Crypto World

No Email, No Account, No KYC: How GhostSwap Swaps 1,600+ Coins in One Step

The traditional crypto exchange experience is anything but simple. You need to create an account, then verify your email, and submit identity documents. Then wait for approval and set up two-factor authentication. Deposit funds. Withdraw to your wallet. The process can take days and goes on and on before you actually own the asset you wanted.

For many users, this process can be completely unnecessary. Not everyone wants to trade on margin or place limit orders. Some just want to swap one cryptocurrency for another; quickly, privately, and without the overhead of creating yet another online account.

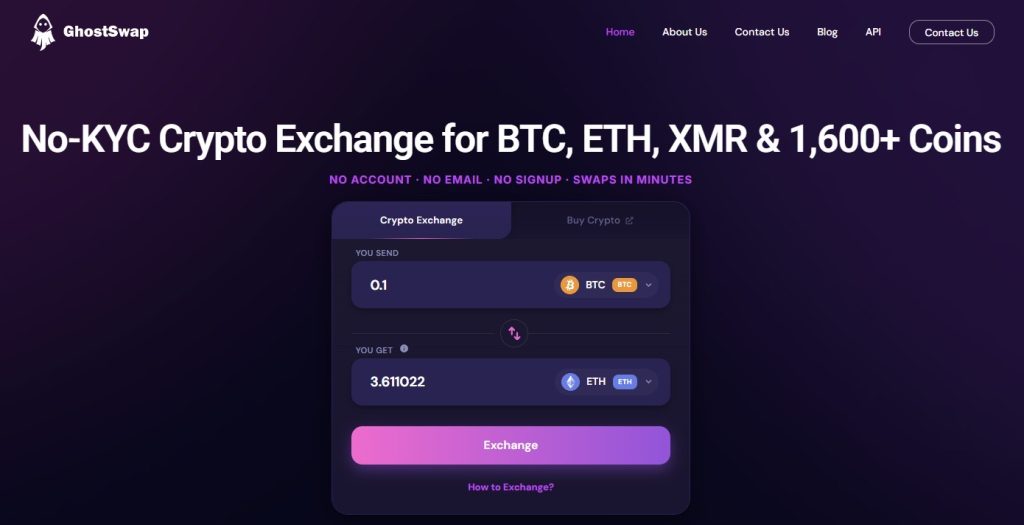

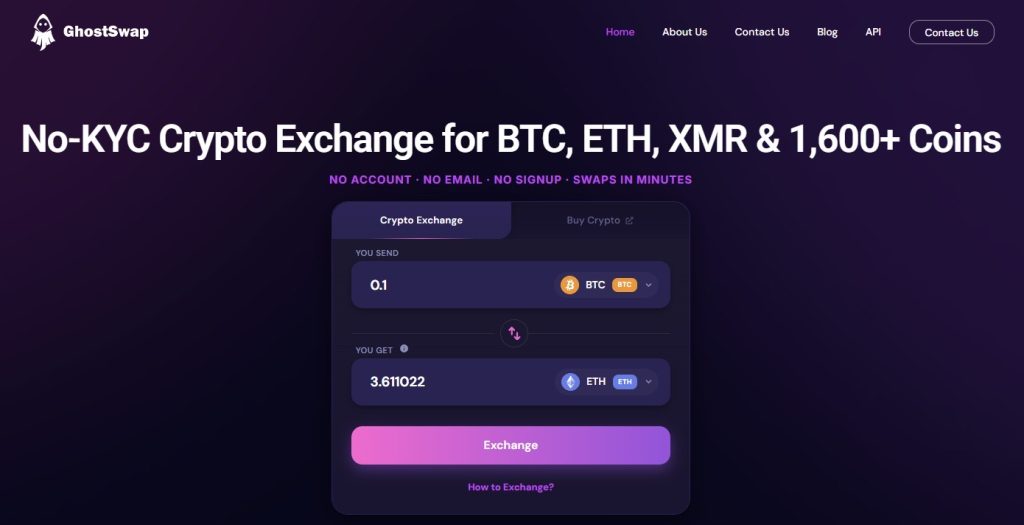

GhostSwap offers exactly that. It’s a non-custodial “instant swap” platform that lets users exchange cryptos without creating an account or providing personal information.

The process actually can’t be more simple: choose a pair, enter a destination address, send the source coin to a one-time deposit address, and receive the new coin, typically within minutes. No email, and no KYC. Just a swap.

What Is GhostSwap?

GhostSwap is a non-custodial swap aggregator that connects user transactions across multiple liquidity sources to find the best available rate. GhostSwap never takes long-term control of user assets, unlike centralized exchanges. Funds move directly from the user’s wallet through the swap process and land in the destination wallet.

GhostSwap supports over 1,600 tokens across major blockchains, including Bitcoin, Ethereum, Solana, Polygon, and (maybe most importantly) privacy-focused assets like Monero (XMR) and Zcash (ZEC). This deep support for privacy coins sets GhostSwap apart from many competitors that have delisted these assets due to regulatory pressure.

Key features, or let’s say, unique selling points, include:

- No signup, no email, no KYC for standard swaps

- 1,600+ supported assets across multiple chains

- Telegram bot for swaps without leaving the messaging app

- Public API for developers and business integrations

- Flat 2% fee quoted upfront, included in the exchange rate

GhostSwap has processed over $750 million in swaps for around 1.5 million users. The company is registered as a Delaware LLC and operates as an anonymous crypto exchange that prioritizes user privacy and simplicity.

How GhostSwap Works

The user experience is intentionally minimal. Here’s what actually happens during a swap:

Step 1: Choose the Coins You Want to Swap

Users begin by selecting a coin to send and a coin to receive from drop-down menus. The interface supports cross-chain swaps, for example, Bitcoin to Solana or Ethereum to Monero. The source and destination assets can be on completely different blockchains; GhostSwap handles the bridge behind the scenes.

Step 2: Enter a Destination Wallet Address

The only information GhostSwap requires is a receiving wallet address for the output coin. There’s no account creation, no email verification, and no identity documents. Just paste the address where you want your funds to land.

Step 3: Send Your Crypto

Once the user confirms the swap details, GhostSwap generates a unique one-time deposit address. The user sends their source coin to this address directly from their own wallet. The address is temporary and tied exclusively to that specific transaction.

Step 4: Receive the New Asset

After the blockchain confirms the deposit, GhostSwap’s backend automatically executes the swap across its liquidity sources and sends the output coin to the user’s provided destination address. The entire process is on-chain and non-custodial.

Step 5: Verify the Transaction

Users can track their swap’s progress through GhostSwap’s status page or, if using the Telegram bot, through real-time updates in the chat. Once the transaction is complete, the funds are in the user’s wallet; no further action required.

Typical completion times range from a couple of minutes for fast chains like Solana or Polygon to about 30 minutes for slower chains like Bitcoin, depending on network congestion. GhostSwap warns users to have a bit of the chain’s native gas token (e.g., ETH) in their sending wallet to cover network fees.

The User Experience: What Makes GhostSwap Different?

Compare the GhostSwap workflow to a traditional exchange:

Traditional Exchange:

- Create account

- Verify email

- Complete KYC (submit ID, wait for approval)

- Set up 2FA

- Navigate to trading pair

- Place order

- Wait for execution

- Withdraw to wallet

GhostSwap:

- Select pair

- Enter destination address

- Send funds

- Receive coins

That’s it. Four steps instead of eight or more. No password management, no identity verification, no account recovery processes to remember. Fewer steps between intent and execution means less friction and a faster experience.

Supported Coins, Networks, and Privacy Assets

GhostSwap supports over 1,600 coins and tokens across numerous blockchains. The platform’s official documentation promotes cross-chain swaps, for example, Bitcoin to Solana or Ethereum to Polkadot, and specifically lists privacy coins like Monero (XMR) and Zcash (ZEC) among supported assets.

Monero (XMR) support: GhostSwap includes XMR as both a send and receive option. Pairs like BTC to XMR and ETH to XMR are listed among the platform’s top offerings. For users who value financial privacy, this is a pretty big advantage; Monero is the leading privacy coin, and its availability on GhostSwap means users can move in and out of it without creating a paper trail on a centralized exchange.

Zcash (ZEC) support: Similarly, Zcash appears in GhostSwap’s supported pairs list (BTC to ZEC, ETH to ZEC, USDT to ZEC, etc.) on the platform’s “All pairs” page. Zcash offers shielded transactions that hide sender, receiver, and amount; another option for privacy-conscious users.

The platform aggregates liquidity from multiple providers, so depth varies by coin. No official liquidity numbers are published, but GhostSwap claims to find “the best rates across multiple liquidity providers.” For smaller swap sizes (e.g., under several BTC worth), adequate liquidity should be available.

Privacy coins may be more thinly traded on global markets than majors like BTC or ETH, but GhostSwap’s aggregator model helps source liquidity where it exists.

GhostSwap’s Fee Structure

GhostSwap charges a flat 2.0% baseline fee (spread) on every swap, built directly into the quoted rate. Users see this fee upfront as part of the exchange rate and the final receive amount. For example, on a $10,000 swap, the implied cost is roughly $200, plus normal on-chain gas fees.

How the Fee Is Quoted Upfront

When a user selects a pair and enters an amount, the interface immediately shows the estimated output amount and the total fee. GhostSwap explicitly highlights that all fees are “included directly in the exchange rate displayed” before confirmation; no hidden charges appear at checkout.

Are There Additional Costs?

Standard blockchain network fees (miner/gas fees) are extra and come from the user’s wallet. These are not GhostSwap fees but rather costs inherent to sending any on-chain transaction. Additionally, if the market moves dramatically before the deposit confirms, extreme cases of slippage could occur; though GhostSwap does re-quote if confirmations take a long time.

Comparing Fixed-Fee Simplicity to Exchange Pricing

GhostSwap’s 2% fee is higher than some competitors. Changelly advertises fees around 0.25%, Godex charges approximately 0.5%, and FixedFloat offers 1% for fixed-rate and 0.5% for floating-rate swaps.

However, these platforms may not support the same range of privacy coins, may require accounts for certain features, or may have less transparent fee structures. GhostSwap’s simplicity (one flat rate, no tiers, no surprise charges) is good for users who want to know exactly what they’re paying before they commit.

Is GhostSwap Legit?

This is arguably the most important question for any user considering a new crypto platform.

What “Legit” Means in Crypto Swapping

In the context of instant swaps, legitimacy doesn’t mean guaranteed safety or regulatory approval. It means the platform delivers what it promises (fast, private, on-chain swaps) without scamming users or failing to execute transactions.

Signs That Users Commonly Look For

GhostSwap provides a public website and extensive documentation, a transparent swap process, a published API, a functional Telegram bot, and user-facing support channels. The platform has been operational for years and has processed over $750 million in swaps for approximately 1.5 million users.

Independent reviews and user reports generally confirm that swaps execute as advertised.

The Non-Custodial Element

GhostSwap is strictly non-custodial. It never takes long-term custody of user funds. Instead, each swap goes through a temporary deposit address: the user’s coins are sent from their wallet to this address, and immediately upon confirmation, GhostSwap releases the new coins from an upstream liquidity source into the user’s receiving wallet.

No pooled account is ever held on GhostSwap. This avoids many hacking risks associated with centralized exchanges, where large pools of customer funds become attractive targets.

What GhostSwap Does and Doesn’t Promise

GhostSwap delivers fast, anonymous crypto swaps with minimal friction. It does not promise to be the cheapest option, to provide advanced trading features, or to offer regulatory protection in every jurisdiction. Users should treat it as an advanced tool (ideal for moving privacy coins or cross-chain trades) and use small test amounts until comfortable.

Privacy and KYC: How Does GhostSwap Handle Identity Verification?

A core GhostSwap promise is no KYC. The site and terms repeatedly state that users need provide only a destination address; no name, ID, email, or phone. GhostSwap is an anonymous crypto exchange in the sense that it doesn’t collect identity-linked data from users. As one Binance.com guide puts it, GhostSwap has “zero registration, no identity documents.”

However, “no KYC” does not mean no compliance. GhostSwap is a Delaware-registered LLC and explicitly works with licensed crypto processing partners to handle AML/sanctions screening. In practice, each transaction is shared with these partners for automated checks. If a swap is flagged (e.g., for high value or hitting a blacklist), GhostSwap reserves the right to block, reject, or refund it.

The terms of use warn users that transactions may be subject to AML/KYC compliance “by licensed third parties.”

Information Users Are Not Required to Provide

Information needed to trade on GhostSwap is really simple; no email, no name, no address, no ID documents, no phone number. Users can even access GhostSwap via Tor or VPN without issue, which further enhances privacy.

Situations Where Compliance Obligations Could Arise

If a transaction is flagged by automated systems (often due to large size, unusual patterns, or connections to known suspicious addresses) GhostSwap may delay, block, or refund the swap. In some cases, third-party compliance partners may request additional information. This is relatively rare for standard swaps but is explicitly covered in GhostSwap’s terms.

Security Considerations Before Using Any Instant Swap Service

Even though GhostSwap’s non-custodial design eliminates many hacking risks, users should be aware of the risks that remain:

Verify Wallet Addresses Carefully

Once a transaction is sent to a blockchain address, it cannot be reversed. Mistyping a destination address or selecting the wrong network can result in permanent loss of funds. Always double-check addresses before confirming a transaction.

Double-Check Network Compatibility

Sending a coin to an address on the wrong network (e.g., sending BSC tokens to an Ethereum address) can result in loss. GhostSwap provides warnings, but the final responsibility lies with the user.

Start With a Small Test Transaction

Before swapping a large amount, send a small test transaction to verify that the address is correct, the network is compatible, and the swap executes as expected. This is standard practice in crypto and costs little in fees.

Understand Blockchain Confirmation Delays

Swap completion times depend on network confirmations. Bitcoin transactions can take 10–30 minutes; faster chains like Solana complete in seconds. If a transaction is delayed, it’s usually due to network congestion rather than a platform issue.

Keep Control of Your Private Keys

GhostSwap never asks for private keys. If any platform requests your private keys, it’s a scam. GhostSwap’s non-custodial design means the user remains in control of their funds throughout the process.

Beyond the Website: Telegram Bot and Public API

Using GhostSwap Through Telegram

Launched in 2025, the @GhostSwapBot on Telegram allows swaps without a browser. The bot mirrors the web UI: users start a chat, select coins, enter an amount, paste a destination address, and get a deposit address from the bot.

Real-time updates are shown as the swap proceeds. This integration allows users to swap without even leaving Telegram; a standout feature few swap platforms offer.

The Public API

GhostSwap exposes a server-to-server API for business integrations (wallets, apps). GhostSwap’s API is authenticated by bearer tokens. Key endpoints include:

- /v1/quotes (get price quote)

- /v1/addresses/validate (validate a payout address)

- /v1/swaps (create a swap)

The docs stress idempotency (retry safety) and real-time status polling. Rate limits are generous: up to 120 requests per second per IP and 30 requests per second per API key. Partners can quickly integrate swaps into apps with high throughput.

Why These Tools Matter

The Telegram bot and API expand GhostSwap beyond a standard web interface. Users can swap from anywhere – even from a messaging app – and developers can integrate GhostSwap’s swap functionality into their own applications, wallets, and services.

Who Is GhostSwap Best Suited For?

GhostSwap serves several distinct user profiles:

Privacy-Conscious Users

People who value financial privacy and don’t want their transactions linked to their identity. GhostSwap’s no-KYC model and support for privacy coins like Monero and Zcash make it an attractive option.

Users Making Occasional Swaps

For users who swap crypto infrequently – perhaps a few times a year – creating accounts on multiple exchanges is overkill. GhostSwap’s pay-as-you-go model is ideal for occasional needs.

People Who Want to Avoid Exchange Onboarding

Account creation, email verification, KYC, and 2FA setup can take days. GhostSwap eliminates all of this.

Developers and Service Operators Using the API

Businesses and developers integrating crypto swaps into their applications can use GhostSwap’s API to add swap functionality without building their own liquidity infrastructure.

Users Swapping Into or Out of XMR and ZEC

GhostSwap maintains support for privacy coins that many exchanges have delisted. For users who need to move into or out of Monero or Zcash, GhostSwap provides a reliable option.

Potential Drawbacks and Limitations

GhostSwap is not for everyone. Several limitations are worth noting:

- No advanced trading features: GhostSwap is designed for simple swaps, not trading. There are no order books, charting tools, limit orders, or margin trading.

- Not a full exchange account: Users cannot hold balances on GhostSwap or repeatedly trade without paying the 2% fee each time. It’s a swap service, not an exchange account.

- No order books: Prices are set by GhostSwap’s aggregator engine, not by user orders. Users cannot set their own prices or wait for specific market conditions.

- Dependence on blockchain conditions: Swap speed depends entirely on the underlying blockchain. Users cannot accelerate their swap beyond the chain’s confirmation requirements.

- Fees may not always be cheapest compared to active trading platforms: The 2% flat fee is higher than what a user might pay on an exchange with lower trading fees. For very large or frequent swaps, an exchange account might be more cost-effective.

- Regulatory ambiguity: GhostSwap operates in a regulatory gray zone. No formal licenses or public audits are mentioned. Users in jurisdictions with strict crypto laws should consider the legal implications of using an anonymous crypto exchange.

- Potential for flagged transactions: While GhostSwap itself doesn’t require KYC, its compliance partners may flag and block certain transactions, especially large ones.

Frequently Asked Questions

Do I Need an Account to Use GhostSwap?

No. GhostSwap requires no account, no email, and no password. Users simply select a pair, enter a destination address, and send funds.

Does GhostSwap Require KYC?

No. GhostSwap does not require identity documents, name, address, or phone number for standard swaps. Compliance checks are handled behind the scenes by partners and may occasionally flag transactions.

How Long Do Swaps Take on GhostSwap?

Typical completion times range from a couple of minutes for fast chains (Solana, Polygon) to approximately 30 minutes for slower chains (Bitcoin). Most swaps complete within 5–30 minutes.

Which Coins Are Supported on GhostSwap?

GhostSwap supports over 1,600 coins and tokens across major blockchains, including Bitcoin, Ethereum, Solana, Polygon, Monero, Zcash, and stablecoins like USDT and USDC.

Does GhostSwap Support Monero?

Yes. Monero (XMR) is fully supported as both a send and receive option. Pairs like BTC to XMR and ETH to XMR are available.

What Is the GhostSwap Fee?

GhostSwap charges a flat 2% fee built into the quoted exchange rate. This is the total service fee; users also pay standard blockchain network fees (gas).

Can I Use GhostSwap Through Telegram?

Yes. The @GhostSwapBot on Telegram allows users to perform swaps directly within the messaging app. The bot mirrors the web interface and provides real-time updates.

Does GhostSwap Offer an API?

Yes. GhostSwap has a Partners API for business integrations with endpoints for quotes, address validation, and swap creation. Rate limits are generous (120 requests/sec per IP, 30 requests/sec per API key).

Is GhostSwap Custodial or Non-Custodial?

Non-custodial. GhostSwap never takes long-term custody of user funds. Each swap uses a temporary deposit address, and funds are routed directly to the user’s destination wallet.

What Happens if I Send the Wrong Asset?

Sending the wrong asset to a deposit address can result in permanent loss. GhostSwap’s terms explicitly state that users are responsible for sending the correct coin to the correct address. Always double-check before confirming a transaction.

Wrapping Up

All in all, GhostSwap delivers on its core promise: fast, private, non-custodial crypto swaps without the overhead of traditional exchange onboarding. It’s not the cheapest option, and it doesn’t offer advanced trading features, but for users who value simplicity and privacy, it’s a compelling choice.

The platform’s support for Monero and Zcash, along with its Telegram bot and public API, make it a versatile tool for both individual users and developers.

The post No Email, No Account, No KYC: How GhostSwap Swaps 1,600+ Coins in One Step appeared first on Cryptonews.

Dario Amodei, co-founder and CEO of Anthropic, during the company’s Builder Summit in Bengaluru, India, Feb. 16, 2026.

Samyukta Lakshmi | Bloomberg | Getty Images

Anthropic is lining up meetings with investors ahead of a potential initial public offering later this year, a person with knowledge of the plans told CNBC.

Bankers leading the offering are scheduling meetings between prospective investors and executives of the artificial intelligence firm behind the popular Claude models, said the person, who declined to be identified speaking about the process.

The meetings suggest Anthropic’s IPO preparations are advancing, as bankers begin sounding out investor demand before a formal roadshow and eventual share sale. Anthropic confidentially filed its IPO prospectus with the Securities and Exchange Commission last month, but hasn’t disclosed when it plans to debut.

The giant AI startup could hit the public markets as soon as October, though the timing could change, according to Bloomberg, which first reported the investor meetings. An Anthropic spokesperson declined to comment.

An Anthropic listing would build on momentum from June’s massive SpaceX IPO and further open the public markets to companies at the center of the AI boom. It follows years in which the industry’s biggest names remained private while raising hundreds of billions of dollars from investors.

Anthropic appears poised to beat rival OpenAI to the public markets, which could be an advantage for the startup if AI enthusiasm later wanes. OpenAI also confidentially filed for an IPO with the SEC in June, but it has not disclosed any additional details.

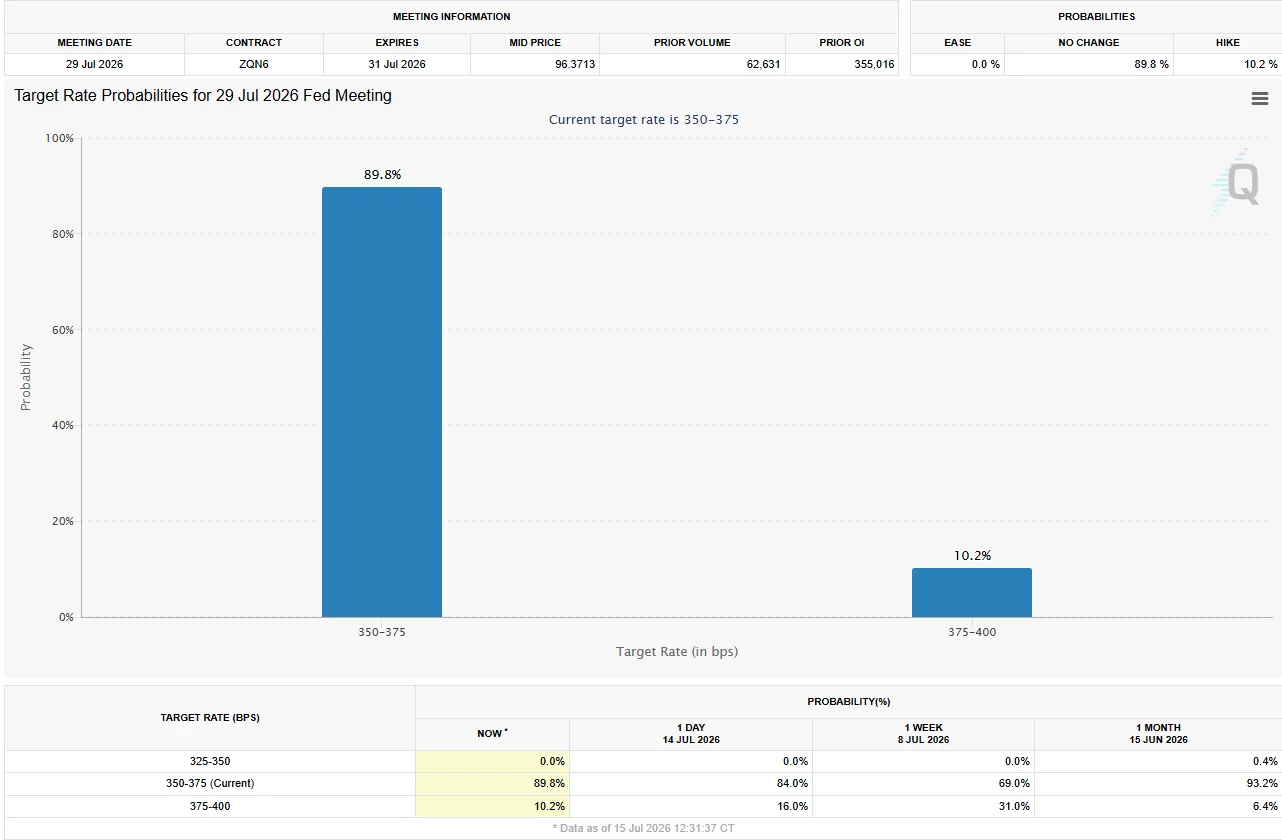

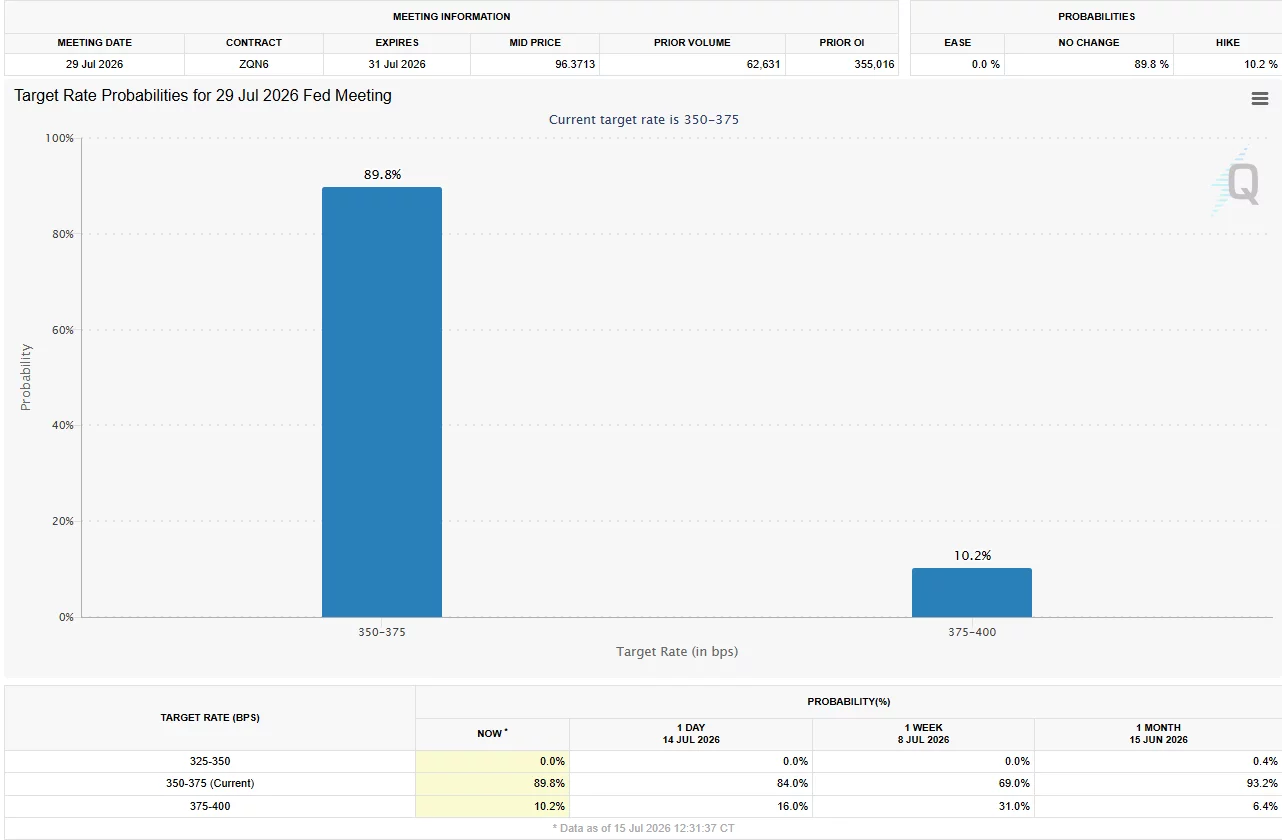

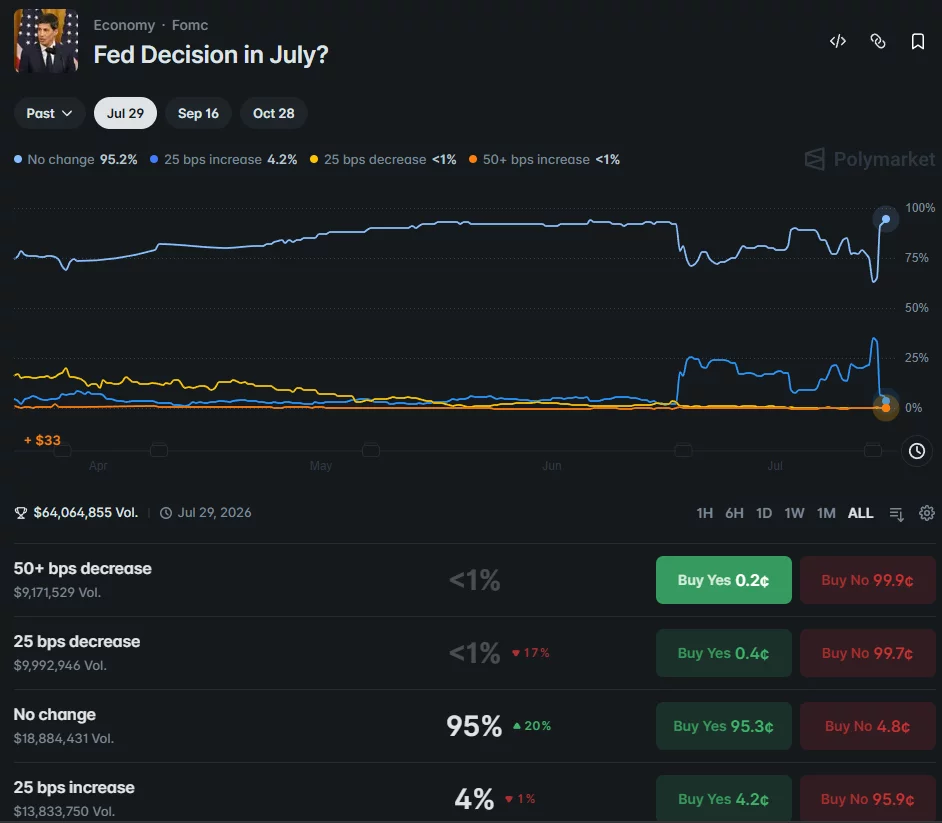

Bitcoin has climbed above $65,000 after softer-than-expected U.S. producer inflation reduced expectations of a Federal Reserve rate hike later this month.

Summary

- Bitcoin climbed above $65,000 after weaker-than-expected U.S. PPI data boosted risk appetite.

- Cooling inflation reduced expectations of a July Fed rate hike in both traditional and crypto markets.

- Ethereum topped $1,900 as the total crypto market capitalization rose above $2.3 trillion.

According to data from the U.S. Bureau of Labor Statistics, June’s Producer Price Index (PPI) added fresh momentum to risk assets after inflation came in below economists’ forecasts.

The total crypto market gained more than 2% to climb above $2.3 trillion, while Bitcoin reclaimed the $65,000 level and Ethereum moved above $1,900 for the first time since early June. The latest move extends the rally that began after June’s Consumer Price Index (CPI) report also surprised to the downside.

Softer inflation cuts expectations for a July Fed rate hike

The Bureau of Labor Statistics reported that headline PPI fell 5.5% year over year in June, below the 6.2% consensus estimate. On a monthly basis, producer prices declined 0.3%, the sharpest monthly drop since April 2025. Core PPI, which excludes food and energy, rose 4.7% from a year earlier, also below the expected 5.1%, while the monthly increase slowed to 0.2%, missing expectations of 0.3%.

Coming one day after a softer CPI report, the latest inflation figures strengthened investor confidence that price pressures continue to ease. The June CPI release had already lifted Bitcoin and the wider crypto market after recording the largest monthly decline in consumer prices since April 2020.

Analysts have linked part of last month’s cooling inflation to lower energy costs following the now-ended ceasefire agreement between the United States and Iran.

The combination of weaker CPI and PPI readings has encouraged traders to reassess the Federal Reserve’s next policy move, with markets increasingly expecting policymakers to keep interest rates unchanged at their July meeting.

Rate markets and prediction platforms scale back tightening bets

Expectations for another Federal Reserve rate increase dropped further after the PPI report. According to the CME FedWatch Tool, traders now assign only a 10.2% probability of a rate hike at the July 29 Federal Open Market Committee meeting, down from roughly 16% following the CPI release and well below levels above 30% seen last week.

Crypto-based prediction markets have become even more confident that policymakers will stay on hold. Data from Polymarket places the probability of a July rate hike at just 4%, showing a wider gap between crypto traders and traditional interest-rate markets.

Markets have also lowered the probability of an additional rate hike before the end of 2026. CME FedWatch data shows those odds have eased to about 51%, compared with around 55% a day earlier and roughly 71% at last week’s peak.

Even with inflation data moving in a favorable direction, Federal Reserve Chair Kevin Warsh has urged caution. During testimony before the House on Tuesday, Warsh warned that one encouraging inflation report does not mean the central bank has completed its work.

According to his remarks, the Federal Reserve remains committed to returning inflation to its long-term 2% target before declaring victory over price pressures.

For crypto investors, however, the latest inflation releases have shifted attention back toward monetary policy. With both CPI and PPI surprising to the downside in consecutive sessions, digital assets have benefited from renewed expectations that borrowing costs may remain unchanged in the near future, supporting demand for risk-sensitive assets including Bitcoin and Ethereum.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Securitize and Cantor Fitzgerald have partnered to support blockchain-based initial public offerings (IPOs) and follow-on equity offerings for listed companies, a move that could further expand the use of tokenized securities in traditional capital markets.

The companies said Wednesday that they are developing a framework for primary issuances that would allow companies to raise capital through tokenized securities while remaining within the existing regulatory framework for public offerings. The framework would support both IPOs and follow-on, or secondary, offerings, in which already public companies issue additional shares to raise capital.

Under the agreement, Securitize will provide the tokenization infrastructure used to issue, distribute and service the digital securities. Its SEC-registered broker-dealer affiliate, Securitize Markets, will participate in the offering and settlement process. Cantor will contribute its equity capital markets and trading capabilities typically associated with public offerings.

The announcement comes as tokenized securities gain traction across traditional finance. While tokenization has largely focused on private credit and Treasurys, companies are increasingly exploring blockchain-based infrastructure for public equities as well.

The collaboration builds on an existing relationship between the companies. Securitize, which provides blockchain infrastructure for tokenized real-world assets, went public through a merger with a special purpose acquisition company (SPAC) backed by Cantor Fitzgerald.

Related: Kraken acquires tokenization platform Magna ahead of potential IPO

Tokenized stocks attract Wall Street interest

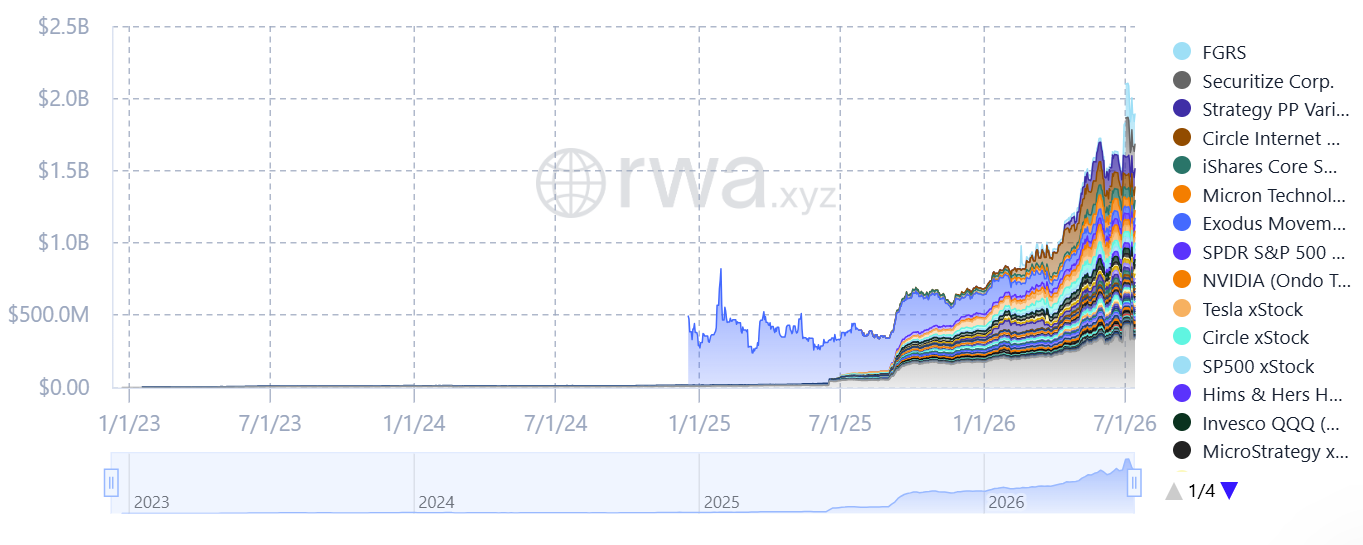

The market for tokenized stocks has expanded rapidly over the past year, outpacing much of the broader digital asset market. The value of tokenized stocks onchain has increased 16% over the past 30 days to nearly $1.9 billion, according to RWA.xyz.

The value of tokenized stocks has grown rapidly over the past year.

Source: RWA.xyz

The growth is drawing established financial institutions deeper into the sector. As The Wall Street Journal reported Wednesday, the Depository Trust & Clearing Corp. (DTCC) plans to pilot the tokenization of stocks and US Treasurys with nearly 40 financial companies, including JPMorgan and Goldman Sachs. The trial follows DTCC’s May announcement that it aims to roll out tokenized trading services by October.

Assets slated for tokenization include shares of Microsoft (MSFT) and stablecoin issuer Circle (CRCL), as well as exchange-traded funds tracking the S&P 500 index, the Nasdaq 100 index and short-term US Treasury bonds.

Related: US, UK treasuries to align transatlantic rules on tokenization and stablecoins

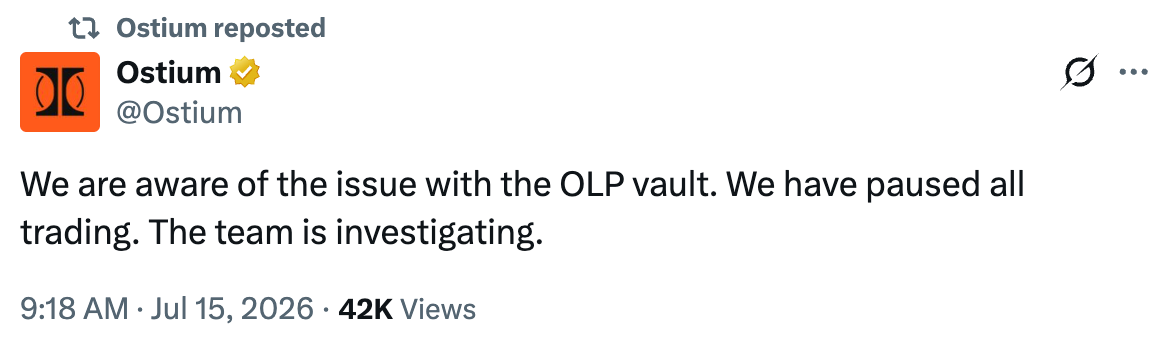

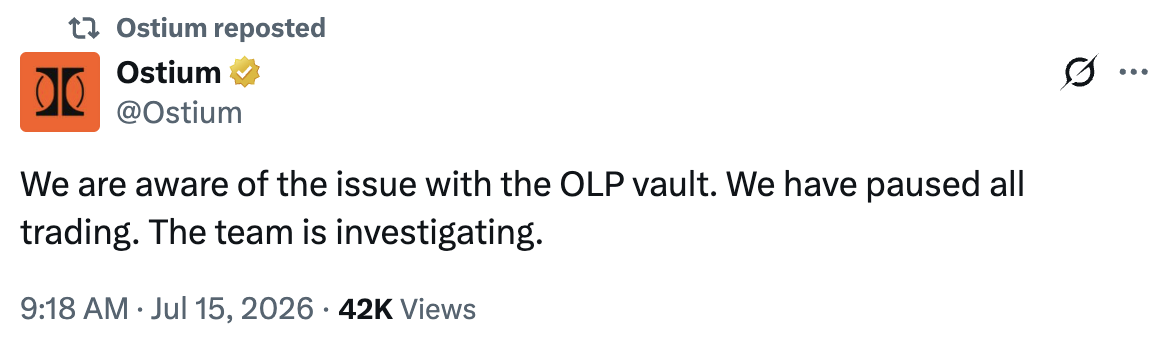

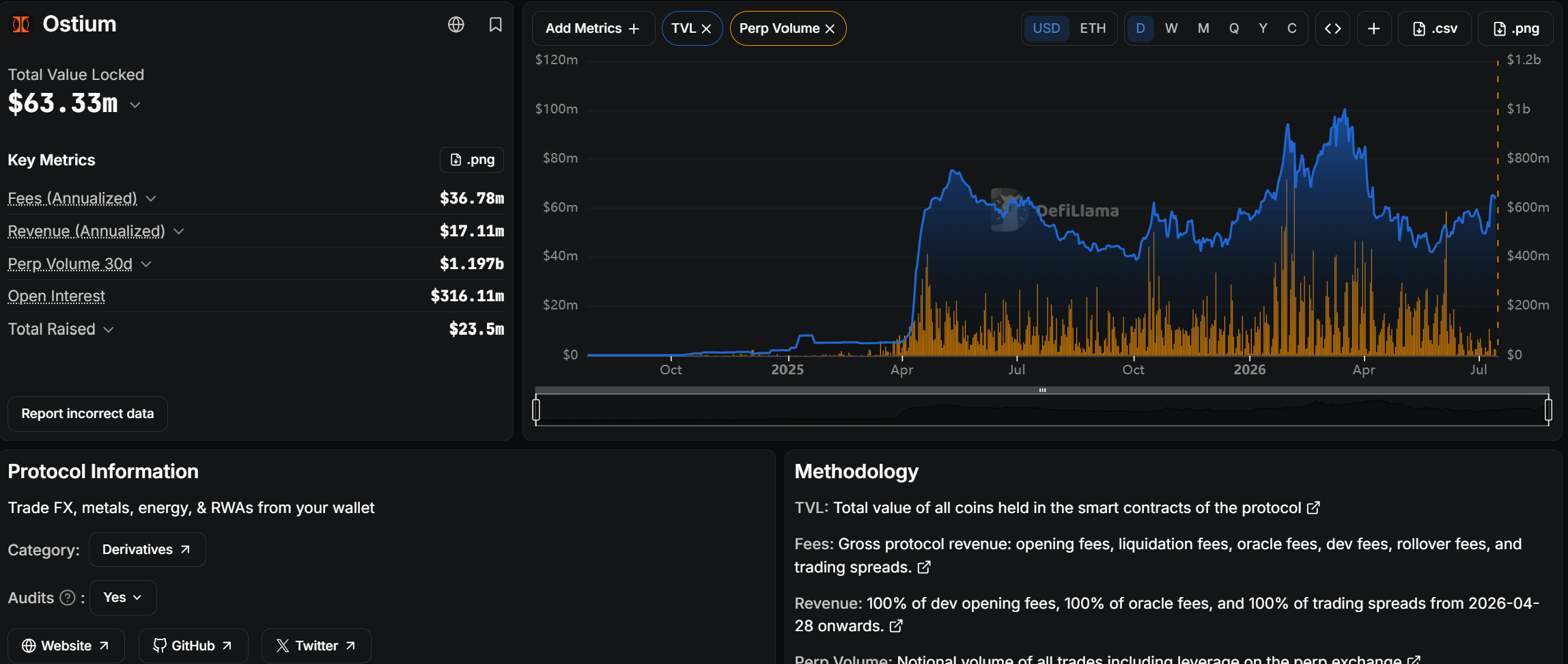

Decentralized trading protocol Ostium paused trading Wednesday after blockchain security firms Blockaid and CertiK reported an apparent exploit of its OLP liquidity vault.

Blockaid estimated the exploit resulted in roughly $18 million in losses, while CertiK placed the figure at about $22 million. Both firms attributed the incident to an apparent compromise of Ostium’s oracle system, which supplies external price data to the protocol.

Source: Ostium

Ostium announced on X that it paused all trading after identifying an issue affecting the vault. It subsequently said: “With user security being our first concern, we recommend that all users temporarily revoke approvals for our contracts until we can further investigate the recent incident.”

The protocol said its team is investigating and has not yet confirmed the cause of the incident or the estimated losses reported by blockchain security firms.

Built on Arbitrum, Ostium is an onchain perpetuals trading platform offering leveraged exposure to 75 trading pairs spanning stocks, ETFs, commodities, indices, foreign exchange and cryptocurrencies.

Source: CertiKAlert

Related: Crypto hacks fell 47% in H1 but ecosystem is no safer: CertiK

DeFi hacks remain persistent challenge

The incident is the latest in a series of high-profile attacks targeting decentralized finance protocols this year, despite broader efforts to strengthen security across the sector.

According to DeFiLlama, crypto hacks resulted in nearly $630 million in losses during April, the highest monthly total since February 2025. DeFi protocols accounted for the vast majority of those losses, with exploits at KelpDAO and Drift Protocol making up more than 80% of the month’s total.

Security researchers have said recent DeFi attacks increasingly target offchain infrastructure such as oracle systems, privileged access and key management rather than exploiting flaws in smart contracts alone.

The attacks have also fueled concerns about DeFi’s readiness for institutional adoption. In an April research note, JPMorgan analysts said bridge security remains a key challenge for the sector, raising questions about whether DeFi can scale to support broader institutional participation.

Industry executives have warned that shrinking DeFi yields are making security risks harder to justify. Speaking to Cointelegraph in May, the CEO of smart contract security firm Statemind and Symbiotic co-founder, Misha Putiatin, said institutions increasingly struggle to quantify hack risk, making them less willing to accept the sector’s returns despite growing interest in blockchain-based finance.

Magazine: Strategy became a symbol of the dot-com crash: Could history repeat?

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Institutional crypto OTC markets are evolving beyond block trades as firms demand liquidity, settlement, and cross-border infrastructure services.

Summary

- Institutional crypto OTC desks are evolving beyond block trades into full-service execution and settlement infrastructure.

- Growing institutional demand is reshaping crypto OTC desks into providers of execution, settlement, and treasury infrastructure.

- Crypto OTC markets are expanding beyond large trades as institutions seek integrated execution and liquidity solutions.

For most of its early history, the institutional crypto OTC market was defined by a single problem: how to move large blocks of Bitcoin or Ethereum without those orders moving the market against themselves. OTC desks existed to solve that problem, and the mechanics were straightforward. A desk aggregated liquidity across venues, quoted a price, and settled the transaction off-exchange. That was the value proposition, and for the institutions active in the market at the time, it was sufficient.

The market that exists today is considerably more complex. The institutions using OTC infrastructure now range from payment companies running millions of stablecoin conversions per month to sovereign wealth funds building digital asset exposure to regional exchanges managing fiat liquidity across multiple jurisdictions simultaneously. Their requirements go well beyond block execution, and the desks serving them have had to evolve accordingly. Understanding how that evolution unfolded and what it means for institutions evaluating OTC partners today is increasingly important as off-exchange activity accounts for a larger share of total institutional crypto volume.

From block trading to execution infrastructure

The original institutional OTC use case was straightforward: an investor wanted to acquire or liquidate a significant position in Bitcoin or Ethereum, and the depth available on public exchange order books at any given moment was insufficient to absorb the order without meaningful price impact. OTC desks solved this by aggregating liquidity from multiple venues simultaneously, executing the full position off-exchange at a single blended rate. The client received a cleaner outcome than exchange execution could deliver at a comparable size, and the desk managed the inventory risk.

As institutional participation broadened, the use cases multiplied faster than most desks anticipated. Payment companies discovered that stablecoin-to-fiat conversion at scale required the same off-exchange execution logic as block trades, but at far higher frequency and with much tighter settlement timing requirements. Mining operations needed to convert consistent production volumes without compressing spot prices on public markets. Funds allocating across a broader digital asset universe needed OTC access to assets with limited exchange liquidity. Each of these use cases placed different demands on OTC infrastructure, and the desks that grew with their clients were the ones that treated execution as a starting point rather than an end product.

The shift from block trading to execution infrastructure represents the most significant structural change in the institutional OTC market over the past several years. A desk operating as execution infrastructure is not just quoting prices on large orders. It involves managing settlement rails, maintaining credit relationships, operating compliance frameworks across multiple jurisdictions, and providing the reporting and operational integration that institutional treasury functions require. The technical and operational gap between a desk capable of this and one that handles only straightforward block trades is substantial.

Settlement as the real differentiator

Among the structural changes in institutional OTC, none has been more consequential than the shift in how clients evaluate settlement capability. For the first generation of institutional OTC clients, settlement was binary: did the transaction complete, and did it complete accurately? Speed was a secondary consideration because the use cases did not require it.

For the current generation of institutional users, settlement infrastructure is often the primary criterion for evaluation. Payment companies and fintechs running real-time stablecoin conversion flows cannot absorb settlement delays lasting hours. Treasury operations managing liquidity across multiple jurisdictions in different time zones need finality that is reliable rather than probabilistic. Regional exchanges facilitating local fiat pairs need settlement rails that are actually present in their markets rather than routing through correspondent banking chains that add latency and introduce clearing risk.

The desks that have responded to this have built onshore banking infrastructure across the regions where their clients operate, rather than relying on cross-border correspondent relationships to approximate regional settlement. The operational investment required to do this genuinely, with actual banking licenses, compliance infrastructure, and local operational presence, is one of the more significant barriers to entry in the institutional OTC market today. Recent developments reinforce why this matters: central banks moving to blockchain-based settlement rails is raising the baseline of what institutional settlement infrastructure is expected to deliver, making the gap between desks with genuine regional presence and those with nominal coverage more consequential. It is also one of the reasons that headline spread comparisons between desks are increasingly insufficient as an evaluation framework. A desk offering tight spreads with slow or uncertain settlement is, in practice, more expensive than one offering slightly wider spreads with second-level finality across all relevant markets.

The role of multi-venue aggregation in modern OTC execution

Multi-venue aggregation has always been part of the OTC value proposition, but how it is executed and the depth at which it operates have changed considerably as the crypto market structure has matured. In the early institutional OTC market, aggregation across a handful of major exchanges was sufficient to source competitive pricing on the assets clients needed. As the asset universe expanded and trading activity was distributed across more venues globally, connectivity requirements grew accordingly.

The practical implication is that the quality and quantity of multi-venue aggregation have become a primary differentiator among OTC desks, rather than just a baseline capability. A desk with deep connectivity across a broad network of exchanges can source liquidity and lock pricing for a wide range of digital assets simultaneously, giving clients certainty on the rate before execution begins, regardless of where the underlying liquidity happens to be distributed at that moment. The infrastructure required to deliver this, low-latency connections to a large number of venues, real-time pricing engines operating across all of them, and price-locking mechanisms that hold the rate through execution, represents a meaningful operational investment that separates the leading desks from the rest of the market.

Counterparties offering crypto OTC trading at this level of infrastructure depth provide a fundamentally different execution environment than lighter-touch alternatives. The difference is not primarily visible in a standard spread comparison. It shows up in execution consistency across a wide range of assets, in settlement reliability during volatile market conditions, and in the operational continuity that high-frequency clients depend on when their own business processes are built around it.

Emerging market demand and what it requires

One of the more underappreciated developments in institutional crypto OTC over the past few years has been the expansion in demand from emerging-market participants. Exchanges operating in Southeast Asia, Latin America, and MENA now represent a significant and growing share of institutional OTC activity, and their requirements are specific enough to constitute a distinct market segment rather than a geographic variation of the same use case.

The core challenge for emerging market participants is not execution pricing. Spreads on major pairs are competitive across most institutional desks. The challenge is regional settlement: reliably getting fiat in and out of local markets at speed, without the correspondent banking dependencies that introduce unpredictable latency. An exchange in Southeast Asia managing local fiat pairs needs a counterparty that can settle in the local market in seconds, not one that routes through a chain of correspondent banks and delivers settlement on the following business day.

This requirement has pushed institutional OTC desks toward genuine regional operational presence as a competitive necessity rather than a growth aspiration. The desks with onshore banking infrastructure and compliance frameworks in the markets where their emerging-market clients operate can serve this segment in ways those without it simply cannot replicate at the service levels these clients require. As emerging market institutional participation continues to grow, this regional operational depth is likely to become one of the most important factors in OTC counterparty selection.

How institutional clients are evaluating OTC desks today

The evaluation framework that institutional clients apply to OTC desks has become considerably more sophisticated as their use of OTC infrastructure has deepened. The clients who are now moving the most volume through OTC desks, payment companies, active trading operations, exchanges, and large fund managers have developed detailed views of what genuinely capable infrastructure looks like, and they apply those views when selecting or reviewing counterparties.

Settlement speed and regional coverage have already been discussed, but two additional dimensions are worth examining. Capital structure, specifically whether the desk operates on its own balance sheet or relies on borrowed inventory, shapes how risk is distributed within the arrangement and has direct implications for same-day settlement capability and credit availability. Desks operating on their own institutional capital can hold inventory, extend credit facilities to eligible counterparties, and absorb the timing differences between client execution and position management. These capabilities underpin the kind of operational reliability that high-frequency clients require.

Reporting and integration capability have also emerged as significant evaluation criteria for institutional treasury operations. Clients running high transaction volumes need real-time, granular visibility into execution quality, API integration that removes manual steps from the execution workflow, and operational transparency that enables their finance teams to accurately account for every transaction. Desks that treat reporting as an afterthought are increasingly unsuitable for the more sophisticated segment of the institutional OTC market, regardless of how competitive their pricing appears.

Where the institutional OTC market is heading

Several structural trends are likely to shape institutional crypto OTC over the coming years. Stablecoin adoption by major financial institutions is already changing the settlement economics of cross-border institutional flows, and OTC desks positioned within that infrastructure are likely to see volume growth that differs structurally from traditional block-trading demand. Visa’s CFO recently outlined how stablecoin settlement is reshaping institutional payment infrastructure, a signal that stablecoin-denominated settlement is moving from an emerging capability to an operational expectation across a significant segment of institutional payment flows, with direct implications for the OTC desks serving those clients.

Regulatory development across key markets is creating both clarity and new compliance requirements for institutional OTC operations. Desks with the compliance infrastructure to operate across multiple regulated jurisdictions are better positioned to serve the institutional segment as regulatory frameworks mature, while those without it face increasing friction in markets where institutional participation is growing fastest.

The consolidation dynamic evident in the institutional OTC market over the past few years is likely to continue. The operational investment required to maintain competitive execution infrastructure across a broad asset universe, genuine regional settlement capability, and the compliance frameworks that institutional clients now require is substantial. The desks that have built this infrastructure are pulling further away from those that have not, and the evaluation gap between them is becoming more visible to institutional clients with each passing cycle.

What this means for institutions evaluating OTC partners

The evolution of institutional crypto OTC from a block-trading service to a genuine financial infrastructure has significant implications for how institutions should approach counterparty evaluation. A framework built around spread comparison was adequate when OTC desks were doing a simpler job. It is insufficient for evaluating the kind of operational relationships that institutional crypto participation now requires.

The institutions best positioned in this market have treated their OTC counterparty decision as a strategic infrastructure choice rather than a transactional one, selecting partners with the settlement depth, regional presence, capital structure, and operational integration capability to support their business as it scales. The quality of that decision tends to compound over time. The desks with the right infrastructure today are the ones whose clients transact the most volume, and the gap between them and lighter alternatives is becoming harder to close from the outside.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

Peter Schiff renewed his long-running criticism of Bitcoin (BTC) on the July 15 episode of “The Peter Schiff Show,” arguing that investors who hold the asset near its current price will eventually regret not selling, as he expects another major decline.

He also questioned Strategy’s decision to sell $450 million in common stock rather than touch its BTC holdings, saying it shows how boxed Michael Saylor’s company has become.

Schiff Lays Out His Bitcoin Case, and Takes Another Shot At Saylor

In the podcast, Schiff admitted that Bitcoin has been surprisingly resilient despite what he believes are growing risks beneath the surface. The economist said that he regretted not buying BTC when he first heard of it 15 years ago, but watching the asset in the last few years had tempered that regret.

“I don’t regret not buying it three, four, five years ago,” he told listeners. “But yeah, 15 years ago, sure, I should have bought it.”

However, he claimed that those who currently hold the OG crypto and still refuse to sell will soon rue their choice. Referring to the cryptocurrency’s current trading range, he argued that there is resistance around $65,000 while support is near $58,000. According to him, if that level fails, Bitcoin could fall below $50,000 before eventually hitting rock bottom at $30,000 or even $20,000.

‘The people who don’t sell it now, they’re going to be the ones that are going to have a lot of regrets,” he warned.

At the time of writing, CoinGecko data showed that BTC was trading a couple hundred bucks under $65,000, having gone up nearly 4% following the release of lower-than-expected US CPI numbers.

The economist then turned to another of his pet subjects, Strategy, which he noted had gone three straight weeks without buying Bitcoin and hadn’t sold any either since disposing of 3,588 BTC last week. Instead, Saylor’s firm raised $450 million through a common stock sale, pushing up its cash reserves to $3 billion, all while the stock traded at a huge discount to the value of its Bitcoin.

Schiff called it a needless dilution and argued that Strategy had avoided selling BTC only because doing so would tank the cryptocurrency’s price.

“Saylor knows if he starts really selling Bitcoin, the price is going to crash,” he claimed. “Now, the problem is it’s going to crash anyway because the market realizes the bind he’s in, and even if he doesn’t sell the market is going to crash out from under him.”

Corporate Treasury Debate In Focus

Schiff’s criticism has come at a time when analysts are reassessing the corporate Bitcoin accumulation story, of which Strategy is the biggest player. According to a recent report from QCP Capital, when Saylor’s firm sold some of its Bitcoin for the first time in late May, the amount, though small (32 BTC out of an over 847,000 BTC stash), still changed the way investors looked at such companies.

Many of them are now paying more attention to their cash reserves, equity issuances and the funding conditions of such operations to determine whether future purchases remain sustainable instead of just being swept away by the latest headline-grabbing buys.

The post Peter Schiff: Bitcoin Holders Will Soon Regret Not Selling at Current Levels appeared first on CryptoPotato.

Securitize and Cantor Fitzgerald have announced a partnership aimed at enabling blockchain-based primary issuances and follow-on equity offerings for listed companies using tokenized securities. The initiative is designed to fit within existing regulatory pathways for public offerings, positioning tokenization as a potential upgrade to traditional IPO and secondary capital-raising workflows.

According to the companies, they are developing a framework that would allow issuers to raise capital through tokenized securities while maintaining compliance with the rules applicable to public offerings. The plan covers both initial public offerings and subsequent, or secondary, share sales by companies that are already publicly listed.

Key takeaways

- Securitize and Cantor Fitzgerald plan to build a regulated issuance and settlement framework for tokenized securities covering both IPOs and follow-on equity offerings.

- Securitize will provide the tokenization infrastructure, while its SEC-registered broker-dealer affiliate, Securitize Markets, is set to participate in offering and settlement.

- Cantor will contribute its equity capital markets experience and trading capabilities associated with public offerings.

- The move aligns with a broader shift toward tokenized stocks and real-world assets as institutional infrastructure efforts accelerate.

A framework designed for public-offering compliance

The partnership is structured around the mechanics required to issue and distribute digital securities in a way that can be administered under the current public-offering regulatory environment. The companies said the framework is intended to support both IPOs and follow-on offerings—where an already listed company issues additional shares to raise capital.

Under the agreement, Securitize is expected to handle the tokenization infrastructure that underpins issuance, distribution, and ongoing servicing of the digital securities. Its SEC-registered broker-dealer affiliate, Securitize Markets, will take part in the offering and settlement process, bridging the digital issuance layer with the traditional market structure.

Cantor Fitzgerald, for its part, will bring its equity capital markets and trading capabilities—capabilities that are typically central to underwriting, market execution, and the infrastructure surrounding public equity transactions.

Why this matters as tokenized equities gain momentum

The announcement arrives as tokenized securities continue to attract increasing attention from established finance. While tokenization has historically found early traction in areas such as private credit and tokenized U.S. Treasurys, the latest wave of interest is increasingly directed at public equity markets.

RWA.xyz data cited in the announcement indicates that tokenized stocks onchain have grown notably: the value of tokenized stocks is reported to have increased 16% over the last 30 days to nearly $1.9 billion. That rate of growth, according to the piece, outpaces much of the broader digital asset market—an important sign for investors watching where tokenization is scaling beyond niche use cases.

More significantly for traditional market participants, the narrative is shifting from isolated pilots to recurring questions about issuance, trading, custody, and settlement at institutional scale. Even when tokenized products are still being explored, the industry attention itself is a signal that infrastructure and compliance teams are beginning to treat tokenization as a serious operational track rather than an experimental technology.

Institutional infrastructure: DTCC’s plans and Wall Street pilots

Tokenized equities are also being pursued through mainstream market infrastructure efforts. Earlier coverage cited in the announcement points to moves by the Depository Trust & Clearing Corp. (DTCC). In a report published Wednesday by The Wall Street Journal, DTCC said it plans to pilot tokenization of stocks and U.S. Treasurys with nearly 40 financial companies, including JPMorgan and Goldman Sachs.

The DTCC trial is described as following its May announcement that it aims to roll out tokenized trading services by October. If the timeline holds, it would represent another step toward standardizing how tokenized assets could be cleared and settled in ways that mirror current institutional workflows.

The WSJ report also notes that the assets targeted for tokenization include shares of Microsoft and Circle, as well as exchange-traded funds tracking major indexes such as the S&P 500 and the Nasdaq 100, alongside short-term U.S. Treasury bonds. The selection is notable because it spans both equity and high-liquidity fixed-income benchmarks—assets that tend to draw heavy institutional participation and could therefore stress-test infrastructure at scale.

For investors and market operators, the practical question is not whether tokenization can “work,” but whether it can interoperate with existing systems for corporate actions, settlement finality, and operational risk controls. Partnerships like Securitize and Cantor’s can be interpreted as one answer on the issuance side, while efforts like DTCC’s pilot focus on the post-trade and market structure layers.

Building on an existing relationship

The partnership is also not starting from zero. Securitize previously moved into public markets via a merger with a special purpose acquisition company (SPAC) backed by Cantor Fitzgerald, according to the announcement. That prior connection helps explain why the two firms are positioning themselves to collaborate on a more ambitious use case: applying tokenization infrastructure to new public-offering activity rather than limiting it to private markets or narrow asset classes.

Even so, key details about implementation and scope remain to be seen. The announcement emphasizes the intent to remain within existing regulatory frameworks, but readers should watch for additional specifics on how the framework will be executed in practice—such as which markets or jurisdictions it initially targets, what types of issuers it prioritizes, and how the settlement and servicing process will be operationalized for tokenized IPOs and follow-on sales.

As tokenized equities continue to attract both infrastructure investment and growing onchain activity, the next phase will likely hinge on regulatory clarity, market-structure integration, and whether pilot projects can graduate into repeatable issuance pipelines for mainstream public companies.

Crypto World

DTCC moves tokenized securities into live trading, marking a milestone for Wall Street’s blockchain push

DTCC safeguards more than $114 trillion in securities, making it one of the most important pieces of financial market infrastructure. Every day, it records ownership and settles transactions involving stocks, bonds and other securities. Rather than creating new digital assets, DTCC’s system converts existing securities into blockchain-based “digital twins” that retain the same legal ownership, dividend and governance rights as the underlying assets.

That distinction separates DTCC’s approach from many tokenized stock offerings available today.

Some crypto platforms issue tokenized “wrappers” that mirror a stock’s price but do not necessarily provide investors with the legal rights associated with owning the underlying shares.

DTCC’s model instead allows institutions to convert existing securities between traditional electronic records and blockchain-based tokens without changing ownership.

“They’re the ones who are flipping from one settlement regime to the next,” Mark Wendland, CEO of Canton Strategic Holdings, said in an interview. “I cannot understate the importance of a firm like DTC piloting and doing these real transactions given the role they play in U.S. financial markets.”

Throughout the day, participants demonstrated several use cases. JPMorgan converted holdings of the Invesco QQQ Trust ETF into tokenized assets before using tokenized collateral to satisfy central counterparty margin requirements with CME Group. DTCC also processed tokenized Treasury transactions, equity trades and collateral pledges, while the SPDR S&P 500 ETF Trust, one of the world’s largest ETFs, was also tokenized during the event.

BlackRock has joined a Depository Trust & Clearing Corporation pilot that has begun tokenizing stocks and U.S. Treasuries within a market infrastructure that safeguards about $114 trillion in assets.

Summary

- DTCC has launched a tokenization pilot with BlackRock, JPMorgan, Goldman Sachs, and nearly 40 financial firms.

- Microsoft, Circle, QQQ, SPY, and BlackRock Treasury ETF are among the first assets being tokenized.

- The pilot uses Hyperledger Besu and Canton, while Stellar-based custody tokenization is planned for 2027.

According to a Wall Street Journal report, BlackRock, JPMorgan, Goldman Sachs, Vanguard, the New York Stock Exchange, and nearly 40 financial firms are participating in DTCC’s latest tokenization initiative.

The pilot focuses on securities already held at the clearinghouse, allowing participating firms to test blockchain-based versions of traditional financial assets while keeping them within DTCC’s existing custody framework.

Live tokenization begins with major public market assets

The first phase of the pilot has started with DTCC tokenizing shares of Microsoft and Circle alongside the Invesco QQQ Trust, the State Street SPDR S&P 500 ETF, and BlackRock’s iShares 0–3 Month Treasury Bond ETF. DTCC has stated that these tokenized assets will be stored at the clearinghouse using blockchain infrastructure.

Participating firms will use the assets in live blockchain transactions covering collateral transfers, repo agreements, and equity trades during the trial. The program is expected to move into its formal operational phase in October after the current testing period.

Separately, DTCC confirmed through a live update that JPMorgan completed the first conversion in the pilot by turning shares of the Invesco QQQ Trust ETF into a tokenized real-world asset.

According to DTCC, the conversion demonstrates that tokenized versions of traditional securities can function inside existing market infrastructure while preserving the same liquidity, investor protections, transparency, and ownership rights as the underlying assets.

Private blockchain leads current rollout while public network plans continue

Rather than using public layer-1 blockchains such as Ethereum or Solana, DTCC has chosen to settle transactions on either its private Hyperledger Besu blockchain or the Canton Network, depending on the infrastructure selected by participating institutions. The approach keeps settlement within permissioned blockchain environments designed for regulated financial markets.

Meanwhile, the project arrives as tokenization continues to gain traction across major financial institutions. The United Kingdom’s Treasury is also advancing a £33 billion tokenization initiative through its Wholesale Digital Markets Taskforce, with BlackRock, Morgan Stanley, and Goldman Sachs among the firms participating in that effort.

Additional plans extend beyond the current pilot. As previously reported by crypto.news, DTCC and the Stellar Development Foundation are preparing DTC custody asset tokenization services on the Stellar public blockchain.

The partners have targeted the first half of 2027 for the launch of live tokenized assets, introducing Stellar as one of the public blockchain networks in DTCC’s developing multi-chain tokenization strategy.

For now, however, the active pilot remains centered on permissioned blockchain infrastructure, giving participating firms an opportunity to test tokenized securities within DTCC’s existing clearing and custody system before the program expands further.

Arbitrum’s RWA perpetual platform Ostium lost nearly $18 million USDC today after attackers compromised an oracle signer key and manipulated prices.

The root cause was a compromised oracle signer private key. This allowed the attacker to bypass verification checks and submit favorable future prices. They executed around 20 looped trades through delegated actions, instantly profiting at the protocol’s expense without genuine market exposure.

Exploit Drains One-Third of Vault in Hours

Security firm Blockaid first flagged the incident, indicating that the attacker used a registered PriceUpKeep forwarder and future-dated authorized oracle reports to generate artificial trading profits. This triggered repeated open-and-close loops that drained funds from Ostium’s main liquidity vault.

Follow us on X to get the latest news as it happens

On-chain data shows roughly $11.86M–$18M USDC extracted from the vault, representing about 28% of its $63 million TVL at the time of the attack. The primary exploit transaction is publicly verifiable on Arbiscan.

Ostium is a leading decentralized perpetuals exchange focused on real-world assets, including equities, commodities, forex, and indices, built on Arbitrum.

Major Backing Meets Major Setback

The protocol had raised approximately $27.8 million from top-tier investors including General Catalyst, Jump Crypto, Coinbase Ventures, Wintermute, and GSR.

Despite strong institutional support and multiple audits, the incident exposes persistent risks in oracle-dependent RWA infrastructure.

The exploit is under active investigation. Users should monitor official channels for withdrawal guidance and security updates. The event highlights the need for hardened oracle key management and real-time monitoring in hybrid DeFi protocols.

As the RWA perpetuals sector grows rapidly, this breach serves as a timely reminder: even well-funded projects remain vulnerable to private-key and oracle attacks.

The post Ostium Perp DEX Hit for $18 Million in Brutal Oracle Exploit appeared first on BeInCrypto.

rinashappylife#short#shorts#success#money#lawofattraction

‘If it wasn’t for my hero neighbour’s quick action during fire, my daughter may not be here’

Just Shrimp jumps overboard into Harris Teeter retailers

No Jackpot Winner as $257 Million Prize Rolls Over to $269 Million Monday Draw

Renter of Home in Anne Heche Crash Denies Settlement With Son

Weekend Open Thread: Staud – Corporette.com

rinashappylife#short#shorts#success#money#lawofattraction

What you need to know and do to improve your financial situation. #viralshorts #howtoinvest

The Psychology of Money Explained in Hindi | Life-Changing Money Lessons

-

Fashion6 days ago

Fashion6 days agoLoro Piana Fall 2026 Enters Houston’s Art Scene

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

Sports6 days ago

Sports6 days ago2026 Genesis Scottish Open Thursday TV coverage: Round 1

-

Sports5 days ago

Sports5 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Tech6 days ago

Tech6 days agoCharacter.AI enters the microdrama arena with its own productions, but there’s a twist

-

Politics6 hours ago

Politics6 hours agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

News Videos22 hours ago

News Videos22 hours agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech2 days ago

Tech2 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Tech22 hours ago

Tech22 hours agoDark Secrets Emerge When Jailbreaking LLMs

-

News Videos7 days ago

News Videos7 days agoCrypto Just Entered Its Most Important 6-Month Candle (Could Decide Everything!)

-

Tech6 days ago

Tech6 days agoLevel Infinite Launches Gangstar Mirage City in India with Pre-Registrations

-

NewsBeat6 days ago

NewsBeat6 days agoMajor update after Huntingdon train attack as man enters plea

-

News Videos2 days ago

News Videos2 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Tech2 days ago

Tech2 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

Tech7 days ago

Tech7 days agoEntra passkey enrollment vishing targets Microsoft 365 users

-

Crypto World7 days ago

Crypto World7 days agoDeFi Dashboard Zapper to Shut Down After 7 Years

-

Crypto World1 day ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

-

Crypto World7 days ago

Crypto World7 days agoMark Cuban-Backed DeFi Dashboard Zapper Shuts Down After 7 Years

-

Tech6 days ago

Tech6 days agoClaude’s New Reflect Dashboard Wants To Help You Log Off Of Claude

-

Crypto World7 days ago

Crypto World7 days agoFed minutes June 2026: officials split on rates

You must be logged in to post a comment Login