Crypto World

DOJ Charges Crypto Investor in Alleged $20M Investment Fraud

Cointelegraph is committed to providing independent, high-quality journalism across the crypto, blockchain, AI, and fintech industries.

All news, reviews, and analyses are produced with full journalistic independence and integrity. For more details on our standards and processes, please read our Editorial Policy.

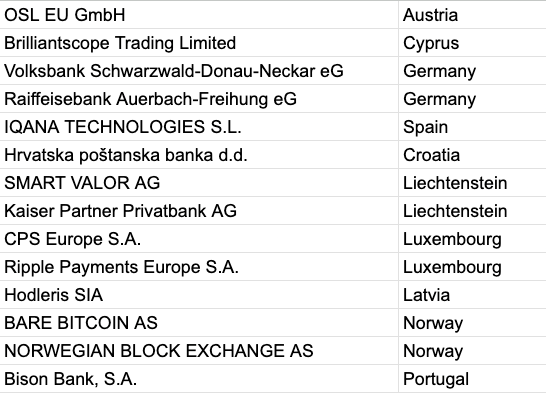

European authorities added 14 crypto companies to the Markets in Crypto-Assets (MiCA) framework register in the second post-deadline update, signaling a slower licensing pace after an initial surge.

The European Securities and Markets Authority (ESMA) updated its interim MiCA register on Thursday, bringing the total number of licensed crypto-asset service providers (CASPs) to 294.

The new entries include Ripple Payments Europe, the European payments arm of blockchain company Ripple, as well as Portugal-based Bison Bank and Croatia’s state-owned bank, Hrvatska poštanska banka (HPB).

The update follows ESMA’s previous register expansion on July 3, when the regulator added 37 CASPs in the first major post-deadline update after MiCA’s transitional period ended.

Banks deepen MiCA presence

Several newly added companies highlight the continued entry of traditional financial institutions into Europe’s regulated crypto market.

In addition to Bison Bank and HPB, the MiCA register added two cooperative banks from Germany, namely Volksbank Schwarzwald-Donau-Neckar and Raiffeisenbank Auerbach-Freihung.

The update also included Liechtenstein-based Kaiser Partner Privatbank, expanding the presence of private banking groups offering regulated crypto services under MiCA.

14 newly approved CASPs in the MiCA register update on July 16, 2026. Source: ESMA

The register counts dozens of traditional finance institutions, including Spain’s BBVA and CaixaBank, Germany’s Commerzbank, France’s CACEIS Bank and Standard Chartered Luxembourg.

EMT and ART registers remain unchanged

ESMA reported no changes to its registers for electronic money tokens (EMTs), a category of crypto-assets designed to maintain a stable value against a single official currency, or asset-referenced tokens (ARTs), which are linked to multiple assets such as currencies or commodities.

As of the latest update, the EMT register counted 21 unique issuers, while the ART register continued to list no approved issuers.

Related: MiCA licensing only the beginning as crypto custodians face scrutiny

The regulator also added two entities to its non-compliant register following actions by Italy’s securities regulator, the Commissione Nazionale per le Società e la Borsa (CONSOB).

The new additions were Reversal Investment Group and Kortex, bringing the total number of entries on the non-compliant list to 164, including crypto exchange MEXC.

Magazine: Will the crypto lobby’s $189M campaign get CLARITY over the line?

Prediction markets have stopped being a niche crypto experiment for some time now, and they’ve ventured well into the mainstream. They’re even cited in political debates, news channels, and just about everywhere on social media.

Even regulated exchanges are competing with on-chain protocols for the same traders, and the biggest sportsbooks and brokerages have piled into the race.

In this guide, I’ll break down the five platforms that matter most right now: what each one is, how the trading actually works, what you pay in fees, and what makes each one special.

Best Prediction Markets in 2026: A Quick Rundown

We ranked the platforms on liquidity, market breadth, fees, access, regulation and custody, and the actual trading experience. Keep in mind every figure in this guide was checked against primary data in July 2026, including CFTC’s registries of designated exchanges, analytics dashboards, official fee schedules, company announcements, etc.

In a nutshell:

- Polymarket: best prediction market overall, with a record June and a regulated US arm

- Kalshi: best regulated US prediction exchange and the sector’s volume leader

- Limitless: best up-and-coming on-chain market, built on Base

- Myriad Markets: best media-native prediction market

- Azuro: best on-chain prediction infrastructure, powering over 50 apps

.cp-only-mobile{display:none}

@media(max-width:720px){

.cp .table .price .cp-only-mobile{display:inline;font-weight:600;margin-right:.25rem}

}

| Name | Features | Rating |

|---|---|---|

|

||

|

||

|

||

|

||

|

Polymarket: Best Prediction Market Overall

- Over $10B traded in June 2026

- Non-custodial wallet custody

- Backed by ICE & X partnership

- No maker fees for liquidity

- Oracle resolution dispute risks

- Thinner market selection in US

- Wallet setup can confuse beginners

As a surprise to no one, Polymarket is the biggest prediction market in the world and the one that turned event trading into a spectator sport.

NYSE parent Intercontinental Exchange has committed up to $2 billion to the company at a valuation around $9 billion, X made Polymarket its official prediction market partner with odds piped into the feed alongside Grok analysis, and the company told CNBC in late June that annualized revenue had passed $1 billion.

Executives have confirmed a POLY token and an airdrop are coming, though nothing had launched as of July 2026.

The platform runs on Polygon and settles in USDC, with funds held in your own wallet. Since December 2025, it also operates a separate, CFTC-regulated US exchange, the product of its $112 million acquisition of licensed operator QCEX.

Trading works on a central order book. You basically buy Yes or No shares priced from 0.1 cent to 99.9 cents, with winning shares redeemable at $1, and you can exit any position before resolution. On the international venue, outcomes are decided by UMA’s optimistic oracle, where token holders confirm or dispute proposed results.

The US exchange requires full identity verification and resolves under its regulated rulebook.

Polymarket Fees

Fees are modest and skewed against takers:

- International venue: takers pay a formula-based fee across 10 market categories, with the highest at 50/50 odds. Sports peak at 0.75% and crypto markets at 1.80%, while geopolitics markets remain fee-free. Makers pay nothing and earn a daily share of taker fees.

- US venue: takers pay at most $1.50 per 100 contracts at 50 cents, and resting orders earn a small rebate.

- No deposit or withdrawal fees on either venue beyond network gas.

Pros and Cons of Polymarket

Pros:

- Deepest liquidity and market breadth of any prediction platform. Over $10B traded on the international venue in June 2026 alone

- Self-custody: funds stay in your wallet (USDC on Polygon), no counterparty holding your balance

- Now has a CFTC-regulated US arm after the QCEX acquisition, so US users have a legal on-ramp

- Low fees: makers pay nothing, takers pay only on some categories, geopolitics markets are free

- Institutional credibility, with ICE (NYSE’s parent) backing, official X partnership, $1B+ reported annualized revenue

Cons:

- Oracle resolution risk: UMA disputes have flipped outcomes that looked settled (the $160M Zelensky suit market), and the fact that disputes still happen post-overhaul

- The regulated US venue has a much thinner market list than the global one, and the global one blocks US users

- Wallet-based onboarding still confuses newcomers used to normal fintech apps

- Trustpilot reviewers cite account disablements without explanation and slow support

Kalshi: Best Regulated US Prediction Market

- Segregated US customer funds

- Direct USD fiat on-ramps

- Deep regulated US market menu

- Supports institutional APIs

- Mandatory KYC requirements

- No crypto/self-custody support

- Ongoing state-level sports lawsuits

Kalshi has been a CFTC-designated contract market since 2020.

In June alone, the platform was valued at $2B after its latest funding round. Its World Cup winner market alone attracted more than $1.4 billion.

It works quite similarly to Polymarket. You just deposit dollars, pass full KYC, and trade Yes/No contracts on an order book, from Fed decisions and inflation prints to sports and award shows.

Kalshi contracts are also reachable through brokers, which is how Robinhood users trade them. Once US-only, the exchange now accepts customers from around 143 countries, though it remains restricted in about 54 jurisdictions, including the UK, Canada and Australia.

Kalshi’s specialty could be the fact it offers the deepest regulated market menu in the US, institutional-grade APIs, and the confidence of trading on a federally supervised venue.

The drawbacks? Depends on how you see it, but the design obviously carries KYC on everything, no self-custody (and the fact there’s an ongoing legal war over its sports contracts, with several states and tribal groups challenging them in court, but it’s the same with Polymarket).

Kalshi Fees

Fees are taker-only on most markets and depend on price: roughly 7 cents to $1.75 per 100 contracts, most expensive at 50/50 odds and cheapest at the extremes. Most resting orders pay nothing, there are no settlement or membership fees, and ACH deposits and withdrawals are free.

Pros and Cons of Kalshi

Pros:

- Sector volume leader: $31.5B in June 2026, roughly triple Polymarket’s international venue

- Full federal oversight as a CFTC-designated exchange since 2020; customer funds in segregated accounts

- Fiat-native: free ACH deposits and withdrawals, no crypto knowledge needed, clean purpose-built app

- Reachable through brokers like Robinhood, and now open to users in roughly 143 countries

Cons:

- Depending on how much you value your privacy, there’s basically KYC on everything and no self-custody

- The ongoing legal war over sports contracts: blocked or contested in several states (Nevada injunction in force, losses in Maryland, Ohio, New York), as we mentioned.

- Fees peak at 50/50 odds, which is exactly where most action is

Limitless: Best Up-and-Coming On-Chain Market

- 15-min crypto price contracts

- Smooth Base network settlement

- Features LMTS token utility

- AMM & order-book hybrid

- Strictly prohibits US users

- Airdrop points inflate activity

- Thinner liquidity outside crypto

Limitless is one of the fastest-growing crypto-native prediction markets, and it looks nothing like Polymarket.

Built on Base, it leans into rapid-fire trading: hourly and 15-minute crypto price markets alongside daily and longer-dated questions.

Trading is wallet-based with no default KYC, settled in USDC on Base. Most markets run on a central order book, with an AMM handling some of the rest. Getting started takes a wallet and a deposit, and there is no account approval process.

Limitless Fees

The fee model rewards liquidity providers:

- Makers pay nothing across the board.

- AMM markets charge a flat 0.40%.

- Order-book buys cost 0.40% to 3.00% depending on price, and sells 0.42% to 1.50%, peaking at 50/50 odds.

- Taker fees on the short-duration crypto markets are currently rebated 100% to makers.

Its LMTS token went live in October 2025, and in May 2026 the team filed an application with the CFTC to launch a regulated US exchange offering five-minute Bitcoin event contracts, which is still pending.

Pros and Cons of Limitless

Pros:

- Fastest-growing on-chain venue: 61,808 monthly active traders in June, from double digits in early 2024

- Rapid-fire markets nobody else offers at scale: hourly and 15-minute crypto price contracts on Base

- No KYC, wallet-in-and-trade onboarding; makers pay zero fees and short-duration taker fees are currently rebated to makers

- Serious regulatory ambition: CFTC application filed May 2026 for regulated 5-minute BTC contracts; LMTS token already live

Cons:

- US users are just outright prohibited by its terms of service

- Activity metrics are flattered by airdrop-points seasons. Team-reported volume ($3.4B) runs well above independent measurement ($1.7B), something to keep in mind

- Unsurprisingly, liquidity can be thin next to Polymarket and Kalshi, especially outside crypto markets

- Order-book trading on short timeframes has a real learning curve for casual users

Myriad Markets: Best Media-Native Prediction Market

- Predict while reading articles

- Backed by Hack VC & Jump

- No identity checks needed

- Easy casual user onboarding

- Thin overall exit liquidity

- Lacks advanced trading tools

- Fragmented across three chains

Myriad is a bit of an outlier here, and we could even say it takes the opposite approach to everyone else on this list. So, instead of building a destination exchange, it just embeds prediction markets where audiences already are.

The platform was built by DASTAN, the company formed by the merger of crypto publisher Decrypt and Rug Radio, and its markets appear inside articles, apps and games rather than on a standalone trading screen.

It’s essentially a non-custodial AMM where outcome prices always sum to $1. Markets live on Abstract, BNB Chain and Linea, funds stay in your own wallet, no KYC is required, and Chainlink serves as the official oracle, including for its World Cup markets.

Myriad Fees

Fees are light and simple:

- Buys carry a 0% to 2% fee depending on the market, plus a flat $0.0085 per transaction that covers gas.

- Fees are shared between liquidity providers, the protocol and the builders who integrate it.

Pros and Cons of Myriad Markets

Pros:

- Unique distribution: markets embedded directly in content and apps (built by DASTAN, Decrypt’s parent), so you predict where you already read

- Non-custodial and KYC-free, with cheap, simple fees (0 to 2% plus a flat $0.0085 per transaction)

- Chainlink as the official oracle, a more standardized resolution setup than most small venues

- Credible backing: $20M pre-Series A in Feb 2026 from Hack VC and Jump Crypto; 430K+ users within two months of mainnet

Cons:

- Small on-chain footprint; many markets feel thin and exit liquidity can be poor

- More an engagement product than a trading venue (serious traders will outgrow it)

- Spread across three chains (Abstract, BNB Chain, Linea), which fragments the experience

- Relatively a young platform with limited track record on contested resolutions

Azuro: Best On-Chain Prediction Infrastructure

- No liquidity fragmentation

- Multiple frontends like DexWin

- Earn shares of pool revenue

- Polygon, Base & Arbitrum support

- No primary destination app

- Indirect fees via odds spreads

- Highly skewed to sports betting

Azuro is technically not a prediction market, but more like a liquidity layer that prediction and betting frontends build on. In other words, the protocol hosts markets and pooled liquidity in smart contracts, and every app plugged into it shares that same pool: a bet placed on one frontend draws from the same liquidity as a bet on another.

In practice you use Azuro through those frontends. bookmaker.XYZ was the first independent one, DexWin offers a gasless sportsbook experience, PinWin extends Azuro liquidity to Solana users, etc.

Builders earn a share of pool profits generated by their own users, which is why new frontends keep appearing.

Azuro fees

There is no maker/taker fee schedule to compare. Costs sit inside the odds spread, the way a bookmaker builds margin into its prices, so the practical move is to compare quoted odds across frontends rather than hunt for a fee page.

Note that your experience depends on whichever frontend you choose and on the protocol’s scale, while real, is modest compared to the consumer giants above.

Pros and Cons of Azuro

Pros:

- It has quite a robust infrastructure, reaching well above $414M in all-time volume, $5.1M protocol revenue, and at least 54 apps built on its shared liquidity layer so far

- One pooled liquidity base across every frontend, so even new apps launch with usable depth

- Permissionless and KYC-free at the protocol level, live across Polygon, Gnosis, Base and Arbitrum

- Choice of experiences: sportsbook-style (bookmaker.XYZ, DexWin) or Solana-friendly (PinWin) without fragmenting liquidity

Cons:

- Not a destination app; quality of your experience depends entirely on the frontend you pick

- No transparent fee schedule; costs hide in the odds spread, so comparing value takes effort

- Sports-heavy in practice, with less breadth in politics and culture markets

- Modest scale overall next to the consumer giants, and the protocol’s TVL has been drifting down

What Are Prediction Markets?

Prediction markets let you trade contracts on the outcome of real-world events: elections, sports, interest rates, crypto prices, even award shows.

Each market has Yes and No shares priced between 1 cent and 99 cents, and the price doubles as a probability. So, if Yes trades at 60 cents, the market collectively thinks the event has about a 60% chance of happening. The idea is pretty simple: correct shares redeem at $1 when the market resolves and wrong ones expire worthless.

You can also sell at any time before resolution and lock in a profit or cut a loss.

And how different is it from sports betting? Well, you trade against other people rather than a bookmaker, prices move like any market, and you can exit early instead of riding a bet to the end.

Risks to Know Before You Trade

In July 2025, a Polymarket market asking whether Ukraine’s president would wear a suit before July drew roughly $160 million in wagers and resolved No after nine days of oracle disputes, despite plenty of media outlets describing his NATO summit outfit as exactly that.

UMA overhauled how Polymarket resolutions are proposed afterward, but disputed markets have surfaced again since, including a $16 million market that spent weeks in dispute limbo in April 2026. On any oracle-resolved platform, read the resolution rules before you size a position.

CryptoPotato once covered a report from the WSJ that claimed Polymarket paid college-age creators to stage up to $1.9 million in fake bets, and that the majority of the winning bets, and the reason for the platform’s viral growth, had to do with copycat versions of its website.

Regulation is another front, particularly for Kalshi’s sports contracts. They have won in some courts, including a federal appeals ruling in its favor, and lost in others, with courts in Maryland, Ohio, Nevada and New York siding against it as of early July 2026.

Why Trust CryptoPotato

As we always say, CryptoPotato is a veteran cryptocurrency-focused media outlet, and we cover the industry since 2016.

Every figure in this guide was verified against primary sources, including registry of designated

exchanges, official fee documentation, and raw data from sources and company statements.

We carefully examine each narrative and its triggers (as well as effects) to bring you the full picture.

FAQ

Are prediction markets legal in the US?

Trading on CFTC-designated exchanges such as Kalshi, Polymarket US, and Crypto.com’s derivatives venue is federally regulated and legal.

Keep in mind that sports event contracts remain contested, with several states and tribal groups challenging them in court, so availability can vary by state. Moreover, offshore and on-chain platforms generally block US users (or fall into a gray zone).

What is the difference between a prediction market and sports betting?

At a sportsbook, you bet against the house at fixed odds, whereas on a prediction market you trade against other people, prices float with the crowd’s information, and you can sell your position early.

The margin you pay is a visible fee or spread rather than odds shaded against you.

Which prediction market is best for crypto users?

Polymarket’s international venue offers the deepest on-chain liquidity and self-custody in USDC. Limitless is the pick for fast crypto price markets on Base, and Myriad is the easiest way to dip in casually without visiting an exchange at all.

How do prediction market odds work?

Prices and probabilities are the same thing, so a “Yes” share trading at 25 cents implies a 25% chance, and if the event happens, it pays out $1, quadrupling your money.

That also means the market updates in real time: when news breaks, the price moves before most headlines do, which is why traders treat these markets as a live probability feed as much as a way to bet.

Conclusion: Best Prediction Markets in 2026

Prediction markets have managed to evolve far beyond a crypto niche – as we established in this guide. They offer a sophisticated way to trade on everything from politics to macroeconomics and sports. Whether you prioritize deep liquidity, regulatory oversight, self-custody, or fast-moving crypto markets, there’s definitely a platform that’s tailored to your trading style.

Just remember that regardless of the platform you choose, you have to understand the rules that govern market resolution, the fee structure, as well as any possible jurisdiction restrictions – this is just as important as identifying opportunities.

As our industry continues to mature, informed users will be better positioned to take advantage of this rapidly expanding market.

The post Best Prediction Markets in 2026: The Complete Guide appeared first on CryptoPotato.

In one week of July 2025, the House passed three crypto bills. One is law. One is law by accident and the President will not sign it. The third has not had a Senate vote in 365 days, and it was supposed to be the important one.

Summary

- On July 17, 2025, the House passed the CLARITY Act 294-134 with more than 70 Democrats crossing over, the strongest congressional endorsement of digital asset legislation in American history. It has not received a Senate floor vote in the year since.

- It was the middle bill of Crypto Week, when the House passed three digital asset measures in rapid succession. Tracking all three one year later produces a scorecard nobody in the industry wants to read aloud.

- GENIUS became law on July 18, 2025 and hits its first major rulemaking deadline tomorrow. The Anti-CBDC Surveillance State Act cleared the House 219-217, stalled, then reached law by riding inside a housing bill the President is refusing to sign.

- CLARITY is stuck on ethics. The merged Senate draft released July 14 omits the provision Democrats named as their price, and three senators declared opposition the same day.

- The pattern across all three is the same: what passed was what could be attached to something else or what nobody had a personal stake in blocking. CLARITY is neither.

Washington called it Crypto Week. In a handful of days in July 2025, the House of Representatives passed three digital asset bills in succession, and the industry treated the sequence as the moment its lobbying decade finally paid. The CLARITY Act cleared 294-134 on July 17. The GENIUS Act cleared 308-122 the same day and was signed into law on July 18. The Anti-CBDC Surveillance State Act squeaked through 219-217. Three bills, one week, one chamber, and a widespread assumption that the Senate was a formality. Today is the one-year anniversary of the first of those votes. Exactly one of the three arrived where it was supposed to. Tracking what happened to the other two explains more about how crypto legislation actually works than any amount of vote-counting on the bill still pending.

The bill that made it

GENIUS is the success case, and it is worth being precise about why, because the reason is not that it was the best bill.

It passed the Senate 68-30 in June 2025, cleared the House 308-122 on July 17, and was signed into law on July 18, creating the first federal framework for payment stablecoins. It reaches its first major rulemaking deadline on July 18, 2026, one year to the day. White House digital assets adviser Patrick Witt has repeatedly pointed to that anniversary as proof that coordinated action produces results, which is true and also somewhat beside the point.

GENIUS passed because almost nobody with power had a reason to stop it. Banks wanted rules for stablecoins because stablecoins were happening regardless and they preferred a framework they could live inside. The industry wanted legitimacy. Regulators wanted reserve requirements. The politics of requiring an issuer to hold full reserves in liquid assets and disclose them monthly are not politics at all; they are housekeeping. There was no ethics dimension, no jurisdictional turf war between agencies, and no obvious way for anyone in office to profit from the outcome in a manner that made colleagues uncomfortable.

That is the template for what Congress can pass on crypto. Narrow scope, clear beneficiary, no personal stakes. Note how little of that describes CLARITY.

The bill that made it by accident

The Anti-CBDC Surveillance State Act is the strangest entry on the scorecard, and its path is worth tracing because it shows what happens when a crypto bill cannot pass on its own.

It cleared the House by two votes, 219-217, which is not a mandate. Then it stalled. A promise to attach it to the defense authorization bill went unkept, which in Washington is a soft burial. It should have died there.

Instead it reached law by an unlikely route: a provision barring the Federal Reserve from issuing a central bank digital currency through 2030 rode inside the 21st Century ROAD to Housing Act, a bipartisan housing package that passed the Senate 85-5 and the House 358-32. The crypto industry got its anti-CBDC win as a passenger on a bill about construction permitting.

And then the President refused to sign it. Not over the CBDC provision, which he supports, having argued that a central bank digital currency would threaten financial stability, individual privacy, and American sovereignty. He is withholding signature over the SAVE America Act, an unrelated elections bill demanding proof of citizenship and photo identification for federal voting. The housing measure becomes law without his signature once the ten-day window closes, so the maneuver functions as leverage instead of a veto. The CBDC ban arrives regardless, delivered by a President who declined to sign the vehicle carrying it.

The lesson is not subtle. A crypto priority that could not pass on its own merits became law by attaching itself to something that could, and then survived the President’s own obstruction because the mechanism did not require his cooperation. That is three separate accidents in a row producing the right outcome, and it is not a strategy anyone can repeat on purpose.

The bill that did not

Which brings us to CLARITY, and to the number that should embarrass everyone involved: 365 days on the Senate side with no floor vote.

The bill did not stall for lack of support in the abstract. It passed the House with more than 70 Democrats, which is the strongest bipartisan showing any crypto legislation has ever produced. It cleared the Senate Banking Committee 15-9 on May 14, 2026. On June 1 it was placed on the Senate Legislative Calendar under General Orders as Calendar No. 423, making it eligible for a floor vote at any moment leadership chooses to schedule one. Nobody has scheduled one.

The arithmetic explains part of it. Cloture requires 60 votes. Republicans hold roughly 53 seats, so the bill needs at least seven Democrats. Only two crossed over in committee, Ruben Gallego and Angela Alsobrooks, and both subsequently warned that their committee votes do not guarantee floor support absent further progress. The Republican margin has since narrowed further: Senator Lindsey Graham died on July 11 and Mitch McConnell has been absent, which leaves the conference almost no room for error.

But the arithmetic is downstream of the actual obstacle, which is ethics. Democrats have conditioned their votes on provisions restricting government officials from profiting from the industry they regulate. The reason such a provision exists is that the President’s most recent financial disclosure showed roughly $1.4 billion in crypto-related income, including about $636 million from the memecoin bearing his name and more than $500 million tied to World Liberty Financial. The merged Senate draft combining the Banking and Agriculture texts was released on July 14 and omits any ethics provision. That same day, Senators Chris Murphy, Chris Van Hollen, and Jeff Merkley held a press conference formally opposing the bill.

The rest of the picture is a machine running out of track. Majority Leader John Thune has pledged a floor vote before the August recess, with the week of July 20 under active discussion. The House leaves July 23; the Senate leaves around August 7. A high-level White House meeting was convened on July 15 to hash out the ethics section, with the President himself in attendance. The White House crypto adviser begins military leave on July 27, inside the closing window. A House field hearing convenes at Federal Hall today. Prediction markets have priced 2026 passage in the mid-20s to upper-30s percent range, down from above 70% earlier in the year, and Galaxy’s research head cut his estimate to roughly 50% from 75% in late May. CFTC Chairman Michael Selig has publicly complained that ethics additions are derailing the bipartisan opportunity, calling it mission creep.

The bull case for the anniversary meaning nothing

The optimistic reading is that a year is not long by legislative standards and the anniversary is a media artifact rather than a signal.

Major financial legislation routinely takes multiple Congresses. Dodd-Frank was a crisis response and still consumed most of a year with a supermajority. The fact that CLARITY sits on the calendar eligible for a vote, with committee work finished in both relevant committees, is genuinely further than any market structure bill has ever reached. House Agriculture’s digital assets subcommittee chair has said the House will move fast on whatever the Senate produces, which removes one procedural obstacle entirely: if the Senate delivers a passable text, the House has committed to compressing its own timeline to nothing.

The negotiation is also live rather than dead. A White House meeting with the President attending is not what a corpse looks like. Senators from both parties, including Gillibrand, Lummis, Boozman, and Scott, are described by House Financial Services Chair French Hill as working to get to yes. Kristin Smith of the Solana Policy Institute points to returning lawmakers and fresh bill text as evidence momentum is building. Three working weeks is short but it is not zero, and Congress passes things in the final hours as a matter of institutional habit.

And crucially, the absence of CLARITY has not left a vacuum. The SEC and CFTC joint interpretation of March 17, 2026 classified 16 named digital assets, including Bitcoin, Ether, and XRP, as digital commodities under a five-category taxonomy. That framework is binding on both agencies and is already being cited in fund registration statements. The industry has a working rulebook. The bill would improve it; the bill’s absence has not stopped the market from operating.

The bear case for the anniversary meaning everything

The pessimistic reading is that a year of failure on a bill with 70 Democratic House votes tells you the obstacle is structural, and structural obstacles do not resolve because a calendar page turns.

The compliance cost is the part the vote-counting misses. Businesses cannot build durable compliance programs against jurisdictional lines that remain uncertain, which means the gridlock is not a political story but an operating one, and it has now run for a full year. Firms have responded exactly as they have since 2018, by domiciling offshore, which means the activity continues and American oversight does not.

The taxonomy that makes the bull case is also the bear case. It is administrative action. Any future administration can direct its agencies to reinterpret without a congressional vote. So the industry’s working rulebook is a reversible one, and the entire argument for CLARITY is that a reversible rulebook is not a rulebook. If the bill dies, what protects Bitcoin, Ether, and XRP from a future enforcement posture is one interpretive release from an agency whose position changed once already because its leadership changed.

Then there is the political clock, which does not reset. If CLARITY misses the August recess, it lands in a fall calendar that runs directly into November midterms, when legislative activity slows and the bill’s outlook becomes hostage to a chamber composition nobody can predict. The lame-duck session is the theoretical fallback and it is where well-positioned bills go to be forgotten.

And the ethics impasse has no natural resolution. Democrats argue it is incoherent to build a federal framework for digital assets while the sitting President earns his largest income stream from those assets with no enforceable restriction. The White House position, per Witt, is that it will accept ethics language applying across the board, from the president to the intern, but nothing targeting the President’s holdings specifically. Both positions are internally consistent. Together they are irreconcilable without a concession, and the July 14 draft showed which way the drafting is currently leaning.

The thing a year of delay actually cost

Vote math is the wrong lens for the anniversary, because it measures whether the bill will pass instead of what its absence has already done. A year is long enough for the delay itself to become the story.

Start with the offshore drift, which is not theoretical. Firms domicile where the rules are legible. For a year, American builders have faced a jurisdictional question with no statutory answer, and the rational response has been to incorporate elsewhere, serve American users through structures designed by lawyers, or simply exclude Americans outright. Robinhood’s Stock Tokens are the clean illustration: tokenized equity products available across more than 120 countries and barred to US persons, built by an American brokerage. That is not a company fleeing regulation. It is a company reading the rules that exist and concluding that the safest jurisdiction for its newest product is anywhere else.

Then the compliance cost, which Forbes framed correctly this week: the gridlock has stopped being a political problem and become an operating one. A firm cannot build a durable compliance program against lines that may move. It cannot hire against them, budget against them, or sign multi-year vendor contracts against them. Every quarter of delay is a quarter in which the responsible actors, the ones who would comply if told how, spend money on legal opinions instead of product, while the irresponsible ones proceed exactly as before. Regulatory uncertainty is a tax that falls hardest on the firms most inclined to follow rules.

Then the institutional opportunity cost, which is the largest and least visible. The March taxonomy unlocked a great deal: fund issuers now cite it in registration statements, and accredited investors can structure compliant holdings without waiting for GENIUS implementation in November. But an interpretive release is not what a pension committee wants underneath a multi-decade allocation. Institutions do not ask whether an asset is currently permitted. They ask whether it will still be permitted after the next election, and the honest answer today is that nobody can promise it. That question has a statutory answer or it has no answer, and for a year it has had no answer.

The rebuttal deserves stating: none of that stopped the market. Spot volumes on centralized exchanges rose for the first time in five months in June, climbing 15.3% to $1.11 trillion, and real-world-asset perpetual volumes hit a record $311 billion. Tokenized Treasury products passed $15 billion. The industry is not waiting politely for permission, and the argument that legislation is existential looks weaker every quarter the sector functions without it.

Both readings are true, which is the uncomfortable part. The market does not need CLARITY to operate. The market needs CLARITY to stop rebuilding its legal assumptions every time an administration changes. Those are different needs, and only one of them shows up in a volume chart.

What the scorecard actually shows

Line the three bills up and a pattern emerges that is more useful than any individual vote count.

GENIUS passed because it was narrow and nobody with leverage had a personal reason to block it. The anti-CBDC provision passed because it stopped trying to pass and hitched a ride on something that could, then survived presidential obstruction because it did not need his signature. CLARITY has not passed because it is broad, it touches agency turf, and the one person whose endorsement it carries most loudly is also the reason its opponents will not vote for it.

The uncomfortable implication is that the American legislative system handled crypto’s easy questions and has not handled its hard one. Stablecoin reserves are an easy question. Whether the Fed can issue a digital dollar is a question with a clear partisan valence and an available vehicle. Who regulates the entire digital asset market, and whether the officials writing that answer may personally profit from it, is a hard question, and hard questions require someone to give something up.

A year ago today, the House answered the hard question 294-134 and the industry declared victory. The Senate has spent the twelve months since proving that the House vote was the easy part. Whether the next three weeks change that will come down to a room in the White House and whether anyone in it is willing to trade. If they are not, the anniversary that matters will not be this one. It will be the second one.

Disclaimer: This article is for information and educational purposes only and does not constitute financial, investment, or legal advice. It describes pending legislation and the political debate around it, and legislative outcomes are inherently uncertain. Nothing here is a recommendation to buy or sell any asset. Always do your own research. Information is accurate as of July 17, 2026, and this situation is developing quickly.

Frequently Asked Questions

What happened one year ago today?

On July 17, 2025, the House of Representatives passed the Digital Asset Market Clarity Act by a vote of 294-134, with more than 70 Democrats joining Republicans. It was the strongest congressional endorsement of digital asset legislation in American history and part of what Washington called Crypto Week, during which the House passed three crypto bills in rapid succession.

What was Crypto Week?

A stretch of July 2025 in which the House passed the CLARITY Act 294-134, the GENIUS Act 308-122, and the Anti-CBDC Surveillance State Act 219-217. GENIUS was signed into law on July 18, 2025. The anti-CBDC measure stalled before reaching law inside a housing bill. CLARITY passed to the Senate and has not received a floor vote since.

Did the GENIUS Act become law?

Yes. It passed the Senate 68-30 in June 2025 and the House 308-122 on July 17, 2025, and was signed on July 18, 2025, creating the first federal framework for payment stablecoins. It requires US payment stablecoin issuers to hold full reserves in liquid assets and disclose composition monthly, and it reaches its first major rulemaking deadline on July 18, 2026.

What happened to the anti-CBDC bill?

It cleared the House 219-217, then stalled when a promise to attach it to the defense bill went unkept. A provision barring the Federal Reserve from issuing a central bank digital currency through 2030 later rode inside the 21st Century ROAD to Housing Act. The President has refused to sign that package over an unrelated elections bill, but it becomes law without his signature once the ten-day window closes.

Why has CLARITY not had a Senate vote?

Primarily ethics. Democrats have conditioned support on provisions restricting officials from profiting from the crypto industry, prompted by the President’s disclosure of roughly $1.4 billion in crypto income. The merged Senate draft released July 14 omitted any ethics provision, and Senators Murphy, Van Hollen, and Merkley announced opposition the same day. Disputes over DeFi developer protections and stablecoin yield also remain live.

What are the odds it passes in 2026?

Traders have grown sharply more pessimistic. Prediction markets priced 2026 passage in roughly the mid-20s to upper-30s percent range in mid-July, down from above 70% earlier in the year. Galaxy’s research head cut his estimate to about 50% from 75% in late May. Those figures move quickly and should be checked against current markets.

What is the deadline?

The House leaves for recess on July 23 and the Senate around August 7. Majority Leader John Thune has pledged a floor vote before the recess, with the week of July 20 under discussion. After that, the bill lands in a fall calendar running into November midterms, when the outlook becomes considerably harder to predict.

What governs crypto in the meantime?

The SEC and CFTC joint interpretive release of March 17, 2026, which classified 16 named assets including Bitcoin, Ether, and XRP as digital commodities under a five-category taxonomy. It is binding on both agencies and is cited in fund registration statements. But it is administrative action, not statute, so a future administration could direct a reinterpretation without any congressional vote, which is the central argument for passing the bill.

CASHCAT is a token named after a company name that was thrown away sixteen years ago. It reached a $156 million market cap, briefly outweighed every real asset on Robinhood’s blockchain, and its own website calls it fan fiction with a ticker.

Summary

- CASHCAT is a community memecoin on Robinhood Chain with a fixed supply of one billion tokens. It has no affiliation with Robinhood Markets, and its own site says so.

- The name comes from real history: before Robinhood was Robinhood, Vlad Tenev and Baiju Bhatt called their company CashCat. A New Yorker profile preserved the detail and a token resurrected it.

- It surged more than 2,100% in a week to a market cap near $156 million, at one point worth roughly twelve times every tokenized real-world asset on the chain combined.

- CEO Vlad Tenev dismissed utility-free assets on July 2, then posted six days later that the chain works great for memes too, and followed the token’s account.

- The token fell more than 33% in 24 hours after Noxa, the launchpad driving the boom, stopped accepting launches on July 11 and went dark two days later.

In 2010, two Stanford graduates building a trading company had a name for it. The name was CashCat. They discarded it, called the company Robinhood instead, and the detail survived only in a New Yorker profile and in the memory of people who read startup lore for fun. Sixteen years later, Robinhood launched a blockchain designed to settle tokenized stocks for institutions, and within days the busiest thing on it was a token named after the name they threw away. CASHCAT reached a market capitalization near $156 million, out-massed every real asset the chain was built for, and made a handful of anonymous wallets millionaires. Its website describes it as fan fiction with a ticker. That is not a criticism. It is the project’s own self-assessment, and it is more honest than most.

The basics

CASHCAT is a memecoin native to Robinhood Chain, the Ethereum layer 2 that Robinhood launched on July 1, 2026. For readers new to the network, crypto.news has also explained the chain it launched on.

Its supply is fixed at one billion tokens, with no further issuance. Its contract address is 0x020bfC650A365f8BB26819deAAbF3E21291018b4, and verifying that string against a trusted source before any transaction is the single most useful thing in this article. It does not have its own blockchain or application. It is a fungible token deployed on someone else’s chain, which is what almost every memecoin is.

It has no product, no roadmap in any meaningful sense, and no utility. The project does not pretend otherwise. Asked what the utility is, the site answers that the utility is cat.

Most importantly, and against what a large number of buyers appear to believe: it is not a Robinhood product. It is not owned, endorsed, backed, listed, or affiliated with Robinhood Markets in any way, and the token’s own website disclaims any connection to the company or to Tenev personally.

Where the name comes from

The connection is entirely historical and it is worth getting right, because the ambiguity is the asset.

Before the company became Robinhood, Tenev and co-founder Baiju Bhatt called their venture CashCat. The detail appears in a New Yorker profile of the company and had circulated among people who follow startup history for years. When Robinhood Chain launched, someone recognized that a discarded corporate name attached to a live corporate blockchain was a nearly perfect memecoin: instantly legible to anyone who knew the story, plausible to anyone who did not, and impossible for the company to claim without endorsing it.

That is the entire link. A name the founders rejected in 2010, revived as a token in 2026 by people with no relationship to them. There is no corporate partnership, no licensing arrangement, and no shared ownership. What exists is a shared piece of trivia, and the token converted that trivia into a market capitalization.

There is a small extra layer that fueled it: Tenev himself had tweeted about CashCat back in April 2021, which meant the lore was not merely documented but personally acknowledged by the CEO years before the token existed. None of that constitutes affiliation. All of it makes affiliation feel more plausible than it is.

What happened

The timeline is short and steep.

Robinhood Chain went live on July 1. CASHCAT deployed shortly after. Within roughly 24 hours it had rallied more than 1,700%, and over its first week it climbed more than 2,100%, reaching an all-time high above $0.17 and a market capitalization near $156 million, with some measurements putting the peak higher.

At its peak day on July 8, the token generated roughly $98 million in 24-hour volume, which was about 17% of the entire chain’s decentralized exchange volume. Set that against what the chain was built for: tokenized real-world assets on Robinhood Chain totalled roughly $12.8 million. At its high, one joke token was worth approximately twelve times every real asset on the network combined.

It did not stay alone. Cash Dog in Hood, Little John, Hoodrat, and Arrow followed within days, none of which existed before July 1. Noxa, the launchpad feeding the wave, was averaging roughly 18,600 new token launches per day. On July 8, Pump.fun added Robinhood Chain support, opening the chain to Solana’s memecoin crowd without bridging. For more context, crypto.news has covered the full story of the takeover.

Then it turned. On July 11, at the precise moment CASHCAT was hitting peak trading volume, Noxa stopped accepting new token launches. Two days later it went dark, citing concerns about low-quality tokens flooding the platform, having generated an estimated $12 million in cumulative fees. CASHCAT fell more than 33% in 24 hours. One prominent trader who claims to have ridden the token from a $10,000 market cap to $230 million dismissed the selloff as noise.

The Tenev problem

The CEO’s involvement is the reason this token is confusing rather than merely amusing, and the sequence matters.

On July 2, the day after the chain went live, Tenev told CNBC that the future of crypto is in real-world assets, drawing a line between productive tokenized assets and speculative tokens without underlying utility. His framing was that an asset not tied to an underlying utility is not a productive asset. It was a clean statement of the thesis the entire chain was built to prove, and it was, in effect, a dismissal of exactly the category CASHCAT belongs to.

Six days later, as CASHCAT climbed, he posted on X that while the company is building Robinhood Chain to be the best chain for real-world assets, it works great for memes too. He then followed the token’s account.

Both readings of that reversal are defensible. The charitable one: a permissionless chain cannot control what deploys on it, refusing to acknowledge the most visible thing on your own network would look ridiculous, and a light-hearted post is not an endorsement. Robinhood’s crypto chief stayed rigorously on message throughout, saying the company remains focused on building a secure and scalable foundation for real-world assets.

The uncharitable one: the follow and the post told the market what the company actually values, which is volume, and a retail buyer who sees the CEO engaging with a token named after his own company is going to draw a conclusion the disclaimer will not undo. The distinction between acknowledging and endorsing is clear to a lawyer and invisible to someone who just downloaded a wallet.

Who made money, and from whom

This is the part that gets celebrated and should be read carefully, because every one of these numbers has a counterparty.

One early buyer spent $838 and received 15.04 million tokens. They sold roughly 13.5 million for about $917,600 and held a remainder worth around $133,700, producing a return in the region of 1,250 times. A second wallet turned $85 into 17.4 million tokens and realized about $687,700 while sitting on roughly $1.2 million more on paper. The five most profitable wallets banked close to $3.7 million between them.

Now the other side. That $3.7 million came from the opposite end of roughly 12,300 sell orders. Every dollar of realized profit in a memecoin is a dollar someone else paid at a higher price, because the token produces no revenue and holds no assets. There is no external cash flow funding those returns. The gains are transfers.

The liquidity structure makes it worse than the market cap suggests. CASHCAT’s trading pool has been worth far less than the token’s headline capitalization, which means a $156 million number sits on a pool that cannot absorb anything close to $156 million of selling. Large trades swing price hard in both directions. A market capitalization is a multiplication, not a promise that the money is there.

And the standard verification does not exist. Security audits of the CASHCAT contract were not possible because Robinhood Chain is too new for the tooling to have caught up. That is a chain-wide condition, not a CASHCAT-specific failure, but it removes the check that would ordinarily flag a malicious contract before a nine-figure market cap forms on top of it.

How a memecoin actually prices

Because CASHCAT is the first token most Robinhood users will look at closely, it is worth walking exactly how a number like $156 million comes to exist, since almost nobody who quotes it understands what it measures.

Market capitalization is a multiplication. Take the last traded price, multiply by circulating supply, print the result. CASHCAT has a fixed supply of one billion tokens, so at a price above $0.15 the arithmetic produces something in the region of $156 million. That is the whole calculation. It is not a valuation, not an appraisal, and not a statement that $156 million exists anywhere.

What makes the number misleading is where the price comes from. The last trade might have been for a few hundred dollars. In an automated market maker, price is set by the ratio of assets in a liquidity pool, and the pool behind CASHCAT has been worth far less than the token’s headline capitalization. So a relatively small purchase moves the ratio, moves the price, and instantly revalues all one billion tokens at the new level. That is why memecoins can add nine figures of notional value in a day: a thin pool is a lever, and modest buying at the margin repriced the entire supply.

The lever works identically in reverse, which is what July 13 showed. When Noxa exited and sentiment turned, sellers hit the same shallow pool and the price fell more than 33% in a day. Nothing about the token changed. Supply was still one billion. The contract was unaltered. The only thing that moved was the ratio in the pool, and the market cap followed it down mechanically.

This is why the comparison that ran through every headline, that CASHCAT was worth twelve times every real-world asset on the chain, is both true and slippery. It is true as arithmetic: $156 million against $12.8 million. It is slippery because the two numbers are not the same kind of thing. The tokenized asset figure represents real instruments with real backing that could be redeemed. The memecoin figure represents a price multiplied by a supply, sitting on a pool that could not absorb a fraction of it. One number is a balance. The other is an echo.

The practical implication for anyone holding: your position is worth the market cap right up until you try to sell, at which point it is worth whatever the pool gives you. In a token where five wallets extracted roughly $3.7 million against 12,300 sell orders, the people who found out first were the ones who tried. That is why thin liquidity moves price so hard.

What this token actually shows

Set the price action aside and CASHCAT is the cleanest available case study in how new chains actually bootstrap, which is why it is worth understanding even if you would never touch it.

The optimistic reading, which serious traders make: memecoins are the ignition sequence. A new chain needs transactions, wallets, and liquidity to look alive, and speculation delivers all three faster than tokenized Treasuries do. Solana grew through a memecoin cycle before producing serious infrastructure, and one veteran trader explicitly compared Robinhood Chain’s early ecosystem to Solana’s. The automated market makers, oracles, and routing built to service speculation are the same rails that tokenized equities will eventually need. In that reading CASHCAT is not a distraction from the strategy; it is the first stage of it. That in the category CASHCAT belongs to.

The pessimistic reading, which the timeline supports: memecoin traders are mercenary by construction, loyal to activity rather than to any chain, and the moment a flashier venue offers quicker returns the volume leaves and the $12.8 million of tokenized assets is what remains. The launchpad that produced the entire boom extracted $12 million in fees and exited within eleven days of the chain going live. That is not the profile of a bootstrapping sequence. It is the profile of an extraction cycle, and the 33% drop when the launchpad left is the evidence.

Which reading is right gets settled by a single number, and it is not CASHCAT’s price. It is whether tokenized real-world assets on Robinhood Chain grow well beyond roughly $13 million while the speculation fades. Robinhood’s second-quarter earnings on July 29 are the first real look. Until then, CASHCAT is a token named after a discarded company name, worth more than everything the chain was built to carry, running on an unaudited contract, on a network whose CEO spent one week explaining why assets like it do not last and the next week noting they work great anyway.

What to watch

If you are tracking this token instead of trading it, three things carry information.

Whether the ecosystem keeps spawning. STONKCAT opened a $SCAT presale on July 16, and a MemeToro presale is running alongside it, both borrowing Robinhood Chain’s branding and pitching future products. New entrants arriving weeks after the launchpad that started the wave exited tells you the branding gap is now a repeatable business, which is bearish for CASHCAT specifically: every new token competes for the same attention that is the only thing holding its price up. It also shows how launchpads mint tokens on demand.

Whether the chain’s real assets grow. Tokenized real-world assets on Robinhood Chain sit around $12.8 million against roughly $312 million in total value locked. That figure, not CASHCAT’s price, decides whether the memecoin wave was an ignition sequence or an extraction cycle. Robinhood’s second-quarter earnings on July 29 are the first look at Stock Token adoption from the company’s own books.

Whether liquidity deepens or thins. The pool behind CASHCAT has been worth far less than the token’s headline capitalization, which is the mechanism behind both the rise and the 33% single-day fall. A token whose pool deepens is a token that can absorb selling. A token whose pool thins as attention rotates is a token whose market cap becomes progressively more theoretical. Also relevant: Robinhood Chain’s 90-day gas subsidy has been making trading artificially cheap, and its expiry is a real test.

The broader point for anyone reading this as a lesson instead of a trade: CASHCAT did nothing unusual. It is a well-executed example of an entirely standard pattern, distinguished only by the quality of its joke and the fact that a public company’s CEO engaged with it. The pattern will repeat on the next chain, with a different name, and the mechanics will be identical. What makes this instance worth remembering is the setting. Most memecoins erupt on chains built by anonymous developers for exactly this kind of activity, where nobody claims to be surprised. CASHCAT erupted on a network built by a listed American brokerage, marketed to institutions, staffed with compliance officers, and launched with a keynote about the future of finance. It took six days for the joke to become the chain’s largest asset by market capitalization, and the company could do nothing about it, because permissionless means permissionless. That is the lesson worth carrying: a corporate chain cannot choose its users any more than a public square can. Robinhood built the venue and the crowd decided what it was for.

Frequently asked questions

What is CASHCAT?

A community memecoin on Robinhood Chain, the Ethereum layer 2 Robinhood launched on July 1, 2026. It has a fixed supply of one billion tokens and a contract address of 0x020bfC650A365f8BB26819deAAbF3E21291018b4. It has no product, no utility, and no affiliation with Robinhood. Its own website describes the project as fan fiction with a ticker and says the utility is cat.

Is CASHCAT affiliated with Robinhood?

No. It is not owned, endorsed, backed, or listed by Robinhood Markets, and the token’s own website disclaims any connection to the company or to Vlad Tenev. The name references CashCat, the working name Tenev and co-founder Baiju Bhatt used before the company became Robinhood, a detail preserved in a New Yorker profile. That is trivia, not a relationship.

Why did CASHCAT rise so fast?

A combination of legible lore and a new chain with nothing else on it. The name connected instantly to Robinhood’s founding story, Robinhood Chain had just launched with cheap fees and easy token creation, and attention concentrated on the first breakout token. It rallied more than 1,700% in 24 hours and more than 2,100% over its first week, reaching a market cap near $156 million.

Did Vlad Tenev endorse CASHCAT?

Not formally. On July 2 he told CNBC that assets not tied to an underlying utility are not productive assets. On July 8, as the token climbed, he posted that while the company is building the chain for real-world assets, it works great for memes too, and he followed the token’s account. That is acknowledgement rather than endorsement, but the distinction is clearer to a lawyer than to a retail buyer.

How much was CASHCAT worth compared to the chain’s real assets?

At its peak, roughly twelve times more. Tokenized real-world assets on Robinhood Chain total around $12.8 million, while CASHCAT reached a market capitalization near $156 million. On its biggest day the token generated approximately $98 million in 24-hour volume, about 17% of the entire chain’s decentralized exchange volume.

Why did CASHCAT crash?

Noxa, the launchpad driving the chain’s memecoin wave, stopped accepting new launches on July 11 as CASHCAT hit peak volume, then went dark two days later, citing low-quality tokens flooding the platform. It had generated an estimated $12 million in cumulative fees. CASHCAT fell more than 33% in 24 hours following the exit.

Who made money on CASHCAT?

A small number of early wallets. One turned $838 into roughly $1.05 million across realized and unrealized value, about 1,250 times. Another turned $85 into roughly $687,700 realized plus $1.2 million on paper. The five most profitable wallets took close to $3.7 million between them. That money came from the other side of roughly 12,300 sell orders, since a memecoin produces no revenue and gains are transfers between participants.

What are the risks?

Considerable. The trading pool is worth far less than the headline market capitalization, so large trades swing price sharply and the stated value cannot be exited at that value. Security audits of the contract were not possible because Robinhood Chain is too new for verification tooling. The token has no revenue, no assets, and no utility, so price depends entirely on attention, which has already proven it can leave in a day.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. Memecoins are extremely speculative, frequently trade on thin liquidity, and most participants lose money. Contract addresses and project claims should be verified independently before any transaction. Nothing here is a recommendation to buy any token. Always do your own research. Figures are accurate as of July 17, 2026 and move rapidly.

XRP price is trading around $1.09 as momentum remains soft. The $1.00 level is still acting as key psychological support, although buyers have yet to seize control. For now, the next big move may depend less on charts and more on what happens in Washington.

Ripple has continued engaging U.S. lawmakers as stablecoin legislation moves through Congress. The company has argued that clearer digital asset rules could strengthen blockchain-based payment infrastructure, where XRP has long been positioned as a bridge asset. After years of legal uncertainty, even a little clarity feels like fresh air.

That regulatory push has caught the attention of institutional participants who largely stayed on the sidelines during Ripple’s court battle with the SEC. While sentiment has improved around key hearings, price action has remained stubbornly quiet. Markets have a habit of making everyone wait, then moving all at once.

Meanwhile, XRP’s 24-hour trading volume sits near $1.03 billion, with a market capitalization of around $68.1 billion. That keeps liquidity healthy enough for sharp moves once a real catalyst appears. Until then, traders may need patience, which is usually the hardest position to hold.

Discover: The Best Token Presales

Can XRP Price Double From Current Levels?

XRP is consolidating around the $1.09 to $1.13 price range, with $1.05 acting as immediate support. If that level gives way, the next meaningful floor sits near $0.85. Meanwhile, resistance starts around $1.13, followed by stronger selling pressure near $1.32. Nobody ever said climbing walls was easy.

The bull case, and the one that could send XRP toward the $2 mark, depends on the Clarity Act making meaningful progress through the Senate. That would strengthen XRP’s case as a compliant payment asset instead of a purely speculative token. It is less about chart patterns and more about a shift in market perception.

From a technical standpoint, a sustained move above $1.13 could open the door to $1.32. If buyers keep pressing, the next hurdle sits near $1.46. Exchange reserves also remain worth watching, as a lower available supply can magnify price swings once momentum finally shows up.

For now, the base case remains a sideways market between $1.05 and $1.13 until lawmakers provide clearer direction. However, delays to the Clarity Act or renewed regulatory uncertainty could drag XRP back toward the $0.85 support zone. A weekly close below that level would seriously weaken the current bullish outlook. The setup looks real, but the market still refuses to wear a watch.

Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Bitcoin Hyper Targets Early-Mover Upside as XRP Tests Key Levels

XRP at $1.09 with a potential double on the table sounds compelling, until you account for a $68 billion market cap that needs billions in fresh capital to move meaningfully. Early-stage infrastructure plays operate on entirely different math. This is where Bitcoin Hyper ($HYPER) enters the picture.

Bitcoin Hyper is positioning itself as the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration. It powers a combination that targets the two biggest criticisms of Bitcoin simultaneously: slow throughput and zero programmability.

The chain has sub-Solana latency on a Bitcoin-secured base layer, with a decentralized canonical bridge for native BTC transfers and low-cost smart contract execution built in. The presale has raised close to $33 million at a current token price of $0.0136832, with staking available for early participants.

Early-stage presales carry meaningful risk, liquidity is thin, and post-launch price discovery is unpredictable. But the infrastructure narrative around Bitcoin scalability has been building for two years. If XRP’s regulatory catalyst takes longer than expected to materialize, capital looking for asymmetric exposure has to go somewhere.

Discover: The Best Crypto to Diversify Your Portfolio

The post XRP Price Could Double as Ripple Pushes Senate for Clarity Act appeared first on Cryptonews.

Pi Network’s coin, PI, rose by more than 3.5% over the past 24 hours, outpacing a broader crypto market that lost nearly 3%.

The rise came as Pi Network began a design refresh of its mining app. The gain offered brief relief for a token that hit a record low days earlier. PI traded near $0.078, though it remains down more than 22% over the past week.

Pi Network Price Bounces Off a Record Low

PI touched an all-time low near $0.071 on July 14. The token has since recovered roughly 11% from that level.

Even after the bounce, PI trades about 97% below its February 2025 peak near $2.99. Its 30-day loss stands at roughly 42%.

Rising supply has weighed on the altcoin already stuck in a downtrend. About 10.9 billion PI circulate against a maximum of 100 billion, leaving room for further dilution.

According to PiScan data, roughly 4.25 million PI unlock each day, worth about $333,672 at current prices. That steady daily release adds fresh sell-side pressure with each session.

Follow us on X to get the latest news as it happens

Pi Network Begins a Mining App Refresh

Pi Network redesigned the side menu and the app profile page in its mining app, marking the first step in a broader design refresh. The team said that the redesign lets Pioneers reach key account details and ecosystem tools faster.

The redesign lands ahead of Protocol v25, scheduled for July 22. The upgrade aims to improve network stability and add privacy-preserving smart contracts.

Whether the update push can offset supply-driven selling remains the key test. The July 22 upgrade will show if utility gains start to translate into demand.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Pi Coin Defies a Falling Crypto Market as Pi Network Overhauls Its App appeared first on BeInCrypto.

Bitcoin price is hovering around the mid $63,000 range after one of the year’s sharpest leverage flushes in a bearish prediction environment. BlackRock CEO Larry Fink blamed Bitcoin’s recent volatility on excessive derivatives leverage, and not on weakening fundamentals. The liquidation data support his view, with billions wiped out during the selloff. Most of those losses came from overleveraged longs, not panic selling.

Now that the dust has settled, Bitcoin is trying to hold the $62,000 to $65,000 range. That puts the spotlight on upcoming options expiry and fresh signals from the Federal Reserve. Price action alone may not tell the whole story this time.

Instead, institutional demand is becoming the market’s favorite scoreboard. ETF flows and large investor positioning could decide whether Bitcoin regains momentum or stalls below resistance. For now, traders seem happy buying dips, but nobody is rushing to crank the leverage back up.

Discover: The Best Token Presales

Bitcoin Price Prediction: Reclaim $70,000 After Another Leverage Flush?

Bitcoin is trading around $62,850 after slipping from this week’s highs near $65,000. During the past 24 hours, BTC traded between $62,700 and $64,000, while daily trading volume hovered near $27 billion. Activity remains elevated compared with quieter sessions, showing traders are still working through the recent liquidation wave.

Technically, the next test is whether Bitcoin can defend the low $62,000 area, which has attracted buyers repeatedly this month. The rebound from those levels showed real demand, yet bulls still need to reclaim the $64,500 to $65,000 zone. Until that happens, every rally risks feeling like a dress rehearsal instead of opening night.

Three scenarios remain in play. In the bullish case, leverage continues cooling, institutional demand absorbs supply, ETF inflows stay healthy, and Bitcoin pushes above $65,000 before challenging $70,000. That would finally give buyers something to smile about besides green candles lasting five minutes.

The base case is less dramatic. Bitcoin could keep chopping between $62,000 and $65,000 while traders wait for the next macro catalyst, whether that comes from the Federal Reserve or ETF flows. It is not exciting, but markets rarely hand out fireworks every day.

The bearish case still deserves respect. Another derivatives-driven flush after disappointing macro data could drag Bitcoin below $62,000 and put the recent recovery under pressure. Larry Fink may remain bullish, but leverage has not disappeared overnight. For now, holding above support matters far more than anyone’s crystal ball.

Trade Bitcoin and Don’t Miss Out on Our $1,000 USDT Airdrop on ByBit

Bitcoin Hyper Targets Early-Mover Upside as Bitcoin Tests Key Levels

Spot BTC at $64k carries a $1.29 trillion market cap. The upside math from here, while real, is measured in percentages for most holders. Early-stage infrastructure bets on the Bitcoin ecosystem operate on entirely different return profiles, which is where projects like Bitcoin Hyper enter the conversation.

Bitcoin Hyper ($HYPER) is positioning as the first Bitcoin Layer 2 with Solana Virtual Machine (SVM) integration, a combination that targets the three core limitations Bitcoin itself has never resolved: slow throughput, high fees, and no native programmability.

These Backrooms hit a little different. — Bitcoin Hyper (@BTC_Hyper2) July 17, 2026

https://t.co/VNG0P4GuDo pic.twitter.com/mU0O0EpPV1

https://t.co/VNG0P4GuDo pic.twitter.com/mU0O0EpPV1

The presale is priced at $0.0136832 and has raised $32.9 million to date, with a staking mechanism offering high APY for early participants. The SVM integration is the technical differentiator; lower latency than Solana itself on a Bitcoin security layer is an aggressive benchmark.

For traders watching BTC consolidate at current levels and looking for asymmetric exposure to Bitcoin ecosystem growth, research Bitcoin Hyper’s presale terms here before the next stage pricing moves.

Discover: The Best Crypto to Diversify Your Portfolio

The post Bitcoin Price Prediction: Larry Fink Turns Bullish on BTC, Blames Leverage Trading appeared first on Cryptonews.

Bitcoin Japan has secured plans to raise approximately 9.66 billion yen (approx $59.5 million), with 662 million yen (approx $4.08 million) earmarked for its first Bitcoin treasury allocation since adopting its new corporate identity.

Summary

- Bitcoin Japan has planned a 9.66 billion yen fundraising, with 662 million yen allocated for its first Bitcoin purchases.

- Most of the proceeds will go toward private equity, rare earth mining, and Robot as a Service investments, while Bitcoin receives about 7% of the total.

- The funding follows an earlier capital raise that failed to finance its Bitcoin treasury strategy after falling short of its fundraising target.

Japanese crypto news outlet CoinPost reported that Tokyo Stock Exchange-listed Bitcoin Japan, formerly Horita Marusho, will issue 1.5 billion yen in unsecured convertible bonds with stock acquisition rights alongside a second series of stock acquisition rights through Cayman Islands-based investment fund EVO FUND.

If the securities are fully exercised, the company expects net proceeds of about 9.657 billion yen.

Bitcoin receives 7% of planned fundraising

Company filings cited by CoinPost show that Bitcoin purchases will receive 662 million yen, or about 7% of the planned financing. The largest share, 3.756 billion yen, has been set aside for undisclosed private equity investments, followed by 3.503 billion yen for rare earth mining projects in South Africa and 1.446 billion yen for investments in a Robot-as-a-Service (RaaS) business. Another 290 million yen has been allocated for working capital.

Convertible bonds allow investors to exchange debt for company shares at a predetermined price. CoinPost noted that the structure can reduce immediate pressure on the share price by spreading conversions over time, although the company remains responsible for repayment if the bonds are not converted.

Bitcoin Japan changed its name from Horita Marusho in 2024 and announced plans to transition from a textile trading business into a digital asset treasury company centered on Bitcoin and AI infrastructure. Even so, the company has yet to acquire any Bitcoin.

The latest allocation follows an earlier fundraising effort that fell short of expectations. Company disclosures previously showed that Bitcoin Japan planned to raise as much as 5.715 billion yen in December 2025, including 988 million yen for a Bitcoin treasury strategy. Weak share price performance limited investor participation, reducing the total amount raised to 3.095 billion yen and leaving no funds available for Bitcoin purchases.

Current filings state that the newly allocated Bitcoin funds will be deployed selectively depending on market conditions. The company has not disclosed a purchase timeline, targeted Bitcoin holdings, or performance metrics, although it continues to describe Bitcoin as a long-term hedge against the erosion of fiat currency value.

Financing comes after technology investment push

The fundraising follows Bitcoin Japan’s recent expansion into technology investments beyond digital assets.

In May, the company disclosed an investment in SpaceX through its wholly owned U.S. subsidiary, BTCJPN US LLC, using a U.S.-based private secondary market transaction. At the time, Bitcoin Japan said it was targeting sectors including AI compute infrastructure, satellite communications, digital assets, and next-generation technologies as part of its long-term investment strategy.

The latest financing could also substantially increase the company’s share count. According to documents cited by CoinPost, full conversion of the convertible bonds and exercise of all stock acquisition rights at the minimum price would result in dilution of up to 110%, or 115% on a voting rights basis.

Because the transaction qualifies as a large third-party allotment under Japanese rules, the company obtained an opinion from an independent committee consisting of outside legal experts, which concluded that the financing was necessary and reasonable.

Financial results released by the company showed consolidated revenue of 2.959 billion yen and an operating loss of 462 million yen for the fiscal year ending March 2026, extending its streak of operating losses to eight consecutive years. Against that backdrop, the planned Bitcoin allocation represents the company’s first funded step toward executing the treasury strategy it announced after its rebranding.

Crypto World

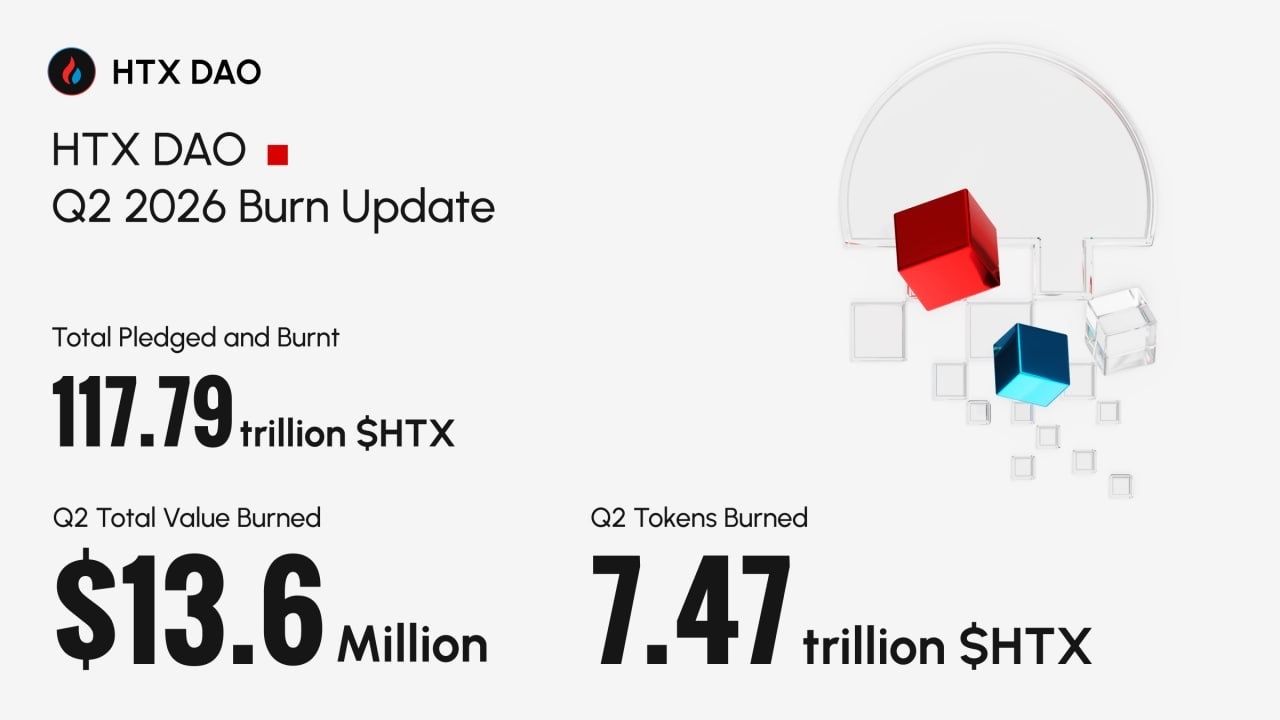

HTX DAO Burns Over $32.82 Million Worth of $HTX in H1 2026, Highlighting Strong Business Resilience

HTX DAO announced the successful completion of its $HTX token burn for Q2 2026 on July 15, 2026. On-chain data shows that a total of 7,474,935,439,560 $HTX tokens were burned in this round, valued at over $13.6 million. Following this latest burn, the cumulative volume of $HTX burned and pledged has reached 117.79 trillion tokens (backed by verifiable on-chain burn proofs.)

Combined with Q1 data, HTX DAO burned a total of over $32.82 million worth of $HTX in the first half of 2026. At a time when broader market liquidity remains under sustained pressure, this deflationary track record stands out as a highly compelling achievement.

Retaining Strong “Value Generation” Capabilities in a Downturn

Looking back at the first half of the year, the crypto market experienced highly complex sentiment shifts and tight liquidity conditions—with BTC temporarily slipping below the $60,000 threshold. These headwinds were largely driven by macro factors, including diminished expectations for Fed rate cuts and consecutive net outflows from Spot ETFs.Concurrently, spot and derivatives trading volumes across the industry fell sharply, and the aggregate stablecoin supply contracted on a quarterly basis for the first time since Q3 2023.