Crypto World

Coinbase Wins UK License, Paving the Way for Stocks and Derivatives Trading

The largest US-based cryptocurrency exchange has expanded its scope of regulatory authorizations across the world by securing the necessary approval to provide investment services in the United Kingdom.

This is considered one of its most significant expansions in the market since launching there several years ago.

The statement from the company reveals that the approval will allow it to offer traditional financial products alongside cryptocurrencies through a single platform.

The new authorization enables the exchange to expand beyond digital assets and introduce a new set of products, such as derivatives and equities, to UK-based users.

Coinbase said institutional and advanced traders will gain access to crypto, equity, and commodity perpetual futures. At the same time, retail investors will be able to trade stocks directly on the platform for the first time.

The post Coinbase Wins UK License, Paving the Way for Stocks and Derivatives Trading appeared first on CryptoPotato.

“To deliver on President Trump’s goal to ensure that the United States is the crypto capital of the world, we are embracing innovation to bring more products onshore, creating clear rules of the road for capital raising with crypto assets, and providing clarity as to how market participants can custody and facilitate trading of tokenized securities onchain,” Atkins said in a statement on Tuesday, mentioning his agency’s crypto agenda before any other specific rulemaking effort.

As the process to advance a crypto market structure bill has languished in Congress, the SEC has been a bright spot for the industry’s regulatory hopes, though the agency has sometimes moved more slowly to issue policies than expected. When Atkins addressed this coming regulation almost four months ago in mid-March, he said it would be proposed in the “coming weeks.”

The busy new SEC agenda has “Regulation Crypto” slated for July, though it’s still under review at the White House Office of Information and Regulatory Affairs. When proposed, it would mark the first major crypto-specific rulemaking pursued under Atkins’ leadership. Though the regulator has established a wide range of staff statements and guidance on crypto, those positions don’t carry the weight of a full rule, which can’t be changed as easily when future leaders arrive at the agency with different ideas.

Binance Alpha-listed TAC suffered one of the sharpest crypto flash crashes of the year after its token plunged more than 90% in roughly 15 minutes on July 7.

While no security breach or protocol failure has been confirmed, the crash has renewed concerns about liquidity risks and token concentration among newly listed crypto assets.

TAC Suffers Violent Flash Crash

TAC dropped from around $0.06 to nearly $0.004 within minutes, with trading volume surging as panic selling accelerated. The token later stabilized near its lows, remaining down more than 90% from prices seen earlier in the day.

The move came just one week after TAC reached an all-time high of approximately $0.067, highlighting the extreme volatility that can accompany newly listed digital assets.

Strong Backers, But No Official Explanation

TAC is developing an Ethereum Virtual Machine (EVM)-compatible blockchain designed to bring Ethereum applications into the TON and Telegram ecosystem.

The project has raised roughly $11.5 million from prominent crypto investors, including TON Ventures, Hack VC, Animoca Ventures, Symbolic Capital, Primitive, and Spartan Group.

Despite the dramatic price collapse, neither the TAC team nor Binance had announced a confirmed cause at publication. There is also no evidence that today’s move resulted from a hack or network exploit.

Liquidity and Token Concentration Under Scrutiny

Market observers have pointed to several possible factors behind the collapse, including thin order-book liquidity, large holder selling, and cascading liquidations.

Unverified on-chain discussions have also questioned whether a small number of wallet clusters control a significant share of circulating supply. However, these claims remain unconfirmed and should not be treated as established fact.

The selloff follows TAC’s May 2026 cross-chain bridge exploit, which resulted in approximately $2.8 million in losses before affected users were later compensated. Although unrelated to today’s price action, the earlier incident may have contributed to fragile market sentiment.

What’s Next for TAC?

Investors are now watching for an official statement from the TAC team, exchange updates, and on-chain data that could explain the sudden collapse. Until more information emerges, TAC is likely to remain highly volatile, with liquidity conditions and large-wallet activity becoming key indicators for traders assessing the token’s recovery prospects.

The post Binance Alpha Token TAC Wipes Out 90% in Sudden Collapse appeared first on BeInCrypto.

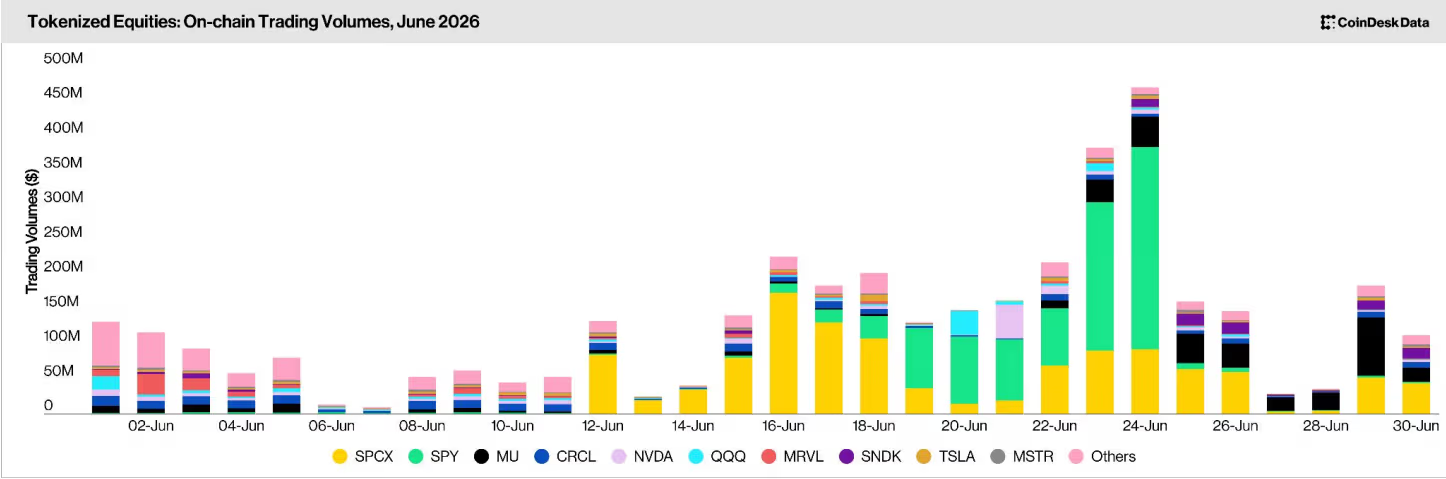

Tokenized equities posted record trading activity in June as investors piled into blockchain-based versions of SpaceX (SPCX) stock following the aerospace company’s blockbuster initial public offering.

On-chain trading volume climbed 145% from May to $3.86 billion, according to CoinDesk Data’s latest Stablecoins & Tokenized Assets report. Tokenized SpaceX shares accounted for $1.19 billion of the total, or about 31% of all tokenized equity trading during the month.

The surge followed SpaceX’s $75 billion IPO, the largest on record, which valued the company at roughly $1.8 trillion on a fully diluted basis.

Backpack Securities’ SPCX token was the most popular tokenized version of the stock, with $1.08 billion in onchain trading volume, followed by xStocks’ SPCXx, which reached $852 million.

The figures point to a change in what is driving demand for tokenized equities. Established names like Nvidia, Tesla, SPY and QQQ remained actively traded, but none matched the interest in SpaceX. For context, Backpack’s tokenized instruments traded $1.42 billion for the month, the lion’s share of which was in SPCX tokens.

The sector reached a record $1.53 billion in market capitalization during June, up 6.64% from the previous month and marking its fifteenth straight month of growth, the report adds.

Richard Heathcote, who until earlier this year served as Tether Holdings SA's chief investment officer, is planning to sell a small stake in the stablecoin issuer, Bloomberg reported Monday, citing people familiar with the matter. Heathcote is working with investment bank PJT Partners to sell part… Read the full story at The Defiant

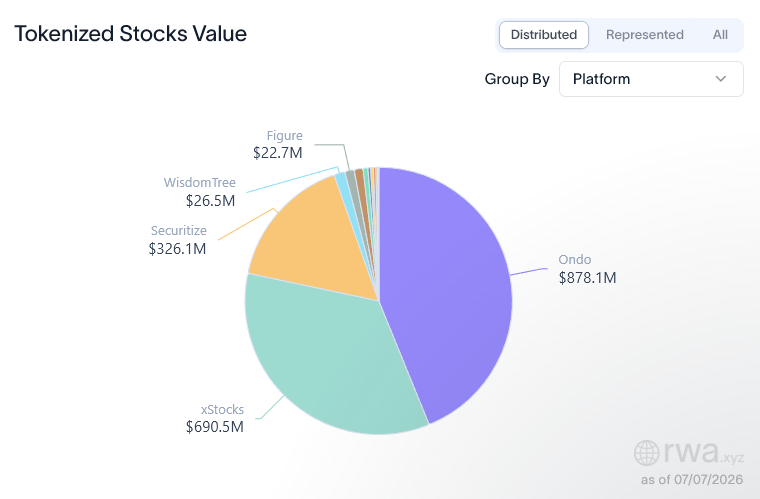

Tokenized stocks are still tiny compared with traditional equity markets, but they are no longer an experiment inside crypto. Tokenized stocks have surged to nearly $1.08 billion in total value and $2.10 billion in monthly transfer volume.

Ondo leads the category with 405 tokenized stock assets valued at about $870 million and 43.61% market share. Now, Ondo is trying to push this growing market into derivatives.

Ondo Perps launched in public beta in June, giving selected eligible users outside the United States access to perpetual futures on tokenized versions of US stocks, ETFs, commodities, and indices.

The platform offers up to 20x leverage and 24/7 trading on markets linked to assets such as Nvidia, Tesla, gold, oil, silver, the US 100, and the US 500.

In simple terms, users can take long or short leveraged positions on real-world markets without waiting for traditional exchange hours. They can also use tokenized securities as collateral, rather than relying only on stablecoins.

That collateral feature is the real story. Ondo is trying to turn tokenized stocks from passive market exposure into working infrastructure for on-chain trading.

Ondo Already Has the Stock Base

Ondo Perps does not start from a blank market. It builds on Ondo Global Markets, the company’s tokenized stocks and ETFs platform for eligible non-US users.

Ondo announced in May that Global Markets had crossed $1 billion in TVL in under eight months. At the time, the platform offered more than 260 tokenized US stocks and ETFs across Solana, Ethereum, and BNB Chain, and had passed $18 billion in cumulative trading volume.

Its distribution has expanded since then. Blockchain.com added 173 new tokenized stocks and ETFs through Ondo in June, bringing its total Ondo-powered tokenized asset offering to more than 430 across Ethereum, Solana, and BNB Chain.

These assets are designed to give users economic exposure to traditional securities. They are not the same as holding the actual stock, ETF, or ADR, and Ondo’s own disclosures say holders do not receive rights to the underlying assets themselves.

That distinction matters. Tokenized stocks are still wrapped in financial exposure, with jurisdictional restrictions and product-specific risks. However, they now have enough on-chain distribution for derivatives platforms to build around them.

Ondo Perps is the first major test of that next step.

Why the Collateral Model Matters

Most crypto perpetual exchanges use stablecoins or crypto assets as margin. That works well for Bitcoin, Ethereum, and other native crypto markets. It becomes less efficient when the product is tied to equities, ETFs, commodities, or indices.

A trader might hold tokenized Nvidia or Tesla exposure, but still need to post stablecoins separately to trade a perp. A market maker might quote an equity perp on-chain, then hedge through traditional brokers off-chain. The result is a split system where collateral, pricing, and hedging sit in different places.

Ondo Perps tries to narrow that gap by allowing tokenized securities to serve as collateral.

A user holding tokenized stocks can use those assets as margin for leveraged trades. A market maker can manage exposure with collateral linked to the same real-world markets it is quoting. That can improve capital efficiency because fewer assets need to sit idle across separate systems.

It also gives Ondo a clearer liquidity argument. The platform is connecting those perps to an existing tokenized stock ecosystem with users, integrations, and market access already in place.

The Hard Part Comes After Launch

RWA perps are difficult because they promise crypto-style access to markets that still depend on traditional infrastructure. Traders want 24/7 exposure. The deepest liquidity for stocks and ETFs still lives inside traditional exchanges, brokers, and clearing systems.

That creates pressure during volatile periods. Equity prices can react to earnings, macro data, or company news when traditional venues are closed. A 20x leveraged position can move from profitable to liquidated quickly if pricing, collateral valuation, or hedging fails to keep up.

This is why Ondo Perps should be judged less by the number of markets it lists and more by how it performs under stress. Tight spreads, reliable depth, clean liquidations, and accurate collateral pricing will matter more than launch-day asset coverage.

The broader opportunity is clear. Crypto traders already understand perpetual futures. Tokenized stocks give them a route into US equity exposure without leaving blockchain-based accounts. Ondo is now trying to combine the two into one trading environment.

The risk is also clear. Once tokenized stocks become collateral for leverage, the quality of the collateral layer becomes central to the market. Any weakness in pricing, liquidity, or redemption can spread faster through derivatives than through spot trading.

Ondo Perps, therefore, marks a useful shift in the RWA market. The category is moving beyond the question of whether stocks can be tokenized. The next question is whether those tokens can support serious trading infrastructure.

The post Ondo Perps Pushes Tokenized Stocks Into 20x Leveraged Trading appeared first on BeInCrypto.

Ripple’s cross-border token is among the most polarizing, often being the center of attention within the cryptocurrency community for major price predictions (whether bullish or bearish).

One of the recent examples came from EGRAG CRYPTO, among the most optimistic XRP commentators on X, who outlined a highly favorable chart for the asset. On the other hand, shah wondered what all the hype is about the token.

XRP’s Chart Doesn’t Lie

EGRAG has made some major price predictions in the past for XRP, many of which sound unreasonable now given the asset’s struggles to remain above $1.10. However, the analyst tends to focus on the long-term price performance, trying to isolate the structure from the noise and emotion.

In their latest post on the matter, they published a chart mapping out the token’s possible future movement. It first envisions a price dip to $0.95, which aligns with other analysts’ expectations for a new low beneath $1.00, before the next major leg up.

The promising green wick for the bulls charts a run toward a new all-time high and well above. In fact, EGRAG has frequently posted targets of up to $27 for XRP during the most intense expansions of the next bull cycle.

#XRP – CHART, No Comment

:

Men Lie, Women Lie But Charts and Numbers do not Lie.

Structure > Noise > Emotion. ONLY FEW

pic.twitter.com/GLbM1W1Xpd

— EGRAG CRYPTO (@egragcrypto) July 7, 2026

What’s All This Hype?

In contrast to EGRAG’s bullish charts on XRP, shah asked their over 400,000 followers on X to explain all the hype around XRP. They wondered, “Why on Earth would this coin ever go to hundreds per coin?”

The comments below were quite unfavorable for the cross-border token and those who believe it may go beyond $100. Kendall Tart explained that a triple-digit price tag would require its market cap to rocket past $6 billion. This would make XRP bigger than Apple, which sounds far-fetched, to say the least, at the moment.

Others compared XRP holders to MAGA believers, indicating that Ripple’s CEO, Brad Garlinghouse, is “their president and his cabinet are paid influencers that say buzzword points that get regurgitated over multiple social media platforms.”

Another comment predicted that it can’t and won’t go anywhere near $100. Moreover, the user proclaimed XRP as “dead” given its tokenomics, never-ending selling pressure, and “horrible internal organization.”

The post XRP’s Chart Doesn’t Lie: Analysts Clash Over Ripple’s Next Move appeared first on CryptoPotato.

Crypto World

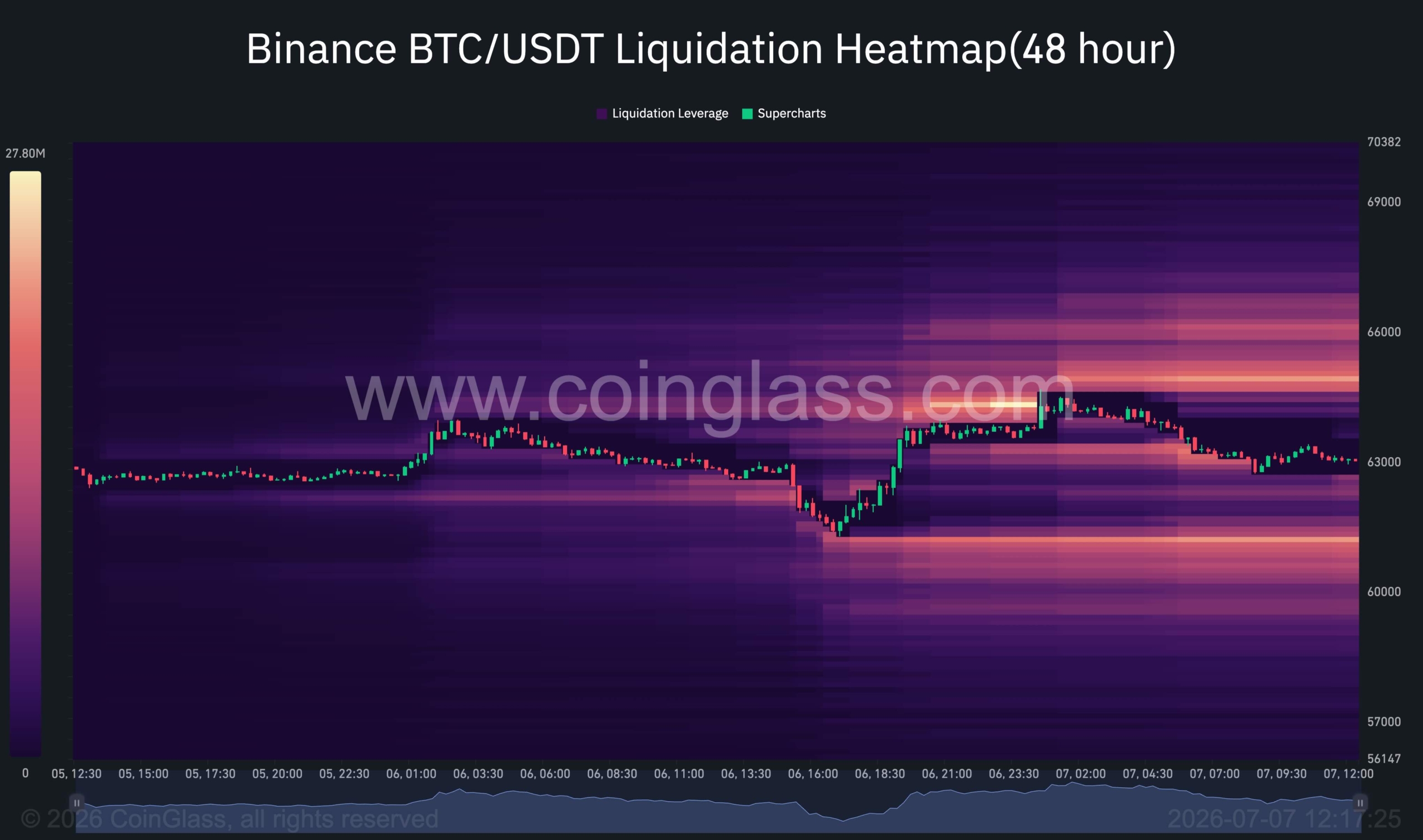

Bitcoin Price Analysis: BTC’s Structure Remains Bearish Until This Key Level Is Reclaimed

Bitcoin continues to recover from its recent sell-off, but the market remains trapped beneath a major resistance cluster that has capped every relief rally since the June breakdown. While short-term momentum has improved, BTC is now approaching a decisive area where the next move could determine whether the recovery evolves into a larger trend reversal or remains a corrective bounce within a broader bearish structure.

Bitcoin Price Analysis: The Daily Chart

On the daily timeframe, Bitcoin remains in a clear downtrend, trading below the 100-day and 200-day moving averages, both of which continue to slope lower. The recent recovery from the $58K-$61K demand zone has helped stabilize the price action, but the asset is still trading beneath the major resistance area between $64K and $66.5K.

It recently formed another higher low inside the broader support region, while the RSI has continued to print higher lows despite the weakness seen throughout June. This developing bullish divergence suggests that downside momentum is fading and that buyers are gradually regaining control.

However, the market structure remains bearish until Bitcoin can reclaim the $64K-$66.5K supply zone. This area aligns with previous support turned resistance and continues to act as the primary obstacle preventing a larger recovery. A successful breakout above this region would likely expose the next major resistance near $72K-$74K, while rejection could send the price back toward the $60K support zone.

BTC/USDT 4-Hour Chart

The 4-hour chart shows a much more constructive picture. After establishing a base around the $58K-$59K demand region, Bitcoin produced a strong impulsive rally and pushed directly into the descending trendline that has defined the corrective structure since mid-June.

The asset recently swept the local liquidity resting above previous highs within the $61K-$62K region before encountering resistance near the descending trendline. This liquidity grab is important because it removed nearby buy-side liquidity and allowed the market to test a key technical level.

The current structure suggests that Bitcoin is attempting to transition from a series of lower highs into a potential breakout formation. A confirmed move above the descending trendline and the $64K-$66K resistance zone would significantly improve the bullish outlook and could accelerate upside momentum toward higher resistance levels.

Conversely, failure to break the trendline could trigger another period of consolidation between the $60K support and the $64K-$66K supply zone. As long as Bitcoin holds above the $60K-$61K support area, the short-term recovery structure remains intact.

Sentiment Analysis

The 48-hour liquidation heatmap highlights a notable concentration of liquidity above the current market price, particularly around the $64K-$66K region. This cluster aligns closely with the resistance zone identified on the 4-hour chart, reinforcing its significance as a major magnet for price action.

Importantly, the intra-range liquidity highlighted on the technical chart is also confirmed by the liquidation heatmap. The recent push into the $61K-$62K area successfully targeted nearby liquidity resting within the range, validating the idea that price has been moving between liquidity pockets rather than trending directionally.

At present, the largest liquidation concentration remains overhead near $65K-$66K, making it a logical target if buyers maintain momentum. Markets often gravitate toward these liquidity pools before determining the next directional move.

If Bitcoin manages to sweep this overhead liquidity and secure acceptance above the $64K-$66K region, it would strengthen the case for a broader recovery toward the higher resistance zones. However, if the sweep is followed by rejection and an inability to sustain prices above resistance, the move could simply represent a liquidity-driven rally before another test of lower support levels.

For now, both the technical structure and the liquidation data suggest that the path of least resistance remains slightly higher, with the overhead liquidity cluster acting as the most likely near-term destination.

The post Bitcoin Price Analysis: BTC’s Structure Remains Bearish Until This Key Level Is Reclaimed appeared first on CryptoPotato.

WEMIX, the Layer-1 blockchain ecosystem developed by gaming brand WEMADE, today announced that its native coin (WEMIX) has been officially listed on Kraken, one of the world’s longest-standing, most liquid and secure cryptocurrency exchanges. Trading is scheduled to commence on 7 July 2026, allowing Kraken’s global user base to deposit, withdraw, and trade WEMIX against the USD.

Listing on Kraken represents a pivotal shift in liquidity and market exposure for WEMIX. While WEMIX has historically maintained an entrenched position within South Korea, South America, and regional Asian markets, this integration into Kraken vastly expands its global reach. It opens access for Western institutional and retail investors across regions including the U.S., Canada, the U.K., and Australia, which will serve as a base for international users interacting with WEMIX’s extensive digital economy.

Shane Kim, CEO of WEMIX and Vice President of WEMADE, said: “Aligning with partners who share our commitment to compliance and security is paramount. Given Kraken’s reputation, we are honored to collaborate with them as we scale our market reach, establish a strategic foothold in the U.S. — the world’s largest financial market — alongside other key Western regions, and evolve into a truly global blockchain ecosystem.”

As WEMIX sets its sights on scaling its Real-World Asset (RWA) initiatives, securing this major listing by tapping into the immense capital pool of the biggest financial market in the world also significantly elevates WEMIX’s global visibility, enables deeper liquidity, and positions the ecosystem to attract a vast new wave of participants.

WEMIX’s listing on Kraken comes amid its parent company’s aggressive expansion across fintech, cross-border payments, and the RWA market. Along with upcoming AAA game launches designed to solidify its market leadership and deepen the WEMIX Web3 gaming ecosystem, WEMADE recently launched StableNet, Korea’s first dedicated Layer-1 blockchain for KRW-backed stablecoins, and established the Global Alliance for KRW Stablecoin (GAKS). Key alliance members include Web3 behemoths such as Chainlink, Chainalysis, and CertiK.

“Bolstered by massive infrastructure leaps like StableNet and the GAKS alliance, WEMADE is building the future of Web3 gaming and its convergence with fintech. Now, cementing our footprint in the Western financial ecosystem further proves that WEMIX, our Web3 arm, is built for the global stage,” Kim added.

Beyond its milestone listing on Kraken, WEMIX remains committed to securing further high-profile exchange integrations, systematically driving global liquidity, and expanding access for its growing international community.

About WEMIX

WEMIX is a leading blockchain ecosystem for gaming and digital economies, powered by its highly scalable, EVM-compatible Layer-1 mainnet, WEMIX3.0. With a wide range of integrated services including NFTs, DeFi, stablecoin payments, and tokenized in-game assets, WEMIX enables seamless integration between gameplay and real-world value. Designed to be transparent, sustainable, and developer-friendly, WEMIX serves as the foundation for the global Web3 gaming ecosystem. For more information, please visit the official website.

About WEMADE

WEMADE is the only company combining over two decades of AAA game development success with a fully operational, game-proven blockchain ecosystem-built entirely on its proprietary Layer-1 mainnet, WEMIX3.0. Known for global hits such as The Legend of Mir, MIR4, NIGHT CROWS and Legend of YMIR, WEMADE is leading the industry in seamlessly integrating gameplay, tokenomics, NFTs, stablecoin payments, and blockchain infrastructure. Through WEMIX PLAY, WEMADE delivers a unified digital economy where players, creators, and investors can own, trade, and benefit from digital assets-powering the next generation of interactive entertainment and driving the evolution of Web3 gaming. For more information, please visit the official website.

About Kraken

Founded in 2011, Kraken is one of the world’s longest-standing and most secure crypto platforms globally. Kraken clients trade more than 600 digital assets, traditional assets such as US futures and US-listed stocks and ETFs, and 6 different national currencies, including GBP, EUR, USD, CAD, CHF, and AUD. Trusted by millions of institutions, professional traders and consumers, Kraken is one of the fastest, most liquid and performant trading platforms available.

Kraken’s suite of products and services includes the Kraken App, Kraken Pro, the Krak App, Kraken Institutional, Kraken’s onchain offerings and the Ninja Trader retail trading platform. Across these offerings, clients can buy, sell, stake, earn rewards, send and receive assets, custody holdings, and access advanced trading, derivatives, and portfolio management tools.

Kraken has set the industry standard for transparency and client trust, and it was the first crypto platform to conduct Proof of Reserves. It complies with regulations and laws applicable to its business, while actively protecting client privacy and maintaining the highest security standards.

For more information about Kraken, please visit the official website.

The post WEMIX Solidifies Global Reach with Listing on Kraken appeared first on BeInCrypto.

On July 6, 2026, someone spent about four million dollars buying BONK, used it to control almost a hundred percent of a seven-wallet vote, and legally walked off with twenty million from the DAO’s treasury. No code was hacked. The voting worked exactly as designed. Here is how governance attacks work, why they are getting more common, and what actually stops them.

Summary

- BonkDAO lost about $20 million after an attacker bought enough BONK tokens to dominate a governance vote without exploiting any code.

- Governance attacks allow attackers to use legitimate voting systems to approve malicious proposals when token ownership is concentrated and voter participation is low.

- Timelocks, quorum requirements, and emergency controls remain the main safeguards against governance attacks by making treasury takeovers harder to execute.

Most crypto thefts break something: a smart-contract bug, a stolen key, a spoofed website. A governance attack breaks nothing. It uses a decentralized organization’s own voting system, exactly as intended, to pass a proposal that hands the attacker the treasury. The code performs flawlessly. The rules are followed to the letter. And the money leaves anyway, because the rules themselves allowed it.

That is what happened to BonkDAO on July 6, 2026. An attacker quietly bought roughly four million dollars of the BONK token on exchanges over several days, accumulated a dominant share of voting power, and submitted a proposal to the DAO’s treasury. When the vote closed, wallets linked to the attacker controlled about 99.878 percent of the votes cast, the proposal passed, and around twenty million dollars in BONK drained from the treasury to attacker-controlled wallets. Only seven addresses voted at all. There was no exploit in the usual sense; there was a takeover, executed through the front door.

Governance attacks are becoming more common precisely because they require no elite technical skill, only capital and a poorly defended voting system, and a growing number of DAOs, many of them memecoin projects with outsized treasuries, hold large treasuries behind exactly such systems. This guide explains what a governance attack is, walks through the BonkDAO case in detail, covers the main variants including the flash-loan version that needs no upfront capital at all, surveys the historical record from Beanstalk to Compound to Tornado Cash, and lays out the defenses that actually work along with the reasons they are so rarely fully deployed. The through-line is a single uncomfortable idea: in a system where money votes, whoever can rent enough votes can rewrite the rules, a vulnerability distinct from the code exploits and key compromises that drain cross-chain bridges.

What a governance attack is

A decentralized autonomous organization, or DAO, replaces executives and boards with token-holder voting. Holders of the governance token submit proposals, other holders vote, and if a proposal reaches the required threshold, a smart contract executes it automatically. Proposals can adjust parameters, upgrade code, or move treasury funds, and the appeal is that no single person controls the outcome; the community does, transparently and on-chain.

A governance attack turns that openness into a weapon. Instead of finding a bug in the DAO’s code, the attacker acquires enough voting power through entirely legitimate means, usually by buying the governance token, and then uses that power to pass a proposal that benefits the attacker at everyone else’s expense, most often by transferring the treasury to themselves, a purely economic attack that needs no transaction-ordering exploit or mempool trickery. Because the acquisition of tokens and the casting of votes are both permitted actions, the attack is what security researchers call purely in-protocol: it cannot be prevented by cryptography or better code auditing, because nothing is being exploited except the voting mechanism working as designed.

This is what makes governance attacks conceptually different from every other crypto theft. A reentrancy bug or a stolen private key is a failure of implementation; the system did something it was not supposed to do. A governance attack is a failure of design; the system did exactly what it was supposed to do, and the outcome was still a robbery. Fixing it requires rethinking the rules of the vote, not patching a line of code, which is why these attacks keep succeeding against protocols whose smart contracts are flawless.

The root vulnerability is almost always token-weighted voting, the default model in which one token equals one vote. Token-weighted voting quietly assumes that large holders are aligned with the protocol’s success, because they have money at stake. That assumption fails completely against an attacker who does not care about the protocol’s future and only wants to control one vote long enough to drain the treasury. To that attacker, buying tokens is not an investment in the project; it is the purchase of a weapon, discarded the moment it has fired.

The BonkDAO case, step by step

The July 2026 BonkDAO attack is a near-perfect illustration, because it used no exploit at all and every step was visible on-chain.

The setup was patient accumulation. Over several days, the attacker bought roughly four million dollars of BONK using exchange wallets, building voting power gradually instead of in one conspicuous purchase. Because BonkDAO used ordinary token-weighted voting on a standard governance platform, that accumulated BONK translated directly into accumulated votes, and because the buying was spread out and routed through exchanges, it did not trigger alarm. To any observer, it looked like ordinary accumulation of a memecoin.

The execution was a proposal to the treasury. The attacker submitted a governance proposal and let it sit live for six days, the normal voting window. Here the fatal weakness showed: almost nobody else voted. When the window closed, only seven wallet addresses had participated, and wallets controlled by the attacker held about 99.878 percent of the total voting weight. The four-million-dollar token position was more than enough to dominate a vote that essentially no one else showed up for. The proposal passed, and the DAO’s smart contract did what passed proposals do: it executed, moving roughly twenty million dollars in BONK from the treasury to the attacker’s wallets.

Three design failures converged. There was no meaningful quorum requirement, so a vote decided by seven wallets counted as legitimate. There was no timelock strong enough to let the community notice and react to an anomalous treasury proposal before it executed. And there was no emergency check, such as a multisignature control over large treasury movements, to catch a proposal that would drain the treasury. Any one of these, properly set, might have stopped the attack; their combined absence made a four-million-dollar purchase sufficient to steal twenty million.

The aftermath followed the now-familiar script. BonkDAO traced the exchange wallets used to accumulate the tokens and began working with exchanges, cross-chain bridges, the network’s foundation, and law enforcement to pursue recovery, while at least one exchange suspended BONK transfers. But governance-attack recoveries are notoriously hard, precisely because the theft was executed through the DAO’s own legitimate process, not an exploit that might be reversed, and the token’s price fell sharply on the news. The attack also did not stand alone: it landed in a stretch of DeFi security incidents that had the market on edge, underscoring how quickly value can leave when the weakest link is the governance layer instead of the code.

The main variants

Governance attacks share a logic but come in several forms, distinguished mainly by how the attacker acquires voting power and how quickly they strike.

The slow accumulation attack is the BonkDAO model: buy tokens gradually over days or weeks, avoid suspicion, and strike when you control enough votes and turnout is low. A patient attacker can go further, spreading purchases across many anonymous wallets so the accumulation looks like healthy, distributed participation instead of a single entity building a weapon. Low voter turnout is the enabling condition because it lowers the number of tokens needed to dominate; in a DAO where almost no one votes, a modest position can control outcomes.

The flash-loan attack is the most dramatic variant, because it requires no upfront capital at all. A flash loan lets a user borrow a very large sum with no collateral, provided the loan is repaid within the same transaction. An attacker borrows a huge amount, uses it to buy or otherwise acquire a controlling block of governance tokens, votes to pass a malicious proposal, extracts the treasury, and repays the loan, all atomically in a single transaction that either fully succeeds or fully reverts. Because everything happens in one block, there is no window for anyone to react. This variant is what makes timelocks so important, since a mandatory delay between a vote passing and its execution breaks the single-transaction requirement that flash-loan attacks depend on.

Other paths to voting power exist. An attacker might exploit a flaw in how the protocol distributes or mints governance tokens, acquiring votes without paying market price. They might manipulate a price oracle to acquire tokens cheaply, exploiting a swap’s slippage and price impact to move a thin market in their favor. Or they might use a sybil strategy, splitting holdings across many accounts to appear as many independent voters while acting as one. What unites all variants is the goal: assemble enough voting weight, by whatever means, to pass a proposal the rest of the community would never approve, then convert that proposal into stolen funds before anyone can stop it.

A short history of governance attacks

The BonkDAO attack was severe but far from the first, and the historical record shows both the pattern’s persistence and how defenses have evolved in response.

The Beanstalk attack in 2022 is the textbook flash-loan case. An attacker took an enormous flash loan, used it to acquire a supermajority of the stablecoin protocol’s governance tokens, passed a proposal that drained the treasury, and repaid the loan, all in a single transaction. The haul was well over a hundred million dollars, and the entire operation lasted one block. Beanstalk became the canonical example of why any governance system that lets freshly acquired tokens vote immediately, with no delay before execution, is dangerously exposed to flash loans.

The Compound episode in 2024 showed a subtler form. A group associated with a well-known whale pushed through a proposal directing tens of millions in the protocol’s tokens to a vehicle they controlled, after delegating enough tokens to meet quorum. The community was divided over whether to call it an attack or aggressive-but-legitimate governance, and the resolution came partly through the threat of centralized intervention and partly through negotiation, a reminder that many DAOs retain a centralized backstop precisely because pure token voting can produce capture. It also illustrated that governance attacks are not always anonymous outsiders; they can be sophisticated insiders exploiting low participation and misaligned incentives in plain sight, the same fragility that shadows liquid staking tokens when one provider dominates.

The Tornado Cash case in 2023

The Tornado Cash case in 2023 delivered a chilling twist: an attacker passed a malicious proposal that granted themselves a controlling number of votes, effectively seizing the entire governance system, then, after extracting value, used their captured power to reset the malicious changes. The privacy protocol’s governance briefly ceased to exist as a decentralized entity because one proposal handed one actor total control. Smaller cases, from Build Finance to various memecoin DAOs, repeat the pattern at lower stakes. The consistent lesson across all of them is that treasuries are only as safe as the voting rules guarding them, and that a flawless smart contract offers no protection when the vote itself is the attack surface.

Why this is so hard to fix

If the defenses are known, a fair question is why governance attacks keep succeeding. The answer is that every defense trades away something a DAO values, and the trade-offs are genuinely uncomfortable, which is why so many projects postpone them until an attack forces the issue.

Consider the central tension. The entire premise of a DAO is open, permissionless participation: anyone can hold the token, anyone can propose, anyone can vote, and outcomes reflect the community instead of a gatekeeper. Every strong defense against governance attacks chips at exactly that openness. A high quorum requirement can paralyze a DAO whose members rarely vote, leaving it unable to pass even benign proposals. A long timelock slows the organization’s ability to respond to genuine emergencies, the very speed that on-chain governance was supposed to improve. An emergency multisignature or veto committee reintroduces a trusted group, which is a form of the centralization DAOs exist to escape. Each safeguard makes the DAO safer and less decentralized at the same time, and communities are understandably reluctant to give up the ideal that drew them together.

Low participation compounds the problem and resists easy solution. Most DAOs suffer chronically low voter turnout, with studies finding that a large share have only a handful of active voters, and low turnout is the single condition that makes governance attacks cheap, because it lowers the token threshold an attacker must reach. Yet turnout cannot simply be mandated; it reflects the reality that most token holders are passive, hold for price rather than participation, and have little time or expertise to evaluate proposals. Delegation, where holders assign their votes to engaged representatives, helps, but it concentrates power in delegates and introduces its own capture risks. The passivity that enables attacks is a structural feature of token ownership, not a bug that a single mechanism can eliminate.

There is also the deeper problem that a token market cannot distinguish a supporter from an attacker. Both are simply buyers willing to pay for tokens, and from the market’s perspective they are indistinguishable right up until the malicious proposal executes. Token-weighted governance assumes economic alignment, that anyone holding many tokens must want the protocol to succeed, but an attacker who plans to drain the treasury and discard the tokens has no such alignment, and no purchase-time signal reveals the difference. This is why some researchers argue that token voting alone can never be fully secure and that durable solutions require non-token inputs, reputation, identity, or contribution history, that markets cannot simply buy. Those approaches are early and hard to implement without reintroducing gatekeepers. The uncomfortable conclusion is that governance security is not a solved problem with a checklist to apply, but a live design frontier where every fix costs some decentralization, and where the cheapest, most open configuration, the one many DAOs default to, is precisely the one attackers find most inviting.

The defenses that work

Because governance attacks exploit design, not code, the defenses are matters of mechanism design, and a well-configured DAO can make an attack unprofitable even if it cannot make it impossible.

Timelocks are the single most important defense. A timelock imposes a mandatory delay between a proposal passing and its execution, and it does two things at once. It breaks flash-loan attacks entirely, because the borrowed tokens cannot be held across the delay, defeating the single-transaction requirement. And it gives the community a window to notice an anomalous proposal and respond before the treasury moves. The BonkDAO attack, with its six-day live window but apparently no effective execution delay or reaction, shows that a voting period is not the same as a timelock; what matters is a hard delay between approval and execution during which defenders can act.

Quorum requirements raise the bar for legitimacy. A quorum sets a minimum amount of voting participation for a proposal to pass, so a vote decided by a handful of wallets does not count. Had BonkDAO required a substantial quorum, a seven-wallet vote would have failed regardless of how the attacker’s tokens were distributed. Related measures include conviction voting, where voting power builds the longer tokens are committed, penalizing the sudden accumulation that attacks rely on, and delegation systems that raise overall turnout, which mechanically increases the tokens an attacker must acquire.

Emergency controls provide a last line. A multisignature control over large treasury movements, or a veto mechanism allowing trusted actors to pause or reject a clearly malicious proposal, can stop a drain even after a vote passes. These measures reduce decentralization, which is a real trade-off DAOs must weigh, but they exist precisely because pure token voting has repeatedly proven drainable. Many protocols keep a centralized safeguard for exactly the scenario Compound faced.

Finally, limiting what governance can do shrinks the prize. If a single proposal cannot unilaterally move the entire treasury, and if large disbursements require additional steps or approvals, the value an attacker can extract falls, and with it the incentive to attack at all. The unifying principle across every defense is to make the cost of acquiring enough votes exceed the value that could be stolen, or to insert enough delay and friction that the community can intervene before the theft completes. A DAO that has done neither, holding a large treasury behind cheap, immediate, low-turnout token voting, is not running a governance system so much as an unlocked vault with a suggestion box. BonkDAO’s twenty-million-dollar lesson is that the suggestion box, in the wrong hands and with enough tokens behind it, opens the vault.

The wider context is that governance is becoming a bigger target as DAOs hold more value. Memecoin communities in particular have accumulated substantial treasuries, often denominated in volatile tokens whose value can swing sharply, while running the simplest possible voting systems, and the combination of a rich prize behind a weak lock is exactly what attackers seek. As on-chain governance spreads from experimental protocols to organizations managing serious money, the gap between DAOs that have hardened their voting and those that have not becomes one of the clearest dividing lines in crypto security. The attacks are not going away, because the incentive is structural and the cheapest configuration is the most vulnerable one. What changes, DAO by DAO, is whether the treasury sits behind defenses proportionate to its size, or behind a vote that four million dollars and an empty room can win.

Frequently asked questions

What is a governance attack?

A governance attack is when someone acquires enough voting power in a DAO, usually by buying its governance token, and uses that power to pass a proposal that benefits them at the community’s expense, typically draining the treasury. It exploits the voting mechanism working as designed, not a bug in the code, which is what makes it different from a typical smart-contract hack.

How did the BonkDAO attack work?

The attacker spent roughly four million dollars buying BONK on exchanges over several days, accumulating dominant voting power. They submitted a treasury proposal that sat live for six days, and because only seven wallets voted, the attacker’s wallets controlled about 99.878 percent of the vote. The proposal passed, and roughly twenty million dollars in BONK drained from the treasury, with no smart-contract exploit involved.

Was any code hacked in a governance attack?

No. In a governance attack, the smart contracts perform exactly as designed. The theft happens because the voting rules themselves allowed a malicious proposal to pass and execute. This is why governance attacks cannot be prevented by better code audits alone; they require changes to the voting mechanism, such as timelocks, quorums, and emergency controls.

What is a flash-loan governance attack?

It is a variant that needs no upfront capital. The attacker borrows a large sum with no collateral, uses it to acquire a controlling block of governance tokens, passes a malicious proposal, drains the treasury, and repays the loan, all within a single transaction. The 2022 Beanstalk attack, which took over a hundred million dollars, is the canonical example, and timelocks are the main defense because they prevent execution within one transaction.

Why are governance attacks becoming more common?

They require capital and a weak voting system rather than elite technical skill, which lowers the barrier compared with finding code exploits. Many DAOs, especially memecoin projects, hold large treasuries behind simple token-weighted voting with low voter turnout, making them attractive targets. Accumulating enough tokens to control a low-turnout vote is often cheaper than the treasury it can capture.

Can stolen funds from a governance attack be recovered?

Recovery is difficult because the theft was executed through the DAO’s own legitimate process rather than an exploit that might be reversed. Projects typically trace the wallets, coordinate with exchanges, bridges, and law enforcement, and hope to freeze funds before they are laundered, but success is uncertain. BonkDAO began such efforts after its attack, with recovery unresolved.

What defenses stop governance attacks?

The main defenses are timelocks that delay execution after a vote passes, quorum requirements that invalidate low-turnout votes, conviction voting that penalizes sudden token accumulation, emergency multisignature or veto controls over large treasury movements, and limits on what a single proposal can do. Together, they aim to make an attack cost more than it could steal or to give the community time to intervene.

Is token-weighted voting the problem?

Token-weighted voting is the core vulnerability because it assumes large holders are aligned with the protocol when in fact, an attacker can buy votes purely to drain the treasury. Alternatives and supplements like conviction voting, quorum floors, delegation to raise turnout, and non-token reputation systems all aim to weaken the assumption that whoever holds the most tokens should control the outcome.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile, and you can lose your entire investment. Always do your own research. Information current as of July 7, 2026.

Key Takeaways

- Gemini rolled out commission-free U.S. stock trading Tuesday, providing access to thousands of exchange-listed equities through its mobile platform.

- Shares of GEMI declined 3.9% following the launch announcement; Coinbase (COIN) lost 2.4% and Robinhood (HOOD) slipped 2.3%.

- Real-time market data will be provided by Nasdaq; Apex Clearing Corp. serves as the clearing and custody partner.

- Alabama, Arkansas, Illinois, Massachusetts, Texas, Puerto Rico, Washington D.C., and Guam residents cannot access the new service.

- GEMI is currently priced at $4.35, representing an 86% decline year-over-year, despite recording 39% revenue growth over the trailing twelve months.

Gemini Space Station unveiled its commission-free stock trading platform for U.S. investors on Tuesday, marking a strategic expansion beyond cryptocurrency as the Winklevoss brothers pursue their vision of creating a comprehensive financial services application.

The cryptocurrency exchange will enable eligible users to access thousands of publicly traded U.S. securities through its existing mobile application. Market data will stream in real-time from Nasdaq, while Apex Clearing Corp., part of Apex Fintech Solutions, handles custody and clearing operations.

Gemini Galactic Markets, LLC, registered with FINRA and protected by SIPC, facilitates the securities offerings. While commission-free for standard trades, certain transaction categories may incur fees.

Gemini Space Station, Inc., GEMI

Prior to the announcement, GEMI stock was changing hands at $4.35 but tumbled 3.9% in early Tuesday session following the product launch. The equity has plummeted 86% over the past twelve months, leaving the company with approximately $526 million in market capitalization. Despite achieving 39% revenue expansion in the most recent twelve-month period, profitability remains elusive.

“Building financial platforms is something we’ve been doing for more than ten years,” noted Cameron Winklevoss, who co-founded Gemini and serves as president. “Crypto was our starting point, and stocks represent our expansion so customers can consolidate their financial activities within the Gemini ecosystem.”

Tyler Winklevoss, serving as CEO, stated: “We’re working toward integrating multiple financial instruments—ranging from cryptocurrencies and stocks to derivatives—within a single regulated infrastructure.”

This strategic pivot creates head-to-head competition with established players Robinhood (HOOD) and Coinbase (COIN). Market participants responded negatively to both competitors—COIN retreated 2.4% while HOOD declined 2.3% during Tuesday’s session.

Established Regulatory Framework

Gemini enters the brokerage space with regulatory infrastructure already established. The platform obtained broker-dealer authorization from FINRA in 2022. Subsequently, the company modified its registration to function as an introducing broker, enabling customer order routing for all NMS securities through Apex for trade execution and settlement.

Additionally, Gemini obtained a Derivatives Clearing Organization registration from the CFTC in April 2026—furthering its ambitions of constructing a comprehensive regulated trading ecosystem.

Currently, the stock trading functionality remains unavailable to residents of Alabama, Arkansas, Illinois, Massachusetts, Texas, Puerto Rico, Washington D.C., and Guam.

Financial Performance Shows Revenue Growth Amid Losses

During the first quarter of 2026, Gemini reported a loss of $0.93 per share, falling short of analyst expectations of -$0.61—representing an earnings miss of approximately 52%. Quarterly revenue reached $50.27 million, marking a 42% increase compared to the prior-year period.

Mizuho Securities revised its GEMI price objective downward from $12 to $10 earlier in the year while maintaining its Outperform recommendation, highlighting the firm’s transformation into a diversified financial markets operator.

During the company’s shareholder meeting, investors re-elected six board members, including both Tyler and Cameron Winklevoss, for terms extending through 2027.

According to InvestingPro analysis, GEMI shares appear undervalued based on current trading levels.

U.S. SEC to propose crypto rule as soon as this month to ease startups, fundraising

Quentin Tarantino’s Final Movie Gets Major Production Update After 7 Year Delay

Bernie Sanders says he told Graham Platner to ‘step aside’

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: High Hopes

-

Fashion24 hours ago

Fashion24 hours agoOpen Thread: What Great Books Have You Read Recently?

-

NewsBeat3 days ago

NewsBeat3 days agoTaylor Swift and Travis Kelce wedding staffer hilariously struggles to keep her cool while checking in megastars

-

Politics4 days ago

Politics4 days agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

Crypto World6 days ago

Crypto World6 days agoAirdrop Registration Becomes Key Focus For Remittix As RTX Launch Updates Approach

-

Business22 hours ago

Business22 hours agoAXT Shares Jump Nearly 14% as Semiconductor Materials Maker Rebounds on AI-Linked Indium Phosphide Demand

-

Sports6 days ago

Sports6 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

Crypto World5 days ago

Crypto World5 days agoBinance stock trading tops $1B in first month after launch

-

Crypto World4 days ago

Crypto World4 days agoStandard Chartered Secures MiCA License as ESMA Adds 37 New Crypto Firms

-

NewsBeat7 days ago

NewsBeat7 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

-

Crypto World6 days ago

Crypto World6 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

Crypto World21 hours ago

SK hynix (000660.KS) Stock Dips as $28B Nasdaq ADR Offering Drives AI Memory Expansion

-

Crypto World2 days ago

Crypto World2 days agoSouth Africa proposes crypto tax guidance under existing rules

-

News Videos1 day ago

News Videos1 day agoBest Time to Enter Small Caps Right Now? Another Bull Run? | Financially Free

-

Tech2 days ago

Tech2 days agoLenovo laptops are now shipping with YMTC SSDs, a sign of Chinese NAND entering the mainstream

-

Business6 days ago

Business6 days agoMeta Platforms Stock Jumps 7% Today as Bloomberg Reports Company Plans to Enter the Cloud Business

-

NewsBeat5 days ago

NewsBeat5 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

News Videos12 hours ago

News Videos12 hours agoWhats Hidden Inside This Cash Register? #treasure #reselling #money

-

Business5 days ago

Business5 days agoWhat a 10 Percent Drop Means for Buyers, Sellers and Renters

-

Crypto World5 days ago

Crypto World5 days agoBinance Re-Enters Philippines As EU MiCA Rules Restrict Access

You must be logged in to post a comment Login