Crypto World

Fed chair nominee Kevin Warsh not necessarily a hawk, says close colleague Stanley Druckenmiller

The knee-jerk reaction to Donald Trump’s pick of Kevin Warsh to replace Jerome Powell as chairman of the Federal Reserve is that the president made the most hawkish selection among the four reported finalists for the job.

In the wake of last night’s leak that Warsh was to be the choice, risk markets — crypto among them — fell sharply, with bitcoin plunging all the way back to $81,000.

“The branding of Kevin as someone who’s always hawkish is not correct,” Stanley Druckenmiller told the FT on Friday. “I’ve seen him go both ways.”

Druckenmiller — who made billions working alongside George Soros at Quantum Fund and with his own family office, Duquesne Capital Management — is surely in a position to know. Warsh has been a partner at Duquesne since 2011.

The relationship between them has previously been described as close to father-son, with the two speaking and/or texting more than a dozen times per day.

“I could not think of a single other individual on the planet better equipped,” Druckenmiller continued.

Where does Treasury Secretary Scott Bessent fit in?

Druckenmiller also has very close ties to Scott Bessent. It was Druckenmiller who hired Bessent at Quantum Fund more than 30 years ago, where the to-be U.S. Treasury Secretary made his own billions.

“The pair [Bessent and Warsh] embody the way Druckenmiller interprets markets and economic policy,” wrote the FT in a profile roughly one year ago.

“I’m really excited about the partnership between [Warsh] and Bessent,” Druckenmiller said today. “Having an accord between the Treasury secretary and Fed chair is ideal.”

Rising Japanese bond yields are quietly draining global liquidity, and Bitcoin is caught in the crossfire.

That’s the core argument from XWIN Research’s latest analysis, which connects Japan’s surging government bond yields to Bitcoin’s sluggish price action.

How Japan’s Bond Market Hits Bitcoin

Japan’s 10-year bond yield recently hit 2.39%, its highest level since 1999. With roughly ¥390 trillion in government bond holdings, even a 1% rise in yields can trigger tens of trillions of yen in unrealized losses for banks, insurers, and pension funds.

These institutions must then shore up their balance sheets. That means selling risk assets and pulling capital home. Since Japan is the world’s largest foreign creditor, this repatriation shrinks liquidity everywhere.

Bitcoin, as a risk asset, depends heavily on global liquidity. History shows it rises during easy-money periods and stalls when rates climb. The current environment fits that pattern.

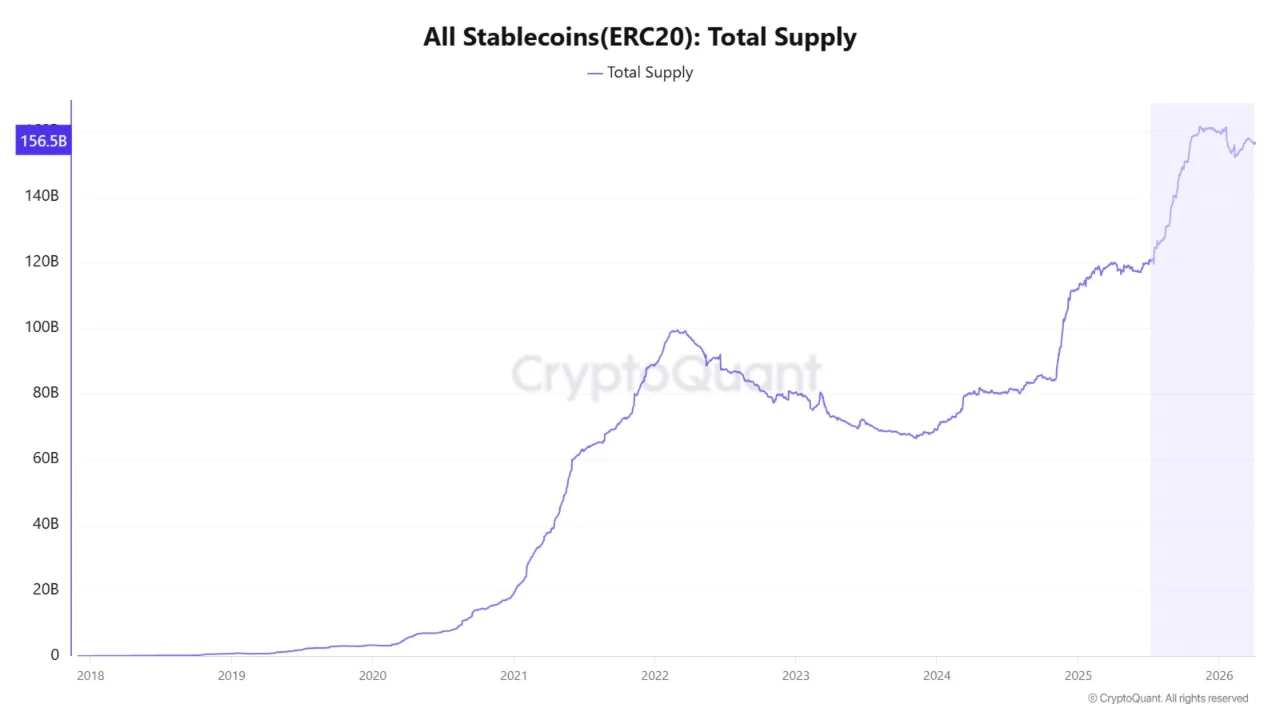

Stablecoin data adds nuance. ERC-20 stablecoin supply has returned to all-time highs, suggesting plenty of sidelined capital exists. Yet that money is not flowing into Bitcoin. Early 2026 saw roughly $9.6 billion exit BTC, with funds rotating into stablecoins instead.

Why This Matters Now

Rising rates do more than create selling pressure. They raise borrowing costs, reduce leverage, and discourage new capital from entering risk markets. The yen’s relative strength also pulls funds away from dollar-denominated assets, including crypto.

XWIN Research argues that understanding Bitcoin now requires looking beyond on-chain metrics. Rates, currencies, and capital flows tell the deeper story.

The post Japan’s Bond Crisis Is Quietly Strangling Bitcoin’s Rally appeared first on BeInCrypto.

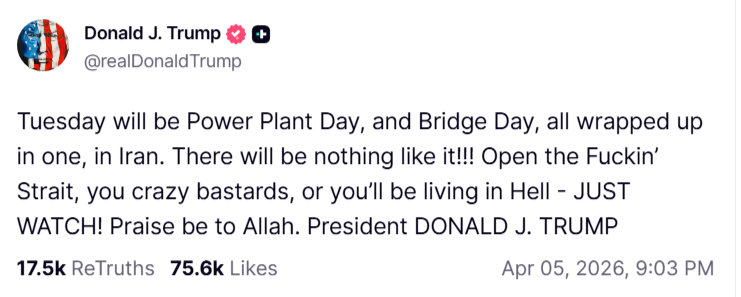

Oil prices extended gains in early Asian trading on Monday as President Donald Trump sharply escalated threats against Iran. He vowed to strike power plants and bridges unless Tehran reopens the Strait of Hormuz by Tuesday.

The latest ultimatum signals that the six-week-old conflict is entering a more dangerous phase with no diplomatic off-ramp in sight.

Trump’s Ultimatum: ‘Power Plant Day, and Bridge Day’

In a social media post, Trump declared Tuesday would be “Power Plant Day, and Bridge Day” and demanded Iran “open the f—ing Strait,” warning Tehran would “be living in Hell.” The unprecedented language signals Washington’s growing frustration with stalled diplomacy over the critical waterway.

Brent crude climbed above $111 a barrel, up 1.9%, while West Texas Intermediate traded near $112 during the Asian morning session. Tehran rejected the demands, and the Strait of Hormuz remains closed to most shipping traffic. The war has triggered a supply shock now threatening to become a full-blown global energy crisis.

Rising oil and fuel prices are stoking inflation, slowing economic growth, and squeezing businesses and consumers worldwide. US gasoline pump prices have risen by roughly $1 per gallon since the conflict began. Analysts expect the March consumer price data on Friday to show the sharpest monthly increase since 2022.

OPEC+ members approved a modest 206,000 barrel-per-day output increase for May after a weekend meeting. However, the move was largely symbolic, as key producers cannot increase output due to the war. Russian supply has also been disrupted by Ukrainian drone strikes on its Baltic Sea export terminal.

Market stress indicators are flashing red. Brent’s prompt spread widened beyond $10 a barrel in backwardation. That gap exceeds peaks seen during Russia’s 2022 invasion of Ukraine. Physical market prices tell an even starker story. Dated Brent surged past $140, reaching levels not seen since 2008.

Diplomacy Stalls as Attacks Continue

Iran has officially told mediators it will not meet US officials in Islamabad, and ceasefire efforts have stalled. Tehran has allowed limited passage through the Strait of Hormuz for select vessels from countries it deems friendly. Iraq received an exemption from Iran’s shipping curbs, though carriers remain cautious about entering the strait. Oman said it discussed options with Tehran to restore shipping flows.

Global buyers are now aggressively bidding for alternative crude supplies from the US Gulf Coast and the North Sea. Israeli strikes continued across Iran over the weekend, while Tehran hit Kuwait Petroleum Corp. headquarters and shut down an Emirati petrochemicals plant.

Asian equity markets opened cautiously. Japan’s Nikkei rose 0.7% and South Korean shares gained 2%. Gold fell about 1% to around $4,630 as surging energy costs undermined expectations of interest rate cuts.

The post Trump’s Hormuz Ultimatum Sends Oil Past $110, Highest Since March appeared first on BeInCrypto.

The Drift Protocol, a Solana-based decentralized finance platform, is drawing renewed scrutiny after a $280 million exploit exposed persistent gaps in its security posture. A post-incident review and commentary from legal counsel frame the breach as something that could have been prevented with basic operational security measures, prompting discussions about civil negligence and the broader risk landscape facing DeFi projects.

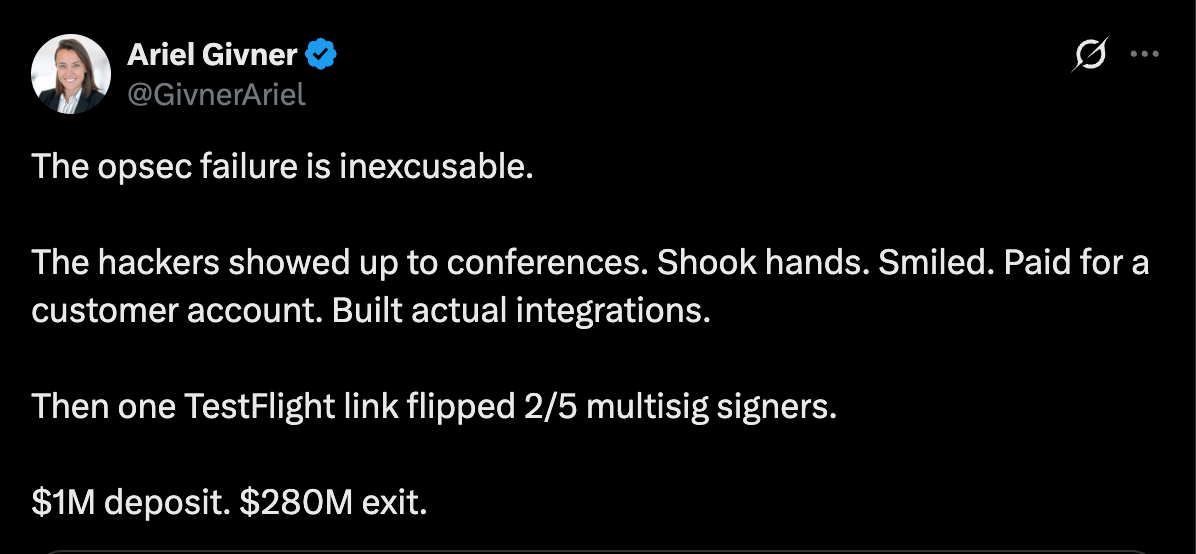

Attorney Ariel Givner described the scenario as a failure to safeguard user funds, saying, “In plain terms, civil negligence means they failed their basic duty to protect the money they were managing.” Her assessment followed Drift’s post-mortem detailing how the attack unfolded and how the platform responded. The comments come as critics question the adequacy of Drift’s procedures in a space where attackers frequently rely on social engineering and supply-chain compromises to breach multi-signature setups and other critical controls.

“Every serious project knows this. Drift didn’t follow it,” she said, adding, “They knew crypto is full of hackers, especially North Korean state teams.” Givner continued, “Yet their team spent months chatting on Telegram, meeting strangers at conferences, opening sketchy code repos, and downloading fake apps on devices tied to multisignature controls.”

The debate underscores a larger concern: social engineering and project infiltration remain among the most effective attack vectors in crypto, capable of draining user funds and eroding trust in platforms that users otherwise rely on for high-stakes liquidity and yield opportunities.

Key takeaways

- Drift Protocol is facing scrutiny over basic security practices after a $280 million exploit, with legal perspectives labeling the incident as civil negligence in light of alleged operational shortfalls.

- Experts point to missteps such as storing signing keys on non-air-gapped systems and insufficient vendor and developer due diligence, particularly with personnel encountered at conferences.

- The attackers’ approach reportedly involved months of planning, culminating in targeted social engineering and malware introduced through developer machines.

- There are signals of a possible link to North Korea–aligned threat actors, with Drift stating a “medium-high confidence” that the same group behind the Radiant Capital hack (October 2024) was involved.

- Radiant Capital’s 2024 incident has become part of the narrative tying industry-wide risks to well-known escalation patterns in state-sponsored cyber operations.

Attack narrative and defensive lessons

Drift Protocol published an update detailing how the breach unfolded, asserting that the assault was the product of six months of planning. The attackers reportedly approached Drift at a major crypto industry conference in October 2025, signaling interest in potential integrations and partnerships. Over the following months, the bad actors cultivated relationships with Drift developers, ultimately delivering malicious links and embedding malware that compromised the developers’ machines used to manage the protocol’s multisignature controls.

Drift’s account emphasizes that those involved were not North Korean nationals, though the firm conceded that the threat actors were linked to a broader pattern associated with state-backed cyber campaigns. In a contemporaneous assessment with “medium-high confidence,” Drift tied the incident to actors believed to have previously orchestrated the October 2024 Radiant Capital hack. Radiant Capital had disclosed that its breach involved malware spread via Telegram from an operator posing as an ex-contractor connected to North Korea. While Drift’s update stops short of confirming a direct line of responsibility, these correlations highlight a persistent threat environment in which sophisticated adversaries leverage social channels to compromise engineering workflows.

Legal and security observers highlight a recurring theme: even mature crypto teams can underestimate the risk of supply-chain and social-engineering exploits if governance practices do not enforce strict separation between development activities and sensitive credentials. Givner’s critique goes beyond the specifics of Drift’s incident, pointing to a universal expectation that “air-gapped” signing keys should be kept separate from day-to-day developer work, and that engaging with third-party developers or contractors requires rigorous vetting and ongoing due diligence. In her words, many projects already adhere to these principles because the crypto landscape is “full of hackers,” and a lapse can be costly both financially and reputationally.

Industry context: echoes of a broader security paradigm

The Drift incident arrives as a broader discussion unfolds about how DeFi projects manage risk in a period of heightened adversarial activity. Social engineering, phishing, and malware campaigns targeting developer ecosystems have been repeatedly implicated in high-profile hacks. The Radiant Capital case from late 2024, which involved a North Korea–linked operator impersonating an ex-contractor to disseminate malware, is frequently cited in security analyses as a cautionary tale about the limits of conventional defensive measures when human factors become the weakest link.

Industry observers note that the Drift episode reinforces the need for robust governance frameworks around key management, formal vendor assessment processes, and stringent controls on how and where signing keys are stored and used. If the attackers exploited trusted relationships with developers and relied on compromised devices to gain access to multisignature controls, the path to remediation likely involves reinforcing air gaps, implementing hardware security modules for key management, and institutionalizing continuous monitoring and key rotation practices. The emphasis on “due diligence” also raises questions about how conferences, hackathons, and third-party collaborations are vetted, and whether drift toward more rigorous third-party risk management will become standard practice across the sector.

What this means for investors and builders

For investors, the Drift incident is a reminder that risk management remains a primary driver of platform credibility and capital allocation in DeFi. Projects that can demonstrate resilient onboarding, robust key management, and rigorous vendor scrutiny may distinguish themselves in a market where security shocks can quickly alter perceptions of value and reliability. Builders, in turn, face a delicate trade-off between openness and security. While collaboration and rapid integration are hallmarks of DeFi innovation, the Drift episode suggests that even well-resourced teams must normalize security drills, red-teaming, and clear separation of duties to prevent supply-chain breaches from translating into user losses.

As regulators and industry groups debate standardized best practices, Drift’s experience could accelerate conversations about mandatory security benchmarks for on-chain protocols, particularly those relying on multi-party computation and multisignature frameworks. In the meantime, users should monitor how Drift and similar platforms respond—through security upgrades, partner vetting, and transparent post-incident reporting—as a practical barometer for the sector’s willingness to translate rhetoric about security into measurable safeguards.

Meanwhile, Drift has not publicly detailed its next steps beyond the immediate remediation measures described in its update. The extent to which the platform will overhaul its governance, vendor risk management, and incident response cadence remains to be seen, as does the broader industry adoption of stricter security controls that could alter how quickly and fluidly DeFi protocols can operate with external partners.

What remains uncertain is how quickly the market will react to these revelations and whether Trust signals built on vulnerability disclosure will translate into a longer-term commitment by users to platforms that publicly address security gaps. For now, the incident underscores a recurring lesson: in DeFi, the difference between resilience and ruin often hinges on the discipline with which teams implement and enforce fundamental security practices—before a breach, not after.

As the investigation and remediation continue, market watchers will be paying close attention to Drift’s communications, the evolution of industry security standards, and any subsequent movements by competitors to raise the bar for securing developer environments and signing-key management. The path forward for the sector will be shaped by whether this incident catalyzes meaningful adoption of stronger controls and more rigorous third-party risk governance across the ecosystem.

The Ethereum Foundation just staked $93 million worth of ETH in a single day, pushing its total past 69,500 ETH and nearly hitting its 70,000 ETH target. The move shifts the Foundation from selling ETH to earning yield, cutting one of the biggest sources of sell pressure the market has faced for years.

The ethereum price prediction points to solid targets ahead, but Pepeto is the layer that helps regular traders find what big money finds before the crowd gets there. With $8.68 million raised and analysts projecting 100x, the presale shuts once the Binance listing arrives.

The Ethereum Foundation staked 45,034 ETH on April 3 in batches of 2,047 ETH each, bringing its total staked position to roughly $143 million and completing the target it set in February, per CoinDesk. The program is projected to generate $3.9 to $5.4 million in annual yield, replacing the need to sell ETH for operating costs.

The Foundation still holds over 100,000 ETH beyond the staked amount, per Arkham Intelligence. This treasury pivot removes a persistent overhang that weighed on price for years.

Reduced selling pressure lifts the outlook, but the exchange still at presale pricing and set to catch volume when capital flows on chain is where the return math shifts completely before listing.

Where the ETH Targets Meet Presale Returns Before the Final Window Closes

Pepeto

As dormant institutional capital starts moving on chain, the number of new tokens, scams, and opportunities grows faster than any single trader can track. Pepeto was built for exactly this kind of market, and every tool went live before the flood arrived.

With $8.68 million raised at $0.0000001862 and 100x projected by analysts, the case for this exchange being the top presale gets harder to argue against every day. The Binance listing will open full access to the contract scanner that flags dangers before your money moves, PepetoSwap with zero trading costs, and the cross-chain bridge at zero cost.

While institutional moves like the Foundation’s staking unlock dormant capital, Pepeto builds the layer that gives regular traders access to what that capital finds next. Staking at 188% APY grows early positions while stages fill. SolidProof cleared the full codebase, a former Binance executive shaped the tools, and the founder who took the original Pepe token to $11 billion on a 420 trillion supply built the exchange.

The returns that defined past bull runs all started with one choice made during fear, and Pepeto at $0.0000001862 is that choice sitting in front of you while the Binance listing window still holds. Once trading opens, this presale price disappears and daily utility drives consistent value rather than a spike that fades after listing week.

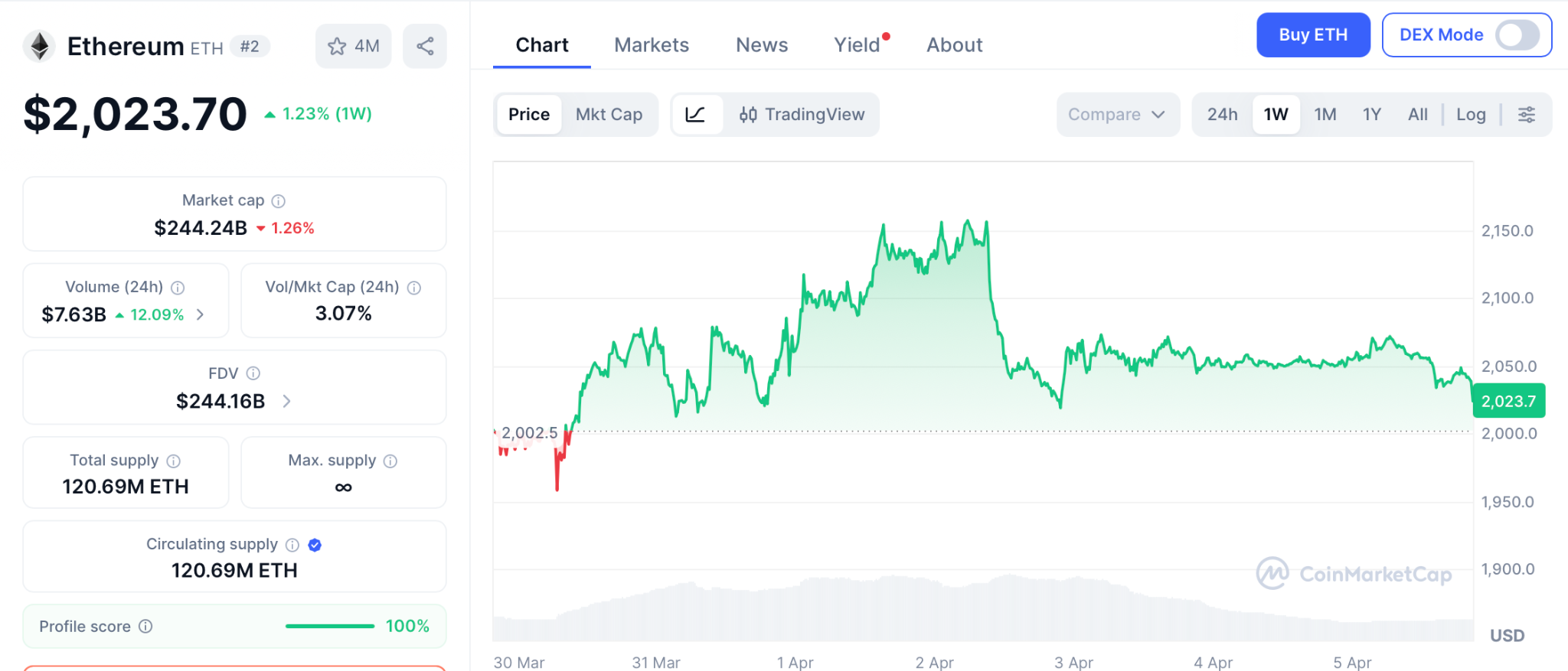

Ethereum Price Prediction: Can ETH Break $2,250 and Reach $3,000?

Ethereum trades near $2,034 as of April 5, sitting 58% below its $4,953 all-time high from August 2025 while the Foundation’s staking move cuts sell pressure, per CoinMarketCap.

The ETH forecast depends on clearing $2,200 to $2,250, which opens $2,500. From there, $3,000 becomes a real target based on historical zones that preceded major runs in past cycles. Standard Chartered holds a $7,500 year-end call, meaning $3,000 sits at the halfway mark and could arrive much sooner if macro conditions improve and the Iran conflict cools.

Support holds at $2,000 with the structure at risk if that level breaks. The ethereum price prediction is strong for patient holders, but the path from $2,034 to $3,000 is a 46% move over months, not the 100x the presale compresses into one listing event.

Conclusion

The Foundation just locked $93 million into staking instead of selling. The ETH outlook firms up as sell pressure drops and infrastructure matures. When that kind of money stays on chain instead of hitting the market, the ceiling lifts for the entire ecosystem.

But the gains that reshape portfolios come from being early in what the market finds after the listing, not from recovery. The founder behind Pepe plus working exchange tools plus a Binance listing is the rarest mix crypto produces. The Pepeto official website is where that entry stays open, and the wallets that caught ETH below $100 in 2019 already know which path they would take again.

Click To Visit Pepeto Website To Enter The Presale

FAQs

Can ETH reach $3,000 based on the ethereum price prediction?

Yes. $3,000 is a 46% gain from current levels and sits halfway to Standard Chartered’s $7,500 target. Realistic if macro eases.

What does the ethereum price prediction reveal about the current market?

ETH holds above $2,000 as the Foundation stops selling and starts staking at Pepeto targets 100x before listing.

What drives Pepeto’s returns beyond the ethereum price prediction?

Five live exchange tools scale with on-chain growth. The Binance listing compresses what months of ETH recovery delivers into one event.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

Harvard economist Kenneth Rogoff believes the Chinese yuan will become a global reserve currency within five years. He argues that President Xi Jinping’s explicit call for yuan internationalization marks a turning point.

Rogoff says investors worldwide are desperate to diversify away from the US dollar, making China’s push well-timed.

China’s Path to Reserve Status

In a recent interview with the South China Morning Post, Rogoff outlined the key steps China must take. Beijing needs to open its government bond markets to foreign investors. It also needs forward markets and interest rate swaps to support international participation.

Rogoff noted that fully open capital markets are not required. The US itself maintained many restrictions on foreign investment through the 1970s. It was still the world’s dominant reserve currency during that period.

China must also build financial rails independent of the SWIFT system. Rogoff said modern blockchain technology can duplicate existing systems at much lower cost. The country’s Cross-border Interbank Payment System already serves as a foundation for this effort.

Crypto’s Role in Dollar Erosion

Rogoff also addressed how cryptocurrencies are reshaping currency competition. He estimated the global underground economy at roughly 20% of total output. That amounts to at least $20 trillion.

Cryptocurrency, particularly stablecoins, has already captured a significant share of illicit transactions. Physical cash once dominated this space. Digital assets now offer faster and harder-to-trace alternatives.

Stablecoins Face Regulatory Reckoning

However, Rogoff warned that crypto will never replace the dollar in the legal economy. Governments have more than enough regulatory power to prevent that outcome.

He criticized the US Genius Act as overly liberal in its stablecoin regulation. Stablecoins remain difficult to trace once they leave their issuer. Rogoff predicted that future rules will eventually mirror central bank digital currency requirements.

The race for currency dominance is accelerating. Both Europe and China are building independent financial systems to reduce vulnerability to US sanctions.

The post Yuan, Not Crypto, Will Challenge Dollar Within 5 Years appeared first on BeInCrypto.

TLDR:

- Coinbase filed a formal SEC submission opposing mandatory issuer approval for third-party stock tokenization on April 1, 2026.

- The filing argues issuer consent mandates contradict Section 4(a)(1) of the Securities Act and decades of SEC legal precedent.

- Coinbase warns that requiring issuer approval could create anticompetitive barriers and push blockchain innovation offshore.

- A flexible dual framework supporting both issuer-led and third-party tokenization would unlock T+0 settlement and 24/7 trading.

Coinbase filed a formal submission with the SEC’s Crypto Task Force on April 1, 2026, addressing third-party tokenization of publicly traded securities.

The document argues against requiring issuer approval for blockchain-based representations of existing stocks. The filing responds to the SEC’s ongoing effort to modernize securities markets through blockchain technology.

Coinbase’s position centers on protecting secondary market activity from unnecessary regulatory barriers.

Coinbase Challenges Issuer Veto Power Over Secondary Markets

The full title of the submission is “Re: Why Third-Party Tokenization of Publicly Traded Securities Should Not Require Issuer Approval.”

Coinbase argues that mandating issuer consent contradicts established U.S. federal securities law. Specifically, the filing references Section 4(a)(1) of the Securities Act, which permits resale without issuer involvement in many secondary-market scenarios.

The company also cited Rule 17Ad-20, which governs transfer agents and secondary market restrictions. Decades of SEC precedent support free transferability of securities in secondary markets. Issuers traditionally hold no veto power over how investors transfer or custody shares after entering public markets.

According to the tweet by @martypartymusic, Coinbase warned that requiring issuer approval would grant companies unprecedented control over lawful secondary-market activity.

This could create anticompetitive barriers and favor incumbent-controlled closed systems. Such a mandate would directly stifle innovation in the tokenization space.

Coinbase further clarified that third-party tokenization does not create a new security. Instead, it represents existing shares on a blockchain while fully preserving shareholder rights, including voting, dividends, and corporate actions.

Flexible Framework Would Support Both Issuer and Third-Party Tokenization

Coinbase advocates for a dual approach that accommodates issuer-led and third-party tokenization simultaneously.

Under this framework, companies could issue their own blockchain versions of shares if they choose. Independent platforms, however, would also be free to create tokenized representations of existing stocks.

The filing points to recent SEC-friendly developments as evidence that issuer consent is unnecessary. Nasdaq’s tokenized trading pilots and the DTCC’s Tokenization Services have both advanced without imposing such requirements. Adding a consent mandate now would represent a reversal of regulatory progress already underway.

A flexible framework, Coinbase argues, would unlock key market efficiencies. These include T+0 instant settlement, 24/7 trading, reduced intermediary costs, greater transparency, and peer-to-peer transfers.

Tokenized stocks could also integrate with decentralized finance protocols while maintaining regulatory compliance.

Coinbase also warned that overly restrictive rules could push blockchain innovation offshore. This would limit the SEC’s ability to oversee markets and gather data for future rulemaking.

The filing ties directly to the SEC’s planned “innovation exemption,” urging that access to it not be unnecessarily restricted.

TLDR:

- Stellar’s open network design attracts broader adoption than XRP’s institution-focused approach.

- XLM demand ties directly to real network activity, giving it stronger organic economic foundations.

- XRP’s legal battles with the SEC have slowed adoption and weakened institutional confidence over time.

- Stellar’s diverse ecosystem, spanning payments, stablecoins, and NGOs, reduces reliance on single partners.

Stellar (XLM) and XRP remain two of the most discussed blockchain payment networks in crypto. Both target cross-border transactions, yet their approaches differ sharply.

Those differences may determine which asset captures greater long-term value. Stellar’s open design, usage-driven tokenomics, and lower regulatory exposure give it structural advantages.

Meanwhile, XRP leans heavily on institutional partnerships and faces ongoing legal scrutiny in key markets.

Open Network Design and Real Usage Demand

Stellar was built to support financial inclusion from the ground up. Anyone — individuals, startups, or institutions — can issue assets and interact freely on its network.

This open access model drives broader adoption compared to XRP’s bank-focused design. The wider a network grows, the more value it tends to attract over time.

XRP, by contrast, targets large financial institutions as its primary users. That focus concentrates value among a limited group of participants.

Open network effects, which Stellar benefits from, tend to compound as more users join. This structural difference matters significantly when measuring long-term growth potential.

Stellar’s tokenomics also tie XLM demand directly to real network activity. Every transaction, account creation, and asset exchange requires XLM, creating consistent organic demand.

XRP often functions as a temporary bridge asset in liquidity operations. Tokens are held only briefly, which weakens sustained structural demand for the asset.

This usage-driven demand model gives Stellar a more reliable economic foundation. As transaction volumes grow on the network, so does the need for XLM.

That relationship between usage and demand is a strong indicator of long-term value retention. Developers and institutions building on Stellar contribute directly to that demand cycle.

Regulatory Environment and Ecosystem Diversity

XRP has faced considerable legal challenges, particularly in the United States. The Ripple lawsuit created uncertainty around market perception, adoption, and liquidity.

Even as some regulatory clarity has emerged, the damage to institutional confidence lingers. Lower legal risk makes an asset more attractive to developers and financial partners.

Stellar has largely avoided such regulatory friction and operates in a more stable environment. The Stellar Development Foundation maintains a relatively neutral governance image.

That neutrality appeals to developers who prioritize decentralization and compliance. It also reduces the kind of institutional hesitation that has slowed XRP’s growth in certain markets.

Beyond regulation, Stellar supports a diverse real-world ecosystem. Its network powers low-cost cross-border payments, stablecoins, and humanitarian finance projects.

NGOs and financial inclusion initiatives in emerging markets actively use the network. This breadth of application reduces dependence on any single sector or partner group.

XRP, while technically efficient, relies more heavily on specific institutional agreements. A concentrated ecosystem carries greater risk if key partnerships shift or dissolve.

Stellar’s multi-sector presence provides a more resilient foundation for sustained network growth. That diversity, combined with lower regulatory pressure, positions XLM as a strong long-term contender.

TLDR:

- Walmart recorded a 66% conversion drop when embedding agentic checkout directly inside ChatGPT’s interface.

- OpenAI phased out Instant Checkout after merchants reported poor results with chatbot-based purchase experiences.

- The Machine Payments Protocol lets AI agents pay via HTTP requests, using cards, wallets, or stablecoins natively.

- Know Your Agent frameworks are now being developed to secure invisible payments before autonomous spending scales further.

Invisible commerce is emerging as the next frontier in AI-driven payments, replacing the checkout model. Walmart recently recorded a 66% drop in conversion rates when embedding agentic checkout inside ChatGPT.

OpenAI subsequently phased out its Instant Checkout feature. These developments signal a major shift. The payments industry built agentic commerce on the wrong foundation.

Agents do not need better checkouts — they need payments that happen automatically, without human intervention.

Walmart’s Checkout Experiment Exposed a Fundamental Flaw

Walmart’s conversion rate collapse was a clear indicator that something was broken. Embedding a human-optimized checkout inside a chatbot created friction rather than reducing it. The process was designed for human eyes, not machine logic.

OpenAI responded by pulling Instant Checkout entirely. Merchants now handle purchases through their own app-based systems instead.

This retreat confirmed what many in the payments space suspected — agentic commerce built on traditional checkout rails does not work.

Fintech analyst Simon Taylor captured this tension clearly. He noted that agentic commerce protocols now outnumber actual agentic transactions.

The infrastructure is ahead of the real-world use case, and the use case itself may have been wrong from the start.

Stripe previously outlined five levels of agentic commerce, borrowing from autonomous driving. Each level still assumed a visible purchase event. Even at the highest level, an agent reacts to human intent. That model is now being questioned.

The Parking Agent Demonstrates a New Payment Paradigm

A hackathon project changed how some in the industry are thinking about this problem. A developer built a parking AI agent that detects a user’s location and pays the local parking authority automatically. No checkout appeared. No purchase intent was required.

The payment happened because an event occurred in the physical world. The agent inferred what was needed and completed the transaction. This is the model that Taylor refers to as invisible commerce.

This approach mirrors how Uber handles payments. A rider exits a vehicle and money moves — no cart, no confirmation screen, no “pay now” button. Uber achieved this by owning both sides of the marketplace. The challenge now is replicating that experience across open agent ecosystems.

Developer Steve Krouse shared a related observation on X, noting that giving agents a USDC wallet produced a genuinely magical product experience. That sentiment reflects growing interest in agent-native payment infrastructure.

Machine Payments Protocol Points Toward Agent-Native Commerce

The Machine Payments Protocol (MPP) launched recently as one attempt to solve this infrastructure gap. It allows agents to initiate payments through a simple HTTP request. The protocol supports credit cards, digital wallets, and stablecoins.

Early use cases include agents purchasing API access, compute resources, stock footage, and real-time data feeds. However, the first viral use case was far simpler. Users had their agents buy them sandwiches, as shared by developer Josh on X, citing MPP and related tools.

Google is also releasing new agentic protocols regularly. X402 is another protocol operating in this space. The competition signals that the market sees real demand for machine-native payment rails.

Security remains an open question. When agents spend autonomously, audit trails become harder to track. Liability for compromised agents is still unresolved. Researchers are now working on Know Your Agent (KYA) frameworks to close that gap before the technology scales further.

Crypto World

Crypto Market Loses $1.5 Trillion in Two Quarters: Is the Worst Still Ahead for Bitcoin?

TLDR:

- Crypto markets shed over $1.5 trillion across Q4 2025 and Q1 2026, with Bitcoin driving nearly 60% of total losses.

- Gold outperformed Bitcoin by nearly 40% in recent months, a strong signal that large capital favors safety over risk assets.

- Bitcoin has traded flat between $65K and $69K for weeks despite rising oil prices and growing geopolitical tensions globally.

- BTC dominance and the gold-to-Bitcoin ratio remain the two most critical metrics to watch for early signs of market recovery.

The crypto market sits at a crossroads as Bitcoin consolidates within a narrow range. Over the past two quarters, digital assets lost over $1.5 trillion in total market value.

Institutional capital has pulled back, and macro forces are weighing on risk appetite. Traders are watching carefully as the market weighs potential recovery against further downside, with conditions outside crypto likely determining the next major move.

Bitcoin’s Recent Losses Point to Broader Institutional Retreat

Bitcoin led the market lower across Q4 2025 and Q1 2026. Combined, those two quarters wiped out roughly 45% in value from the broader market. BTC accounted for nearly 60% of total losses recorded during that period.

That detail changes how analysts read the sell-off. When Bitcoin drives the drawdown, it is not retail traders dumping speculative tokens. It reflects real capital reducing exposure across the entire asset class.

As MR Black noted on X, “When BTC is leading the drawdown, it isn’t a sector rotation. It isn’t retail panic selling memecoins.” That observation carries weight, especially for investors trying to time a re-entry into the market.

Gold’s Outperformance Sends a Clear Risk-Off Signal

The XAU/BTC ratio has shifted nearly 40% in gold’s favor over recent months. Gold offers no yield and carries no technological narrative. Its strength signals that large capital holders are choosing preservation over growth.

That ratio matters because it reflects institutional psychology, not retail sentiment. When the biggest players move into gold, it means confidence in risk assets remains low. Crypto has not yet shown the kind of recovery that would pull that capital back.

However, analysts note that this ratio could become one of the first signs of a turnaround. When it begins reversing, it may indicate that risk appetite is returning and that institutional money is ready to rotate back into Bitcoin.

Sideways Price Action Raises Questions About What Comes Next

Bitcoin has traded between roughly $65,000 and $69,000 for several weeks. That range has held despite rising geopolitical tension, higher oil prices, and growing inflation concerns. Normally, any of those factors would trigger sharp movement in crypto markets.

The muted reaction suggests one of two things. Either the market has already absorbed much of the uncertainty, or it remains so undecided that it needs a strong external trigger to break either way. That ambiguity makes directional calls difficult right now.

BTC dominance remains a key metric to track through this period. When dominance rises, capital clusters in Bitcoin and altcoins suffer.

When it falls, capital rotates into higher-risk assets, and historically that rotation has preceded some of the strongest alt-season runs in a given cycle.

The path forward for crypto depends heavily on macro developments in the coming weeks. If oil cools and geopolitical risks ease, the current consolidation could prove to be a base for recovery.

If conditions worsen, further downside remains possible, with altcoins likely absorbing the most pressure. Traders watching signals beyond the price chart may be better positioned for whatever move comes next.

The hack of the Solana-based decentralized finance (DeFi) platform Drift Protocol could have been prevented if standard operational security procedures were followed by the Drift team, and may constitute “civil negligence,” according to attorney Ariel Givner.

“In plain terms, civil negligence means they failed their basic duty to protect the money they were managing,” Givner said in response to the post-mortem update provided by the Drift team and how it handled Wednesday’s $280 million exploit.

The Drift team failed to follow “basic” security procedures, including keeping signing keys on separate, “air-gapped” systems that are never used for developer work, and conducting due diligence on blockchain developers met through industry conferences.

“Every serious project knows this. Drift didn’t follow it,” she said, adding, “They knew crypto is full of hackers, especially North Korean state teams.” Givner continued:

“Yet their team spent months chatting on Telegram, meeting strangers at conferences, opening sketchy code repos, and downloading fake apps on devices tied to multisignature controls.”

Advertisements for class action lawsuits against Drift Protocol are already circulating, she said. Cointelegraph reached out to the Drift Team but did not receive a response by the time of publication.

The incident is a reminder that social engineering and project infiltration by malicious actors are major attack vectors for cryptocurrency developers that could drain user funds and permanently erode customer trust in compromised platforms.

Related: Drift explains $280M exploit as critics question Circle over USDC freeze

Drift Protocol says attack took “months” of planning

The Drift Protocol team published an update on Saturday outlining how the exploit occurred and claimed that the attackers planned the attack for six months before execution.

Threat actors first approached the Drift team at a “major” crypto industry conference in October 2025, expressing interest in protocol integrations and collaboration.

The malicious actors continued to build rapport with the Drift development team in the ensuing six months, and once enough trust was built, they began sending the Drift team malicious links and embedding malware that compromised developer machines.

These individuals, who are suspected of working for North Korea state-affiliated hackers and physically approached the Drift developers, were not North Korean nationals, according to the Drift team.

Drift said, with “medium-high confidence,” that the exploit was carried out by the same actors behind the October 2024 Radiant Capital hack.

In December 2024, Radiant Capital said the exploit was carried out through malware sent via Telegram from a North Korea-aligned hacker posing as an ex-contractor.

Magazine: Meet the hackers who can help get your crypto life savings back

Asian shares mostly gain while oil prices keep rising

Super Micro Computer: Don't Buy Into Lawsuit (Rating Downgrade)

He’s Had a Few Teeth Pulled

-

NewsBeat3 days ago

NewsBeat3 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business3 days ago

Business3 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread: Spanx – Corporette.com

-

Entertainment7 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Crypto World4 days ago

Crypto World4 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business3 hours ago

Business3 hours agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Crypto World6 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech7 days ago

Tech7 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Sports1 day ago

Sports1 day agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business4 days ago

Business4 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Tech6 days ago

Tech6 days agoApple will hide your email address from apps and websites, but not cops

-

Tech6 days ago

Tech6 days agoEE TV is using AI to help you find something to watch

-

Sports5 days ago

Sports5 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Politics6 days ago

Politics6 days agoShould Trump Be Scared Strait?

-

Tech6 days ago

Tech6 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech6 days ago

Daily Deal: StackSkills Premium Annual Pass

-

Fashion7 days ago

Fashion7 days agoThe Best Spring Trends of 2026

-

Crypto World6 days ago

Crypto World6 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Sports6 days ago

Sports6 days agoWomen’s hockey camp eyes fitness boost, tactics ahead of WC 2026 campaign | Other Sports News

-

Tech6 days ago

Tech6 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

You must be logged in to post a comment Login