Crypto World

Nasdaq Tokenization Could Create Dual Trading Venues

Nasdaq’s drive to tokenize equities could reshape capital markets by introducing a two-tier landscape where regulated US exchanges sit alongside blockchain-based trading venues. A TD Securities note suggests the move may create parallel systems capable of splintering trading activity and producing price differences across platforms as tokenized stocks gain traction.

The bank’s analysis highlights Nasdaq’s parallel push, joining NYSE’s tokenization efforts, to advance three main tracks: modernizing post-trade settlement for tokenized assets, enabling issuances of tokenized shares, and extending trading to offshore venues such as Kraken. Taken together, these efforts could lead to a split market where one stream operates within the traditional US regulatory framework and another on offshore, blockchain-enabled platforms.

TD Securities cautions that offshore venues—while backed by real securities—could escape the American regulatory perimeter. If tokenized shares trade on these platforms, prices could diverge from those on standard US venues, complicating price discovery and potentially siphoning activity away from established exchanges. Cointelegraph reached out to TD Securities for comment but did not receive a response in time for publication.

Key takeaways

- Nasdaq’s tokenization strategy comprises three parallel efforts: post-trade settlement upgrades, tokenized equity issuance, and offshore trading support on platforms such as Kraken.

- The initiatives could yield a two-tier market: a regulated US market and an offshore, blockchain-based trading ecosystem, with potential price differentials between venues.

- Tokenized equities are gaining real traction, as shown by Kraken’s xStocks platform, which has surpassed $25 billion in cumulative trading volume and grown about 150% since November.

- Trading across multiple venues may create 24/7 access and broader round‑the‑clock liquidity, but it also introduces new risks around activity concentration and inconsistent pricing.

- Industry context shows broader momentum: Coinbase expanding tokenized stock offerings and NYSE’s collaboration with Securitize to explore 24/7 tokenized securities, signaling growing competition for traditional equity trading.

Nasdaq’s tokenization roadmap could redefine how equities are traded

The TD Securities note frames Nasdaq’s tokenization ambitions as a triad of initiatives designed to integrate blockchain-based trading into mainstream markets without waiting for a single, wholesale overhaul of market structure. First, settlement modernization would adapt clearing and custody processes to handle tokenized shares more efficiently after trade execution. This is a prerequisite for reliable, scalable on-chain settlement that can coexist with existing post-trade infrastructure.

Second, Nasdaq is examining mechanisms to issue tokenized shares themselves, potentially enabling corporate issuers to digitalize equity ownership in a way that can be traded on both traditional venues and compatible blockchain networks. Third, the exchange is said to be exploring offshore trading opportunities, effectively enabling tokenized equities to be traded on platforms outside the domestic regulatory perimeter, with Kraken cited as an example of such a venue.

Taken together, these moves imply a market where the “same” stock could be represented and traded across different rails. In practice, that means investors might access tokenized versions of equities in a 24/7 framework outside normal exchange hours, while the same underlying share remains available through standard US listings during regular hours.

For market participants, the implications are twofold. On one hand, the potential for continuous liquidity and new liquidity pools could improve access and price discovery in certain scenarios. On the other hand, the emergence of parallel offshore venues raises questions about regulatory alignment, investor protection, and the coherence of pricing across ecosystems.

Markets adapting to tokenized competition and regulatory risk

Today’s crypto-enabled trading ecosystems already feature a growing set of tokenized equities, with traders increasingly engaging a broader, cross-border audience. Cointelegraph reported that Kraken’s xStocks platform, which provides tokenized versions of publicly traded shares on blockchain-based venues, has surpassed $25 billion in cumulative trading volume, reflecting around 150% growth since November. The momentum underscores a real appetite for around-the-clock access to equities in a tokenized format, even as traditional venues continue to operate within their established hours and rules.

Behind this expansion sits a broader industry trend: the push by major exchanges to experiment with tokenization while contemplating how to regulate, govern, and ultimately integrate these assets with existing equity markets. The NYSE, for its part, has been pursuing tokenization through a partnership with Securitize to develop a platform for tokenized securities that could support extended or non-traditional trading hours. This collaboration mirrors a wider market push toward an “everything exchange” model, where tokenized assets compete for space alongside conventional securities.

From an investor perspective, the emergence of multiple venues tied to the same underlying asset could alter how portfolios are constructed and how risk is assessed. If tokenized shares trade at different prices across regulated and offshore platforms, traders may need to track multiple price signals and navigate potential arbitrage opportunities. The prospect of 24/7 trading, while attractive for liquidity and access, also introduces new layers of risk—especially if regulatory guardrails diverge between venues or jurisdictions.

Regulators will likely weigh the benefits of broader access and innovation against the need to preserve investor protections and market integrity. The current conversation highlights a tension between accelerating tokenization and maintaining a cohesive, transparent market framework. As market participants deploy more tokenized offerings, observers will be looking for alignment in settlement standards, custody controls, and cross-venue price discovery mechanisms.

Beyond Nasdaq and NYSE, other industry players have already begun positioning for tokenized trading. Coinbase has pushed into tokenized stock offerings as part of an “everything exchange” strategy, signaling a competitive push from crypto-native platforms into equity trading. In parallel, NYSE’s collaboration with Securitize points to a broader ecosystem of tokenized securities designed to enable more flexible trading paradigms, including around-the-clock access that challenges traditional market hours.

What remains uncertain is how regulators will reconcile these parallel rails. Will there be harmonized standards for settlement and custody across on-chain and off-chain venues? How will investor protections translate when trading occurs on offshore platforms? And how quickly will price discoveries across venues converge or diverge under a regime of tokenized equities?

In interviews and briefings, contributors like Reid Noch of TD Securities emphasize that while tokenization promises to broaden access and liquidity, it also introduces new complexities. The coming months are likely to bring more concrete regulatory guidance, clearer cross-venue interoperability standards, and perhaps pilot programs that test tokenized trading in controlled environments before any broad rollout.

As the market digests these developments, investors and traders should monitor several cues: the pace at which settlement and custody workflows adapt to tokenized assets, the degree of cross-venue price convergence, and the regulatory responses that could either unlock or constrain offshore trading activity. The balance between innovation and oversight will shape how tokenized equities evolve from experimental concepts into mainstream instruments.

Readers should watch for updates from Nasdaq and NYSE on timing and scope of tokenized trading pilots, along with any new clarity from US regulators on cross-border trading and tokenized securities. The coming months could reveal whether tokenization simply augments existing markets or fundamentally reconfigures how equities are priced, traded, and owned.

Mochi founder Azeem Ahmed sold 550K CVX from a Curve-linked stash as on-chain probes allege over $8M in diverted rewards and $54M in DeFi losses.

Summary

- Mochi Finance founder Azeem Ahmed sold about 550,285 CVX for roughly $946,000, pushing the token down more than 10%.

- The CVX stack traces back to a 2021 Curve pool drain that left liquidity providers with an estimated $54 million in losses.

- Ahmed now faces years of on-chain fraud allegations spanning at least four DeFi projects, with diverted rewards and liquidity drains topping $8 million.

Azeem Ahmed, founder of Mochi Finance and GaiaDAO, has sold approximately 550,285 Convex Finance (CVX) tokens from wallets linked to a 2021 Curve Finance drain, netting around $946,000 and triggering a double‑digit intraday slide in CVX’s price. On March 19, the tokens were liquidated at an average price of about $1.72, sending CVX from roughly $1.88 to $1.68, a drop of more than 10% according to on-chain data reviewed by Crypto Daily. The proceeds were routed to a multisig associated with the Mochi protocol, which held about $864,858 in assets after the sale, while another 500,000 CVX remain locked on Convex Finance.

The CVX position itself originates from Mochi’s controversial November 2021 move to mint its USDM stablecoin against MOCHI and drain roughly $46 million in DAI-equivalent liquidity from the USDM/3CRV pool on Curve. At the time, Mochi used 10 billion MOCHI tokens—assigned a hard‑coded oracle price despite near‑zero market value—to mint 46 million USDM, convert the proceeds into 9,876 ETH, and purchase about 1,050,285 CVX, which were then locked on Convex Finance, according to certified crypto‑trace reports by forensics firm IFW Global. Curve’s Emergency DAO responded by killing Mochi’s gauge and blocking further emissions after characterizing the maneuver as a “clear governance attack,” a clash that became part of the broader “Curve Wars” over CVX and CRV voting power and emissions.

In the aftermath, Ahmed re-emerged through GaiaDAO with a Peg Rebalancing Module (PBM) pitched as a mechanism to distribute CVX staking rewards from the locked position to USDM holders and gradually restore the stablecoin’s peg. The PBM charged a 2% management fee and 20% performance fee payable to Ahmed, but according to Curve governance forum records, he unilaterally hiked the performance fee to 50% before community backlash forced him to reverse the change. By November 2025, reward distributions from the 1,050,285 vlCVX position had stopped entirely, and on-chain data indicates those rewards were rerouted to a wallet that also acts as a signer on the CVX multisig, with the value of diverted staking rewards alone estimated at more than $1.6 million.

Beyond staking flows, investigators allege that about 2,198 ETH—worth roughly $6.67 million at the time—and $471,429 in USDC were drained from Mochi/ETH liquidity pools and never returned to depositors, while airdrops from protocols including Prisma, CNC, VELO, LFT, and YB reportedly remained unclaimed or undistributed. Aggregate investor losses tied to the Mochi ecosystem and its associated pools are now estimated at over $54 million, according to IFW Global’s certified reports.

Ahmed’s track record stretches back to at least 2020 and spans Yieldfarming.insure (SAFE), Armor.fi, Mochi Finance, and GaiaDAO, with repeated accusations of misappropriating community funds. During the original Mochi‑Curve confrontation, Curve alleged that Mochi’s strategy amounted to a governance attack, while Ahmed insisted in an interview with Crypto Briefing that the team had simply taken a “bold approach to gaining voting power in the DAO” and argued that the “DeFi Cartel … feels threatened that a small player on the outskirts” could challenge incumbents. Robert Forster, Ahmed’s former co‑founder at Armor.fi, later accused him publicly of stealing “millions in LP tokens,” a charge Ahmed denied by claiming the funds were “returned in full” and counter‑alleging that Forster had taken money for personal use.

Legal pressure has also followed the on‑chain drama into courts. A prior lawsuit by an Armor.fi user in San Francisco Superior Court (Chen v. Ahmed, Case No. CGC‑21‑589609) ended in an out‑of‑court settlement after a temporary restraining order application, according to filings referenced in IFW Global’s reports. Attorneys now point to potential U.S. claims spanning securities fraud under Section 10(b), racketeering (RICO), common‑law fraud, conversion, and unjust enrichment, and affected investors have been directed to file complaints with the Securities and Exchange Commission, Commodity Futures Trading Commission, and the FBI’s IC3 portal.

Ahmed’s March 19 liquidation is the most aggressive on-chain move from Mochi‑linked wallets since the 2021 Curve incident and is being read by many affected investors as confirmation that the locked CVX will be used for exit liquidity rather than restitution. With roughly 500,000 CVX still locked on Convex Finance and controlled via the same governance structure, any further sales could become major liquidity events for CVX and reignite questions over how DeFi protocols respond when governance power is acquired through exploits rather than open‑market buying. Ahmed, described in IFW documentation as a UK citizen, has not publicly responded to the latest allegations, and his social media profiles have been inactive for months.

US President Donald Trump is set to become the first sitting president in history to have his signature put on US paper currency.

In an announcement on Thursday, the US Department of the Treasury said the move would mark the 250th anniversary of the US. It will put both Trump and Treasury Secretary Scott Bessent’s signatures on future US notes.

“There is no more powerful way to recognize the historic achievements of our great country and President Donald J. Trump than U.S. dollar bills bearing his name, and it is only appropriate that this historic currency be issued at the Semiquincentennial,” Bessent said.

Until now, the tradition has been to put the signatures of the treasurer and the Treasury secretary on US paper currency. This move would mark the first time in history that a sitting president is placing his signature on US currency.

According to a report from Reuters on Thursday, the first $100 bills with Trump and Bessent’s signatures will be printed in June, with other bills following in later months.

Trump’s name and likeness have also made their way to cryptocurrencies, famous landmarks and commemorative coins.

Alongside the Treasury’s plans to put Trump’s signature on US notes, there are also potentially $1 coins with the president’s face on them that could enter circulation as part of the US’s 250th anniversary.

In late 2025, the US Mint released three proposed designs bearing Trump’s face and the caption “In God We Trust.”

Trump has also helped oversee the renaming of major US landmarks such as the John F. Kennedy Center for the Performing Arts.

The board of the Kennedy Center, reportedly filled with Trump appointees, voted in late December to change the name to the “Donald J. Trump and the John F. Kennedy Memorial Center for the Performing Arts.”

Related: SEC is no longer a ‘cop on the beat’ on crypto, says US lawmaker

This has prompted pushback, however, with lawmakers arguing that the move is illegal when done without authorization from Congress.

In the crypto world, Trump has a memecoin named after himself, and also has released multiple NFT projects including the Trump Digital Trading Cards.

Magazine: Clarity Act risks repeat of Europe’s mistakes, crypto lawyer warns

Mezo will stream 2.25% of MEZO supply to Aerodrome’s veAERO voters over 30 days, betting Base’s vote-escrow whales can bootstrap deep MEZO and MUSD liquidity for Bitcoin DeFi.

Summary

- Mezo will route 2.25% of MEZO supply to Aerodrome’s veAERO voters over 30 days to seed MEZO and MUSD liquidity on Base.

- The campaign follows Mezo’s “Bring Bitcoin Home” push, which migrated roughly $23 million in BTC assets and helped lift its TVL to about $76.3 million.

- By plugging into Aerodrome’s vote-escrow flywheel, Mezo is betting Bitcoin can host the same deep, incentive-driven liquidity that has made Base one of DeFi’s fastest-growing hubs.

Mezo, a Bitcoin (BTC)-native lending layer, has struck a strategic deal with Aerodrome Finance, the largest decentralized exchange on Coinbase’s Base network, to make Aerodrome the primary DeFi liquidity hub for the MEZO token. Under the agreement, Mezo will allocate 2.25% of total MEZO supply to veAERO voters over a 30-day period, aiming to bootstrap deep, decentralized liquidity for both MEZO and MUSD, its Bitcoin-backed stablecoin. Aerodrome already anchors Base’s liquidity, having previously pushed its own total value locked (TVL) past $1 billion amid a surge in AERO emissions-driven yield.

Mezo taps Aerodrome’s veAERO to grow MEZO, MUSD

The move is explicitly designed to pull Base’s most sophisticated vote-escrow capital into Bitcoin’s emerging DeFi stack. Aerodrome’s veAERO voter base includes protocols, high-net-worth traders, and institutions such as Coinbase Ventures and Animoca Brands, which have used AERO’s ve(3,3) governance model to direct emissions and fees toward the most productive pools. “Aerodrome’s community wrote the playbook for sustainable DeFi yield through vote-escrow economics,” Mezo founder and CEO Matt Luongo said. “We partnered with them because we wanted that audience to see what happens when you apply those mechanics to Bitcoin. Their users understand the model better than anyone. Now we’re giving them a reason to expand their capital across.”

By directing veAERO voters to MEZO and MUSD pairs, Mezo is effectively importing a proven liquidity engine from Base into Bitcoin DeFi. Mezo’s own “Aerodrome for Bitcoin lending” design channels borrower interest on MUSD loans, origination charges, and DEX swap fees into yield for BTC lockers, who currently earn around 4% APR through incentives and rewards. That sits against a broader DeFi backdrop where sector-wide TVL rebounded to roughly $129 billion in 2024, up 137% year-on-year as rising crypto prices and cheaper Layer-2 infrastructure pulled capital back on-chain.

The Aerodrome Finance tie-up comes on the heels of Mezo’s “Bring Bitcoin Home” campaign, which migrated about $23 million in tBTC, cbBTC, WBTC, and USDT from Ethereum pre-deposit vaults on Mellow Protocol into Mezo’s mainnet, with deposits routed via DeFi yield network Turtle Club. Mezo’s TVL now sits near $76.3 million, with roughly $500 million in lifetime MUSD volume, more than 2,000 loans issued at a fixed 1% APR, and over 43,500 mainnet users. That footprint is still small next to leaders like Aerodrome or top DeFi chains tracked by dashboards such as DeFiLlama, but it signals growing appetite for Bitcoin-first yield strategies as BTC itself becomes a larger share of total DeFi TVL.

Behind the yield mechanics, Mezo has focused heavily on infrastructure, security, and institutional access. Its validator set includes P2P, Chorus One, and Everstake, while smart contracts have been audited by Quantstamp and Thesis Defense. Anchorage Digital provides custody and compliance rails for larger allocators, a piece traditional institutions increasingly prioritize when deploying into DeFi. On the capital side, Mezo has raised $28.5 million in seed funding led by Pantera, with Multicoin, Paradigm, Polychain, Draper, Nascent, a16z, and ParaFi among backers, placing it alongside other BTC-centric projects that venture firms have backed to capture the next leg of on-chain credit markets.

Bitcoin’s role in DeFi expanding

As Bitcoin’s role in DeFi expands, Mezo is positioning itself as the lending and liquidity layer that lets BTC holders borrow, earn, and deploy capital without leaving the Bitcoin economy. Its core products — MUSD, veBTC yield positions, and a native DEX — mirror the stack that has helped Base and Aerodrome dominate liquidity and trading in their own ecosystem. With Aerodrome’s veAERO voters now financially incentivized to seed MEZO and MUSD pools, Mezo is effectively testing whether the same vote-escrow incentives that drove Base’s growth can be replicated atop Bitcoin and its wrapped representations, potentially shifting a larger slice of DeFi’s $100 billion-plus collateral base toward BTC-backed credit.

XDC price is consolidating just above $0.03 as tokenized debt deals, trade-finance pilots and an Ethereum-aligned upgrade deepen its role in enterprise RWA infrastructure.

Summary

- XDC Network is trading around $0.032 per token, with a market cap near $640 million and 24-hour volume in the mid-teens of millions.

- Price has inched higher by roughly 2–3% over the last day, but remains down on the week, reflecting a slow grind after a broader altcoin pullback.

- Recent upgrades, tokenized debt deals and trade-finance pilots signal growing real-world asset usage even as speculative flows stay modest compared with higher-beta altcoins.

XDC Network (XDC), a hybrid Layer-1 focused on enterprise and trade-finance applications, is currently changing hands at about $0.032 per coin, according to both Binance and third-party price aggregators. Binance lists the live XDC price at $0.03206, with a market capitalization of roughly $639.15 million and 24-hour trading volume of $16.29 million, based on a circulating supply of 19.94 billion XDC. A parallel snapshot from 3Commas shows XDC at $0.03214, a 2.8% gain over the last 24 hours, on a $14.73 million trading volume and market cap of $640.9 million.

Historical data from Yahoo Finance place XDC’s recent trading range between $0.0304 and $0.0324 over the past several sessions, underscoring how the token has been consolidating just above $0.03 after earlier weakness in March. CoinMarketCap’s price-history table likewise records daily closes clustered in the $0.031–$0.034 band throughout early March 2026, with no single breakout day but a sequence of tight ranges. That pattern contrasts with the sharp spikes seen in high-volatility memecoins, and instead reflects more measured spot flows into and out of a large-cap infrastructure asset.

Under the hood, XDC Network markets itself as an EVM-compatible, enterprise-grade blockchain for real-world asset tokenization, cross-border payments and trade-finance settlement, placing XDC in the RWA and L1 categories rather than pure DeFi or meme segments. CoinGecko reports a circulating supply of 16 billion XDC in another widely used dataset, with a fully diluted valuation of roughly $3.49 billion assuming a maximum supply of 38 billion tokens. That configuration gives XDC one of the larger RWA/L1 market caps, even if daily volume remains below the most aggressively traded smart-contract platforms.

February’s XDC Network update outlined several major developments that help explain why institutions are watching the chain even as price moves remain subdued. The network completed its v2.6.8 “Cancun” upgrade at block 98,800,200, aligning with Ethereum’s Cancun standard and introducing EIP-1559-style fee mechanics, improved EVM efficiency, and stronger consensus performance on mainnet. Separate to the protocol changes, XDC supported a $75 million tokenized debt issuance in Brazil, expanding its Latin American footprint and positioning the chain as a settlement layer for structured credit in emerging markets.

The combination of hybrid architecture, compliance-by-design tooling and EVM compatibility has led some industry observers to describe XDC as part of a blueprint for institutional-grade blockchain adoption in 2026. At the same time, market data from CoinGecko show 24-hour XDC trading volume around $46.1 million on certain days, a figure that has recently risen by over 11% in a single session, signalling that liquidity is gradually deepening as more venues list the token.

Cross-border payment infrastructure provider Tazapay said it closed an extension to its Series B funding round led by Circle Ventures, bringing the total raised to $36 million. The round included participation from Coinbase Ventures, CMT Digital, Peak XV Partners and Ripple.

Tazapay said on Thursday that the funding will be used to • expand its digital settlement technology for cross-border payments, secure additional licenses, expand across Asia, Latin America, the Middle East and the Americas, and build infrastructure for so-called “agentic payments.”

Tazapay said it serves over 1,000 enterprises and fintechs across 30 countries. It holds licences across Singapore, Canada, Australia, and the United States, with active applications underway in the European Union, United Arab Emirates and Hong Kong.

“The demand we’re seeing from enterprises and fintechs across Asia, LATAM, and the Middle East is unmistakable; businesses want to move money faster, cheaper, and with full regulatory confidence,” said Kanupriya Sharda, chief business officer at Tazapay.

Cointelegraph asked Tazapay whether it would disclose the size of the extension tranche and the company’s valuation, but had not received a response by publication.

Stablecoin payment infrastructure draws backers

The extension comes as crypto and fintech firms push deeper into stablecoin-based cross-border payments infrastructure.

On March 3, Ripple said it had expanded Ripple Payments into an end-to-end stablecoin and fiat platform for banks and fintechs. The company said the platform is live in more than 60 markets and has processed more than $100 billion in volume.

Related: Ripple joins Singapore sandbox to test RLUSD in trade finance

In May 2025, Boston-based cross-border payment company Conduit raised $36 million in a Series A funding round led by Dragonfly and Altos Ventures to scale its payment system and expand fiat and stablecoin currency offerings.

Conduit positions its payment system as an alternative to the SWIFT messaging network, which banks have relied on to process wire transfers since the 1970s.

Magazine: Crypto wanted to overthrow banks, now it’s becoming them in stablecoin fight

SIREN is trading near $2.35 after a 340% weekly spike to a $1.8b valuation, with one wallet cluster holding 88% of supply and nearly $1b in unrealized profit.

Summary

- SIREN trades around $2.35 after a volatile week that saw the token jump more than 340% and briefly surpass a $1.8 billion market cap.

- Trading volume remains elevated in the $50 million range over the last full day, but on‑chain data shows one cluster still controls roughly 88% of circulating supply.

- Analysts warn concentration and unrealized profit in whale wallets could amplify downside, even as SIREN remains one of the most talked‑about BNB Chain meme tokens this week.

SIREN, a BNB Chain meme coin built around high‑volatility speculation, is changing hands near $2.35 today after a week in which its price jumped from below $0.90 to above $3.00 before retracing. Historical data from CoinLore shows SIREN closing at $0.9422 on March 21, 2026, then $2.30 on March 22, and $2.35 on March 23, marking a gain of roughly 149% in 48 hours and over 340% across the week. Over that same March 22–23 window, reported daily trading volume ranged between about $53.7 million and $195 million, locking SIREN into the top tier of actively traded meme assets on BNB Chain.

MEXC’s market wrap notes that SIREN’s fully diluted valuation pushed past $1.8 billion at the height of the rally, driven by aggressive spot buying and options‑style speculation. Yet Arkham and Dune Analytics data cited in that report highlight a single wallet cluster holding around 644 million SIREN tokens, or roughly 88% of circulating supply, with more than $950 million in unrealized profit at peak prices. A separate technical summary from CoinCodex places SIREN’s daily relative strength index around 64.78, with multiple simple and exponential moving averages still flashing “buy,” underscoring how momentum indicators remain elevated despite the recent pullback.

Headline‑driven price action has also pulled SIREN into broader meme‑coin narratives. BeInCrypto recently listed Siren among three meme tokens to watch into the final week of March 2026, citing its outsized weekly move compared to other BNB Chain names. In that context, SIREN’s profile now sits alongside other speculative meme assets covered by outlets like crypto.news, which has tracked similar surges in tokens such as PEPE and BONK during prior market risk‑on phases.

The race to make blockchains quantum-resistant is shaping into a test of governance, and decentralized networks may be at a disadvantage.

Quantum upgrades don’t stop at protocol-level changes. For major networks, they require wallet-level migration across millions of users, making coordination the bottleneck.

“The hard part is not changing the node itself, it’s having the wallets do the same,” said Yoon Auh, founder of BOLT Technologies, adding that each asset holder would need to migrate and do so in a coordinated way.

“If you go talk to Bitcoin or Ethereum, it’s a bit more perplexing because of the really decentralized and kind of ad hoc participation. It seems like whenever I hear about it, it’s more like herding cats.”

A sufficiently powerful quantum computer could theoretically break the public-key cryptography that underpins digital signatures and secure communications, threatening both blockchain wallets and core financial infrastructure.

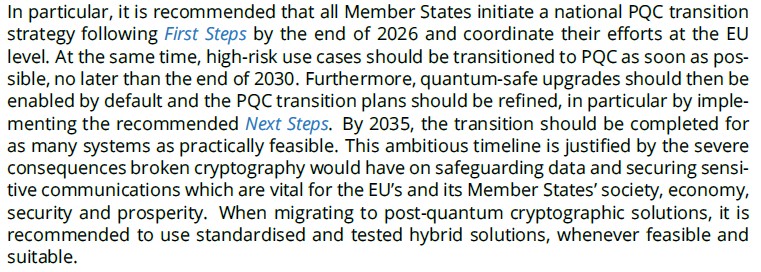

Post-quantum cryptography (PQC) is the proposed countermeasure, and the transition is already underway. The National Institute of Standards and Technology (NIST) has urged organizations to begin preparing for “harvest now, decrypt later” threats, while US policy sets 2035 as the target for completing migration across federal systems.

Institutional governance is accelerating quantum upgrades

One place coordination may be easier is in institutional blockchain networks, where governance is tighter and the chain of authority is clearer.

Auh’s BOLT Technologies is running a pilot with the Canton Network to test a system that allows institutions to use and switch between multiple cryptographic signature schemes. Canton describes itself as an open blockchain for regulated institutions, designed to let participants exchange data and value without giving up privacy or control.

In regulated financial markets, infrastructure changes must meet internal controls, risk management standards, privacy requirements and interoperability demands across firms.

Canton is built around those constraints, positioning itself as infrastructure for regulated institutions and a way to connect siloed financial systems without sacrificing control.

In August 2024, NIST finalized its first set of post-quantum cryptography standards and explicitly urged system administrators to begin transitioning to them as soon as possible.

For regulated institutions, that kind of guidance makes delays harder to justify. Once migration becomes a recognized security and compliance issue, the networks most likely to move first are the ones that can turn technical advice into a managed operational process. Auh said that is one reason permissioned networks may be better positioned to move first.

“Because of their governance structure, you only need a few people there who are very knowledgeable to understand what’s going on,” he said. “And then because their governance is a lot quicker and a lot more organized, you can make those changes quicker.”

That does not mean permissioned networks have solved the post-quantum problem. It means they may be better equipped to test, approve and stage upgrades under real-world constraints.

Related: Banks will run RWAs on two blockchain rails, says RedStone co-founder

Coordination slows quantum upgrades on public networks

Public blockchains face a different coordination problem because major protocol changes cannot be approved by a small governing group.

On Bitcoin, protocol changes are suggested through the Bitcoin Improvement Proposal (BIP) process, and the project’s own documentation says that “acceptance and adoption rests with the Bitcoin users.”

That makes a system-wide cryptographic migration harder to stage on public chains than on permissioned ones.

Given these coordination constraints, a post-quantum upgrade may require more disruptive upgrade paths, including a hard fork.

“I think it’s a very difficult thing to do with a soft fork,” he said. “They’re going to have to take the bitter medicine at some point and do a hard fork.

I know that it’s very traumatic for something like Bitcoin.”

On Ethereum, core changes move through the EIP process, where authors are expected to build consensus within the community and document dissenting opinions.

Ethereum’s governance documentation describes a process involving multiple stakeholder groups, including node operators, validators and EIP authors, while the AllCoreDevs process exists to coordinate technical work across contributors from different organizations.

Related: Are quantum-proof Bitcoin wallets insurance or a fear tax?

The real challenge in quantum migration is coordination

The post-quantum transition is often framed as a technical race to find the right cryptography, but the harder question may be whether a network can carry out the migration at all.

Auh said the industry should spend less time trying to predict the exact arrival of a cryptographically relevant quantum computer — often called “Q-Day” — and more time thinking about whether blockchain networks are structurally capable of responding.

“The recognition of the risk should spur you into action,” he said, arguing that preparation matters more than timeline guessing.

For permissioned blockchains, that process can be channeled through tighter governance, formal approval paths and institutional pressure to act. For public chains, the same migration has to pass through a wider and slower process shaped by developers, client teams, wallet providers and users.

General investors are more likely to focus on post-quantum readiness for networks like Bitcoin and Ethereum, whose growth has tracked the broader industry, though views on the risk remain split. Jefferies strategist Christopher Wood removed Bitcoin from a model portfolio, citing quantum concerns, while Blockstream CEO Adam Back has said the threat may still be decades away.

Magazine: Bitcoin may face hard fork over any attempt to freeze Satoshi’s coins

Kite is trading around $0.21–$0.22 with ~$400m market cap as profit‑taking and a broader AI‑token cooldown knock the AI payment chain about 30% off its early‑March high.

Summary

- Kite trades near $0.21–$0.22 with market cap around $400 million and 24h volume between roughly $114 million and $152 million.

- The AI-focused token sits around 30% below its early March all-time high near the $0.30–$0.32 range after a series of sharp rallies.

- Heavy volume, rapid gains since late 2025 and a broader cooldown in AI crypto have combined to push recent profit-taking.

Kite (KITE), a token tied to an AI-centric blockchain and payments ecosystem, is changing hands around $0.21–$0.22 today, easing back after a stretch of explosive gains. CoinMarketCap lists KITE at approximately $0.2148 with a 24-hour trading volume of $114.68 million and a live market capitalization of about $394.2 million, based on a circulating supply of 1.83 billion tokens. MEXC’s latest market note shows Kite trading at $0.22, up 20.3% in a prior 24-hour rally that saw volume hit $152.78 million, with the token briefly topping the platform’s gainer list. Those shifts underscore how quickly capital has rotated into and out of KITE as traders chase momentum.

Recent price action marks a comedown from early March highs. Phemex reported on March 5 that Kite surged 26% to a new all-time high, pushing above $0.30 amid what it described as strong market participation. By comparison, current prices near $0.21–$0.22 leave KITE roughly 30% off that peak, even as it remains up sharply versus late-2025 levels. Earlier coverage from AInvest highlighted Kite’s “market debut” in late 2025, noting rapid appreciation from initial listings and positioning the token as a high-beta AI play.

Kite is marketed as an AI-focused infrastructure and payments token, aligning it with the broader cluster of AI-related cryptocurrencies that saw outsized gains in late 2025 and early 2026. Binance’s coverage of the token’s early trading framed KITE as part of a wave of “AI payment chain” assets that rebounded alongside sector-wide AI sentiment. Mitrade’s February 2026 brief, titled “Kite Price Forecast: KITE surges 14%, outpacing other AI crypto tokens,” noted that Kite was outperforming its AI peers during that period, reflecting strong speculative demand. Together, those data points place KITE within the AI and infrastructure category rather than in DeFi or memecoin niches.

While detailed on-chain whale analytics for Kite are limited in public dashboards, the size and persistence of recent volume spikes hint at substantial large-trader participation. MEXC’s report emphasizes that KITE’s single-day volume of $152.78 million represented a jump of more than 70% versus its prior average, suggesting both new entries and active profit-taking. CoinMarketCap’s volume figures, consistently above $100 million in recent sessions, support the view that price swings are being driven more by short-term trading flows than by slow, organic accumulation.

Kite’s trajectory also mirrors a broader cooling in AI crypto after an overheated start to 2026. Sector-wide pieces have documented how AI tokens rallied aggressively before giving back part of their gains as traders reassessed valuations and rotated into other narratives. For readers tracking performance in real time, the Kite price page on the crypto.news market-cap dashboard offers live quotes, market cap and volume metrics, and can be used to compare KITE’s volatility and liquidity against other AI-focused tokens and major benchmarks like Bitcoin and BNB.

Stand With Crypto (SWC), the advocacy organization launched by cryptocurrency exchange Coinbase, said that its strategy for turning out crypto-minded voters in the 2026 US midterm elections will prioritize races in Ohio and Pennsylvania.

In a Thursday announcement, SWC said its November 2026 battleground races would include industry-supported candidates in Iowa, Nevada, New York, North Carolina, Ohio, and Pennsylvania, where “crypto voters represent a meaningful and potentially decisive share of the electorate.”

The advocacy group added that its priority for the midterms would be in Ohio’s 9th Congressional District and Pennsylvania’s 10th Congressional District, where the respective incumbents Democrat Marcy Kaptur and Republican Scott Perry “have concerning records on crypto policy.” Perry voted against the GENIUS Act in 2025, while Kaptur voted against the payment stablecoins bill and the CLARITY market structure bill.

Stand With Crypto said it would use an “aggressive, get-out-the-vote effort” with its advocates, including “paid media campaigns across digital and direct mail, targeted SMS outreach, and robust digital organizing through email and social platforms” as well as groundwork to turn out crypto voters. The group’s platform includes information on candidates’ positions on crypto policy based on their public statements, voting records and their responses to the organization’s questionnaire.

Launched in 2023 as part of an effort to “unite global crypto advocates,” SWC is one of several crypto-affiliated organizations expected to influence voters in 2026. The group reported about 270 “pro-crypto” candidates won seats in the US House of Representatives and Senate in 2024, with many of the same candidates up for reelection this year.

Related: Crypto-backed PAC spends $8.6M in Illinois races ahead of US midterms

Stand With Crypto said in November 2025 that how US lawmakers vote on a crypto market structure bill could impact their reelection prospects. At the time, the Senate was expected to move forward on market structure legislation, but it is still unclear if or when the bill will advance out of committee and for a full floor vote.

“[As] market structure legislation continues to be negotiated in Congress, 74% of crypto owners say they would be more likely to support a candidate who supports making clearer regulations for cryptocurrency, with nearly a third (31%) who say they would be much more likely to support such a candidate,” SWC said as part of a February survey of 1,000 crypto holders.

2026 races seen testing crypto industry’s impact on candidates

Money from the crypto industry funneled through political action committees (PACs) like Fairshake may have already influenced 2026 voters in early state primaries.

Protect Progress, a Fairshake affiliate spent $1.5 million opposing the reelection of Texas Representative Al Green, who has served in Congress since 2005. Although Green did not lose the Democratic primary, he will head to a runoff with Christian Menefee in May. SWC rated Menefee as “strongly supports crypto.”

However, in Illinois, Lieutenant Governor Juliana Stratton won the Democratic Senate primary against Representatives Raja Krishnamoorthi and Robin Kelly. The victory came despite crypto-tied lobbyists spending millions of dollars on media buys supporting Krishnamoorthi. Stratton is expected to win in the general election and take the seat of retiring Democratic Senator Dick Durbin.

In 2024, Ohio saw some of the biggest spending from the crypto industry and other PACs to unseat Senator Sherrod Brown. Although the Democrat lost to Republican Bernie Moreno, he announced in August 2025 that he plans to run again, potentially leading to the industry eyeing the US state as a battleground for crypto.

“I would assume given the politics and the candidates in Ohio that there will be a s–tload of money spent here again,” former Ohio Representative Tim Ryan, who also sits on Coinbase’s Global Advisory Council, told Cointelegraph.

Magazine: The dirty secret about quantum signatures: No one knows if they work

Elon Musk’s X has hired crypto-native product designer Benji Taylor as its new head of design, ahead of a wider rollout of the platform’s X Money payments product next month.

Taylor announced the move on X on Wednesday, saying he was “honoured” to join the company and looking forward to working closely with Musk and X’s head of product Nikita Bier. Taylor’s crypto-native background is notable, previously founding Los Feliz Engineering, a consumer software studio that was acquired by decentralized lending protocol Aave Labs in 2023.

Bier said that he had followed Taylor’s work for years and knew that he was “on track to become one of the best designers in the world,” and that X was “finally teaming up and building the greatest design team in the industry.”

The appointment comes as X prepares to expand X Money, an integrated payments and financial services layer that will introduce peer-to-peer payments, wallet services and a debit card tied to user accounts.

Aave and Base roles

After the Aave acquisition in 2023, Taylor became chief product officer until October 2025, according to his LinkedIn profile, overseeing the company’s product strategy and development for its decentralized lending protocol and related applications.

Before joining X, he led design for Coinbase’s Ethereum layer-2 network Base, where he was responsible for the network’s product and interface design across its user and developer-facing experiences. He earlier served as senior vice president of product and design at Avara, the renamed Aave Companies group.

Related: Musk confirms X Money beta testing ahead of planned 2025 launch

X Money rollout

The timing also stands out. In early March, Musk announced that X Money would begin public access next month, as an integrated payments and financial services layer for the social platform.

The product is currently in limited external beta and offers users a 6% annual percentage yield on cash balances held in an X Money wallet, a personalized metal Visa debit card engraved with the user’s X handle, and peer-to-peer payments linked directly to the X app.

Musk has described X Money as part of his plan to turn the platform into an “everything app” that combines social networking, messaging and financial services.

Magazine: How crypto laws changed in 2025 — and how they’ll change in 2026

Starmer makes pathetic excuses for McSweeney

‘The Pitt’ Just Reached a 5-Minute Breaking Point That Changes Everything

Man arrested for sexually assaulting fan during Gunna’s O2 Arena concert

-

Crypto World6 days ago

Crypto World6 days agoNIO (NIO) Stock Plunges 6.5% as Shelf Registration Sparks Dilution Worries

-

NewsBeat2 days ago

NewsBeat2 days agoManchester United reach agreement with Casemiro over contract clause amid transfer speculation

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Adidas – Corporette.com

-

Politics6 days ago

Politics6 days agoJenni Murray, Long-Serving Woman’s Hour Presenter, Dies Aged 75

-

Crypto World5 days ago

Crypto World5 days agoBest Crypto to Buy Now: Strategy Just Spent $1.57 Billion on Bitcoin During Fear While Early Investors Quietly Enter Pepeto for 150x Potential

-

Crypto World5 days ago

Crypto World5 days agoBitcoin Price News: Bhutan Sells $72 Million in BTC Under Fiscal Pressure, but the Smart Money Entering Pepeto Sees What the Market Does Not

-

Tech7 days ago

Tech7 days agoinKONBINI Lets You Spend Summer Days Behind the Register

-

News Videos23 hours ago

News Videos23 hours agoParliament publishes latest register of MPs’ financial interests

-

Sports4 days ago

Sports4 days agoRemo Stars and Kano Pillars Strengthen Survival Hopes in NPFL

-

Sports4 days ago

Sports4 days agoGary Kirsten Accuses Pakistan Cricket Board Of ‘Interference’, Mohsin Naqvi Responds

-

Tech4 days ago

Tech4 days agoGive Your Phone a Huge (and Free) Upgrade by Switching to Another Keyboard

-

Business4 days ago

Business4 days agoNo Winner in March 21 Drawing as Prize Rolls to $133 Million for Next

-

Sports6 days ago

Sports6 days ago2026 Kentucky Derby horses, odds, futures, preview, date: Expert who nailed 12 Derby-Oaks Doubles enters picks

-

Tech4 days ago

Tech4 days agoAI enters the chat: New Seattle dating app relies on tech to facilitate meaningful human connections

-

Business6 days ago

Columbia Sportswear enters $500 million credit agreement with JPMorgan Chase

-

Tech5 days ago

Tech5 days agoToday’s NYT Connections Hints, Answers for March 22 #1015

-

News Videos4 days ago

News Videos4 days agoCh 9 Financial Management Part 1 | Detailed One Shot | Class 12 Business Studies Boards 2026

-

Business5 days ago

Business5 days agoWill Duke Basketball Win It All? Duke Basketball Enters Second Round as Third Favorite to Claim NCAA Title

-

Business5 hours ago

Business5 hours agoInstagram, YouTube Found Responsible for Teen’s Mental Health Struggle in Historic Ruling

-

Crypto World6 days ago

Crypto World6 days agoSmall-cap Russell 2000 enters correction territory

You must be logged in to post a comment Login