Crypto World

JPMorgan faces test on bank liability in $328M Goliath Ponzi case

JPMorgan faces a U.S. class action for allegedly enabling Goliath Ventures’ $328M crypto Ponzi via Chase accounts and exchange transfers.

Summary

- Investors claim Goliath raised $328M from 2,000+ victims through JPMorgan business accounts, routing $123M to Coinbase while paying out only $50M in “profits.”

- The suit alleges JPMorgan ignored AML red flags on high‑velocity, circular transfers, effectively extending the scheme’s life and investor losses.

- The case could set precedent on when banks become liable as “enablers” of crypto fraud, tightening KYC/AML expectations on fiat rails into exchanges.

JPMorgan is facing a new class-action lawsuit in the U.S. over its alleged role in banking a $328 million crypto Ponzi scheme that funneled investor funds through Chase accounts and onto major exchanges, according to recent court filings and monitoring data.

JPMorgan sued over alleged $328M crypto Ponzi exposure

A group of investors has filed a class-action complaint in federal court in Northern California, accusing JPMorgan Chase of knowingly or negligently providing banking services to a large-scale crypto Ponzi scheme operated by Goliath Ventures. The lawsuit alleges that roughly $253 million in investor funds were first deposited into Chase accounts controlled by the scheme’s operators, before approximately $123 million was routed to Coinbase and other exchanges, while only about $50 million was returned to investors as purported “profits.”

According to the complaint, plaintiffs claim JPMorgan failed to act on multiple anti–money laundering red flags, including rapid, large-value transfers inconsistent with declared business activities and repeated inflows from retail investors. They argue that the bank’s alleged failure to file or escalate suspicious activity reports allowed the scheme to continue far longer than it otherwise would have, dramatically increasing total losses. The case seeks damages for investors and aims to hold one of the world’s largest banks liable for what plaintiffs frame as willful blindness to obvious fraud patterns.

Potential precedent for banking rails in crypto fraud

If the case proceeds, it could become a test of how far U.S. courts are willing to extend liability to traditional financial institutions that provide fiat on- and off-ramps to crypto-related investments. Plaintiffs are effectively arguing that banks cannot treat crypto fraud as an external problem while continuing to profit from deposit flows and payment processing tied to suspicious schemes.

For the broader digital asset sector, the lawsuit underscores a growing regulatory and legal focus on “enablers” of fraud, not just token issuers or platform operators. Exchanges and custodians already sit under heavy scrutiny; extending that lens to global banks that process billions in flows for crypto investment products could reshape compliance expectations around KYC/AML, transaction monitoring, and de-banking of high-risk promoters. The outcome is likely to be closely watched by both Wall Street and major crypto venues, given the central role of banking rails in market structure and liquidity.

Ethereum price is trading at $2,060, barely moving with just 0.8% gain in the last 24 hours, but the surface calm masks something far bigger, building bullish prediction underneath.

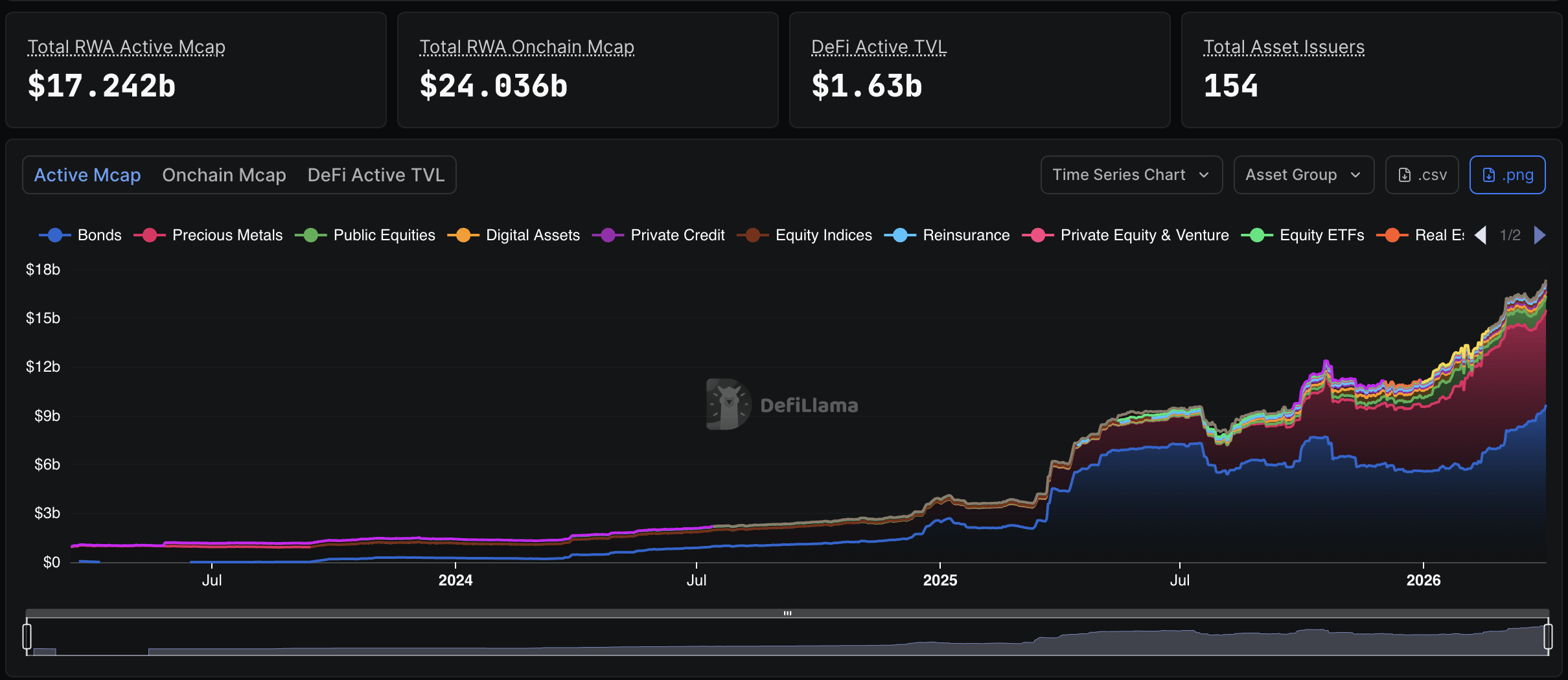

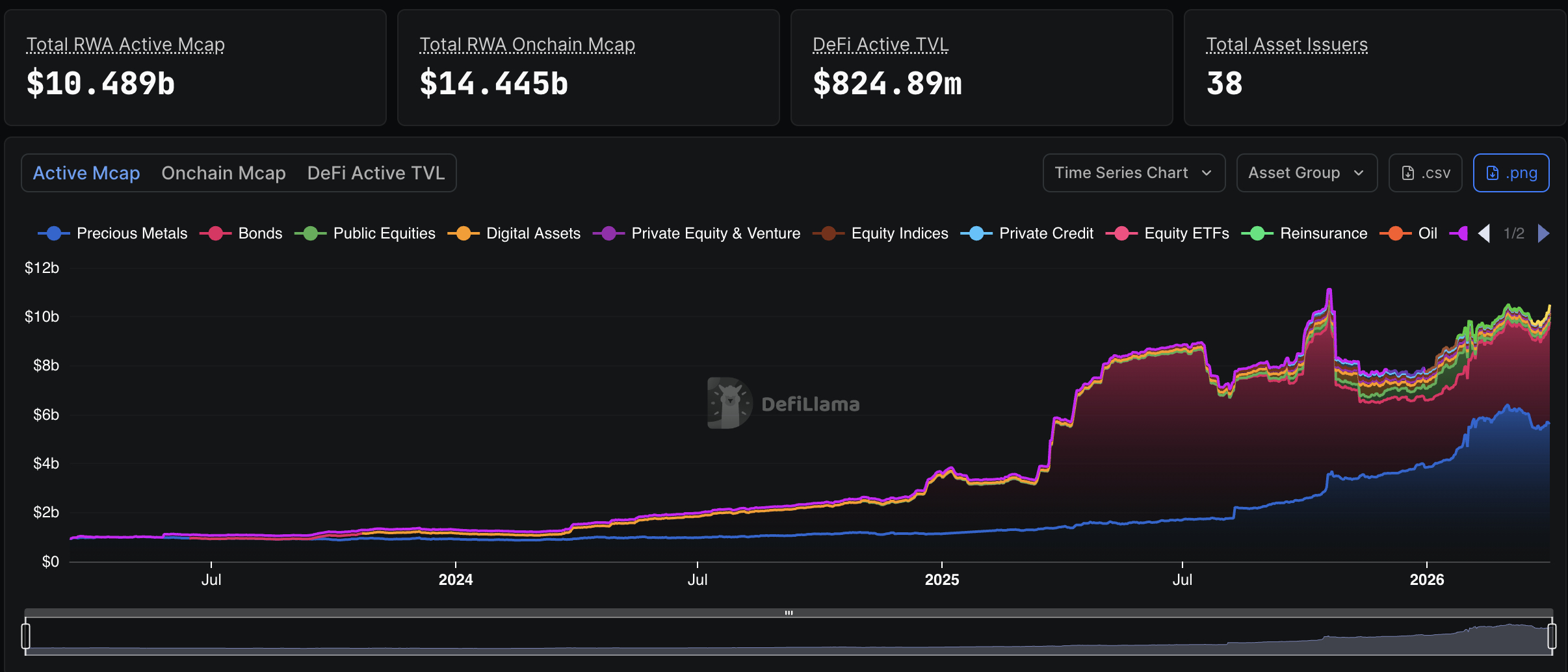

The IMF’s April 2026 “Tokenized Finance” note validated and warned about the tokenized real-world asset boom that Ethereum is dominating. To put it into perspective, on-chain RWA value has already hit $24 billion, excluding stablecoins, with the trajectory points far higher. On that $24 billion value, $14 billion is locked in Ethereum.

However, the IMF’s note flagged genuine systemic risks: flash crashes from rapid automated transactions, market fragmentation across siloed ledgers, and liquidity instability. But it also acknowledged RWA’s structural benefits, atomic settlement, continuous liquidity, and operational savings from smart contract automation.

— Real World Asset Watchlist (@RWAwatchlist_) April 2, 2026

BREAKING: IMF (International Monetary Fund) says tokenization is reshaping regulated finance.

BREAKING: IMF (International Monetary Fund) says tokenization is reshaping regulated finance.

Assets moving onto programmable ledgers = efficiency gains.

But strong policy + trust still needed to protect stability.

RWA shift is getting official.  pic.twitter.com/I9eUzA6Gwo

pic.twitter.com/I9eUzA6Gwo

Tokenized US Treasuries alone have reached $10.8 billion, buoyed by the SEC’s constructive regulatory posture. Peter Thiel has publicly positioned Ethereum as “Wall Street’s base layer” for this market as a bullish signal.

Projections from McKinsey ($2–4T by 2030), BCG ($16T), and Standard Chartered ($30T by 2034) suggest the current $36B figure is a rounding error by comparison. ETH is the rails.

Discover: The best pre-launch token sales

Ethereum Price Prediction: RWA Momentum is Building, But Price Lags

At $2,060, ETH sits at a psychologically significant level, holding above $2,000 but well below the peak it approached in late 2025 when Bitcoin cracked $125,000. That prior high now functions as a long-term resistance ceiling. The current range feels like consolidation.

Volume context is muted relative to the RWA narrative building on-chain. Network activity data suggests ETH is “booming under the hood,” with RWA deployments, smart contract throughput, and institutional settlement flows, while spot price remains range-bound. That divergence between fundamentals and price is a lagging indicator setup.

The $2,000 level is load-bearing right now. If it holds, the RWA growth story has room to translate into price. If it doesn’t, the next meaningful support is well below current levels.

Discover: The best crypto to diversify your portfolio with

LiquidChain Targets Early Mover Upside as Ethereum Tests Key Levels

ETH is a multibillion-dollar asset with institutional adoption already baked into its thesis, and any upside from here requires the entire RWA narrative to keep compounding at scale. That’s a reasonable bet, but it’s not a small-cap return profile.

Traders sizing for asymmetric exposure are already rotating attention toward infrastructure plays that sit beneath the Ethereum layer. The fragmentation problem the IMF specifically flagged, like siloed ledgers, disconnected liquidity, is exactly the problem one early-stage project is being built to solve.

A new layer emerges. Only a few see it first. — LiquidChain (@getliquidchain) March 24, 2026

The future is LiquidChain  ⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

LiquidChain ($LIQUID) is a Layer 3 infrastructure project positioning itself as the cross-chain liquidity layer, fusing Bitcoin, Ethereum, and Solana liquidity into a single execution environment. Developers deploy once and access all three ecosystems. The architecture includes a Unified Liquidity Layer, Single-Step Execution, Verifiable Settlement, and Deploy-Once Architecture.

The presale is live at $0.014 per token, with more than $630K raised to date, and a 1700% APY in staking bonus. The contract itself is also audited by Certik, the leading crypto auditor, to ensure investors safety.

Explore LiquidChain’s presale details here.

This article is for informational purposes only and does not constitute financial advice. Crypto assets are highly volatile. Always conduct your own research before investing.

The post Ethereum Price Prediction: IMF Warns Tokenization, ETH RWA Booming appeared first on Cryptonews.

Crypto World

Naoris Protocol’s quantum-resistance blockchain goes live as Bitcoin and Ethereum face ‘Q-Day’ threats

Naoris Protocol debuted its quantum-resistant blockchain Thursday, which it says is designed to stay secure even against future powerful quantum computers that could break modern day cryptography.

“Mainnet represents the transition from proof-of-concept to production infrastructure. The network has already validated over 100 million transactions using post-quantum cryptography. That is not a roadmap promise; it is measured, operational capacity,” Nathaniel Szerezla, chief growth officer of Naoris Protocol, said.

The debut comes as legacy chains Bitcoin and Ethereum confront the threat of a “quantum apocalypse.” Known as Q-Day, this is the point when future quantum computers could crack the encryption securing most blockchains.

Concerns escalated this week after Google reported that a sufficiently powerful quantum computer could break Bitcoin’s blockchain with fewer than 500,000 qubits — far lower than previous estimates. At the same time, another report flagged potential vulnerabilities in Ethereum that could put $100 billion on the blockchain at risk.

Because blockchain transactions such as those on Bitcoin and Ethereum are permanent, any weakness today could be exploited by future quantum computers with the necessary power.

Naoris is built different

This is where Naoris stands out. It is built from the start using post-quantum cryptography and algorithms approved by the U.S. National Institute of Standards and Technology to protect accounts, transactions, and digital assets, according to the press release shared with CoinDesk.

The system incorporates an “irreversible security transition.” This means that once a user adopts post-quantum keys, it has to use quantum-resistant signatures for transactions. The protocol automatically blocks transaction attempts using traditional, vulnerable cryptographic methods, helping protect assets even if classical cryptography becomes vulnerable.

More importantly, while its quantum-resistant security is right now available only on its own mainnet, the system is build with a broad scope in mind for potential support to wallets, exchanges, Layer 2 networks, and DeFi platforms in the future.

The mainnet launched with an invite-only group of strategic participants who operate the first validator nodes and form the network’s initial trust layer, laying a strong foundation before broader expansion. The protocol was tested at scale in an extensive testnet phase, during which it detected and mitigated over 603 million threats, processed more than 106 million post-quantum transactions, created over 3.3 million wallets, and activated more than one million security nodes globally.

The protocol’s native token NAORIS drives how the network works, helping secure transactions, enforce rules, and build trust among users. At press time, the token’s market cap was $36 million.

MEXC, one of the world’s fastest-growing digital asset exchanges and a pioneer in zero-fee trading, has announced a series of initiatives to integrate and expand the use of USD1, a US dollar stablecoin, across its ecosystem. By incorporating USD1 into its trading infrastructure and product suite, MEXC aims to broaden its use cases across the platform, including trading support, product integration, and wider ecosystem participation, while providing global users with more diverse and resilient stablecoin options.

USD1 is a stablecoin redeemable on a 1:1 basis for U.S. dollars. Each USD1 is 100% backed by a reserve consisting of short-term U.S. government Treasuries, U.S. dollar deposits, and other cash equivalents. These reserve assets are held or maintained by BitGo Trust Company, Inc. and/or its affiliates. USD1 is issued by BitGo, while World Liberty Financial provides branding and certain operational support.

MEXC remains committed to offering a broad range of high-quality assets. Through this integration, MEXC will leverage its established product suite to expand the utility of USD1 across its ecosystem:

- Deep Product Integration: MEXC plans to gradually integrate USD1 across its product offerings, including Launchpool, Savings, and Futures collateral, subject to platform availability. Through these integrations, USD1 may be used as payment and settlement asset within the ecosystem, broadening its utility across the platform.

- Liquidity and Zero-Fee Support: MEXC will introduce additional USD1 trading pairs and launch associated zero-fee promotions. Leveraging the platform’s deep liquidity and industry-leading low-fee structure, MEXC provides global users with a more convenient and cost-effective channel for USD1 interaction.

- Ecosystem Activity Empowerment: To enhance user awareness and experience with the stability of USD1, MEXC will launch a series of ecosystem incentive programs. Through various interactive mechanisms, these initiatives aim to lower the barrier to entry and accelerate the adoption of USD1 in real-world trading scenarios.

Vugar, Chief Operating Officer of MEXC, stated: “USD1 strengthens our mission to make high-quality assets more accessible, efficient, and usable at scale. Stablecoins are only as powerful as their distribution. By integrating USD1 into the MEXC ecosystem, we are expanding compliant stablecoin choice while enhancing trading and capital allocation tools. With over 40 million users and a strong zero-fee conviction, MEXC delivers immediate scale, deep liquidity, and real utility for USD1, accelerating its adoption across global markets.”

As USD1 trading pairs and related features go live, MEXC will continue to explore practical use cases that bring added value to users across the platform. More details on upcoming initiatives will be shared in the coming weeks.

About MEXC

Founded in 2018, MEXC is committed to being “Your Easiest Way to Crypto.” Serving over 40 million users across 170+ countries, MEXC is known for its broad selection of trending tokens, everyday airdrop opportunities, and low trading fees. Our user-friendly platform is designed to support both new traders and experienced investors, offering secure and efficient access to digital assets. MEXC prioritizes simplicity and innovation, making crypto trading more accessible and rewarding.

MEXC Official Website| X | Telegram |How to Sign Up on MEXC

The post MEXC Integrates USD1 into Full-Spectrum Infrastructure for Global Users appeared first on BeInCrypto.

Algorand price shot up 21% on Friday, April 3, becoming the top gainer of the day, bucking the relative stillness of the broader crypto market that has gone cold amid the escalating war situation in the Middle East.

Summary

- Algorand price jumped 21% to a nine-week high, becoming the top gainer as the broader crypto market remained subdued amid geopolitical tensions.

- The rally was driven by a Google Quantum AI research mention, Revolut enabling ALGO staking, and dip-buying after a recent all-time low.

- A confirmed falling wedge breakout and bullish indicators signal potential upside toward $0.139, with further gains possible if resistance is cleared.

According to data from crypto.news, Algorand (ALGO) price rallied to a 9-week high of $0.122 on Friday before settling at $0.121 at press time. Its gains pushed it to become the leading gainer among the top cryptocurrencies by market cap in both the daily and weekly timeframes.

There are three main reasons why Algorand price rallied today.

First, Algorand was recently cited by Google Quantum AI in a research paper focused on threats faced by major blockchains from quantum computing. The paper made several mentions of Algorand for its post-quantum security and advanced Falcon signature technology, placing it ahead of other major players and trailing only behind Bitcoin and Ethereum.

This citation from one of the most prominent tech labs gave the project a big push to new investors while increasing hype for existing ones.

Second, Revolut has officially enabled staking for Algorand on its platform. This enables its customer base of over 70 million investors to stake ALGO directly from the app.

The move has increased investor demand for the token as it triggered a jump in the total amount being staked on the platform, effectively removing those tokens from circulation and hence lowering potential selling pressure.

Third, Algorand’s rebound follows the token hitting an all-time low just five days ago. The token dropping to its floor likely made it very attractive for buyers who bought the dip following its high-profile citation.

On the daily chart, Algorand price has formed a multi-month falling wedge pattern. Following its recent rebound, it has broken out from the upper trendline of the pattern, thereby confirming a bullish reversal. When such patterns are confirmed, the asset often enters a period of sustained growth.

At press time, a similar bullish outlook for ALGO was supported by technical indicators. Notably, the Supertrend has turned green, a notable sign of a trend shift. The Chaikin Money Flow index read 0.19, a strong positive reading hinting that buyers are in control.

For now, $0.139, which sits at the 23.6% Fibonacci retracement level, is the most immediate resistance level to keep an eye on for identifying more upside. A decisive break above that could potentially trigger a rally to $0.225, a target calculated by adding the height of the wedge to the point at which the breakout occurred.

On the contrary, a drop below the $0.085 support level can invalidate this bullish setup.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Key Insights

- Crypto market reversed fast as Trump’s Iran war stance crushed hopes of de-escalation and triggered risk-off selling.

- Bitcoin trades like a macro asset, while altcoins lead losses as oil spikes, yields rise, and the dollar strengthens.

- Market outlook remains fragile, with traders watching war signals and dollar strength for the next crypto move

What happens when markets price in peace but receive a tougher war stance instead? They sell first and reassess later. That is exactly what unfolded after Donald Trump addressed the Iran conflict from the White House on April 1.

Ahead of the speech, expectations had been building around a possible de-escalation. Analysts, including Kobeissi Letter, pointed to signals suggesting a potential wind-down. Instead, Trump reinforced a hardline position, stating that the United States would continue its aggressive posture toward Iran.

The next big question tonight:

Tons of major news outlets reported the same information ahead of President Trump’s address to the nation, sending markets sharply higher.

Almost all “insider sources” signaled Trump would be “winding down” the war tonight.

What just happened?

— The Kobeissi Letter (@KobeissiLetter) April 2, 2026

The reaction was immediate and broad-based—crypto, equities, oil, and the U.S. dollar all reversed sharply.

Crypto Market Reverses After Trump’s Iran Remarks

The crypto market quickly erased its short-lived relief rally following the speech. Investors hoping for clarity on de-escalation or a reopening timeline for the Strait of Hormuz were left disappointed.

Source: Coinmarketcap

As a result, selling pressure returned across digital assets:

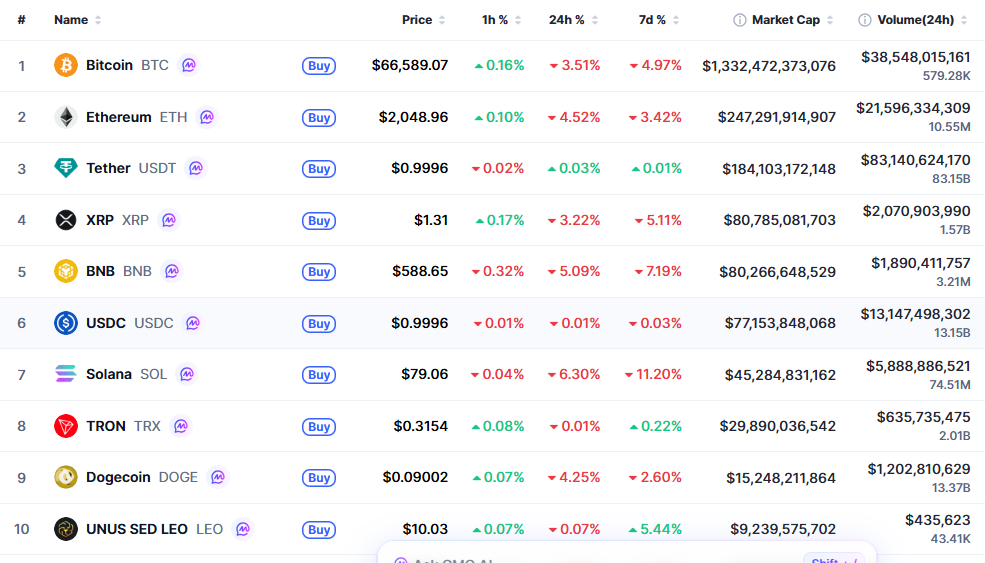

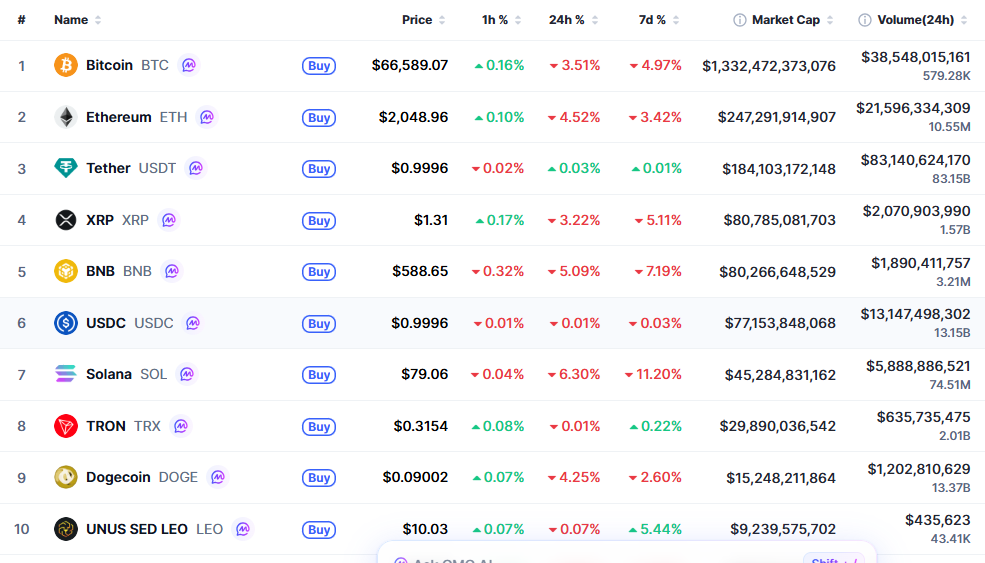

- Bitcoin hovered around $66,600

- Ethereum dropped near $2,050

- XRP traded around $1.31

- BNB held near $590

- Solana led losses among major altcoins

This price action reinforces a key trend: Bitcoin is not behaving as a traditional safe-haven asset during this conflict. Instead, it is trading more like a macro-sensitive risk asset.

The speech effectively dismantled the emerging peace narrative, pushing markets back into a defensive stance. Altcoins, particularly high-beta assets like Solana, absorbed the heaviest losses as traders reduced risk exposure.

Oil Surge and Macro Pressure Weigh on Crypto

Beyond crypto, the broader macro environment shifted rapidly. Following Trump’s remarks, Brent crude surged over 6% to $107.69, reflecting heightened geopolitical risk and concerns over supply disruptions.

Global markets reacted sharply:

- U.S. stock futures fell 1.3%

- Japan’s Nikkei dropped 2.4%

- South Korea’s Kospi declined 4.7%

For crypto markets, this macro shift is critical.

Rising oil prices can fuel inflation expectations, which in turn strengthens the U.S. dollar and keeps bond yields elevated. These conditions typically pressure risk assets, including cryptocurrencies.

At the same time:

- The 10-year Treasury yield climbed to 4.376%

- The U.S. Dollar Index (DXY) held firm above 100

This environment explains why altcoins sold off more aggressively than Bitcoin, as traders moved to reduce volatility exposure rather than chase uncertain upside.

Traders Shift to Risk-Off Mode

The immediate takeaway from the market reaction is clear: traders are prioritizing capital preservation.

Going forward, markets will focus on two key signals:

- Any softening in geopolitical rhetoric

- Reduced risk to global shipping routes, particularly the Strait of Hormuz

Without improvement on either front, the crypto market is likely to remain highly sensitive to headlines and prone to sharp swings.

The pre-speech rally demonstrated that bullish sentiment still exists—but it is fragile and easily disrupted by macro developments.

Macro Now Drives Crypto

The latest selloff highlights a broader shift in how digital assets are behaving.

Geopolitics is influencing crypto through macroeconomic channels rather than crypto-native factors. Oil prices, bond yields, the U.S. dollar, and equity markets are now leading indicators, with crypto reacting afterward.

While blockchain-specific developments still matter, traders increasingly need to interpret global macro conditions before making crypto decisions.

Outlook: Defensive Trend Likely to Continue

Looking ahead, digital assets are expected to remain in a defensive posture as long as geopolitical tensions persist in the Middle East.

Although April seasonality has historically favored bullish momentum, the current environment is dominated by a hope → headline → reversal cycle. The Trump Iran speech is a clear example of how quickly sentiment can shift.

A sustained recovery in crypto will likely depend on:

- A formal ceasefire or de-escalation

- Stabilization in oil prices

- Weakness in the U.S. dollar

Until then, the U.S. Dollar Index (DXY) remains a critical indicator. A strengthening dollar continues to act as a major headwind for Bitcoin and the broader altcoin market.

Researchers at Google DeepMind have warned that the open internet can be used to manipulate autonomous AI agents and hijack their actions.

Summary

- DeepMind researchers have identified six attack methods that can be used to manipulate autonomous AI agents as they browse and act online.

- The study warned that hidden instructions, persuasive language, and poisoned data sources can influence agent decisions or override safeguards.

The study titled “AI Agent Traps” comes as companies deploy AI agents for real-world tasks and attackers begin using AI for cyber operations.

Instead of focusing on how models are built, the research looks at the environments agents operate in. It identifies six types of traps that take advantage of how AI systems read and act on information from the web.

The six attack categories outlined in the paper include content injection traps, semantic manipulation traps, cognitive state traps, behavioural control traps, systemic traps, and human in the loop traps.

Content injection stands out as one of the most direct risks. Hidden instructions can be placed inside HTML comments, metadata, or cloaked page elements, allowing agents to read commands that remain invisible to human users. Tests showed these techniques can take control of agent behaviour with high success rates.

Semantic manipulation works differently, relying on language and framing rather than hidden code. Pages loaded with authoritative phrasing or disguised as research scenarios can influence how agents interpret tasks, sometimes slipping harmful instructions past built-in safeguards.

Another layer targets memory systems. By planting fabricated information into sources that agents rely on for retrieval, attackers can influence outputs over time, with the agent treating false data as verified knowledge.

Behavioural control attacks take a more direct route by targeting what an agent actually does. In these cases, jailbreak instructions can be embedded into normal web content and read by the system during routine browsing. Separate tests showed that agents with broad access permissions could be pushed into locating and transmitting sensitive data, including passwords and local files, to external destinations.

System-level risks extend beyond individual agents, with the paper warning that coordinated manipulation across many automated systems could trigger cascading effects, similar to past market flash crashes driven by algorithmic trading loops.

Human reviewers are also part of the attack surface, as carefully crafted outputs can appear credible enough to gain approval, allowing harmful actions to pass through oversight without raising suspicion.

How to defend against these risks?

To counter these risks, researchers suggest a mix of adversarial training, input filtering, behavioural monitoring, and reputation systems for web content. They also point to the need for clearer legal frameworks around liability when AI agents execute harmful actions.

The paper stops short of offering a complete fix and argues that the industry still lacks a shared understanding of the problem, leaving current defenses scattered and often focused on the wrong areas.

Crypto World

Algorand Crypto Jumps 20% Thanks to Google AI Paper: Cited 32 Times, Revolut Integration Adds Momentum

Algorand (ALGO) is experiencing a +23% surge in 24 hours, the sharpest single-day move up since the name faded from the crypto space after the 2021 bullrun. The catalyst is not a protocol upgrade or exchange listing. A Google Quantum AI whitepaper dropped at the end of last month comes with the Algorand name appearing 32 times. Why?

The Google Quantum AI research examined quantum computing threats across major blockchains, ranking chains by post-quantum cryptography readiness. Algorand landed third by citations, behind only Bitcoin and Ethereum, acknowledged for live deployments covering signatures, state proofs crypto, key rotation, and smart contracts.

Solana received 16 mentions, XRP just 14. Hedera and Avalanche: zero. YouTuber Zach Humphries summarized the community reaction bluntly: “Google Quantum AI basically published a landmark paper yesterday on quantum threats to every major blockchain.” Trading volume spiked +429% to a reported $440 million in 24 hours.

Discover: The best pre-launch token sales

Algorand Crypto Momentum: More Upward Movement?

Apart from Google AI Paper, the simultaneous integration of PostFinance and Revolut opened ALGO exposure to 2.5 million Swiss banking customers, adding institutional weight to what might otherwise have been a short-lived spike.

The confluence of technical recognition, banking access, and a rebound from an all-time low creates a setup worth mapping precisely. Here’s where the levels stand:

ALGO bottomed at $0.08 on just 4 days ago, an all-time low, before reversing +27% to an 8-week high of $0.1052 within 48 hours. The 24-hour range printed $0.085–$0.105, with the close above $0.10 representing a decisive reclaim of a key psychological level.

Support now sits at $0.082 as the former wedge base and horizontal shelf. Resistance clusters near $0.115–$0.12, the zone where overhead sellers from the previous range are likely concentrated. Market cap sits around $930 million, still sub-$1B, meaning any sustained institutional rotation could move price aggressively. But remember, Algo is 96% below its all-time high in 2019, a good 7 years ago, the day it launched.

Discover: The best crypto to diversify your portfolio with

LiquidChain Targets Early Mover Upside Just Like ALGO 7 Years Ago

ALGO’s move is real, but at a $930M market cap off an all-time low, the asymmetric upside is already partially priced in. Early buyers who caught $0.08 are sitting on +27%. Those entering at $0.105 are chasing a narrative that’s now front-page. That compression of entry quality is exactly where early-stage presales become relevant.

LiquidChain ($LIQUID) is a Layer 3 infrastructure project positioning itself as the cross-chain liquidity layer, fusing Bitcoin, Ethereum, and Solana liquidity into a single execution environment. The architecture centers on a Unified Liquidity Layer, Single-Step Execution, Verifiable Settlement, and a Deploy-Once model that lets developers access all three ecosystems without redeployment.

A new layer emerges. Only a few see it first. — LiquidChain (@getliquidchain) March 24, 2026

The future is LiquidChain ⟁https://t.co/vqvBcdSj94 pic.twitter.com/R7ZeZ0NPGl

Current presale price is $0.01445, with more than $630K raised to date. Not just cheap and early, the contract is audited by Certik to ensure investors’ safety, plus a bonus of 1700% staking APY for early believers.

Still, for traders who missed the ALGO entry and want exposure to infrastructure-level crypto bets at ground floor, research LiquidChain here.

This article is not financial advice. Crypto assets are highly volatile. Always conduct your own research before investing.

The post Algorand Crypto Jumps 20% Thanks to Google AI Paper: Cited 32 Times, Revolut Integration Adds Momentum appeared first on Cryptonews.

Crypto World

Microsoft (MSFT) Commits $10B to Japan AI Infrastructure with SoftBank and Sakura Internet Partnership

Key Highlights

-

- Sakura Internet’s stock price climbed 20.27% following Microsoft’s revelation of a $10 billion AI commitment in Japan

- The tech giant will deploy 1.6 trillion yen from 2026 through 2029 focusing on AI systems and cybersecurity initiatives

- Partnership includes Sakura Internet and SoftBank delivering Japan-based AI computational power, featuring GPU resources

- Training initiative targets 1 million Japanese engineers and developers by the end of the decade

- SoftBank Group shares increased 0.22% while SoftBank Corp. climbed 1.02% following the announcement

Shares of Sakura Internet experienced a significant 20.27% surge on Friday following Microsoft’s revelation of a substantial AI investment strategy in Japan, with the cloud services provider designated as a primary collaborator along with SoftBank.

Microsoft announced a four-year, $10 billion investment package in Japan, part of the US company’s Asia-wide push to expand in a region hungry for artificial intelligence services- Bloomberg

•$10B for data centers and AI infrastructure through 2029

•Builds on $2.9B announced… pic.twitter.com/laIAvfd383— Yeboah Walee (@YeboahWalee) April 3, 2026

The Redmond-based technology giant confirmed plans to deploy 1.6 trillion yen — approximately $10 billion — across Japan from 2026 to 2029. This capital allocation encompasses AI infrastructure development, cybersecurity collaboration efforts, and an ambitious commitment to educate 1 million engineers and developers over the next six years.

Brad Smith, Microsoft Vice Chair and President, disclosed these plans during his Tokyo visit, which included meetings with Prime Minister Sanae Takaichi.

Sakura Internet, operating a network of data centers throughout Japan, will collaborate with SoftBank to deliver AI computational capabilities through this alliance. The partnership specifically includes graphics processing units situated physically inside Japanese borders.

This infrastructure arrangement enables corporations and governmental bodies to handle confidential information domestically while maintaining access to Microsoft Azure cloud services.

Additional discussions between SoftBank and Microsoft Japan involve creating a combined solution allowing Azure users to access SoftBank’s AI computing infrastructure seamlessly.

Friday’s trading saw SoftBank Group finish 0.22% higher, with SoftBank Corp. posting gains of 1.02%.

Japan’s Strategic Importance

Microsoft highlighted Japan’s robust AI adoption rates as a key motivation behind this investment decision. Data from Microsoft’s AI Diffusion Report indicates that approximately 20% of Japan’s working-age population currently utilizes generative AI technologies, surpassing the global average of roughly 16%.

Smith emphasized the expanding demand for cloud computing and AI capabilities in Japan, noting that this investment supports Prime Minister Takaichi’s strategic vision of leveraging cutting-edge technology for economic expansion and national security objectives.

Extended Collaboration Framework

In addition to Sakura Internet and SoftBank, Microsoft revealed partnerships with five additional prominent Japanese technology firms to achieve its goal of training 1 million AI professionals by 2030. This roster includes industry leaders such as NTT Data Corp., NEC, Fujitsu, and Hitachi.

The collaborative framework will also facilitate advancement of indigenous large language models within Japan’s technology ecosystem.

Microsoft’s cybersecurity collaboration with Japanese authorities encompasses intelligence exchange regarding cyber threats and coordinated crime prevention measures.

Sakura Internet concluded Friday’s session at 2,967.00 JPY, representing a 500.00 JPY increase for the trading day.

In a recent note, the International Monetary Fund (IMF) has warned that tokenized finance poses four distinct risks to the global financial system.

Authored by Tobias Adrian, the IMF’s Financial Counselor and Director of the Monetary and Capital Markets Department, the note frames tokenization as a structural reconfiguration of how trust, settlement, and risk management are organized.

4 Risks the IMF Sees in Tokenized Finance

The first risk centers on interoperability and fragmentation. Multiple platforms operating without common standards could split liquidity across digital silos, reduce netting efficiency, and impair par convertibility between assets.

Second, the IMF warns that tokenized systems amplify financial stability threats. Automated margin calls, continuous settlement, and algorithmic feedback loops compress the time available for intervention during stress events.

Traditional end-of-day buffers disappear, and shocks propagate faster, especially in highly interconnected systems.

Follow us on X to get the latest news as it happens

“Public authorities have a key role to play in setting interoperability standards and promoting common protocols. International coordination is essential to ensure that cross-border transactions achieve atomic settlement and legally recognized finality. Absent such coordination, tokenization may exacerbate existing inefficiencies in cross-border finance, rather than resolve them,” the note read.

Third, cross-border resolution becomes far harder. Tokenized transactions span multiple jurisdictions on shared ledgers, yet resolution powers remain nationally anchored.

This mismatch could produce jurisdictional conflict or paralysis precisely when decisive action is most needed.

Fourth, Emerging and Developing Economies (EMDEs) face acute exposure. Dollar-denominated stablecoins could accelerate currency substitution, volatile capital flows, and erosion of monetary sovereignty in countries with weaker financial systems.

The IMF’s five-pillar policy roadmap calls for anchoring settlement in safe money, applying consistent regulation across equivalent activities, establishing legal certainty for tokenized assets, promoting interoperability standards, and adapting central bank liquidity tools for 24/7 automated environments.

The note concludes that the window for shaping tokenized finance remains open but will not remain so indefinitely. This comes amid strong growth in the tokenization sector.

The total on-chain distributed RWA value has climbed 4% over the past month to $26.7 billion. The represented asset value has jumped 31.61% in the same period. The number of asset holders also increased to 710,792, up 5.56%.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post IMF Identifies 4 Risks Tokenized Finance Poses to Global Financial System appeared first on BeInCrypto.

Crypto World

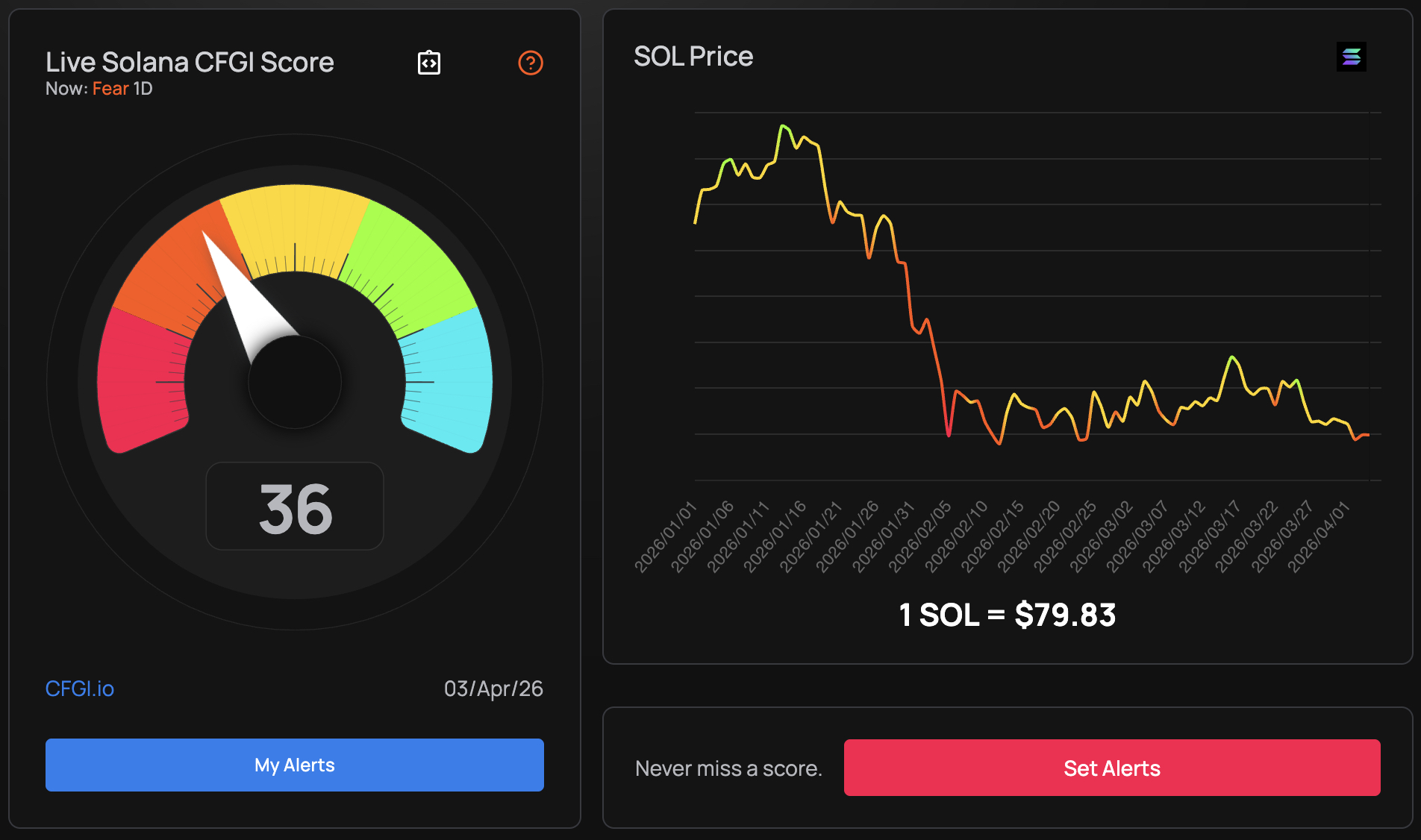

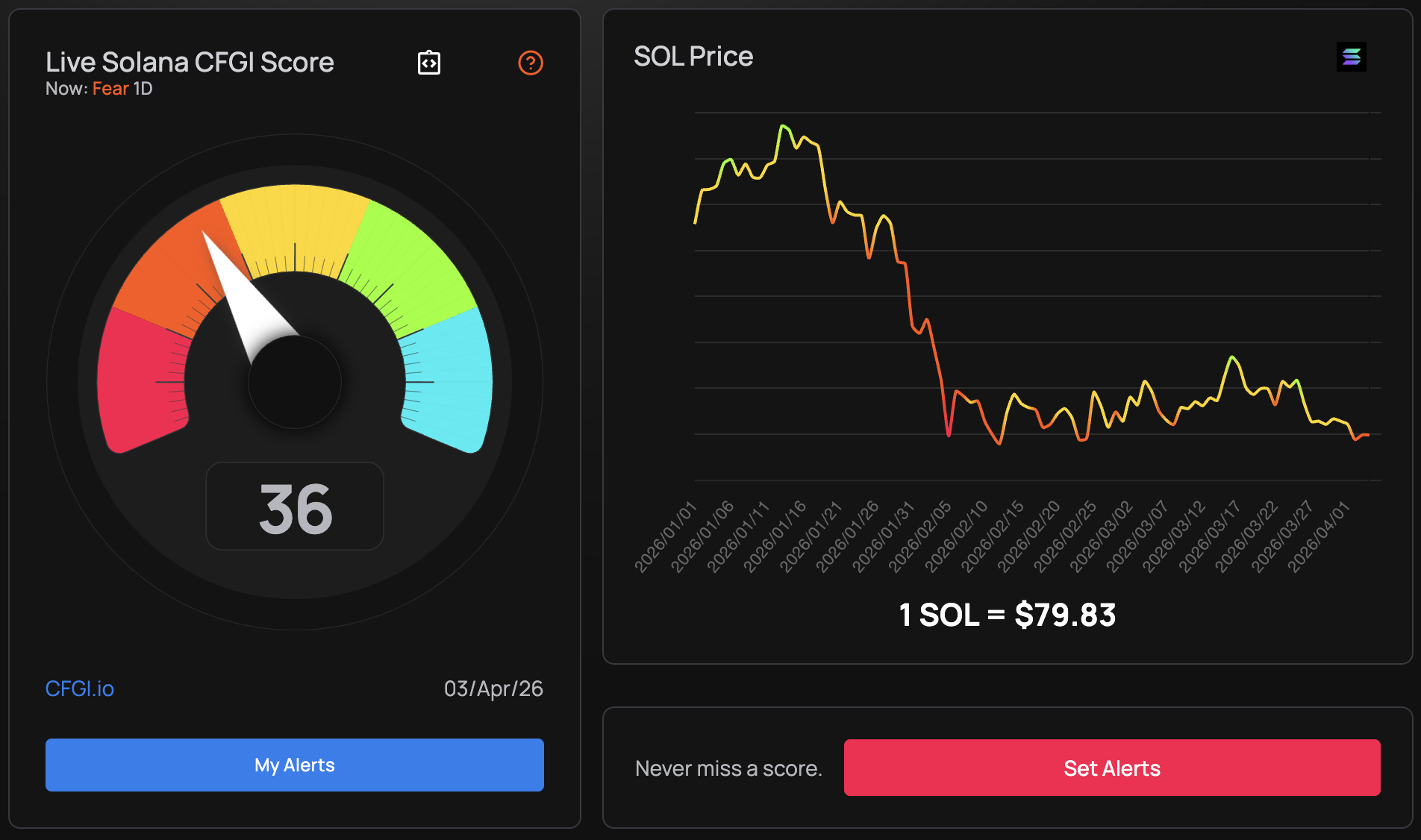

Solana Price Prediction: After The Exploit, Is The Network Still Safe? Will Price Recover?

Solana price appears to be stabilizing below $80, but the Drift Protocol exploit raised questions, followed by bearish prediction. Is the network’s infrastructure fundamentally compromised, or is this selloff noise masking a recovery setup?

The Drift Protocol attack drained at least $270 million in under 60 seconds, but notably, no code was broken. The attacker exploited “durable nonces,” a legitimate Solana feature that allows transactions to remain valid indefinitely by replacing the standard 60–90 second expiring blockhash with a fixed on-chain code.

Security council members were tricked into pre-signing administrative transfers weeks before execution, with no way to revoke approval once given. The exploit required more than a week of setup and less than a minute to detonate.

That distinction of feature abuse versus protocol failure is critical for price recovery timing. Macro headwinds compound the damage, BTC hovering at $66,000, S&P 500 under pressure, and oil above $100 stoking stagflation fears that are already suppressing risk appetite across the crypto markets.

Discover: The best crypto to diversify your portfolio with

Solana Price Prediction: Hold $80 Support, or a Drop to $50

SOL’s technical picture is unambiguously bearish. The RSI sits at 32 on the daily, approaching oversold, but it looks like bears haven’t exhausted themselves just yet. The 50-day SMA at $117 is overhead resistance; the 200-day SMA at $30 is dropping to the 100-day SMA. Only 13% of technical signals read bullish, with the Fear & Greed Index locked at 29 for 46 consecutive days.

The critical level is $85, and failure to reclaim it confirms the breakdown. Analyst warns a sustained break below $85 opens a flush toward the $50–$30 Fair Value Gap accumulation zone. Network revenue remains 93% below January peaks, undermining any near-term fundamental rebound argument.

The exploit doesn’t erase Solana’s infrastructure roadmap. It does reset near-term trust, and trust is priced faster than fundamentals.

Discover: The best pre-launch token sales

Maxi Doge Targets Early-Mover Upside as Solana Tests Key Levels

SOL at $80 is a setup, but it’s also a waiting game with real downside risk attached. Traders rotating out of established-layer-one volatility are increasingly eyeing early-stage presales where entry price, not recovery timing, does the heavy lifting.

Maxi Doge ($MAXI) is one attracting attention. Built on Ethereum (ERC-20), the project packages a 240-lb canine mascot with genuine community mechanics: holder-only trading competitions with leaderboard rewards, a Maxi Fund treasury dedicated to liquidity and partnerships, and a meme-first marketing engine built around gym-bro culture and the tagline “Never skip leg-day, never skip a pump.”

It’s unambiguously meme-first, which, in this market, is exactly where retail attention is rotating. We know risk-off macro tends to funnel speculative capital toward low-cap narratives, not $80 SOL recovery bets.

Hard numbers: current presale price is $0.0002811, with $4.7 million raised to date and 66% staking APY as a bonus.

Research Maxi Doge before the next price increase.

This article is not financial advice. Crypto markets are highly volatile. Always conduct your own research before investing.

The post Solana Price Prediction: After The Exploit, Is The Network Still Safe? Will Price Recover? appeared first on Cryptonews.

Dave Portnoy Blasts ‘Snake’ Amanda From ‘Summer House’

MLB roundup: Braves beat Diamondbacks 17-2 after eight-run fifth inning

Shadow Lord’ season 2 confirmed

-

NewsBeat7 days ago

NewsBeat7 days agoThe Story hosts event on Durham’s historic registers

-

NewsBeat15 hours ago

NewsBeat15 hours agoSteven Gerrard disagrees with Gary Neville over ‘shock’ Chelsea and Arsenal claim | Football

-

Sports6 days ago

Sports6 days agoSweet Sixteen Game Thread: Tide vs Michigan

-

Entertainment4 days ago

Fans slam 'heartbreaking' Barbie Dream Fest convention debacle with 'cardboard cutout' experience

-

Entertainment5 days ago

Entertainment5 days agoLana Del Rey Celebrates Her Husband’s 51st Birthday In New Post

-

Crypto World2 days ago

Crypto World2 days agoGold Price Prediction: Worst Month in 17 Years fo Save Haven Rock

-

Crypto World3 days ago

Dems press CFTC, ethics board on prediction-market insider trades

-

Tech4 days ago

Tech4 days agoThe Pixel 10a doesn’t have a camera bump, and it’s great

-

Sports3 days ago

Sports3 days agoTallest college basketball player ever, standing at 7-foot-9, entering transfer portal

-

Tech3 days ago

Tech3 days agoEE TV is using AI to help you find something to watch

-

Business10 hours ago

Business10 hours agoNo Jackpot Winner and $194 Million Prize Rolls Over

-

Fashion5 days ago

Fashion5 days agoAmazon Sundays: Soft Spring Layers

-

Business1 day ago

Business1 day agoLogin and Checkout Issues Spark Merchant Frustration

-

Crypto World3 days ago

Crypto World3 days agoU.S. rule change may open trillions in 401(k) funds to crypto

-

Tech3 days ago

Tech3 days agoHow to back up your iPhone & iPad to your Mac before something goes wrong

-

Tech4 days ago

Tech4 days agoAvatar Legends: The Fighting Game comes out in July and it looks pretty slick

-

Tech4 days ago

Tech4 days agoApple will hide your email address from apps and websites, but not cops

-

Politics4 days ago

Politics4 days agoShould Trump Be Scared Strait?

-

Tech3 days ago

Tech3 days agoFlipsnack and the shift toward motion-first business content with living visuals

-

Tech5 days ago

Tech5 days agoElon Musk’s last co-founder reportedly leaves xAI

You must be logged in to post a comment Login