Crypto World

Georgia’s Crypto Rules Shape Tether’s GELT Stablecoin Strategy

Stablecoin issuer Tether and the government of Georgia are pursuing a new digital asset initiative: GELT, a stablecoin pegged to the Georgian lari that would operate under Georgia’s evolving digital asset regulatory framework. The collaboration aims to facilitate cross-border commerce and digital payments within the country, though key details—such as legal issuance arrangements, reserve custodians, and redemption rights—remain to be disclosed as the program unfolds.

On Monday, Tether stated that GELT’s structure, rollout plan, and regulatory implementation would be announced at a later stage. The announcement comes as Georgia advances a regulatory regime for digital assets, including stablecoins, with an emphasis on reserve management, redemption rights, issuer oversight, and anti-money laundering compliance. In March, the National Bank of Georgia signaled it had developed rules governing the initial offering of so‑called “stable virtual assets,” including requirements for full reserve backing, the provision of offering documents, and external auditor verification. According to authorities, the framework is designed to bolster consumer protection, strengthen risk management, and align with international standards.

Georgian Prime Minister Irakli Kobakhidze described the GELT partnership as a step toward a more connected and transparent financial system. Natia Turnava, president of the National Bank of Georgia, welcomed the collaboration as part of the central bank’s broader plan to advance digital financial infrastructure. The announcement did not specify who would legally issue GELT, where reserves would be held, or whether holders would have direct redemption rights. Tether did not provide a definite launch timeline. The company confirmed it had received Cointelegraph’s inquiry but did not offer additional details at publication time.

Key takeaways

- GELT represents a formal collaboration between Tether and the Georgian government to issue a lari‑pegged stablecoin under Georgia’s digital asset rules, with cross-border payments and digital commerce as primary use cases.

- Georgia’s March framework for stablecoins requires prior written consent from the National Bank, mandates full reserve backing with liquidity‑quality assets, and obliges issuers to prepare offering documents verified by external auditors. Non‑VASPs must register before offering stablecoins.

- Specifics about GELT’s issuer identity, reserve custody, and whether holders would have direct redemption rights remain undisclosed; no launch timeline has been announced.

- GELT would extend Tether’s non‑dollar stablecoin portfolio, which already includes MXNT (Mexican peso) and CNHT (offshore Chinese yuan), with plans for a UAE dirham‑pegged token and the recently launched USAT (federally regulated US‑dollar stablecoin). Earlier tokens such as EURT have been wound down or moved toward non‑redeemable status.

- The development sits within a broader regulatory and policy context, reflecting ongoing efforts to harmonize cross‑border crypto activities with established financial regulation and to align with international standards, including potential parallels to MiCA outside the EU framework.

Georgia’s stablecoin regime and the GELT initiative

The March 2024 framework released by the National Bank of Georgia establishes the guardrails for stablecoin issuance within the country. The central bank’s guidance makes clear that stablecoins may not be offered without prior written consent from the regulator, signaling a strict supervisory posture for digital asset offerings. The framework covers virtual asset service providers (VASPs) registered with the central bank; issuers not registered as VASPs must obtain registration before launching any stablecoin offering or related services. Importantly, the rules require that circulating stablecoins be fully backed by reserve assets that satisfy predefined liquidity and credit quality requirements. This emphasis on reserve integrity reflects a broader global regulatory concern around reserve adequacy and risk management for stablecoins serving as payment rails or settlement vehicles.

Additionally, the central bank requires issuers to prepare documentation for the initial issuance and submit these materials for external auditor verification. The regulator said the goal is to strengthen consumer protection, reinforce risk controls, and ensure alignment with international standards. For institutions and market participants, the regime signals a formal path to licensing, ongoing oversight, and heightened due‑diligence requirements for entities seeking to operate stablecoins in Georgia.

GELT’s architecture, governance, and regulatory questions

The public statement outlining GELT’s plans stops short of disclosing critical operational specifics. Notably absent are details about who would legally issue the GELT token, where any reserves would be held, and whether GELT holders would have direct redemption rights or access to reserves. The lack of a launch timeline further underscores the project’s early stage and the regulatory conditioning embedded in Georgia’s framework. As authorities emphasize, any stablecoin formation under the regime would require compliance with reserve standards, disclosure obligations, and independent verification, all of which would shape GELT’s risk profile and usability in commercial contexts.

From a policy and enforcement standpoint, the GELT initiative highlights several compliance considerations for financial institutions, banks, and technology providers operating in Georgia. First, the necessity of obtaining NBG consent points to a formal licensure process that would likely involve ongoing oversight of reserve management practices and governance. Second, the requirement for robust AML/KYC controls and external audit verification aligns GELT with internationally recognized controls that regulators monitor in cross-border payments ecosystems. Finally, the framework’s emphasis on consumer protection and risk management suggests that any GELT‑related products would be evaluated for compliance with disclosure standards, redress mechanisms, and governance transparency, which are critical for institutional confidence and retail trust alike.

Tether’s broader non‑dollar stablecoin strategy and regulatory alignment

GELT would extend Tether’s multi‑currency stablecoin lineup beyond its flagship USDT. The issuer has previously launched MXNT, a peso‑pegged token introduced in 2022 with initial support on Ethereum, Tron, and Polygon. It also operates CNHT, a yuan‑pegged token issued offshore, which has been expanded to multiple networks, and has announced a planned UAE dirham‑pegged token with backing from UAE‑based liquidity. In 2026, Tether launched USAT, a US‑regulated dollar stablecoin designed for the American market, reflecting the company’s strategic pivot toward compliance‑driven, regulator‑friendly offerings. At the same time, Tether has wound down some earlier non‑US‑dollar stablecoins; EURT’s minting was halted, and CNHT is slated to become non‑redeemable in February 2027. These moves illustrate a broader pattern: Tether is diversifying its product suite while tightening compliance and governance around its non‑USD assets.

The GELT development sits within this broader strategic arc, where Tether seeks to provide currency‑specific stablecoins that may appeal to regional economies and financial ecosystems seeking faster, cheaper cross‑border settlement options. For Georgia, the GELT plan could create a new interface between digital assets and traditional financial infrastructure, potentially enabling smoother cross‑border payments, remittances, and digital commerce—subject to the regulatory guardrails and the stability and transparency of reserve arrangements. From a regulatory standpoint, GELT also raises questions about how non‑dollar stablecoins will be treated in Georgia’s licensing framework, how cross‑border activities will be monitored, and how such instruments will interact with global AML/KYC standards and correspondent banking relationships.

Implications for banks, VASPs, and cross‑border settlement

The Georgian framework appears to be designed with a structured approach to licensing, oversight, and risk management. For banks and VASPs operating in or with Georgia, GELT could entail new compliance channels, including enhanced customer due diligence, ongoing monitoring of reserve holdings, and transparent audit reporting. The requirement for reserve backing and external audits would necessitate robust third‑party verification and clear disclosure to customers and counterparties. In cross‑border contexts, GELT could become part of a wider network of currency‑specific tokens that facilitate cross‑border payments, provided jurisdictions recognize and harmonize stability, governance, and regulatory compliance standards. Policymakers and industry participants alike will be watching how Georgia’s approach harmonizes with international standards and how it aligns with broader regional efforts to standardize stablecoin oversight.

From a historical and policy perspective, Georgia’s approach reflects a growing trend toward formalizing stablecoins within national financial architectures. The regime’s emphasis on consent, reserve adequacy, disclosure, and external audit mirrors requirements that have gained traction globally as jurisdictions reconcile innovation with investor protection and systemic risk mitigation. For institutional readers, this case underscores the importance of regulatory calendars, licensing pathways, and cross‑border compliance considerations when engaging with regional digital asset programs and payment rails.

Closing perspective

Georgia’s GELT plan emblemizes a cautious but ambitious avenue for integrating stablecoins into a regulated financial system. While many details remain to be announced, the initiative signals a clear intent to bridge digital assets with traditional monetary infrastructure under formal supervision. As regulators refine reserve and disclosure standards and as Tether outlines governance and issuance details, GELT’s trajectory will likely influence regional discussions on stablecoin licensing, cross‑border settlement, and the resilience of digital asset ecosystems in transitioning economies.

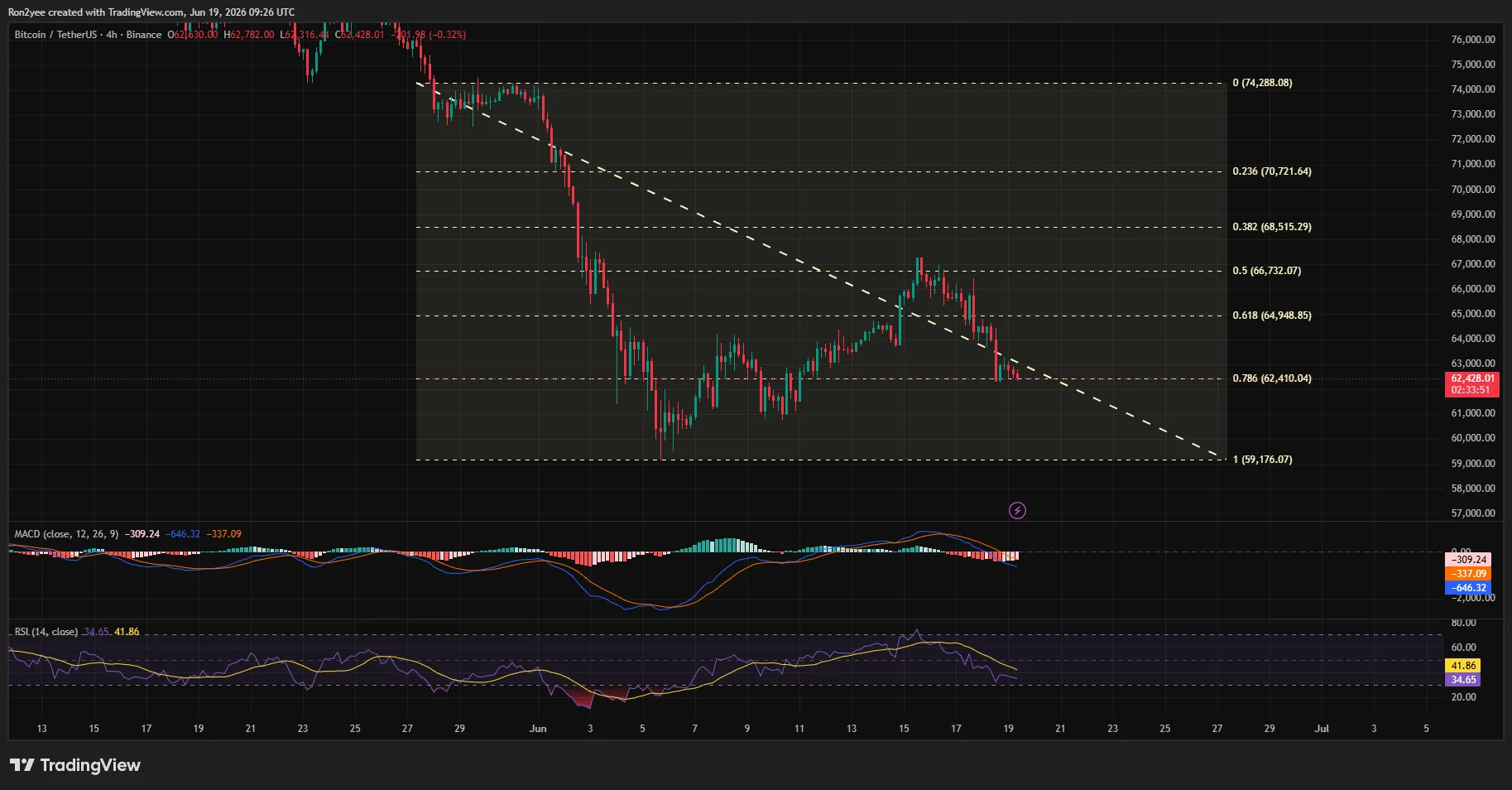

Bitcoin has fallen to around $62,400 after a combination of options-expiry volatility, long liquidations, and renewed concerns over corporate Bitcoin selling weighed on sentiment across the crypto market.

Summary

- Bitcoin fell to around $62,400 as options expiry, long liquidations, and Strategy sale concerns weighed on sentiment.

- Nearly $136 million in BTC positions were liquidated, with long traders accounting for roughly $122 million of losses.

- Analysts are closely watching the $61K-$62K support zone, with a break below potentially exposing a move toward $59K.

According to data from crypto.news, Bitcoin (BTC) fell nearly 3% over the previous 24 hours to an intraday low near $62,300 on June 19. The decline extended losses after roughly $2.13 billion in Bitcoin and Ethereum options contracts expired.

Investors also digested reports that Strategy could potentially sell between $3 billion and $4 billion worth of Bitcoin to support its STRC preferred stock, which recently traded below its $100 par value.

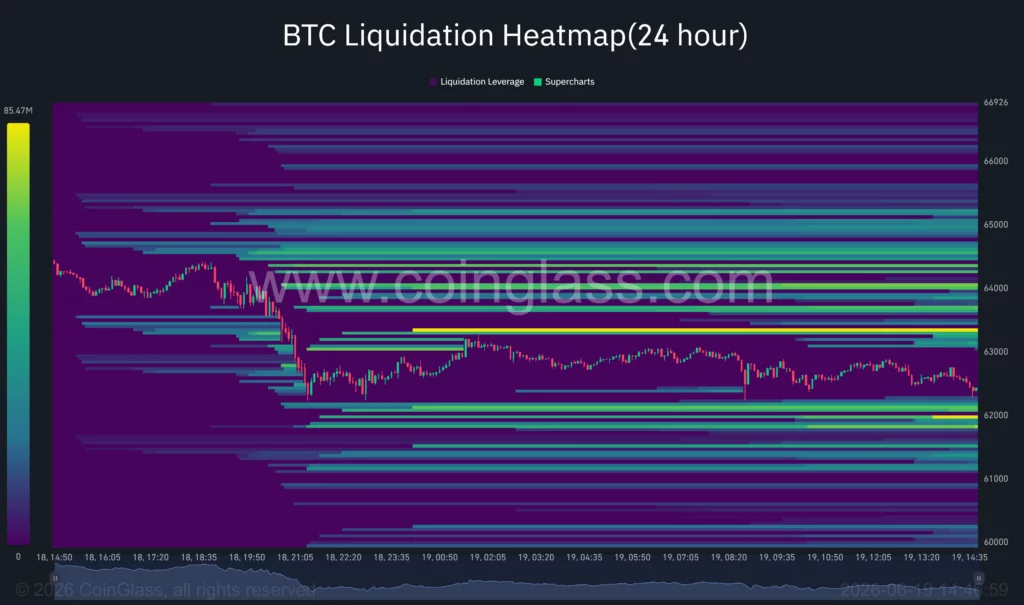

Further, CoinGlass data showed nearly $136 million worth of Bitcoin positions were liquidated over the past 24 hours, with about $122 million coming from long positions. The concentration of bullish liquidations added selling pressure as leveraged traders were forced out of positions during the drop below $63,000.

Outside crypto, investors faced another restrictive macro backdrop. The market continued to assess the implications of Federal Reserve Chair Kevin Warsh’s first policy meeting, where policymakers reinforced expectations that interest rates could remain elevated for longer. The stronger U.S. dollar that followed added pressure to risk assets, including cryptocurrencies.

Energy markets offered little relief. Crude oil rebounded from roughly $75 to above $77 per barrel after planned U.S.-Iran talks in Switzerland were canceled and Israel continued strikes against Hezbollah targets in Lebanon. Even so, oil remained on track for a weekly decline as traders continued to price in improved shipping conditions through the Strait of Hormuz following the interim U.S.-Iran peace arrangement.

Another source of pressure emerged from the mining sector. Institutional analytics showed Bitcoin has spent five consecutive months below an estimated network production cost of approximately $78,000. The prolonged gap has reportedly forced some mining operators to liquidate holdings to cover operating expenses and debt obligations.

Bitcoin tests critical Fibonacci and moving-average support

Technical indicators show BTC trading at a key inflection point. On the four-hour chart, price has fallen to the 78.6% Fibonacci retracement level near $62,410, measured from the June low around $59,176 to the recent recovery high near $74,288. A break below that level would leave the June bottom as the next major support zone.

Momentum indicators remain weak. The four-hour RSI has dropped to roughly 35 while the MACD remains below its signal line with expanding negative histogram bars.

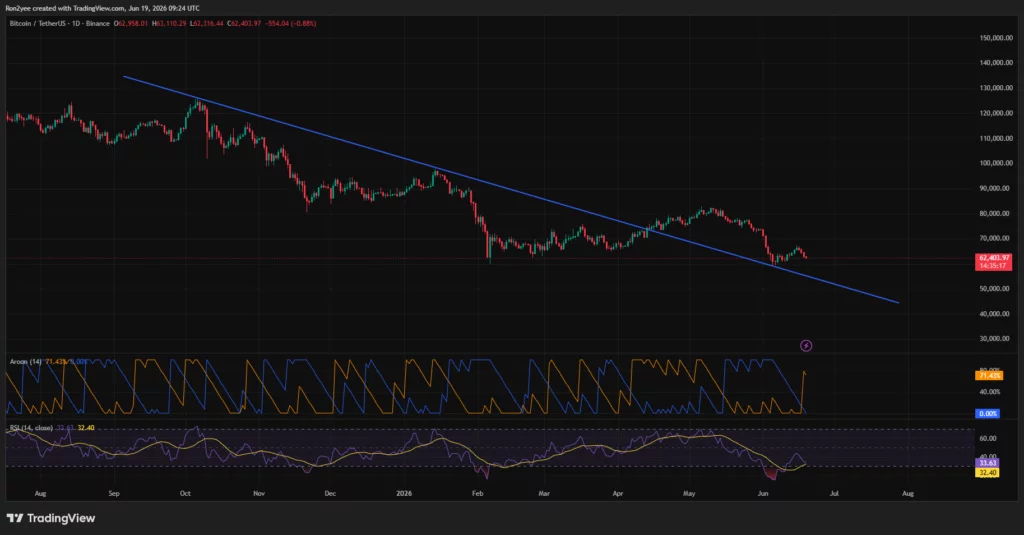

On the daily chart, Bitcoin continues to hold above a former descending resistance trendline that has now turned into support. Maintaining that structure remains important for bulls as the asset’s price approaches the $61,000-$62,000 support zone. The daily RSI sits near 34, while the Aroon indicator shows bearish dominance with the downtrend reading above 70 and the uptrend near zero.

Commenting on the setup, crypto analyst Daan Crypto Trades noted that Bitcoin is attempting to hold a major support region.

“Bulls need to hold that $61K-$62K region otherwise things get ugly real quick I think.”

Liquidity data highlights why that zone matters. CoinGlass heatmaps show dense liquidation clusters between $63,500 and $65,000, while another concentration of liquidity sits near $62,100. A recovery into the upper band could trigger short liquidations, whereas a move lower would expose fresh downside liquidity pockets.

According to crypto analyst Lennaert Snyder, Bitcoin’s drop to roughly $62,300 fulfilled a key liquidity target. He noted that $60,500 represents the first area where a bounce could emerge, while a deeper move below $59,000 would provide a more attractive setup for a sustained reversal.

Failure to reclaim $65K could expose lower support zones

The primary risk for bulls remains Bitcoin’s inability to reclaim overhead resistance. The 61.8% Fibonacci retracement level sits near $64,950, while the midpoint of the recent range is located around $66,700. Those levels coincide with significant liquidation clusters identified on derivatives exchanges.

Another concern comes from institutional positioning. Recent ETF outflows and continued capital rotation toward technology and artificial-intelligence equities have reduced demand for Bitcoin during a period of heightened macro uncertainty.

Should BTC lose the $61,000-$62,000 support area, traders may shift attention toward the June low near $59,000. A decisive break below that level would strengthen the case for a deeper correction and place longer-term support zones in the mid-$40,000 region back into focus.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

For the first time on Venus, tokenized stock positions can be used as collateral while maintaining exposure to stock price movements.

Venus Protocol today launched the first tokenized stocks collateral market on BNB Chain, integrating Binance tokenized stocks (bStocks) into Venus Core Pool. The launch marks a meaningful expansion of what on-chain lending markets can support: tokenized stocks are no longer limited to passive holding, they can now serve as collateral within DeFi.

What You Can Do with bStocks on Venus

Eligible users can supply bStocks to Venus Core Pool as collateral, maintaining exposure to price movements of tokenised stock instruments while unlocking borrowing power on-chain. Those positions can be used to borrow any supported asset in Venus Core Pool, including stablecoins such as USDT, USDC, and U, as well as other listed tokens without requiring a sale.

Venus Core Pool is the largest decentralized lending market on BNB Chain. With bStocks listed alongside BTC, ETH, BNB, and major stablecoins, tokenized stocks now participate in the same shared liquidity infrastructure that supports billions in active on-chain lending, part of the core financial stack, not a standalone product.

The addition of bStocks follows growing adoption of tokenized assets on Venus. Earlier tokenized commodity markets, including XAUm, demonstrated demand for using real-world asset exposure within DeFi. With bStocks, Venus extends that model from commodities to equities, broadening the range of tokenized assets that can participate in on-chain collateral markets.

Built Across the BNB Chain Ecosystem

This launch reflects close collaboration across the BNB Chain ecosystem, with Venus serving as the lending layer at the center.

Binance provides the tokenization infrastructure: users can convert existing Direct Stock holdings into bStocks at no fee, or purchase them directly on Binance Spot. PancakeSwap and Trust Wallet provide access to on-chain secondary market liquidity. Once held in a self-custody wallet, bStocks can be supplied to Venus or deployed as collateral, completing the path from tokenized stock exposure to active DeFi participation.

“Tokenized assets are becoming a real bridge between traditional finance and on-chain infrastructure, not just a concept, but a working product. By letting users access liquidity against their tokenized stock positions without selling, Venus Protocol is expanding what collateral looks like on BNB Chain.” — Leon, Head of BD, Venus Protocol

A Phased Rollout

The initial rollout supports a limited set of assets under conservative risk parameters set through Venus governance. Any expansion to additional tokenized stocks or related markets would be determined through Venus governance.

Important Risk Information

Capital is at risk.

Tokenized stocks represent exposure to underlying stock markets and may be affected by market volatility, trading hours, corporate actions, and other factors related to the underlying asset. Their value also depends on third-party issuers, market makers, available liquidity, and on-chain price feeds.

Borrowing positions may be liquidated automatically and without notice if collateral values fall below applicable thresholds.

Participation is subject to eligibility requirements, geographic restrictions, onboarding procedures, and applicable Terms of Use. Rights associated with tokenized stocks may differ from those associated with direct ownership of the underlying stock.

This material is for information only and is not investment advice. Users should carefully review all relevant disclosures and market documentation before participating.

About Venus Protocol

Venus is the leading decentralized lending protocol on BNB Chain. Founded in 2020 as the first lending protocol on the network, Venus supports over 30 assets and reached $2.8 billion in TVL in 2025. The protocol offers two products: Venus Core, the flagship product for participants seeking deep liquidity and broad asset coverage, and Venus Flux, a product built for enhanced capital efficiency.

Security is foundational to Venus’s development practice. Every smart contract change undergoes an independent audit before deployment — resulting in over 80 completed audits across leading firms, among the most extensive audit records in DeFi.

The post Venus Protocol Launches Tokenized Stocks as Collateral on BNB Chain appeared first on BeInCrypto.

The two assets the world buys to protect against uncertainty and debasement are the only two losing money this year, while stocks of every kind climb. It has never happened before. Untangling why reveals what is actually driving markets in 2026, and what it means for the stories crypto tells about itself.

Summary

- Bitcoin and gold are the only major asset classes in the red for 2026.

- The weakness is driven by rotation, mean reversion, a stronger dollar, and higher real yields.

- Bitcoin’s digital-gold thesis is being stress-tested, not fully disproven.

- The lesson is that short-term safe-haven claims are weaker than long-term store-of-value claims.

Something has happened in 2026 that has never happened before. Bitcoin and gold, the two assets most commonly held as protection against uncertainty and the debasement of money, are the only two major asset classes in the red for the year, with Bitcoin down roughly 27% and gold down about 3%, according to market analyst Charlie Bilello.

Meanwhile almost everything else is up: the S&P 500 has gained around 9%, small-cap stocks have risen about 19%, value stocks are up roughly 15%, and emerging-market equities are outperforming. The two assets people buy when they fear chaos are falling while the assets people buy when they feel confident are climbing.

According to 15 years of Bilello’s data, Bitcoin and gold have never before finished a calendar year together as the two worst performers among the majors.

This is truly strange, and it is worth sitting with rather than explaining away, because the explanation reveals what is actually driving markets in 2026 and forces a hard question about the stories crypto tells about itself. Bitcoin’s bull narrative has long leaned on two ideas: that it is digital gold, an uncorrelated store of value, and that it is a hedge against monetary debasement and uncertainty.

A year in which both Bitcoin and gold fall while every flavor of stock rises puts both ideas under stress at once. This piece works through why the two safe havens are the only losers, what the rotation into equities is really about, why the Fed and the dollar matter so much, what it does and does not mean for the digital-gold thesis, and how to read a divergence this unusual without overreacting to it.

The numbers, and why they are so strange

The strangeness is in the pattern, not just the losses, so it is worth laying out clearly before explaining it.

Through this point in 2026, Bitcoin is down about 27% and gold is down about 3%, and they are the only two major asset classes in negative territory for the year. Set against them, the breadth of the gains everywhere else is striking: the S&P 500 up around 9%, small-cap stocks up roughly 19%, value stocks up about 15%, and emerging-market and international equities outperforming as well.

This is not a case of a weak market dragging everything down, where safe havens falling might make sense as part of a general decline. It is close to the opposite: a broadly strong market for risk assets in which the two classic safe havens are the conspicuous exceptions, falling while nearly everything else rises.

That combination is what makes the year unprecedented in Bilello’s 15-year record, because Bitcoin and gold falling together to the bottom of the table has simply not happened before.

The contrast with recent history sharpens the oddity. Gold gained more than 63% in 2025 and about 27% in 2024, an extraordinary two-year run, and Bitcoin returned 121% in 2024 during one of its strongest periods.

These are assets coming off enormous gains, not assets in long structural decline, which is part of what makes their simultaneous 2026 weakness so notable. They are not failing assets; they are former leaders that have abruptly become the year’s laggards while the rest of the market does the opposite of what they are doing.

Bitcoin in particular is suffering its longest and deepest drawdown since 2022, a decline stretching beyond 200 days and exceeding 50% from its peak, having given back the gains it made after the 2024 election on the expectation of a crypto-friendly administration. The puzzle is not that two assets fell; it is that these two assets, with these histories, fell together and alone while everything else climbed.

The rotation: where the money went

The first and largest part of the explanation is rotation, the movement of capital from one part of the market to another, and 2026 has been a year of dramatic rotation.

Capital does not vanish when it leaves an asset; it goes somewhere else, and in 2026 it has rotated out of the assets that led in prior years and into the ones that lagged. Bilello has described the year as a “reversal of everything,” in which the patterns of recent years inverted.

Emerging and international stocks are beating the S&P 500, value stocks are beating growth, small and mid-caps are beating large caps, and even the dominant technology megacaps that led the market for years have struggled. The so-called Magnificent Seven are in the red for the period.

This is a wholesale rotation away from the recent winners and into the recent laggards. Bitcoin and gold, having been among the biggest winners of 2024 and 2025, are natural sources of the capital flowing out and natural targets of the profit-taking that rotation produces.

Money that sat in gold and Bitcoin after their huge runs has been moving into the cheaper, previously-unloved corners of the equity market. That is one reason capital rotating out of crypto matters: crypto exposure is no longer isolated from public-market rotation, especially as more crypto-linked stories enter traditional portfolios.

Part of this is simple mean reversion, the tendency of assets that have risen far above their averages to pull back toward them. Gold up 63% in a year and Bitcoin up 121% the year before are assets that ran far and fast, and some of their 2026 weakness is the natural give-back after extraordinary gains.

The market is taking profits in the leaders and redeploying into laggards that look cheap by comparison. Bilello has attributed the safe-haven weakness specifically to a combination of mean reversion, a stronger dollar, and higher nominal and real interest rates.

Those three forces together explain much of why gold and Bitcoin have struggled while equities have thrived. The rotation is the visible flow; mean reversion, the dollar, and rates are the deeper currents driving it.

The short version is that capital rotated out of the crowded safe-haven trade and into the rest of the market, and the assets it left behind are the ones now in the red.

The dollar and real yields: the deeper force

Underneath the rotation sits a macro force that hits gold and Bitcoin with particular precision, and it explains why these two assets specifically are the ones falling.

Gold and Bitcoin share a defining feature that makes them uniquely sensitive to interest rates: neither pays a yield. Gold generates no interest or dividend, and neither does Bitcoin, so the entire return from holding either comes from price appreciation.

The cost of holding them is the yield you forgo by not putting that money into something that pays. When interest rates are low, that forgone yield is small and holding a non-yielding asset costs little, which is part of why gold and Bitcoin thrived in the low-rate years.

When real interest rates, rates adjusted for inflation, rise, the calculus flips. Holding a non-yielding asset means giving up a meaningful, safe return available elsewhere, which makes gold and Bitcoin less attractive and pressures their prices.

Rising real yields are a specific, mechanical headwind for exactly the two assets that are falling, because they are the two major assets that pay nothing to hold. That is why the Fed turn behind the move matters so much.

The dollar compounds the effect. Gold and Bitcoin are both priced in dollars and both function, in part, as alternatives to the dollar as a store of value, so when the dollar strengthens, they tend to weaken.

That happens both mechanically, because a stronger dollar buys more of a dollar-priced asset, and thematically, because a strong dollar undercuts the case for holding alternatives to it. The dollar index has been strong in 2026 and, by some readings, on the verge of a major breakout, and a rising dollar is a direct headwind for both safe havens at once.

Put the pieces together and the picture is coherent: a hawkish Fed keeps rates high and the dollar strong, high rates raise real yields, high real yields and a strong dollar both pressure non-yielding dollar-alternative assets, and gold and Bitcoin are precisely those assets. The macro environment of 2026, higher real rates and a stronger dollar, is almost custom-built to pressure the two assets that are in the red.

That is also the energy-inflation backdrop, where oil, inflation, and Fed policy feed directly into the rates and dollar setup hurting safe havens.

What it means for the digital-gold thesis

Now the uncomfortable question for crypto specifically, because a year like this puts Bitcoin’s core narrative under direct stress, and the honest reading is more nuanced than either the bulls or the bears would have it.

Bitcoin’s bull case has long rested partly on two related claims: that it is “digital gold,” an uncorrelated store of value that holds up when other assets fall, and that it is a hedge against monetary debasement and uncertainty. A year in which Bitcoin falls 27% while equities rise complicates the uncorrelated-store-of-value claim.

An uncorrelated safe haven is supposed to hold its value when risk assets are volatile, not fall while they climb, and Bitcoin’s deep drawdown amid a strong equity market looks more like a risk asset selling off than a safe haven doing its job. And the fact that gold, the original safe haven, is also falling does not rescue the digital-gold comparison so much as extend the problem.

If Bitcoin is digital gold, then it is tracking gold straight to the bottom of the table, which is not the behavior the safe-haven thesis promises in a strong-market year. That is why crypto’s correlation with risk assets remains one of the hardest questions for the thesis.

But the nuance matters, and it cuts in Bitcoin’s favor too. The fact that Bitcoin and gold are falling together is itself evidence that they are responding to the same macro forces, higher real yields and a stronger dollar, which is exactly what you would expect of two non-yielding stores of value.

In that sense, Bitcoin is behaving like digital gold, just digital gold in a year when gold itself is out of favor. The thesis was never that gold or Bitcoin rises every year; it is that they serve a particular role over long horizons.

A single year of rotation-driven, rate-driven weakness after two years of enormous gains does not refute a multi-year store-of-value case any more than gold’s frequent down years refuted its role over centuries. The honest synthesis is that 2026 is a real stress test of the digital-gold narrative.

It exposes that Bitcoin still trades with significant risk-asset sensitivity and does not reliably act as a safe haven in the short run. It also shows Bitcoin moving in sympathy with gold under shared macro pressure, which is at least consistent with the longer-term comparison.

The year challenges the thesis without settling it.

How to read a divergence this unusual

A pattern this rare invites overreaction in both directions, so the discipline is to read it for what it is without forcing it into a story it does not support.

The bearish overreaction is to declare the safe-haven and digital-gold theses dead, to treat one unusual year as proof that Bitcoin and gold have lost their roles permanently. This goes too far, because a single year of rotation and rate-driven weakness, following two years of exceptional gains, is well within the normal range of how these assets behave over time.

Both have long histories of significant down years that did not end their long-run roles. Gold has been a store of value across centuries punctuated by frequent declines, and Bitcoin’s longer record, despite this drawdown, remains one of extraordinary cumulative returns.

One strange year is a data point, not a verdict, and reading it as a verdict is the kind of narrative-following-price that markets punish.

The bullish overreaction is the mirror image: to dismiss the year entirely as noise and insist nothing has changed, ignoring what the divergence reveals. That also goes too far, because the year does carry a real lesson.

Bitcoin still behaves with meaningful risk-asset sensitivity and does not reliably provide safe-haven protection in the short term, which is clearly relevant for anyone holding it for that purpose. The measured reading sits between the overreactions.

2026 shows that the macro environment of higher real yields and a stronger dollar can pressure Bitcoin and gold together, that Bitcoin’s safe-haven behavior is unreliable over short horizons, and that the rotation out of recent winners can hit even the strongest prior performers. None of that refutes the long-term store-of-value case or proves the assets have lost their roles.

The right response to an unusual year is to update toward humility about short-term safe-haven claims without abandoning the longer-term thesis, holding both the lesson and its limits at once.

What it means for investors

For anyone holding or considering Bitcoin or gold, the 2026 divergence offers a concrete and useful lesson about what these assets are and are not.

The lesson is that Bitcoin, and to a lesser degree gold, do not reliably function as short-term safe havens or uncorrelated hedges, and that in a macro environment of higher real yields and a stronger dollar they can fall even as risk assets rise. An investor holding Bitcoin specifically for downside protection or non-correlation should weigh this year as evidence that those properties are unreliable on short horizons, and should not assume Bitcoin will hold up when they most want it to.

At the same time, the year does not invalidate the long-term case for either asset. An investor with a multi-year horizon who holds Bitcoin or gold as a long-run store of value can reasonably view 2026 as a rotation-and-rates-driven drawdown rather than a structural break, especially given both assets’ histories of recovering from down years.

The horizon matters enormously. The short-term safe-haven claim looks weak this year, while the long-term store-of-value claim remains a separate question this year does not settle.

The practical discipline is to hold these assets for the role they actually play over your horizon rather than the role the narrative promises in every environment. If you want short-term, reliable downside protection, 2026 is a reminder that Bitcoin does not consistently provide it, and that other tools may suit that purpose better.

If you hold Bitcoin or gold as a long-term store of value and can tolerate years like this one, the divergence is a stress test passed or failed only over time, not in a single year. Watching the macro forces driving the divergence, real yields and the dollar, gives a clearer sense of when the pressure on these assets might ease than any narrative about safe havens can.

This is the bigger drawdown question: whether this is a cyclical reset inside a longer thesis, or the beginning of a deeper reassessment of crypto’s role in portfolios.

None of this is investment advice; it is a frame for reading an unusual year accurately, without the overreactions that an unprecedented pattern tends to provoke.

The safe havens that were not, this year

The defining oddity of 2026 is that the two assets the world holds to protect against uncertainty and debasement, Bitcoin and gold, are the only two major asset classes losing money, while stocks of every kind, large and small, value and emerging, climb around them.

It has never happened before in 15 years of data, and it is truly strange, but it is not inexplicable. Capital rotated out of the crowded safe-haven trade after two years of enormous gains, mean reversion pulled the former leaders back, and a hawkish Fed delivered higher real yields and a stronger dollar that fall with particular force on exactly the two non-yielding, dollar-alternative assets now in the red.

The pattern is unusual; the forces behind it are not mysterious.

What it means is more nuanced than either the death of the safe-haven thesis or business as usual. The year is a real stress test, showing that Bitcoin still trades with significant risk-asset sensitivity and does not reliably protect on short horizons, and that even the strongest prior performers can become a rotation’s casualties.

It also shows Bitcoin moving in sympathy with gold under shared macro pressure, which is at least consistent with the digital-gold comparison, just in a year when gold itself is out of favor. The measured reading updates toward humility about short-term safe-haven claims while leaving the long-term store-of-value case unsettled, a question only years can answer.

Bitcoin and gold being the only assets red in 2026 is a striking fact and a genuine lesson about what they are in the short run. But it is one unusual year, and the assets that have been left behind by this rotation have been left behind before, and have not always stayed there.

Frequently asked questions

Are Bitcoin and gold really the only major assets down in 2026?

Yes. According to market analyst Charlie Bilello, Bitcoin and gold are the only two major asset classes in the red for 2026, with Bitcoin down roughly 27% and gold down about 3%, while the S&P 500 is up around 9%, small-cap stocks up about 19%, and value stocks up roughly 15%.

Per Bilello’s 15-year data, Bitcoin and gold have never before finished a year together as the two worst-performing major assets.

Why are the two safe-haven assets falling while stocks rise?

Mainly rotation and macro forces. Capital has rotated out of the recent winners, including gold and Bitcoin after two years of huge gains, and into previously lagging areas like small-caps, value, and emerging markets, a shift Bilello calls the “reversal of everything.”

Underneath, a stronger dollar and higher real interest rates pressure gold and Bitcoin specifically because both are non-yielding, dollar-priced assets, making them less attractive when safe yields rise and the dollar strengthens.

Does this disprove that Bitcoin is digital gold?

Not exactly. A year where Bitcoin falls while stocks rise does complicate its claim to be an uncorrelated safe haven, showing it still trades with real risk-asset sensitivity.

But the fact that Bitcoin and gold are falling together suggests both are responding to the same macro forces, which is consistent with the digital-gold comparison, just in a year when gold itself is out of favor. The year stress-tests the thesis without settling the long-term store-of-value case.

Why do higher interest rates hurt Bitcoin and gold specifically?

Because neither pays a yield. The entire return from holding gold or Bitcoin comes from price appreciation, and the cost of holding them is the yield you give up elsewhere.

When real interest rates rise, that forgone yield becomes significant, a safe return you sacrifice to hold a non-yielding asset, which makes both less attractive and pressures their prices. This is why rising real yields are a precise headwind for exactly the two assets that are falling.

Is the drop in Bitcoin and gold a sign they have lost their role?

Probably not, though it is a real stress test. A single year of rotation-driven, rate-driven weakness, following two years of exceptional gains, is within the normal range of how these assets behave, and both have long histories of down years that did not end their long-run roles.

Declaring the safe-haven thesis dead over one unusual year overreaches. But the year does carry a genuine lesson that Bitcoin’s short-term safe-haven behavior is unreliable.

What should investors take from this divergence?

That Bitcoin, and to a lesser extent gold, do not reliably function as short-term safe havens, and can fall even as risk assets rise in a high-real-yield, strong-dollar environment. Investors holding Bitcoin for short-term downside protection should weigh that those properties are unreliable on short horizons.

Those holding it as a long-term store of value can view 2026 as a rotation-and-rates drawdown rather than a structural break. The horizon matters: the short-term claim looks weak this year; the long-term question remains open.

As of June 19, 2026. Markets are volatile and figures change quickly; verify current data before relying on this analysis. This article is information, not investment advice.

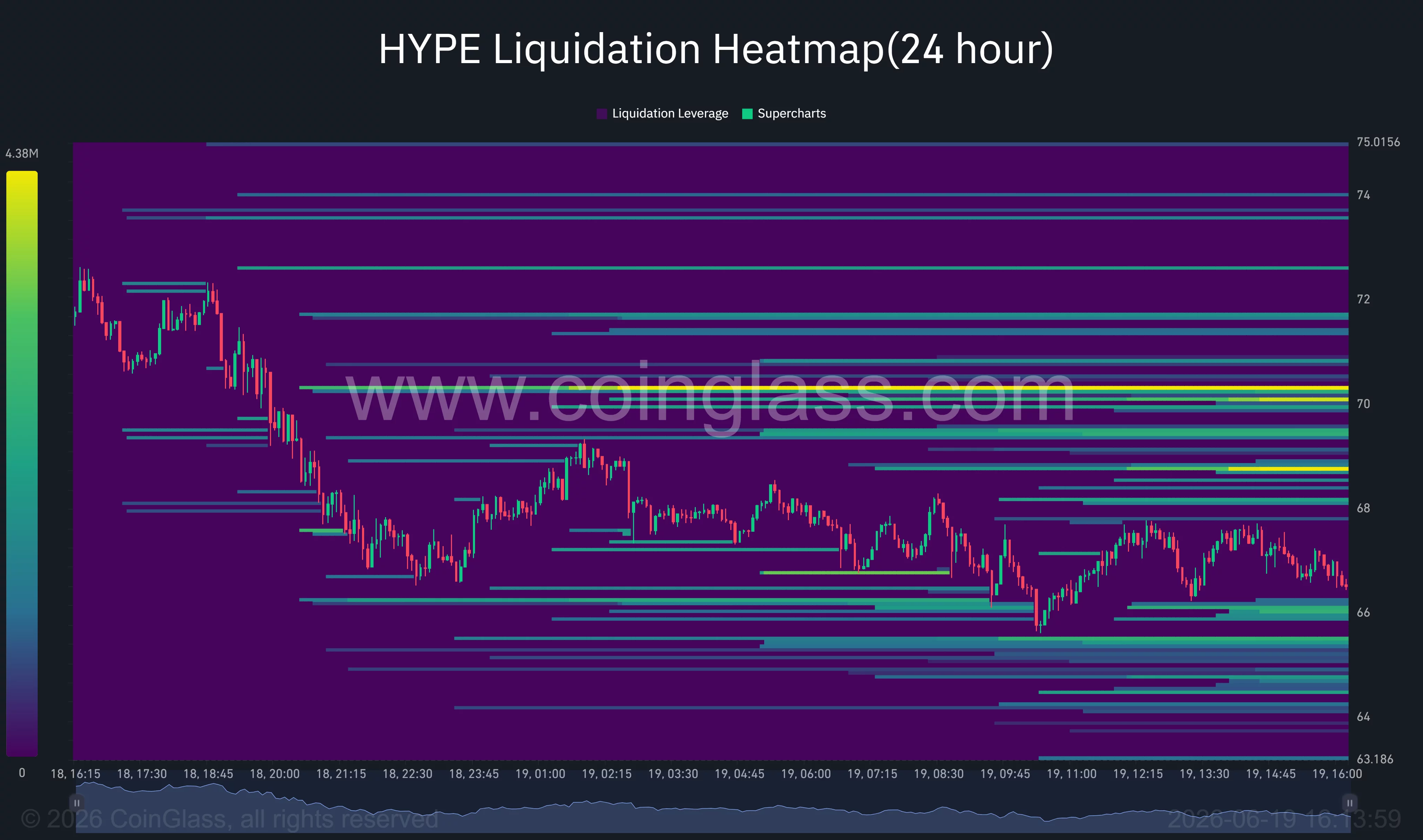

Hyperliquid has retreated more than 13% from its record high after a wave of profit-taking hit HYPE, while traders assess whether a newly formed double-top pattern could trigger a deeper correction.

Summary

- HYPE has dropped more than 12% from its $76.70 all-time high as profit-taking accelerates.

- A double-top pattern on the 4-hour chart puts key support levels near $65 and $62 in focus.

- Liquidation clusters between $70 and $72 could fuel volatility as traders battle for direction.

According to data from crypto.news, Hyperliquid (HYPE) price fell to an intraday low near $65.7 on June 19, extending losses from its June 16 all-time high of $76.70.

The pullback followed one of the strongest rallies in crypto this month, fueled by heavy derivatives activity, a short squeeze, and enthusiasm surrounding tokenized SpaceX exposure on the Hyperliquid ecosystem.

The decline has unfolded alongside a risk-off move across digital assets after Federal Reserve Chair Kevin Warsh reinforced a hawkish policy stance during his first meeting at the helm of the U.S. central bank. Higher-for-longer rate expectations strengthened the dollar and pressured speculative assets, prompting traders to reduce exposure across altcoins.

Additional pressure came from Hyperliquid’s recent token unlock. Earlier this month, roughly 9.9 million HYPE tokens entered circulation as part of a scheduled vesting event worth about $700 million at prevailing prices. Although Hyperliquid’s fee-funded buyback mechanism helped absorb much of that supply during the rally, the market has become more sensitive to any slowdown in trading activity.

Network activity remains elevated by historical standards, but perpetual trading volume has eased from the peak levels recorded during HYPE’s surge toward $77. With fewer buyback-driven purchases entering the market, short-term traders have become more willing to lock in gains after the token’s rapid ascent.

Double-top pattern puts key support levels in focus

The four-hour chart shows HYPE carving out a clear double top near the $76.70-$77 region, a pattern that often appears near local market peaks. HYPE has already broken below the 0.618 Fibonacci retracement level around $67.7 and is testing support between $64.8 and $65.

A decisive break beneath the $64.8 neckline area would strengthen the bearish setup and increase the probability of a move toward the next Fibonacci support near $62, followed by the $58.4 region. The measured target derived from the double-top structure also aligns with a potential decline toward the upper-$50 range.

Momentum indicators have weakened. On the four-hour chart, the MACD has crossed lower and remains below its signal line, while Chaikin Money Flow has slipped into negative territory at approximately -0.06, suggesting capital has been leaving the asset during the recent selloff.

The daily chart presents a mixed picture. HYPE continues to trade above major support near $56.5, but price remains below the daily Supertrend resistance at roughly $74.3. Bulls would need to reclaim the $70-$72 zone to invalidate the immediate bearish structure and reopen the path toward the recent highs.

Liquidation clusters create battleground between $70 and $72

CoinGlass liquidation heatmap data shows a dense concentration of leveraged positions between $69.5 and $72. Strong liquidation bands are clustered around $70 and $71.8, creating a magnet zone if buyers regain control.

Meanwhile, sizeable liquidity pockets have formed below the market around $65 and $64. A breakdown into those levels could trigger another round of long liquidations and accelerate downside volatility.

According to analyst Lennaert Snyder, Bitcoin recently swept liquidity around $62,300 and may seek lower levels before establishing a durable bottom. While Snyder’s comments focused on Bitcoin, continued weakness in the market leader could add pressure across high-beta assets such as HYPE.

“$BTC swept 62.3K liquidity and hit our target,” Snyder wrote, adding that he would prefer to see fresh lows below $59,000 before considering a more durable reversal.

A recovery in crypto sentiment, renewed derivatives activity, and a move back above $70 would improve HYPE’s outlook. Until then, traders remain focused on whether the double-top breakdown extends toward the mid-$50 support zone or stabilizes before a larger trend reversal develops.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

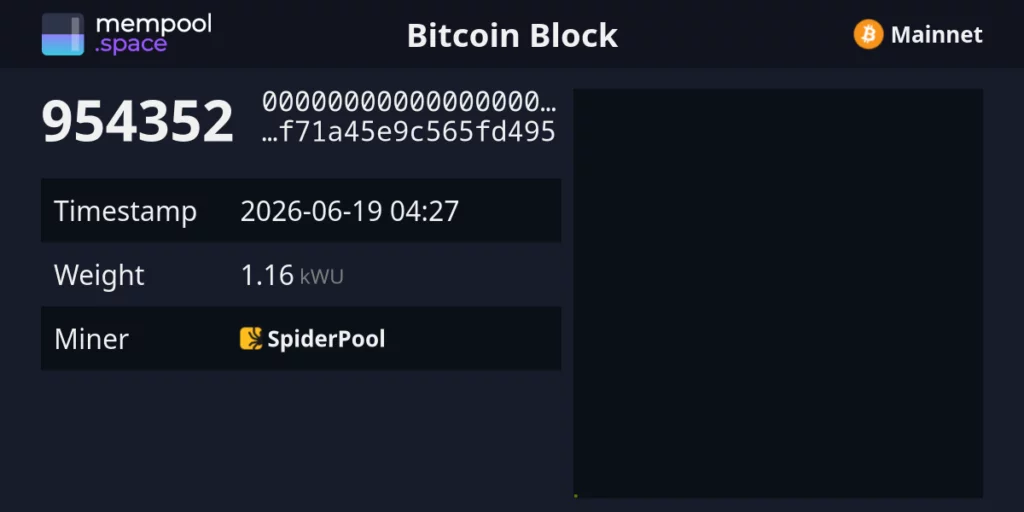

Bitcoin mined an empty block at height 954,352, according to Mempool data.

Summary

- SpiderPool mined Bitcoin block 954,352 with only the coinbase transaction and no user transactions included.

- The 62-second gap points to fast miner template timing, not a clear network problem today.

- Empty Bitcoin blocks have happened before, but repeated cases would draw closer miner behavior scrutiny.

The block contained only the coinbase transaction, meaning it carried the miner reward but no regular user transactions.

The block was mined by SpiderPool. Mempool data showed a timestamp of 2026-06-19 04:27 and a block weight of 1.16 kWU.

Short block gap draws attention

The empty block came about 62 seconds after the previous Bitcoin block. That short gap is the main reason traders and network watchers flagged the event.

A fast block gap can leave miners working with a coinbase-only template before a fuller transaction template reaches mining hardware. That can produce a valid empty block.

Meanwhile, empty Bitcoin blocks are not new. In June 2024, Mempool Research noted that empty blocks have appeared throughout Bitcoin’s history, though they are now rare.

The research explains that mining pools may send empty templates because they are smaller and faster to transmit. The tradeoff is that the miner gives up transaction fees from that block.

Repeated behavior would matter more

A single empty block does not show a Bitcoin network issue. It does not halt settlement, reverse transactions, or break consensus rules.

The event would matter more if empty blocks appeared repeatedly. That could raise fresh questions about miner timing choices and whether some pools are prioritizing speed over fee revenue.

As previously reported by crypto.news, miner timing incentives have been discussed in research around selfish mining risks. This empty Bitcoin block is not the same as selfish mining, but it adds another data point for analysts watching miner behavior.

Moreover, as crypto.news covered in 2022, Bitcoin SV faced empty-block issues, though that case involved a different network and a more severe pattern. For Bitcoin, block 954,352 is best read as a rare but known mining event unless the pattern continues.

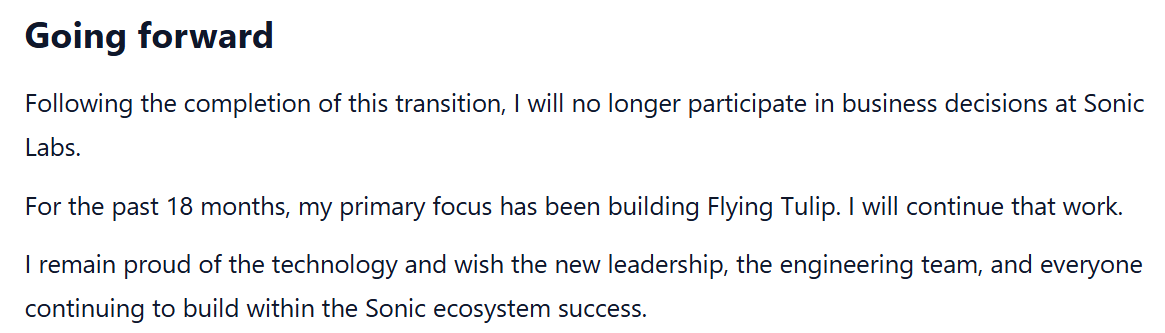

The S token, the native utility asset behind the Sonic blockchain, fell 5% on Friday after Sonic Labs, formerly known as the Fantom Foundation, announced the resignation of three former executives from its board.

The S token fell to 0.031 on Friday, down 5% over 24 hours. The resignations include Michael Kong, a former CEO of the Fantom Foundation and director at Sonic Labs; David Richardson, who served as executive chairman of Sonic Labs; and Andre Cronje, who previously served as its chief technology officer.

Statement from Andre Cronje about his resignation from the board. Source: Andre Cronje

“These are the people who built what Sonic is today. They remain invested in Sonic’s success and are handing off their responsibilities the right way, in full. From here, they will no longer make business decisions for the organization,” Sonic Labs said as it announced Matt Visser as its new CEO and Kosta Kourkoumelis as chief operating officer.

Sonic Labs is overhauling its leadership and governance structure as it attempts to address growing community dissatisfaction and a prolonged decline in its S token, which has fallen 97% since launching in January 2025 as part of a network upgrade.

“We are not going to open with a victory lap. The token is down. Community sentiment is down. We see both clearly, we are not spinning it, and we are not asking anyone to pretend otherwise,” said Sonic Labs.

Related: Ethereum faces core development funding crisis, former contributor warns

Sonic Labs, the research and development organization behind the Sonic EVM-compatible layer-1 blockchain, is the successor to the Fantom Foundation, which was founded in 2018.

The blockchain is focused on speed, claiming to provide 10,000 transactions per second and subsecond finality. Its rebrand from Fantom to Sonic introduced a major structural and technical upgrade to the network as it replaced its legacy Fantom Opera network.

Sonic Labs said the leadership change will also come with a commitment to more transparent governance, clear communication about project updates, and the creation of a dedicated risk and compliance committee.

The leadership shuffle comes just days after Ethereum Foundation co-executive director Hsiao-Wei Wang announced that she had stepped down on Thursday, adding to a list of 19 layoffs and departures from the foundation this year.

Magazine: The end of anon? AI could unmask crypto’s hidden identities

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

As football fans celebrate the World Cup journey, CoinEx highlights the shared values of perseverance, growth, and long-term commitment in crypto.

Summary

- CoinEx links World Cup ambition with crypto growth, celebrating belief, resilience, and long-term progress.

- Inspired by football’s road to glory, CoinEx highlights persistence, user focus, and blockchain opportunity.

- CoinEx marks the World Cup season with a campaign honoring believers, contenders, and champions in crypto.

Every four years, the world comes together to witness football’s greatest stage. On the pitch, glory is never achieved overnight. Behind every victory lies years of preparation, discipline, setbacks, and perseverance. Long before champions lift the trophy, they begin with a simple belief — that their effort can lead to something greater.

The same spirit exists beyond football. In crypto, every user is a challenger navigating uncertainty, opportunity, and constant change. Success is never defined by a single moment. It is built through persistence, learning, and the willingness to move forward through every cycle.

As the world celebrates the pursuit of glory on the pitch, CoinEx celebrates the same spirit shared by millions across the global blockchain community.

Every champion starts as a believer

Before victories, recognition, or defining moments, there is always a first step. For football players, it is the belief that years of training can lead to the world’s biggest stage. For crypto users, it is the belief that blockchain can unlock new possibilities and global opportunities.

Belief is the beginning of every journey. It gives people the courage to embrace uncertainty, explore new paths, and pursue undefined goals.

Since its founding in 2017, CoinEx has shared this belief. Guided by its mission: “Via blockchain, make the world a better place”, CoinEx has enabled more people to participate in the blockchain economy. What began as a belief has grown into a global platform serving users across regions, languages, and market cycles.

Great challenges create great contenders

No World Cup campaign is won in a single match, and no meaningful progress in crypto is achieved through a single trade. Every journey is shaped by uncertainty and resilience.

Over the past decade, the blockchain industry has gone through multiple cycles of transformation. Through every phase, users have continued to learn and adapt through real participation.

CoinEx has moved through these cycles alongside its users. From a trading platform to a broader ecosystem — including CoinEx Wallet, CoinEx Vault, CoinEx Smart Chain, CoinEx Explorer, and CoinEx Charity — CoinEx has grown around one core principle: User Centric.

Every decision and product iteration is guided by one commitment: understanding user needs and supporting their journey. Because every contender deserves a platform that stands with them through every challenge.

Expertise is earned through every cycle

In football, experience builds trust. The most respected teams are defined not by a single victory, but by consistent performance over time. Their reputation is proven, not declared.

The same is true in crypto. “Being your crypto trading expert” is not about predicting every market move, but about remaining reliable across conditions and helping users navigate uncertainty with clarity and confidence.

It is about understanding users, responding to their needs, and continuously improving the trading experience.

CoinEx has spent nearly a decade building a secure, accessible, and reliable trading environment. Across changing market conditions, one principle has remained unchanged: putting users first.

Glory belongs to those who keep moving forward

Champions are not defined solely by the trophies they lift. They are defined by the persistence that carries them through uncertainty, setbacks, and moments of doubt.

This World Cup season, CoinEx celebrates every challenger pursuing their own version of success. To bring this spirit into action, CoinEx has launched three core World Cup experiences:

The limited-edition CoinEx × ViaBTC World Cup jerseys, each representing a stage on the road to glory:

- The BELIEVER — the courage to begin

- The CONTENDER — the drive to compete through challenges

- The CHAMPION — the moment persistence becomes achievement

More than designs, they represent a shared journey from belief to glory.

At the same time, CoinEx opens the All In The Glory Futures PnL Ranking, where users enter a global competitive arena and compete for a share of the 15,000 USDT prize pool. Every trade becomes part of a real-time contest of skill, discipline, and performance.

For those just beginning their journey, the Newcomer Exclusive Reward Program provides a structured first step into the arena:

- Deposit & ≥ 40 USDT → 40 USDT fee rebate

- Spot trading & ≥ 50 USDT → 30 USDT fee rebate

- Futures trading & ≥ 300 USDT → 30 USDT fee rebate

- Up to 100 USDT total rewards for new users

Every journey begins with a first step. And every step deserves recognition.

All In The Glory

- Every champion starts as a believer.

- Every contender is shaped through challenges. Every expert is earned through every cycle.

- And every moment of glory is achieved through perseverance.

This World Cup season, CoinEx salutes every challenger continuing their journey toward something greater.

The Believer. The Contender. The Champion.

ALL IN THE GLORY.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Ethereum is facing an urgent funding squeeze for its core development work, according to a warning from a former Ethereum Foundation contributor. Trenton Van Epps said the network’s funding apparatus could be pushed into a “slow-burning funding crisis” within the next three to nine months as key Foundation spending cuts and program expirations reduce the pool of ecosystem support.

The concern arrives amid a broader period of organizational churn at the Ethereum Foundation. Cointelegraph reported a continuing wave of leadership exits, including co-executive director Hsiao-Wei Wang announcing Thursday that she would step down—bringing departures and layoffs at the Foundation to 19 so far this year, according to the report.

Key takeaways

- Former Ethereum Foundation contributor Trenton Van Epps warns that the Ethereum ecosystem may need about $30 million annually to sustain core development.

- He links the risk to the Foundation’s spending reduction and the expiration of the Client Incentive Program in April.

- Ethereum co-founder Vitalik Buterin previously argued the Foundation has limited resources and framed its remaining ETH holdings as supporting “longevity over breadth.”

- Earlier treasury actions—un-staking and sales of ETH—suggest the Foundation has been adjusting its strategy to raise funds for protocol work.

A looming gap in core development support

In a blog post published Thursday, Van Epps said he is drawing his assessment from discussions with core development contributors. His central claim is that Ethereum’s core development ecosystem currently requires roughly $30 million in annual funding to function effectively.

Van Epps attributed the funding pressure to two concrete developments: the Ethereum Foundation’s reduction in spending and the expiration of the Client Incentive Program in April. Those changes, he argues, reduce recurring support for the teams and contributors that help keep Ethereum’s core clients and infrastructure moving.

“Slow-burning” is the key phrase here—rather than an immediate collapse, Van Epps suggests the situation may worsen gradually as funding for ongoing engineering efforts becomes harder to maintain. For readers, the practical takeaway is that ecosystem reliability and delivery timelines could become increasingly sensitive to how quickly new or replacement funding streams are established.

Treasury strategy shifts: “sell less ETH” and fund development

The funding debate is closely tied to how the Ethereum Foundation manages its ETH holdings. In a May 24 X post, Ethereum co-founder Vitalik Buterin described the Foundation’s resources as limited, noting that it holds about 0.16% of Ether’s total supply—far below the share held by some other networks’ foundations.

Buterin said the Ethereum Foundation was originally designed for a narrower scope: advancing Ethereum’s core software and helping the network reach major roadmap milestones. He argued that many of those milestones were largely completed by 2022, which frames a strategic shift toward what he described as longevity-focused use of remaining resources.

“And so today, the EF is choosing to use its remaining resources to pursue longevity over breadth (yes, this means we sell less ETH),” Buterin wrote.

According to Cointelegraph coverage, the Foundation has already taken steps that adjust its ETH exposure and liquidity. It reportedly un-staked 17,000 ETH in late April and then un-staked another 21,270 ETH in early May, after nearly surpassing 70,000 ETH staked earlier in the year. Cointelegraph also reported that the Foundation sold 10,000 ETH to Bitmine in an OTC deal on May 1.

Blockchain analytics platform Arkham suggested the un-staking may have been tied to the Foundation’s need for funds to continue developing the network. While Arkham’s explanation is not a formal confirmation of intent, it aligns with the broader pattern: if development funding needs remain, the treasury will face pressure to provide capital without destabilizing its longer-term strategy.

Policy update attempts to balance staking and sell pressure

The Foundation’s stance on treasury management has also evolved in response to community reaction. Cointelegraph reported that the Ethereum Foundation published a June 2025 policy update stating that increasing its staking participation could help fund protocol development while limiting future ETH sales after backlash over earlier disposals.

That approach matters because it highlights a tension investors and builders may be watching closely: the Foundation needs enough liquidity to support core work, but it also faces political and reputational costs when selling ETH is perceived as excessive. The reported mix of un-staking, OTC sales, and a subsequent policy pivot toward staking suggests the Foundation is trying to thread a needle—raising funds while reducing the rate of direct ETH disposals.

At the same time, Van Epps’ warning raises a different question: even if treasury mechanics are tweaked, is the resulting funding level sufficient and stable enough to cover the ecosystem’s real-world costs?

Why the funding crisis risk is now more than theoretical

The reason this story is likely to matter beyond internal governance debates is that “core development” is not a static category. Client teams, security research, protocol maintenance, and infrastructure improvements are continuous efforts. If funding drops abruptly—especially through the expiration of a program like the Client Incentive Program in April—then the ecosystem may need time to reallocate responsibilities or secure replacement support.

Van Epps’ estimate of an approximately $30 million annual requirement provides a concrete yardstick for measuring whether proposed changes—whether treasury adjustments, new funding mechanisms, or redesigned incentives—can offset the gap created by earlier spending reductions. If the gap persists, the most likely consequences are slower delivery, fewer funded contributors, or increased reliance on volunteers and short-term grants.

Layered on top of this are the leadership changes highlighted by Cointelegraph, including Hsiao-Wei Wang stepping down. Organizational transitions don’t automatically determine engineering outcomes, but they can affect how quickly decisions get made and how funding priorities are implemented—particularly during a period already flagged as vulnerable.

For now, readers should watch whether the Ethereum Foundation’s funding strategy adjustments translate into sustained support at the ecosystem level—especially once the next funding cycles approach. The open uncertainty is whether treasury policy changes and ETH management actions can fully cover the annual core development needs Van Epps outlined, or whether Ethereum will need genuinely new funding sources sooner than expected.

A Bitcoin ETF lets you own Bitcoin’s price through an ordinary brokerage account, with no wallet, no keys, and no crypto exchange. But there are three different kinds, and they behave very differently. Here is the complete guide to what they are, how they work, and which one fits.

Summary

- Spot Bitcoin ETFs hold actual Bitcoin and offer the closest tracking to the cryptocurrency’s market price.

- Futures Bitcoin ETFs rely on derivative contracts, while income ETFs generate yield by selling options and sacrificing part of Bitcoin’s upside potential.

- Bitcoin ETFs simplify access through traditional brokerage accounts but investors give up direct ownership, self custody, and 24/7 market access.

A Bitcoin ETF is an exchange-traded fund that gives you exposure to Bitcoin’s price through a regular stock brokerage account, without you ever having to buy, store, or secure actual Bitcoin yourself.

When you buy shares of a Bitcoin ETF, you are buying into a fund, and the fund handles the Bitcoin, whether by holding it directly or through related instruments, so that the value of your shares moves with the price of Bitcoin while the fund manages the complexity behind the scenes.

This matters because it lets anyone with a brokerage account gain Bitcoin exposure as easily as buying a share of a company, with no wallets, no private keys, no seed phrases, and no crypto exchange, which removed one of the biggest barriers that kept traditional investors and institutions out of Bitcoin for years.

When US regulators approved spot Bitcoin ETFs in early 2024 after more than a decade of rejections, these funds attracted tens of billions of dollars within months, one of the most successful launches in the history of exchange-traded funds.

This guide explains Bitcoin ETFs in plain English: what an ETF is to begin with, the three distinct types of Bitcoin ETF, spot, futures, and the newer income ETFs, and exactly how each works and differs, the mechanism that keeps an ETF’s price tracking Bitcoin, the advantages that made these funds so popular, the real tradeoffs including fees and the things you give up versus holding Bitcoin yourself, and how to think about whether a Bitcoin ETF fits your needs.

It assumes no background in either crypto or investing, and it pays special attention to the differences among the three types, because they behave differently in ways that matter enormously depending on what you are trying to do, and confusing them is the most common and costly mistake a new ETF buyer makes.

What an ETF is, to start

Before the Bitcoin part, it helps to understand what an exchange-traded fund is in general, because the Bitcoin versions are a specific application of a familiar structure.

An exchange-traded fund, or ETF, is an investment fund that holds a collection of assets and trades on a stock exchange like an ordinary share. When you buy a share of an ETF, you are buying a slice of whatever the fund holds, and the share’s price moves with the value of those underlying holdings. ETFs are popular because they make it easy to gain exposure to something, an index, a sector, a commodity, through a single, liquid, regulated share you can buy and sell in any brokerage account during market hours, without having to buy the underlying assets individually.

A gold ETF, for example, lets you gain exposure to the price of gold without buying and storing gold bars, by holding gold on your behalf and issuing shares that track its value. The ETF structure is trusted, well-understood, and accessible through the same accounts people use to buy stocks, which is exactly why wrapping Bitcoin in an ETF was so significant.

A Bitcoin ETF applies this familiar structure to Bitcoin. Instead of holding gold or a basket of stocks, the fund holds Bitcoin or Bitcoin-related instruments, and it issues shares that track Bitcoin’s price, letting investors gain Bitcoin exposure through the same brokerage account and the same simple buy-and-sell process they use for any other ETF. The fund handles the parts that make owning Bitcoin directly intimidating for many people, the custody, the security, the technical complexity, and packages the price exposure into a regulated share.

The shares trade during stock-market hours, settle like normal securities, and fit into retirement accounts and brokerage portfolios alongside everything else, which is why the Bitcoin ETF became the bridge that brought a great deal of traditional and institutional money into Bitcoin. The whole appeal is taking something that lived in the unfamiliar world of crypto exchanges and wallets and making it available through the thoroughly familiar wrapper of an ETF.

The three types of Bitcoin ETF

This is the most important section, because there are three fundamentally different kinds of Bitcoin ETF, and they work and behave so differently that treating them as interchangeable is the central mistake to avoid. Understanding the distinction is understanding Bitcoin ETFs.

The first and most important type is the spot Bitcoin ETF, which holds actual Bitcoin. When you buy a share of a spot Bitcoin ETF, the fund owns real Bitcoin, stored with a custodian, and your share represents a claim on that Bitcoin, so the share price tracks Bitcoin’s price directly and closely.

This is the most straightforward and the most popular type, the one approved in the United States in early 2024 after years of rejections, and it offers the most direct price exposure available through a brokerage: when Bitcoin rises ten percent, a spot ETF rises roughly ten percent, minus small costs. Spot ETFs are what most people mean now when they say “Bitcoin ETF,” and they are generally the best fit for an investor who simply wants their share to mirror Bitcoin’s price as closely as possible, because the fund literally holds the asset it tracks.

The second type is the futures Bitcoin ETF, which does not hold Bitcoin at all but instead holds Bitcoin futures contracts, agreements to buy or sell Bitcoin at a set price on a future date, traded on a regulated exchange. Futures ETFs track Bitcoin’s price indirectly through these contracts, and they were actually approved earlier than spot ETFs, with the first launching in 2021 before spot funds were permitted.

The crucial complication is that futures contracts expire, so the fund must continually sell expiring contracts and buy new ones, a process called rolling, and this rolling carries costs, particularly when longer-dated contracts are more expensive than near-dated ones, a condition called contango. These roll costs create a persistent drag that can cause a futures ETF to underperform Bitcoin over time, meaning that over a long holding period, a futures ETF may noticeably lag the actual price of Bitcoin even as it broadly follows it. Futures ETFs were an important early bridge, but for most investors wanting straightforward Bitcoin exposure, the roll-cost drag makes them inferior to spot ETFs for long-term holding.

The third type is the newer income, or covered-call, Bitcoin ETF, which is built to generate income, not to track Bitcoin’s price directly from Bitcoin’s volatility. These funds hold Bitcoin exposure, often through a spot ETF, and then sell options against that exposure, collecting the premiums other traders pay and distributing them to shareholders as regular income, targeting yields that can be substantial.

The catch is that selling those options caps the fund’s upside: in exchange for the income, the fund gives up some of Bitcoin’s gains in a sharp rally, so an income ETF can pay a steady yield while capturing less of Bitcoin’s price appreciation than a spot ETF would. Income ETFs suit investors who want a yield from their Bitcoin exposure and expect a choppy or moderately rising market, while they are a poor fit for investors who want full participation in Bitcoin’s upside.

The three types, spot for direct price exposure, futures for indirect exposure with roll-cost drag, and income for yield with capped upside, serve genuinely different purposes, and choosing among them depends entirely on what an investor is trying to achieve.

How a Bitcoin ETF keeps tracking Bitcoin’s price

It is worth understanding the mechanism that keeps an ETF’s share price aligned with the value of what it holds, because it is clever and it explains why a well-built spot ETF tracks Bitcoin so closely.

The alignment comes from a process called creation and redemption, carried out by large financial firms called authorized participants. If demand pushes an ETF’s share price above the value of the Bitcoin it holds per share, authorized participants can create new shares by delivering the appropriate amount of Bitcoin or cash to the fund, increasing the supply of shares and pushing the price back down toward the value of the underlying Bitcoin.

If the share price falls below the value of the underlying Bitcoin, they can redeem shares, taking Bitcoin or cash out of the fund and reducing the share supply, pushing the price back up. This constant creation and redemption, driven by the profit authorized participants make from any gap between the share price and the underlying value, continuously keeps the ETF’s price closely tracking the value of the Bitcoin it holds, which is the same arbitrage mechanism that keeps all ETFs aligned with their underlying assets.

This mechanism is why a spot Bitcoin ETF tracks Bitcoin so faithfully, because any meaningful divergence between the share price and the value of the held Bitcoin creates a profit opportunity that authorized participants act on, closing the gap. Some small tracking differences still occur, because the fund charges a management fee that slightly reduces returns over time, and there can be minor timing and cash-management effects, so a spot ETF tracks Bitcoin very closely but not perfectly.

Futures ETFs track less closely because of the roll costs described earlier, which the creation-redemption mechanism cannot eliminate since they are inherent to holding expiring contracts. Understanding the creation-redemption process demystifies how an ETF share stays tied to Bitcoin’s price without the fund needing to constantly adjust prices manually, and it explains why the spot structure, holding the actual asset, produces the tightest tracking, while the futures structure introduces a persistent gap.

The advantages: why Bitcoin ETFs became so popular

The explosive success of spot Bitcoin ETFs, attracting tens of billions of dollars quickly, came from a set of real advantages over buying Bitcoin directly, and understanding them explains the appeal.

The first advantage is simplicity and accessibility. A Bitcoin ETF lets you gain Bitcoin exposure through the brokerage account you may already have, with no need to open a crypto exchange account, set up a wallet, manage private keys, or worry about the security of self-custody, which are exactly the steps that intimidate many would-be Bitcoin owners and keep institutions out. Buying a Bitcoin ETF is as easy as buying any stock, which dramatically lowers the barrier to entry.

The second advantage is security and custody handled for you: the fund stores the Bitcoin with professional custodians, removing the risk that you lose your coins by mishandling a wallet or losing a seed phrase, a real and common way people lose Bitcoin directly. For an investor uncomfortable with the responsibility of securing crypto themselves, having a regulated fund handle custody is a real benefit.

The third set of advantages is institutional and structural. Many institutions, funds, and retirement accounts can only or much more easily hold regulated securities like ETFs, not crypto held directly, so the ETF wrapper opened Bitcoin to enormous pools of capital that were effectively barred from buying it before, which is a large part of why the launches drew so much money. ETFs also fit cleanly into the existing financial system, into tax-advantaged accounts, into portfolios managed by advisors, into the familiar reporting and brokerage infrastructure, making Bitcoin exposure a normal portfolio holding, not an exotic outside asset.

These advantages, simplicity, handled custody, and seamless integration into traditional finance and institutional portfolios, are why the spot Bitcoin ETF was such a watershed, because it made Bitcoin exposure available and respectable to a vast audience that direct ownership had excluded, and the flood of money that followed reflected how much demand had been waiting for exactly this kind of access.

The tradeoffs: fees and what you give up

A Bitcoin ETF is not free and not identical to owning Bitcoin, and an honest accounting requires understanding the costs and the things you give up in exchange for the convenience.

The most direct cost is fees. ETFs charge an annual management fee, expressed as an expense ratio, and while spot Bitcoin ETF fees are relatively low, they are not zero, and over time they slightly reduce your returns compared to holding Bitcoin directly with no ongoing fee. Income and futures ETFs typically charge higher fees than plain spot ETFs, reflecting their more active management, so the type of ETF affects the cost.

These fees are usually modest, but they compound over long holding periods and are a real, if small, drag on returns that direct ownership avoids. The second cost is tracking imperfection: even a good spot ETF tracks Bitcoin very closely but not perfectly because of fees and minor effects, and futures ETFs track noticeably less well because of roll costs, so an ETF’s return can lag Bitcoin’s actual return, especially for futures funds over time.

The more fundamental tradeoff is what you give up by owning exposure instead of owning Bitcoin. With a Bitcoin ETF, you own shares in a fund, not Bitcoin itself, which means you do not hold the keys and cannot use the Bitcoin in the ways direct ownership allows: you cannot send it to someone, use it in decentralized finance, hold it in self-custody beyond the reach of any institution, or transact with it on the Bitcoin network, because you have exposure to the price, not the asset.

You are also subject to the ETF’s structure and the traditional market’s constraints: ETF shares trade only during stock-market hours, so you cannot react to Bitcoin’s around-the-clock price moves on weekends or overnight when the market is closed, whereas Bitcoin itself trades every hour of every day. And you carry a degree of counterparty reliance on the fund and its custodian, trusting that they hold and manage the Bitcoin properly, which is different from the self-reliance of holding your own keys.

None of these tradeoffs makes the ETF a bad choice, but they define what it is: a convenient, regulated wrapper for price exposure that deliberately trades away the control, utility, and round-the-clock access of owning Bitcoin directly, in exchange for the simplicity and safety of the familiar ETF structure.

ETF versus holding Bitcoin yourself

The choice between a Bitcoin ETF and direct ownership comes down to what you value, and laying out the comparison clarifies which suits whom.