Crypto World

Kraken’s FIFA deal: Crypto’s first world cup

For the first time in the tournament’s near-century of history, a crypto exchange sits inside FIFA’s official partner ecosystem. Six billion viewers, sixteen host cities, one industry trying to prove it has outgrown the arena-naming era. Here is what the deal actually is, and what it has to survive.

Summary

- Kraken became FIFA’s first official crypto exchange supporter, marking the first time a crypto exchange has joined the tournament’s official partner ecosystem.

- The partnership focuses on fan engagement through activations, education, and onboarding as Kraken looks to turn World Cup viewers into long term users.

- The sponsorship reflects a more regulated and compliance focused approach to crypto sports marketing following the industry’s high profile sponsorship failures in 2021 and 2022.

On June 9, 2026, two days before the biggest World Cup ever staged kicked off, FIFA announced something that would have sounded like satire during the last tournament: an official crypto exchange partner. Kraken, through its parent company Payward, became the Official Crypto Exchange Supporter of the FIFA World Cup 2026, the first designation of its kind in the competition’s nearly one hundred years.

The timing was almost comically last-minute. FIFA was still adding sponsors in the final weeks before kickoff, slotting Kraken into the partner stable alongside a Colombian courier company and Salesforce. But the category was brand new, the exclusivity real, and the stage without equal: 48 teams, 104 matches, 16 host cities across the United States, Canada, and Mexico, and a projected cumulative audience of more than six billion people across seven weeks. When Qatar hosted in 2022, crypto’s World Cup presence amounted to Crypto.com signage and a fan token hangover. Four years later, the industry has a seat inside the official partner ecosystem of the most-watched event on Earth.

Whether that seat is worth having is the more interesting question, because crypto’s history with marquee sports sponsorship is a graveyard with famous headstones. This deal is structured differently, arrives in a different market, and will be judged by a different metric. It might still fail. But it will fail or succeed on new terms.

What the deal actually is

Strip away the press-release language and the arrangement has four defining features.

First, it is a category-exclusive partnership with the governing body itself, not with a team, a venue, or a broadcaster. No other exchange can hold the crypto exchange designation for this tournament. That distinction matters commercially: Coinbase, Binance, and the rest of the industry spent years accumulating club deals and stadium naming rights, and Kraken jumped the queue to the sport’s top table in a single announcement.

Second, it is tournament-wide rather than asset-specific. Kraken’s branding attaches to the event, meaning every fixture from the group stage to the final doubles as an impression. The activation window runs the full June 11 to July 19 tournament, and it opened a day early with the FIFA World Cup 2026 Countdown Concert series, a multi-city music event on the eve of the opening match that put the exchange in front of fans before a single ball was kicked.

Third, the deal is structured around fan engagement instead of pure signage. The announced program centers on activations and product experiences across the host cities and Europe: ticket giveaways, educational programming, and onboarding experiences meant to convert viewers into account holders. FIFA’s chief business officer Romy Gai framed the partnership as a fan experience play, and Payward and Kraken co-CEO Arjun Sethi supplied the thesis statement, arguing that football and open financial systems share the same borderless logic and that six billion people watching the same game is the natural audience for money that works the same way everywhere.

Fourth, nobody is saying what it costs. Financial terms remain undisclosed, which is standard for FIFA supporter-tier arrangements but leaves the return-on-investment math to outside guesswork.

The deal did not come from nowhere. Kraken has run a sports playbook for years: partnerships with Tottenham Hotspur, Atletico Madrid, and RB Leipzig in football, a Formula 1 arrangement with Williams Racing running since 2023, and ambassador relationships with transfer-news oracle Fabrizio Romano and World Cup winner Lukas Podolski. The FIFA deal is that strategy graduating from clubs to the institution that governs the sport.

Where a Supporter sits in FIFA’s food chain

The word Supporter in Kraken’s title is doing specific work, and decoding it clarifies both what the exchange bought and what it did not.

FIFA sells commercial access in tiers. At the top sit FIFA Partners, the multi-cycle, global relationships of the Coca-Cola and Adidas variety, with rights spanning every FIFA property. Below them, World Cup Sponsors buy tournament-level global rights for a single edition. Supporters occupy the third tier, typically with regional rather than fully global rights packages; Kraken’s activation footprint concentrating on North America and Europe fits the template, covering the host region and the exchange’s core growth markets while leaving Asia and Latin America outside the headline scope. Salesforce and the Colombian logistics firm Inter Rapidisimo joined at similar levels in the same late window.

The tier matters for cost-benefit math. Supporter packages run at a fraction of Partner economics, historically in the low tens of millions for a tournament cycle against the hundreds of millions that top-tier global deals command. Nobody outside the deal knows Kraken’s number, but the structure suggests the exchange bought the maximum symbolic value, first and only crypto exchange in FIFA history, at the minimum viable rights tier, which is either shrewd procurement or clever hedging depending on how the activation performs. The category exclusivity is the asset with option value: if the tournament converts, Kraken holds the incumbent’s chair when the 2030 rights negotiation starts, and category incumbents historically get first refusal.

There is a precedent inside the tournament itself for how crypto categories evolve. Crypto.com entered the FIFA ecosystem as a Qatar 2022 sponsor when the industry was still radioactive from that year’s collapses, and its presence was mostly signage. Four years later, the category has a named exchange tier, a blockchain running FIFA’s own collectibles, and a prediction market partner. Commercial categories at mega-events tend to ratchet: once a governing body books the revenue, the line item survives, and the only question is which company’s logo fills it.

The 2021 wave, and why it drowned

To measure how different this deal is, run the tape back to the last time crypto money flooded sports.

Between early 2021 and mid-2022, the industry committed billions to sports marketing in the space of eighteen months. Crypto.com paid $700 million for twenty years of naming rights to the former Staples Center and layered UFC, Formula 1, and World Cup deals on top. FTX put $135 million on the Miami Heat arena, bought the naming rights to MLB umpire patches, sponsored Mercedes in F1, and made Tom Brady and Steph Curry brand faces. Coinbase became the NBA’s exclusive crypto platform partner. Binance signed African football legends and Italian club deals. Even mid-tier exchanges bought jersey patches and stadium signage, and Kraken itself entered the era with its Tottenham, Atletico, and RB Leipzig arrangements.

The wave’s logic was customer acquisition at mania prices: exchanges were earning record trading fees, retail was pouring in, and sports offered the largest untapped audiences on Earth. The unwinding was faster than the building. FTX’s deals became bankruptcy-court exhibits, with the Heat arena renamed and the Mercedes logos removed mid-season. Crypto.com’s commitments, signed at the top, became the textbook case of pro-cyclical marketing. League partners quietly let crypto deals lapse; the NBA relationship wound down; jersey patches vanished. By 2023, sports business publications ran post-mortems on the crypto sponsorship era as a closed chapter, and the surviving deals, Kraken’s F1 and club portfolio among them, kept notably lower profiles.

The lesson the survivors internalized was not that sports marketing fails. It was that sports marketing amplifies whatever the sponsor already is. FTX’s sponsorships did not cause its fraud, they broadcast it; Crypto.com’s deals did not cause the bear market, they timestamped it. Amplification cuts the other way too, which is the bet Kraken is now making: a compliance-forward, fifteen-year-old exchange amplified across six billion impressions projects durability, provided the underlying story holds.

The 2021 wave drowned because the sponsors’ fundamentals could not survive their own visibility. That is the specific failure mode this deal was structured to avoid, and the one that remains entirely in Kraken’s hands.

The ghosts this deal has to outrun

Any analysis of crypto sports marketing has to walk through the cemetery first, because the industry’s previous splashes at this scale ended as cautionary tales.

FTX put its name on the Miami Heat arena and collapsed into fraud proceedings; the county spent months legally scrubbing the branding off the building. Crypto.com committed $700 million to rename the Staples Center and stack UFC sponsorships at the exact peak of the 2021 mania, a timing decision that became shorthand for bull-market excess within a year. Fan tokens sold to supporters during the Qatar cycle bled value the moment the tournament ended. By early 2023, crypto sports marketing was the punchline in every retrospective about the bubble.

The comparison Kraken has to defeat is not really about logos. It is about what the sponsorships revealed: companies buying legitimacy with customer deposits at cycle tops. Three structural differences give this deal a fighting chance at a different ending.

The buyer is different. Kraken is one of the longest-operating exchanges in the industry, founded in 2011, serving users in more than 190 countries, and it spent the FTX era being the boring firm that published proof-of-reserves. Its parent Payward has been expanding into regulated territory, including opening tokenized US IPO access to retail investors this spring.

The market is different. The deal was struck during a drawdown, with Bitcoin near $61,000, sentiment indexes in fear territory, and the market trading like leveraged tech exposure, not during a euphoria top. Sponsorships signed in bear conditions tend to be priced on strategy instead of vanity.

The counterparty is different. FIFA accepting a crypto exchange into its official ecosystem, after watching the FTX era unfold, is itself the reputational signal. Governing bodies are conservatism machines; their sign-off implies diligence that a stadium landlord never performs.

None of that guarantees the deal works. It only means the failure modes of 2021 do not map cleanly onto 2026.

The tournament crypto built around the deal

What makes this genuinely crypto’s first World Cup is not the Kraken logo alone. It is that the sponsorship sits inside a tournament where blockchain infrastructure runs through nearly every commercial layer.

FIFA moved its own collectibles platform, FIFA Collect, onto a custom Avalanche-based network it calls the FIFA Blockchain, built to carry digital collectibles and ticketing features. ADI Predictstreet operates as FIFA’s first official prediction market partner, running on Chainlink oracle infrastructure. And beyond the official perimeter, the parallel economy has been enormous: prediction markets processed billions in World Cup wagers, with combined June volume across the major venues hitting $44.8 billion, a story we cover in depth in our companion feature on Polymarket’s tournament.

The fan token layer adds the retail texture. Chiliz-powered Socios tokens tied to national teams have traded through every knockout swing: Portugal’s $POR token, now available omnichain including on Solana, moves with every Cristiano-era nostalgia run, while Argentina’s $ARG volume climbs as the favorites advance. The pattern is well documented and brutal: engagement spikes during group stages, peaks in knockouts, and collapses when a side goes home. Elimination is a token event. A team’s exit can crater its token overnight, which makes fan tokens less an investment class than a volatility instrument wearing a scarf. The Qatar cycle wrote the reference chart: national team tokens ran up through the group stage, peaked around the knockouts, and gave back most of the move within weeks of the final, a decay curve every trader in this market now prices from memory. Traders sizing positions around match outcomes are effectively running event-driven strategies with concentrated single-name risk, closer to cross-margined derivatives exposure than to holding a fan club card, and the thin liquidity means exits get expensive at exactly the moments everyone wants one.

The on-pitch product has cooperated with the commercial one. England’s Round of 32 comeback against DR Congo, sealed by two late Harry Kane goals, was the country’s first World Cup win from behind since the 1966 final and played out under Kraken-branded boards to a global broadcast audience. DR Congo’s first knockout appearance since 1974, Cape Verde emerging from a group containing Spain and Uruguay, and a bracket pointing toward a possible France and Argentina rematch have kept audiences, and therefore impressions, at maximum through three weeks.

What Kraken actually has to sell the fans it reaches

Awareness only converts if there is a product on the other end of the funnel, and the shape of Kraken’s 2026 product surface explains why the exchange believed a mass-audience play was worth buying now instead of in 2021.

The core exchange remains the anchor: spot trading across the majors in 190-plus countries, with the fifteen-year operating history and proof-of-reserves posture doing the trust work that a first-time depositor needs. Around it, the offering has widened into exactly the products a football fan is likelier to want than an order book. Payward opened tokenized access to US IPOs for retail investors this spring, part of a broader tokenized equities push that turns “invest in things you know” into an on-chain pitch. Staking products give the passive audience a reason to hold instead of churn. Payments and card products make a funded account useful between trades. And the Formula 1 and club partnerships already taught the firm which fan-facing mechanics convert, knowledge now being redeployed at tournament scale.

The sequencing matters more than any single product. A ticket-giveaway sign-up costs the fan nothing and creates a verified account; an app install during a host-city activation puts the exchange one notification away; a first deposit, even a small one, starts a relationship whose lifetime value the exchange measures in years. This is the standard consumer fintech ladder, and the World Cup is functioning as its top rung.

The 2021 wave mostly bought the billboard and skipped the ladder. The difference between those two designs is the difference between impressions and customers, and it is the entire operational thesis of this deal.

Running the numbers on success and failure

Since the fee is undisclosed, precise return math is impossible, but the scenario logic is straightforward enough to sketch, and it clarifies what a win would even look like.

Assume a Supporter-tier package in the low tens of millions, consistent with FIFA’s historical tier structure. Consumer crypto exchanges have paid anywhere from $50 to several hundred dollars to acquire a funded account through paid channels during competitive periods. At a blended $100 acquisition cost equivalent, a mid-tens-of-millions deal needs a few hundred thousand funded accounts across the seven-week window and its afterglow to beat Kraken’s alternative marketing spend, a conversion rate measured in the low ten-thousandths of the six-billion-viewer audience. Framed that way, the bar is strikingly low, which is precisely why exchanges chased sports at mania prices last cycle.

The catch is in the words funded and retained. Sign-ups from giveaways are cheap and mostly worthless; deposits are the product, and deposit behavior among sports-acquired users is the great unknown. The Qatar-cycle evidence says event-driven crypto interest decays within weeks. The counter-evidence from this tournament, majority-newcomer participation in prediction markets, regulated on-ramps in most target jurisdictions, says the friction that killed past funnels has thinned. Kraken’s dashboard will settle it privately; the public will read the answer in whether the exchange renews for 2030 and whether competitors bid the category up.

Renewal is the tell, and it arrives on a public calendar. Nobody re-buys a failed sponsorship at a mega-event, and nobody with a functioning commercial team lets a working one go to a rival.

The only metric that matters

Six billion cumulative viewers is a marketing number. The business question is narrower and colder: how many of them open a Kraken account, and at what acquisition cost relative to the undisclosed fee.

This is where the fan engagement structure earns its keep or does not. Signage builds recall; activations build funnels. Ticket giveaways require sign-ups. Product experiences at host-city events end with an app install. Educational programming is onboarding content wearing a lanyard. Every mechanism in the announced program points at conversion, which means the deal’s success is measurable in a way the arena-naming era never was, even if only Kraken and Payward see the dashboard.

The skeptical read has real evidence behind it. Sports viewers are not natural traders, and the crossover audience may be smaller than the impression counts imply. The Panama fixture drew $1.76 million in prediction market wagers while the on-chain response in adjacent assets barely registered, and even England’s marquee comeback produced no meaningful fan token volume for either side, a reminder that attention and allocation are different behaviors. Seasonal decay is the default outcome for tournament-driven crypto activity, with the Qatar cycle as the controlling precedent.

The optimistic read has newer evidence. Prediction market user studies during this tournament found a majority of active participants had no prior on-chain history at all, direct proof that the World Cup is reaching people crypto never touched. Regulatory infrastructure that did not exist in 2022, from MiCA in Europe to spot ETFs and commodity classifications in the US, means a curious viewer in most of Kraken’s target markets can now act on the curiosity legally and simply. The funnel from broadcast to wallet has never had fewer broken steps.

Three host countries, three rulebooks

There is also a jurisdictional wrinkle the tournament map makes vivid, and it deserves its own accounting because no previous sponsor in this category ever had to solve it.

The United States hosts the majority of matches, including the final, and offers Kraken its most valuable and most complicated market. Federal clarity has improved dramatically since 2022, with commodity classifications, spot fund approvals, and the ETF flow battle now shaping institutional allocation, but the state layer remains a patchwork: adjacent products like event contracts face active gaming-commission litigation in more than a dozen states, and marketing rules for financial products vary by jurisdiction in ways that make a uniform national activation legally impossible.

Canada brings provincial securities regulators with registration regimes that have already pushed several international exchanges out of the market entirely; operating activations in Vancouver and Toronto means satisfying regulators that have historically been among the strictest in the G7. Mexico sits at the other extreme, with a fintech law that predates the modern crypto industry and enforcement capacity that leaves large gray zones.

Europe, the other half of the activation footprint, is paradoxically the easy part. MiCA gives Kraken a single passportable framework across the EU, which is why a fan in Austria or Germany can move from broadcast to funded account with less regulatory friction than a fan in the host countries themselves. The asymmetry is a small preview of the industry’s strange 2026 geography: the tournament is in North America, but the cleanest conversion funnel runs through Brussels.

For Kraken, the patchwork is a cost. For the category, it is a moat. Any rival weighing a bid for the 2030 slot now knows the compliance overhead a global football activation carries, and incumbency in that knowledge is worth almost as much as the logo rights.

The scoreboard after the final

Crypto’s first World Cup has already produced its symbolic result: the industry is inside the perimeter, on the boards, in the partner list, treated by the sport’s governing institution as a normal commercial category rather than a reputational hazard. Given where crypto sports marketing stood three years ago, that alone is a recovery arc worth noting.

The financial result stays open past July 19. If Kraken converts even a sliver of six billion impressions into funded accounts, the deal becomes the template, and the 2030 tournament will have exchanges bidding for the category the way airlines bid for alliance slots. If the activity decays on schedule and the funnel leaks, the deal joins a quieter graveyard, the one for sponsorships that were merely expensive instead of catastrophic, and the industry learns that legitimacy and growth are separate purchases.

Either way, the precedent is set and cannot be unset. A World Cup now comes with a crypto exchange the way it comes with an airline and a soft drink. Whether that turns out to be the moment adoption bent upward or just the most expensive brand-awareness campaign in the industry’s history is a question with a hard deadline: the next four years, starting at full time on July 19. For a sector that measures its own maturity in cycles, the 2026 tournament will be remembered as the one where crypto stopped crashing the party and got printed on the invitation.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Digital asset markets are volatile and you can lose your entire investment. Always do your own research. Information current as of July 3, 2026.

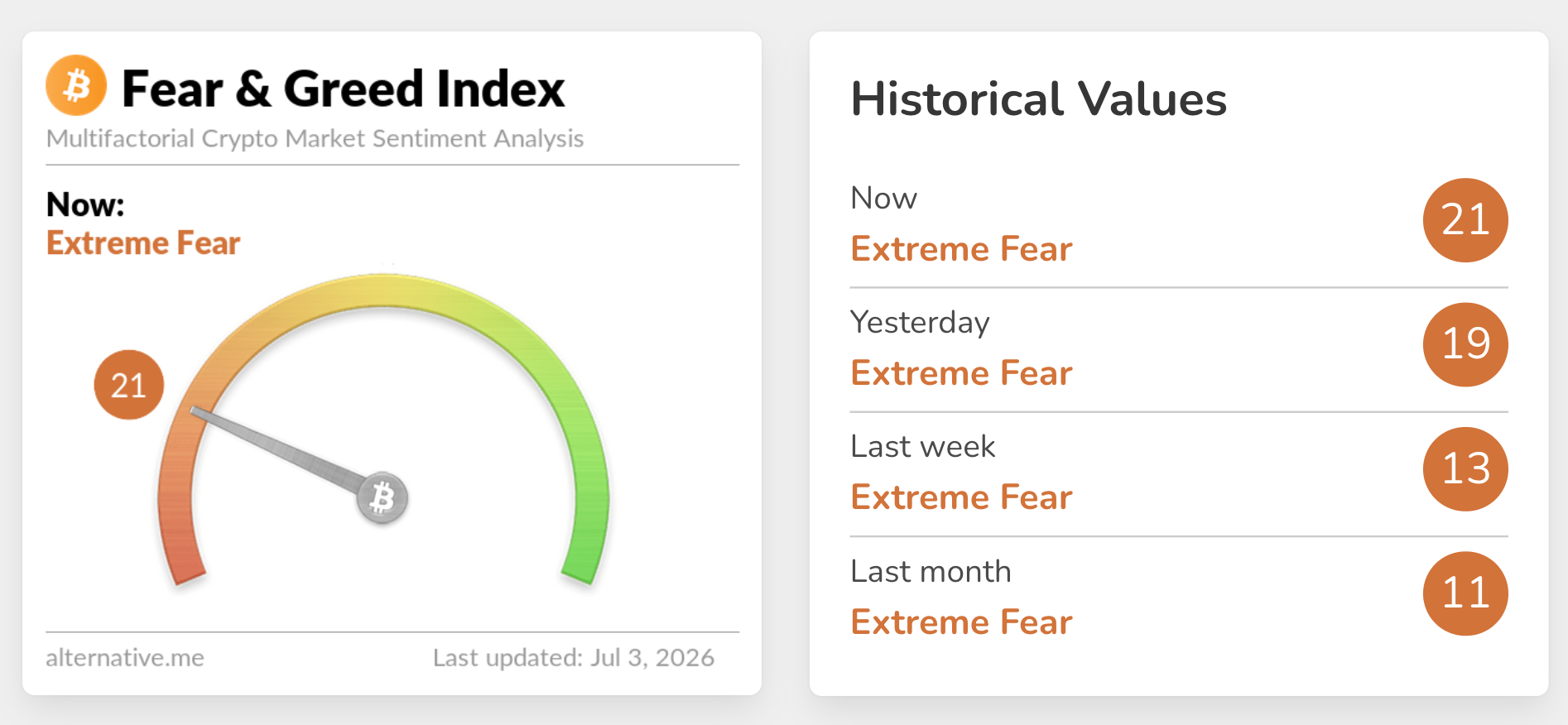

Bitcoin (BTC) rallied, $50 short of $63,000, on July 3, and Ether (ETH) outperformed the wider market, pushing to $1,775. The end-of-week rally comes a few days after BTC fell to a 21-month low and ETH sank to fresh year-to-date lows. Highlighting the negative sentiment, the Crypto Fear & Greed index registered “Extreme Fear” at 11 out of 100.

Crypto Fear & Greed Index. Source: Alternative.me

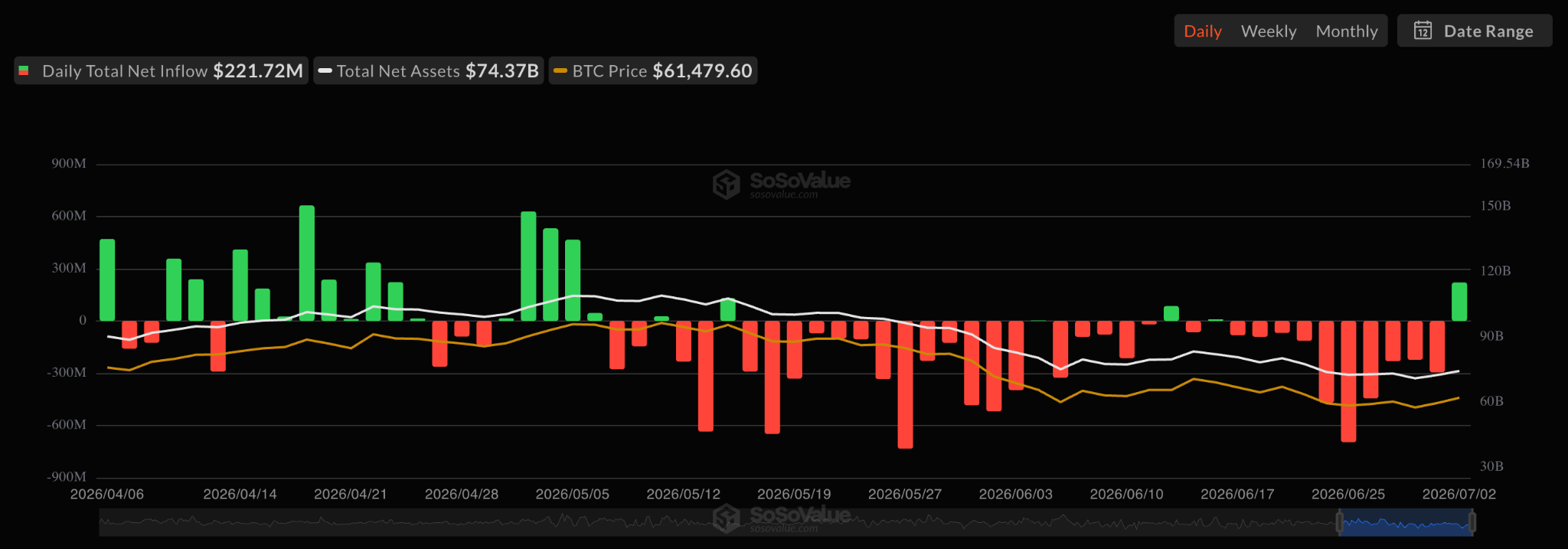

That gap between the “Extreme Fear” reading and Friday’s bullish market activity is worth noting. On July 2, US spot Bitcoin exchange-traded funds (ETFs) took in a net $221.7 million, their largest single-day inflow since early May and a break from 10 consecutive days of outflows.

Spot Bitcoin ETF netflows. Source: SoSoValue.com

Futures markets fuel Bitcoin and Ether gains

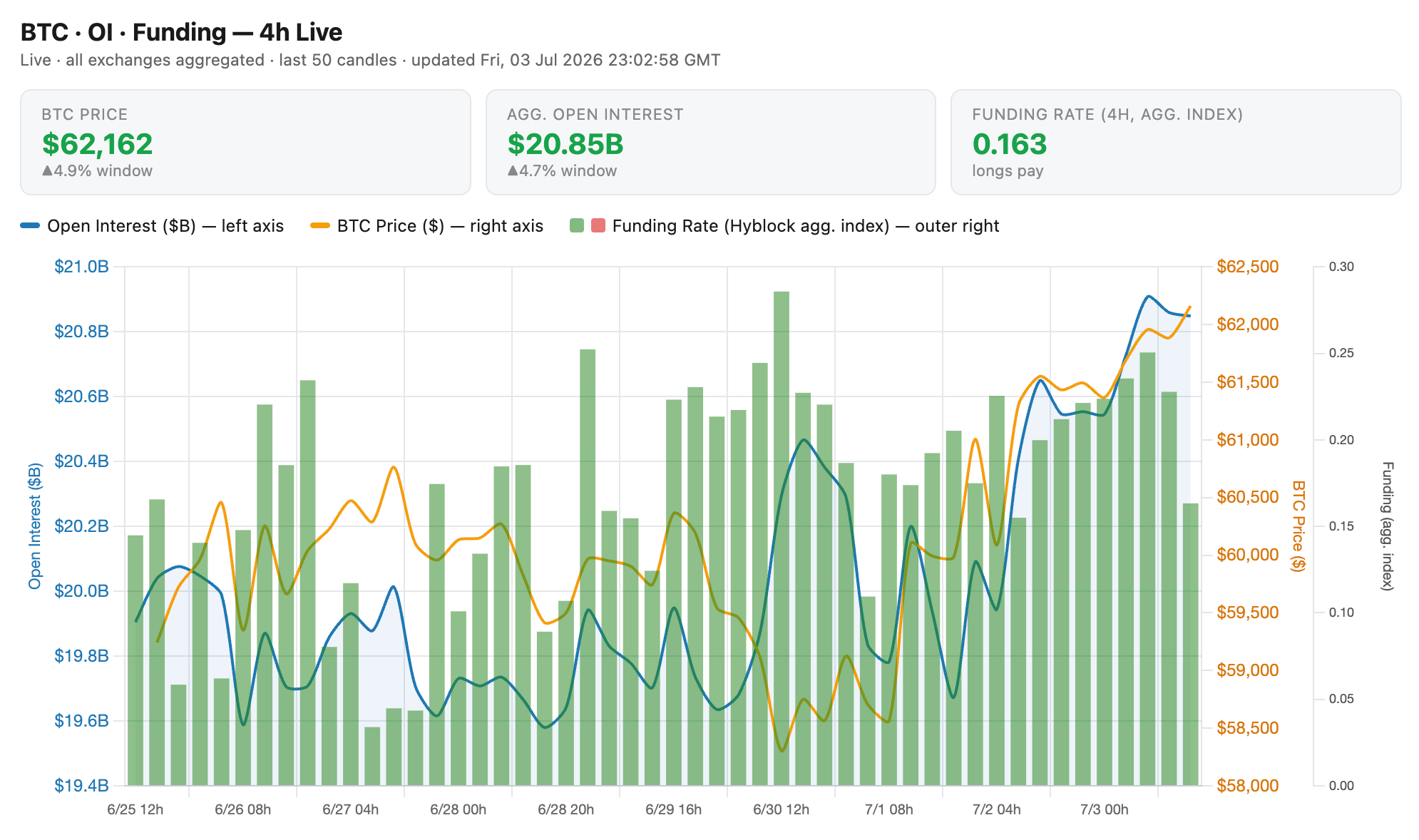

The leverage side of the crypto market looks more one-sided than the spot buying data alone would suggest. “Funding,” the periodic payment traders holding bets on higher prices make to traders betting on lower prices when the market leans bullish, has stayed positive for the past eight days and has been climbing throughout this period.

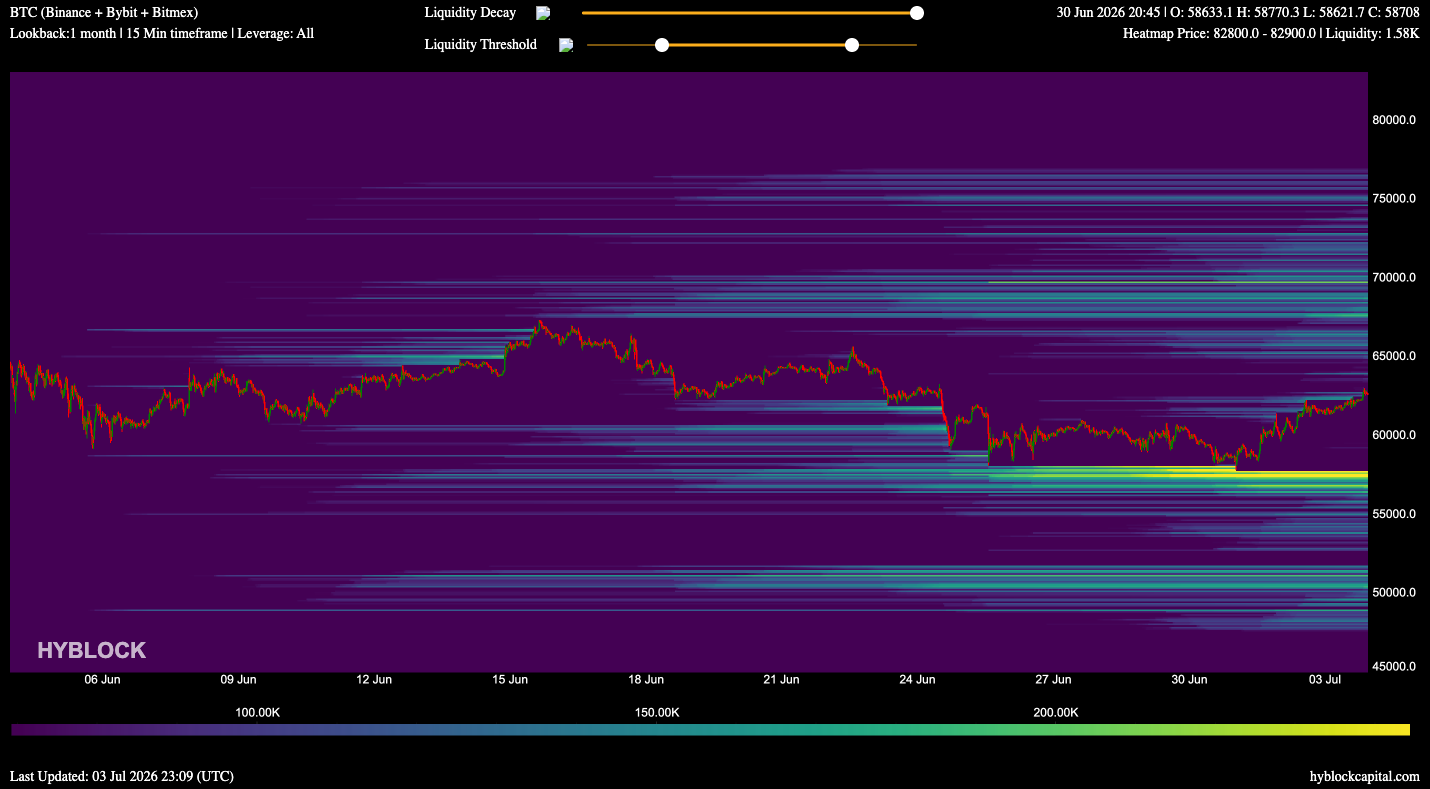

Bitcoin open interest, funding rate. Source: Hyblock

The total amount of outstanding leveraged Bitcoin positions is also near its highest level in the past several days, even though the price has mostly moved sideways. Leverage building up without price making much progress is generally viewed as a caution sign rather than confirmation that a rally is underway.

Related: Bitcoin holds $61K after US jobs data report, AI sector weakness: Did BTC bottom?

Can bulls keep their pace?

Looking at the next few trading sessions, a few reference points stand out. On the cautious side, whether Bitcoin holds above roughly $61,000, where a large cluster of leveraged buy positions sits, matters, and so does whether Wednesday’s ETF inflow turns out to be a one-day event or the start of a new trend.

On the more encouraging side, a move back above $62,500 would put Bitcoin within reach of price levels where leveraged short positions become more exposed, and continued positive buying activity alongside a still-growing pool of leveraged positions would extend the pattern seen over the past few days.

Bitcoin liquidation heatmap. One-month view. Source: Hyblock

The overall market read is mixed rather than clearly bullish or bearish. Spot buying and a rebound in ETF flows suggest sentiment may be improving faster than the fear-and-greed number implies, but a market this deeply fearful and this leveraged toward higher prices tends to be more fragile. The upcoming US holiday-weekend stretch of typically thinner trading adds another layer of uncertainty to the current setup.

U.S. President Donald Trump has pushed back against criticism over his 2025 financial disclosures, telling CNBC that there was “nothing illegal” and “nothing wrong” with profiting from crypto-related investments while in office. In the interview, Trump also suggested that other parties were responsible for certain investment activity, adding that he did not “even know who they are,” an answer that did not directly address conflict-of-interest concerns.

The comments came after the U.S. Office of Government Ethics released Trump’s 2025 financial disclosure report, which shows he received more than $2 billion from business and investment holdings during the year, with roughly $1.4 billion tied to crypto ventures. Advocacy groups have argued that such earnings create incentives to shape policy in ways that benefit related projects.

Key takeaways

- Trump told CNBC he saw “nothing illegal” in profiting from crypto investments while president, even as critics highlighted potential conflicts.

- The 2025 disclosure report from the U.S. Office of Government Ethics ties about $1.4 billion of Trump’s income to crypto-related activity.

- Disclosure breakdown cited in the report includes $636 million from a memecoin, $588 million from World Liberty, and $197 million connected to equity in a stablecoin venture.

- Public Citizen says crypto-linked contributors have put $189 million into the 2026 U.S. election cycle as of June.

What Trump said after the disclosure release

During a Thursday appearance on CNBC with Joe Kernen, Trump responded to questions surrounding the 2025 financial disclosures. He maintained that profiting from crypto investments as president was not improper, framing the controversy as baseless.

When pressed on the issue of who managed or executed the investments, Trump did not provide a straightforward explanation of how he handled potential conflicts. Instead, he argued that others were responsible for the investments and said he did not know the people involved, leaving open key questions that critics say are central to public trust.

Trump’s remarks followed the release of his 2025 disclosure report by the U.S. Office of Government Ethics, an agency responsible for collecting and publishing high-level financial information from top federal officials.

How the 2025 figures connect to crypto projects

According to coverage of the filing, Trump reported more than $2 billion in income from his businesses and investments in 2025, with about $1.4 billion connected to crypto-related activities. Among the crypto-linked components cited were his memecoin, the family platform World Liberty Financial, and an equity stake associated with a stablecoin venture.

Specifically, the crypto-related totals described include approximately $636 million generated by his memecoin, about $588 million from World Liberty sales, and roughly $197 million from equity in a stablecoin venture. Together, these figures form the bulk of the reported $1.4 billion crypto-related income highlighted by critics.

Advocacy organizations have characterized these investments as a form of “grift,” arguing that political influence—whether direct or indirect—could advantage projects tied to Trump and his family. One such critique referenced in the reporting linked the donations and leverage question to proposed legislative efforts, including the Digital Asset Market Clarity (CLARITY) Act.

Earlier reporting on the disclosure emphasized the scale of the crypto-linked earnings and the overlap with areas where U.S. policy could affect digital asset markets.

From skepticism to industry alignment

Trump’s evolving posture toward crypto has been a defining theme of the past several years. In the wake of his first term, he had referred to Bitcoin as a “scam.” However, in the period leading up to the 2024 election, he increasingly associated himself with high-profile crypto figures and industry executives.

As described in the reporting, the shift included engagement with Gemini co-founders Cameron and Tyler Winklevoss, alongside relationships with executives from mining companies and crypto exchanges. During that same broader period, Trump launched a memecoin known as Official Trump (TRUMP), while his family’s involvement with World Liberty and American Bitcoin placed additional attention on crypto-native business activity.

The contrast between earlier skepticism and later engagement is central to why the disclosure controversy has attracted significant attention: critics argue the president’s financial exposure to crypto projects makes it harder to separate policy decisions from personal or business incentives.

Election spending: crypto money looks set to stay active in 2026

The controversy over Trump’s disclosures arrives amid evidence that crypto-related money is becoming a fixture of U.S. electoral spending. After digital asset firms and figures reportedly spent $170 million to support “pro-crypto” candidates to Congress in 2024, political action committees and aligned organizations appear to be applying a similar approach for 2026.

According to Public Citizen, companies and individuals tied to the crypto industry contributed $189 million to this year’s election cycle as of June. Public Citizen also reported that the $189 million figure makes up most of $294 million spent so far by crypto, AI, Big Tech, and online betting companies to support or oppose politicians.

With Trump’s term ending in January 2029, the current political landscape matters for more than symbolic scrutiny: all 435 seats in the U.S. House of Representatives and 35 seats in the Senate are up for election in 2026. For digital asset firms, stablecoins, exchanges, miners, and token issuers, legislative outcomes in the next cycle could shape compliance rules, market structure, and the pace of regulatory clarity.

Related coverage pointed to how these spending patterns reflect a sustained effort to influence policy direction during election years.

Pressure and counterpressure from within Trump’s orbit

Criticism is not limited to advocacy groups outside Trump’s circle. In comments relayed from a Friday interview with CNN’s Anderson Cooper, Mary Trump—his niece—accused him of pushing boundaries and argued that people could evade consequences due to the president’s use of the presidential pardon power.

While her remarks were not directly focused on the legal interpretation of financial disclosure rules, they underscore the broader narrative opponents are advancing: that public officials with substantial financial exposure to crypto-related enterprises face intensified scrutiny over potential conflicts of interest and the consequences for those who invest based on political proximity.

What to watch next

As scrutiny continues, the next signals to monitor are how regulators and watchdogs interpret the disclosure details in the context of federal ethics rules, and whether the 2026 election cycle brings additional policy movement on digital assets—especially in areas that intersect with stablecoins, token issuance, and broader market structure.

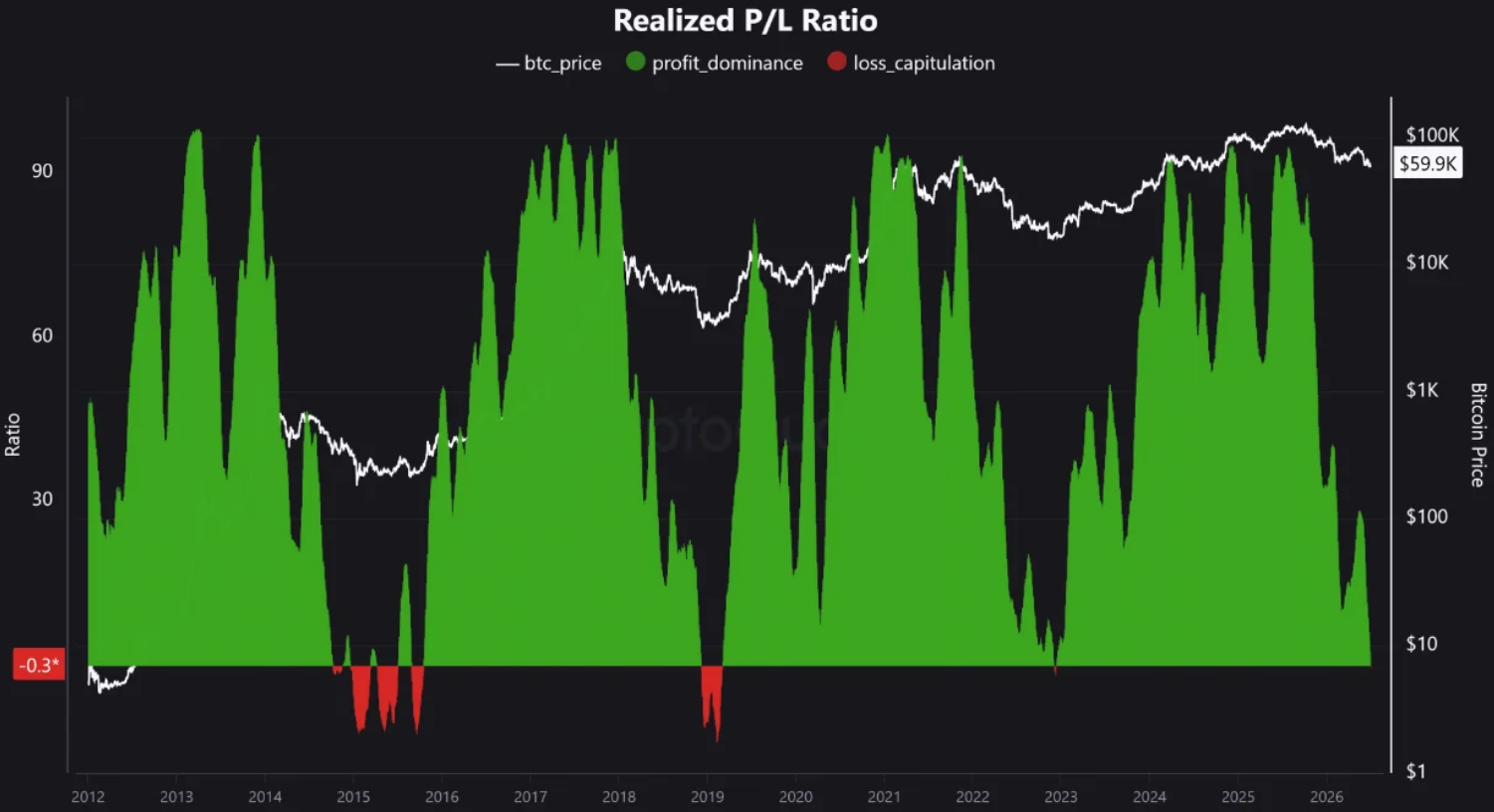

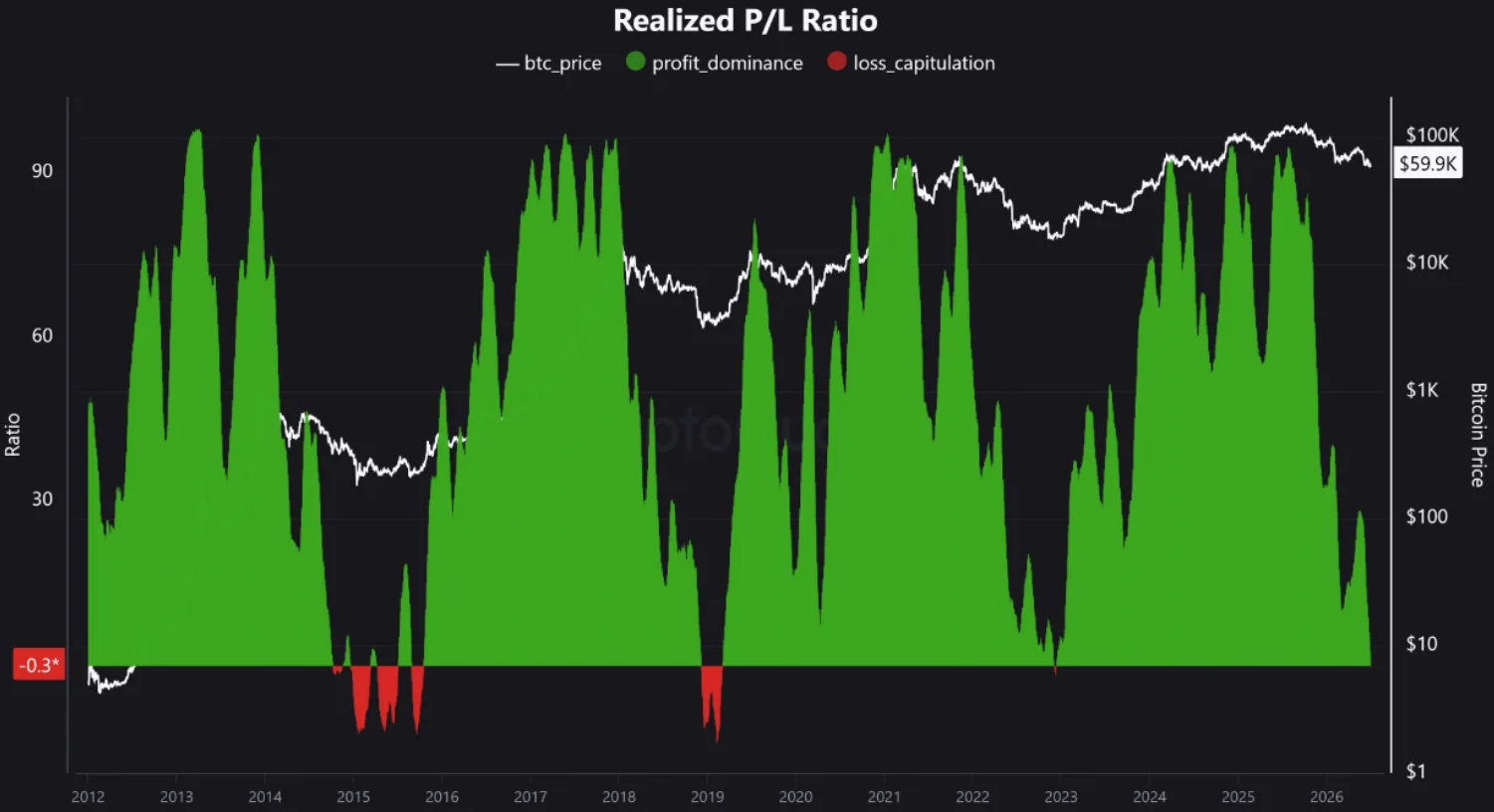

Bitcoin is flashing a highly unusual on-chain signal: its realized profit-and-loss ratio has fallen to a 43-month low of -0.35, an indicator CryptoQuant says reflects “extreme” loss conditions across the market. Historically, CryptoQuant adds, that type of reading has tended to appear close to major price bottoms.

The metric has not been this low since shortly after the FTX collapse, when Bitcoin traded below $16,000 in late 2022. With BTC still recovering from a steep drawdown that began after a peak near $126,080 in October, the new data is adding fuel to a broader debate among analysts over whether the market is past its worst stress—or merely approaching it.

Key takeaways

- CryptoQuant reports Bitcoin’s realized P&L ratio hit -0.35, the lowest reading in 43 months, last seen around late 2022.

- CryptoQuant says past occurrences of readings below -0.35 in 2015 and 2019 preceded subsequent rallies.

- CryptoQuant’s on-chain stress signal is arriving as “Fear and Greed” sentiment has moved off near-record lows and Bitcoin has bounced more than 7% from a June 25 trough near $58,190.

- Some analysts link the current drawdown to Strategy’s Stretch (STRC) preferred-stock offering and related concerns about dividend coverage.

- Other commentators argue investors should not wait for a “bottom” to be obvious because historical discount zones have been associated with strong 6- and 12-month forward returns.

Realized P&L reaches a historically rare loss zone

According to CryptoQuant, the Bitcoin realized profit-and-loss (P&L) ratio has dropped to -0.35. The realized P&L ratio measures the net percentage of Bitcoin currently in profit or loss relative to total supply, using on-chain cost basis information. In practical terms, a more negative reading indicates that a larger share of holders are underwater on their realized entry prices.

CryptoQuant emphasized that the -0.35 threshold has shown a strong historical relationship with major bottoming behavior. In its analysis published Thursday, the firm said that realized P&L has “marked BTC bottoms with extreme precision,” citing earlier periods where the ratio slipped below -0.35 before later rebounds.

The indicator’s last comparable level came around December 2022, shortly after the FTX collapse exposed fragile market liquidity. Back then, Bitcoin fell to levels under $16,000—an episode that many market participants still reference as a stress test for crypto’s risk assets.

What the signal may mean for sentiment and timing

CryptoQuant’s indicator arrives during a sharp correction cycle that began from a high set in October near $126,080, after which Bitcoin experienced a roughly 50% drawdown. While past realized P&L readings can be informative, timing remains the key question for investors: a bottom signal can appear before prices fully recover, and it does not rule out additional volatility.

Still, broader sentiment gauges show signs of stabilization. The “Fear and Greed” index has risen cautiously over the past 10 days, according to the index page on Alternative.me. During the same window, Bitcoin has climbed more than 7% after falling to a near two-year low of about $58,190 on June 25, as reflected in prior reporting by Cointelegraph.

In other words, the on-chain data and the sentiment recovery are moving in the same direction, even if they don’t provide a precise “day of the bottom” forecast.

Strategy’s STRC episode and the leverage unwind narrative

A significant part of the discussion around the latest selloff centers on corporate Bitcoin exposure. Cointelegraph previously reported that analysts attributed much of the recent weakness to Strategy—the largest corporate Bitcoin holder—after its top perpetual preferred stock offering, Stretch (STRC), deviated from its $100 par value. The move reportedly pushed STRC below $75, raising concerns that Strategy’s dividend model may have been strained.

On Thursday, Cointelegraph noted that Bitwise chief investment officer Matt Hougan said the STRC incident likely helped “squeeze out excess leverage” and could be pushing the market closer to a bottom as participants work through the fallout.

For traders and long-term holders alike, this matters because leveraged positioning can magnify moves on the way down. If leverage is truly being unwound—whether through forced deleveraging, hedging adjustments, or repricing of capital-market products—then the market may become less mechanically vulnerable to sudden liquidations. What remains unclear is how much of that unwind is complete and whether new risk reappears as prices rise.

Why some analysts say buying before the “bottom” may be rational

Not all commentary is framed around waiting for confirmation. Swan Bitcoin analyst Adam Livingston pointed to how close Bitcoin is currently trading relative to its realized price—the network’s aggregate cost basis, which often acts as a reference point in on-chain analysis.

According to Livingston, Bitcoin is trading about 16% above the realized price. He argued that this historically aligns with strong forward returns, citing research showing 41% gains over six months and 81% gains over 12 months following similar discount conditions.

Livingston acknowledged that buying at this stage “feels awful,” but he argued the psychological discomfort is part of why the opportunity can appear. In his view, waiting for a “bottom” is flawed because bottoms rarely announce themselves in a way that’s reliable enough to time entries perfectly.

While that argument is not a guarantee, it reframes the debate: rather than trying to predict the exact turn, investors may focus on whether market-wide indicators—on-chain loss concentration, realized valuation levels, and sentiment—suggest that downside pressure is fading.

What to watch next

For the near term, traders and investors will likely keep comparing this realized P&L trough with subsequent price action: if Bitcoin continues to stabilize while sentiment improves and leverage unwinds, the market may be shifting from capitulation toward consolidation. The key uncertainty is whether the current signals mark a decisive bottoming phase—or simply another stage in a volatile transition.

Bitcoin’s realized profit and loss ratio has fallen to a 43-month low of -0.35, a figure that signals extreme market-wide loss conditions but has historically coincided with market bottoms, blockchain analytics platform CryptoQuant said.

The Bitcoin realized P&L ratio — which measures the net percentage of Bitcoin (BTC) in profit or loss relative to total supply — hasn’t fallen this low since December 2022, shortly after FTX shockingly collapsed and sent Bitcoin below $16,000.

“Historically the indicator has marked BTC bottoms with extreme precision,” CryptoQuant said on Thursday. In 2015 and 2019 the Bitcoin realized P&L ratio also fell below -0.35 before price rallies followed.

Change in Bitcoin’s P/L ratio since 2012. The data was taken when Bitcoin was trading at $59,000. Source: CryptoQuant

The data could lift market sentiment, which has repeatedly fallen to near-record lows during the course of Bitcoin’s latest 50% drawdown from $126,080, set in October. Market sentiment has risen cautiously over the last 10 days, with Bitcoin up more than 7% since tanking to a near two-year low of $58,190 on June 25.

Many analysts blamed that drop on Strategy — the largest corporate Bitcoin holder — after its top perpetual preferred stock offering, Stretch (STRC), broke from its $100 par value to below $75, raising fears that its dividend model was unsustainable.

Related: Crypto Biz: Bitcoin maximalism meets the realities of capital markets

On Thursday, Bitwise chief investment officer Matt Hougan said the STRC incident squeezed out excess leverage and likely moved the market one step closer to a bottom.

“As the market continues to sort things out, I’m convinced the bottom is closer than ever — and that we will enter a new bull market in the fall.”

Don’t wait for the bottom, analyst says

Swan Bitcoin analyst Adam Livingston noted that Bitcoin is currently trading only 16% above the realized price — the network’s aggregate on-chain cost basis — a level that has historically coincided with strong forward returns of 41% at six months and 81% at 12 months.

Livingston acknowledged that buying Bitcoin right now “feels awful,” but that’s precisely why it’s trading at a discount, he argued.

“Waiting for ‘the bottom’ is a wonderful plan with one flaw. The bottom never announces itself,” Livingston said, recommending investors buy now rather than overpay at the top.

Magazine: Bitcoin slides to $58K, XRP hits $1 but onchain data promising: Market Moves

Senator Kirsten Gillibrand, a leading US lawmaker involved in negotiations on digital-asset market regulation, has proposed a new ethics rule aimed at preventing elected officials—and the president and their spouse—from issuing or backing their own tokens. The push comes as renewed scrutiny continues around conflicts of interest in the crypto space.

In a notice released on Friday, Gillibrand said Congress should consider legislation that would bar elected officials and their spouses from “issuing or sponsoring their own digital assets.” Her proposal specifically covers the US president and their spouse, while not clarifying whether the restriction would also apply to other family members or, for example, the vice president’s office.

Key takeaways

- Senator Kirsten Gillibrand is calling for a ban on elected officials and their spouses issuing or sponsoring their own digital assets.

- The draft she outlined would cover the president and the president’s spouse, according to her Friday statement.

- The proposal targets concerns about self-dealing and insider influence in crypto-related policy.

- Gillibrand’s ethics push ties into broader legislative negotiations around the Digital Asset Market Clarity (CLARITY) Act, where ethics issues have contributed to delays.

- The new restriction does not explicitly extend to other relatives, even as other criticisms have focused on family involvement in crypto-linked activities.

A targeted ethics rule aimed at token issuance

Gillibrand framed her proposal as a practical safeguard for a sector still working toward consistent federal rules. In her comments, she argued that officials and their spouses should not be able to issue memecoins, emphasizing the risk that personal financial incentives could undermine consumer protections and efforts to combat illicit activity.

Her statement links the ethics concern directly to conflicts of interest: she said “self-dealing” should not be allowed to weaken the policy work required to strengthen safeguards and expand financial access. Gillibrand also pointed to the broader public interest in ensuring enforcement and rulemaking are not distorted by insider advantages.

The senator’s notice also suggested that any workable solution must be broad enough to address the integrity of the legislative process, particularly when lawmakers have influence over market structure and consumer-facing rules.

How this connects to the CLARITY Act negotiations

Gillibrand is not introducing the idea in isolation. She is also among the lawmakers negotiating the Digital Asset Market Clarity (CLARITY) Act in the Senate—a bill that has reportedly faced delays linked to ethics concerns, tokenization questions, and how stablecoin incentives would be handled.

According to earlier reporting, Gillibrand expected the chamber to vote on the CLARITY Act by the Senate’s August state work period, but said no one would support the bill without addressing ethics concerns. Her reasoning centered on the possibility that elected officials could “get rich” from crypto markets due to their insider status.

That legislative backdrop helps explain why a narrower proposal about memecoin issuance by officials and spouses could still be politically important: it would target a concrete scenario—token sponsorship or issuance by those with rulemaking power—rather than leaving ethics questions as a vague debate.

Earlier coverage from Cointelegraph noted that lawmakers were wrestling with ethical and structural concerns in the broader package, including issues related to tokenization and stablecoin-linked rewards.

GENIUS Act history and memecoin conflict concerns

Gillibrand’s latest proposal also aligns with a moment in the development of stablecoin regulation. During consideration of the Guiding and Establishing National Innovation for US Stablecoins Act (GENIUS Act) in 2025, she said that senators had removed provisions specifically targeting Trump’s connections to the crypto industry, including the president’s memecoin Official Trump.

At the time, Gillibrand said the memecoin was likely “illegal based on current law,” but she acknowledged that fully addressing Trump’s ethics problems would require a “very long and detailed bill.” Trump later signed the GENIUS Act into law in July 2025.

That history highlights a recurring tension in Washington’s approach to crypto ethics: even when lawmakers see potential conflicts, crafting a solution that both clears legal scrutiny and achieves political consensus can be difficult. Gillibrand’s new initiative appears designed to shorten that distance by creating a rule that directly restricts token issuance or sponsorship by officials and their spouses.

Trump’s response and the wider conflict-of-interest debate

The proposal arrives amid continued debate over whether crypto profits by political figures create improper influence. This week, Cointelegraph reported that Trump said he earned about $1.4 billion from crypto ventures in 2025, the same year he took office.

According to Cointelegraph’s earlier reporting, Trump also asserted there was “nothing illegal” and “nothing wrong” with profiting from investments as president, while not directly answering questions about perceived conflicts of interest. The underlying concern for critics is not only whether transactions are legally permissible, but whether they erode trust in policymaking when an official’s financial exposure is tied to the regulatory outcomes.

Gillibrand’s proposal also stops short of explicitly extending the ban to all relatives. While she focused on elected officials and spouses, other criticisms have targeted the role of Trump’s sons in crypto-adjacent ventures, including World Liberty Financial and American Bitcoin, as reported in the article’s discussion of prior controversy.

That gap may matter for supporters of stricter rules: if spouses and officials are barred, critics may still ask how regulators should treat token sponsorship that is effectively enabled through broader family involvement, especially where family-linked businesses or holdings can influence perception—even if not always statutory ethics triggers.

As the CLARITY and stablecoin-related policy agendas continue to evolve, the key question for investors, builders, and market participants is whether ethics restrictions become part of a final legislative package—or remain a recurring obstacle that slows major crypto bills. Watch closely for whether Gillibrand’s proposal gains bipartisan traction, and whether negotiators are willing to translate ethics objections into enforceable rules rather than leaving them to case-by-case scrutiny.

Irish authorities have recovered another 500 BTC from wallets tied to convicted drug trafficker Clifton Collins.

Summary

- Irish authorities recovered another 500 BTC, raising total seized funds from Collins wallets to 1,500 BTC.

- Arkham data shows roughly 4,500 BTC still tied to dormant wallets linked to the case.

- Europol’s cybercrime unit helped investigators access wallets once believed unreachable due to lost private keys.

The Criminal Assets Bureau said in a Facebook statement that the latest seizure was made with support from Europol’s European Cybercrime Centre.

The latest recovery brings CAB’s total in the Collins case to 1,500 BTC. The bureau said the Bitcoin was identified as proceeds of crime. It marks the third 500 BTC recovery from the same wider wallet cluster this year, after earlier seizures in March and May.

Case traces back to lost private keys

The Collins case became known because the Bitcoin was long believed to be out of reach. The Irish Times reported in 2020 that Collins bought most of the coins in late 2011 and early 2012 using proceeds from cannabis sales. He later split more than 6,000 BTC across 12 wallets, with 500 BTC in each wallet.

According to that report, Collins printed the private keys on paper and hid them in the aluminum cap of a fishing rod case at a rented home in County Galway. The property was later cleared after his arrest, and the fishing gear was believed to have been taken to a dump. The keys were then viewed as lost.

Europol support remains central

Europol has helped Irish investigators in the wallet recovery work. The Irish Times reported in March that CAB accessed the first 500 BTC wallet with support from Europol’s European Cybercrime Centre. Garda Headquarters said at the time that Europol provided “highly complex technical expertise and decryption resources” for the operation.

As previously reported, Irish authorities first accessed a lost Bitcoin wallet tied to Collins in March. That wallet held 500 BTC and was part of the same 6,000 BTC stash. The recovery was notable because the funds had been viewed as locked for years.

Dormant wallets still hold large value

As crypto.news reported in May, the seizure later reached 1,000 BTC after CAB and Europol secured a second 500 BTC wallet. At the time, Arkham said another 500 BTC had moved from the Collins-linked entity after years of inactivity.

The latest move raises the total known recovery to 1,500 BTC. Onchain data from Arkham still tags wallets linked to Collins and shows remaining activity tied to the entity. Lookonchain also said in a July 2 post on X that another 500 BTC had been deposited to Coinbase Prime, while about 4,500 BTC remained in wallets linked to the case.

Recovery keeps case under scrutiny

The Collins case remains one of Ireland’s best-known crypto crime recoveries because the funds were tied to old private-key storage and years of inactivity. Each wallet recovery reduces the amount still considered dormant, but a large balance remains under watch by onchain analysts.

The case also shows how law enforcement agencies are using technical support and blockchain tracking in asset recovery. CAB has not fully explained how investigators gained access to the latest wallet. For now, the confirmed recoveries show that Bitcoin once viewed as lost may still be reachable when agencies combine legal seizures, cybercrime support, and onchain tracing.

The U.S. Securities and Exchange Commission (SEC) is studying a more orderly process for ETF approvals as the agency faces a sharp rise in new product filings.

Summary

- SEC officials want a clearer ETF process as crypto and prediction market filings increase sharply.

- Confidential filings could protect ETF issuers from copycats before new products become public.

- Prediction market ETFs remain under review while regulators seek feedback on novel fund structures.

Bloomberg ETF analyst Eric Balchunas said in a post on X that SEC Investment Management Division official Brian Daly said the agency receives about 200 ETF applications each month.

Daly made the comments during a Trillions interview with Balchunas and Joel Weber. According to Balchunas, Daly said the SEC “did a bad job with crypto” and wants to rebuild trust through an “orderly process” for novel products, including prediction market ETFs.

Confidential filings under review

Balchunas said in a second post on X that the SEC is also considering confidential ETF filings. The idea would allow some issuers to file products privately before their applications become public. That could protect early ideas and reduce copycat filings.

The SEC raised a similar issue in its public review of novel ETFs. As crypto.news reported, the agency asked whether ETF filings should stay confidential for part of the 75-day review period before becoming public. The agency said this could give applicants more room to develop products without rushing incomplete filings into the market.

Prediction market ETFs remain paused

The review comes while prediction market ETFs remain under SEC scrutiny. As crypto.news reported, the SEC delayed several prediction market ETF proposals while seeking public input on how event-based funds should be regulated. Bitwise, Roundhill Investments, and GraniteShares had filed products tied to elections and other event contracts.

The SEC’s official June 30 request asks for feedback on ETFs that invest in innovative assets or use novel strategies. SEC Chair Paul Atkins said ETF innovation depends on a “consistent, transparent, and efficient regulatory framework.” Daly also said ETF assets grew from $4 trillion in 2019 to more than $12 trillion at the end of 2025.

Crypto ETFs add to the filing wave

The agency’s review also matters for crypto funds. As previously reported, the SEC approved the T. Rowe Price Active Crypto ETF, a multi-asset product that may hold Bitcoin, Ethereum, XRP, Solana, Dogecoin, Shiba Inu, and other assets. That approval showed how crypto products are moving beyond single-asset funds.

Other issuers are also testing the new ETF path. Bitwise filed an S-1 for a spot SUI ETF, while the SEC’s generic listing standards have shortened parts of the approval process for qualifying products. The rising number of applications has made process questions more urgent.

The SEC is also reviewing wider digital asset rules. Previously, crypto.news reported that Atkins backed a limited innovation exemption for tokenized securities. That work sits beside the ETF review as the agency tries to support new products while keeping investor disclosures clear.

For ETF issuers, confidential filings could change how new products reach the market. For investors, the main question is whether the SEC can speed up reviews without weakening oversight. The current review shows the agency is trying to avoid another uneven approval cycle as crypto, tokenization, and prediction markets enter the ETF market.

CACEIS, the custody banking arm of Crédit Agricole, is in exclusive talks to acquire French crypto investment platform Meria, according to a BlockStories report.

Summary

- CACEIS is reportedly targeting Meria to expand beyond crypto custody into brokerage and staking services.

- Meria’s MiCA license gives the French platform stronger regulatory access across Europe’s crypto market.

- The talks show banks are buying crypto-native firms as MiCA raises compliance pressure across Europe.

The deal has not been formally announced by either company.

Meria, formerly known as Just Mining, was co-founded by Owen Simonin, known online as Hasheur. The company serves about 150,000 users and manages roughly €350 million in assets under management, according to the report. Its main services include crypto brokerage and staking products.

A bank push into crypto services

CACEIS already has a digital asset business line focused on custody. The company says its crypto services target asset managers, institutional investors, and other clients seeking regulated access to digital assets. Its parent group, Crédit Agricole, is one of France’s largest banking groups.

CACEIS also holds French and European crypto permissions. The AMF’s public record says CACEIS Bank has been authorized to provide crypto-asset services under MiCA through the Article 60 notification route. That allows the group to offer services such as custody, order reception, and transfer of crypto-assets.

Meria adds retail reach and staking

A Meria deal would give CACEIS access to a crypto-native platform with a retail user base and staking expertise. BlockStories reported that staking is one of the activities of interest to CACEIS, as Meria serves both retail and institutional clients in that area.

The reported talks come shortly after Meria received MiCA CASP authorization in France. A market intelligence listing shows Meria SAS as a France-based MiCA Crypto-Asset Service Provider authorized by the AMF on June 22. That timing gives the platform added value as Europe’s new licensing regime takes full effect.

MiCA changes the deal market

The talks reflect a wider shift in Europe’s crypto market. The MiCA transition period ended on July 1, forcing many crypto firms to secure CASP licenses or stop serving users under the old national regimes.

MiCA gives licensed firms a European passport, but it also raises compliance costs. As previously reported, France and other EU markets have seen a divide between firms that secured authorization and those still working through the process. That gap may push banks and larger regulated firms to buy licensed crypto platforms instead of building everything internally.

Banks move closer to regulated crypto

The reported Meria talks also fit a broader pattern of regulated finance moving into digital assets. As crypto.news reported, Coinbase opened its Luxembourg MiCA hub as the EU deadline approached. The exchange used Luxembourg as its base for serving customers across the bloc under one licensing setup.

Other firms have taken similar steps. As reported by crypto.news, Ripple moved closer to full MiCA compliance through Luxembourg CASP approval, while B2C2 secured MiCA approval to expand regulated crypto trading across Europe.

The National Organization of Black Law Enforcement Executives has endorsed the Digital Asset Market Clarity Act, giving the crypto market structure bill its first formal public backing from a major law enforcement group.

Summary

- NOBLE became the first major law enforcement group to formally back the CLARITY Act.

- The endorsement challenges warnings from police and prosecutor groups over Section 604 language.

- The bill still needs Senate floor time and 60 votes before reaching final passage.

Journalist Eleanor Terrett reported the endorsement in a July 2 post on X, citing a letter sent to Senate leaders John Thune and Chuck Schumer.

NOBLE National President Reneé Hall signed the letter. According to Terrett, the group said the bill “contains several provisions” that could give law enforcement new tools while keeping existing criminal authorities in place. The endorsement arrives as Senate talks continue over crime, oversight, and developer protections in the bill.

Endorsement breaks from other groups

NOBLE’s position differs from earlier warnings by several police and prosecutor groups. Four U.S. law enforcement organizations raised concerns that Section 604 may weaken crypto crime investigations. Their concerns centered on the Blockchain Regulatory Certainty Act language inside the CLARITY Act.

Section 604 would protect some non-custodial developers and software providers from automatic money transmitter treatment. Critics argue that the language may make it harder to trace illicit finance in decentralized systems. Supporters say the section protects software builders who do not control user funds and should not be treated like banks or brokers.

DOJ pushback adds to debate

The debate widened after the Department of Justice pushed back on claims that the bill would create broad enforcement gaps. As crypto.news reported, the DOJ challenged law enforcement claims and said criticism of the bill’s crime-fighting language was not accurate.

NOBLE’s letter now gives supporters another argument as they seek Senate votes. The group said the bill does not change federal criminal tools used in money laundering, unlicensed money transmission, conspiracy, sanctions, and other cases. That point directly addresses one of the main objections raised by other law enforcement groups.

Senate clock remains tight

The endorsement comes as the bill faces a narrow window in the Senate. The CLARITY Act’s path depends on a pre-August vote because the chamber has limited floor time before recess. If the bill misses that window, its realistic path could move into 2027.

The bill also needs 60 votes on the Senate floor. As previously reported, the Senate math requires Democratic support because Republicans cannot pass the measure alone. That makes law enforcement concerns important, especially for senators focused on illicit finance, consumer protection, and national security.

Industry keeps pressure on lawmakers

Industry groups are also pressing senators to act. Stand With Crypto urged supporters in a July 2 post on X to call for a vote when the Senate returns from recess on July 13. The group argued that delay could push builders, jobs, and capital outside the U.S.

Every day without clear rules, innovation drifts overseas.

When the Senate is back from recess on July 13, Senators can vote YES on the Clarity Act to keep American builders, jobs, and capital here at home instead of heading abroad.

The window is narrow. Tell your Senators to… — Stand With Crypto🛡️ (@standwithcrypto) July 2, 2026

The CLARITY Act would create a market structure framework for digital assets and define roles for the SEC and CFTC. The bill would classify digital assets, set registration paths, and add compliance rules for crypto firms.

A pseudonymous defendant has asked a New York court to dismiss a lawsuit seeking ownership of 39,069 dormant Bitcoin addresses, arguing that Bitcoin addresses are simply public data and cannot be sued under the state’s jurisdictional rules.

In a motion filed Thursday, the defendant—using the name “John Doe 33”—contends that the plaintiff’s theory of “finding” and claiming abandoned property fails because a Bitcoin address is not a legal person or entity. The filing also challenges the effort to treat on-chain addresses as recoverable under New York lost-property law.

Key takeaways

- The motion argues that Bitcoin addresses are data strings that cannot be the subject of a lawsuit, rather than legal entities that courts can exercise jurisdiction over.

- The plaintiffs’ lost-property claim is framed as legally defective because the addresses were always publicly visible on the blockchain.

- Even if ownership were determined, recovering the Bitcoin would still require access to the corresponding private keys.

- Blockchain-linked reporting cited in the case suggests the defendant may control a long-dormant wallet holding roughly 5,000 BTC.

Why the court fight centers on “addresses” rather than keys

The lawsuit, filed in May by plaintiff “Noah Doe” along with two Wyoming-based LLCs identified as ABC Company and XYZ Company, targets what it describes as abandoned Bitcoin associated with 39,069 dormant addresses. The plaintiffs allege the Bitcoin tied to those addresses is abandoned property, which they reported to the New York Police Department before asserting claims under New York lost-property law.

In the motion to dismiss, John Doe 33 argues the complaint is legally defective for a threshold reason: Bitcoin addresses are not “persons” or legal entities and therefore cannot be sued. The filing further claims that the plaintiffs cannot establish that an address was “found,” as required by lost-property concepts, because the relevant address information has been publicly viewable on the blockchain since the coins were received.

For investors and builders, the procedural dispute matters because it goes beyond a single wallet list. It asks whether traditional legal frameworks for identifying owners and claiming property can map onto the blockchain’s structure—where addresses are public identifiers and control is enforced through private keys rather than through legal status.

The alleged “abandoned” wallets include famous names

The complaint lists 39,069 Bitcoin addresses that include wallets widely associated with well-known Bitcoin labels, such as addresses attributed to Bitcoin creator Satoshi Nakamoto and to the Mt. Gox hacker. The addresses collectively are reported—via an estimate attributed to Sani, founder of Bitcoin analytics platform Timechain Index—to hold roughly 3.7 million BTC, valued at about $234 billion at the time of that estimate.

That scale is a key reason the case has attracted attention. A ruling could influence how courts treat claims that attempt to convert blockchain identifiers into claimable “property” within existing state laws.

At the same time, the filing acknowledges a practical hurdle that remains independent of any jurisdictional debate: even if the court were to rule on ownership of the assets associated with the addresses, the plaintiffs would still need the private keys to move any Bitcoin. Without those keys, the Bitcoin remains inaccessible regardless of how a court characterizes ownership or abandonment.

Defendant says they control a long-dormant wallet

Separate from the legal arguments, the motion’s credibility is bolstered—at least in part—by blockchain data cited in public commentary. According to an X post on Friday by Alex Thorn, head of research at Galaxy Digital, blockchain information suggests John Doe 33 controls a wallet that received 5,000 BTC in April 2014 and has remained untouched for more than 12 years.

Thorn indicated the wallet’s current value is above $300 million at prevailing market prices, and he characterized the defendant as a “real holder” with meaningful standing rather than a bystander who could be targeted without any real ability to defend the claim.

Thorn also wrote that the filing helped avoid what had been described as a “near-certain” default judgment, while simultaneously challenging jurisdictional and statutory defects raised by the plaintiffs’ approach.

Dormancy data underscores why recovery questions persist

Beyond the specific defendants and plaintiffs, the broader question of what happens to lost or inaccessible Bitcoin continues to drive legal scrutiny. Bitbo data cited in the reporting indicates that about 3.5 million BTC, valued around $215 billion, have been dormant for at least 10 years, while another 6.6 million coins—worth roughly $406 billion—have been dormant for over five years.

Those figures highlight a persistent imbalance in how on-chain “time” translates to legal rights. Blockchain dormancy may signal lost control, but it does not automatically yield a mechanism for third parties to access private keys. This case, therefore, tests whether legal systems can bridge the gap between public address records and the cryptographic controls that govern ownership in practice.

For readers tracking regulation and legal precedent in crypto, the important development is not only who named which addresses, but how courts handle the mismatch between legal concepts like “found property” and the blockchain reality that addresses are public labels—while control is determined privately.

As the New York case progresses, the key questions to watch are whether the court agrees that addresses cannot be sued as entities, and—if the case survives procedural challenges—what standard it may apply to abandonment and recoverability when private keys are necessary to access any funds.

Netflix Streaming Hit Is Every Man’s Worst Nightmare

Hot dog eating champs seek to repeat in Nathan’s Famous contest

Bristol Myers Squibb: Pain First, Payoff Later?

-

Tech6 days ago

Tech6 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Tech6 days ago

Tech6 days agoClaude Code turned every engineer into three. Now companies need more product thinkers

-

Fashion10 hours ago

Fashion10 hours agoWeekend Open Thread: High Hopes

-

Crypto World4 days ago

Crypto World4 days agoStrategy authorizes up to $1.25B in Bitcoin sales under new capital plan

-

Politics17 hours ago

Politics17 hours agoThe House | “Reframing the debate from a binary discussion of winners and losers”: Yuan Yang reviews ‘We Are Not Machines’

-

News Videos5 days ago

News Videos5 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Tech4 days ago

Tech4 days agoAnonymous researcher drops 0-day ‘exploitarium’ repo

-

Crypto World7 days ago

Crypto World7 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business4 days ago

Business4 days agoAustralia treasurer says alleged access of prime minister’s bank data ’incredibly concerning’

-

Crypto World7 days ago

Crypto World7 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Tech7 days ago

Tech7 days agoRussian hackers now target Signal backup recovery keys

-

Business4 days ago

Business4 days agoThe AI boom won’t burst all at once. It will pop in ‘rolling bubbles’: Macquarie

-

Sports3 days ago

Sports3 days agoBroncos roster: OL Ben Powers (No. 74) entering final year of contract

-

NewsBeat3 days ago

NewsBeat3 days agoPresenter Caroline Flack’s brother Paul Flack dies aged 55

-

Tech6 days ago

Tech6 days agoSilicon Valley paid to kill AI regulation, now it wants the rules back

-

Crypto World2 days ago

Crypto World2 days agoBinance stock trading tops $1B in first month after launch

-

Tech7 days ago

Tech7 days agoOpenAI mulls delaying IPO over valuation concerns

-

Crypto World2 days ago

Crypto World2 days agoAlibaba-affiliate Ant Group enters the humanoid robot market with 12 deals

-

NewsBeat2 days ago

NewsBeat2 days agoNew exhibition reflects five decades of movement between island of Ireland and GB

-

News Videos4 days ago

News Videos4 days agoHow to Build INSANE Live Financial Dashboards With Claude

You must be logged in to post a comment Login