Crypto World

Jamie Dimon says ‘watch out’ as lofty asset prices add to economic risks: ‘My anxiety is high’

Jamie Dimon, chief executive officer of JPMorgan Chase & Co., during the 2025 IIF annual membership meeting in Washington, Oct. 16, 2025.

Samuel Corum | Bloomberg | Getty Images

JPMorgan Chase CEO Jamie Dimon said Monday that he was anxious over the U.S. economy, citing elevated asset prices and a competitive environment in banking that reminded him of the pre-2008 crisis years.

Even as economists tout the Trump administration’s tax and deregulatory policies as boosting economic growth this year, Dimon said during an annual investor update that his own tendencies were to consider what could go wrong when expectations are riding high.

“My own view is people are getting a little comfortable that this is real, these high asset prices and high volumes, and that we won’t have any problems,” said Dimon, who was dressed in black and wore a brace on one of his hands.

Inevitably, Dimon said, the economic cycle will turn, leading to a wave of borrower defaults that would broadly affect lenders, and often impacting industries few people expect, he said.

“There will be a cycle one day… I don’t know what confluence of events will cause that cycle. My anxiety is high over it,” Dimon said. “I’m not assuaged by the fact that asset prices are high. In fact, I think that adds to the risk.”

While fears over how artificial intelligence models from Anthropic and OpenAI could disrupt a myriad of industries — especially software firms — have churned markets in recent weeks, the broader S&P 500 isn’t far off from its all-time record level.

At the same time, concerns over loans to software companies at the nexus of AI worries have walloped private credit lenders after Blue Owl spooked markets last week when it announced it had to sell assets to satisfy investors clamoring to exit one of its funds.

The episode, which dragged down the shares of larger alternative asset managers including Apollo, KKR and Blackstone, led some market observers to wonder if the start of a broader downturn in credit had begun.

Doing ‘dumb things’

“There’s always a surprise in a credit cycle,” Dimon said. “The surprise has often been which industry” is impacted most, he said. “You didn’t expect utilities and phone companies in ’08, ’09, and this time around, it might be software, because of AI.”

Dimon also said that he endorsed his deputies’ comments about private credit from earlier in the investor event.

Troy Rohrbaugh, co-head of the firm’s commercial and investment bank, said that he didn’t think issues would likely be contained to private credit lenders, but instead be “more broad-based.”

“At this point, it feels a bit isolated to a handful of situations, but that could quite easily change, and we’re prepared for that,” Rohrbaugh said.

In response to a question from the veteran banking analyst Mike Mayo, Dimon said the current environment felt similar to the three years leading into the 2008 financial crisis in that “everyone is making a lot of money, people were leveraging, the sky was the limit.”

The JPMorgan chief said that some financial firms were “doing some dumb things” that involved chasing interest income, which is made through lending and investing activities, though he didn’t name the companies doing so.

“You feel stupid when everyone’s coining money and everyone’s great… it does feel really good,” Dimon said.

“And then when I think about all the factors taking place,” Dimon added, “I take a deep breath and say `watch out’.”

Dimon also addressed the perennial question of CEO succession at JPMorgan, which he built into the world’s largest bank by market capitalization over his two-decade tenure.

While he has often given a specific time frame for the number of years he had remaining as CEO, he avoided doing so on Monday.

“I was told to say this very specifically,” Dimon said to scattered laughter among the analysts in attendance. “I’m here for a few years as CEO, and maybe few after that as executive chairman.”

Key Highlights

-

XRP attracts record $119M, dominating weekly digital asset investment flows

-

Ethereum suffers continued decline with $52M withdrawal amid policy concerns

-

Bitcoin records $107M inflows while bearish positioning expands significantly

-

Swiss markets dominate global flows as American investor appetite weakens

-

Economic data triggers late-week reversal in cryptocurrency investment momentum

Cryptocurrency investment products attracted $224 million in fresh capital over the past week, representing a short-lived bounce following previous withdrawals. However, macroeconomic headwinds dampened enthusiasm as the week concluded. XRP emerged as the clear winner while Ethereum’s outflow streak extended.

XRP Commands Investment Flows with Record Weekly Performance

[[LINK_START_0]]XRP[[LINK_END_0]] captured the lion’s share of investment activity, pulling in $119.6 million during the week. This represented the digital asset’s most impressive showing since late December 2025. The momentum persisted even as broader cryptocurrency markets displayed vulnerability. Year-to-date, XRP has accumulated $159 million in net inflows.

The impressive performance followed sustained investor interest after the introduction of spot XRP exchange-traded products in American markets. These investment vehicles enhanced accessibility and facilitated continuous capital movement into the asset. Consequently, XRP now represents approximately seven percent of aggregate assets managed across cryptocurrency funds.

European financial centers played a significant role in driving XRP’s success. Switzerland emerged as the top contributor with more than $157 million in capital inflows, while Germany and Canada also participated strongly. This geographic distribution indicated evolving capital deployment strategies across international cryptocurrency markets.

Bitcoin Displays Conflicting Trends as Investor Sentiment Splits

Bitcoin attracted $107.3 million in new investments, demonstrating modest revival following earlier capital withdrawals. However, monthly performance remained in negative territory, with cumulative outflows reaching $145 million. This divergence underscored persistent indecision regarding the asset’s trajectory.

Inverse bitcoin products drew $16 million in capital, revealing heightened pessimistic positioning among certain market participants. Simultaneously, American spot bitcoin exchange-traded funds contributed minimally to overall flows. These contradictory indicators exposed a fundamental divide in investor outlook.

Meanwhile, Solana accumulated $34.9 million in inflows, extending its positive momentum throughout the current year. Its aggregate inflows now constitute roughly ten percent of total managed assets. This reliable performance reinforced broader portfolio diversification trends within digital asset investment products.

Ethereum Suffers Substantial Withdrawals Amid Legislative Uncertainty

Ethereum maintained its negative trajectory, experiencing $52.8 million in weekly capital flight. This followed an even larger $222 million exodus the preceding week. The asset’s year-to-date outflows have now reached $327 million.

Legislative ambiguity surrounding the Digital Asset Market Clarity Act continued exerting downward pressure on Ethereum-focused investment vehicles. The proposed legislation remained gridlocked in the Senate due to disputes regarding stablecoin yield components. This impasse negatively impacted sentiment toward Ethereum’s ecosystem positioning.

Ethereum’s fundamental importance to stablecoin infrastructure heightened its vulnerability to regulatory developments. This strategic exposure amplified pressure on capital movements during periods of policy ambiguity. Ethereum stood out as the poorest performer among leading cryptocurrency assets.

Broader economic conditions also shaped overall investment product activity throughout the period. Robust American retail sales figures reinforced projections of continued restrictive monetary policy. This evolution diminished risk tolerance and prompted modest withdrawals as the week closed.

Simultaneously, rising crude oil valuations and receding interest rate reduction expectations intensified market headwinds. These dynamics interrupted early-week positive momentum across digital asset investment vehicles. Ultimately, the weekly recovery proved incomplete and varied substantially across geographic regions and individual assets.

Ether treasury companies may need to use liquid staking and other active yield strategies if they want to offer investors something beyond the staking rewards already available through listed Ether products, Kean Gilbert, head of institutional relations at Lido, told Cointelegraph at ETHCC 2026.

Liquid staking lets Ether (ETH) holders stake their tokens while receiving a transferable token that can still be deployed elsewhere in decentralized finance (DeFi).

Gilbert said strategies such as posting ETH as collateral and borrowing against it could help treasury companies generate higher returns than passive staking products.

US-listed staked ETH products now include the REX-Osprey ETH + Staking ETF, launched in September 2025, Grayscale’s Ethereum Staking ETF and Ethereum Staking Mini ETF, and BlackRock’s iShares Staked Ethereum Trust ETF, introduced on March 12.

Issuer disclosures show different staking economics across Ether products, making direct yield comparisons difficult. Grayscale’s ETHE page showed 2.26% net staking rewards as of April 6, while Grayscale’s ETH page showed 2.56% as of April 2. Native ETH staking was yielding about 2.72% annually, according to Staking Rewards.

Related: Bitmine paper loss nears $8.8B as Ether slump tests cyclical thesis

Still, Jimmy Xue, co-founder and chief operating officer of quantitative yield platform Axis, said Ether treasury companies do not necessarily need to beat staked Ether products on headline yield because they are different investment vehicles.

“A staked ETH ETF is a passive vehicle. A DAT trading at a meaningful mNAV premium is promising something a passive ETF structurally cannot deliver, which is active, dynamic deployment of spot inventory across opportunities as they arise.”

“The mNAV premium investors pay reflects confidence in management’s ability to put that treasury to work,” Xue said, adding that basis trading is a major yield source for treasury companies.

Public filings show liquid staking adoption

Public disclosures show several Ether treasury firms using staking or liquid-staking-related strategies, though the level of detail varies by company.

Sharplink Gaming, the second-largest corporate Ether holder, has generated 14,516 ETH (around $30.8 million) in staking rewards as of March. It derived 33% of these rewards from liquid staking and 66% from native staking, according to a March 1 filing with the US Securities and Exchange Commission.

Sharplink reported a $734 million net loss for 2025, largely driven by the sharp crypto market downturn in the second half of the year.

BTCS Inc., the 10th-largest Ether treasury company by returns, has also staked a part of its Ether holdings through the liquid staking protocol Rocket Pool. Out of its total 29,122 ETH holdings, the company has liquid staked 4,160 ETH ($8.8 million) through Rocket Pool nodes, according to a July 2025 SEC filing.

Cointelegraph has approached BitMine, SharpLink and The Ether Machine for comment on the role of liquid staking in their strategies.

Magazine: Sharplink exec shocked by level of BTC and ETH ETF hodling — Joseph Chalom

Phone logs obtained by federal prosecutors in Argentina show seven calls between President Javier Milei and entrepreneur Mauricio Novelli – one of the architects of the LIBRA crypto token, on the same night in February 2025 that Milei posted the now-infamous promotion on X, directly contradicting Milei’s public claim of no connection to the coin’s launch.

Recovered notes from Novelli’s phone outline a $5 million deal structure tied to Milei’s official endorsements, including payments contingent on Milei naming Hayden Davis of Kelsier Ventures as a cryptocurrency advisor.

The documents place Milei inside the deal’s mechanics, not outside them.

- The Core Evidence: Argentine federal prosecutors have obtained phone logs showing seven calls between Milei and Novelli before and after his February 14, 2025, X post promoting $LIBRA at 7:01 pm local time.

- The Financial Trail: A deleted note recovered from Novelli’s phone describes a $5 million arrangement with an individual identified as “H” – likely Davis – including $1.5 million upon Milei announcing Davis as a crypto advisor.

- The Scale of Losses: An estimated 114,410 wallets lost funds in the $LIBRA collapse, with total investor losses ranging from $251 million to $400 million; only 36 wallets cleared more than $1 million in profit.

- Milei’s Legal Status: Milei is named as a person of interest in the ongoing federal probe but has not been formally charged; he has not publicly responded to the call logs or recovered documents.

- Obstruction Signal: Milei dissolved Argentina’s Investigation Task Unit (UTI) via Decree 332/2025 in May 2025 – after the UTI had forwarded insider trading findings to prosecutors.

- What to Watch: Argentina’s Chamber of Deputies begins questioning government officials on April 8, 2026; any move toward formal charges or new forensic disclosures from that session will be the next inflection point in this investigation.

Discover: The Best Crypto Presales Live Right Now

What the Phone Logs Actually Show – and Why Milei “No Connection” Defense No Longer Holds

Milei posted about LIBRA crypto at 7:01 pm Argentina time on February 14, 2025. The seven documented calls to Novelli occurred in the hours immediately before and after that post – a timeline that prosecutors are now treating as evidence of coordination, not coincidence.

The contents of the calls remain unknown, but the pattern of contact alone is legally significant: it establishes proximity between Milei and the token’s operators at the precise moment of maximum promotional impact.

The recovered deleted note from Novelli’s phone goes further. Forensic analysis of the document – dated October-November 2024 – describes a three-tranche payment structure: $1.5 million upfront to “H,” $1.5 million upon Milei’s public announcement of Davis as an advisor, and $2 million in blockchain and AI advisory contracts involving both Milei and his sister Karina Elizabeth Milei.

Milei met Davis at Casa Rosada on January 30, 2025, posting a selfie on X that same day and describing him as a cryptocurrency advisor – the precise trigger for the second $1.5 million tranche outlined in Novelli’s note.

Computer experts confirmed that the 44-character $LIBRA contract code Milei included in his February promotional post was not publicly available online prior to the post, meaning Milei had access to insider technical data before the token launched publicly.

WhatsApp audio messages reviewed as part of the investigation also reference recurring payments made to Milei during his time as a congressman, with specific sums reportedly allocated to Karina Milei as well.

Novelli allegedly brokered regulatory favors in exchange, including tax exemptions, suggesting the financial relationship predates the $LIBRA launch by years. Milei’s dissolution of the UTI via Decree 332/2025 in May 2025, after that body had already forwarded insider trading findings to prosecutors, adds an obstruction dimension that investigators are unlikely to set aside.

Explore: The Best Pre-Launch Token Sales With Asymmetric Upside Potential

The post New Evidence Emerges in Argentina President Milei’s Libra Token Probe appeared first on Cryptonews.

A Nobel Prize–winning physicist who helped build Google’s quantum computers warned that Bitcoin may be among the earliest real-world targets of the technology.

In an interview with CoinDesk, John M. Martinis said recent Google research showing how a quantum computer could break bitcoin encryption in minutes should be taken seriously.

“I think it’s a very well-written paper. It lays out where we are right now,” Martinis said, referring to Google’s latest work on quantum threats to cryptography. “It’s not something that has zero probability; people have to deal with this.”

READ: A simple explainer on what quantum computing actually is, and why it is terrifying for bitcoin

The Google paper outlines how a sufficiently advanced quantum computer could derive a bitcoin private key from its public key, potentially within minutes, dramatically reducing the computational barrier that currently secures the network, Martinis highlighted, adding this is one of the issues that must be taken most seriously..

READ: Here’s what ‘cracking’ bitcoin in 9 minutes by quantum computers actually means

While the idea of quantum computers breaking encryption is often framed as distant or theoretical, Martinis said one of the first practical applications may be far more immediate.

Lowest hanging fruit for quantum computers

“It turns out that breaking cryptography is one of the easier applications for quantum computing, because it’s very numeric,” he said. “These are the smaller, easier algorithms. The low-hanging fruit.”

That places bitcoin, which relies on elliptic curve cryptography, directly in the line of fire, Martinis suggested, confirming what the Google paper warns.

Unlike traditional financial systems, which can migrate to quantum-resistant encryption standards, bitcoin faces a more complex challenge. Its decentralized structure and historical design make upgrades slower and more contentious, the Nobel Prize winner said.

“You can go to quantum-resistant codes” in banking and other systems, Martinis said. “Bitcoin is a little bit different, which is why people should be thinking about this right now.”

The concern centers on a specific vulnerability window. When a bitcoin transaction is broadcast, its public key becomes visible before it is confirmed onchain, Martinis explained. A powerful quantum computer could, in theory, use that window to derive the corresponding private key and redirect funds before final settlement, he noted.

However, Martinis cautioned against assuming the threat is imminent. Building a quantum computer capable of executing such an attack remains one of the hardest engineering challenges in modern science.

“I think it’s going to be harder to build a quantum computer than people are thinking,” he said, pointing to major hurdles in scaling, reliability and error correction.

No reason for inaction

Estimates for when cryptographically relevant quantum machines could emerge vary widely. Martinis suggested a rough five- to ten-year window, but warned that uncertainty is not a reason for inaction.

“Given the serious consequences, you deal with it. You have time, but you have to work on it,” he said.

The warning highlights a growing shift inside the quantum research community, where scientists are increasingly flagging risks to existing cryptographic systems while withholding sensitive technical details — a strategy borrowed from traditional cybersecurity disclosure practices.

For bitcoin developers and investors alike, the message is becoming harder to ignore.

“The crypto community has to plan for this,” Martinis said. “It’s a serious issue that has to be dealt with.”

Martinis is a 2025 Nobel Prize–winning physicist recognized for his work on macroscopic quantum phenomena and is widely known for leading Google’s quantum hardware program, including the 2019 “quantum supremacy” experiment. He is currently CTO and co-founder of Qolab, a hardware company developing utility-scale superconducting quantum computers.

After topping $70,000 on Monday, bitcoin has pulled back to the $68,000 area as time draws near for President Trump’s Tuesday deadline for Iran to reopen the Strait of Hormuz.

“A whole civilization will die tonight, never to be brought back again,” said Trump in a Tuesday morning Truth Social Post. “I don’t want that to happen, but it probably will,” he continued. “We will find out tonight, one of the most important moments in the long and complex history of the world.”

Alongside declines in crypto, U.S. stock index futures are poised to open lower, led by the Nasdaq 100’s 0.65% decline. WTI crude oil is higher by 1.7% to $114.22 per barrel.

Tempering declines across markets were comments from vice president J.D. Vance, who — while reiterating the 8 pm ET deadline — said the military objectives of the Iran war have been completed.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Crypto presales gain traction as investors position early for the next market cycle.

Summary

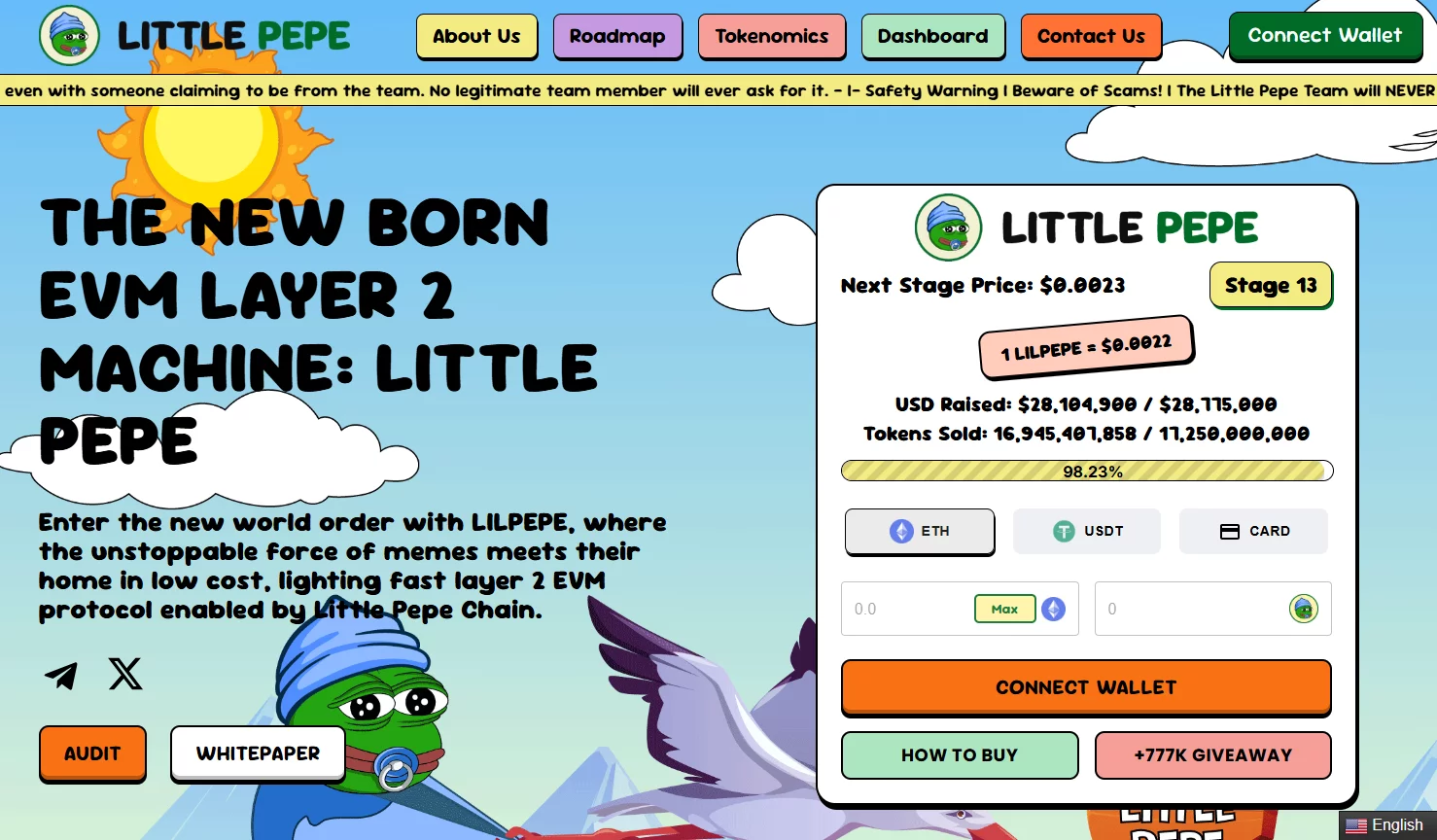

- Little Pepe (LILPEPE) presale surpasses $28 million in Stage 13, approaching next price tier at $0.0023

- LILPEPE leverages Layer 2 Ethereum tech, zero-tax trades, staking, DAO governance, and meme-based rewards

- Presale investors in 2026 eye Little Pepe for high early-stage growth and community-driven crypto utility

As the crypto market gets ready to take its next big leap, presale projects are gaining significant traction from investors. This is because, at such an early stage, they tend to have the greatest growth potential, particularly when they have a strong story behind them. The 2026 crypto cycle is on the horizon, and finding growing presales early on could be the key to making the most of them.

Little Pepe (LILPEPE)

One of the most advanced projects in terms of presale is Little Pepe (LILPEPE). The project has already secured more than $28 million in funding and is currently in Stage 13, nearing completion. The current price of each token is $0.0022, and in the next stage, each token will cost $0.0023.

The project has a fixed total token supply of 100 billion tokens, out of which 26.5 billion is allocated for the presale. The project is based on a Layer 2 blockchain technology compatible with Ethereum and has zero tax trades, sniper bot protection, staking rewards, DAO governance, and a meme launchpad. The project also has some amazing giveaways and rewards that increase community engagement and participation.

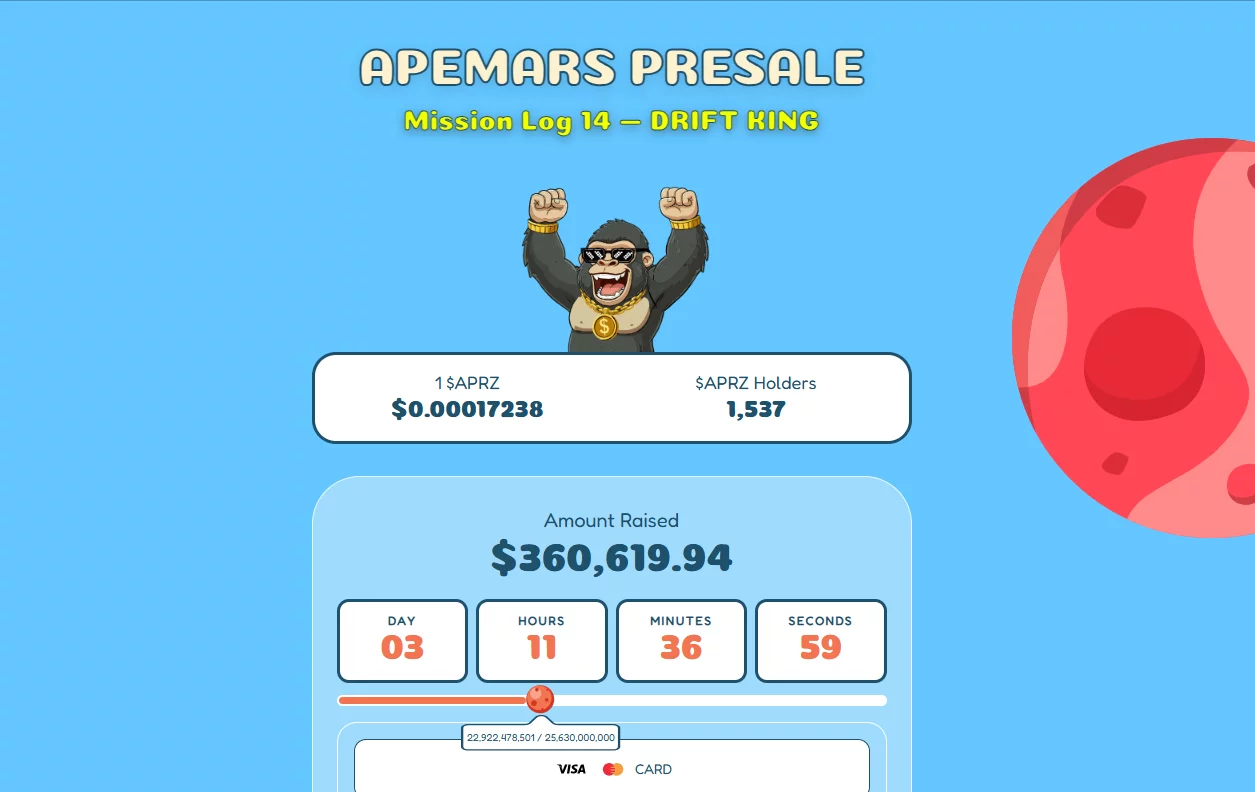

ApeMars (APRZ)

ApeMax is a new presale project that stands out from the rest due to its ‘Boost to Earn’ mechanism. The presale stage is divided into different stages. The presale stage 14 has gathered more than $360,619. The APRZ token is sold for $0.00017238 per token. The project is significant due to its focus on early token use cases, allowing investors to use the tokens right away. The total token supply is also a key feature of ApeMax.

Bitcoin Hyper (HYPER)

Bitcoin Hyper is one of the largest presales in the current market. It seeks to add the much-needed scalability to the Bitcoin blockchain. So far, the project has managed to raise over $32.2 million. It is trading at the early stages of the micro-cap level, with each token costing $0.0136778. It is expected to rise with the phases. It is one of the utility-driven presales heading into 2026, considering its aim to add Bitcoin to the Defi space using smart contracts.

Maxi Doge (MAXI)

Maxi Doge is a meme-driven presale project focused on high-energy community engagement and staking rewards. The presale has already raised approximately $4.7 million, reflecting growing retail participation. The current token price is around $0.0002811, with incremental increases planned across presale phases. While exact total supply figures vary, the project includes large staking pools (over 10 billion tokens allocated) and reward mechanisms designed to incentivize early holders.

DogeBall (DOGEBALL)

DogeBall is a new presale project, which is still in development, with a concept involving meme culture and a sports/gaming-based ecosystem. The project has a series of stages in its presale, with currently priced at $0.0004 in its presale stage 2, which will increase in later stages. The funding is still in development, but the project is getting attention due to its unique niche and community-based concept, making DogeBall a new and promising contender in the presale space for 2026.

Early presales could define the next winners

As the crypto market continues to head into a new boom in 2026, presale projects are a significant focus for high-growth opportunities. Although all these tokens have different characteristics, Little Pepe stands out due to its impressive funding milestone and presale growth. Presale projects are essential for investors who want to gain access to new and promising projects early.

For more information about Little Pepe, visit the official website, X, and Telegram.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Samsung Electronics’ shares got a nice boost on Tuesday morning after the company predicted a record-breaking quarter fueled by the massive boom in AI hardware. The stock jumped as much as 4.8% during the day before settling into a 1.76% gain by the close.

Summary

- Samsung Electronics shares rose after forecasting record Q1 profit, driven by strong AI memory demand.

- Operating profit is projected at 57.2 trillion won, more than eight times higher year over year and above analyst estimates.

- Supply chain risks tied to Middle East tensions could disrupt chip materials like helium and weigh on the outlook if prolonged.

According to its early estimates, Samsung is looking at an operating profit of roughly 57.2 trillion won, which is about $37.8 billion, for the first quarter. To put that massive figure in perspective, it is more than eight times what the company made during the same time last year.

If these numbers hold, it will set a brand new quarterly record for the company. The projected profit is nearly triple their previous all-time high and easily crushed the 42.3 trillion won that analysts were originally expecting.

The revenue side looks just as impressive. Samsung expects sales to hit about 133 trillion won, which is a nearly 70% jump year over year. This would also mark the first time the company’s quarterly revenue has ever crossed the 100 trillion won threshold.

MS Hwang, a research analyst at Counterpoint Research, told CNBC that Samsung’s latest numbers are so huge that they are now rivaling the scale of global Big Tech giants.

The strong outlook is largely tied to demand for high-bandwidth memory, or HBM, a critical component used in accelerators from companies like NVIDIA and AMD that power artificial intelligence workloads. Expansion of data centers and rapid growth in AI model training have significantly increased memory requirements, tightening supply and pushing prices higher.

Industry projections suggest memory prices tied to data center applications will continue rising in the coming months. Samsung’s earnings trajectory shows how deeply the AI boom has translated into financial performance, with memory chips forming the core of its profit engine.

Demand for HBM has surged over the past year, leading to supply shortages across the memory market and driving sharp increases in both pricing and shipment volumes. Hwang noted that commodity memory prices could rise by more than 50% in the second quarter, with tight supply conditions expected to persist.

Samsung is also looking to regain its footing in the high-bandwidth memory segment after ceding early leadership to domestic rival SK Hynix, which was quicker to supply advanced AI memory.

Samsung’s Device Solutions division, which houses its memory chip business, accounted for 39% of total revenue and 57% of operating profit in 2025, underlining the segment’s importance to overall earnings.

The company is set to release its full earnings report later this month. While current projections point to strong performance, external risks remain.

Geopolitical risks in focus

Rising tensions in the Middle East are starting to disrupt semiconductor supply chains, with shipments of key materials such as helium facing delays.

The U.S.–Israel conflict involving Iran has raised concerns about access to these inputs, which are essential for chip production, increasing the risk of operational challenges for major manufacturers like Samsung Electronics and SK Hynix.

“If the Middle East conflict ends quickly, it will not significantly impact profits. However, if it persists for several months or longer, it will lead to severe consequences,” Hwang said.

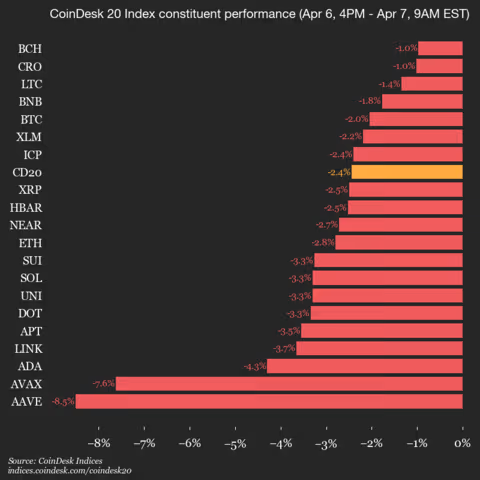

CoinDesk Indices presents its daily market update, highlighting the performance of leaders and laggards in the CoinDesk 20 Index.

The CoinDesk 20 is currently trading at 1917.55, down 2.4% (-47.87) since yesterday’s close.

All 20 assets are trading lower.

Leaders: BCH (-1.0%) and CRO (-1.0%).

Laggards: AAVE (-8.5%) and AVAX (-7.6%).

The CoinDesk 20 is a broad-based index traded on multiple platforms in several regions globally.

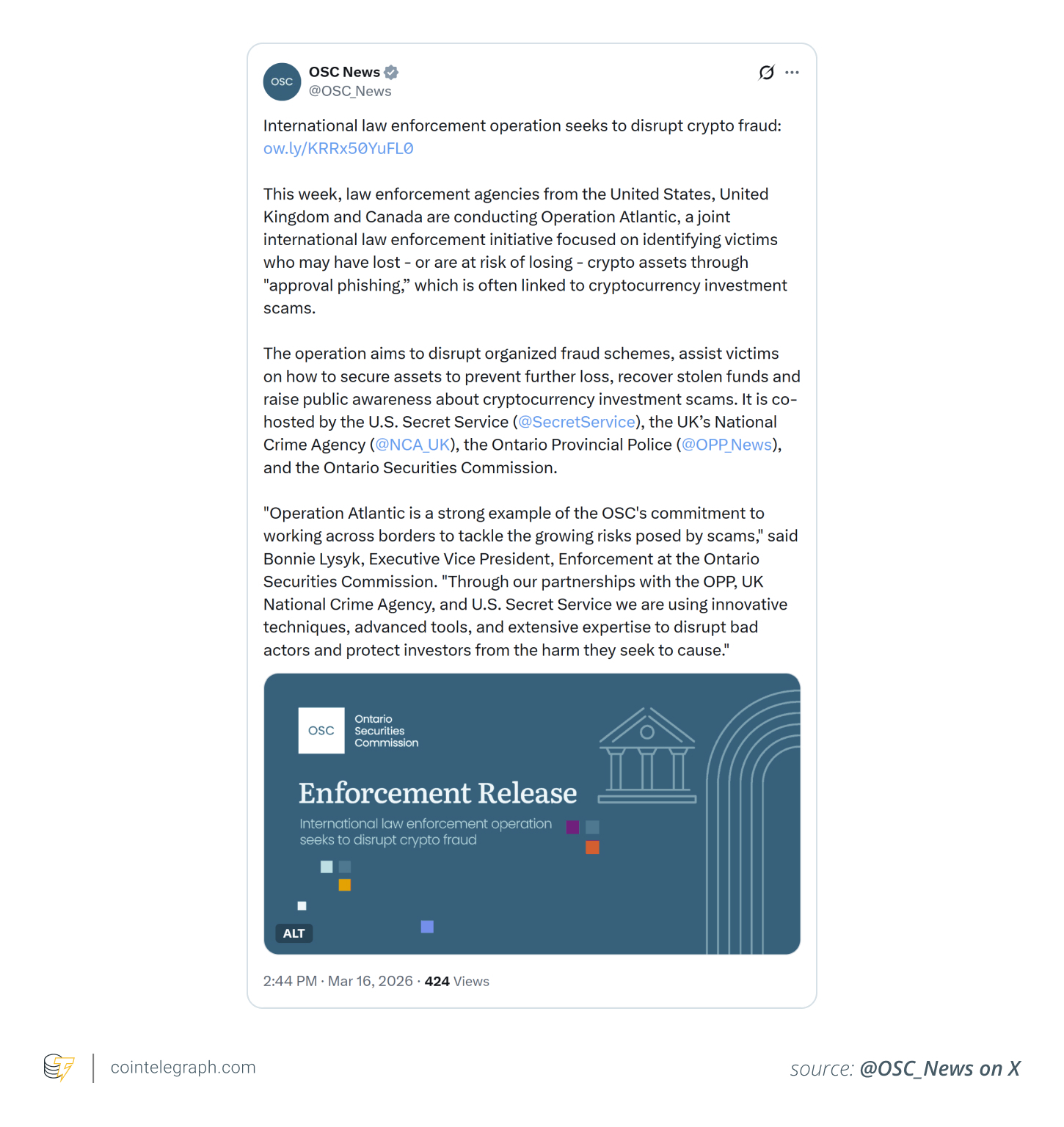

Operation Atlantic: A proactive strike against evolving crypto scams

Crypto scams have become highly sophisticated cross-border operations that exploit advanced technology and human psychology. By the time victims become aware of the fraud, the stolen cryptocurrency is often rapidly dispersed across a chain of wallets and exchanges in multiple countries.

Operation Atlantic represents a coordinated international effort by law enforcement agencies from the US, the UK and Canada to counter this threat. Rather than limiting itself to post-incident investigations, the operation focuses on identifying, tracking and disrupting crypto scams while they are still in progress.

The initiative brings together key agencies, including the US Secret Service, the US Attorney’s Office for the District of Columbia, the Ontario Provincial Police, the Ontario Securities Commission, the Royal Canadian Mounted Police, the UK Financial Conduct Authority, the UK National Crime Agency and the City of London Police.

Contrary to conventional investigations that begin only after funds have been stolen, Operation Atlantic is structured to:

-

Identify victims who are at risk

-

Detect active scam infrastructure

-

Interrupt fraudulent transactions

-

Help recovery efforts where feasible

Officials have stressed that the primary objective is to disrupt scams in near real time, marking a significant shift toward faster, more proactive enforcement strategies.

Why approval phishing lies at the heart of Operation Atlantic

A particular form of fraud known as approval phishing lies at the center of Operation Atlantic. Rather than stealing private keys or seed phrases, attackers deceive users into signing what appear to be legitimate blockchain transactions.

These transactions grant scammers permission to spend tokens directly from a victim’s wallet. Once approval is given, the attacker gains the ability to:

This makes approval phishing particularly dangerous. Victims often remain unaware that anything is wrong until their assets begin disappearing.

Scammers frequently integrate this technique into larger scams, such as fake investment platforms or gradual trust-building schemes.

From investigation to intervention

The standout feature of Operation Atlantic is its emphasis on real-time disruption rather than post-event analysis.

This strategy rests on a straightforward idea: While crypto transactions are irreversible, they are also public and fully traceable.

By using blockchain analytics, authorities and private-sector partners can:

-

Detect suspicious wallet activity

-

Identify addresses linked to known scams

-

Track fund flows toward exchanges or liquidity pools

-

Alert platforms and investigators

-

Contact victims before their funds are completely drained

This model does not guarantee full recovery, but it opens a critical window during which meaningful intervention remains possible.

Did you know? The US Secret Service, originally established to combat currency counterfeiting in 1865, now tracks crypto fraud using blockchain analytics. It is one of the oldest agencies adapting to one of the newest financial systems.

Building on earlier initiatives

Operation Atlantic did not happen overnight. It builds upon earlier efforts such as Project Atlas, which was launched in 2024 by Canadian authorities in partnership with the US Secret Service to target crypto fraud networks.

It also draws on lessons from Operation Spincaster, an effort that involved blockchain analytics firms, exchanges and law enforcement agencies.

Spincaster demonstrated that coordinated action could deliver tangible results:

-

Thousands of scam-linked wallet leads identified

-

Significant losses mapped across jurisdictions

-

In some cases, victims were warned in time to revoke malicious approvals

These initiatives suggest that crypto fraud can be interrupted while it is still in progress.

What “real time” actually means

The concept of real-time disruption is sometimes misunderstood. It does not mean instant recovery or guaranteed prevention.

Instead, it operates across three stages:

-

Pre-loss prevention: spotting suspicious approvals before funds are moved

-

Mid-transaction disruption: flagging or freezing assets during transfers

-

Post-loss response: attempting recovery after funds have been dispersed

Operation Atlantic concentrates mainly on the first two stages, where intervention is still feasible.

Its success depends on how quickly data can be analyzed, shared and acted upon across borders and platforms.

Did you know? Approval phishing scams often exploit wallet permissions rather than passwords, which means victims technically authorize the theft themselves. This psychological twist makes these scams harder to detect than traditional hacking attempts.

Why scams now operate like organized networks

Approval phishing scams are generally not standalone events. They typically operate as structured networks with several interconnected parts:

-

Social engineering pipelines to attract victims

-

Fake interfaces or decentralized applications

-

Wallet approval mechanisms

-

Consolidation addresses used to pool stolen funds

-

Exchange off-ramps for cashing out

This layered setup allows scammers to scale their operations while reducing the likelihood of detection.

Operation Atlantic treats these scams as coordinated financial networks rather than isolated crimes, an approach that is central to its real-time disruption strategy.

The scale of the problem

The urgency behind Operation Atlantic stems from the enormous scale of crypto fraud.

Approval phishing alone has been linked to billions of dollars in losses in recent years, affecting thousands of victims across multiple jurisdictions.

Even more concerning is that many incidents go unreported, suggesting the true losses may be substantially higher.

Monthly figures also show that while overall exploit losses may vary, phishing attacks continue to rise, confirming that user-targeted scams remain one of the most persistent threats in crypto.

Did you know? Law enforcement agencies increasingly use blockchain clustering to map entire scam networks, sometimes revealing thousands of linked wallets behind a single fraud operation. This forensic technique groups related wallet addresses.

The role of public-private coordination

A key aspect of Operation Atlantic is the close partnership between law enforcement and private-sector organizations.

Each participant contributes in specific ways:

-

Blockchain analytics firms identify suspicious patterns and wallet clusters

-

Exchanges monitor inflows and flag deposits linked to scams

-

Stablecoin issuers may help freeze funds in targeted cases

-

Platforms and wallets can warn users or block malicious interactions

This level of coordination enables faster responses than conventional investigations, which often rely on slower legal procedures.

At the same time, it raises expectations for platforms to play a more active role in fraud detection.

The limits of real-time disruption

Despite its goals, Operation Atlantic faces several structural constraints:

-

Once funds are bridged or layered across multiple services, recovery becomes extremely difficult

-

User behavior remains a major vulnerability, particularly in social engineering scenarios

-

Cross-border legal processes can still delay enforcement actions

-

Wallet anonymity makes victim identification more complicated

In many cases, the most realistic outcome is preventing further losses rather than achieving full recovery of stolen assets.

What this means going forward

Operation Atlantic reflects a broader shift in how crypto-related crime is being tackled.

Rather than viewing fraud as a fixed, one-time event, authorities now treat it as a dynamic, ongoing process that can be monitored and disrupted while it is still in progress.

For users, this shift may result in:

-

More frequent warnings about suspicious transactions

-

Greater emphasis on understanding wallet permissions

-

Increased awareness of scam risks

For platforms, it could lead to:

-

Higher expectations for transaction monitoring

-

Deeper collaboration with law enforcement

-

Integration of real-time risk detection tools

Key Takeaways

- Biogen has entered into a multi-target partnership with Alloy Therapeutics to leverage Alloy’s AntiClastic™ ASO technology for developing antisense therapeutics.

- Financial terms include upfront compensation for Alloy, along with potential milestone-based payments and tiered royalty structures.

- The partnership builds on an existing relationship dating back to 2020, which initially centered on antibody-based therapies.

- RBC Capital reduced Biogen’s price target from $233 to $213 while maintaining its Outperform recommendation.

- Wall Street analysts have established a consensus price target of $210.30 for BIIB with an overweight rating.

Biogen has formalized a strategic partnership with Alloy Therapeutics, securing rights to utilize Alloy’s proprietary AntiClastic™ antisense oligonucleotide (ASO) technology platform for developing therapies targeting several yet-to-be-disclosed disease areas.

Under the terms of the arrangement, Alloy Therapeutics will collect an initial payment, with opportunities to earn additional compensation through development and commercial milestones, plus royalty payments tied to any successfully marketed products.

While the two biotechnology firms have maintained a collaborative relationship since 2020, their previous work concentrated on antibody-based treatment development. This latest agreement marks a strategic shift toward genetic medicine applications.

Biogen brings substantial experience to ASO drug development. The company’s Spinraza, approved for treating spinal muscular atrophy, represents one of the commercial success stories in antisense therapy. This new collaboration aims to expand that expertise through Alloy’s technology platform.

Alloy CEO Errik Anderson characterized the partnership straightforwardly: “Biogen is a leader in the space and has made huge contributions to ASO technologies. We view this as validation and an opportunity to build on their experience.”

The collaboration will prioritize three key objectives for Alloy’s platform: increasing therapeutic potency, reducing immunogenic responses, and improving targeted tissue delivery.

Alloy’s Expanding Partnership Portfolio

Headquartered in Waltham, Massachusetts, Alloy has established a business model centered on collaborative drug discovery and development with biopharmaceutical companies. Since launching in 2017, the company has executed approximately 200 partnership agreements, with over 100 producing licensed therapeutic candidates.

The platform has contributed to 22 drug candidates that have advanced into clinical testing. In 2024, Sanofi entered into an agreement potentially worth up to $400 million to access this same ASO technology for developing central nervous system treatments.

Christian Cobaugh, who leads Alloy’s Genetic Medicine Division as CEO, indicated the Biogen collaboration will enable the company to expand its involvement beyond initial discovery phases into later-stage development activities.

Alloy differentiates itself from typical platform biotechnology companies by focusing exclusively on partnerships rather than developing an internal proprietary pipeline.

Wall Street’s Perspective on Biogen

From an analyst perspective, RBC Capital Markets revised its price target for BIIB downward to $213 from a previous $233 on April 7, though the firm maintained its Outperform rating.

According to FactSet’s analyst consensus data, the mean price target for Biogen shares currently sits at $210.30, accompanied by an overweight rating across the Street.

BIIB shares declined 2.82% on the trading day when the partnership was publicly announced.

Ottoman Hands Pearl Earrings for Women Collection

‘Outstanding’ thriller hailed ‘best show I’ve seen’ lands new UK streaming home

Beyond The Deadline: What Markets Are Still Not Pricing In

-

NewsBeat5 days ago

NewsBeat5 days agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Business5 days ago

Business5 days agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Spanx – Corporette.com

-

Crypto World6 days ago

Crypto World6 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Business2 days ago

Business2 days agoThree Gulf funds agree to back Paramount’s $81 billion takeover of Warner, WSJ reports

-

Sports3 days ago

Sports3 days agoIndia men’s 4x400m and mixed 4x100m relay teams register big progress | Other Sports News

-

Business3 days ago

Business3 days agoExpert Picks for Every Need

-

Business5 days ago

Business5 days agoLogin and Checkout Issues Spark Merchant Frustration

-

Sports7 days ago

Sports7 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Crypto World7 days ago

Crypto World7 days agoBitcoin enters the public bond market as Moody’s gives a first-of-its-kind crypto deal a rating

-

Crypto World7 days ago

Bitcoin stalls below key resistance as technical signals skew bearish

-

Tech5 days ago

Tech5 days agoCommonwealth Fusion Systems leans on magnets for near-term revenue

-

Business2 days ago

No Jackpot Winner, Prize to Climb to $231 Million

-

Politics7 days ago

Politics7 days agoStarmer’s centre has collapsed, and the left was right all along

-

Fashion1 day ago

Fashion1 day agoMassimo Dutti Offers Inspiration for Your Summer Mood Board

-

Crypto World7 days ago

AI Memory Rout Wipes 9% Off Nvidia Stock: Chart Says More Pain Ahead

-

Crypto World6 days ago

Crypto World6 days agoWhy It’s Partnering, Not Issuing

-

Crypto World6 days ago

Crypto World6 days agoRipple rolls out enterprise crypto treasury platform for corporates

-

Tech7 days ago

Tech7 days agoOakcastle MP300 review: the super-cheap MP3 player that can

-

Politics7 days ago

Politics7 days agoRupert Lowe has his dog shot, don’t forget

You must be logged in to post a comment Login