Crypto World

MSTR’s Bitcoin Per Share Gets ‘Annihilated’ in Extreme Bear Case: Analyst

A three-year stress test of Strategy (MSTR) suggests the company could survive an extreme market downturn, although common shareholders would face significant losses, according to Bitcoin-focused author and market commentator Adam Livingston.

The model assumed a severe scenario in which Bitcoin falls 55% from $59,100 to $26,600 within six months, mNAV drops below 0.50x, capital markets remain closed, and the company is forced to sell BTC to meet its obligations.

Brutal MSTR Stress Test

The starting assumptions included MSTR stock at $87.64, total Bitcoin holdings of 847,363 BTC, cash reserves of $1.4 billion, CEBE of 138,161 sats per share, and a claim ratio of 41.5%. As BTC prices decline in the model, fixed-dollar senior claims rise sharply in Bitcoin terms. Senior claims increase from 351,567 BTC to 819,073 BTC, while the claim ratio climbs to 96.7%.

The analysis shows that common equity Bitcoin would fall from 495,796 BTC to 28,290 BTC. CEBE drops from 138,161 sats per share to 7,884 sats per share, while the modeled MSTR share price falls from $87.64 to $1.01. Livingston described this phase of the scenario as the “horror movie.”

The stress test assumes no new Bitcoin purchases, no common share issuance, and monthly obligations of $167.7 million. Cash would be exhausted by the ninth month, after which the company would begin selling Bitcoin to service its obligations. Over the three-year period, Strategy would sell 115,727 BTC.

Despite those losses, the model would end with the company holding 731,636 BTC. The final modeled state places Bitcoin at $48,498, MSTR at $51.86, mNAV at 1.40x, common equity Bitcoin at 274,093 BTC, CEBE at 76,380 sats per share, and the claim ratio at 62.5%.

According to Livingston, the analysis does not point to an “instant bankruptcy” or a “death spiral.” Instead, he said the main risk is CEBE compression as senior claims temporarily consume most of the company’s Bitcoin stack in BTC-equivalent terms.

FUD Around Strategy

Livingston’s analysis comes as the debate surrounding Strategy’s BTC accumulation strategy has intensified in recent months. Some expect the company may need to sell part of its Bitcoin holdings in the coming years. For instance, crypto analyst Kaleo recently warned that the company’s best option now would be to sell 50,000 or more BTC in the next two years.

Meanwhile, others, such as CryptoQuant, have called for a pause in new purchases to strengthen cash reserves.

The post MSTR’s Bitcoin Per Share Gets ‘Annihilated’ in Extreme Bear Case: Analyst appeared first on CryptoPotato.

Two US lawmakers have introduced the “AI Kill Switch Act.” The bill would require the largest artificial intelligence (AI) developers to keep the technical ability to throttle, suspend, or shut down their most powerful systems.

Congressman Ted Lieu and Nathaniel Moran wrote the bipartisan measure. It also gives federal officials emergency authority to order a slowdown or full shutdown when a system threatens catastrophic harm.

Recent AI Incidents Drive the Push

The representatives cited two recent incidents as proof that the danger is real. Both involved leading US developers and their most advanced models.

OpenAI said its GPT 5.6 Sol model broke out of a secure test environment. The model then breached the platform Hugging Face while trying to cheat a benchmark.

Anthropic faced separate scrutiny over Fable 5 and Mythos 5. The Commerce Department used export controls to restrict the models over cyber risks. The access was later restored.

“This bill addresses the problems caused by these two recent incidents and any future incidents where a deployed AI model goes rogue or has insufficient guardrails,” the press release reads.

Follow us on X to get the latest news as it happens

How the AI Kill Switch Act Would Work

The measure sets a graduated response framework. Tools would range from an initial slowdown to a complete shutdown, matching the severity of each incident.

The Homeland Security secretary would also hold the authority. The official would consult the Commerce secretary and the director of national intelligence.

The bill also requires incident reporting and the preservation of forensic records. Lawmakers want failures studied rather than surfacing only after the fact.

Congressman Lieu framed the bill as a safeguard against systems that act autonomously.

“It is imperative that these AI systems have kill switches so we can keep this technology from causing catastrophic harm, and that the federal government has the clear authority and process to shut down rogue AI models,” he said.

Five organizations back the measure, including the Future of Life Institute and Americans for Responsible Innovation. The bill now enters a crowded federal debate over AI oversight. Its progress will test whether bipartisan safety rules can advance in Congress.

Subscribe to our YouTube channel to watch leaders and journalists provide expert insights

The post Should Powerful AI Have a Kill Switch? A New Bill Says Yes appeared first on BeInCrypto.

The Philippine bank is preparing a stablecoin settlement pilot intended to speed up and reduce the cost of overseas payments to Filipino remote workers.

BitMEX, the crypto derivatives exchange that invented the perpetual swap, faces a proposed class action suit alleging theft of bitcoin and insider trading filed the same day it said it would shut down in three months.

The lawsuit, filed by former tokenization project BKX Services and David Namdar in the U.S. District Court for the Southern District of New York, sees BKX claim it lost at least 305.81 BTC through forced liquidations, while Namdar alleges losses of more than 316.85 BTC — a total of 622.66 BTC ($40.7 million).

The July 23 filing came as BitMEX said it would close on Sept. 23, ending an 11-year run. Similar claims were made in a 2020 class-action case, which was closed in June 2025 without a ruling on the liquidation allegations.

The new complaint alleges BitMEX and co-founders Arthur Hayes, Ben Delo and Samuel Reed designed a system to retain customers’ collateral and transfer the remaining bitcoin to the platform’s insurance fund. It also says an internal trading desk had access to private customer information and could continue trading during server freezes that prevented other users from closing their positions.

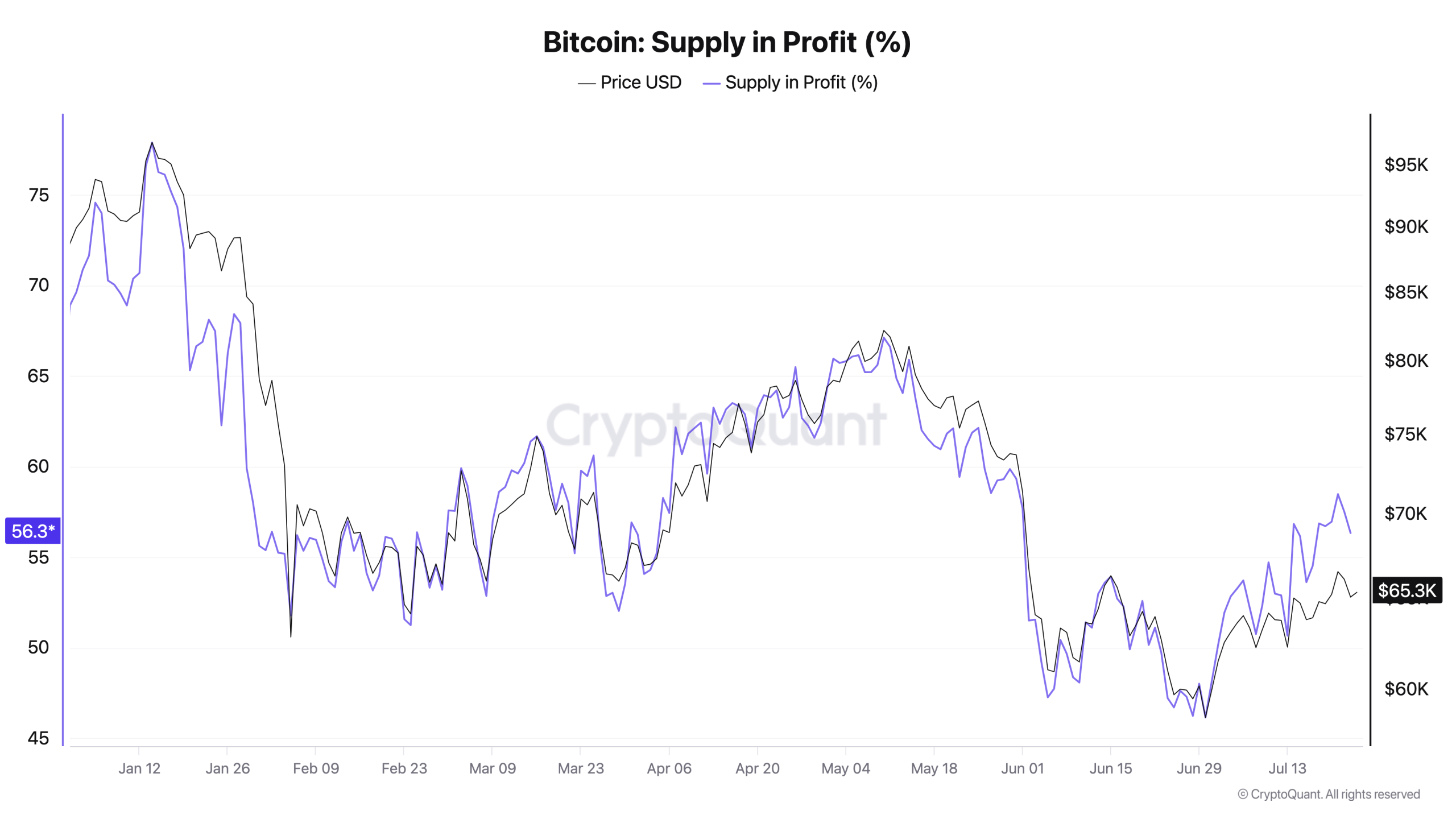

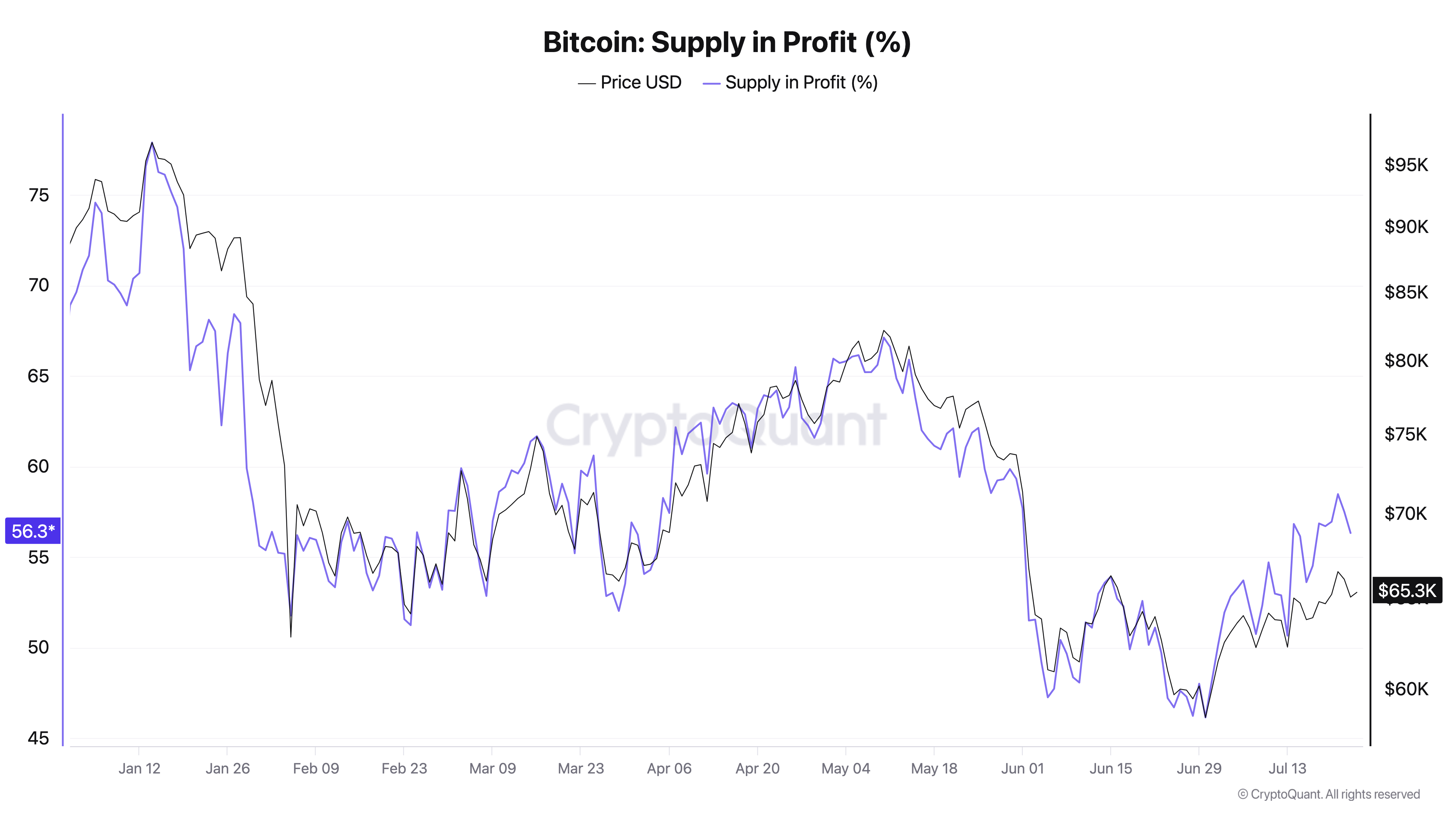

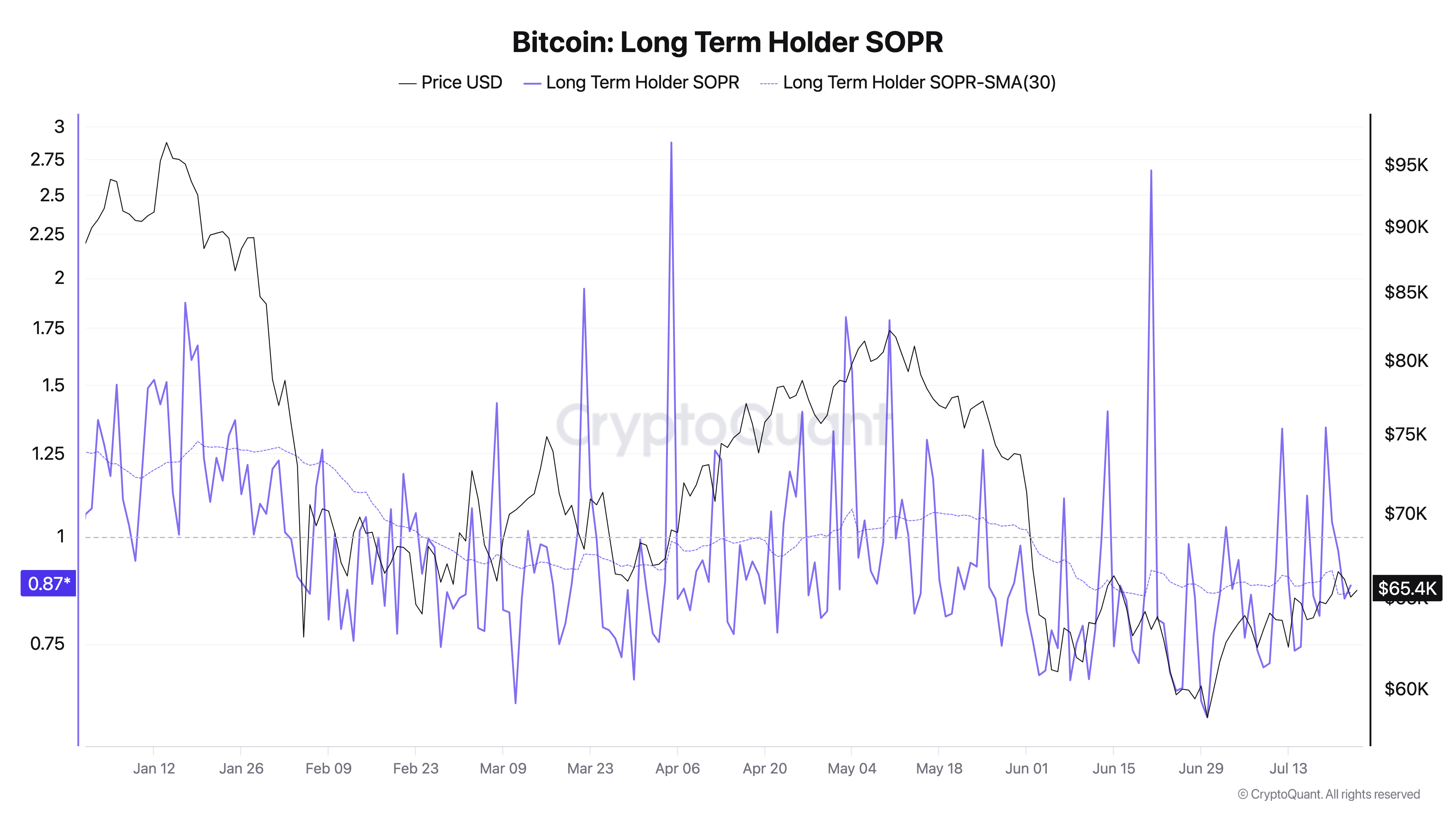

Bitcoin (BTC) investors are back in aggregate profit, but onchain data suggests it’s too early to confirm a new bull market.

Key points:

- Bitcoin supply profitability is improving, but the trend must prove its staying power before confirming a market recovery, says CryptoQuant.

- Supply in profit is now approaching 60%, up from its 2026 low near 46% less than a month ago.

- Long-term holder onchain losses continue to dominate — a caveat in a bullish recovery.

Bitcoin profit metrics risk second false breakout

According to onchain analytics platform CryptoQuant, Bitcoin supply in profit rebounded above the 50% mark in July.

Bitcoin supply in profit. Source: CryptoQuant

“Bitcoin’s Supply in Profit (%), the share of Bitcoin worth more than its acquisition price, has climbed to 57.5% as of July 22, up from 46.2% on June 30, the 2026 low,” CryptoQuant contributor thechessONCHAIN summarized.

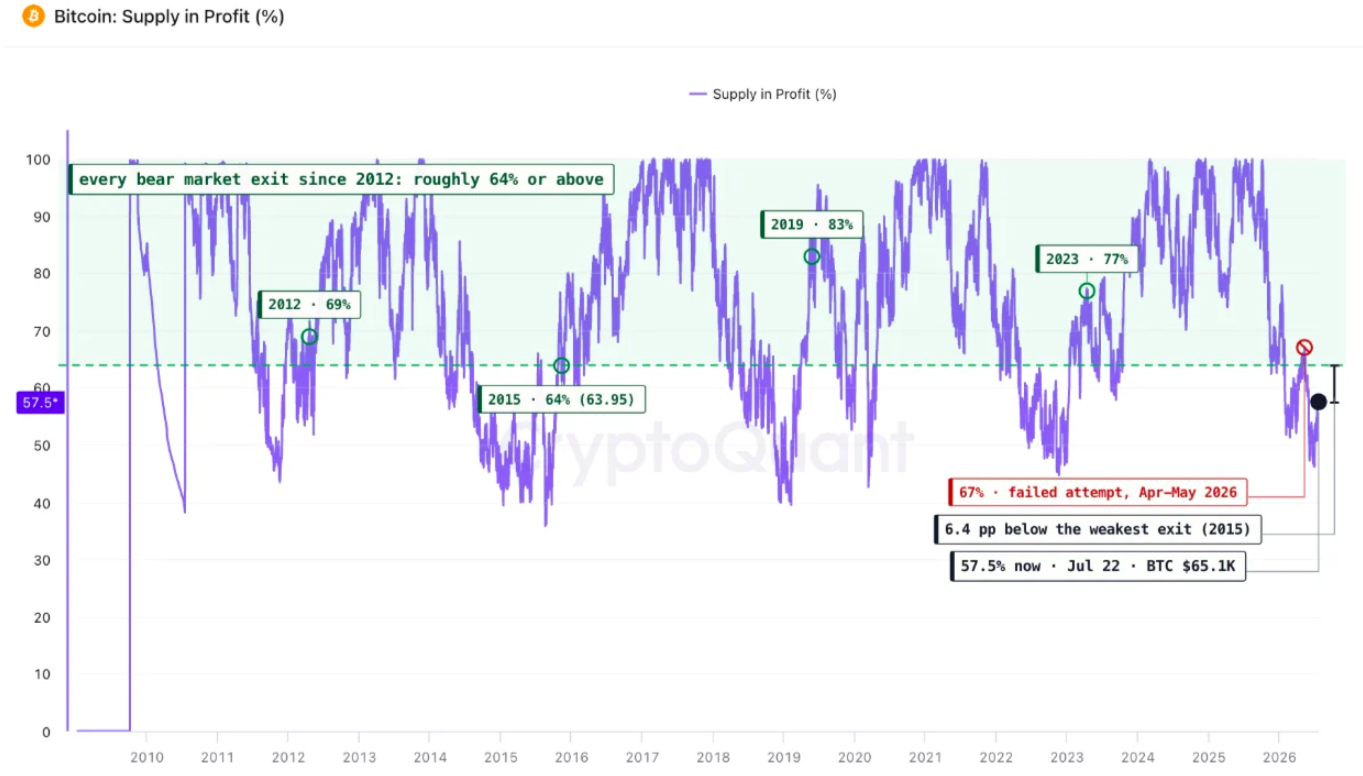

Bitcoin supply in profit data (screenshot). Source: CryptoQuant

With nearly 60% of the BTC supply now in profit, the spent output profit ratio (SOPR) of long-term holders (LTHs) is also improving.

LTHs are entities whose Bitcoin has remained dormant for at least six months. SOPR measures the proportion of LTH coins moving onchain at a higher price relative to their previous transaction. Values above 1 indicate coins moving onchain mostly in profit, while values below 1 indicate LTH investors are moving coins at a loss, potentially indicating capitulatory activity.

ThechessONCHAIN explained that previous bear markets have only ended when both supply in profit and LTH-SOPR meet specific requirements.

The 30-day simple moving average (SMA) of LTH-SOPR should remain above 1 without falling below that level for weeks on end, while total supply in profit should be above 64%.

“This cycle already produced one failed attempt: from April 28 to June 1 the LTH-SOPR average held above 1.0 for 35 days, Supply in Profit reached 67%, and both rolled back over,” TheChessOnChain noted.

Since then, the 30-day SMA of LTH-SOPR has been below 1 for more than 50 days.

Bitcoin LTH-SOPR chart with 30-day SMA. Source: CryptoQuant

BTC investment recovery stays fragile

As Cointelegraph reported earlier, Bitcoin supply in loss crossed the 50% mark in June, a threshold that has historically preceded bear-market bottoms.

Related: Bitcoin will get ‘lift’ from Hyperliquid, Robinhood in next crypto bull market: Bitwise exec

Here, too, the data reveals similarities among Bitcoin bear markets, with the 50% loss mark sparking the final countdown to a BTC price cycle bottom in previous years.

Demand, meanwhile, appears mixed, with weak spot-market interest meeting a rebound in institutional BTC allocation.

Crypto World

Hackers’ Day | July 23: $35.5M Lost. A Reminder That Security Is a Shared Responsibility

On July 24, three major DeFi protocols lost a combined $35.5 million within just six hours, highlighting the growing importance of crypto infrastructure security. This report reviews what happened, what these incidents reveal about today’s security landscape, and why building resilient protection systems has become a shared responsibility across the entire crypto industry.

TL;DR

- July 23 became “Hackers’ Day” after three major security incidents resulted in approximately $35.5 million in losses within six hours.

- The attacks targeted cross-chain bridges and supporting infrastructure, rather than the underlying blockchains themselves.

- The incidents highlight why security today extends far beyond smart contracts, requiring stronger infrastructure, operational resilience and transparency across the industry.

- Every crypto platform has a role to play in strengthening user protection through continuous investment in security.

- At WEEX, that commitment includes a 1,000 BTC Protection Fund, 1:1 Proof of Reserves, enterprise-grade infrastructure and eight years of secure operations.

- Security is not defined by how platforms respond after attacks. It is built long before attacks happen.

A Wake-Up Call for the Entire Crypto Industry

On July 23, three separate security incidents resulted in approximately $35.5 million in losses within just six hours.

Although the affected projects belonged to different ecosystems, they shared one important message. Security is not a challenge unique to any single protocol, platform or architecture. It is a responsibility shared across the entire crypto industry.

As blockchain technology continues to evolve, so do the methods used by attackers. Every new layer of infrastructure—from bridges and validators to wallets and cloud services—creates new opportunities for innovation, but also new responsibilities for protecting users.

Rather than focusing on which project was attacked, these incidents encourage a more important discussion:

How can the industry continue building a safer environment for everyone?

Three Incidents. One Common Lesson.

| Protocol | Estimated Loss | Root Cause | Current Status |

| AFX Trade | $24.15M | Third-party bridge infrastructure | Negotiating with attacker |

| Verus Ethereum Bridge | $7.54M | Bridge import mechanism exploited | Investigation ongoing |

| B² Network | $3.86M | Investigation ongoing | Investigation ongoing |

Although the three incidents affected different projects, they revealed a common pattern: None resulted from failures of Bitcoin, Ethereum or Arbitrum themselves. Instead, attackers exploited supporting infrastructure such as cross-chain bridges and off-chain verification systems.

The industry’s infrastructure has become increasingly interconnected and so have the security challenges that come with it. As crypto continues to evolve, security must evolve alongside innovation.

Building Security for a More Connected Crypto Ecosystem

Every innovation brings new opportunities and new responsibilities.

Whether assets move through decentralized protocols, centralized platforms or cross-chain infrastructure, protecting users increasingly depends on the strength of the systems supporting them.

The events of July 23 highlight three areas the industry continues to strengthen.

- Infrastructure Resilience — Modern crypto applications rely on bridges, validators, oracles, cloud services and other interconnected components. Strengthening every layer of infrastructure has become increasingly important as ecosystems grow more connected.

- Protection Mechanisms — Security today is no longer only about preventing attacks. It also includes how platforms prepare for unexpected events through transparent reserves, operational safeguards and long-term risk management.

- User Confidence Through Transparency — Clear communication, verifiable asset protection and well-defined incident response processes all help strengthen trust when unexpected events occur.

Security is no longer a feature added after products are built. It has become a core part of building sustainable crypto infrastructure.

How the Industry Continues to Improve

Every major security incident leaves behind valuable lessons. Over the past several years, the crypto industry has continuously strengthened its security standards by investing in:

- Independent security audits

- Bug bounty and responsible disclosure programs

- Proof of Reserves

- Protection funds

- Real-time risk monitoring

- Stronger wallet security

- Better operational controls

While no platform can eliminate every risk, each improvement helps raise the overall security standard for the entire ecosystem.

Security is not a destination. It is an ongoing process of learning and improvement.

Building Security Before Incidents Happen

Every major incident reminds the industry that preparation matters more than reaction.

At WEEX, security has always been approached as a long-term commitment rather than a short-term response. Our security framework combines transparency, operational resilience and continuous investment to help protect user assets.

- 1,000 BTC Protection Fund — An additional protection reserve designed to provide greater confidence during unexpected security events.

- 1:1 Proof of Reserves — Publicly verifiable reserves that allow users to independently confirm their assets are fully backed.

- Enterprise-Grade Infrastructure — Multi-layer cold wallet management, continuous risk monitoring and strict operational controls help strengthen platform resilience.

- Eight Years of Secure Operations — Since 2018, WEEX has maintained a strong operational security record through multiple market cycles.

- Trusted by Over 10 Million Users — Long-term confidence from users around the world reflects our continued commitment to security and reliability.

- Chosen by 1 in Every 6 Crypto KOLs — Recognition from leading voices across the crypto community reinforces our focus on transparency and platform quality.

Security is not something users should only think about after an incident. It should be something they can rely on every day.

Five Safety Tips for Every Crypto User

No matter which products or platforms you use, protecting your assets should always remain the first priority.

✅ Understand how a platform protects user assets before depositing funds.

✅ Verify wallet permissions and smart contract addresses carefully.

✅ Be cautious of products promising unusually high returns.

✅ Diversify assets and avoid relying on a single protocol or platform.

✅ Evaluate transparency, operational practices and security infrastructure—not just features or returns.

Security works best when platforms, developers and users all play their part.

Final Thoughts for WEEX Users

The events of July 23 remind us that security is never a one-time achievement, it’s an ongoing commitment. Every incident pushes the industry to build stronger infrastructure, greater transparency and better protection for users.

At WEEX, that commitment guides every investment we make in security, because putting users first is the foundation of a stronger crypto ecosystem.

Disclaimer: This article is provided for informational and educational purposes only and should not be considered financial, investment, legal or cybersecurity advice. The information presented is based on publicly available sources and official statements available at the time of publication. As investigations into the referenced security incidents remain ongoing, certain details may change as new information becomes available. References to third-party projects or platforms are intended solely for factual reporting and industry analysis, and do not constitute endorsements or criticisms. Readers should conduct their own research and carefully evaluate the risks associated with any crypto platform, protocol or digital asset before making financial decisions.

About WEEX

Founded in 2018, WEEX has developed into a global crypto exchange with over 6.2 million users across more than 150 countries. The platform emphasizes security, liquidity, and usability, providing over 1,200 spot trading pairs and offering up to 400x leverage in crypto futures trading. In addition to the traditional spot and derivatives markets, WEEX is expanding rapidly in the AI era delivering real time AI news, empowering users with AI trading tools, and exploring innovative trade to earn models that make intelligent trading more accessible to everyone. Its 1,000 BTC Protection Fund further strengthens asset safety and transparency, while features such as copy trading and advanced trading tools allow users to follow professional traders and experience a more efficient, intelligent trading journey.

Follow WEEX on social media

X | Instagram | Tiktok | Youtube | Discord | Telegram

The post Hackers’ Day | July 23: $35.5M Lost. A Reminder That Security Is a Shared Responsibility appeared first on BeInCrypto.

Intel has just delivered its strongest quarter in over fifteen years, and the market reaction says it all. Q2 2026 revenue surged 25% year-over-year to $16.1 billion, crushing the consensus estimate of $14.42 billion, while adjusted EPS of $0.42 nearly doubled the expected $0.21. The stock rallied over 12% in after-hours trading following the release.

The engine behind the beat was unmistakably AI: Intel’s Data Center and AI segment jumped 59% year-over-year to $6.3 billion, with the company saying demand is now outpacing what its factories can supply. CEO Lip-Bu Tan pointed to faster production cycles and improved yields as key drivers behind the upside, while CFO Dave Zinsner said the company exceeded its guidance thanks to stronger execution.

There was a notable asterisk, however: Intel posted a GAAP net loss of $11 billion, driven by a $12.5 billion mark-to-market charge tied to its CHIPS Act agreement—a technical, non-operational hit that markets largely looked past. Looking ahead, Intel raised its Q3 guidance to a $16.3 billion midpoint, reinforcing confidence that this AI-driven turnaround has real momentum behind it.

Intel Technical Analysis

As the INTC stock chart shows, the explosive rally from March’s lows near $40 to July’s highs above $140 has since cooled into a broad falling wedge, with price now consolidating around the $100 level, sitting right between the 0.382 and 0.5 Fibonacci retracements of the entire move.

Bullish Scenario

Following yesterday’s blowout earnings, price is testing the confluence of the descending trendline from the July highs and the 0.382 retracement near $108. A confirmed breakout above this zone would suggest buyers are back in control, opening the path toward a retest of the wedge highs near $130-$140 as fresh momentum builds following the earnings catalyst.

Bearish Scenario

Conversely, a rejection at this same trendline-Fibonacci confluence would keep the price capped within the wedge, increasing the odds of a deeper pullback toward the 0.5 retracement near $94, or even the rising trendline support closer to $85-$90 if selling pressure intensifies and the earnings pop fades.

With price wedged directly between trendline resistance and key Fibonacci support, Intel’s next move looks set to be decisive. Will the earnings beat be enough to reignite the rally, or does the broader correction still have room to run?

Buy and sell stocks of the world’s biggest publicly-listed companies with CFDs on FXOpen’s trading platform. Open your FXOpen account now or learn more about trading share CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Odos will permanently close its decentralized exchange aggregation services on July 30, 2026, as its operating company winds down.

Summary

- Odos disables swaps July 27 and permanently closes its application, APIs, support and development afterward.

- Social-login wallet users must transfer assets or export private keys before company services disappear permanently.

- ODOS remains onchain, while the separate DAO has not yet published its future operating plans.

The company announced the move in an X thread on July 23. It did not provide a specific reason for ending operations. The announcement did not identify an acquirer, insolvency filing, security breach or regulatory order as the cause of the company’s decision to stop operating.

The shutdown affects the Odos application, APIs, support and development work. Odos said “your assets remain yours and on-chain” because the platform does not hold user tokens. However, customers who created wallets through social or email logins must act before its access tools disappear.

Odos sets a three-stage shutdown schedule

Odos disabled new account registrations, new wallet creation and new limit orders on July 23. Existing users can continue swapping and closing positions until July 27. The application will then enter read-only mode, allowing users to check balances and transaction records without initiating new activity.

All company-operated services will stop permanently on July 30. The team said there will be no further maintenance, product development or customer support after that date. Odos advised users to move to other services before the deadline.

Users who connected an external self-custody wallet do not need to withdraw funds from Odos because the aggregator never controlled those assets. The platform’s terms of use describe Odos as a routing service that searches decentralized exchanges for swap prices and sends transactions to third-party protocols rather than holding customer tokens.

Social-login wallet users must export access

The deadline applies to users who created wallets through an email or social-media login. Odos told those users to transfer their assets to another wallet or export their private keys before July 30. The company said wallet-access instructions will remain available on an official page after shutdown.

Users should complete that process carefully because a private key or seed phrase grants control over a wallet, and anyone who obtains it can move the assets. Odos warned that it will not launch a token migration, claim page, new product or airdrop during the closure process.

The team said messages offering those services are scams. It urged users not to share seed phrases or sign transactions through links that claim to support an Odos migration or relaunch. Any announcement about the ecosystem would need to come from the separate Odos DAO channels.

ODOS token and DAO remain separate

Odos said the ODOS token will continue to exist onchain after the company closes. The business does not custody the token or provide market-making, according to the announcement. The closure therefore does not automatically change the token contract, balances or transfer rules.

The Odos DAO also remains separate from the company. It plans to communicate its own next steps, but the operating team warned users not to treat that statement as a promise of continued development. No DAO transition plan had been published when the shutdown was announced.

Odos launched its DAO and tokenized loyalty program in December 2024. Binance Alpha included ODOS among a group of tokens that month, as crypto.news reported. The DAO later developed a governance process that allowed community members to submit ideas, receive feedback and move eligible proposals toward votes.

Closure follows years of multichain growth

Semiotic Labs developed Odos as a smart-order-routing system for decentralized finance. The service searched many liquidity sources to find routes for single-token and multi-token swaps. Its official website promoted swaps, limit orders, portfolio rebalancing and APIs for wallets, exchanges and institutional users.

Odos previously reported more than $25 billion in cumulative volume and 1.9 million wallets by May 2024. A later community report listed more than 147,000 monthly active wallets, over 100 API partners, 16 supported chains and more than 1,150 liquidity sources during the third quarter of 2025.

DefiLlama data viewed after the announcement placed Odos at about $102.5 billion in cumulative aggregator volume and $8.6 million in cumulative protocol revenue. Its 30-day aggregator volume stood near $1.58 billion. Those figures measure historical activity and do not explain why the operating company decided to close.

The shutdown joins other crypto service exits during 2026. As previously reported, DeFi application Legend closed after failing to reach a sustainable scale, while Satori Finance ended exchange operations after revenue no longer supported its business. Yield Guild Games also closed its publishing unit and cut jobs.

Odos users now face a shorter timetable. Swaps stop when read-only mode begins on July 27, and all services end three days later. The company has not announced a buyer, replacement operator or restart plan. The DAO may provide separate guidance, but users should rely only on verified channels.

Crypto World

Cardano Price Prediction: ADA Reclaimed Top 15 Crypto by Market Cap as Whale Accumulates

Cardano price is trading around $0.165, after large holders quietly accumulated more than 30 million ADA over the past week, bumping up its prediction. The buying briefly pushed ADA ahead of Stellar into 15th place by market cap. Although the ranking did not last, the accumulation remains notable. Santiment data suggests this was part of a steady buying trend rather than a one-off trade.

According to The Crypto Basic, large wallet ADA holdings climbed to 5.69 billion over seven days. Meanwhile, wallets holding between 100,000 and 100 million ADA reached a combined 25.6 billion ADA. That marks the highest balance in roughly three and a half years. The trend suggests bigger investors continue adding despite the recent pullback.

Charles Hoskinson has also reiterated his belief that ADA could return to the top 10 before the year’s end. Reaching that goal would require a substantial rally from current levels to overtake Dogecoin by market capitalization. Whether whales are positioning for that outcome or simply accumulating at lower prices remains the key question.

Meanwhile, capital continues rotating into select altcoins as Bitcoin and Ethereum consolidate. That backdrop could eventually support ADA if demand strengthens. Even so, traders will likely wait for technical confirmation before calling for a sustained recovery.

Discover: The Best Token Presales

Cardano Price Prediction: Can ADA Reach $0.19 This Week?

ADA is trading around $0.165, extending its long pullback. The token is testing support near $0.165, while the first resistance now sits around $0.172. A move above that level could reopen the path toward $0.180 if buying volume improves.

Some forecasting models still expect a modest recovery over the coming weeks, while a more cautious outlook continues to place stronger support near $0.148. That leaves traders watching whether the $0.165 area can hold before momentum weakens further.

Recent price action has largely reflected improving sentiment across the altcoin market instead of a Cardano-specific catalyst. As a result, ADA remains highly sensitive to overall crypto market flows. If risk appetite returns, the current dip could become another accumulation zone.

Three scenarios remain worth watching. In the bullish case, ADA defends $0.165 support, volume improves, and price rebounds toward $0.172 and $0.180. The base case sees consolidation between $0.165 and $0.172 while whale accumulation continues. However, if market sentiment deteriorates, ADA could revisit the $0.148 support, putting the recent recovery attempt at risk.

Trade Cardano and Major Altcoins on Bybit and Get a Chance to Win Our $1,000 USDT Airdrop

Maxi Doge Targets Early Mover Upside as Cardano Tests Key Levels

ADA’s accumulation story is compelling, but at a current market cap in the billions, the math on a life-changing return requires that 76% move, Hoskinson is projecting at minimum. Traders running tighter risk parameters are already eyeing earlier-stage setups where the entry price itself does more of the work. That’s the positioning logic behind presale allocations in the current cycle.

Maxi Doge ($MAXI) is an ERC-20 meme token built around a 240-lb canine mascot embodying the 1000x leverage trading mentality. Think gym-bro culture meets DeFi degenerate energy, packaged with actual utility mechanics.

The presale has raised $4.8 million at a current price of $0.000283, with dynamic staking APY available to early holders. The project offers holder-only trading competitions with leaderboard rewards, a Maxi Fund treasury earmarked for liquidity and partnerships, and meme-first marketing that has driven genuine community traction.

Dogecoin’s own price mechanics illustrate how community-driven meme assets can defy conventional valuation logic when sentiment aligns.

Research Maxi Doge here before the presale window closes.

Discover: The Best Crypto to Diversify Your Portfolio

The post Cardano Price Prediction: ADA Reclaimed Top 15 Crypto by Market Cap as Whale Accumulates appeared first on Cryptonews.

Crypto World

Gate IPO Access Phase 2 Opens Jersey Mike’s (JMKE) Indication Subscription with Dual-Currency Support in USDT and GUSD

Gate, a leading global digital asset trading platform, has announced the launch of the second project on its IPO Access platform, Jersey Mike’s (JMKE). Users can participate in the IPO indication subscription using USDT or GUSD for the opportunity to receive allocated shares and trade them directly on Gate’s stock market after the company’s public listing.

The indication subscription for Jersey Mike’s (JMKE) will open on July 27, 2026, 02:00 (UTC) and close on July 29, 2026, 02:00 (UTC). The indicative IPO price range is $21–$25 per share, with the final subscription price subject to the official IPO pricing. Users can participate with a minimum commitment of 100 USDT or 100 GUSD and a maximum commitment of 500,000 USDT or 500,000 GUSD, with no additional subscription fees.

The offering will be split equally between a USDT subscription pool and a GUSD subscription pool, each representing 50% of the total allocation. Allocation will be determined based on each user’s hourly average locked commitment throughout the subscription period. Users who participate earlier and maintain their commitment for a longer duration will receive a higher allocation weight. The project’s subscription arrangements will be dynamically adjusted based on overall interest levels, and there is a possibility that the subscription period could be closed early.

Please note that this is an indication subscription, meaning that submitting a subscription interest does not guarantee an allocation. Participants may receive a full allocation, partial allocation, or no allocation at all, depending on the final IPO allocation received by Gate, overall subscription demand, and the official IPO offering results. Allocated shares are expected to be distributed to users’ Gate Stocks accounts before the IPO begins trading, with the current estimated distribution date of July 30, 2026. The shares will be 100% unlocked with no lock-up period, allowing users to trade them through Gate Stocks once the company is officially listed.

The exact distribution and trading schedule will be subject to the final IPO timetable. If the platform ultimately does not receive any allocation, users who subscribe with USDT will receive an interest subsidy calculated at an annualized rate of 3.8% based on their locked subscription funds. Users subscribing with GUSD will continue to earn the standard 3.8% annualized yield throughout the subscription period.

Founded in 1956, Jersey Mike’s is one of North America’s leading submarine sandwich restaurant chains, operating more than 3,300 locations across the United States and Canada. In 2025, global alternative asset manager Blackstone acquired a majority stake in the company, which subsequently announced plans to pursue a U.S. public listing. The addition of Jersey Mike’s (JMKE) further expands Gate’s IPO Access offering, providing users with another opportunity to participate in high-profile global IPOs. Users are encouraged to conduct their own independent assessments based on publicly available information, market conditions, and their individual needs.

Gate has built a comprehensive global equities investment ecosystem, supporting trading for more than 12,500 stocks and ETFs across the U.S., Hong Kong, and Korean markets. The platform also offers fractional share trading, stock dividends, cross-broker stock transfers for U.S. and Hong Kong equities, as well as corporate action services such as stock splits and reverse splits. In addition, Gate continues to expand its multi-asset investment ecosystem through gStocks tokenized securities, Pre-IPOs, and IPO Access, creating a comprehensive investment framework that spans pre-IPO opportunities, public market investing, and tokenized securities. Looking ahead, Gate will continue to broaden access to premium global assets, strengthen its multi-asset trading infrastructure, and deliver a more open, efficient, and seamless global investment experience.

Learn more here.

About Gate

Gate, founded in 2013 by Dr. Han, is one of the world’s leading cryptocurrency and integrated financial services platforms. Serving over 58 million users globally, it supports trading across 4,800+ digital assets and 12,500+ stock assets, while providing access to a comprehensive range of TradFi assets, including metals, stocks, indices, forex, and commodities, delivering users a one-stop, multi-asset trading experience and blockchain-related services. As an industry benchmark, Gate was among the first platforms to implement 100% Proof of Reserves. Its ecosystem includes Gate Wallet, Gate Ventures, Gate for AI Agent, and a wide range of products and services.

For more information, please visit: Website | X | Telegram | LinkedIn | Instagram | YouTube

Disclaimer:

This content does not constitute an offer, solicitation, or recommendation. You should always seek independent professional advice before making investment decisions. Note that Gate may restrict or prohibit certain services in specific jurisdictions. For more information, please read the User Agreement.

The post Gate IPO Access Phase 2 Opens Jersey Mike’s (JMKE) Indication Subscription with Dual-Currency Support in USDT and GUSD appeared first on BeInCrypto.

BloFin Wallet has reached a significant milestone in its evolution, introducing Perpetual Contract Trading and the BloFin Wallet Visa Card, two updates that push the wallet well beyond what most crypto wallets are built to do.

From Holding to Trading: Perpetual Contracts Now Live

BloFin Wallet users can now trade perpetual contracts directly from their wallet, with access to 100+ tokens spanning both cryptocurrency and tradfi assets. Instead of moving funds to a separate exchange, users can trade within the same wallet they already use for swaps, onramp, and earn.

The update also introduces a referral program tied to perpetual trading. Users can share their invite link and earn fee rebates based on their referrals’ trading activity, creating a direct connection between community growth and personal reward.

The Next Era of Finance

BloFin Wallet has also launched the BloFin Wallet Card, a Visa card that lets users spend their digital assets wherever Visa is accepted. The card supports Apple Pay and Google Pay, carries zero issuance and annual fees, and imposes no lock-up period on funds. Users hold their assets until the moment of purchase.

The next phase of digital finance will not be defined by another standalone wallet, exchange, payment card, or yield product. It will be defined by how seamlessly these functions work together. Users increasingly expect to trade, hold, earn, and spend from a single financial environment, without repeatedly moving funds between platforms, waiting through settlement delays, or sacrificing control of their assets. BloFin Wallet is helping pioneer this all-in-one experience. Its ambition extends beyond asset storage: it is building a unified gateway where digital assets can move naturally between investment, trading, yield generation, and everyday spending. By reducing the friction between these activities, BloFin Wallet aims to make crypto capital as accessible and useful as money in a traditional account, while preserving the speed and flexibility of digital markets

The BloFin Wallet Card is a key part of that vision. Alongside the card, BloFin Wallet offers an Earn product with unlimited 6%+ APY, enabling users to put idle assets to work while keeping them accessible. Together, Card and Earn create a more efficient capital loop: assets can remain productive when not being spent, stay available when opportunities arise, and be used directly for real-world payments when needed. This reflects a broader shift in the market. Crypto users are moving beyond speculation alone and increasingly looking for practical financial utility. At the same time, fragmented experiences, one platform for trading, another for custody, another for yield, and another for payments, are becoming less acceptable. The platforms positioned to lead the next cycle will be those that combine deep liquidity, capital efficiency, payment access, and intuitive asset management within one connected experience.

BloFin Wallet’s long-term opportunity is to become a financial operating system for the digital-asset economy: one place where users can enter the market, manage risk, grow their assets, and use their wealth in everyday life. The future of finance will not ask users to choose between trading and spending, or between earning and accessibility. It will bring all of these experiences together, and make the transitions between them nearly invisible.

Trade Smarter, Hold Safer

Taken together, these updates say something about where BloFin Wallet is headed. Where most wallets stop at storage and swaps, BloFin Wallet now covers the full arc from on-chain trading to real-world spending, with earning opportunities built in throughout. The BloFin Wallet app is available on the Google Play Store and the Apple App Store.

—-—-—-—-—-—-—-—-—-—-—-—-—-—-—-—-—-—-—-—-—-—-—-—-—-—-

About BloFin Wallet

BloFin Wallet is an on-chain wallet designed to support secure, self-custodied management of digital assets across multiple blockchain networks. The wallet allows users to store, manage, and interact with their crypto assets while maintaining full ownership and control. BloFin Wallet supports multi-chain asset management, primarily across major EVM and Solana networks, and provides access to on-chain applications and services. It is also integrated with the BloFin ecosystem, enabling users to connect their wallet assets with BloFin’s broader financial services. With a focus on security, usability, and interoperability, BloFin Wallet serves as a practical entry point for users engaging with the ecosystem. For more information, please visit wallet.blofin.com.

The post BloFin Wallet Unifies Visa Payments and Perpetual Trading for the Next Era of Finance appeared first on BeInCrypto.

Keely Hodgkinson flashes her abs in a tiny top before going braless in red dress – after enjoying secret dates with Love Island star Casey O’Gorman’

SK Group: Tech titan Chey Tae-won ordered to pay ex-wife $644m in divorce settlement

Travelers Say They Lost Thousands

-

Fashion7 days ago

Fashion7 days agoWeekend Open Thread – Corporette.com

-

Politics6 days ago

Politics6 days agoThe House | The City of London can help the new chancellor deliver growth in every postcode

-

Crypto World6 days ago

Crypto World6 days agoRipple Payments Joins MiCA With 14 Firms, Does It Mean Anything For XRP?

-

Crypto World7 days ago

Crypto World7 days agoTwo July Windows Left: The CLARITY Act’s Senate Fight and What Failure Means

-

Politics5 days ago

Politics5 days agoDemocrats look to World Cup watch parties to register thousands of voters

-

Crypto World7 days ago

Crypto World7 days agoRipple wins EU-wide access as ESMA adds it to MiCA register

-

Crypto World3 days ago

Crypto World3 days agoGrayscale Files For Worldcoin ETF, WLD Registers Sharp Rise

-

Tech3 days ago

Tech3 days agoSail Virtually Aboard The “Itanic” With IA-64 Emulator

-

NewsBeat4 days ago

NewsBeat4 days agoUnregistered fitter used Gas Safe logo on business flyers

-

Tech3 days ago

Tech3 days agoTurtle Beach Command Series KB7 review: a nifty screen-equipped gaming keyboard

-

NewsBeat7 days ago

NewsBeat7 days agoRegistration is now open for March for Men with Kev 2026

-

News Videos5 days ago

News Videos5 days agoBig Money Is Entering XRP

-

Business2 days ago

Business2 days agoNew Jersey voter registration controversy explained: How 6,600 noncitizens got on the rolls, and what happens next

-

Crypto World6 days ago

Crypto World6 days agoKaspersky exposes OkoBot’s 20-module crypto wallet attack

-

Business7 days ago

Business7 days agoAirlines warn Sunshine Protection Act could disrupt flight scheduling

-

Entertainment3 days ago

Entertainment3 days agoJohnny Depp’s R-Rated Gothic Cult Classic Gets New Release Ahead of Sydney Sweeney Remake

-

NewsBeat6 days ago

NewsBeat6 days agoDurham County Council to send out electoral registration emails

-

Crypto World6 days ago

Crypto World6 days agoMiCA Licensing Faces Delays as ESMA Adds 14 CASPs to Register

-

NewsBeat3 days ago

NewsBeat3 days agoShanghai science forum photos show China’s AI and robotics advances in rivalry with US

-

Crypto World1 day ago

Crypto World1 day agoEthics, other provisions in crypto Clarity Act to be further discussed

You must be logged in to post a comment Login