Crypto World

Echo Protocol Hack Autopsy: The $76 Million Exploit That Wasn’t Really a Hack

2026 DeFi losses crossed $1 billion in four months, with April alone draining $634 million across 28+ incidents, the worst month on record.

Drift ($285M) and KelpDAO ($292M) alone accounted for $577 million of April’s losses, and neither was a code exploit.

DefiLlama’s 2026 hack breakdown tells the same thing.

The biggest slices are LayerZero bridge exploits (18%), compromised admin keys (16%), spoof tokens (14%), and private key compromises (11%).

Combined, operational and key-management failures account for the majority of all stolen value this year. Smart contract bugs like re-entrancy and oracle manipulation barely register.

Echo Protocol just became the latest data point.

On May 18, an attacker broke into the Echo Protocol on Monad and printed 1,000 fake eBTC for themselves. That’s $76.7M on paper.

The problem is, fake tokens don’t buy you anything unless you can trade them for something real. So they took a small chunk, dropped it into Curvance’s lending app as collateral, and borrowed real Bitcoin against it.

Then bridged that Bitcoin to Ethereum, swapped it for ETH, and ran it through Tornado Cash. Final take: around $816,000.

Everyone’s calling it $76.7 million but the real number is $816,000, and why those two numbers are so far apart is the main story here.

This breakdown covers what happened, how, and what it says about DeFi security right now.

The bottom line: The contract was fine. A stolen admin key and lazy controls did everything else, and that’s how most of 2026’s DeFi losses are happening.

Post Mortem (The Summary)

- Echo Protocol was not hacked through bad smart contract code. The attacker stole or accessed an admin key.

- That admin key controlled minting rights for Echo’s eBTC token on Monad. One private key was enough to create fake Bitcoin-backed tokens.

- The attacker minted 1,000 fake eBTC, worth about $76.7 million on paper. But those tokens had no real BTC backing.

- They could not cash out the full amount because Monad liquidity was thin. So they used 45 fake eBTC as collateral on Curvance.

- Curvance accepted the fake eBTC as normal collateral and let the attacker borrow real WBTC.

- The attacker escaped with about $816,000 in real value, not $76.7 million.

- Echo later burned the remaining 955 fake eBTC and paused affected functions.

- Monad itself was not hacked. Curvance’s main protocol was not directly hacked either. The failure came from Echo’s admin setup and Curvance trusting newly minted collateral.

- The core lesson: DeFi attackers are now targeting keys, admins, bridges, infrastructure, and team operations more than smart contract bugs.

- Basic protections could have reduced or stopped this: multisig admin control, timelocks, mint caps, rate limits, and collateral checks.

- Echo got lucky. The attacker only failed to drain more because there was not enough liquidity to cash out the fake tokens.

The Players

Here’s the full breakdown of what happened, and how.

- Echo Protocol

A BTCFi (Bitcoin DeFi) project. Their pitch: take your BTC, get a yield-bearing wrapped version of it that works in DeFi.

Their home base is Aptos, where the token is called aBTC. They hit a peak TVL of $878 million on Aptos in May 2025, currently sitting around $254 million.

Echo expanded to Monad as part of Monad’s mainnet ecosystem push. On Monad, their wrapped BTC token is called eBTC.

This is critical: aBTC and eBTC are completely separate, non-bridgeable assets. They’re parallel deployments, not connected. The hack hit eBTC on Monad only.

- Monad

A new high-performance parallelized EVM L1. One of the hyped chains of 2025-26. Just out of the mainnet, with lots of protocols deploying fresh.

Echo is one of them. Monad itself was NOT compromised in any way. Co-founder @keoneHD confirmed the network ran normally throughout. It was a protocol-level failure on top of Monad.

- Curvance

A lending protocol deployed on Monad. Functions like Aave but with isolated markets, where each collateral asset lives in its own siloed pool so a compromised asset can’t infect the rest of the lending protocol.

They had listed eBTC as a collateral asset.

- Tornado Cash

Sanctioned ETH mixer. You send ETH in, you get ETH out from a different wallet, and break the on-chain trail. Standard exit tool for hackers.

What Got Exploited

Echo’s eBTC token on Monad is a standard ERC-20 contract that uses OpenZeppelin’s role-based access control system. This is industry standard, used by basically every serious DeFi project.

Two roles matter in its setup:

- DEFAULT_ADMIN_ROLE: the master role. Can grant or revoke any other role on the contract.

- MINTER_ROLE: can call mint() and create new eBTC tokens.

Normally, only Echo’s team holds these. Minting only happens when real BTC gets locked somewhere, and the team mints the matching eBTC. That’s the entire trust model behind a wrapped token.

Here’s where Echo messed up.

The DEFAULT_ADMIN_ROLE sat on a single EOA, basically just a normal wallet with one private key behind it. And the wallet had no safety nets. Whoever held that key could mint as much as they wanted, whenever they wanted, with nothing to slow them down.

So the entire $254M+ Echo ecosystem on Monad was, in security terms, sitting behind one private key. That key got stolen. Nobody’s said how yet. Could be phishing, malware on a team laptop, an infra breach, an insider, secrets leaked in a repo, supply chain attack through a dev tool. Echo hasn’t disclosed.

The Attack Step by Step

Date: May 18, 2026, around 5:55 PM ET

- Step 1: Attackers use the stolen admin key to grant themselves DEFAULT_ADMIN_ROLE on a fresh wallet. They’re now admin too.

- Step 2: From that new admin role, they grant themselves MINTER_ROLE. They can now mint.

- Step 3: They call mint(attacker_wallet, 1000e8). 1,000 eBTC shows up in their wallet. Notional value $76.7M. Real BTC backing: zero. These tokens are completely fake, phantom claims on Bitcoin that don’t exist anywhere.

- Step 4: They revoke the original Echo admin and their own admin role too. Cleanup move so it looks less suspicious on-chain. From the outside, it just looks like a random wallet holding 1,000 eBTC.

At this point, the peg is mathematically broken. There are 1,000 more eBTC tokens than there is BTC backing them.

But the attacker hasn’t actually taken anything yet. Fake tokens are worthless unless you can convert them into real money.

The Cashout Flow

You can’t just dump 1,000 fake eBTC on a DEX. Monad’s DEXs don’t have anywhere close to that liquidity. You’d crash the price to zero before extracting anything, and arbitrageurs would catch it instantly. So the attacker went to a lending market instead.

- Step 5. Deposit 45 eBTC ($3.45M paper value) into Curvance as collateral. Curvance accepts it because, from the contract’s view, eBTC is eBTC. No oracle or check that separates “freshly minted fake eBTC” from “legit BTC-backed eBTC.” That’s the second failure of this hack. Lending markets just accept new collateral at face value without checking where it came from.

- Step 6. Borrow 11.29 WBTC against it, about $868K of real wrapped Bitcoin. WBTC is the major BTC-on-Ethereum token, deep liquidity, fully backed. They now have $868K of real value, secured by $3.45M of fake collateral they’re never coming back for.

- Step 7. Bridge the WBTC to Ethereum. That’s where liquidity lives and where Tornado works.

- Step 8. Swap WBTC to ~384 ETH on Ethereum (~$822K).

- Step 9. Run the 384 ETH through Tornado Cash. Trail breaks. Funds land in fresh wallets that can’t be traced back.

Total real money out: approximately $816,000.

How Echo Responded

Within hours of the hack going public, Echo reclaimed the admin key, burned the 955 eBTC still sitting in the attacker’s wallet (which no longer exists), and paused all cross-chain functionality on Monad.

They also paused the Aptos bridge and Aptos lending even though Aptos was clean, just to be safe. Pushed a contract upgrade on Monad to restrict the affected operations and said they’d patch their other EVM bridge deployments too.

Curvance paused the eBTC market, confirmed that their own contracts were fine, and noted that their isolated market design prevented the damage from spreading to other lending pools.

Keone from Monad clarified the chain was untouched and pegged the actual loss at around $816K.

The Breakdown

The gap between $76.7 million and $816,000 is the whole story. Curvance was the only viable exit, and its depth capped the borrow at approximately $868,000.

eBTC minted

1,000 (notional $76.7M)

Deposited to Curvance

45 eBTC

WBTC borrowed

11.29 (~$868K)

Sent through Tornado

~384 ETH (~$822K)

Actually stolen

~$816K

eBTC burned by Echo

955

Aptos exposure

~$71K

ECHO drawdown

~11-12%

The other 955 eBTC had nowhere to go until Echo burned it. Monad’s thin liquidity saved Echo from a much bigger loss. On Ethereum, this would’ve been close to $76M out the door.

Why this was an operational hack, not a smart contract hack

The code wasn’t the issue. It worked the way it was supposed to. The real problem was how Echo set things up around the contract:

- The admin role was held by a single wallet instead of a multisig. Stealing a single private key was enough to take over the entire protocol.

- There was no time lock. When the attacker granted themselves admin and then minter rights, those changes went live immediately. No delay, no window for the team to notice and respond.

- The contract had no maximum supply. Minting 1,000 eBTC with zero BTC backing was technically allowed by the rules of the contract itself.

- No rate limit either. The attacker minted the entire 1,000 in a single transaction, rather than being forced to spread it out.

- Curvance accepted the freshly minted eBTC as collateral without checking whether it was legitimately backed. The lending market just saw eBTC tokens in a wallet and treated them the same as real ones.

None of these are obscure or experimental fixes. Multisigs, timelocks, mint caps, and supply checks are stuff serious DeFi protocols have been shipping for years. Echo just didn’t bother with any of them.

May 2026 looks like this

Echo is the 14th hack this month. The year so far:

| Protocol | Loss | Vector |

| KelpDAO (Apr) | $292M | RPC poisoning + DDoS (Lazarus) |

| Drift | $285M | Social engineering (Lazarus, UNC4736) |

| THORChain (May 15) | $10M+ | Vault breach |

| Verus bridge (May 17) | $11.6M | Cross-chain verification |

| Echo (May 18) | $816K | Admin key |

| Transit Finance | $1.88M | Deprecated contract |

Approximately $328.6 million lost to bridge hacks in 2026 across 8 incidents. None of these were Solidity bugs. Keys, signers, RPC endpoints, off-chain verifiers, that’s where the money is leaving now. The attackers moved up the stack. A few from this year worth paying attention to:

- Drift (April): Not a technical exploit. UNC4736 (North Korea) spent six months social engineering Drift employees, then drained $285M in 12 minutes. Six months of prep, 12 minutes of execution. That’s a military op, not a hack.

- KelpDAO (17 days later): Same group, completely different vector. They poisoned LayerZero’s RPC infrastructure and forged cross-chain messages for $292M. State-sponsored teams running multiple playbooks in parallel.

- AI is showing up too: Google confirmed the first AI-powered mass exploit on May 11 (AI found a zero-day and wrote bypass code for 2FA). GoPlus reported a 231% MoM jump in Web3 losses partly tied to AI. CrowdStrike puts the average eCrime breakout time at 29 minutes, with the fastest at 27 seconds. The attack side is automating, defense mostly isn’t.

- Resolv Labs (March): Admin key compromise on a stablecoin issuer. Attacker minted 80M unbacked USR, drained $25M, and USR depegged by 80%. Same root cause as Echo, completely different protocol type. The pattern doesn’t care what you’re building.

Ondo Finance put it bluntly in their post-incident analysis: “there is no single class of vulnerability to defend against.” That’s the part most protocols still haven’t internalized.

So when Echo got drained through a stolen admin key, it didn’t happen in a vacuum. It happened during the most hostile threat environment DeFi has ever seen, and the protocol was set up as if it were still 2022.

So what?

DeFi spent the last five years getting good at smart contract security. Audits, bug bounties, formal verification, all of it.

So the attackers stopped targeting the code and started targeting everything else. Keys, infrastructure, employees, signers. None of that gets audited.

For any wrapped BTC protocol, the only security question that actually matters is who can mint, and how hard is it for someone to take that power from them.

If the answer is “a multisig with a timelock, a mint cap, and a lending market that checks where new collateral came from,” you have a real protocol. If the answer is “one wallet with one key,” you have $254M sitting there waiting to be taken. Echo was the second kind.

The damage doesn’t stay in one place either. Aave wasn’t hacked in April, but it lost $5.4B in TVL within 48 hours of the KelpDAO exploit anyway. People just panicked and pulled their money out of everything. That’s what happens now. One protocol gets hit and the whole sector gets repriced.

The fixes are not new. They’ve been around for years. Multisig the admin, timelock the changes, cap the supply, check the collateral. It’s just that none of it makes a protocol more competitive on the front end, so nobody ships it until they’re the next headline.

Echo got off easy because Monad’s liquidity was too thin for the attacker to fully cash out. The next protocol probably won’t have that excuse.

The post Echo Protocol Hack Autopsy: The $76 Million Exploit That Wasn’t Really a Hack appeared first on BeInCrypto.

Binance’s renewed accessibility in the Philippines through a local arrangement with BlockShoals Technologies is being framed as a matter of regulatory jurisdiction rather than licensing clearance by the country’s central bank, according to a legal adviser speaking at Philippine Blockchain Week 2026. The position hinges on a key distinction: the parties describe the structure as limiting activities to regulated crypto trading access under the Securities and Exchange Commission (SEC), while excluding peso transfers and other functions that would fall under Bangko Sentral ng Pilipinas (BSP) oversight.

In separate feedback to Cointelegraph, the BSP stated that neither Binance nor BlockShoals is authorized to operate as a virtual asset service provider (VASP). The exchange’s approach also references participation in the SEC’s Strategic Sandbox (StratBox), which regulators say does not remove firms from applicable licensing obligations or cross-agency compliance requirements.

Key takeaways

- The SEC framework is presented as covering Binance’s crypto trading access in the Philippines, while BSP oversight is linked to peso transfer and other central-bank–regulated activities.

- The BSP said it has not authorized either Binance or BlockShoals to operate as a VASP, and noted ongoing coordination with the SEC.

- Participation in the SEC’s Strategic Sandbox does not eliminate requirements to comply with laws and any licensing conditions imposed by relevant regulators.

- Binance’s renewed accessibility follows earlier SEC actions in 2023–2024 related to registration and licensing concerns, including requests to block website access.

Jurisdictional split: SEC trading access vs. BSP-regulated payments

Marie Antonette Quiogue, head of legal at BlockShoals, argued that Binance’s local offering can operate without a VASP license from the BSP, provided the arrangement does not include activities the BSP regulates. In her account, trading access falls under SEC jurisdiction, whereas peso movement—described as “clearly under the jurisdiction of the BSP”—is not part of the proposed workflow.

Quiogue said BlockShoals acts as a crypto asset intermediary that connects Philippine users to Binance’s global trading platform. She acknowledged that neither Binance nor BlockShoals has applied for a local VASP license. The legal adviser did not dispute the BSP’s characterization that the entities lack VASP authorization, but maintained that the absence of such a license does not, by itself, preclude services that are governed by the SEC.

She also emphasized that if the companies introduce products or activities that fall under a different regulator’s remit, they must obtain the relevant authority. This point is operationally significant for compliance teams: it implies that the scope of the product offering—particularly any integration that could be interpreted as facilitating payment flows—could determine whether additional permissions are required.

BSP warning: sandbox participation is not a substitute for licensing

The BSP’s position, as relayed to Cointelegraph, was direct: neither Binance nor BlockShoals is authorized to operate as a VASP. The BSP further stated that entry into a regulatory sandbox does not exempt an entity from meeting applicable legal and regulatory requirements, including licensing obligations assigned to the relevant authorities.

The regulator said it was coordinating with the SEC regarding the matter. For institutional observers, this matters because sandbox participation is often used to allow experimentation while compliance frameworks are being developed; however, regulators in many jurisdictions clarify that sandbox status does not create a legal safe harbor for conduct outside the sandbox’s defined scope or outside the permissions granted by other agencies.

Unresolved questions typically arise around boundaries—particularly where technology, payments, and customer onboarding processes can be interpreted as payment facilitation, asset custody, or other regulated services. In this case, the dispute is not framed as customer trading activity alone, but rather whether the operational model introduces regulated peso transfer or other BSP-governed functions.

SEC StratBox structure and how it is being used

Quiogue said the arrangement is presented as part of the SEC’s Strategic Sandbox, or StratBox. The structure is described as: BlockShoals, operating under the SEC’s crypto asset intermediary framework, introduces users to Binance’s platform, while the parties avoid “moving pesos.”

From a policy perspective, the framing highlights a common regulatory architecture in crypto: trading and certain market-facing activities are sometimes handled by securities or investment regulators, while payment-related issues and fiat conversion are addressed by central banks or financial authorities. The practical compliance impact is that firms must map product flows to regulator-specific concepts (for example, what constitutes a payment service, a VASP activity, or another regulated financial function).

Quiogue also stated that authorization must be sought from the “relevant regulator” when services fall outside the SEC’s remit. This statement signals that the parties’ legal risk is likely to increase if new services are rolled out that involve elements potentially characterized as regulated by other Philippine agencies.

Background: earlier SEC actions and attempts to restrict access

Binance’s situation in the Philippines has been under scrutiny for some time. According to records cited by Cointelegraph, the SEC issued warnings in November 2023 that Binance was not authorized to sell or offer securities in the country because it had not obtained necessary licenses and registrations. The SEC’s notice also tied its concerns to Binance’s corporate and offering status within the jurisdiction.

In March 2024, the SEC said it asked the National Telecommunications Commission to block access to Binance’s website and related webpages, and internet providers subsequently restricted access following the order. At the time referenced by Cointelegraph’s reporting, Binance’s platform was again accessible to users in the Philippines.

This sequence underscores a compliance and enforcement dynamic frequently seen in cross-border crypto operations: regulators may challenge the legal basis for offering services to residents, then require structural changes or legal clarifications to resume access. The present dispute appears to revolve around whether the reconfigured arrangement sufficiently addresses licensing gaps or jurisdictional conflicts, particularly in relation to BSP-controlled payment functions.

What to watch next

Key developments to monitor include whether the SEC and BSP reach a formal alignment on the scope of permitted activities under the current StratBox-linked arrangement, and whether the parties’ operational model changes in ways that could bring peso transfer or other payment-regulated functions into the transaction flow. For compliance teams, the central question remains practical: how each element of onboarding, payments, and customer interaction is interpreted under Philippine licensing and cross-agency oversight frameworks.

- Shiba Inu (SHIB) trades near $0.00000476 with weak short-term momentum.

- Shiba Inu burn activity has dropped to about $5 worth of SHIB daily.

- SHIB’s price remains below all major EMAs, maintaining a bearish trend.

Shiba Inu is trading at $0.00000476, holding a tight range between $0.000004638 and $0.000004789 over the past 24 hours.

The memecoin has remained under pressure in recent sessions, with a -0.4% daily change, extending a broader weakness that has seen it fall 17% over the past 30 days and nearly 59% over the past year.

Market activity, however, remains elevated, with 24-hour trading volume at roughly $54.7 million.

SHIB price structure tightens as support zone comes under pressure

Shiba Inu is testing a support region around $0.0000046, while a deeper support level sits at $0.00000430.

On the upside, resistance is forming near $0.0000048, with a further barrier at $0.00000491.

Notably, SHIB is trading below all major daily exponential moving averages (EMAs), including the 10-day, 20-day, 50-day, 100-day, and 200-day EMAs.

This alignment places the broader trend firmly in bearish territory, with no short-term average currently supporting price from below.

In addition, out of 23 tracked technical indicators, 13 are bearish, 9 neutral, and only 1 bullish, giving bears roughly 57% control of the signal distribution.

The RSI (14) sits around 35.47 on the daily chart, while the weekly reading is near 35.68, both pointing to nearly oversold conditions.

While this does not confirm a reversal, it does suggest the market is approaching levels where short-term reactions have historically occurred.

A close below $0.00000455 would expose SHIB to lower support levels, while a recovery above $0.0000048 would be required to shift short-term momentum toward $0.00000507.

Burn activity and Shibarium engagement decline

Shiba Inu token burn activity has weakened significantly.

Data from the Shibburn website shows that daily burns have fallen to extremely low levels, with estimates indicating only around 1 million SHIB burned per day, valued at roughly $5.

Weekly burn totals remain similarly small, around 15 million SHIB, worth approximately $75.

At current levels, the burn activity has minimal effect on SHIB’s total supply dynamics.

The scale of the supply reduction is too small to influence price behaviour in the short or medium term, especially during periods of weak demand.

Shibarium activity has also shown limited market impact recently.

While the Layer-2 network continues to process transactions, there has been no measurable effect on SHIB price stability or upside momentum in recent trading sessions.

The lack of strong network-driven demand has left price action largely dependent on broader market sentiment and technical levels.

Exchange flows show accumulation, but price response remains weak

Exchange flow data presents a mixed picture.

CryptoQuant has stated that total SHIB exchange reserves have dropped below 80 trillion tokens.

Net outflows of approximately 266 billion SHIB in 24 hours have been recorded, suggesting that holders are moving tokens off exchanges, a behaviour often associated with accumulation or longer-term holding.

Despite this, the Shiba Inu price has not reacted strongly to the shift in flows.

SHIB continues to trade near the lower end of its recent range, indicating that buying pressure has not yet outweighed broader selling activity.

This divergence between on-chain accumulation and price response highlights a market that is still waiting for stronger confirmation from demand-side activity.

Prediction market platform Kalshi is reportedly in early, informal discussions with investment banks about pursuing an initial public offering (IPO), according to sources cited by The Information. The report comes as regulators in the United States intensify scrutiny of sports-related contract trading on prediction market platforms.

Separately, Kalshi’s business momentum appears to be tied closely to sports betting contracts. Dune data indicates sports-related markets make up the majority of Kalshi’s weekly notional trading volume, even as legal challenges by US states continue to expand.

Key takeaways

- Kalshi is reportedly in early talks with investment banks about an IPO, after surpassing $2 billion in annualized revenue.

- Sports betting contracts drive most of Kalshi’s weekly notional trading volume, raising regulatory exposure as lawsuits grow.

- Dune data shows sports-related betting accounts for about 53% of Kalshi’s weekly notional volume; Polymarket’s sports share is about 69%.

- US states continue to sue prediction market operators, with the CFTC also weighing in through regulatory actions and court efforts.

- Regulators argue event-based sports contracts require state-level licensing, while prediction markets contend they fall under federal commodities “swap” rules.

IPO discussions emerge alongside revenue growth

Kalshi’s reported IPO path is being discussed informally, with unidentified sources telling The Information that the platform is in early-stage conversations with investment banks. The catalyst, per the report, is that Kalshi has surpassed $2 billion in annualized revenue.

Kalshi did not comment on the IPO speculation, according to a spokesperson cited by the report.

For investors and market participants, the timing matters: prediction market platforms are operating in a regulatory gray area where legality often hinges on how specific contracts are categorized. Any move toward a public listing typically increases pressure for clearer regulatory treatment, stronger compliance frameworks, and more predictable oversight—especially in the face of active litigation.

Sports contracts remain the engine of trading volume

While Kalshi has positioned itself within the broader prediction market category, sports-linked contracts dominate its trading activity. According to Dune data, sports betting represents about 53% of Kalshi’s weekly notional trading volume.

Kalshi’s sports concentration mirrors trends at rival platform Polymarket. Cointelegraph previously noted that sport-related betting accounts for about 69% of Polymarket’s weekly trading volume, according to data cited from Dune and related market analysis.

This matters because sports markets have become a focal point for legal disputes. The more a platform’s volume depends on sports event contracting, the more its growth strategy can be affected by court rulings, licensing requirements, or regulatory interpretations that vary across states.

Growing state lawsuits and the federal-vs-state regulatory fight

The IPO chatter arrives amid escalating legal conflict in the US. Cointelegraph reported earlier that Kentucky became the latest state to sue multiple prediction market operators, including Kalshi and Polymarket, alleging they are “operating unlicensed and illegal sports betting and gambling platforms.”

As coverage from Cointelegraph noted, at least 17 other states have also taken prediction market operators to court, prompting involvement from the US Commodity Futures Trading Commission (CFTC).

The core dispute centers on classification. State authorities argue that sports event contracts need licenses under existing state gambling frameworks. Prediction market operators counter that their event contracts should be treated as swaps regulated under federal commodities law.

The CFTC has argued that event contracts can qualify as “swaps” because they are based on binary outcomes. In May, the agency issued a no-action letter intended to ease certain reporting requirements tied to event contracts, according to Cointelegraph’s report on the CFTC’s guidance.

Cointelegraph also reported that the CFTC has sued at least five states to cement its authority over prediction markets, naming Wisconsin, New York, Arizona, Connecticut, and Illinois in that coverage.

What’s changed since Kalshi’s recent funding and valuation jump

Kalshi’s reported IPO discussions build on a recent surge in market attention. Cointelegraph reported on May 7 that Kalshi doubled its valuation to $22 billion after closing a $1 billion Series F funding round led by Coatue Management.

That update provides context for why an IPO conversation could surface now: a higher valuation and additional capital can accelerate expansion, strengthen compliance and infrastructure, and make public-market fundraising feasible. But it can also sharpen scrutiny, particularly when regulators are challenging the legality of a platform’s most important products.

In other words, Kalshi’s trajectory is shaped by two forces moving in parallel: commercial momentum driven largely by sports-linked trading, and a regulatory environment that increasingly tests whether the platform’s contracts fit within federal commodities oversight or state gambling rules.

With the legal landscape still evolving—and state and federal positions continuing to clash—investors watching Kalshi’s next steps will likely focus less on the IPO headline itself and more on what happens to the platform’s sports-contract exposure as courts and regulators continue to act.

For the near term, readers should watch for any formal confirmation around underwriting talks and, more importantly, for legal developments that could change how sports event contracts are treated—whether through additional state rulings, further CFTC actions, or clarifying regulatory guidance.

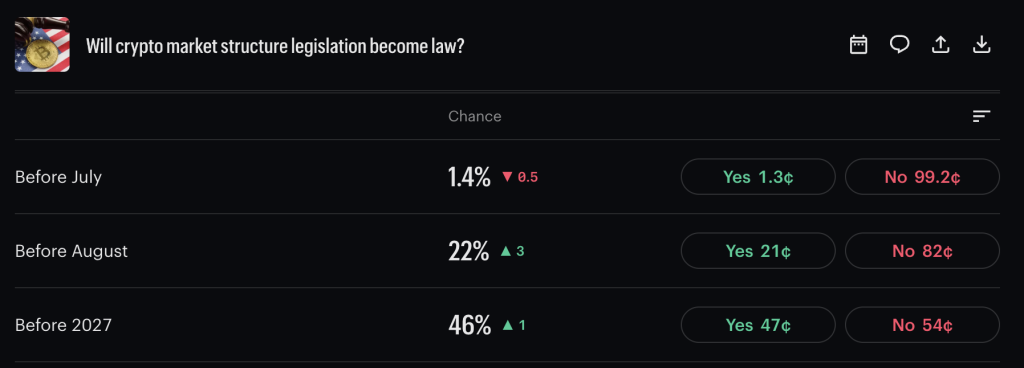

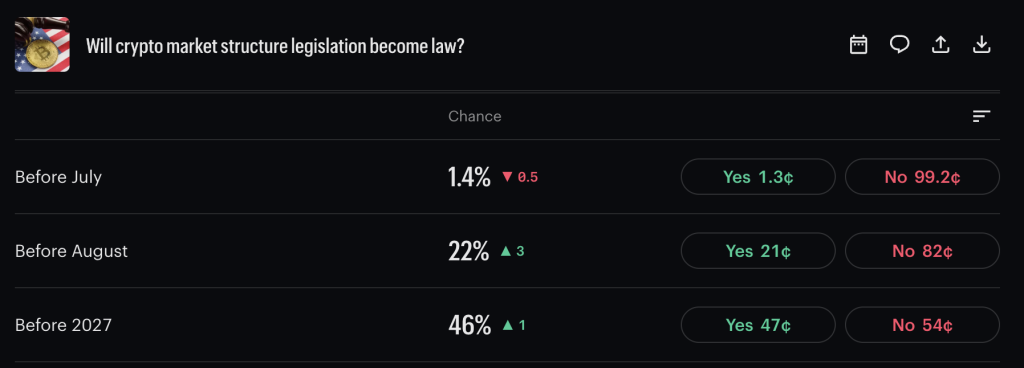

Senator Bill Hagerty told FOX Business on June 18 that he still hopes the Digital Asset Market Clarity Act can clear the Senate before the July 4 recess, even while conceding the bill may slip past Independence Day.

His optimism lands against a wall of procedural reality: the CLARITY Act has not yet received a Senate floor vote, still needs to clear a 60-vote cloture threshold, and requires reconciliation between two competing Senate committee texts before any House-Senate alignment can even begin.

The gap between Hagerty’s stated hope and the legislative calendar is measurable. Congress has fewer than 9 working days before the July 4 recess.

Prediction markets on Kalshi currently price Senate passage by August 2026 at roughly 22%, which reflects the broader analyst read: passage this summer is possible, passage before July 4 is a different question entirely.

The House passed its version of the bill on July 17, 2025, by a 294–134 margin, a bipartisan result that gave the legislation genuine momentum.

The Senate Banking Committee followed with a 15–9 approval on May 14, 2026, advancing the bill to the Senate’s legislative calendar. That step made floor action procedurally possible. It did not make it imminent.

At its core, the crypto legislation would establish a CFTC-led regulatory regime for digital commodities – classifying assets like Bitcoin and Ethereum under CFTC oversight while assigning the SEC narrower jurisdiction over certain broker-dealer and exchange activity.

That division of authority is the bill’s central policy architecture, and it carries real market implications: Standard Chartered has estimated that passage could unlock $8 billion in XRP ETF inflows alone, based on the regulatory certainty the framework would provide.

Three Obstacles Between the Clarity ACT Bill and a Senate Vote

The 60-vote cloture threshold is the first hard constraint. The Senate Banking Committee’s 15–9 approval demonstrates committee-level support, but converting that into 60 floor votes requires bipartisan buy-in that has not yet been publicly secured.

That threshold does not move regardless of how aligned lawmakers and industry are on the bill’s substance.

The second obstacle is inter-committee reconciliation. The Senate Banking Committee text and a separate Senate Agriculture Committee text must be merged into a single floor-ready bill.

Those two committees share jurisdiction over the CFTC-SEC authority split at the heart of the legislation, and any manager’s amendment resolving their differences needs to be filed before a floor vote can be scheduled. That step alone typically takes weeks of staff-level negotiation.

The third, and currently most active, obstacle is the ethics provision dispute. David Nage, managing director and portfolio manager at Arca, said after meetings with Senate offices that lawmakers and industry participants are roughly 80–85% aligned on the bill’s substance, and that stablecoin yield provisions, despite continued criticism from JPMorgan CEO Jamie Dimon, are no longer the primary friction point.

JUST IN: — Bitcoin Magazine (@BitcoinMagazine) June 18, 2026

The Federal Reserve proposes a stablecoin issuer identification program

The Federal Reserve proposes a stablecoin issuer identification program

This is the first GENIUS Act rulemaking from the Fed. pic.twitter.com/Obej8CfbZy

What remains is a conflict-of-interest fight over how to restrict senior government officials from participating in crypto-related business activities while in office.

Senator Kirsten Gillibrand has reportedly conditioned her support on explicit ethics language barring senior officials from profiting off crypto holdings, warning of withheld votes without the clause.

That is not a minor drafting issue, it is a named senator with leverage over the 60-vote math making a specific demand. Nage characterized the remaining disagreement as a political and implementation question rather than a dispute over market structure, but political questions are precisely the kind that stall floor scheduling.

A coalition of gaming associations, tribal governments, and labor unions has separately pressed the Senate to include language banning prediction markets from offering sports and casino-style event contracts under the CLARITY Act framework, another contentious provision that adds to the reconciliation load before any floor vote is viable.

The post Senate CLARITY Act Faces 3 Blockers With Under 9 Days Until July 4 Recess appeared first on Cryptonews.

Binance’s troubled progress toward securing a MiCA license in Greece has sparked scrutiny over whether EU institutions beyond the formal licensing authorities could be influencing outcomes. The issue comes at a critical point in the MiCA rollout, with a hard transitional deadline approaching on July 1 that will determine which crypto-asset firms can continue operating across the EU under the new regulatory framework.

According to reports cited by Cointelegraph, speculation has grown that communication from European Central Bank (ECB) leadership may have affected political support for the exchange. Lawyers contacted by Cointelegraph, however, emphasized that MiCA’s design places the licensing decision with national competent authorities (NCAs), while also leaving room for other EU institutions to provide input.

Key takeaways

- Under MiCA, crypto-asset service provider (CASP) licenses are issued by national regulators, not directly by ECB or other EU-level bodies.

- Legal analysis suggests MiCA does not bar EU institutions such as the ECB from providing an opinion or sharing concerns with an NCA during a CASP review.

- In Binance’s reported Greece case, the relevant authority is the Hellenic Capital Market Commission (HCMC), while ESMA’s role is supervisory and not equivalent to granting the CASP license.

- ECB rhetoric on stablecoins has elevated the policy stakes, even though stablecoin-specific provisions in MiCA are distinct from the exchange licensing chapter.

- The situation highlights the compliance risk for EU market participants as the transitional period ends and licensing decisions become binding for continued operation.

MiCA licensing: national decisions with EU-level input

MiCA establishes a licensing regime for CASPs that is executed through national competent authorities. The regulation assigns authorization responsibilities to NCAs, meaning that an EU institution like the ECB does not, by itself, grant or deny an exchange license.

In Binance’s case, the licensing authority in Greece is the Hellenic Capital Market Commission (HCMC). Binance said in January that it had applied for a MiCA license in Greece. In the days that followed subsequent reporting about the application, Binance also indicated that the application had been reviewed for MiCA compliance and that it had been subject to an ESMA-level review as well, while maintaining that authorization would be decided at a future board meeting.

Legal practitioners contacted by Cointelegraph stressed that MiCA’s wording does not prevent other EU institutions from communicating with national regulators during the review. David Lesperance, founder at Lesperance & Associates, told Cointelegraph that “nothing in the MiCA framework would prevent a third party like the ECB from offering its opinion to that national authority on Binance’s application.”

Similarly, Yuriy Brisov of Digital & Analogue Partners noted that MiCA does not explicitly restrict the ECB from advising or sharing concerns with an NCA. At the same time, he pointed out an important structural detail: ECB involvement is expressly defined in specific parts of MiCA, especially regarding stablecoin issuance, rather than in the CASP licensing provisions that apply to exchanges.

In practice, this distinction matters for compliance and governance. Firms seeking MiCA authorization must address requirements assessed by the NCA, but they may also face broader regulatory scrutiny where EU institutions publicly or informally signal policy concerns that could affect how national regulators evaluate risk.

What the Greece reports suggest—and what remains unclear

Reports cited by Cointelegraph stated that Greece’s market regulator was preparing to reject Binance’s MiCA application. A subsequent report alleged that ECB President Christine Lagarde had signaled, through communication with Greece’s prime minister, that Binance should not be welcomed in Europe. These accounts were reported as the end of MiCA’s transitional period approached, increasing the practical importance of the final authorization outcome for firms’ continued EU operations.

However, public clarity around the exact decision status of the application has been limited. Brisov noted that the HCMC had not published a decision on Binance’s application. Cointelegraph also reported that ESMA does not itself authorize CASP licenses under MiCA, reinforcing that the decisive authority remains at the national level.

For institutional stakeholders, the unresolved question is not only whether an NCA will approve or reject a specific applicant, but also how cross-institutional signaling may shape the direction and tone of the licensing process. Even where legal authority is clearly assigned, the regulatory ecosystem often includes multi-layer interactions that can influence supervisory expectations, risk tolerance, and the evidentiary standards applied to applicant reviews.

ESMA and HCMC did not immediately respond to Cointelegraph’s requests for comment. The ECB and France’s securities regulator, Autorité des marchés financiers (AMF), also declined to comment.

Stablecoins and the ECB’s policy position: why it colors the debate

While the immediate dispute centers on a CASP license in Greece, the policy background is strongly linked to stablecoins. The ECB has repeatedly expressed concerns about privately issued stablecoins and has argued for payment and settlement infrastructure that is anchored in central bank money or otherwise tightly integrated with regulated financial systems.

According to reporting referenced by Cointelegraph, the alleged Lagarde intervention was tied, at least in part, to the stablecoin question. ECB officials have also argued in public remarks that Europe should prioritize regulated settlement systems rather than rely on private stablecoins. In separate commentary, ECB leadership has warned that stablecoins could reinforce the dominance of the US dollar.

This policy emphasis has compliance implications for exchanges and liquidity providers because stablecoin activity can affect how regulators assess systemic risk, market integrity, and the potential for regulatory arbitrage across jurisdictions.

Separately, market positioning is frequently cited in discussions of regulatory significance. Cointelegraph reported that CryptoQuant data indicated Binance held a large share of centralized-exchange stablecoin reserves, including USDT and USDC. The underlying point for institutional readers is not the particular figure itself, but the broader relevance: entities with large stablecoin footprints may become central to regulators’ expectations even when the formal decision concerns an exchange licensing application rather than stablecoin issuance permissions.

Cross-border compliance at the July 1 deadline

MiCA’s transitional period is designed to bring market participants into a harmonized regulatory regime. For exchanges and other CASPs, the July 1 deadline can determine whether continued EU operations require renewed authorization, restructuring, or cessation of certain activities under the new licensing framework.

This case illustrates a recurring compliance challenge across the EU: while legal responsibilities and licensing powers sit with NCAs, the regulatory environment is shaped by the priorities of EU-level institutions. Where institutions focus on stablecoins, payment settlement architecture, or financial stability, national regulators may adjust how they interpret MiCA’s risk-based requirements for CASPs—especially where an applicant’s business model intersects heavily with stablecoin liquidity and on- and off-ramp ecosystems.

Cointelegraph also reported that France could be another potential route for Binance, though it noted that no formal French application had been filed at the time of reporting. The broader compliance takeaway for firms operating across multiple EU jurisdictions is to avoid treating MiCA authorization as a purely jurisdiction-specific process; the effective evaluation can reflect an interplay of national supervision and EU policy priorities.

Closing perspective

As MiCA authorization outcomes tighten around the July 1 deadline, the Binance Greece situation underscores that the licensing process is not only a legal question of MiCA compliance checklists, but also a test of how EU regulatory institutions coordinate—formally and informally—around financial stability, stablecoin policy, and cross-border market integrity. Observers will likely focus next on whether the HCMC issues a decision and how other jurisdictions handle similar applications under the harmonized but politically charged MiCA landscape.

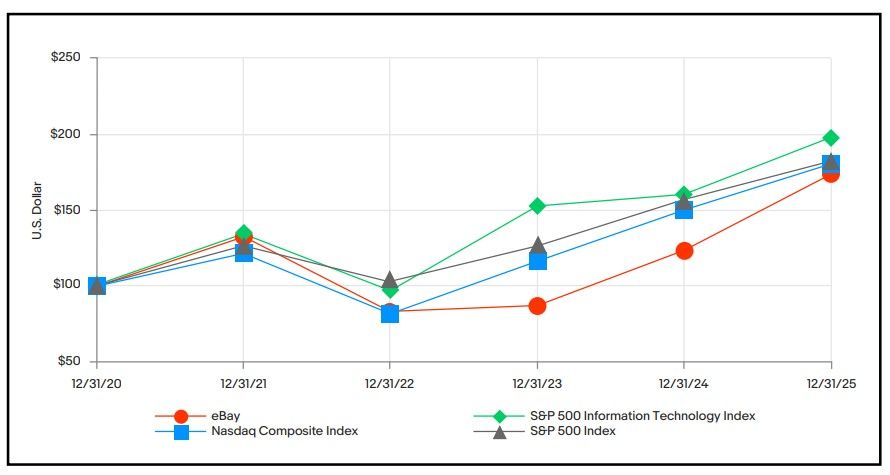

eBay shareholders rejected a governance proposal at the company’s virtual annual meeting that would have lowered the threshold to call a special shareholder meeting from 20% to 10%.

The outcome directly affects GameStop CEO Ryan Cohen, who holds a stake of nearly 9% in eBay. At 10%, Cohen would have had the power to force a special shareholder meeting independently, without needing to build a wider coalition.

The standoff has produced conflict outside the boardroom as well. eBay suspended Cohen’s personal seller account shortly after the takeover bid surfaced. The ban has since been lifted, but the episode fueled a public feud with the company.

Proposal 4 Fails, Closing a Key Governance Path

Proposal 4 failed decisively. Preliminary voting results indicate that about 210 million shares voted against the measure, while roughly 157 million voted in favor. eBay’s board had recommended a vote against the proposal ahead of the meeting.

The result closes one of the governance paths Cohen had available. GameStop proposed acquiring eBay at $125 per share earlier this year. That price represented a 46% premium to eBay’s unaffected closing price on Feb. 4, 2026.

The bid comprised a mix of cash and GameStop stock, valuing the e-commerce company at roughly $56 billion. Nevertheless, eBay’s board rejected the offer as “neither credible nor attractive” and declined to enter negotiations.

Cohen has not held back in his criticism of eBay’s management. He has publicly challenged the company’s $2.4 billion marketing budget, arguing the spending has done little to improve core functionality. He has also described eBay as a well-run asset that management has failed to capitalize on.

The acquisition push has moved markets, too. GameStop stock jumped 9% when the bid first became public. That reflected how tightly investors connect Cohen’s ambitions to GameStop’s transformation narrative.

The broader stakes extend beyond both companies. A successful hostile bid would mark one of the more unusual corporate acquisitions in recent memory. It would see a video game retailer seeking to absorb a global e-commerce platform worth far more than itself.

A Possible GameStop Hostile Tender Offer?

With that governance option now closed, attention has turned to the possibility of a hostile tender offer. That approach would let Cohen take the bid directly to eBay shareholders, bypassing the board’s authority entirely. A tender offer would also test how eBay investors respond, independent of the board’s recommendation.

With formal governance routes now exhausted, a direct appeal to eBay’s shareholders remains Cohen’s most viable option. Whether he moves quickly or waits for better conditions may determine how far this confrontation goes.

The post GameStop and eBay Tensions Rise After Key Shareholder Vote Fails appeared first on BeInCrypto.

In April 2026, Aave faced one of the sharpest liquidity shocks in recent DeFi history. According to Galaxy’s analysis referenced in the coverage, users withdrew roughly $8.45 billion from the protocol in the aftermath of the KelpDAO rsETH bridge exploit. The key point for investors and users: Aave’s contracts were not compromised, but connected markets still experienced severe stress.

The episode quickly became a referendum on what “survival” really means for decentralized lending. Aave continued operating, yet analysts and risk observers argued that a functioning core does not automatically translate into comprehensive safety—especially when collateral, borrowing demand, and liquidity are tied to external assets and across multiple protocols.

Key takeaways

- Aave was not hacked; the turmoil followed an external rsETH bridge incident that propagated into Aave via collateral and liquidity linkages.

- Roughly $8.45 billion flowed out after the April 2026 rsETH exploit, illustrating how quickly DeFi can experience bank-run-like dynamics.

- Aave relied on built-in risk tooling and emergency controls to contain damage as some pools hit full utilization, limiting immediate withdrawals.

- Surviving a single stress event does not settle debates about DeFi systemic risk, including concentration and fast-moving user behavior.

- For users, protocol size and transparency are not substitutes for understanding the assets behind lending markets and governance changes.

A stress event triggered outside Aave

The pressure did not originate in Aave’s own code. It began with the KelpDAO rsETH bridge exploit in April 2026, where attackers stole about $292 million worth of rsETH from KelpDAO’s LayerZero bridge. That theft intensified concerns that some rsETH holdings might not be fully backed.

Those concerns mattered to Aave because rsETH was used beyond its source ecosystem. As the token’s perceived backing came into question, the risk spread to DeFi markets that accepted rsETH as collateral. In practical terms, when collateral loses credibility, lenders face increased exposure to bad debt, while borrowers and depositors tend to reposition to reduce risk—often by withdrawing.

That is where liquidity stress accelerated. As more users attempted to exit, some Aave markets saw utilization climb toward the ceiling. When pools approach or reach full utilization, withdrawals become harder for certain participants because the liquidity needed to satisfy redemptions is already deployed. In other words, the episode looked like a DeFi version of a bank run—not because Aave failed to follow its internal rules, but because DeFi markets can react instantly and continuously on-chain.

What Aave’s founder argues—and why it isn’t the end of the debate

Aave founder Stani Kulechov framed the event as evidence of resilience: the core protocol logic continued to work as designed even amid high stress. That distinction is important. Aave did not suffer a direct exploit of its own contracts; however, the surrounding markets were still forced into emergency modes as external asset disruption rippled through collateral and borrowing channels.

Supporters point to the transparency and determinism of DeFi lending—features that differ from traditional banking crises. Collateral and risk settings are visible on-chain, liquidation mechanisms follow predefined smart contract rules, and participants can inspect activity in real time. In theory, such properties reduce some information asymmetries that have historically contributed to conventional financial breakdowns.

Yet independent analysts, as reflected in the coverage, took a more cautious view. The core argument is not that Aave failed to function; it is that “functioning under stress” may not be sufficient to prove that the system is safe in the broader sense. If adverse shocks continue to arrive from connected components—bridges, collateral issuers, or other DeFi venues—then Aave’s ability to limp through one crisis does not guarantee it will navigate the next without more severe outcomes.

Survival versus safety: the role of concentration and network effects

Critics warn against treating a single successful defense as full validation. Stress events can be interpreted through multiple lenses: strong design helps, but favorable conditions and the specific nature of the shock also matter. In the rsETH case, the market still experienced liquidity strains severe enough to require emergency action, including freezes and risk parameter adjustments.

Another concern highlighted in the coverage is concentration risk. Independent observers noted that large exposures can be spread across many DeFi platforms at once. If a small number of actors control outsized positions, their decisions—such as exiting or closing during volatility—can amplify instability system-wide. The same concentration dynamic has been a longstanding concern in traditional finance, and DeFi’s composable architecture can translate it into a faster-moving ecosystem.

Beyond actor concentration, DeFi’s composability is a double-edged sword. Interoperability helps protocols grow and coordinate liquidity across the ecosystem, but it also creates more pathways for stress to spread. When a lending market depends on collateral that is itself linked to leveraged positions and other connected systems, the resulting network can become harder to unwind during shocks. The condition of the wider DeFi system therefore cannot be separated from a single protocol’s performance.

Unlike regulated banks that can run supervised stress tests under defined frameworks, DeFi’s stress tests happen live—using real user funds, real collateral, and no rehearsals. That doesn’t mean DeFi lacks testing; it means the “test” may occur while markets are already under strain.

How Aave’s risk controls shaped the outcome

Even though the incident began elsewhere, Aave’s internal safeguards influenced what happened next. The platform manages borrowing and liquidation through structured limits such as loan-to-value parameters and liquidation thresholds, while also using mechanisms like supply caps and borrow caps to control how much exposure can build around specific assets.

Aave also uses features designed to reduce cross-asset contagion. Isolation Mode can restrict the impact of higher-risk collateral, while Efficiency Mode (E-Mode) applies special settings for assets that typically move together. Governance, with support from risk advisers, is intended to adjust these parameters as needed—though, as observers note, governance changes can take time, and risk models may not fully anticipate rapid spillover during novel conditions.

During the withdrawal surge, these measures generally held, with core protocol functions continuing to operate. Still, utilization reached 100% in major pools in the coverage description, which helps explain why some withdrawals could not be processed smoothly. The takeaway is not that controls prevented all harm; it’s that they likely narrowed the scope of what might otherwise have become a complete failure.

What users and builders should watch next

The rsETH episode shows that Aave can survive extreme liquidity stress without a direct protocol exploit, but it also highlights how external asset failures can quickly propagate through collateral and liquidity connections. Going forward, readers should focus on how quickly risk parameters can be adapted through governance, how effectively protocols manage external collateral dependencies, and whether the ecosystem’s concentration and composability risks are addressed with the same urgency as smart-contract security.

Crypto World

Nvidia (NVDA) Captures Top Data Center Ethernet Switching Position in Historic Market Shift

Key Takeaways

- Nvidia secured the leading position in data center Ethernet switching revenue during Q1 2026 — marking its first time at the top

- The company’s switching revenue surged 192.7% compared to the previous year, reaching $2.1 billion and capturing 21.5% market share

- Spectrum-X platform fueled this growth, securing major contracts with hyperscalers and AI-focused cloud service providers

- Total Ethernet switch market expanded 39.8% to $15.4 billion; data center category grew 61% to reach $10 billion

- Arista maintained a strong second-place position in data centers; Cisco continues dominating the broader Ethernet switching landscape

Nvidia recorded $2.1 billion in switching revenue during Q1 2026, representing a remarkable 192.7% increase year over year. This performance propelled the company to claim the leading position in data center Ethernet switching by revenue — a segment where it wasn’t even the frontrunner twelve months earlier.

These figures emerged from IDC’s Quarterly Ethernet Switch Tracker, published this Thursday.

NVDA shares climbed 2.95% during trading.

The driving force behind this dramatic expansion is Spectrum-X, Nvidia’s comprehensive AI networking solution. This platform combines Spectrum Ethernet switches, BlueField DPUs, and LinkX cables into a unified system specifically engineered for massive GPU cluster deployments.

This integration strategy is proving decisive in competitive situations. Hyperscalers and AI-focused cloud platforms constructing AI factories require networking infrastructure capable of supporting the demands of contemporary training and inference operations. Spectrum-X was purpose-built to address precisely these requirements.

Paul Nicholson, Research VP at IDC, stated emphatically: “NVIDIA’s rise to #1 in datacenter Ethernet switching in a single year is one of the most significant vendor landscape shifts IDC has tracked in enterprise networking.”

He continued, noting that Spectrum-X is “winning AI factory deals that incumbent networking vendors cannot match with standalone hardware alone.”

Widespread Market Expansion

The data center switching category delivered robust performance beyond just Nvidia — the entire segment demonstrated strength. IDC’s research showed the category expanded 61% year over year, reaching $10 billion in Q1. Meanwhile, the complete Ethernet switch market increased 39.8% to achieve $15.4 billion.

AI infrastructure investments are powering this growth. Hyperscalers and major enterprises alike are implementing AI technologies at scale, creating substantial demand for high-speed, minimal-latency networking solutions. The campus and branch category also recorded impressive performance, climbing 12.3% to $5.4 billion, supported by hardware modernization cycles and increasing component costs.

Arista (ANET) secured the second position in data center switching and similarly gained 2.87% by market close. Cisco maintains its leadership in the comprehensive Ethernet switching market, encompassing campus and enterprise segments alongside data center.

Future Outlook

IDC projects sustained momentum in the Ethernet switch market throughout 2026, fueled by ongoing AI investments from hyperscalers and enterprise customers. Demand for 800G and higher-capacity switching is anticipated to remain strong as inference deployment expands alongside training operations.

Nvidia’s leadership position won’t go uncontested. IDC identified Cisco, Arista, and Broadcom (AVGO) as competitors poised to intensify their competitive strategies within the data center segment.

For the campus market, IDC observed that revenue growth might decelerate if memory supply limitations diminish and reduce the pricing advantages that have recently elevated average selling prices.

IDC additionally highlighted macroeconomic concerns — including tariffs and regional economic uncertainty — as potential factors that could dampen expenditures in certain markets.

During Q1, Nvidia’s data center switching revenue represented 21.5% of the total segment, derived entirely from data center applications rather than campus or branch deployments.

- Cardano (ADA) trades near $0.160 with weak momentum and fading buying pressure.

- The key support at $0.157 is critical, with $0.13 risk if it breaks.

- Oversold signals and the Leios testnet could trigger a short rebound soon.

Cardano (ADA) continues to trade under pressure, holding near the lower end of its recent range as both spot and derivatives markets reflect cautious sentiment.

The token is priced at $0.1607, down 3.2% in the past 24 hours.

Over longer timeframes, the token is down 6.1% over the past 7 days, down 35.6% over the past month, and down 73.2% in the past year, reflecting sustained downside pressure across the broader trend structure.

Daily trading activity, however, remains active, with $368.8 million in 24-hour volume.

Weak derivatives positioning and fading participation

In the derivatives market, the long-to-short ratio stands at 0.96, indicating slightly more short positions than long positions among traders.

Futures open interest is around $348 million, continuing a broader decline from mid-May levels.

This reduction in open interest signals lower speculative engagement and suggests that traders are reducing exposure rather than building conviction positions in either direction.

On-chain indicators also reflect strain in market behaviour.

The Network Realised Profit/Loss (NPL) metric has dropped sharply, showing that a large portion of recent holders have been realising losses rather than gains.

This type of activity is commonly associated with capitulation phases, where weaker holders exit positions under sustained price pressure.

Cardano technical analysis

Cardano remains below its major long-term moving averages, confirming that the broader trend is still bearish.

The altcoin’s price is trading under the 50-day, 100-day, and 200-day exponential moving averages (EMAs), which typically reinforces resistance during attempted recoveries.

The RSI (14) on the daily chart is around 31, suggesting bearish control is still present, though no longer in extreme oversold territory.

Cardano price outlook heading into the Leios testnet catalyst

A key event in the near-term outlook is the expected Leios scaling upgrade testnet around June 23.

This upgrade testnet is being closely watched as a potential catalyst for renewed activity within the Cardano ecosystem.

The current market structure at this stage remains weak, but conditions are showing early signs of compression.

Oversold readings on higher timeframes, combined with reduced selling momentum, suggest that price is approaching a decision point rather than continuing in a steady decline without interruption.

If bulls step in around the $0.157 support zone, a short-term rebound toward $0.172 remains the primary recovery scenario.

However, failure to hold this level would keep downside projections toward $0.148 and potentially $0.13 in focus, depending on how market liquidity and sentiment evolve.

Notably, a bearish flag breakdown has also been noted in recent technical assessments, a formation that typically signals continuation of an existing downtrend after a brief consolidation phase.

This adds weight to the downside risk scenario unless buyers regain control above key resistance levels.

Key Highlights

- Shares of TSM have skyrocketed 102.41% in the past twelve months, dramatically outperforming the S&P 500’s 25.39% return.

- First quarter 2026 revenue reached $35.90 billion, marking a 35.1% increase compared to the prior year, driven by High-Performance Computing at 61% of sales.

- Monthly revenue for May climbed 30.1% year-over-year, maintaining a consistent 30% growth rate across the first five months.

- Analysts project FY2026 earnings per share at $15.76, placing TSM at approximately $462 with a forward price-to-earnings multiple near 29x.

- The company carries a Zacks Rank #2 (Buy) alongside a Momentum Style Score of B; Wall Street consensus shows Strong Buy with an average target of $465.

Taiwan Semiconductor (TSM) has delivered extraordinary returns — climbing more than 100% over the past year — and market watchers believe there’s more upside ahead.

Taiwan Semiconductor Manufacturing Company Limited, TSM

Shares of TSM are currently changing hands near $462. The stock has climbed 24.27% in just the past three months and has doubled in value over the trailing year. By comparison, the broader S&P 500 index advanced only 25.39% during the same timeframe.

At least one analyst now suggests TSM has the potential to hit $500 per share, pointing to what they characterize as underappreciated earnings strength and a dominant position in cutting-edge chip production.

The Street’s consensus earnings forecast for fiscal year 2026 sits at $15.76 per share, implying a forward valuation multiple of approximately 29x. With the semiconductor sector’s median multiple hovering around 33x, some observers see opportunity for TSM’s valuation to expand.

A bullish perspective suggests actual earnings power may be closer to $18.48 for FY2026, which would place the stock at roughly 25x forward earnings — a more attractive valuation than headline figures indicate.

Consistent Top-Line Momentum

TSMC delivered first quarter 2026 revenue of $35.90 billion, representing a 35.1% jump from the year-ago period. High-Performance Computing applications contributed 61% of total revenue, while cutting-edge manufacturing processes at 3nm, 5nm, and 7nm nodes generated 74% of wafer revenue.

The 3nm process technology alone represented 25% of wafer revenue — highlighting where TSMC’s premium pricing capability resides.

Recent monthly figures support the growth trajectory. May revenue increased 30.1% versus the prior year. The five-month cumulative revenue expansion for 2026 stands at 30%.

TSMC has adjusted its full-year 2026 capital expenditure guidance toward the upper boundary of its $52 billion to $56 billion range. The chipmaker is scaling capacity to address substantial order volumes from major clients including Nvidia, Apple, and AMD.

The Path to $500 Per Share

Chief Executive C.C. Wei has stated that worldwide semiconductor supply will fall short of AI-related demand for the foreseeable future.

TSMC is expanding manufacturing operations with new fabrication facilities in Taiwan, Arizona, and Japan. The company is simultaneously advancing Chip-on-Panel-on-Substrate (CoPoS) packaging solutions designed for next-generation artificial intelligence processors.

What Analysts Are Saying

TSM currently holds a Zacks Rank #2 (Buy) classification along with a Momentum Style Score of B. During the previous 60 days, two earnings projections for FY2026 were revised upward while none were lowered. The full-year consensus figure increased from $15.10 to $15.30 throughout that window.

Among Wall Street firms, TSM carries a Strong Buy consensus derived from five Buy recommendations and one Hold rating. Zero analysts currently assign it a Sell rating.

The mean price objective among these analysts stands at $465, suggesting modest upside of approximately 0.62% from present levels within the coming 12 months.

TSM’s weekly price movement shows a gain of 2.11%, in line with the Zacks Semiconductor – Circuit Foundry industry benchmark. The stock’s average 20-day trading volume registers around 11.6 million shares.

6% Inflation vs 4% Savings – You’re Losing #Inflation #Finance #PersonalFinance

Victim of Byker ‘murder’ named as Newcastle man Gino Robb

Iran-US sign 14-point deal at Versailles: In 1919, the same place hosted a treaty after World War I that created conditions for World War II

-

Business5 days ago

Business5 days agoNo Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Tuckernuck – Corporette.com

-

Crypto World5 days ago

Crypto World5 days agoZimbabwe Requires Crypto Businesses to Register Annually Under New FIU Regulations

-

Crypto World6 days ago

Crypto World6 days agoBitget enters Argentina’s regulated crypto market through PSAV registration

-

Tech7 days ago

Tech7 days agoNanoClaw integrates JFrog registries to secure AI agent downloads

-

NewsBeat7 days ago

NewsBeat7 days agoFBI searches office of Ohio voter registration group

-

Entertainment5 days ago

Entertainment5 days agoMatt Damon’s Viral Sci-Fi Thriller Has Taken Over HBO Max

-

Business5 days ago

Business5 days agoAnthropic staff to meet White House officials next week, Axios reports

-

Tech5 days ago

Tech5 days agoAs AI companies race to go public, who else is along for the ride?

-

Crypto World5 days ago

Crypto World5 days agoBitcoin could crash to $48,000, if this historical pattern is triggered

-

Politics5 days ago

Politics5 days ago“Israel’s” ban on ICRC visits ruled illegal, but Knesset moves to stop them permanently

-

NewsBeat5 days ago

NewsBeat5 days agoWarning of disruption as Cardiff Crossrail works to start

-

News Videos5 days ago

News Videos5 days agoFinancial Accounting | Last Day Revision Strategy and Booster | CMA Inter – June 2026

-

NewsBeat5 days ago

NewsBeat5 days agoTributes to former deputy head teacher at Cambridge school among death and funeral notices

-

NewsBeat5 days ago

NewsBeat5 days agowhat doctors are seeing in ebike crashes

-

Entertainment6 days ago

Entertainment6 days agoDeion Sanders Shares Powerful Post After Viral Advice To Deiondra

-

Entertainment5 days ago

Entertainment5 days agoKate Middleton Glare Goes Viral After Kids Booed At Royal Event

-

Crypto World5 days ago

Crypto World5 days agoXRP ETFs Outperform As Bitcoin And Ethereum Funds Extend Outflow Trend

-

Crypto World5 days ago

Crypto World5 days agoMarket Preview: SpaceX (SPCX) IPO Record, Federal Reserve Meeting, and Iran Nuclear Agreement

-

Business5 days ago

Business5 days agoInvesco Quality Income Fund Q1 2026 Commentary

You must be logged in to post a comment Login