Crypto World

Fed, FDIC, OCC Clear Tokenized Assets for Bank Balance Sheets

TLDR:

- The Fed, OCC, and FDIC confirmed tokenized securities get identical capital treatment to traditional assets at U.S. banks.

- Banks can now use tokenized stocks and bonds as loan collateral under the same rules as conventional securities.

- The guidance covers both public blockchains like Ethereum and private permissioned networks without distinction.

- Derivatives tied to tokenized assets also receive standard regulatory treatment, expanding the scope significantly.

U.S. banking regulators have issued landmark joint guidance clearing banks to hold tokenized securities under the same rules as conventional financial assets.

The Federal Reserve, Office of the Comptroller of the Currency, and Federal Deposit Insurance Corporation released the coordinated announcement together.

It confirms that a tokenized stock, bond, or other asset carries identical capital treatment to its off-chain equivalent. The move removes a regulatory barrier that major financial institutions had cited for years as a reason to stay off blockchain rails.

Banks Can Now Use Tokenized Assets as Standard Collateral

The guidance covers three core operational changes for U.S. banks.

First, tokenized securities are now eligible collateral for loans, treated identically to traditional stocks or bonds. Second, the rules apply regardless of whether the token sits on a public blockchain like Ethereum or a private permissioned network.

Third, financial derivatives linked to tokenized assets receive the same treatment as conventional derivatives.

That last point carries significant weight. Derivatives markets dwarf spot markets in volume. Extending identical regulatory treatment to tokenized derivatives opens a much larger surface area for blockchain adoption.

The announcement does not require new legislation. It is guidance, meaning banks can act on it immediately. No waiting period applies.

For institutions like JPMorgan, Goldman Sachs, and Bank of America, the obstacle was never technological.

According to posts on X, including commentary from @BullTheoryio and @markchadwickx, major banks were awaiting exactly this kind of regulatory clarity before moving capital onto blockchain infrastructure.

Tokenization Market Stands to Absorb Trillions in Traditional Capital

The addressable pool of assets is enormous. Global equity markets alone exceed $100 trillion. Bond markets add tens of trillions more.

Real estate sits on top of that. Most of that capital has remained off-chain, not due to technical limitations, but due to unresolved regulatory questions around how tokenized versions would be treated on bank balance sheets.

That question now has a clear answer. A tokenized Apple share carries the same legal claim, the same ownership rights, and the same balance sheet weight as a traditional share. Regulators have confirmed this directly.

The practical effect is that banks can begin integrating tokenized securities into existing workflows without restructuring their risk or compliance frameworks. This lowers the operational cost of adoption substantially.

Public blockchains are specifically included in the guidance. That detail matters. Many institutions assumed regulators would favor private, permissioned networks.

The explicit inclusion of public chains broadens the infrastructure eligible to handle institutional-grade asset flows

Investment bank Morgan Stanley is seeking to launch its spot Bitcoin exchange-traded fund at a 0.14% fee, which would make it the cheapest in the US market and potentially force rivals to cut fees to stay competitive.

The 0.14% fee, proposed in Morgan Stanley’s latest S-1 registration statement on Friday, would be one basis point below the Grayscale Bitcoin Mini Trust ETF (BTC), currently the cheapest in the US market, and 11 basis points below the BlackRock-issued iShares Bitcoin Trust ETF (IBIT).

“Big move here. They are not messing around,” Bloomberg ETF analyst James Seyffart said, predicting that the Morgan Stanley Bitcoin Trust (MSBT) is “likely to launch in early April.”

Fellow Bloomberg ETF analyst Eric Balchunas said the low fee means that none of Morgan Stanley’s roughly 16,000 financial advisors — which manage $6.2 trillion in client assets — would feel conflicted in recommending the product to its clients.

Given that spot Bitcoin ETFs track the price movements of Bitcoin (BTC), Morgan Stanley’s ultra-low fee could spark a fresh fee war in the $83 billion market, putting immediate pressure on rivals to cut costs or risk losing assets.

Regulatory approval would make Morgan Stanley the first bank to issue a spot Bitcoin ETF, expanding access to Bitcoin exposure for millions of its high-net-worth clients.

“They are the ultimate gatekeepers of rich boomer money,” Balchunas added.

Morgan Stanley previously selected Coinbase and Bank of New York Mellon as the proposed custodians for its Bitcoin ETF.

Morgan Stanley seeking suite of crypto ETFs, banking charter

Morgan Stanley, previously one of the more crypto-hesitant Wall Street firms, filed for the spot Bitcoin ETF in the first week of January, along with a Solana (SOL) ETF.

Related: Bitcoin traders see 53% odds of sub-$66K BTC by April 24

It then filed papers for a staked Ether (ETH) ETF later that week, and by the end of the month, the bank appointed one of Morgan Stanley’s longest-standing executives, Amy Oldenburg, to lead its digital asset team.

Morgan Stanley also applied for a national trust banking charter on Feb. 18, seeking to custody certain digital assets and execute purchases, sales and swaps for clients in addition to staking services.

In October, before the investment bank adopted its institutional crypto strategy, it recommended a 2% to 4% allocation to crypto portfolios for investors. It also allowed its financial advisors to recommend crypto funds to clients with individual retirement accounts (IRAs) and 401(k)s.

Magazine: Bitcoin may face hard fork over any attempt to freeze Satoshi’s coins

Crypto World

XRP Price Prediction in 2026: MARA Sells $1.1B in BTC While Pepeto Targets 100x Over Coins Like XRP and DOT

Mortgage rates at 7% are trapping American families in $2,300 monthly payments for 30 years, and the XRP forecast pointing toward 16% annual growth is not going to change that math for anyone. MARA just sold 15,133 Bitcoin for $1.1 billion to cut its debt by 30%, and that tells the reader everything about what even the largest miners think about holding BTC at these levels.

The XRP forecast is one conversation, but Pepeto is a different one entirely, with more than $8 million raised, a verified exchange already running, and analysts projecting 100x as the Binance listing approaches, the kind of entry that pays off the house.

MARA Holdings sold 15,133 Bitcoin for approximately $1.1 billion between March 4 and March 25, using the proceeds to repurchase $1 billion in convertible notes at a 9% discount according to Bitcoin Magazine.

The move cuts MARA’s debt by 30%. According to Phemex, the market showed little reaction suggesting the sale was anticipated. The XRP forecast sits at 16% while presale entries target 100x, and the gap between those numbers is the gap between 30 more years of payments and owning the house.

The Real Opportunity and Why the XRP Forecast Points Somewhere Else

Pepeto: The Exchange Where One Entry Pays Off the Mortgage While the XRP Price Prediction Delivers 16%

MARA needed to sell $1.1 billion in BTC just to manage debt, while the wallets entering Pepeto at presale are building positions that target 100x from one listing event. Pepeto is the exchange that gives every wallet the protection institutional desks keep for themselves, and the XRP forecast is not the path to the kind of returns that clear a $2,300 monthly mortgage payment permanently.

PepetoSwap processes every trade at zero commission so capital stays fully deployed, the network bridge transfers tokens across chains at no deduction, and the pre entry scanner confirms every contract is clean before capital commits, confirmed by a SolidProof audit.

The builder who launched the first Pepe token to an $11 billion valuation with zero utility assembled this platform with an experienced operator from Binance’s listing division, and more than $8 million raised during a Fear and Greed reading of 10 proves whale capital is positioned inside.

The people who bought Pepe coin during its presale turned small entries into fortunes that most investors spend entire careers chasing, and every one of them says they wish they had entered bigger. Analysts project 100x from the current entry at $0.000000186, and 192% APY staking rewards grow the holdings of every wallet inside as the listing draws closer. The same window is open right now, and the Binance listing is approaching fast.

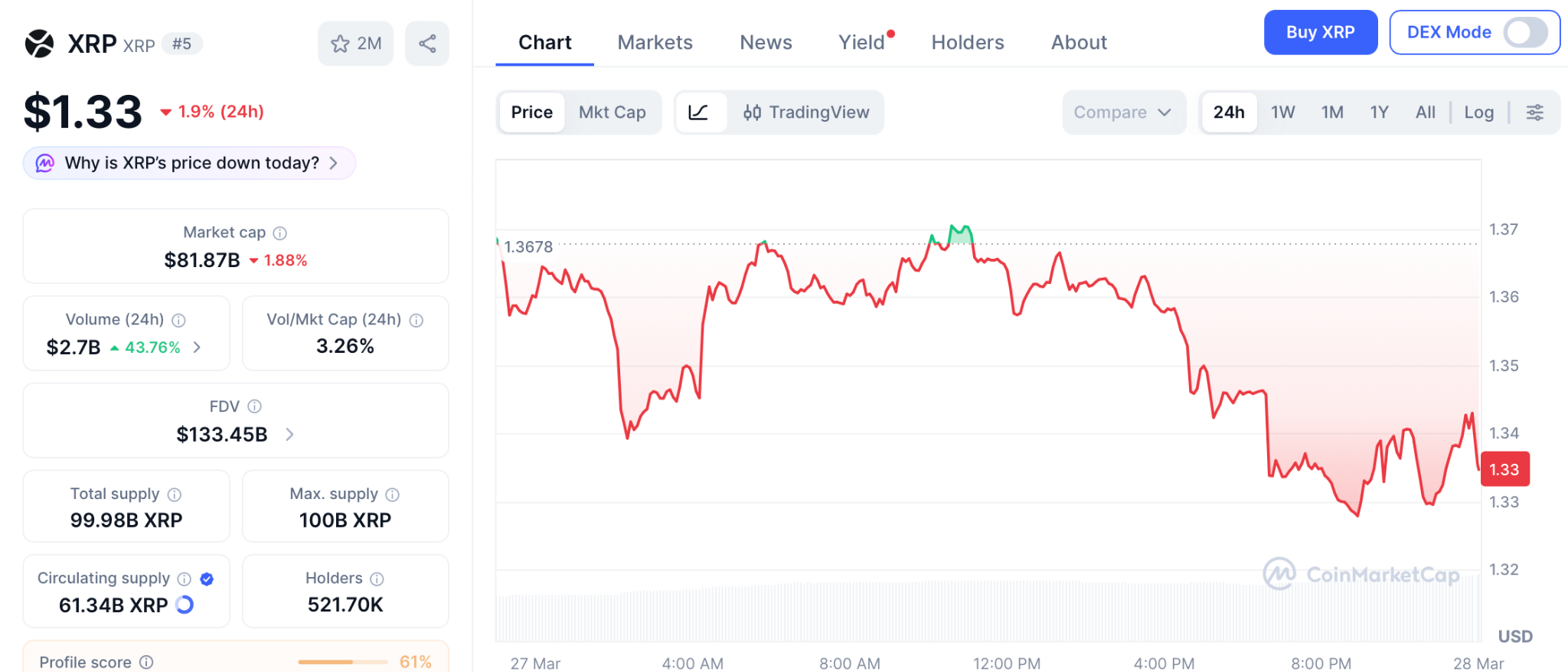

XRP

XRP trades at $1.34 per CoinMarketCap, sitting well below its 200 day moving average with a neutral RSI of 52 and medium volatility.

The xrp price prediction for 2026 targets $1.69 at maximum, a 25% return over months, meaningful for patient holders but far from the math that pays off a mortgage, while the forecast conversation is shifting toward presale entries where $2,300 monthly mortgage payments become a memory from one listing event.

Polkadot (DOT)

DOT trades at $1.28 per CoinGecko, deep in extreme fear territory with the index at 11, trading well below its 200 day moving average of $2.50.

Models project DOT falling to $0.66 by 2030, a 48% decline over four years, and established tokens like XRP and DOT share the same structural problem: neither can deliver the multiples that presale entries produce.

The XRP Price Prediction Delivers 16% but the Wallets That Entered Pepe’s Presale Built Fortunes

MARA just sold $1.1 billion in BTC to manage debt, and the xrp price prediction points toward 16% while American families carry $2,300 mortgage payments for 30 years. The people who entered Pepe’s presale turned small positions into the kind of wealth most investors chase for entire careers, and no large cap recovering from this crash delivers the returns that pay off a house.

The same window is open right now through the Pepeto official website, and the Binance listing is approaching, which means once Pepeto lists the presale entry disappears permanently and the wallets inside hold the positions that turn $2,300 monthly payments into a chapter that is already closed.

Click To Visit Pepeto Website To Enter The Presale

FAQs

Should investors follow the xrp price prediction or enter the Pepeto presale?

The xrp price prediction targets 16% annually while Pepeto targets 100x from one listing event, and the presale entry is the path that clears mortgage debt from one position.

Why look past the xrp price prediction right now?

An XRP forecast pointing toward 25% growth suits passive holders, but the Pepeto official website is where the 100x entry that changes the reader’s financial life is still open.

Does the xrp price prediction for 2026 matter?

The xrp price prediction sets realistic expectations of 16%, but Pepeto’s presale with a verified exchange and Binance listing targets the 100x that only presale entries with a Binance listing produce.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

with little attention.

0G says it crossed an important threshold months ago. Now it is retraining the same model in public, with the goal of showing what decentralized AI can actually deliver and why its earlier result deserved more attention.

In July 2025, 0G trained a 107 billion parameter model called DiLoCoX-107B with China Mobile. The research later appeared on arXiv after peer review. According to the paper, the system reached 357 times better communication efficiency than traditional AllReduce methods. Even so, the result barely landed in the market.

The team says the timing worked against it. Mid-2025 crypto attention was fixed on mainnet launches and token stories, while technical results drew far less interest. The work was serious, but it did not get much traction outside a small circle following the field closely.

Now, with decentralized AI back in focus, 0G wants to bring the result back into view.

A public retraining effort

This time, the company is putting the retraining process out in the open.

0G plans to document each stage, including checkpoints, convergence metrics, and data sourcing. It also says the run will be verified through Trusted Execution Environments using zerogAuth. Once the work is complete, the model weights will be open sourced.

Ultimately, 0G wants to show that decentralized AI can be audited, reproduced, and verified in a way most closed systems cannot match.

More than a parameter race

A lot of AI coverage still revolves around parameter counts. Bigger numbers attract attention, but 0G argues that a model’s value comes from the full system around it.

For the team, the real test starts with training and continues through verification, storage, serving, and integration into working products.

One of the main technical points is communication efficiency. DiLoCoX uses pipeline parallelism, a dual optimizer policy for local and global updates, a one-step delay overlap mechanism, and adaptive gradient compression. In plain terms, the design cuts the amount of communication needed during distributed training, which is often where these systems slow down.

0G also puts the model inside a full stack that includes onchain verification, decentralized storage, data availability, inference, and settlement. The result is a working environment rather than a one-off research demo.

Verification is another part of the pitch. With Trusted Execution Environments, users can check more than the existence of a model. They can inspect how it was trained and what data went into the process. For decentralized AI, that changes the trust model in a meaningful way.

The real story is bandwidth

According to 0G, the most important part of the DiLoCoX-107B result was the way the model was trained.

The team says the 107B model ran on standard one gigabit per second internet connections rather than specialized data center setups. That point goes straight at one of the biggest assumptions in AI, namely that frontier training requires rare and expensive networking conditions.

If that holds up over time, the impact could be substantial. Lower technical requirements open the door to far more participants, from research groups to companies and public institutions. In that setup, coordination becomes the main challenge, and decentralized systems are built for exactly that kind of problem.

A different cost model

0G also says its system cuts costs by about 95% compared with centralized alternatives.

The company attributes that reduction to the removal of expensive centralized overhead rather than cheaper hardware. If those numbers hold in real-world use, advanced model training becomes accessible to far more organizations, including universities, enterprises, and governments that do not have the budget for hyperscale AI spending.

That could change who gets to build serious models in the first place.

Can decentralized AI compete?

Skeptics have long argued that decentralized AI cannot keep up on performance. 0G believes the old tradeoff is starting to weaken.

As results improve and costs fall, the discussion becomes less about ideology and more about output. Can the system train strong models, verify them, and do it at a price point more teams can afford?

Open participation still comes with real risk. Distributed training can expose systems to data poisoning, gradient manipulation, and uneven contributor quality. 0G says it addresses those issues with architectural safeguards, anomaly detection, and cryptographic verification.

The point is not perfect safety. The point is making failures visible and traceable.

What verifiable AI actually means

For 0G, verifiable AI is about replacing trust by reputation with trust by inspection.

Instead of taking a provider at its word, users get a way to independently check how a model was trained and how it operates. That idea has obvious value in areas where accountability carries real weight, including finance, healthcare, and government.

This is where decentralized AI starts to stand apart, with systems people can inspect rather than simply trust.

From research demo to working system

The decentralized AI field has come a long way in a short time. Early proof-of-concept work is giving way to systems designed for training, verification, storage, inference, and economic settlement inside one environment.

0G wants DiLoCoX-107B to stand as proof of that progression. The public retraining effort is as much about process as performance. The company is trying to show that decentralized AI can produce serious models while staying open to inspection.

The road ahead

Larger models are still on the horizon. 0G believes models in the hundreds of billions, and eventually trillions, are within reach.

The next stage depends less on a single scientific leap and more on better coordination and stronger network participation. In decentralized AI, organization may prove just as important as compute.

The retraining of DiLoCoX-107B is an attempt to reopen a conversation 0G believes the market missed the first time. It is also a test of whether open, verifiable AI can win attention on the strength of results rather than hype.

For now, the company is betting that public retraining, transparent documentation, and open access will give decentralized AI a stronger footing in the next round of competition.

The post 0G Retrains 107B Model in Public as Decentralized AI Enters a New Phase appeared first on BeInCrypto.

Ethereum (ETH) is trading at $2,068, pressing directly against the 0.236 Fibonacci level at $2,055. The token has been pulled in two directions simultaneously — long-term holders booking profits from elevated cost bases while whale-tier addresses absorb that supply to prevent a structural breakdown.

The $2,000 level is the line separating these two forces. Which cohort wins determines the next significant move.

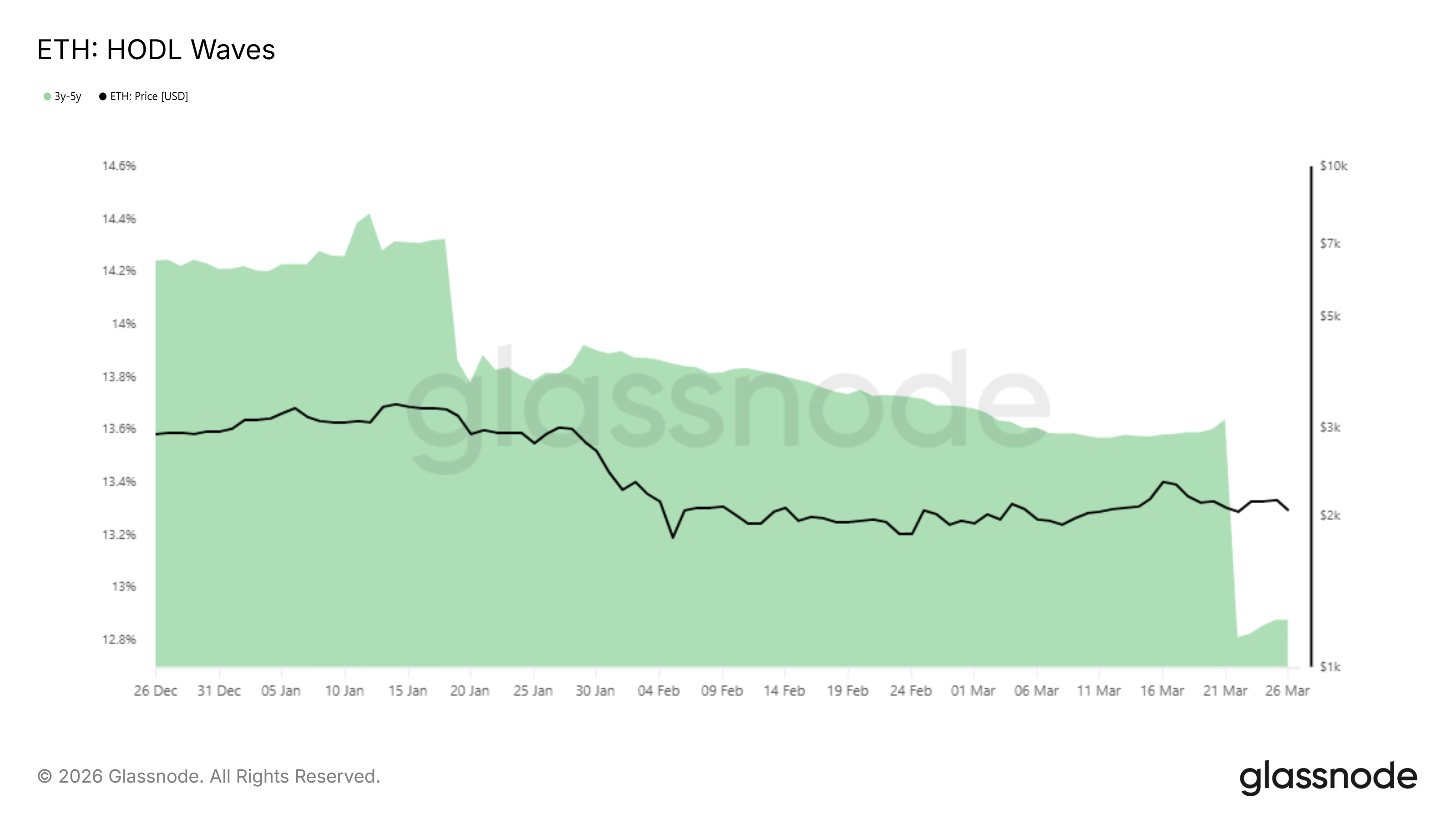

Old ETH Holders Are Selling

The Glassnode HODL Waves chart tracking the 3-to-5 year holding cohort spans December 26, 2025, through March 26, 2026. That band held relatively stable between 14.2% and 14.4% of total ETH supply from late December through January 20 before beginning a gradual decline.

The decline accelerated sharply at the right edge of the chart. Between March 21 and March 26, the 3-to-5 year cohort dropped from approximately 13.6% to 12.8% of supply — a fall of nearly 0.8 % in under a week. This represents the second-largest distribution event from this cohort visible in the 2026 data, behind only the drop recorded in late January.

Holders in this cohort acquired ETH between 2021 and 2023, a period that includes both the 2021 bull market peak near $5,000 and the 2022 bear market lows. Many of those who bought near the top are still underwater.

Those who accumulated during the bear market are now sitting on meaningful profits at current prices and are choosing to realize them. Their exit is not panic — it is deliberate profit-taking at a price level they may not see again soon.

Whales Are Absorbing Smaller Holders Are Selling

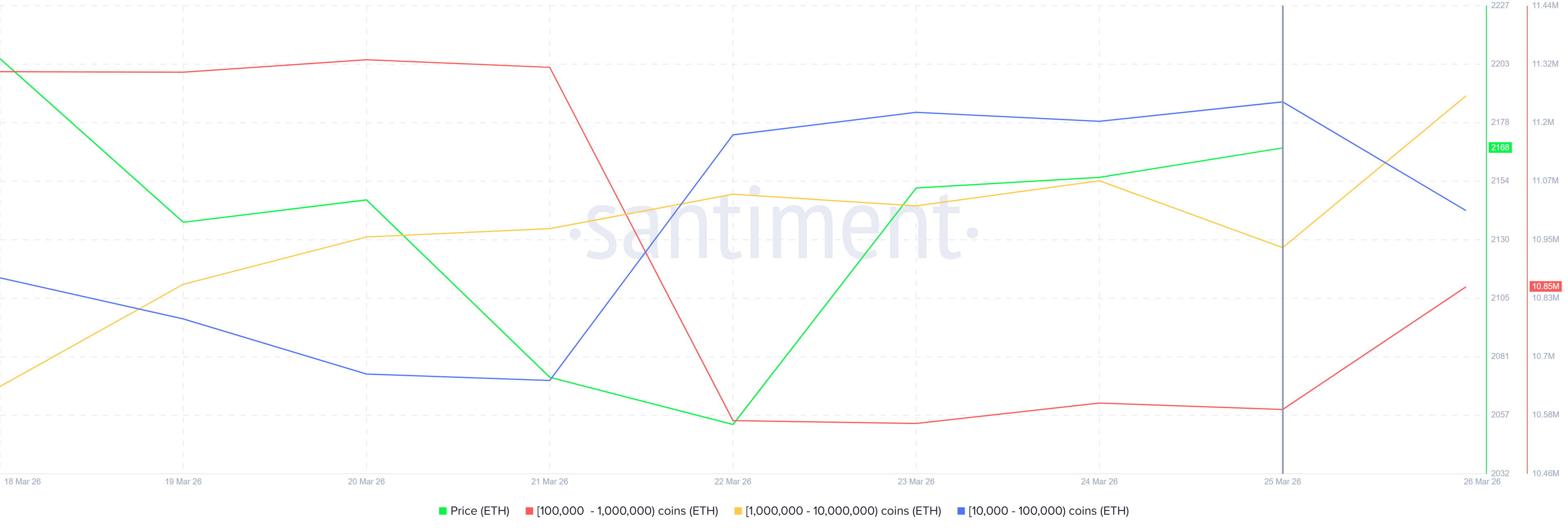

The Santiment address supply distribution chart tracking three cohorts — addresses holding 10,000 to 100,000 ETH (blue), 100,000 to 1,000,000 ETH (red), and 1,000,000 to 10,000,000 ETH (yellow) — shows a clear shift in supply ownership since March 25.

The blue cohort sold approximately 370,000 ETH between March 25 and the time of writing. That selling did not push the price lower in any meaningful way.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

Instead, the red and yellow cohorts absorbed that supply collectively, with the two larger whale tiers increasing their balances in direct proportion to the blue cohort’s exit. At the current Ethereum price, that transfer of 370,000 ETH represents approximately $765 million changing hands from mid-tier holders into the largest whale addresses on the network.

This dynamic — larger addresses absorbing supply that smaller addresses are offloading — is what will likely keep ETH above $2,000. As long as that buying continues to absorb available sell-side supply, it acts as a structural floor against further price decline.

ETH Price Trajectory Going Forward

The daily chart shows Ethereum price at $2,068, sitting at the 0.236 Fibonacci level at $2,055, with the red 50-day EMA sloping downward at $2,186 acting as immediate resistance. The Fibonacci retracement grid runs from the zero level at $1,750 to the 1.0 level at $3,045.

The 0.236 level at $2,055 has been the battleground since early March. Every session that has tested it has either closed above or produced a recovery. Ethereum price is currently pressing it again, and the outcome of this test determines the next destination. Below $2,055, the $1,928 horizontal support is the next level on the chart and represents the last defense before the $1,838 floor comes into play.

The bullish invalidation requires reclaiming the 0.382 level at $2,244. Above that, the 0.5 level at $2,397 becomes the next target, followed by the 0.618 level at $2,550.

A sustained move toward $2,550 would require whale accumulation to accelerate as the 3-to-5-year holder selling pressure subsides. This is a scenario that becomes more likely only if the broader market stabilizes above $2,000.

The post $765 Million ETH Changes Hands As Whales Anchor Ethereum Price Above $2,000 appeared first on BeInCrypto.

California Governor Gavin Newsom signed an executive order Friday expanding restrictions on insider trading linked to prediction markets. The move targets gubernatorial appointees and those closely connected to them, prohibiting the use of confidential or non-public information gained through official duties to profit from markets tied to political or economic events they can influence or which they are privy to. The measure also extends to spouses, family members, and former business partners of the appointed officials.

Newsom’s office framed the order as a guardrail against conflicts of interest and cronyism, with the governor stating that public service should not become a vehicle for personal enrichment. “Public service should not be a get-rich-quick scheme,” Newsom said, underscoring a broader push for stronger ethics standards in state governance. The administration contends that officials must adhere to a clear boundary between their duties and financial bets tied to real-world events they might shape.

“If you serve the public as a political appointee, you serve the public — period. We’re not going to tolerate this kind of corruption in California,” Newsom asserted, characterizing the new rules as a bright line against insider profiteering.

According to the governor’s office, the executive order lists several episodes that allegedly involved political insiders using non-public information to profit from prediction markets. Among the cited cases are six individuals suspected of exploiting information related to U.S. military actions in Iran. The document also points to a January incident in which a Polymarket trader earned about $410,000 betting on the arrest of Nicolás Maduro, the former Venezuelan president.

Prediction markets have long drawn scrutiny from U.S. lawmakers who fear that insiders may unfairly capitalize on privileged information and that wagers on sensitive developments—such as war or major political changes—could raise national-security concerns. The California order aligns with a broader national conversation about the governance of prediction markets and the potential for conflicts of interest to distort outcomes or undermine public trust.

Key takeaways

- The executive order expands insider-trading prohibitions to gubernatorial appointees and their close associates, extending protections to spouses, family members, and former business partners.

- The scope centers on non-public information gained through official duties used to profit from prediction markets tied to events officials can influence.

- California cites internal cases where insiders allegedly profited from sensitive events, such as U.S. strikes in Iran and the Maduro arrest bet on Polymarket, as rationale for the tightened rules.

- The move sits within a broader U.S. policy debate, as lawmakers push federal legislation to curb insider trading on prediction markets.

- Two parallel bills propose to bar high-ranking government officials from betting on prediction markets, with different emphases on war and sensitive operations—signaling potential cross-cutting regulation at state and federal levels.

Regulatory momentum beyond California

In response to ongoing concerns about insider access, Texas Congressman Greg Casar and Connecticut Senator Chris Murphy introduced the Bets Off Act in March 2026. The proposal would prohibit government insiders from placing bets on markets tied to war or other sensitive operations. At roughly the same time, Representatives Adrian Smith and Nikki Budzinski introduced the PREDICT Act, which would bar the President, lawmakers, and other high-ranking officials from participating in prediction markets. The bills collectively reflect a growing consensus that current frameworks do not sufficiently guard against conflicts of interest or the exploitation of privileged information.

Industry observers note that the new California directive does not replace federal action but rather adds a state-level layer of oversight that could influence how prediction-market platforms operate within the state. While enforcement mechanisms and timelines were not detailed in the order itself, the development underscores a widening regulatory lens on predictive markets and the potential for broader, more harmonized standards if federal measures advance.

Implications for the market and governance

For traders, policymakers, and platform operators, the California move highlights several practical considerations. First, it raises the cost and complexity of participation for officials and their networks, potentially shrinking the pool of publicly connected insiders who might have leveraged non-public information in prediction markets. Second, it reinforces a governance signal that conflicts of interest—once deemed a gray area—will be treated as a compliance risk with real consequences. Platforms hosting prediction markets may respond by tightening verification checks, enhancing disclosures, and imposing stricter controls around politically sensitive topics to avoid regulatory scrutiny and reputational risk.

In the broader regulatory landscape, the California action dovetails with federal proposals that seek to curb real-time exploitation and insider trading in state or federal decision environments. While the specifics of enforcement and cross-border applicability remain to be seen, the convergence of state and federal efforts points to a more proactive stance on governance in prediction markets. Analysts say this trend could slow the growth of speculative activity around politically sensitive events and push participants toward higher standards of transparency and accountability, even as some observers worry about chilling effects on legitimate market price discovery and risk assessment.

What comes next

What remains uncertain is how California will implement and police the new rules, and whether other states will adopt similar measures that could create a patchwork regulatory environment for prediction markets. Federal bills, if enacted, could provide uniform standards that affect both users and platforms nationwide. Observers will be watching for any enforcement actions tied to the executive order, as well as how platforms respond to the evolving mix of state and federal expectations around insider information and public-interest safeguards.

The evolving policy landscape also raises broader questions about how prediction markets should be governed as tools for forecasting versus potential channels for improper gain. As lawmakers and regulators weigh the balance between innovation, market liquidity, and integrity, readers should monitor whether new rules push prediction-market ecosystems toward stronger compliance or toward strategic shifts in participation and product design.

Readers should watch for updates on enforcement actions in California, any follow-on guidance from the governor’s office, and the fate of federal proposals like the BETS OFF and PREDICT Acts, which could redefine how insiders interact with markets tied to sensitive political and security developments.

In the near term, the California order marks a notable step toward closing perceived loopholes in prediction-market governance and signals that public service will increasingly be measured not just by duties performed but by the integrity of decisions surrounding information access and financial risk.

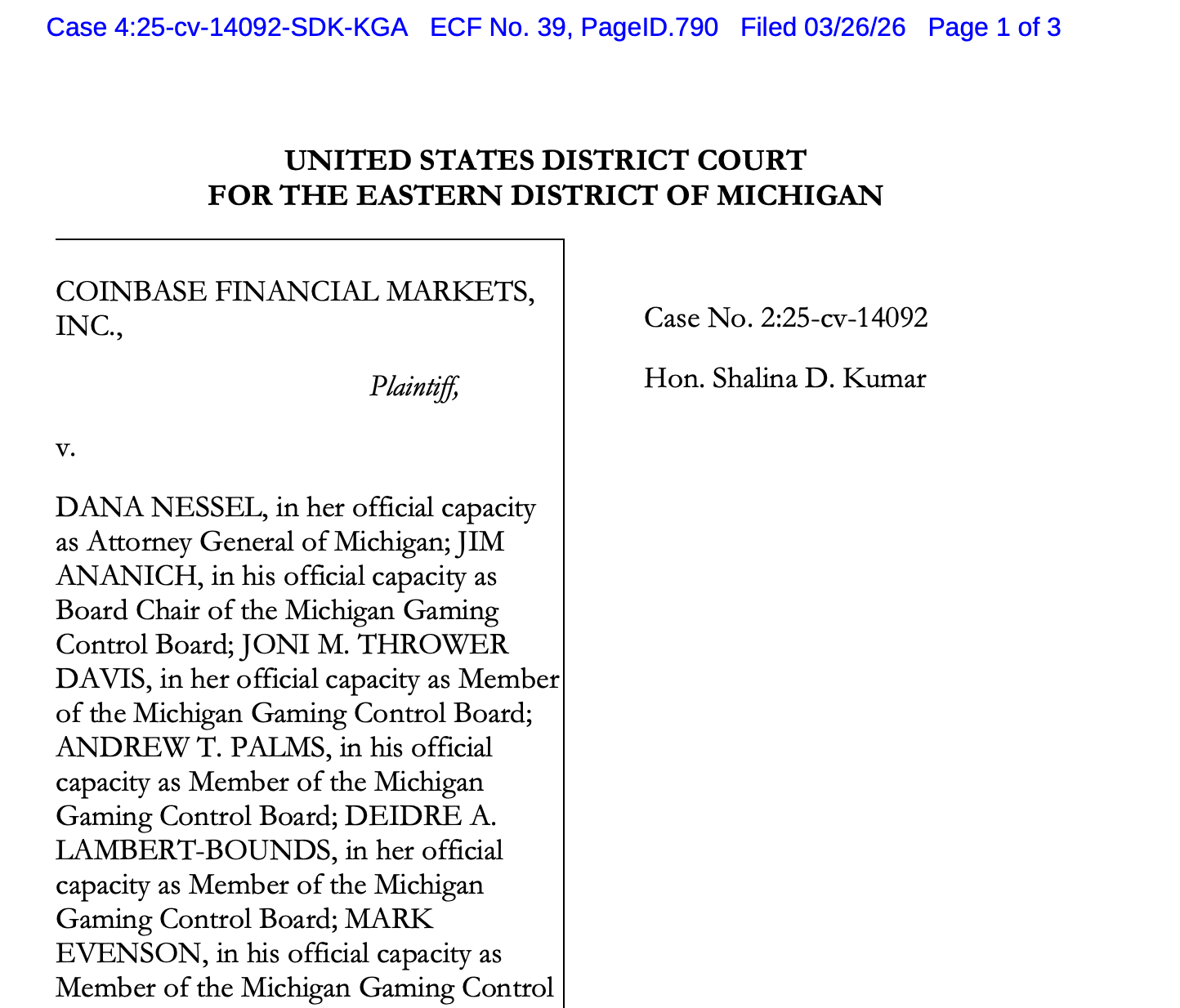

Lawyers representing the US city of Detroit plan to file an amicus brief in Coinbase’s lawsuit against Michigan, which argues that federal regulators should have authority in overseeing prediction markets and not states.

In a Thursday filing in the US District Court for the Eastern District of Michigan related to state officials’ motion for a preliminary injunction, District Judge Shalina Kumar approved an order which will allow Detroit to file a brief supporting state authorities in their lawsuit against Coinbase. Kumar gave Detroit’s lawyers until April 3 to make the filing as the lawsuit continues.

In December, Coinbase filed its lawsuit against Michigan, as well as gaming authorities in Connecticut and Illinois, more than a month before the crypto exchange announced the launch of its prediction market services on the platform.

The company’s argument is centered on claims that prediction markets fall under the purview of the US Commodity Futures Trading Commission (CFTC) rather than state gambling regulators, challenging Michigan’s enforcement.

Companies offering event contract bets on prediction markets like Coinbase, Kalshi and Polymarket already face state-level lawsuits in multiple jurisdictions. Although the platforms have been supported by efforts from CFTC Chair Michael Selig, who proposed new rules for the commission, it was still unclear as of Friday how the legal battle between state authorities and federal regulators would unfold.

Related: Federal regulation looms as 11 states go after prediction markets

Where will the chips fall for platforms dealing with state and federal authorities?

“The more the CFTC can do in this space [prediction markets] to put a comprehensive regulatory regime around it, the more likely it is for courts who are looking at the issue to say ‘actually, yes, this is a CFTC jurisdiction issue — this really is not just an end run around sports gambling bans in particular states,’” Stephen Piepgrass, a partner at international law firm Troutman Pepper Locke, told Cointelegraph.

According to Piepgrass, the cases could ultimately end up going back to the US Supreme Court, given its 2018 decision in Murphy v. National Collegiate Athletic Association. That case gave US states the authority to regulate sports gambling, striking down a federal law that attempted to impose a ban on such activities.

US states have largely pushed back against lawsuits over prediction markets, but courts have sided with the platforms in some cases.

This month, a judge ordered Kalshi to temporarily stop operating in Nevada, and the platform faces criminal charges in Arizona over alleged illegal gambling on sports and elections. However, a Tennessee judge blocked state authorities from enforcing gambling laws against the platform in February.

The Michigan Gaming Control Board reported that casinos based in Detroit casinos generated more than $200 million in revenue for January and February, providing more than $24 million in taxes for the US state.

Magazine: XRP yet to ‘price in’ 3 bullish catalysts, Bitcoin to $80K? Trade Secrets

Key points:

-

Bitcoin’s fall below the $66,000 support heightens the risk of a drop to the $62,500 level.

-

Select major altcoins have broken below their immediate support levels, opening the gates for further downside.

Bitcoin (BTC) is under pressure from the bears, who are attempting to sustain the price below the $66,000 level. The uncertainty regarding the US and Israel-Iran war is capping the upside and putting downside pressure. US spot Bitcoin exchange-traded funds recorded $171 million in outflows on Thursday, the biggest since the $348 million in redemptions on March 3, according to Farside Investors data.

Although BTC is facing selling on rallies, the bulls have successfully defended the $60,000 level since Feb. 6. Glassnode said in its latest Week On-chain newsletter that the sharp contraction in BTC’s entity-adjusted realized profit from $3 billion per day in July 2025 to $0.1 billion currently suggests that the bear market is transitioning into its later stages.

A positive sign in favor of the bulls is that BTC whales and sharks have continued to accumulate. Santiment said in a post on X that large BTC holders owning between 10 and $10,000 BTC have boosted their holdings by 0.45% in the past month. Historically, an upside breakout happens when large wallets are accumulating, and retail is selling.

Could BTC and select major altcoins hold on to their crucial support levels? Let’s analyze the charts of the top 10 cryptocurrencies to find out.

Bitcoin price prediction

Buyers could not maintain BTC above the $72,000 level on Wednesday. That may have attracted sellers who pulled the price below the support line of the ascending triangle pattern on Friday.

If the BTC price closes below the support line, the bullish pattern will be invalidated. That may intensify selling, pulling the BTC/USDT pair to the $62,500 to $60,000 support zone.

Instead, if the price turns up sharply from the current level and breaks above the $72,000 level, it suggests that the bulls are attempting to get back into the driver’s seat. The pair may then challenge the crucial $74,508 resistance. If buyers overcome the barrier, the pair may surge to $84,000.

Ether price prediction

Ether (ETH) turned down and fell below the breakout level of $2,111 on Thursday, indicating that the bears are trying to make a comeback.

Sellers kept up the pressure and pulled the ETH/USDT pair below the 50-day SMA ($2,044) on Friday. The ETH price may decline to the $1,900 level, which is likely to attract buyers. However, if the bears prevail, the pair may collapse to the vital $1,750 support.

This negative view will be invalidated in the near term if the price turns up sharply and breaks above the $2,200 level. That enhances the prospects of a rally above the $2,400 level.

BNB price prediction

BNB (BNB) has been oscillating between $570 and $687 for the past few weeks, signaling buying near the support and selling close to the resistance.

There is minor support at $607, but if the level gives way, the BNB/USDT pair may slump to the $570 level. A strong bounce off the $570 support suggests that the pair may remain inside the range for a while longer.

The next trending move is expected to begin on a close below $570 or above $687. If buyers clear the overhead hurdle, the BNB price may jump to $790. Alternatively, a close below $570 might sink the pair to the psychological level at $500.

XRP price prediction

XRP (XRP) turned down from the moving averages on Thursday, indicating that the bears remain in control.

The XRP price may slide to $1.32 and then to $1.27. Buyers will attempt to aggressively defend the $1.27 level, but if the bears prevail, the XRP/USDT pair may decline to the support line.

The first sign of strength will be a close above the moving averages. The pair may then rise to the breakdown level of $1.61, which is expected to pose a substantial challenge for the bulls. If buyers pierce the $1.61 level, the next stop is likely to be the downtrend line.

Solana price prediction

Buyers attempted to push Solana (SOL) above the $95 resistance on Wednesday, but the bears held their ground.

The SOL price has dipped below the 50-day SMA ($86), indicating that the bulls have given up. That suggests the SOL/USDT pair may extend its stay inside the $76 to $95 range for some more time.

The next trending move is expected to begin on a break above or below the range. If the bulls propel the price above $95, the pair may reach the $117 level. On the downside, a close below $76 might sink the pair to $67.

Dogecoin price prediction

Dogecoin (DOGE) rose above the moving averages on Wednesday, but the bulls could not sustain the higher levels.

The DOGE price turned down on Thursday, and the bears have pulled the DOGE/USDT pair below the critical $0.09 support. If the sellers sustain the price below $0.09, the pair may collapse to $0.06.

Buyers are unlikely to give up easily. They will attempt to defend the $0.09 level and swiftly push the price above the moving averages. If they succeed, the pair may ascend to $0.10 and later to $0.12.

Hyperliquid price prediction

Hyperliquid (HYPE) turned down from $41.59 on Wednesday but is likely to find support in the zone between the 20-day EMA ($37.64) and the breakout level of $36.77.

If the HYPE price bounces off the $36.77 level, it suggests that the bulls are trying to flip the level into support. Buyers will endeavor to strengthen their position by pushing the HYPE/USDT pair above the $43.77 level. If they can pull it off, the pair may start its northward march toward $50.

Contrary to this assumption, if the price continues lower and breaks below $36.77, it suggests that the bulls are losing their grip. The pair may tumble to the 50-day SMA ($33.34), which is likely to attract buyers.

Related: Ether traders see ‘further decline’ as ETH price slips below $2K

Cardano price prediction

Buyers pushed Cardano (ADA) above the 50-day SMA ($0.27) on Wednesday but could not sustain the higher levels.

The ADA/USDT pair turned down sharply on Thursday, signaling that the bears had renewed their selling. There is strong support at $0.25, but if the level breaks down, the ADA price may slump to $0.22.

This negative view will be invalidated in the near term if the price turns up sharply from the $0.25 level and closes above the moving averages. That clears the path for a rally to the downtrend line.

Bitcoin Cash price prediction

Bitcoin Cash (BCH) fell below the 20-day EMA ($468) on Thursday, indicating that the bears are attempting to retain control.

The BCH/USDT pair may descend to the $443 support, which is a crucial level to watch out for. If the bears sink the BCH price below the $443 level, the pair will complete a bearish head-and-shoulders pattern. That may start a drop to $375.

On the contrary, if the price turns up from the $443 level, it signals solid buying at lower levels. The pair may form a range between $443 and the 50-day SMA ($491) for some time. Buyers will have to push and maintain the price above the 50-day SMA to signal the start of a sustained recovery toward $520.

Chainlink price prediction

Chainlink’s (LINK) rebound fizzled out at $9.50 on Wednesday, indicating that the bears are selling on rallies.

The price turned down sharply on Thursday, and the bears have pulled the LINK/USDT pair below the support line of the ascending channel pattern. If the LINK price closes below the channel, the pair may drop to $8.05 and then to $7.15.

Buyers are likely to have other plans. They will attempt to retain the price inside the channel and push the pair above the $9.50 level. If they do that, the pair may rally to the resistance line.

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

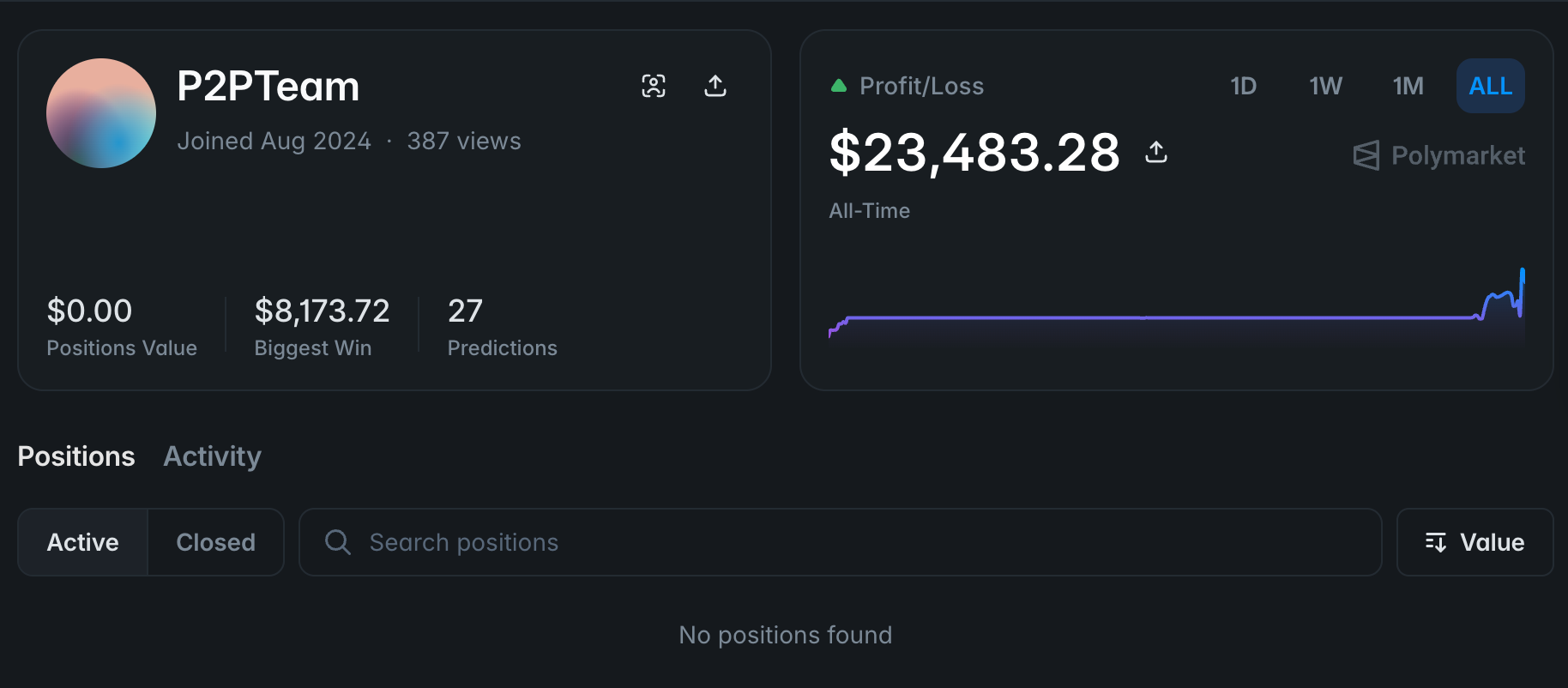

The team behind the P2P.me decentralized trading platform disclosed that it opened positions on the Polymarket prediction market related to its recent capital raise.

The team opened the positions 10 days before the raise went live, wagering whether the project would hit its $6 million fundraising target, according to a disclosure published on the X social media platform.

At the time the positions were opened, P2P.me had only one “oral commitment” from venture firm Multicoin Capital for $3 million in funding, “no signed term sheets” and “no guaranteed allocations,” the team said.

However, the project only managed to raise $5.2 million in the funding round, which resulted in the market resolving to a “no.” Following the outcome, the team said:

“Trading on an outcome you can influence erodes trust. We don’t believe we were trading on a done deal, but we recognize reasonable people can see it differently. We named the account “P2P Team” deliberately to give a marketing signal of our presence. But intent isn’t the same as action. Not disclosing at the time was a mistake we own.”

Any profits made from the prediction market positions will be funneled back into the project’s MetaDAO treasury, the reserve for the decentralized autonomous organization (DAO) governing the platform, the P2P.me team said.

The team also said it is liquidating all open positions on Polymarket and adopting a “formal company policy” on prediction market trading activity.

Cointelegraph reached out to P2P.me about the disclosure, but did not receive a response by the time of publication.

Prediction markets have come under increased scrutiny from US lawmakers for insider trading activity, and in response, popular prediction market platforms like Polymarket and Kalshi have announced countermeasures to curb insider trading.

Related: Federal regulation looms as 11 states go after prediction markets

US lawmakers take steps to curb insider trading activity on prediction markets

US lawmakers are seeking to restrict insider trading activity on prediction markets, particularly those linked to elections, legislation and geopolitical issues with national security implications.

Congress members Adrian Smith and Nikki Budzinski introduced the “Preventing Real-time Exploitation and Deceptive Insider Congressional Trading Act,” also known as the PREDICT Act, on Wednesday to ban the US president and lawmakers from prediction markets.

A competing bill was also introduced on Thursday, aiming to curb political insider trading activity on prediction market platforms.

Magazine: IronClaw rivals OpenClaw, Olas launches bots for Polymarket — AI Eye

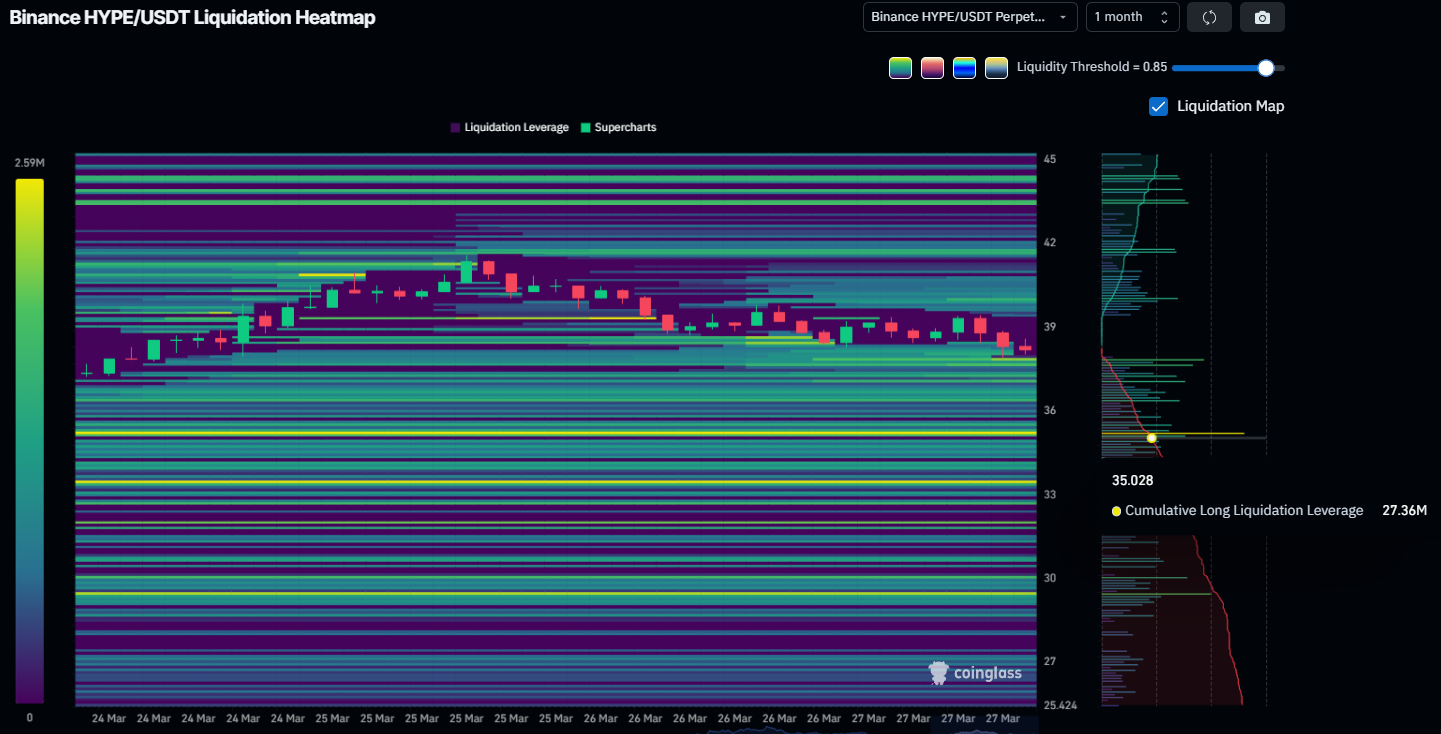

Hyperliquid (HYPE) price is trading at $38.27, down 2.31% on the day, as a completed double top pattern and a dense liquidation cluster at $35.03 raise the odds of an accelerated leg lower.

The token has failed to hold gains above $42.67, and the price is now consolidating. Two independent signals now define the near-term trend line.

HYPE Long Traders Should Be Worried

The HYPE liquidation heatmap shows a dense band of leveraged long positions clustered around $35.03. Cumulative long liquidation leverage at that level totals $27.36 million.

A move below $35.03 would trigger the forced closure of those positions in rapid succession. This would create mechanical selling pressure that could accelerate any decline well beyond the initial breakdown.

Want more token insights like this? Sign up for Editor Harsh Notariya’s Daily Crypto Newsletter here.

The heatmap shows relatively thin liquidation stacking between $38 and $35, suggesting the price could slice through that range with limited friction. The absence of significant long-side leverage above $39 further limits the likelihood of a demand-driven reversal before the $35.03 test arrives.

Selling Pressure Set Dominates HYPE

The Klinger Oscillator (KVO) is currently reading 8.09K on the daily chart, sitting just above the zero line with a clear downward trajectory. The signal line (green) has already turned lower, and the KVO (blue) is converging toward a bearish crossover.

The Klinger Oscillator measures the difference between two volume-weighted EMAs of price to gauge whether money is flowing into or out of an asset. When it rises above zero, buying pressure dominates; when it falls below zero, selling pressure takes control.

The indicator peaked near 25K in early March, coinciding with HYPE’s rally to $43.76. Since then, momentum has declined in three successive lower highs, a pattern of deteriorating buying pressure that mirrors the price action.

A confirmed cross below zero on the KVO would shift volume-weighted momentum from bullish to bearish. Historically, on the HYPE daily chart, both prior KVO zero-line breaks preceded drawdowns.

The 0.382 Fibonacci retracement level sits at $36.83, offering the first meaningful demand zone before price reaches the $35.03 liquidation cluster. Should the KVO break below zero while the price is below $36.83, the path to $32.33 — the 0.618 Fibonacci level — becomes the primary scenario.

HYPE Price Levels To Watch

The daily chart shows HYPE has completed a double top breakdown, now underway. Price is currently sitting at $38.27, hovering around the support at the same level.

The pattern’s full downside projection is calculated from the breakdown point at the $35.03 neckline. This points HYPE to $21.64 on a confirmed breakdown, matching the 37.49% decline annotated on the chart.

Holding $35.03 is therefore non-negotiable for bulls. Only a daily close below it would confirm the double top and open the door to $32.33 first, then $28.69.

For the bearish thesis to be invalidated, HYPE would need to reclaim $38.80 and then push through $42.67 with conviction. A break above $42.67 would negate the double top structure entirely, shifting the bias back toward the $47.15 resistance.

The post 2 Reasons Why $35 Is a Critical Juncture for Hyperliquid (HYPE) Price appeared first on BeInCrypto.

Bitget CEO Gracy Chen says a $1t single‑day US stock wipeout is accelerating a global macro risk reset, while lower leverage helps Bitcoin act more like a neutral portfolio allocation than a pure risk punt.

Summary

- Over $1 trillion was wiped from US stocks in a single day as risk assets sold off.

- Bitget CEO Gracy Chen says the slide has accelerated a global “reassessment of macro risks.”

- Bitcoin’s smaller drawdown and lower leverage hint at growing status as a neutral allocation.

In the wake of a sharp US equity selloff that erased more than $1 trillion in market value in a single session, Bitget CEO Gracy Chen says the rout is forcing investors to reprice macro risk at a much faster clip while Bitcoin (BTC) is starting to behave more like a neutral, portfolio-level allocation than a pure risk-on punt. According to ChainCatcher, the CEO’s remarks are the latest on top of a broader drawdown that has already knocked trillions off US benchmarks since President Donald Trump’s second-term tariff agenda reignited inflation fears and hit tech-heavy names. As of Friday morning, Bitcoin was trading around $66,500, down roughly 4% on the day but still outpacing major stock indices on a relative basis.

Gracy Chen: $1t US stock selloff shows Bitcoin becoming neutral allocation

Chen argued that the current move is less about idiosyncratic crypto stress and more about global portfolios digesting a new regime of higher energy prices, stickier inflation, and geopolitical conflict spilling over into capital allocation decisions. “This round of adjustment reflects that global markets are reassessing macro risks at a faster pace,” she said, adding that as oil spikes again, “the impact of geopolitical changes is no longer limited to the energy market but is beginning to more directly affect global capital allocation.” The comment comes as strategists at Bloomberg and elsewhere flag how renewed tariff salvos and conflict risk have turned the post-2024 equity boom into what one Bloomberg analysis called a “$1 trillion wreckage,” even as Bitcoin’s institutional scaffolding has largely held.

Despite warning that Bitcoin will “still maintain high volatility in the short term,” Chen highlighted that the asset’s behavior this week has been “relatively robust” compared with previous episodes when risk appetite collapsed. She pointed to a sharp reduction in derivatives leverage as a key reason: “The overall leverage in the crypto market has significantly decreased, thereby limiting the scale of forced liquidations that typically amplify downward pressure during market stress.” That fits with recent flows data showing Bitcoin spot ETFs have seen bouts of outflows but not the kind of capitulation that marked prior crashes, while Bitget’s own protection and risk systems have been tightened as volatility climbed.

For Chen, the resilience is sending a signal about how Bitcoin is being used. “In an increasingly fragmented macro environment, Bitcoin is starting to be viewed by some portfolios as a more neutral allocation choice,” she said. That echoes her earlier comments that recent drawdowns are “tightly linked to the macro cycle,” with investors rotating between crypto, equities, and gold as they navigate Trump’s tariff-led policy shock and rising odds of a US recession. According to a recent crypto.news story, US markets have wiped out $9.6 trillion in value since Trump’s second inauguration, even as Bitcoin has repeatedly bounced after single-day drops of 1%–5%, underlining its evolving role in a world where macro risk is now the dominant driver of asset prices.

In earlier coverage, crypto.news detailed how a previous wave of selling erased $1.1 trillion from digital assets in just 41 days as leverage cascades intensified the downside, a backdrop that makes today’s more orderly drawdown stand out. Another recent story examined how the same tariff and inflation shock that hit tech stocks has rippled through crypto, while a separate report tracked how Bitcoin’s price has stayed comparatively resilient even as US equity indices flirt with bear-market territory. For live market data on Bitcoin, readers can follow its price page on crypto.news, alongside dedicated pages for other major assets involved in these rotations, including Ethereum, XRP, Solana, and Dogecoin.

Markets drown in Red Sea: Rupee bleeds, bears maul Street

Joan Vassos and Kathy Swarts Predict the Future of Bachelor Nation

Kevin Gausman breaks Blue Jays’ opening-day strikeout record

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

8 Things That Are a Complete WASTE of Your Money

SPECIALE Guerra e mercati, primo bilancio e guida agli investimenti | Morning Finance

Mine Bitcoin 5X Cheaper Without Rigs? How to Stake HNO Coin #bitcoinmining #Crypto #Altcoin #shorts

-

NewsBeat3 days ago

NewsBeat3 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

Crypto World6 days ago

Crypto World6 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World6 days ago

Crypto World6 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

News Videos2 days ago

News Videos2 days agoParliament publishes latest register of MPs’ financial interests

-

Sports5 days ago

Sports5 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

Sports5 days ago

Sports5 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Business5 days ago

Business5 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Tech5 days ago

Tech5 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Tech5 days ago

Tech5 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

News Videos5 days ago

News Videos5 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

Tech6 days ago

Tech6 days agoToday’s NYT Connections Hints, Answers for March 22 #1015

-

Business1 day ago

Business1 day agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Business6 days ago

Business6 days agoWill Duke Basketball Win It All? Duke Basketball Enters Second Round as Third Favorite to Claim NCAA Title

-

Sports5 days ago

Sports5 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who hit 12 Derby-Oaks Doubles enters picks

-

NewsBeat5 days ago

NewsBeat5 days agoUpdate on Wisbech river crash as search for teenage boy enters fifth day

-

Entertainment4 days ago

Entertainment4 days agoCynthia Bailey Dishes on ‘RHOA’ Season 17, Discusses Kandi

-

Tech4 days ago

Tech4 days agoSamsung will soon let you control smart home devices from your car’s dashboard

-

NewsBeat2 days ago

NewsBeat2 days agoTesco is selling new Cadbury Dairy Milk bar and people can’t wait to try it

-

Fashion3 days ago

Fashion3 days agoDoes It Matter What You Wear When You’re Laid Off and Looking?

-

NewsBeat4 hours ago

NewsBeat4 hours agoThe Story hosts event on Durham’s historic registers

You must be logged in to post a comment Login