Crypto World

Ondo Finance (ONDO) Price Prediction 2026, 2027-2030

ONDO

$0.3757

24h Volume$422.79M

Market Cap$1.83B

24h Low/High$0.3511 / $0.4289

Last updated: June 04, 2026 07:12 · Live price: $0.3757 (-10.88% 24h)

Ondo Finance Price Statistics

| Ondo Finance Price | $0.3757 |

|---|---|

| Price Change 24H | -10.88% |

| Price Change 7D | +5.32% |

| Price Change 30D | +17.49% |

| Market Cap | $1.83B (#46) |

| 24H Volume | $422.79M |

| 50-Day SMA | $0.3413 |

| 200-Day SMA | $0.3417 |

| 14-Day RSI | 44.2 |

| Technical Signal | bearish, neutral |

Ondo Finance trades between $0.43 and $0.45 in late May 2026, market cap around $2.19 billion (#44), roughly 79 percent below its $2.14 high from early 2024. The setup is unusual because most RWA platforms remain speculative. Ondo has shipped product that is processing real institutional volume. Tokenized US Treasury market on Ethereum hit $8 billion ATH in May 2026 with Ondo’s products among the leading contributors. OUSG (Ondo Short-Term US Government Treasuries) holds $680 million in TVL, with BlackRock’s BUIDL fund aongside allocations to Franklin Templeton, WisdomTree, Fidelity, and Wellington/FundBridge vehicles. Ondo Global Markets (the tokenized stocks and ETFs platform) crossed $1.5 billion in TVL by May 2026. The company acquired Oasis Pro in late 2025, securing SEC licenses that removed key US regulatory barriers for institutional products. EU regulatory approval came simultaneously, allowing tokenized stocks and ETFs across 30 European markets. ONDO is deployed across Ethereum, Solana, Sui, and the XRP Ledger with continued multi-chain expansion. The platform integrates with Ripple, J.P. Morgan, and other major institutional finance firms. On May 21, 2026, ONDO surged 10 percent on SEC rumor that tokenized stock trading might be permitted with TVL surpassing $1.5 billion. MEXC launched a $1 million Ondo Stocks Carnival the same day featuring zero-fee trading. The honest read is Ondo represents the cleanest pure-play exposure to institutional RWA tokenization in 2026, with the real advantage being that the platform actually has institutional products processing real volume rather than speculative roadmap promises. The real challenges are also concrete: ONDO token has limited direct value capture from platform operations, 4.87 billion circulating of 10 billion max supply creates ongoing unlock pressure, competition from BlackRock’s BUIDL, Franklin Templeton’s BENJI, and emerging institutional tokenization initiatives is intensifying, and broader RWA market growth could happen with or without ONDO token appreciation. This piece walks through what the data actually says, the bull case ($1.50-$4 by 2030), the base case ($0.60-$1.20), and the bear case ($0.20-$0.50), with the variables that determine which one plays out.

Short-Term Ondo Finance Price Targets

| 2026 full-year range | $0.35 – $0.80 |

|---|---|

| 2026 year-end (base) | $0.40 – $0.65 |

| 2026 year-end (bull) | $0.80 – $1.40 |

| 2026 year-end (bear) | $0.30 – $0.42 |

Long-Term Ondo Finance Price Prediction (2026-2030)

| Year | Bear case | Base case | Bull case |

|---|---|---|---|

| 2026 | $0.30 – $0.42 | $0.40 – $0.65 | $0.80 – $1.40 |

| 2027 | $0.25 – $0.40 | $0.50 – $0.80 | $1.20 – $2.20 |

| 2028 | $0.22 – $0.45 | $0.55 – $0.95 | $1.50 – $3.00 |

| 2029 | $0.20 – $0.48 | $0.60 – $1.10 | $1.50 – $3.60 |

| 2030 | $0.20 – $0.50 | $0.60 – $1.20 | $1.50 – $4.00 |

The 2030 range across scenarios is wide ($0.20 to $4.00, a 20x spread). That width reflects the core disconnect: Ondo-the-platform is clearly growing and institutional, while ONDO-the-token has limited direct value capture and ongoing supply pressure. Which scenario wins depends largely on whether governance ships a value-capture mechanism (fee distribution, staking, or buyback) while the platform keeps scaling.

Summary

Ondo Finance is two businesses in one company. The first business is tokenized US Treasuries through OUSG and USDY ($680M and growing). The second is tokenized stocks and ETFs through Ondo Global Markets ($1.5B+ TVL with EU approval across 30 markets and SEC licenses via Oasis Pro acquisition). Both businesses are real, both are growing, and both compete against institutional incumbents (BlackRock BUIDL, Franklin Templeton BENJI) with bigger balance sheets and longer institutional relationships. The bull case for 2030 ($1.50-$4) requires Ondo Global Markets to scale to $10-30 billion TVL, OUSG to grow to $5-10 billion, ONDO token value capture to materialize through governance fees or revenue distribution, regulatory clarity supporting tokenized stocks at federal level, and competitive moat maintenance against BlackRock and Franklin Templeton. The base case ($0.60-$1.20) assumes moderate growth across both business lines, ONDO maintains its position as one of multiple RWA tokenization leaders, governance value remains limited, and competitive dynamics stay balanced. The bear case ($0.20- $0.50) assumes BlackRock and traditional institutional incumbents capture the bulk of institutional tokenization volume, ONDO governance token fails to capture meaningful value despite platform growth, token unlocks continue creating supply pressure, and the broader RWA narrative cools.

Why Ondo is at $0.43 right now

The current Ondo price reflects multiple competing forces unique to RWA tokenization platforms.

The starting point: ONDO peaked at $2.14 in early 2024 during peak RWA narrative momentum. The decline to current $0.43 reflects multiple specific pressures: token unlock pressure as scheduled distributions continue, broader altcoin weakness through 2024-2026, and the disconnect between platform-level growth and token value capture that affects most governance tokens without direct fee accrual mechanisms.

The platform fundamentals are concrete and growing. OUSG holds $680 million across tokenized US Treasury products built on top of institutional money market fund vehicles (BlackRock BUIDL, Franklin Templeton BENJI, WisdomTree, Fidelity, Wellington/FundBridge). The 30-day APY of approximately 3.19 percent reflects actual short-term Treasury yields. The product structure is genuinely institutionalgrade: holders are limited to US Qualified Purchasers, the underlying assets are real-world securities, and the infrastructure is built for compliance with traditional finance regulatory frameworks.

USDY (Ondo’s dollar-yielding stablecoin alternative) provides yield-bearing dollar exposure without requiring qualified purchaser status. The product is positioned for retail and non-US institutional accessibility. Combining OUSG (institutional-restricted, higher-yield) and USDY (broader-access, loweryield) provides differentiated product set.

Ondo Global Markets is the tokenized stocks and ETFs platform. TVL crossed $1.5 billion by May 2026 with EU regulatory approval allowing the platform to offer tokenized stocks across 30 European markets. The platform allows institutional and retail users to trade tokenized representations of US stocks and ETFs with on-chain settlement.

The Oasis Pro acquisition in late 2025 secured SEC licenses for institutional products. The acquisition removed key US regulatory barriers and enables broader institutional access to Ondo’s tokenized products. The licenses cover alternative trading system operations and broker-dealer activities required for institutional tokenization.

The institutional integrations are real. Ondo integrates with Ripple (covered in detail in your XRP piece – tokenized US Treasury pilot announced February 2026 by J.P. Morgan, Mastercard, and Ondo). J.P. Morgan’s involvement extends to multiple settlement and tokenization initiatives. The integrations provide validation that institutional finance views Ondo as legitimate infrastructure partner.

The May 21, 2026 catalyst pushed ONDO 10 percent higher on SEC rumor regarding tokenized stock trading permissions. The actual SEC announcement remained pending but the rumor showed market sensitivity to regulatory developments affecting Ondo’s core business. MEXC’s $1 million Ondo Stocks Carnival the same day promoting zero-fee trading provided additional exposure and accessibility.

The competitive context matters. BlackRock’s BUIDL fund grew to over $2.5 billion. Franklin Templeton’s BENJI continued expanding. The tokenized US Treasury market on Ethereum hit $8 billion ATH in May 2026 with multiple participants. Ondo competes against well-capitalized traditional finance incumbents but with the advantage of being crypto-native and having stronger DeFi integration.

The token economics are the structural challenge. ONDO is a governance token without direct fee accrual mechanism. Platform revenue from OUSG management fees (0.15 percent), USDY yields, and Ondo Global Markets transaction fees flows to the underlying business rather than the ONDO token directly. Governance value depends on DAO decisions about future value capture mechanisms, which haven’t been clearly set.

Supply dynamics create ongoing pressure. 4.87 billion ONDO are in circulation out of 10 billion max supply. Continued scheduled unlocks add to circulating supply throughout 2026-2027 period. The January 2025 unlock of 1.94 billion tokens created significant supply expansion that the market is still absorbing.

At $0.43, the market is rewarding Ondo’s platform but penalizing the token. The platform keeps shipping product (OUSG, USDY, Mastercard, BlackRock integration) but ONDO itself has no direct fee accrual. The supply keeps expanding through unlocks. Governance tokens for traditional-finance-style infrastructure businesses are a category the market hasn’t decided how to price.

The bull case: $1.50-$4 by 2030

The bull case requires multiple variables resolving favorably and assumes ONDO captures meaningful value from platform growth.

Ondo Global Markets scaling to $10-30 billion TVL. The platform reached $1.5 billion by May 2026 with growth trajectory. Bull case requires continued scaling through expanded asset coverage (more stocks, more ETFs, additional asset classes), geographic expansion beyond current EU 30-market approval, and institutional adoption from major financial institutions seeking on-chain access to tokenized securities. The 7-10x scaling from current TVL is plausible given the broader RWA market trajectory ($8 billion tokenized Treasury market on Ethereum alone, growing).

OUSG and USDY scaling to $5-10 billion combined. The current $680 million OUSG and additional USDY represent meaningful but small share of the $8 billion tokenized Treasury market. Bull case requires Ondo capturing larger market share through superior product structure, institutional relationships, and regulatory positioning. The institutional preference for tokenization-as-service (which Ondo provides) versus building proprietary tokenization could drive market share gains.

ONDO token value capture mechanism deployment. The bull case requires the DAO or company to set direct value capture from platform revenue. Possible mechanisms: governance-driven fee distribution to ONDO holders, staking yields backed by platform revenue, buyback-and-burn programs funded by platform fees, or other mechanisms creating direct economic linkage between platform growth and token value. The mechanism doesn’t currently exist meaningfully but is a possible future development.

Regulatory clarity supporting tokenized stocks at federal level. The SEC rumor that produced May 21 catalyst would need to crystallize into actual approval for tokenized stock trading in US markets. Combined with CLARITY Act framework providing broader crypto regulatory clarity, the regulatory environment could support Ondo Global Markets US expansion. US institutional access would dramatically expand the platform’s TVL potential.

Competitive moat maintenance against BlackRock and Franklin Templeton. The bull case requires Ondo to defend its position as institutional crypto-native partner rather than getting displaced by traditional finance incumbents building proprietary tokenization. Differentiation: Ondo’s DeFi integration capabilities, multi-chain deployment (Ethereum, Solana, Sui, XRPL), and developer ecosystem create advantages BlackRock’s BUIDL doesn’t match in pure-crypto-native contexts.

The Trump administration RWA policy support. The current administration has signaled pro-tokenization policies. The CLARITY Act provides regulatory framework. Specific RWA-friendly policies (covered in your CLARITY Act and Strategic Bitcoin Reserve pieces) create supportive environment for Ondo’s institutional positioning.

The crypto cycle supporting altcoin appreciation. Bitcoin reaching new highs sustained above $150K. Altcoin rotation producing institutional capital flow to mid-cap altcoins. Broader crypto market dynamics support ONDO appreciation alongside platform-level growth.

Targets if bull case conditions materialize: – 2026 year-end: $0.80-$1.40 – 2027 year-end: $1.20-$2.20 – 2028 year-end: $1.50-$3.00 – 2029 year-end: $1.50-$3.60 – 2030 year-end: $1.50-$4.00

The upper end ($4) requires sustained execution across all variables including ONDO governance token capturing meaningful value from $30+ billion platform TVL. The lower bull case ($1.50) is achievable through platform scaling combined with moderate value capture mechanism deployment.

The base case: $0.60-$1.20 by 2030

The base case assumes meaningful platform growth with limited token value capture mechanism deployment.

Ondo Global Markets scaling to $4-8 billion TVL. Growth continues from current $1.5 billion levels through expanded asset coverage and geographic reach but at slower pace than bull case. The platform captures specific institutional niches without dominating the broader tokenized securities market.

OUSG and USDY scaling to $2-4 billion combined. Continued growth from current levels but with intensifying competitive pressure from BlackRock BUIDL, Franklin Templeton BENJI, and emerging institutional tokenization initiatives. Ondo maintains its position as significant but not dominant tokenized Treasury platform.

ONDO token value capture remains limited. The DAO discusses but doesn’t deploy transformative value capture mechanisms. Governance token continues to derive value primarily from speculative trading rather than direct economic linkage to platform revenue. Some moderate developments (staking introduction, limited governance-driven distributions) may occur.

Regulatory developments produce mixed outcomes. EU framework continues supporting platform expansion. US regulatory developments are positive but slow. CLARITY Act deployment supports general crypto adoption but specific tokenized stock SEC approval remains delayed.

Competitive dynamics stabilize. BlackRock BUIDL and Franklin Templeton BENJI capture significant institutional tokenization volume but Ondo maintains its niche. Crypto-native and DeFi-integrated positioning provides defensible competitive position without dominating.

Supply dynamics play out predictably. Continued scheduled unlocks add to circulating supply through 2027-2028 period before unlock pressure compresses. Token economics improve gradually but don’t transform.

The broader crypto cycle provides moderate support. Bitcoin reaches $130-160K range with altcoin rotation producing periodic Ondo rallies. ONDO participates in altcoin cycles without leading.

Targets in base case: – 2026 year-end: $0.40-$0.65 – 2027 year-end: $0.50-$0.80 – 2028 year-end: $0.55- $0.95 – 2029 year-end: $0.60-$1.10 – 2030 year-end: $0.60-$1.20

The base case represents moderate appreciation from current $0.43 levels but stays well below the $2.14 all-time high. The support comes from continued platform growth and gradual institutional adoption. The structural pressure comes from limited token value capture and ongoing supply expansion.

The bear case: $0.20-$0.50 by 2030

The bear case requires adverse outcomes across multiple variables.

Traditional finance incumbents dominate institutional tokenization. BlackRock BUIDL scales to $20+ billion. Franklin Templeton BENJI captures growing institutional share. Major banks (JPMorgan Onyx, State Street, BNY Mellon) build proprietary tokenization platforms. Ondo’s institutional positioning erodes to specialty product rather than primary platform.

Ondo Global Markets growth stalls. EU expansion produces limited additional TVL beyond current levels. US regulatory approval for tokenized stocks remains delayed indefinitely. The platform captures specific niches without scaling to bull-case-required levels.

ONDO token value capture fails to develop. The DAO doesn’t deploy meaningful value capture mechanisms. Governance token continues to derive value from speculation rather than fundamental economics. Token holders increasingly question the value proposition relative to direct holding of underlying assets (USDY for yield, traditional ETFs for stock exposure).

Token unlocks overwhelm demand. Continued scheduled distributions create persistent sell-pressure that fundamental demand can’t absorb. Combined with broader altcoin weakness, supply expansion pushes price below current $0.43 levels sustainably.

Regulatory deterioration. CLARITY Act stalls or fails to provide expected framework. Post-2029 administration reverses RWA-friendly policies. International regulatory pressure increases on tokenization platforms. SEC takes adverse action under shifting priorities.

Competitive displacement by emerging RWA platforms. New entrants with stronger institutional relationships, better technology, or more favorable tokenomics capture market share Ondo was positioning to serve. Securitize, Centrifuge, or new platforms grow faster than Ondo.

The RWA narrative cools. Broader institutional adoption develops slower than expected. The “tokenization will eat traditional finance” narrative that supported RWA valuations doesn’t deliver on aggressive timelines. Institutional capital flows to other crypto themes.

The macro deterioration. Higher US interest rates reduce relative attractiveness of tokenized Treasury yields. Broader altcoin weakness during sustained risk-off periods. Crypto market weakness affects all altcoins including RWA-themed assets.

Targets in bear case: – 2026 year-end: $0.30-$0.42 – 2027 year-end: $0.25-$0.40 – 2028 year-end: $0.22- $0.45 – 2029 year-end: $0.20-$0.48 – 2030 year-end: $0.20-$0.50

The bear case represents 5-55 percent downside from current $0.43 levels. Even in bear scenarios, ONDO retains some value given platform fundamentals and continued operation. Complete failure scenarios would require platform-level operational issues combined with broader market collapse.

The five variables that determine the outcome

Five variables that track which scenario is materializing.

Variable 1: Ondo Global Markets TVL trajectory. The single most important platform variable. Currently $1.5 billion. Bull case requires $10-30 billion by 2030. Monitor: monthly TVL reporting, asset coverage expansion (additional stocks, ETFs, asset classes), geographic expansion (EU markets activation, additional jurisdictions), institutional adoption announcements, and competitive positioning versus traditional finance incumbents.

Variable 2: OUSG and USDY market share in tokenized Treasury market. Currently $680 million OUSG in $8 billion total tokenized Treasury market (8.5 percent share). Bull case requires significant share expansion. Monitor: monthly OUSG and USDY market cap, total tokenized Treasury market growth, BlackRock BUIDL trajectory, Franklin Templeton BENJI growth, competitive dynamics among institutional tokenization providers.

Variable 3: ONDO token value capture mechanism deployment. Currently limited. Monitor: DAO governance proposals for fee distribution, staking mechanisms introduction, buyback-and-burn programs deployment, revenue distribution discussions, and any direct economic linkage between platform growth and ONDO token value.

Variable 4: Regulatory developments affecting institutional tokenization. SEC tokenized stock rulings, CLARITY Act deployment specifics, EU MiCA framework operational impact, additional jurisdictional approvals beyond current EU 30-market access. Monitor: SEC announcements, CLARITY Act deployment milestones, Ondo regulatory filings and approvals, competitor regulatory developments.

Variable 5: Competitive positioning versus BlackRock BUIDL and Franklin Templeton BENJI. The largest institutional incumbents in tokenization. Monitor: BlackRock BUIDL TVL trajectory, Franklin Templeton BENJI growth, JPMorgan Onyx and other bank tokenization initiatives, emerging cryptonative competitors (Securitize, Centrifuge, etc.).

The variables interact significantly. Platform TVL growth supports token interest. Market share gains create defensible competitive position. Token value capture mechanism deployment transforms governance token value proposition. Regulatory developments enable institutional adoption. Competitive positioning determines which institutional capital flows to Ondo versus competitors. All variables compound in producing the eventual price outcome.

What this means for ONDO holders and traders

What this means for ONDO holders and traders For current ONDO holders, the practical implication is the asset’s setup is solid at the platform level but uncertain at the token level. Platform fundamentals (OUSG, USDY, Ondo Global Markets growth, regulatory wins) support the broader investment thesis. Token economics (limited direct value capture, supply expansion) create headwinds that platform growth alone may not overcome.

For potential ONDO buyers, current $0.43 reflects substantial discount from all-time high combined with developing institutional adoption. The risk-reward depends on assessment of platform growth probability (high given current trajectory), value capture mechanism deployment probability (uncertain), and competitive dynamics versus traditional finance incumbents (Ondo well-positioned but facing strong competition). Entry at current levels has asymmetric upside if value capture develops, modest upside if platform grows but value capture remains limited.

For traders, ONDO has showed catalyst sensitivity around: regulatory announcements (SEC tokenized stock rumors produce 10+ percent moves), TVL milestones, institutional partnership announcements, and broader RWA narrative momentum. Trading the catalysts requires monitoring regulatory developments, partnership announcements, and TVL reporting alongside broader crypto market dynamics.

For institutional investors evaluating ONDO allocation, the platform offers exposure to institutional RWA tokenization through crypto-native infrastructure. The investment case depends on belief in RWA tokenization scaling combined with confidence that crypto-native platforms (versus traditional finance incumbents) capture meaningful share. ETF accessibility could develop following set crypto ETF patterns but is not yet available.

For developers and ecosystem participants, Ondo provides institutional-grade tokenization infrastructure that’s accessible across multiple chains (Ethereum, Solana, Sui, XRPL). The multi-chain deployment creates opportunities for DeFi protocol integration of tokenized RWA assets. The technical infrastructure supports building applications that combine traditional finance assets with DeFi composability.

For traditional finance professionals exploring tokenization, Ondo represents a tested operational alternative to building proprietary tokenization platforms. The platform’s regulatory positioning, institutional partnerships, and technical infrastructure provide reference deployment. Whether to build with Ondo versus building proprietary versus using BlackRock BUIDL or Franklin Templeton BENJI depends on specific use case requirements.

Connection to broader market dynamics

Ondo’s setup connects to several broader dynamics covered in your existing crypto.news editorial work.

The XRP institutional tokenization piece directly connects through the J.P. Morgan, Mastercard, and Ondo XRP Ledger tokenized US Treasury pilot announced February 2026. The pilot shows Ondo’s integration capabilities across major institutional infrastructure providers. The XRPL deployment provides multichain expansion that competing platforms haven’t matched at similar scale.

The CLARITY Act framework (covered in the CLARITY Act series) provides regulatory pathway for tokenized stocks and broader institutional crypto adoption. The Act’s deployment supports Ondo Global Markets US expansion and removes structural barriers for institutional participation.

The Strategic Bitcoin Reserve piece (covered in your Strategic Bitcoin Reserve analysis) creates broader pro-crypto policy environment that benefits institutional tokenization infrastructure. The administration’s crypto-friendly approach supports Ondo’s regulatory positioning.

The WLFI RWA platform comparison (covered in WLFI price prediction) provides direct competitive context. Both Ondo and WLFI’s RWA platform target institutional tokenization but with different capital bases (institutional traditional finance for Ondo, politically-aligned capital for WLFI). The two platforms occupy adjacent positioning rather than direct competition.

The Hyperliquid HYPE buyback comparison provides analytical contrast for value capture mechanisms. HYPE has aggressive direct value capture (99 percent fee-to-buyback). ONDO has indirect value capture dependent on future governance decisions. The contrast highlights why HYPE has produced stronger token appreciation despite less institutional positioning than Ondo.

The TON Pay 2.0 comparison provides framework for institutional infrastructure adoption. TON has Telegram distribution advantage. Ondo has institutional finance partnership advantage. Both target consumer/institutional adoption pathways but through different mechanisms.

The honest bottom line

Ondo is the pure-play institutional RWA tokenization investment. Not the only RWA token, but the only one where BlackRock’s BUIDL fund sits inside an Ondo product, where Mastercard is using Ondo infrastructure to settle stablecoin transactions, and where the team has been shipping institutional-grade product since before “RWA” was a category most analysts knew how to spell.

The platform fundamentals are concrete: $680 million OUSG holding BlackRock’s BUIDL fund and other institutional money market vehicles, $1.5 billion Ondo Global Markets TVL, EU regulatory approval across 30 markets, SEC licenses via Oasis Pro acquisition, J.P. Morgan and Ripple integrations, multichain deployment across Ethereum, Solana, Sui, and XRP Ledger. These are not speculative roadmap items. They are operational businesses processing real volume.

The institutional partnerships validate the positioning. BlackRock’s BUIDL backing OUSG. Franklin Templeton products in OUSG portfolio. Fidelity allocations. Wellington/FundBridge vehicles. JP Morgan tokenized Treasury pilots. Ripple integration. The institutional finance establishment treats Ondo as legitimate tokenization infrastructure partner.

The regulatory wins are substantial. EU 30-market approval for tokenized stocks and ETFs. SEC licenses via Oasis Pro. Operating across multiple jurisdictions with appropriate compliance. The regulatory positioning provides barriers to entry that competing platforms haven’t matched.

The real challenges are equally concrete. ONDO governance token lacks direct value capture mechanism from platform operations. Platform revenue flows to underlying business rather than token holders. 4.87 billion circulating of 10 billion max supply creates ongoing unlock pressure. Competition from BlackRock BUIDL and Franklin Templeton BENJI is intensifying with their stronger balance sheets and longer institutional relationships.

The 2030 range across scenarios is wide: $0.20 to $4.00, representing 20x range. The wide range reflects the disconnect between platform-level growth and token-level value capture. If platform grows substantially and value capture develops, bull case materializes. If platform grows without value capture or competition intensifies, base or bear case dominates.

For holders, the variables that matter are the ones connecting platform success to token value: governance proposals for fee distribution or buyback mechanisms (most important), Ondo Global Markets TVL trajectory (validates platform thesis), regulatory developments (enables expansion), and competitive positioning (determines market share). Platform fundamentals can be excellent while token value stays constrained without value capture mechanism deployment.

For buyers, the question is whether you’re buying ONDO as a platform-growth bet (where moderate appreciation is achievable through platform success) or as a value-capture-deployment bet (where transformative appreciation requires governance mechanism evolution). Different theses have different time horizons and risk profiles.

For the broader market, Ondo represents the test case for whether crypto-native platforms can compete with traditional finance incumbents in institutional tokenization. If Ondo successfully scales against BlackRock BUIDL and Franklin Templeton BENJI, the success shows that crypto-native infrastructure can capture institutional finance market share rather than getting displaced. The outcome affects how the broader RWA category develops.

For 2026, expect ONDO in a $0.35 to $0.80 range with significant catalysts around SEC tokenized stock approval timing, Ondo Global Markets TVL milestones, governance proposals for value capture, and broader RWA market growth. The floor near $0.35 reflects current platform positioning. The upside ($0.65 to $0.80) needs catalysts to land.

For 2027-2030, the question is whether governance evolves to capture platform value. If Ondo’s DAO ships fee distribution or buyback mechanisms while the platform keeps scaling, ONDO trades $1.50 to $4. Without value capture, even strong platform growth produces $0.60 to $1.20. Adverse competitive or regulatory dynamics produce $0.20 to $0.50.

ONDO is the trade for someone who thinks the next leg of crypto adoption comes through traditional finance tokenization rather than memecoin rotation or DeFi innovation. The platform thesis is sound and shipping. The token value capture question is what determines whether holding ONDO produces returns proportional to the platform’s success.

For analysts, the cleanest framework is: separate Ondo-the-platform (clearly growing, clearly institutional) from ONDO-the-token (limited direct value capture, ongoing supply pressure, dependent on future governance decisions). Conflating them produces analytical mess. The platform’s success doesn’t automatically translate to token appreciation without the governance evolution that enables value capture.

What everyone should watch: the next major DAO proposal addressing ONDO value capture from platform revenue. That proposal’s outcome and deployment will largely determine whether bull case or base case becomes the operative trajectory through 2030.

Ondo Finance Technical Analysis

As of June 04, 2026 07:12, Ondo Finance (ONDO) trades at $0.3757. The 50-day SMA ($0.3413) sits below the 200-day SMA ($0.3417), and the 14-day RSI of 44.2 reads as neutral. The combined short-term technical signal is bearish, neutral. Based on realized daily volatility of ~7.81%, the model projects the following short-term ranges:

Ondo Finance Short-Term Projection

| Horizon | Low | Average | High |

|---|---|---|---|

| Today | $0.3473 | $0.3766 | $0.4060 |

| This week | $0.3041 | $0.3817 | $0.4594 |

| Next week | $0.2779 | $0.3877 | $0.4975 |

| Next month | $0.2407 | $0.4015 | $0.5622 |

Short-term ranges are statistical projections from live price and realized volatility, refreshed continuously. They are not guarantees.

Ondo Finance Price Prediction FAQ

What is Ondo Finance’s price prediction today?

Based on live price and current volatility, Ondo Finance (ONDO) is projected to trade between $0.3473 and $0.4060 today, with an average around $0.3766. The current technical signal is bearish, neutral.

What is Ondo Finance’s price prediction for tomorrow?

Tomorrow, Ondo Finance is expected to stay near today’s range of $0.3473–$0.4060, barring a major catalyst. The live model refreshes this estimate continuously from market data.

What is the Ondo Finance price prediction for this week?

For this week, the model projects Ondo Finance between $0.3041 and $0.4594 (average ~$0.3817), based on a realized daily volatility of about 7.81%.

What will the price of Ondo Finance be next month?

Over the next month, Ondo Finance is projected in a $0.2407–$0.5622 range (average ~$0.4015). Short-term ranges widen with the time horizon as uncertainty grows.

What is Ondo Finance and how does it differ from other RWA platforms?

Ondo Finance is a tokenization platform that brings real-world assets like US Treasuries, stocks, and ETFs onto blockchain through institutional-grade infrastructure. Key products include OUSG (tokenized US Treasuries with $680M TVL), USDY (yield-bearing dollar alternative), and Ondo Global Markets (tokenized stocks/ETFs with $1.5B TVL). Ondo differs from competitors through: SEC licenses via Oasis Pro acquisition, EU regulatory approval across 30 markets, BlackRock BUIDL backing for OUSG, multichain deployment (Ethereum, Solana, Sui, XRP Ledger), and integration with J.P. Morgan and Ripple. Differs from BlackRock BUIDL by being crypto-native; from Securitize by having stronger DeFi integration.

Can Ondo reach $4 by 2030?

$4 is at the upper end of the bull case range ($1.50-$4 by 2030). Required conditions: Ondo Global Markets scaling to $10-30 billion TVL, OUSG and USDY combined reaching $5-10 billion, ONDO governance token deploying meaningful value capture mechanism, federal regulatory clarity for tokenized stocks, competitive moat maintenance against BlackRock and Franklin Templeton, and broader crypto cycle supporting altcoin appreciation. The base case for 2030 is $0.60-$1.20.

What is OUSG and how does it work?

OUSG (Ondo Short-Term US Government Treasuries) is a tokenized fund providing on-chain exposure to US Treasuries by investing in institutional money market funds. Portfolio primarily holds BlackRock’s BUIDL fund alongside allocations to Franklin Templeton, WisdomTree, Fidelity, and Wellington/ FundBridge vehicles. Current TVL approximately $680 million. NAV around $115. 30-day APY approximately 3.19 percent. Eligible investors limited to US Qualified Purchasers. Management fee 0.15 percent. Performance fee 0 percent. Inception January 26, 2023.

How does Ondo Global Markets work?

Ondo Global Markets is the tokenized stocks and ETFs platform that received EU regulatory approval allowing trading across 30 European markets. Platform TVL crossed $1.5 billion by May 2026. Allows institutional and retail users to trade tokenized representations of US stocks and ETFs with on-chain settlement. The Oasis Pro acquisition secured SEC licenses removing US regulatory barriers for institutional products. Continued geographic expansion and asset coverage growth represent key bull case variables.

What is the ONDO token’s relationship to platform revenue?

ONDO is currently a governance token without direct fee accrual mechanism. Platform revenue from OUSG management fees (0.15 percent), USDY yields, and Ondo Global Markets transaction fees flows to the underlying business rather than ONDO token directly. Governance value depends on DAO decisions about future value capture mechanisms which haven’t been clearly set. The token’s eventual price appreciation depends substantially on whether governance mechanism evolution creates direct economic linkage between platform growth and token value.

How does Ondo compete against BlackRock BUIDL?

BlackRock BUIDL is the largest tokenized Treasury fund ($2.5+ billion TVL). Ondo competes through: crypto-native infrastructure versus BlackRock’s traditional finance positioning, multi-chain deployment across Ethereum/Solana/Sui/XRPL versus BlackRock’s Ethereum-only initial deployment, stronger DeFi integration capabilities, OUSG product structure (which actually holds BUIDL among other vehicles, making them complementary rather than purely competitive). The competitive dynamic includes both competition (for direct institutional clients) and collaboration (OUSG uses BUIDL as portfolio holding).

What are the main risks to Ondo?

Six primary risks. First, traditional finance incumbents (BlackRock, Franklin Templeton, major banks) dominate institutional tokenization at Ondo’s expense. Second, ONDO governance token fails to develop meaningful value capture mechanism from platform revenue. Third, ongoing token unlocks create persistent sell-pressure. Fourth, regulatory deterioration affecting tokenized stocks specifically (SEC delays, EU framework changes). Fifth, Ondo Global Markets growth stalls below required levels. Sixth, broader RWA narrative cools as institutional adoption develops slower than expected.

Should I buy Ondo given the institutional partnerships?

This piece does not provide investment advice. Current $0.43 reflects substantial discount from all-time high combined with strong platform fundamentals and uncertain token value capture. The risk-reward depends on assessment of platform growth probability (high given current trajectory), value capture mechanism deployment probability (uncertain), competitive dynamics versus traditional finance (Ondo well-positioned but facing strong competition), and broader RWA market growth. Position sizing should reflect that platform success and token appreciation may follow different timelines. The five-variables framework provides objective monitoring signals.

How we forecast Ondo Finance price

Our ONDO forecasts combine platform fundamentals (OUSG and USDY TVL, Ondo Global Markets TVL, institutional partnerships, regulatory approvals) with token-level dynamics (supply schedule and unlocks, governance value-capture status) and broader crypto-cycle context. Rather than a single number, we model bear, base, and bull scenarios tied to five trackable variables, and update the figures as new data lands. Forecasts are scenario-based and inherently uncertain.

This article is for informational purposes and does not make up financial or investment advice. Cryptocurrency markets are highly volatile and price predictions are inherently speculative. The figures and analysis described reflect data available as of late May 2026. Always do your own research and consult with qualified financial professionals before making investment decisions.

Latest Ondo News

Read more – Nathan Allman’s sudden death leaves Ondo Finance at a turning point

Ondo Finance founder Nathan Allman dies unexpectedly, with Ian De Bode taking over as CEO while the RWA firm says its mission remains unchanged.

Ondo Finance’s native token $ONDO has broken above $0.46 and is trading near $0.466 with a 24 hour gain above 15 percent, according to data from Gate. Spot market shows ONDO (ONDO) testing the $0.46 level and printing around $0.466…

Read more – Ondo price confirms bull flag breakout, eyes upside to $0.55 as key metrics surge

Ondo price extended its recovery this week after confirming a bullish continuation setup on the daily chart, with rising demand for tokenized real-world assets and strong platform growth metrics reinforcing the bullish outlook. According to data from crypto.news, Ondo (ONDO)…

Read more – Ondo price pauses after rally to yearly highs, bullish setup keeps upside hopes alive

Ondo price cooled slightly on Monday after surging to its highest level of the year, though the broader technical structure still points to growing bullish momentum across the tokenized real-world asset sector. According to data from crypto.news, Ondo (ONDO) price…

Russia’s FSB says Telegram founder Pavel Durov faces a terrorism-related charge and an international arrest warrant, while a separate French case remains open.

US spot Bitcoin ETFs recorded four straight sessions of outflows totaling $526 million as Bitcoin faced renewed selling pressure after failing to hold $65,000.

Crypto World

The Most Unpredictable FOMC Meeting in Years Is Here: What Bitcoin Investors Should Know

The United States Federal Reserve will announce its interest-rate decision later today, but, unlike essentially every meeting in the past six years, markets remain divided over what comes next.

Bitcoin investors seemingly de-risked yesterday in what appeared to be a blatant sell-off ahead of the key event. The question now is what follows.

Why So Much Unpredictability Now

The Federal Open Market Committee began its two-day meeting on July 28 and will publish its decision at 2:00 p.m. ET today. Chairman Kevin Warsh’s press conference will follow approximately 30 minutes later, in which investors will seek clues for what the central bank’s policy will be for the remainder of 2026.

The current benchmark rate stands between 3.50% and 3.75%. Although most experts still believe it will be left unchanged, futures markets recently assigned a probability of up to 38% to a surprise 25-basis-point hike. According to the analyst at the Kobeissi Letter, these expectations are among the most divided in recent history.

They explained that nearly every Fed meeting since the COVID-19 pandemic in March 2020 entered decision day with roughly 99% agreement about the outcome. The situation now is different for the first time in over six years, given the aforementioned odds on futures markets and prediction platforms.

The uncertainty partly stems from Warsh’s decision to reduce the central bank’s reliance on forward guidance. Minutes from the June meeting showed that policymakers discussed shortening the Fed’s statement and removing language indicating the likely direction of the next move. Warsh’s approach is expected to preserve flexibility, but it has also left traders without the clear policy signals they became accustomed to under Jerome Powell.

Change or No Change

The Kobeissi Letter analysts said they believe the Fed will leave rates unchanged. A recent Reuters survey of over 100 forecasters reached the same conclusion, with more than three-quarters predicting no policy shift until the end of the year. ING economists shared the same opinion.

One of the reasons for this is the softer-than-expected inflation data for June. The labor market has also shown signs of weakening, giving the Fed another reason not to tighten financial conditions further.

There’s also the opposite side of the coin, though, as some experts believe the central bank might lose credibility if it waits too long. Inflation remains well above the 2% target, while renewed geopolitical tension, tariffs, and energy-market instability could push prices higher again.

Several Fed officials have reportedly become more open to the idea of raising rates if inflation fails to improve. Warsh has also avoided giving markets a clear roadmap, meaning that a hike cannot be easily dismissed simply because officials did not prepare investors for one in advance.

Crypto Impact

Crypto analytics platform Santiment Intelligence outlined a notable rise in social-media discussions about the interest-rate hikes ahead of today’s meeting. The data showed a similar spike in such fears before the previous meeting on June 16. However, as it typically happens, the social chatter was wrong as the Fed left rates unchanged.

“Crowd conviction can get loud right before it gets wrong, especially when traders are trying to price Fed uncertainty into Bitcoin,” said Santiment.

Let’s talk prices. BTC dipped by $3,000 yesterday in a de-risking development ahead of the meeting. It has recovered half of the losses, currently sitting above $64,000.

If the Fed doesn’t change rates and Warsh doesn’t signal strongly for a September hike, BTC could rebound further as the uncertainty might have already been priced in. If there’s no rate change but the Chairman sounds hawkish, bitcoin might jump initially as there would be no hike now, but it’s likely to retreat toward $60,000 in the next few weeks.

A surprise 25-basis-point increase, though, will be the most bearish immediate outcome for the cryptocurrency. The decision will likely strengthen the dollar, push Treasury yields higher, and cause investors to further reduce exposure to speculative assets.

The post The Most Unpredictable FOMC Meeting in Years Is Here: What Bitcoin Investors Should Know appeared first on CryptoPotato.

Jump Capital has closed a $350 million venture fund with a stronger focus on crypto investments.

Summary

- Jump Capital has closed a $350 million venture fund with a stronger focus on early stage crypto investments.

- The firm said the new fund will back blockchain infrastructure, DeFi, Web3, fintech, and enterprise software startups.

- Jump Capital has expanded its crypto portfolio through investments in Securitize, Shelby, and KGeN over the past year.

- The venture firm has completed more than 100 investments and nearly 30 exits since its launch.

According to a July 29 announcement, Jump Capital has closed its seventh venture fund with $350 million in total capital commitments, describing it as the firm’s largest fund to date and outlining plans to increase investments across the crypto ecosystem while continuing to back early-stage technology startups.

The firm’s official announcement said the new vehicle will continue investing in fintech, IT and data infrastructure, future of commerce and media, and B2B SaaS, while allocating more resources to blockchain and digital asset companies.

The fund follows nearly a decade of venture investing that has resulted in more than 100 portfolio companies and close to 30 exits.

Jump Capital has expanded its crypto allocation

Founded in 2012 alongside Jump Trading, Jump Capital said it originally focused on software and technology companies outside traditional coastal venture markets while supplying Series A and Series B funding to underserved founders across the United States.

The firm said market conditions have changed considerably since then. Access to Series A and Series B capital has become more limited, while investor attention toward startups in the Midwest increased during the pandemic.

At the same time, blockchain emerged as what Jump Capital described as a technology capable of changing financial markets and introducing new models of ownership and value transfer.

According to the announcement, the venture firm began investing in crypto roughly seven years ago before building a dedicated investment team led by partners Saurabh Sharma and Peter Johnson. It said experience across distributed systems, computing infrastructure, fintech, and capital markets encouraged it to commit more resources to the sector through its latest fund.

The announcement added that Jump Capital and its affiliate Jump Trading now invest globally across the crypto market, citing increasing institutional participation, continued retail adoption, and rapid product development as factors supporting that strategy.

Crypto investments already span infrastructure and tokenization

According to Jump Capital, its crypto portfolio already includes investments across exchanges that support fiat on-ramps, lending and credit platforms, compliance software, asset management platforms, decentralized finance, gaming, Web3 infrastructure, and blockchain networks.

In May 2025, Jump Crypto, the digital asset division of Jump Trading, acquired a significant equity stake in Securitize for an undisclosed amount. At the time, Securitize said the partnership would expand institutional access to tokenized real-world assets, including U.S. Treasurys, private credit, and private equity, while improving collateral management solutions. Securitize Chief Operating Officer Michael Sonneshein said the investment demonstrated growing institutional conviction in tokenization and its role in capital markets.

The company made another infrastructure-focused move in June 2025, when Aptos Labs and Jump Crypto introduced Shelby, a decentralized hot storage network designed to provide cloud-grade infrastructure for Web3 applications. Aptos Labs said Shelby would deliver decentralized, monetizable storage with sub-second data access across multiple blockchains, while Jump Crypto said the protocol addresses blockchains’ inability to efficiently serve large datasets at scale.

Earlier collaborators announced for Shelby included Metaplex, Pipe Network, Story, Myco, DoubleZero, and Flashback Labs, with Aptos serving as the network’s initial settlement layer.

Portfolio activity has continued across emerging Web3 projects

Jump Crypto has also continued backing consumer-facing blockchain applications.

In September 2025, Web3 distribution protocol KGeN announced a $13.5 million strategic funding round backed by Jump Crypto, Accel, and Prosus Ventures, increasing the company’s total funding to $43.5 million.

KGeN said the proceeds would support expansion of its POGE identity and reputation framework, which helps Web3 applications manage user acquisition, commerce, and loyalty programs on-chain. At the time, the company reported operations across more than 60 countries, serving 38.9 million verified users, generating $48.3 million in annualized revenue, and recording roughly 780,000 daily active users.

Following that investment, Jump Crypto Chief Investment Officer Saurabh Sharma said KGeN’s distribution model introduced more accountability into digital user acquisition, while Accel and Prosus Ventures credited the platform’s ability to scale measurable engagement.

New fund builds on nearly a decade of venture investing

Alongside its crypto activity, Jump Capital said its venture business has completed more than 100 investments and nearly 30 exits since launch.

The firm pointed to exits involving Personal Capital, acquired by Empower, Flashpoint, acquired by Audax, and Tubi, acquired by Fox, while also highlighting companies including SPIRE, Fast Radius, M1 Finance, Degreed, TradingView, LogicGate, and LinkSquares among its portfolio.

According to Jump Capital, its investment process continues to rely on sector-specific research and discussions with industry participants before identifying founders whose businesses align with the firm’s investment themes.

With Fund VII now closed, the venture firm said it plans to continue supporting early-stage technology companies while dedicating additional capital and personnel to blockchain infrastructure, decentralized finance, crypto networks, gaming, and other parts of the digital asset ecosystem.

The US dollar continues to hold the upper hand against most major currencies ahead of the outcome of the latest Federal Reserve meeting. While the base-case scenario remains for interest rates to stay unchanged, markets are also pricing in the possibility of a rate hike. The Fed’s decision, together with its comments on inflation, economic conditions and the future path of monetary policy, could determine the direction of the US dollar over the coming weeks.

Another factor supporting the dollar is the ongoing geopolitical uncertainty in the Middle East. Despite the temporary suspension of US strikes on Iran and renewed diplomatic efforts, the risk of further military escalation remains, prompting investors to remain cautious ahead of this week’s key events. Geopolitical uncertainty continues to underpin demand for the US dollar as a safe-haven asset. At the same time, USD/JPY’s approach towards multi-year highs has increased expectations of fresh warnings from Japanese authorities and raised the risk of currency intervention. For USD/CAD, oil prices remain another important driver: weaker crude prices continue to limit support for the Canadian dollar and help preserve the pair’s bullish potential.

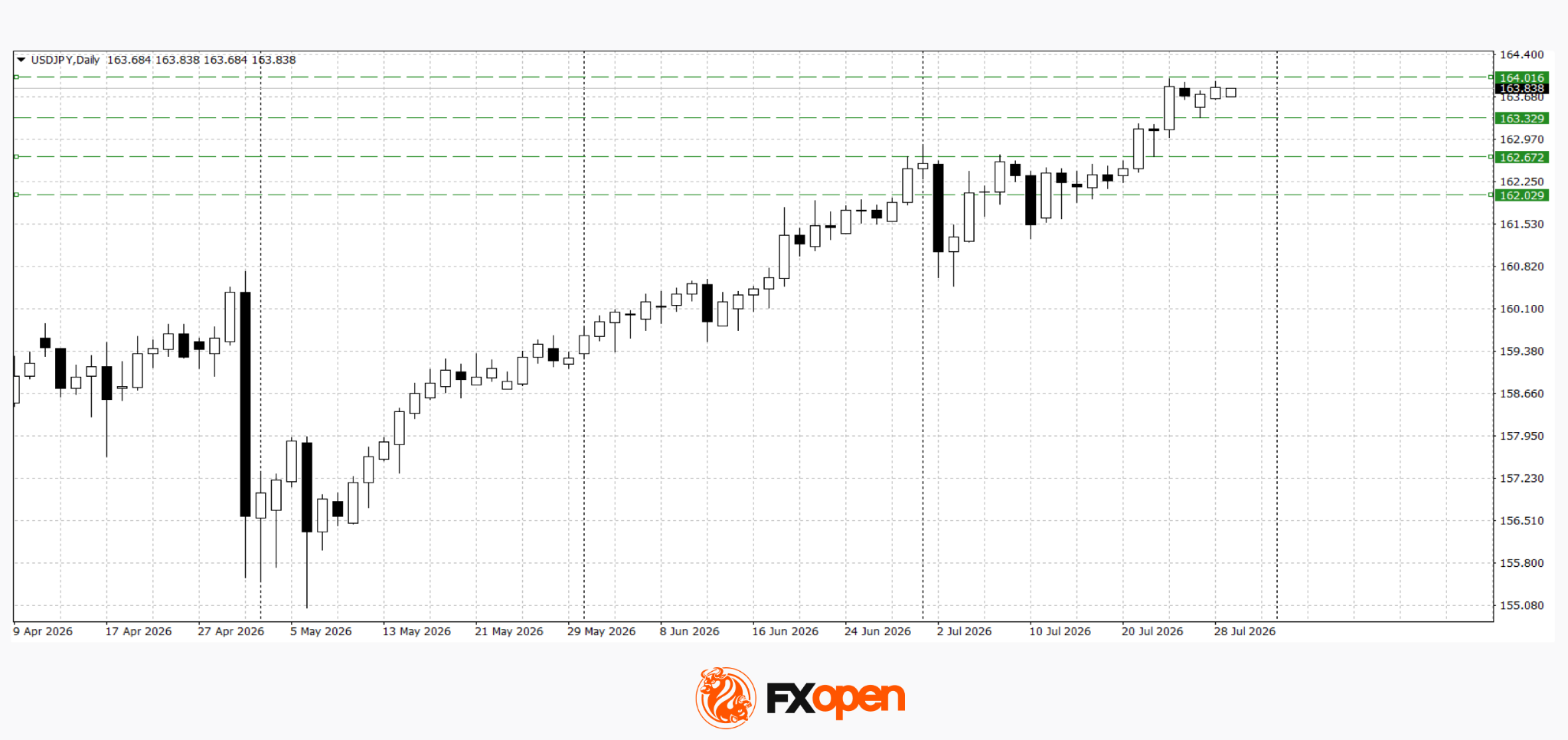

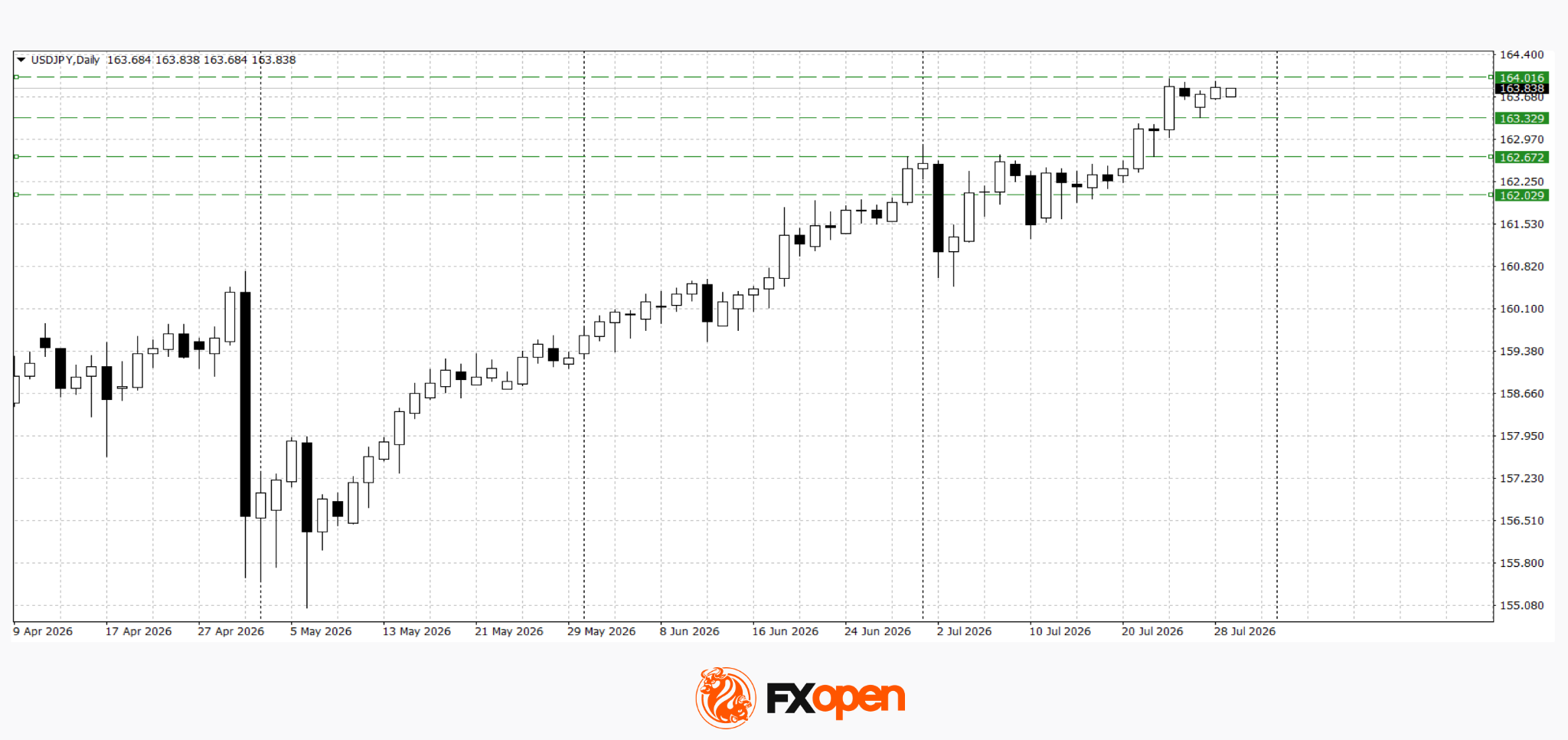

USD/JPY

USD/JPY tested another multi-year high near 164.00 last week. Following the strong rally, the pair has entered a modest pullback. However, if the Federal Reserve delivers a more hawkish outcome or maintains its hawkish tone, the pair could extend its advance towards 165.00–165.50. A decisive move below 163.30 could trigger a deeper correction towards the 162.00–162.60 support area.

Key events for USD/JPY:

- Today at 21:00 (GMT+3): US Federal Reserve interest rate decision;

- Today at 21:30 (GMT+3): Federal Open Market Committee (FOMC) press conference;

- Tomorrow at 15:30 (GMT+3): US Core Personal Consumption Expenditures (PCE) Price Index.

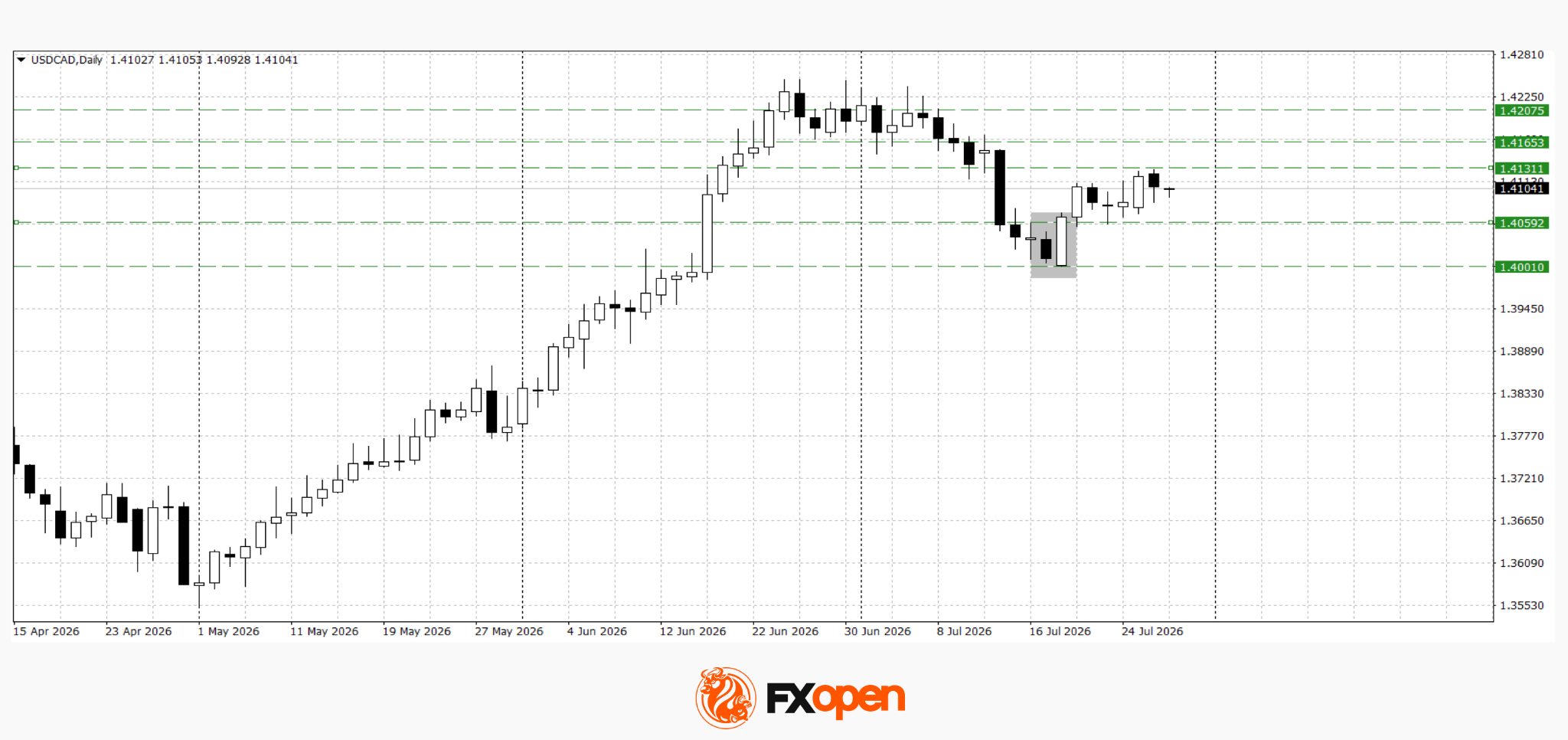

USD/CAD

USD/CAD’s recovery following the formation of a bullish engulfing pattern has stalled near resistance at 1.4130. The pair is currently consolidating within the 1.4060–1.4130 range. A decisive break above the upper boundary of this range could pave the way for further gains towards 1.4160–1.4200. Conversely, a move below 1.4060 could lead to a retest of the recent low near 1.4000.

Key events for USD/CAD:

- Today at 17:30 (GMT+3): US crude oil inventories;

- Today at 20:30 (GMT+3): Bank of Canada Summary of Deliberations;

- Tomorrow at 15:30 (GMT+3): US GDP data.

Overall, the near-term direction of both USD/JPY and USD/CAD will depend primarily on the Federal Reserve’s decision and its guidance on the future path of interest rates. A more hawkish stance could support a breakout above nearby resistance levels and reinforce the US dollar’s strength. Conversely, a more dovish message could trigger a correction in the greenback, particularly against the Japanese yen, where the proximity of multi-year highs increases the likelihood of renewed warnings from Japanese officials. For USD/CAD, oil price movements and the Bank of Canada’s Summary of Deliberations will remain important additional drivers.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips (additional fees may apply). Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

XRP trades near $1.06 in late July 2026, roughly 71 percent below the $3.65 cycle top set on July 17, 2025. This piece walks through the escrow-versus-ETF equation, the bull case ($4.50–$7.00 by 2030), the base case ($1.80–$3.20), and the bear case ($0.60–$1.40).

Cointelegraph is committed to providing independent, high-quality journalism across the crypto, blockchain, AI, and fintech industries.

All news, reviews, and analyses are produced with full journalistic independence and integrity. For more details on our standards and processes, please read our Editorial Policy.

Crypto World

HTX’s First TradFi “Trade to Earn” Campaign Unleashes New Trading Momentum: Rewards Exceed $23,000, Fee Savings Reach 1.8 Billion $HTX

Recently, HTX’s first-ever TradFi “Trade to Earn” campaign concluded successfully. The campaign leveraged innovative gameplay – “24/7 mining” and “up to 110% fee rebates” – to ignite significant trading enthusiasm for traditional finance assets within the crypto market.

HTX’s official data reveals impressive results: the campaign generated a total trading volume of 63.37 million USDT, crowned a top winner claiming 5,206 USDT in rewards, and collectively saved users 22,238 USDT in trading fees. These achievements underscore the event’s effectiveness in enhancing the user trading experience and reducing trading costs.

Amid current market volatility, HTX’s TradFi perpetual futures contracts offer users an excellent hedging and cross-market investment tool. Through the “mining via trading” model, users can capture macro opportunities such as surging U.S. equities and gold volatility using familiar USDT capital without trading fee friction.

Enjoy Negative Trading Fee Rates 24/7

Official data reveals that the inaugural “Trade to Earn” campaign generated a robust trading volume of 63.37 million USDT. Over the campaign period, the platform distributed 23,477 USDT in rewards while saving traders 22,238 USDT in fees (an equivalent of roughly 1.8 billion $HTX). These impressive metrics highlight HTX’s trading innovations with negative fee rates and 24/7 continuous rewards.

During the campaign, users trading designated TradFi perpetual futures contracts earned $HTX rewards of up to 110% of their actual trading fees incurred. This means the platform not only covers all trading costs but also provides additional rewards, transforming trading costs from an expense into profit and truly achieving “the more you trade, the more you earn.” Additionally, the platform offered a daily prize pool of 6,000 USDT, distributed hourly to ensure round-the-clock incentives.

Notably, the campaign-designated trading assets span a diverse range of core TradFi instruments: from safe-haven and inflation-hedging tools like gold (XAU) and crude oil (USOIL), to major indices like the Nasdaq (QQQ) and tech giants including NVIDIA (NVDA) and Microsoft (MSFT). This diverse selection of assets offers users versatile macro allocation, hedging, and cross-market trading opportunities, further expanding practical use cases at the intersection of Web3 and traditional finance.

Fees for $HTX Buyback and Burn, Constructing a Positive Cycle of Trading and Ecosystem Value

Beyond trading rewards, another standout feature of this campaign is its deep integration of user trading activity with $HTX ecosystem value.

During the campaign, all trading fees generated from designated TradFi contracts were allocated to buy back $HTX tokens, with buybacks executed and burned according to the platform’s quarterly burning schedule. This mechanism links platform trading growth with $HTX value creation, continuously incentivizing user participation while reinforcing the token’s deflationary characteristics. This fosters a positive cycle: “trading growth – token buyback and burn – value accumulation.”

With the first campaign successfully concluded, HTX’s second-phase TradFi “Trade to Earn” is now in preparation. The campaign will continue to adopt negative-fee trading and 24/7 rewards, while further expanding access to popular TradFi asset trading scenarios. This will enable users to capture global market opportunities while continuously enjoying the innovative experience of “trading as earnings.”

Looking forward, HTX will leverage more diverse products, increasingly competitive incentives, and an enhanced ecosystem to drive deeper integration between crypto and TradFi, delivering a more professional and efficient digital asset trading platform for global users.

About HTX

Founded in 2013, HTX has evolved from a virtual asset exchange into a comprehensive ecosystem of blockchain businesses that span digital asset trading, financial derivatives, research, investments, incubation, and other businesses.

As a world-leading gateway to Web3, HTX harbors global capabilities that enable it to provide users with safe and reliable services. Adhering to the growth strategy of “Global Expansion, Thriving Ecosystem, Wealth Effect, Security & Compliance,” HTX is dedicated to providing quality services and values to virtual asset enthusiasts worldwide.

To learn more about HTX, please visit https://www.htx.com/ or HTX Square , and follow HTX on X, Telegram, and Discord.

The post HTX’s First TradFi “Trade to Earn” Campaign Unleashes New Trading Momentum: Rewards Exceed $23,000, Fee Savings Reach 1.8 Billion $HTX appeared first on BeInCrypto.

Russia has escalated its long-running dispute with Telegram by charging founder Pavel Durov with facilitating terrorist activities and issuing an international arrest warrant, marking one of the most significant legal actions yet against the messaging platform’s billionaire founder.

The move comes as governments worldwide intensify pressure on technology platforms over content moderation, encryption, and their responsibilities in preventing criminal activity. The latest accusations also add to Durov’s ongoing legal challenges outside Russia, including an active investigation in France.

The post Russia Targets Telegram Founder Pavel Durov With Terrorism Charges appeared first on BeInCrypto.

Bitcoin climbed 1% to about $63,800 on Wednesday while Asian equity markets suffered one of their worst stretches of the year, the second time in a seven-day period that crypto has held through a sharp unwind in the artificial intelligence trade.

The majors moved with it. Ether rose 1% to $1,899, XRP added 2% to $1.07, BNB gained to $567, solana held at $73, and dogecoin edged up. Hyperliquid’s HYPE was the only major in the red, down 3% to $54.

The damage in equities was concentrated in chipmakers. South Korea’s benchmark tumbled 11%, following an 11% drop on Tuesday and putting the index on course for a record two-day decline. SK Hynix fell about 17% after reporting a 557% surge in quarterly profit that still came in below expectations, and

Samsung slid 12% ahead of its own results on Thursday. The MSCI Asia Pacific index dropped 2% to its lowest since mid-April, and Nasdaq 100 futures fell 1%, extending a five-day losing streak for the tech-heavy gauge, its longest this year.

Major fire breaks out under roller coaster tracks at Italy’s largest amusement park

He attacked family and passers by at retail park a year after killing nan

all 106 sites to shut 10 September

-

Fashion5 days ago

Fashion5 days agoWeekend Open Thread: Brooks Brothers

-

Sports2 days ago

Sports2 days agoCommonwealth Games boxing: Jadumani Singh seals dominant 5-0 win over Pakistan’s Sumama Rehman to enter quarter-finals | Commonwealth Games News

-

Tech2 days ago

Tech2 days agoIntel is reversing course and bringing hyper-threading back to its server chips

-

Crypto World6 days ago

Crypto World6 days agoEthics, other provisions in crypto Clarity Act to be further discussed

-

Politics2 days ago

Politics2 days agoLuke Littler dismantles Gerwyn Price to retain title in Blackpool

-

Sports5 days ago

Sports5 days ago2026 3M Open leaderboard: Scottie Scheffler finds putter in Round 1, sits three back

-

Fashion5 days ago

Fashion5 days ago16 Dresses for the High Summer Event

-

Politics23 hours ago

Politics23 hours agoThe Part of the Electric Transition Nobody Wants to Discuss

-

Entertainment5 days ago

Entertainment5 days agoA New Post-Apocalyptic Gundam Anime Series Blasts Into SDCC

-

News Videos2 days ago

News Videos2 days agoBITCOIN JUST ENTERED THIS CRITICAL ZONE…

-

News Videos6 days ago

News Videos6 days agoThe Peugeot Family: How 200 Years of an “Old Money” Dynasty Died in A Boardroom

-

Crypto World4 days ago

Crypto World4 days agoRipple bought a bank in pieces. The $4 billion audit

-

Politics3 days ago

Politics3 days agoSpain sweeps the board at 2026 World Cup with individual awards

-

Business3 hours ago

Business3 hours agoMajor shareholder moves on Canyon

-

Crypto World3 days ago

Crypto World3 days agoXRP Ledger adds $2.6B as RWA inflows rank second

-

Crypto World6 days ago

Crypto World6 days agoUniswap (UNI) pushes deeper into tokenized RWAs with permissioned trading pools

-

Tech4 days ago

Tech4 days agoAnthropic launches Claude Opus 5, a cheaper AI model for coding, agents and enterprise workflows

-

Entertainment13 hours ago

Entertainment13 hours ago‘Stargate’ Creator’s New Sci-Fi Series Returns for Season 3 Tomorrow

-

Crypto World6 days ago

SEC Agrees to Overhaul Recordkeeping After Settling Coinbase Lawsuit Over Gensler’s Lost Texts

-

Business5 days ago

Business5 days agoAlliance Entertainment Holding Corporation (AENT) Discusses Evolution Into Omnichannel Distribution and Fulfillment Platform for Media and Collectibles Transcript

You must be logged in to post a comment Login