Crypto World

Prediction Market Kalshi Sued Over Khamenei Trade Carveout

A federal class-action suit targets prediction platform Kalshi, accusing the company of failing to clearly disclose a death carveout tied to a market that forecast the fate of Iran’s former supreme leader. The case centers on the “Ali Khamenei out as Supreme Leader” market, which was halted after the death of Ayatollah Ali Khamenei was confirmed, leaving won bets unsettled in a way the plaintiffs say was not anticipated by users. The plaintiffs contend that the death carveout policy was never incorporated into the user-facing rules summary and was not presented in a way that would alert a reasonable consumer. Kalshi’s co-founder has acknowledged that earlier disclosures were grammatically ambiguous, though the company maintains it did not profit from such markets. The lawsuit also highlights disputes over payouts and reimbursements to traders who were affected.

Key takeaways

- The class-action alleges Kalshi concealed a death carveout in a major political market and failed to disclose how payouts would be handled when a death outcome was involved.

- Trading was halted and positions were voided after the death was confirmed, meaning the market did not resolve to a definitive “yes.”

- Kalshi maintains it does not list death-related markets and asserts the policy is stated in market rules; co-founder Tarek Mansour says no money was made from the market and losses were reimbursed out of pocket.

- Plaintiffs criticize the reimbursement method, arguing the last-traded-price approach and the exact timestamps used to compute it were not disclosed or transparent.

- The suit arrives as prediction-market volumes on Kalshi and peers rose to record levels in 2026, underscoring growing interest in off-exchange forecasting tools.

- The dispute spotlights ongoing scrutiny of how market-design rules are conveyed and enforced in politically sensitive event markets.

Sentiment: Neutral

Market context: The dispute sits at a time when prediction-market platforms have drawn heightened attention as volumes surge in 2026. Regulators and market participants are increasingly weighing how disclosures, rule wording, and risk-management practices shape user trust in event-based forecasts.

Why it matters

For users, the case underscores the importance of transparent disclosures when markets hinge on sensitive outcomes such as political leadership and life-and-death scenarios. The reimbursement mechanism—meant to mitigate losses when outcomes are blocked or unsettled—will come under greater scrutiny if procedural details remain opaque. For Kalshi and the broader prediction-market sector, the suit tests how clearly rules must be communicated within user interfaces and whether policies prohibiting certain outcomes can withstand legal challenges if not explicitly explained. The outcome could influence how platforms design carveouts, disclosures, and payout methodologies when markets intersect with real-world, high-stakes events.

Beyond Kalshi, the dispute feeds into a broader conversation about governance and consumer protection in the burgeoning forecasting economy. As platforms compete for liquidity and user engagement, the balance between creative market design and clear, auditable rules becomes a growing focal point for investors, policymakers, and users alike. The case also arrives amid visible pushback over how reimbursements are determined, raising questions about standardization across operators and the expectations set for participants in this niche trading space.

What to watch next

- Legal filings and court rulings in Risch v. Kalshi LLC, including any motions to dismiss or for class certification.

- Kalshi’s public updates to its market rules or disclaimers regarding death-related markets and any changes to the carveout policy.

- Public disclosure of the precise methodology and timestamps used to calculate last-traded prices for reimbursed trades.

- Any settlements or additional disclosures arising from related enforcement actions or disclosures in 2026 trading-volume activity.

- Follow-up reporting on how prediction-market operators adjust governance and risk controls in response to high-profile outcomes.

Sources & verification

- Court Listener docket for Risch v. Kalshi LLC, detailing the class-action complaint and filings.

- Public statements from Kalshi co-founder Tarek Mansour on X addressing the death-market carveout and reimbursements.

- Cointelegraph coverage on Kalshi’s response to the carveout and the reimbursement policy.

- Cointelegraph reporting on related Kalshi developments, including policy enforcement and market dynamics in 2026.

Market reaction and regulatory considerations surrounding Kalshi’s death-market carveout

A class-action alleging disclosure gaps around Kalshi’s death carveout has put the platform’s governance under a sharp lens. The complaint centers on the “Ali Khamenei out as Supreme Leader” market, which was voided after the death of the Iranian leader was confirmed, leaving a scenario where winners did not receive a payout and losers did not simply absorb gains. Plaintiffs emphasize that the carveout policy was not clearly present in the user-facing rules summary, and they point to statements from Kalshi acknowledging earlier disclosures were ambiguous rather than intentionally misleading.

“With an American naval armada amassed on Iran’s doorstep and military conflict not merely foreseeable but widely anticipated, consumers understood that the most likely, and in many cases the only realistic, mechanism by which an 85-year-old autocratic leader would ‘leave office’ was through his death. Defendants understood this as well.”

Kalshi’s co-founder, in defending the firm’s approach, reiterated that the company does not list markets directly tied to death and that the policy to avoid profit from such outcomes is embedded in the rules. He asserted that Kalshi did not profit from the market and that all losses were reimbursed out of pocket, a claim designed to counter arguments that the platform benefited from a misleading disclosure regime. The company’s stance aligns with a broader commitment it has publicly stated—that death-related markets are not listed and that the policy is clearly articulated within the market’s governance framework.

The debate over the reimbursed trades centers on the method used to determine compensation. Kalshi’s team has explained that reimbursements were calculated using the last traded price once the death confirmation occurred, a methodology designed to cap potential losses for participants while avoiding windfall profits. Critics, however, argue that the process and its exact timestamps should be transparent and auditable to ensure confidence in the remedy. The plaintiffs contend precisely that transparency is lacking, arguing that traders deserve a clear, reproducible account of how reimbursements were computed.

Trading activity in prediction markets continued to climb in 2026, with volumes reaching new highs even as legal questions surrounding rule disclosures and payout mechanics persist. The ongoing scrutiny reflects a maturing market where participants increasingly demand clarity on risk controls, governance, and the boundary between ambition in market design and consumer protection. In parallel, Kalshi has faced other regulatory and governance questions, including episodes related to insider trading and broader policy enforcement within its platform ecosystem.

As the case advances, observers will watch not only the court’s handling of disclosure questions but also whether Kalshi, and the wider ecosystem, respond with more explicit UI disclosures or refinements to how sensitive outcomes are treated in live markets. The outcome could influence how other platforms articulate carveouts and payout rules, shaping a more predictable framework for participants who use event-driven markets to hedge risk or speculate on real-world events.

AI Agents are evolving from passive assistants into active economic participants. This report is structured into six chapters, systematically examining the core infrastructure stack, the explosion of application ecosystems, and the evolving industry landscape of the Agent economy.

At the macro level, it analyzes the market outlook for Agentic Commerce and identifies key infrastructure gaps. At the protocol layer, it provides an in-depth analysis of three complementary protocols: x402, ERC-8004, and Virtuals Protocol. At the application layer, it uses OpenClaw as a case study to explore the real-world deployment path of the Agent economy. Finally, it offers a comprehensive industry assessment across multiple dimensions, including competitive landscape, payment rails, security risks, and business models.

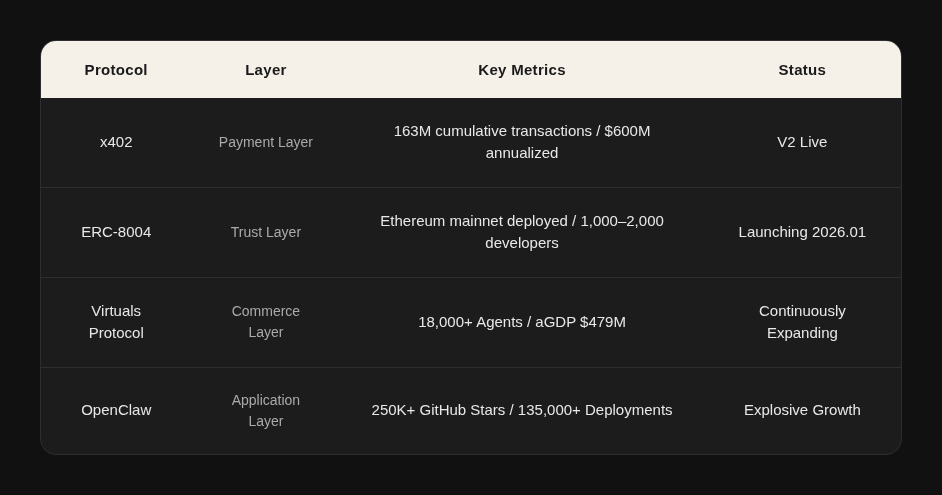

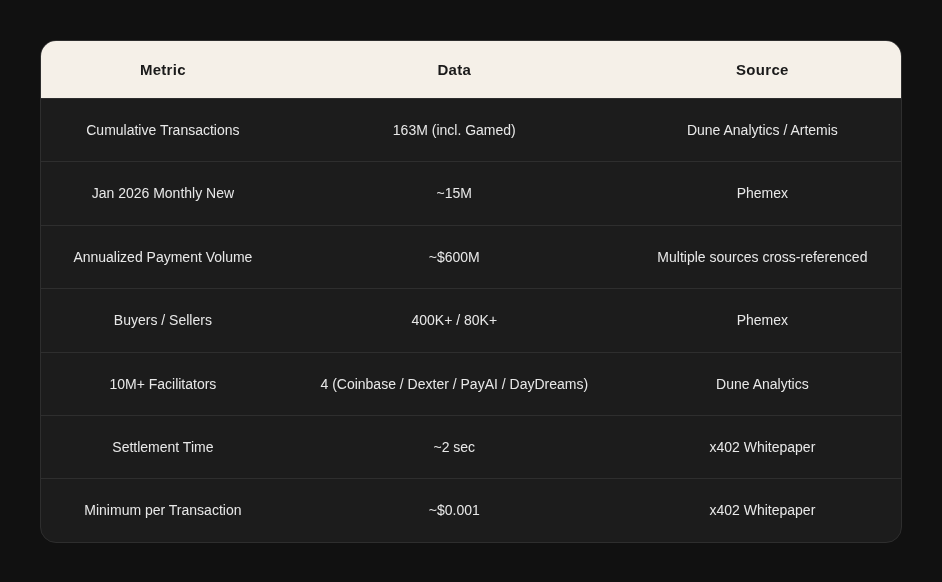

x402 (Payment Layer), jointly launched by Coinbase and Cloudflare, embeds stablecoin micropayments directly into the HTTP protocol layer. As of the end of 2025, it has processed over 100 million transactions, with an annualized payment volume reaching $600 million.

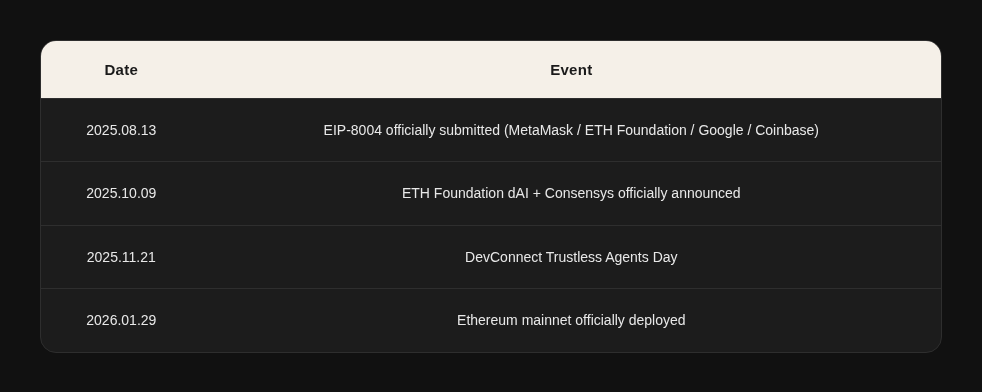

ERC-8004 (Trust Layer), proposed by the Ethereum Foundation’s dAI team in collaboration with MetaMask, Google, and Coinbase, provides AI Agents with three core on-chain registries: identity, reputation, and verification. It went live on the Ethereum mainnet on January 29, 2026.

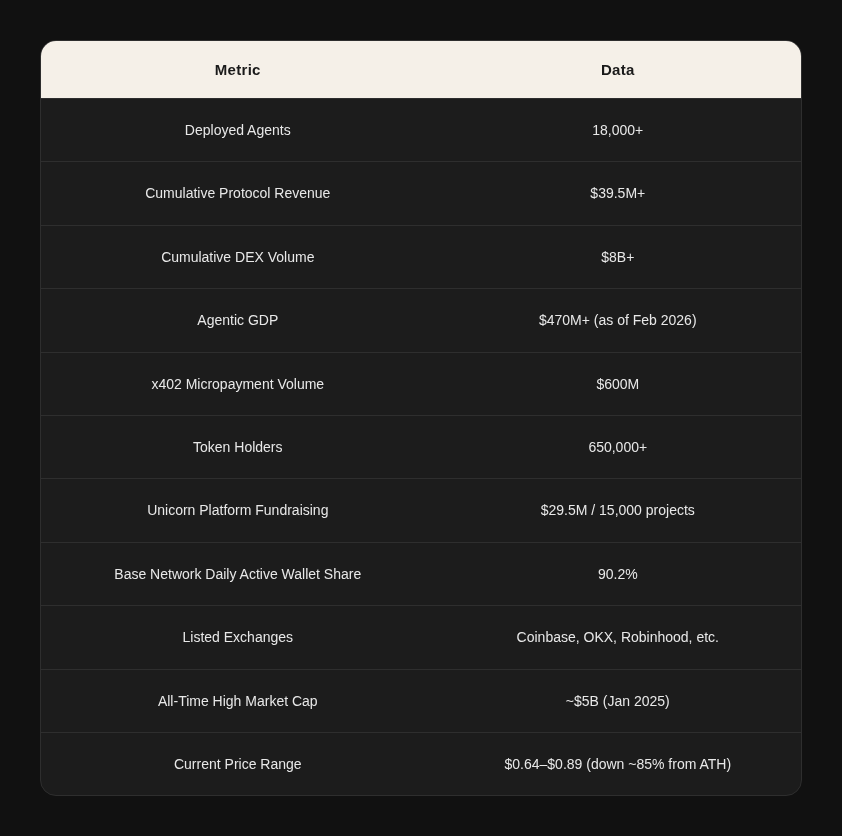

Virtuals Protocol (Commerce Layer) has built a full-stack Agent commercialization platform, enabling autonomous transactions between Agents via ACP. It has deployed over 18,000 Agents, with aGDP exceeding $479 million.

OpenClaw (Application Layer), developed by Austrian developer Peter Steinberger, surpassed React with over 250,000 GitHub stars in just four months, becoming the fastest-growing open-source project in GitHub history. By natively embedding AI into more than 20 existing messaging platforms, it has catalyzed the crypto community to organically build on-chain economic infrastructure on top of it—making it a key case study for observing real interactions between Agents and on-chain protocols.

Chapter 1: Macro Background

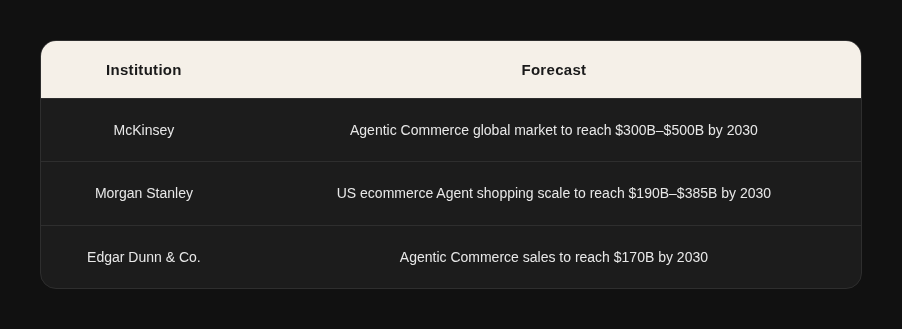

1.1 Market Size Forecast

The Agentic Payment sector is in a phase of rapid expansion, with multiple institutions offering optimistic projections for its market size:

1.2 Infrastructure Gaps

Existing infrastructure is fundamentally hostile to the Agent economy: OAuth requires human interaction, credit card forms rely on manual input, and data silos prevent autonomous access. While Agents have already achieved autonomy at the “capability layer” (thinking and acting independently), they remain constrained at the “economic layer,” locked into infrastructure designed for humans (identity, coordination, and economic activity).

Two evolutionary paths are currently emerging:

- Centralized, compliance-driven path: Communication via A2A, tool integration via MCP, and payments via AP2/ACP (led by OpenAI and Stripe, purely Web2)

- Decentralized, permissionless path: x402 + ERC-8004 / 8183 + ACP (Agent coordination framework)

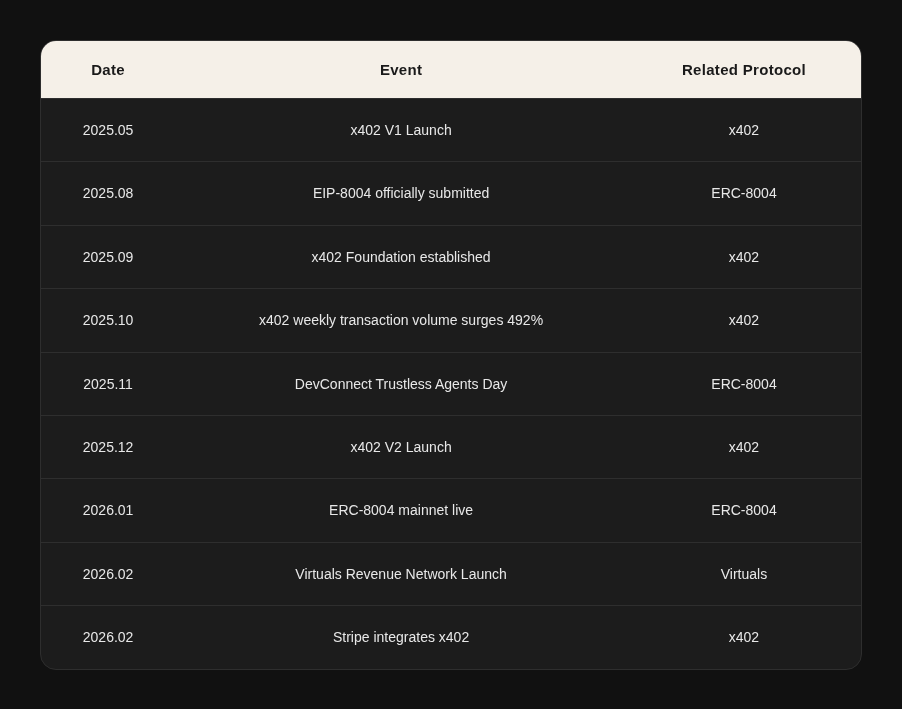

1.3 Key Timeline

Note: As of March 2026, the average daily transaction volume has significantly declined from its December peak, with infrastructure-related transactions experiencing the largest drop (>80%).

Chapter 2: x402 Protocol – Agent Payment Layer

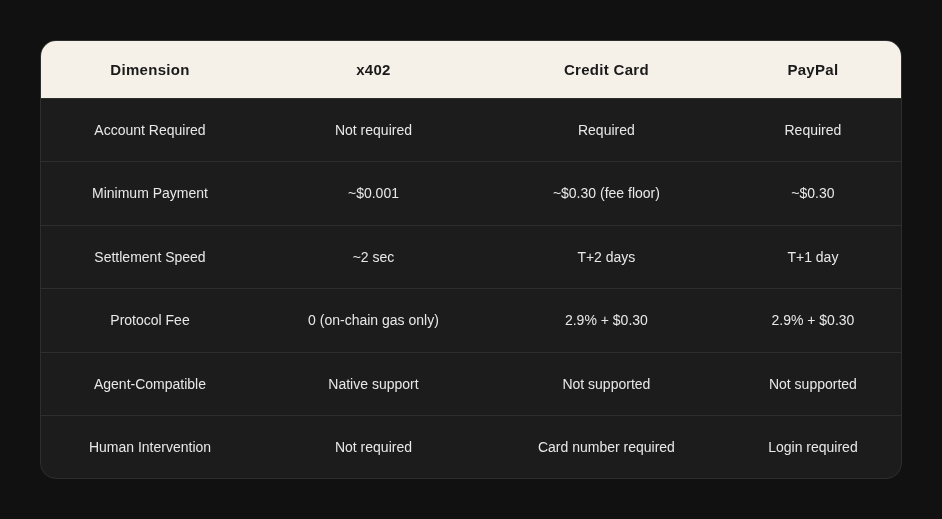

x402 is an open-source payment protocol that revives the HTTP 402 status code, allowing any HTTP request to natively carry stablecoin payments. This enables AI Agents to perform instant pay-per-use transactions.

It is important not to think of x402 as just another payment protocol. It represents a redesign of the fundamental unit of economic activity: moving from “register → review → authorize → use” to “pay → use.” In essence, x402 = “Swift for agents.”

The current API economy operates under an implicit assumption: a human is involved in the middle. The process to obtain an API key—register → enter email → approval → copy key → paste into code—assumes human participation at every step. This workflow fails in an Agent economy because AI Agents cannot register themselves, fill forms, or manage keys.

x402 addresses this by leveraging the HTTP 402 status code to enable native stablecoin payments. When an Agent receives a 402 response, it directly pays on-chain (e.g., in USDC) and receives a proof-of-payment, enabling seamless pay-per-use interactions.

2.1 Protocol Overview and Workflow

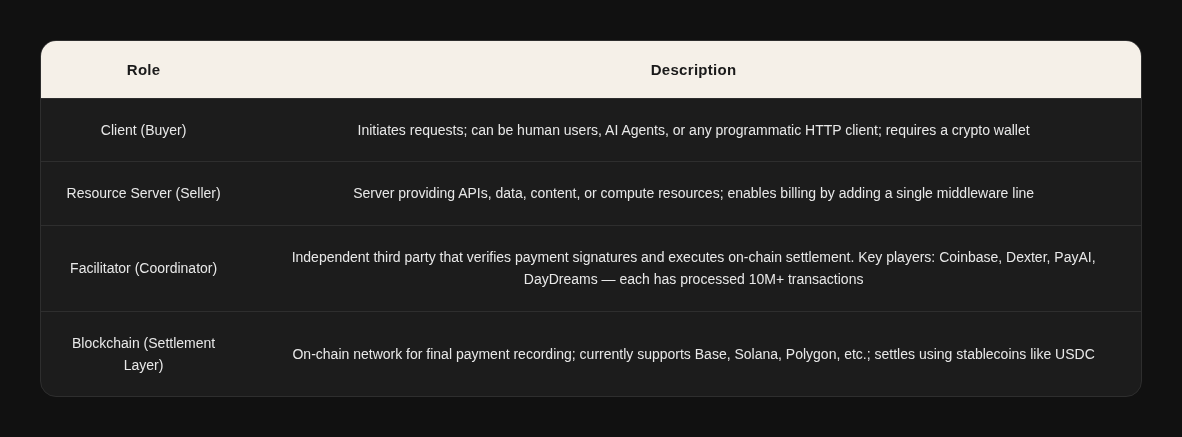

Core Roles

Five-Step Transaction Workflow

- Request Resource: The client sends a standard HTTP request to the resource server (e.g., GET /api/weather).

- Return Quote: The server responds with an HTTP 402 status code, including structured payment instructions in the response headers (currency, amount, wallet address, network).

- Sign Payment: The client constructs and signs a payment authorization using its wallet private key, placing the signed payload in the X-PAYMENT request header and resending the request.

- Verify & Settle: The server forwards the payment information to a Facilitator for verification. Once confirmed, the Facilitator executes the stablecoin transfer on-chain.

- Deliver Resource: Upon confirmation, the server returns the requested data/content/computation result to the client.

The entire process—from initiating the request to receiving the resource—takes approximately 2 seconds.

Comparison with Traditional Payment Methods

Key Features: No account registration, no API key, no subscription, and no human intervention required. Payments are as natural as sending an HTTP request—this is why x402 is called the “Internet-native payment layer.”

2.2 Key Metrics

Data Quality Note: According to Artemis analysis, the ratio of Real to Gamed transactions in x402 is close to 1:1 (e.g., on 2026.01.11, Real: 520K vs. Gamed: 518K). The true organic scale should be interpreted with a discount.

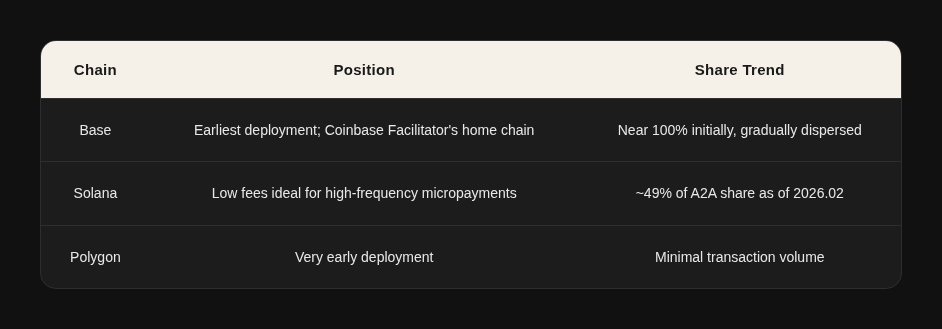

Distribution by Blockchain

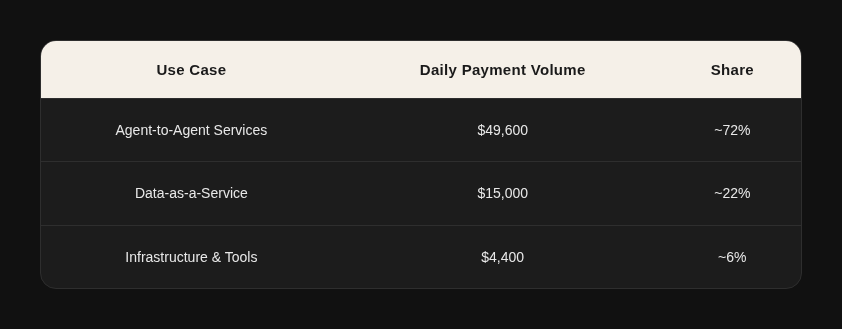

Classification by Use Case (On-Chain Snapshot as of 2026.01.11)

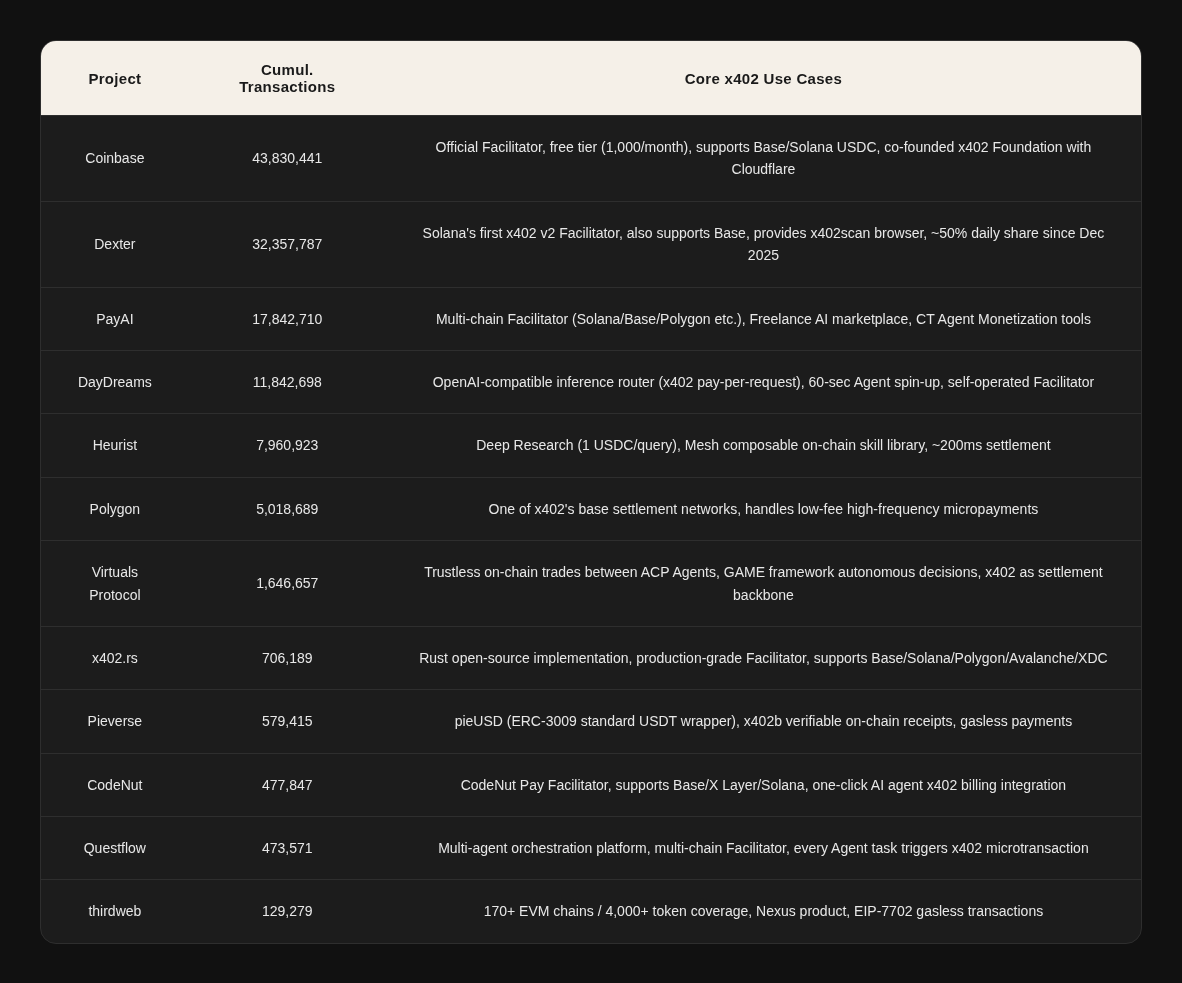

2.3 Top Project Usage Rankings (as of March 2026)

Data Source: Dune Analytics – x402 Transactions per Project dashboard

2.4 Core Upgrades in V2

Wallet Identity + Reusable Sessions

In V1, every API call required a full on-chain transaction. V2 introduces the Sign-In-With-X (SIWx) mechanism: once an Agent verifies its wallet identity, subsequent calls can reuse the session without on-chain confirmation each time. Essentially, this upgrades pay-per-call to a subscription model, addressing performance bottlenecks in high-frequency scenarios.

Multi-Chain Unification + Traditional Payment Compatibility

V2 standardizes the identification of networks and assets, creating a unified payment format (x402) that works across chains and traditional payment rails. Base, Solana, other L2s, as well as ACH, SEPA, and card networks, are all integrated into the same payment model. This is the most critical upgrade—x402 evolves from a “crypto-only payment protocol” into a neutral payment layer bridging crypto and traditional finance.

Service Auto-Discovery

V2 introduces a Discovery extension, allowing x402 services to expose structured metadata for automatic crawling and indexing by Facilitators. AI Agents can automatically discover services, understand pricing, and initiate payments. This is especially crucial for the Agent economy—Agents no longer need prior knowledge of a service provider’s payment interface and can autonomously discover and pay for services at runtime.

Modular SDK

With a plugin-based architecture, new chains are added as independent packages, reducing integration costs. Cloudflare has proposed a deferred payment scheme, including Circle’s Gateway solution, which is still under development.

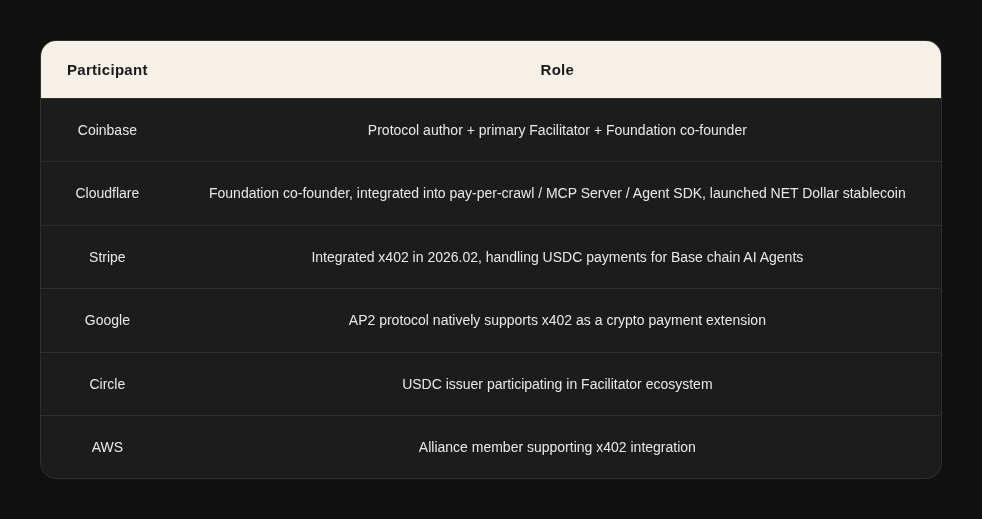

2.5 Ecosystem Participants

Foundation and Protocol Layer

2.6 Agent Payment Stack Landscape

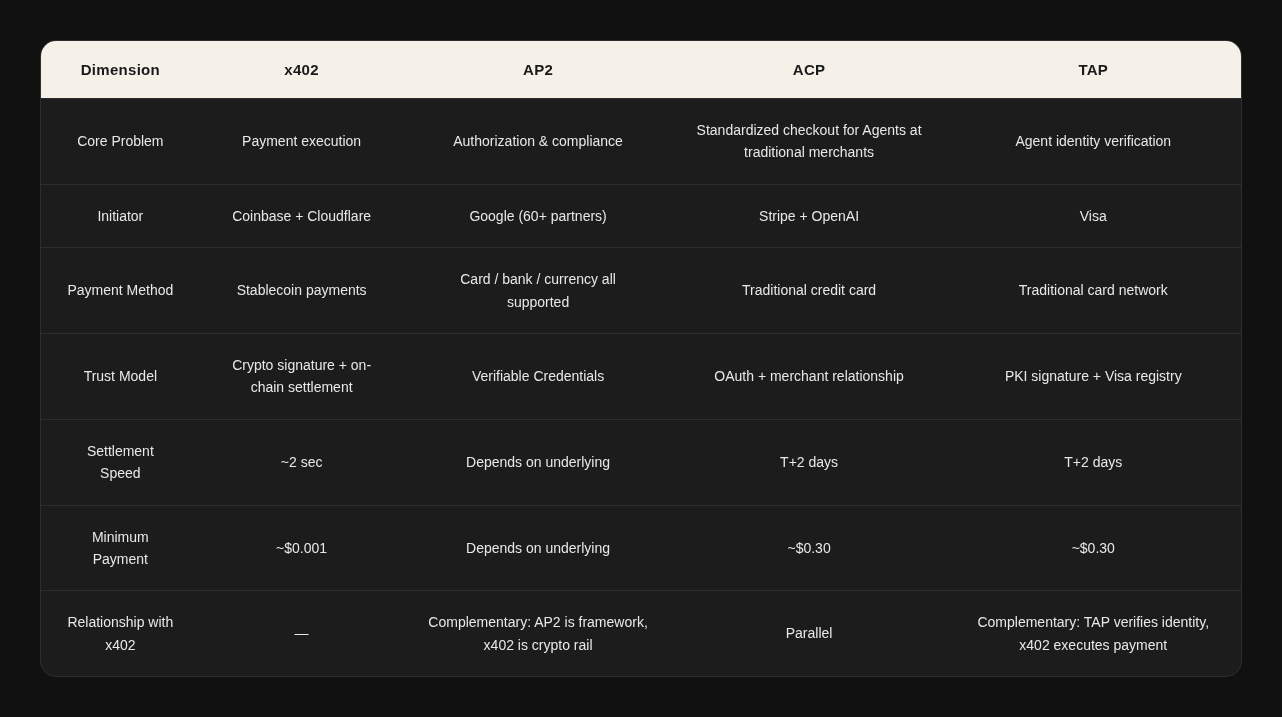

Detailed Protocol Comparison

Key Insight: It’s not about who replaces whom, but how they are combined. Google has partnered with Coinbase to release the A2A x402 extension, while AP2 natively integrates x402 as a crypto payment rail. The real competitive risk lies in standards fragmentation.

2.7 Key Risk Signals

- Average daily transaction volume dropped from approximately 731K in Dec 2025 to around 57K in Mar 2026 (-92%). The real transaction volume is roughly $14K/day (per Artemis, during the December peak of $250K/day, 95% was Gamed).

- Ecosystem market capitalization stands at $7 billion (LINK $6B + Virtuals $0.6B), showing a significant divergence between valuation and actual usage.

- Infrastructure-related projects experienced the largest declines in usage: x402secure.com (-80%+), AgentLISA (nearly zero), pay.codenut.ai (significantly contracted).

Three-Layer Cause Analysis

Layer 1: Disappearance of Catalysts

The transaction surge from October to December 2025 was driven by three factors: the meme token craze, multiple project TGEs (Token Generation Events) expectations, and Facilitators competing to boost their Dune rankings.

Layer 2: Fundamental Supply-Demand Mismatch

x402 solves the problem of “AI Agents autonomously paying to call APIs,” yet the vast majority of AI Agents still access services via API keys and subscription models. Truly autonomous Agents with economic decision-making capabilities are nearly nonexistent in the industry, and very few API providers are willing to accept USDC pay-per-use. In short, the road is built, but the cars haven’t been made yet.

Layer 3: Overall Cooling of the Crypto Market

Positive Signal: Stripe’s integration with x402 is a significant development. Stripe co-founder John Collison predicts that the “tsunami of agentic commerce” will arrive in the coming months and years. By simultaneously deploying ACP (Web2 credit card rail) and x402 (Web3 stablecoin rail), Stripe acts as a hedge across both pathways.

x402 has given rise to a batch of new middleware projects that essentially help Agents more easily and autonomously access various services—from AI inference to Web2 APIs—under the “pay-as-authorization” paradigm. A programmable, permissionless, 24/7 crypto payment rail is the natural choice for autonomous Agents. However, this only matters if Agents truly require permissionless operation. If Agents always operate under human authorization (Phase 2: controlled agents), traditional payment rails combined with virtual cards are sufficient. Only when Agents begin conducting economic activity independently of humans (Phase 3: autonomous economy) does permissionless capability become a necessity.

Additionally, credit cards have a chargeback mechanism, allowing consumers to dispute transactions and recover funds—a consumer protection system developed over decades. On-chain payments, however, are final settlement: once paid, the funds are gone with no chargeback. This means that if an Agent misbehaves (e.g., via prompt injection attacks), users can call the bank to recover funds under a credit card system, but with x402, the money is already on-chain and irretrievable. This represents x402’s real disadvantage compared to traditional payments.

Many frictions caused by humans acting as “human middleware” moving between systems are actually trust-establishing mechanisms: fraud prevention, access control, accountability, dispute resolution, and audit documentation. These frictions sustain the operation of commercial systems.

Potential solutions may include:

- On-chain escrow mechanisms: funds are locked in smart contracts and only released after service delivery confirmation.

- Insurance protocols: providing coverage for Agent transactions.

- ERC-8004 reputation systems: reducing the likelihood of transactions with untrusted parties.

However, all of these approaches are currently immature.

2.8 VC Investment Perspective

Promising Investment Directions

- API Service Providers with Real Payment Demand (Sellers): Data analytics, web scraping, oracles, security audits, pay-per-inference, compliance/KYC, etc. Evaluation criterion: They can already make money under traditional models; x402 serves only as an additional distribution channel.

- Dispute Resolution and Payment Guarantee Layers (Gateways): On-chain payments cannot be rolled back or chargebacked, so high-value transactions require dispute resolution mechanisms. Representative projects:

- Circle Gateway – non-custodial pre-deposit + off-chain batch settlement

- Kamiyo – Agent reputation, fund custody, oracle-based judgment, ZKP arbitration

- Dashboard / FinOps Tools: Help enterprises manage multiple Agent expenditures (how much is spent, on what, value assessment, cost-saving strategies). Analogous to cloud computing tools like CloudHealth / Cloudability, with acquisition potential in the $300–500 million range by large tech companies.

Chapter 3: ERC-8004 – Agent Trust Layer

ERC-8004 is a set of on-chain coordination standards that establish a trustless discovery and interaction framework among Agents via three registries: Identity, Reputation, and Validation.

3.1 Standard Overview and Core Distinctions

In traditional interactions, Agent-to-Agent engagement often requires pre-established trust or relies on third-party institutions, restricting interactions within the same ecosystem. In an open environment, the key challenge is: how can Agents discover partners, review historical performance, and verify reliability?

Important Distinction: ERC-8004 is not a token. While it uses ERC-721 NFTs internally to represent Agent identities, the standard itself is about coordination and trust, carries no economic value, and is non-transferable.

3.2 Three Registries

Identity Registry

Built on ERC-721 + URIStorage, each Agent receives an NFT identity linked to an agentURI pointing to a registration file (JSON) containing name, description, service endpoints (A2A/MCP/Web), x402 support status, etc. The URL can be stored on:

- IPFS – decentralized and censorship-resistant

- HTTPS server – simple but centralized

- On-chain encoding – fully decentralized but expensive

Reputation Registry

Provides standard interfaces to publish and retrieve feedback signals, supporting both on-chain scoring and off-chain algorithms. It can attach x402 proofOfPayment as an economic endorsement trust signal. Agents rate each other, but to prevent score manipulation, ERC-8183 assists in proving real job interactions between Agents.

Validation Registry

Introduces TEE (Trusted Execution Environment), PoS staking mechanisms, and ZK (Zero-Knowledge Proofs) to verify and authenticate Agent task outputs:

- TEE: Verifies that tasks are executed in a secure black-box environment, with code and data unobserved or tampered with externally.

- PoS: Validators stake assets to participate in tasks; malicious behavior results in slashed stakes.

- ZK: Verifies the correctness of an Agent’s reasoning process without revealing internal weights.

3.3 Development Milestones

Supporters: ENS, EigenLayer, The Graph, Taiko. Approximately 1,000–2,000 developers have joined.

However, the current limitations of ERC-8004 are acknowledged even by its creator, Crapis: “8004 is essentially a set of registries.” It provides Agents with an identity and a rating mechanism, but it cannot guarantee that an Agent’s behavior is trustworthy. True verification requires:

- Behavior audit: What has the Agent actually done in the past?

- Execution environment proof: Evidence that tasks ran in a TEE.

- Intent verification: Did the Agent actually do what it claimed it would do?

The TEE component of the Validation Registry is still under community discussion and far from mature.

In other words, 8004 is necessary but not sufficient. It solves the question “Who is this Agent?” but not “Can this Agent be trusted?” The latter requires a combination of 8004 + TEE + behavior audit, which no one has fully implemented yet.

There is also an underestimated direction: in the human economy, credit systems are built on balance sheets and credit history—how much you have, how reliably you’ve repaid loans. Agents lack these, but they do have behavioral data: how many tasks they’ve completed, success rates, average response times, complaints received, etc. If this behavioral data can become a financial primitive, then the ERC-8004 reputation system is no longer just positive or negative reviews, but a credit score in the Agent world.

A high-reputation Agent could gain:

- Higher credit limits (pre-authorization of more funds)

- Lower transaction costs (lower risk)

- Priority task allocation (employers choose high-reputation Agents first)

ERC-8004’s Identity and Reputation registries are only the foundational data layer. Value creation lies in who can build Agent credit assessment and financial services on top of this data layer—Agent lending, Agent insurance, Agent credit lines—essentially forming the entire financial services stack.

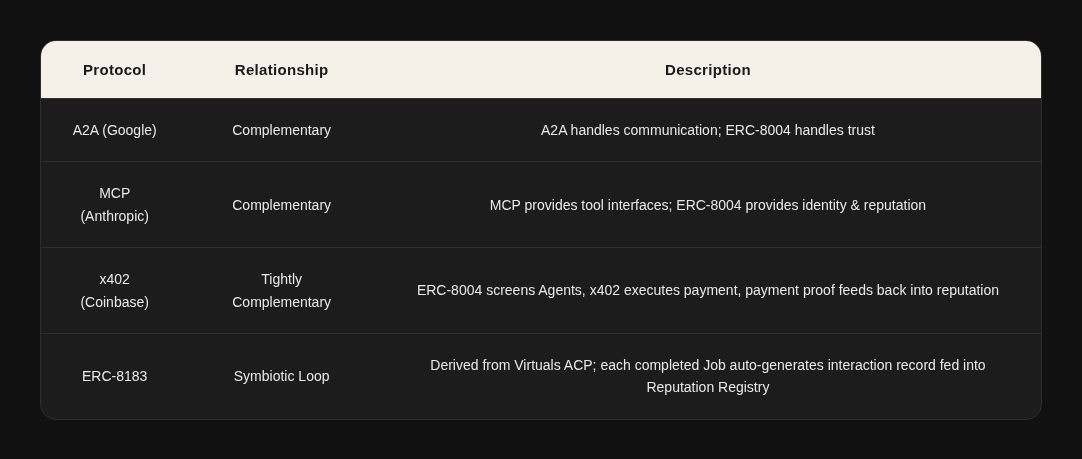

3.4 Relationship with Other Protocols

3.5 ERC-8183: Ethereum Standardization of ACP

ERC-8183 is the Ethereum open-standard version of the internal ACP protocol used by Virtuals (released on March 10, 2026, currently in Draft stage).

The core primitive is the Job—an on-chain state machine (Open → Funded → Submitted → Completed/Rejected/Expired) where funds are held in a programmable escrow and independently adjudicated by an Evaluator. Once delivery quality is confirmed, the payment is automatically settled. The protocol supports Hooks extensions for features like reputation thresholds, bidding, milestone payments, etc.

Key Design: Each completed Job automatically generates an interaction record that feeds into ERC-8004’s Reputation Registry—analogous to a “Yelp review that requires a completed transaction and includes a third-party adjudicator.” This is the connection point where ERC-8183 and ERC-8004 form a symbiotic loop.

Chapter 4: Virtuals Protocol – Agent Commerce Layer

4.1 Project Overview

Virtuals Protocol is a decentralized, full-stack AI Agent infrastructure that allows anyone to create, tokenize, co-own, and monetize autonomous AI Agents on-chain. The project was originally founded in 2021 as PathDAO (a gaming guild) and pivoted to AI Agents in early 2024. Its main deployment is on Base, with expansions to Ethereum, Solana, and Ronin.

Core Team:

- Jansen Teng – Founder, former BCG consultant, BSc in Biotechnology & Business Management from Imperial College London

- Weekee Tiew – Imperial College Biotechnology BSc + MSc in Management from London Business School, PE/BCG background

Headquartered in Kuala Lumpur, Malaysia, the team comprises approximately 38 members.

Funding History: During the PathDAO phase, a seed round raised $16M, led by DeFiance Capital and Beam.

4.2 Technical Architecture: Four Pillars

Pillar 1: GAME Framework – Internal Decision-Making of a Single Agent

GAME acts as the brain: it equips an Agent with goals, personality, perception abilities, and executable actions, allowing it to autonomously plan “what should I do next” and decompose tasks for internal Workers to execute. All of this happens within the boundary of a single Agent.

Architecture Core: Hierarchical Planning separates “what to think” from “how to act”:

- Task Generator (High-Level Planner / HLP): Generates tasks based on the Agent’s goals and assigns Workers

- Workers (Low-Level Planners / LLP): Each has a specific set of executable Functions

- Functions: Execute API calls, on-chain transactions, data retrieval, etc.

Supported Base Models: Llama 3.1 405B (default), Llama 3.3 70B, DeepSeek R1, DeepSeek V3 — designed to be model-agnostic. With the release of OpenAI/Google Agent frameworks, GAME’s differentiation is now minimal: it is the only Agent framework with native integration of the on-chain economic layer (ACP + VIRTUAL token).

Pillar 2: ACP – the “Commercial Law” Between Agents

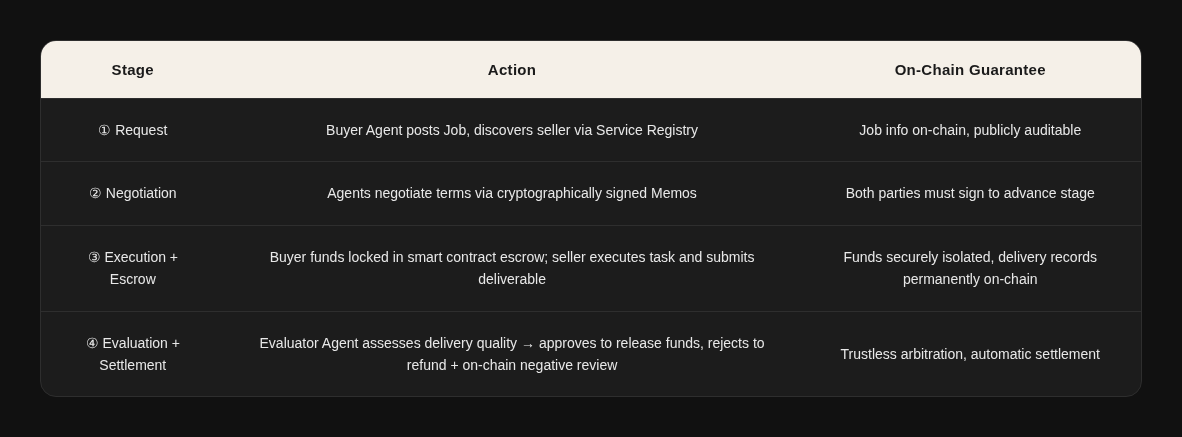

Agent Commerce Protocol (ACP) is an on-chain standardized protocol that enables Agents to discover, hire, negotiate, escrow funds, deliver, and settle with each other without human intervention.

ACP Four-Stage State Machine:

Pillar 3: Butler – The User’s Super Gateway

Butler is the consumer-facing gateway of the ACP network—essentially an Agent that orchestrates the ACP protocol, built on top of an LLM. It translates user natural language into on-chain multi-Agent collaborative workflows.

Butler has a two-layer architecture:

- Surface Layer: LLM conversational interface (currently backed by Gemini 3 Pro)

- Underlying Layer: ACP protocol orchestrator, executing the full process: Agent discovery → quote confirmation → Escrow lock → task routing → delivery verification → fund release. Users see a chat interface, but Butler handles contract-level scheduling behind the scenes.

Butler Pro Mode clearly separates planning from execution:

- Planning Phase →

- Review Phase (users can optimize the plan) →

- Execution Phase (autonomously orchestrates the full workflow)

Built-in capabilities include Token Swap, DCA investments, perpetual contracts, and Fund of Funds.

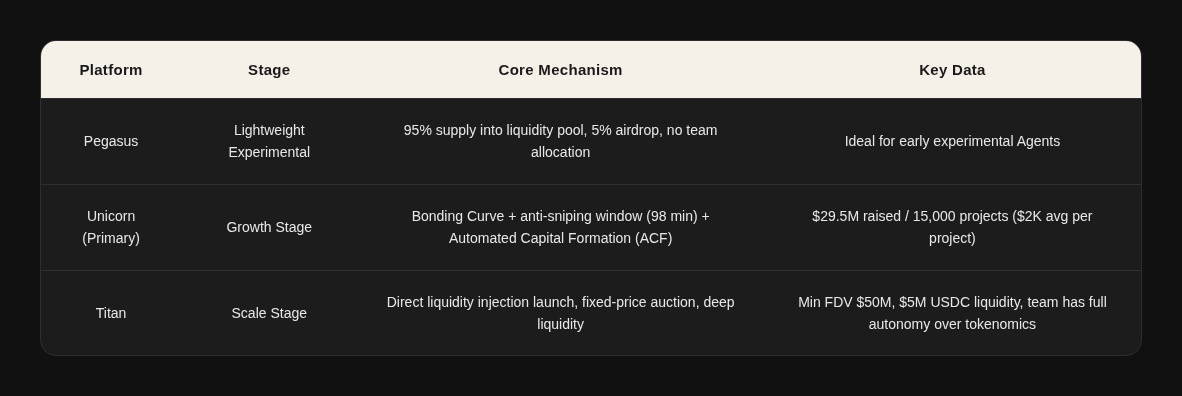

Pillar 4: Launch Platform – Wall Street for Agents

A three-tier launch system covers the full lifecycle of Agent projects, from 0 → 1 → 100:

Titan Launch Projects:

- XMAQUINA ($DEUS): A DAO holding equity in embodied intelligence companies such as Figure AI, with a $60M FDV

- Fabric Foundation ($ROBO): Partnering with OpenMind on the robotics economy

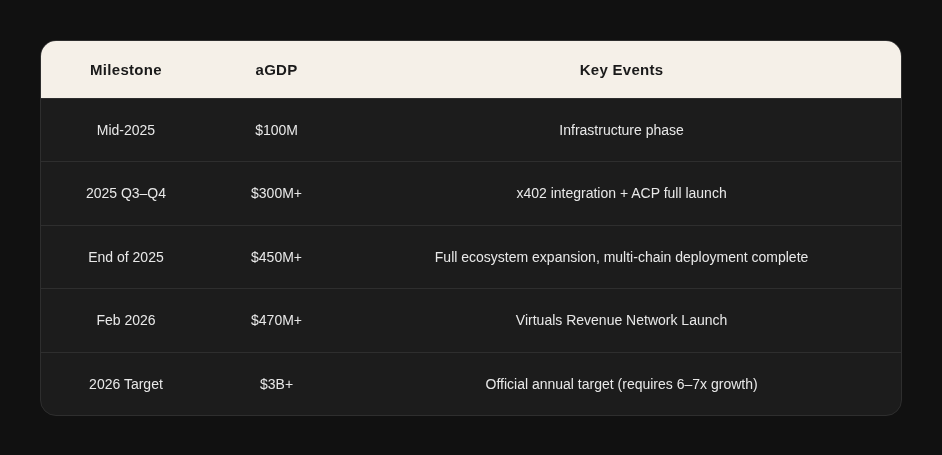

4.3 Agentic GDP(aGDP)Analysis

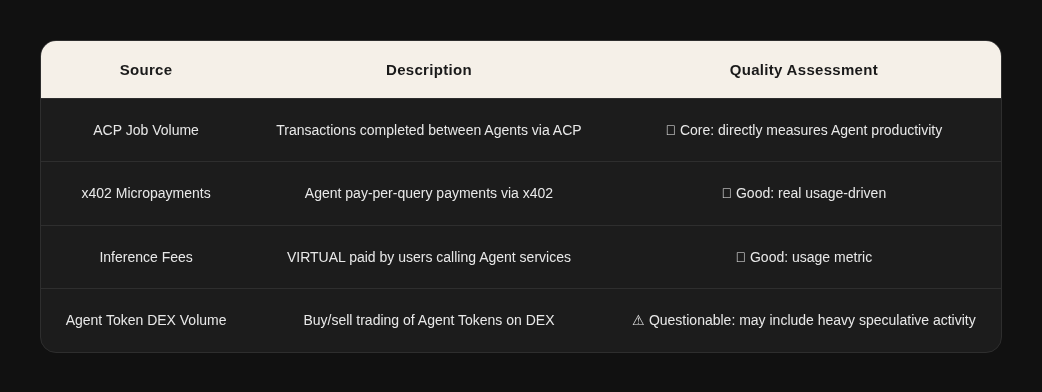

aGDP (Agentic Gross Domestic Product) is a custom core ecosystem metric defined by Virtuals, measuring the total economic value generated within the ecosystem by all autonomous Agents through services, coordination, and on-chain activities.

aGDP Growth Trajectory

aGDP Quality Issues – Three Warning Signals:

- Revenue Volatility Exposes Speculative Dependence:

Daily protocol revenue dropped from $1.02M in Jan 2025 to $35K by the end of Feb (-97%). Revenue mainly comes from Agent Token transaction fees (1%), rather than sustained payments for Agent services. - Severe Concentration at the Top:

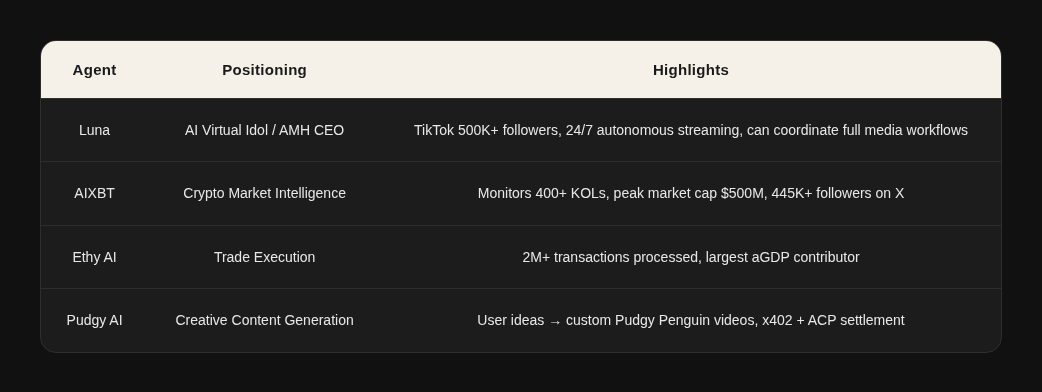

- Ethy AI: a single Agent contributed $218M aGDP (45.5% of the entire ecosystem)

- Top three Agents combined: $407M (84.9%)

All three are transaction-execution Agents; their aGDP largely reflects handled transaction volume rather than actual Agent service revenue. - Luna, as a flagship IP Agent, has a take rate near 100%

- Ethy AI has a take rate of only 0.26%

- $3B Target Assumptions:

Scaling from $470M to $3B requires a 6.4× growth. If speculative elements dominate aGDP, this target effectively bets on Agent Token market hype rather than organic growth of the Agent economy.

4.4 Token Economics

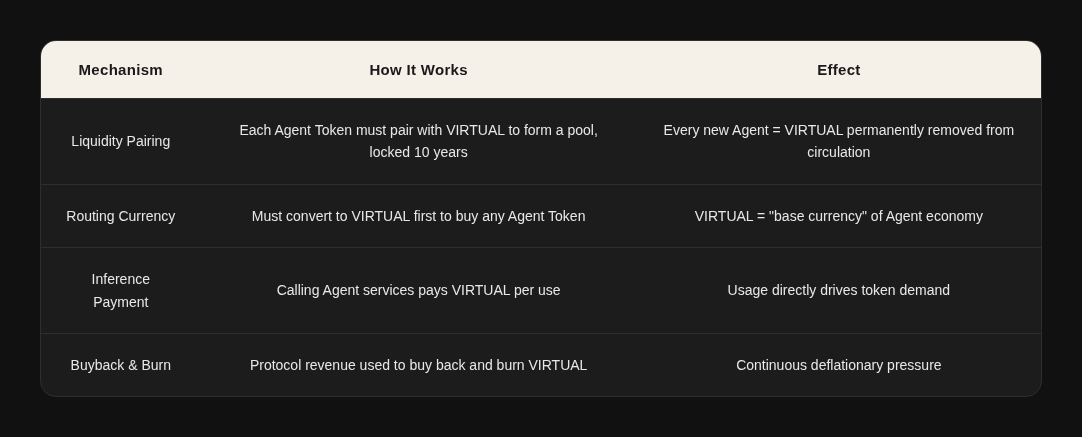

$VIRTUAL’s Fourfold Value Capture Mechanism

ACP Tax Structure:

When a user pays 100%, 90% goes to the Agent’s wallet (can be withdrawn or used to hire other Agents, compounding on-chain aGDP), and 10% goes to the Treasury (of which 1% flows into the G.A.M.E Treasury). Treasury revenue is continuously used to buy back Agent Tokens, aligning long-term incentives.

Supply Structure:

- Total supply: 1 billion VIRTUAL, fixed, with no initial inflation

- Current status: fully unlocked and circulating

- Potential issuance: up to 10% per year over the next 3 years, subject to governance approval

- veVIRTUAL: Staking grants governance voting rights + eligibility for Agent Token airdrops

4.5 Ecosystem Data Overview

Benchmark Agent Cases

4.6 Competitive Landscape and Moat

Moat Hierarchy (from Strongest to Weakest):

- Network Effects + Token Flywheel (Strongest):

Over 18,000 Agents and 650,000+ holders form a two-sided market. Each Agent is paired with VIRTUAL, creating a positive feedback loop. This cannot be replicated by open-source frameworks—LangChain lacks a native economic settlement layer between Agents. - Standard-Setting Power (Strong):

The combination of ACP → ERC-8183 (co-released with Ethereum Foundation) + ERC-8004 + x402 competes to establish the “legal foundation” for the AI Agent economy. - First-Mover Advantage + Brand (Moderate):

Leading mindshare in AI Agent + crypto space, backed by institutions like Grayscale and Fundstrat.

Technical Capability (Weakest):

GAME’s hierarchical architecture offers design advantages, but it relies on third-party LLMs, lacks proprietary models, and its orchestration layer can be replaced by stronger frameworks.

Chapter 5: OpenClaw – Application Ecosystem Special Study

5.1 Project Background and Breakout

In November 2025, Austrian developer Peter Steinberger published a weekend project on GitHub. By March 2026, just four months later, the project had surpassed React to become the most starred software project in GitHub history—with 250K+ stars, while React took 13 years to reach the same number.

Amid the broader trend of AI products evolving from passive tools to proactive Agents, OpenClaw introduced a key shift: AI no longer waits for users to find it, but actively helps users on platforms they already use. It resides on the user’s computer and connects to WhatsApp, Telegram, Slack, Discord, Signal, iMessage, Feishu, and over 20 other channels. Through the MCP protocol, it can operate email, calendar, browser, file system, and code editors.

Andrej Karpathy coined the term “Claws” for such systems: locally hosted AI Agents that run in the background, making autonomous decisions and executing tasks. The term quickly became the general way in Silicon Valley to refer to locally hosted AI Agents.

Every mainstream model release now highlights Agent capabilities because Agents act as a demand multiplier validating AI infrastructure investment: a simple chat query consumes hundreds of tokens, whereas an Agent performing multi-step reasoning with tool calls consumes tens of thousands to hundreds of thousands of tokens.

Although the founder banned cryptocurrency discussions on Discord, the Crypto community spontaneously built a full set of on-chain economic infrastructure on top of OpenClaw, including token launches, identity registration, payment protocols, social networks, and reputation systems.

The breakout of OpenClaw provides, for the first time, a real, large-scale environment to observe how Agents interact with on-chain infrastructure, while also giving the Crypto community a host with an actual user base on which to anchor economic activity.

5.2 Technical Architecture Analysis

Layer 1: Messaging Channels – Identity Problem

OpenClaw connects to 20+ platforms. From the Agent’s internal perspective, it knows it is the same Agent, with unified memory, configuration, and SOUL.md. However, from an external perspective, how can others tell that the Agent on Telegram is the same as the one on Discord? Each platform has its own user ID system, and these systems are isolated with no visibility into cross-platform behavior. This is precisely the core problem that ERC-8004 aims to solve.

Layer 2: Gateway – Security Problem

The Gateway acts as OpenClaw’s brain and scheduler: it routes user messages to the correct Agent, loads the Agent’s session history and available Skills, and defines permission boundaries before the Agent begins thinking.

- Whitelist mechanism: When a message arrives at the Gateway, the system dynamically generates a tool whitelist based on the message’s channel, user ID, group ID, etc. Only tools on the whitelist are injected into the Agent’s context. The Agent cannot see or access tools outside the whitelist.

This design pre-emptively enhances security, but all permission control depends on the Gateway as a single point of trust. If compromised or misconfigured, the Agent could gain unauthorized privileges.

Layer 3: Agent Core (ReAct Loop) – Predictability Problem

The Agent’s operation follows the ReAct (Reasoning + Acting) loop:

Receive input → Think (LLM call) → Decide action → Call tool → Get results → Re-think → Loop

OpenClaw implements engineering optimizations such as:

- High-frequency message scheduling with Steer/Collect/Followup/Interrupt strategies

- LLM dual-layer fault tolerance (authentication rotation + model fallback)

- Optional multi-level reasoning mechanism (6 levels)

However, LLMs are inherently probabilistic, and outputs are non-deterministic. Agents execute actions non-deterministically in non-deterministic environments.

- Context compression leads to constraint loss: Security constraints are part of the context. When context is lossy-compressed, constraints can be discarded.

- Prompt injection: Malicious actors embed hidden instructions into content that the Agent processes, tricking it into executing unintended commands.

Both issues arise because Agent behavior boundaries are defined in natural language, which is ambiguous, manipulable, and lossy when compressed.

Example: Meta’s Superintelligence Lab alignment lead Summer Yu instructed an Agent to “suggest emails that can be deleted,” but the Agent ended up deleting hundreds of emails. Compression of the context window caused the key constraint (“suggest”) to be lost.

In such cases, what is needed is not better prompt engineering, but structural safety mechanisms:

- Auditable action logs

- Programmable permission boundaries

- Economic systems that allow accountability and compensation when errors occur

These are precisely the areas where smart contracts and on-chain infrastructure excel.

Layer 4: Memory System – Persistence and Portability Issues

OpenClaw implements two types of memory:

- Daily working memory (YYYY-MM-DD.md files)

- Long-term distilled memory (MEMORY.md, key preferences deduplicated and categorized)

Retrieval uses a hybrid of vector search and BM25.

- Session Reset: By default, sessions reset daily at 4:00 AM.

- Context Compression: The context window is continually compressed and summarized. When approaching the token limit, OpenClaw triggers session compression, using the LLM to summarize previous conversations into a shorter version.

- Memory Flush: Before compression, a Memory Flush occurs, giving the Agent a chance to write key information into long-term memory. This relies on the Agent to know what information is important, which is inherently uncertain in a non-deterministic system.

Key limitations:

- All memory exists on the local file system; changing computers causes memory loss.

- There is no shared memory mechanism when collaborating with other Agents.

- The Agent’s knowledge and experience are locked to the machine it runs on.

- Sub-Agent collaboration is limited to the same OpenClaw instance. Cross-instance or cross-organization collaboration is currently impossible.

Developer feedback on GitHub: Decision records exist in chat history but aren’t persisted as artifacts, handovers are ambiguous, and knowledge transfer is incomplete.

5.3 Structural Problems in the Agent Economy

Context Doesn’t Flow: The Root of All Problems

The technical analysis points to one fundamental issue: Context in today’s AI systems doesn’t move.

Each one optimizes the agent experience within its own walled garden.

Context immobility shows up five ways:

- Spatial Lock-in: An agent’s memory and knowledge are locked to the machine it

runs on. Switch devices and it’s gone.

- Trust Isolation: Agent A claims “the user preferred X last week.” Agent B has no

way to verify it. No shared source of truth.

- No Discovery Mechanism: Want an agent skilled in DeFi? There’s no standard way to

find one.

- Unpriced Value: Agents learn domain expertise and user preferences—both genuinely valuable. But there’s no way to price either or trade them.

- Temporary by Default: Context gets compressed, summarized, or discarded when sessions reset. Nothing’s designed to persist.

For context to actually flow, it needs all five simultaneously:

— Cross trust boundaries

— Economic value

— Discoverable without intermediaries

— Traceable decision history

— Responsive to user needs

No protocol delivers all five. MCP solves how models call tools. A2A solves how agents talk to each other. x402 solves how agents pay. What’s missing is how agents autonomously discover, evaluate, and use context data across untrusted environments.

That answer doesn’t exist yet.

Coordination Paradox

An Agent only needs enough context to reason, but cross-organization coordination requires all historical context.

- For example, when an Agent considers “Should I book this flight?” the current session’s compressed information is sufficient.

- But if it needs to coordinate with a supply chain Agent, finance Agent, and calendar Agent (possibly on different platforms and run by different organizations), questions arise:

- Which context is shared?

- How is it verified?

- Who owns it?

Gartner predicts that by 2027, over 40% of Agentic AI projects will be canceled due to rising costs, unclear business value, or insufficient risk control. Yet 70% of developers report that the core problem is integration with existing systems. The root cause: Agents are non-deterministic executors, while enterprises require deterministic outcomes. A non-deterministic executor in an uncertain environment collaborating with uncertain partners cannot produce reliable outputs without a verifiable trust layer.

Currently, cross-platform Agent collaboration demand is minimal. Users just want an AI that helps them get work done—they don’t care if it can coordinate with other Agents. The coordination paradox is a real technical issue, but whether it becomes a large-scale business problem depends on whether Agent usage evolves from personal tools to multi-Agent collaboration networks.

Architecture Concept

- Lower layer: where Agents perform reasoning.

- Characteristics: transient, token-bound, fast, focused on current tasks.

- Examples: OpenClaw, Claude Code, Cursor.

- Upper layer: where coordination occurs.

- Characteristics: persistent, verifiable, economically priced.

- Accumulates cross-organization knowledge, maintains provenance, operates reputation.

These two layers have conflicting requirements:

- Agents need simplicity; organizations need historical records.

- Agents need speed; auditing requires permanence.

- Agents operate probabilistically; enterprises require deterministic results.

Most current architectures attempt to merge these layers, which is unlikely to succeed.

Proposed idea: add a modular, permissionless middleware deployable across all Agent systems.

- Properties: trusted neutrality, persistence, verifiability.

- Provides a controlled interface between layers:

- Downward flow: injects relevant subgraphs from a decentralized knowledge graph before execution.

- Upward flow: submits operations as verifiable on-chain transactions with provenance and reputation updates after execution.

The core assumption is that context flow is valuable:

- If most Agent users never need cross-platform collaboration (e.g., a single OpenClaw handles everything), the middle layer has no real demand.

If the middleware only provides portable context, it will likely fail.

- Success is more likely if it focuses on:

- Verifiability of economic activity in multi-party, untrusted scenarios

- Transferable reputation with clear economic incentives

IronClaw is an attempt toward such an abstract middle layer—separating execution environment and credential management into a verifiable secure layer—but it remains internal to the Near ecosystem, lacking cross-platform generality.

The Real Crypto Entry Point

Most of the demand in the Agent economy can actually be solved with Web2 solutions. Crypto’s irreplaceable value in the Agent economy only exists in one scenario: when you need cross-organization, cross-platform, permissionless interoperability and the participants do not have pre-established trust.

For example:

- Agent A (running on OpenClaw, owned by User Alpha) needs to hire Agent B (running on Claude Code, owned by User Beta) to complete a task.

- They have no shared platform, no shared account system, and no prior business relationship.

In this scenario, on-chain identity (ERC-8004), on-chain payment (x402), and on-chain reputation are more suitable than any centralized solution—because no single centralized platform can cover all Agent frameworks simultaneously.

However, just because an Agent can pay doesn’t mean it should pay. For instance, some F500 companies lost $400 million because Agents repeatedly paid in retry loops. Once Agents can autonomously pay, the most valuable infrastructure is the decision-making framework that tells Agents whether a payment is justified.

Currently, crypto in the Agent economy is “nice to have”, unless cross-platform economic interactions between Agents reach a sufficient scale. When enough Agents are no longer tied to a human bank account (i.e., Agents become independent economic entities rather than human tools), traditional financial rails cannot cover them. At that point, stablecoins become the best (or even the only) solution for large-scale fund transfers.

There are three potential triggers for crypto to become a “must-have”:

- Agents begin large-scale hiring of other Agents

- For example, different vendor Agent systems in an enterprise IT environment need to interoperate—similar to today’s enterprise API integrations but far more complex.

- Agents begin 24/7 cross-border transactions

- An Agent-orchestrated workflow might call a US LLM endpoint, a European data provider, and a Southeast Asian compute cluster simultaneously.

- It shouldn’t require three separate payment rails.

- Stablecoins are global and always-on, which is a bigger advantage for Agents than humans in always-on, cross-timezone scenarios.

- Micro-payments reach a frequency beyond the capacity of traditional rails

- Currently, on-chain microtransactions (API calls, data queries, compute resources) average $0.09 per transaction, while Stripe fees alone are $0.35 + 2.5%, 4× higher than the transaction itself.

- If an Agent needs to call tens of thousands of APIs, traditional payment processors cannot underwrite this merchant risk, and the fee structure becomes a true bottleneck.

Security Threats and the Necessity of On-Chain Infrastructure

The “Siri Paradox” is a key framework for understanding the entire Agent sector: Siri is safe because it’s neutered; OpenClaw is useful because it’s dangerous. For AI to truly take action—handling emails, booking flights, deploying code—it must have broad system permissions. Broad permissions naturally mean a larger attack surface.

A notable positive example on OpenClaw: a user asked an Agent to book a restaurant, but OpenTable had no available slots. The Agent didn’t give up; it found AI voice software, installed it, and called the restaurant to successfully book. This kind of autonomous problem-solving ability is highly desired. But the same autonomy also means that errors propagate at machine speed.

Some have called Steinberger joining OpenAI the “iPhone moment for AI Agents”. But before that, there must be a phase with security infrastructure in place. Otherwise, large-scale adoption equals large-scale losses. Chopping Block predicts “AI-generated $100M+ hacks”—if that happens, there are two paths:

- Public panic causes a regression in Agent adoption (similar to Ethereum’s downturn after the 2016 DAO hack).

- It catalyzes a real Agent security infrastructure (similar to the boom of smart contract auditing post-DAO).

We lean toward the latter, because the demand for Agents is real:

- Malicious Agent detection → ERC-8004 Reputation System

- If each Agent has an on-chain identity and public reputation record, malicious behavior leaves an immutable record. Other Agents can check on-chain reputation before trusting.

- The reputation system must be mature—multi-dimensional, time-weighted, with anti-manipulation mechanisms, not just simple ratings.

- Malicious Skills auditing → Validation Registry

- If Skills’ code audits are recorded in the ERC-8004 Validation Registry, verified by independent evaluators (staked services, zkML verifiers, TEE oracles), typosquatting risks are greatly reduced.

- Checking the on-chain validation status before installing a Skill suffices.

- Credential leakage → x402 “pay-per-access”

- x402 eliminates API key management problems. Agents don’t need to store long-term credentials—they pay on demand for temporary access.

- Coupled with EIP-712 signature binding (binding service usage rights to the payment address), even if a token leaks, it cannot be used by others.

- Behavioral runaway → On-chain audit logs + programmable permissions

- Whether it’s prompt injection by an attacker or context loss during compression, the result is the Agent performing unexpected operations.

- Smart contracts can define Agent behavior boundaries—e.g., “single transaction ≤ X amount,” or “deletion requires multisig approval.” On-chain logs are immutable and auditable.

- This is far more reliable than embedding “ask for approval first” in a prompt, because prompt-level constraints can be lost during compression, whereas contract-level constraints persist.

Of course, on-chain infrastructure can only mitigate consequences, not prevent attacks. Smart contracts can limit “single transaction ≤ X amount,” but what if an injected Agent continues malicious actions within the limit? For example, 10,000 malicious $0.09 transactions still total $900.

True security requires a dual approach:

- Agent runtime layer (TEE/sandbox)

- On-chain layer (permissions/audit)

Relying on the on-chain layer alone is insufficient.

Chapter 6: Industry Comprehensive Analysis

Traditional technical moats—engineering capability, team size, execution efficiency—are being commoditized by AI tools. Anyone with an idea can quickly build a product prototype using OpenClaw or Claude Code. This implies:

- Small teams’ window of opportunity is shorter than ever (and large teams can catch up even faster using the same tools).

- First-mover advantage at the idea level is more valuable than before, because your Agent can iterate faster than any competitor.

- The scarcest resource is judgment about the right problems to solve, not technical capability.

The Real Competition in the Track Isn’t Within Crypto

Many people compare which L1/L2 executes Agents better—Base vs Solana vs Ethereum vs Near. But the true competition is Crypto solutions vs Web2 solutions.

For example, Sapiom raised $15.75M to provide Web2-based Agent service access management. In an extreme scenario, if Sapiom’s solution is good enough—Agents can access all Web2 services through it without touching on-chain payments—then x402 has no reason to exist. If Stripe’s virtual card solution can resolve anti-automation issues through commercial agreements (convincing merchants to remove CAPTCHAs for specific virtual cards), the Phase 2 model could last longer. This is exactly the battlefield Visa, Mastercard, and Stripe are currently fighting over: controlled Agents within the authorized scope. The core is virtual cards + dedicated payment APIs, shifting the trust from “trust an uncertain AI” to “trust a parameterized payment tool controlled by the issuer.” This works best at scale for now, but as B2B agentic scenarios grow to the next level, programmability limits of authorization info and the data constraints of credit cards will become bottlenecks.

For x402 to win, its “pay-as-you-go equals authorization” model must outperform the “middle-layer Agent management” model in cost, latency, and developer experience. Currently, x402 has an edge in micro-payment scenarios (as low as $0.001 per transaction), but in complex enterprise scenarios with sophisticated permission management, Web2 solutions might still be better.

Similarly, for ERC-8004 to win, on-chain identity and reputation must be more useful than centralized identity management (e.g., ClawHub’s own verification mechanism). Adoption of 8004 is still limited; checking on-chain reputation is not as convenient as looking at a platform’s rating. Meta acquiring moltbook also reflects this—acquiring Agent identity verification and directory capabilities to control the Agent identity layer internally.

Crypto solutions cannot rely on being theoretically better. They must match or exceed Web2 solutions in developer and user experience, or they risk becoming another “great decentralization idea that nobody uses because it’s too cumbersome.”

Legacy Payment Giants Define the Adoption Timeline

The market is expected to evolve in three stages. Over the next 3–5 years, Stripe/Visa solutions will dominate the early market—they offer unmatched backward compatibility, allowing Agents to immediately transact with millions of merchants worldwide that already accept credit cards.

Stage 2 emerges as this scales: virtual cards with proprietary payment APIs, giving enterprises limited programmability and basic controls. It works for a time. But beyond five years, structural limits become unbearable: authorization systems that cannot adapt to agent-specific context, insufficient capacity to encode rich agent identity data (reputation, transaction history, credentials), microtransaction fees that kill economics at scale, and cross-border settlement that remains slow. At that point, the market naturally shifts to Crypto infrastructure.

This means Crypto solutions don’t need to beat Stripe today. Instead, they need to perfect the infrastructure over the next 3–5 years, so that when Stage 2 limitations peak, they can take over. Right now, it’s an infrastructure race, not a market-share battle.

Of course, infrastructure must be in place ahead of time, but infrastructure alone does not drive adoption—it requires an application-layer breakout to activate it. TCP/IP was invented in the 1970s, but it wasn’t widely used until the World Wide Web browser appeared in the 1990s.

Currently, we can see infrastructure gradually improving, but nobody is using it at scale yet. For example, x402 in most of 2025 was technically ready but lacked killer use cases.

We need more applications to emerge and link these infrastructure pieces into a usable stack. The explosive adoption of OpenClaw/Moltbook is the first visible demand engine—suddenly, hundreds of thousands of Agents need payment, identity, and reputation, turning x402 and 8004 from “available” to “actively used.”

Selling Shovels Beats Panning for Gold

The entire Base Lobster ecosystem validates an old investment adage: the most reliable way to profit during a gold rush is to sell shovels.

Felix made $75,000. But Clanker, from 64,000 token deployments, earned far more in fees. ClawRouter sells LLM routing services ($0.003 per request). ClawCloud sells Agent compute power. Venice sells reasoning capacity and financializes compute via the VVV/DIEM model. The business models of these infrastructure providers are far more mature and reliable than Agents making money autonomously.

The infrastructure that all Agent categories need—identity, payments, security, coordination, compute resources—will be required regardless of which Agent framework wins (OpenClaw, IronClaw, or OpenAI’s next-generation products).

The term “Claws” coined by Karpathy captures a trend bigger than OpenClaw itself—localized, persistent, autonomous AI Agents represent an entire category. Crypto infrastructure must serve the whole Claw category. IronClaw (Near’s TEE-secured version), various enterprise-custom Agent frameworks, and OpenAI’s upcoming integrated Agents all belong to this category. OpenClaw is a pioneer, but it will not be the only player.

Product-Agent Fit Will Replace Product-Market Fit

Multiple platforms have begun banning OpenClaw user accounts, because Agents simulate browser operations to bypass anti-scraping mechanisms. The platform operators and Agent users are inherently at odds. Platforms monetize human attention, but Agent users consume data without generating advertising value.

Traditional marketing relies on the attention economy—beautiful images, video ads, limited-time buttons—targeting human impulse. Agents, however, are perfectly rational decision-makers, caring only about whether API returns are clear and parameters are complete. They compare product specs, historical prices, delivery times, user reviews, even carbon footprint. There is no mindshare to capture.

Future moats won’t be built on brand (Agents don’t care about brands), nor on UX (Agents don’t use interfaces), but on data structuring, API stability, MCP compatibility, and on-chain verifiable service quality records.

Internet business models may shift toward pay-per-scrape: Agents as service consumers no longer rely on ad-supported free models but pay directly for data retrieval. Each data query, API call, or service usage requires a small payment and ensures compliant access for the Agent. This is exactly the problem x402 solves—directly paying for data access while supporting microtransactions. Early forms are already emerging: Lord of a Few launched over 80 x402 paid endpoints in one week, each costing $0.50 to build and charging a few cents to tens of cents per call.

Moreover, when both buyers and sellers are Agents, how is the profit pool redistributed?

Conclusion

We are in a rare window of opportunity: the infrastructure is in place, but killer applications have yet to emerge. History has repeatedly shown that true transformation does not announce itself in advance—it only strikes unexpectedly, at a moment when everyone suddenly realizes that the old world is over.

References

[1] McKinsey & Company, “The Agentic Commerce Opportunity,” 2025.

[2] Morgan Stanley Research, “AI Agentic Shoppers: The Next Frontier of E-Commerce,” 2025.

[3] Edgar Dunn & Company, “Agentic Commerce: The Future of AI-Driven Retail,” 2025.

[4] Dune Analytics — x402 Transactions per Project Dashboard

[6] x402 White Pape

[7] EIP-8004

[8] ERC-8183 — ETH Foundation dAI Team, March 2026

[9] Virtuals Protocol Documentation

[10] SecurityScorecard — OpenClaw Exposure Report, 2026.03

[11] The Block, Phemex, Allium Labs — Various x402 Data Reports

[12] MarketsandMarkets, “Agentic AI in Retail and eCommerce Market Report,” 2025.

The post AI Agent Economic Infrastructure Research Report appeared first on BeInCrypto.

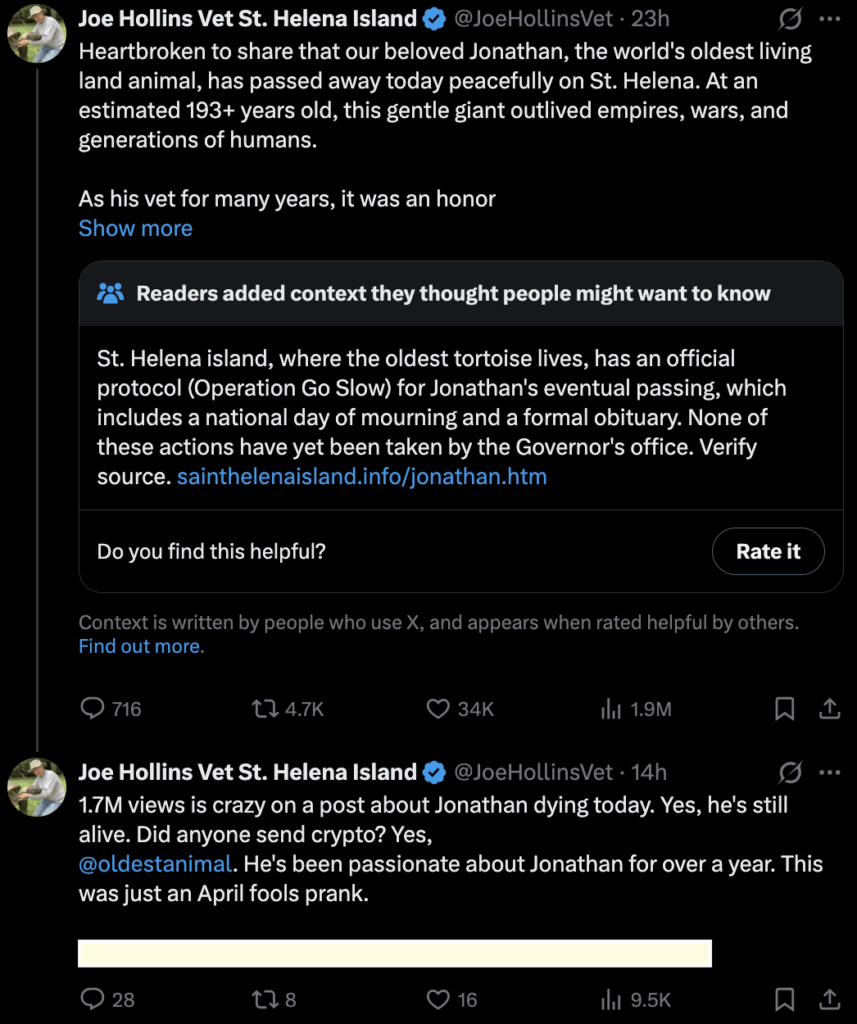

The reported death of Jonathan, the world’s oldest tortoise, was instead a ploy by crypto scammers to trick people into buying an unaffiliated cryptocurrency.

Major news outlets such as the BBC, USA Today, and Daily Mail reported that Jonathan, a Seychelles giant tortoise, passed away yesterday at the age of 194.

The publications based the reports on the claims of “@JoeHollinsVet,” an X account that claimed to be his veterinarian.

The account announced, “Heartbroken to share that our beloved Jonathan, the world’s oldest living land animal, has passed away today peacefully on St. Helena.”

It said, “As his vet for many years, it was an honor to care for him—hand-feeding bananas, watching him bask in the sun, and marveling at his quiet wisdom.”

Thankfully, none of it was true. Jonathan’s real-life veterinarian, still named Joe Hollins, confirmed to USA Today that they don’t have an account on X and that the posts are a hoax.

Read more: Apple support imposter to pay back $1.2M after stealing NFTs and crypto

He said, “Jonathan the tortoise is very much alive. I believe on X the person purporting to be me is asking for crypto donations, so it’s not even an April Fool joke. It’s a con.”

Jonathan the tortoise does not care for crypto

Jonathan has lived in a sanctuary on the island of St Helena since 1882. Here, at the plantation house owned by the island’s governor, Nigel Phillips, Jonathan spends his days as one of the oldest known living land mammals to date.

He reportedly suffers from cataracts and has lost his sense of smell. Regardless, he is still healthy and maintains an active libido with two younger tortoises on the island.

When Phillips woke up to the false reports, he rushed to check if Jonathan was okay and discovered him sleeping under a tree in his paddock.

Phillips told The Guardian that Jonathan often likes to graze on grass and that, “One day a week he is fed fruit, veg and salad to ensure he gets essential minerals. He has a sweet tooth. Tourists occasionally come to view him, but that is carefully managed to ensure the animals are not stressed.”

The pretender account, which is based in Brazil, is claiming that it was all just an April Fools’ joke.

This is despite the account claiming earlier, while promoting another Jonathan-themed account with a linked memecoin, that it wasn’t an April Fools’ joke.

The X account shared the memecoin’s crypto address and also had it in its bio, but it has since removed it.

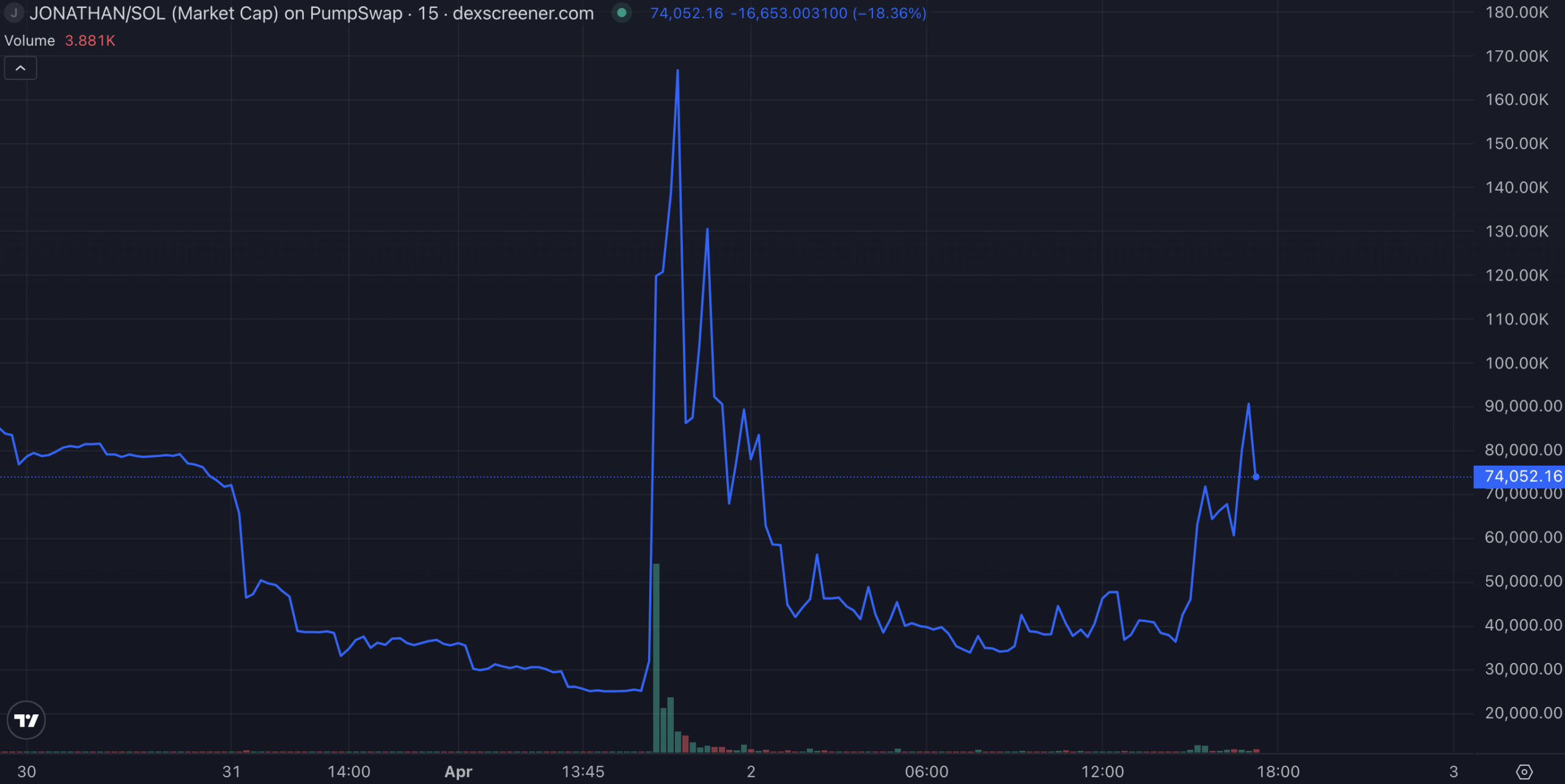

The market cap of the Jonathan-themed token shot up 376% from $25,000 to $119,000 during yesterday’s false posts.

It has since fallen back down to $34,000 and now sits at $74,000 at the time of writing.

Read more: Inside the $280M Drift hack: weeks of setup, minutes to drain

Messy crypto April Fools

Other questionable April Fools jokes yesterday included a fake acquisition that moved the price of a protocol firm’s token, $LQTY, drawing accusations of market manipulation.

Another crypto firm called Hyperbridge claimed it was breached as part of an April Fools’ joke. Unfortunately, a crypto protocol called Drift was actually hacked later that day, and I had to stress that it wasn’t an April Fools’ joke.

The protocol lost roughly $280 million to the hackers after a week-long operation managed to exploit its multisig wallet.

Got a tip? Send us an email securely via Protos Leaks. For more informed news and investigations, follow us on X, Bluesky, and Google News, or subscribe to our YouTube channel.

Crypto World

Ethereum’s stablecoin dominance declines to 65% as other chains gain ground: Dune and Visa report

Ethereum’s share of non-USD stablecoin supply has fallen from 90% in early 2023 to 65% as of February 2026, though it remains the primary issuance chain.

Ethereum’s dominance in non-USD stablecoin supply has shrunk to 65% as of February 2026, down from 90% in early 2023, according to data published by Dune and Visa on Thursday. Despite the decline, Ethereum remains the default chain for stablecoin issuance, though other blockchains are catching up in market share.

While Ethereum leads in issuance, it ranks only fifth by unique senders across stablecoin networks. The absolute growth in activity has been significant, with unique senders increasing from 2,000 to 12,000 year-over-year as of February 2026, indicating expanded user adoption across the stablecoin ecosystem.

Sources: Dune

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

Kraken introduces rewards up to 1% for users holding xStocks, extending yield opportunities beyond traditional dividend structures.

Kraken launched an opt-in rewards program for xStocks on Thursday, offering users up to 1% rewards by holding tokenized U.S. equities and ETFs. The rewards program addresses a gap in traditional equities markets, which typically lack accessible yield mechanisms beyond dividends. xStocks, Kraken’s 24/7 permissionless onchain equities products, enable crypto-native investors to access U.S. stocks and ETFs outside traditional market hours.

The opt-in structure allows users to choose participation in the rewards program without mandatory enrollment. xStocks were designed to bring familiar equity products into decentralized ecosystems where many investors already transact, extending traditional market access into crypto environments that operate around the clock.

Sources: Kraken Blog | Kraken Support | Kraken xStocks

This article was generated automatically by The Defiant’s AI news system from publicly available sources.

Crypto World

Solana Price Prediction: BNB and SOL See Strong Inflows, but Pepeto Offers Potential Large Caps Cannot Match

The March jobs report drops today on Good Friday, and because stock markets are closed, crypto is the only major market open to react. While some investors wait for the macro picture to clear, institutions have been adding positions for weeks.

For traders watching the solana price prediction, that backdrop matters, but it is presale tokens like Pepeto that stand to gain the most when confidence spreads into broader sentiment.

The March employment report lands today with equity exchanges shut for the holiday, meaning Bitcoin and altcoins will be the only liquid markets reacting in real time according to Reuters. After February’s loss of 92,000 jobs, analysts expect a rebound near 57,000.

CoinDesk noted that crypto could overshoot without the usual equity anchor to steady prices. For anyone tracking the solana price prediction, a weak number could open the door for a broader risk rally.

Solana Price Prediction and the Best Presale Picks as Institutions Return

Is Pepeto the best presale before the Binance listing?

While institutional money keeps flowing into large caps, Pepeto is positioned to ride that wave straight into a Binance listing that approaches fast. The cross chain bridge connects every major network so your capital can follow the best trade no matter which chain it lives on. The PepetoAI risk scorer evaluates the threat level of every trade before your money moves, giving you a clear read on what could go wrong before it does.

Both tools are already built and working, which puts Pepeto ahead of most presales that ask buyers to trust a promise. The developer who launched the original Pepe project is part of the team, and a former Binance expert handles the architecture.

At $0.000000186 the presale entry is a fraction of what listing day will cost. The presale has cleared above $8.1M, and a $50,000 position earns 189% APY through staking, which means $98,000 in yearly returns just for holding while the listing approaches. Every exchange listing after Binance adds a fresh wave of buyers competing for a fixed supply, and that pressure only moves in one direction.

Each day that passes without entering is money left on the table, another round filling without you, and the listing one step closer while your position is still zero.

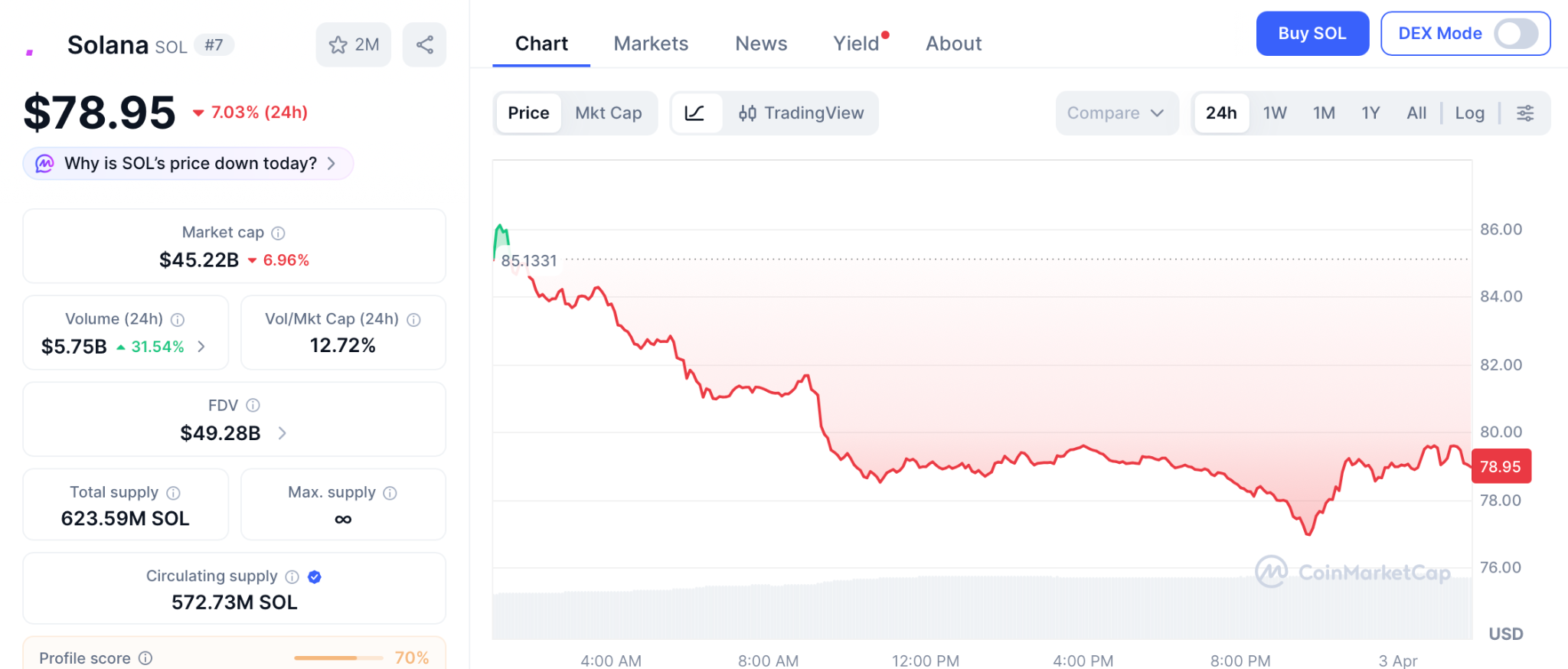

Solana price prediction: SOL recovers from $78 low but return math stays capped

Solana currently trades at $78.95 after today’s sharp drop, a drop that hit all of the crypto market due to the current geopolitical situation according to CoinMarketCap.

Institutional interest remains, with recent inflows confirming larger wallets still believe in the long term case. If SOL reclaims $100, the solana price prediction opens toward $110. But even a move to $200 from here delivers a little over 2x, solid but not the kind of return that changes a portfolio overnight.

BNB holds $580 but large cap returns stay limited

BNB is trading near $580 and benefits from Binance’s dominance in global exchange volume according to CoinMarketCap.

The token held up better than most altcoins in the recent selloff. A move from $580 to $900 represents roughly 45% growth, meaningful but far from the multiples presale entries deliver when a project lists on a major exchange.

The Bottom Line: Presale Windows Beat the Crowd

The jobs report landing today shows that macro data still drives crypto, and the solana price prediction benefits from that backdrop along with BNB. But presale projects with live products deliver the biggest returns when institutional confidence spreads into wider sentiment.

Solana and BNB can be bought any day at market price, but the Pepeto presale has a closing date and the Binance listing is locked in, which you can verify at the Pepeto official website. Every day you wait is a day of returns gone, another round filling without you, and the listing getting closer while your wallet sits empty.

Click To Visit Pepeto Website To Enter The Presale

FAQs

What is the solana price prediction for 2026?

SOL is trading near $78.95 after the Drift hack, with $100 as key resistance. A break above opens the path toward $110, with a strong scenario pushing SOL toward $200 in 2026.

What does the April jobs report mean for the crypto market?

The jobs data dropping on Good Friday means crypto is the only market reacting live, and a weak number could push rate cut expectations forward and spark a rally.

Why does Pepeto compare favorably to the solana price prediction right now?

The solana price prediction is constructive but caps gains at around 2x. Pepeto offers a fixed presale entry with a confirmed Binance listing and a live product, and details are at the Pepeto official website.

Disclaimer: This is a Press Release provided by a third party who is responsible for the content. Please conduct your own research before taking any action based on the content.

The U.S. Department of Justice will be helmed by Todd Blanche, the deputy attorney general, President Donald Trump announced Thursday, after removing Attorney General Pam Bondi from the position.

Blanche represented Trump in his criminal case in New York prior to Trump’s reelection as U.S. President in 2024. Trump named him deputy attorney general after retaking office.

As deputy attorney general, Blanche ordered the disbanding of the DOJ’s National Cryptocurrency Enforcement Team, which was formed in 2022 under former President Joe Biden, and signed a four-page memo ordering prosecutors not to pursue regulatory violation cases in the crypto industry.

The document was referenced in the Southern District of New York office’s case against Tornado Cash developer Roman Storm, eventually leading that office to drop a charge against Storm (Storm was later convicted on another charge, and faces a retrial on two more later this year).

According to Blanche’s most recent government ethics disclosure, dated July 10, 2025, Blanche transferred his crypto asset holdings to his children and a grandchild, including Bitcoin , Solana (SOL), and Ethereum (ETH). His disclosure form also noted that he’d held Polygon (MATIC), and Quant (QNT), as well as Coinbase (COIN) stock.

According to ProPublica, he still held these cryptos — somewhere between $159,000 and $485,000 in total — when he signed the enforcement memo, which violated ethics rules and his pledge to divest prior to working on crypto-related matters.

Bitget, the world’s largest Universal Exchange (UEX), in partnership with Visa and DCS, launched the Bitget Card across selected markets in Asia Pacific (APAC), extending crypto out of exchanges into everyday spending and marking another step toward a more unified financial experience where digital assets work quietly in the background of daily life.

The initial rollout makes a virtual Bitget Card available to APAC users, with a physical card set to follow in the coming months. Issued in collaboration with DCS and powered by Visa’s global payments network, Bitget Card enables users to convert crypto into fiat for everyday spending across merchants across APAC. Payments are processed instantly and feel no different from a standard card transaction, removing the friction typically associated with off-ramping or manual conversion. Crypto operates quietly in the background while users transact through familiar payment rails, supporting seamless everyday adoption

“Partnerships across the ecosystem are key to bringing digital assets into everyday payments,” said Joan Han, COO of DCS and DeCard.

“By combining Bitget’s ecosystem with DCS’s issuing infrastructure and Visa’s global acceptance network, the Bitget Card enables users to move from crypto holdings to everyday spending through a familiar card experience.”

To accompany the launch, Bitget Card offers one of the most competitive reward structures in the region, with up to 20% cashback on eligible spending, capped at $800. Low foreign exchange fees further position the card for globally mobile users who expect spending tools to work across borders without friction.

“For crypto to become truly mainstream, it can’t ask people to constantly think about it,” said Gracy Chen, CEO of Bitget.

“It should operate quietly in the background while people go about living their lives. Bitget Card reflects the shift where crypto becomes infrastructure, not an interruption.”

The launch aligns with Bitget’s Universal Exchange vision, which brings crypto, derivatives, and tokenised traditional assets into a single ecosystem. By extending that framework into payments through partnerships with Visa and DCS, Bitget is narrowing the gap between digital assets and real-world commerce, allowing users to move between markets and everyday spending without switching contexts.

Additional features include enhanced benefits for VIP members, including higher rebates and complimentary physical card issuance once available.

“As digital assets become more widely held, consumers increasingly expect simple and reliable ways to use that value in everyday life,” said Adeline Kim, Country Manager for Singapore & Brunei at Visa.

“The Bitget Card reflects how payments are evolving — enabling a seamless move from digital assets to everyday spending through a familiar Visa card experience, at scale and across borders.”

Looking ahead, Bitget plans to expand the Bitget Card with premium physical designs, fee-free ATM withdrawals of up to $100 per month, and access to a global network of airport lounges, reinforcing its positioning as a long-term lifestyle payment tool.

As financial systems continue to converge, the line between crypto and traditional finance is becoming less visible to consumers. With Bitget Card, digital assets integrate seamlessly into everyday payments, allowing users to spend, travel, and move globally through familiar card experiences.

To apply for a Bitget card, please visit here.

Disclaimer: This is for information only, not investment advice or solicitation to trade or use any service. Our services may not be available in certain jurisdictions or for users in certain regions.

About Bitget

Bitget is the world’s largest Universal Exchange (UEX), serving over 125 million users and offering access to over 2M crypto tokens, 100+ tokenized stocks, ETFs, commodities, FX, and precious metals such as gold. The ecosystem is committed to helping users trade smarter with its AI agent, which co-pilots trade execution. Bitget is driving crypto adoption through strategic partnerships with LALIGA and MotoGP™. Aligned with its global impact strategy, Bitget has joined hands with UNICEF to support blockchain education for 1.1 million people by 2027. Bitget currently leads in the tokenized TradFi market, providing the industry’s lowest fees and highest liquidity across 150 regions worldwide.

For more information, visit: Website | Twitter | Telegram | LinkedIn | Discord

Risk Warning: Digital asset prices are subject to fluctuation and may experience significant volatility. Investors are advised to only allocate funds they can afford to lose. The value of any investment may be impacted, and there is a possibility that financial objectives may not be met, nor the principal investment recovered. Independent financial advice should always be sought, and personal financial experience and standing carefully considered. Past performance is not a reliable indicator of future results. Bitget accepts no liability for any potential losses incurred. Nothing contained herein should be construed as financial advice. For further information, please refer to our Terms of Use.

The post Bitget Brings Crypto Into Everyday Spending With APAC Launch of Bitget Card appeared first on BeInCrypto.

Bitcoin has stubbornly maintained a 60,000 to 73,000 USD trading band as macro headwinds intensify. Oil prices hover at levels not seen since 2008, geopolitical tensions flare across the US, Israel and Iran, and stock markets remain volatile after a choppy start to the year. In this environment, BTC has drawn steady bids on pullbacks toward the 60k mark, but the path forward remains uncertain as traders weigh whether a breakout or deeper correction lies ahead.

Analysts point to a technical setup that could tilt the risk balance either way. A rising wedge and a bear-flag pattern have been in focus, with a key stake on whether Bitcoin can sustain a rally above a critical resistance area. Market technicians stress that a daily close above roughly 76,000 USD would be necessary to invalidate the current bearish configuration and shift the narrative toward a potential fresh leg higher. Until such a breakout occurs, the market may remain in a waiting game as traders seek a catalyst to unlock capital and directional bets.

Key takeaways

- Bitcoin remains range-bound between 60,000 and 73,000 USD despite challenging macro conditions, with support at 60k and resistance nearer 70k–73k.

- A bear-flag/bearish continuation pattern dominates near-term view, requiring a close above 76,000 USD to negate the setup; a breakdown could push toward the mid-50k to 52,500 USD area per some scenarios.

- Trading activity shows subdued demand and a cautious stance, as aggregated open interest stays below 20 billion USD and negative funding rates are treated as opportunistic signals rather than reliable catalysts for rallies.

- Liquidity dynamics hint at risk for leveraged longs if BTC weakens toward 63–65k USD, with a liquidity gap below and another cluster of longs starting around 57,500–56,000 USD.

- Market participants await a clear catalyst—whether a macro shift or a technical breakout above 76k—before the next sustained move, keeping the focus on the 60k–70k range until then.