Crypto World

Polygon CEO announces job cuts amid Coinme acquisition

The round of layoffs was part of Polygon transitioning operations to payments following a $250 million deal to acquire Coinme and Sequence in January.

Robinhood spent months positioning its blockchain as regulated infrastructure for tokenized stocks. Two weeks after launch, tokenized assets account for about 4% of it, a cat token was worth twelve times the entire real-world asset base, and the CEO was posting that it works great for memes too.

Summary

- Robinhood Chain launched July 1 as a permissionless Ethereum layer 2 built for tokenized real-world assets, and within two weeks became one of crypto’s busiest new networks with roughly $312 million locked and 3.6 million daily transactions.

- Tokenized real-world assets, the entire reason the chain exists, account for only about $12.8 million of value and roughly 4% of activity.

- CASHCAT, a memecoin named after Robinhood’s original working name, reached a market cap near $156 million and at its peak was worth about twelve times every tokenized asset on the chain combined.

- CEO Vlad Tenev said on July 2 that assets without utility do not last. Six days later he posted that the chain works great for memes too, and followed the token’s account.

- The cycle has already turned: Noxa, the launchpad driving the boom, earned an estimated $12 million in fees, stopped accepting launches on July 11, and went dark two days later as CASHCAT fell sharply.

On July 1, at a London keynote billed as The World Is Flat, one of America’s largest retail brokerages turned on its own blockchain. Robinhood Chain went live as an Ethereum layer 2 built on Arbitrum’s Orbit stack, carrying 95 tokenized equities priced by Chainlink oracles, a Uniswap deployment for liquidity, Morpho-powered lending, and access wired into a wallet used across more than 120 countries. The pitch was specific and repeated for months: a regulated venue where tokenized real-world assets plug into decentralized finance. For readers new to the launch, crypto.news has also explained the full architecture and Stock Token rules. Two weeks later the chain is a genuine success by every headline metric and a conspicuous failure at the one thing it was built for. The busiest thing on Robinhood’s real-world-asset chain is a cartoon cat.

What the chain actually built

Start with the architecture, because Robinhood did the engineering seriously. Robinhood Chain is a permissionless layer 2 on Arbitrum’s Orbit stack, using ether for gas, running roughly 100-millisecond block times, and settling to Ethereum mainnet from day one. Fees run a fraction of a cent. The flagship product is Stock Tokens, on-chain versions of equities including Nvidia, Apple, and Alphabet that trade around the clock and can move through DeFi as collateral. Day-one partners included Uniswap with a dedicated automated market maker, Chainlink providing oracle pricing across the 95 equities, Morpho for lending, and BitGo for custody.

The strategic logic behind it is coherent and worth taking seriously. Robinhood spent 2025 assembling the pieces: it acquired Bitstamp for trading and institutional infrastructure, WonderFi for Canadian licensing, and ran European tokenized-equity pilots as legal and product rehearsal. A public testnet processed millions of transactions from February. The July launch composed those pieces into a single architecture: assets tokenized on its own network, traded through its own wallet and partner venues, financed through integrated lending, and custodied through its own stack. The composition, more than any single component, is the product. It is a vertically integrated on-chain brokerage built around the use case the chain was built for.

The business case is equally clear once you read the earnings. Robinhood’s crypto transaction revenue fell 47% year over year to $134 million in the first quarter of 2026, and native-app crypto trading volume dropped 48% to $24 billion. The company cut roughly 10% of its workforce, about 290 employees, weeks before the launch, absorbing $28 million in restructuring charges. Total revenue of $1.07 billion and platform assets growing 39% to $307 billion show the wider business is healthy, but the blockchain pivot is explicitly designed to swap volatile transaction revenue for infrastructure and distribution income. Robinhood is not dabbling. It is trying to become the rails.

What actually showed up

The traffic arrived immediately, and it was spectacular. Within two weeks Robinhood Chain had drawn roughly $312 million in total value locked, nearly 800,000 lifetime active addresses, and processed 3.6 million transactions in a single day, with $838 million of decentralized exchange volume over 24 hours. A Bernstein research note counted $3.1 billion in DEX activity across the first seven days, and the network briefly ranked third in daily DEX volume behind only Solana and BNB Chain. More than 65,000 users held around $320 million in stablecoins on it. By any conventional measure of a chain launch, this was a triumph.

Then look at the composition, and the picture inverts. According to Dune Analytics data, asset management accounts for about 40.5% of value locked and lending 38.3%, with spot exchanges at 11.9% and perpetual futures at 5.2%. Real-world assets, the flagship use case behind the chain’s existence, sit at roughly 4.1%. In dollar terms, tokenized real-world assets on the chain total about $12.8 million, of which roughly $10.68 million is stocks, with the remainder split across commodities, tokenized ETFs, and a $410,000 allocation to Treasuries. Robinhood built a settlement layer for tokenized equities and attracted less than eleven million dollars of tokenized equities.

What arrived instead was CASHCAT, a cat-themed token named after the working name Tenev and co-founder Baiju Bhatt used before the company became Robinhood. It has no official affiliation with the company. It surged more than 2,100% in a week, hit an all-time high above $0.17, reached a market capitalization around $156 million and briefly higher, and on its peak day generated roughly $98 million of 24-hour volume, about 17% of the chain’s entire daily DEX figure. At its high, one joke token was worth roughly twelve times every tokenized real-world asset on the network combined. It spawned an ecosystem within days: Cash Dog in Hood, Little John, Hoodrat, Arrow, none of which existed before July 1. Noxa, a launchpad on the chain, averaged roughly 18,600 new token launches per day. For context on how launchpads mint tokens on demand, the mechanism matters as much as the mascot. On July 8, Pump.fun added support for Robinhood Chain tokens, letting Solana’s memecoin crowd trade them without bridging.

The bull case: liquidity is liquidity

The optimistic reading is that this is exactly how successful chains begin, and that treating it as failure misunderstands how crypto adoption works. A new blockchain needs transactions and wallets to look alive, and speculative trading delivers both far faster than tokenized Treasuries do. Permissionless networks with cheap fees and easy token creation reliably attract retail speculators before complex financial products find traction. That is why speculative tokens bootstrap new chains. The comparison traders keep making is Solana, which grew through a memecoin cycle of MYRO and SILLY before producing serious infrastructure and billion-dollar tokens, and one veteran trader explicitly framed Robinhood Chain as resembling Solana’s early ecosystem: rapid token-driven growth, engaged leadership, and a wave of new launches.

There is a bootstrapping argument underneath the noise. Liquidity begets liquidity. Market makers deploy where volume exists, DeFi protocols integrate where users are, and the infrastructure built to service speculation, the AMMs, the oracles, the routing, is the same infrastructure tokenized equities will eventually need. A chain with 800,000 addresses and $3.1 billion of weekly DEX volume is a chain that can credibly ask a tokenized-asset issuer to deploy on it. A chain with $12 million of RWAs and no traffic cannot ask anyone anything. Speculation, in this framing, is the ignition sequence rather than the engine.

Robinhood also has the one asset earlier tokenization projects lacked, which is distribution. This is not a startup trying to persuade strangers to try blockchain equities. It is a brokerage with nearly 28 million customers across 38 countries adding tokenized products to a platform people already use. And the company has profited from joke-driven investing before without apparent damage: it sat at the center of the GameStop episode in 2021, and in the second quarter of that year 62% of its crypto revenue came from Dogecoin. Robinhood has always monetized retail enthusiasm and then sold those users more products. Memecoins on its chain may simply be the top of a familiar funnel.

The bear case: the wrong audience, permanently

The skeptical reading is that this is the oldest failure mode in crypto infrastructure, which is building for one audience and attracting another that never converts. Memecoin traders are mercenary by construction. They run to wherever activity is and are loyal to no chain, which means Robinhood Chain’s current users may have no overlap whatsoever with the investors it hopes to attract. The moment a flashier chain offers quicker profits, the volume leaves, and what remains is the $12.8 million of tokenized assets that was there all along. Traffic that departs on a whim never becomes a user base.

The proof arrived faster than anyone expected. Noxa, the launchpad feeding the entire boom, generated an estimated $12 million in cumulative fees, then abruptly stopped accepting new token launches on July 11, at the precise moment CASHCAT was hitting peak trading volume, and went dark two days later, citing concerns about low-quality tokens flooding the platform. Its business model shows how launchpads like Noxa earn from launches. CASHCAT fell more than 33% in 24 hours. One prominent trader who claims to have ridden the token from a $10,000 market cap to $230 million dismissed the selloff as noise. The infrastructure that produced the traffic exited within eleven days of the chain going live, which is not the profile of a bootstrapping sequence. It is the profile of an extraction cycle.

The distributional facts are worse than the price action. An early buyer spent $838 on 15.04 million CASHCAT tokens, sold about 13.5 million for roughly $917,600, and held a remainder worth about $133,700, a return in the region of 1,250 times. A second wallet turned $85 into 17.4 million tokens and realized about $687,700 while sitting on roughly $1.2 million more on paper. The five most profitable wallets banked close to $3.7 million between them. Every dollar of that came from the other side of roughly 12,300 sell orders, which is to say from people who bought later and worse. And the headline metrics deserve an asterisk: a 90-day gas fee subsidy is inflating transaction counts, which makes direct comparisons with chains like Base unreliable.

The Tenev problem

Sitting on top of all this is a contradiction the company has not resolved, and it belongs to the chief executive personally. On July 2, the day after the chain went live, Tenev told CNBC that assets without utility do not serve a lasting purpose and that tokenized real-world assets were the durable direction for crypto. It was a clean statement of the thesis the entire chain was built to prove. Six days later, as CASHCAT climbed, he posted on X that while the company is building Robinhood Chain to be the best chain for real-world assets, it works great for memes too. He then followed the token’s account.

The charitable reading is that he was simply describing reality with good humor, and that a CEO refusing to acknowledge the most visible thing happening on his own network would look ridiculous. Robinhood’s crypto chief, Johann Kerbrat, stayed rigorously on message when asked, saying the company remains focused on building a secure and scalable foundation for real-world assets. Companies contain multitudes, and a permissionless chain by definition cannot control what deploys on it. Robinhood did not create CASHCAT and has no affiliation with it.

The uncharitable reading is that the endorsement, however light, told the market what Robinhood actually values, which is volume. There is a real cost to that. The entire regulatory proposition of Robinhood Chain is that it is a compliant venue where a licensed brokerage extends institutional standards into DeFi. That proposition is what would eventually persuade issuers and institutions to tokenize serious assets there. A CEO cheerleading a memecoin one week after dismissing memecoins does not obviously advance that case, particularly while Stock Tokens are structured as tokenized debt securities that grant no shareholder rights and remain unavailable to Americans. The company is asking regulators and institutions to take it seriously as financial infrastructure while its most famous product is a cat.

The corporate chain question

Robinhood Chain did not arrive in isolation, and the pattern it belongs to is arguably more consequential than anything happening on the chain itself. Coinbase has Base. Stripe has Tempo. Robinhood now has its own layer 2. A category of corporate-backed networks is forming in which crypto and payments companies build their own rails instead of relying on neutral public infrastructure, and each one shifts attention, liquidity, and value away from the developer-led ecosystems that defined the industry’s first decade.

The appeal to the company is obvious. Owning the settlement layer means owning the economics: transaction fees, sequencer revenue, and the ability to route order flow through infrastructure you control instead of renting someone else’s. It also means control over compliance, which for a licensed brokerage is not a nice-to-have. Robinhood’s competitive advantage over crypto-native rivals is its brokerage licenses and regulatory relationships, and a chain it operates is a chain where it can attempt to extend those standards into DeFi. The challenge is that those licenses govern its traditional operations, while the chain is an experiment in whether a regulated institution can impose compliance on an inherently borderless, permissionless environment. CASHCAT is the first evidence on that question, and the answer so far is that it cannot.

The value-capture math is where this gets genuinely uncomfortable for the wider ecosystem. Robinhood Chain runs on Arbitrum’s stack and settles to Ethereum, and one analysis circulating in mid-July calculated that of roughly $816,000 in revenue the chain had grossed since inception, Arbitrum took about 10% as the middleware provider, and Arbitrum in turn paid Ethereum a settlement bill measured in four figures. Ethereum provides the security that makes the whole arrangement credible and captures almost none of the economics. That is the layer-2 value drain in a single line item, and it is the same dynamic that has collapsed Ethereum’s fee burn and pushed its net issuance mildly inflationary since activity migrated off the base layer.

So the strategic picture is stranger than the memecoin story alone suggests. A brokerage under real revenue pressure built a chain to capture infrastructure economics, chose Arbitrum’s stack to do it, and inherited Ethereum’s security nearly for free. The chain then filled with speculation the brokerage says it did not want but has not discouraged. Meanwhile the neutral chains that made this architecture possible collect a rounding error. Whether or not tokenized equities ever show up on Robinhood Chain, the launch is already a useful data point about who captures value in a world of corporate rails, and the answer is not the people who built the roads.

The verdict, for now

The fair conclusion is that both stories are still live, and the next few months settle it. The test Robinhood set for itself is measurable and specific: if tokenized real-world assets grow well beyond roughly $13 million while memecoin activity fades, the strategy is working and the speculation was just ignition. If real-world assets stay flat while the speculation moves on to the next chain offering quicker profits, then Robinhood Chain becomes another entry in crypto’s long catalogue of infrastructure that attracted a wave of speculation and never became the thing it was built to support.

The first real evidence arrives with Robinhood’s second-quarter earnings on July 29, which should give the first genuine look at Stock Token adoption rather than chain-level vanity metrics. Watch the RWA number specifically, not TVL, not transactions, and not DEX volume, all of which are currently measuring something other than the product. Watch whether liquidity depth on the chain’s AMMs persists after the gas subsidy expires. And watch whether any tokenized-asset issuer of consequence chooses to deploy there, because that is the decision the entire architecture was designed to win.

What makes this genuinely interesting is that Robinhood may be right about tokenization and still lose this particular bet. The thesis that equities eventually settle on-chain, trade around the clock, and function as collateral is a serious one held by serious institutions, and the DTCC is moving tokenized securities into live trading while ICE and OKX form joint ventures aimed at the same market. Robinhood is the only brokerage in that group that also built the settlement layer, which is either visionary or premature. The company spent months and a great deal of engineering building a venue for the future of finance. What showed up first was a cat with a fistful of cash, and a chief executive who spent the previous week explaining why that was exactly the thing crypto needed to outgrow.

Frequently asked questions

What is Robinhood Chain?

It is a permissionless Ethereum layer 2 blockchain launched by Robinhood on July 1, 2026, built on Arbitrum’s Orbit stack. It uses ether for gas, runs roughly 100-millisecond block times, and settles to Ethereum mainnet. It was designed for tokenized real-world assets, with Stock Tokens as the flagship product, alongside DeFi applications including lending, trading, and perpetual futures.

Why are memecoins dominating it?

Because it is permissionless, meaning anyone can deploy a token without approval, and because cheap fees plus easy token creation reliably attract speculative traders faster than institutional products. CASHCAT, named after Robinhood’s original working name, surged more than 2,100% in a week to a market cap near $156 million, and spawned a wave of Robinhood-themed tokens that did not exist before July 1.

How much in real-world assets is actually on the chain?

Roughly $12.8 million, according to Dune Analytics data, of which about $10.68 million is tokenized stocks and the remainder is commodities, tokenized ETFs, and about $410,000 in Treasuries. That is approximately 4.1% of activity on the network. At its peak, the CASHCAT memecoin alone was worth around twelve times the entire real-world asset base.

What did Vlad Tenev say about memecoins?

On July 2 he told CNBC that assets without utility do not serve a lasting purpose and that tokenized real-world assets were the durable direction for crypto. On July 8, as CASHCAT climbed, he posted on X that while the company is building the chain to be best for real-world assets, it works great for memes too, and he followed the token’s account.

What happened to the Noxa launchpad?

Noxa was the largest token launchpad on Robinhood Chain, averaging roughly 18,600 new token launches per day. It generated an estimated $12 million in cumulative fees, then stopped accepting new token launches on July 11 as CASHCAT hit peak volume, and went dark two days later, citing concerns about low-quality tokens flooding the platform. CASHCAT fell more than 33% in 24 hours.

Are Robinhood Stock Tokens the same as owning shares?

No. They are structured as tokenized debt securities, not equity. They track the economic performance of the underlying stock, meaning price movements, but confer no voting rights, no shareholder rights, and no direct legal ownership claim on the shares. They are available in more than 120 countries but not to US persons, and jurisdictional restrictions vary.

Why did Robinhood build a blockchain at all?

Business pressure and strategic positioning. Crypto transaction revenue fell 47% year over year to $134 million in the first quarter of 2026 and native-app crypto volume dropped 48%, so the pivot aims to replace volatile transaction revenue with infrastructure income. Robinhood is also the only brokerage building its own settlement layer while rivals including ICE, OKX, and Binance target tokenized equities.

How will we know if the strategy is working?

Watch the real-world asset figure rather than total value locked, transactions, or DEX volume, which currently measure speculation. If tokenized assets grow well beyond roughly $13 million while memecoin activity fades, the traffic converted. Robinhood’s second-quarter earnings on July 29 should offer the first real look at Stock Token adoption. A 90-day gas subsidy is also inflating transaction counts.

Disclaimer: This article is for information and educational purposes only and does not constitute financial or investment advice. It analyzes a company strategy and on-chain activity, not the merits of any asset. Memecoins are highly speculative, trade on thin liquidity, and most participants lose money. Nothing here is a recommendation to buy any token or use any platform. Always do your own research. Figures are accurate as of July 16, 2026, and move daily.

Polygon Labs has cut another round of jobs as it completes the integration of crypto exchange Coinme, part of a restructuring that the company says is intended to support profitability by 2027.

Summary

- Polygon Labs has reduced its workforce as it completes the integration of Coinme and moves toward a payments focused business model.

- CEO Marc Boiron said the restructuring is intended to help position the company for profitability by 2027 while expanding through the Coinme merger.

- The latest cuts extend a multi year restructuring as Polygon continues shifting its focus from blockchain infrastructure to payment services.

According to Polygon Labs CEO Marc Boiron, the workforce reduction comes as the company enters the final stages of acquiring Coinme and prepares to merge its operations into Polygon Labs, a move he said will expand the organization while changing its focus from a blockchain foundation to a blockchain-enabled payments company.

In a post on X, Boiron said the layoffs were a difficult but necessary part of the transition. He added that integrating the Coinme team would increase the company’s headcount overall even as existing roles were eliminated during the restructuring.

The latest changes extend a strategy Polygon Labs has been pursuing for months. In January, the company spent about $250 million to acquire crypto exchange Coinme and wallet infrastructure provider Sequence, describing both businesses as core building blocks of its Polygon Open Money Stack.

The platform is designed as a vertically integrated payments infrastructure that allows blockchain-based payments to operate with fewer intermediaries while making transfers as seamless as traditional payment systems.

Restructuring continues as payments become the priority

Although Polygon has traditionally focused on blockchain infrastructure, its priorities have changed over the past year. In mid-2025, Polygon co-founder Sandeep Nailwal became CEO of the Polygon Foundation and announced plans to retire the Polygon zkEVM chain, which had been built using technology acquired through Hermez Network and Mir Protocol.

Thursday’s layoffs also continue a series of workforce reductions across the company. Polygon previously eliminated about 100 roles, or roughly 20% of its workforce, in February 2023, followed by another 60 positions during a 19% reduction in 2024. Earlier this year, the company cut another 60 employees, a move widely linked to preparations for integrating the Coinme and Sequence acquisitions.

A Polygon Labs spokesperson declined to disclose how many employees were affected in the latest round. The spokesperson said affected workers will receive severance packages and transition support, while some employees have been asked to remain temporarily to help complete the organizational changes.

In an internal message shared with employees, Boiron said the company decided to act now rather than keep an organizational structure that could affect execution. He acknowledged that two rounds of workforce changes in a single year were difficult for employees but said the restructuring would provide a stronger financial foundation for long-term growth and support the company’s goal of becoming profitable in 2027.

Payments strategy expands despite industry-wide job cuts

Polygon said the restructuring is separate from the Polygon Foundation, which continues to oversee the network, treasury, ecosystem development and protocol upgrades. According to a company spokesperson, Polygon’s stablecoin supply has reached $3.37 billion, making it the eighth-largest stablecoin ecosystem across blockchains, while on-chain payment volume climbed to a record $9.12 billion in June.

The latest cuts come as several crypto firms continue reshaping their businesses through restructuring. In June, Robinhood announced plans to eliminate about 290 jobs, or roughly 10% of its workforce, saying the move would simplify management and improve efficiency even as Chief Executive Officer Vlad Tenev described the business as financially strong.

Workforce reductions have also remained common across non-engineering roles in the digital asset industry. Earlier this year, the Plexus State of Crypto Hiring report found that women accounted for less than 8% of crypto hires despite a sharp increase in female Web3 placements, noting that marketing, communications, community and events positions remain more exposed to layoffs than technical roles. The report said those functions have frequently been targeted as companies reduce costs and reorganize around new business priorities.

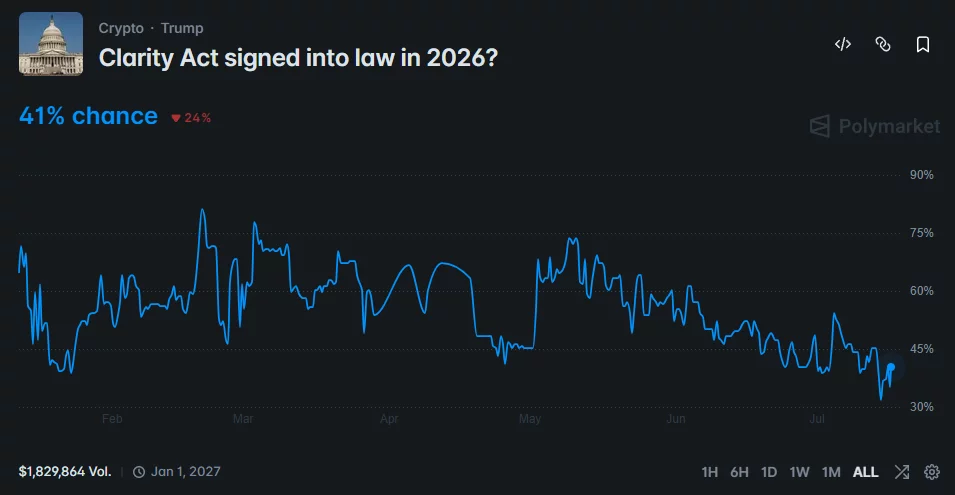

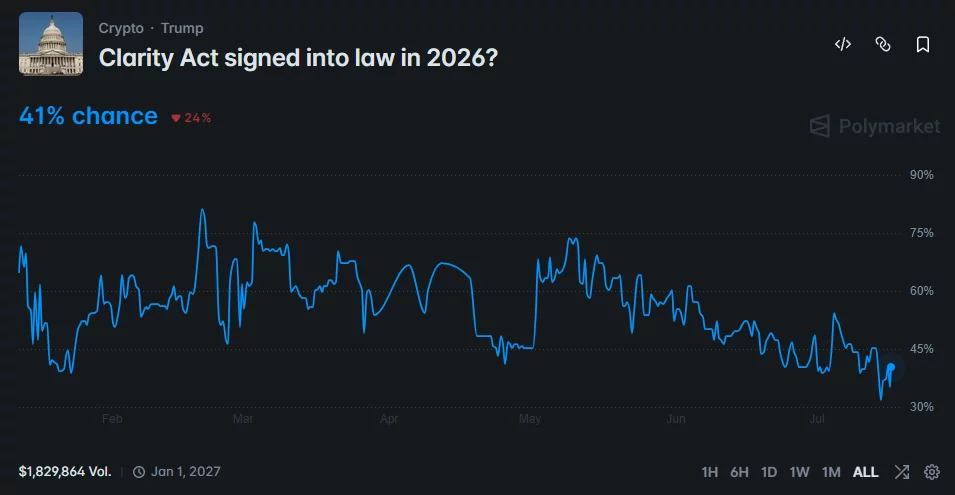

President Donald Trump has convened key Republican senators at the White House as Ripple warned that rejecting the CLARITY Act would preserve regulatory gaps linked to the FTX collapse.

Summary

- Trump will meet Republican senators to address disputes holding up the CLARITY Act.

- Ripple warned that rejecting the bill would leave major crypto regulatory gaps open.

- Polymarket places the bill’s chance of becoming law in 2026 at 36%.

According to Politico, Trump is scheduled to meet several Republican senators on Thursday to discuss the crypto market structure bill and the remaining work needed to secure a Senate vote.

Senator Bernie Moreno told the publication that lawmakers would brief Trump on the legislation and “its path to success.” A Senate Republican aide also confirmed that Senator Cynthia Lummis, a leading supporter of crypto legislation, would attend the meeting.

“We’ll be talking about the entirety of the bill. I mean, obviously the president’s been very engaged in this bill,” Moreno told Politico. “He’s the one who’s really driven the innovation that I think will pay dividends.”

Republican lawmakers are seeking to pass the CLARITY Act before Congress leaves Washington for the August recess. According to Politico, several lawmakers view the current work period as their best chance to move the measure before campaigning for the midterm elections takes up more of the Senate’s schedule.

Ethics provisions remain a key source of disagreement. Senator Thom Tillis expressed hope that lawmakers and the White House could settle the dispute within days.

“I’m hoping that we can come up with some agreement by the end of this week,” Tillis said.

Ripple warns regulatory gaps will remain open

As negotiations continue in Washington, Ripple chief legal officer Stuart Alderoty has urged lawmakers to support the legislation, arguing that a failed vote would leave the crypto industry exposed to misconduct under the existing system.

Alderoty linked his warning to the collapse of FTX, which left customers unable to access billions of dollars held on the exchange.

“We’ve seen this movie. Let’s not watch the sequel,” Alderoty wrote.

Lauren Belive, Ripple’s global co-head of public policy and government, also argued that lawmakers have yet to close the loopholes that contributed to past crypto failures.

“The same regulatory gaps that let bad actors like FTX collapse and wipe out customer funds are still wide open today.”

Under the bill, authority over the crypto market would be divided between the Commodity Futures Trading Commission and the Securities and Exchange Commission. Ripple maintains that the framework would clarify each agency’s role and introduce oversight before qualifying digital assets reach the market.

Political odds fall as the Senate deadline tightens

Doubts about the bill’s prospects have increased on prediction markets despite the White House talks. Polymarket traders have lowered the probability of the CLARITY Act becoming law in 2026 to about 41%.

Negotiations over ethics rules and the limited number of legislative days before the August recess have weighed on those odds. However, the planned White House meeting indicates that Trump and Senate Republicans are still working to resolve the remaining disputes before the window closes.

Separately, the House Financial Services Committee is scheduled to hold a July 17 hearing titled “Building the Future of Finance: How the CLARITY Act Unlocks Innovation.” According to the committee’s description, the session will examine how the legislation could support U.S. leadership in blockchain technology and digital assets.

The committee is also expected to discuss the American Reserve Modernization Act, which concerns the proposed Strategic Bitcoin Reserve. Witnesses will provide views on the measures as Senate Republicans continue their push for a floor vote before the recess.

Tradable is expanding its tokenization push into private credit by planning to bring as much as $1 billion of tokenized real-world assets (RWAs) onto the Stellar blockchain. The effort is designed to help institutions access onchain private markets while handling core operational requirements such as compliance, investor onboarding, and asset lifecycle management.

Tradable said it expects $500 million in notional value to be available at launch, with the amount scaling to $1 billion over time. The company did not provide a launch date.

Key takeaways

- Tradable plans to tokenize up to $1 billion of private credit assets on Stellar, starting with $500 million notional value.

- The Stellar integration is aimed at institutional workflow components, including compliance, onboarding, and asset lifecycle management.

- Tradable reports it has already tokenized $1.7 billion across nearly 30 institutional-grade private credit positions, and Stellar is intended to widen availability.

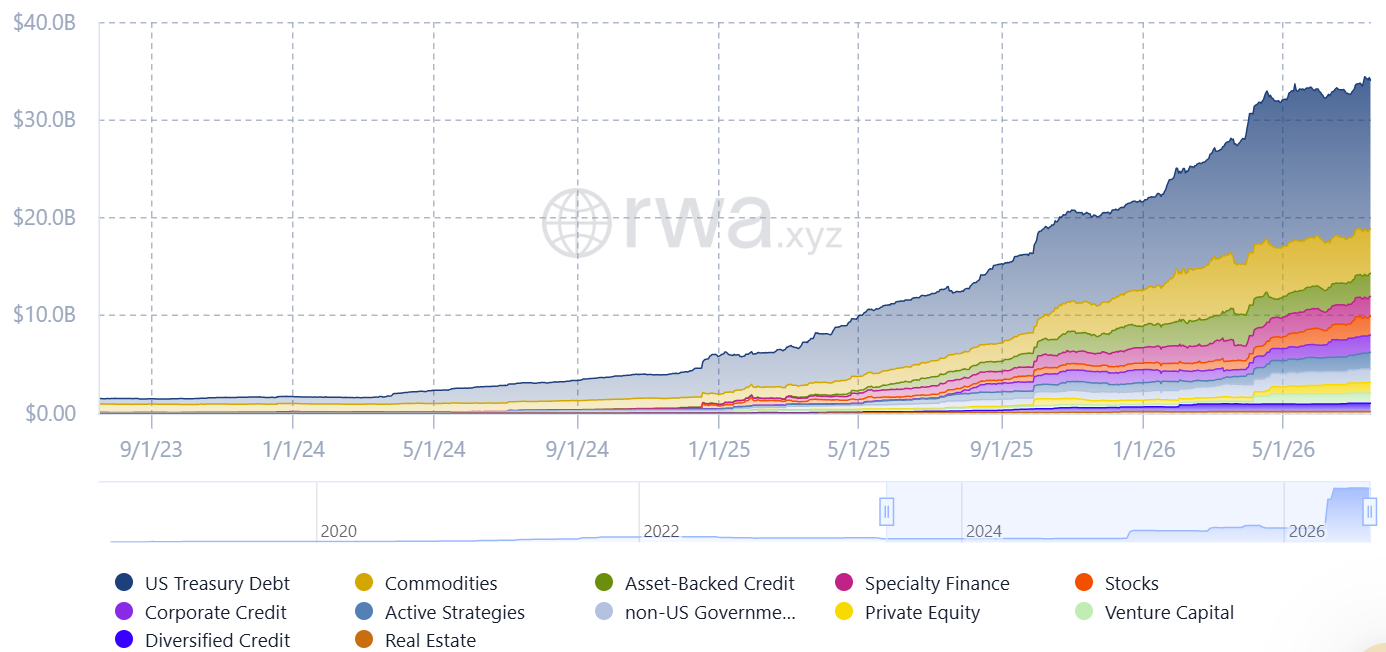

- The announcement aligns with broader growth in tokenized RWAs, with RWA.xyz citing the sector above $34 billion.

- Private credit remains the largest RWA segment, representing about 44% of the market value, according to Bernstein analysts.

Stellar integration targets institutional private credit workflows

The new initiative centers on moving Tradable’s private credit tokenization onto Stellar’s network. Tradable said Stellar will be used to support functions critical to institutional participation—specifically compliance tooling, investor onboarding, and asset lifecycle management.

Denelle Dixon, CEO of the Stellar Development Foundation, characterized the agreement as evidence of growing institutional interest in using Stellar for tokenized RWAs. For market participants, the significance of this type of integration is practical: tokenization efforts often stall not at issuance, but in the day-to-day processes required to meet regulatory and operational expectations.

While Tradable did not disclose when the initiative would go live, the staged rollout—from $500 million notional at launch to as much as $1 billion over time—suggests a ramp strategy rather than an immediate full deployment.

Tradable’s existing footprint in tokenized private credit

Tradable is not starting from scratch. The company said it has already tokenized $1.7 billion in private credit assets across nearly 30 institutional-grade private credit positions. The Stellar integration is therefore positioned as an expansion of distribution and access for those tokenized exposures.

For investors and platform operators, this matters because it implies continuity in Tradable’s product and operational track record. Instead of treating Stellar as a standalone pilot, the company is extending an established portfolio of tokenized private credit assets to a broader blockchain infrastructure.

RWA momentum and the growing role of tokenized credit

The move comes as tokenized RWA activity continues to accelerate across multiple asset classes. RWA.xyz data, referenced in the report, indicates the tokenized RWA market has pushed above $34 billion, supported by institutional adoption.

Stellar’s broader strategy also emphasizes RWAs. The network has increasingly focused on tokenization, and the announcement notes institutional interest that includes the Depository Trust & Clearing Corporation, which has said it plans to connect its tokenization service to the Stellar network.

Taken together, the Tradable news reflects a sector pattern that has become more common in recent months: major public blockchain networks are competing to become the settlement and tokenization rails for regulated, institution-facing capital markets products.

Why private credit is leading tokenized RWAs

Private credit is emerging as the dominant segment of the tokenized RWA market. Bernstein analysts, as cited in the report, estimate private credit accounts for roughly 44% of the sector’s value.

That share has been rising as institutions look to blockchain-enabled systems to improve parts of the private lending lifecycle—origination, servicing, and settlement. In a May research note, Bernstein pointed to Figure Technology Solutions as one driver of growth, referencing its blockchain-based lending platform and loan settlement infrastructure.

Token Terminal has also highlighted private credit as a key contributor to the tokenization boom, attributing momentum to the continued migration of traditional financial assets onto blockchain infrastructure.

For readers trying to gauge where liquidity and product development may concentrate, the recurring theme is that private credit’s economics and documentation-heavy nature are areas where onchain workflows can potentially reduce friction—provided compliance and operational standards are met.

As Tradable scales tokenized private credit on Stellar, the key question for institutions will be how effectively onchain infrastructure supports real-world processes at scale, not just issuance. Observers will likely watch for the timing of the launch, the pace at which notional value rises from $500 million toward the $1 billion target, and whether Stellar’s growing network of tokenization partners continues to broaden access to institutional-grade RWAs.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Following Binance’s European changes, self-custody reportedly attracted most user withdrawals, underscoring growing demand for direct crypto asset control.

Summary

- Binance says 70% of EU user funds moved to self-custody wallets, signaling a shift away from centralized exchanges.

- European Binance users favored self-custody over rival exchanges after MiCA changes, according to Binance figures.

- Binance data suggests EU traders are increasingly choosing self-custody wallets instead of migrating to other exchanges.

Binance switched off the lights for its European users this July. Financial experts and regulators predicted that all those stranded traders would shuffle over to another regulated exchange, sign up, pass the checks, and carry on as before. That is how the story was supposed to play out according to regulators. Rules tighten, one venue closes, users file politely into the next approved CEX down the road. But that’s not what played out.

By Binance’s own count, 70% of the funds pulled off the platform did not go to another exchange at all. They went into personal wallets. Only 30% went to rival regulated venues. So when the door shut behind them, people did not look for another exchange to hold their funds, instead opting to hold their own funds.

These are Binance’s own figures, which are unaudited, so it’s best to leave a bit of room for error. But even if it’s roughly true, it says something that makes every exchange a little nervous. The uncomfortable truth for the big platforms is that most people were never loyal customers, but only felt comfortable to keep their money there temporarily.

Rewinding back a few years, buying Bitcoin and later swapping it for something on another chain (like SOL or ETH) requireda centralized exchange. It held the coins, ran the trades, and handled the messy work between blockchains that required a PhD-level understanding of cryptography. Users parked their money there because there was nowhere else sensible to store it because of a serious lack of alternatives.

But users shouldn’t fret, because more alternatives have arrived since, and they don’t require expert-level knowledge to navigate. Self-custody wallets like MetaMask turned “be your own bank” from a scary slogan into a few taps on a phone. Hardware wallets made cold storage boring, which is exactly what people want it to be. And the protocol THORChain solved the swapping part everyone assumed only an exchange could do, letting users trade one chain’s native asset for others without first handing crypto to a centralized entity. They keep custody the whole time and swap only when they actually want to.

Stack those advancements together and the old deal starts to look a bit lackluster. The main reason to leave a big balance sitting on a centralized exchange was convenience, not necessity. When trading directly from a personal wallet is this easy, keeping a permanent pile of money on someone else’s platform is merely a habit, not a requirement.

None of this makes self-custody a free lunch, and it would be dishonest to pretend otherwise. Holding keys personally means more responsibility. There is no support line to call the recovery phrase is lost and there’s no reset button. The exchange took that burden off people’s hands, and for plenty of people that trade is worth making. Convenience is a real feature in this aspect of holding funds.

But the data from European users suggests the balance has shifted for a growing crowd. Given the choice between re-registering somewhere new and keeping their own coins, most people chose the latter. That is not in protest against any single rulebook, but was meant more as a quiet vote of confidence in tools that may not have existed when they first signed up.

The assumption was users needed an exchange and would always find their way to the next one. Post-July 1st, what was actually revealed is that the middleman was just a convenience all along, useful, popular, and, for a large share of people, no longer essential. The platforms were never as sticky as they looked. Their customers just had not been handed a reason to leave until someone finally opened the door.

Disclosure: This content is provided by a third party. Neither crypto.news nor the author of this article endorses any product mentioned on this page. Users should conduct their own research before taking any action related to the company.

SBI Group has partnered with Ondo Finance to tokenize Japanese stocks and use its yen-backed JPYSC stablecoin for settlement and collateral.

Summary

- SBI has partnered with Ondo to bring tokenized Japanese stocks into its financial ecosystem.

- JPYSC will support settlement and collateral for Ondo’s tokenized financial products.

- The deal follows SBI’s launch of a tokenized Japanese equity fund on Solana.

According to the companies, the agreement will bring Ondo’s tokenized financial products into SBI’s financial ecosystem while connecting Japanese assets with international markets for tokenized securities. The partnership will also use SBI’s customer network to offer the products to millions of investors.

Under the agreement, Ondo Global Markets (BVI) Limited will issue tokenized financial products linked to Japan. SBI, a long-time Ripple partner, will distribute the products through its financial platforms and introduce them to existing customers.

Both companies will also conduct joint marketing and explore distribution through strategic partners. SBI and Ondo did not disclose a launch date, the first assets planned for tokenization, or the regulatory structure that will govern investor access.

JPYSC will support settlement and collateral

As part of the partnership, SBI plans to integrate JPYSC as a settlement and collateral asset for Ondo’s tokenized products. The stablecoin is backed by the Japanese yen and is designed to support transactions within SBI’s digital asset services.

Using JPYSC could allow investors to settle purchases of tokenized Japanese assets with a yen-denominated digital currency. The companies also plan to explore its use as collateral, although they have not provided details about eligible products or collateral requirements.

For Ondo, the agreement provides access to SBI’s position in Japan’s banking, brokerage, asset management, and digital asset sectors. SBI, in turn, gains another route for offering blockchain-based securities through an issuer focused on tokenized real-world assets.

Commenting on the partnership, Ondo Finance CEO Ian De Bode described Japan as an important market for the sector.

“Japan is one of the most sophisticated capital markets in the world, and SBI sits at the center of it. This collaboration creates a path to bring Japanese assets onchain and to connect Japan with the global tokenized economy.”

SBI Chairman, President and CEO Yoshitaka Kitao described Ondo as a potential long-term partner as the Japanese financial group develops links between domestic and overseas digital asset markets.

“We believe Ondo will be a key strategic partner as SBI Group forms a global corridor for digital assets, and we look forward to rapidly advancing a wide range of initiatives together.”

SBI is building an onchain equities pipeline

The Ondo partnership follows SBI Global Asset Management’s launch of a tokenized Japanese equity fund on Solana with DigiFT, a regulated real-world asset exchange.

As reported by crypto.news, SBI Global Asset Management launched the SBI Japan High Dividend Equity Strategy Token, known as the JX token, on July 15. The token gives accredited and institutional investors blockchain-based access to a high-dividend Japanese equity strategy managed by SBI Asset Management Co.

For DigiFT, the JX token is its first onchain tokenization of a Japanese equity fund. SBI described the product as the world’s first tokenized Japanese equity fund, adding another channel for professional investors to access the country’s stock market through blockchain infrastructure.

While the JX token focuses on a managed equity strategy for qualified investors, the Ondo agreement covers tokenized financial products, distribution through SBI’s ecosystem, and JPYSC integration. Together, the two initiatives show SBI is testing separate routes for bringing Japanese securities and yen-based settlement onto public blockchain networks.

A White House teleprompter operator has been placed on paid leave after allegedly earning more than $90,000 from Kalshi bets tied to words President Donald Trump would use in his speeches.

Summary

- The CFTC is investigating Gabriel Perez over more than $90,000 in reported Kalshi profits.

- Kalshi froze most of the gains after flagging bets tied to Trump’s speeches as suspicious.

- The case comes as Trump Media begins selling real-time Truth Social data to financial firms.

According to an ABC News report, the Commodity Futures Trading Commission is investigating Gabriel Perez over trades placed in Kalshi’s “mentions” markets, where users bet on whether Trump will use certain words or discuss specific topics during public appearances.

Perez has reportedly worked on Trump’s speeches since the 2016 presidential campaign, giving him direct access to prepared remarks before they were delivered. Sources familiar with the investigation told ABC News that the CFTC identified bets linked to Trump’s State of the Union address.

Over three months, Perez allegedly traded contracts connected to more than a dozen presidential appearances. ABC News reported that the events included a December prime-time address, Trump’s January speech at the World Economic Forum in Davos and his March remarks at a Medal of Honor ceremony.

Kalshi froze most of the disputed profits

Kalshi flagged the activity as suspicious, froze most of Perez’s reported gains and referred the matter to the CFTC, according to ABC News. The report said Perez has acknowledged some of the trades and is cooperating with the regulator’s inquiry.

Federal prosecutors, however, declined to open a criminal investigation into the betting activity, ABC News reported. The CFTC’s review remains focused on whether Perez used nonpublic information while trading event contracts on the regulated prediction market.

White House Press Secretary Karoline Leavitt confirmed the investigation during a press briefing and said President Trump knew about the case. Describing the president’s reaction, Leavitt said he “believes it’s deeply unfortunate and, frankly, a disgrace.”

Leavitt also confirmed that Perez had been placed on paid administrative leave while cooperating with the CFTC. According to the press secretary, another operator would handle the teleprompter for Trump’s scheduled address that evening.

Prediction markets have faced another case involving alleged access to restricted government information. In April, the Department of Justice charged a U.S. soldier with using classified material to trade Polymarket contracts linked to the capture of former Venezuelan President Nicolás Maduro.

Political posts are gaining value as trading data

Trump’s scheduled remarks already had mentions of markets available, including contracts linked to whether he would reference China. Leavitt said the address would cover the administration’s findings on alleged foreign interference in the 2020 election, adding that Trump’s statements would be supported by evidence.

The investigation has emerged as political statements become a paid source of market data. As previously reported by crypto.news, Trump Media & Technology Group has introduced the Truth API, a licensed service that will send real-time Truth Social posts from high-ranking accounts to financial firms, data providers and news organizations.

Trump Media said subscribers would receive immediate access to public posts that could contain time-sensitive political, policy or market information. Interim CEO Kevin McGurn described the product as an alternative to unauthorized data scraping and said trading firms could use it to monitor influential accounts.

“Markets already move on Truth Social posts,” McGurn said.

While Trump Media expects the API to produce recurring revenue, the Perez investigation concerns a separate issue: whether someone with advance access to presidential remarks used that information to profit from Kalshi contracts.

Tokenization platform Tradable plans to bring up to $1 billion in private credit assets onto the Stellar blockchain, expanding institutional access to tokenized real-world assets (RWAs) as demand for onchain private markets continues to grow.

Tradable said Thursday that $500 million in notional value is expected to be available when the initiative launches, and it will increase the amount to $1 billion over time. The company will use Stellar’s network to support institutional functions, including compliance, investor onboarding and asset lifecycle management.

The timing of the initiative’s launch was not disclosed.

Stellar Development Foundation CEO Denelle Dixon said the agreement reflects growing institutional interest in using the network for tokenized real-world assets.

The move builds on Tradable’s existing business. The company said it has already tokenized $1.7 billion in private credit assets across nearly 30 institutional-grade private credit positions, with the Stellar integration expanding the availability of those assets.

Stellar, one of the oldest public blockchains, has increasingly focused on tokenized real-world assets. The strategy has attracted institutional partners, including the Depository Trust & Clearing Corporation, which plans to connect its tokenization service to the network.

The developments reflect broader momentum in the tokenized RWA market, where institutional adoption has helped drive the sector’s value above $34 billion, according to RWA.xyz.

The tokenized RWA market has expanded rapidly since early 2025. Source: RWA.xyz

Related: DTCC to use Chainlink to power 24/7 collateral management network

Private credit dominates the tokenized RWA market

Private credit has emerged as the largest segment of the tokenized RWA market, accounting for roughly 44% of the sector’s value, according to Bernstein analysts.

The segment has grown as financial institutions increasingly use blockchain technology to originate, service and settle private loans more efficiently. In a research note published in May, Bernstein cited Figure Technology Solutions as a key driver of that expansion, pointing to the company’s blockchain-based lending platform and loan settlement infrastructure.

Token Terminal recently highlighted the role of private credit in fueling the tokenization boom, attributing the expansion to the continued migration of traditional financial assets onto blockchain infrastructure.

Related: Securitize, Cantor target tokenized IPOs for public markets

President Donald Trump has promoted more than 20 companies, including Nvidia, Tesla and Apple, within days of purchasing their shares, according to a CNN investigation.

Summary

- CNN linked Trump’s company promotions to stock purchases made only days earlier.

- Trump bought up to $500,000 in Nvidia shares before announcing faster AI permits.

- The findings have added pressure to include ethics rules in the CLARITY Act.

CNN found that several Truth Social posts announced or praised government actions that could benefit companies held in Trump’s investment accounts. The report has renewed questions about whether his financial interests conflict with decisions made by his administration.

Among the cases examined, CNN pointed to a 2025 post in which Trump announced that his administration would speed up the permits needed by Nvidia and similar companies to build artificial intelligence supercomputers in the United States.

Financial records reviewed by CNN showed that Trump had purchased between $200,000 and $500,000 worth of Nvidia shares several days before publishing the post. The investigation also linked the timing of his purchases to later public comments involving Tesla, Apple and other major companies.

CNN did not report evidence that Trump personally ordered the trades or made the related government decisions to raise the value of his holdings. However, the outlet reported that Trump has not placed his assets in a blind trust, leaving open the possibility that he could know what his investment managers are buying or selling.

White House denies Trump controls the trades

Responding to the report, White House spokesperson Anna Kelly said Trump does not manage the accounts involved in the transactions. According to Kelly, his assets are “held in fully discretionary accounts managed by independent third-party financial institutions.”

Trump has also previously said that professional fund managers control his investments, according to an earlier crypto.news report. His defense separates the timing of the trades from his own actions, although CNN noted that the arrangement does not meet the requirements of a blind trust.

Rep. Rosa DeLauro criticized the transactions after CNN published its findings. Writing on X, the Democratic lawmaker described the situation as: “Profits for him and his billionaire friends, higher prices for you.”

Neither the White House response cited by CNN nor Trump’s earlier comments addressed every company identified by the investigation. CNN also reported no finding that the trades broke federal securities law.

Stock scrutiny adds pressure to CLARITY talks

Questions over Trump’s stock holdings have surfaced as lawmakers debate whether the CLARITY Act should restrict senior government officials from participating in the crypto industry. According to the report, an ethics provision remains a key point of disagreement in efforts to secure bipartisan support for the market structure bill.

Trump’s 2025 annual financial disclosure has added to the dispute by showing that he received as much as $1.4 billion from crypto-related activities. Critics in Congress have cited those earnings while calling for rules that would limit the president’s ability to profit from digital assets during his term.

When previously questioned about his crypto income, Trump denied knowing the amount he had earned, according to CNN. He also argued that receiving the income would not be illegal even if he knew about it.

The stock investigation is expected to follow Trump into his meeting with senators on the CLARITY Act. Lawmakers have yet to resolve whether the bill will include conflict-of-interest restrictions covering the president and other senior officials.

Polygon Labs announced its second round of layoffs in 2026 on Thursday, the same day 1inch co-founder Anton Bukov revealed he was fired in November. Both firms are reorganizing around commercial priorities while their tokens trade near record lows.

The parallel shakeups show a hard truth taking hold across the industry. The people who built crypto’s infrastructure era are paying the price of its push for real revenue.

Polygon Layoffs Mark Fourth Round of Cuts in Three Years

CEO Marc Boiron said Polygon Labs is completing its transformation from a blockchain foundation into a blockchain-enabled payments company, targeting profitability in 2027. He stressed the cuts reflect strategy rather than performance, with severance and career support for affected staff.

Thursday’s move extends a steady drumbeat. Polygon cut roughly 100 roles in 2023, another 60 in 2024, and around 60 more this January after its $250 million-plus deal to acquire Coinme, a US payments firm licensed in 48 states, and wallet developer Sequence.

The business case is visible on-chain. Stablecoin supply on Polygon stands at $3.36 billion, the eighth-largest on any blockchain, per DefiLlama, while the company says volume hit a record $9.12 billion in June. Visa also added Polygon to its stablecoin settlement program earlier this year.

“We chose to move now because momentum like this deserves a company built to run with it. Revenue is strong, stablecoin volume keeps setting records, our customer pipeline is stronger than any of us imagined, and our on-chain payments solution went live in record time,” Boiron explained.

Polygon Foundation CEO Sandeep Nailwal separately said a third of the team built 13 AI projects in a three-day sprint, signaling how leadership expects the remaining staff to work.

Follow us on X to get the latest news as it happens

1inch Co-Founder Says He Was Fired, Launches Second Tier

Hours earlier, Bukov disclosed that 1inch fired him in late November 2025 despite his 50% stake. The co-founder, who led the DEX aggregator’s protocol architecture and security since May 2019, said he retains no operational or security oversight.

Where Polygon frames its restructuring as a strategy, Bukov describes his exit as a leadership dispute. He said he pushed for changes in management and communication after user and teammate feedback, and was dismissed.

“The most important lesson that stayed with me: the long-term success of any project stands on two pillars of equal weight – technical excellence and leadership grounded in values that hold under pressure,” Bukov stated.

He is now building Second Tier, an infrastructure startup he says will pursue an open financial system without friction or middlemen.

Tokens Near Record Lows as Builders Bear the Cost

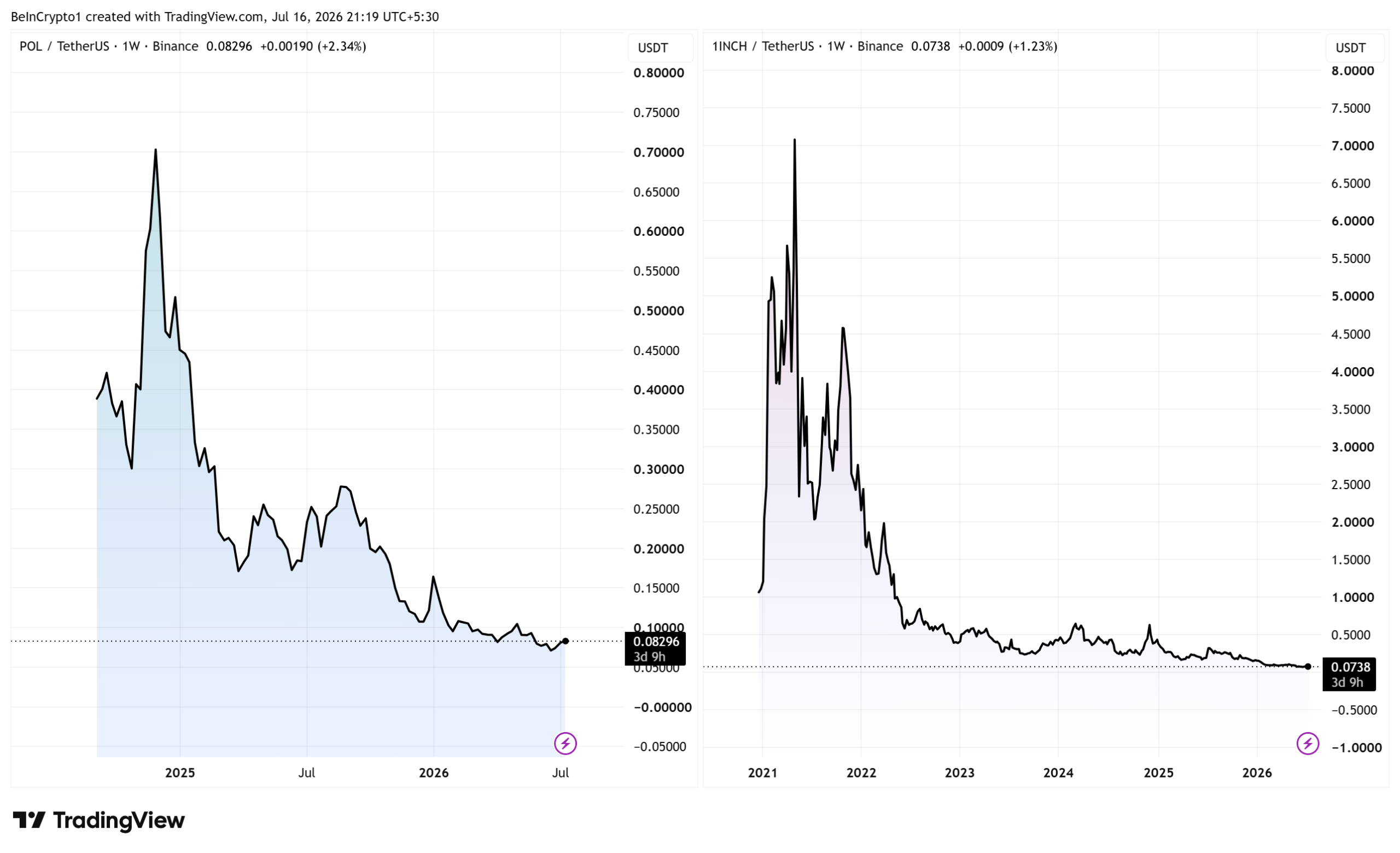

The market has yet to reward either shakeup. Polygon Ecosystem Token (POL) hit an all-time low of $0.068 on July 1 and traded at $0.0838 at press time, down nearly 64% in a year, per BeInCrypto markets data.

“I understand why Polygon Labs is making this transition. But as a long-term POL holder who has absorbed huge losses, this raises an important question. Polygon Labs is becoming a for-profit payments company, while POL is roughly 98% below its ATH. Holders have no equity in Polygon Labs and no claim on its future profits. How will the success of this company create measurable value for POL?” one user posed.

Meanwhile, 1inch (1INCH) trades at $0.0739, down 78% over the same period after its own all-time low on June 6.

Both stories point the same direction. Crypto firms are trading protocol-era talent for commercial discipline, and the coming quarters will show whether token holders ever share in the payoff.

The post Polygon Layoffs and 1inch Founder Exit Expose Crypto’s Costly Pivot to Revenue appeared first on BeInCrypto.

Keir Starmer Makes London Mayor Sadiq Khan A Peer

Diploma PLC (DPMAY) Q3 2026 Sales/Trading Call Transcript

Robinhood built an RWA chain. Memecoins took it.

-

Fashion6 days ago

Fashion6 days agoWeekend Open Thread: Nutriplenish Leave-In Conditioner

-

NewsBeat8 hours ago

NewsBeat8 hours agoLondon Mayor Sadiq Khan handed a peerage by Keir Starmer alongside 15 other Labour figures… just days before the PM leaves No10

-

Sports7 days ago

Sports7 days agoSuper Eagles star Moses Simon opens up on Liverpool transfer regret

-

Crypto World23 hours ago

Crypto World23 hours agoCFTC blocks Kalshi from unwinding Michigan trades after court order

-

Business21 hours ago

Business21 hours agoNvidia Stock Slips After Big Tuesday Rally as Huang Confirms Vera Rubin Chip Is Now in Production Today

-

Politics1 day ago

Politics1 day agoYoung campaigners urge incoming PM to act on outdoor junk food ads

-

News Videos2 days ago

News Videos2 days agoXRP BOMBSHELL… XRP OMBOARDED FOR TRANSACTIONS!!!

-

Tech3 days ago

Tech3 days agoGet Your ESP32 Sunny Side Up With This Solar Dev Board

-

Entertainment1 day ago

Entertainment1 day agoDisney’s Most Ambitious Failed Star Wars Attraction Is Coming to SDCC

-

Tech2 days ago

Tech2 days agoDark Secrets Emerge When Jailbreaking LLMs

-

Crypto World3 hours ago

Crypto World3 hours agoInjective Submits SEC Transfer-Agent Registration to Onchain Ownership Records

-

Sports1 day ago

Sports1 day agoNew Cornerback Enters Vikings Trade Rumor Mill

-

Tech3 days ago

Tech3 days agoCloudflare Precursor Watches Your Mouse and Keyboard To Decide If You Are Human

-

News Videos3 days ago

News Videos3 days agohow to make coin bank box with cardboard #scienceproject #money #diy #shorts

-

Entertainment1 day ago

Entertainment1 day agoVicki Gunvalson Defends Discussing Heather Dubrow’s Money

-

Crypto World2 days ago

Ripple, Coinbase, Circle Join Linux x402 Foundation to Help Shape AI Payments

-

Business2 days ago

Business2 days agoACCC warns AI could lift insurance costs in risk-prone areas

-

NewsBeat1 day ago

NewsBeat1 day agoWatch: Is Donald Trump facing a popular backlash on immigration?

-

Sports24 hours ago

Sports24 hours agoMichigan officials not expected to discuss AD Warde Manuel at Thursday meeting

-

Business2 days ago

Business2 days agoSubaru recalls 541,000 vehicles over federal safety sticker mistake: NHTSA

You must be logged in to post a comment Login