Crypto World

Most of Ripple’s bank partners never touch XRP. Here is the real problem

Ripple says it has more than 300 institutional partners. The XRP community hears that as 300 banks buying XRP. The reality is that most of them use Ripple’s software without ever touching the token, and even the ones that do rarely hold it. This is the structural gap at the heart of why XRP’s price stays stuck while Ripple keeps winning.

Summary

- Ripple has more than 300 institutional partners, but roughly 60 percent use its messaging and software rails without ever touching XRP, while only about 40 percent use the On-Demand Liquidity product that involves the token.

- Even the partners that use On-Demand Liquidity generally do not hold XRP, because licensed exchanges and market makers handle the buying and selling, and the banks see only fiat in and fiat out.

- This split is the mechanical explanation for the long-standing gap between Ripple’s corporate success and XRP’s stuck price, since network adoption does not automatically translate into sustained token demand.

- The bullish rebuttal is that On-Demand Liquidity volume is real where it runs, that even momentary XRP demand creates buy pressure, and that token demand can come from ETF flows and regulation independent of settlement.

- For holders, the honest read is that partner counts measure Ripple’s business, not XRP demand, and the token’s fate depends on whether the On-Demand Liquidity share grows and its volume scales, plus channels like ETFs and regulatory clarity.

Ripple likes to say it has more than three hundred institutional partners, and the number sounds like exactly the validation XRP holders have waited years to see: hundreds of banks and payment companies, all signed up to Ripple, all presumably driving demand for the token. That is how the figure is usually heard in the community, as three hundred institutions buying and using XRP. The reality is very different, and confronting it honestly is essential for anyone who holds the token.

The large majority of Ripple’s partners use the company’s messaging and payment software without ever touching XRP, and even among the minority that use the product built around the token, almost none actually hold XRP. The partner count measures the size of Ripple’s business, not the demand for its associated asset, and the gap between those two things is the single best explanation for one of the most frustrating puzzles in crypto: why XRP’s price has stayed pinned near a dollar through 2026 even as Ripple racks up settlement deals, bank partnerships, and institutional wins.

This is not an argument that Ripple is failing or that XRP is worthless. It is an argument that the popular story, in which corporate adoption mechanically pulls the token price up with it, rests on a misunderstanding of how Ripple’s products actually work. There are really two Ripples: one that sells messaging and payment software to banks, which does not require XRP, and one that offers a liquidity service that uses XRP as a bridge, which does. Most partners signed up for the first. Understanding that split, and what it means for whether Ripple’s success ever reaches the token, is the purpose of this piece.

It covers the two different products Ripple sells, why even the token-using product rarely puts XRP on a bank’s balance sheet, the value-accrual problem this creates, the genuine bull-case rebuttal, the geographic concentration of the volume that does exist, and what would actually have to change for Ripple’s growth to start pulling XRP demand with it. The goal is to give holders an accurate map of where the token stands in Ripple’s empire, rather than the flattering version the partner count implies.

There are two different Ripples

The root of the confusion is that Ripple sells more than one thing, and only some of what it sells involves XRP. For most of its history, Ripple’s core enterprise offering has had two distinct components. The first is messaging and payment-connectivity software, historically associated with products that let banks send payment instructions and connect to one another more efficiently than the old correspondent system allows.

This software improves how banks communicate and process cross-border payments, but it does not require XRP at all; a bank can adopt it, become a Ripple partner, and never go near the token. The second component is On-Demand Liquidity, or ODL, the service that actually uses XRP as a bridge asset to move value between currencies without pre-funded accounts. ODL is the part of Ripple’s business that creates real XRP usage.

The crucial fact is how Ripple’s partners split between these two. By most accounts, only around forty percent of Ripple’s roughly three hundred partners use On-Demand Liquidity, the XRP-based product, while the other sixty percent or so use the messaging and software rails that do not touch XRP at all. So when the community hears three hundred partners and pictures three hundred sources of XRP demand, the accurate picture is closer to a bit more than a hundred partners using the token-based product, and a larger group using Ripple software that bypasses XRP entirely.

This is not hidden or scandalous; it simply reflects that many institutions wanted Ripple’s payments technology without taking on a volatile crypto asset. But it has enormous implications for the token, because it means the headline partner count overstates XRP demand by a wide margin. A bank can be a proud, public Ripple partner and contribute precisely nothing to XRP usage, and many are exactly that. The first step to understanding XRP’s stuck price is to stop counting all of Ripple’s partners as XRP customers, because most of them are not.

Even ODL partners do not hold XRP

It would be natural to assume that the forty percent of partners using On-Demand Liquidity are therefore buying and holding XRP, generating steady demand, but even that is largely not the case, and the reason cuts to the core of the value-accrual problem. The way ODL works, banks do not generally buy or hold XRP themselves. Instead, licensed exchanges and liquidity providers sit in the middle of the transaction.

When a bank uses ODL to send value across a corridor, the source currency is converted into XRP, the XRP moves across the ledger in seconds, and it is converted into the destination currency on the other side, but this buying and selling is handled by market makers and exchanges, not by the bank. From the bank’s perspective, it puts fiat in on one side and receives fiat out on the other, never holding the token in between. The XRP is touched only momentarily, by the liquidity providers facilitating the swap, before it is converted back.

This structure is deliberate and is actually part of ODL’s appeal to institutions: it lets banks access the speed and capital efficiency of XRP-based settlement while staying in their regulatory comfort zone, seeing only fiat on their books and never holding a volatile crypto asset. For the banks, that is a feature.

For XRP holders hoping that institutional adoption means institutions accumulating XRP, it is a disappointment, because it means even the token-using corner of Ripple’s business does not create the kind of sustained, buy-and-hold demand that would steadily lift the price. The demand ODL creates is real but fleeting: XRP is bought and sold in the same moment to bridge a payment, generating transactional throughput rather than lasting accumulation.

The momentary buying does create some genuine buy pressure, which the bull case rightly emphasizes, but it is a different and weaker force than the image of banks adding XRP to their reserves. So the picture sharpens: most partners do not touch XRP, and most of those that do touch it only in passing, through intermediaries, without ever holding it.

The value-accrual problem this creates

Put these facts together and you arrive at the deepest issue in the entire XRP story, the one that explains the stuck price more convincingly than any other: the problem of how value accrues to the token. A blockchain network, or in this case a payments business built around a token, can grow impressively while the token itself fails to capture that growth, if the activity does not translate into sustained demand for the asset.

That is precisely the situation the two-Ripples split creates. Ripple the company can keep signing partners, opening corridors, and processing more payments, and most of that growth flows through software that bypasses XRP or through an ODL process that touches XRP only momentarily via intermediaries. The corporate success is real, but the channel connecting it to token demand is far narrower than the partner count suggests.

This is the mechanical explanation for the puzzle that has frustrated XRP holders all year: Ripple keeps winning, and XRP keeps trading near a dollar beneath its major moving averages. The wins are concentrated in parts of the business that do not require holding the token, so they do not generate the buy-and-hold demand that would lift the price.

Layered on top is XRP’s large supply, including the enormous quantity Ripple holds in escrow and periodically releases, which means that even meaningful transactional demand must contend with substantial available supply. For demand to overwhelm that supply and move the price durably, the token would need usage on a scale that the current adoption pattern, heavy on XRP-free software and light on XRP accumulation, does not produce.

None of this means XRP cannot rise; it means the path from Ripple’s business growth to XRP’s price is not the automatic, mechanical link the bullish narrative assumes. The token does not appreciate simply because Ripple succeeds. It would appreciate if usage of the specific XRP-based product grew large enough that the momentary demand it generates, compounded across enormous volume, finally outweighed the supply. That is a much higher bar than signing the three-hundredth partner.

The escrow overhang that makes it worse

There is a supply-side dimension to the value-accrual problem that deserves its own attention, because it raises the bar that token demand must clear. A very large quantity of XRP sits in escrow controlled by Ripple, released into the market on a schedule over time, and this steady stream of new available supply is a structural feature of the token that has no equivalent in a fixed-supply asset. Whatever demand the network generates, whether the momentary buying of On-Demand Liquidity or the buy-and-hold demand of ETFs, must contend not only with the XRP already circulating but with the additional supply that periodically enters from escrow. This is part of why even real demand has struggled to move the price durably: it is pushing against a supply that keeps replenishing.

The interaction between the demand pattern and the supply schedule is the crux. If the token-using share of Ripple’s business were large and growing fast, the transactional demand it generates might comfortably absorb the escrow releases and then some, letting the price rise. But because most of Ripple’s activity bypasses the token, and the part that uses it does so only momentarily through intermediaries, the demand side has been too thin to overwhelm the supply side decisively. The result is a token that can trade sideways even during periods of corporate success, because the modest, fleeting demand from settlement is roughly matched by available and incoming supply.

Critics of Ripple have long pointed to the escrow releases as a persistent headwind, while the company argues the releases are managed responsibly and that it has an incentive not to suppress its own largest holding. Either way, the practical point for holders is that the value-accrual gap is not only about weak demand capture; it is about weak demand capture meeting a large and replenishing supply, which together explain why the price has been so resistant to the steady drumbeat of adoption headlines. For the token to break higher durably, demand would need to grow enough to clear both the circulating float and the escrow overhang at once, which is a higher bar than demand alone.

The bull case deserves a fair hearing

The picture so far is sobering, but the bullish rebuttal is substantive and deserves a fair hearing, because the situation is not as one-sided as the skeptical read alone implies. The first point in XRP’s favor is that the momentary demand ODL creates is still real demand. Every time the XRP-based product bridges a payment, XRP is genuinely bought, even if it is sold moments later, and at sufficient volume that continuous buying and selling represents real, ongoing market activity rather than nothing.

If the corridors using ODL grow and the volume flowing through them scales up, the cumulative buy pressure from all that bridging could become a meaningful force, particularly because it recurs constantly instead of being a one-time event. The bull case holds that the token-touching share of Ripple’s business is the part that matters, and that as it grows, so does the demand that flows through XRP.

The second point is that the forty percent is not fixed. Partners that adopted Ripple’s messaging software first can later convert to On-Demand Liquidity, and Ripple has every incentive to push that conversion, since it is the largest holder of XRP and benefits directly when XRP usage rises. If a meaningful share of the messaging-only majority converts to the XRP-based product over time, the demand base expands substantially.

The third and perhaps strongest point is that settlement throughput is not the only channel to XRP demand. The forces most capable of moving XRP, the institutional flows into spot ETFs and the regulatory clarity that the CLARITY Act would provide, operate largely independent of whether banks hold XRP in their settlement flows. ETF demand is buy-and-hold demand of exactly the kind ODL does not generate, and it has already drawn over a billion dollars into XRP funds.

Tokenized real-world assets settling on the XRP Ledger represent another growing source of activity. So the bull case is that the partner-count critique, while accurate about settlement mechanics, misses the channels, ETFs and regulation, that could drive XRP regardless of how banks handle their payment corridors. These are genuine counterpoints, and an honest holder should weigh them against the structural concern instead of dismissing either.

The geographic reality nobody mentions

A further dimension that rarely makes it into the bull-or-bear debate is where Ripple’s XRP-based volume actually flows, and it complicates the global-rail narrative in an important way. On-Demand Liquidity has been live in production for years, but its real usage has been concentrated in specific cross-border corridors instead of spread evenly across global finance.

The meaningful volume has historically clustered in particular regions, such as certain Middle East and Southeast Asia corridors, and more recently in Latin American routes involving institutions like Braza Bank and Mexican corridors involving Bitso. These are real flows with real value, and the busiest names on the XRP Ledger include identifiable financial institutions instead of anonymous wallets, which is a genuine point in the network’s favor. But the volume is geographically concentrated, not the worldwide banking rail the headline narrative implies.

This concentration matters for two reasons. First, it means XRP’s settlement demand depends heavily on a relatively small set of corridors, so the token’s utility-driven demand is less diversified and more exposed to the fortunes of those specific routes than a global-rail framing would suggest. Second, in the corridors where institutional settlement does happen on-chain, XRP increasingly competes for share against alternatives, including dollar stablecoins like USDC and Ripple’s own RLUSD, as well as emerging central-bank digital-currency projects, according to blockchain-analytics observations.

So even within the settlement niche where XRP is used, it is not unchallenged; it is one option competing for institutional flow against instruments that offer dollar stability. The honest synthesis is that XRP’s real settlement footprint is meaningful but concentrated and contested, which is a more accurate and more modest picture than the image of a token quietly powering the world’s bank transfers. For holders, this is another reason to track the actual volume in the actual corridors instead of the partner count or the global ambition.

What would actually change the picture

If the partner count is the wrong thing to watch, the natural question is what the right things are, and identifying them gives holders a far better framework than counting Ripple’s deals. The first and most direct change would be conversion: the messaging-only majority of partners moving onto On-Demand Liquidity, which would expand the share of Ripple’s business that actually uses XRP.

Watching whether the roughly forty percent figure grows over time is more informative than watching the total partner number rise, because growth in the token-using share is what expands XRP demand. The second is volume: even within the existing ODL base, the total value flowing through XRP-bridged corridors is what generates the cumulative buy pressure, so rising corridor volume matters more than new logos. A handful of high-volume corridors can move more XRP than dozens of low-volume partnerships.

Beyond settlement, the channels most likely to drive durable XRP demand are the ones that operate independent of how banks handle payments. Spot ETF flows are the clearest, because they represent genuine buy-and-hold demand, and their trajectory, whether they compound or stall, will say more about XRP’s institutional demand than any partner announcement. Regulatory clarity from the CLARITY Act is the second, because codifying XRP’s status could unlock institutional capital that settlement adoption alone never reaches. The growth of tokenized real-world assets on the XRP Ledger is a third, since it brings a different kind of activity and demand to the network.

The honest framework for a holder is therefore to stop treating Ripple’s partner count and corporate wins as proxies for XRP demand, because most of that activity bypasses or only momentarily touches the token, and to focus instead on the metrics that actually connect to demand: the ODL share and its volume, ETF flows, regulatory progress, and on-chain asset growth. The partner count tells you Ripple is a successful company. It tells you very little about whether XRP, the token, is capturing that success, which is the only question that matters for the price.

Frequently Asked Questions

Do banks that partner with Ripple actually use XRP?

Mostly not. Ripple has more than three hundred institutional partners, but only around forty percent use On-Demand Liquidity, the product that involves XRP as a bridge asset. The other sixty percent or so use Ripple’s messaging and payment software, which does not touch XRP at all. So a large majority of Ripple’s partners can be active customers without ever using the token. This is the key reason the partner count overstates XRP demand: many partners signed up for Ripple’s payments technology specifically without taking on a volatile crypto asset, and they contribute nothing to XRP usage despite being counted as partners.

If a bank uses On-Demand Liquidity, does it hold XRP?

Generally no, and this surprises many people. In On-Demand Liquidity, banks do not buy or hold XRP themselves. Licensed exchanges and liquidity providers handle the conversion: the source currency becomes XRP, the XRP moves across the ledger in seconds, and it is converted to the destination currency, all managed by market makers. The bank sees only fiat in and fiat out, never holding the token. This is deliberate, letting banks access XRP-based settlement speed while staying in their regulatory comfort zone. The result is that even the token-using part of Ripple’s business creates only momentary, transactional XRP demand instead of the buy-and-hold accumulation that would steadily lift the price.

Why does XRP’s price stay stuck if Ripple is so successful?

Because most of Ripple’s success flows through channels that bypass the token or touch it only momentarily. The majority of partners use XRP-free software, and even On-Demand Liquidity touches XRP only in passing through intermediaries, so Ripple’s corporate growth does not mechanically translate into sustained XRP demand. Add XRP’s large supply, including the escrow Ripple periodically releases, and transactional demand has to be very large to move the price durably. This value-accrual gap, between a thriving business and a token that does not capture its success, is the clearest explanation for why XRP has stayed near a dollar through 2026 even as Ripple keeps winning deals.

Is this a reason to be bearish on XRP?

Not necessarily, but it is a reason to be realistic about what drives the token. The structural critique shows that partner counts and corporate wins are poor proxies for XRP demand. But the bull case has real merit: On-Demand Liquidity volume is genuine demand where it runs, the token-using share of partners can grow as banks convert from messaging to liquidity, and the strongest demand channels, spot ETF inflows and regulatory clarity from the CLARITY Act, operate independent of bank settlement entirely. So the picture is not simply bearish; it is that XRP’s demand depends on specific things, the growth of On-Demand Liquidity volume and the independent channels of ETFs and regulation, instead of on Ripple’s overall business success.

Where is XRP actually used for settlement?

On-Demand Liquidity volume has historically been concentrated in specific cross-border corridors instead of spread across global banking. Meaningful usage has clustered in certain Middle East and Southeast Asia routes and, more recently, Latin American corridors involving institutions such as Braza Bank and Mexican routes involving Bitso. These are real flows, and the busiest names on the XRP Ledger are identifiable financial institutions. But the volume is geographically concentrated, not the worldwide rail the narrative implies, and within those corridors XRP competes for share against dollar stablecoins like USDC and Ripple’s own RLUSD. So XRP’s settlement footprint is meaningful but concentrated and contested instead of dominant.

What should XRP holders watch instead of the partner count?

Focus on the metrics that actually connect to token demand. The most direct is the share of partners using On-Demand Liquidity, currently around forty percent; whether that grows matters more than the total partner number. The second is the volume flowing through XRP-bridged corridors, since cumulative throughput is what generates buy pressure. Beyond settlement, watch spot ETF flows, which represent true buy-and-hold demand, regulatory progress on the CLARITY Act, which could unlock institutional capital, and the growth of tokenized assets on the XRP Ledger. These tell you whether XRP the token is capturing demand, which the partner count does not, because most partners never touch XRP.

This article is information, not investment advice. Figures on Ripple’s partners, On-Demand Liquidity usage, and corridor volumes reflect reporting and estimates available as of June 27, 2026, and can change. The relationship between Ripple’s business and XRP demand is a debated topic. Nothing here is a recommendation to buy or sell XRP or any asset. Verify current details from primary sources and consider your own circumstances before making any decision.

Key Takeaways

- Solana is currently testing a critical demand zone between $65 and $71 after retreating to $71.37.

- Over 60 million SOL tokens were transacted within the $65–$71 range, establishing it as a significant support area.

- Failure to maintain $70 could trigger declines toward $64, followed by $53.10, based on URPD analysis.

- Technical indicators show RSI at 51.60 with a bullish MACD crossover, hinting at potential momentum shifts.

- World Xyz, a Solana-based project, officially launched, injecting renewed enthusiasm into the community.

Solana’s price has retreated to $71.37 in the last 24 hours. This decline mirrors Bitcoin’s broader market correction that affected most cryptocurrencies.

Blockchain data reveals that over 60 million SOL tokens were traded between the $65 and $71 price levels. This concentration of activity establishes this range as a formidable nearby support area.

When significant supply clusters form within a specific price band, they typically function as a buffer during market downturns. Numerous investors established their positions within this zone and may actively defend these levels.

Should SOL maintain support above $70, the asset could enter a consolidation phase. Subsequently, it might challenge the resistance barrier near $73.

A breach below $70 would alter the technical outlook significantly. Market participants would then monitor for potential movement toward the $64 level, according to recent technical assessments.

Critical Support Zones Under Watch

Should the $64 level give way, additional support areas exist at $53.10, $23.60, and $8.85. The $53.10 zone carries particular significance for near-term price action, with approximately 7 million SOL having changed hands at that level.

The present downturn isn’t driven by Solana-specific factors. Bitcoin declined 1.43% during the same timeframe, while overall cryptocurrency market capitalization contracted 1.18%.

This correlation demonstrates that Solana continues exhibiting high-beta characteristics. When Bitcoin experiences selling pressure, alternative cryptocurrencies typically amplify those movements.

The Fear and Greed Index currently registers 16, reflecting prevailing market caution. SOL is positioned beneath its 30-day EMA around $72.48.

The daily RSI indicator hovers near 34.83, indicating subdued momentum. While MACD remains in negative territory, the histogram displays marginal improvement.

Alternative technical analysis presents a more optimistic scenario. RSI has advanced to 51.60, with the signal line at 45.95, while the MACD line exhibits a bullish crossover with a histogram reading of 0.68730.

These technical signals indicate potential easing of downward pressure. Validation would require increased trading activity and decisive closes above resistance thresholds.

Project Developments and Market Commentary

The enigmatic Solana initiative World Xyz has officially unveiled itself following extended speculation. The project previously acquired the world.xyz domain for $80,000.

Vibhu from the Solana Foundation characterized World as an agentic, intent-focused settlement infrastructure constructed on the x402 protocol. The platform functions as a decentralized framework for tokenizing tangible assets.

Following this revelation, SOL’s price appreciated 2.86% over 24 hours. Market analyst 0xNeena indicated that losing the $65–$75 support corridor would leave SOL vulnerable to further declines toward the $50–$55 range.

On X, analyst Sjuul from AltCryptoGems observed that SOL “has been showing some strength on lower time frames” while noting that “on higher time frames it is still in trouble.” Sjuul emphasized that meaningful recovery requires SOL to recapture the $78 threshold.

Solana’s trading volume allegedly surged over 3,200% during Q2, hitting $67 billion. Memecoin trading, staking protocols, and diverse applications contributed to this substantial growth.

Solana ETF flow data indicated $5.8 million in net outflows throughout June. A $15 million short position has sparked discussion regarding whether the current correction might intensify.

CryptoPatel identified an extended support corridor between $40 and $60, projecting ambitious long-term targets at $500 and $1,000 should SOL reclaim higher resistance zones eventually. Analyst Ardi suggested one final capitulation below present levels remains plausible before any substantial recovery materializes.

CFTC has opened a wide ranging investigation into Polymarket’s business activities, including its social media operations, according to new reports.

Summary

- The CFTC has opened a broad investigation into Polymarket covering its business activities and social media operations.

- The inquiry follows reports that Polymarket used fake trading videos and undisclosed influencer promotions to attract users.

- The investigation comes as Polymarket works to restore access to the U.S. market while facing renewed regulatory scrutiny.

According to Bloomberg, the Commodity Futures Trading Commission is conducting an extensive investigation into prediction market platform Polymarket that covers multiple parts of its business, including its social media activities.

The report follows a Wall Street Journal investigation published last week that alleged Polymarket hired dozens of mostly college-aged content creators to post fake trading videos designed to attract new users. Bloomberg reported that the CFTC inquiry extends beyond those marketing practices into other aspects of the company’s operations.

CNBC has separately reported, citing a person familiar with the matter, that the investigation remains active, although the source did not disclose when it began.

Both the CFTC and Polymarket have yet to issue an official statement regarding the matter.

Investigation follows scrutiny over promotional campaign

The Wall Street Journal has also alleged that Polymarket used replica versions of its trading platform to create promotional videos showing fabricated bets and winnings.

According to the newspaper, it reviewed 1,105 videos posted between December 2025 and mid-May and found that about 70% contained simulated trades rather than real market activity. The report said the campaign displayed roughly $1.9 million in fake bets, including nearly $900,000 in fabricated winnings that would instead have resulted in losses if placed on the live platform.

Further, it alleged that creators were paid about $2,000 to $3,000 per month through marketing contractor Virality and were instructed not to disclose the sponsorships. Analytics firm Tubular, separately, estimated the videos generated more than 140 million views across TikTok, YouTube, and Instagram.

Responding to those allegations, Polymarket told CNBC it is conducting a comprehensive audit of its active promotional content to ensure it complies with company standards as well as regulatory and legal disclosure requirements.

Questions over U.S. access continue

Bloomberg reported that the CFTC previously closed, alongside the U.S. Department of Justice, an investigation into whether Polymarket violated restrictions on U.S. users without filing charges last year.

The company has barred Americans from its main platform since reaching a settlement with the regulator in 2022, although the report noted that some users continue accessing the service through virtual private networks.

The company has also been working to restore access to the U.S. market. As crypto.news has previously covered, Polymarket launched a CFTC-regulated U.S. exchange in December.

In the meantime, Senators Adam Schiff and John Curtis asked CFTC Chair Michael Selig last week to confirm whether the agency had opened an investigation into Polymarket’s advertising practices and to explain how it has prevented the platform from attracting U.S. users since the 2022 settlement.

According to their letter, the senators also questioned whether the agency has sufficient oversight tools to supervise prediction markets and requested details on advertising standards, influencer disclosure rules, consumer safeguards and age verification requirements.

The current inquiry would be the first major investigation into an event contract platform under CFTC Chair Michael Selig, whose tenure has generally been viewed as supportive of prediction markets.

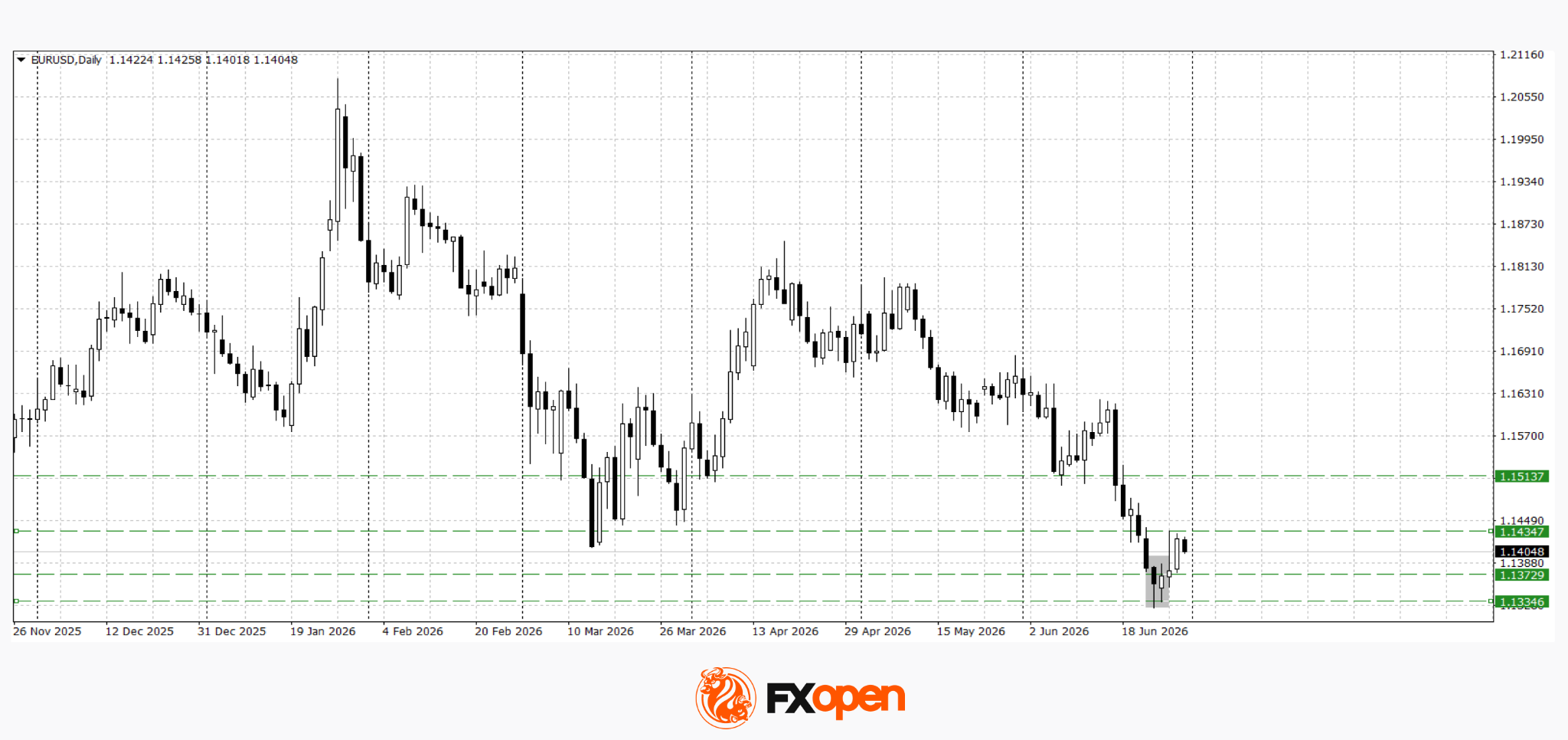

Following the US dollar’s notable strength last week, European currencies have entered a period of consolidation. Investors and market participants have temporarily reduced trading activity ahead of a series of key macroeconomic releases from the euro area, the UK and the US, which could determine the next direction for EUR/USD and GBP/USD. At the same time, markets continue to monitor developments in the Middle East, as easing geopolitical tensions have somewhat reduced demand for safe-haven assets, allowing investors to shift their focus back to economic fundamentals.

Investor sentiment has also been supported by reports suggesting that the US and Iran may be close to reaching an agreement to halt mutual strikes and resume negotiations. The restoration of shipping through the Strait of Hormuz has reduced concerns over disruptions to global oil supplies and contributed to greater stability across financial markets. Nevertheless, ongoing disagreements over the situation in the Strait of Hormuz and conflicting statements from Iranian officials indicate that geopolitical risks have not yet fully subsided.

EUR/USD

Following a test of the March low, a bullish Piercing Line candlestick pattern formed on the daily timeframe. Technical analysis suggests that EUR/USD is trading within a sideways range between 1.1340 and 1.1430. Price action around these boundaries, together with the incoming macroeconomic data, should provide further clues regarding the pair’s next directional move.

Key events for EUR/USD:

- Today at 09:45 (GMT+3): France CPI.

- Today at 15:00 (GMT+3): Germany CPI.

- Today at 17:00 (GMT+3): US JOLTS Job Openings.

GBP/USD

After testing this year’s March low at 1.3160, sterling buyers regained the initiative and formed a bullish Piercing Line candlestick pattern. The pair has since rebounded towards 1.3270, although any further upside is likely to depend on incoming macroeconomic data. Technical analysis suggests the pair may retest the 1.3270 level. A decisive break and close above this resistance could pave the way for further gains towards 1.3300–1.3310, while rejection from current resistance may trigger a decline back towards the 1.3140–1.3160 area.

Key events for GBP/USD:

- Today at 09:00 (GMT+3): UK GDP.

- Today at 13:40 (GMT+3): Speech by Bank of England Financial Policy Committee member Sarah Breeden.

- Today at 17:00 (GMT+3): US CB Consumer Confidence Index.

Following the sharp moves seen in recent sessions, the foreign exchange market has entered a wait-and-see mode. The release of key economic data on both sides of the Atlantic is likely to determine whether the current consolidation becomes the starting point for a recovery in European currencies or gives way to a renewed strengthening of the US dollar.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

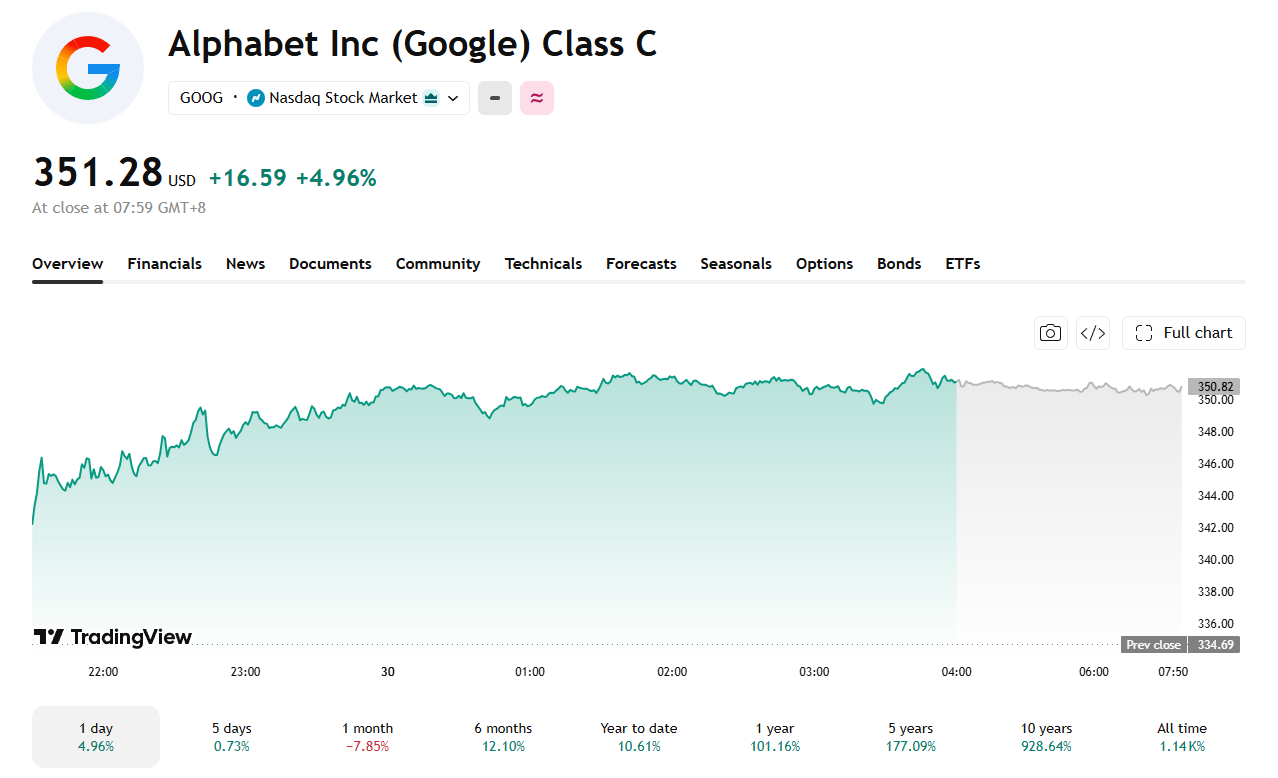

The Dow Jones Industrial Average (DJIA) closed above 52,000 for the first time on Monday, June 29, powered by Alphabet’s blue-chip debut and a broad rally in semiconductor stocks.

The index gained 306.63 points, or 0.59%, to finish at 52,182.74. The S&P 500 rose 1.18% to 7,440.43, and the Nasdaq Composite surged 2.07% to 25,820.14.

Alphabet’s Dow Debut Lifts Sentiment

Alphabet (GOOGL) climbed nearly 5% on its first session as a Dow member after replacing Verizon in the index. The addition carries more symbolic weight than mechanical impact, as the stock already sits in the S&P 500 and Nasdaq 100, limiting forced fund buying from the change.

Despite Monday’s pop, Alphabet is still on pace for its worst month since February of last year, with six of the past seven weeks ending in negative territory. Investor concerns center on AI execution, with Nvidia chip stock flows drawing renewed attention across the sector as compute access tightens.

Semis and Geopolitics Drive the Broader Move

The VanEck Semiconductor ETF gained more than 3%, led by Astera Labs, KLA, and Applied Materials, which rose roughly 16%, 12%, and 11%, respectively.

Macro relief also played a role. The US and Iran agreed to pause hostilities and allow commercial vessels to transit the Strait of Hormuz freely.

Brent and West Texas Intermediate climbed slightly, as traders weighed whether the ceasefire would hold. BeInCrypto previously covered how Iran’s oil ceasefire deals move crude and downstream inflation expectations.

Whether the rally extends into a shortened week ahead of the July 4 holiday will depend on whether the Iran ceasefire holds and if semiconductor momentum carries through.

The post Dow Closes Above 52,000 for First Time as Alphabet Debuts appeared first on BeInCrypto.

U.S. spot bitcoin ETFs lost a net $231 million on Monday, with BlackRock’s IBIT accounting for $300 million of outflows that other funds partly offset, including $50 million into ARKB and $35 million into GBTC, per SoSoValue data.

The outflow lands as risk appetite elsewhere is surging. Wall Street’s technology rally spread into Asia on Tuesday, with the MSCI Asia Pacific index up 1% on the year’s final trading day after a semiconductor rebound helped the S&P 500 snap a five-session losing streak. The Asian benchmark is on track for its biggest quarterly gain in almost 17 years.

South Korea’s Kospi, which crashed 10% in a single session earlier this month, climbed 2.1% to extend its lead as the world’s best-performing major benchmark this year. Samsung is up more than 100% this quarter, and SK Hynix has gained almost 240% since April. The yen slid to its weakest level against the dollar since 1986, a sign investors are funding the AI trade by borrowing in yen.

Bitcoin ETFs are not participating in that capital rotation, however. The same AI infrastructure spending fueling record quarters in Seoul and Tokyo is the trade competing for the dollars that might otherwise flow into bitcoin, a dynamic that has run through the month’s coverage of SpaceX, Anthropic and the chip sector.

Key Highlights

- BitMine acquired 27,084 ETH in the past week, marking its fourth-smallest weekly accumulation this year, pushing total reserves to 5.7 million ETH.

- US-based spot Ethereum ETFs experienced their seventh consecutive week of net redemptions, shedding $273.3 million in the steepest weekly decline since January.

- Sharplink re-entered the market after an eight-month hiatus, acquiring 39,196 ETH valued at $62.4 million across three consecutive days.

- Ethereum has declined approximately 50% year-to-date and approaches the possibility of recording three consecutive quarterly losses.

- Derivatives markets reveal $4.09 billion in short positions compared to $1.31 billion in long positions, highlighting prevailing bearish sentiment among traders.

Ethereum’s market value hovers around $1,580 as the blockchain network contends with diminishing corporate accumulation and persistent outflows from investment vehicles. The cryptocurrency has found it difficult to maintain critical price thresholds throughout June.

BitMine Immersion, holding the distinction of being the largest institutional ETH holder, acquired 27,084 ETH during the previous week. This transaction elevated the company’s aggregate holdings to 5.7 million ETH, representing approximately $9.22 billion in value. The purchase volume represents one of the company’s most modest weekly acquisitions this year.

Simultaneously, BitMine allocated 160,480 ETH to its staking infrastructure. The firm’s staked portfolio now encompasses 4.879 million ETH, producing approximately $211 million in annual staking rewards.

BitMine Chairman Thomas Lee attributed the reduced acquisition pace to end-of-quarter “window dressing” activities. He observed that market participants frequently reduce exposure to underperforming assets during quarterly closings, regardless of positive fundamental developments.

Investment Fund Redemptions Accelerate

US spot Ethereum exchange-traded funds registered their seventh straight week of negative net flows. These investment vehicles experienced redemptions totaling $273.3 million over the past week, representing the most substantial weekly decline since January, based on SoSoValue tracking data.

BlackRock’s iShares Ethereum Trust experienced the largest redemptions among ETF providers. The trend demonstrates retail and institutional fund investors reducing allocations while certain corporate treasuries maintain their accumulation strategies.

This divergence has generated an atypical market dynamic. Corporate balance sheet strategies continued adding ETH exposure while traditional fund investors redirected capital to alternative investments.

Sharplink, another prominent institutional ETH holder, re-initiated purchases following an eight-month dormant period. Blockchain analytics from Lookonchain documented the company’s acquisition of 39,196 ETH valued at $62.4 million through three separate transactions during the previous week.

Arkham Intelligence data identified the initial purchase batch through FalconX on Thursday. Sharplink executed additional transactions on Friday, complemented by substantial over-the-counter trades throughout the weekend.

As of June 21, Sharplink maintained holdings of 876,285 ETH, establishing its position as the second-largest public corporate ETH holder after BitMine. The company has not publicly addressed the rationale behind resuming its accumulation strategy.

Quarter-End Performance and Derivatives Market Positioning

Ethereum has experienced a decline approaching 50% since the beginning of January. This downturn temporarily allowed Tether’s USDt stablecoin to surpass ETH in overall market capitalization during the past week.

Cryptocurrency analyst Max Crypto highlighted in a social media post that ETH approaches the possibility of recording three consecutive quarterly losses for the first time in its history. He characterized this pattern as a structural concern extending beyond temporary price volatility, prompting market observers to monitor whether the asset can prevent a fourth consecutive negative quarter.

Derivatives market information from CW indicated that high-leverage short positions on ETH totaled $4.09 billion. Long positions registered $1.31 billion on the identical platform, suggesting that speculative traders anticipate continued downward price movement.

From a technical perspective, ETH trades beneath its 20-day, 50-day, and 100-day Exponential Moving Averages, which range between $1,670 and $2,004. The Relative Strength Index currently registers 35, while the Stochastic indicator stands at 26, both metrics indicating persistent downward momentum with minimal signals of reversal.

Market analyst Daan Crypto Trades remarked on social platform X that Ethereum has been unable to successfully recapture previous support zones. He indicated that a recovery above $1,750 would represent the initial indication of bullish strength on extended timeframes, whereas a breach below the current $1,500 support level, which has provided a floor on two prior occasions, could trigger a decline toward April 2025 price lows.

Near-term resistance levels for ETH are positioned at $1,626, followed by additional barriers at $1,670 and $1,741. Support zones are established near $1,524, with a secondary support foundation at $1,404.

Key Takeaways

- XRP currently hovers around $1.05, maintaining stability above the critical $1 threshold following a June 25 dip to $1.01—the lowest level in 19 months.

- Tokens flowing out of exchanges increased dramatically, jumping from 40.7 million to approximately 123 million XRP within days, suggesting potential accumulation by holders.

- Spot XRP ETFs recorded their eighth consecutive week of positive inflows, bringing total cumulative inflows to approximately $1.47 billion.

- Network engagement surged with daily active addresses climbing 72% over a two-week period, moving from 23,000 to nearly 39,500.

- Derivatives open interest contracted sharply from 1.3 billion to under 150 million, indicating a significant deleveraging event.

XRP maintains its position around the $1.05 level following a challenging June performance. The digital asset touched approximately $1.01 on June 25, marking its lowest valuation in 19 months, yet purchasing pressure has successfully defended the psychologically important $1.00 threshold in subsequent trading sessions.

While price action has remained subdued, the underlying XRP Ledger has demonstrated notable vitality. The blockchain recorded 4,941 newly created wallets within a 24-hour window, representing the most significant single-day expansion in wallet creation observed over the past three months.

Concurrently, daily active addresses have experienced substantial growth. The metric expanded from approximately 23,000 on June 14 to nearly 39,500 by June 27, reflecting a 72% increase within a fortnight.

Token Movement and Institutional Capital Flow

Blockchain analytics reveal an accelerating trend of tokens being withdrawn from centralized exchanges. The exchange net position change metric shifted from roughly 40.7 million XRP on June 22 to approximately 123 million XRP several days afterward, representing an increase of nearly 200%.

Such withdrawal patterns typically indicate that holders are moving assets into self-custody rather than positioning for immediate sales. Meanwhile, institutional appetite for XRP exposure continues unabated.

Spot XRP exchange-traded funds have maintained positive net inflows for eight consecutive weeks. Total cumulative inflows now approach $1.47 billion, with an additional $22.99 million recorded during the week ending June 26.

Notably, on June 26, XRP-focused ETFs attracted $15.6 million in capital while bitcoin-based products experienced $444.5 million in withdrawals and ethereum funds recorded $12.9 million in outflows.

The derivatives market has undergone significant consolidation. Open interest across primary trading venues declined from a peak exceeding 1.3 billion to beneath 150 million, eliminating substantial speculative positioning that accumulated during XRP’s previous upward movement.

Market intelligence firm Santiment Intelligence highlighted this divergence between price weakness and growing network participation in a recent analysis. The firm observed that new wallet creation and optimistic market sentiment are materializing even as price threatens the $1 level, with sentiment analysis revealing 3.7 positive comments for each negative one—the highest ratio in three months.

Critical Technical Zones Under Observation

XRP has remained confined within a descending price channel throughout the past year. The 20-period exponential moving average, which tracks near-term momentum, currently aligns with the upper boundary of this channel in the $1.18 to $1.22 range.

This region also coincides with a Fibonacci retracement level at $1.178 and a concentration of approximately 22.8 million XRP in cost basis distribution between $1.18 and $1.19. An additional 27.4 million XRP are positioned between $1.21 and $1.22.

These price zones represent areas where previous purchasers may attempt to exit positions at breakeven, establishing resistance. A decisive move above $1.18 followed by $1.22 would push XRP beyond its established downtrend into more neutral technical territory.

For downside protection, immediate support is established near $1.02. A violation of this level could potentially trigger a decline toward $0.87, according to Fibonacci extension analysis.

In the near term, market participants are monitoring $1.06 as initial resistance, followed by the $1.09 to $1.10 zone where previous recovery attempts have encountered selling pressure. A sustained move above $1.20 would represent the first meaningful indication of a potential trend reversal.

The 4-hour relative strength index has recovered to 46 after entering oversold territory, though it remains below the neutral 50 threshold. Price action recently consolidated within a $1.03 to $1.06 range, with peak trading volume occurring on June 29 at 17:00 UTC when 86.5 million XRP were exchanged.

The pickup began about 18 months ago, before MiCA’s first rules took effect, she said. Stablecoin regulations began applying about a year ago, and crypto-asset service providers have been working through a transition period before the July 1, 2026, deadline. After that date, firms relying on legacy national regimes will no longer be able to provide MiCA-regulated services in the EU.

The inquiries come from entrepreneurs frustrated by bureaucracy and regulatory burdens in Europe.

“They’re not just some random guys,” she said. “They’re former founders or current founders, somebody with multiple exits, somebody with years of experience in crypto.”

The deadline is already reshaping the competitive landscape. Binance, the world’s largest cryptocurrency exchange by trading volume, withdrew its MiCA application in Greece last week and notified EU users it would suspend some services while seeking another regulatory route. The company said it remains committed to Europe.

“Our ambitions in Europe remain the same, and we are confident we will secure a MiCA licence in the coming months,” Binance said in a statement to CoinDesk on Thursday.

Rivals are trying to capitalize. OKX and Coinbase (COIN) announced bonuses of up to 8% of total deposits and transfers for new users the following day.

Sovereign wealth funds are reportedly increasing exposure to spot Bitcoin, a development MidChains CEO Basil Al Askari said may reflect growing institutional interest at current price levels. Speaking on Cointelegraph’s “Chain Reaction” podcast on Monday, Al Askari said he could confirm at least one—and potentially two—in the coming weeks—sovereign wealth funds accumulating spot Bitcoin.

While retail participation has slowed, Al Askari pointed to stronger momentum from institutions and corporates, arguing that the present price environment is functioning as an “entry level” for larger funds that can wait through long accumulation cycles.

Key takeaways

- MidChains CEO Basil Al Askari says one, possibly two, sovereign wealth funds are accumulating spot Bitcoin, potentially in the coming weeks.

- Al Askari frames the current price level as attractive “entry level” positioning for mega funds with long time horizons.

- He expects the effect on markets to be gradual rather than a rapid cascade, but sees it as a clear signal to other institutions.

- Coinbase institutional strategy head John D’Agostino earlier said institutional buyers view the dip as an opportunity, particularly among UAE family offices and sovereign-linked investors.

- Despite spot Bitcoin ETF outflows in the U.S., corporate treasuries—especially Strategy—continue adding to BTC holdings.

Sovereign funds add spot Bitcoin exposure

Al Askari’s remarks center on state-backed capital moving into Bitcoin at a time when retail demand appears to be cooling. A sovereign wealth fund is typically a government-owned investment pool funded by national reserves, so the implication is less about short-term trading and more about long-term allocation decisions.

To help contextualize the scale of that player base, the article notes sovereign wealth funds collectively control more than $13 trillion globally, citing Visual Capitalist. Al Askari described these allocations as experiments for institutions that may have been waiting for a more compelling price to begin building positions.

Importantly for investors, he argued that this type of activity is unlikely to trigger an immediate, dramatic repricing. Instead, it can act as a confidence signal—encouraging other institutions that view larger funds as leaders to “start to get involved.”

Why a “long horizon” matters for Bitcoin supply dynamics

Al Askari suggested the strategic value of such accumulation lies in Bitcoin becoming “more and more scarce” over time as larger holders with longer investment horizons lock in supply. In his view, the key mechanism is not just who buys, but how long they plan to hold.

That distinction matters because it reframes the narrative from near-term momentum to liquidity and available float over extended periods. If more institutional capital transitions from sporadic exposure to sustained accumulation, the market’s effective supply can tighten gradually—potentially influencing volatility and depth even when short-term flows look mixed.

“I do think this is what will happen, is that over the longer term period, we’ll start to see Bitcoin becoming more and more scarce as a result of larger holders with much longer time horizons on their holding periods as far as looking at investments.”

ETFs see U.S. outflows even as corporate treasuries buy

The broader picture is mixed across investor segments. According to the source, sustained U.S. spot Bitcoin ETF outflows have totaled more than $4.1 billion so far this month, referencing Cointelegraph coverage of ETF flow performance and noting that Bitcoin ETF outflows are exceeding that threshold.

At the same time, corporate treasuries—particularly Strategy—continue accumulating. The article states that Strategy has scooped up 3,657 BTC this month, pointing to Cointelegraph reporting on the company’s reserve purchases.

This divergence—ETF outflows on one side and corporate accumulation on the other—can be read as a shift in where new demand is showing up. When exchange-traded product flows weaken but corporate balance-sheet demand persists, it suggests the marginal buyer may be changing rather than demand disappearing altogether.

Institutional “discount buying” and sovereign-linked appetite

Coinbase’s head of institutional strategy, John D’Agostino, previously weighed in on how institutional investors interpret the current market. In a CNBC interview earlier this month, D’Agostino said the “dip” is being welcomed by institutional investors, adding that he had just returned from the Middle East and observed that UAE family offices and sovereign-linked investors were not unhappy to buy at a discount.

The remarks underscore a practical reality for large-scale allocation: for patient capital, drawdowns can improve entry terms and reduce the risk of buying at potentially overextended levels. For traders, it also highlights that short-term market declines may not deter longer-term participants—especially those able to execute steadily rather than chase trends.

Known sovereign examples: Mubadala and Bhutan

The source highlights specific sovereign-related examples to illustrate the pattern. It notes that Abu Dhabi’s Mubadala Investment Company invested $437 million in BTC via BlackRock’s iShares Bitcoin Trust (IBIT) shares in February 2025. It also points to Bhutan’s Druk Holding and Investments as an early and more direct sovereign holder, while stating that the company has been selling some BTC this year, referencing Cointelegraph coverage of those sales.

Taken together, these examples point to a broader institutional learning curve: sovereign entities have already tested mechanisms for gaining Bitcoin exposure, and the current phase may be characterized by more deliberate scaling and timing—potentially shifting from ETF vehicles toward spot accumulation, as Al Askari suggested.

For readers, the next thing to watch is whether ETF outflows remain elevated as corporate and sovereign-related buyers continue adding, and whether Al Askari’s “one, possibly two” additional sovereign funds materialize publicly in the weeks ahead. That will help clarify whether this is a one-off window for discounted entries—or the start of a more durable institutional accumulation cycle.

Crypto exchange users in Australia will soon face stricter rules on all transfers as the country’s travel rule is set to come into force on Wednesday, aligning it with similar rules in the EU, US and UK.

From July, all crypto sent and received on locally-regulated crypto exchanges will require users to provide additional information, such as the name of the person the crypto is being sent to or received from, and the name of the platform.

Gabby Lewis, the head of fraud and financial crime at Swyftx, told Cointelegraph that for most exchange users, “the impact should be very limited. They’ll provide the required details once, and then these will be saved for future use.”

The rules are set to bring Australia in line with other countries that have implemented the travel rule for years, which the Financial Action Task Force, an international policy-making body, first extended to crypto in 2019.

Crypto users have long expressed concern that the rule would impact the anonymity of the technology and the risks of data linking crypto transfers to personal information being leaked.

However, Lewis said that the “travel rule isn’t crypto-specific. It already applies across financial services and has been implemented in areas including Singapore, the United States, New Zealand and the UK. Australia is now following suit.”

The rule aims to prevent money laundering, terrorist financing and scams by increasing the traceability of crypto transfers. It will be enforced by the Australian Transaction Reports and Analysis Centre (AUSTRAC), the country’s financial intelligence agency.

Transfers from a regulated crypto exchange to a self-custodial address, such as a cold storage wallet, will also prompt a user to verify and declare that they are the owner of that address.

“We’re generally talking about a quick confirmation that the wallet is theirs,” Lewis said. “The additional steps mainly come into force for transfers that involve another party or another exchange.”

Australia’s travel rule has no minimum value threshold, meaning a transfer of any size will require an exchange to gather information, aligning it with countries including France, the Netherlands and Japan that have no minimum.

Source: Sam Green

Other countries have set minimum reporting thresholds, such as the US, which only collects information on transfers starting at $3,000.

Some crypto exchanges operating in Australia have already begun to implement the travel rule, such as Kraken, which started on March 31, and CoinJar, which started on Tuesday.

Related: Australia passes digital asset bill bringing crypto platforms under licensing

Crypto users online have recently given mixed reactions to the rule, which the Australian parliament passed into law in 2024.

“With these new rules, you can forget about sending crypto anonymously,” a Reddit user wrote earlier this month.

“New travel rule is insane,” another Reddit user wrote earlier in June. “Thinking of moving everything to cold storage instead now.”

In response, one Reddit user said that “the regulated platforms were never anonymous.”

“This is less of a problem than you’re making it out to be unless you’re involved in activities the authorities would be interested in already,” another user wrote.

Magazine: Crypto scammers face death, Aussie CGT makes Asian hubs attractive: Asia Express

‘Another nightmare’: German media react to shock World Cup exit at the hands of Paraguay

SIS announces share buyback worth up to Rs 120 cr

Solana (SOL) Price at Critical Juncture: Will $70 Support Hold or Break?

-

Sports7 days ago

Sports7 days agoTwo goals and an assist by sheer aura: Cristiano Ronaldo just entered the World Cup chat

-

Fashion4 days ago

Fashion4 days agoWeekend Open Thread: Staud – Corporette.com

-

Politics4 days ago

Politics4 days agoThe House | Manchesterism won’t survive the painful trade-offs unless it gets citizens on board

-

Politics4 days ago

Politics4 days agoPotential 2028er World Cup attendee leaderboard

-

News Videos2 days ago

News Videos2 days agoMAJOR BITCOIN & MARKET UPDATE!!!! (MUST WATCH ASAP!!!)

-

Business4 days ago

Business4 days agoAsia stock markets slide as tech shares slump

-

Tech4 days ago

Tech4 days agoA Look At A Gaggle Of Transputer Boards

-

Crypto World6 days ago

Crypto World6 days agoSecuritize Wraps Roubini's SEC-Registered ETF as Dubai VARA Digital Security

-

Crypto World6 days ago

Bitcoin (BTC) Dips Below $62K, Ethereum (ETH) Plunges 6% Daily: Market Watch

-

Crypto World5 days ago

Crypto World5 days agoDell (DELL) Shares Tumble Over 5% Following Analyst Downgrade to Hold

-

Crypto World3 days ago

Crypto World3 days agoCoinbase, Circle Deepen Crypto Stock Losses Despite Resilient S&P 500

-

Business6 days ago

Entergy settles forward sale agreements, raises $672 million in cash proceeds

-

Crypto World3 days ago

Crypto World3 days agoKraken's xStocks Opens Bending Spoons IPO Registration to EEA Retail

-

Sports3 days ago

Sports3 days agoFIH Pro League: India defeat Pakistan 7-1, register biggest win of campaign | Other Sports News

-

Tech2 days ago

Tech2 days agoBluekit phishing kit adopts browser-in-the-middle for login theft

-

Crypto World4 days ago

Crypto World4 days agoBitcoin Sparks $600M Hourly Liquidations With $65,000 Set To Become Resistance

-

Tech3 days ago

Tech3 days agoRussian hackers now target Signal backup recovery keys

-

Crypto World4 days ago

Crypto World4 days agoHyperliquid Named on Singapore MAS Investor Alert Register

-

Crypto World4 days ago

Crypto World4 days agoRTX holders must register wallets before token distribution begins

-

Crypto World5 days ago

Crypto World5 days agoRipple and SBI launch RLUSD in Japan after JFSA approval

You must be logged in to post a comment Login