Crypto World

Drift Incident Could Constitute Civil Negligence

The Drift Protocol, a Solana-based decentralized finance platform, is drawing renewed scrutiny after a $280 million exploit exposed persistent gaps in its security posture. A post-incident review and commentary from legal counsel frame the breach as something that could have been prevented with basic operational security measures, prompting discussions about civil negligence and the broader risk landscape facing DeFi projects.

Attorney Ariel Givner described the scenario as a failure to safeguard user funds, saying, “In plain terms, civil negligence means they failed their basic duty to protect the money they were managing.” Her assessment followed Drift’s post-mortem detailing how the attack unfolded and how the platform responded. The comments come as critics question the adequacy of Drift’s procedures in a space where attackers frequently rely on social engineering and supply-chain compromises to breach multi-signature setups and other critical controls.

“Every serious project knows this. Drift didn’t follow it,” she said, adding, “They knew crypto is full of hackers, especially North Korean state teams.” Givner continued, “Yet their team spent months chatting on Telegram, meeting strangers at conferences, opening sketchy code repos, and downloading fake apps on devices tied to multisignature controls.”

The debate underscores a larger concern: social engineering and project infiltration remain among the most effective attack vectors in crypto, capable of draining user funds and eroding trust in platforms that users otherwise rely on for high-stakes liquidity and yield opportunities.

Key takeaways

- Drift Protocol is facing scrutiny over basic security practices after a $280 million exploit, with legal perspectives labeling the incident as civil negligence in light of alleged operational shortfalls.

- Experts point to missteps such as storing signing keys on non-air-gapped systems and insufficient vendor and developer due diligence, particularly with personnel encountered at conferences.

- The attackers’ approach reportedly involved months of planning, culminating in targeted social engineering and malware introduced through developer machines.

- There are signals of a possible link to North Korea–aligned threat actors, with Drift stating a “medium-high confidence” that the same group behind the Radiant Capital hack (October 2024) was involved.

- Radiant Capital’s 2024 incident has become part of the narrative tying industry-wide risks to well-known escalation patterns in state-sponsored cyber operations.

Attack narrative and defensive lessons

Drift Protocol published an update detailing how the breach unfolded, asserting that the assault was the product of six months of planning. The attackers reportedly approached Drift at a major crypto industry conference in October 2025, signaling interest in potential integrations and partnerships. Over the following months, the bad actors cultivated relationships with Drift developers, ultimately delivering malicious links and embedding malware that compromised the developers’ machines used to manage the protocol’s multisignature controls.

Drift’s account emphasizes that those involved were not North Korean nationals, though the firm conceded that the threat actors were linked to a broader pattern associated with state-backed cyber campaigns. In a contemporaneous assessment with “medium-high confidence,” Drift tied the incident to actors believed to have previously orchestrated the October 2024 Radiant Capital hack. Radiant Capital had disclosed that its breach involved malware spread via Telegram from an operator posing as an ex-contractor connected to North Korea. While Drift’s update stops short of confirming a direct line of responsibility, these correlations highlight a persistent threat environment in which sophisticated adversaries leverage social channels to compromise engineering workflows.

Legal and security observers highlight a recurring theme: even mature crypto teams can underestimate the risk of supply-chain and social-engineering exploits if governance practices do not enforce strict separation between development activities and sensitive credentials. Givner’s critique goes beyond the specifics of Drift’s incident, pointing to a universal expectation that “air-gapped” signing keys should be kept separate from day-to-day developer work, and that engaging with third-party developers or contractors requires rigorous vetting and ongoing due diligence. In her words, many projects already adhere to these principles because the crypto landscape is “full of hackers,” and a lapse can be costly both financially and reputationally.

Industry context: echoes of a broader security paradigm

The Drift incident arrives as a broader discussion unfolds about how DeFi projects manage risk in a period of heightened adversarial activity. Social engineering, phishing, and malware campaigns targeting developer ecosystems have been repeatedly implicated in high-profile hacks. The Radiant Capital case from late 2024, which involved a North Korea–linked operator impersonating an ex-contractor to disseminate malware, is frequently cited in security analyses as a cautionary tale about the limits of conventional defensive measures when human factors become the weakest link.

Industry observers note that the Drift episode reinforces the need for robust governance frameworks around key management, formal vendor assessment processes, and stringent controls on how and where signing keys are stored and used. If the attackers exploited trusted relationships with developers and relied on compromised devices to gain access to multisignature controls, the path to remediation likely involves reinforcing air gaps, implementing hardware security modules for key management, and institutionalizing continuous monitoring and key rotation practices. The emphasis on “due diligence” also raises questions about how conferences, hackathons, and third-party collaborations are vetted, and whether drift toward more rigorous third-party risk management will become standard practice across the sector.

What this means for investors and builders

For investors, the Drift incident is a reminder that risk management remains a primary driver of platform credibility and capital allocation in DeFi. Projects that can demonstrate resilient onboarding, robust key management, and rigorous vendor scrutiny may distinguish themselves in a market where security shocks can quickly alter perceptions of value and reliability. Builders, in turn, face a delicate trade-off between openness and security. While collaboration and rapid integration are hallmarks of DeFi innovation, the Drift episode suggests that even well-resourced teams must normalize security drills, red-teaming, and clear separation of duties to prevent supply-chain breaches from translating into user losses.

As regulators and industry groups debate standardized best practices, Drift’s experience could accelerate conversations about mandatory security benchmarks for on-chain protocols, particularly those relying on multi-party computation and multisignature frameworks. In the meantime, users should monitor how Drift and similar platforms respond—through security upgrades, partner vetting, and transparent post-incident reporting—as a practical barometer for the sector’s willingness to translate rhetoric about security into measurable safeguards.

Meanwhile, Drift has not publicly detailed its next steps beyond the immediate remediation measures described in its update. The extent to which the platform will overhaul its governance, vendor risk management, and incident response cadence remains to be seen, as does the broader industry adoption of stricter security controls that could alter how quickly and fluidly DeFi protocols can operate with external partners.

What remains uncertain is how quickly the market will react to these revelations and whether Trust signals built on vulnerability disclosure will translate into a longer-term commitment by users to platforms that publicly address security gaps. For now, the incident underscores a recurring lesson: in DeFi, the difference between resilience and ruin often hinges on the discipline with which teams implement and enforce fundamental security practices—before a breach, not after.

As the investigation and remediation continue, market watchers will be paying close attention to Drift’s communications, the evolution of industry security standards, and any subsequent movements by competitors to raise the bar for securing developer environments and signing-key management. The path forward for the sector will be shaped by whether this incident catalyzes meaningful adoption of stronger controls and more rigorous third-party risk governance across the ecosystem.

Crypto World

Could Pepeto Be the Best Crypto to Buy in 2026 While BTC Tests $80K and ETH Holds Above $2,300?

The crypto market just flipped into greed territory for the first time in weeks, and the Fear and Greed Index hitting 60 has every trader asking which token carries the biggest returns from here.

Finding the best crypto to buy in 2026 means looking past coins that already ran and finding entries that still carry distance between where they sit and where they go.

BTC is testing $80,000 with $996 million in weekly ETF inflows, and a presale launched by the mind behind the first Pepe token has gathered more than $9.5 million from wallets that verified the live tools before sending capital.

Bitcoin touched $79,388 on April 22 before pulling back to $77,800 as profit taking hit altcoins harder than the leader.

Weekly ETF inflows reached $996 million with Bitcoin products leading the charge according to 24/7 Wall Street, and growing expectations around the CLARITY Act markup in the Senate added a regulatory tailwind that the market had not priced in.

The rally is real, but the question now is whether the best returns from here come from large caps or from entries that have not hit the open market yet.

Tokens Positioned for the Next Leg of the Recovery

Pepeto

While the market watches BTC test resistance, the best crypto to buy in 2026 might be sitting in a presale most traders have not found yet. Pepeto is a marketplace that turns meme coin trading into a verified ecosystem where every tool runs live and every contract carries a SolidProof audit. It was built by the cofounder who created the original Pepe coin, with 420 trillion supply matching the same token structure that went from zero to billions the first time.

The risk scorer scans contracts for warning signs before capital gets committed, catching scams that move faster than news so the wallet stays protected during fast rotations that follow big BTC moves. PepetoSwap handles zero fee trades across tokens, keeping the full value of each position inside the wallet instead of leaking to platform charges.

178% APY staking layers returns above the presale position, and the expected Binance listing draws closer while that reward compounds. The presale sits at $0.000000186, and more than $9.5 million has been gathered from wallets that ran through the live platform before committing.

The 100x target from one expected Binance debut holds because presale to exchange is the window where every previous crypto fortune started, and the wallets buying now join that group before the crowd pays full price. Visit Pepeto to check the tools live.

Ethereum (ETH)

ETH trades near $2,316 according to CoinMarketCap, holding above $2,300 while BTC leads the rally.

The network still dominates smart contract development with over 31,000 active developers, but ETH needs to reclaim $2,800 before the recovery pattern confirms.

From $2,400 the path to the $4,800 peak is a 2x, solid for a portfolio anchor but far from the multiplier math that presale entries carry ahead of a listing event.

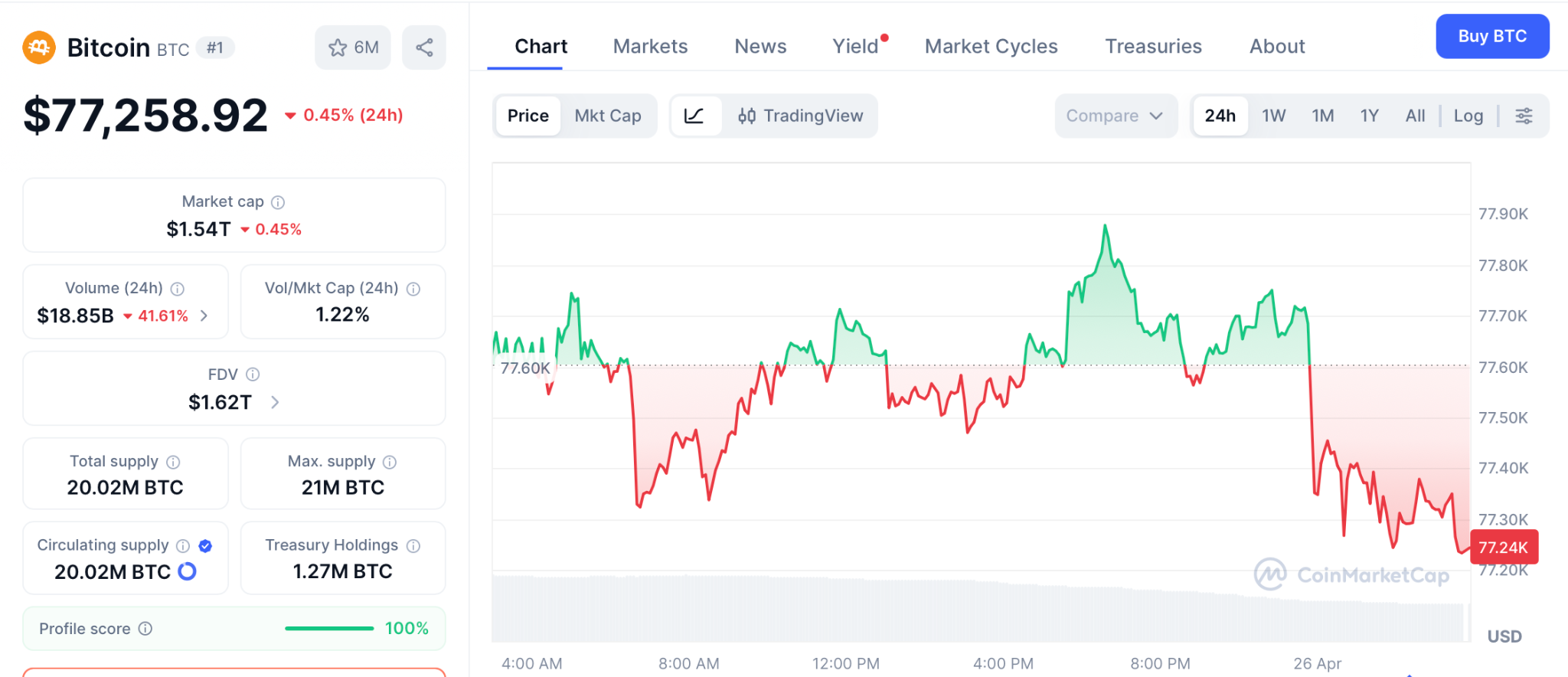

Bitcoin (BTC)

BTC sits near $77,258 according to CoinMarketCap, testing the $80,000 level that has acted as resistance since the pullback from the October 2025 peak of $126,000. Weekly ETF inflows at $996 million show institutional demand is real, and the CLARITY Act could open the door to bigger allocations.

The math from $77,258 to a new high above $126,000 is a 1.6x, strong by traditional standards but modest compared to presale entries that carry 100x projections from a single listing event.

Conclusion

Will BTC break $80,000? The signals point toward higher levels as ETF demand and regulation clarity build across the market. But the signals for Pepeto point at something beyond a market recovery, they point at the same setup that produced every early buyer success story in crypto.

Every cycle creates winners who entered during fear and collected wealth during recovery, and the expected Binance listing will separate the wallets that entered from everyone who reads about them afterward.

Entering the Pepeto official website enow is how those wallets plan to be on the right side of that line when trading opens.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the best crypto to buy in 2026 right now?

BTC and ETH carry strength, but presale entries like Pepeto offer the distance between current price and listing that large caps cannot match.

Why are traders choosing Pepeto over large caps?

A SolidProof audit, zero fee trading, and an expected Binance listing at presale pricing explain why more than $9.5 million entered the Pepeto official website.

Will BTC reach $100,000 this year?

That is a real possibility if ETF inflows continue and the CLARITY Act passes, but the timeline depends on broader market conditions.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

The Ethereum Foundation has moved to unwind part of its staking position shortly after nearing its stated goal of 70,000 staked ETH.

On Saturday, the Ethereum Foundation unstaked 17,035.326 ETH, worth roughly $40 million, according to Arkham data. The move involved depositing wrapped staked ETH (wstETH) into Lido’s unstETH contract, with ETH expected to be returned once the withdrawal queue completes.

In Ethereum, unstaking is the process of withdrawing ETH that was previously locked to help secure the network through validators. When ETH is staked, it’s deposited into the Ethereum Beacon Chain, where it remains locked while earning rewards. To unstake, a withdrawal request is initiated, and the funds enter a queue period after which the funds are released.

The Ethereum Foundation has not yet revealed why it unstaked 17,000 ETH, prompting some users to speculate it could be preparing to sell. “The biggest seller of ETH continues to be the people who created ETH,” one user wrote.

Related: Another DeFi protocol hacked as Sui-based Volo hit by $3.5M exploit

Ethereum Foundation nears 70K staked ETH goal

The EF started staking ETH after updating its policy in June 2025. At the time, the foundation said that staking and decentralized finance participation would help fund protocol research, development and ecosystem grants.

Since February, the foundation has steadily expanded its position, staking 2,016 ETH initially, followed by 22,517 ETH in March. Earlier this month, the foundation staked more than 45,000 ETH in a series of transactions, bringing the total to around 69,500 ETH, just shy of its internal 70,000 ETH staking target.

However, concerns remain over governance risks. Ethereum co-founder Vitalik Buterin has cautioned that large-scale staking by the foundation could complicate neutrality during potential contentious hard forks, where competing chains may emerge.

Related: Ethereum Risks 10% Dip Versus Bitcoin Despite ETH Staking Milestone

DeFi protocols unite to back rsETH

As Cointelegraph reported, decentralized finance protocols have joined forces to stabilize rsETH after a $293 million exploit on the Kelp restaking platform triggered market disruption. The incident involved hackers stealing over 116,000 restaked ETH tokens and using them as collateral to borrow funds, leaving roughly $195 million in bad debt on Aave and straining the broader DeFi lending market.

Backers have pledged over 43,500 ETH (around $101 million) in a coordinated “DeFi United” effort led by Aave, with participation from Lido DAO, Golem Foundation and major contributions from EtherFi Foundation and Mantle.

Magazine: Ethereum’s Fusaka fork explained for dummies: What the hell is PeerDAS?

TLDR:

- Open Interest spiked sharply in April, signaling crowded and unstable positioning across Bitcoin derivatives markets.

- Negative funding rates during the rally confirm shorts are being squeezed out, not that bulls are leading organically.

- Perp CVD is rising while Spot CVD stays flat, proving the current move lacks genuine spot market buying support.

- Bitcoin must hold above $80,000 to target $85,000 — a breakdown below that level reopens significant downside pressure.

Bitcoin short squeeze activity is currently driving prices higher in the cryptocurrency market. The Consumer Price Index rose again recently, pointing to sticky inflation that shows no clear resolution.

Despite this, Bitcoin is pushing into a key resistance zone. Analysts note this is not a one-way market. Mixed scenarios and liquidity moves are expected as conflicting signals continue to play out across the market.

Open Interest Spike Points to Crowded and Fragile Market Conditions

Open Interest in Bitcoin’s derivatives market spiked sharply during April. Market analyst Boris of @Fundingvest described the rapid buildup as aggressive and unhealthy positioning.

Such a surge indicates that positions are becoming deeply crowded. This overcrowding makes the current price move unstable and exposed to sudden and sharp reversals.

After the OI spike, funding rates remained negative even as prices climbed. Negative funding during a price rally is a direct indication of crowded short positioning.

In response, the market pushed prices higher, forcing short sellers to cover their positions. This pattern reflects a textbook short squeeze playing out within the derivatives segment.

Meanwhile, Perpetual CVD has been driving prices higher throughout this period. Spot CVD, however, remained largely flat during the same time frame.

Boris pointed out that this divergence makes the analysis straightforward. The current rally is derivative-driven and lacks support from genuine spot market buying activity.

Without spot market backing, the sustainability of this rally remains questionable. Price increases unsupported by spot buyers tend to be temporary. The liquidity built through the short squeeze may later be used against new long positions. This sets up the next key risk forming in the market.

Long Trap Risk Builds as Shorts Exit and New Longs Enter

As shorts exit under pressure, longs are now beginning to take their place. Boris flagged this transition as a possible setup for a long trap in the coming weeks.

A long trap forms when buyers enter aggressively near highs, only to face a sharp reversal. This cycle is a recurring pattern in Bitcoin’s derivatives-driven market.

Bitcoin’s price structure is also forming a minor Higher High and Higher Low sequence. On the surface, this HH-HL pattern carries a mild bullish reading.

However, Boris outlined two clear scenarios based on where price holds from here. A failure to maintain above $80,000 would open the door to further downside pressure.

Conversely, holding above $80,000 could push Bitcoin toward the next target near $85,000. The $80K level is therefore acting as the market’s key line in the sand.

Traders monitoring this structure will seek confirmation of either a breakdown or continuation. The outcome around this price level may define Bitcoin’s short-term trajectory.

CPI data continues to add uncertainty to an already complicated macro setup. Sticky inflation does not offer a clear directional signal for Bitcoin.

With the current derivatives positioning, the market remains exposed to sharp moves in either direction. Caution and active risk management remain essential for all market participants.

Adam Back, inventor of Hashcash and a pioneering figure in Bitcoin’s early development, has dismantled the new Satoshi Nakamoto documentary by challenging its core technical assumptions about Bitcoin mining patterns and coin ownership.

Back’s detailed response on X points to critical flaws in how the documentary interprets early mining data and the so-called Patoshi pattern used to estimate Satoshi’s holdings.

The Patoshi Pattern Problem

The documentary relies heavily on the Patoshi pattern, a statistical analysis of Bitcoin block timestamps that researchers claim can identify blocks mined by Satoshi. The analysis suggests Satoshi controlled 500,000 to 1 million Bitcoin by mining roughly 20-40% of blocks in Bitcoin’s first year.

Back argues that this analysis is fundamentally unreliable.

“Clearly there were many other miners (60-80% of hashrate or more even in the first year),” Back wrote.

As the Bitcoin network grew and more participants joined, the pattern became increasingly ambiguous and impossible to verify with certainty.

It has been suggested that as miner participation increased over time, attribution became increasingly unclear, with the Patoshi pattern potentially blending into background noise. This implies the documentary may overstate how precisely early mining activity can be linked to specific actors.

The Flawed “Never Sold” Assumption About Satoshi

The documentary’s central claim rests on the assumption that Satoshi never sold a single Bitcoin, which they argue proves the creator is dead.

This narrative hinges on the belief that a living Satoshi would have spent or sold coins given the extraordinary price appreciation from $0 to $100,000 per Bitcoin.

Back challenges this logic directly. He questions whether the Patoshi pattern can actually prove that Satoshi holds all those coins unsold. Even if the pattern correctly identifies Satoshi’s early mining, it does not prove that those specific coins remain untouched.

“If Satoshi sold any, he could have sold from more recent, more ambiguous coins first,” Back argued.

In other words, Satoshi could have strategically liquidated coins from the ambiguous later mining period when the Patoshi pattern becomes unreliable, and attribution becomes impossible.

Timeline Inconsistencies and Technical Flaws

Back also flagged the documentary’s sloppy handling of timeline evidence. He referenced earlier work by Jameson Lopp showing that Hal Finney was running a marathon at the exact moment Satoshi was sending test transactions on the Bitcoin network, a direct contradiction that disqualifies Finney from the theory.

Back described the documentary’s approach as suffering from “Gell-Mann amnesia,” a term referring to the tendency to dismiss contradictory evidence that emerges after an initial theory is proposed. When the Finney timeline objection was raised, the filmmakers simply shifted their claim to include Len Sassaman without addressing why their original evidence failed.

Additionally, the documentary dismisses EU timezone residents based on forum post analysis, then later pivots to naming Sassaman despite these timezone inconsistencies, Back noted.

This pattern suggests the documentary started with a conclusion. It then worked backward to find supporting evidence rather than following evidence to a conclusion.

The C++ and Windows Problems

Back also highlighted the devastating objection raised by Cam and Len Sassaman’s widow. Sassaman did not know C++ and had never owned a Windows machine. Bitcoin’s original code is written in C++, creating a critical technical barrier.

Additionally, Sassaman was a vocal Bitcoin critic during his lifetime, making his secret role as co-creator highly implausible.

What This Means for the Satoshi Mystery

Back’s analysis does not definitively solve the Satoshi mystery, but it does demolish the documentary’s theory piece by piece. His core argument is that early Bitcoin mining data is too ambiguous. The “never sold coins” assumption is unfounded. It cannot support firm conclusions about Satoshi’s identity.

The debate reveals how difficult it is to prove Satoshi’s identity solely through technical forensics. Even the most sophisticated pattern analysis loses precision over time as the number of network participants grows and mining becomes more distributed.

Other candidates, like Nick Szabo, gained renewed discussion following the documentary’s failure. Some researchers suggest the mystery may never be solved unless Satoshi voluntarily reveals themselves or new evidence surfaces.

The post Adam Back Challenges the Biggest Claim About Satoshi’s Bitcoin Holdings appeared first on BeInCrypto.

The Ethereum Foundation has unstaked 17,035.326 ETH, worth about $40 million, shortly after moving close to its 70,000 ETH staking target.

Summary

- Ethereum Foundation unstaked 17,035 ETH worth $40 million after nearing its 70,000 ETH staking target.

- The foundation deposited wstETH into Lido’s unstETH contract and awaits ETH after withdrawal queue completion.

- Market users questioned a possible sale, but the foundation has not explained the transaction yet.

Arkham data showed the transaction on Saturday. The foundation deposited wrapped staked ETH into Lido’s unstETH contract. The ETH will return after the withdrawal queue completes, based on Ethereum’s normal unstaking process.

The Ethereum Foundation began staking ETH after changing its policy in June 2025. The group said staking and DeFi activity would help fund protocol research, development, and ecosystem grants.

Since February, the foundation has increased its staked ETH balance. It started with 2,016 ETH, added 22,517 ETH in March, and later staked more than 45,000 ETH this month.

Those transactions lifted its total staked ETH to about 69,500 ETH. The figure placed the foundation close to its stated 70,000 ETH staking goal before the latest withdrawal.

Unstaking raises market questions

The Ethereum Foundation has not explained why it unstaked over 17,000 ETH. The lack of a public reason led some market users to question whether the ETH could move to exchanges or be sold.

One user wrote, “The biggest seller of ETH continues to be the people who created ETH.” The comment reflected market concern, though no official statement has linked the unstaking move to a sale.

In Ethereum, staking locks ETH to help secure the network through validators. Unstaking starts a withdrawal request, places funds in a queue, and releases ETH after the waiting period ends.

DeFi recovery efforts continue after rsETH exploit

The move also comes as DeFi protocols work to support rsETH after a large Kelp restaking exploit. The incident involved more than 116,000 restaked ETH tokens and left bad debt across lending markets.

Aave has led a DeFi United recovery effort with support from Lido DAO, Golem Foundation, EtherFi Foundation, and Mantle. Backers have pledged more than 43,500 ETH, worth about $101 million, to help stabilize rsETH.

Ethereum co-founder Vitalik Buterin has also warned about risks tied to large foundation staking. He said heavy staking by the foundation could create governance concerns during disputed hard forks.

TLDR:

- Bitcoin surged to $79,447 on April 22 as futures Open Interest expanded by nearly $3 billion.

- Spot Bitcoin ETFs recorded a net outflow of $1.845 billion on the same day BTC hit its peak.

- Open Interest fell from $27.56B to $25.26B between April 22 and 24, confirming position unwinding.

- Dual pressure from spot ETF outflows and futures closures explains why Bitcoin stalled at $79,447.

Bitcoin’s April 22 price surge to nearly $79,447 has drawn renewed scrutiny from on-chain analysts. Data reviewed by CryptoQuant verified analyst Carmelo Alemán points to futures market activity, not spot buying, as the primary driver of the move.

Spot Bitcoin ETFs recorded a net outflow of $1.845 billion on the same day prices peaked. The pattern challenges the narrative that institutional spot demand powered the rally.

Futures Expansion Drove Bitcoin’s Short Squeeze Above $79,000

Open Interest in Bitcoin futures expanded by nearly $3 billion on April 22. That expansion preceded the intraday high of $79,447 recorded that day.

Analysts often associate large OI increases with aggressive positioning in derivatives markets. In this case, the data points to a short squeeze as the mechanism behind the price move.

A short squeeze occurs when rising prices force traders holding short positions to close them. That closing process generates additional buying pressure, pushing prices even higher.

However, this type of rally lacks the organic demand needed to sustain the move. Without spot buyers absorbing supply, the price eventually loses momentum.

The ETF outflow figure of $1.845 billion on April 22 adds weight to that reading. Institutional money was not flowing into spot Bitcoin products during the rally.

Instead, capital was moving out of those vehicles at a notable pace. That divergence between futures activity and spot flows is a critical detail in understanding the move.

Alemán’s analysis concludes that the rally was led by derivatives, not by underlying spot demand. The timing of the ETF outflows, occurring near the peak of the move, further supports that conclusion. The combination of futures-driven price action and simultaneous spot selling created a fragile top.

Open Interest Decline After April 22 Confirmed Position Unwinding

After Bitcoin peaked, Open Interest began to fall sharply in the sessions that followed. OI dropped from $27.56 billion on April 22 to $26.10 billion on April 23, a reduction of $1.46 billion.

It then fell again to $25.26 billion by April 24, shedding another $839 million. Price followed that decline, moving toward the $77,400 area.

By April 25, OI had only decreased by around $230 million, and price movement was minimal. The largest price drops matched the periods of heaviest futures unwinding. That correlation reinforces the view that derivatives positioning was central to the move in both directions.

The dual pressure of spot ETF outflows and futures position closures explains why Bitcoin failed to hold above $79,447. Neither force was acting in isolation. Together, they removed the buying support needed to sustain the rally.

The data available through April 25 remained incomplete, though the trend was already clear. The sequence, futures expansion, short squeeze, ETF outflows, then OI contraction, tells a consistent story. Bitcoin’s April rally was a derivatives event, not a spot-driven breakout.

Crypto World

Coinbase’s John D’Agostino says crypto platform stands alone as industry’s full-service prime broker

Coinbase (COIN) has quietly crossed a threshold that Wall Street would recognize immediately: it has become, by its own definition, the only full-service prime brokerage in crypto.

John D’Agostino, head of strategy at Coinbase Institutional, said the definition of a prime broker still follows a familiar Wall Street checklist: trading, custody, financing, derivatives and cross-margining. In crypto, he added, there’s an extra layer, staking. “If you can do all of those at scale, you’re a prime,” he said.

In equities and fixed income, only a handful of firms, Goldman Sachs (GS), Morgan Stanley (MS) and Bank of America (BAC), truly qualify as full-service primes, D’Agostino said. Smaller brokers can support funds, but they don’t offer the full stack. “A $100 million hedge fund isn’t getting everything from the top tier. They’re piecing it together,” he said. “The big primes do everything.”

Crypto, until recently, worked the same way, just more fragmented. Funds stitched together custody from one provider, derivatives from another, financing elsewhere. “You can synthetically replicate a prime by patching services together,” D’Agostino said. “But Coinbase is the only one doing all of it natively.”

Coinbase is the largest U.S.-based cryptocurrency exchange and a major provider of infrastructure for institutional investors, offering trading, custody and financing services through its Coinbase Institutional unit.

Its flagship platform, Coinbase Prime, bundles these functions into a single system, allowing hedge funds and asset managers to trade, store and finance digital assets under one roof. Prime holds over $350 billion in assets under custody, about 12% of the total crypto market cap, and serves as custodian for more than 80% of U.S. bitcoin and ether ETF assets.

The firm has become a key bridge between traditional finance and crypto markets, serving as custodian for a significant share of U.S. bitcoin and ether (ETH) exchange-traded fund (ETF) assets and operating under a growing regulatory framework, including oversight from New York regulators

Crypto prime brokers provide institutional clients with a bundled suite of services designed to mirror traditional offerings in markets like equities and FX. They help funds manage counterparty risk and access liquidity across fragmented venues. Prominent players include Coinbase Prime, Galaxy Digital (GLXY), FalconX and Anchorage Digital.

Cross-margining

The final piece fell into place in March with the rollout of cross-margining between spot and derivatives positions, allowing market makers and institutional traders to reduce capital requirements by as much as 10% to 20%. “That was the last pillar,” D’Agostino said. “Now we’re a prime by any standard, substitute crypto for any asset class.”

Coinbase’s institutional platform processes roughly $236 billion in quarterly trading volume and supports more than 470 assets across 20-plus blockchains.

Beyond trading and custody, Coinbase runs a $1 billion lending book and what D’Agostino describes as the industry’s largest listed derivatives footprint through its Deribit integration. Its staking business spans 10 to 20 tokens at institutional scale, including dedicated products through Coinbase Asset Management.

“Those are the core components. There are firms doing well in custody, others in derivatives, others in lending,” he said. “No one is solving all of those problems in one place.”

That gap has persisted in part because of crypto’s relative size. At roughly 3% to 5% of global equities and fixed income markets, it remains too small for major banks to fully commit.

D’Agostino instead expects banks and incumbents to partner. “Buy, build or rent,” he said. “Banks will rent. It’s cheaper and smarter to rent the best brand than build a so-so version.”

Longer term, that calculus could change if crypto grows to 20% or 30% of global markets. “Then you’ll see full-scale competition,” D’Agostino said. “But that’s years away.”

For now, the bigger threat isn’t Wall Street, it’s startups. “I’m less concerned about JPMorgan than I am about the next Brian Armstrong,” he added.

Read more: Coinbase, Bybit said to be working together on tokenization, custody and distribution of U.S. stocks

The US CLARITY Act, a cornerstone proposal aimed at delivering regulatory clarity for the crypto industry, appears poised for finalization in May, according to Galaxy Digital CEO Mike Novogratz. In a SkyBridge Capital podcast with Anthony Scaramucci, Novogratz forecast that the bill would move to the committee in the first week of May and could reach the president’s desk for signing as soon as June, signaling a potential climate shift for US crypto policy. He stressed that bipartisan consensus is crucial for sustaining American innovation in finance and technology.

The forecast comes amid a thinner-than-expected week for crypto legislation in Congress, as the Senate Banking Committee did not schedule a markup hearing by Friday—crucial momentum that markets had anticipated. Even as the timetable remains uncertain, Novogratz argued that the CLARITY Act would unlock new pathways for institutional participation, including tokenizing and selling major U.S. entities to global investors.

Key takeaways

- May emergence: Galaxy Digital’s Mike Novogratz forecasts the CLARITY Act’s finalization in May, with a potential June signing, hinging on committee action and bipartisan alignment.

- Tokenization promise: The bill is framed as enabling the tokenization of large institutions—an idea Novogratz says could broaden access to global markets for US-based assets.

- Current friction: The Senate Banking Committee did not hold a markup as expected, underscoring ongoing negotiations and political headwinds that could affect timing.

- Backstop from lawmakers: Senator Cynthia Lummis warned that the window to pass the CLARITY Act may be narrowing, framing it as a critical juncture for America’s financial future.

The CLARITY Act in a moment of regulatory tension

Novogratz’ outlook reflects a broader market longing for clarity after years of regulatory ambiguity that contributed to some crypto firms relocating operations abroad during the prior administration. He argued that the CLARITY Act’s passage would be a watershed, not only for crypto markets but for broader innovation in the United States. The explicit prospect of tokenizing globally accessible corporate assets—such as SpaceX and Google—could redefine how capital markets allocate risk and reward across borders.

“This phone with a crypto wallet is going to be the way the kid in Bhutan or Batswana or Bolivia or Paraguay, you name it, is participating in the American economy.”

The notion that personal devices could serve as gateways to a broad, tokenized financial system underscores the Act’s potential reach. Still, the road to passage has been far from smooth. The bill previously cleared the House in July 2025 with bipartisan support, raising expectations that a broader consensus might now carry it through Senate deliberations. Yet, disputes over how stablecoins interact with traditional banking—particularly whether yields from stablecoins could erode banks’ competitiveness—have kept the legislation in a gridlock that many market participants find frustrating.

Industry sentiment: timelines and odds

Industry insiders remain divided on the likelihood of timely passage. Galaxy Digital chief of firmwide research Alex Thorn suggested in a social post that the current odds of the CLARITY Act becoming law in 2026 were around 50%. Thorn noted in accompanying commentary that the Senate Banking, Housing, and Urban Affairs Committee was expected to set a markup hearing in the near term, a signal that momentum could resume, though a concrete timetable did not materialize as anticipated. He cautioned that if markup slips past mid-May, the odds of passage could deteriorate appreciably.

The regulatory backdrop remains the primary overhang for the sector. Proponents argue that clear, durable rules would unlock capital access and catalyze domestic innovation, while critics warn of potential risk gaps if the framework does not fully address the evolving realities of digital assets, including stablecoins and tokenized assets. The tension between banking interests and crypto advocates has been a persistent feature of the debate, complicating simple pass/fail predictions for the CLARITY Act.

As part of the broader narrative, investors and builders are watching how the bill’s provisions would interact with existing financial infrastructure. A successful enactment could potentially redraw the map for institutional participation in digital assets and open new funding channels for innovative projects that have faced regulatory hurdles in the current environment. The House’s prior passage in 2025 offered a signal that lawmakers recognize the strategic importance of crypto regulation—yet the Senate pace and its negotiations have so far determined the pace of any final approval.

What changes, what remains uncertain, and what to watch next

The core shift proposed by the CLARITY Act is regulatory clarity—reducing the ambiguity that has long stoked caution among banks, insurers, and asset managers contemplating digital-asset exposure. If enacted, the law could pave the way for more standardized treatment of digital securities, stablecoins, and tokenized equities, while clarifying enforcement expectations for issuers and platforms. That kind of clarity can have a tangible impact on capital formation, product development, and the strategic decisions of large tech and industrial players contemplating tokenized offerings.

At the same time, several critical uncertainties remain. The precise legislative language, the final stance of key committee chairs, and the political dynamics across both parties will shape whether the bill can clear the Senate in 2026. The parallel discussions around stablecoin regulation and the accounting of tokenized assets will also influence how aggressively firms pursue tokenized products once a framework is in place. For investors, the takeaway is not a guaranteed breakthrough but the potential for a meaningful policy inflection that could reorient risk, funding, and growth trajectories in the crypto economy.

Meanwhile, proponents emphasize that the clock is not just about passing a single bill but about signaling to the global market that the United States remains open to responsible innovation. The House’s July 2025 vote underscores a legislative appetite for a credible regulatory path, yet the Senate’s pace underscores how political, regulatory, and industry fault lines can extend timelines. Those dynamics will be crucial as the spring and early summer sessions unfold and the crypto policy discourse moves from committee rooms to a broader national conversation.

What readers should watch next is how the Senate addresses the markup process and whether a bipartisan framework can crystallize around the act’s provisions. If May brings a committee referral followed by timely floor action, the CLARITY Act could emerge as a defining moment for crypto regulation in the United States—one that not only clarifies the rules of the road for digital assets but also shapes the market’s willingness to embrace tokenized capital in the years ahead.

Source tracking and attribution: Statements about timing and committee action reflect remarks attributed to Mike Novogratz on a SkyBridge Capital podcast with Anthony Scaramucci, and the broader timeline context comes from coverage surrounding the bill’s progress, including Lummis’ warning about the window to pass the CLARITY Act and Galaxy Digital’s commentary on the likelihood of a 2026 passage. Past House passage and related industry chatter provide additional context for the current momentum and the anticipated debate in the Senate.

Key Takeaways

- Jane Street generated $39.6B in trading revenue with only 3,500 employees in 2025.

- Legal scrutiny in India and the U.S. challenges Jane Street’s trading practices.

- Crypto market faces stricter transparency and compliance standards

Jane Street Outpaces JPMorgan in Trading Revenue

Jane Street recorded a remarkable $39.6 billion in trading revenue in 2025, surpassing JPMorgan’s $35.8 billion despite operating with only 3,500 employees. By comparison, JPMorgan employs more than 316,000 people globally. The contrast highlights one of the largest productivity gaps in modern finance, with each Jane Street employee generating an estimated $11 million in revenue.

The firm operates as a proprietary trading company, meaning it trades using its own capital rather than managing client funds. Jane Street has built its reputation through market-making activities, particularly in exchange-traded funds and options markets. Reports suggest that 87% of its $662 billion portfolio is tied to options, positioning the firm to benefit heavily from market volatility and rapid trading opportunities.

Market-Making Strategy Raises Regulatory Questions

Jane Street’s success has also attracted growing regulatory attention. In India, the Securities and Exchange Board of India (SEBI) accused the company of manipulating bank stocks and index options during expiry sessions. Authorities reportedly impounded $567 million linked to the alleged activity.

Beyond India, scrutiny has expanded into the crypto sector. Jane Street often acts as a liquidity provider and market maker, roles that give firms visibility into order flow and market behavior. Regulators are increasingly examining whether these informational advantages create unfair trading conditions or allow firms to benefit from early market signals.

Terraform Lawsuit Intensifies Legal Pressure

In the United States, Jane Street is facing allegations tied to the collapse of Terraform Labs and the Terra-Luna ecosystem. A federal complaint claims the firm used non-public information to avoid substantial losses during the stablecoin’s breakdown.

Central to the lawsuit is a narrow 10-minute period in May 2022. Terraform Labs reportedly removed $150 million in TerraUSD liquidity from Curve’s 3pool without public notice. Minutes later, a wallet linked to Jane Street withdrew $85 million, fueling allegations that the company acted on privileged information.

What Comes Next for Crypto Market Makers

The next several months could determine how regulators approach proprietary trading firms in both traditional and crypto markets. A favorable legal outcome for Jane Street may strengthen the argument that firms simply react to public blockchain activity. However, stricter rulings could reshape compliance standards across the industry.

Crypto market makers are already tightening internal controls as regulators focus more closely on liquidity management, insider communication, and order-flow transparency. These developments may mark a turning point for how high-frequency trading firms operate in digital asset markets.

🚨 A FIRM WITH 3,500 EMPLOYEES MADE $39.6 BILLION LAST YEAR AND MOST OF IT CAME FROM MARKETS THEY ARE ALSO ACCUSED OF MANIPULATING : JANE STREET

And they just had their best year ever while facing a market manipulation fine in India and an insider trading lawsuit in the US.… pic.twitter.com/x9CkE2SzDg

— Bull Theory (@BullTheoryio) April 25, 2026

Peter Schiff is warning that MicroStrategy’s Bitcoin-backed yield strategy is heading toward a death spiral, claiming the company’s expanding STRC preferred stock issuance now threatens both MSTR shares and Bitcoin itself.

The economist and longtime Bitcoin (BTC) critic argues that Strategy’s variable 11.5% dividend cannot be funded without selling Bitcoin or attracting an endless stream of new STRC buyers, a setup he calls structurally unstable.

Inside Schiff’s MicroStrategy Thesis

In recent posts on X, Schiff said the gap between Strategy’s Bitcoin holdings and its growing cash obligations defines the danger. Strategy, formerly MicroStrategy, now holds 815,061 BTC after a $2.54 billion purchase on April 20, financed mostly through equity issuance.

Bitcoin produces no native cash flow, while STRC pays a variable 11.5% annualized dividend each month to holders. Schiff says that math eventually forces Strategy into a binary choice.

Either it sells BTC to fund payouts, or it keeps issuing fresh STRC to a shrinking pool of yield buyers.

Why Strategy Must Keep Issuing STRC

STRC has financed roughly 50,792 BTC since launching in July 2025 at a 9% dividend. Seven consecutive monthly increases have lifted the rate to its current 11.5%. Schiff argues that climb proves the model depends on capital raises rather than recurring operations.

Strategy purchased 64,948 BTC in 2026 alone before the latest tranche, tracking far ahead of its historical buying pace. That acceleration depends on capital markets staying open and STRC retaining demand near current yields.

Each fresh STRC issuance compounds the recurring cash burden, raising the share Strategy must cover from external sources. Other analysts have flagged similar concerns about how the security might behave during periods of credit-market stress or rising rates.

What Could Break the Yield Loop

If STRC demand cools, Schiff predicts forced Bitcoin sales would follow, pressuring BTC prices and Strategy’s net asset value. He also notes perpetual preferred dividends carry no firm legal floor, meaning the company could pause payments without triggering a formal default.

Some commentators have separately framed the resulting exposure as a systemic risk for the wider crypto market.

Saylor has repeatedly rejected those framings, citing MSTR’s long-run outperformance and the company’s $42 billion at-the-market program announced in March.

He has also publicly challenged Schiff to debate the STRC structure on his terms. Whether buyers keep absorbing STRC near current yields, and at what dividend level, will largely decide whose framing holds in the coming months.

The post Peter Schiff Warns of a “Death Spiral” in MicroStrategy’s Bitcoin Strategy appeared first on BeInCrypto.

Waller one group one from 200 after 2026 Adelaide Oaks success with Panova

This Tesla Model Y Feature Got One Unlucky Driver Pulled Over

Why People are Shifting to Crypto Trading?

Manchester United reach agreement with Casemiro over contract clause amid transfer speculation

US brings back mandatory military draft registration

Steven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business7 days ago

Business7 days agoPowerball Result April 18, 2026: No Jackpot Winner in Powerball Draw: $75 Million Rolls Over

-

Fashion2 days ago

Fashion2 days agoWeekend Open Thread – Corporette.com

-

Entertainment7 days ago

NBA Analyst Charles Barkley Chimes in on Ice Spice McDonald’s Fiasco

-

Crypto World18 hours ago

Hyperliquid $HYPE Rally Builds Momentum as AI Sector Enters Prove-It Phase

-

Politics6 days ago

Politics6 days agoGary Stevenson delivers timely reminder to register to vote as deadline TODAY

-

Crypto World6 days ago

Bank of Hawai’i (BOH) Q1 2026: Net Income Drops to $57.4M as Net Interest Margin Expands

-

Politics4 days ago

Politics4 days agoMaking troops accountable for war crimes threatens US alliance, ex-SAS colonel warns

-

Politics4 days ago

Politics4 days agoDisabled people challenge government SEND proposals over segregation concerns

-

Business4 days ago

Business4 days agoRolls-Royce Voted UK’s Most Iconic Trade Mark as IPO Register Hits 150

-

Politics4 days ago

Politics4 days agoZack Polanski responds to home secretary’s taser threat

-

Politics4 days ago

Politics4 days agoStarmer handler McSweeney to be dragged from shadows by Foreign Affairs Committee

-

Politics4 days ago

Wings Over Scotland | How To Get Away With Crimes

-

Crypto World5 days ago

Crypto World5 days agoFive Value Stocks with Recovery Potential in 2026: PayPal (PYPL), Nike (NKE), and More

-

Crypto World5 days ago

Crypto World5 days agoNew York sues Coinbase, Gemini over prediction market offerings

-

Politics4 days ago

Politics4 days ago‘Iran is still a nuclear threat’

-

Sports3 days ago

Sports3 days agoTim Bradley names the current best in the world: “Better than Inoue and Usyk”

-

Business4 days ago

Business4 days agoHCL Tech share price tank over 9% after weak Q4. JPMorgan, HSBC & 3 others cut target price

-

Crypto World5 days ago

Crypto World5 days agoCrypto’s great hope in Senate’s Clarity Act still has a path to survive tight calendar

-

NewsBeat4 hours ago

NewsBeat4 hours agoLK Bennett closes all stores after entering administration

-

Business4 days ago

Business4 days agoThe Job Benefits Most Men Don’t Know to Negotiate

You must be logged in to post a comment Login