Crypto World

GameStop and eBay Tensions Rise After Key Shareholder Vote Fails

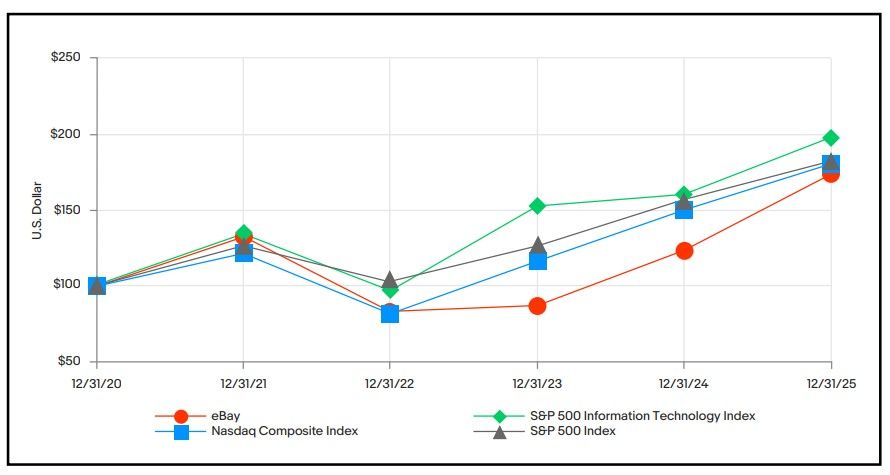

eBay shareholders rejected a governance proposal at the company’s virtual annual meeting that would have lowered the threshold to call a special shareholder meeting from 20% to 10%.

The outcome directly affects GameStop CEO Ryan Cohen, who holds a stake of nearly 9% in eBay. At 10%, Cohen would have had the power to force a special shareholder meeting independently, without needing to build a wider coalition.

The standoff has produced conflict outside the boardroom as well. eBay suspended Cohen’s personal seller account shortly after the takeover bid surfaced. The ban has since been lifted, but the episode fueled a public feud with the company.

Proposal 4 Fails, Closing a Key Governance Path

Proposal 4 failed decisively. Preliminary voting results indicate that about 210 million shares voted against the measure, while roughly 157 million voted in favor. eBay’s board had recommended a vote against the proposal ahead of the meeting.

The result closes one of the governance paths Cohen had available. GameStop proposed acquiring eBay at $125 per share earlier this year. That price represented a 46% premium to eBay’s unaffected closing price on Feb. 4, 2026.

The bid comprised a mix of cash and GameStop stock, valuing the e-commerce company at roughly $56 billion. Nevertheless, eBay’s board rejected the offer as “neither credible nor attractive” and declined to enter negotiations.

Cohen has not held back in his criticism of eBay’s management. He has publicly challenged the company’s $2.4 billion marketing budget, arguing the spending has done little to improve core functionality. He has also described eBay as a well-run asset that management has failed to capitalize on.

The acquisition push has moved markets, too. GameStop stock jumped 9% when the bid first became public. That reflected how tightly investors connect Cohen’s ambitions to GameStop’s transformation narrative.

The broader stakes extend beyond both companies. A successful hostile bid would mark one of the more unusual corporate acquisitions in recent memory. It would see a video game retailer seeking to absorb a global e-commerce platform worth far more than itself.

A Possible GameStop Hostile Tender Offer?

With that governance option now closed, attention has turned to the possibility of a hostile tender offer. That approach would let Cohen take the bid directly to eBay shareholders, bypassing the board’s authority entirely. A tender offer would also test how eBay investors respond, independent of the board’s recommendation.

With formal governance routes now exhausted, a direct appeal to eBay’s shareholders remains Cohen’s most viable option. Whether he moves quickly or waits for better conditions may determine how far this confrontation goes.

The post GameStop and eBay Tensions Rise After Key Shareholder Vote Fails appeared first on BeInCrypto.

Much of the adoption, however, benefits established financial institutions rather than token holders, Seiler said. As traditional finance integrates blockchain tech into existing workflows, less value accrues directly to crypto assets than investors expected several years ago.

Founded in 2021, STS Digital is a Bermuda-regulated crypto options market maker that provides 24/7 liquidity and pricing for institutional clients trading digital asset derivatives. The firm specializes in over-the-counter (OTC) trading.

AI, regulation add to crypto headwinds

Another barrier to growth is artificial intelligence. Investor enthusiasm for AI has diverted both attention and capital away from crypto, Seiler said.

High-profile developments around companies such as OpenAI, Anthropic and the SpaceX (SPCX) IPO have made AI the market’s dominant growth narrative, according to Seiler.

He also pointed to delays in U.S. market structure legislation, including the Clarity Act, as another factor weighing on sentiment.

Regulatory certainty would help to accelerate traditional finance’s shift toward 24/7 trading and settlement, while creating a more constructive backdrop for digital assets, he says.

Options selling caps volatility

Seiler also said the rapid growth of the institutional crypto options market is suppressing bitcoin’s price volatility.

Bitcoin’s implied volatility has remained unusually subdued in recent months, with the BVIV Index, a measure of expected 30-day volatility derived from bitcoin options, falling into the mid-30% range in recent months, among its lowest levels of the current cycle, before beginning to edge higher in July.

Champpixs | Istock | Getty Images

The stock market looked unusually tranquil. Beneath the surface, one of Wall Street’s fastest-growing funds devoted to artificial intelligence investments was unraveling.

In a matter of weeks, Leopold Aschenbrenner’s Situational Awareness went from managing roughly $45 billion to being forced into a sweeping reduction of its listed-stock positions as a historic momentum reversal triggered losses on both sides of its portfolio and set off margin calls and compulsory sales.

Situational Awareness had built concentrated positions in one of Wall Street’s most popular trades: owning companies expected to supply the chips, data centers, power and other infrastructure behind the AI boom while betting against software firms viewed as vulnerable to the technology’s disruption.

Its long positions were concentrated among some of the market’s biggest AI beneficiaries. Public filings showed large stakes in Nebius, Bloom Energy, Sandisk, CoreWeave, SharonAI and IREN as of March 31. By Wednesday’s close, those shares had fallen between by 50% and 78% from recent peaks.

At the same time, software stocks like Adobe that had been used as the short leg of the trade rallied. That meant the fund wasn’t protected by its hedges. Instead, the longs and shorts lost money simultaneously.

“People get over leveraged in this market, and they get seduced by the big returns that some of these companies can deliver,” said Bob Lang, founder and chief strategist at Explosive Options. “If you’re not managing your risk properly, this is the sort of thing that’s going to happen to you.”

As the value of the portfolio fell, the fund’s equity cushion shrank and its prime brokers demanded additional collateral. Raising cash required selling more holdings, adding further pressure to sliding stocks and generating additional losses. What might otherwise have been a painful drawdown became a deleveraging spiral. Ken Griffin’s Citadel hedge fund reached a deal to buy the fund’s publicly traded assets.

“Running somebody out the door like this is as old as time,” Lang said. “I’ve seen it happen a lot in oil markets … there’s a lot of things that are happening underneath the surface that we really don’t know about.”

Momentum crash

The episode offers a stark example of how a hedge fund can sustain devastating losses even when major stock indexes appear relatively calm. The S&P 500 remained near record levels as the damage unfolded, masking one of the most violent reversals in market leadership in decades.

“There is no other way to put it, we just witnessed the largest/ fastest momentum crash in modern history,” Jonathan Krinsky, chief market technician at BTIG, said in a note. “And it wasn’t particularly close.”

Morgan Stanley’s sector-neutral Momentum Index tumbled 17.4% in just four trading days, its worst such decline on record, according to BTIG. The drop surpassed the momentum reversals that followed the dot-com bust, the pandemic shock and the 2022 inflation-driven bear market.

The iShares MSCI USA Momentum Factor ETF posted its best month ever as recently as April, and is now on pace for its worst month, illustrating how quickly one of the year’s strongest strategies turned into one of its weakest.

iShares MSCI USA Momentum Factor ETF year to date

Clearing event?

AI infrastructure stocks rebounded sharply Thursday as investors increasingly interpreted the previous several weeks of volatility as the product of a technical dislocation rather than a deterioration in the industry’s fundamentals.

With one of the market’s largest forced sellers stepping back, traders rushed into many of the same chipmakers, power companies and data-center plays that had been at the center of the selloff. The tech-heavy Nasdaq Composite jumped for a second day Friday, on track for a weekly gain of 0.9% after suffering steep losses the last two weeks.

Nasdaq Composite 5 days

Still, not everyone believes the forced unwind marks the end of the AI selloff.

Among the most prominent skeptics is Michael Burry of “The Big Short” fame. Burry has been one of Wall Street’s most vocal critics of the AI boom, arguing that much of the industry’s demand is being sustained by financing arrangements rather than end customers.

Rather than viewing Thursday’s rebound as a turning point, Burry used the rally to add to bearish positions in Micron, the VanEck Semiconductor ETF and Nvidia put options, according to a Thursday Substack post.

“The knee jerk reaction to the Paired Momentum unwind yesterday has been to put it back on today,” Burry wrote. “This was a historic reversal, even more so than what happened 26 years ago,” when the dot-com bubble began to burst in 2000.

Burry said oversold and overbought conditions made a short-term bounce unsurprising, but he questioned whether the trade still had staying power.

“The legs,” Burry wrote, already “they look tired.”

Bitcoin slipped Friday and tested its weakest levels in more than two weeks as market participants pushed risk assets toward the end of the monthly trading window. According to TradingView data, BTC/USD dropped about 3.5% to trade near $62,369 on Bitstamp, a price zone last seen on July 14.

While crypto did not seem to receive the same tailwind as parts of Asia’s equity rebound, the day’s macro cross-currents were hard to ignore. QCP Capital pointed to the outsized role of semiconductor and AI-related exposures in driving swings across regional markets—an environment that appears to be feeding back into crypto liquidity and positioning.

Key takeaways

- BTC/USD fell roughly 3.5% to around $62,369 on Bitstamp, the lowest level in over two weeks.

- US stocks weakened around the monthly close, contrasting with Asia’s rally—especially South Korea’s KOSPI.

- QCP Capital linked crypto activity to the relationship between equity positioning, regional tech sentiment, and crypto liquidity.

- Analysts at CoinGlass showed July ended with strong gains, but at least one trader warns August could bring a rollover similar to 2022.

- Rekt Capital highlighted the 50-month EMA around $65,820 as ongoing resistance after failed breakouts since mid-June.

BTC drifts lower as US equities soften into month-end

TradingView indicated BTC/USD lost ground during Friday’s session, moving toward $62,000 amid broader pressure into the monthly close. The move came despite a rebound elsewhere earlier in the day, when parts of Asia stabilized after a semiconductor-led sell-off.

According to the same macro framing cited by QCP Capital, semiconductor stocks drove both the decline and subsequent recovery because major indices remain heavily weighted to the global AI and memory-chip cycle. That concentration helps explain why an equity catalyst can quickly translate into shifts in sentiment—and potentially liquidity—across correlated markets, including crypto.

QCP Capital added that crypto trading activity increased around the KOSPI’s sharp swings, describing it as evidence of a growing relationship between crypto liquidity, regional equity positioning, and broader technology-sector sentiment. The firm’s argument is less about a single day’s price and more about how the plumbing of liquidity may be changing alongside technology-driven equity narratives.

Asia rebounds while the US turns cautious

US stocks traded red at the open before leveling out, which diverged from the earlier rebound seen in Asia. South Korea’s KOSPI index finished the day up 17.9%, its largest single-day gain on record, according to figures referenced in the market commentary.

The day’s backdrop also included currency and rate dynamics. The commentary noted that both Japan and Korea reportedly engaged in currency interventions on Thursday, while Japan’s central bank kept benchmark interest rates at 1.0% after the US Federal Reserve decided to hold steady earlier in the week, following the US PCE inflation update.

For crypto traders, the practical takeaway is that “risk-on” can appear in pockets while “risk management” remains active in other major venues. When that happens, BTC can still underperform even as some regional equities bounce—particularly when liquidity flows are being reallocated quickly between markets.

July strength sets up a test for August

Even with Friday’s pullback, BTC’s monthly performance has looked constructive. CoinGlass data referenced in the article showed BTC/USD was up 8.5% for the month as of the end of the monthly candle, its strongest July showing since 2022.

That improvement mattered because earlier positioning had already shifted toward the idea of a relief bounce extending into August. The comparison traders were drawing was specifically to the 2022 bear-market structure: a rally that ultimately transitioned into a subsequent move toward a next longer-term bottom.

Rekt Capital—one of the analysts cited for that 2022 mapping—forecast that any bullish attempt might not hold immediately. In an X post on Friday, he wrote that price could try to “maintain these highs in the early stages of August,” but that history suggests a rollover similar to what occurred in 2022.

Technical resistance remains in focus near the 50-month EMA

Rekt Capital also pointed to a technical level that has limited follow-through. He reiterated that Bitcoin’s 50-month exponential moving average (EMA), currently around $65,820, has continued to act as resistance. In his view, that has been visible through two failed breakouts since mid-June.

For investors and traders, the implication is straightforward: even when BTC can put together a strong July, the next phase depends on whether it can clear longer-term trend resistance rather than merely bounce within an existing range. Levels like the 50-month EMA tend to attract both systematic and discretionary attention because they represent a longer horizon for trend definition.

That context also helps reconcile the mixed picture on Friday. BTC weakening toward the low-$60,000 area may be consistent with traders taking profits or reducing exposure as the market transitions from a month-end catalyst period into a new monthly cycle—especially if macro uncertainty and equity volatility persist.

Going forward, readers should watch whether BTC can reclaim and hold above the mid-$60,000 resistance area highlighted by the 50-month EMA and whether August follows through on the “rollover” scenario traders cite from 2022—or instead breaks the pattern and sustains higher levels despite the month-start shift.

Wintermute reported that institutional investors accounted for a record 72% of spot OTC trading volume on its desk in the first half of 2026, up from roughly 61% in the second half of 2024, a structural shift that the firm says makes broad-based altcoin rallies significantly less likely going forward.

The implication is direct: the capital formation mechanism that historically sent profits cascading from Bitcoin into ETH and then down the altcoin long tail is no longer functioning the same way, and retail traders still positioning for an indiscriminate altseason may be running an outdated playbook.

Discover: Everyone’s Got a Take. Get Free $25 to Actually Trade Yours

Wintermute: Capital Is Concentrating, Not Dispersing

Wintermute’s analysis frames the shift as fundamentally about mandate-driven versus speculation-driven capital. Institutional participants operate under defined risk limits and hold positions over longer periods, which means their flow concentrates in assets with demonstrated liquidity, regulatory clarity, and identifiable fundamentals, not in tokens riding narrative momentum.

The report noted that realized volatility has declined from roughly 70% in earlier market cycles to around 45% in the current one, a direct consequence of institutional order flow replacing retail-driven speculation as the marginal price setter.

Lower volatility compresses the explosive upside that defined 2021-style altseasons, but it also reduces the severity of the unwind.

For traders, the operational takeaway is that OTC block flow, executed away from public order books, is increasingly where price direction gets established. Retail participants reacting to exchange order book moves may consistently find themselves a step behind positioning that was set in bilateral institutional trades.

This dynamic is visible in the institutional infrastructure buildout accelerating across major crypto venues.

Discover: Your Market Calls Are Worth Something. Start With Free $25 on Kalshi

RWA Tokenization as the Institutional On-Ramp

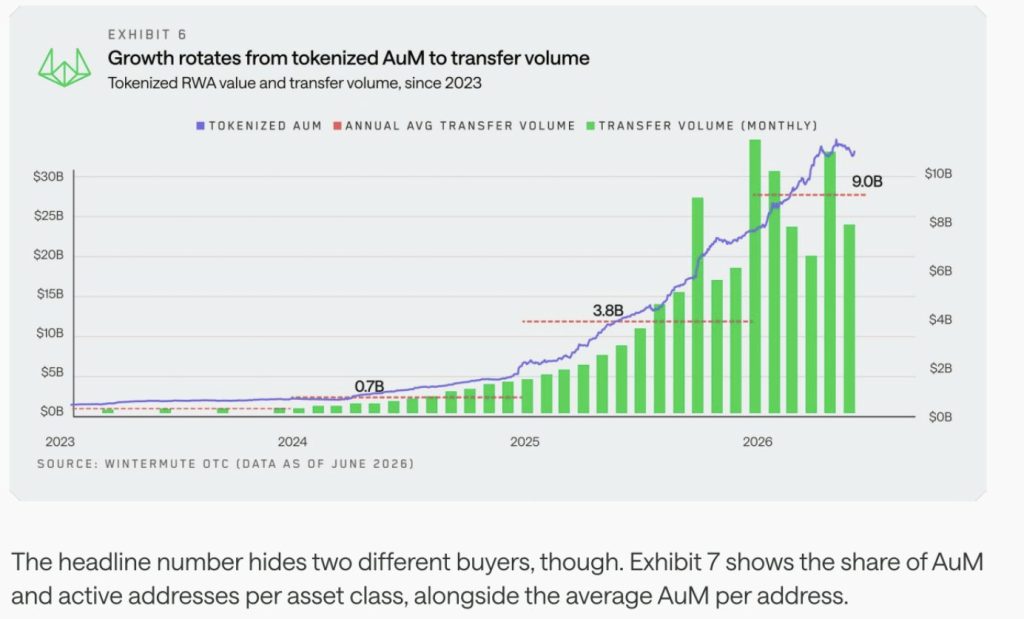

The tokenized real-world asset market reached $31 billion in H1 2026, representing roughly a 50% increase over the prior period, according to Wintermute’s data.

Average monthly transfer volume more than doubled to $9 billion, which signals operational adoption rather than speculative positioning, institutions are moving these assets, not just accumulating them.

The primary instruments attracting institutional capital are U.S. Treasuries, money market funds, and private credit, yield-bearing products where blockchain infrastructure delivers settlement efficiency and programmatic compliance without changing the underlying risk-return profile. This is not institutions chasing crypto-native yield; it is traditional finance running familiar instruments on new rails.

Wintermute also noted that altcoin options notional volume on its OTC desk increased approximately 3.4 times from the second half of 2025 to the first half of 2026, driven by yield-seeking strategies rather than outright directional bets.

Contracts for difference are being deployed across a wider range of tokens for hedging and basket strategies. The derivatives expansion reinforces the same thesis: institutional participants want structured exposure, not raw token speculation. The pattern mirrors broader institutional demand for collateral-grade crypto assets with defined utility.

Discover: Get Paid to Be Right, $25 to Start on Kalshi

The post Wintermute Data Shows Institutional Flow Is Killing Broad Altcoin Rallies appeared first on Cryptonews.

Unlike AI, which has driven a surge in demand for graphics processors to train and run large language models, quantum computing targets a different class of challenges. Researchers say the technology could accelerate molecular simulations, optimize complex logistics networks, advance materials science and improve cryptography.

Krishna said IBM has already demonstrated some of that potential, using quantum computers to uncover properties of materials that conventional computers had been unable to model. Those insights could eventually contribute to longer-lasting batteries, new materials, fusion energy research and drug discovery.

Growing confidence around commercialization has been matched by rising investment. In May, IBM announced plans for a standalone quantum chip foundry backed by a $1 billion commitment from the U.S. Department of Commerce through the CHIPS incentive program, alongside a matching $1 billion investment from the company. Other developers have also expanded manufacturing capacity and research partnerships as they push toward fault-tolerant quantum computers.

The industry’s progress is also drawing attention from the digital asset sector. Several publicly traded bitcoin miners, including MARA Holdings (MARA), Riot Platforms (RIOT) and CleanSpark (CLSP), have diversified into AI and high-performance computing, leveraging their data centers and power infrastructure for new computing workloads.

Quantum computers won’t simply slot into today’s AI data centers. They require entirely different hardware and operating environments, meaning the industry will need new facilities and supply chains as the technology matures.

Bitcoin is still under pressure across the higher time frame despite stabilizing above recent swing lows. While the short-term structure has shifted into consolidation, the broader trend continues to favor sellers unless BTC can reclaim several key resistance levels.

Meanwhile, futures market data shows aggressive market buying beginning to return, potentially laying the groundwork for a relief rally if the price confirms the move.

Bitcoin Price Analysis: The Daily Chart

The daily chart shows BTC trading around $63.3K after its sharp late May breakdown from the $74K region. The selloff pushed the asset well below both the 100-day moving average, currently around $69K, and the 200-day moving average near $71K, leaving the broader market structure bearish.

Since the decline, BTC has entered a sideways consolidation between roughly $60K and $67K. Buyers have repeatedly defended the lower boundary of this range, while the $67K resistance zone continues to cap every recovery attempt.

Beyond the major resistance at $67K, the confluence of the 200-day moving average and the $72K to $74K supply zone is the next potential target, if an upside move materializes. A successful reclaim of those levels would improve the medium-term outlook and could expose the next resistance around $82.5K.

On the downside, immediate support remains around $60K. Losing this level would likely shift attention toward the broader support area around $54K if selling pressure accelerates, which will make the bear market both longer and deeper.

BTC/USDT 4-Hour Chart

The 4-hour timeframe shows Bitcoin consolidating after breaking below a rising channel that had supported the recovery throughout July. The channel breakdown suggests that bullish momentum has weakened and that the recent advance has transitioned into a corrective phase.

The price is currently testing the short-term support around $63K to $63.5K after rejecting the $65K resistance area. As long as this support holds, BTC could continue ranging inside this zone or potentially have another go at the $65K resistance in the coming weeks. On the other hand, a decisive breakdown below $63K would likely increase the probability of another move toward the previous demand zone around $60K.

On the upside, reclaiming the resistance area around $65K to $65.5K would be the first indication that buyers are regaining control, with the broader resistance near $67K remaining the key hurdle for a stronger recovery.

Sentiment Analysis

The Taker Buy Sell Ratio offers insight into whether market participants are executing more aggressive buy orders or sell orders. Values above 1 generally indicate buyers are taking the initiative, while readings below 1 suggest sellers remain dominant.

Although Bitcoin’s price has remained trapped near $64K, the 100-period EMA of the Taker Buy Sell Ratio has climbed above the neutral 1.0 level and continues to hold above the threshold. This divergence indicates that aggressive buying activity has strengthened even as price has failed to respond meaningfully.

Historically, sustained periods where taker buying leads while price consolidates can precede stronger directional moves if spot demand eventually absorbs overhead supply. While this does not guarantee an immediate breakout, it suggests underlying demand is improving beneath the surface.

For now, this bullish futures signal still requires confirmation from price. A break above the $67K resistance zone would align improving order flow with bullish price action, while a loss of the $60K support area would invalidate the near-term constructive outlook despite the positive shift in taker behavior, and potentially lead to another long liquidation cascade.

The post Bitcoin Price Analysis: Is BTC Heading Below $60K After the Latest Rejection? appeared first on CryptoPotato.

Treasury Secretary Scott Bessent posted a lengthy statement on X on July 30, 2026 demanding the Senate vote immediately on the Clarity Act, closing with Bitcoin creator Satoshi Nakamoto’s dismissal, that he had no time to convince those who don’t understand, in what amounted to the most aggressive public pressure campaign from a sitting Treasury Secretary on crypto legislation in recent memory.

The move followed Bessent’s earlier Wall Street Journal op-ed arguing the U.S. risks forfeiting its role as a global financial leader if Congress fails to act.

Bessent argued that Senate Banking and Agriculture Committee staff had spent thousands of hours negotiating bipartisan revisions since the House passed the Clarity Act over a year ago, and that Republicans now have a floor-ready bill awaiting a vote. His post framed the Democratic holdout not as principled opposition but as political deference to Warren’s bloc, a direct accusation that the delay is manufactured rather than substantive.

The op-ed Bessent published through The Hill made the economic case explicitly: the U.S. risks pushing the digital assets industry offshore through regulatory inaction, ceding ground that cannot easily be reclaimed.

He pointed to the GENIUS Act, signed into law last year and establishing the first federal stablecoin framework, as proof that bipartisan progress is achievable when the political will exists.

“The U.S. didn’t become the world’s financial center by hesitating in moments of technological change. It led by setting standards that others followed. By passing comprehensive digital-asset market-structure legislation, Congress will ensure that the next generation of financial innovation is built on American rails, backed by American institutions, and denominated in American dollars.”

Bessent also pushed back on Democratic claims that the bill lacks consumer protections, arguing that Titles II and III would substantially expand compliance requirements for digital asset intermediaries, moving them closer to the standards applied to traditional financial institutions.

He additionally defended the Blockchain Regulatory Certainty Act provision within the Clarity Act, which protects decentralized software developers from Bank Secrecy Act registration requirements, noting the Fraternal Order of Police, which previously opposed the measure, now supports it.

Discover: Everyone’s Got a Take. Get Free $25 to Actually Trade Yours

Clarity ACT: The Ethics Provisions Deadlock

The substantive obstacle to passage is not consumer protection language, it is the ethics provisions Senate Republicans introduced in May 2026.

Those provisions would bar the president and other federal officials from issuing or sponsoring digital assets while in office, language explicitly aimed at curtailing President Trump’s crypto activity after disclosures showed he generated over $1.2 billion from crypto ventures in 2025 alone.

Democrats have criticized the proposal on three grounds: the restrictions expire in 2029, enforcement rests solely with the Justice Department, and the language does not extend to officials’ children.

That gap between what Republicans offered and what Democrats consider minimally credible enforcement is where negotiations have stalled. Sens. Angela Alsobrooks and Thom Tillis appeared to reach a bipartisan agreement late last month, but whether that deal commands sufficient support from both industries remains unresolved, per The Hill’s reporting.

Meanwhile, the broader crypto market on July 30 was digesting the FOMC decision and ETF flow data, with Bitcoin largely shrugging off the political noise around Senate scheduling, a pattern that held into the following session, where Bitcoin price continued ignoring the political stalemate even as the legislative calendar compressed.

Discover: Get Paid to Be Right, $25 to Start on Kalshi

The post Bessent Invokes Satoshi to Force Senate Vote on Crypto Clarity Act appeared first on Cryptonews.

The team behind the second-largest meme coin introduced an interesting challenge for its community aimed at increasing the token’s global popularity.

Some members said they plan to take advantage of the initiative soon, while others pointed to important reasons to avoid it.

SHIB in the Air

Earlier this week, the major international airline Emirates shook hands with Crypto.com, thus allowing UAE residents to book flights using the digital payment solution on the exchange’s website and application.

Shiba Inu’s official X account shared the update, reminding that SHIB is among the numerous tokens supported by the platform. It also encouraged its community to put the initiative to the test.

Many users applauded the news, and some asserted that they will use the meme coin as a payment method in the coming days. Others said they will never part with their coins, reminding the case of the programmer Laszlo Hanyecs, who bought pizza with Bitcoin (BTC) in 2010.

“Never using my SHIB for paying for anything, I don’t wanna end up being like that guy that bought pizza with his Bitcoin,” CryptoKing stated.

In the crypto world, Hanyecs’s story is considered both legendary and deeply instructive. 16 years ago, he spent 10,000 BTC to buy two pizzas, showing that the cryptocurrency can already be used as a payment method. At that time, the stash was worth around $40, yet at current rates it equals over $630 million.

Alongside promoting the idea of purchasing flight tickets with SHIB, the team has kicked off preparations for its sixth birthday, set for August 1. The community is already speculating whether the celebration will come with a major ecosystem update, but so far there are no signs that this will happen.

SHIB Price Outlook

Last weekend, the self-proclaimed Dogecoin killer posted a sudden and somewhat unexpected daily increase of 35%. Among the potential catalysts that have triggered the pump are a mysterious whale who has resumed accumulating after more than half a year of inactivity, as well as the notable resurgence of the burning mechanism.

In the following days, though, the bears stepped in and erased most of the gains, with SHIB currently trading at around $0.000004702, which is still a 12% jump on a weekly scale. According to Santiment, there were 52 whale transactions amid the rally, suggesting that large holders took profits. At the same time, retail investors joined the party too late and gave whales the necessary liquidity to reduce their exposure.

The analytics platform suggested that the optimal approach with meme coins like SHIB is to exit when retail FOMO surges and return once the crowd turns hostile and labels the token a scam.

The post Shiba Inu Team Sets a New Challenge for the SHIB Army: Who Goes First? appeared first on CryptoPotato.

What is Ceuta?

The city of Ceuta, a peninsular region covering 19.9 sq. km (7.7 sq. mi) on Africa’s northern coast, is one of two Spanish exclaves on the continent, along with Melilla, which is about 220 km (140 mi) southeast. The two Spanish autonomous cities represent the European Union’s only land borders with Africa. Spain has possessed Ceuta, which is separated from mainland Spain by the Strait of Gibraltar, since 1580.

Ceuta has a population of more than 83,000, a mix of Christians and Muslims, including residents and day workers from Morocco and Spain. Ceuta’s population has generally lived harmoniously.

But Morocco, which largely surrounds the two exclaves, still treats them as occupied lands and challenges Spain’s sovereignty, citing history dating back to the Islamic conquests during the 8th century.

Over the years, Rabat, the political seat of the African nation, has triggered diplomatic incidents as part of the dispute. In 2002, Morocco and Spain had a standoff after both sent forces to a small uninhabited island off Ceuta. And in May 2021, amid a deepening diplomatic spat over the disputed Western Sahara region, the Moroccan government loosened its border controls, resulting in nearly 8,000 people from Morocco and sub-Saharan countries pouring into Ceuta in just two days. Some of the migrants eventually returned, but the diplomatic rupture was only repaired when Spain backed Morocco’s autonomy plan for Western Sahara in 2022.

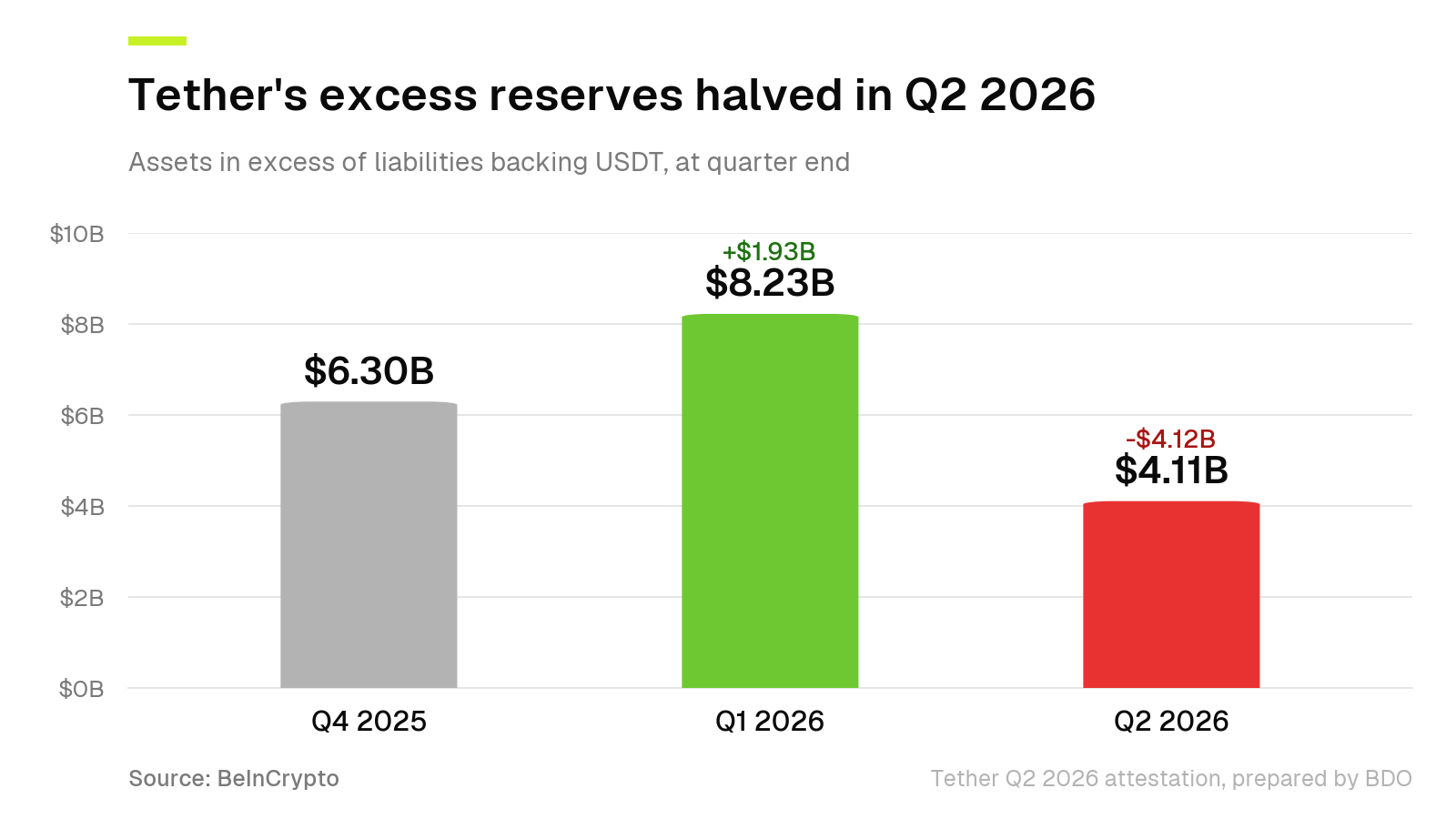

Tether earned roughly $1.5 billion in the second quarter, yet the cushion protecting Tether (USDT) holders shrank by half. Excess reserves closed June at $4.11 billion, down from a record $8.23 billion.

The stablecoin issuer published its Q2 2026 attestation on Friday, prepared by accounting firm BDO. The report confirms USDT stays overcollateralized. It does not explain where more than $5 billion of surplus went.

The Arithmetic the Report Skips

Tether reported total assets of $187.75 billion against liabilities of $183.64 billion on June 30. Three months earlier, assets stood at $191.77 billion.

The asset side therefore fell about $4 billion while token liabilities barely moved. In May, the record Q1 reserve buffer was the company’s headline number.

Add the $1.5 billion earned during the quarter and the gap implies roughly $5.6 billion of unrealized losses or outflows. Tether entered April holding about $20 billion in gold and $7 billion in Bitcoin.

The wording moved as well. The Q1 release reported “net profit.” Friday’s release reports “net operating profit.”

That second measure strips out mark-to-market swings on exactly those assets. Gold and Bitcoin both saw sharp moves during the quarter.

Three Disclosures That Disappeared

Tether’s Q1 report attached a dollar figure to every major asset class. It listed $141 billion in Treasury bills, roughly $20 billion in gold, and about $7 billion in Bitcoin.

Friday’s report attaches none of the three. Gold now appears only as a tonnage count of more than 146 tons.

Meanwhile, Tether’s US Treasury holdings are described as a majority share of reserves. Readers get no figure to compare against the $141 billion disclosed in May.

The company also dropped a boast. In Q1 it noted the buffer alone would rank as the third-largest stablecoin in circulation.

CEO Paolo Ardoino set a different standard in March, when the company hired a Big Four firm.

“Trust is built when institutions are willing to open themselves fully to scrutiny,” the attestation read, citing Paolo Ardoino, CEO of Tether said.

Follow us on X to get the latest news as it happens

The Audit Clock Is Still Running

Tether signed its auditor on March 24. The Financial Times identified KPMG as its auditor three days later. Four months on, Friday’s release says only that the process continued.

That March announcement also stated the group retains earnings instead of paying out profits. If that still holds, distributions cannot explain the decline, which leaves asset values.

Ardoino conceded pressure without sizing it. He said the assets behind part of the reserves came under direct strain during the quarter.

USDT itself never wobbled. The token held its peg near $0.9986 and keeps a third-place market capitalization of $183.5 billion.

Demand held up too, even after Revolut announced a USDT delisting in Europe this month. Tether says it added more than 30 million users during the quarter.

A halved buffer on a $183 billion book is not a solvency event. It is a disclosure question.

At $4.11 billion, the cushion now sits below the $6.3 billion Tether carried at the end of 2025. KPMG will be the first outside party in a position to explain why.

The post Tether Made $1.5 Billion in Q2 and Its Reserve Cushion Still Halved appeared first on BeInCrypto.

STS Digital CEO sees three major headwinds for crypto markets

Mahershala Ali Speaks Out on Marvel’s Canceled Blade Movie

Indiana Senate leader who defied Trump stepping down after defeats

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread: Brooks Brothers

-

Sports5 days ago

Sports5 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Business2 days ago

Business2 days agoWhy Trees Belong on the Risk Register

-

Tech5 days ago

Tech5 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World6 days ago

Crypto World6 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics4 days ago

Politics4 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Politics3 days ago

Politics3 days agoThe Part of the Electric Transition Nobody Wants to Discuss

-

News Videos5 days ago

News Videos5 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

Business2 days ago

Business2 days agoMajor shareholder moves on Canyon

-

Crypto World5 days ago

Crypto World5 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

News Videos1 day ago

News Videos1 day agoBitcoin Enters the 3rd Stage of the Bear Market

-

Politics5 days ago

Politics5 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Entertainment3 days ago

Entertainment3 days ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Entertainment6 days ago

Entertainment6 days agoSara Gilson Killed By Husband After Viral “Pedophile” TikTok Video

-

Crypto World3 days ago

Crypto World3 days agoKraken Enables Retail Access to Jersey Mike’s IPO via Tokenized Shares

-

Tech7 days ago

Tech7 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

Tech4 days ago

Tech4 days agoNew macOS Sequoia & Sonoma security updates for older Macs

-

News Videos3 days ago

News Videos3 days agoClaude: Build Financial Dashboards in Minutes (2026)

-

Politics1 day ago

Politics1 day agoLuke Littler’s dominance sparks GOAT debate

-

Sports16 hours ago

Sports16 hours agoSeema Kaliramna Wins Discus Throw Bronze, Takes India’s CWG Medals Tally To 17

You must be logged in to post a comment Login