, he compared the recent trajectory of the Philadelphia Semiconductor Index (SOX) to the run-up that preceded the collapse of technology stocks in March 2000, saying the current environment feels like “the last months of the 1999-2000 bubble.”

Burry said he is maintaining “a significant leveraged short position” against a portfolio of companies he views as depressed and cheap, a similar strategy he employed in 2000.

However, Burry warned that directly betting against the rally through short selling is risky and impractical for most investors, particularly as bearish trades have become increasingly expensive.

“Shorting is not the answer. It is not something most people should ever do,” he said. “Right now it is expensive, in general, to buy put options and directly shorting stocks can still cause significant pain.”

The comments add to a growing debate on Wall Street over whether the AI-driven rally in U.S. equities has become detached from fundamentals. Major stock indexes have repeatedly hit record highs despite the ongoing war in the Middle East as investors pile into semiconductor makers and megacap companies.

“The idea is to raise cash, and prepare to put it to work when it makes more sense to do so,” Burry wrote. “History tells us that even if the party goes on for another week, month, three months or year, the resolution will be to much lower prices.”

Consensus, the annual cryptocurrency conference hosted by CoinDesk, threw its post-conference closing party at E11even, the same club where several years ago World Liberty Financial founder Zach Witkoff was arrested with cocaine.

This Miami club, described as a “strip club” by Jess Zhang, the founder and chief executive of Blockus, was criticized as a poor choice for an industry that was supposed “to be moving towards institutional maturity.”

Zhang further noted that this type of event “diminishes women to sexual objects and enforces a stale, exclusionary culture.”

Additionally, Amanda Wick, formerly a federal prosecutor, told Bloomberg that “as a gender equality advocate, the event was horrifying.”

E11even has a long history with cryptocurrency; E11even Partners decided to partner with FTX US before its collapse.

This partnership would have made FTX US “the sole converter of cryptocurrency transactions for acquiring residences” in this development by the same group as the aforementioned nightclub.

Read more: Crypto Miami apparently has a deodorant problem

At least one cryptocurrency executive rushed to defend the event: Michael Khekoian, the senior business development manager at Consensys who also does product safety at Metamask, posted, “I never knew the women working there are forced sex slaves.”

He continued, “its as if there was no actual conference or networking outside of a closing party.”

Eventually, this escalated to Khekoian threatening to sue Zhang.

Additionally, this is the same nightclub where in 2022 World Liberty Financial founder Witkoff was arrested with cocaine.

During a video of the arrest you can hear Witkoff repeatedly insist that he was friends with Marc Roberts, who runs E11even.

Witkoff wasn’t prosecuted following this arrest.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Osmosis is debating a merger with Cosmos Hub via a 1.998 OSMO‑for‑0.0355 ATOM swap funded by DEX revenue, raising existential questions for OSMO, ATOM and the broader IBC DeFi stack.

Summary

- OSMO rallied 185% in 24 hours on May 11, 2026, amid renewed speculation about a revised Cosmos Hub merger proposal

- The original COSMOSIS proposal to convert OSMO to ATOM at a rate of 1.998 OSMO for 0.0355 ATOM failed narrowly in April 2026

- Social media activity from @osmosis and community accounts suggests a potential revised path forward for the integration

Osmosis (OSMO) jumped 185% in 24 hours on May 11, reigniting debate across X about the failed COSMOSIS merger proposal that would have integrated the decentralized exchange directly into the Cosmos Hub. The sharp price movement comes less than a month after Cosmos Hub governance narrowly rejected the acquisition plan in April 2026, with speculation now centering on whether a revised proposal could succeed.

The original proposal, posted March 11, would have allowed holders to convert all circulating OSMO tokens into ATOM at a fixed rate of 1.998 OSMO for 0.0355 ATOM over a six-month window. Under that structure, approximately 665.1 million OSMO would have been eligible for conversion, with any unclaimed ATOM returning to the Cosmos Hub community pool after the deadline. The plan aimed to consolidate Osmosis liquidity, governance, and security onto a single chain, effectively making the DEX a native component of the Hub rather than an independent app-chain.

Failed Vote Sparks Renewed Speculation

After the governance vote failed by a narrow margin in mid-April, Osmosis stated it would continue operating as “an independent, profitable blockchain” and develop its next-phase roadmap. Yet recent posts from the official Osmosis account and Cosmos-focused community members suggest discussions around a revised integration path have resumed, driving heavy trading activity across OSMO markets.

The OSMO-to-ATOM conversion narrative has been trending heavily among Cosmos ecosystem participants, with some forum posts exploring whether a modified proposal could address concerns that led to the original vote’s failure. An updated version referenced in early April removed new ATOM minting from the plan, instead proposing to fund the conversion over time using Osmosis’s own DEX revenue. That revision aimed to mitigate dilution risk for ATOM holders, a key point of contention during the initial governance debate.

Consolidation Versus Sovereignty

The COSMOSIS proposal represents one of the most aggressive consolidation moves in Cosmos history, testing whether ecosystem-wide mergers can boost liquidity and valuations or undermine the sovereignty that defines the network’s app-chain model. If a revised proposal passes both Osmosis and Cosmos Hub governance, it would set a precedent that could pressure other independent chains to consider similar integrations.

Market observers note the debate mirrors broader tensions across multi-chain architectures, where projects must balance the benefits of shared security and liquidity against the risks of governance centralization. Concentrating the ecosystem’s primary DEX and hub chain under a single governance framework creates potential single-point-of-failure risks, as contentious votes could simultaneously affect trading infrastructure and network security.

Following the April rejection, some Cosmos community members floated the idea of a hostile takeover offer, arguing that nothing prevents Hub governance from drafting a proposal and presenting it directly to OSMO holders for their own vote. Whether renewed speculation translates into formal governance action remains unclear, but the 185% price surge signals that markets are pricing in a meaningful probability of eventual integration.

The US Supreme Court in Washington, DC, US, on Monday, April 20, 2026.

Graeme Sloan | Bloomberg | Getty Images

Two court rulings in the past two weeks have hit the chances that Democrats flip control of the House in November, according to traders on prediction markets platform Kalshi.

Odds that the party wins control of the lower chamber have fallen to 75% from 85.3% on April 28.

On April 29, the Supreme Court ruled in Louisiana v. Callais that a majority-Black congressional district in Louisiana was invalid, limiting how much race can be considered when drawing congressional maps and weakening part of the Voting Rights Act.

That district, like many of the other majority-black congressional districts across the South, is represented by a Democrat. Louisiana is moving to redraw its maps in a move that will likely see one less Democratic member of Congress sent from the state.

Other states have rushed to redraw their maps in reaction to the decision too. Tennessee last week approved a map to alter the boundaries of a majority-Black district in Memphis, endangering the re-election of Democrat Rep. Steve Cohen. Alabama and South Carolina are also considering redrawing their maps, potentially endangering up to three Democratic incumbents.

Democrats were dealt another blow on Friday when the Virginia Supreme Court overruled a referendum that voters narrowly approved in April to alter their congressional map, which could have sent up to four additional Democratic members to Congress. That decision will leave Virginia’s current congressional districts in place for the 2026 election, and limit the number of seats Democrats can expect to win in the state in their quest for House control.

After the Virginia referendum, Florida moved to redistrict their map, hoping to add four additional Republican seats. That proposal was signed by Gov. Ron DeSantis, a Republican, after the U.S. Supreme Court ruled in Callais.

While Democrats are still favored to win control of the House, the odds they do it are at their lowest level since late December.

The redistricting scramble comes as primary election season is well underway. West Virginia and Nebraska go to the polls on Tuesday, where Kalshi traders favor John Cavanaugh to be the Democratic nominee in Nebraska’s second congressional district, a seat the party will have to win if they want to flip control of the House. Kalshi traders think President Donald Trump-backed Brinker Harding is certain to be the Republican nominee.

Disclosure: CNBC and Kalshi have a commercial relationship that includes customer acquisition and a minority investment.

Markets shift and headlines fade, but the core principles of building long-term wealth remain constant. Join us for our third CNBC Pro LIVE, where investors of all backgrounds – from financial professionals to everyday individuals – come together to cut through the noise and gain actionable strategies for smarter, more disciplined investing. No matter where you’re starting from, you’ll leave with clearer thinking, stronger strategies. Enter your email here to get a discount code.

Key takeaways

- SEI is up 10%, outperforming the broader cryptocurrency market.

- The coin could extend its rally towards the $0.092 daily swing high in the near term.

The cryptocurrency market opened the new weekly candle mixed as some coins rallied while others underperformed.

SEI, the native coin of the Sei blockchain, is one of the best performers among the top 100 cryptocurrencies by market cap.

The coin is up by 10% in the last 24 hours and could extend its rally in the near term. Technical indicators suggest that SEI could surge past a key resistance level as the broader market remains strong.

SEI rallies as Sei Labs completes EVM Transition

The primary catalyst behind SEI’s latest rally is the completion of its unified EVM architecture.

The team announced over the weekend that it has completed its transition to a unified, EVM-only architecture.

This means that exchanges and custodians supporting the SEI token need to migrate customer holdings before support for Cosmos and IBC-related functionality is deprecated.

The team’s core message: Sei EVM is not a separate chain. “It’s the same chain with a second way to interact with it,” Sei Labs said in the announcement. Any venue that treats “Sei” and “Sei EVM” as two distinct integrations needs to consolidate them into one.

The push closes out SIP-3, the May 2025 governance vote that approved Sei’s pivot to a fully EVM-only architecture.

The transition has rolled out in stages through 2026, with EVM staking added in January, inbound IBC transfers disabled in February, and the native oracle replaced by Chainlink, Pyth, and API3 in March.

SEI bulls target the $0.080 resistance level

The SEI/USD 4H chart is bearish and inefficient thanks to Sei’s latest rally. The momentum indicators suggest that the bulls remain in control of the market.

The RSI of 70 means that SEI is approaching the overbought region, which could signal incoming selling pressure. The MACD lines are also within the positive territory, adding further confluence to the bullish narrative.

If the bullish trend persists, SEI could rally past the $0.0800 level in the near term. The swing high on the daily chart at $0.09248 could be SEI’s target in the coming days and weeks.

However, if the sellers regain control, SEI could drop to the support level at $0.07021. Losing this level could see the bears push the price lower towards the $0.06490 pyschological level.

MARA Holdings (MARA) is scheduled to report first quarter earnings after the market close on May 11, with Wall Street analysts expecting the company to post losses on revenue and earnings (EPS) of $184.21 million and $2.34 respectively.

Results are expected to reflect the sharp decline in bitcoin prices during the first quarter, with BTC falling roughly 25% over the period, from roughly $87,000 to $67,000, creating significant mark-to-market losses on MARA’s digital asset holdings.

However, investor focus is likely to center less on short term bitcoin price volatility and more on the company’s strategic transition into artificial intelligence and high performance computing infrastructure. MARA has increasingly positioned itself as part of a broader industry shift in which bitcoin miners are leveraging their existing energy assets and data center expertise to secure more stable, long term AI-related revenue streams.

The AI transition includes FTAI Infrastructure agreeing to sell Long Ridge Energy to MARA in a $1.5 billion transaction. The deal is expected to provide MARA with long-term power-generation capacity and exposure to steadier cash flow opportunities tied to AI and data center contracts, reducing reliance on the highly cyclical bitcoin mining business, where revenues fluctuate with bitcoin prices, network difficulty, and transaction fees.

In the fourth quarter, MARA reported declining revenue of 6% year-over-year from $214 million to $206 million, though it also announced a partnership with Starwood to develop AI data centers delivering approximately one gigawatt of computing capacity in the near term.

During Q1, MARA sold 15,133 BTC, valued at approximately $1.1 billion, using proceeds to repurchase $1.0 billion of convertible notes, strengthen liquidity, and continue funding its AI expansion strategy.

The broader bitcoin mining sector is increasingly following a similar path. IREN (IREN) recently expanded its AI transition through a $3.4 billion AI cloud agreement with NVIDIA (NVDA), while also recording a $140.4 million non-cash impairment charge tied to the sale of ASIC mining hardware as it reallocates infrastructure toward AI cloud services.

In addition, HIVE Digital Technologies (HIVE) announced additional investments into AI and digital infrastructure, including $3.1 million to install high speed fiber infrastructure supporting a planned 50MW AI factory.

MARA shares rose 1% to $13 in pre-market trading.

Starmer’s ‘make or break’ speech just broke him

My math comes in handy!! #math #siblings #shorts #brother #money

how stimulating the muscles with electricity may help manage the condition

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Crypto World3 days ago

Crypto World3 days agoHarrisX Poll Found 52% of Registered Voters Support the CLARITY Act

-

Fashion3 days ago

Fashion3 days agoWeekend Open Thread: Marianne Dress

-

Crypto World4 days ago

Crypto World4 days agoUpbit adds B3 Korean won pair as Base token gains Korea access

-

Tech7 days ago

Tech7 days agoImage AI models now drive app growth, beating chatbot upgrades

-

NewsBeat4 days ago

NewsBeat4 days agoNCP car park operator enters administration putting 340 UK sites at risk of closure

-

Tech2 days ago

Tech2 days agoAuto Enthusiast Carves Functional Two-Stroke Engine from Solid Metal

-

Politics2 days ago

Politics2 days agoPolitics Home Article | Starmer Enters The Danger Zone

-

Business2 days ago

Business2 days agoIgnore market noise, India’s long-term story intact, say D-Street bulls Ramesh Damani and Sunil Singhania

-

Crypto World6 days ago

Crypto World6 days agoUAE Free Zone Deploys Blockchain IDs to Verify Registered Firms

-

Tech12 hours ago

Tech12 hours agoGM Agrees To Pay $12.75 Million To Settle California Lawsuit Over Misuse Of Customers’ Driving Data

-

Crypto World5 days ago

Crypto World5 days agoBlackRock CEO Larry Fink Discusses a New Asset Class

-

Crypto World5 days ago

Crypto World5 days agoRobinhood says Wall Street is building onchain

-

Entertainment7 days ago

Serena Williams hits Met Gala in metallic dress after GLP-1 reveal

-

Tech6 days ago

Tech6 days agoApple and Samsung are dominating smartphone sales so thoroughly that only one other company makes the top 10

-

Tech6 days ago

Tech6 days agoI tested the Xiaomi 17 Ultra’s camera and I don’t think I’ll ever go back to an iPhone

-

Fashion5 days ago

Fashion5 days agoThe Best Work Pants for Women in 2026

-

Tech4 days ago

Tech4 days agoAI agents are missing all the discussions your team is having. SageOX has an answer: agentic context infrastructure

-

Entertainment5 days ago

Entertainment5 days agoSarah Paulson Called Out For Met Gala ‘Hypocrisy’

-

Sports7 days ago

Sports7 days agoEverton v Man City LIVE: Haaland’s two-word response as visitors collapse to hand Arsenal advantage in Premier League title race

-

Politics6 days ago

Politics6 days agoMet Gala 2026: Madonna’s Dramatic Red Carpet Look Steals The Show

You must be logged in to post a comment Login