Crypto World

Hyperliquid whale wiped out as $458 million in crypto longs vanish

Crypto saw $458m in liquidations in 24 hours as Iran’s Gulf strikes and $110 oil triggered a brutal flush of overleveraged BTC and ETH longs led by a Hyperliquid whale.

Summary

- Total crypto liquidations hit $458 million in 24 hours, with $357 million of that from long positions and just $101 million from shorts, as 128,087 traders were wiped out.

- Bitcoin longs lost $138 million versus $24.3 million for shorts after BTC broke below $69,000, while Ethereum longs saw $82.6 million in liquidations as ETH briefly slipped under $2,100.

- A $10.8 million BTC-USD long on Hyperliquid was the day’s largest single liquidation, underscoring how the on-chain perps venue has become a bellwether for extreme leverage and stress.

The cryptocurrency derivatives market absorbed another brutal session on Thursday, with total liquidations across the network surging to $458 million over a 24-hour period as Iranian missile strikes on Gulf energy infrastructure sent shockwaves through global risk assets. The wipeout hit leveraged long positions hardest — a sign that traders positioned for recovery were caught off-guard by a fresh escalation in the Middle East war.

According to Coinglass data, long positions accounted for $357 million of the total liquidations, while shorts were cleared for $101 million — a roughly 3.5-to-1 long-to-short ratio that reflects a market in which bullish positioning was overwhelmed by a sudden surge in risk-off sentiment. A total of 128,087 traders were liquidated globally across the session, with the largest single forced closure — a $10.8 million BTC-USD position — occurring on Hyperliquid, the decentralized perpetuals exchange that has repeatedly featured in this cycle’s most notable liquidation events.

Bitcoin long positions were wiped for $138 million, while BTC shorts saw $24.3 million in liquidations — a clear indication that bulls attempting to hold the line near key support levels were flushed out as prices broke below $69,000 earlier in the session. Ethereum (ETH) long liquidations reached $82.6 million, with shorts cleared for $37.5 million, as ETH briefly fell below $2,100 — a psychologically significant level that had acted as near-term support.

The session’s liquidation profile is consistent with a broader pattern observed throughout the Iran war, which began on February 28. With Brent crude surging above $110 per barrel and Iranian strikes on Qatar’s Ras Laffan LNG terminal and Kuwaiti refineries driving a fresh wave of macro fear on Thursday, leveraged crypto traders found themselves caught on the wrong side of a correlation that has reasserted itself with full force: when global energy infrastructure is under fire, risk assets — including crypto — sell off.

The figures represent a meaningful acceleration from recent sessions. On March 15, total liquidations reached only $77 million across the market, with the largest single Hyperliquid event clocking in at $1.1 million. By March 19, that largest single liquidation had grown nearly tenfold to $10.8 million, underscoring how rapidly conditions deteriorated as news of the refinery strikes broke.

Hyperliquid’s continued dominance of single-event liquidation records is notable. The platform, which operates an on-chain order book and settles trades and liquidations on its own Layer 1, has become a focal point for large leveraged positions in this cycle — and consequently a bellwether for stress in the broader derivatives market.

Bitcoin’s (BTC) price remained below $70,000 as of Thursday afternoon, down over 3% on the day, while ETH traded near $2,100 — levels that keep a large body of leveraged long positions at elevated liquidation risk should conditions deteriorate further. With the quarterly Deribit options expiration looming and geopolitical uncertainty at its highest point since the war began, the risk of additional cascading liquidations remains elevated.

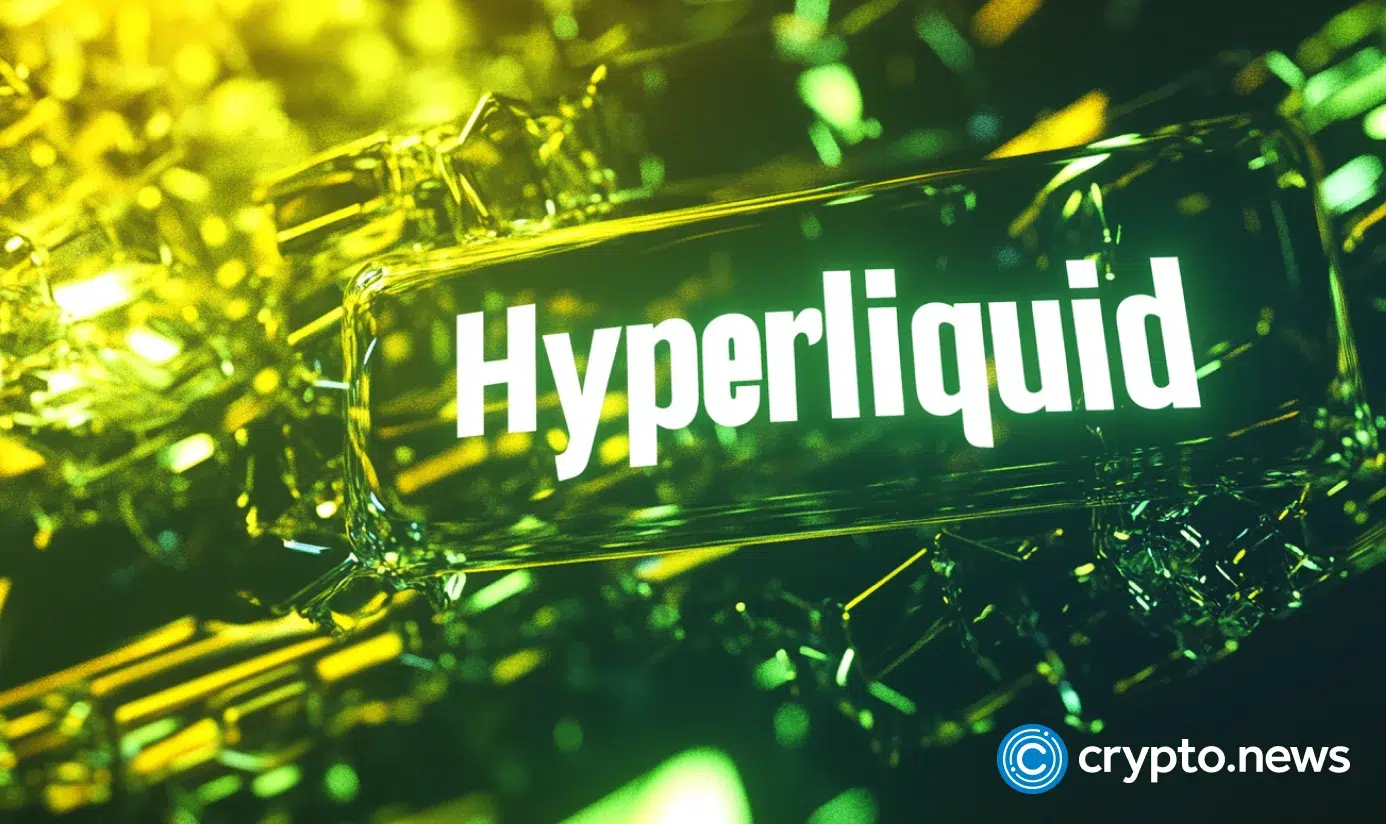

Singapore-headquartered cryptocurrency exchange Crypto.com is set to cut up to 12% of its workforce due to company-wide artificial intelligence (AI) integrations, joining a growing list of companies announcing AI-linked mass layoffs, according to the exchange’s founder and CEO, Kris Marszalek.

Crypto.com recently expanded its AI offering and launched the AI agent platform ai.com on Feb. 9, which it positioned as a core business. The company also said it was the first crypto platform to receive the ISO/IEC 42001:2023 certification for AI system management in February.

“We are joining the list of companies integrating enterprise-wide AI,” Marszalek said in a Thursday X post, warning that companies that don’t pivot will fail.

Crypto.com lists around 1,500 employees, meaning that the 12% layoff would affect about 180 staff members. It marks the latest AI-linked large-scale layoff in the crypto and tech space, underscoring concerns over AI replacing more of the human workforce.

“We are joining the list of companies integrating enterprise-wide AI,” a spokesperson for Crypto.com told Cointelegraph, adding that the layoffs are part of the platform’s plans to “prioritize resources around key growth areas.” The spokesperson declined to comment on the roles that were affected by the layoffs.

Crypto and tech companies stage AI-linked mass layoffs

Other large crypto and tech companies have also announced AI-linked mass layoffs in recent months.

On Monday, blockchain analytics platform Messari announced more staff cuts as part of its pivot to an AI-first company. The company previously laid off roughly 15% of its full-time employees in January 2025 and made a similar workforce reduction in February 2023.

On Wednesday, the Algorand Foundation, the organization behind Layer-1 blockchain Algorand, also announced a 25% staff reduction, citing macroeconomic uncertainty and the current crypto market slump.

On Feb. 26, Jack Dorsey’s payment company Block announced cutting about 40% of its staff, citing the rapid acceleration of AI. However, some of the 4,000 fired workers have already returned to the company, according to multiple employees who were part of the initial layoffs.

Related: Nvidia’s Huang: AI will boost jobs as it needs trillions in infrastructure

Large tech companies have also announced AI-linked mass layoffs. On Jan. 27, visual discovery engine Pinterest announced it was cutting up to 15% of its staff to pivot to an AI-centric approach.

On March 11, software company Atlassian announced it was cutting 10% of its staff, or about 1,600 employees, as part of a restructuring to self-fund further AI investments.

Meta, Facebook’s parent company, is also reportedly planning a workforce cut of up to 20%, seeking to enable AI efficiencies and offset the costs of AI infrastructure, insiders familiar with the matter told news outlet Reuters on Saturday.

Magazine: 9 weirdest AI stories from 2025

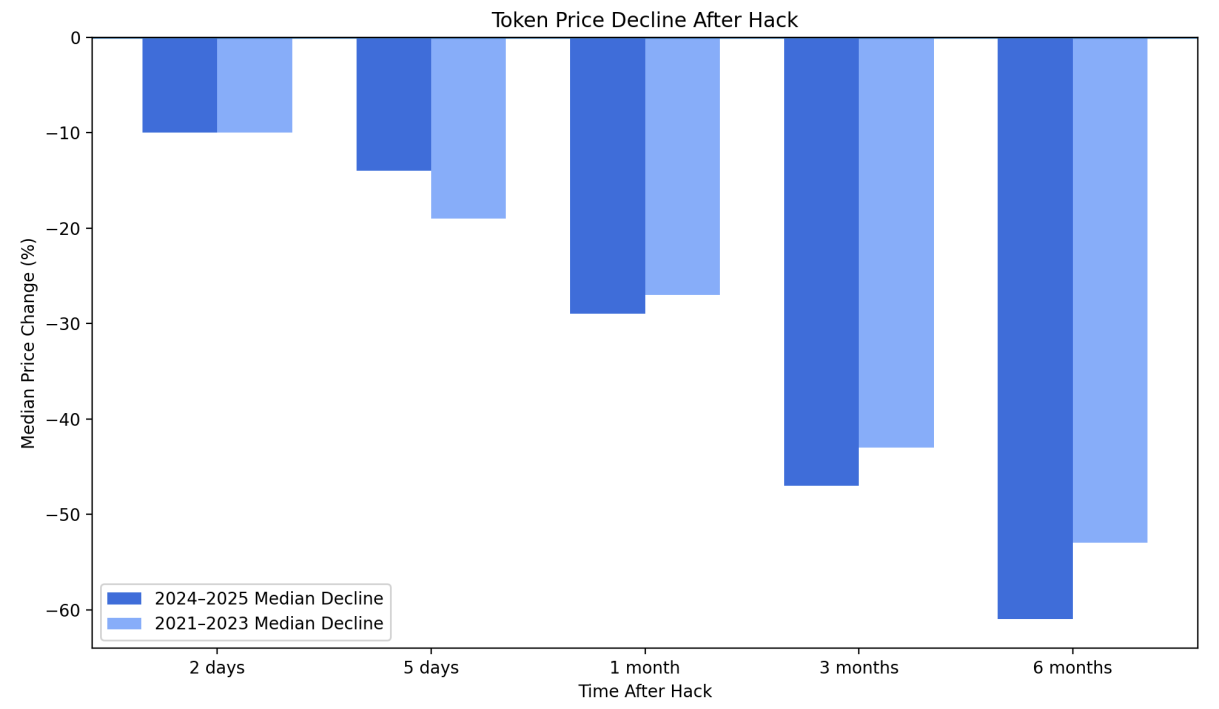

A new security report from Immunefi finds that crypto hacks continue at a steady pace while losses are becoming more concentrated in a small number of massive exploits.

Analyzing 425 publicly known incidents between 2021 and 2025, the report estimates that the average hack now results in about $25 million in stolen funds. In 2024 and 2025 alone, 191 hacks led to $4.67 billion in losses, with just five incidents accounting for 62% of the total.

Despite representing fewer incidents, centralized exchange breaches drove the majority of losses. Twenty exchange hacks accounted for roughly $2.55 billion, or about 55% of the total, reflecting how large pools of user funds are concentrated behind fewer points of failure.

Token markets also appear to be reacting more harshly to breaches. Across 82 hacked tokens tracked in the study, prices fell a median 61% within six months, with 83.9% remaining below their hack-day price over that period.

“The market has become less forgiving because expectations have changed,” Immunefi CEO Mitchell Amador told Cointelegraph, adding that breaches are now seen as signals of deeper issues in engineering, governance and operational resilience.

Amador said the long-term impact of exploits often extends well beyond the initial loss:

The stolen funds are only the first layer of damage. What follows is often more destructive: sustained token price suppression, reduced treasury capacity, leadership disruption, lost development time, and erosion of user trust.

The report also highlighted how interconnected DeFi systems can amplify the fallout from a single incident, with failures cascading across lending, collateral and liquidity networks.

One example involved the collapse of Elixir’s deUSD stablecoin in November 2025. Elixir had parked roughly 65% of deUSD’s collateral with Stream Finance, which disclosed a $93 million loss from an external fund manager. As Stream’s stablecoin xUSD fell 77%, deUSD’s backing deteriorated, redemptions halted and panic selling hit Curve pools, ultimately pushing deUSD down more than 97%.

Related: South Korea sells $21.5M in recovered Bitcoin after custody breach

Recent exploits highlight ongoing security risks in crypto

While crypto-related hack losses fell to $26.5 million in February, the lowest monthly total in nearly a year, according to PeckShield, several security incidents have already surfaced in March.

Researchers at Google reported a new exploit kit targeting Apple iPhone users that is designed to steal cryptocurrency wallet seed phrases. The toolkit, known as Coruna, contains multiple exploit chains capable of targeting devices running various versions of Apple’s iOS and has been linked to phishing websites posing as crypto platforms.

The Bitcoin-based DeFi platform Solv Protocol also reported that one of its token vaults was exploited for roughly $2.7 million, affecting fewer than 10 users. The project said it would cover the losses and offered the attacker a 10% bounty in exchange for returning the funds while security firms investigate the breach.

Separately, the domain of Bonk.fun was hijacked after attackers gained access to a team account and deployed a wallet-draining scheme through the site. The project warned users not to interact with the platform while the team worked to regain control of the domain.

Meanwhile, NFT lending platform Gondi disabled a faulty smart contract after an exploit allowed an attacker to steal roughly $230,000 worth of NFTs. The project said it is compensating affected users while investigating the vulnerability, which involved a contract used to sell escrowed NFTs and repay loans.

Magazine: All 21 million Bitcoin is at risk from quantum computers

A long-dormant Bitcoin whale wallet has offloaded 1,000 BTC on Wednesday.

Summary

- Long dormant Bitcoin whale offloads 1,000 BTC, extending total transfers to 3,500 BTC since November 2024 with roughly $330 million in realised profit.

- Additional selling from early investor Owen Gunden and Bhutan-linked wallets points to a pattern of distribution from large holders into the market.

On-chain data tracked by analytics provider EmberCN showed that the wallet “bc1q…6ym” has transferred a total of 3,500 BTC since November 2024.

The whale began accumulating around 13 years ago and reportedly bought Bitcoin at an average price of $332 per BTC and has sold at an average price of around $94,786, generating approximately $330 million in profits. At its peak, the wallet held 5,000 BTC.

After the latest sales, the wallet still holds around 1,500 BTC valued at $106.8 million at current prices.

Such transaction activity is not limited to this wallet. Separate data from early Bitcoin investor Owen Gunden shows he has sold another 650 BTC worth about $46.3 million on Wednesday, bringing his total disposals to roughly 11,000 BTC, or more than $1 billion.

The investor has yet to confirm ownership of the wallet, and such on-chain attributions remain unverified.

Meanwhile, crypto.news reported earlier that Bhutan has transferred roughly $72.3 million in Bitcoin. Wallets connected to Druk Holding and Investments have been offloading portions of its holdings, and the country’s reserves have significantly shrunk since their peak levels.

Recent whale activity may have contributed to this pressure. According to CryptoQuant data, the bitcoin exchange whale ratio, which tracks the share of top 10 deposits relative to total exchange inflows, hit 0.83 on March 14.

Whales have also been observed shorting. Notably, a pseudonymous whale called Jason has repeatedly taken large short positions on Bitcoin, including a recent 2,281 BTC short on Binance opened at around $74,238.

Bitcoin (BTC) price in the meantime has fallen over 4.5% and is down nearly 43% from its all-time high.

Apex Group’s Tokeny has tapped Polygon Labs to launch T-REX Ledger, a compliance-focused blockchain designed to help regulated tokenized assets move across networks without repeating investor checks and transfer restrictions.

In a Thursday release shared with Cointelegraph, the project said it targets a key friction point in tokenized markets. ERC-3643 is an Ethereum-based token standard for permissioned tokens representing real-world assets that can support compliant issuance of RWAs, but identity checks, eligibility rules and transfer restrictions often remain fragmented when the same asset is distributed across multiple blockchains.

T-REX Ledger is being pitched as a shared compliance layer that other chains can query, while settlement continues to take place on external networks. Built with Polygon’s Chain Development Kit and connected to Agglayer, the system is intended to act as a common registry for investor eligibility and transfer rules across tokenized securities.

The launch comes as financial and crypto infrastructure groups race to build infrastructure for tokenized markets. The New York Stock Exchange parent company, Intercontinental Exchange, has outlined plans for a new platform for tokenized stocks and exchange-traded funds (ETFs), while the Depository Trust and Clearing Corporation (DTCC) joined the ERC-3643 Association in 2025 as institutions push deeper into tokenized collateral and securities infrastructure.

Fixing fragmented compliance

In the release, the network was described as a “shared source of truth” for investor eligibility and transfer rules.

The core problem T-REX aims to solve is that ERC-3643 enables compliant issuance but does not maintain a shared compliance state across chains. The same security measures applied to Ethereum and Polygon, for example, still run separate eligibility checks, identity attestations and transfer restrictions.

Joachim Lebrun, co-founder of T-REX Network and chief blockchain officer of Tokeny, told Cointelegraph that T-REX Ledger would support the issuance and lifecycle management of regulated digital securities, including bonds, funds, equities and structured products, with identity, eligibility and transfer rules embedded directly into ERC-3643 tokens.

Apex Group will act as the first onchain transfer agent and plans to adopt T-REX Ledger as its default multi-chain orchestration layer with an initial target of $100 billion in tokenized assets by June 2027.

Related: New Ethereum standard aims to set baseline for real-world asset tokenization

T-REX Ledger centralizes compliance logic in a dedicated chain that other networks can query, while settlement remains on external chains.

Lebrun said, “The market has grown into a multi-chain world for tokenization” and argued that T-REX Ledger turned other blockchains into “distribution channels,” enabling regulated assets to move to “wherever liquidity exists with speed, compliance, and control.”

Slotting into the tokenization race

Related: SEC gives go-ahead to Nasdaq for tokenized trading trial

T-REX is pitching itself as a neutral registry layer that can sit alongside players in the tokenization race. Lebrun said that a security issued via T-REX Ledger “could ultimately settle at DTCC” because “the compliance validation doesn’t need to live on the same network as the settlement.”

The chain itself will run as a sovereign Polygon CDK network governed by a dedicated steering committee, while ERC-3643 and its compliance framework remain open source under the ERC-3643 Association, not Polygon.

Magazine: Ethereum’s Fusaka fork explained for dummies — What the hell is PeerDAS?

Key Highlights

- Figma’s shares plummeted approximately 8% on Wednesday following Google’s unveiling of significant enhancements to its Stitch AI design tool

- Google introduced “vibe designing” functionality — an innovative prompt-driven method for creating user interfaces and generating frontend code

- The Stitch platform now connects seamlessly with Google Workspace applications including Docs and Drive, appealing to organizations already embedded in Google’s suite

- Figma disclosed $1.06B in fiscal 2025 revenue, representing a 41% year-over-year increase, though net losses expanded to $1.25B

- FIG shares are currently down approximately 80% from their post-IPO peak of $142.92

Figma has endured a challenging period, and Wednesday’s trading session offered no relief. Shares declined roughly 8% following Google’s announcement of substantial upgrades to Stitch, its artificial intelligence-driven user interface design platform. By Thursday midday in New York, FIG continued trading lower by approximately 5%.

The market reaction was swift. Investors didn’t require detailed feature-by-feature analyses — the mere involvement of Google proved sufficient to trigger selling pressure.

While Stitch had already registered on Figma’s competitive landscape, Wednesday’s reveal brought the threat into clearer view. Google Labs centered its announcement around a fresh approach dubbed “vibe designing” — fundamentally leveraging conversational language prompts to create refined UI layouts and frontend code, bypassing traditional wireframing stages.

“When ‘vibe designing’ in Stitch, you can explore many ideas quickly leading to a higher quality outcome,” Google stated in its release. The platform now supports voice commands as well, enabling users to request instant modifications such as alternative color schemes or revised navigation elements.

The updated Stitch also introduced templates spanning multiple sectors including SaaS dashboards, healthcare applications, entertainment platforms, and utility services — sectors that align directly with Figma’s core customer segments.

The Significance of Google’s Strategic Play

The worry extends beyond feature parity. The underlying infrastructure presents the larger challenge. Stitch’s integration with Google Docs, Drive, and the broader Workspace environment — platforms already woven into the daily workflows of countless organizations — substantially lowers migration barriers for companies contemplating alternatives to Figma.

Google’s proven ability to rapidly scale products adds weight to the competitive threat. This historical capability gives market participants legitimate grounds for concern, regardless of Stitch’s current maturity level.

Figma CEO Dylan Field commented on market fluctuations during a February CNBC appearance, noting: “I think volatility is probably good at strengthening companies long-term.”

Nvidia CEO Jensen Huang challenged the prevailing narrative suggesting AI platforms will entirely displace established software firms. “It is the most illogical thing in the world and time will prove itself,” Huang remarked during a Cisco AI conference.

Analyzing Figma’s Financial Performance

Figma’s financial results present a complex picture. The company achieved $1.06 billion in revenue for fiscal 2025, marking a 41% year-over-year climb. Net dollar retention reached 136%, indicating existing customers increased their platform spending by 36% compared to the previous year.

However, losses are accelerating. Net losses totaled $1.25 billion in 2025, climbing from $732 million in 2024. Escalating stock-based compensation and operational expenditures are widening this deficit.

Shares initially surged following the Feb. 18 earnings disclosure, buoyed by projections of 38% revenue expansion in Q1 2026. That momentum proved short-lived.

FIG currently trades near $24.50 — substantially beneath its IPO price of $33 per share, and nearly 80% below its post-IPO zenith of $142.92. The 52-week trading range spans from $19.85 to $142.92.

With a price-to-sales multiple hovering around 13, the valuation remains elevated but increasingly reasonable compared to comparable high-growth SaaS companies demonstrating similar revenue trajectories.

The stock has yet to retest its early February nadir, which certain market observers interpret as potential support establishing itself.

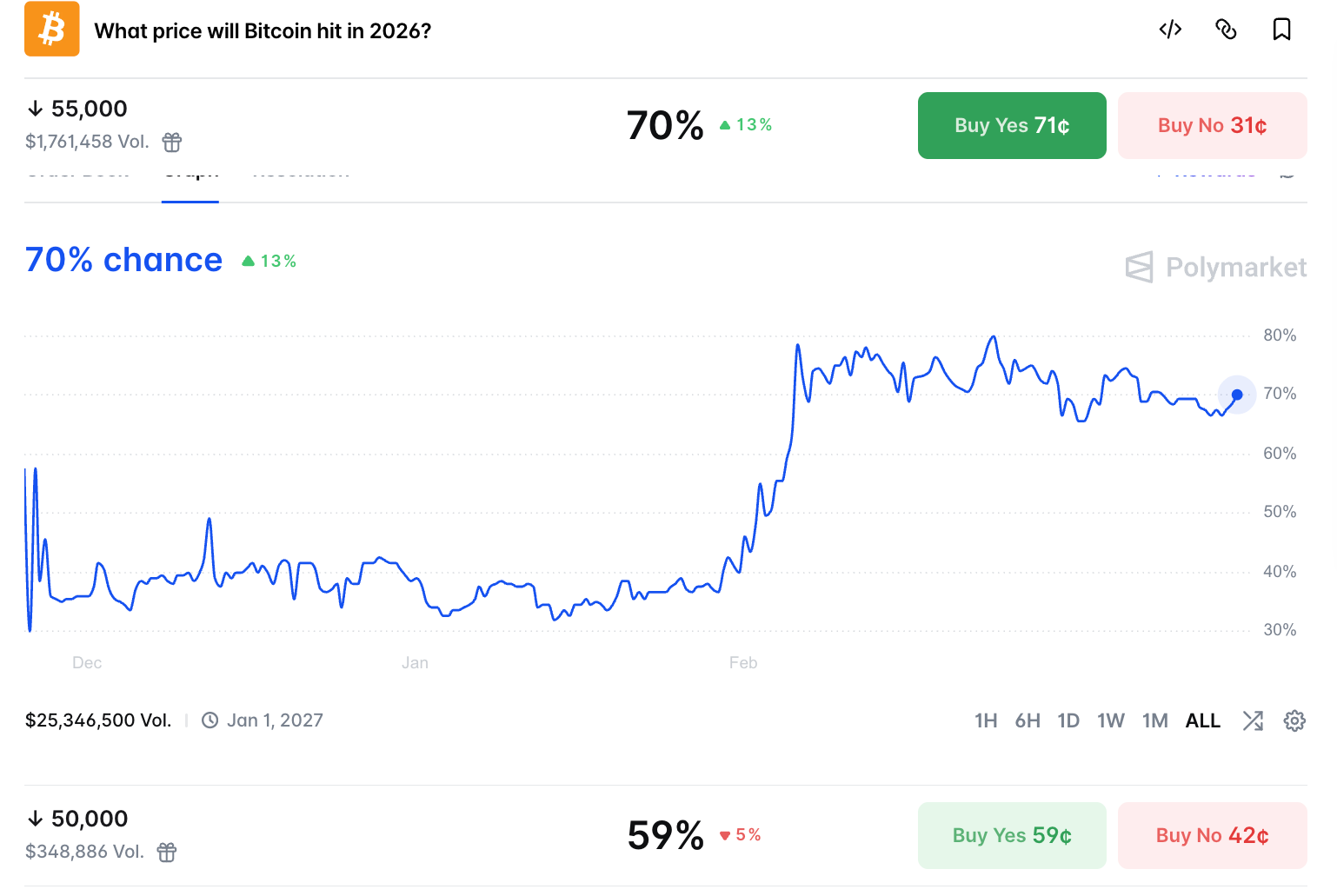

Bitcoin (BTC) may go as low as $55,000 in 2026 as the market lacks bullish catalysts amid macroeconomic uncertainties.

Key takeaways:

-

BTC price has a 65%-71% chance of dropping below $55,000 before Dec. 31, according to prediction markets.

-

Bettors don’t expect Strategy to sell its BTC holdings in 2026.

-

Whale selling and negative ETFs flows add to Bitcoin’s sell-side pressure.

Prediction markets see BTC bear market continuing

The majority of traders on Polymarket and Kalshi expect Bitcoin to resume its downtrend throughout 2026, with targets as low as $40,000.

Related: Bitcoin tests old 2021 top as gold falls to six-week lows under $4.7K

As of Thursday, Polymarket bettors are pricing in about 71% odds of BTC dropping below $55,000 before Dec. 31, a 13% increase from the previous day.

Traders set 59% odds of BTC crossing below the $50,000 psychological level and a 46% chance that it goes as low as $45,000 before the end of the year.

The lower price target forecasts for BTC mimic those elsewhere. On fellow prediction site Kalshi, traders set 71% odds of Bitcoin dropping below $60,000, with a 65% chance that it drops below $55,000. The lowest price target on Kalshi is $40,000, with a 31% possibility that BTC drops to this level before Dec. 31.

Bitcoin’s low for 2026 sits at $59,940, reached on Feb. 6, and the last time the BTC/USD pair traded below $55,000 was in February 2024.

As Cointelegraph reported, some analysts believe that the long-term BTC price downtrend is still in play, warning that the rebound to $76,000 was a bull trap.

Will Strategy sell Bitcoin in 2026?

Bitcoin’s recent drop to $69,000 saw it slide below Strategy’s average BTC cost price, which is $75,696 at the time of writing.

But despite the expected drawdown in price, Polymarket odds for Strategy selling Bitcoin in 2026 remain below 15%, while expectations for routine buys remain elevated.

Polymarket traders still see routine Strategy purchases throughout the year as a high-probability event, with a 96% chance of it holding over 800,000 BTC by Dec. 31.

Last week, Strategy expanded its Bitcoin treasury to 761,000 BTC after buying 22,337 coins for roughly $1.6 billion.

Bitcoin ETF flows tread water

Meanwhile, the US spot Bitcoin exchange-traded funds (ETFs) returned to net negative flows on Wednesday.

These were driven mostly by outflows from the Fidelity Wise Origin Bitcoin Fund (FBTC), data from investment firm Farside shows.

As Cointelegraph reported, the largest ETF offering from asset manager BlackRock saw $34 million in outflows as investor sentiment returned to “extreme fear.”

This article does not contain investment advice or recommendations. Every investment and trading move involves risk, and readers should conduct their own research when making a decision. While we strive to provide accurate and timely information, Cointelegraph does not guarantee the accuracy, completeness, or reliability of any information in this article. This article may contain forward-looking statements that are subject to risks and uncertainties. Cointelegraph will not be liable for any loss or damage arising from your reliance on this information.

Key Takeaways

- Micron’s fiscal Q2 2026 delivered $23.86 billion in revenue with adjusted EPS of $12.20, surpassing analyst expectations

- The company projected fiscal Q3 2026 revenue of approximately $33.5 billion, significantly exceeding Street estimates

- Capital expenditure guidance for fiscal 2026 increased to more than $25 billion, roughly $5 billion higher than previous projections

- Shares declined following the earnings announcement despite impressive financial performance, primarily due to elevated spending concerns

- Analyst sentiment remains overwhelmingly positive with 29 Buy ratings, 5 Strong Buys, and no Sell recommendations according to MarketBeat data

Micron Technology unveiled exceptional quarterly results on March 19, yet the market’s response told a more complex story. Despite impressive revenue figures and unprecedented free cash flow generation, shares retreated as Wall Street digested the company’s ambitious capital investment strategy.

The memory chip giant reported fiscal second-quarter 2026 revenue reaching $23.86 billion alongside adjusted earnings of $12.20 per share. Micron also highlighted that it closed the period with $16.7 billion in cash and investments, marking a company record for free cash flow generation.

While these figures impressed, it was the forward-looking commentary that captured the most attention—both positive and negative.

For fiscal Q3 2026, Micron projected revenue of approximately $33.5 billion, substantially exceeding Wall Street’s expectations. The company attributed this robust outlook to explosive demand for high-bandwidth memory (HBM) products, which are essential components in AI data centers and acceleration hardware.

HBM represents today’s most sought-after memory technology. Micron operates within an oligopoly of just three major global producers, joined by Samsung and SK hynix. This concentrated supply structure has bolstered pricing power and supported healthy profit margins.

Understanding the Post-Earnings Decline

Notwithstanding the impressive financial performance, Micron’s stock price declined following the announcement. The catalyst? A significantly revised capital spending forecast.

The company disclosed that fiscal 2026 capital expenditures would surpass $25 billion, representing an approximate $5 billion increase from earlier guidance. Management explained the investment is necessary to expand clean-room infrastructure and accelerate DRAM manufacturing capacity to satisfy AI-driven demand.

This scenario represents a classic semiconductor industry dilemma—deploying massive capital to capture growth opportunities while risking oversupply if market conditions deteriorate. Memory manufacturers have historically encountered this challenge, and investors maintain vivid memories of past overcapacity cycles.

Additionally, the stock’s valuation had already reflected substantial optimism. Prior to Thursday’s retreat, Micron had surged more than 61% during 2026, building on strong momentum from 2025. At such elevated levels, any hint of risk can trigger profit-taking behavior.

Wall Street Maintains Conviction

The analyst community showed no signs of wavering. According to MarketBeat data released on March 19, Micron holds five Strong Buy ratings, 29 Buy ratings, and four Hold ratings. Notably, zero analysts recommend selling the stock.

This represents nearly unanimous bullish positioning. The four Hold ratings suggest some analysts advocate patience at current valuations, but bearish recommendations remain completely absent.

Price targets underwent revisions as analysts updated their financial models following the report. MarketBeat’s consensus tracking indicated a range settling between approximately $425.62 and $446.66.

Several firms subsequently raised their targets. Needham elevated its price objective to $500. UBS similarly increased its target while reaffirming its Buy rating. Both institutions cited the sustained strength of AI-related memory demand as their primary rationale.

These $500 price targets represent more than optimistic projections—they embody a conviction that Micron’s AI-driven growth trajectory extends further than current market pricing acknowledges.

The investment debate surrounding Micron has evolved. Questions no longer center on whether the company is emerging from a downturn. Instead, the focus has shifted to whether Micron can sustain expansion without excessive capital deployment.

Presently, analysts are answering affirmatively. With 34 Buy or Strong Buy ratings and zero Sell recommendations in current MarketBeat data, Micron stands as one of the most broadly supported equities in the AI semiconductor sector.

The stock declined on March 19. The analyst community’s conviction remained intact.

The European Central Bank is looking for experts who can help define how a potential digital euro can be used across ATMs and payment terminals.

Summary

- ECB opens applications for expert workstreams to define how a digital euro would function across ATMs and payment terminals.

- Workstreams will focus on technical specifications and certification frameworks to ensure integration with existing payment systems, including offline capability.

The ECB published an announcement on Wednesday, opening applications for two workstreams under its Rulebook Development Group. The first will focus on implementation specifications for ATM and terminal providers, while the other will work on certification and approval frameworks for payment solutions.

Experts joining the workstreams would contribute to how a potential digital euro would integrate across existing payment systems and technologies, including offline functionality and interoperability with standards used across Europe.

The workstreams will report to the Rulebook Development Group, which includes representatives from merchants, payment service providers and consumers.

“The draft rulebook currently being developed will be sufficiently flexible to accommodate any future adjustments and will be updated in accordance with the outcome of the digital euro legislative process. A possible decision by the ECB’s Governing Council to issue a digital euro would only be taken after the legislative act has been adopted,” the ECB said.

As previously reported by crypto.news, last year, the ECB announced providers for five components and services after a similar call for applications published in 2024.

The banking regulator had also put out invitations to tender for firms that could offer technology solutions and components around alias lookup, fraud and risk management, offline services and software development kits, among others.

While the ECB is making progress around the digital euro rollout, it has continued issuing public warnings about the risks of stablecoins, which are seen as one of the biggest competitors to any central bank digital currency.

The ECB is concerned that if euro-denominated stablecoins gain serious traction, it could weaken the effectiveness of monetary policy and reduce the funding base of traditional banks.

Arthur Hayes, a veteran trader and co-founder of BitMEX, has once again placed a bet in ETHFI nearly a month after a possible exit from the token.

Summary

- Arthur Hayes re entered ETHFI with a $72,800 purchase shortly before Upbit announced a KRW listing, drawing attention to the timing of the move.

- ETHFI price briefly surged nearly 12% following the listing before retracing, highlighting volatility tied to exchange driven catalysts.

- Technical signals remain mixed, with a breakout above trendline resistance suggesting upside potential, while MACD and RSI indicate lingering bearish pressure.

According to a March 19 X post by on-chain tracker Lookonchain, Hayes invested around 132,730 ETHFI tokens worth $72,800 today. The tokens were received from Anchorage Digital at an average price of $0.55 each.

While such transfers are common for institutional players, the report highlighted the significance of the timing of the purchase. It revealed that the transfer from Anchorage Digital happened just five hours ahead of a KRW market listing for the token by South Korea’s largest crypto exchange, Upbit.

Typically, a KRW listing on Upbit has often acted as a major catalyst for crypto assets. As reported by crypto.news earlier, CPOOL, the native token of the DeFi institutional credit protocol Clearpool, soared over 70% in a single day following a similar listing. However, the token later gave up a portion of those gains as profit-taking set in.

Lookonchain added another twist to the development. Notably, Hayes had transferred 2.15 million ETHFI tokens worth around $1 million out of his wallet a month ago, likely exiting from the position.

The latest receipt of ETHFI tokens could likely mark a potential re-entry into the token, though at a much smaller scale than when Hayes previously exited the position. Hayes has also historically rotated capital across DeFi tokens, including PENDLE, LDO, ENA, and ETHFI, depending on market conditions.

Ether.Fi (ETHFI) shot up nearly 12% to $0.60 within an hour after Upbit listed the token. It, however, retraced back to around $0.54 at press time, down 2.3% over the past 24 hours.

On the daily chart, ETHFI price has broken out of a descending trendline that had been acting as dynamic resistance for the token following its decline since early October. A sharp breakout from the pattern typically signals a potential trend reversal and opens the door for further upside if supported by volume.

Technical indicators like the MACD and the RSI also suggest mixed momentum. Notably, the MACD lines were still pointing downwards, indicating lingering bearish pressure, while the RSI hovered near the neutral zone, reflecting indecision among traders.

For now, $0.649 would be the key resistance level traders would be keeping an eye on. A break above that could strengthen bullish momentum and push the price toward higher levels.

On the contrary, $0.500 would be the key support level. A drop below that could lead to a retest of the Feb. 6 low of $0.381.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Bitcoin sinks below $71k as Powell’s hawkish tone and Iran’s oil shock trigger a $542M liquidation wave across leveraged crypto markets.

Summary

- Bitcoin drops to about $71,313, Ethereum to $2,201, as crypto and stocks sell off on Fed projections and oil shock fears.

- Powell flags oil-driven inflation, keeps just one 2026 rate cut in the dot plot, crushing hopes for easier policy and triggering a risk-off move.

- Over $542M in mostly long liquidations and Brent above $110 show how leveraged crypto positioning collides with Iran-driven energy turmoil.

Crypto markets extended their slide into Thursday as the combined aftershock of the Federal Reserve’s March policy meeting and an escalating oil shock from the Iran conflict continued to rattle risk assets. Bitcoin (BTC) fell to approximately $71,313 (-4.62%), Ethereum dropped to $2,201 (-5.92%), and a cascade of leveraged long positions was wiped out — with total network-wide liquidations reaching $542 million over 24 hours, of which $448 million were long positions. It was the largest liquidation event in weeks, and the most heavily one-sided since the early stages of the U.S.-Iran conflict in late February.

The proximate trigger was Wednesday’s Federal Open Market Committee decision and, more critically, the press conference that followed. The Fed held its benchmark rate at 3.5%–3.75% as universally expected, with the FOMC voting 11-1 to maintain that range. But the new Summary of Economic Projections — the first of 2026 — delivered the information markets least wanted to hear. The Fed raised its 2026 PCE inflation forecast to 2.7%, up from a prior estimate of 2.4%, citing the oil shock stemming from Iran’s blockade of the Strait of Hormuz as a direct driver. The dot plot’s median remained anchored at just one 25-basis-point cut for all of 2026, dashing residual hopes for a more accommodative path.

Fed Chair Jerome Powell was unambiguous in his press conference. “The oil shock for sure shows up,” he said, referring to its impact on the central bank’s projections. In his opening statement, he noted that near-term inflation expectations “have risen in recent weeks, likely reflecting the substantial rise in oil prices caused by the supply” disruption — a reference to the Hormuz closure that has taken roughly 20% of global oil flows offline since late February. Core PCE rose 3.0% in the 12 months through February, well above the Fed’s 2% target. Powell rejected comparisons to 1970s stagflation, arguing unemployment remains near normal levels, but acknowledged the tension between the Fed’s dual mandate goals in the current environment.

The market reaction was swift and familiar. Bitcoin dropped from approximately $74,000 to $70,900 within hours of the press conference — its eighth decline following an FOMC meeting out of the last nine. The Nasdaq closed down 1.5% on Wednesday, the Dow and S&P 500 reversed five consecutive sessions of gains to hit their lowest levels since November, and 10-year Treasury yields climbed more than 5 basis points. On Thursday, the selloff continued, with the Dow opening down 420 points (-0.91%), the S&P 500 -0.89%, and the Nasdaq -1.23%.

The liquidation breakdown tells its own story: Bitcoin longs alone accounted for $172 million in forced selling, ETH longs for $126 million, with a total of 143,776 traders liquidated globally. The largest single liquidation — an ETH position worth $17.98 million on Aster — underscores how aggressively leveraged some participants were ahead of the FOMC. Long-term Bitcoin holders were also reported to have sold over 1,650 BTC worth approximately $117 million in the wake of Powell’s remarks.

With Brent crude now above $110 per barrel following renewed Iranian attacks on regional energy facilities, and a Fed that has explicitly incorporated oil-driven inflation into its baseline forecast, the conditions for a near-term rate cut have seldom looked more remote.

Iran war unleashes ‘world energy shock’ and ‘King of the coast’

FDA recalls 90,000 bottles of children’s ibuprofen over foreign substance

Crypto.com to Cut 12% of Workforce due to Enterprise AI Integration

Smart energy pays enters the US market, targeting scalable financial infrastructure

Why Israel is blocking foreign journalists from entering

Bitcoin: We’re Entering The Most Dangerous Phase

Financial condition right now#viral #comedy #funny #ytshorts #trending #trend #financial #shorts

Saturday evacuation orders were due to Iranian missiles targeting residential areas in Doha

How Fake Money is Printed – Inside North Koreas Dollar Factory

-

Crypto World6 days ago

Crypto World6 days agoHYPE Token Enters Net Deflation as HyperCore Buybacks Outpace Staking Rewards

-

Tech4 days ago

Tech4 days agoYour Legally Registered ‘Motorcycle’ Might Not Count Under Proposed US Law

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Addict Lip Glow

-

Tech2 days ago

Tech2 days agoAre Split Spacebars the Next Big Gaming Keyboard Trend?

-

Sports5 days ago

Why Duke and Michigan Are Dead Even Entering Selection Sunday

-

Business4 days ago

Business4 days agoSearch for Savannah Guthrie’s Mother Enters Seventh Week with No Arrests

-

Business6 days ago

Business6 days agoUS Airports Launch Donation Drives for Unpaid TSA Workers as Partial Government Shutdown Enters Fifth Week

-

Crypto World5 days ago

Coinbase and Bybit in Investment Talks: Could Bybit Finally Enter the US Crypto Market?

-

Business4 days ago

Business4 days agoAustralian shares drop as Iran war enters third week

-

Business6 days ago

Business6 days agoCountry star Brantley Gilbert enters growing non-alcoholic beer market

-

Crypto World4 days ago

Crypto World4 days agoCrypto Lender BlockFills Enters Chapter 11 with Up to $500M in Liabilities

-

Sports6 days ago

Sports6 days agoCollege Basketball Best Bets: Conference Tournament Semifinal Picks

-

Politics2 days ago

Politics2 days agoThe House | The new register to protect children from their abusers shows Parliament at its best

-

Fashion4 days ago

Fashion4 days ago25 Celebrities with Curly Hair That Are Naturally Beautiful

-

News Videos1 day ago

News Videos1 day agoRBA board divided on rate cut, unusually buoyant share market | Finance Report | ABC NEWS

-

Crypto World1 day ago

Crypto World1 day agoCanada’s FINTRAC revokes registrations of 23 crypto MSBs in AML crackdown

-

Crypto World5 days ago

Crypto World5 days agoCrypto Losses Drop 87% in February, But Hackers Are Now Targeting People, Not Code

-

Politics2 days ago

Politics2 days agoReal-time pollution monitoring calls after boy nearly dies

-

NewsBeat1 day ago

NewsBeat1 day agoResidents in North Lanarkshire reminded to register to vote in Scottish Parliament Election

-

Business4 days ago

Business4 days agoMeta planning major layoffs as AI spending and automation reshape workforce

You must be logged in to post a comment Login